AccountAncy futures Ha mi i g f a cia p i g I amic fac A collaboration between ACCA an KPMG

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 1/24

AccountAncy futures

Hamiig facia pig Iamic fac

A collaboration between ACCA an KPMG

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 2/24

2

© The Association o Chartere Certie Accountants,2010

About ACCA

ACCA (the Association o Chartere CertieAccountants) is the global bo or proessionalaccountants. We aim to oer business-relevant,

rst-choice qualications to people o application,abilit an ambition aroun the worl who seek arewaring career in accountanc, nance anmanagement.

We support our 140,000 members an 404,000stuents throughout their careers, proviing servicesthrough a network o 83 oces an centres. Ourglobal inrastructure means that exams an supportare elivere – an reputation an infuenceevelope – at a local level, irectl benetingstakeholers wherever the are base, or plan to moveto, in pursuit o new career opportunities.

About KPMG

KPMG is a global proessional services organization,with member rms in 144 countries across the worl.KPMG’s Global Financial Services practice has morethan 21,000 partners an proessionals across ourglobal network, who provie auit, tax an avisorservices to retail banking, corporate an investmentbanking, investment management an insurancesectors.

As leaing international proviers o proessionalservices, KPMG rms have alrea plae a signicant

role in assisting organisations aroun the worlealing in Islamic nance. This was recentlrecognise in their being name Euromone’s ‘BestIslamic Assurance an Avisor Services Provier’ orthe thir ear in a row, at the 2010 Euromone IslamicFinance Awars, in Lonon.

About ACCountAnCy Futures

The economic, political an environmental climate hasexpose shortcomings in the wa public polic anregulation have evelope in areas such as nancialregulation, nancial reporting, corporate transparenc,

climate change an assurance provision.

In response to the challenges presente to theaccountanc proession b this new businessenvironment, ACCA’s Accoutac Futurs programmehas our areas o ocus – access to nance, auit ansociet, carbon accounting, an narrative reporting.Through research, comment an events ACCA willcontribute to the orwar agena o the internationalproession, business an societ at large.

.accaga.cm/a

© The Association o Chartere Certie Accountants,September 2010

With istitutios rportig addisclosig similar trasactios idirt was, problms o markt

codc ad comptitivssbcom mor acut or thosistitutios thmslvs as wll asor th dvlopmt o Islamicac i gral. It is importat that all stakholdrs across thglobal markts com togthr adharmois acial rportig o Islamic ac.

This report contains inormation in a summar orm an is o a

general nature. It is not intene to aress all o the issues o a

specic entit an is not a substitute or etaile research or the

exercise o proessional jugement.

While ever care has been taken in the preparation o this paper, no

responsibilit or loss occasione to an person acting or reraining

rom acting as a result o an material in this publication can be

accepte b the authors or the publisher.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 3/24

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 4/24

4

Islamic nance has oten been quote to be growinggloball at a rate o 10–15 per cent per ear, an there aresigns rom major inustr plaers that this growth willcontinue, i not increase, ollowing the nancial crisis.However, the inustr i not emerge rom the crisisunscathe an one o the current challenges is to resolve anumber o critical issues that have arisen rom the crisis.

As i th widr covtioal acial srvics commuit, KPMG blivsow is th right tim to tak a rshlook at th approach to som o ths issus icludig th qualit o acial rportig ad disclosursor Islamic ac.

ACCA is one o the leaing global accountancqualication proviers in the worl with eep resources inke Islamic nance markets, an KPMG is elighte towork with ACCA in this area o thought leaership.

settInG tHe AGendA

The use o International Financial Reporting Stanars(IFRS) has sprea to over 100 countries,2 making them theglobal accounting stanars o choice. Man o thecountries where Islamic nance is prevalent have eitherincorporate IFRS into their nancial reporting rameworksor have committe to oing so. These inclue suchcountries as Inonesia, Iran, Malasia, Pakistan, SauiArabia an Turke, all o whom are also active members othe Asian-Oceanian Stanars-Setters Group (AOSSG).This group o national stanar setters was create to lookat regional issues in the implementation an application oIFRS an to lobb the International Accounting StanarsBoar (IASB) accoringl. Following the rst meeting o thegroup in November 2009, it was also agree that nancialreporting relate to Islamic nance woul be ae to thework programme, with the Malasian AccountingStanars Boar (MASB) taking the lea role.

Similarl the IASB itsel, in its active engagement withother countries an regions, has acknowlege the neeto consier an specic nees or Islamic nance withinthe bo o IFRS. On a visit to the Gul in March 2009, BobGarnett, IASB boar member, note the nee or the IASBto have iscussions with organisations such as AAOIFI(Accounting an Auiting Organisation or Islamic FinancialInstitutions) in orer to unerstan their concerns an howthe can be accommoate within IFRS.

‘Islamic acial products hav baroud much logr tha th IASB.It’s quit a dautig task but it’smor tha just a itllctualchallg. It is importat or thglobal markts that w brig ourslvs togthr.’

