Global Automotive Report Chemicals Prices News Analysis August 2015 Editor: Mark Victory n ICIS analyses Volkswagen emissions scandal impact n Global IBAP reaches record low n Macroeconomic conditions deteriorate n Europe and US auto sales robust n Green shoots remain Asia Executive summary 2 IBAP 2 Macroeconomic outlook 2 Global new passenger car registrations 5 The VW emissions scandal 7 Executive summary 11 Macroeconomic outlook 11 IBAP 12 New passenger car registrations 12 Petrochemical market summaries 13 Price tables 14 Executive summary 17 Macroeconomic outlook 17 IBAP 18 New passenger car registrations 19 Price tables 20 Petrochemical market summaries 20 Executive summary 23 Macroeconomic outlook 23 IBAP 24 New passenger car registrations 25 Price tables 26 Petrochemical market summaries 26 Global Europe Americas The ICIS Global Automotive Report | October 2015 | Published by ICIS | www.icis.com | 29 pages

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Global Automotive Report

Chemicals Prices News Analysis

August 2015

Editor: Mark Victory

n ICIS analyses Volkswagen emissions scandal impactn Global IBAP reaches record lown Macroeconomic conditions deterioraten Europe and US auto sales robustn Green shoots remain

Asi

aExecutive summary 2IBAP 2Macroeconomic outlook 2Global new passenger car registrations 5The VW emissions scandal 7

Executive summary 11Macroeconomic outlook 11IBAP 12New passenger car registrations 12Petrochemical market summaries 13Price tables 14

Executive summary 17Macroeconomic outlook 17IBAP 18New passenger car registrations 19Price tables 20Petrochemical market summaries 20

Executive summary 23Macroeconomic outlook 23IBAP 24New passenger car registrations 25Price tables 26Petrochemical market summaries 26

Glo

bal

Euro

pe

Am

eric

as

The ICIS Global Automotive Report | October 2015 | Published by ICIS | www.icis.com | 29 pages

2

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

SUMMARYThe Volkswagen (VW) diesel emissions scandal is dominating global automotive discussions.

Nevertheless, the scandal is in its early stages and the potential effects are too nebulous and contingent to be dealt with in a few cursory lines asides from saying that its effects have the potential to be long-lasting and far reaching once it has moved out of the news cycle. ICIS maps out the potential fallout in a special section of the report here.

The weighted Global ICIS Basket of Automotive Petrochemicals (IBAP) is at its lowest level since ICIS began tracking the indicator in March 2014 as negative Asian macroeconomic conditions and volatile upstream crude oil prices weighed on prices. The Global IBAP for September is provisional because US PVC contract prices remain under negotiations and the August PVC value has been used in its stead to create the provisional Global IBAP. Nevertheless, US PVC contract prices are expected to fall, the arguments remain about how much, meaning that the final Global IBAP figure is likely to be even lower.

Negative conditions in Asia have continued into October, the US macroeconomic environment has become more confused, and Eurozone growth is disappointing expectations.

Automotive-linked petrochemical raw materials are broadly expected to decline in October in all three regions. Nevertheless, September auto sales in the US and Europe were strong and China auto sales have rebounded.

Coupled with this, in Europe and the US petrochemical prices are largely being driven down by upstream costs, with demand in several major markets strong.

While more negative macroeconomic trading conditions and the potential fallout of the VW scandal mean that there is a great deal of uncertainty, there are also several green shoots.

Global auto and petchem trading conditions are on a knife-edge and could move in either direction in the fourth quarter.

For the Asia executive summary, click hereFor the Europe executive summary, click hereFor the US executive summary, click here

IBAPThe provisional September Global IBAP fell to its lowest level since ICIS began calculating the index in March 2014 as petrochemical prices fell in all three of the major auto producing regions of Europe, the US and Asia, for the second consecutive month.

Falls in the Global IBAP came amid continued global macroeconomic uncertainty and broadly falling building block petrochemical prices in all three regions.

Unsurprisingly, Asia was the major contributor to the drop in the Global IBAP. Asia is the dominant global consumer of automotives, accounting for around half of worldwide automotive purchases.

The provisional September Global IBAP is now more than $100/TTVW below its September 2014 level, and the basket has shed 26.76% of its value in the past 12 months due to a combination of falling crude oil values and weakening Global macroeconomic conditions.

The provisional September Global IBAP fell by $8.99/TTVW compared with August.

Regional IBAPs are weighted based on the percentage amount of each petrochemical used in an average passenger car to give a petrochemical-based raw material cost per tonne of overall vehicle weight. The regional IBAPs are then weighted based on each region’s share of the global car production market to give a Global IBAP cost per tonne of a vehicle’s total weight.

For the Asia IBAP, click hereFor the Europe IBAP, click hereFor the US IBAP, click here

GLOBAL MACROECONOMICSLast month we probably depressed you with our article about how the end of the Babyboomer economic boom in the West and the permanent reversal of China’s 2008-2014 stimulus policies promise a much-weaker global economy.

And sadly the news has become even worse since our last report because of growing evidence that these two key dynamics are pushing the world into a deep deflationary down cycle.

GLOBAL IBAP

SOURCE: ICIS

$/to

nn

e

250

275

300

325

350

375

400

Sep2015

Mar2014

Note: September values are provisional pending the US PVC contract settlement

Global

3

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

“There is a chance that we are moving towards global deflation,” Alberto Gallo, head of European macro credit research at RBS told the Financial Times, as reported in its 4 October edition.

“We have overleveraged everywhere and, instead of reducing capacity, we are creating a prolonged state of industrial overcapacity that is driving down prices. China is the biggest example,” he added.

Producer prices in South Korea, Taiwan and Singapore have been falling for three years, according to Morgan Stanley.

The epicentre of this problem is again, of course, China where the government’s official producer price index has been on the decline for 42 consecutive months. Even more alarming is the gathering pace in the fall of factory gate prices: Last August they fell by only 1.1% but in August 2015 the decline was 12.8%.

As the prices of manufactured goods continue to fall, so does the price of the commodities needed to make all of these goods, such as oil, iron ore and copper. The sad reality is that vast oversupply in commodities has been built on the assumption of demand growth that simply hasn’t happened and will not happen.

Take oil as perhaps the best example, where total inventories in the Organisation of Economic Cooperation Development (OECD) countries were at an all-time high 2.9m barrels at the end of July. They are expected to have risen further since then, according to energy watchdog the International Energy Agency.

