Friday July 15, 2016 www.bloombergbriefs.com French Terror Attack; U.S. Retail Sales, CPI, Empire, IP BEN BARIS AND JAMES BATTY, BLOOMBERG BRIEFS EDITORS WHAT TO WATCH: A terrorist attack in France has killed at least 80 people. The Nice assault is the third major terrorist attack in France since January 2015. ECONOMICS: The Bloomberg consensus calls for a 0.1 percent advance in June from a month earlier following a 0.5 percent rise in May, 8:30 a.m. Released retail sales concurrently, the is expected to rise 0.3 percent in June. Also at consumer price index 8:30 a.m. the survey will give the first look at factory output in Empire Manufacturing July. may rebound to a 0.3 percent gain last month after a 0.4 Industrial production percent decline in May, 9:15 a.m. The preliminary print of the University of Michigan survey for July is released at 10 a.m. consumer sentiment CENTRAL BANKS: Minneapolis Fed President and St. Louis Fed Neel Kashkari President discuss the role of the U.S. in the global economy at an James Bullard Official Monetary and Financial Institutions Forum meeting in St. Louis, 1:15 p.m. MARKETS: European stocks halted this week’s rally as French shares retreated following the Nice attack. (All times local for New York.) Click to view a live version of this chart on the Bloomberg terminal. here QUOTE OF THE DAY "I’m prepared to believe that this very unusual election season ... is influencing businesses to some extent on the margin in some of their decisions, and perhaps households as well, in big-ticket decisions." — Atlanta President Dennis Lockhart, answering questions after a in Victor, Idaho speech COMMENTARY IN THIS ISSUE The U.S. — an element of financial dollar markets considered out of the Federal Reserve’s control — may dictate the timing of the next interest-rate hike: TJ and Marta Vincent Cignarella. While several indicators point to a slight increase in activity, manufacturing weakness abroad and the unknown consequences from Brexit could further weigh on the pace of output for a prolonged period: Richard Yamarone. Morgan Stanley Chief U.S. Economist Ellen Zentner discusses Fed monetary policy, the global growth outlook, and what should most concern investors: and Tom Keene Michael McKee. EQUITIES DATA MONITOR FX Developed Economy Central Banks Pushing Rates Lower The Fed's December rate hike helped push the aggregate GDP-weighted central bank rate for developed economies to 0.66 percent in the fourth quarter from 0.55 percent the previous quarter. That was the first increase for the index since the first quarter of 2014, when New Zealand kicked off a new tightening cycle and Turkey’s central bank dramatically increased rates to counter a plunging currency. At the start of 2016, economists were forecasting that the aggregate rate for developed economies would end the year at 1 percent, 36 basis points above the current level. That consensus has since plunged to 0.6 percent. The shift in developed markets from net tightening to easing during the first half of 2016 helps to explain the recent strength in equities, while yields have been pushed to new lows. Read the daily Macro Musings column on the Bloomberg terminal at NI ECOMUSINGS <GO>. — Michael McDonough, Bloomberg Intelligence Economist Source: Bloomberg In Asia, equities rose for a fifth day as Chinese economic data beat estimates after a strong start to the U.S. earnings season.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Friday

July 15, 2016

www.bloombergbriefs.com

French Terror Attack; U.S. Retail Sales, CPI, Empire, IPBEN BARIS AND JAMES BATTY, BLOOMBERG BRIEFS EDITORS

WHAT TO WATCH: A terrorist attack in France has killed at least 80 people. The Nice assault is the third major terrorist attack in France since January 2015.

ECONOMICS: The Bloomberg consensus calls for a 0.1 percent advance in June from a month earlier following a 0.5 percent rise in May, 8:30 a.m. Releasedretail sales

concurrently, the is expected to rise 0.3 percent in June. Also at consumer price index8:30 a.m. the survey will give the first look at factory output in Empire ManufacturingJuly. may rebound to a 0.3 percent gain last month after a 0.4 Industrial productionpercent decline in May, 9:15 a.m. The preliminary print of the University of Michigan

survey for July is released at 10 a.m.consumer sentiment

CENTRAL BANKS: Minneapolis Fed President and St. Louis Fed Neel KashkariPresident discuss the role of the U.S. in the global economy at an James BullardOfficial Monetary and Financial Institutions Forum meeting in St. Louis, 1:15 p.m.

