April 2013 Foreign Exchange Risk Management: Perspectives From Financial Executives

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

April 2013

Foreign Exchange Risk Management:

Perspectives From Financial Executives

Defining and Understanding FX Risk

Defining and Understanding FX Risk – Survey results

Overview of Survey Results:

What is clear according to this study* by the Canadian Financial Executives Research Foundation (CFERF) is that foreign exchange risk is a major issue

In fact, 90% of organizations surveyed rated foreign exchange management as an important consideration in their business

Canadian businesses continue to adapt to an increasingly complex currency universe

For most organizations, foreign exchange risk – and its management are challenges for which there exists an emerging and ever-more sophisticated set of policies, procedures and tools

*The Foreign exchange risk management: Perspectives from financial executives report is based on the results of an online survey that took place between November 26, 2012 and January 3, 2013, during which time 109 respondents completed the survey.

Defining and Understanding FX risk: Survey Results

Overview of Survey Results: Three out of four respondents reported

some percentage of their revenue is denominated in foreign currency

17% reported that 76% to 100% of revenue is denominated in a foreign currency

Export credit agency Export Development Canada noted in a recent foreign exchange white paper that Canadian companies that are active in international markets view volatility in the Canadian dollar as the number one constraint to growing exports

The CFERF foreign exchange risk management study similarly found that organizations consider the management of FX risk to be a critical task

More than two-thirds of respondents (68%) rated foreign exchange management ‘extremely important’ or ‘important.’ Just 10% rated FX management ‘not at all important.’

However, only about half actually had a policy or procedure in place to manage risk

What Percentage of Revenue Comes From Foreign-Denominated Currency?

25%

18%

13%

10%

9%

8%

17%

0% 5% 10% 15% 20% 25% 30%

None

1-5%

6-15%

16-25%

26-50%

51-75%

76-100%

Defining and Understanding FX Risk

What is currency risk?

It is financial risk posed by exposures to movements in the exchange rates between two currencies. Multinational Businesses, Importers, Exporters and Investors are all faced with currency risk

These risks can have a material financial impact if they are not identified and managed appropriately

What is Risk Management (Hedging)?

The process of analyzing risks and determining how to prioritize and handle exposures

“To take risk is the essence of economic activity….the main goal must be to enable companies to take the right risk…by providing

knowledge and understanding of the alternatives”

Peter Drucker, 1974

Defining and Understanding FX Risk

Types of risk

There are essentially three types of risks: Transactional

Economic

Translation

Any or all of these exposures can pose fluctuations in value, cash-flow and financial reporting which can materially affect a firm’s performance and competitiveness

Defining and Understanding FX Risk

Before market risk can be managed it must be understood

Identify: What market risks is the company exposed to, directly and

indirectly?

Where do the market risks impact the business?

What impacts the amount of exposure the company has?

Quantify:

What is the impact of unfavorable market moves on the company?

Expectations of the market risk impact depends upon:

The forecasted exposure

The expected/potential market rates

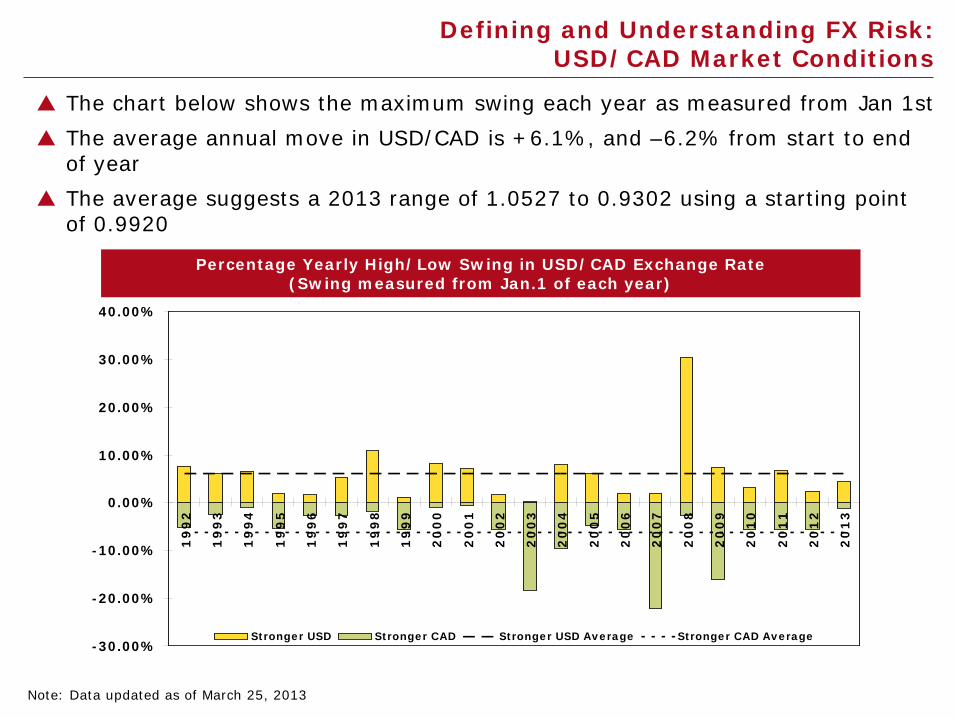

Defining and Understanding FX Risk: USD/CAD Market Conditions

The chart below shows the maximum swing each year as measured from Jan 1st The average annual move in USD/CAD is +6.1%, and –6.2% from start to end

