© The Treasury New Zealand’s Economic & Fiscal Outlook, Treasury’s Long-Term Fiscal Statement, and Treasury’s Living Standards Framework September 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© The Treasury

New Zealand’s Economic & Fiscal Outlook,Treasury’s Long-Term Fiscal Statement, and

Treasury’s Living Standards Framework September 2013

© The Treasury

Short-Term (next five years) Economic and

Fiscal Outlook

© The Treasury

Five Key Judgements § International Economic Situation§ Effects of the Drought§ Canterbury§ Terms of Trade§ Monetary Conditions

3

© The Treasury

Global Context

© The Treasury

Global Outlook steady ...

-1

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014 2016Years ending 31 December

Annual average % changeAnnual

ForecastTrading Partner Growth

© The Treasury

Global Economic Forecasts

2012 2013 2014 2015 2016 2017Actual Forecast Forecast Forecast Forecast Forecast

Australia 27% 3.6 2.7 2.9 3.0 3.0 3.0China 17% 7.8 8.0 7.6 7.3 7.0 7.0United States 11% 2.2 1.7 2.4 2.5 2.5 2.5Japan 9% 2.0 1.0 1.4 1.1 1.0 1.0Euro area 8% -0.5 -0.4 1.0 1.2 1.3 1.4United Kingdom 4% 0.3 0.7 1.4 1.8 2.0 2.0Canada 2% 1.8 1.6 2.3 2.4 2.5 2.5Other Asia* 23% 3.8 4.3 4.7 5.0 5.0 5.0Trading Partner Growth (TPG) 100% 3.5 3.4 3.8 3.8 3.8 3.9TPG - Consensus (April 2013) 3.5 3.5 3.9 4.1 4.1 4.0TPG - IMF WEO (April 2013) 3.5 3.5 4.1 4.2 4.3 4.4

* South Korea, Taiwan, Hong Kong, Singapore, Malaysia, Indonesia, Thailand, Philippines, India

2013 weights

© The Treasury

Changing export and import markets

Exports Imports

© The Treasury

... and risks have receded a little

• Euro area officials have helped settle thedebt crisis a touch

• US avoided the “fiscal cliff”• China is experiencing modest slowdown

© The Treasury

Domestic Outlook

© The Treasury

Growth outlook influenced by supportiveand constraining factors...

On the supportive side:– The Canterbury rebuild– A high terms of trade– Low interest rates– Less risk-averse households

and firms

Factors constraining growth include:– An elevated exchange rate

© The Treasury

...but the overall economic outlook issimilar to the Half Year Update

-4

-2

0

2

4

6

8

Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16Quarterly

BEFU HYEFU

Annual average % change

ForecastReal GDP growth

© The Treasury

Growth to be driven primarily throughInvestment and Consumption...

-4-3-2-10123456

2012 2013 2014 2015 2016 2017Years ended 31 March

Exports Total consumptionNon-residential investment & stocks Residential investmentImports Total GDP (annual average growth %)

Percentage point contribution to annual real GDP growth

© The Treasury

Summary(March Years, %)

2012 2013 2014 2015 2016 2017 Actual Estimate Forecast Forecast Forecast Forecast

Economic (March years, %)

Economic growth 1.9 2.5 2.4 3.0 2.6 2.2 Unemployment rate 6.7 6.9 6.0 5.9 5.5 5.2 CPI inflation 1.6 0.9 1.9 2.0 2.0 2.2 CA balance -4.4 -4.8 -4.8 -5.2 -5.8 -6.5 Fiscal (June years, % of GDP) Total Crown OBEGAL -4.4 -2.9 -0.9 0.0 0.3 1.0 Net debt 24.3 27.1 28.4 28.7 28.1 27.3

© The Treasury

...and in an international context, growthlooks good

-0.50.00.51.01.52.02.53.03.54.04.5Forecast trading partner growth (calendar years), % change

2013 2014 2015Source: Treasury

© The Treasury

Relative growth performance has also improved

© The Treasury

...but there is still a large gap to closeGDP per capita (Index)

1970197119721973197419751976197719781979198019811982198319841985198619871988198919901991199219931994199519961997199819992000200120022003200420052006200720082009201020111970

1970

1972

1972

1974

1974

1976

1976

1978

1978

1980

1980

1982

1982

1984

1984

1986

1986

1988

1988

1990

1990

1992

1992

1994

1994

1996

1996

1998

1998

2000

2000

2002

2002

2004

2004

2006

2006

2008

2008

2010

2010

8012016020080

80

120

120

160

160

200

200

Australia

© The Treasury

Export volume growth is affected by thedrought...

-20-16-12-8-4048

121620

2000 2002 2004 2006 2008 2010 2012 2014 2016Quarterly

Exports Imports

Annual average % change

Forecast

© The Treasury

...but higher dairy prices will support aturnaround in the goods terms of trade

900

1000

1100

1200

1300

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016Quarterly

Index (1995/96 = 1000)

Forecast

© The Treasury

Labour market is expected tostrengthen over forecast period...