MARKETS: European stocks halted this week’s rally as French shares retreated following the Nice attack.

(All times local for New York.)

Click to view a live version of this chart on the Bloomberg terminal.here

QUOTE OF THE DAY

"I’m prepared to believe that this very unusual election season ...is influencing businesses to some extent on the margin in some of their decisions, and perhaps households as well, in big-ticket decisions."

— Atlanta President Dennis Lockhart, answering

questions after a in Victor, Idahospeech

COMMENTARY IN THIS ISSUE

The U.S. — an element of financial dollarmarkets considered out of the Federal Reserve’s control — may dictate the timing of the next interest-rate hike: TJ

and Marta Vincent Cignarella.

While several indicators point to a slight increase in activity, manufacturingweakness abroad and the unknown consequences from Brexit could further weigh on the pace of output for a prolonged period: Richard Yamarone. Morgan Stanley Chief U.S. Economist Ellen Zentner discusses Fed monetarypolicy, the global growth outlook, and what should most concern investors:

and Tom Keene Michael McKee.

EQUITIES DATA MONITOR

FX TJ MARTA AND VINCENT CIGNARELLA, BLOOMBERG FIRST WORD STRATEGISTS

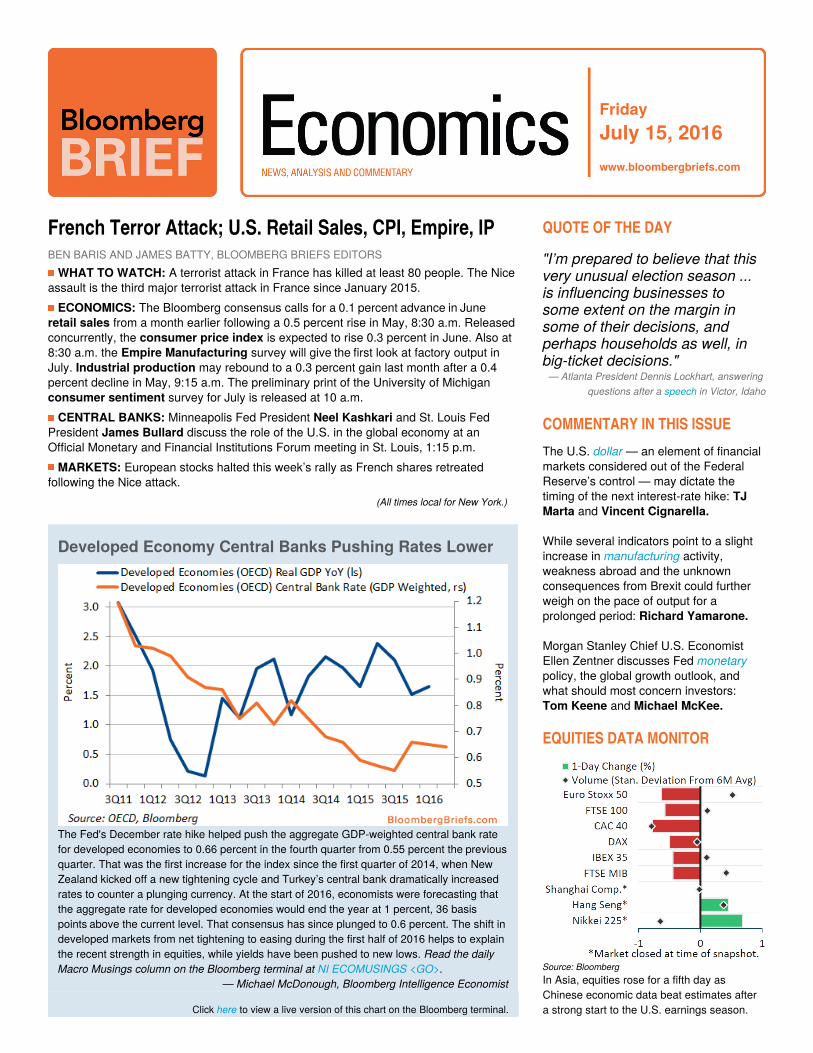

Developed Economy Central Banks Pushing Rates Lower

The Fed's December rate hike helped push the aggregate GDP-weighted central bank rate for developed economies to 0.66 percent in the fourth quarter from 0.55 percent the previousquarter. That was the first increase for the index since the first quarter of 2014, when New Zealand kicked off a new tightening cycle and Turkey’s central bank dramatically increased rates to counter a plunging currency. At the start of 2016, economists were forecasting that the aggregate rate for developed economies would end the year at 1 percent, 36 basis points above the current level. That consensus has since plunged to 0.6 percent. The shift in developed markets from net tightening to easing during the first half of 2016 helps to explain the recent strength in equities, while yields have been pushed to new lows. Read the daily Macro Musings column on the Bloomberg terminal at NI ECOMUSINGS <GO>.

— Michael McDonough, Bloomberg Intelligence Economist

Source: Bloomberg

In Asia, equities rose for a fifth day as Chinese economic data beat estimates after a strong start to the U.S. earnings season.

July 15, 2016 Bloomberg Brief Economics 2

FX TJ MARTA AND VINCENT CIGNARELLA, BLOOMBERG FIRST WORD STRATEGISTS

Fed May Be Handcuffed If Dollar Strengthens FurtherThe U.S. dollar — an element of