of year The average suggests a 2013 range of 1.0527 to 0.9302 using a starting point

of 0.9920

Percentage Yearly High/Low Swing in USD/CAD Exchange Rate(Swing measured from Jan. 1 of each year)

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Stronger USD Stronger CAD Stronger USD Average Stronger CAD Average

Percentage Yearly High/Low Swing in USD/CAD Exchange Rate (Swing measured from Jan.1 of each year)

Note: Data updated as of March 25, 2013

Defining and Understanding FX Risk: USD/CAD Market Conditions

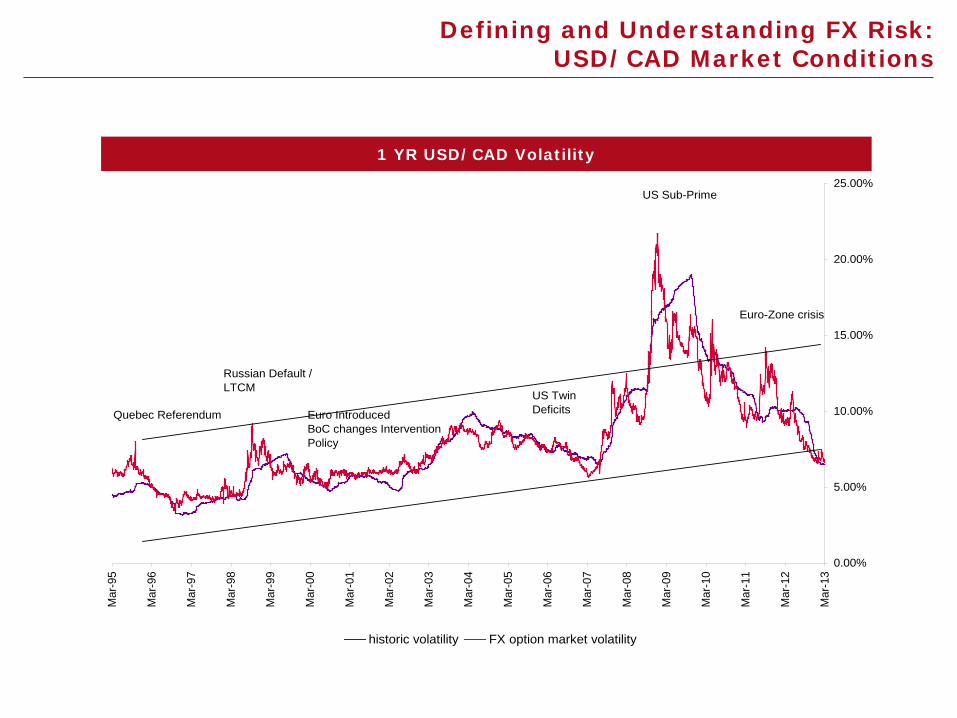

Has the Canadian Dollar stabilized?

The “Risk on – Risk off” pattern is expected to continue with uncertainty in Europe and escalating risks of a global slowdown

Financial markets volatility is expected to continue

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

Mar

-75

Mar

-77

Mar

-79

Mar

-81

Mar

-83

Mar

-85

Mar

-87

Mar

-89

Mar

-91

Mar

-93

Mar

-95

Mar

-97

Mar

-99

Mar

-01

Mar

-03

Mar

-05

Mar

-07

Mar

-09

Mar

-11

Mar

-13

9 years

6 years

10.5 years

5.1 years

1 year

1.4 years

2.0 years

CAD per USD Historical Exchange Rate

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

historic volatility FX option market volatility

Quebec Referendum

US Sub-Prime

US Twin DeficitsEuro Introduced

BoC changes Intervention Policy

Russian Default / LTCM

Euro-Zone crisis

Defining and Understanding FX Risk: USD/CAD Market Conditions

1 YR USD/CAD Volatility

Defining and Understanding FX Risk

Common ways to measure risk:

Notional (dollar) amount Forecasted exposure necessary for any risk measure

Simple

Doesn’t tell you about implications to financial results

Sensitivity to a static move (e.g. 10% or 1 cent move) Gives you a gauge

Doesn’t tell you what is likely

Market forecast/view (e.g. future expectations of economists) Directional prediction of what will happen

