FOREIGN EXCHANGE RISK AND EXPOSURE

Risk associated with Foreign Exchange

Aug 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FOREIGN EXCHANGE RISK AND EXPOSURE

INTRODUCTION

The FOREIGN EXCHANGE MARKET is a global, worldwide financial market for trading currencies.

Most of the transactions are channelled through world wide interbank market which is a wholesale market in which major banks trade with each other.

The primary purpose of the foreign exchange is to assist international trade and investment, by allowing businesses to convert one currency to another currency.

In a typical foreign exchange transaction, a party purchases a quantity of one currency by paying a quantity of another currency.

Foreign Exchange Exposure and Risk and Risk Management

Foreign exchange rate is the price of one currency quoted in terms of another currency.

Exposure refers to the degree to which a company is affected by exchange rate changes.

Exchange rate risk is defined as the variability of a firm’s value due to uncertain changes in the rate of exchange.

Managing Foreign Exposure with the concept of Risk Management is called Hedging.

Types of Exposure

• Translation Exposure

• Transaction Exposure

• Economic Exposure

Transaction Exposure

This risk involves the possible exchange loss or gain on existing foreign currency denomination.

Transaction exposure arises from:

Purchasing or selling on credit goods or services whose prices are stated in foreign currencies.

Borrowing or lending funds when repayment is to be made in a foreign currency.

Acquiring assets or incurring liabilities denominated in foreign currencies.

Translation Exposure

Translation exposure of foreign exchange is of an accounting nature and is related to a gain or loss arising from the conversion or translation of the financial statements of a subsidiary located in another country. Eg - ranbaxy

Four Methods to translate foreign currency to home currency:

1. Current/Non-Current Method: All current assets and current liabilities are translated at current exchange rate and non current at historic rate.

2. Monetary/ Non-Monetary Method: All monetary assets(eg. cash, a/r,a/p) and liabilities(loans) are translated at current exchange rate and non monetary (like inventory , fixed asset) at historic price.

3. Temporal Method: Same as Monetary/Non-Monetary method BUT inventory may be translated at current exchange rate IF it is shown at market value

4. Current Rate Method: All balance sheet and income statement items are translated at current exchange rate

Economic Exposure

Economic exposure is a rather long-term effect of the transaction exposure.

If a firm is continuously affected by an unavoidable exposure to foreign exchange over the long-term, it is said to have an economic exposure.

Such exposure to foreign exchange results in an impact on the market value of the company as the risk is inherent to the company and impacts its profitability over the years.

Three types of Exposure

1. Translation or AccountingExposureChange in FE rate =change in Accountingstatements

2. Transaction Exposure change in FE rate = change in outstandingobligations

3. Economic ExposureChange in FE rate = change in future cashflows

INTERNATIONAL PARITY RELATIONSHIPS

Managers of multinational firms, international investors, importers and exporters, and government officials deal with these fundamental issues:

Are changes in exchange rates predictable? How are exchange rates related to interest rates? What, at least theoretically, is the “proper”

exchange rate?

To answer these questions we need to first understand the economic fundamentals of international finance, known as parity conditions.

ARBITRAGE AND THE LAW OF ONE PRICE

Identical goods sell for the same price worldwide.

If the prices after exchange-rate adjustment were not equal, arbitrage of the goods ensures eventually they will worldwide.

parity conditions resulting from these arbitrage activities

1. Purchasing Power Parity (PPP)

2. The International Fisher Effect(IFE)

3. Interest Rate Parity (IRP)

4. Unbiased Forward Rate (UFR)

PURCHASING POWER PARITY

states that spot exchange rates between currencies will change to the differential in inflation rates between countries.

Price levels adjusted for exchange rates should be equal between countries i.e One unit of currency has same purchasing power globally.

PPP says the currency with the higher inflation rate is expected to depreciate relative to the currency with the lower rate of inflation.

PURCHASING POWER PARITY

1. In mathematical terms:

where et = future spot rate

e0 = spot rate

ih = home inflation

if = foreign inflation

t = the time period

tf

tht

i

i

e

e

1

1

0

FISHER EFFECT

Nominal interest rate comprises of real interest rate and expected rate of inflation.

The nominal Rate of interest is higher when higher inflation rate is expected and lower when lower inflation rate is expected.

1+nominal interest rate = (1+ real interest rate)(1+ inflation rate)

This is referred to as FISHER EFFECT

14

The International Fisher Effect

Because of the arbitrage equilibrium exist in the real returns of two countries, then as per fisher effect nominal interest rate of two countries will adjust exactly for change in inflation rates.

Nominal interest differential must be equal to expected inflation rate differential in two countries.

