European Journal of Scientific Research ISSN 1450-216X / 1450-202X Vol. 157 No 1 July, 2020, pp.27 - 42 http://www. europeanjournalofscientificresearch.com Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) Fatma Ali Alyousif College of Business studies, PAAET, Kuwait E-mail: [email protected] Bedour Mohammad Alsaleh Industrial Engineering Department, College of Engineering Kuwait University E-mail: [email protected] Amani Sulaiman Alrashdan College of Business studies, PAAET, Kuwait E-mail: [email protected] Abstract The study in this paper was attempted to build a statistical model for forecasting the GBP/KWD exchange rate. A variety of statistical time series techniques were analyzed such as exponential smoothing models, and ARIMA models including autoregressive and moving average process. The data was collected for five years started from 6 th of January 2014 till 8 th of November 2019. ARIMA (p,d,q) models were analyzed also to identify the adequate of the models, the stationary of the series was tested by applying the trend test such as ADF-Augmented Dickey-Fuller and PP-phillips-perron unit root tests. Performance of the competitive models for Arima models was assessed with AIC and BIC criteria. Statistical model fit measures indicate that the best candidate model among the competitive arima models was ARIMA (1,1,1): 1 1 9299 . 0 9139 . 0 - - - = t t t e Z Y . Statistical analysis for the exponential smoothing models were analyzed. The accuracy measures criteria such as: mean absolute error (MAE), and mean absolute percentage error (MAPE), sum square error (SSE), mean squared error(MSE),and mean percentage error(MPE) assessed. The results of the analysis reveal the fact that the best model among the exponential models was the single exponential smoothing model. Keywords: Exchange rates, Exponential smoothing, ARIMA. 2019 Mathematical subject classification: 62M10 Overview The local currency of the State of Kuwait is “Kuwaiti Dinar – K.D “, it was introduced in 1960 to replace the “Gulf Rupee “which was equal to “Indian Rupee “. Kuwaiti Dinar was equal to 1-pound sterling in 1960; it was issued by Central Bank of Kuwait. Due to the solid foundation of Kuwait economy, which is based on petroleum and foreign investments, the Kuwait Dinar became one of the highest valued monetary units in the world. Kuwaiti Dinar is linked to a basket of currencies since 2007, before that it was linked with U.S Dollar in the period from 2003 – 2007.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

European Journal of Scientific Research

ISSN 1450-216X / 1450-202X Vol. 157 No 1 July, 2020, pp.27 - 42

http://www. europeanjournalofscientificresearch.com

Forecasting the Exchange Rate of Kuwaiti Dinar

(KWD) with the British Pound Sterling (GBP)

Fatma Ali Alyousif

College of Business studies, PAAET, Kuwait

E-mail: [email protected]

Bedour Mohammad Alsaleh

Industrial Engineering Department, College of Engineering

Kuwait University

E-mail: [email protected]

Amani Sulaiman Alrashdan

College of Business studies, PAAET, Kuwait

E-mail: [email protected]

Abstract

The study in this paper was attempted to build a statistical model for forecasting the

GBP/KWD exchange rate. A variety of statistical time series techniques were analyzed

such as exponential smoothing models, and ARIMA models including autoregressive and

moving average process. The data was collected for five years started from 6th

of January

2014 till 8th

of November 2019. ARIMA (p,d,q) models were analyzed also to identify the

adequate of the models, the stationary of the series was tested by applying the trend test

such as ADF-Augmented Dickey-Fuller and PP-phillips-perron unit root tests. Performance

of the competitive models for Arima models was assessed with AIC and BIC criteria.

Statistical model fit measures indicate that the best candidate model among the competitive

arima models was ARIMA (1,1,1): 11 9299.09139.0 −− −= ttt eZY .

Statistical analysis for the exponential smoothing models were analyzed. The

accuracy measures criteria such as: mean absolute error (MAE), and mean absolute

percentage error (MAPE), sum square error (SSE), mean squared error(MSE),and mean

percentage error(MPE) assessed. The results of the analysis reveal the fact that the best

model among the exponential models was the single exponential smoothing model.

Keywords: Exchange rates, Exponential smoothing, ARIMA.

2019 Mathematical subject classification: 62M10

Overview The local currency of the State of Kuwait is “Kuwaiti Dinar – K.D “, it was introduced in 1960 to

replace the “Gulf Rupee “which was equal to “Indian Rupee “. Kuwaiti Dinar was equal to 1-pound

sterling in 1960; it was issued by Central Bank of Kuwait. Due to the solid foundation of Kuwait

economy, which is based on petroleum and foreign investments, the Kuwait Dinar became one of the

highest valued monetary units in the world. Kuwaiti Dinar is linked to a basket of currencies since

2007, before that it was linked with U.S Dollar in the period from 2003 – 2007.

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 28

In this research, we attempt to study the exchange rate of Kuwaiti Dinar in term of the British

Sterling Pound (G.B.P). It is known that the exchange rate is a crucial element that plays an important

role in Kuwait economy with respect to trading and Oil export prices. The British Pound is one of the

major international currencies in the world. It is very well known that Kuwait has a strong relationship

with the United Kingdom of Britain, they share historic relations and Kuwait owns big investments in

the U. K, therefore it is important to study the behavior of the exchange rate of Kuwaiti Dinar in terms

of the British Sterling Pound (G.B.P).

Forecasting financial time series is essential to the investors and governments, by

understanding the movement of the exchange rate and its forecast, this helps the decision makers in

the country to design the best financial policy to achieve their goal of price stability, and monitoring

the foreign investments.

1. Introduction Forecasting the exchange rate is very important in money transactions. The exchange rate plays an

important rule in the economy and it has a significant impact in economy with respect to trading and

oil prices as well as monetary market. Therefore, it is important for the researcher in the area of finance

and economy to study the behavior of currencies and to forecast the fluctuations of the currencies over

time. In case of Kuwaiti Dinar, it pegged with a basket of different major currencies. One of the most

major currency that Kuwaiti Dinar was pegged with is the GBP. There are a lot of time series models

used for forecasting short term period data. ARIMA and exponential smoothing models can be used for

estimating and forecasting the exchange rate. The British Sterling Pound (GBP) is considered one of

the major international currency world wide and has a significant impact on the economy of most

countries through trade and monetary transactions, therefore, the Kuwaiti Dinar was pegged with GPB.

Study the exchange rate of currencies play an important role in the economy of the countries

with respect to give an indication of economy situation for example if the exchange rate of the currency

for the country is low against major international currencies that give indication of worse economy for

that country, but if the price of the exchange rate is high this indicate that the economy is in good

situation. Also the exchange rate of the currencies plays an important impact in business transaction

and oil prices, therefore it is important to built a statistical model for forecasting the exchange rate of

the currency in the sense that forecasting is very crucial in many types of organizations since

predictions of future events must be incorporated into the decision-making process. In finance, interest

rates must be predicted so that the new capital acquisitions can be planned and financed. Financial

planners must also forecast the exchange rate of currencies in money transaction market in order to

study the fluctuations of exchange rate prices and its impact in business market.

It is known that the exchange rate is very important in money transactions. The exchange rate

plays an important role in the economy and it has a significant impact in economy with respect to

trading and oil prices as well as monetary market. Therefore, it is important to study the behavior of

currencies and to forecast the fluctuations of the currencies over time. Forecasting financial time series

such as stock prices or exchange rates is important to the investors and the government. A good

forecasting of a financial time series requires strong domain knowledge and good analysis tools.