Someone’s opinion based on information currently available

Volatility measures (e.g. EBITDA at risk) Provides you with a probability based on market price of risk – view neutral

A little more complex to model and calculate

0.9500

0.9700

0.9900

1.0100

1.0300

1.0500

1.0700

3/4/2013 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q4 2013 Q4 2013

CIBC TD BNS Royal BMO AVG

Canadian Multi-Bank Economist Forecasts

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q4 2013 Q4 2013

CIBC 1.0300 1.0500 1.0400 1.0300 1.0100 0.9800 0.9600 0.9800TD 1.0000 1.0000 0.9900 0.9800 0.9800 0.9800 0.9700 0.9700

BNS 1.0400 1.0400 1.0200 1.0100 1.0100 1.0000 1.0000 0.9900Royal 1.0200 1.0400 1.0500 1.0400 1.0300 1.0200 1.0200 1.0200BMO 1.0090 1.0440 1.0290 1.0070 0.9970 0.9920 0.9870 0.9820AVG 1.0198 1.0348 1.0258 1.0134 1.0054 0.9944 0.9874 0.9884

Defining and Understanding FX Risk

Some key questions to address

What is the company’s appetite for uncertainty?

What outcomes/aspects of the business are we trying to protect?

What potential impact can the business withstand?

For how long does the business need to be protected? How long to adjust the business?

What are competitors doing?

Defining and Understanding FX Risk

How has your company’s focus on FX risk changed in the last five years?

Panel Discussion

Doing Business In Emerging Markets

Doing Business In Emerging Markets

Emerging Markets

Global FX market turnover grew 20% in 2010 vs 2007, with average daily volume of US$4.0 trillion. The increase was driven by a 48% jump in spot transactions, which represent 37% of total FX turnover. (Source: BIS)

USD (85%), EUR (39%), and JPY (19%) hold the dominant market share of daily turnover, although significant increases have been seen in the Chinese Renminbi, Turkish Lira, Brazilian Real, and Korean Won. Each hold around a 1% share (CAD accounts for 5.3%)

FX markets have become more global, with cross-border dealer transactions accounting for 65% of trading activity, while local dealer transactions represent 35%, it’s lowest share ever

The Canadian government and industry groups have encouraged Canadian companies to lessen their dependence on the US market to expand their trade opportunities into emerging markets. These countries continue to seek new sources of natural resources and goods to further their industrial and infrastructure development

FEI survey shows 42% of respondents are doing business in an emerging market country

Doing Business In Emerging Markets

Growth in Swift Payments

While the Euro has seen its share slip, it remains the dominant currency in international SWIFT payments

The US dollar has increased, partly due to its role in payments to emerging market countries

While still very small, the Chinese Yuan has risen to 13th place, with a 171% increase from Jan 2012 to Jan 2013. The growth is due to falling government trade restrictions and businesses growing in size where they are no longer reliant on the US dollar

Swift Payments

0 0.1 0.2 0.3 0.4 0.5

NZD – New Zealand Dollar

ZAR – South African Rand

RUB – Russian Rouble

DKK – Danish Krone

CNY – Chinese Yuan

NOK – Norwegian Krone

THB – Thai Baht

SEK – Swedish Krone

HKD – Hong Kong Dollar

SGD – Singapore Dollar

CAD – Canadian Dollar

CHF – Swiss Franc

AUD – Australian Dollar

JPY – Japanese Yen

GBP – British Pound

USD – US Dollar

EUR – Euro

0.6%

33.5%

39.9%

Jan 2013 Jan 2012

Doing Business In Emerging Markets

Chinese Renminbi (CNY vs. CNH)

CNY (onshore) is restricted to trading by entities registered in China. It is convertible under certain conditions and trades within a set trading range

CNH (offshore) is the same as CNY, but free floating and deliverable. CNH has gained in popularity as markets are more transparent, have less restrictive delivery and trading hours, and there are a greater number of investment products and growing bond market “Dim Sum Bonds”

As trading in CNH has grown and market acceptance increased, the spread between CNY and CNH has converged, moving spot spread close to zero

12 month Onshore vs Offshore Fwd vs NDF

6.25

6.30

6.35

6.40

6.45

6.50

6.55

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13

NDFOnshoreOffshore

Source: BIS, Bloomberg. and CIBC World Markets

20

40

60

80

100

120

140

160

180

200

Dec-05 Dec-06 Dec-07 Dec-08 Jan-10 Jan-11 Jan-12 Feb-13

Real Exchange Rate Index Dec 2002 =100

Argentina

Brazil

Mexico

Colombia

Peru

Chile

Venezuela

LATAM Currencies: Brazil Strongest, Mexico Weakest

Source: BIS, Bloomberg. and CIBC World Markets

50

70

90

110

130

150

170

190

210

Dec-05 Jul-06 Mar-07 Oct-07 Jun-08 Jan-09 Sep-09 May-10 Dec-10 Aug-11 Mar-12

Real Exchange Rate Index2010=100

Argentina

Brazil

Mexico

Turkey

Hungary

Phillipines

EM Currency performance has been mixed

Doing Business in Emerging Markets

Managing EM FX Risk

Widely accepted practice of using a proxy currency which is more predictable and has no restrictions

Often use foreign currency accounts to manage flows in local currencies

How Do You Manage Exposure To Emerging Markets Currencies?

