Fundraising NOT Everything Startups would like to know about the process of convincing VC to invest Perspective - Poland

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Fundraising

NOT Everything Startups would like to know about the

process of convincing VC to invest

Perspective - Poland

INVESTMENT PROCESS

Knowing The Game

Startup stages of development

Beta

Alfa

Scaling

Idea

Feedback

from customers

MVP

Time

When asking for investment?

• AS LATE AS POSSIBLE BUT…

• FFFF• Idea

• BA• Idea

• Prototype

• Seed funds• Idea

• Prototype / MVP

• First Client(s)

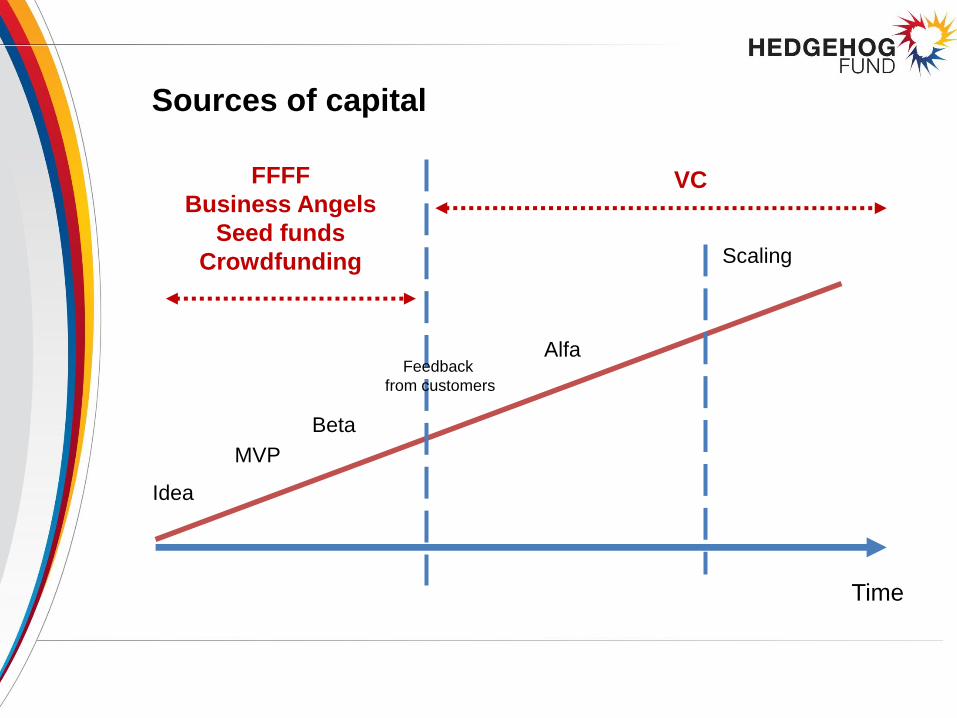

Sources of capital

FFFF

Business Angels

Seed funds

Crowdfunding

VC

Beta

Alfa

Scaling

Idea

Feedback

from customers

MVP

Time

Investments (PL perspective)

FFFF ~ 100 k PLN *

BAs

~ 100–500 k PLN *

Seed funding

~ 500 k – 2 M PLN *

Crowdfunding

~ 1 M PLN

Early Stage

Round A

~ 3–8 M PLN *

Time

Later Stage

Round B, C+…

~ >15 M PLN *

VCs

* Flexible

Shares

FFFF ~ 0–10%

BAs

~ 5–20% *

Seed funding

~ 5–30% **

Equity crowdfunding

~ 5–30%

Early Stage

Round A

~ 20–35% **

Time

Later Stage

Round B, C+…

~ 30–70%

* Flexible

** The higher initial % of shares taken by BA/VC the bigger issue for later rounds

VCs

VENTURE CAPITAL

Knowing Your Partner

Sources of projects for VC

Referrals /

Hunters

Conferences

/ Meetups

Incubators /

accelerators

Inbound /

www

applications

Open Hours

Valuations

• Different industries / business models = different valuations

• Market potential is important, but…

• Valuations based on i.e.:

– Current value of the team / technology / IP

– To recreate the project from scratch

– Benchmarking to other transactions („apple to apple”)

– Financial indicators (i.e. Net Rev., EBITA)

– Metrics Multiples (i.e. MRR, TTM)

– DCF

– Demand of the crowd

• IMHO Valuation is a metrics driven game. More you know about your (and your competitors) metrics - the better.

