Future of the Indian power sector

Nov 11, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

India’s Capacity Addition Targets

Plan YearTarget (in MW)

Thermal Hydro Nuclear Total

11th 2007 - 2012 50,757 8,237 3,380 62,374

12th 2012 - 2017 67,686 9,204 2,800 79,690

13th 2017 - 2022 49,200 12,000 18,000 79,200

* 11th Plan target revised after Mid Term Appraisal (MTA)

“Coal shall remain India’s most important energy source till

2031-32 and possibly beyond”

– Report of the Expert Committee on Integrated Energy Policy, Aug’06,

Planning Commission, Govt. of India

• As per the Integrated Energy Policy (IEP) Report, Indian Coal Requirement in 2031 - 32 is projected to be between 1580 – 2555 Million Tons.

• But CIL has set a target of domestic coal production to 839 Million Tons (maximum) by 2025.

• CIL target is therefore way below the annual coal requirement.

India’s Coal Demand Forecast by Forbesin million tons

• Indigenous coal resources enable economic development and can be transformed to guard against import dependence and price shocks.

• India is the 5th largest proven coal reserve in the world and contributes to around 6% of global coal production.

• But, there still exists a supply – demand gap.

• Supply demand Gap has increased at a CAGR of 38.47% from 2008 – 09 to 2011 – 12.

Coal Supply Demand Gap

FinYear

Gap

(Million Tonnes)

Increase in Gap

(wrt ’08-09)

2008 – 09 60.83 –

2009 – 10 90.50 48.77 %

2010 – 11 132.00 117.00 %

2011 – 12 161.50 165.50 %

The Bottlenecks causing Coal Supply – Demand Gap

Stringent environmental laws causing considerable delay in obtaining forestry clearances.Tenancy Land Acquisition and associated Resettlement & Rehabilitation (RR) issues.Growing Naxalism & prominence of coal mafia.Skewed concentration of Coal Deposits.Lack of proper transportation infrastructure & considerable slow progress in development of the same.Monopolistic pattern of the Indian Coal Sector (CIL having 94% market share) Outdated mining technologies & poor maintenance of associated equipmentPoor geophysical mapping (~ 3%) & geochemical mapping (~ 4%) of India’s hard rock area. Institution with a broader scope then GSI required.

• Under New Coal Distribution Policy (NCDP) framework, CIL would only commit up to 50% of TPPs Annual Coal Quantity (ACQ) from domestic sources only.

• Therefore the TPPs are left with no other option but to realize the remaining coal requirement through imports.

• Importing thermal coal seems imperative if a +8% of GDP growth is to be sustained.

Global Coal Trade Flows (as on 2004)

Source: International Energy Agency

World Main Fossil Fuel Reserves (Gigatons of oil equivalent)

Source: World Coal Association

USA: World’s largest coal reserve

• US leads the pack with 237.3 billion tons, i.e. 22.6% of Global proven coal reserve.

• The Powder River Basin of Montana and Wyoming is the single largest source of coal in the US.

• Montana has 74.81 billion tons of estimated recoverable reserves, the most in the US, and Wyoming has 39.19 billion tons of estimated recoverable reserves, second highest reserves in the U.S

• Peabody Energy & Arch Coal are eyeing the Chinese & Indian markets.

• Peabody has stated that global coal shipments to the Asia-Pacific region could reach 140 million metric tons per year, by 2015

• India can therefore have a sizeable chunk of its annual coal requirement from the US

Kazakhstan: Central Asia’s largest coal reserve

• Survey of Energy Resources by World EnergyCouncil in 2010 revealed Kazakhstan to have 33.6billion tons of recoverable coal reserves, 3rd inAsia after China & India.

• By 2014 Kazakhstan plans to boost its annual coalexports to 32 Million tons from present 20 – 22million tons.

• Evident from the geographical proximity, Indiacan surely exercise the option of importing coalfrom Kazakhstan

Facts & Figures…

1. The electricity supply-demand gap in terms of both capacity (MW) and energy (MWh) has been steadily growing in India.

2. Gap as on December 2011 was 13.9%3. Transmission and distribution losses stood at

35 – 45% .

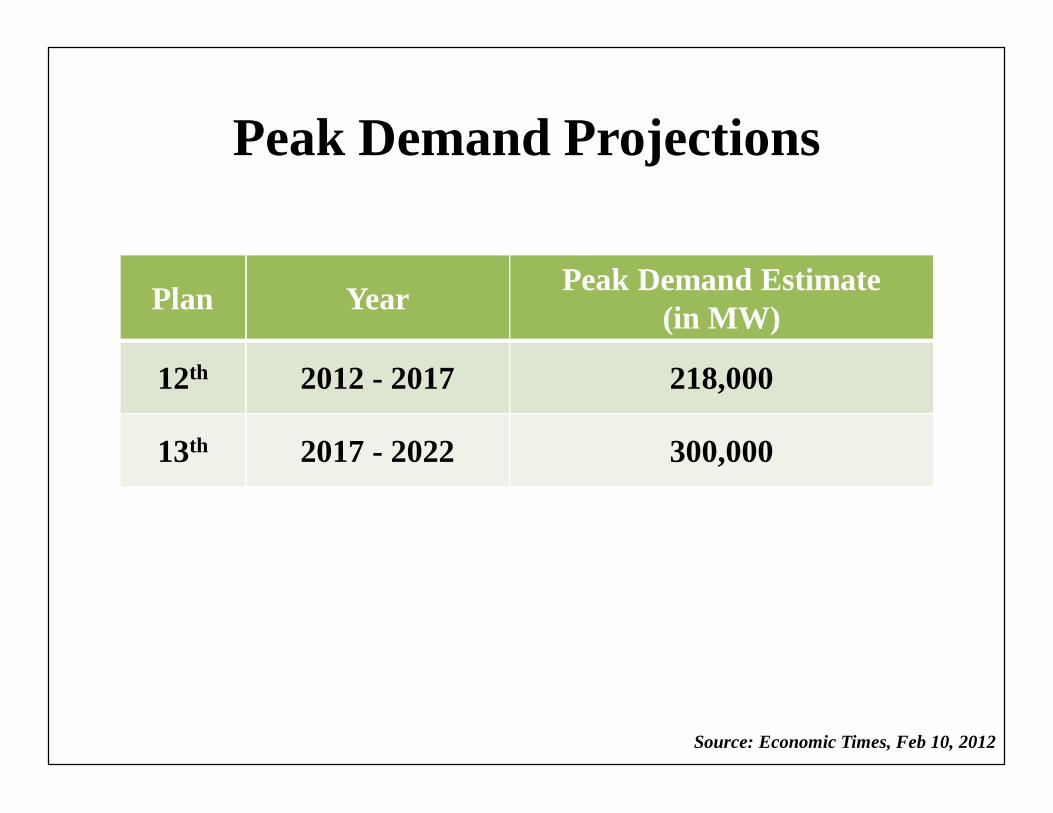

Peak Demand Projections

Plan Year Peak Demand Estimate(in MW)

12th 2012 - 2017 218,000

13th 2017 - 2022 300,000

Source: Economic Times, Feb 10, 2012

With increase in demand, inthe present system thefollowing are augmented:

1) Distribution Infrastructure2) Transmission

Infrastructure3) Generation Capacity

Increased T&D Infrastructurecauses increased T&D losses.Generation capacity needs tobe increased to supply theincreased demand as well asthe increased T&D losses.