9%

15%

17%

22%

37%

0% 20% 40%

Other

Combination of dealing incurrency and using proxy

Deal directly in thecurrency

Products such as forwardcontracts, non-deliverableforward contracts, options

Use proxy e.g. USD, EURO, AUD

Doing Business In Emerging Markets

How does your FX Policy differ for G10 vs. EM currencies?

Is there pressure to deal in local currency vs. a proxy?

Panel Discussion

FX Risk in Action

FX Risk in Action: Who’s in Charge?

Who’s responsible for FX Risk Management?

Survey clearly shows that the Finance Dept. has the responsibility for recommending and implementing policies and procedures

In the majority of companies surveyed (54%) said the CFO was accountable; followed by the VP Finance/Director of Finance (24%) and Treasurer (19%) depending on the size and structure of the company

Most companies have multiple levels of monitoring and compliance within their organization

Risk Committee is responsible for evaluating the transactional elements of risk management in the firm

Senior Management is responsible for evaluating the performance of their policy, deciding when or when not to hedge and ensuring their policy is in line with the needs of the business

Ultimately the Board of Directors approves the overall direction of the policy and ensures management is in compliance

FX Risk in Action: Policies and Procedures

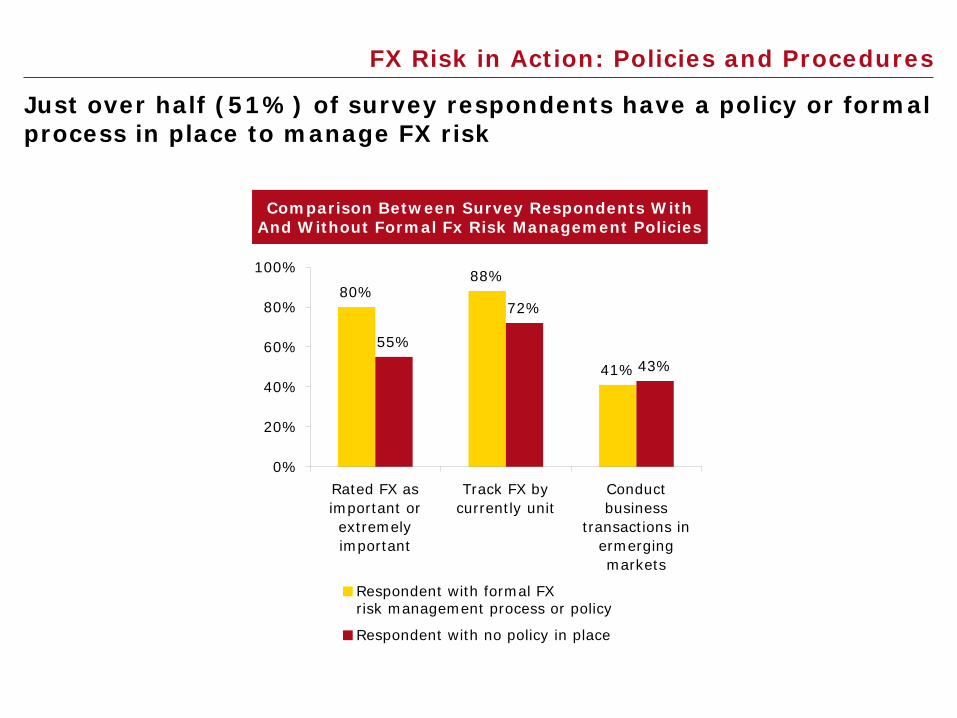

Just over half (51%) of survey respondents have a policy or formal process in place to manage FX risk

80%88%

41%

55%

72%

43%

0%

20%

40%

60%

80%

100%

Rated FX asimportant orextremelyimportant

Track FX bycurrently unit

Conductbusiness

transactions inermergingmarkets

Respondent with formal FX risk management process or policy

Respondent with no policy in place

Comparison Between Survey Respondents With And Without Formal Fx Risk Management Policies

FX Risk in Action: Why Establish a FX Hedging Policy?