How a VC works?

• Time limit (5-10 years; usually 7-10 years)

• 2 and 20 rule

– Approx. 2% of management fee (yearly)

– Approx. 20% of management carry (success fee)

• In Poland the financial efficiency of funds starts from approx. min.

30 mln PLN

• Usually investors expect 3x CoC (Cash on Cash) return from the

fund (all portfolio)

– IRR approx. 25%

• Example of fund’s portfolio return:

– 15 projects:

• 9 projects = 0 return

• 3 projects = 2-3x CoC

• 2 projects = 5-7x CoC

• 1 project = 10-50x CoC

How the process works?

Application / Teaser

Project evaluation

Investment

Committee

Term Sheet /

Invest. agreement

SHA1-2

w.

2-8

w.

1-2

w.

4-8

w.

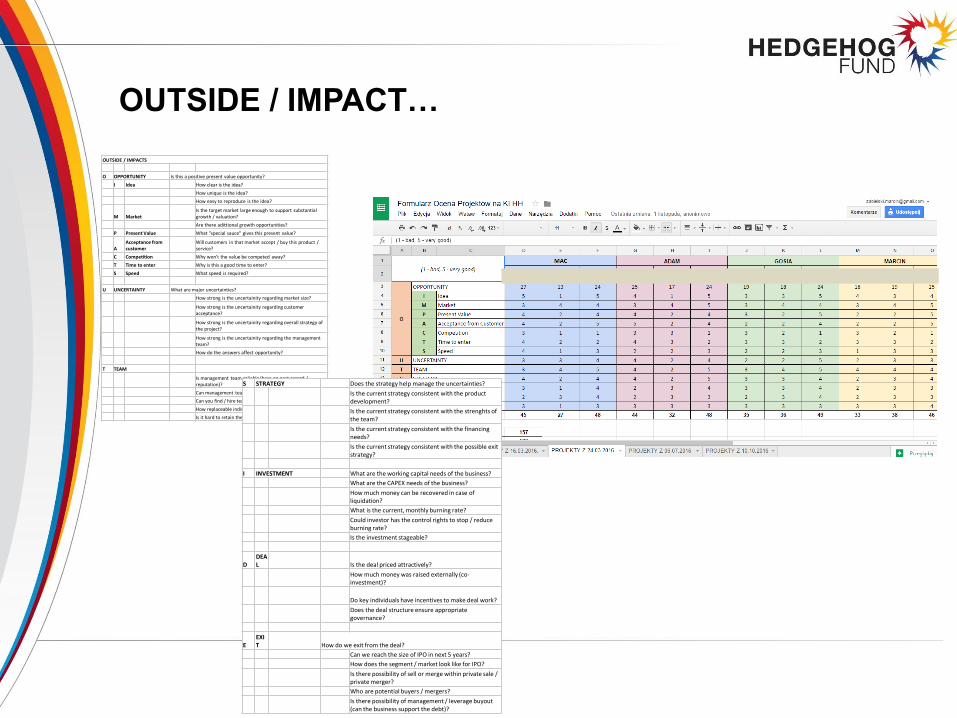

OUTSIDE / IMPACT…

OUTSIDE / IMPACTS

O OPPORTUNITY Is this a positive present value opportunity?

I Idea How clear is the idea?

How unique is the idea?

How easy to reproduce is the idea?

M MarketIs the target market large enough to support substantial growth / valuation?

Are there adittional growth opportunities?

P Present Value What "special sauce" gives this present value?

AAcceptance from customer

Will customers in that market accept / buy this product / service?