-2

-1

0

1

2

3

4

2

3

4

5

6

7

8

2000 2002 2004 2006 2008 2010 2012 2014 2016Quarterly

Unemployment rate Employment (right scale)

% of labour force

Forecast

Annual average % change

© The Treasury

... while inflationary pressures pick up

-3-2-101234567

Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16

CPI inflation Tradables Non-tradables

Annual % change

Forecast

Quarterly

© The Treasury

Low interest rates and the Canterbury rebuild

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16Quarterly

Real residential investment Excluding Canterbury rebuild

$billions (in 1995/96 prices)

Forecast

© The Treasury

Risks

• Risks more balanced compared to HYEFU• Global uncertainties remain

– Fiscal adjustments– Monetary policy– China and impact on Australia

• Domestic risks– Mother nature - earthquakes and drought– Saving behaviour and exchange rate

© The Treasury

Current Account

1615141312111009080706050403020100

0

-2

-4

-5

-7

-9

0.50.0-0.5-1.0-1.5-2.0-2.5

% %-pt deviationCurrent Account Deficit as % of GDP

PREFU forecast BEFU 2012 forecastBEFU less PREFU (RHS) Forecast date

© The Treasury

Higher investment drives current accountdeficit ...

© The Treasury

... higher investment drives currentaccount deficit

-10-9-8-7-6-5-4-3-2-10

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% of GDP

Current account Current account ex Canterbury rebuild

© The Treasury

1987Q21987Q31987Q41988Q11988Q21988Q31988Q41989Q11989Q21989Q31989Q41990Q11990Q21990Q31990Q41991Q11991Q21991Q31991Q41992Q11992Q21992Q31992Q41993Q11993Q21993Q31993Q41994Q11994Q21994Q31994Q41995Q11995Q21995Q31995Q41996Q11996Q21996Q31996Q41997Q11997Q21997Q31997Q41998Q11998Q21998Q31998Q41999Q11999Q21999Q31999Q42000Q12000Q22000Q32000Q42001Q12001Q22001Q32001Q42002Q12002Q22002Q32002Q42003Q12003Q22003Q32003Q42004Q12004Q22004Q32004Q42005Q12005Q22005Q32005Q42006Q12006Q22006Q32006Q42007Q12007Q22007Q32007Q42008Q12008Q22008Q32008Q42009Q12009Q22009Q32009Q42010Q12010Q22010Q32010Q42011Q12011Q22011Q32011Q42012Q12012Q22012Q31987Q2

1987Q2

1990Q3

1990Q3

1993Q4

1993Q4

1997Q1

1997Q1

2000Q2

2000Q2

2003Q3

2003Q3

2006Q4

2006Q4

2010Q1

2010Q1

040801201602000

0

40

40

80

80

120

120

160

160

200

200

TradableNon-tradable

Non-tradable

Tradable

Tradeables and Non-tradeables

© The Treasury

Long Term Economic Outlook

Why am I an optimist?§Food

§Education

§Tourism

§ Health

27

© The Treasury

© The Treasury

Falling Poverty in Asia

© The Treasury

Falling Poverty in Asia

© The Treasury

Key Questions

§ How can we exploit this opportunity? § What economic and social outcomes are we aiming for? § How can government policy help us make progress

towards the achievement of these outcomes? § How do we know if we are succeeding?

31

© The Treasury

Fiscal Strategy

© The Treasury

Overview of fiscal strategy

• Restore Government’s financial strength,reduce vulnerabilities

• Restrain expenditure growth• On track for 2014/15 OBEGAL surplus• Target net debt below 20% of GDP by 2020

33

© The Treasury

Budget Decisions

© The Treasury

• Responsibly managing the Government’sfinances

• Building a more productive andcompetitive economy

• Delivering better public services withintight fiscal constraints

• Rebuilding Christchurch

Government’s economic plan

© The Treasury

Budget 2013 - $5.1bn in operatinginitiatives, $1.5bn in capital

$3,600

$893

$313$303

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Budget 2013 operating spending, $ million

Net new spending Savings Revenue Contingencies0.0

0.5

1.0

1.5

2.0

Budget 12 Budget 13 Budget 14 Budget 15 Budget 16 Unallocated

Future Investment Fund spending profile, $ billions

© The Treasury

Four-year Plans

• $800 million allowance divided up • Most Votes directed to plan on the basis of