financial markets considered out of the Federal Reserve’s control — may dictate the timing of the next interest-rate hike. As the dollar rises, financial conditions tighten, making a hike improbable.

The dollar could strengthen amid concerns over Brexit, European growth and the apparent slowdown in China. If it rebounds to January highs, the odds of a Fed rate hike this year will diminish.

The U.S. Trade-Weighted Dollar Index is currently at 90.62, up from the year-to-date low of 87.71 registered on May 2. The index is nearing resistance at the May 31 high of 90.96. It reached its year-to-date high of 95.80 on January 20. The index tends to lead the Goldman Sachs Financial Conditions Index, with a current positive correlation of 0.72.

The trade-weighted dollar index surged 23 percent from June 2014 to March 2015. It remains 6 percent above the 2008-2009 crisis peak and near highs since 2003. Markets calculate a 4 percentcurrency move in either direction as equivalent to a 25-basis-point rate change.A 23 percent rise suggests the economy already digested 150 basis points of hikes, in addition to the explicit

quarter-point hike from the Fed in December.

New York Fed and Fed economistsVice Chair have noted Stanley Fischerthe negative impact of a strong dollar on both growth and inflation.

Cleveland Fed President Loretta Mester also expressed about the U.S. concerndollar on Tuesday, indicating that further, lasting appreciation of the greenback

resulting from Brexit could hurt the U.S. economy. On Wednesday, Dallas Fed President Robert Kaplan said the central bank is “very ” to the impact of a sensitivestronger dollar.

NOTE: Vincent Cignarella and TJ Marta are FX

strategists who writes for Bloomberg. The

observations they make are their own and are not

intended as investment advice.

INDUSTRIAL PRODUCTION RICHARD YAMARONE, BLOOMBERG INTELLIGENCE ECONOMIST

Financial Conditions Would Tighten on Dollar Rise

July 15, 2016 Bloomberg Brief Economics 3

INDUSTRIAL PRODUCTION RICHARD YAMARONE, BLOOMBERG INTELLIGENCE ECONOMIST

U.S. Industrial Output Likely Advanced in JuneU.S. manufacturing output has

struggled to register a promising trend since peaking in late-2014. U.S. dollar strength and diminished global demand have been the primary culprits behind the production decline. While several indicators including worker-hours and the PMIs point to a slight upward increase in manufacturing activity last month, continued weakness abroad and the unknown economic consequences from the U.K. referendum, which may impede business decisions, could further weigh on the pace of U.S. manufacturing output for a prolonged period.