Economic vitality and inflation rate are highly affected by monetary policies. Financial players must be

sure about the monetary policies in the country they act which is possible by understanding movements

of exchange rates. Therefore, by understanding the movement of exchange rate better, the policy

makers will be able to extract the relevant information about the economic and financial conditions of

the economy. This will enable them to design a better monetary policy for the future which will help

them to achieve their desired objective of price stability and greater employment. Practically most of

the countries have been managed by floating exchange rate system in which the central bank restricts

the free movement of exchange rates. The interventions from central bank are needed to prevent

undesirable or disruptive movements in the exchange rates which cause harm both internal and external

sector of the economy. Similarly, firms or investors might wish to forecast exchange rates to make

asset allocation decisions. Exchange rate is the most important elements of monetary transmission

29 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

process and movement in this price that has a significant pass-through to consumer price. Exchange

rate forecasting is an extensively discussed issue in the literature. Time series models such as ARIMA,

exponential smoothing methodology can be used for estimating, checking and forecasting exchange

rate. There has been an increased number of papers in the literature in recent years, applying several

methods and techniques for exchange rate prediction. Despite the general acceptance of exponential

smoothing, the choice of a specific smoothing model is often a difficult problem. This paper will

briefly cover more simple models, exponential smoothing models proposed by Holt and Brown.

Despite the simpler and clear mathematical tools, forecasting using exponential smoothing models

often leads to results comparable with the results obtained using ARIMA model. One of the major

motivation for this study was the non-existence of research in forecasting exchange rate using an

exponential smoothing models in the countries of the Gulf Cooperation Council’s (GCC) region.

2. Literature Review The important techniques for studying the behavior of the exchange rate of currencies with respect to

modeling and forecasting time series of the exchange rate data of the currencies is the exponential

smoothing models and ARIMA models. There was a lot of studies have been done in the literatures for

modeling and forecasting of the exchange rate values of the currencies. Empirical studies use some

approach like exponential smoothing models to forecast the exchange rate of Kuwaiti Dinar against

Euro and Winter's method was the most suitable for modeling KWD/Euro exchange rate [1]. Another

study was performed in order to illustrate predictability performance among different competitive

models of exponential smoothing models to forecast the exchange rate of Kuwaiti Dinar against US

Dollar. The results of the study reveals that the best models were the Triple Exponential Smoothing

(Winter's) [2]. One of the most and simple techniques used for forecasting the time series data which

fluctuated within short period of time is the simple exponential smoothing method, and it is the method

that use weighted moving average of past data as the basis for forecast [3].

Also, a debate through a survey of literature indicate that the exchange rate follows a random

walk or it can be modeled, recent studies in the literatures shows that the exchange rate can be modeled

using time series models such as exponential smoothing models and Arima models. Compared time

series models for the exchange rate based on out of sample forecasting accuracy have done and found

that in the short period of time random walk model outperforms a fundamental based in determination

the exchange rate.

3. The Scope of the Study The scope of the study is attempted to tackle the following goals:

1. The main goal of the study is to compare the predictability performance among different

competitive models to forecast the exchange rate of Kuwaiti Dinar against British pound

sterling in terms of international trade.

2. Study the contribution of the British Pound Sterling on the stability of Kuwaiti Dinar.

3. Study the impact of the exchange rate of the British pound sterling on Kuwait economy with

respect to trade transaction and oil export.

4. Methodology Data Analysis: The data of the exchange rate of British Sterling pound (GBP) against Kuwaiti Dinar

was collected in a daily basis for a period of five years which started from 6th

of January 2014 till 8

th

of November 2019.

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 30

A Descriptive Statistics for the Actual Data

In order to assess the normality of the data which is the fundamental assumption of many financial

model, the measures of shape – skewness and kurtosis are of interest. The results show skewness equal

to 0.308080 (positive value) that means the distribution of the data is approximately symmetric with

tail extending toward more positive values. Kurtosis (Kenney and Keeping 1951) characterizes the

relative peakedness or flatness of a distribution compared with the normal distribution. Since the data

has a kurtosis equal to 1.561385 (less than 3), then the data has lighter tail than the normal distribution.

Jarque-Bera for normality test is significant at 5% reveals that the normality is satisfied as shown in

table-1.

Table 1: Result of descriptive statistic for the actual data

Series GBPKWD

Sample 1/06/2014 11/08/2019

Observations 1525

Mean 0.420214

Median 0.405300

Maximum 0.483600

Minimum 0.365500

Std. Dev 0.035214

Skewness 0.308080

Kurtosis 1.561385

Jarque-Bera 155.6305

Probability 0.000000

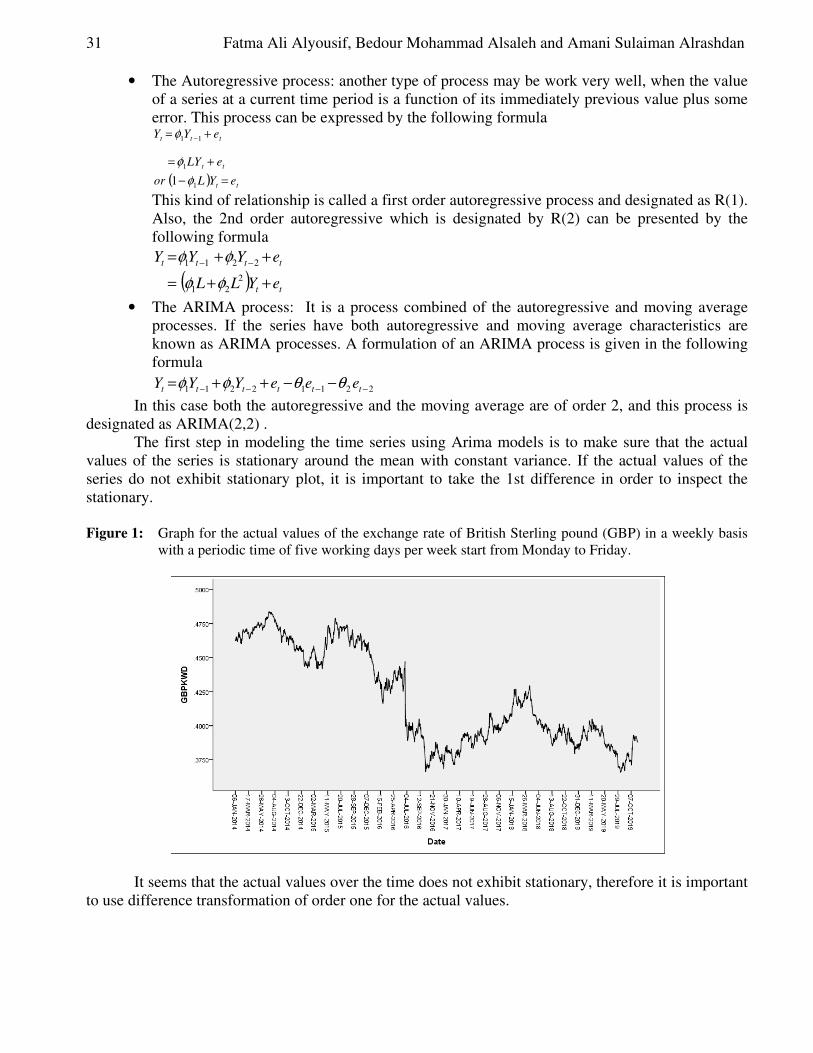

In order to forecast the time series, it is important to plot the actual data to inspect the

qualitative features of the observations over time, such as seasonality trend and non-seasonality trend

as well as the outliers. Figure-1 shows the plot of the actual exchange rate of GBP against Kuwaiti

Dinar (KD). The series exhibit a seasonal with major peaks for the period from 6th

of July 2014 to 8th

of November 2019 and with several minor peaks for the rest of the periods.

