© OECD/IEA 2014 Renewables and climate change mitigation Cédric Philibert On behalf of Paolo Frankl, Head, Renewable Energy Division International Energy Agency Our Common Future under Climate Change – Paris – 9 July 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© OECD/IEA 2014

Renewables and climate change mitigation

Cédric Philibert

On behalf of Paolo Frankl,

Head, Renewable Energy Division International Energy Agency

Our Common Future under Climate Change – Paris – 9 July 2015

© OECD/IEA 2015

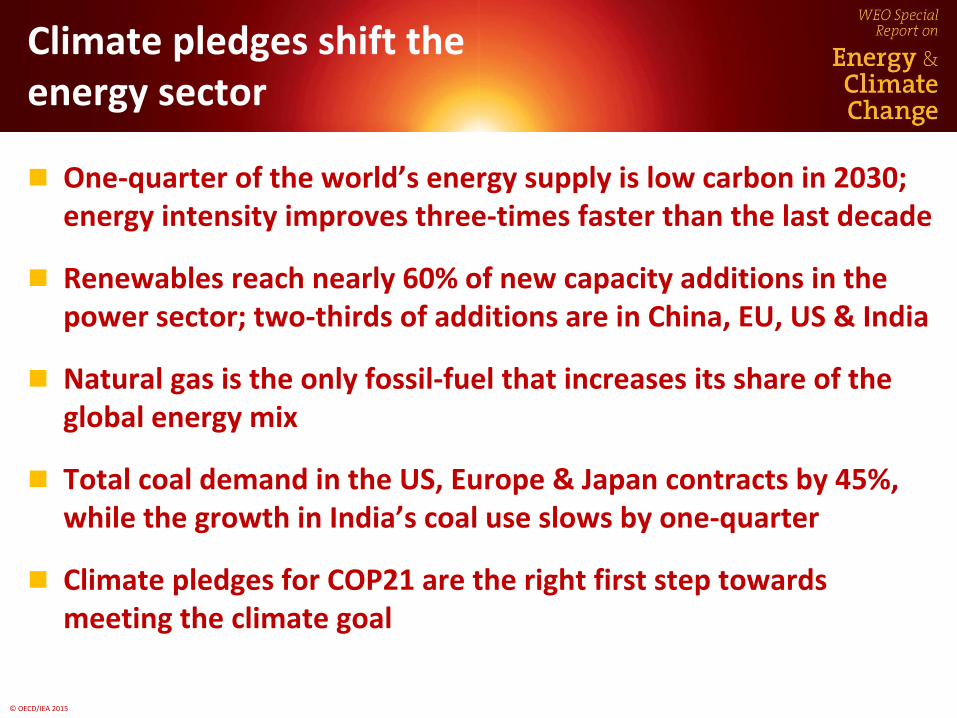

Climate pledges shift the energy sector

One-quarter of the world’s energy supply is low carbon in 2030; energy intensity improves three-times faster than the last decade

Renewables reach nearly 60% of new capacity additions in the power sector; two-thirds of additions are in China, EU, US & India

Natural gas is the only fossil-fuel that increases its share of the global energy mix

Total coal demand in the US, Europe & Japan contracts by 45%, while the growth in India’s coal use slows by one-quarter

Climate pledges for COP21 are the right first step towards meeting the climate goal