no new funding

104

150

350

60

5086

Emissions Trading SchemeEducation

Health

Welfare

Contingency

Unallocated

© The Treasury

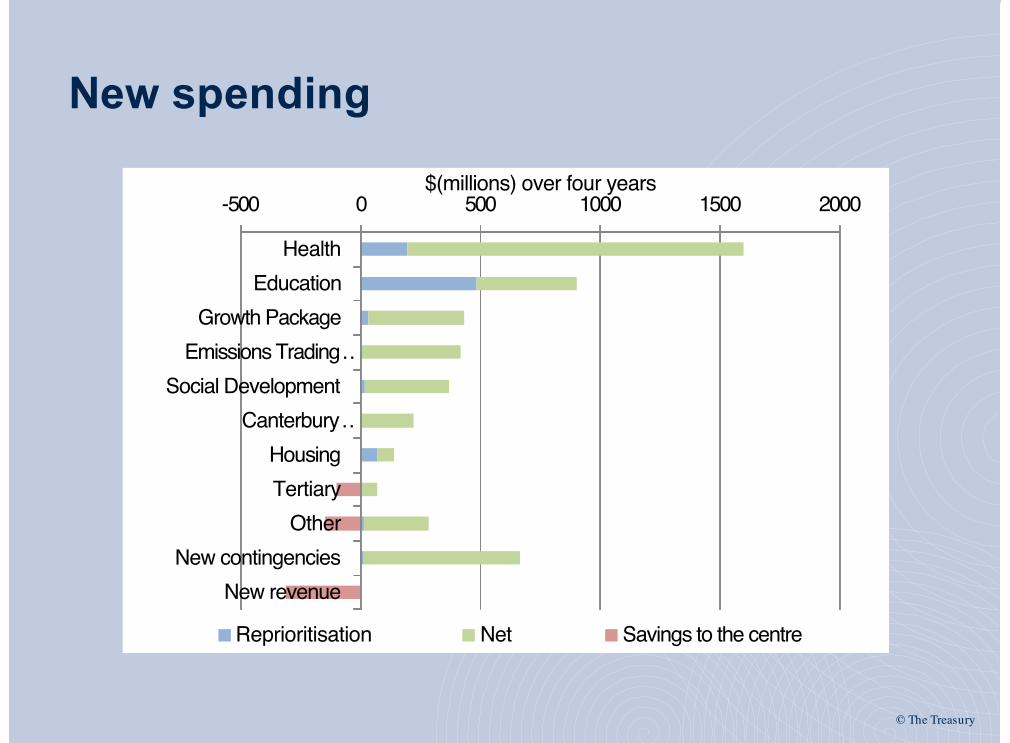

New spending

-500 0 500 1000 1500 2000

HealthEducation

Growth PackageEmissions Trading …

Social DevelopmentCanterbury …

HousingTertiary

OtherNew contingencies

New revenue

$(millions) over four years

Reprioritisation Net Savings to the centre

© The Treasury

Other

• Significant ACC levy reductions signalled– $300m in 14/15– $1 billion in 15/16

• Superfund contributions deferred until Net Debt at 20% of GDP

39

© The Treasury

Future Investment Fund

• $6 billion to be smoothed over the next fewBudgets for new capital spending

• $1.5 billion of spending in Budget 2013

0

0.5

1

1.5

2

Budget 2012 Budget 2013 Budget 2014 Budget 2015 Budget 2016 Unallocated

Expected Future Investment Fund spend

?

© The Treasury

Government share of rebuild now $15b

Local infrastructure,

$2.4 billion

Crown assets, $1.6 billion

Land zoning, $1.2 billion

Christchurch central rebuild,

$0.9 billionOther recovery costs, $1.5

billion

EQC and other Crown entities,

$7.6 billionNet earthquake-related expenses

$15.2 billion

© The Treasury

Fiscal outlook

Revenue, Expenses, OBEGAL,Net debt, Net worth

© The Treasury

From record deficit to surplus...

0

10

20

30

40

50

60

70

80

-25

-20

-15

-10

-5

0

5

10

15

2000 2002 2004 2006 2008 2010 2012 2014 2016

$ billion$ billion

Years ended 30 JuneCore Crown residual cash OBEGAL Net debt (RHS)

Forecast

-2

-1

0

1

2

3

4

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015%

of G

DP

Fiscal Years

Fiscal Impulse Expansion

Contraction

© The Treasury

...via slower spending growth

26

28

30

32

34

36

2003/04 2005/06 2007/08 2009/10 2011/12 2013/14 2015/16 2017/18 2019/20

Core Crown revenue & expenses, % of GDP

Core Crown expenses Core Crown revenue-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2006 2008 2010 2012 2014 2016

New Operating Spending per Budget, $ billions

© The Treasury

Total Crown OBEGAL

-10

-8

-6

-4

-2

0

2

4

6

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027

Budget 2013 Half Year Update 2012

% of GDP

ForecastsActuals Projections

Year ended 30 June

© The Treasury

Tax revenue increases by $14.5b

-

5

10

15

2014 2015 2016 2017Individuals Corporate GST Other

$billions

Cumulative change relativeto 2012/13 fiscal year

© The Treasury

Core Crown expenses grow $5.5b (but grow slower than tax revenue)

-4

-2

0

2

4

6

8

2014 2015 2016 2017

$billi

ons

Budget 2013 Future allowances Social assistance Finance costsEarthquake Other Total increase

Cumulative change relativeto 2012/13 fiscal year

© The Treasury

$75m OBEGAL surplus in 14/15OBEGAL = total Crown revenue less total Crown

expenses

-12-10-8-6-4-20246

2012 2013 2014 2015 2016 2017SOE Crown Entity Core Crown OBEGAL

© The Treasury

Core Crown residual cash

-8

-6

-4

-2

0

2

4

6

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027

Budget 2013 Half Year Update 2012

% of GDP

Year ended 30 JuneActuals Forecasts Projections

© The Treasury

Net debt peaks: 28.7% of GDP in 14/15

Borrowing$ 32b over

next four years Borrowing

costs$ 3.5b per

year roughlythe same astotal annualspending onlaw & order

0

5

10

15

20

25

30

35

0

10

20

30

40

50

60

70

80

2003 2005 2007 2009 2011 2013 2015 2017

$billions

Year ended 30 June

Net debt ($b) % GDP

Forecast

% of GDP

© The Treasury

Core Crown Net Debt

-10

0

10

20

30

40

50

60

70

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027

Budget 2009 Budget 2009 without policy responseHalf Year Update 2012 Budget 2013

% of GDP Year ended 30 June

© The Treasury

Affording Our Future The Treasury’s 2013 Statement on the Long-Term Fiscal Position

What’s the story and why does it matter for you?

