Firstsource Solutions Limited August 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Firstsource Solutions Limited

August 2011

Firstsource © 2011 | Confidential | August 29, 2011 | 2

Disclaimer

Certain statements in this presentation concerning our future growth prospects are forward-looking

statements, which involve a number of risks, and uncertainties that could cause actual results to differ

materially from those in such forward-looking statements. The risks and uncertainties relating to these

statements include, but are not limited to risks and uncertainties regarding fluctuations in earnings, our

ability to manage growth, intense competition in BPO services including those factors which may affect our

cost advantage, wage increases, our ability to attract and retain highly skilled professional, time and cost

overruns on fixed-price, fixed-time frame contracts, client concentration, our ability to manage ramp-ups and

growth, our ability to manage our international operations, reduced demand in our key focus verticals,

disruptions in telecom infrastructure and technology, our ability to successfully complete and integrate

potential acquisitions, liability for damages on our service contracts, performance of our subsidiaries,

withdrawal of government fiscal incentives, political instability, legal restrictions on raising capital and

acquiring companies outside India, unauthorized use of our intellectual property and general economic

conditions affecting our industry. Firstsource may, from time to time, make additional written and oral

forward-looking statements, including our reports to shareholders. The company does not undertake to

update any forward-looking statements that may be made from time to time by or on behalf of the company.

Firstsource © 2011 | Confidential | August 29, 2011 | 3

Agenda

Overview

Business Units

Financial Summary

Firstsource © 2011 | Confidential | August 29, 2011 | 4

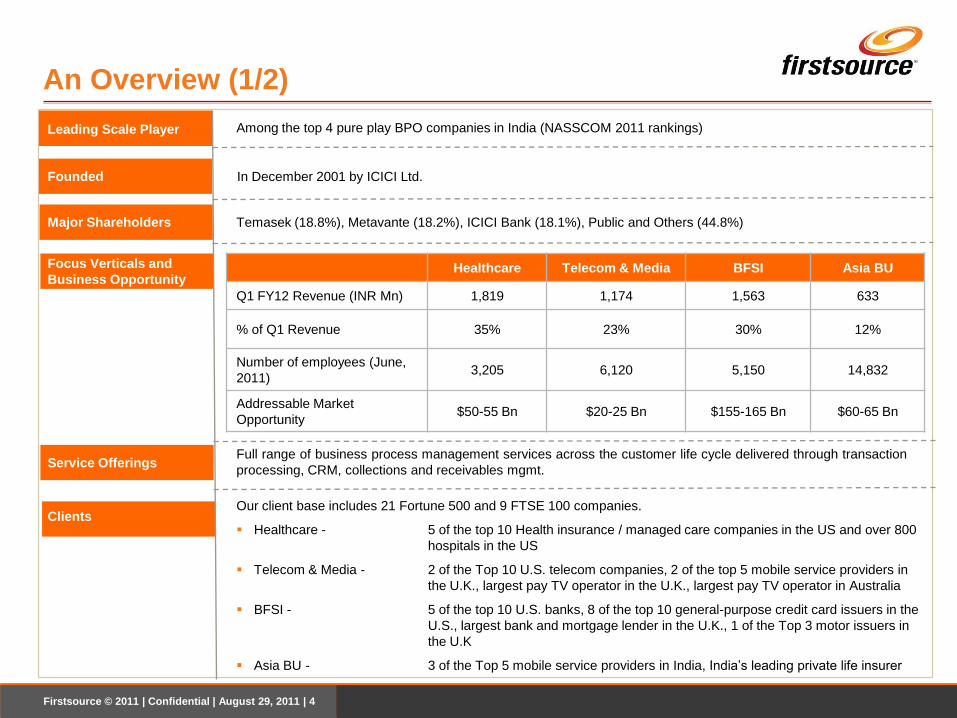

An Overview (1/2)

Leading Scale Player

Founded

Major Shareholders

Focus Verticals and

Business Opportunity

Service Offerings

Clients

Among the top 4 pure play BPO companies in India (NASSCOM 2011 rankings)

In December 2001 by ICICI Ltd.