Increased generation capacity implies fasterconsumption of energy resources. This shalllead to faster depletion of resources, therebyposing a serious threat to the national energysecurity. To finance increase in T&D &Generation infrastructure, electricity priceswill escalate.

This will definitely burn holes in the commonman’s pocket.

But, electricity demand is bound to increase ina growing economy.

So what is the solution?

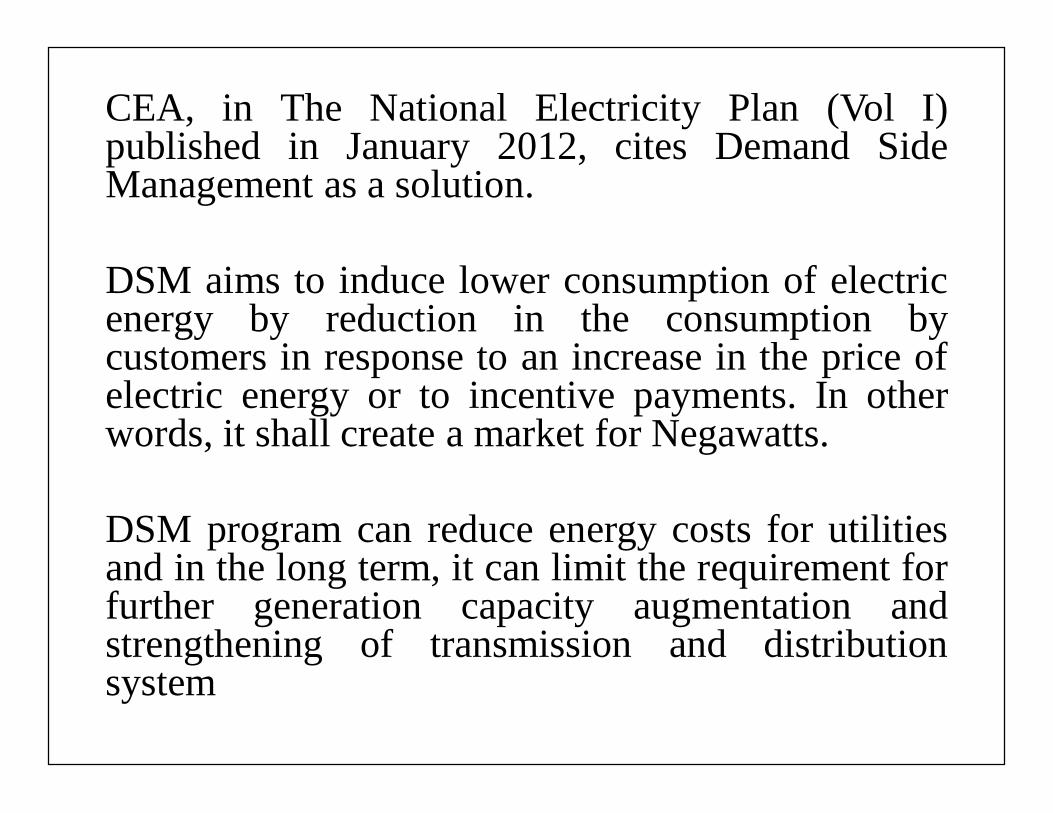

CEA, in The National Electricity Plan (Vol I)published in January 2012, cites Demand SideManagement as a solution.

DSM aims to induce lower consumption of electricenergy by reduction in the consumption bycustomers in response to an increase in the price ofelectric energy or to incentive payments. In otherwords, it shall create a market for Negawatts.

DSM program can reduce energy costs for utilitiesand in the long term, it can limit the requirement forfurther generation capacity augmentation andstrengthening of transmission and distributionsystem

DSM framework in India• Demand Response: Create additional capacity

during peak hours by voluntary load curtailmentby consumers, load shifting or by energyefficiency measures.

• Load Management Programs: real time pricingbased on supply & demand, time-of-use ratestructure

• Smart meters: Enabling communication betweencustomer & DISCOMs informing about rates,demand & supply; enabling accurate real timemeasurements; load connect-disconnect facility

DSM framework as cited by CEA calls for Smart Grid

technology already in vogue, globally.

Smart Grid Characteristic Demand Dispatch Synergy

1)Enable active participation by the consumers

Demand Dispatch will provide incremental motivation for consumer participation by creating opportunities to reduce cost, generate revenues & reduce environmental impacts

2)

Accommodate all generation & storage options

Provides a mechanism for increased penetration of distributed & renewable resources on the grid

3) Enable new products, services & markets

New Demand Dispatch markets attracts consumers & innovations

4) Provide quality power for digital economy

Demand Dispatch applications can include control of power quality and voltage regulation at the feeder level

5) Optimize asset utilization and operate efficiently

Enables complete system optimization by allowing grid operators to coordinate supply & demand to meet reliability, efficiency, economic & environmental goals

6)Anticipate & respond to system disturbance (Self Heal)

Demand dispatch monitoring & control of demand resources enhances the self healing nature of the smart grid. This will virtually eliminate chances of cascading outages

7) Operate resiliently against attack & natural disaster

Demand dispatch monitoring & control of demand resources allows faster restoration from outages. Increased penetration of distributed resources reduces grid vulnerability.

Source: Smart from Start, PwC

Case Study 1: Singapore• In November 2009, the Energy Market Authority (EMA) of Singapore

launched a pilot smart grid test program, the Intelligent Energy System (IES), to develop and test new smart grid technologies and solutions

• IES will permit both providers and consumers the opportunity to make more informed decisions about electricity use.

• IES would enable outage management systems, integration of a growing number of small and variable sources of power into the grid in a ‘plug-and-play’ manner, time-of-use pricing, load shifting in line with time related tariffs.

• The trial achieved an average reduction of overall electricity consumption of 2.4% and a 3.9% reduction in peak usage.

• The trial revealed that not only are the customers benefitted but also peak demand was lowered easing the pressure on generation plants –making for savings in terms of energy infrastructure spend for Singapore.