It is clear from that the series does not exhibit a stationary series as the values of the series does

not fluctuate around a constant mean and variance. There are no outlier values appear in the graph also.

Forecasting Techniques

The forecasting techniques will employ the following methodologies.

The Box-Jenkins Methodology

Box-Jenkins time series analysis requires a complete time series. If the series has outliers, these

outliers may follow from aberrations in the series. The researcher may consider them missing values

and use the missing value replacement process to replace them. In this way, he can prepare a complete

time series, with equally spaced temporal intervals, prior to Box-Jenkins analysis. In order to identify

and use the Box-jenkins methodology it is important to determine and check the stationary of the

series. The Box - Jenkins methodology consists of the following process:

• The Moving average process; can be expressed by the following moving average formula

( )LeeeY tttt 111 1 θθ −=−= − where ty is the original series , µ is the mean of the series , tY is the mean centered series or

µ−= tt yY is the shock at time t, 1−te is the previous shock, and 1θ is the moving average

coefficient. This kind of relation is called first moving average and designated as M(1) .

31 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

• The Autoregressive process: another type of process may be work very well, when the value

of a series at a current time period is a function of its immediately previous value plus some

error. This process can be expressed by the following formula

( ) tt

tt

ttt

eYLor

eLY

eYY

=−

+=

+= −

1

1

11

1 φ

φ

φ

This kind of relationship is called a first order autoregressive process and designated as R(1).

Also, the 2nd order autoregressive which is designated by R(2) can be presented by the

following formula

( ) tt

tttt

eYLL

eYYY

++=

++= −−

2

21

2211

φφ

φφ

• The ARIMA process: It is a process combined of the autoregressive and moving average

processes. If the series have both autoregressive and moving average characteristics are

known as ARIMA processes. A formulation of an ARIMA process is given in the following

formula

22112211 −−−− −−++= tttttt eeeYYY θθφφ

In this case both the autoregressive and the moving average are of order 2, and this process is

designated as ARIMA(2,2) .

The first step in modeling the time series using Arima models is to make sure that the actual

values of the series is stationary around the mean with constant variance. If the actual values of the

series do not exhibit stationary plot, it is important to take the 1st difference in order to inspect the

stationary.

Figure 1: Graph for the actual values of the exchange rate of British Sterling pound (GBP) in a weekly basis

with a periodic time of five working days per week start from Monday to Friday.

It seems that the actual values over the time does not exhibit stationary, therefore it is important

to use difference transformation of order one for the actual values.

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 32

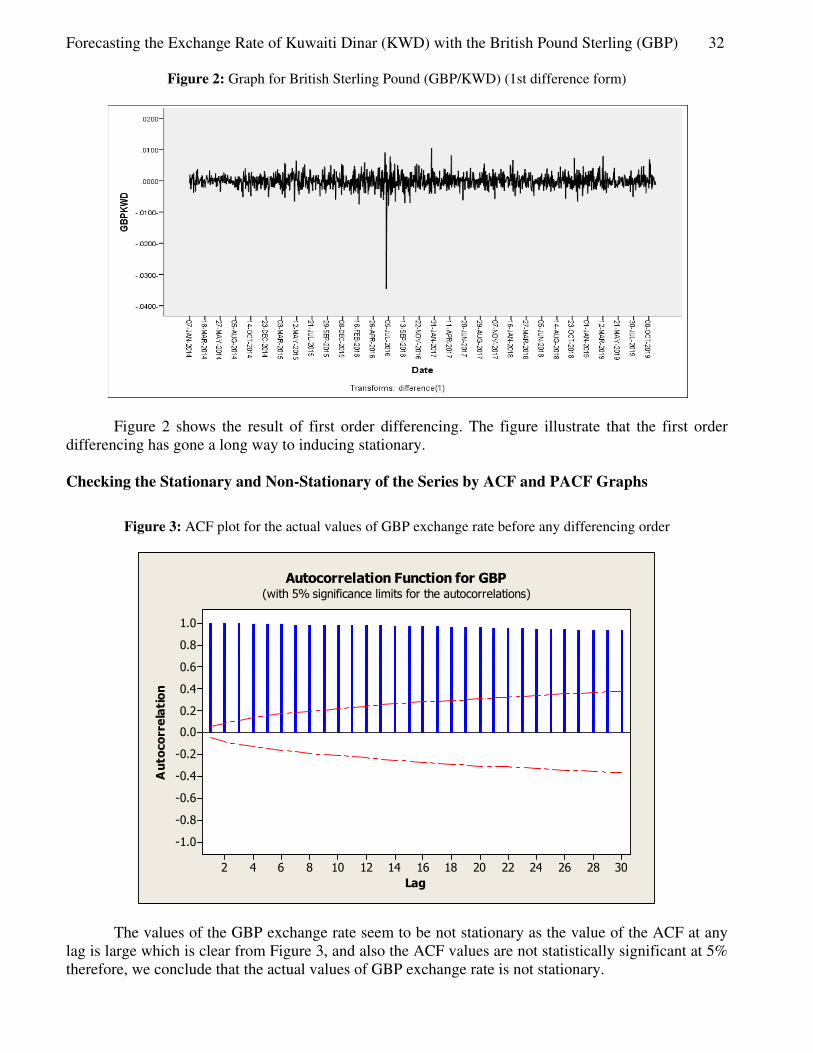

Figure 2: Graph for British Sterling Pound (GBP/KWD) (1st difference form)

Figure 2 shows the result of first order differencing. The figure illustrate that the first order

differencing has gone a long way to inducing stationary.