Healthcare Telecom & Media BFSI Asia BU

Q1 FY12 Revenue (INR Mn) 1,819 1,174 1,563 633

% of Q1 Revenue 35% 23% 30% 12%

Number of employees (June,

2011)3,205 6,120 5,150 14,832

Addressable Market

Opportunity$50-55 Bn $20-25 Bn $155-165 Bn $60-65 Bn

Temasek (18.8%), Metavante (18.2%), ICICI Bank (18.1%), Public and Others (44.8%)

Full range of business process management services across the customer life cycle delivered through transaction

processing, CRM, collections and receivables mgmt.

Our client base includes 21 Fortune 500 and 9 FTSE 100 companies.

Healthcare - 5 of the top 10 Health insurance / managed care companies in the US and over 800

hospitals in the US

Telecom & Media - 2 of the Top 10 U.S. telecom companies, 2 of the top 5 mobile service providers in

the U.K., largest pay TV operator in the U.K., largest pay TV operator in Australia

BFSI - 5 of the top 10 U.S. banks, 8 of the top 10 general-purpose credit card issuers in the

U.S., largest bank and mortgage lender in the U.K., 1 of the Top 3 motor issuers in

the U.K

Asia BU - 3 of the Top 5 mobile service providers in India, India‟s leading private life insurer

Firstsource © 2011 | Confidential | August 29, 2011 | 5

An Overview (2/2)

Client Revenue

Contribution

Employees / Seats

(June2011)

Best in Class Delivery

Financial Snapshot

Largest client - 13%, Top 5 clients – 39%

29,664 / 23,342

Multi-shore delivery model across four countries (India, US, UK and Philippines, Sri Lanka) with 43 delivery locations

Rs. million Q1 FY2011 Q4 FY2011 FY2011 Q1 FY2012 Growth (Y-o-Y)

Operating Revenue ($ mn) $107 $119 $448 $116

Operating Revenue (Rs.) 4,907 5,464 20,553 5,231 6.6%

Operating EBITDA681

13.9%

792

14.5%

2,896

14.1%

429

8.2%-37.0%

Operating EBIT468

9.5%

558

10.2%

2,005

9.8%

209

4.0%-55.3%

PAT321

6.5%

383

7.0%

1,385

6.7%

106

2.0%-66.8%

Firstsource © 2011 | Confidential | August 29, 2011 | 6

Scalable, Global Delivery Platform

USAPhilippines

United Kingdom

India

Enhanced business continuity capability Blended 70% onshore and 30% offshore model Strong Domain Expertise driven business model

Centers:

USA - 14

UK - 2

India - 25

Philippines - 1

14 Centers

3,387 Employees

1 Center

1,089 Employees

2 Centers

2,408 Employees

25 Centers

22,482 Employees

17,755 Seats3,242 Seats

853 Seats

974 Seats

Sri Lanka

Sri Lanka - 1

1 Center

298 Employees

518 Seats

Firstsource © 2011 | Confidential | August 29, 2011 | 7

Agenda

Overview

Business Units

Financial Summary

Firstsource © 2011 | Confidential | August 29, 2011 | 8

Congressional lawmakers continue their

focus on the entitlement programs,

Medicare and Medicaid

U.S. unemployment rose to 9.2% for the

second consecutive month

Provider sector continues to focus on

returning to pre-recession profitability with

increased M&A activity expected

Payer segment remains concentrated on

administrative cost reductions and

implementation of Health Information

Exchanges (HIE)

Healthcare

Headed ByKey Segments

Payer

Provider

Geography

Delivery

Market

Revenue

Employees

35%

Income from

services

(Q1 FY12)