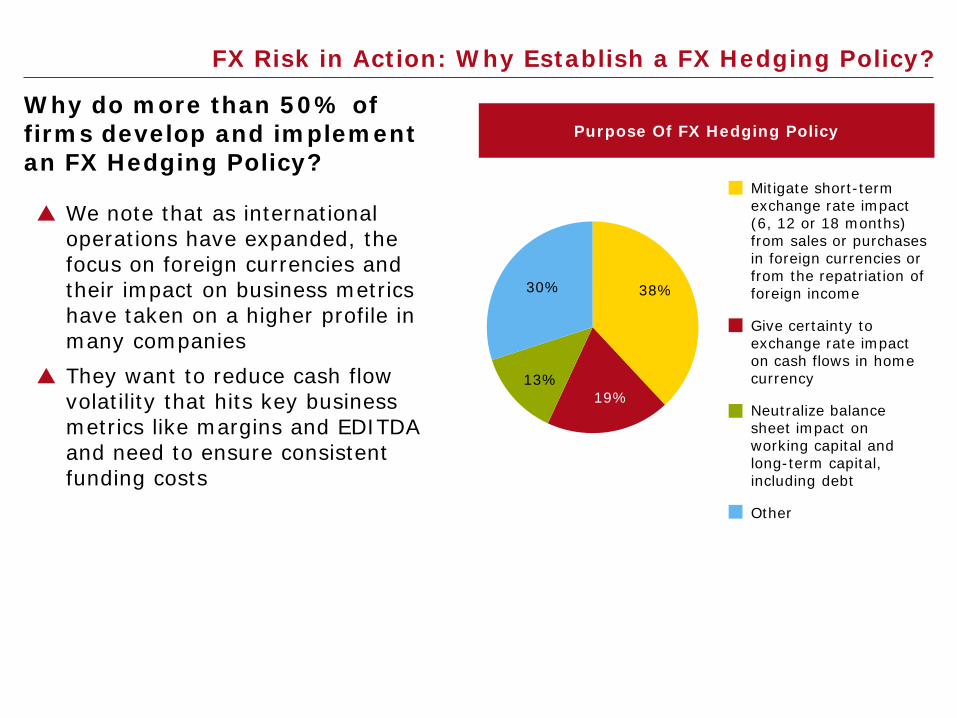

Why do more than 50% of firms develop and implement an FX Hedging Policy?

We note that as international operations have expanded, the focus on foreign currencies and their impact on business metrics have taken on a higher profile in many companies

They want to reduce cash flow volatility that hits key business metrics like margins and EDITDA and need to ensure consistent funding costs

19%13%

30% 38%

Purpose Of FX Hedging Policy

Mitigate short-term exchange rate impact (6, 12 or 18 months) from sales or purchases in foreign currencies or from the repatriation of foreign income

Give certainty to exchange rate impact on cash flows in home currency

Neutralize balance sheet impact on working capital and long-term capital, including debt

Other

FX Risk in Action: Instruments to Mitigate Risk

As confirmed by the study, the majority of firms hedge their exposures with the use of financial instruments

Companies recognize that any exposure not naturally hedged may need to be managed by way of a derivative instrument

Financial Instruments Used To Mitigate Risk

15%

8%

13%

23%

41%

0% 20% 40% 60%

Other

Foreign Exchange Swaps

Currency options (vanillaoptions or structures)

Futures contracts (exchangetraded contracts that allow youto buy or sell a currency at aset exchange rate in a given

month)

Forwards (OTC agreements tobuy or sell a given amount of a

currency at a set exchangerate on a specific future date)

FX Risk in Actions: Risk and Reward

Derivative Products change a company’s risk profile and have differing risk/reward characteristics Let it float

Exchange in the spot market Lock it in

Fixed price forward contract Insure it

Purchased option Combination of lock it in and insure – Option based strategies with different

risk/reward scenarios Collar Expandable Forward Ratio Collar Variable Rate Forward

Structured Hedging Solutions Structured solutions can be designed to provide either perfect or partial protection

while allowing for participation in a potentially favourable spot movement Certain strategies are designed to “boost” the forward rate available and can be

tailored to take into account the client’s risk appetite and/or market views. e.g. At-Maturity Variable Rate Forward, Conditional Forward, Fade-In Forward