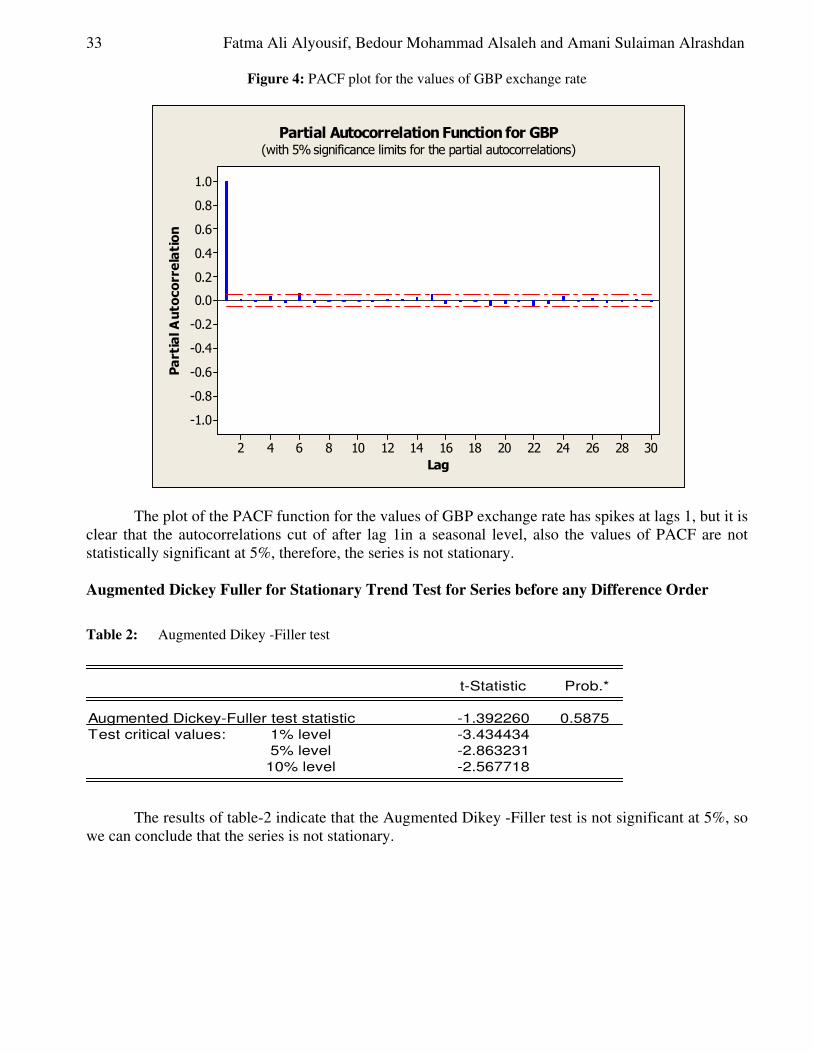

Checking the Stationary and Non-Stationary of the Series by ACF and PACF Graphs

Figure 3: ACF plot for the actual values of GBP exchange rate before any differencing order

30282624222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Au

toco

rre

lati

on

Autocorrelation Function for GBP(with 5% significance limits for the autocorrelations)

The values of the GBP exchange rate seem to be not stationary as the value of the ACF at any

lag is large which is clear from Figure 3, and also the ACF values are not statistically significant at 5%

therefore, we conclude that the actual values of GBP exchange rate is not stationary.

33 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

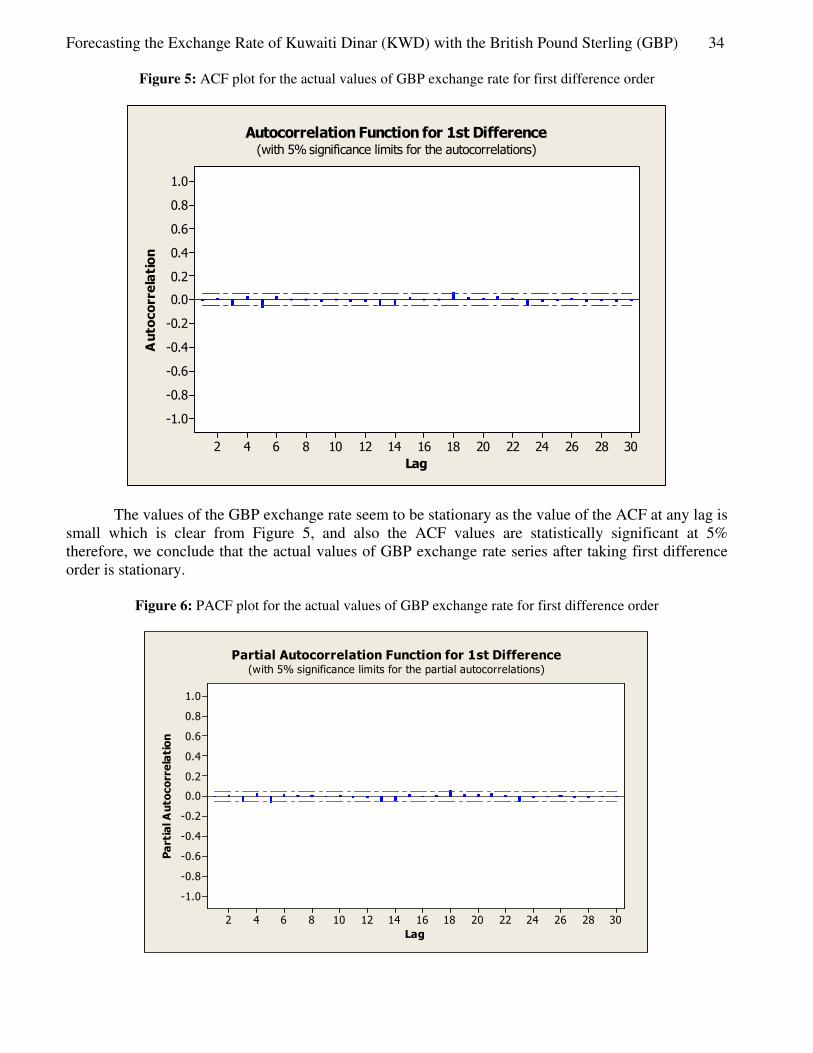

Figure 4: PACF plot for the values of GBP exchange rate

30282624222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Pa

rtia

l A

uto

co

rre

lati

on

Partial Autocorrelation Function for GBP(with 5% significance limits for the partial autocorrelations)

The plot of the PACF function for the values of GBP exchange rate has spikes at lags 1, but it is

clear that the autocorrelations cut of after lag 1in a seasonal level, also the values of PACF are not

statistically significant at 5%, therefore, the series is not stationary.

Augmented Dickey Fuller for Stationary Trend Test for Series before any Difference Order

Table 2: Augmented Dikey -Filler test

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -1.392260 0.5875

Test critical values: 1% level -3.434434

5% level -2.863231

10% level -2.567718

The results of table-2 indicate that the Augmented Dikey -Filler test is not significant at 5%, so

we can conclude that the series is not stationary.