BOB GARNETT, IASB BOARd MEMBER ANd CHAIRMAN OF IFRIC

2. International Financial Reporting Stanars (IFRS) are now either

permitte or require or omestic liste companies in some 122

jurisictions, an permitte or unliste companies in 10 others. IAS Plus,

June 2010.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 5/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 5

sCoPe And objeCtIves

This report assesses the extent to which institutionsoering Islamic nance report in a common nancialreporting language an what rives their reportingpractices. It urther outlines ke practices in Islamicnance that are markel istinct rom those oun inconventional nance an that coul thereore lea tomisrepresentations o nancial inormation i the wereaccounte or using IFRS.

As the number o countries requiring the application oIFRS increases, an thereore more nancial institutionsoering Islamic nance are compelle to use thosestanars, these challenges will become more apparentor stanar setters. In commencing this project, ACCAan KPMG aim to take orwar the ebate on how best tointernationalise the nancial reporting practices o Islamicnancial institutions, ocusing in particular on the role that

the IASB an its stanars can pla.

ACCA an KPMG will be engaging with leaing experts anstakeholers internationall an irectl through a serieso roun tables in three major hubs or Islamic nance:Kuala Lumpur, Bahrain an Lonon. These centres haveinfuence throughout the international Islamic nanceinustr, an have alrea riven its evelopment throughsoun expertise an thought leaership.

ACCA an KPMG believe that the nings rom the roun-table conerences an an subsequent research outputswill lea to a set o resh recommenations which canurther ai the evelopment o policies an propositions tostrengthen the nancial reporting o Islamic nancialinstitutions an to ultimatel to encourage the globalevelopment o this important wa o accessing nance.

IntroduCtIon And bACKGround

despite the recent global economic ownturn, Islamicnance has continue to grow at unpreceente levels,having now become an important part o the internationalnancial services lanscape. This evelopment, althoughle b traitional stronghols such as Malasia, Bahrainan Pakistan, is now increasingl being witnesse in aiverse range o countries aroun the worl. As Islamicnancial institutions are oune in these countries anconventional, multinational nancial institutions oerShari’a-compliant proucts, new challenges are ace bthe inustr. This is especiall the case as thoseinstitutions seek to operate, invest an access uningacross borers an in countries where the regulator annancial reporting rameworks are quite ierent.

Islamic nancial institutions, wherever the operate, o sowithin the same global nancial sstem as their

conventional counterparts an users o their nancialreports nee to make similar ecisions to those oconventional banks. Thus or competitive reasons or ratingpurposes, it is not surprising that some Islamic nancialinstitutions woul preer to report in the global accountinglanguage o choice, IFRS.

Nonetheless, Islamic nance b enition is istinct romconventional nance. Because o the nuances inherentwithin it, man countries require their Islamic banks toappl accounting stanars that take into account thoseierences, rather than simpl appling the more neutralIFRS suite o stanars.

The act that institutions can report an isclose similartransactions in ierent was poses problems or thoseinstitutions themselves as well as or the evelopment oIslamic nance in general.

exci mma

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 6/24

6

Key Issues For ConsIderAtIon

A review o leaing international Islamic nancialinstitutions shows that a number o reporting rameworksare use across the inustr. Although man use IFRS,some use partl converge IFRS-base stanars, someuse IFRS with aitional requirements or Islamic banks,an others use stanars exclusivel or Islamic banks.Questions over comparabilit an consistenc within theinustr an the broaer nancial services sector as wellas the impact such issues can have on uning aninvesting are airl obvious. Other consierations remainunaresse. This report sets out to highlight some othese questions. The wier project will aim to resolve someo these issues an, ultimatel, to inorm answers to theke question as to whether Islamic nancial institutionswoul benet rom reporting:

within the existing IFRS ramework•

within the IFRS ramework but with a specic stanar•

or Islamic nance

through a globall recognise suite o Islamic nancial•

stanars?

reACHInG An oPtIMAl solutIon

As Islamic finance moves beyond its natural boundaries and

increasingly becomes a mainstream form way accessing finance

around the world, greater standardised financial reporting will be

important for both Islamic finance and the institutions offering it

to reach their full potential.

Whether such reporting will be within the IFRS framework or

through a set of globally accepted accounting standards for the

Islamic finance industry depends on the needs of all stakeholders

in the industry. Careful debate and assessment of the different

alternatives is the only way to reach a satisfactory solution.

What is clear is that IFRS, as is already the case for a significant

number of financial institutions around the world, IFRS will play a

major role. Even if a set of international Islamic financial

accounting standards are used, they will have to be aligned with

IFRS as much as possible. Likewise, the IASB, as the issuers of

IFRS, will need to continue to engage with stakeholders in the

various Islamic finance markets to ensure that the standards arerelevant, considering the need for either supplementary guidance

or an industry specific standard.

Pi ciai

The ke consierations woul inclue generalconceptual issues, such as:

ientiing the users, an the objectives, o•

nancial reporting b Islamic nancial institutionsan whether the ier rom those o conventionalnancial institutions

the nee to use istinct Islamic accounting•

principles to provie a aithul representation othe nature o Islamic nance transactions.

whether non-nancial institutions that consume•

Islamic nance proucts have ierent accountingissues to Islamic nancial institutions?