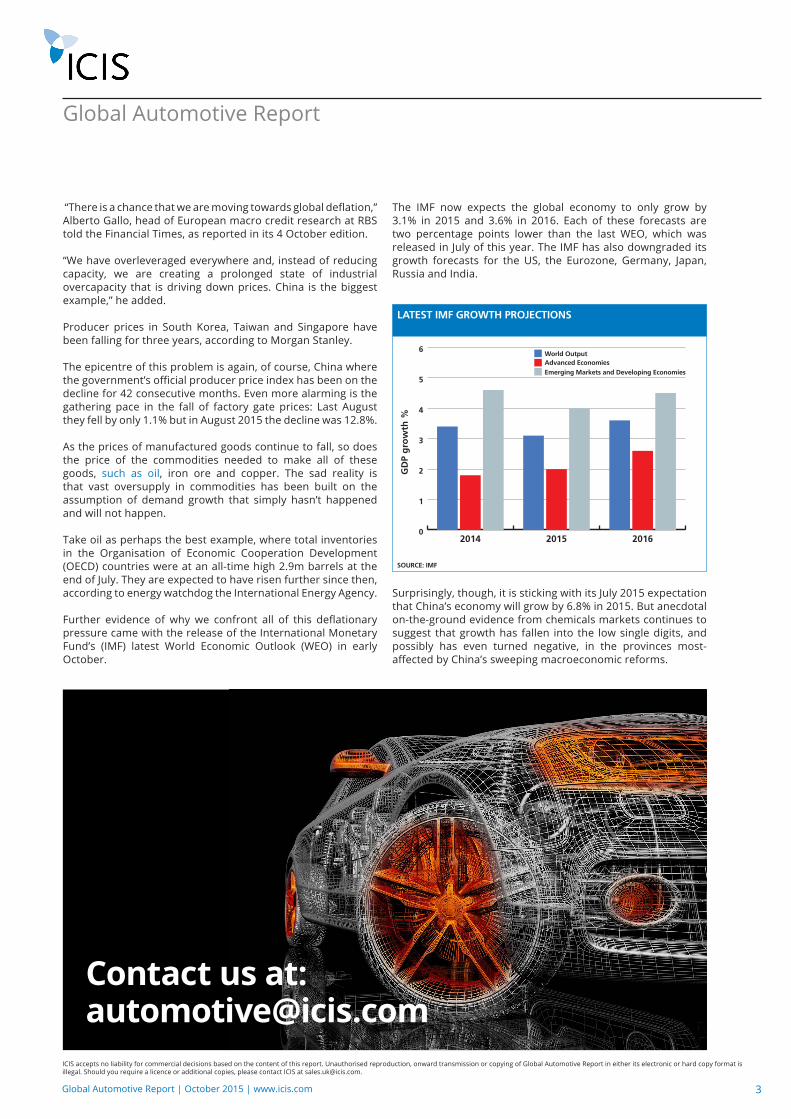

Further evidence of why we confront all of this deflationary pressure came with the release of the International Monetary Fund’s (IMF) latest World Economic Outlook (WEO) in early October.

The IMF now expects the global economy to only grow by 3.1% in 2015 and 3.6% in 2016. Each of these forecasts are two percentage points lower than the last WEO, which was released in July of this year. The IMF has also downgraded its growth forecasts for the US, the Eurozone, Germany, Japan, Russia and India.

LATEST IMF GROWTH PROJECTIONS

GD

P g

row

th %

0

1

2

3

4

5

6

201620152014

World OutputAdvanced EconomiesEmerging Markets and Developing Economies

SOURCE: IMF

Surprisingly, though, it is sticking with its July 2015 expectation that China’s economy will grow by 6.8% in 2015. But anecdotal on-the-ground evidence from chemicals markets continues to suggest that growth has fallen into the low single digits, and possibly has even turned negative, in the provinces most-affected by China’s sweeping macroeconomic reforms.

Contact us at: [email protected]

4

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

“Six years after the world economy emerged from its broadest and deepest post-war recession, the holy grail of robust and synchronised global expansion remains elusive,” said Maurice Obstfeld, the IMF Economic Counsellor and Director of the Research Department.

“Despite considerable differences in country-specific outlooks, the new forecasts mark down expected near-term growth marginally but nearly across the board. Moreover, downside risks to the world economy appear more pronounced than they did just a few months ago,” added Obstfeld.

The IMF said the downside risks included:

■ Lower oil and other commodity prices, which although benefiting commodity importers, would complicate the outlook for commodity exporters, some of whom already face strained initial conditions (e.g., Russia, Venezuela, Nigeria).

■ A sharper-than-expected slowdown in China, with the expected rebalancing towards greater market-based and consumption-driven growth proving more challenging than expected.

■ Disruptive asset price shifts and a further increase in financial market volatility could involve a reversal of capital flows in emerging market economies.

■ A further appreciation of the US dollar could pose balance sheet and funding risks for dollar debtors, especially in some emerging market economies, where foreign–currency corporate debt has increased substantially over the past few years.

■ Increased geopolitical tensions in Ukraine, the Middle East, or parts of Africa could take a toll on confidence.

The problem for most people in the autos and other industries is that they have never experienced anything like this before as since 1989, give or take a few brief recessions, the global economy has been in fantastic health.

That year was of course when the Berlin Wall came down, which was followed by the reunification of Germany and the integration of Eastern Europe in general into the Western way of running the world.

Then came China’s rise following the Deng Xiaoping 1992 “Southern Tour” and the country’s admission to the World Trade Organisation in 2001.

As hundreds of millions of poor eastern Europeans and even poorer Chinese migrant workers found better jobs, global consumption received a tremendous boost.

Simultaneously – and this is crucial to our understanding of what is happening today– waves of strong demand for all things manufactured in eastern Europe and especially in China surged out of the US, Canada and Europe. The reason was that the richest, and also crucially the biggest, middle class demographic cohort in the history of the entire world – the Babyboomers – was coming of age.

From the middle of the first decade of this century, the Babyboomers began to retire - and they are not being replaced.

Quite suddenly, the Babyboomers don’t have as much money as before because they are living on pensions. Not all of them have saved prudently enough for their retirements.

Plus, it is an inescapable fact – all the evidence points this way – that people spend less when they get older as they already own most of us what they need.

So how do automakers start rebuilding their strategies in this very different world? First of all, they need to identify what this all means for them, followed by identifying the new opportunities. Let’s start with the developed world.

THE FUTURE FOR WESTERN AUTO MARKETS

Instead of replacing your car for the sake of replacing your car every few years, both older and younger generations will make “the old Volvo” run for many, many extra years with the help of the rise of the 3D printing industry. It will become much easier to print spare parts locally in order to keep old autos on the road as the 3D printing industry further develops.

It is important to note that young people will also be affected by ageing populations as the shrinking size of working populations mean less demand for manufactured goods and all their raw materials, and so less economic growth. The young will also face the burden of rising taxes necessary to meet private pension shortfalls and soaring healthcare bills.

There are four other factors to consider, which ICIS Consulting and the UK-based consultancy International eChem are evaluating as part of a new study:

1. Older people drive half the number of miles compared to when they were younger, as their children have left home and they no longer need to drive to work.

2. Younger people no longer see gaining a driving license as a “rite of passage”, as they can instead communicate with friends via social media.

3. Volkswagen’s diesel emissions crisis highlights the growing concern over the environmental impact of the auto industry.

4. Disruptive business models such as car-sharing and

Snap

Stil

ls/R

ex S

hutte

rsto

ck

5

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

autonomous cars create further headwinds for future growth.

So the opportunities will be around lower cost mass-market cars that also have higher environmental standards.

Investments in 3D printing auto service centres might even also make sense, along with investments in car-sharing schemes and autonomous car technologies.

Note that the core of our new study will be different oil-price scenarios and what these scenarios would mean for your raw materials suppliers – the chemicals and polymers industries. In this highly volatile and uncertain world, long term oil prices could easily be $100/bbl, $50/bbl or as low as $25/bbl.

What has also changed in China, the most important of all the autos markets in the developing world? And where might the new opportunities lie in China?

NEW NORMAL FOR CHINA AND ITS AUTOS

Here is an extraordinary statistic to ponder: Between late 2008 and October 2013, auto sales rose by no less than 138% in China. Yes, 138%.

This very rapid increase was the result of the 2008-2013 economic stimulus package that boosted upper middle class personal wealth through a surge in real-estate values. There was also plenty of cheap consumer credit available as China’s government tried to compensate for the impact of the Global Financial Crisis.

But since early 2014, the pace of credit growth, and overall economic stimulus, has been steadily reduced as part of the economic rebalancing we discussed earlier in this article.

This explains why sales of autos in August fell by 3% to 1.6m cars compared with the same month in 2014, according to the China Association of Automobile Manufacturers (CAAM). The auto manufacturers’ group had previously expected China’s auto market to grow by 7% in 2015, but in July cut this estimate to 3%.

What this data underlines is that the stimulus package created a “one off” wealth effect that enabled millions of mainly, as we said, rich Chinese to buy automobiles for the first time.

Now that this wealth effect has been removed, however, you are left with some sobering facts on average income levels. The high income group in urban areas had, for example, an average income of $9,000 in 2013, according to the latest government data. And the middle income group had average earnings of just $4,000.

This is a long, long way from Western high and middle income levels, and so this tells us that sales growth will not only be lower now that stimulus is over, but also that affordability has become a much bigger issue.

Environmental concerns are also likely to limit future growth in new-car sales. China’s biggest cities – which are termed a Tier 1 cities – have, for instance, issued quotas on how many new vehicles can be purchased each year in an effort to deal with

worsening air pollution.