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 34

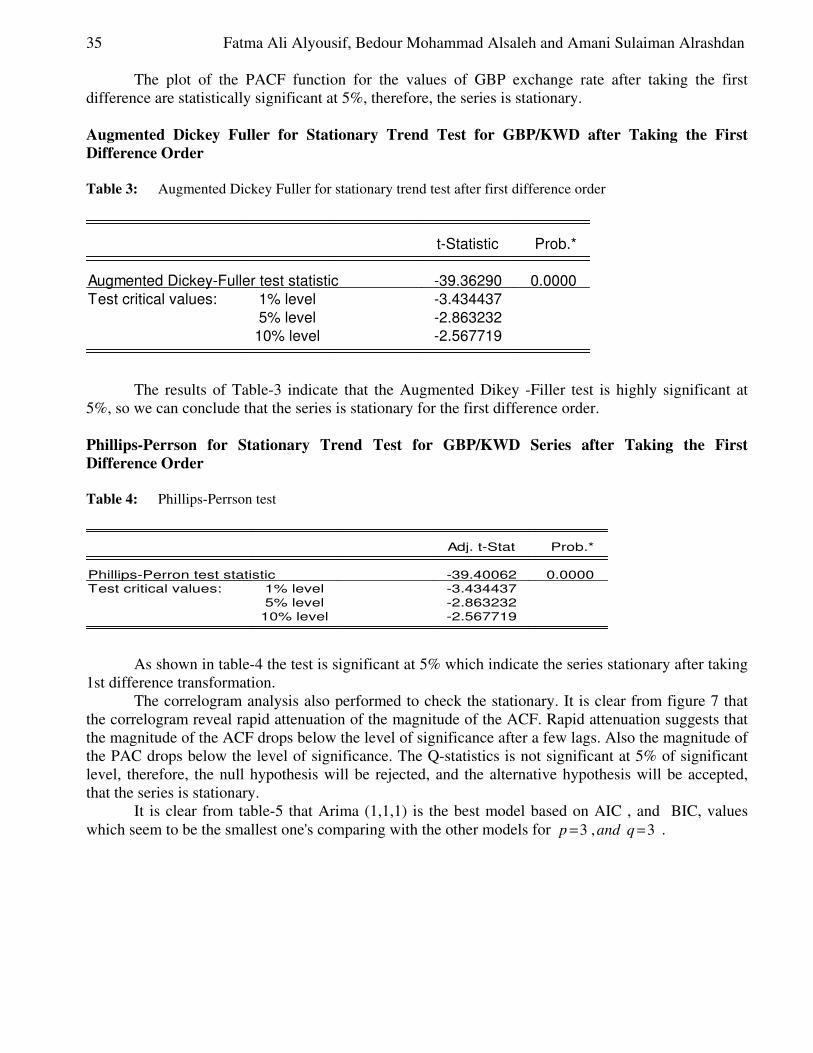

Figure 5: ACF plot for the actual values of GBP exchange rate for first difference order

30282624222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Au

toco

rre

lati

on

Autocorrelation Function for 1st Difference(with 5% significance limits for the autocorrelations)

The values of the GBP exchange rate seem to be stationary as the value of the ACF at any lag is

small which is clear from Figure 5, and also the ACF values are statistically significant at 5%

therefore, we conclude that the actual values of GBP exchange rate series after taking first difference

order is stationary.

Figure 6: PACF plot for the actual values of GBP exchange rate for first difference order

30282624222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Pa

rtia

l A

uto

co

rre

lati

on

Partial Autocorrelation Function for 1st Difference(with 5% significance limits for the partial autocorrelations)

35 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

The plot of the PACF function for the values of GBP exchange rate after taking the first

difference are statistically significant at 5%, therefore, the series is stationary.

Augmented Dickey Fuller for Stationary Trend Test for GBP/KWD after Taking the First

Difference Order

Table 3: Augmented Dickey Fuller for stationary trend test after first difference order

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -39.36290 0.0000

Test critical values: 1% level -3.434437

5% level -2.863232

10% level -2.567719

The results of Table-3 indicate that the Augmented Dikey -Filler test is highly significant at

5%, so we can conclude that the series is stationary for the first difference order.

Phillips-Perrson for Stationary Trend Test for GBP/KWD Series after Taking the First

Difference Order

Table 4: Phillips-Perrson test

Adj. t-Stat Prob.*

Phillips-Perron test statistic -39.40062 0.0000

Test critical values: 1% level -3.434437

5% level -2.863232

10% level -2.567719

As shown in table-4 the test is significant at 5% which indicate the series stationary after taking

1st difference transformation.

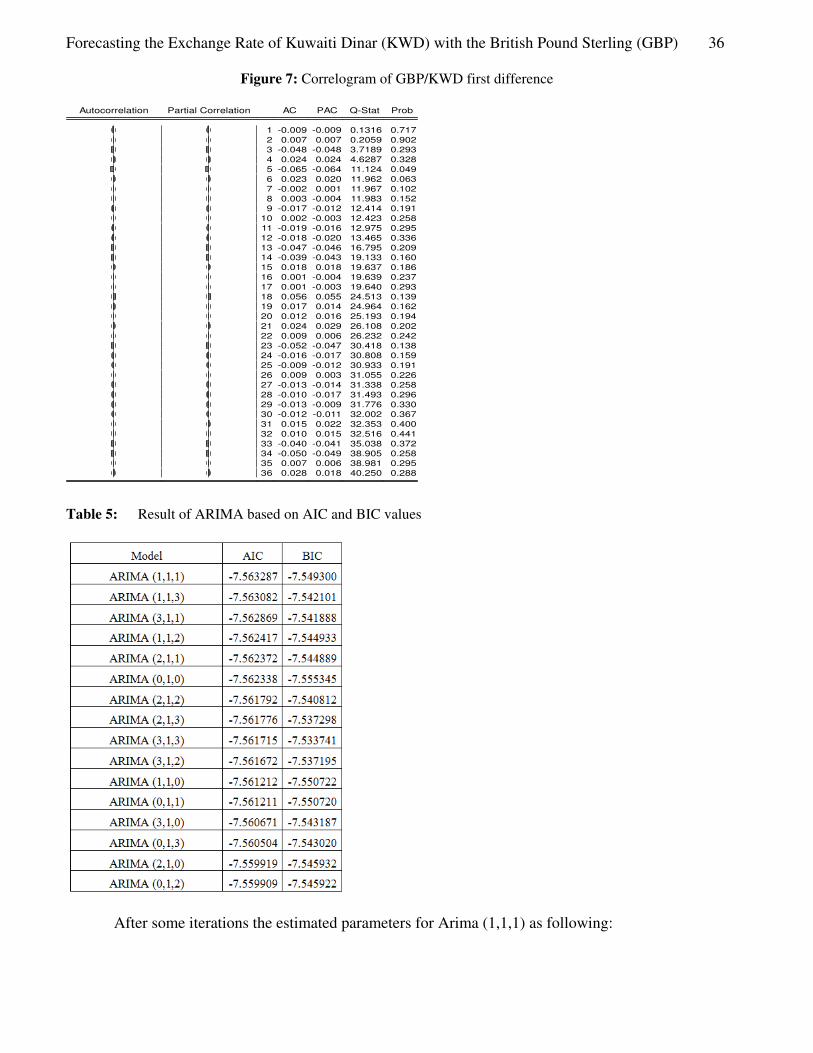

The correlogram analysis also performed to check the stationary. It is clear from figure 7 that

the correlogram reveal rapid attenuation of the magnitude of the ACF. Rapid attenuation suggests that

the magnitude of the ACF drops below the level of significance after a few lags. Also the magnitude of

the PAC drops below the level of significance. The Q-statistics is not significant at 5% of significant

level, therefore, the null hypothesis will be rejected, and the alternative hypothesis will be accepted,

that the series is stationary.

It is clear from table-5 that Arima (1,1,1) is the best model based on AIC , and BIC, values

which seem to be the smallest one's comparing with the other models for 3,3 == qandp .