More specic questions arise over the compatibilit oIFRS with Islamic nance practices such as:

the prohibition on partaking in interest-base•

transactions an whether this shoul aect theuse o iscount rates or measuring nancialinstruments

whether concepts such as ‘control’, ‘risks an•

rewars’ or ‘rights an obligations’, essential inetermining the accounting treatment uner IFRS,,are reail translatable to Islamic nance, wherethe sanctit o contractual orm is so important

the unique structures in Islamic nance that can•

coner rights an obligations on institutions, whichare quite istinct rom apparentl similarconventional proucts (eg prot-sharinginvestment accounts base on murabaha)

whether potential changes to IFRS, such as in the•

areas o lease accounting, nancial instruments,insurance accounting an consoliation ma havean impact on institutions appling IFRS, in theuture.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 7/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 7

IntroduCtIon

Islamic nance is increasingl entering the mainstream onancial services aroun the globe. The rate o growth isunpreceente, an espite the eects o the nancialcrisis, estimates suggest that the global size o the inustrha reache $951 billion at en o 2008 – 25% up rom$758 billion in 2007.3

A large proportion o the Shari’a-compliant assets thatmake up the $951 billion are hel b Islamic nancialinstitutions (IFIs) sprea across a number o ke centres.These are concentrate in South-East Asia an the MileEast, with Malasia an Bahrain, in particular, renowneor well-evelope sectors an increasingl robustregulation. In recent ears, the prole o Islamic nance inthe UK has also accelerate, largel acilitate b therea-mae proessional expertise in the Cit o Lonon,as well as positive regulator changes b the national

government

3. Islamic Fiac 2010, IFSL, 2010.

bACKGround

Although there is much ebate an literature on issuesrelating to Islamic nance, most o these relate to bankingan nance per se an in particular to legalistic mattersrelating to the legitimac o proucts an transactions.The research on accounting matters has hitherto beenrelativel limite.

While man o the national stanars, as well as those oAAOIFI, are closel aligne to IFRS, ierences still remain,an practice can, o course, var consierabl.

One o the major benets o using a common, globallaccepte set o accounting stanars is the comparabilitit oers or users o ierent institutions’ nancialstatements, thereore ultimatel enhancing the abilit oinstitutions to access uning an investmentopportunities across borers. diering accounting

practices can not onl restrict cross-borer operations butcan also cause iculties in the preparation o nancialstatements. For institutions oering Islamic nanceproucts an services, these ierences an icultiesare particularl acute, as applie stanars ma not coverthe concerne proucts or o not oer appropriateisclosure requirements.

Although rom a competitive an ratings perspective, IFIsma wish to report uner IFRS, the are sometimesrestricte because o local regulator requirements orconcerns rom users o their nancial reports aboutwhether these reports provie a air refection o theirIslamic nance activities.

In 2009, the recentl orme AOSSG, which incluesrepresentatives rom Malasia, China, Japan, South Korea,Singapore, New Zealan, Australia, Hong Kong, Macau,Brunei an Inonesia, emphasise the importance o theaccounting nees o IFIs in its representations to the IASB.As the AOSSG is currentl working on a project assessingthe application o IFRS to Islamic nance, we believe it istimel or the ebate to be extene to the ull range ostakeholers in the inustr an in markets where Islamicnance is well evelope but on ierent lines.

1. laig h a

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 8/24

8

objeCtIves

This report sets the scene or a broa project which willaim to inorm the international agena on nancialreporting b IFIs an support the work o accounting anauiting stanar setters in this area. B engaging withleaing stakeholers across a number o importantmarkets or Islamic nance, the project will aim to achievea range o general an specic objectives. Someconsierations relating to the specic practices o IFIs areraise in the bo o this report, although equallimportant conceptual areas will also be investigate, b:

ientiing the main users an user groups o IFI•

nancial reports an assessing whether theirinormation nees ier rom those o users oconventional nancial institutions

gauging perceptions b stakeholers o the nee or/•

benets o having specic nancial reporting stanarsor IFIs

gauging perceptions b stakeholers o the nee or/•

benets o having international nancial reportingstanars or IFIs, an whether these shoul be withinthe IFRS ramework or istinct rom it.

ACCA also believes that stakeholers will see merit inwiening the scope o the ebate to inclue concerns thatcoul generate urther research in the uture. These woulinclue a consieration o:

whether there are an specic assurance requirements•

o or emans b users o IFI nancial statements

the nee or/benets o stanarise international•

governance practices or IFIs, an whether Shari’agovernance practices are sharpl istinct romconventional governance practices in nancialinstitutions.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 9/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 9

Although Islamic nance has grown rapil aroun theworl since the turn o the centur, whether as a result oierent schools o thought or cultural ierences, ahomogeneous coe o Shari’a-compliant nance has et toemerge. While this has not iminishe their acceptancean uptake in markets throughout the worl, the varingegrees o fexibilit accore to Islamic nancetransactions an proucts have in instances le toconficting conclusions on Shari’a compliance.

Not surprisingl, the nancial reporting rameworks thatIslamic nancial institutions (IFIs) appl also var, otenepening on the jurisictional requirements impose onthem. Although this is not ue to ierences in Shari’ainterpretation, but rather ictate b the prevailing generalrequirements or companies within a countr, there is aclear lack o a single nancial reporting ramework,meaning that comparabilit across borers or similarentities becomes icult. With increasing emans b

investors in IFIs, as with other entities an inustries, wholook to global markets or optimal opportunities, this lacko consistenc coul be a major rawback.