© OECD/IEA 2015

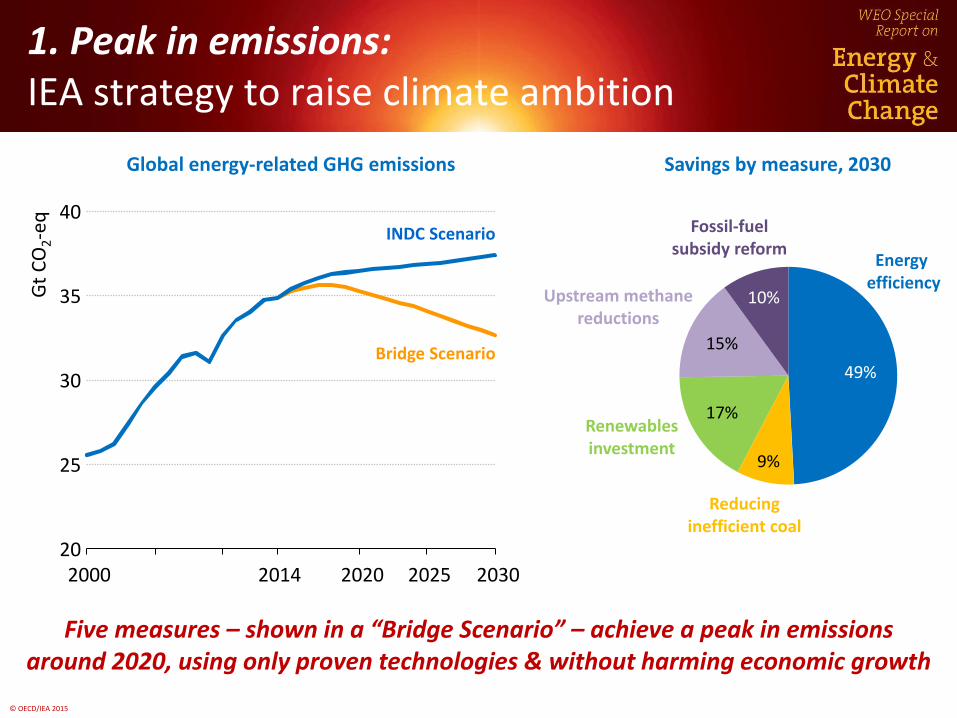

1. Peak in emissions: IEA strategy to raise climate ambition

Global energy-related GHG emissions

Five measures – shown in a “Bridge Scenario” – achieve a peak in emissions around 2020, using only proven technologies & without harming economic growth