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 36

Figure 7: Correlogram of GBP/KWD first difference

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 -0.009 -0.009 0.1316 0.717

2 0.007 0.007 0.2059 0.902

3 -0.048 -0.048 3.7189 0.293

4 0.024 0.024 4.6287 0.328

5 -0.065 -0.064 11.124 0.049

6 0.023 0.020 11.962 0.063

7 -0.002 0.001 11.967 0.102

8 0.003 -0.004 11.983 0.152

9 -0.017 -0.012 12.414 0.191

10 0.002 -0.003 12.423 0.258

11 -0.019 -0.016 12.975 0.295

12 -0.018 -0.020 13.465 0.336

13 -0.047 -0.046 16.795 0.209

14 -0.039 -0.043 19.133 0.160

15 0.018 0.018 19.637 0.186

16 0.001 -0.004 19.639 0.237

17 0.001 -0.003 19.640 0.293

18 0.056 0.055 24.513 0.139

19 0.017 0.014 24.964 0.162

20 0.012 0.016 25.193 0.194

21 0.024 0.029 26.108 0.202

22 0.009 0.006 26.232 0.242

23 -0.052 -0.047 30.418 0.138

24 -0.016 -0.017 30.808 0.159

25 -0.009 -0.012 30.933 0.191

26 0.009 0.003 31.055 0.226

27 -0.013 -0.014 31.338 0.258

28 -0.010 -0.017 31.493 0.296

29 -0.013 -0.009 31.776 0.330

30 -0.012 -0.011 32.002 0.367

31 0.015 0.022 32.353 0.400

32 0.010 0.015 32.516 0.441

33 -0.040 -0.041 35.038 0.372

34 -0.050 -0.049 38.905 0.258

35 0.007 0.006 38.981 0.295

36 0.028 0.018 40.250 0.288

Table 5: Result of ARIMA based on AIC and BIC values

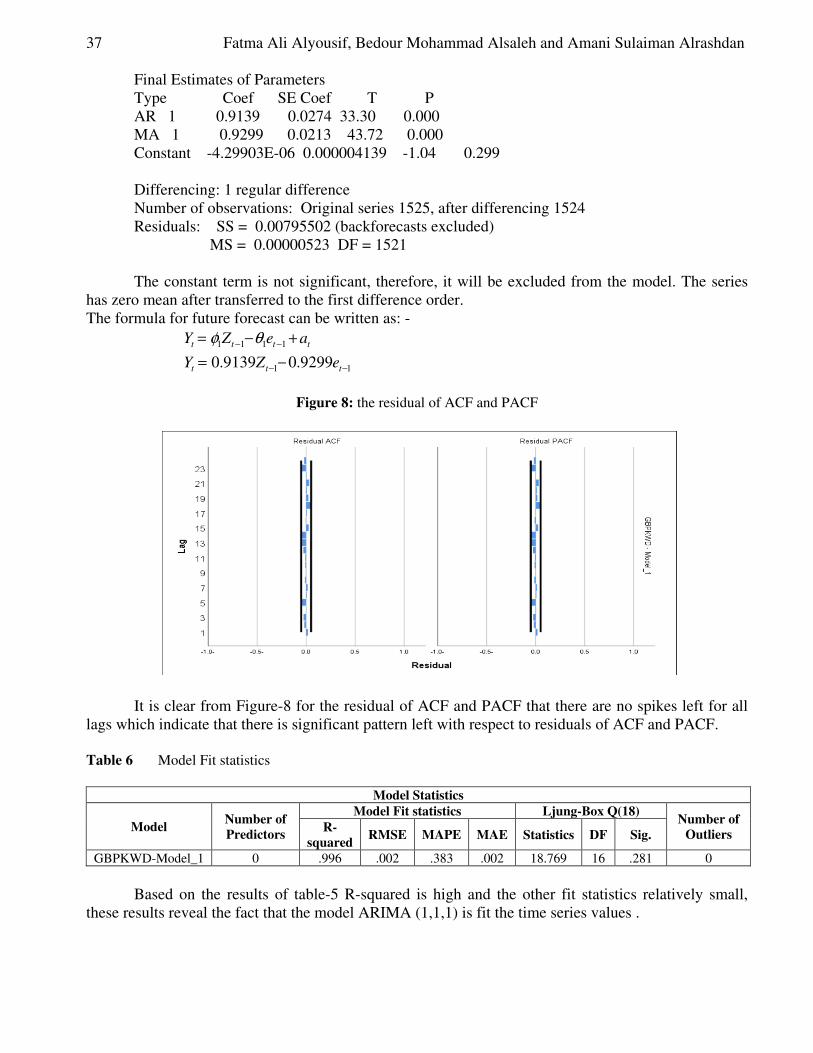

After some iterations the estimated parameters for Arima (1,1,1) as following:

37 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

Final Estimates of Parameters

Type Coef SE Coef T P

AR 1 0.9139 0.0274 33.30 0.000

MA 1 0.9299 0.0213 43.72 0.000

Constant -4.29903E-06 0.000004139 -1.04 0.299

Differencing: 1 regular difference

Number of observations: Original series 1525, after differencing 1524

Residuals: SS = 0.00795502 (backforecasts excluded)

MS = 0.00000523 DF = 1521

The constant term is not significant, therefore, it will be excluded from the model. The series

has zero mean after transferred to the first difference order.

The formula for future forecast can be written as: -

tttt aeZY +−= −− 1111 θφ

11 9299.09139.0 −− −= ttt eZY

Figure 8: the residual of ACF and PACF

It is clear from Figure-8 for the residual of ACF and PACF that there are no spikes left for all

lags which indicate that there is significant pattern left with respect to residuals of ACF and PACF.

Table 6 Model Fit statistics

Model Statistics

Model Number of

Predictors

Model Fit statistics Ljung-Box Q(18) Number of

Outliers R-

squared RMSE MAPE MAE Statistics DF Sig.

GBPKWD-Model_1 0 .996 .002 .383 .002 18.769 16 .281 0

Based on the results of table-5 R-squared is high and the other fit statistics relatively small,

these results reveal the fact that the model ARIMA (1,1,1) is fit the time series values .

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 38

The Exponential Smoothing Models

A Single Exponential Smoothing (SES)

Suppose that the time series is described by the model where the average level

β�

may be slowly changing over time. Then the estimate of β�

made in time period T is given

by the smoothing equation where is smoothing constant between 0 and 1

and is the estimate of β�

made in time period T - 1.

A point forecast made in time period T for is Where .

This model is applied assuming that the series is stationary, without trend. Simple exponential

smoothing is used for short – range forecasting .The value of α is usually determined by minimizing

the sum of squares of the forecast errors.

Holt-Winters' Two-Parameter Double Exponential Smoothing (HDES)

Suppose that the time series described by the model

where the parameters β

� and 1β may be slowly changing over time.

two-parameter double exponential smoothing is a smoothing approach for forecasting such a time

series that employs two smoothing constants.

Suppose that in time period T-1 we have an estimate of the average level of the time

series That is, is an estimate of the intercept of the time series when the time origin is

considered to be time period T-1. Also suppose that in time period T — 1 we have an estimate

of the slope parameter 1β . If we observe Ty in time period T, then we can update

and then we can compute point estimate follows:

If we observe Ty in time period 'T, then

1. We obtain an updated estimate of the intercept parameter β�by using the equation

where α is a smoothing constant between 0 and 1.

2. We obtain an updated estimate of the slope parameter 1β by using the equation

where β is a smoothing constant between 0 and 1.

3. A point forecast of the future value made at time T is

This model is appropriate for series with linear trend and no seasonal variations.

Holt-Winters' Multiplicative Exponential Smoothing (HMES).

Winters' method is an exponential smoothing approach to handling seasonal data .Although the method

is not based on a formal statistical model , multiplicative Winters' method is generally considered to be

best suited to forecasting a time series that can be described by the equation

Where the time series parameters may be slowly changing over time.

The intercept is β� and the slope is 1β and SNt is the multiplicative seasonal factor .