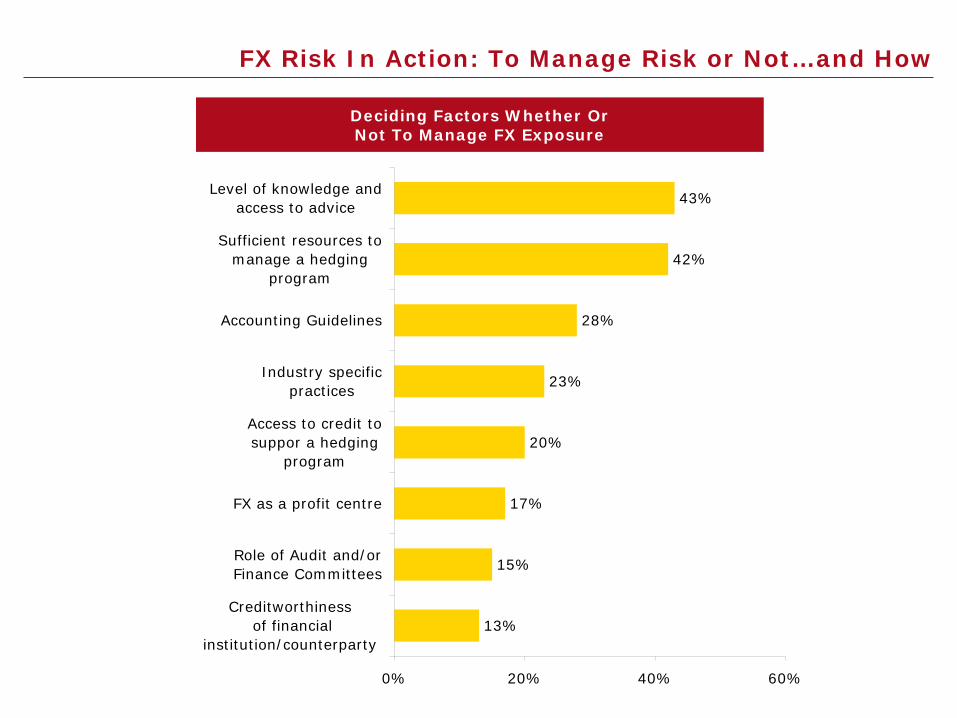

FX Risk In Action: To Manage Risk or Not…and How

Deciding Factors Whether Or Not To Manage FX Exposure

13%

15%

17%

20%

23%

28%

42%

43%

0% 20% 40% 60%

Creditworthiness of financial

institution/counterparty

Role of Audit and/orFinance Committees

FX as a profit centre

Access to credit tosuppor a hedging

program

Industry specificpractices

Accounting Guidelines

Sufficient resources tomanage a hedging

program

Level of knowledge andaccess to advice

FX Risk In Action: To Manage Risk or Not…and How

Observations:

Public companies are more concerned with accounting treatment/Income Statement volatility and therefore favour simple strategies like Forward Contracts. The FEI survey has 64% of companies using either OTC Forwards or Exchange traded futures contracts

Private companies are more open to alternative hedging strategies. Focus is more on economic performance than reducing Income Statement volatility

Lack of knowledge has kept some companies from using option based strategies

An increase in market volatility often attracts more companies to structured option hedges because of their relative attractiveness to simple forward contracts and futures

In the Emerging Markets space, companies with formal FX policies typically hedge more of their exposures but also shy away from the more volatile local currency in favour of proxy currencies such as the USD, EUR and AUD

Those without a formal policy are typically more risk accepting. This is demonstrated by the reduced use of hedging products (9% vs. 35% for those with a policy) and the likeliness of trading in the local currency (22% vs. 13%)

PERSPECTIVE Canadian Dollar Parity, Boon or Hindrance?

Benjamin Tal

Deputy Chief Economist, CIBC

Central Banks Diversify into Broader FX Reserves

0

100

200

300

400

500

600

2000 2002 2004 2006 2008 2010

Reserves of ReportingCentral Banks*Esimate: Global Reserves

Official FX Reserves excl. US$, sterling, Swiss franc, euro & yen (in bns of USD)