20

25

30

35

40

2000 2014 2020 2025 2030

Gt

CO

2-e

q

Bridge Scenario

INDC Scenario

Energy efficiency

49%

Reducing inefficient coal

Renewables investment

Upstream methane reductions

Fossil-fuel subsidy reform

17%

15%

10%

Savings by measure, 2030

9%

© OECD/IEA 2013

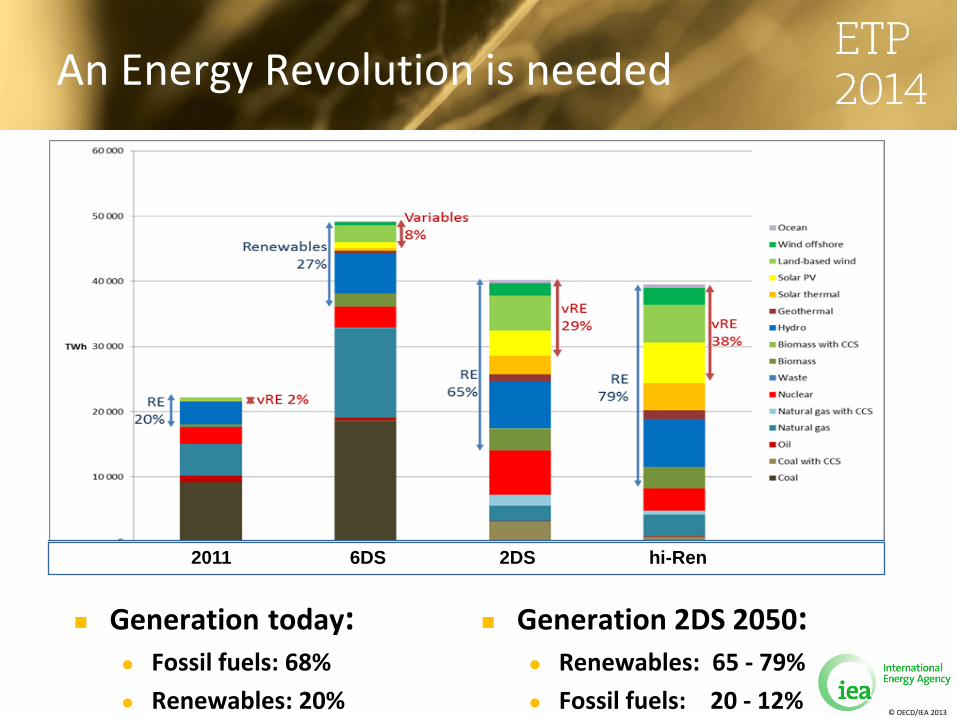

An Energy Revolution is needed

2011 6DS 2DS hi-Ren

Generation today: Fossil fuels: 68%

Renewables: 20%

Generation 2DS 2050: Renewables: 65 - 79%

Fossil fuels: 20 - 12%

© OECD/IEA 2013

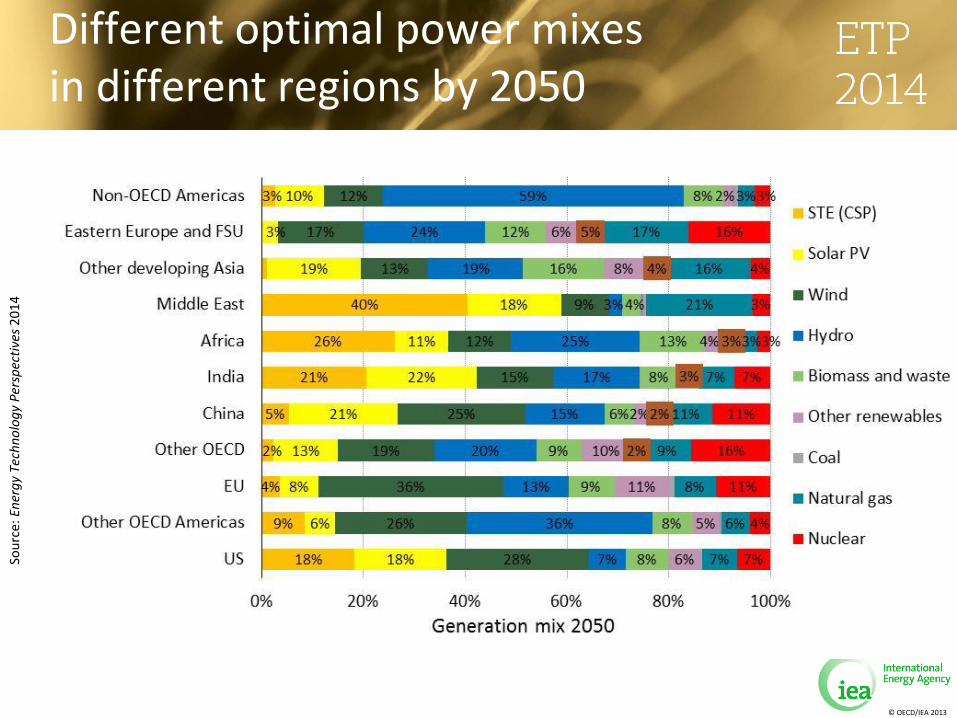

Different optimal power mixes in different regions by 2050

Sou

rce:

En

erg

y Te

chn

olo

gy

Per

spec

tive

s 2

01

4

© OECD/IEA 2013

PV

Contributions to cumulative CO2 emission cuts (hi-REN wrt. 6DS)