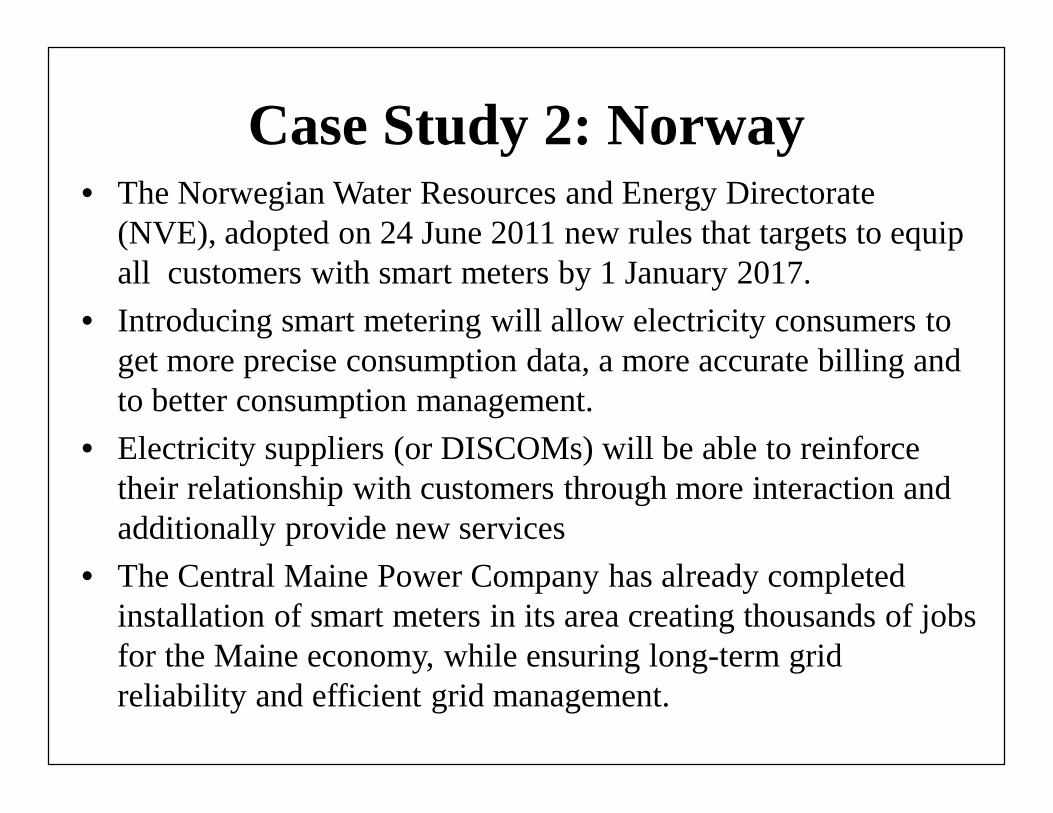

• The Norwegian Water Resources and Energy Directorate (NVE), adopted on 24 June 2011 new rules that targets to equip all customers with smart meters by 1 January 2017.

• Introducing smart metering will allow electricity consumers to get more precise consumption data, a more accurate billing and to better consumption management.

• Electricity suppliers (or DISCOMs) will be able to reinforce their relationship with customers through more interaction and additionally provide new services

• The Central Maine Power Company has already completed installation of smart meters in its area creating thousands of jobs for the Maine economy, while ensuring long-term grid reliability and efficient grid management.

Case Study 2: Norway

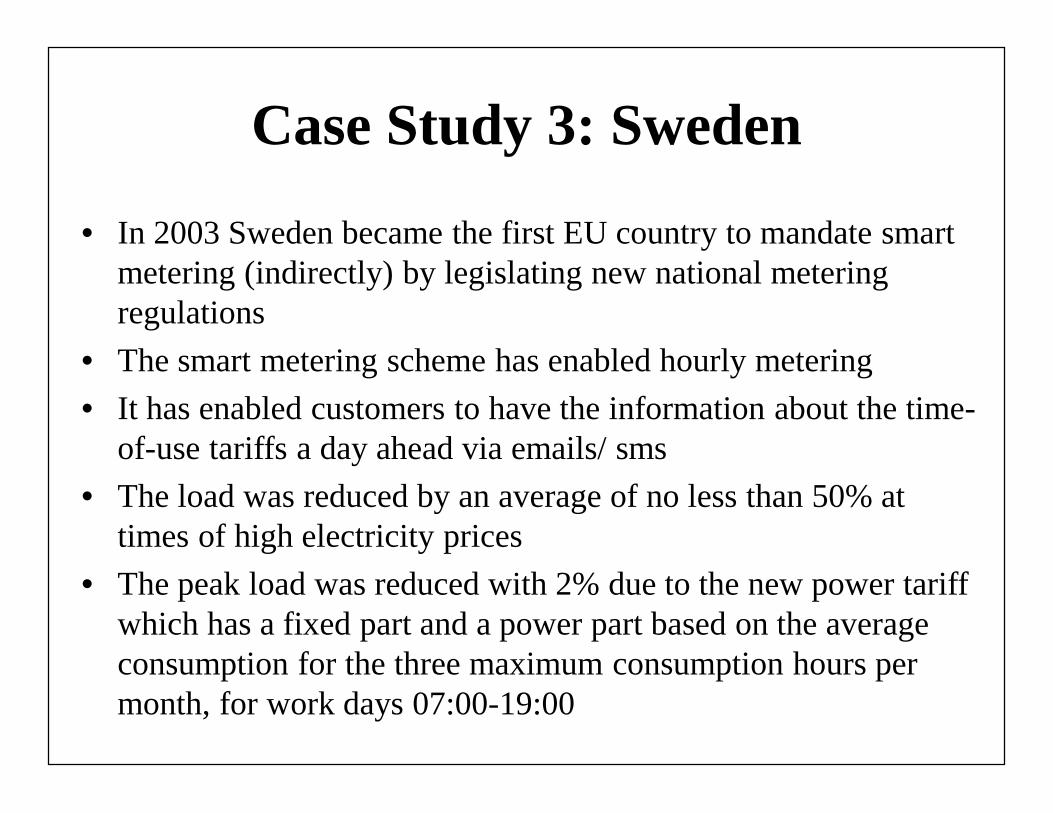

• In 2003 Sweden became the first EU country to mandate smart metering (indirectly) by legislating new national metering regulations

• The smart metering scheme has enabled hourly metering • It has enabled customers to have the information about the time-

of-use tariffs a day ahead via emails/ sms• The load was reduced by an average of no less than 50% at

times of high electricity prices • The peak load was reduced with 2% due to the new power tariff

which has a fixed part and a power part based on the average consumption for the three maximum consumption hours per month, for work days 07:00-19:00