*covers roughly 60% of world official FX

Source: IMF, CIBC

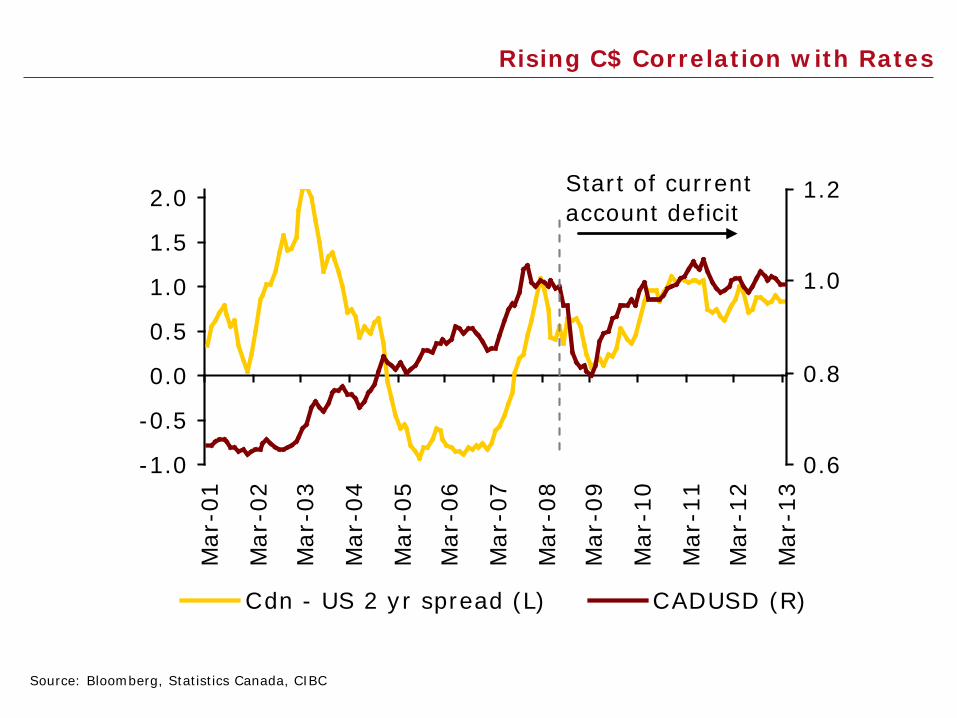

Rising C$ Correlation with Rates

Source: Bloomberg, Statistics Canada, CIBC

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0M

ar-0

1

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

0.6

0.8

1.0

1.2

Cdn - US 2 yr spread (L) CADUSD (R)

Start of currentaccount deficit

Estimated Currency Over/Undervaluation*

-15%

-10%

-5%

0%

5%

10%

15%

Indo

nesi

a

Japa

n

Ger

man

y

Chin

a

Indi

a

Thai

land

S Af

rica

Kore

a

Mex

ico

Euro

Are

a

Braz

il

USA

Switz

erl. UK

Cana

da

Aust

ralia

Spai

n

Overvaluation/undervaluation (%)

*relative to each country's trading partners; midpoint of estimated

range

Source: IMF, BIS, CIBC

The Lost Decade

Source: Statistics Canada, CIBC

Canadian Export Vol. Index (2007=100)

6065707580859095

100105110

97 99 01 03 05 07 09 11

US$/C$ 11%

US$/C$ 35%

US$/C$ 5%

Exchange Rate Vulnerability Index

INDUSTRY Export Import Combined Ranked ByVulnerability Vulnerability Export-Import Total

(% of shpts. Exported (% of shpts. to Can. Mkt) x Vulnerability Vulnerabilityless Imported inputs) (import penetration of Can. Mkts.)

H Furniture 46.2 35.8 82.0 1I Machinery 60.4 12.2 72.6 2G Wood Products 62.1 5.9 68.0 3H Electrical Equipment 32.3 35.7 68.0 4

Paper Manufacturing 57.9 5.7 63.6 5M Computer & Electronics 45.5 11.1 56.6 6E Primary Metals 35.1 10.6 45.7 7D Transportation Equipment 36.6 6.5 43.1 8I Fabricated Metals 13.7 27.9 41.6 9U Printing & Allied -0.9 34.1 33.2 10M Clothing 13.5 18.6 32.1 11

Chemical Manufacturing 25.4 6.3 31.7 12L Food Manufacturing 11.8 15.3 27.1 13O Textiles 2.9 21.9 24.8 14W Beverages/Tobacco 4.0 11.9 15.9 15

Petroleum Refining & Coal Prod -12.1 5.3 -6.8 16

No Clear Correlation Between Dollar Sensitivity and GDP Performance

High vulnerability Low vulnerability

Source: Statistics Canada, CIBC

-7-6-5-4-3-2-10123

-20 0 20 40 60 80 100Index of $ vulnerability

furniture

machinery

wood products

electricalequip.

paper mfg

chemicalmfgtextiles

beverages/tobacco

food mfgpetroleum/

coal

Avg

ann

ual G

DP

% g

row

th (

07-1

2)

transp.equip.