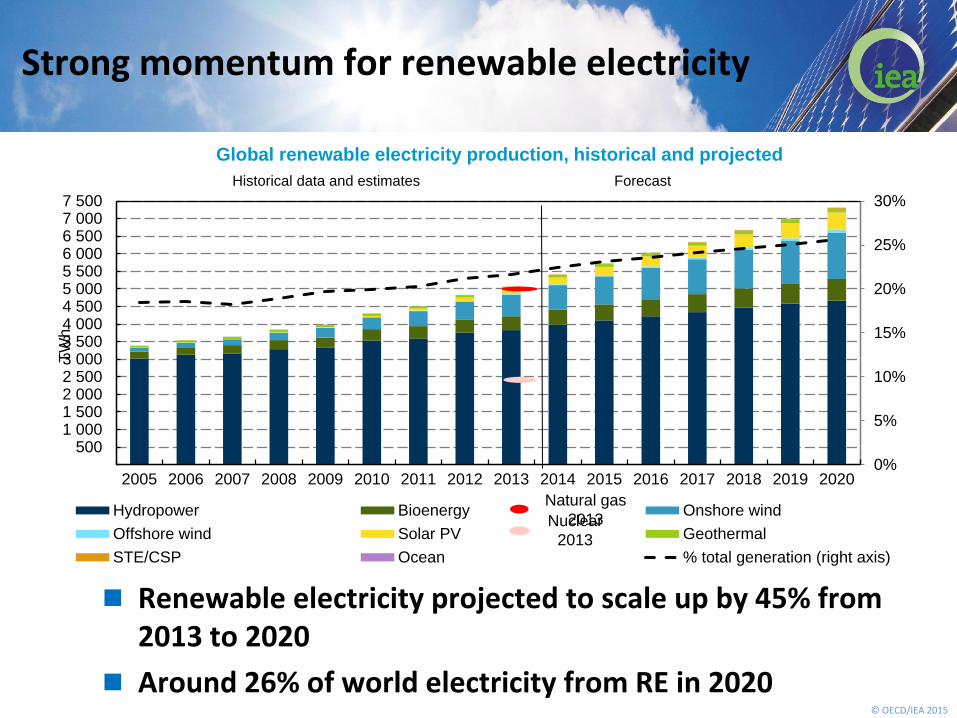

© OECD/IEA 2015

Renewable electricity projected to scale up by 45% from 2013 to 2020

Around 26% of world electricity from RE in 2020

Strong momentum for renewable electricity

Global renewable electricity production, historical and projected

0%

5%

10%

15%

20%

25%

30%

5001 0001 5002 0002 5003 0003 5004 0004 5005 0005 5006 0006 5007 0007 500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

TW

h

Hydropower Bioenergy Onshore wind

Offshore wind Solar PV Geothermal

STE/CSP Ocean % total generation (right axis)

Historical data and estimates Forecast

Natural gas

2013 Nuclear

2013

© OECD/IEA 2014

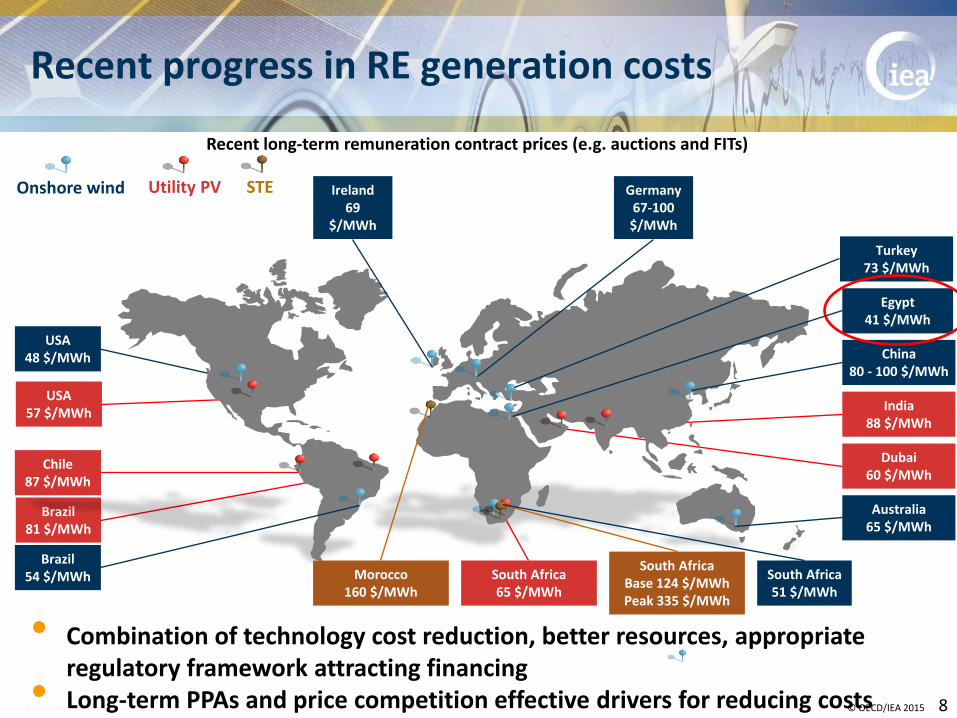

Recent progress in RE generation costs

© OECD/IEA 2015 8

• Combination of technology cost reduction, better resources, appropriate regulatory framework attracting financing