© The Treasury

Background

• The Public Finance Act requires Treasury topublish a Statement on the Long-Term FiscalPosition at least every 4 years

• Must relate to a period of at least 40 years• The 2013 Statement was presented to Parliament

on 11 July• Together with about 40 background papers,

Affording Our Future is available on Treasury’swebsite

© The Treasury

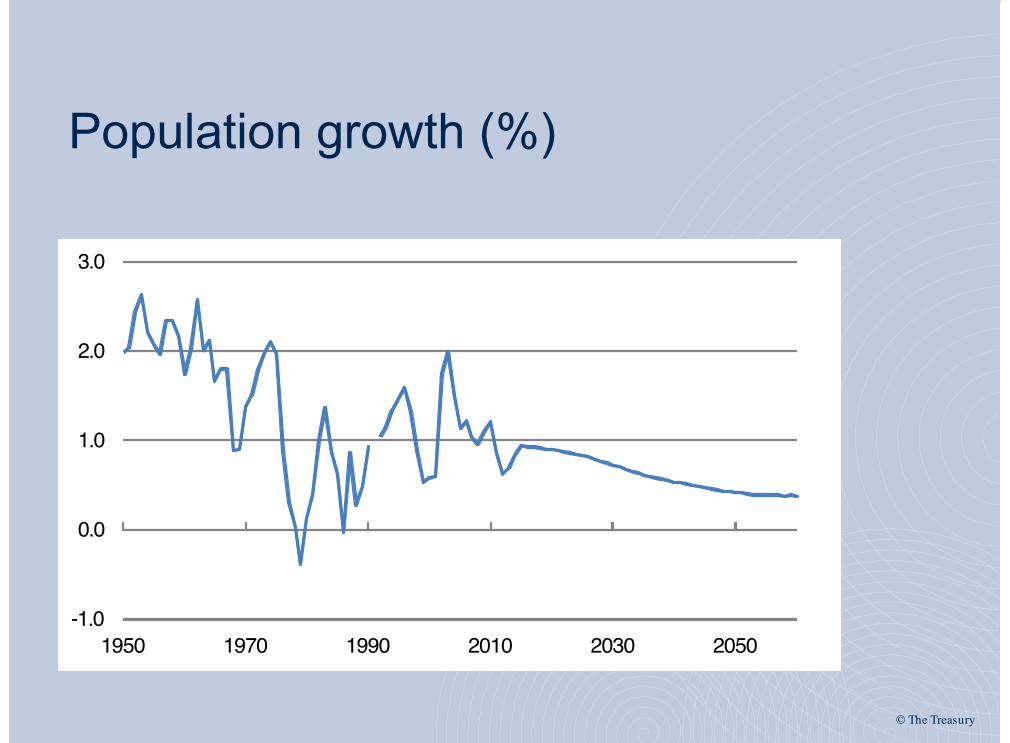

Population growth (%)

-1.0

0.0

1.0

2.0

3.0

1950 1970 1990 2010 2030 2050

© The Treasury

Dependency ratio 65+ to 15-64

People 15-64

2010

2060

People 65+

© The Treasury

Changing balance between work/remaining life for males turning 65

© The Treasury

Slowing growth of the labour force

© The Treasury

Key economic assumptions

• Trend productivity assumption of 1.5% growth in output perhour worked per annum from 2020 (versus 1.1% for thelast 40 years)

• Average weekly hours worked assumed at 33.2 hours(compared with 34.6 hours over the last 35 years)

• Assumes an average annual consumer price inflation rateof 2% (the midpoint of the current inflation range target)

© The Treasury

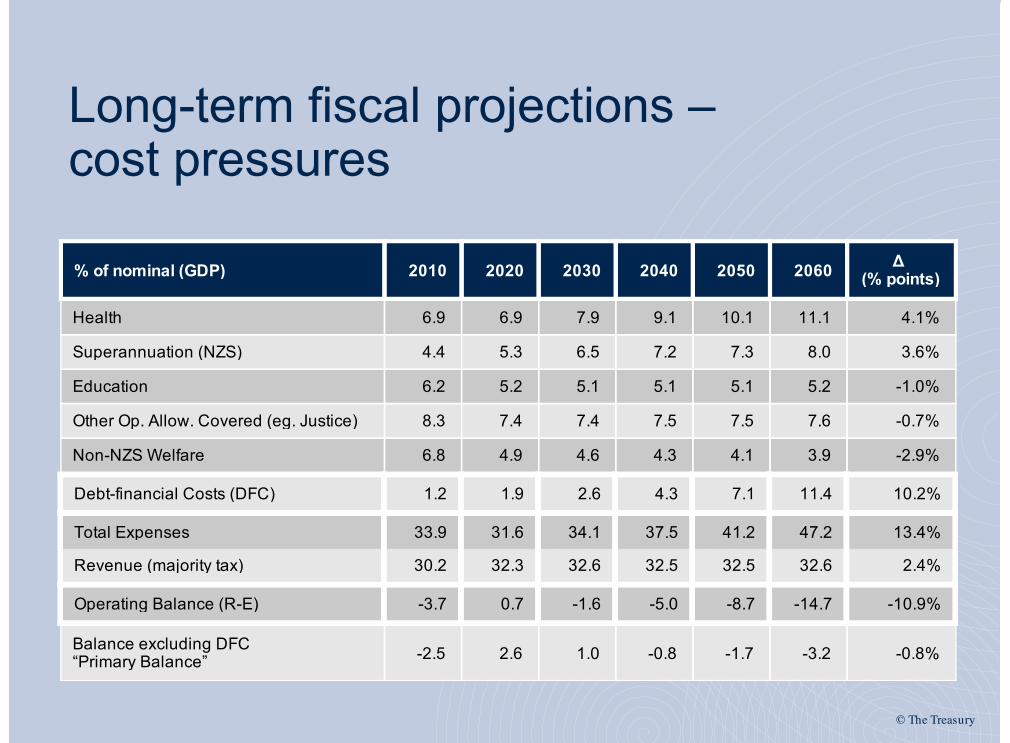

Long-term fiscal projections – cost pressures

% of nominal (GDP) 2010 2020 2030 2040 2050 2060 Δ (% points)