Economists polled by Bloomberg expecta gain of 0.3 percent in the industrial production index for June, which would follow a 0.4 percent decline in May.

The monthly Employment Situation report provides economists with importantdata to produce a rough estimate for the monthly change in industrial production, since not all of the components for the Fed’s industrial production index are available when it analyzes the index. The simplest measure may be calculated by multiplying the total number of employees engaged in manufacturing activity by the level of hours worked.

Read the full analysis with additional live charts on the Bloomberg terminal .here

The number of manufacturing worker-hours in June totaled 500.4, or 0.1 percent higher than May. This alone would suggest a low reading in the manufacturing production index, though one of the most meaningful indicators of manufacturing strength was the surge in the one-month employment diffusion

index of 79 manufacturing industries, which posted an expansionary 55.1 reading in June from a lowly 39.9 in May.

June production data were largely solid, three of the five Fed regional PMIs are now expanding, and the ISM PMI climbed higher to 53.2. This supports some stronger production activity last month.

COMMENTARY NOAH SMITH, BLOOMBERG VIEW COLUMNIST

Manufacturing Output Looks to Have Reversed May Swoon

July 15, 2016 Bloomberg Brief Economics 4

COMMENTARY NOAH SMITH, BLOOMBERG VIEW COLUMNIST

Putting Behind Our Inordinate Fear of InflationHere’s a question: Why do we care so

much about preventing inflation?When I put this query to baby boomers,

they tell me that if I had lived through the inflation of the 1970s and early 1980s, I would understand. But this was also a time of slow growth, deep recessions and terrible asset returns. Inflation was hardly the only problem the U.S. economy was facing. So why does it stand out so strongly in our collective memory?

The harm of inflation cited in economicstextbooks seems laughably unimportant. For example, inflation generates so-calledshoe-leather costs — a term for the hassle of moving money from one’s brokerage or savings account to one’s checking account. This hassle is larger when prices change a lot, since you have to put spending cash in your wallet more often. But in the age of digital-account management, this cost is nonexistent. The same is true of so-called menu costs,a name for the hassle of companies changing their posted prices. In the modern world, these things just don’t matter that much. A more sophisticated argument against inflation is that when companies want to change their prices but for some reason can’t, inflation distorts prices from what they should be, which decreases economic efficiency.

Economists have tried to measure thesecosts, and found that they’re just as smallas we might expect. In 1981, and again in 2000, University of Chicago economics professor Robert Lucas — sometimes cited as the father of modern macroeconomics — investigated the costsof inflation. Lucas’ chosen model told him that inflation doesn’t put much of a dent in human welfare — according to his 2000 paper, 10 percentage points of inflation is only about as harmful as a 1 percent reduction in gross domestic product. In other words, according to Lucas, even a

mild recession is worse for people than the inflation of the 1970s.

Lucas model didn’t take into account the menu costs mentioned above. But economists Ariel Burnstein and Christian Hellwig looked at those in 2008, using data on how often companies change their prices. They find that, as one might expect, inflation has almost no perceptible impact on productivity — and hence, on human well-being.

So the typical arguments for why inflation is bad don't stand up. A better argument is that when prices rise fast, they also tend to be more volatile — high inflation equals uncertain inflation. If inflation is predictable, lenders and

The harm of inflation cited in economics textbooks seems

laughably unimportant

borrowers can build it into their financing deals; nominal interest rates simply rise to take into account the shrinking value of money. Workers can ask for cost-of-living increases in their paychecks, effectively indexing wages to inflation. And businesses can build inflation into their investment plans. But when inflation bounces around from month to month, it’s harder to plan for the future. That makes financing, investing, hiring and any decision that involves forward-looking planning much more of a gamble. Naturally, that will tend to hurt economic growth.

Although the historical correlation between inflation and inflation uncertainty

is well-documented, that doesn’t mean the one causes the other. If the Federal Reserve had a 4 percent inflation target, and managed to hit that target every year — thus eliminating uncertainty — we wouldn’t really be any worse off than if it hit its current 2 percent target.