Case Study 3: Sweden

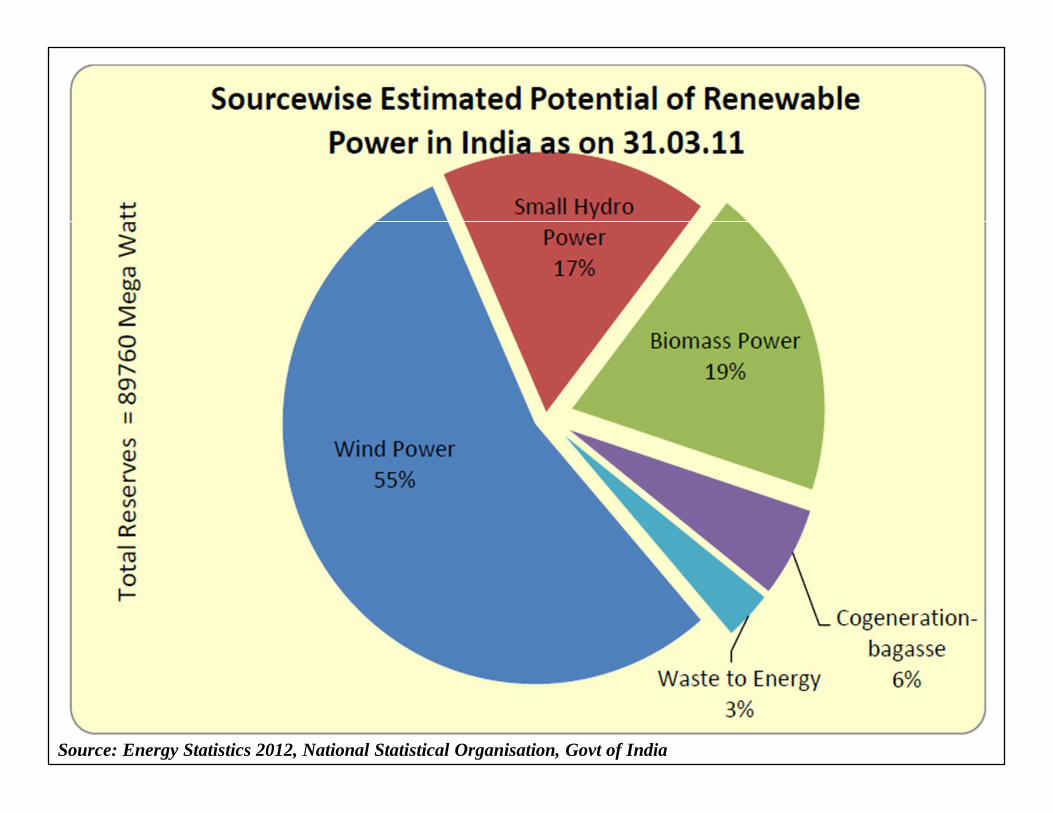

Source: Energy Statistics 2012, National Statistical Organisation, Govt of India

Wind Power• The Indian wind energy sector has an installed capacity of

14158.00 MW (as on March 31, 2011). In terms of wind power installed capacity, India is ranked 5th in the World. Today India is a major player in the global wind energy market.

• The potential is far from exhausted. Indian Wind Energy Association has estimated that with the current level of technology, the ‘on-shore’ potential for utilization of wind energy for electricity generation is of the order of 65,000 MW. The unexploited resource availability has the potential to sustain the growth of wind energy sector in India in the years to come.

• The wind energy generation is expected to increase at an average growth rate of 9% per annum and is expected to reach 7 billion units during FY2011-12

Source: MNRE, Govt of India

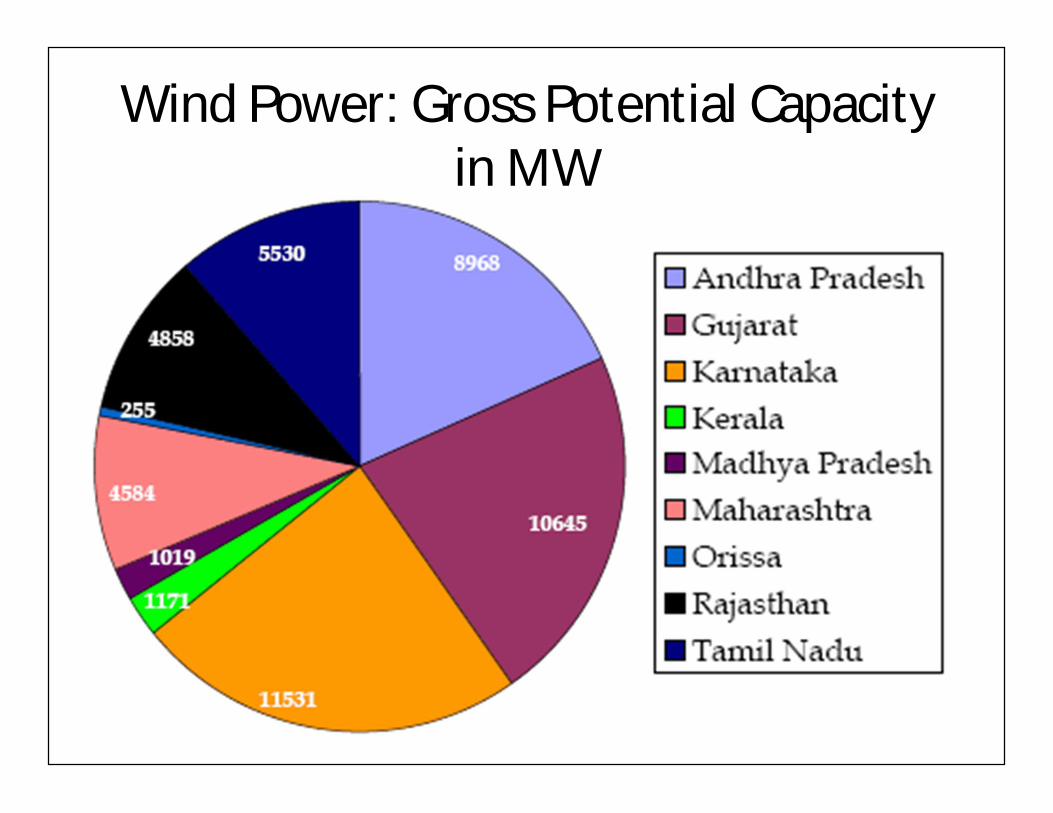

Wind Power: Gross Potential Capacity in MW

Ranking on Wind Index by Ernst & Youngas on May 2012

SOLAR POWER• India has nearly 300 sunny days in most regions, and average

incident solar radiation ranges between 4 to 7 kWh/day/sq.meter— much higher than most other countries.

• The largest state in India, Rajasthan, is roughly the same size asGermany, yet it receives twice the intensity of solar radiation formore than twice the number of days as Germany, which is theworld’s current solar power leader.

• In 2010, India’s solar power capacity was less than 20 MW and the2020 target was larger than the 19,000 MW of existing solar powerworldwide. Now global solar capacity has doubled to 40,000 MWand continues to be one of the world’s fastest growing powertechnologies. India could aim even higher, given the potential andgrowing demand for clean energy.

• Indian industries have responded positively to theMission.

• There were over 400 projects applications in the firstgovernment auction, though only 37 projects wereselected.