• Long-term PPAs and price competition effective drivers for reducing costs

Utility PV Onshore wind

Recent long-term remuneration contract prices (e.g. auctions and FITs)

STE

India 88 $/MWh

Chile 87 $/MWh

USA 57 $/MWh

South Africa 65 $/MWh

Brazil 81 $/MWh

Dubai 60 $/MWh

Morocco 160 $/MWh

South Africa Base 124 $/MWh Peak 335 $/MWh

South Africa 51 $/MWh

USA 48 $/MWh China

80 - 100 $/MWh

Brazil 54 $/MWh

Turkey 73 $/MWh

Germany 67-100 $/MWh

Ireland 69

$/MWh

Australia 65 $/MWh

Egypt 41 $/MWh

© OECD/IEA 2015

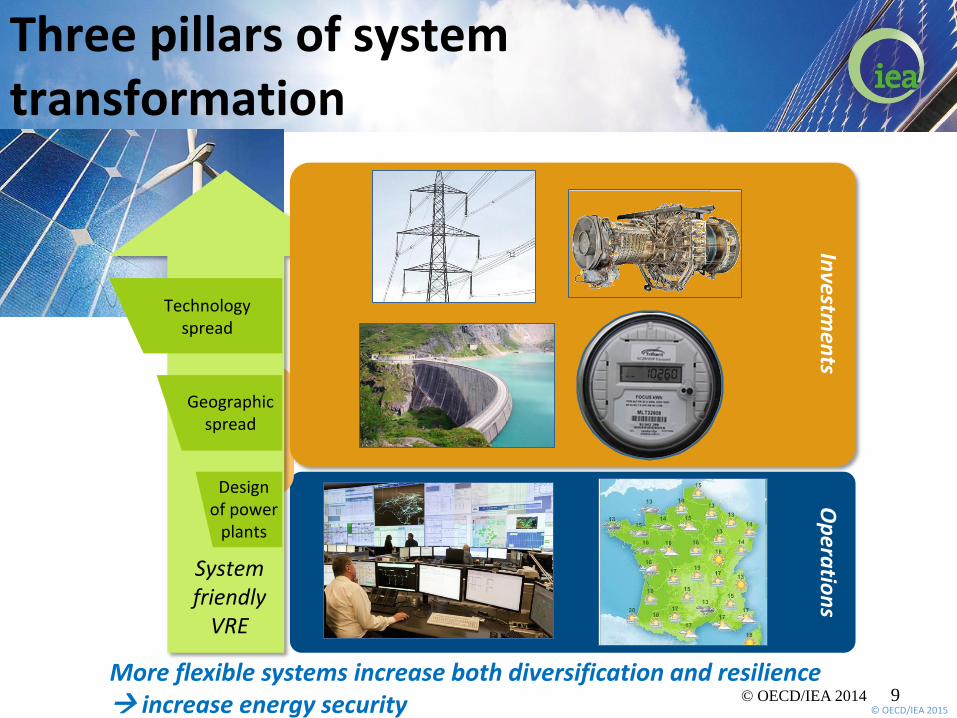

2. Make better use of

what you have

Op

eratio

ns

1. Let wind and solar play their

part

3. Take a system wide-strategic

approach to investments!