Each of these three coefficients are defined by the following recursions:

where α is a smoothing constant between 0 and 1 .

where β is a smoothing constant between 0 and 1.

nyy ....,.........1 tty εβ +=�

( )Ta�

( ) ( ) ( )11 −−+= TayTa T ��αα α

( )1−Ta�

τ+Ty ( ).ˆ TayT �=+τ horizontimeaisτ

nyy ....,.........1

tt ty εββ ++= 1�

( )1−Ta�

( )1−Ta�

( )11 −Tb ( )1−Ta�

( )11 −Tb

( )Ta�

( ) ( ) ( ) ( )[ ]111 1 −+−−+= TbTayTa T ��αα

( )Tb1

( ) ( ) ( )[ ] ( ) ( )111 11 −−+−−= TbTaTaTb ββ��

τ+Ty

( ) ( ) ( )ττ TbTaTyT 1ˆ +=+ �

( ) ttt SNty εββ +×+= 1�

( )( )

( ) ( ) ( )[ ]111 1 −+−−+−

= TbTaLTsn

yTa

t

T��

αα

( ) ( ) ( )[ ] ( ) ( )111 11 −−+−−= TbTaTaTb ββ��

39 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

where γ is a smoothing constant between 0 and

The initial estimate of the trend component , is:

The initial estimate of the intercept component , is :

The initial estimate of the multiplicative seasonal factor ,

Holt-Winters' Additive Exponential Smoothing (HAES)

Additive Winters' method is a modification for handling a time series that displays constant seasonal

variation. The method is generally regarded as best suited to forecasting time series that can be

described by the equation:

Where SN t is the additive seasonal factor, the intercept is β

� and the slope is 1β .

The model parameters may be slowly changing over time.

Each of these three coefficients are defined by the following recursions:

where α is a smoothing constant between 0

and 1 .

where β is a smoothing constant between 0 and 1 .

where γ is a smoothing constant between 0 and 1 .

The statistical analysis was done for the exponential smoothing models and the results for each

model was recorded on appendix-II.

The analysis includes: -

5. Residual Model Diagnostics Residual model diagnostics have been conducted with respect to the following: -

• Normality.

• Constant variance.

• Independence

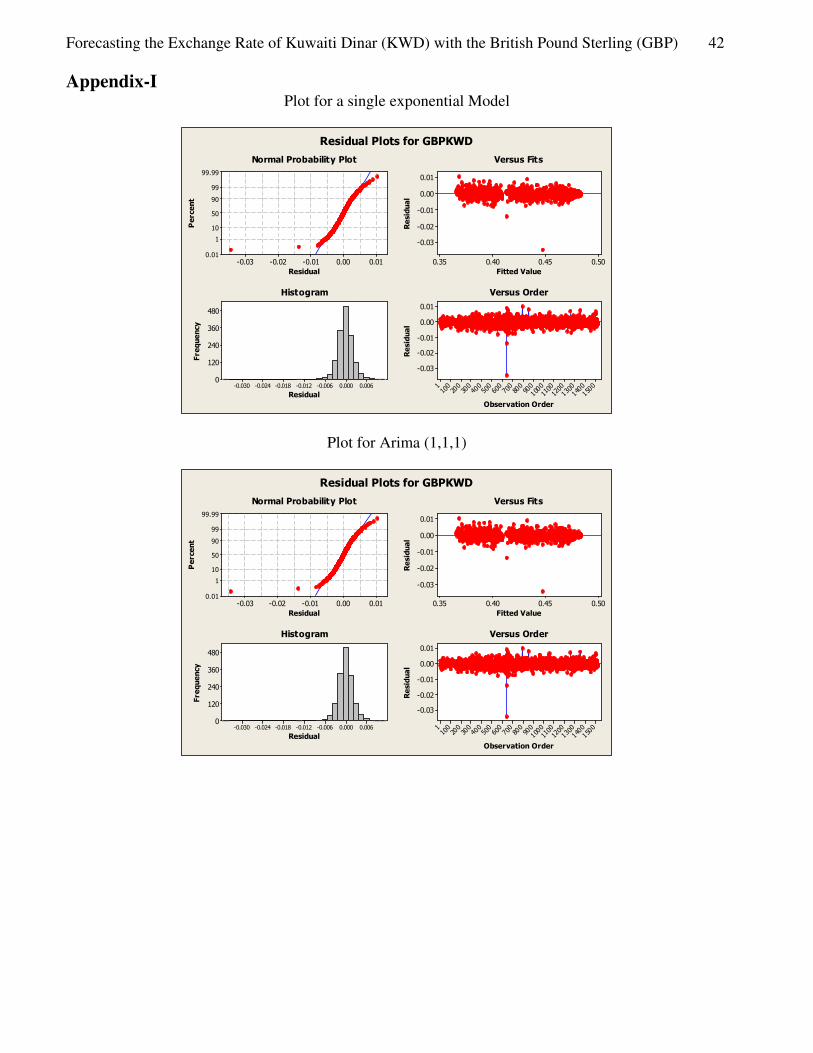

To check the validity of the assumptions, plot of residuals was created for normality, constant

variance and independence assumptions. Plots are in Appendix-I for models.

The normal plot of the residuals have a straight line appearance approximately , which indicate

that a normality assumptions hold , the pattern in which the residuals fluctuate around the zero indicate

the constant variance assumption hold , due to the fact that the residual plot form a horizontal band

appearance and finally a plot of residuals against fit values suggest that , there is no positive or

negative autocorrelation exits in error terms , which indicate that the error terms occur in a random

pattern over time , therefore ,these error terms are statistically independent .

Model Selection Criteria

The following accuracy measures are used to select the best model among the other competitive

models:

Mean absolute error (MAE).

Sum square error (SSE).

Mean squared error (MSE)

Mean percentage error (MPE).

Mean absolute error (MAE).

( )( )

( ) ( )LTsnTa

yTsn T

tt −−+= γγ 1

�

1β ( )( )Lm

yyb m

10 1

1−

−=

�β ( ) ( )0

20 11 b

Lya −=

�

( ) Ltfor

ns

Lnssn

L

t

t

tt ,,,,,,,,,10

1

=

=

=

( ) ttt SNty εββ +++= 1�

( ) ( )[ ] ( ) ( ) ( )[ ]111 1 −+−−+−−= TbTaLTsnyTa TT ��αα

( ) ( ) ( )[ ] ( ) ( )111 11 −−+−−= TbTaTaTb ββ��

( ) ( )[ ] ( ) ( )LTsnTayTsn TTt −−+−= γγ 1�

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 40

These measures are used to compare the forecasting accuracy of the various models. The rule of

thump is the smaller of MAE, SSE, MSE, MPE and MAE the better is the forecasting ability. The

model with the smallest of the accuracy measures will be the best to be used for forecasting.

Table 7: Accuracy Indicators for each exponential model

Exponential Models Accuracy Indicators

MAE SSE MSE MPE MAPE

Single 0.001591 0.008038 0.000005 -0.014720 0.383021

Double Exp. Brown 0.001764 0.009594 0.000006 0.000579 0.424309

Double Exp. Holt 0.001656 0.008537 0.000006 -0.000258 0.398544

Winter's Multiplicative 0.001652 0.008486 0.000006 0.000876 0.397801

Winter's Additive 0.001652 0.008487 0.000006 0.000892 0.397789

An important objective of this study is to search the best predictive performance model among

all the competitive models, table-7 shows the summary results for all five exponential models, the best

one is based on the results of the analysis displayed on table-6, the single exponential model is the best

model comparing with the other models.

6. Conclusion It is concluded that this study assessed the capability of the forecasting models for forecasting the

exchange rate of KWD against GBP. The empirical results reveal the fact that ARIMA (1,1,1) model,

produce a superior result in forecasting KWD/GBP exchange rate data than the other Arima models.

Also, a single exponential model is the best model comparing to the other exponential smoothing

models based on the measure’s accuracy criteria.