Currentl, IFRS remains the onl globall recognise set onancial reporting stanars that oers IFIs a consistentramework, an one that also oers them comparabilitwith conventional banks. It is no surprise, thereore, thatman IFIs prepare their nancial reports base on IFRS. Inpractice, in most countries, there is little choice, becauseomestic regulators ictate the applicable stanars.

2. th acap facia pig Iamic facia iii

ta 2.1: Accig aa appica Iamic ak c

Country Accounting standard(s)

Bahrain AAOIFI an/or IFRS

Inonesia Inonesian GAAP (inc. specic stanars or IFIs)

Kuwait IFRS an AAOIFI

Malasia Malasian GAAP (inc . specic stanars or IFIs)

Pakistan IFRS, with some local amenments or all banks

Qatar AAOIFI

S Arabia IFRS (with aitional requirements or all banks)

UAE IFRS (inc specic requirements or IFIs)

UK IFRS or UK GAAP

Source: base on annual reports o leaing Islamic banks in each othese countries (see Appenix 1)

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 10/24

10

lACK oF stAndArdIsed ACCountInG

A review o the accounting stanars that are applicable toIslamic banks across signicant markets or Islamicnance is shown in Table 2.1. In most countries, theaccounting stanars use b IFIs are usuall inepenento their status as an IFI, with IFRS being the preominantset o stanars. Even so, it is not uncommon, even wherethe banks are require to use IFRS, or them also to haveto ahere to aitional local reporting requirements,specic to IFIs. O the countries reviewe, onl Bahrain anQatar require their IFIs to use specic stanars oaccounting or IFIs (AAOIFI stanars in both cases),although IFRS is note as being applicable where there issilence in the relevant suite o stanars.4 Others, such asPakistan, Inonesia an Malasia, which essentiall requireuse o IFRS or national GAAP base on IFRS, also requirethe application o specic Islamic nance stanars onaccounting, as issue locall.

Most multinational conventional banks that oer Islamicnance ‘winows’ will report accoring to their localrequirements. Owing to the jurisictions in which most othese are locate or reporting purposes, IFRS is the mostcommon orm o reporting. Even though their Islamicnance operations are oten substantial, there is littleevience that these nancial instruments an transactionsare reporte istinctl rom their conventional alternatives.

4. See Exhibit 2, Appenix 1 or such an example

The act that the banks reviewe are signicant global IFIshighlights the heterogeneit o nancial reporting, aneven where IFRS are use, the local reportingrequirements ma well impose rules that are notnecessar consistent with these stanars. This ultimatelmeans that inormation or investment ecisions b userso the IFI nancial reports can be severel restricte, incomparison with that available or both other IFIsinternationall, an conventional nancial institutionslocall (eg conventional banks in Bahrain are require touse IFRS).

The heterogeneit o nancialreporting b global IFIs ultimatelmeans that inormation or

investment ecisions b users othe IFI nancial reports can beseverel restricte, in comparisonwith that available or both otherIFIs internationall, anconventional nancial institutionslocall.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 11/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 11

Avocates o Islamic accounting point to the ierence inobjectives o nancial reporting rom a Shari’a perspectivecompare with that o ‘conventional’ accounting. While ewo those proponents woul argue with the basic premisethat accounting shoul provie inormation to enable itsusers to make inorme ecisions, the woul stress thatthe objectives o the inormation on IFIs is wier. A crucialobjective o nancial reporting rom an Islamic perspectiveis to be able to assess whether the entit is abiing b the‘principles o Shari’a an its concepts o airness, charitan compliance with business values’.5

While the theoretical aspects o Islamic accounting an theaitional socio-economic objectives are important,Islamic nance is a growing phenomenon in globalnancial markets, an IFIs are ace with the ver realilemma o reporting their perormance an positionagainst the same set o user objectives as theirconventional counterparts, while oten carring out

transactions that are quite istinct rom theirs. Thereore,rather than investigate the nee or Islamic accounting at atheoretical level, this report aims to explore the practicalissues o accounting or IF transactions an practices anwhether the can be aequatel covere b existinginternational stanars or whether specic internationallrecognise stanars or IFIs are require.

5. Statement o Financial Accounting (SFA) 1, Objctivs o Fiacial

Accoutig or Islamic Baks ad Fiacial Istitutios , AAOIFI, 2008.

AAOIFI, which has been proucing accounting, auiting,governance an Shari’a stanars specicall or theIslamic nance inustr since 1991, recognises the mansimilarities between the principles unerling conventionalinternational accounting an those that the believe to berelevant or IFIs. Hence, the accept IFRS, as issue b theIASB, as being appropriate in the absence o AAOIFIstanars. AAOIFI evelope its own nancial accountingstanars (FAS) essentiall or two reasons:

1. owing to the specics o Islamic banking an nance,IFRSs cannot be aopte en masse as the can eithercause Shari’a compliance issues or o not ull covercharacteristics o Islamic banking transactions, an

2. there were areas o IF not aequatel covere bprevailing international stanars; where nancialtransactions an practices were unique to IF, equivalentstanars or topics covere in IFRS ha to be evelope.

Some o the problems relating to these areas areiscusse below.