• India’s largest industrial conglomerates (Reliance,Tata & Birla) are increasing solar investments, newplayers have emerged, and government entities(ONGC, NTPC, and Bharat Heavy ElectricalsLimited) are implementing large-scale projects

• The key to scaling up solar power lies in its ability tobe cost competitive. KPMG-India predicts that withpolicy support and investment, solar energy couldachieve grid-parity with fossil fuels by 2019-20

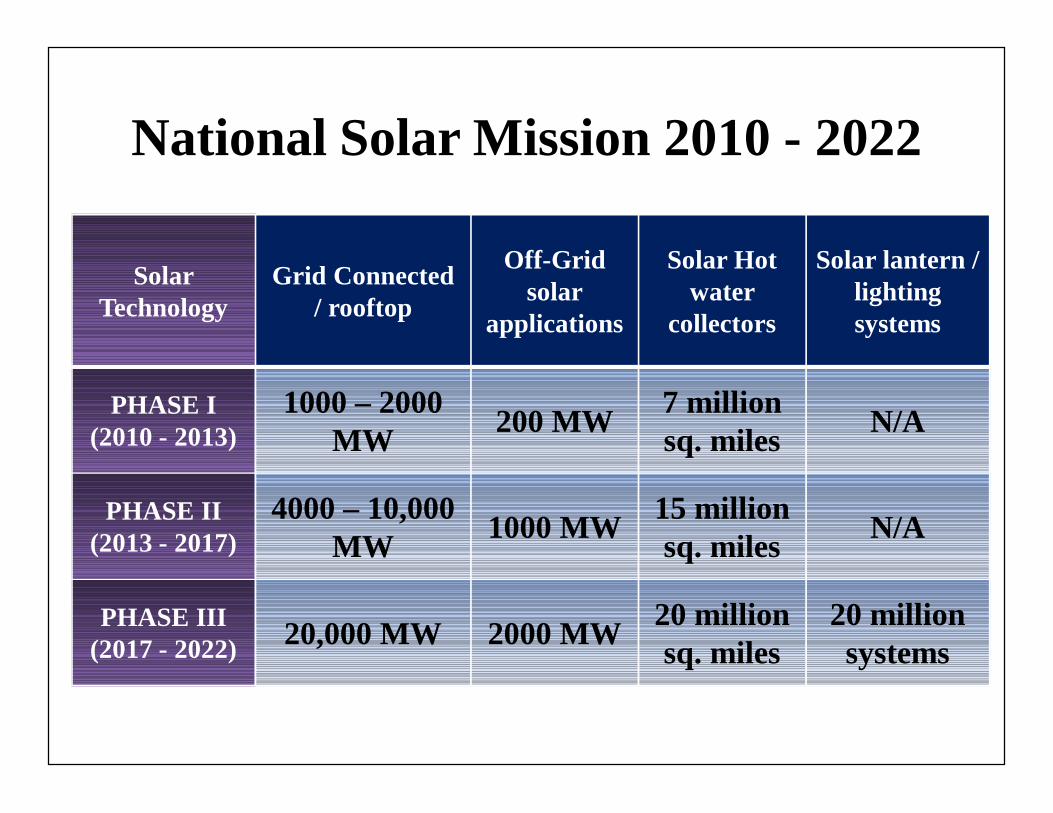

National Solar Mission 2010 - 2022

Solar Technology

Grid Connected / rooftop

Off-Grid solar

applications

Solar Hot water

collectors

Solar lantern / lighting systems

PHASE I (2010 - 2013)

1000 – 2000 MW 200 MW 7 million

sq. miles N/A

PHASE II (2013 - 2017)

4000 – 10,000 MW 1000 MW 15 million

sq. miles N/A

PHASE III (2017 - 2022) 20,000 MW 2000 MW 20 million

sq. miles20 million systems

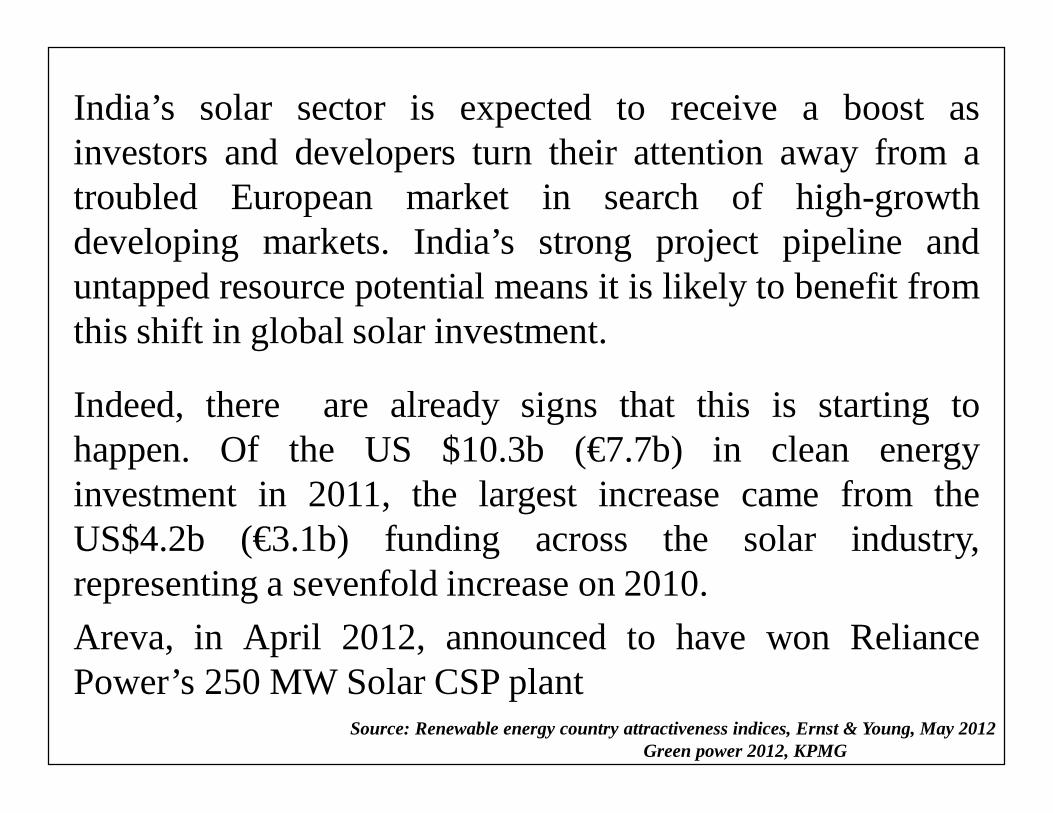

India’s solar sector is expected to receive a boost asinvestors and developers turn their attention away from atroubled European market in search of high-growthdeveloping markets. India’s strong project pipeline anduntapped resource potential means it is likely to benefit fromthis shift in global solar investment.

Indeed, there are already signs that this is starting tohappen. Of the US $10.3b (€7.7b) in clean energyinvestment in 2011, the largest increase came from theUS$4.2b (€3.1b) funding across the solar industry,representing a sevenfold increase on 2010.Areva, in April 2012, announced to have won ReliancePower’s 250 MW Solar CSP plant

Source: Renewable energy country attractiveness indices, Ernst & Young, May 2012Green power 2012, KPMG …………………..