But an emerging opportunity is the second- hand car market, as UK-based chemicals consultant Paul Hodges pointed out in a 14 April 2015 post in his ICIS blog, Chemicals & The Economy.

“Used car sales have been slow to take off, with just 1.5m sales in 2008. But this is now changing very fast, as higher quality, longer-lasting foreign brands now dominate new car sales,” wrote Hodges.

“German brands had 27% market share in 2014, versus just 22% market share for domestic brands. These higher quality cars are now starting to be resold, after the typical five-year initial ownership. And so used car volume is expected to soar to 11m this year, according to China’s Auto Dealer Association,” he added.

As for new cars, just as is the case in the West, there is a huge opportunity in building more lower cost mass-market vehicles, which again will have to meet higher and higher environmental standards.

And do not be surprised if China also ends up leading the world by ploughing huge sums of money into research and development of autonomous cars. This would fit very neatly with its effort to move up the manufacturing and service value chains, in order justify its steep rise in wage costs over the last decade.

For the Asia macroeconomic overview, click hereFor the Europe macroeceonomic overview, click hereFor the US macroeconomic overview, click here

GLOBAL SALESGlobal auto sales in the key auto producing regions of Europe, the US and Asia rose by 2.8% in September year on year, according to ICIS analysis.

The rise follows a rebound in passenger car sales in Europe,

CHINA AUTO SALES 2008-2013

SOURCE: OICA

Sale

s in

mill

ion

s o

f u

nit

s

0

5

10

15

20

25

201320122011201020092008

6

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

the US and Asia in September. The US saw its first year-on-year rise in monthly passenger car sales in 2015. Growth in US and Europe auto sales comes in the wake of improving macroeconomic conditions in those regions.

Nevertheless, risks remain from the contagion of the slowdown in Asian macroeconomic conditions and the potential impact of the Volkswagen emissions scandal.

A total of 17,846 tonnes of diesel vehicles across all types and engine sizes were exported to the US from the EU in June 2015, according to Eurostat, the latest month for which data is available.

From January-June 2015, exports have increased by 4.99% year on year, Eurostat data showed.

VW is a dominant player in the US diesel car market.

VW will be recalling 8.5m diesel cars in Europe, including 2.4m cars in Germany, beginning early 2016, the Germany-based car giant said as it confirmed a recall order by German authorities.

Under the recall, the car giant will have to remove defeat software that allows the cars to pass emissions controls while their actual on-the-road emissions are much higher. And VW will have to take measures to ensure that the cars comply with emissions regulations, Germany’s transport minister said.

VW added that outside the EU, the recalls would be determined by each individual country. Worldwide, about 11m VW diesel cars are affected.

According to motoring publication Autocar, a total of 3.6m of the estimated 11m vehicles affected globally will require hardware changes.

The models requiring hardware upgrades are those featuring the 1.6 litre version of the EA189 turbodiesel engine across the VW, Audi, Skoda and Seat brands.

European models are likely to require new fuel injectors, while US models may need a urea tank added.

Urea tanks are typically composed of non-corrosive plastics such as PE or PP.

An estimated 482,000 US cars arew affected by the scandal, according to media reports.

Global new passenger car registrations in the first nine months of the year grew marginally by 0.92%.

Stripping out China, new passenger car sales preserves the September year-on-year trend, but reverses the year-to-date figures, showing a -0.29% reduction in sales. China measures car registrations as sales to dealerships, rather than sales to end-users, skewing the underlying data.

Nevertheless, new passenger car sales growth in Europe

NEW PASSENGER VEHICLE REGISTRATIONS – AUGUST 2014 VS AUGUST 2015

Mill

ion

un

its

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

BrazilJapanChinaUSEU & EFTA

2015 2014

SOURCE: CAAM, ACEA, AUTODATA, JAMA, ANFAVEA

+8.5

+9.8

+3.3

+6.7

-29.1

-7.4 -8.5

NEW PASSENGER VEHICLE REGISTRATIONS – JANUARY-JULY 2014 VS JANUARY-JULY 2015

Mill

ion

un

its

0

2

4

6

8

10

12

14

16

BrazilJapanChinaUSEU & EFTA

2015 2014

SOURCE: CAAM, ACEA, AUTODATA, JAMA, ANFAVEA

+8.8

+2.8

+8.5

-8.5

-10.7

-2.1

-21.7

DIESEL CAR EXPORT (TONNES) FROM EU TO US, ALL ENGINE SIZES

DATE TONNAGE

Jan 2014 14,687Feb 2014 19,567Mar 2014 18,636

Apr 2014 16,984

May 2014 14,804

Jun 2014 13,457

Jul 2014 14,832

Aug 2014 6,788

Sep 2014 17,167

Oct 2014 22,984

Nov 2014 18,432

Dec 2014 15,475

Jan 2015 15,010

Feb 2015 16,294

Mar 2015 20,093

Apr 2015 18,071

May 2015 15,717

Jun 2015 17,846

Jan-Jun 2014 98,135

Jan-Jun 2015 103,031

SOURCE: Eurostat

7

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

and the US has helped improve the year-to-date figures in regions outside China. January-August global auto sales in key producing regions excluding China showed a year-on-year fall of 0.62%.

Data has been aggregated from the China Association of Automobile Manufacturers (CAAM), the European Automobile Manufacturers Association (ACEA), AutoData, which covers the US market, the Japan Automobile Manufacturers Association (JAMA), and Brazil’s Associação Nacional dos Fabricantes de Veículos Automotores (ANFAVEA).

For Asia sales, click hereFor Europe sales, click hereFor US sales, click here

THE VW EMISSIONS SCANDAL

The saga of the Volkswagen (VW) emissions scandal continues to play out in global media, leading many analysts to predict significant damage to the “Made in Germany” brand.

REPUTATIONAL DAMAGEThe long-term financial value of the German brand has fallen by 4% compared with 2014 in the wake of the scandal, according to a press release from band valuation and strategy firm Brand Finance.

“German industry is lauded for its efficiency and reliability while Germans as a whole are seen as hard-working, honest and law abiding. That such an iconic German brand, the ‘people’s car’, could behave in this way is beginning to undo decades of accumulated goodwill and cast aspersions over the practices of German industry, making the Siemens bribery scandal appear less a one-off than evidence of a broader malaise” said Brand Finance’s CEO, David Haigh in the press release.

The reputational damage, if metastasised, could lead to other auto brands taking share away from VW and wider German brands, which, in turn has the potential to reshape the petrochemical industry.

The biggest reputational risk for VW itself could be in the US where it is a dominant player in the diesel car sales industry, but has a much smaller position in overall US car sales, leading to greater exposure to brand damage due to a closer association with diesel cars in the region in the mind of the consumer. But there is also a risk of loss of share in Europe.

From the European Chemical Industry Council (Cefic), its deputy director general, Alistair Steel, said there are only speculative questions for now until more information is available, but implied if other car manufacturers are to gain market share to be lost by Volkswagen, the chemical industry would be fairly safe.

“Our position is that any active deception to get around regulation or legal requirements is to be criticised and condemned. That’s got to be the case [in this case], but we can’t say anything else beyond that for now,” said Steel.St

eve

Med

dle/

Rex

Shut

ters

tock

NEW PASSENGER VEHICLE REGISTRATIONS IN 2015

EU & EFTA US China Japan Brazil Total

Sep 2015 1,394,223 619,080 1,751,200 399,760 166,358 4,330,621

Sep 2014 1,269,781 580,260 1,696,000 431,823 234,537 4,212,401

Jan-Sep 2015 10,776,666 5,917,573 14,547,800 3,278,790 1,602,112 36,122,941

Jan-Sep 2014 9,905,865 6,046,659 14,155,500 3,671,071 2,014,155 35,793,250

SOURCES: CAAM, ACEA, AUTODATA, JAMA, ANFAVEA

NEW PASSENGER VEHICLE REGISTRATIONS, 2015 VS 2014 (EX CHINA)

EU + EFTA US Japan Brazil Total

Sep 2015 1,394,223 619,080 399,760 166,358 2,579,421

Sep 2014 1,269,781 580,260 431,823 234,537 2,516,401

Jan-Sep 2015 10,776,666 5,917,573 3,278,790 1,602,112 21,575,141

Jan-Sep 2014 9,905,865 6,046,659 3,671,071 2,014,155 21,637,750

SOURCES: ACEA, AUTODATA, JAMA, ANFAVEA

8

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

If any loss of share is taken by a European car brand, then the impact on the European petrochemical industry is likely to be negligible. If, however, lost share is taken up by US or Asian car manufacturers, this may cause a proportional shift away from the European petrochemical industry.