So what does this imply about Fed policy? A lot, actually. The Fed’s so-called dual mandate, as laid out by Congress, is “to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.” But that says nothing about the relative weights that the Fed should put on maximum employment versus stable prices. The central bank is perfectly free to worry more about one than the other.

Many people seem to think that inflation and recession are equal, symmetric dangers. This is implicit in the idea of nominal GDP (NGDP) targeting, which is promoted by economists like Scott Sumner at George Mason University's Mercatus Institute. Since NGDP growth is just the sum of real GDP growth and inflation, Sumner’s policy implies that one percentage point of higher inflation is in some sense just as bad as a one-point reduction in growth. But in reality, a loss of one percentage point of GDP probably is many times worse than a 1 percent rise in inflation.

But economic research says that this probably isn't the best approach for the Fed. As long as inflation can be kept fromfluctuating wildly, or from spiraling upwardinto uncontrollable hyperinflation, the big worry should be about real growth. That means that the Fed probably shouldn’t be afraid of a higher inflation target, if that meant getting more people back into the ranks of the employed.

This column does not necessarily reflect the

opinion of the editorial board or Bloomberg LP

and its owners.

DATA & EVENTS

July 15, 2016 Bloomberg Brief Economics 5

DATA & EVENTS

TIME COUNTRY EVENT SURVEY PRIOR

8:30 U.S. Retail Sales Advance MoM 0.10% 0.50%

8:30 U.S. Retail Sales Ex Auto MoM 0.40% 0.40%

8:30 U.S. Retail Sales Ex Auto and Gas 0.30% 0.30%

8:30 U.S. CPI MoM 0.30% 0.20%

8:30 U.S. CPI Ex Food and Energy MoM 0.20% 0.20%

8:30 U.S. Retail Sales Control Group 0.30% 0.40%

8:30 U.S. CPI YoY 1.10% 1.00%

8:30 U.S. CPI Ex Food and Energy YoY 2.20% 2.20%

8:30 U.S. Empire Manufacturing 5 6.01

9:15 U.S. Industrial Production MoM 0.30% -0.40%

9:15 U.S. Capacity Utilization 75.10% 74.90%

10:00 U.S. Business Inventories 0.10% 0.10%

10:00 U.S. U. of Mich. Sentiment 93.5 93.5

10:00 U.S. U. of Mich. Current Conditions 109.9 110.8

10:00 U.S. U. of Mich. Expectations 83 82.4Source: Bloomberg. Surveys updated at 5:15 a.m. New York time.

Click to view a live version of this chart on the Bloomberg terminal.here

CALENDAR

Click on the to see the full range of economists' forecasts on the terminal. highlighted releases

OVERNIGHT

European car-sales growth slowed in June as the British vote on exiting the

weighed on business European Unionand consumer confidence. Registrations rose 6.5 percent from a year earlier to 1.51 million vehicles, the weakest gain since March, as demand in the U.K., the region’s second-biggest market, slid 0.8 percent. First-half sales increased 9.1 percent to 8.09 million cars, the European Automobile Manufacturers

said today. Association

U.K. construction is on course to shrink for a second straight quarter and economists are warning of worse to come for the industry in the wake of Britain’s vote to leave the European

Building output fell 2.1 percent in Union.May, almost double the decline forecast in a Bloomberg survey of economists, figures from the Office for National

showed today. There were Statistics falls in almost every category of work, with private housing down the most in more than a year.

China's gross domestic product rose 6.7 percent in the second quarter from a year earlier, compared with 6.6 percent seen by economists Bloomberg surveyed and in line with the government’s growth target of at least 6.5 percent for the full year. Industrial output and retail data for June beat estimates, investment slowed, and a report from the central bank showed the broadest measure of new credit beat all 29 analyst forecasts. "The Chinese economy remains stable," Larry

, head of China economics at Hu in Hong Macquarie Securities Ltd.

Kong, wrote in a note. "It makes no sense to ease policy at this moment, given the current growth momentum." Bloomberg’s monthly GDP tracker increased for a second month, indicating a 7.13 percent pace of expansion in June.