Health 6.9 6.9 7.9 9.1 10.1 11.1 4.1%

Superannuation (NZS) 4.4 5.3 6.5 7.2 7.3 8.0 3.6%

Education 6.2 5.2 5.1 5.1 5.1 5.2 -1.0%

Other Op. Allow. Covered (eg. Justice) 8.3 7.4 7.4 7.5 7.5 7.6 -0.7%

Non-NZS Welfare 6.8 4.9 4.6 4.3 4.1 3.9 -2.9%

Debt-financial Costs (DFC) 1.2 1.9 2.6 4.3 7.1 11.4 10.2%

Total Expenses 33.9 31.6 34.1 37.5 41.2 47.2 13.4%

Revenue (majority tax) 30.2 32.3 32.6 32.5 32.5 32.6 2.4%

Operating Balance (R-E) -3.7 0.7 -1.6 -5.0 -8.7 -14.7 -10.9%

Balance excluding DFC“Primary Balance” -2.5 2.6 1.0 -0.8 -1.7 -3.2 -0.8%

© The Treasury

Major spending areas and aggregate revenue

0

5

10

15

20

25

30

35

40

45

50

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

% of GDP

SuperWelfare

HealthEducation

Other

Finance costsRevenue

© The Treasury

NZ Super uncertainty around the median

4

5

6

7

8

9

10

2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

95th percentile75th percentile50th percentile

%of GDP

25th percentile5th percentile

© The Treasury

Primary balance uncertainty

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

95th percentile75th percentile50th percentile

%of GDP

25th percentile5th percentile

© The Treasury

The recent history ofgovernment debt

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

% GDP

Net government debt as a % of GDP

"Prudentdebt" requirement introduced

© The Treasury

Treasury’s long-term projectionsare a “what if” scenario• Treasury’s projections do not include the long-

term consequences of the Government’s fiscalstrategy (the May 2013 FSR)

• Rather, they use a “Resume Historic CostGrowth” scenario from the 2015/16 fiscal year(first full fiscal year of new Parliamentary term)

• Point is to show how expense categories mightgrow in the future, using the past as a guide

© The Treasury

What exactly is the “ResumeHistoric Cost Growth” scenario?

– Historic growth rates per recipient in differentexpense categories; plus

– Current legislative settings (e.g. for welfarebenefits and NZ Super); plus

– Assumptions about future demographics; plus– Assumptions about future economic factors

© The Treasury

The “Resume Historic CostGrowth” scenario shows:• If we allow expenses to grow in accordance with

the “Resume Historic Cost Growth” scenario from 2015/16

• And collect the same amount of tax as in recenthistory (29% of GDP)

• We’ll face a growing gap between revenue andexpenses, which we’ll need to borrow to fill

© The Treasury

What is different from last time interms of our methodology?• We have made a much greater effort to involve

experts from outside Treasury this time• We have revised up assumptions for rate of

growth in non-NZS Welfare, Health andEducation expenses based on us having a muchbetter handle of what has happened in history

© The Treasury

Key Conclusions from “ResumeHistoric Cost Growth” projections Error! Unknown document property name.

% of nominal GDP 2010 2020 2030 2040 2050 2060 Healthcare 6.8 6.8 7.7 8.9 9.9 10.8 NZ Super 4.3 5.1 6.4 7.1 7.2 7.9 Education 6.1 5.3 5.2 5.2 5.1 5.2 Law and order 1.7 1.4 1.4 1.4 1.4 1.4 Welfare (excluding NZ Super) 6.7 4.8 4.4 4.2 4.0 3.8 Other 6.5 5.6 5.7 5.8 5.9 6.1 Debt-financing costs 1.2 1.8 2.5 4.2 7.1 11.7 Total government expenses 33.4 30.8 33.4 36.9 40.6 46.8

Tax revenue 26.5 28.9 29.0 29.0 29.0 29.0 Other revenue 3.2 3.0 3.2 3.2 3.3 3.6 Total government re venue 29.7 31.9 32.2 32.2 32.3 32.6