Ranking on Solar Index by Ernst & Youngas on May 2012

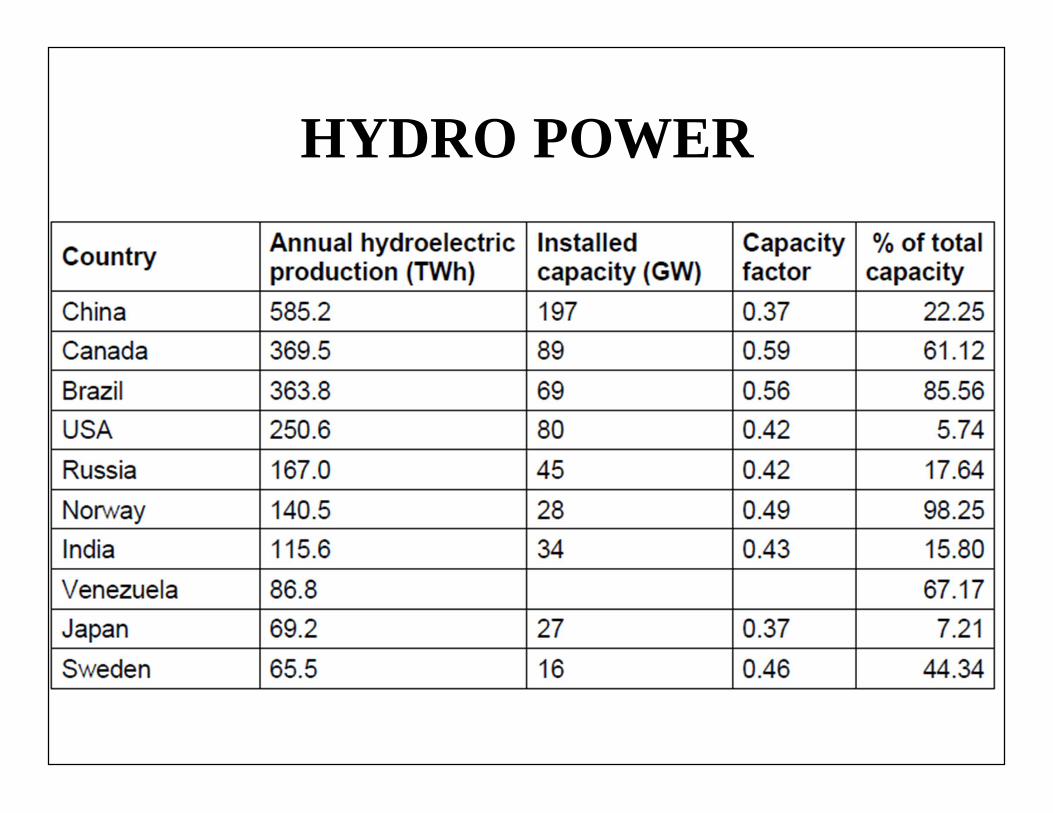

HYDRO POWER

• Only 23% of India’s hydro power potential hasbeen harnessed so far.

• Additional hydropower capacity is desirable inIndia’s generation mix, as it provides the systemoperator with technically vital flexibility to meetthe changes in demand. The high density ofhousehold demand in India means that thesystem can experience a peaking load ofanything between 20,000 to 30,000 MW. Thissudden spurt in demand can be best met byhydropower plants which have the ability to startup and shut down quickly

Limitations of Hydro Projects• Away from load centres; evacuation of power is big problem• Environmental/ Ecological & RR problems due to submergence/

construction activities• Difficulty in Investigations/ Implementation due to remoteness

of the area• Long Gestation periods

• Lack of availability of long term finance

• Geological surprises resulting in time and cost over-runs• Hydro projects suffer from production risks since the project is