C Competition Why won't the value be competed away?

T Time to enter Why is this a good time to enter?

S Speed What speed is required?

U UNCERTAINTY What are major uncertainties?

How strong is the uncertainity regarding market size?

How strong is the uncertainity regarding customer acceptance?

How strong is the uncertainity regarding overall strategy of the project?

How strong is the uncertainity regarding the management team?

How do the answers affect opportunity?

T TEAM

Is management team reliable (base on past record / reputation)?

Can management team implement opportunity?

Can you find / hire team with skills you need?

How replaceable individual members are?

Is it hard to retain them longterm?

S STRATEGY Does the strategy help manage the uncertainties?

Is the current strategy consistent with the product development?

Is the current strategy consistent with the strenghts of the team?

Is the current strategy consistent with the financing needs?

Is the current strategy consistent with the possible exit strategy?

I INVESTMENT What are the working capital needs of the business?

What are the CAPEX needs of the business?

How much money can be recovered in case of liquidation?

What is the current, monthly burning rate?

Could investor has the control rights to stop / reduce burning rate?

Is the investment stageable?

DDEAL Is the deal priced attractively?

How much money was raised externally (co-investment)?

Do key individuals have incentives to make deal work?

Does the deal structure ensure appropriate governance?

EEXIT How do we exit from the deal?

Can we reach the size of IPO in next 5 years?

How does the segment / market look like for IPO?

Is there possibility of sell or merge within private sale / private merger?

Who are potential buyers / mergers?

Is there possibility of management / leverage buyout (can the business support the debt)?

For an investor you’d need…

• Teaser

• Business plan

• Presentation (short / long)

• Financial plan / budget

…but do not forget about i.e.:

• Team members’ more detailed CVs

• References from existing customers („investors love testimonials”)

• Results of market research

• Benchmarks

• More detailed competitive analysis

• Product / site documentation

• Access to statistics

• Legal docs (shareholders agreement, GIODO, other IP docs, patents)

Presentation for an

Investment Committee

• Pitching:

– 20-30 min. = 10-12 slides

– 3 min = do not bother with this VC

• Content (examples of slides)

1. What we do? (1 sentence; problem we solve)

2. Who we are? (team and experiences)

3. How we would like to make money?

4. Demo

5. What is our „Secret Sauce” / unfair advantage?

6. What is market potential?

7. What is our competition / does such a business works anywhere? („think widely”)

8. Go To Market Strategy / KPIs to be achieved

9. What we need and what we offer? (money, know-how, contacts, shares, valuation)

Golden Rules (1)

• Prepare yourself - „You’ll never have a second chance to make the

first impression”

• Materials are important

– Teaser

– Presentation

– Budget

• Make your research - chose right investor

– What is the funds size?

– How much do they invest?

– What kind of projects do they invest in / specialization

– Know VC Partners and their experiences (prior investments, portfolio)

– Ask for opinions

– Decide on what kind of investor you need (money only, money+specific

knowledge, money+contacts)?

Golden Rules (2)

• You can easily find Investors

– „Google is your best friend”

– PSIK

– Lists / Google Docs

– Meetings and conferences

– LI / FB

• Chose 10 investors and prioritize them (i.e. money, know-how, „chemistry”, bureaucracy), and:

– Chose 5 investors from the bottom and talk to them• The best way is to be presented / referred by someone

• Send your materials… and monitor if it was read

– Get feedback and correct your materials

– Present corrected pitch to 5 most desired investors

• Investors are busy! There are approx. 30 projects per VC Partner per month which is more than 1 daily to be evaluated. To be successful you have to be determined. Call, write and ask about current status. If you cannot do this at this stage, what can investor expect from you later on?

Golden Rules (3)

• At the meeting– Show your passion

– Show your knowledge (market, product, competition)

– Be flexible

– Talk and Listen

– Ask the investor Qs !!!• What the % has already been spent? How many projects are in current portfolio?

What are the av. Rounds (money, % shares)?