Expenses less revenue 3.6 -1.1 1.2 4.6 8.3 14.3

Net government debt 13.9 27.4 37.1 67.2 118.9 198.3

© The Treasury

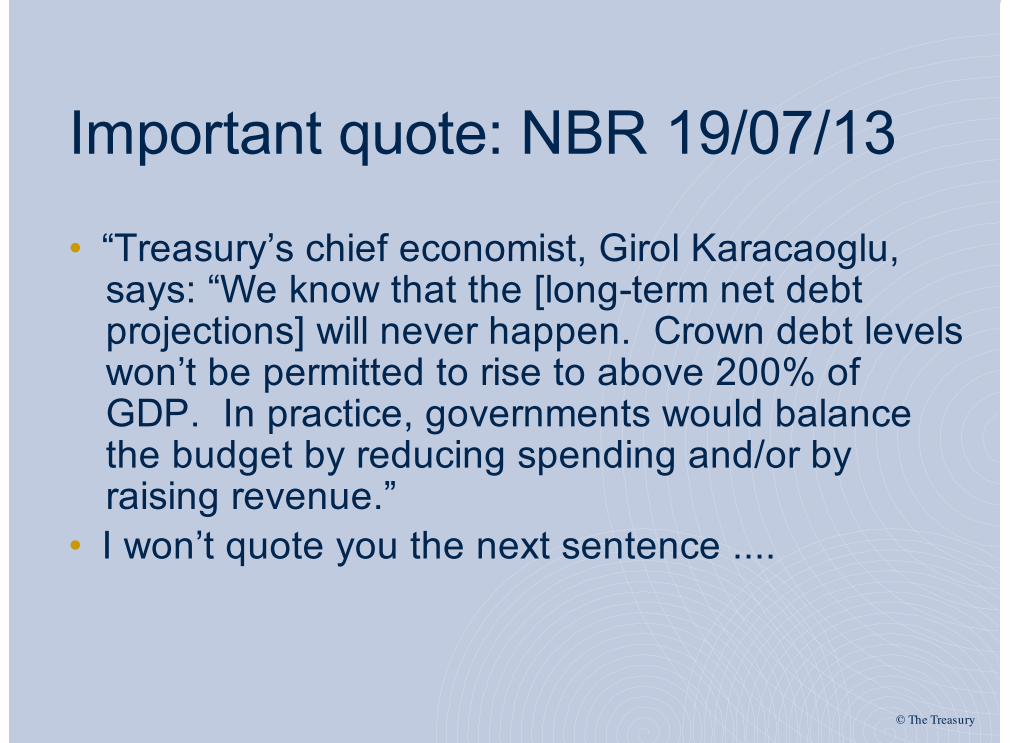

Important quote: NBR 19/07/13

• “Treasury’s chief economist, Girol Karacaoglu,says: “We know that the [long-term net debtprojections] will never happen. Crown debt levelswon’t be permitted to rise to above 200% ofGDP. In practice, governments would balancethe budget by reducing spending and/or byraising revenue.”

• I won’t quote you the next sentence ....

© The Treasury

Background Papers

• Affording Our Future was informed by specialistsfrom across the public service, academics andindependent experts – I’m very interested in yourviews

• Strongly recommend you read the BackgroundPapers Supporting the Statement – these are onour website. They cover Health, Long-TermCare, Education, Welfare, Tax etc

© The Treasury

FSR versus LTFS

• You may have noticed net Crown debt is projected to behigher in 2020 in Affording Our Future compared with theGovernment’s commitment of no higher than 20% of GDPin its May 2013 Fiscal Strategy Report

• That is because Treasury projections capture scale ofpotential expense pressures, based on historic rates ofexpenses growth re-asserting themselves from 2015/16,versus this Government’s commitments should it beresponsible for the annual budgets through to 2020

• The Government’s approach is more fiscally prudent andmore fiscally constrained than recent governments

© The Treasury

Adjusting early, pays bigdividends over time• Stick with the current fiscal strategy (or a different equally prudent

alternative) until 2020, before letting historic rates of Crown expensesgrowth per recipient to re-assert themselves thereafter : Net CrownDebt would be around 39% in 2059/60 and rising

• Maintain fiscal strategy until 2016/17 before you let historic expensepatterns progressively re-assert themselves: Net Crown Debt wouldbe around 124% of GDP in 2059/60 and rising

• Maintain fiscal strategy until we return to surplus in 2014/15, but then

turn on history (from 2015/16) : Net debt would be around 198% ofGDP by June 2060 and rising)

© The Treasury

Putting that into a graph ....

0

10

20

30

40

50

60

1997 2002 2007 2012 2017 2022 2027 2032

Net governmentdebt as % GDP

"Resume Historic Cost Growth" scenario from 2015/16Current fiscal strategy to 2016/17, then "Resume Historic Cost Growth" scenarioCurrent fiscal strategy to 2019/20, then "Resume Historic Cost Growth" scenario

© The Treasury

The current fiscal strategy

NZS Non-NZS benefits and transfers

Operating Allowance controlled expenses

Debt-financing costs (DFC)

0

1

2

3

4

5

6

7

8

Annual average % growth

1996/97 to 2011/12 2012/13 to 2019/20

© The Treasury

The Illustrative Options

• Different governments might make different choices to meet the long-term fiscal challenge – that’s why the Statement analyses someillustrative examples of policy changes that future governments couldconsider to address long-term fiscal issues, including:– Options to increase taxes– Options to constrain growth in health spending– Options to constrain growth in spending on NZ Super

• There are many, many more in the Background Papers Supporting theStatement

• ... And an on-line long-term fiscal calculator athttp://nzpublicfinance.com/ltf-calculator-introduction/

© The Treasury

It isn’t just about money ...

IncreasingEquity

Social Infrastructure

Sustainability forthe Future

Economic Growth

ManagingRisk

Living Standards

© The Treasury

Treasury’s Living Standards Work Programme

© The Treasury

Treasury’s Vision

To be a world class Treasuryworking for higher living standards

for New Zealanders.