3,205As on

June 30, 2011

Capacity and Utilization

3,221seats

As on

June 30, 2011

73% Seat fill factor

Q1 FY12 Highlights Industry Trends

Continued execution of Provider Sales

strategy, with traction gaining on core

products and services

Payer sales segment remains strong with

new logos being signed, as well as a

deeper penetration into existing client base

being realized

Technology enhancements being

implemented in support of Centers of

Excellence initiatives

Very little pricing volatility; either from

existing clients or in the marketplace;

consistent across both segments of the

healthcare vertical

Insurers continue strong focus on achieving

compliance with Medical Loss Ratio (MLR)

mandates and building capacity for

significant enrollment increases

Hospitals looking beyond traditional back

office structures to address reimbursement

pressure and increases in uninsured

population

Expect stable growth with consistent

financial performance

Business Outlook

Domain Capabilities

1. Data Capture

2. Mailroom Operations

3. Claims Processing

1. Eligibility Determination

2. Revenue Cycle Management

Firstsource © 2011 | Confidential | August 29, 2011 | 9

The UK financial services community are

coming under increasing pressure from

regulatory reform and closer scrutiny

Late 2010 and first half of 2011 have seen

UK mortgages drop. Approved mortgages

have dropped by 6% in April 2011 (y-o-y)

Delinquency rate for cards is the lowest in

recent history

Credit card charge offs also fell in the first

quarter of 2011 to a rate of 7.22 percent,

down from 7.80 percent in the previous

quarter.

BFSI

Key Segments Geography

Delivery

Market

Revenue

Employees

30%

Income from

services

(Q1 FY12)