• Do they co-invest? With whom? Are they taking a role of lead investor? How often?

• What are the rules for follow-ons (next round investments)? Do they have budget reserved for it?

• The only goal from the Initial Meeting is to set up next one

• After getting positive, initial decision try to fix legal issues– Ask for an example of term sheet with all clauses

– Do not fight for not important paragraphs

– Take good lawyer

• Listen to investors / mentors… – …but act independently

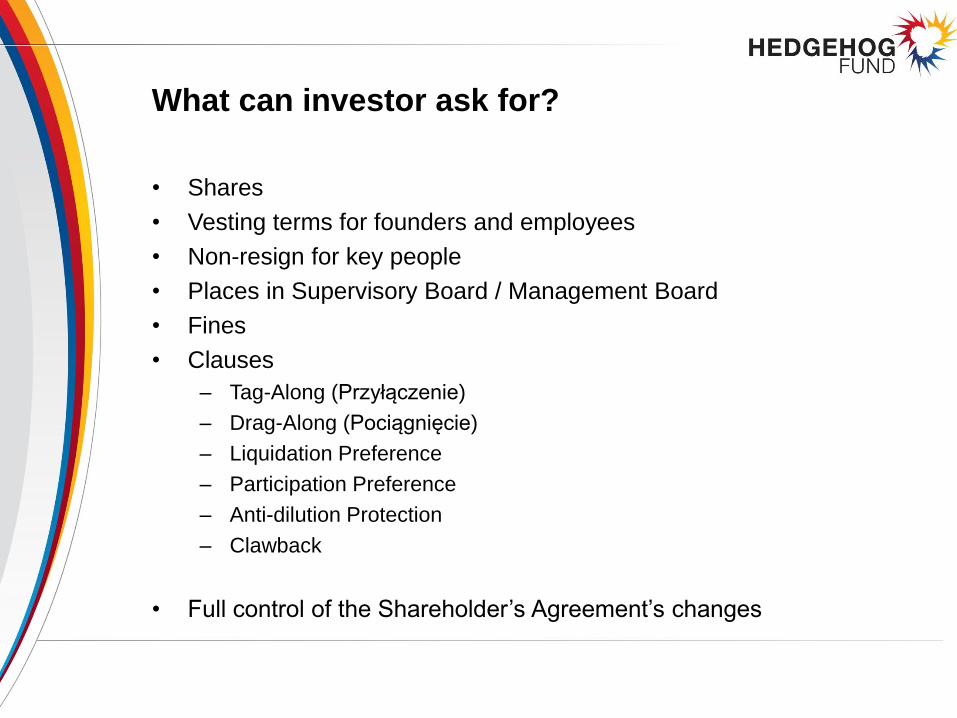

What can investor ask for?

• Shares

• Vesting terms for founders and employees

• Non-resign for key people

• Places in Supervisory Board / Management Board

• Fines

• Clauses

– Tag-Along (Przyłączenie)

– Drag-Along (Pociągnięcie)

– Liquidation Preference

– Participation Preference

– Anti-dilution Protection

– Clawback

• Full control of the Shareholder’s Agreement’s changes

THANK YOU

WWW.HEDGEHOGFUND.PL

WWW.FACEBOOK.COM/HEDGEHOGFUND

http://about.me/marcinzabielski

http://www.linkedin.com/in/marcinzabielski

http://twitter.com/marcinzabielski

Worth to read…

• Lean Startup

– http://theleanstartup.com/principles

• Business Model Canvas

– https://canvanizer.com/new/business-model-canvas

• Teaser

– http://www.slideshare.net/zabiel/startup-teaser-v1example

• OUTSIDE / IMPACTS

– http://faculty.chicagobooth.edu/steven.kaplan/research/kss%20ppt.pdf

• Investment Committee presentation

– http://www.slideshare.net/QuintinAdamis/pitch-deck-template-by-guy-

kawasaki

• Term Sheet

– http://www.slideshare.net/zabiel/term-sheet-hedgehog-fund-wzr

Related Documents