78

© The Treasury

The OECD

79

© The Treasury

Better Life vs. GDP

80

© The Treasury

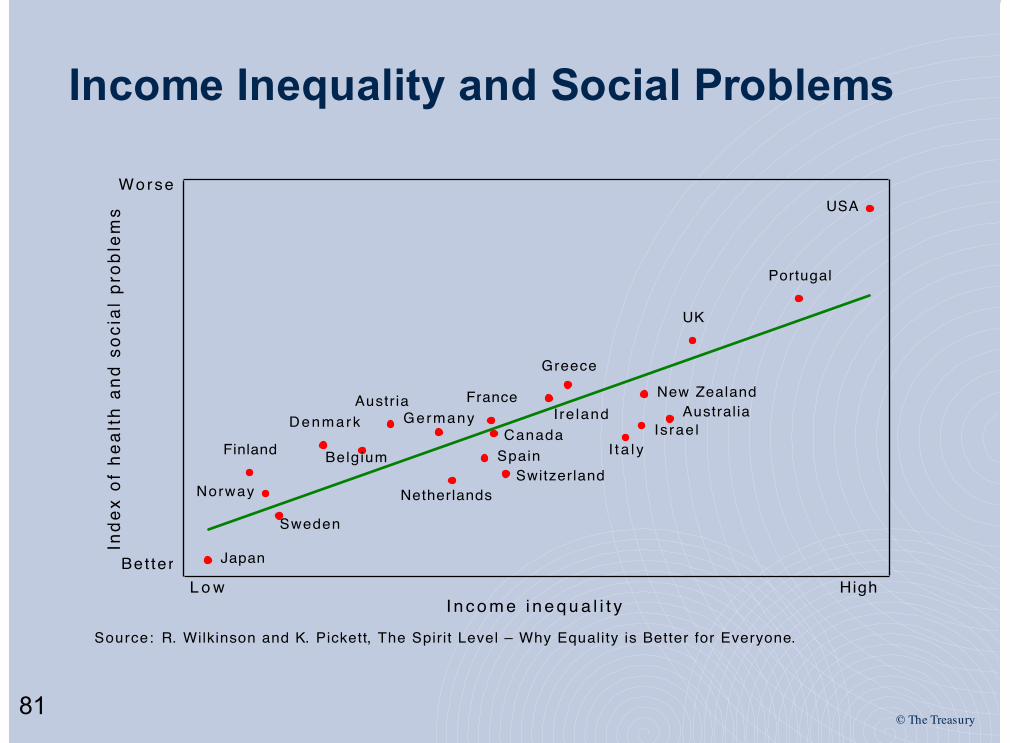

Income Inequality and Social Problems

81

Japan

Sweden

Norway

Finland

Denmark

Belgium

AustriaGermany

Canada

France

Netherlands

SpainSwitzerland

Greece

I re landIsrae l

I t a l y

AustraliaNew Zealand

UK

Portugal

USA

L o w High

Worse

Bet ter

I n c o m e i n e q u a l i t y

Inde

x of

hea

lth

and

soci

al p

robl

ems

Source: R. Wilkinson and K. Pickett, The Spirit Level – Why Equality is Better for Everyone.

© The Treasury

NZ Indicator Rankings

82

Indicator Full Sample Ranking Full Sample Percentile OECD 24 CountryRanking

OECD 24 CountryPercentile

GNI(pc) 28 / 182 15 22 / 24 92

GDP(pc) 25 / 189 13 19 / 21 90

LifeExp 19 / 193 10 12 / 24 50

Fem/Male 132 / 194 68 21 / 24 88

HDI 5 / 187 3 5 / 24 21

EPI 14 / 131 11 11 / 24 46

EcoFprint 22 / 25 88 20 / 23 87

Eco-Glob 21 / 144 15 10 / 24 42

Soc-Glob 30 / 198 15 20 / 24 83

LS-HPI 9 / 25 36 9 / 23 39

OECD-BLI 4 / 33 12 4 / 23 17

LS-Mean 48 / 94 51 18 / 24 75

LS-Sdev 65 / 94 69 22 / 24 92

Gini 51 / 135 38 21 / 24 88

Table 3: New Zealand Indicator Rankings (full sample and 24 OECD countries)A low ranking and a low percentile implies a comparatively high level of wellbeing.

Source: A Grimes, L Oxley, N. Tarrant. “Does Money Buy Me Love: Testing Alternative Measures of Wellbeing,”Motu Working Paper (forthcoming), July 2012.

© The Treasury

Distributionwithin thepopulation and over

time

Subjective Wellbeing

The Living Standards Framework

83

© The Treasury

Fundamentals – WHAT is it all about?

What is “improving standards of living” all about? It is about increasing the freedoms of individuals to enjoy the kindsof lives they wish to live. [Amartya Sen’s concept of justice and human rights. ]

Need to focus on achieving this across society and acrossgenerations – that is what equity and sustainability are all about.

84

© The Treasury

Using LSF to Guide Policy Advice

§Practical §Focused §Measureable

85

© The Treasury

IncreasingEquity

Social Infrastructure

Sustainability forthe Future

Economic Growth

ManagingRisk FINANCIAL &

PHYSICAL

Financial WealthHousing

Infrastructure

NATURAL

ClimateBiodiversity

Water

SOCIAL

InstitutionsTrust

HUMAN

SkillsHealth

Living Standards

86

A Proxy Social WelfareFunction for NZ

© The Treasury

Key Policy Question

Instead of thinking of trade-offs between the five corners of theliving standards cobweb, can we come up with policies thatmake these corners mutually reinforcing – so that we cancreate an expanding dynamic cobweb?