3. Iamic fac agai h ackp IFrs

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 12/24

12

CoMPAtIbIlIty oF IFrs wItH IslAMIC FInAnCe

th phiii i (riba)One o the cornerstones o Shari’a-compliant nance is theaversion to pament or receipt o interest. Interest in theconventional sense inclues an intrinsic assumption o thetime value o mone. This concept is central to IFRS, whichin aiming to allow users to evaluate the ‘abilit o the entitto generate cash an cash equivalents in the uture’6 otenrequire the use o iscounte uture cash fows to measureassets an liabilities.

examp appig ic a i IFrsUner IAS39,7 measuring nancial assets whereactive markets o not exist, requires the use ovaluation techniques that invariabl involve thecalculation o net present value o uture cash fows

iscounte at an appropriate rate o interest. Thus sukuk (or Islamic bons) hel or traing anavailable or sale, where an active market no longerexists woul have to be measure in this wa unerIFRS.

Also uner IAS39, assets classie as loans orreceivables are measure at their amortise costsusing an eective interest rate, in orer to take intoaccount the time value o mone. B contrast, anIstisna’a nance receivable woul be value athistorical cost uner FAS10 o AAOIFI.

Uner IAS36, an impairment exists when thecarring value o an asset excees its recoverableamount, which is the higher o its air value (lesscosts to sell) or its value in use. The value in usecalculation is again base on a iscounte cash fowmoel.

6. Framwork or th Prparatio ad Prstatio o Fiacial Statmts,

IASCF, 2010.

7. In November 2009, the IASB issue IFRS9: Fiacial Istrumts, the

initial part o an overall project to replace the existing IAS39: Fiacial

Istrumts: Rcogitio ad Masurmt . The methos o measuring air

values has not been change in the new stanar.

Pi ciai

1. While the prohibition o partaking in interestbase transactions is clearl unamental to

Islamic nance, it must be note that the use oiscounte cash fows is merel to erive anapproximation o a market value. It oes not resultin an interest charge. does this thereorenecessaril cause a confict with Shari’a?

2. Man Islamic nancial institutions explicitl reerto using iscounte cash fows when calculatingvalue in use or impairment testing an valuationtechniques or their nancial instrumentsmeasure at air value.8

3. Although the nancial accounting stanars (FAS)o AAOIFI essentiall reer to air value as the

‘value agree between the partners’ in atransaction, there is little reerence to themeasurement o this air value in the absence oactive markets – an whether the air value coulbe erive b reerence to net present value outure cash fows. Article 8/8 o AAOIFI Shari’astanar 13 on Muaraba is, however, moreexplicit:

‘I masurig rcivabls, ithr tim valu

(itrst rat) or discout o currt valu or xtsio o priod o pamt shall b tak itocosidratio’.

8. An example is Unicorn Investment Bank B.S.C. in their 2009

nancial statements, which compl with AAOIFI an IFRS (see

Appenix 1, Exhibit 4).

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 13/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 13

sac mThe confict between accounting base on economicsubstance as oppose to Shari’a-compliant orm appearsto be a recurring theme. IFRS is reliant on a strongramework o principles that emphasise the economicnature o transactions, whereas in Islamic nance thecontractual aspect o the transaction is crucial or Shari’acompliance. Unerpinning those contracts are Shari’aprinciples that give rise to proucts (eg mudaraba,musharaka, salam an istisa) that are unique to theinustr an that have ierent rights an obligationsassociate with them.

examp: Ijara a pai a aachOne o the most common structures use in Islamicnance is the Ijara – a orm o leasing arrangement.

The pure Ijara is essentiall an operating lease anthere woul appear to be little confict in accountingor this (either or the lessor or the lessee) uner therequirements o IAS17.

Increasingl use orms o leasing b IFIs are theijara mutahia bittamlk (ijara MB) or ijara wa iqtia,which are similar to a hire purchase agreementpopular in conventional nance. This is essentiall aorm o nancing which, uner IFRS, is treate as anance lease because, as with a hire purchaseagreement, the risks an rewars associate withowning the asset are in substance transerre to thelessee. Thus uner IAS17 the asset woul bebooke as such b the lessee, while the lessor (thenancer) woul book a receivable or the rent anrelate interest receivable.

B contrast, uner both IFAS2, Ijarah (as issue bthe Institute o Chartere Accountants o Pakistan)an AAOIFI’s FAS8, the legal orm o the contract isparamount, meaning that the ownership o the assetremains with the lessor, until legal title is transerreat the en o the lease perio. In this case the IFIwoul remain the owner, an recor the asset on itsbalance sheet in the same wa as an operatinglease or operating Ijara.

In the example above, the salient eature appears to be theact that both Ijarah an Ijarah MB are purel leasingtransactions in which the subject matter is the usuruct othe asset an not the nancing o the asset, as is the caseor a nance lease. In aition to the act that the legal titleremains with the lessor, or the accounting to be consistentwith the Shari’a principle, the lessor woul necessarilhave to account or the lease asset.

The IASB is likel to conclue its long-term project onlease accounting in 2011 with the issue o a reviseaccounting stanar. I this is consistent with theproposals in the exposure rat iscussion paper entitleLass9 (August 2010) there is likel to be a signicantimpact or man companies. In the iscussion paper theIASB conclues that uner an lease contract, ‘the lessee’sright to use a lease item or the lease term meets theenitions o an asset’ an woul thereore be shown assuch on the lessee’s balance sheet. This woul appear to

broaen the incompatibilit between the accountingrequirements o IFRS an the Shari’a-compliant legal ormo Islamic nance leases.