A major talking point during the 49th annual European Petrochemical Asscociation (EPCA) meeting in Berlin 3-7 October, the view from many petrochemical players is that the mid-to-long term reputational impact will be minimal once the scandal moves out of the news cycle.

It remains too early to see the extent of any brand damage, but there is some precedent for this view. Past major recalls and auto scandals have not led to long-term reputational damage, and there a remains the question of how large a factor emissions are in consumer purchasing decisions. .

Granted, other auto scandals have not had the same trust issues as raised by VWs wilful emissions test rigging, but this can be seen as analogous to scandals from other industries such as the British horsemeat scandal of 2013, where long-term brand damage was limited once the topic moved off the news agenda.

Nevertheless, food is a perishable and low-ticket item compared to the high-ticket cost and long-term asset value of a car. Fear of falling resale values for VW diesels – a previous strength of the VW brand – has the potential to drive consumer spending to other manufacturers. As reported by CNBC, Kelley Blue Book’s auction data showed a 13% fall in used Volkswagen US diesel prices in the two weeks following the emissions scandal story breaking, compared with a 2% drop for petrol models.

Whether this will recover will, again, come down to the news cycle and public perception, and as with VW shares, it remains too early to take the figures at face value before they’ve reached a level and settled position.

The fall in resale value has not been the same in Europe. Reuters quotes car valuation firm EurotaxGlass’s Group in a 9 October article stating that the scandal has not had a significant effect on used VW diesel resale prices.

LEGAL AND TESTING ENVIRONMENT CHANGESOf perhaps wider impact is the threat of changes to the legal and testing environment. As emissions come under scrutiny, the difference between real-world and test-environment readings is becoming more apparent. Coupled with the success of VW’s emissions cheat device in the US, it is likely that emissions testing will be overhauled as it has been shown as unfit for purpose.

The scandal has already led VW to delay the release of 2016 diesel models, and a change to test conditions would no doubt delay other brand launches.

This is of concern because auto demand is driven by new launches and delays will affect consumption, for Europe in particular where the diesel market is much larger than in the US. Diesel cars were just 3% of US passenger vehicle fleet in 2013 versus 41% in Europe. As a major end-use for petrochemicals, lower auto demand means lower demand throughout the petchem complex.

Nevertheless, this could be of benefit to smaller petrochemical companies manufacturing parts on a cost rather than innovation basis as the continued production of older models may lead vehicle makers down a cost route for parts as contracts allow.

Tighter testing conditions are also likely to lead to higher cost for car companies, and increasing scrutiny on diesel emissions may prompt legislative action as it moves higher up the political agenda.

This could speed up the long term move away from diesel cars, with potential benefits for electrical and hybrid models, and may also speed up innovation for replacement technologies and lightweight materials such as carbon fibre to meet more stringent emissions regulation with the potential to make diesel an unviable alternative.

Already, the French government plans to boost incentives to lure drivers away from diesel cars, environment minister Segolene Royal said in a webcast television interview on Friday 9 October 2015. Diesel cars account for about 65% of cars on French roads.

Royal said that the government would expand a programme that grants premiums to drivers who give up their old diesel cars to buy electric or hybrid cars instead.

Furthermore, she said that France would end diesel’s tax

Phot

ofus

ion/

Rex

Shut

ters

tock

9

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

advantage over gasoline at the pump.

The tax changes would be phased in over five years, so drivers “will have time to see it coming, and with oil prices currently low, it will be virtually painless,” she added.

However, diesel cars had been under fire before the VW scandal. Earlier this year, the city of Paris said that in order to improve air quality it was aiming to have diesel cars out of the city by 2020.

A French refining industry official has said that less domestic demand for diesel and higher demand for gasoline should be a positive for French refiners who are finding it increasingly hard to export their surplus gasoline production against tough competition from refiners in Asia and the Middle East.

SHIFT FROM DIESELIndustry analysts predict the Volkswagen emissions scandal will impact Europe’s diesel and gasoline landscape more than their US or Asian counterparts.

Gasoline could be the real winner if politicians pull the plug on diesel tax breaks, while the heavier fuel could turn bearish in the long term.

“In a world without diesel, average fuel use for new cars in the UK would be 11% higher,” the Society of Motor Manufacturers and Traders (SMMT) said.

It will be good news for Europe’s refiners who are technically configured to produce more gasoline than the region needs, leaving it exposed to the whims of US consumers to balance the structural oversupply.

Volkswagen’s rigging of emissions tests in as many as 11m diesel vehicles to show up to 40 times less nitrogen oxide fumes could propel a move away from an intense period of growth for diesel in Europe.

Currently, demand for diesel is so high that Europe imports the transportation fuel from the US.

Diesel is also imported in cargo loads from Russia and from new refineries in the Middle East and India.

The automotive scandal has strengthened political campaigns against the energy-dense mid-distillate refined oil product.

“Every successive government since 1990 has incentivised the purchase of diesel vehicles in order to meet their obsession with reducing carbon dioxide emissions irrespective of the health impacts of other diesel exhaust emissions,” Simon Birkett, Founder and Director of Clean Air In London said.

“An investigation by Clean Air In London found that 90-95% of the most harmful particles and nitrogen dioxide from transport exhaust in London come from diesel vehicles,” Birkett said.

A shift away from diesel cars could be prompted by active lobbying from clean energy groups resulting in high-profile political initiatives such as those put forward by mayors of two of Europe’s biggest cities last year.

In 2014, the mayor of Paris Anne Hidalgo announced radical plans to ban diesel cars from the capital by 2020.

The same year, London mayor Boris Johnson said he plans to raise the congestion charge for diesel cars by £10 in the capital.

Any shift in fuel demand will most likely be driven by political initiatives, said Ole Hansen, Saxo Bank’s head of commodity strategy in a note on the company’s website.

Hard-hitting political moves would have to include higher taxation either of the fuel or the cars, Hansen noted.

“It could lead to a shift back towards petrol engines in Europe, where diesel engines now account for more than half of sales. A shift away from diesel would have a bigger impact on European manufacturers than on their US or Asian rivals,” Fitch Ratings said in a report published on 29 September.

Europe’s love affair with diesel followed a drive to reduce carbon emissions after the Kyoto Protocol in 1997.

“Europe has witnessed a strong dieselisation movement over the past 20 years as cars were actively marketed for their lower fuel cost and higher fuel efficiency than petrol models,” Natixis Economic Research said in a recently released report on the impact of the emissions scandal on diesel use.

While counterparts in the US and Japan invested in developing hybrid and electric cars, the European Commission was lobbied by German carmakers including Volkswagen to incentivise diesel.

The year after the Kyoto Protocol, European policymakers asked car markers to reduce carbon emissions by 25% over 10 years. Diesel became the choice of fuel for these car makers as it emits 15% less carbon than petrol.

Consumers also began to be taxed more on gasoline than on diesel.

The trade off for such heavy reliance on diesel was public health as diesel emits four times more nitrogen oxide.D

avid

McH

ugh/

Rex

Shut

ters

tock

10

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

The World Health Organisation in 2012 re-classified diesel engine exhaust from “probably carcinogenic” to “carcinogenic”.

“An investigation by Clean Air In London found that 90-95% of the most harmful particles and nitrogen dioxide from transport exhaust in London come from diesel vehicles,” Birkett said.