87

© The Treasury

0

0

20

20

Status quoPolicy change

Policy change

Status quo

88 Note: This is intended to demonstrate how the diagram could be used, rather than a Treasury view of therecommendations

© The Treasury

WHAT should be the focus of government-policyinterventions (in support of market processes) –Government Roles?

89

• Providing opportunities• Building capabilities• Improving incentives• Removing obstacles

HigherLiving

Standards

Capabilities

Obstacles

Opportunities

Incentives

All of the above are about maintaining and building:• physical/financial capital• human capital• social capital• natural capital

© The Treasury

Current Policy Levers: BIM

90

• Providing opportunities• Building capabilities• Improving incentives• Removing obstacles

HigherLiving

Standards

Capabilities

Obstacles

Opportunities

Incentives

• growth-supporting infrastructure• support business-led R&D• work-based training• youth agenda

• welfare reform• labour market reform• tax reform

• education reform• wide access to health care• international linkages programme

• removing international trade and investment obstacles• improving economic stability• improving public-sector productivity• work on long-term fiscal strategy

All of the above are about maintaining and building:• physical/financial capital• human capital• social capital• natural capital

© The Treasury

Policy Tools

§ Fiscal Tools§ Government Expenditure§ Taxes§ Public Debt and Public Loans

§ Regulatory Tools§ Regulations§ Authorisations

§ Other Tools§ Ownership§ Contingent Liabilities§ Nudging or Cajoling

91

© The Treasury

IncreasingEquity

Social Infrastructure

Sustainability forthe Future

Economic Growth

ManagingRisk FINANCIAL &

PHYSICAL

Financial WealthHousing

Infrastructure

NATURAL

ClimateBiodiversity

Water

SOCIAL

InstitutionsTrust

HUMAN

SkillsHealth

Living Standards

92

How might wemeasure progressfor New Zealand?

• NNI / capita

• NII position of NZ• Reducing crime rate• Reduction in social welfare dependency

• % of population below 50% of median income• Difference in the PISA score between the top andbottom 10% of students

• gross capital formation• GHG emissions tonnes/capita• % aged between 35-34 withtertiary qualifications

• World Bank government effectiveness indicator• World Values Survey: social trust indicator

© The Treasury93

Reduces intergenerational equityIncreases within generation equity

Example: Effect of a PAYGO-funded expansion of New Zealand Superannuation

Reduces investment risk Increases wage growth risk

© The Treasury

Example: Effect of a SAYGO-funded expansion of New Zealand Superannuation

94

© The Treasury0

0

20

20

OECD averageNZ 2000NZ 2010

NZ 2010

NZ 2000

OECD average

Example: NZ's performance �compared to the OECDExample: NZ's performance �compared to the OECD

Example: NZ's performance �compared to the OECD

EconomicGrowth

Sustainabilityfor the future

IncreasingEquity

SocialInfrastructure

ReducingRisks

© The Treasury

Example: Living Standards Assessment: Risk Management Method: Increasing the freedoms of individuals to enjoy desired lifestyles Elements: Physical Human Social Natural Capital Capital Capital Capital Risks Earthquakes Crime Welfare dependency Climate Changee.g. Floods Ill health Economic crises Biodiversity risks Eruptions Skill Deficiency Education failure Erosion Infrastructure disrepair Civic society failure White elephants Mitigations Insurance Education Policy Welfare Reform Emissions

Trading

96

© The Treasury

Next Steps § USE IT

§ Encouraging various teams within Treasury to trial the framework and sharewhat they learn with other teams.

§ Encouraging teams within Treasury to work with people from across thepublic sector in developing and using the framework, and associatedmeasures.

§ PROMOTE IT§ Ongoing presentations to various audiences (universities, public sector

agencies, ...) to explain the work and seek feedback.

§ DEVELOP IT§ Ongoing work to set up teams, within Treasury and across the public sector,

to progress research and measurement within each “corner” of the cobweb.§ Sharing what we learn by trying with all so that we can improve ways in

which we can enhance the framework for better policy guidance.

97

© The Treasury

1. BACK TESTING OUR ADVICE USING THELIVING STANDARDS FRAMEWORK…

© The Treasury

2. MEASURE THE 5 DIMENSIONS FROM1950…

Joey Au and Amy Thomson (Statistics New Zealand)

© The Treasury

3. WHICH DIMENSION ARE POLICIESFOCUSED ON?www.gen.org.nz

3. IDENTIFY WHICH DIMENSION(S) OF POLICIESWE ARE CURRENTLY FOCUSED ON…

Olga Pleijte, Joey Au and Ricky Utting (Treasury)

© The Treasury

4. WEIGHT THE 5 DIMENSIONS OF THEFRAMEWORK

0

1

2

3

4

5

6

7

Economic Growth

Sustainability for the Future

Increasing Equity

Social Infrastructure

Managing Risks

Status Quo Option A

0

1

2

3

4

5

6

7

Economic Growth

Sustainability for the Future

Increasing Equity

Social Infrastructure

Managing Risks

Status Quo Option B

Option A Option B

they are equal

this onethis one

Joey Au, Andrew Coleman (Treasury) and Trudy Sullivan (University of Otago)HUGE thanks to Paul Hansen (University of Otago) and Franz Ombler (1000Minds)

© The Treasury

5. DEVELOP THE LIVING STANDARDS HUB /COMMUNITY www.gen.org.nz

Share

Connect

Discuss

Related Documents