System friendly

VRE

Technology spread

Geographic spread

Design of power

plants

Three pillars of system transformation

© OECD/IEA 2014 9

Investm

ents

More flexible systems increase both diversification and resilience increase energy security

© OECD/IEA 2015

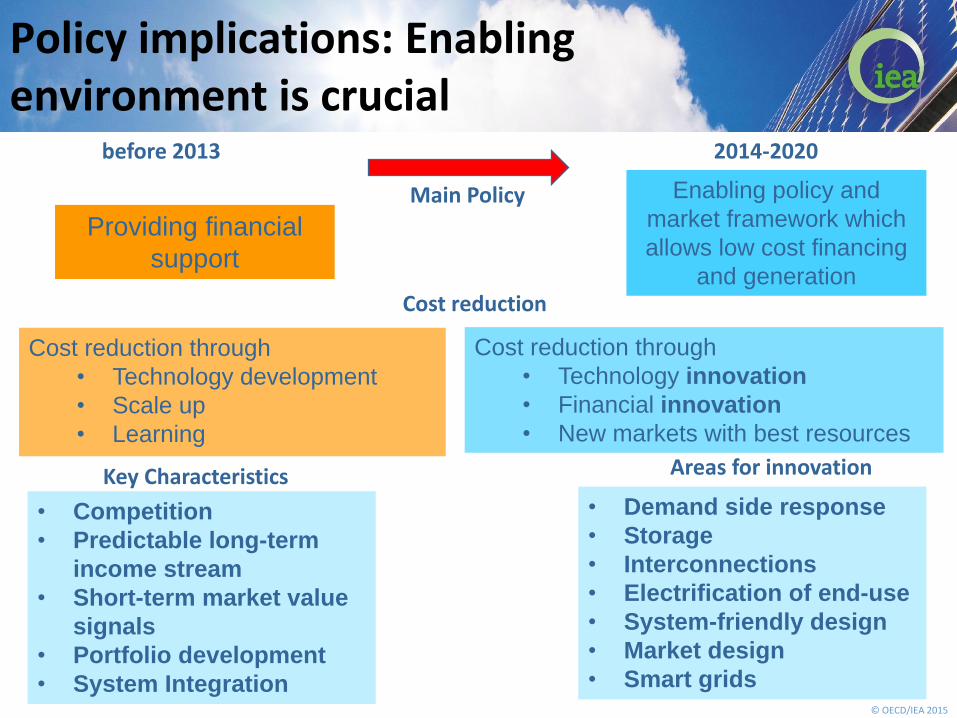

Policy implications: Enabling environment is crucial

Providing financial

support

Cost reduction through

• Technology development

• Scale up

• Learning

before 2013

Enabling policy and

market framework which

allows low cost financing

and generation

• Competition

• Predictable long-term

income stream

• Short-term market value

signals

• Portfolio development

• System Integration

Cost reduction through

• Technology innovation

• Financial innovation

• New markets with best resources

2014-2020

Main Policy

Key Characteristics

Cost reduction

• Demand side response

• Storage

• Interconnections

• Electrification of end-use

• System-friendly design

• Market design

• Smart grids

Areas for innovation