A study by King’s College London – commissioned by Greater London Authority and Transport for London – attributed nearly 9,500 deaths per year in the capital due to long-term exposure to two key air pollutants, nitrogen oxide and fine particulates known as PM2.5s.

Increasing awareness of the toll on health has already begun to lead Europe’s drivers away from diesel cars, but it remains to be seen if the VW scandal will accelerate the pace.

“The diesel penetration of new diesel cars has dropped to 53.1% in 2014, from highs of 55.7% in 2011. The share of gasoline cars sold in the Western Europe is once again rising as there are increasing concerns around diesel car emissions being far more hazardous to the environment compared to new and efficient gasoline cars,” Natixis Economic Research said in its Oil Review 2015.

“A potential reduction in diesel consumption following the current VW scandal as some consumers switch to gasoline cars could put pressure on low sulphur diesel cracks,” the firm said.

Nevertheless, as Stefano Zehnder, an expert at ICIS Consulting told industry participants in an informal presentation on the sidelines of EPCA, even if the manufacturing of diesel vehicles in Europe was to stop straight away, it would still take five or six years before there was knock-on effect as diesel cars would still be a major part of the European fleet until then.

Any turning away from diesel in Europe would not create a mirror-image benefit for gasoline demand, because the long-term trend in vehicle design is toward hybrids and electric-powered cars, Zehnder said.

Looking at the sources of oil demand growth to 2020, ICIS Consulting expects petrochemical feedstock demand to be the star performer, eclipsing diesel and gasoline. Refiners will increasingly focus on the petchem sector, Zehnder said.

FINANCIAL IMPACT ON VWFor VW itself, along with the reputational damage risk, the change in CEO and the delays to its 2016 product line-up, there is also the risk of class-action law suits and regulatory fines.

The costs from penalties, lawsuits and car recalls may well exceed the estimated $70bn costs of BP’s Deepwater Horizon oil spill disaster in the US, said Christoph Bruns, manager at German investment firm Fondsgesellschaft LOYS, in an analysis he contributed to business daily Handelsblatt.

Bruns calculated that Volkswagen may face a cost of about €2,000 per car for recalling and fixing the 11m affected diesel vehicles, coming to €22bn.

Furthermore, the company is facing huge penalties, estimated to come to $18bn (€16bn) in the US alone, from the scandal, he said.

Coupled with this, VW has a high amount of current debt (debt due to expire in the next 12 months) estimated by the Economist at €164 billion. This could cause refinancing problems, especially as the damage to its share price – if sustained – will likely lead to higher borrowing costs, as will the downgrading in VWs credit rating by Standard & Poor’s to A-.

There has been speculation from various commentators that this may lead to a need for VW to be bailed out, as with General Motors in the wake of the global recession, but at this stage that remains at the level of conjecture and contingent on a number of unknown factors playing out in very specific ways.

What seems more certain is that the financial burden may put strain on VWs growth strategy in the short-to-mid-term, and that there may well be further organisational change.

According to German newspaper Handelsblatt on 12 October, VW will seek to extract €3 billion of cost cuts from its suppliers to help off-set the cost of the scandal along with a broad range of other cuts to marketing, pay, sponsorship and its range of models.

If the reports are true, then VW will seek to use its purchasing power to achieve these price cuts from its suppliers, which would add margin pressure back up the chain. Whether market conditions will allow this remains to be seen.

11

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

SUMMARY■ October prices remain under downward pressure■ Asia IBAP falls to record low■ Macroeconomic environment remains hostile

Asian prices of automotive-linked petrochemical raw materials remain on a downward trajectory in October, with bearish macroeconomics in China and volatile stock and oil markets continuing to dominate discussions.

Nevertheless, the outlook is not as overwhelmingly bearish as it was in September as markets recover their equilibrium.

The negative outlook in September lead the Asian ICIS Basket of Automotive Petrochemicals (IBAP) to fall to its lowest level since ICIS began tracking the indicator in March 2014.

Some major end-use markets such as nylon and PVC are now expecting an upswing in prices in October because of upcoming shutdowns.

China auto sales rebounded in September following three months of declines. Auto sales in China, however, are considered as deliveries to dealerships rather than sales to end-user, skewering underlying demand slightly.

For the global executive summary, click hereFor the Europe executive summary, click hereFor the US executive summary, click here

ASIA MACROECONOMICS

Li Keqiang is spending on railways like it is still 2010, according to some analysts.

In other words, they believe that China’s prime minister is pouring more money into this one area of infrastructure in a

desperate and short-sighted attempt to shore up economic growth – and they see this as a backward step in economic reforms that are meant to favour consumption over investment.

This view was formed as a result of the late September government announcement that three new major rail links will be built in south western, eastern and central China. Rail spending this year is likely to exceed the previous peak in 2010, and be maintained at about yuan 850bn ($133.6bn) per year in 2016-2020, wrote Bloomberg in a 29 September article, quoting data from UBS.

Some analysts also talk about the need for “markets to decide” when, to what extent and in what areas future investment takes place in China. By this they mean the Western-style view of how markets work.

But as Henny Sender wrote in a 29 September Financial Times article on China’s latest round of railway spending: “The Chinese version of fiscal stimulus has produced more efficient train and metro services, rather than the property booms and stock market bubbles stemming from quantitative easing in the US”.

Here are some hard facts to back up her conclusions:

■ The 819-mile Beijing-to-Shanghai train service costs $88 for a one-way ticket.

■ The Boston-to-Washington DC train service, which takes almost seven hours to cover 394 miles, costs $300 for a one-way ticket.

Average per capita incomes in the US are a lot higher than those in China, and so this narrows the effective price gap between these two train tickets.

But as US infrastructure, from its bridges to its roads and railways continues to deteriorate, and as China very sensibly spends more money on this type of infrastructure, this big per capita income gap looks set to narrow substantially over the next few decades.

And ironically, as the US struggles to find the political will to deal with its infrastructure shortfalls, it is Chinese companies that are increasingly bidding for the US rail investments that are taking place. For instance, in Boston, again a Chinese company has broken ground on a factory that will build subway trains for the Massachusetts city.

In the short term, overseas projects such as this make sense as they will help keep Chinese engineering workers in jobs whilst painful economic rebalancing continues.

There is also a long-term objective: Exporting higher-value Chinese

Asia

Xinh

ua/R

ex S

hutte

rsto

ck

12

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

engineering skills has led to another Chinese company winning a contract to build a high-speed train link from Las Vegas to Los Angeles. This is part of China’s push to become a “branded goods and services” supplier so that it can escape its middle-income trap.

Additional railway spending is thus in an altogether different category to the trillions of genuinely wasted dollars poured into unneeded high-end real estate and surplus low value, and also environmentally toxic, industrial capacity.

Improved road and rail links will also enable domestic growth to take off through the “search engine” Internet economy.

It is no good just providing better and better broadband connections unless you also have improved road and rail links to efficiently transport the goods that have been bought on line. The further growth of domestic e-commerce giants such as Alibaba is a critical part of rebalancing towards more domestic consumption.

And no matter how much extra money China finds to spend on infrastructure – and on new stimulus in general – over the next few years, it is mathematically impossible for this money to replace the lost momentum from lower spending on real estate and the wrong sorts of industrial capacity.

So in short, you can argue that whilst China has a good chance of getting its long term direction exactly right, a lot more short term pain is on the way. How much pain? You could easily make the argument that the reform process will take at least a further five years to complete.

For the global macroeconomic overview, click hereFor the Europe macroeceonomic overview, click hereFor the US macroeconomic overview, click here

IBAPThe Asia ICIS Basket of Automotive Petrochemicals (IBAP) declined for a fourth consecutive month, taking it to its lowest level since ICIS began tracking the weighted basket in March 2014.

The Asia IBAP fell by $9.87/tonne of total vehicle weight

(TTVW) in September, to $230.57/TTVW, as deteriorating macroeconomic conditions in China and across the region continued to weigh on petrochemical prices.