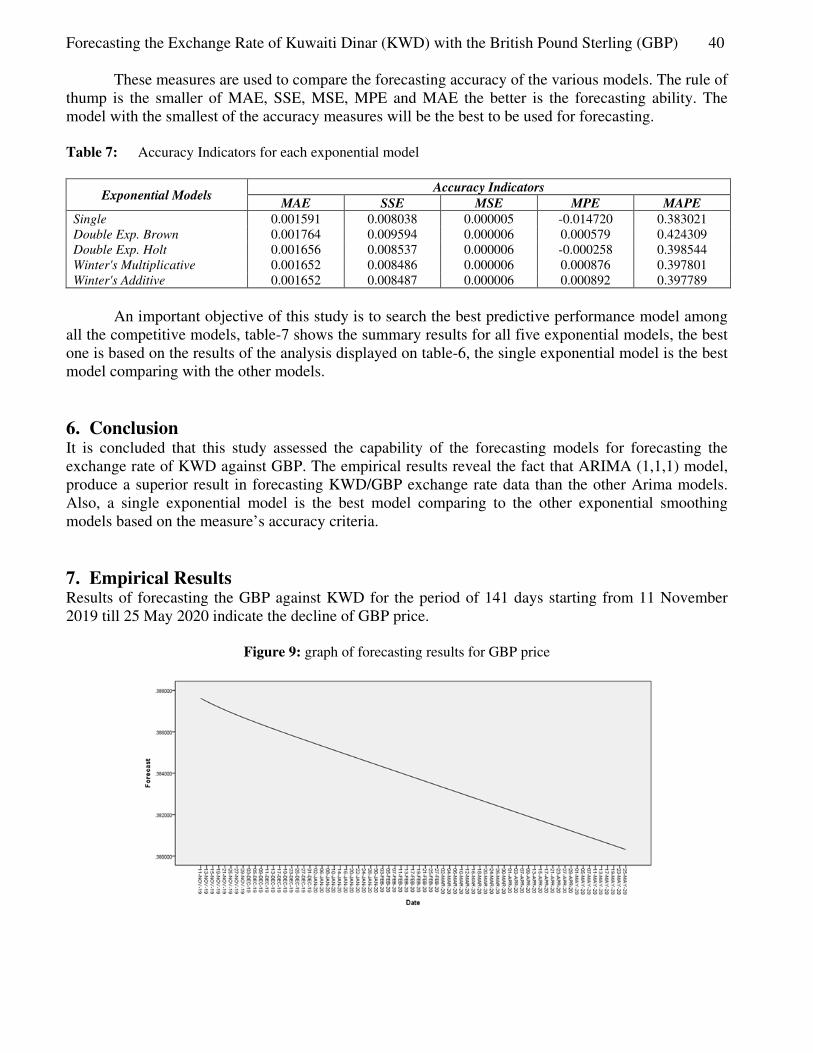

7. Empirical Results Results of forecasting the GBP against KWD for the period of 141 days starting from 11 November

2019 till 25 May 2020 indicate the decline of GBP price.

Figure 9: graph of forecasting results for GBP price

41 Fatma Ali Alyousif, Bedour Mohammad Alsaleh and Amani Sulaiman Alrashdan

References [1] Mohammad Al-Saleh, and Wafaa Al-Khariof, 2014. “Comparing the performance of

Exponential Smoothing Models for Forecasting Exchange”, European Journal of Scientific

Research 119, No 2, pp. 284-293.

[2] Wafaa Al-Khariof, and Adel Hussain Hammuda, 2015. “Comparing the Performance of Time

Series Models for Forecasting the Kuwaiti Dinar Against the UD Dollar “, European Journal of

Scientific Research 129, No 4, pp. 367-379.

[3] Eva Ostertagova, and Oskar Ostertage, 2012. “Forecasting Using Simple Exponential

Smoothing Method”, Acta Electrotechnica 12, No 3, pp. 62-66.

[4] Clark, T., and K. West, 2010. “Approximately Normal Tests for Equal Predictive Accuracy in

Nested Models”, Journal of Econometrics 138, pp. 291-311.

[5] Diebold, F., and R. Mariano, 2009. “Comparing Predictive Accuracy”, Journal of Business and

Economic Statistics 13, pp. 253-265.

[6] Clements, M., and D. Hendry, 1999. “Forecasting Non-Stationary Economic Time Series”,

Cambridge University Press.

[7] J. H. Wilson, and B. Keating. “Business Forecasting”, Irwin (5th edition).

[8] K. Styrin, 2008. “Exchange Rate Forecasting with Structural Shocks as Predictors”, Job Market Paper.

[9] F. Vitek, 2005. “The Exchange Rate Forecasting Puzzles”, University of British Columbia.

[10] Akaike, H., 1974. “A new Look at the Statistical Model identification”, IEEE Transaction of

Automatic control 19: 716-723.

[11] Bartolini, L. and Prati, A., 1999. “Soft exchange rate bands and speculative attacks: Theory, and

evidence from the ERM since August 1993", Journal of International Economics 49: 1—29.

[12] Bekaert, G. and Gray, S. F., 1998. “Target zones and exchange rates: An empirical

Investigation”, Journal of International Economics 45: 1—35.

[13] Bollerslev, T., 1986. “Generalized autoregressive conditional heteroskedasticity”, Journal of

Econometrics 31: 307—327.

[14] Brooks, C. and Rev´eiz, A. H., 2002. “A model for exchange rates with crawling bands - an

application to the Colombian peso”, Journal of Economics and Business 54: 483—503.

[15] Chung, C.-S. and Tauchen, G., 2001. “Testing target-zone models using efficient method of

moments”, Journal of Business and Economic Statistics 19: 255—269.

[16] Forbes, C. S. and Kofman, P., 2000. “Bayesian target zones”. Working Paper, Monash

University.

[17] Granger, C. W. J. and Ter¨asvirta, T., 1993. “Modelling Nonlinear Economic Relationships”,

Oxford University.

Forecasting the Exchange Rate of Kuwaiti Dinar (KWD) with the British Pound Sterling (GBP) 42

Appendix-I Plot for a single exponential Model

0.010.00-0.01-0.02-0.03

99.99

99

90

50

10

1

0.01

Residual

Pe

rce

nt

0.500.450.400.35

0.01

0.00

-0.01

-0.02

-0.03

Fitted Value

Re

sid

ua

l

0.0060.000-0.006-0.012-0.018-0.024-0.030

480

360

240

120

0

Residual

Fre

qu

en

cy

1500

1400

1300

1200

1100

100090

080

070

060

050

040

030

020

010

01

0.01

0.00

-0.01

-0.02

-0.03

Observation OrderR

esid

ua

l

Normal Probability Plot Versus Fits

Histogram Versus Order

Residual Plots for GBPKWD

Plot for Arima (1,1,1)

0.010.00-0.01-0.02-0.03

99.99

99

90

50

10

1

0.01

Residual

Pe

rce

nt

0.500.450.400.35

0.01

0.00

-0.01

-0.02

-0.03

Fitted Value

Re

sid

ua

l

0.0060.000-0.006-0.012-0.018-0.024-0.030

480

360

240

120

0

Residual

Fre

qu

en

cy

1500

1400

1300

1200

1100

100090

080

070

060

050

040

030

020

010

01

0.01

0.00

-0.01

-0.02

-0.03

Observation Order

Re

sid

ua

l

Normal Probability Plot Versus Fits

Histogram Versus Order

Residual Plots for GBPKWD

Related Documents