5.150As on

June 30, 2011

Capacity & Utilization

4,396Seats

As on

June 30, 2011

72% Seat fill factor

Q1 FY12 Highlights Industry Trends

Our Manila operations continue to grow

Introduction to new segments and

increased market share from existing

collections clients on back of strong

operational performance. However,

significant drop in overall collections

volumes has negatively impacted financial

performance

Continued strong SLA performance across

all business units of the vertical

India delivery has seen some pressures on

profitability

Pricing across different parts of business

Business Outlook

Pressure from regulators has resulted in

new opportunities around the complaints

process and compliance in general

Increased interest and traction in onshore

CRM opportunities

Commission rates are expected to continue

on a downward trend as agencies compete

for lower volumes and issuers try to protect

their numbers

Liquidation rates will continue on their

current trajectory and grow at a moderate

pace

Pipeline continues to be healthy

Collections business expected to show a

slow recovery, when new placements are

expected to start moving upwards

Domain CapabilitiesKey Segments

Credit

Cards

Mortgage

Retail

Banking

General

and Life

Insurance

1. Customer service

2. Loans origination &

processing

3. Complaints handling

4. Policy acquisition,

administration & retention

5. Collections and

recoveries

Firstsource © 2011 | Confidential | August 29, 2011 | 10

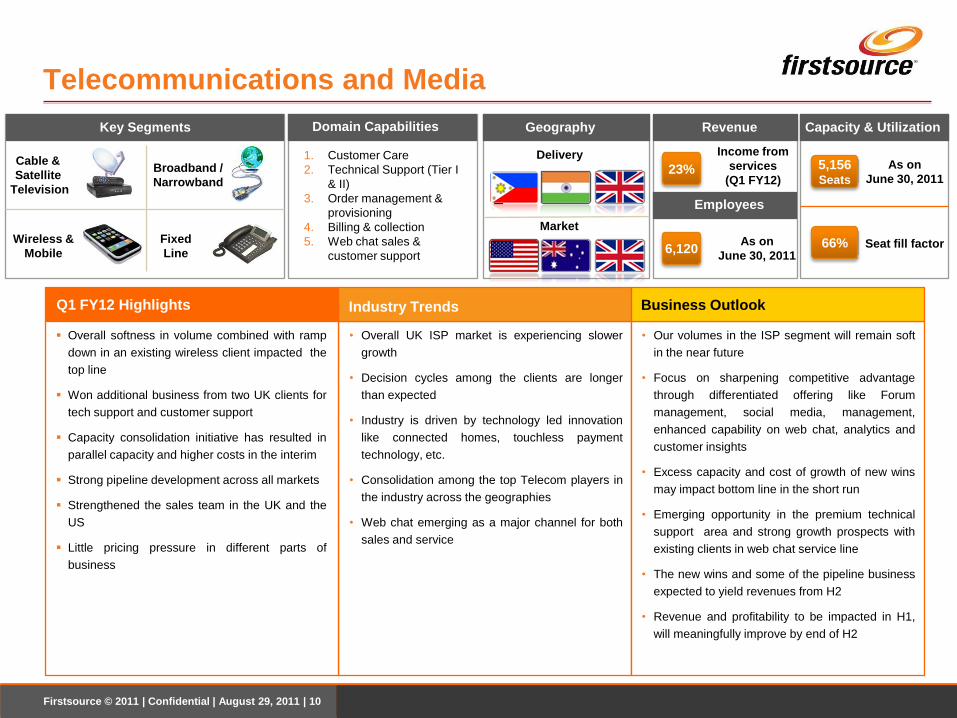

• Overall UK ISP market is experiencing slower

growth

• Decision cycles among the clients are longer

than expected

• Industry is driven by technology led innovation

like connected homes, touchless payment

technology, etc.

• Consolidation among the top Telecom players in

the industry across the geographies

• Web chat emerging as a major channel for both

sales and service

Telecommunications and Media

Key Segments

z

Geography

Delivery

Market

Revenue

Employees

23%

Income from

services

(Q1 FY12)

6,120As on

June 30, 2011

Capacity & Utilization

5,156Seats

As on

June 30, 2011

66% Seat fill factor

Q1 FY12 Highlights Industry Trends

Overall softness in volume combined with ramp

down in an existing wireless client impacted the

top line

Won additional business from two UK clients for

tech support and customer support

Capacity consolidation initiative has resulted in

parallel capacity and higher costs in the interim

Strong pipeline development across all markets

Strengthened the sales team in the UK and the

US

Little pricing pressure in different parts of

business

• Our volumes in the ISP segment will remain soft

in the near future

• Focus on sharpening competitive advantage

through differentiated offering like Forum

management, social media, management,

enhanced capability on web chat, analytics and

customer insights

• Excess capacity and cost of growth of new wins

may impact bottom line in the short run

• Emerging opportunity in the premium technical

support area and strong growth prospects with

existing clients in web chat service line

• The new wins and some of the pipeline business

expected to yield revenues from H2

• Revenue and profitability to be impacted in H1,

will meaningfully improve by end of H2

Business Outlook

Key Segments

Cable &

Satellite

Television

Wireless &

Mobile

Broadband /

Narrowband

Fixed

Line

1. Customer Care

2. Technical Support (Tier I

& II)

3. Order management &

provisioning

4. Billing & collection

5. Web chat sales &

customer support

Domain Capabilities

Firstsource © 2011 | Confidential | August 29, 2011 | 11

Rural BPO expected to be the next inflection

point in the domestic market

„Do Not Call‟ registry expected to be in place

from August 2011

MNP elicits modest response

IT-BPO market in India expected to grow by

17% in 2012

Next wave of growth in Telecom expected

through 3G and VAS

Flurry of activity in the Govt/PSU segment in

India.