The Asia IBAP remains well below the other regional IBAPs and the gap between the European and Asian IBAP has increased to $93.32/TTVW.

With the exception of SBR, which saw a rebound from low levels, Asia auto-linked petrochemical prices universally fell. The sharpest drops were seen in polypropylene (PP) and nylon. PP prices dropped on the back of feedstock propylene falls, and nylon falls were the result of weak demand and oversupply.

For the global IBAP, click hereFor the Europe IBAP, click hereFor the US IBAP, click here

ASIA IBAP

SOURCE: ICIS

$/to

nn

e

200

250

300

350

400

Sep2015

Mar2014

NEW PASSENGER VEHICLE REGISTRATIONS – SEPTEMBER 2014 VS SEPTEMBER 2015

Mill

ion

un

its

0.0

0.5

1.0

1.5

2.0

China

2015 2014

SOURCE: CAAM

+8.5

+3.3

-8.5

NEW PASSENGER VEHICLE REGISTRATIONS – JANUARY-SEPTEMBER 2014 VS JANUARY-SEPTEMBER 2015

Mill

ion

un

its

0

2

4

6

8

10

12

14

16

18

China

2015 2014

SOURCE: CAAM

+2.8

+8.5

-8.5

CHINA NEW PASSENGER VEHICLE REGISTRATIONS

Sep 2015 Sep 2014Jan-Sep

2015Jan-Sep

2014

1,751,200 1,696,000 14,547,800 14,155,500

13

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

ASIA SALESCHINAChina’s vehicles sales in September reached 2.02m units, up by 2.1% year on year and 21.6% higher compared with August, according to data from the China Association of Automobile Manufacturers (CAAM).

Vehicle production in September stood at 1.89m units, down 5.6% year on year but up 20.6% from the previous month.

Sales of passenger cars in September reached 1.75m units, up by 3.3% from the same period last year and 23.4% from August. Production of this type of vehicles totalled 1.62m units, down 6.0% year on year but up 20.8% month on month.

In January-September, China sold a total of 17.06m units of vehicles, up 0.3% from the corresponding period in 2014, with vehicle production slipping 0.8% over the same period to 17.09m units.

Total sales of passenger cars for the nine-month period increased 2.8% on year to 14.55m units, with production up 1.5% at 14.61m units.

JAPANJapan new passenger car registrations fell by 7.43% in September year-on-year, according to data from the Japan Automobile Manufacturers Association (JAMA).

In the first nine months of 2015, Japanese new passenger car registrations have fallen by 10.69%, JAMA data shows.

The biggest falls have been in mini-class vehicles, where registrations have fallen by 16.3% year-on-year in the first nine months.

All of the major brands with the exception of Mazda and Lexus saw year-on-year passenger car sales falls in the first nine months.

For global sales, click hereFor Europe sales, click hereFor US sales, click here

PETROCHEMICAL MARKETSPPPP Import prices in China rebounded in September in line with the increase of PP future prices on the Dalian Commodity Exchange, as converters started restocking in fear of the uptrend in prices. Meanwhile, domestic prices continued to trend down amid persistently weak demand.

In Southeast Asia, PP prices were volatile amid market uncertainties. Prices rose in the first half of September as converters actively sourced for import cargoes to increase their stock levels. The uptrend was not sustainable and prices subsequently dropped on falling feedstock propylene prices in the region, which dampened market sentiment. Market

NEW PASSENGER VEHICLE REGISTRATIONS – SEPTEMBER 2014 VS SEPTEMBER 2015

Million units

0.0

0.5

1.0

1.5

2.0

China

2015 2014

SOURCE: CAAM

+8.5

+3.3

-8.5

JAPAN PASSENGER CAR SALES JANUARY-APRIL 2015

Standard Small Mini Total

TOYOTA 372,113 579,357 13,855 965,325

84.32% 97.25% 72.77% 91.40%

NISSAN 127,605 121,439 140,960 390,004

86.09% 83.57% 81.56% 83.63%

MAZDA 92,383 63,306 28,221 183,910

107.39% 224.40% 74.18% 120.77%

MITSUBISHI 24,196 7,187 38,484 69,867

97.08% 68.29% 79.13% 83.09%

DAIHATSU 212 1,069 356,681 357,962

75.71% 87.76% 87.04% 87.04%

HONDA 94,517 201,861 251,181 547,559

83.42% 80.89% 85.36% 83.33%

SUBARU 95,684 775 19,304 115,763

99.05% 58.35% 84.84% 95.92%

SUZUKI 2,190 55,000 339,504 396,694

84.58% 90.46% 81.95% 83.05%

LEXUS 35,176 35,176

106.14% (%) (%) 106.14%

Others 196,773 19,693 64 216,530

105.38% 76.37% 77.10% 101.85%

TOTAL 1,040,849 1,049,687 1,188,254 3,278,790

91.86% 93.85% 83.70% 89.31%

NOTE: PERCENTAGES ARE VERSUS PREVIOUS YEAR’S SALES

14

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

players also grew more cautious about imports as further depreciation of Asian currencies weighed on the bearish sentiment.

For Europe PP, click hereFor US PP, click here

ISOCYANATES – TDIAsian toluene di-isocyanate (TDI) prices did not find any respite in September and continued to slide on the back of subdued demand and long market supply. China import prices were especially hit hard in the first-half of September amid limited trade due to an ample availability of lower-priced domestic cargoes.

TDI prices may trend stable-to-soft in the near-term amid persistently poor downstream offtake. Prices are expected to stay suppressed for the rest of the year despite several Chinese local plants having been shut since end-July/ early August for turnarounds.

For Europe TDI, click hereFor US TDI, click here

POLYOLSUS dollar-denominated China flexible foam prices were largely range-bound in September after having come off a year-low in mid-August. Buyers were on the sidelines monitoring the market amid volatile domestic feedstock propylene oxide (PO) prices in China.

Price declines in China domestic flexible foam may be curbed with the impending turnaround at a major southern China-based facility from mid-October to mid-December. However, Asian polyether polyols import prices are likely to trend down in the near term on the back of weakening

upstream propylene prices as well as an expected decline in PO prices. Stiff competition among key southeast Asia-based producers is also likely to weigh on prices.

For Europe polyols, click hereFor US polyols, click here

NYLONNylon chip prices drifted lower with a build-up of inventories from prolonged lacklustre spot appetite pressurizing Taiwanese producers to cut operating rates to below 50%. Restocking activities came late in September prior to the National Day holidays in China, and many producers managed to offload cargoes up to mid-October.

Market players are cautiously hopeful that demand in the fourth quarter will be more positive with recovery in the end-use textile sector after the end of the third quarter off-peak season, however, this is dependent on macroeconomic conditions in China, which will drive consumption.

For Europe nylon, click hereFor US nylon, click here

PVCFor the October-loading discussion period, PVC prices were firm in India and stable in China and southeast Asia. Asian producers reported healthy demand from Indian buyers which purchased to replenish their inventories after months of subdued buying activities caused by the monsoon season. Chinese demand remained stable, but low, due to bearish market sentiments and a weak economy. Demand in southeast Asia was slightly improved but prices were unable to firm as various southeast Asia currencies remained weak.