planned based on the historical data which may not occur infuture

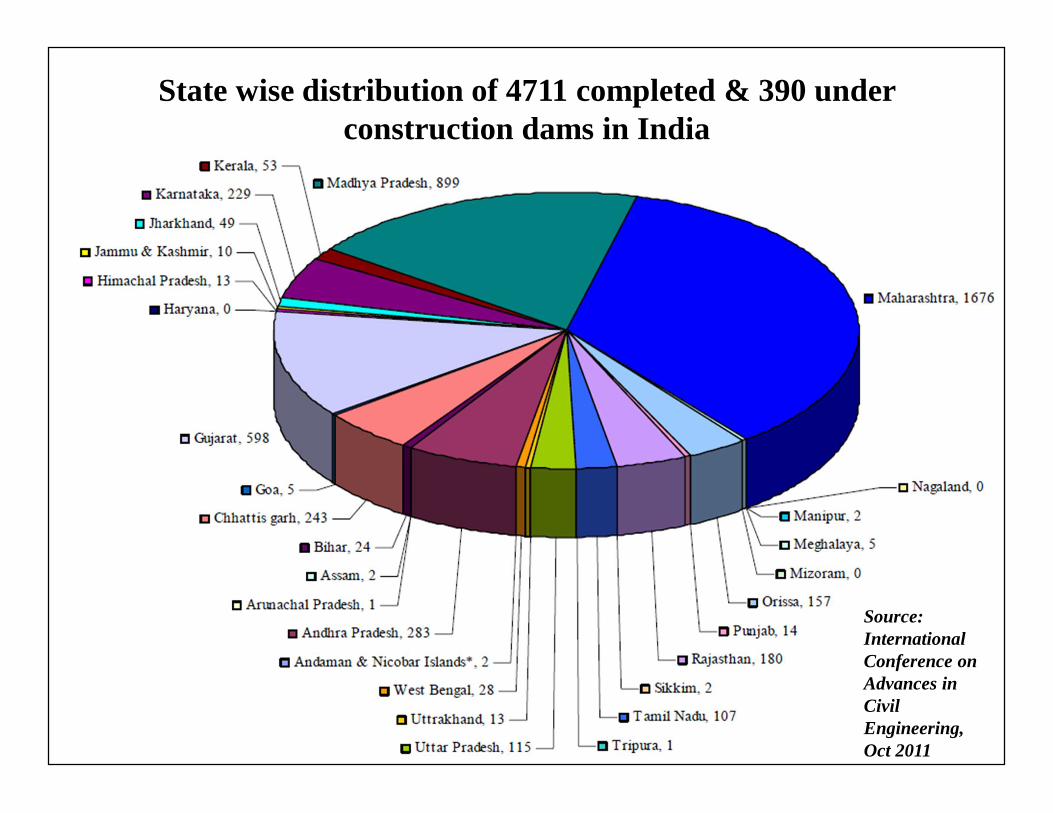

State wise distribution of 4711 completed & 390 under construction dams in India

Source: International Conference on Advances in Civil Engineering, Oct 2011

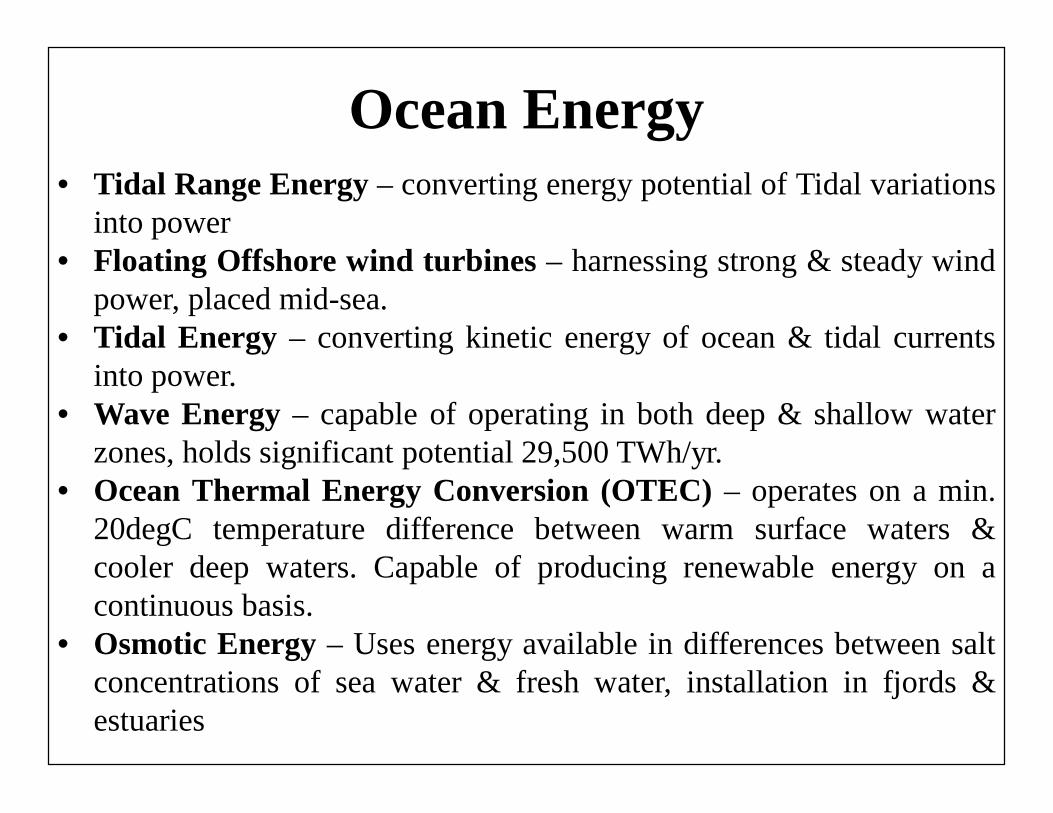

Ocean Energy• Tidal Range Energy – converting energy potential of Tidal variations

into power• Floating Offshore wind turbines – harnessing strong & steady wind

power, placed mid-sea.• Tidal Energy – converting kinetic energy of ocean & tidal currents

into power.• Wave Energy – capable of operating in both deep & shallow water

zones, holds significant potential 29,500 TWh/yr.• Ocean Thermal Energy Conversion (OTEC) – operates on a min.

20degC temperature difference between warm surface waters &cooler deep waters. Capable of producing renewable energy on acontinuous basis.

• Osmotic Energy – Uses energy available in differences between saltconcentrations of sea water & fresh water, installation in fjords &estuaries

Biomass Energy

• Biomass energy is the utilization of organicmatter present and can be utilized for variousapplications:– Biomass can be used to produce heat and electricity, or

used in combined heat and power (CHP) plants.– Biomass can also be used in combination with fossil

fuels (co-firing) to improve efficiency and reduce thebuild up of combustion residues.

– Biomass can also replace petroleum as a sourcefor transportation fuels

Biomass Energy in India• India produces about 450-500 million tonnes of biomass per year. Biomass provides

32% of all the primary energy use in the country at present.• The potential in the short term for power from biomass in India varies from about

18,000 MW, when the scope of biomass is as traditionally defined, to a high of about50,000 MW if one were to expand the scope of definition of biomass.

• The current share of biofuels in total fuel consumption is extremely low and isconfined mainly to 5% blending of ethanol in gasoline, which the government hasmade mandatory in 10 states.

• Currently, biodiesel is not sold on the Indian fuel market, but the government plansto meet 20% of the country’s diesel requirements by 2020 using biodiesel.

• Plants like Jatropha curcas, Neem, Mahua and other wild plants are identified as thepotential sources for biodiesel production in India.

• There are about 63 million ha waste land in the country, out of which about 40million ha area can be developed by undertaking plantations of Jatropha. India usesseveral incentive schemes to induce villagers to rehabilitate waste lands through thecultivation of Jatropha.

• The Indian government is targeting a Jatropha plantation area of 11.2 million ha by2012.

Solar Thermal Energy

Various commercial power plant developmentprojects with unit outputs of 50 to 310 MWe andlarge solar fields of parabolic trough collectorsare currently promoted or are in a progressiveplanning stage by European and U.S. projectdevelopers with grants of the World Bank/GEFor other co-funds world – wide.

• Greece: 50 MWe solar thermal power plant THESEUS on theCrete island; promoted by German and Greece companies; solarfield of approximately 300,000 m2;, 112 GWh of pure solarelectricity per year

• Spain: Various 50 MWe plants group in southern Spain;promoted by international industrial group; based on the newRoyal Decree on the support of renewable electricity generation

• Egypt: 135 MWe natural-gas-fired ISCCS plant in Kuraymat atthe Nile river; 30 MWe equivalent solar capacity; promoted byindustrial groups; with allocated 40 to 50 million US$ GEFgrant.

• Morocco: 150 MWe natural-gas-fired ISCCS plant project; 30 to50 MWe equivalent solar capacity; promoted by industrialgroups; with allocated 40 to 50 million US$ GEF grant.