‘A icrasig proportio o acaroud th world is big providdudr Islamic pricipls ad b Islamic acial istitutios. Udr ths pricipls th majorit o

lass would ot b rcogisd asassts b th lsss. Th proposals ith DP would mov IFRS accoutig urthr awa rom that positio adop up th dircs btw thtwo sstms v urthr. This smsa uhlpul dvlopmt.’

ACCA COMMENT LETTER ABOUT THE IASB dISCUSSION PAPER‘LeASeS: PReLIMInARy VIeWS’, JULy 2009.10

9. http://www.irs.org/Current+Projects/IASB+Projects/Leases/e10/E.htm

10. http://www.iasb.org/NR/ronlres/22dF3CF1-B22E-4475-8C39-

ECAAAFB60B01/11168/20090717150749_leasesR0709.oc

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 14/24

14

Pi ciai

1. While the accounting uner current IFRS appearsto iverge rom that o Islamic accounting

stanars use in other countries, IFRS o not inan wa aect the Shari’a compliance o thetransaction itsel. does this rener the nancialinormation isclose less meaningul or users oIFI nancial reports?

2. Is the concept o incompatibilit between IFRS anShari’a principles so ierent rom theincompatibilities that exist between IFRS anjurisictional legal coes? The latter has notstunte the acceptance an applicabilit o IFRS,although some countries have chosen to aaptIFRS to suit thir jurisdictioal ds. Is adaptatio

o IFRS or IFIs possibl?

3. Woul the accounting or certain Islamic nancecontracts using the principles o IFRS prouce anaccounting treatment that woul generateinormation that was either not useul or non-compliant rom a Shari’a perspective?

4. Coul aitional isclosure aroun the accountingtreatment aress those concerns?

IslAMIC FInAnCe not Covered In IFrs

Caifcai a pai facia imMost Islamic nancial institutions operate a mudaraba-base investment structure, which is a popular orm oeposit mechanism or customers. The specic eatures othese accounts create a istinct ierence between theman conventional eposit accounts, which in turn aectshow the might be reporte uner IFRS.

‘I ordr to apprciat th cssit or distictiv itratioalaccoutig stadards or Islamicac, it is importat to bar i

mid th spcic charactristics o Islamic acial istitutios (IFIs). Thopratios o IFIs ar cocptuall ad markdl dirt rom thos o covtioal acial istitutios.’

dR MOHAMAd NEdAL ALCHAAR, SECRETARy GENERAL, AAOIFI

The nature o unrestricte investment accounts (URIA)means that the are treate as a quasi orm o equituner some Islamic accounting stanars (eg AAOIFI’sFAS6, equit o ivstmt accout holdrs ad thir

quivalt ). The act that an losses in the investment areborne b the investor suggests the are in principle a tpeo resiual claimant or equit investor. Nonetheless, thelosses coul all on the IFI were it prove to be negligent,an increasingl most IFIs provie a ‘trespass or omission’guarantee to customers. This, couple with thecommercial necessit ace b internationall competingIFIs o absorbing losses rom URIA themselves, in orer toensure a smoothe return to customers, woul point to aorm o liabilit not issimilar to conventional eposits.

In practice, Islamic banks in most countries present URIAas liabilities on their balance sheets, whether the use IFRS

or local GAAP (Malasia), again refecting the substance othe arrangements. Onl IFIs reporting uner AAOIFIstanars, such as Qatar Islamic Bank (SAQ) an AlBaraka Banking Group (BSC), reporte them at themezzanine level between liabilit an equit. .

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 15/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 15