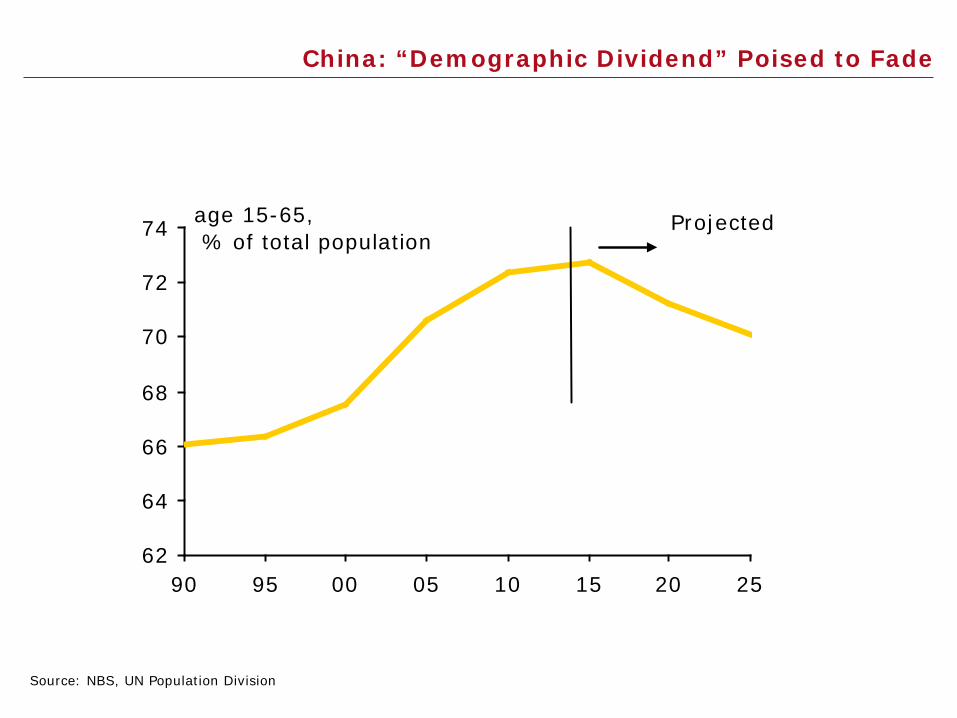

China: “Demographic Dividend” Poised to Fade

Source: NBS, UN Population Division

62

64

66

68

70

72

74

90 95 00 05 10 15 20 25

age 15-65, % of total population

Projected

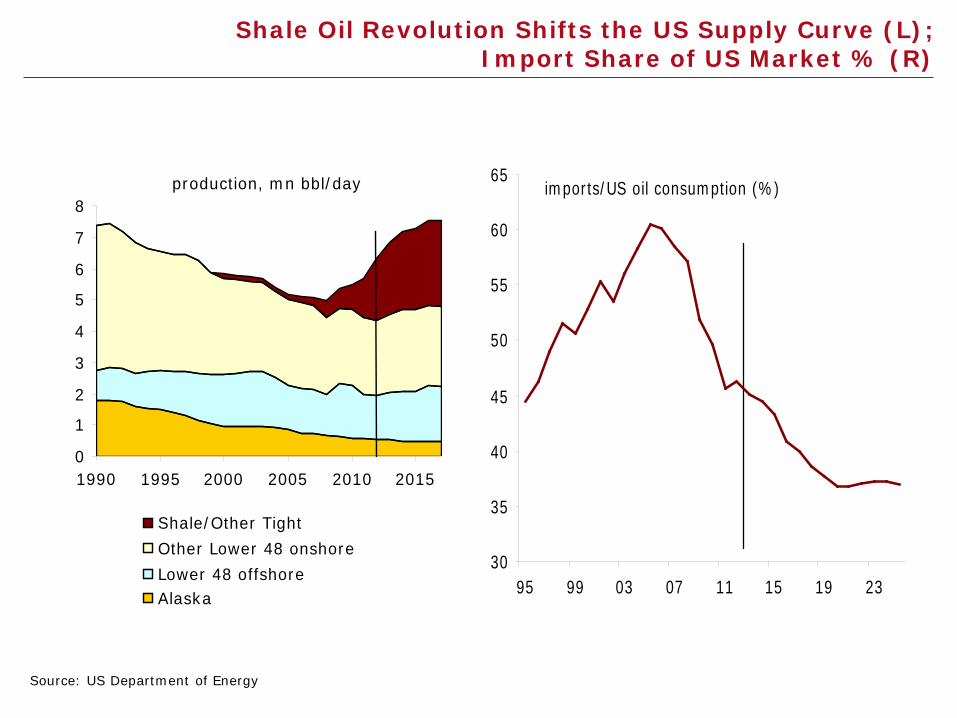

Source: US Department of Energy

Shale Oil Revolution Shifts the US Supply Curve (L); Import Share of US Market % (R)

0

1

2

3

4

5

6

7

8

1990 1995 2000 2005 2010 2015

Shale/Other TightOther Lower 48 onshoreLower 48 offshoreAlaska

production, mn bbl/day

30

35

40

45

50

55

60

65

95 99 03 07 11 15 19 23

imports/US oil consumption (%)

Conclusion

Conclusion

In conclusion, the research study shows that Canadian companies are embracing the need to expand their businesses beyond our borders and deal with the currency risks that come with that strategy. Therefore, Foreign Exchange risk management needs to be part of a Canadian company's international growth strategy.

Because only half of the organizations surveyed have a policy or formal process in place to manage FX risk, it appears there's a need for Canadian businesses to take a more comprehensive, pro-active approach to managing these material risks.

Related Documents