Asia Business Unit (ABU)

Geography

Delivery

Market

Revenue

Employees

12%

Income from

services

(Q1 FY12)

14,832As on

June 30, 2011

Capacity and Utilization

10,275seats

As on

June 30, 2011

79% Seat fill factor

Q1 FY12 Highlights Industry Trends

Entered Sri Lanka through a Joint Venture

with Dialog Axiata (Sri Lanka‟s largest

telecom operator), to address opportunities

in Sri Lanka

Strong growth seen from existing telecom

customers : significant ramps undertaken in

Q1, impacting profitability

Increased footprint with existing customers,

through addition of new lines of business /

geographies

Strong focus on operational improvements

Pricing has been largely stable and

expected to follow the same trend

Strong volumes seen from existing

customers : Ramps undertaken in Q1 will

translate into revenue and improved

profitability in Q2

Q2 will have full quarter impact of

Firstsource Dialog Solutions (Joint Venture

in Sri Lanka) deal

Pursuing opportunities in the Middle East

Continued focus on operational efficiencies

Q2 and FY12 revenues will be significantly

higher

Business Outlook

1. Prepaid and Postpaid

2. Outbound

3. Televerification

4. DTH

5. Collections

6. Managed Services

7. Customer Relationship

Management

Domain CapabilitiesKey Segments

Telecom and

Media

BFSI

Firstsource © 2011 | Confidential | August 29, 2011 | 12

Agenda

Overview

Business Units

Financial Summary

Firstsource © 2011 | Confidential | August 29, 2011 | 13

Financial Performance Highlights (1/2)

Operating Revenues

Operating EBITDA

Firstsource © 2011 | Confidential | August 29, 2011 | 14

Financial Performance Highlights (2/2)

Operating EBIT

Profit After Tax (PAT) – Excluding exchange variation, amortisation and gain on

FCCB

Firstsource © 2011 | Confidential | August 29, 2011 | 15

Financial Performance – Last Five Quarters

(IN INR Million) Q1 FY11 Q2 FY11 Q3 FY11 Q4 FY11 FY 2011 Q1 FY2012

Income from services 4,759 4,900 5,048 5,403 20,110 5,189

Other operating Income 148 136 98 61 443 42

Revenue from operations 4,907 5,036 5,146 5,464 20,553 5,231

Personnel & Operating Expense 4,222 4,328 4,435 4,673 17,657 4,802

Operating EBITDA 685 707 711 792 2,896 429

Operating EBITDA % 14.0% 14.0% 13.8% 14.5% 14.1% 8.2%

Depreciation / amortization 213 213 232 233 891 220

Operating EBIT 472 494 479 559 2005 209

Operating EBIT % 9.6% 9.8% 9.3% 10.2% 9.8% 4.0%

Other Income / (expense) 19 7 112 5 142 15

Interest Income / (expense), net (57) (53) (55) (43) (208) (34)

Gain/(loss) due to exchange var. and amortized (cost ) on fair value of FCCB

(30) (31) (32) (35) (129) (35)

Exchange gain/ (loss) on Foreign currency loan 3 (1) 1 5 7 (1)

Extraordinary (expenses) - - (64) - (64) -

PBT 407 415 441 490 1,753 154

PBT (% of total income) 8.3% 8.2% 8.4% 9.0% 8.5% 2.9%

Taxes and Minority Interest 86 83 92 107 368 47

PAT 321 332 350 383 1385 106

PAT (% of total income) 6.5% 6.6% 6.6% 7.0% 6.7% 2.0%

Reported Basic EPS (Rs.) 0.75 0.77 0.81 0.89 3.22 0.25

Reported Diluted EPS (Rs.) 0.68 0.70 0.73 0.80 2.91 0.25

Firstsource © 2011 | Confidential | August 29, 2011 | 16

Q1 FY2012 Highlights

Q1 FY2012 Performance Analysis

Operating Revenue

– Q1 Revenues at Rs 5,231 million

– Y-o-Y growth of 6.6% in INR terms and 7.3% in constant currency terms

– Q-o-Q decline of 4.3% in INR terms and 4.8% in constant currency terms; largely on account of