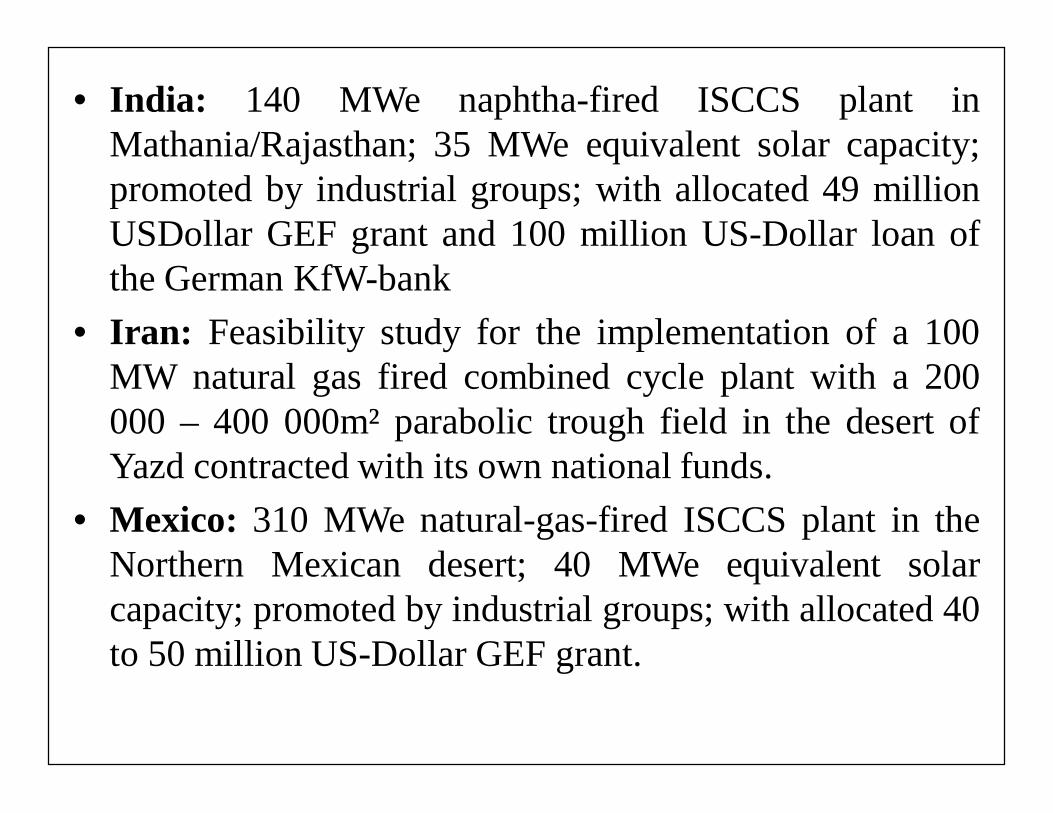

• India: 140 MWe naphtha-fired ISCCS plant inMathania/Rajasthan; 35 MWe equivalent solar capacity;promoted by industrial groups; with allocated 49 millionUSDollar GEF grant and 100 million US-Dollar loan ofthe German KfW-bank

• Iran: Feasibility study for the implementation of a 100MW natural gas fired combined cycle plant with a 200000 – 400 000m² parabolic trough field in the desert ofYazd contracted with its own national funds.

• Mexico: 310 MWe natural-gas-fired ISCCS plant in theNorthern Mexican desert; 40 MWe equivalent solarcapacity; promoted by industrial groups; with allocated 40to 50 million US-Dollar GEF grant.

Future after Fukushima

Nuclear Energy : Future after Fukushima

• In view of the looming climate crisis and dwindling fossil fuelsreserves – peak oil just to mention one – nuclear energy waspropagated in the past decade as a CO2-free, safe and secure,cheap solution to global energy problems.

• But post-Fukushima, international energy policy is at acrossroads. There have been more or less clear signs ofrethinking on the parts of governments in a number ofcountries, including Germany, Switzerland, China and noweven Japan, indicating that they are considering picking up thepace in a fundamental change in energy policy.

• Japan and Germany, the 3rd & the 4th largest economies in theworld have decided to phase out nuclear energy and base futuregrowth more on renewable energies.

• A commercial-type power reactor simply cannot, under any circumstances,explode like a nuclear bomb - the fuel is not enriched beyond about 5%

• Every country which operates nuclear power plants has a nuclear safetyinspectorate and all of these work closely with the IAEA, responsible forglobal nuclear safety.

• Apart from Chernobyl, no nuclear workers or members of the public have everdied as a result of exposure to radiation due to a commercial nuclear reactorincident. Most of the serious radiological injuries and deaths that occur eachyear (2-4 deaths and many more exposures above regulatory limits) are theresult of large uncontrolled radiation sources, such as abandoned medical orindustrial equipment

• No industrial activity can be represented as entirely risk-free. Incidents andaccidents may happen, and as in other industries, & will lead to progressiveimprovement in safety.

• But there is a concern about nuclear waste disposal.

Nuclear Energy : Safety Issues

Nuclear Energy : Climate Change Debate

• Contrary to popular belief, CO2 emissions of nuclear energy inconnection with its production – depending on where the raw materialuranium is mined and enriched – amounts to between 7 and 126gCO2equ/kWh (GEMIS 4.7), one-third as much GHGs as large moderngas power plants.

• So, nuclear energy is not free of CO2 emissions, as often they aretouted.

• Krypton 85 is produced in nuclear power plants and is released on amassive scale in reprocessing.

• A product of nuclear fission, Krypton 85 ionizes the air more than anyother radioactive substance

• Though Krypton 85 levels in the atmosphere have reached a recordhigh, surprisingly it has not received any attention in internationalclimate-protection negotiations till date.

Country Perspective: Brazil

Hydro72.30%

Thermal18.60%

Biomass6.60%

Nuclear1.80%

Wind Power0.70%

Brazil’s power demand is mostlycatered by Hydro-electricity.Angra 1 (657 MW) & Angra 2 (1350MW) are the operating 2 Nuclearpower plants. Angra 3 is underconstruction is expected to beginoperating from 2015.

According to the Brazilian NationalEnergy Plan, installed nuclear capacitywould be 33GW by 2030, accountingfor 4.9 % of total installed capacity. Toprevent melting of fuel rods due tofailure of reactor cooling pumps, aswas the case for Fukushima, smallhydroelectric plants & dedicated powertransmission lines are planned.

Country Perspective: Brazilcontinued

The experience gathered from the design, construction, and operation ofAngra 1, 2, and 3, as well as having 5th largest uranium reserve in the world(309,000 tons), has made Brazil showcase Nuclear energy as a highlycompetitive energy alternative to a guaranteed energy self – sufficiency.Brazil has the potential of wind energy to the tune of 143 GW but only 794MW has been installed. The potential for co-generation using sugarcanebagasse is estimated at around 8 GW, in addition to the possibility for usingbiogas for electrical energy generation. Furthermore, the potential for usingsolar energy, both thermal and photovoltaic, is extraordinary. T&D lossesare 15% which can be reduced to 10%, adding 46,000 GWh every year tothe Brazilian Grid. Extensive R&M of hydroelectric plants that have beenoperating for more than 20 years can contribute to 8000 MW increasedgeneration.Thus, nuclear energy would become absolutely unnecessary as analternative for satisfying Brazil’s energy demands.

Country Perspective: GermanyOn 14th March 2011, 3 days after Fukushima disaster, a three-monthmoratorium was announced as an immediate measure, during whichthe seven oldest German nuclear power plants and the Krümmelreactor in Schleswig-Holstein, which was prone to malfunction, wereto be taken off the grid. This was exactly opposite to what was decidedby the Merkel govt. in September 2010, just 6 months prior toFukushima.

Within a few days, 8,400 MW of nuclear capacity – approx. 41% ofthe total German nuclear power capacity (20,500 MW) – was nolonger available. Complete phase out of installed nuclear capacity isplanned to be within 2022.

Though the decision is understood to be more political, it willinevitably entail a huge increase in the use of renewable energies andrapid improvements in energy efficiency.

Country Perspective: IndiaNuclear power was being given priority by the Indian Govt, as evidentfrom the ambitious 18 GW target set for 13th Plan. India has the world'shighest thorium reserves of 360,000 tons. Thorium can be used withrecycled uranium to fuel reactors. Thus, the argument for nuclear powercame from an energy security angle as well as a climate change angle.But future of the 9.9GW Jaitapur Nuclear Power Project, the US$9.3bnproject, seems bleak as the left and the right wings of civil society havejoined to create a formidable opposition, post Fukushima. NPCIL has notbeen able to provide concrete evidence to support the nuclear programenvisaged. The response of the Indian media is such that it cannot becategorized as being pro- or anti- nuclear, and therefore cannot help tobuild a concrete opinion.

But again the growing economy as India is, energy security is required tofuel the economic growth. The lone option therefore remains as of now isto look for alternative energy resources, which India has plenty.

Related Documents