Europe

Asia

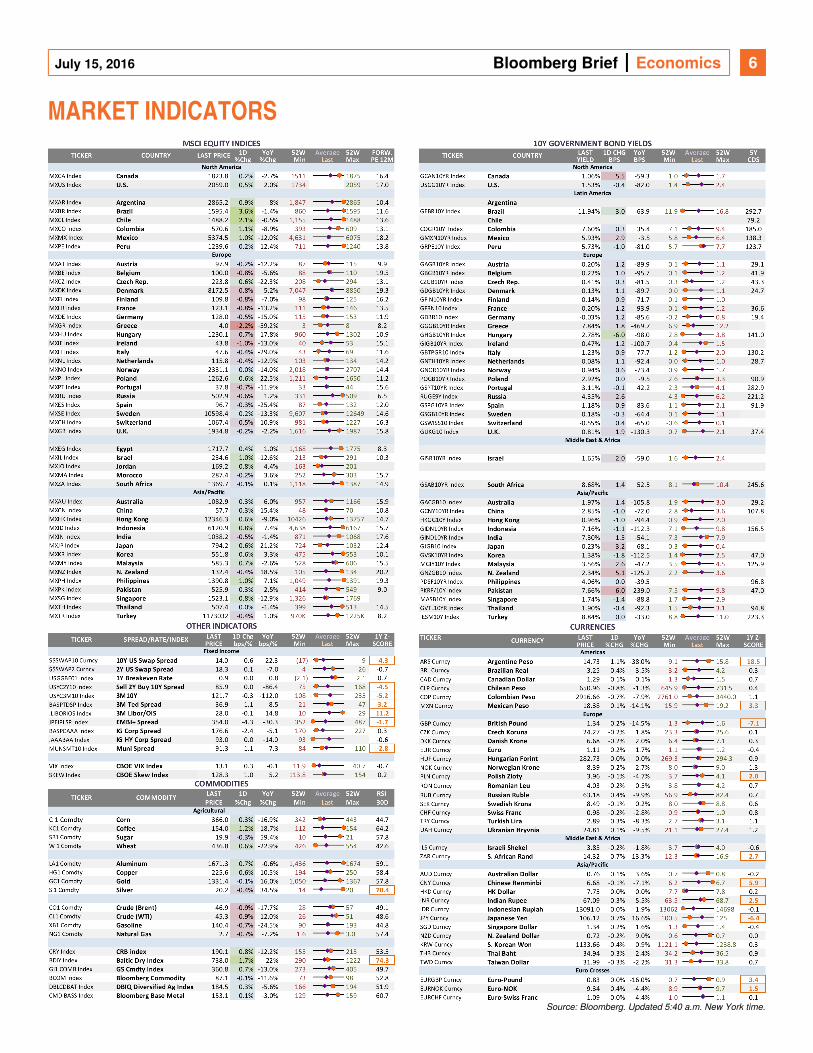

MARKET INDICATORS

Service Inflation Spreading Beyond Rents

Given recent uncertainty regarding the labor outlook, analysts are more focused on real-time indicators of economic output rather than lagging indicators. Still, analysts will monitor the CPI report for increasing evidence of wage pressures feeding into consumer prices, since labor costs are typically the main input cost for most industries. This is particularly true in the service sector, so it is likely to be evident early on in the services ex-rents, ex-energy subcategory, which has been accelerating recently. This should keep upward pressure on the core, despite any renewed weakness on goods prices, due to dollar appreciation.

— Carl Riccadonna and Yelena Shulyatyeva, Bloomberg Intelligence Economists

July 15, 2016 Bloomberg Brief Economics 6

MARKET INDICATORS

SURVEILLANCE WITH KEENE & MCKEE

Source: Bloomberg. Updated 5:40 a.m. New York time.

July 15, 2016 Bloomberg Brief Economics 7

Bloomberg Brief: Economics

SURVEILLANCE WITH KEENE & MCKEE

Ellen Zentner, Chief U.S. Economist for Morgan

Stanley, speaks with Bloomberg's Tom Keene

and Michael McKee about Federal Reserve

monetary policy, the global growth outlook, and

what should most concern investors.