More pronounced BFSI collections volume fall than usual seasonal weakness

Impact on account of T&M client ramp down and softness in business volumes

Operating EBIT

– Q1 FY12 operating EBIT margins at 4.0%, lower by 620 bps compared to Q4FY11; largely on

account of

Lower than expected revenue momentum

– Expect momentum to pick up in H2 on the back of strong pipeline

Cost of growth in Asia Business Unit

Capacity consolidation initiative has resulted in parallel capacity and higher costs in the interim

– Capacity consolidation to be financially beneficial H2 onwards

Firstsource © 2011 | Confidential | August 29, 2011 | 17

Debt Refinancing Update

Debt Refinancing

Raised $180 million term loan from the international loan syndication market

– The Company‟s United States subsidiary has raised $180 million from a consortium of six financial

institutions

The lenders include overseas branches of Axis Bank, Canara Bank, ICICI Bank and Indian Overseas

Bank along with GE Capital, USA and DBS Bank

– Key terms

The interest rate of the new term loan is lower than the current interest rate on existing loans and the yield

on the FCCB

Interest will be paid quarterly, while principal repayment on this new facility will commence in June 2013

with final maturity in March 2017

Rationale and use of proceeds

– The company has refinanced $64 million of ECB and term loans using proceeds from this new facility

The company has taken advantage of lower interest rates and further spread its debt maturity profile

– Proactively addresses part of redemption gap for FCCB ahead of term

The remaining proceeds, net of expenses, will be used towards the company‟s FCCB redemption in

December 2012

Cash Position

Cash balance of $87 million as on June 30, 2011 compared to $103 million as of March 31, 2011

– Repaid $10 million of post shipment credit facility during the quarter

Cash balance is in excess of $200 million as on date including the proceeds from debt refinancing

Firstsource © 2011 | Confidential | August 29, 2011 | 18

Consolidated Balance Sheet

Rs. million 31-Mar-11 30-Jun-11

Sources of Funds

Share Capital 4,306 4,307

Reserves & Surplus 9,921 9,834

Loan Funds – FCCB 11,586 11,841

Loan Funds – Other Borrowing 3,347 2,912

Minority Interest and net deferred tax liability 59 83

Total 29,218 28,976

Application of Funds

Net Fixed Assets 2,285 2,153

Goodwill 20,454 20,513

Sundry Debtors 2,389 3,105

Unbilled Revenue 1,037 866

Loans and advances 1,685 1,599

Current Liabilities and Provisions (3,207) (3,166)

Cash and Bank balance 3,246 2,897

Investments 1,329 1,009

Total 29,218 28,976

Firstsource © 2011 | Confidential | August 29, 2011 | 19

Q1 FY2012 Highlights

By Geography By Verticals

By Delivery Location Client Concentration

Firstsource © 2011 | Confidential | August 29, 2011 | 20

Business Outlook

Revenue momentum to improve in H2

Gradual improvement in margins expected from Q1

- Expected changes over next few quarters include

□ Completion of large scale ramps in ABU

□ Conversion of strong pipeline and commencement of revenues from new wins and ramps in T&M

□ Completion of capacity consolidation initiatives

□ Even stronger focus on operational efficiencies and cost rationalization

- However, we do encounter few industry specific uncertainties and headwinds

□ Declining volumes in BFSI Collections segment

□ Prolonged decision making cycles

- Overall, with revenues expected to grow over the next few quarters, margins will improve from Q1 level

Moving into Q2 FY11

- Expect flattish revenues and margin improvement

THANK YOUFirstsource (NSE: FSL, BSE: 532809, Reuters: FISO.BO, Bloomberg: FSOL@IN) is a

global provider of customised BPO (business process outsourcing) services to the

Banking and Financial Services, Telecom and Media and Healthcare sectors. Its

clients include FTSE 100, Fortune 500 and Nifty 50 companies. Firstsource has a

“rightshore” delivery model with operations in India, US, UK, Philippines and Sri Lanka.

(www.firstsource.com)

Related Documents