(1+rf/1+rd) = E(1+if)/E(1+id)currencies with high interest rates tend to depreciate and currencies with low interest rates tend to appreciate

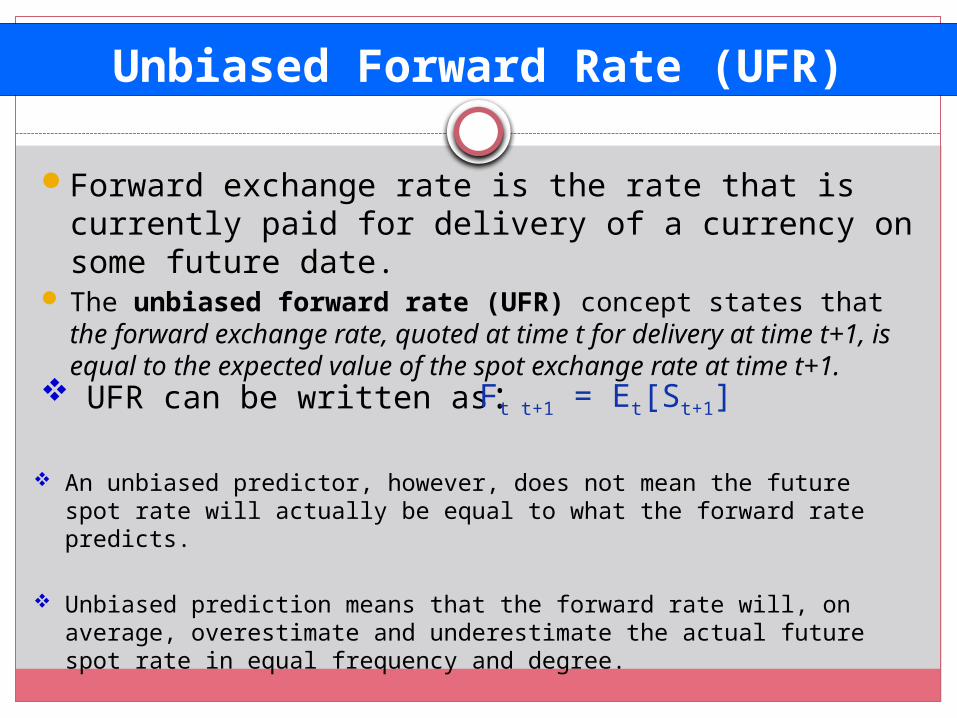

Unbiased Forward Rate (UFR) Unbiased Forward Rate (UFR) Unbiased Forward Rate (UFR)

Forward exchange rate is the rate that is currently paid for delivery of a currency on some future date.

The unbiased forward rate (UFR) concept states that the forward exchange rate, quoted at time t for delivery at time t+1, is equal to the expected value of the spot exchange rate at time t+1.

Unbiased Forward Rate (UFR)

UFR can be written as: Ft t+1 = Et[St+1]

An unbiased predictor, however, does not mean the future spot rate will actually be equal to what the forward rate predicts.

Unbiased prediction means that the forward rate will, on average, overestimate and underestimate the actual future spot rate in equal frequency and degree.

Interest Rate Parity

Characterizes the relationship between interest rate and exchange rate of two countries.

This implies that exchange rate differential will be equal to the interest rate differential between two countries.

(1+rf)/ (1+rd) = f / s Where : f = forward rate between two

countries s = spot exchange rate between two

countries.