Q: You were one of the earliest calls that the Fed would be on hold. Is the economy the reason we're not seeing the Fed move, or is it externality?A: I think we were right to expect them to wait so long to hike rates last year because we knew that they would be extraordinarily cautious. I can tell you before the summer global growth meltdown last year, I was getting nervous that we were going to be wrong and they were going to hike rates earlier in September, and that global growth meltdown was not in my forecast. So in a way, it saved our expectation that they would wait until December.

But we still have a Fed that's extraordinarily cautious, and I think what I noticed the undercurrent right now is that,because financial conditions have not tightened, and actually on net base eased a bit since Brexit, that people assumed that Brexit won't play into the Fed's thinking at all, particularly for this July meeting, and that things are just fine. So they lose sight of what the economy was like before Brexit where business investment was declining, job growth wasslowing, the credit cycle was turned, this is definitely a late phase of the business

expansion, and that has to play in to monetary policy thinking, regardless of an event like Brexit.

Q: What are the things that investors and people need to be concerned about in this post-Brexit world?A: What I think is that we shouldn't hang our hat on Brexit and that Brexit and the fallout from Brexit is the reason why the Fed would not hike rates further. I want investors to focus on, what was the U.S. economy like before Brexit? Through the second quarter of this year, business investment has declined now for three straight quarters. It's difficult to find that outside of recession. Not saying that this is a recession environment in the U.S., but just noting the risks around U.S. growth that were present even before Brexit. And it's not just an energy story.

In the beginning, when oil prices were dropping, it was all energy investment dragging down overall investment numbers. But you can't escape the incredible run up that we've had in the dollar, not expected to start impacting manufacturing and investment in the U.S. in a bigger way, and so it's broadenedout. The decline in investment is more broad based than just an energy story. Forty percent of the jobs in the U.S., manufacturing jobs in the U.S., these are tied to exports, and global growth matters. Global growth is sluggish. And that's a theme that is present in the U.S. regardless of an event like Brexit.

Q: What's weighing on global growth? How do we get out of this?A: The scary thing is that monetary policy around the world has, for the most part, run its course. And Janet Yellen has beenvery realistic and vocal about expressing that they have limited tools to fight downturns, and that's why they have to beextraordinarily cautious in raising rates further. And I think you could say that's the general theme for the entire global economy. And so, I think something that everyone should be focused on is fiscal policy. Fiscal policy around the globe needs to step up, and I know this sounds like a broken record. We've been calling for it in the U.S. for quite some time, and there's a lot of election uncertainty this year. What will a new president mean for the prospects of greater fiscal policy and fiscal stimulus in the U.S.? I can't see howwe get another impetus to boost global demand and global growth without that.

Q: When will Janet Yellen raise rates?A: We've taken rates off the table for this year. In fact, we've taken rates off the table for the foreseeable future. And we'll see how things play out next year. I just, I don't see this as an economy that needs to have tighter financial conditions, that the Fed needs to step in and slow it, that there's areas of overheating. I just don't see that, and so I think policy makers will come to the conclusion that further rate hikes just don't seem appropriate.

This interview has been edited and condensed.

Bloomberg Brief Managing Editor

Jennifer Rossa

Economics Editors

Ben Baris

James Crombie

Global Director Economic

Research & Chief Economist

Michael McDonough

Chief U.S. Economist

Carl Riccadonna

U.S. Economists

Richard Yamarone

Yelena Shulyatyeva

Reprints & Permissions

Lori Husted

+1-717-505-9701 x2204

Marketing & Partnership Director

Johnna Ayres

+1-212-617-1833

Advertising

Christopher Konowitz

+1-212-617-4694

Economics Terminal Sales

Matthew Traum

+1-212-617-4671

Interested in learning more about

the Bloomberg terminal? Request a

free demo .here

© 2016 Bloomberg LP.

All rights reserved. This newsletter

and its contents may not be

forwarded or redistributed without

the prior consent of Bloomberg.

Please contact our reprints group

listed left for more information.

Related Documents