Looking ahead to the November loading period, market

ASIAN AUTOMOTIVE PRICES

Product Delta change Low Price level (€/tonne) Delta Change High

Asia IBAP Sep -9.87/TTVW 230.57/TTVW -9.87/TTVW

PP Block Co-Polymer, General Purpose CFR China Assessment Average Sep Spot

-55.00 1,037.50-1,090.00 -61.25

Isocyanates TDI CFR China and Hong Kong Average Sep Spot -105.00 1,420.00-1,500.00 -75.00

Polyols Flexible Foam - Slabstock DEL China Average Sep Spot

-12.50 1,330.00-1,380.00 -22.50

Nylon Chips Textile Grade CFR ChinaAverage Sep Spot -158.00 1,664.00-1,688.00 -162.00

PVC Ethylene-Based FOB China Average Sep Spot -32.50 747.50-786.25 -21.25

ABS General Purpose, Injection Grade CFR NE Asia Average Sep Spot

-80.00 1,290.00-1,355.00 -70.00

PC GP Moulding CIF Hong Kong Average Sep Spot -135.00 2,090.00-2,310.00 -77.50

PE HDPE Injection CFR China and Hong Kong Assessment Average Sep Spot

-65.00 1,100.00-1,140.00 -65.00

Base Oils Group II N150 CFR NE Asia NE Average Sep Spot -35.00 536.25-545.00 -46.25

SBR 1502, Non-Oil Grade CIF China Average Sep Spot 23.00 1,218.00-1,266.00 -1.50

POM Natural Grade CIF China Average Sep Spot -50.00 1,250.00-1,500.00 N/C

PBT Natural Grade CIF NE Asia Average Sep Spot -50.00 1,350.00-1,410.00 -70.00

PET Fibre Grade CFR NE Asia Average Sep Spot -46.25 837.50-860.00 -50.00

Soda Ash Dense, 99% Purity CFR NE Asia Average Sep Spot -11.75 222.00-240.00 N/C

15

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

participants were optimistic of firmer prices due to higher feedstock ethylene prices, and tighter supply as some vinyl facilities will shut down for turnarounds. However, buyers would be aiming for stable prices as the global economy remains bearish and market outlook remains uncertain, prompting many buyers to continue to purchase on a hand-to-mouth basis.

For Europe PVC, click hereFor US PVC, click here

ABSAsia ABS prices were on a downtrend in September. Chaos in global markets in August snuffed out any remaining demand for resins as ABS users kept to the sidelines. Consequently, ABS sellers concede that September demand was mostly lacklustre, despite it being the last leg of the manufacturing for exports season. Weakness in feedstock styrene, butadiene and acrylonitrile sectors also prompted ABS buyers to expect lower resin values. However, sellers found weak buying interest despite reducing offers consecutively each week. Users of ABS were hesitant to commit to large purchases as orders for finished goods remained below expectations.

Activity in the market tapered off further in late September ahead of the extended holidays in China in early October. Suppliers believe that demand will stay weak after the October holidays as the market heads toward the year end lull. Weak crude and SM values are expected to continue weighing down ABS numbers in the weeks ahead.

For Europe ABS, click hereFor US ABS, click here PCAsian spot polycarbonate (PC) prices were stable-to-soft for most of September, moving from $2,100-2,350/tonne CIF Hong Kong for general-purpose moulding grade PC on 2 September to $2,050-2,250/tonne CIF Hong Kong as of 30 September.

Recent substantial falls in upstream feedstock bisphenol A prices combined with dismal import demand for most grades of PC to create bearishness on the Asia market as a whole. Meanwhile, import demand for optical-grade PC was considered by market players as comparatively weaker, with prices falling from $2,000-2,100/tonne CIF Taiwan to $1,900-1,950/tonne CIF Taiwan during the same period. A lingering supply overhang and poor consumer demand for optical-grade PC used in multi-media storage applications and the automotive sector are expected to exert pressure on prices in the near term.

With increased BPA and PC capacities expected in China going forward, this in part limited any potential upswing in spot prices in the near term.

For Europe PC, click hereFor US PC, click here

PEChina’s HDPE injection grade import prices dropped from early September to end September due to competitively priced cargoes from America. The average prices of import

HDPE injection decreased by $35/tonne from $1,160/tonne CFR China at the beginning of September to $1,125/tonne CFR China at the end of September. Meanwhile, the average prices of import HDPE blow moulding (BM) slightly soften by $10/tonne from $1,110/tonne CFR China to $1,100/tonne CFR China in the same period.

Tight supply for High MI injection grade was expected to ease as Iran’s Jam Petrochemical had sold their High MI injection cargoes for October shipment. As a result, traders lowered their offers.

The market outlook is uncertain. Although local importers’ stock levels were comfortable, traders are unwilling to rebuild inventories as they are worried that volatile stock market and oil prices may weigh down on HDPE injection prices in October.

Southeast Asia’s High Density Polyethylene (HDPE) injection and blow moulding import prices increased slightly week on week throughout the month of September, in line with HDPE film prices.

Improving ethylene price and higher offers from suppliers amid expected tighter supply due to several plants shutdowns in southeast Asia and the Middle east are the main reasons for the price increase.

Average HDPE injection spot cargo prices were recorded at $1,150/tonne CFR SEA at the beginning of September and increased to $1,165/tonne CFR SEA at the close of September while the average HDPE blow moulding spot cargo prices were $5/tonne above injection grade price, according to ICIS data.

The market outlook for Southeast Asia in October is unclear. As southeast Asian currencies remain weak, market confidence has not improved with the majority of converters buying their resins on a need-to basis. There has not been any significant increase in the demand for HDPE in September and market participants were concerned that the demand might not pick up in October when the China market came back from the Golden Week holiday from 1-7 October.

For Europe PE, click hereFor US PE, click here

BASE OILSAsian base oils market prices in September remained plagued by downward pressure brought about by volatility in upstream crude futures, bearish market sentiment and slow cargo uptake from the downstream lubricants sector. Some grades continued to register price declines, whereas other grades largely held steady in pricing amid sluggish trade. High viscosity grades also observed slowing demand, as the approaching winter season traditionally saw weaker consumption of heavy grades as compared with light grade base oils.

Into October, spot prices are expected to remain stable-to-soft, as market fundamentals remain weak. Initial offers for some base oil grades, especially high viscosity, have already emerged at softer levels compared with September. As a result, most market players said it was likely for October base oils prices to continue registering price declines.

16

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

For Europe base oils, click hereFor US base oils, click here

POMSpot prices of POM were largely stable in September, despite persistently weak buying interest from the downstream automotive industry. POM producers were not willing to cut prices further, citing already squeezed margins. In addition, upstream methanol prices had also stemmed price falls, indirectly supporting the largely stable offers being made by the major northeast Asian producers. Going forward, most players expect limited price disruptions in the spot market, given largely stable supply-demand fundamentals.

For Europe POM, click herePBTSpot prices for polybutylene terephthalate (PBT) were largely stable throughout September, amid limited change in market fundamentals.

PBT remained amply-supplied whereas cargo uptake from downstream sectors remained sluggish. The depreciation of Asian currencies against the US dollar also made it less cost-effective for some buyers to import cargoes. In some markets such as China, some buyers were also purchasing on a need-to basis ahead of the long National Day holidays in China from 1-8 October.

Into October, market players said it was unlikely for spot prices to register significant movement as the regional PBT market remained plagued by pessimistic market conditions. Upcoming public holidays in certain import markets such as Diwali in India are also expected to curb buying interest among importers.

For Europe PBT, click here

SBRAsia styrene butadiene rubber (SBR) prices are likely to remain soft in October due to the prevailing weak demand and declining feedstock butadiene (BD) prices.

The weak global tyre market has depressed buying interest for SBR, as tyre makers in Asia cut production output.

The sluggish economies of southeast Asia have also weighed on consumption as tyre makers keep lean inventories and purchase on a hand-to-mouth basis.

Spot prices in India may also be under downward pressure, weighed down by falling feedstock BD prices and ample supply as suppliers offload their surplus stocks in India.

For Europe SBR, click hereFor US SBR, click here

PETPET prices saw a brief rebound in early September, tracking a similar trend in upstream crude values and feedstocks PTA and MEG prices, and in the absence of aggressively-priced Indian cargoes, but appeared to be slightly weakening throughout September with demand slowing down due to the approach of the cooler Autumn season.

The demand outlook for October appears stable-to-soft owing to the approaching winter in the northern hemisphere, which is the typical start of the low demand season. Some producers said they will try to sell more to the southern hemisphere as demand should pick up in that region with warmer weather in summer, but overall sales will dip considering that the southern hemisphere is a smaller market than the northern hemisphere for most Asian sellers. Other producers think that there will not be a significant drop in sales as buyers have been purchasing on a hand-to-mouth basis and will likely continue to buy regularly for continuous end-product production.