© OECD/IEA 2015

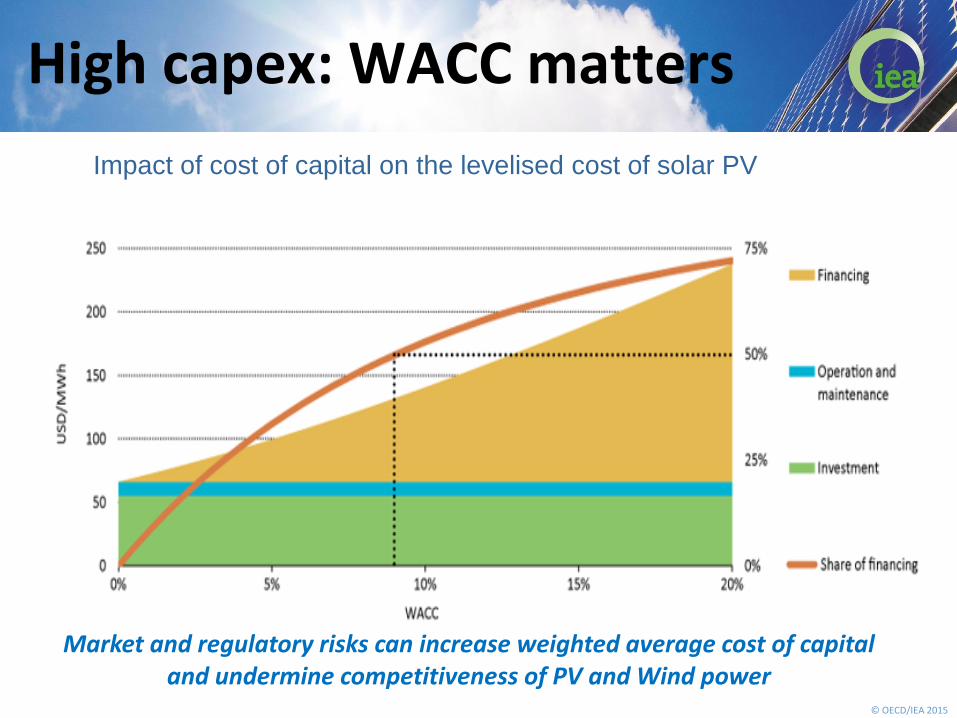

High capex: WACC matters

Market and regulatory risks can increase weighted average cost of capital and undermine competitiveness of PV and Wind power

Impact of cost of capital on the levelised cost of solar PV

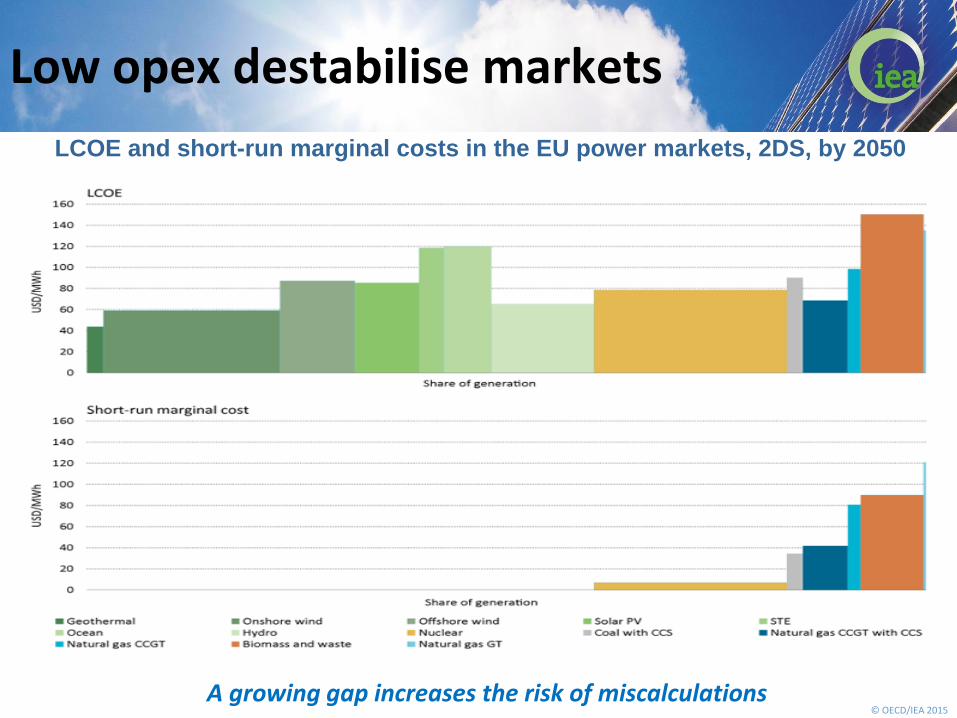

© OECD/IEA 2015 A growing gap increases the risk of miscalculations

Low opex destabilise markets

LCOE and short-run marginal costs in the EU power markets, 2DS, by 2050

© OECD/IEA 2015

Concluding Remarks

Renewables a crucial element for energy security, diversification, and climate change mitigation

As RE become competitive in many markets, the focus is more on market design and less on support policies

A global carbon price would be very welcome, but…

It is difficult in our very diverse world

It must decrease, not increase, volatility of FF use prices

Carbon taxes or trading systems with price corridors

Other tools needed to foster innnovation & investment

in renewables

In most-needed infrastructures

Related Documents