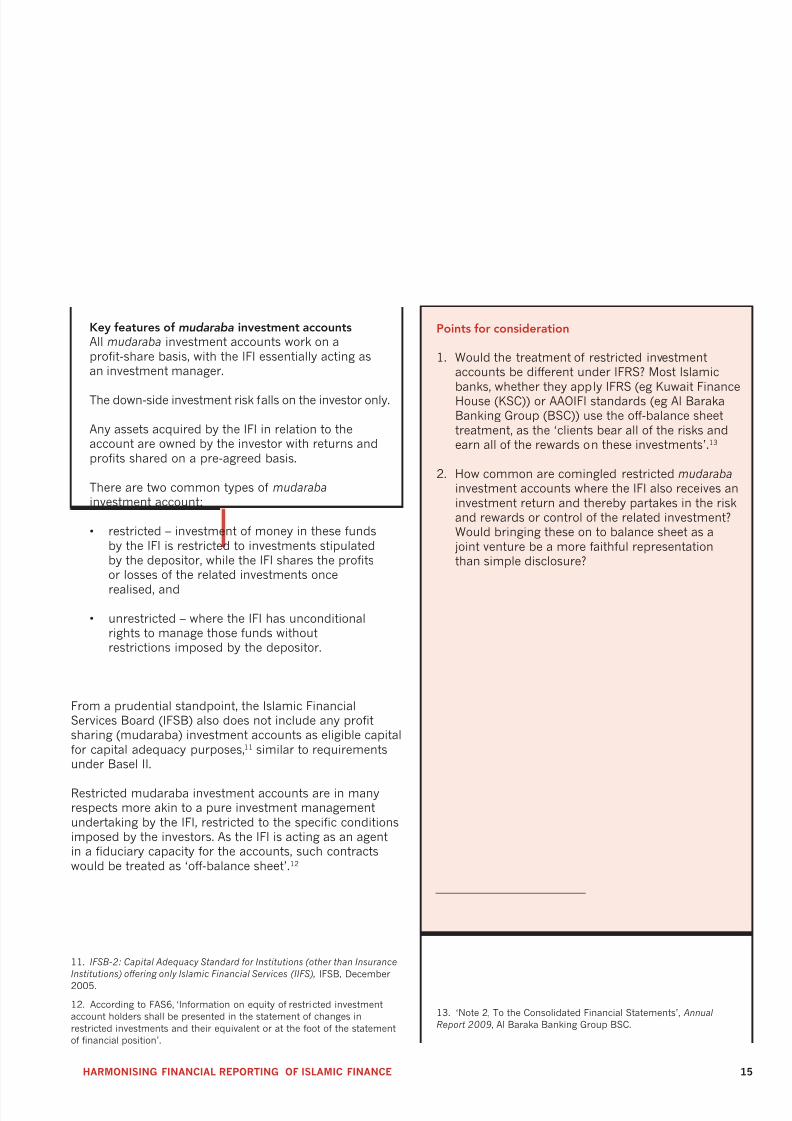

K a mudaraba im accAll mudaraba investment accounts work on aprot-share basis, with the IFI essentiall acting asan investment manager.

The own-sie investment risk alls on the investor onl.

An assets acquire b the IFI in relation to theaccount are owne b the investor with returns anprots share on a pre-agree basis.

There are two common tpes o mudaraba investment account:

restricte – investment o mone in these uns•

b the IFI is restricte to investments stipulateb the epositor, while the IFI shares the protsor losses o the relate investments once

realise, an

unrestricte – where the IFI has unconitional•

rights to manage those uns withoutrestrictions impose b the epositor.

From a pruential stanpoint, the Islamic FinancialServices Boar (IFSB) also oes not inclue an protsharing (muaraba) investment accounts as eligible capitalor capital aequac purposes,11 similar to requirementsuner Basel II.

Restricte muaraba investment accounts are in manrespects more akin to a pure investment managementunertaking b the IFI, restricte to the specic conitionsimpose b the investors. As the IFI is acting as an agentin a uciar capacit or the accounts, such contractswoul be treate as ‘o-balance sheet’.12

11. IFSB-2: Capital Adquac Stadard or Istitutios (othr tha Isurac

Istitutios) orig ol Islamic Fiacial Srvics (IIFS), IFSB, december

2005.

12. Accoring to FAS6, ‘Inormation on equit o restricte investment

account holers shall be presente in the statement o changes in

restricte investments an their equivalent or at the oot o the statement

o nancial position’.

Pi ciai

1. Woul the treatment o restricte investmentaccounts be ierent uner IFRS? Most Islamic

banks, whether the appl IFRS (eg Kuwait FinanceHouse (KSC)) or AAOIFI stanars (eg Al BarakaBanking Group (BSC)) use the o-balance sheettreatment, as the ‘clients bear all o the risks anearn all o the rewars on these investments’.13

2. How common are comingle restricte mudaraba investment accounts where the IFI also receives aninvestment return an thereb partakes in the riskan rewars or control o the relate investment?Woul bringing these on to balance sheet as ajoint venture be a more aithul representationthan simple isclosure?

13. ‘Note 2, To the Consoliate Financial Statements’, Aual

Rport 2009, Al Baraka Banking Group BSC.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 16/24

16

Pii a Uner strict Shari’a rules i there is a loss rom a mudaraba investment, it is onl the epositing customer who bearsthe ull loss. In practice, in such circumstances or whenthe overall prot levels are low, as was the case uring therecent nancial crisis, IFIs have orgone their own share oprots in avour o their customers.

The IFSB escribes this provision o competitive returns as‘isplace commercial risk’. Principall applie to URIA, anIFI achieves this risk-sharing b using reserves set asierom mudaraba prots.

The accounting or these reserves uner IFRS woulepen on whether the IFI is eeme to have an obligation(either contractual or constructive) to pa epositors romthe reserve. A urther issue is that in the case o PER inparticular, the IFI’s share o the prots is inclue, therebeectivel creating an expecte loss provision, currentl

not permitte uner IAS39.

There is inconsistenc in how IFIs aroun the worlaccount or the PER, as shown in Table 3.1 below.

ta 3.1: th pig pf aiai (Per) Iamic ak i i mak

Islamic bank Country

Accounting

regime Classifcation o PER

Bank Islam Malasia

Berha (2009) Malasia

Malasian

GAAP Liabilit

Al Baraka Banking

Group BSC (2009) Bahrain AAOIFI

Nette o against

URIA (separate rom

equit an liabilit)

Islamic Bank o Britain

PLC (2008) UK IFRS Equit

dubai Islamic Bank

PJSC (2009) UAE IFRS Liabilit

Pf-haig Prot-sharing reserves are usuall o two tpes.

In prot equalisation reserves (PER), the•

reserves are set asie rom prots beoreappling the prot-sharing istribution. Tpicall,in such arrangements the IFI gives up a part, orits entire share, o prots, in orer to matchcurrent market returns.