For Europe PET, click hereFor US PET, click here

SODA ASHChina’s dense grade soda ash export prices have dipped 1.7% to $198-210/tonne FOB China over the past month, while the export price of light grade soda ash fell by 5% in value, reaching $185-190/tonne FOB China by end September. The weak macroeconomics in China and Asia was a key factor in the pessimistic outlook on prices, as soda ash output remained ample versus demand, according to several producers. China’s official manufacturing purchasing managers’ index (PMI) in September stood at 49.8, the second month the reading stayed below 50, indicating continued contraction in the country’s overall industrial activities, official data showed on 1 October.

Operating rates at China-based soda ash plants were reported to be stable at around 85% and above. Looking ahead, some China based soda ash producers see prices potentially bottoming out in October, as margins have narrowed to close to production costs. On the demand side however, the northern China-based downstream glass manufacturers are slated for shutdowns of three to four months in winter, which will curtail demand for soda ash.

For Europe soda ash, click hereFor US soda ash, click here

17

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

SUMMARY■ October prices remain under pressure from feeds■ Underlying demand remains strong■ VW impact dominates discussions

Although European automotive linked petrochemical markets remain under pressure from falling building block petrochemical prices in October, underlying demand is broadly positive.

Prices of petrochemical raw materials used in the automotive market continued to drop in September, as shown by the ICIS Basket of Automotive Petrochemicals (IBAP), which declined in Europe by €13.12/tonne of total vehicle weight (TTVW), as a result of upstream pressure.

There are signs, though, from several auto-linked petrochemical markets – chief among them polypropylene (PP) – that prices may have reached the bottom of the cycle as supply and demand overcome upstream pressure.

These signs are not universal, and bearish sentiment remains in several markets such as polyurethanes, nylon, PVC, SBR, POM and PBT creating a mixed outlook. Nevertheless, the declines in petrochemical prices seen over the last three months in Europe may be starting to slow.

European auto sales remain robust, with new passenger car registrations continuing to show strong year-on-year growth in September in spite of the macroeconomic slowdown in China, which remains a background threat. Coupled with this, although Eurozone macroeconomic growth continues, the growth rate is slowing to below expectations, which could potentially impact auto sales in the fourth quarter.

Of course, the impact of the VW emissions scandal on European sales and petrochemicals continues to dominate discussion, and the news broke perhaps too late in the month to have had a significant impact on September registration figures. It remains too early to see the full impact of the scandal, but the potential outcomes are discussed here.

For the global executive summary, click hereFor the Asia executive summary, click hereFor the US executive summary, click here

EUROPE MACROECONOMICSDuring the third quarter of 2015, the Eurozone remained in a relatively privileged position, benefiting from a more competitive exchange rate, lower energy prices, low long-term interest rates and solid demand in the UK and US.

Speaking at the 5th SEEK Conference on “How to Foster Innovation and Entrepreneurship in a Diverging European Economy?”, Peter Praet, Member of the Executive Board of the European Central Bank, (ECB), said that even if the cyclical recovery is progressively taking hold, many Eurozone

countries are confronting a situation of disappointed growth expectations that results in seeping pessimism about the prospects for long-term growth. Consequently, this holds back a stronger recovery, as uncertainty about the future can feed back into weaker investment. Moreover, pessimism about future growth challenges one of the founding rationales for the single currency, which is that it would lead to sustainably higher wealth for all its members, according to Praet.

In line with these remarks, the OECD’s Economic Outlook and Interim Economic Outlook confirmed that growth in the euro area is improving, but not as fast as expected, despite the important tailwinds mentioned above. The euro area is projected to grow at a rate of 1.6% in 2015 and 1.9% in 2016. According to the OECD, growth prospects differ broadly among the major euro area economies. Germany is forecast to grow by 1.6% in 2015 and 2% in 2016, France by 1% in 2015 and 1.4% in 2016, while Italy will see a 0.7% rate in 2015 and 1.3% in 2016.

OECD officials indicated that the Eurozone’s disappointing pace of recovery calls for the prolongation of accommodative monetary and more growth-oriented fiscal policies in order to

Europe

Ikon

Imag

es/R

ex S

hutte

rsto

ck

18

ICIS accepts no liability for commercial decisions based on the content of this report. Unauthorised reproduction, onward transmission or copying of Global Automotive Report in either its electronic or hard copy format is illegal. Should you require a licence or additional copies, please contact ICIS at [email protected].

Global Automotive Report | October 2015 | www.icis.com

Global Automotive Report

add momentum to the expansion and create spill over effects into labour markets, business investment and trade.

According to Ernst & Young, the Eurozone has so far enjoyed a more encouraging pace of growth through 2015, supported in particular by the ECB’s asset purchase program and ambitious reform efforts in some countries. Bearing into consideration the latest published data, stability and growth are returning in the Eurozone and systemic risks seem to be fading especially after the recent deal between Greece and its creditors.

Based on E&Y Eurozone October 2015 Forecast, in the second half of 2015, Eurozone’s real GDP is expected to expand at a moderate pace of 0.4% in Q3 and 0.5% in Q4. In line with OECD’s data, E&Y predicts that growth will accelerate from +0.9% in 2014 to +1.6% in 2015, primarily driven by domestic demand. As business confidence improves, investment spending is expected to pick up in 2016, pushing growth up to 1.8%. E&Y expects growth to remain stable at 1.7% in 2017 and drop slightly to 1.5% in the following years, with oil prices recovering and a weaker euro.

The general Eurozone seasonally-adjusted unemployment rate was 11.0% in August 2015, stable compared to July 2015, and down from 11.5% in August 2014. The EU28 unemployment rate was 9.5% in August 2015, also stable compared to July 2015, and down from 10.1% in August 2014. In August 2015, the youth unemployment rate was 20.4% in the EU28 and 22.3% in the euro area, compared with 21.9% and 23.6% respectively in August 2014. In August 2015, 4.610 million young persons (under 25) were unemployed in the EU28, of whom 3.131 million were in the euro area. Compared with August 2014, youth unemployment decreased by 448 000 in the EU28 and by 262 000 in the euro area. Greece and Spain continue to top the list of Member States with the highest general and youth unemployment rate.

Markit’s Eurozone PMI decreased slightly in September, reaching a four-month low, as the Eurozone showed signs of decelerating growth towards the end of a solid third quarter. However, the region continued to make steady progress in September with economic activity mounting across the “big-four” nations. Ireland and Spain enjoyed a strong expansion in the pace of their growth during the third quarter, with the former one being the region’s star performer. France’s growth accelerated to a three-month high in September meaning that the region’s second-largest economy could achieve growth of 0.2% in the third quarter sending a positive message of a return to growth. Nevertheless, both the failure of the economy to pick up speed over the summer and job creation sliding to an eight-month low raise concern for the ECB over the next months.

Latest data from Markit’s Eurozone Retail PMI Retail trade showed a fifth straight monthly rise in sales in September, with the rate of growth picking up slightly from that seen in August. Of the ‘big-three’ euro area nations, both Germany and Italy recorded rises in retail sales in September, with the former seeing the faster rate of increase. However, in France sales decreased marginally and for the second month in a row.

As reported by Eurostat, in August 2015 compared with July 2015, the seasonally adjusted volume of retail trade remained stable in both the euro area and the EU28, mainly due to rises for automotive fuel and food products. In July retail trade rose by 0.6% and 0.4% respectively. In August 2015 compared with

August 2014 the retail sales index increased by 2.3% in the euro area and by 2.6% in the EU28.

In September 2015, the Business Climate Indicator (BCI) for the euro area increased by 0.14 points to +0.34. Moreover, the Economic Sentiment Indicator (ESI) improved significantly in the euro area by 1.5 points to 105.6 and by 0.6 points to 107.6 in the EU. The enhanced euro-area sentiment rose from improvements in confidence in industry and services and, to a lesser extent, retail trade. Consumer confidence remained broadly unchanged. The potential impact of the Volkswagen emissions scandal on the “made in Germany” brand are discussed here.