Interest Rate Parity

Hedging

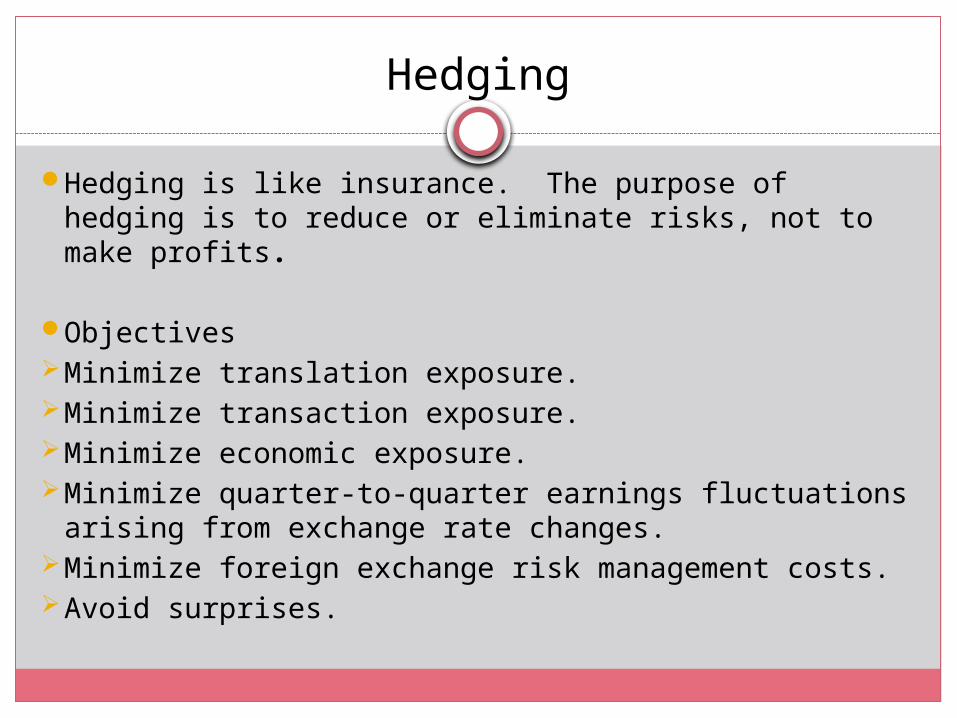

Hedging is like insurance. The purpose of hedging is to reduce or eliminate risks, not to make profits.

Objectives Minimize translation exposure. Minimize transaction exposure. Minimize economic exposure. Minimize quarter-to-quarter earnings fluctuations

arising from exchange rate changes. Minimize foreign exchange risk management costs. Avoid surprises.

Hedging Strategies/ Instruments

Forward contractForeign currency optionSwaps

FORWARD CONTRACT

A forward is a made-to-measure agreement between two parties to buy/sell a specified amount of a currency at a specified rate on a particular date in the future.

Future contract :A futures contract is similar to the forward contract but is more liquid because it is traded in an organized exchange i.e. the futures market.

Forward Market Hedge Future Hedge

Contracts executed by banks Contracts executed by brokerage houses of future exchanges

Tailor-made contracts Standardised contracts

Price quoted reflects banker’s perception of future price

Price paid is determined by forces of demand and supply

Contract bilateral between two parties

Contract with the future exchange

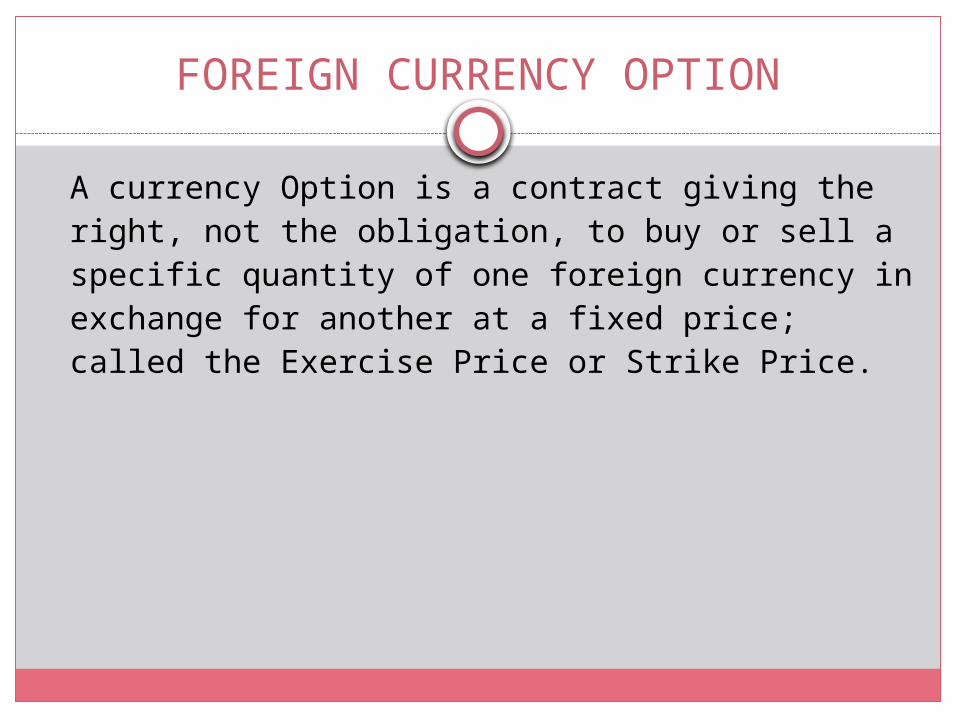

A currency Option is a contract giving the right, not the obligation, to buy or sell a specific quantity of one foreign currency in exchange for another at a fixed price; called the Exercise Price or Strike Price.

FOREIGN CURRENCY OPTION

SWAPS

A swap is a foreign currency contract whereby the buyer and seller exchange equal initial principal amounts of two different currencies at the spot rate. The buyer and seller exchange fixed or floating rate interest payments in their respective swapped currencies over the term of the contract. At maturity, the principal amount is effectively re-swapped at a predetermined exchange rate so that the parties end up with their original currencies.

THANK YOU

Related Documents