In investment risk reserve (IRR), the reserves are•

set asie rom the part o the prots allocate toinvestors, which can onl be use to absorblosses uring a nancial perio.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 17/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 17

Islamic nancial institutions an conventional banksoering Islamic nance proucts aroun the worl havebeen highl resourceul an innovative in their oerings.This has certainl plae a part in the rapi growth o theinustr in a relativel short p erio. That pragmatism hasalso been extene to the wa those institutions accountor an report their Islamic nance transactions.

A nuMber oF ACCountInG reGIMes Currently used

A signicant number o IFIs report uner IFRS or IFRS-equivalent stanars. Others appl national stanars (egIFIs in Malasia an Inonesia) that are to varing egreesaligne with IFRS. While the onl set o specic Islamicaccounting stanars are those issue b AAOIFI (use inBahrain an Qatar, or example), other countries haveissue aitional stanars or guiance or IFIs tosupplement the existing accounting ramework. Forexample, in:

Pakistan – aitional stanars issue b ICAP•

Inonesia – aitional stanars base on AAOIFI•

Malasia – one aitional stanar (presentation onl)•

an guiance rom central bank (Bank Negara).

In those countries where AAOIFI

stanars are not applie an thatare increasingl approaching theIFRS moel, there is little eviencethat the existing reporting regimescause compliance issues or IFIs. Itwoul appear that the substanceover orm principles central to IFRSaequatel accommoate Islamicnance rom an assurance an

regulator perspective.

Nonetheless, questions remain as to whether the increaseapplication o IFRS b IFIs:

actuall leas to consistenc, both between IFIs•

themselves an with conventional institutions

provies a aithul representation o the transactions•

being conucte

can lea to conficting accounting treatments with•

requirements rom national regulators

leas to ecision-useul inormation or the main users•

o their reports.

CoMMon ACCountInG essentIAl For ACCess toGlobAl MArKets

There is little question that IFRS is the onl language or

nancial reporting that has true global recognition anclearl oers cross-borer comparabilit or users o IFInancial reports. This is o vital importance or largemultinational IFIs as well as conventional banks oeringShari’a winows that are seeking to access uning anbreak into new markets. Regional stanars, anespeciall those geare specicall towars IFIs, cannotet oer these benets.

unIque FeAtures oF IslAMIC FInAnCe need to beConsIdered

Specic nancial reporting stanars can oer a moretailore moel or IFI reporting. B taking into account thenature o their transactions the woul potentiall be ableto provie more ecision-useul inormation. For example,man IFIs reporting uner IFRS report URIAs simpl asliabilities an there is little inormation to enable users othe accounts to istinguish URIAs rom conventionalcustomer eposits.

4. sm ccig hgh

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 18/24

18

PossIble APProACHes

IFrs aIFRS coul be use as the eault reporting ramework,although guiance base on existing Islamic nancialreporting moels woul nee to be use to supplementthe stanars or those IF transactions that o not tsimpl into the ramework. This guiance woul bepresentation an isclosure relate, allowing or aitionaltransparenc or such things as unerling assets anterminolog require b users. It is also worth noting thateven within the existing IFRS suite o stanars, there arestanars ealing with specic inustries,14 an thereorea specic stanar aime at Islamic nance transactionscoul be another possibilit.

‘W l that w ca us thItratioal Fiacial Rportig Stadards (IFRS) ulss somoca show us that thr is a clar prohibitio i th Shari’a, th wwill amd it accordigl. Util sucha tim, w’ll us th IFRS.’

MOHAMMAd FAIZ AZMI, CHAIRMAN, MALAySIAN ACCOUNTINGSTANdARdS BOARd (MASB)

14. IFRS4, Isurac cotracts an IFRS6, exploratio or ad valuatio o

miral rsourcs, are examples o inustr-specic stanars within IFRS.

Iamic accig aa aAlternativel, a set o globall recognise Islamicaccounting stanars coul be use b IFIs. Wherepossible these woul be base on IFRS, but woul incluespecic recognition, measurement, presentation anisclosure requirements relevant to Islamic nanceproucts an transactions. In orer to assist IFIs anultimatel, the users o their nancial reports, areconciliation to IFRS coul be also be provie.

As Islamic nance moves beon its traitional geographicbounaries an increasingl becomes a mainstream ormo accessing nance aroun the worl, greaterstanarise reporting will be important to all Islamicnance an the institutions oering it to reach their ullpotential.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 19/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 19

exhii 1: exac, 2009 aa p AbC Iamic bak(e.C.), bahaiBasis o prparatio

Th cosolidatd acial statmts hav b prpard iaccordac with th Fiacial Accoutig Stadards issud b th Accoutig ad Auditig Orgaisatio or Islamic

Fiacial Istitutios (AAOIFI) ad th applicabl provisioso th Bahrai Commrcial Compais Law ad th Ctral

Bak o Bahrai ad Fiacial Istitutios Law. For mattrswhich ar ot covrd b AAOIFI stadards, th Group ussth Itratioal Fiacial Rportig Stadards (IFRS).

exhii 2: exac, 2009 aa p A baaka bakigGp b.s.C., bahaiStatmt o CompliacTh cosolidatd acial statmts ar prpard iaccordac with th Fiacial Accoutig Stadards issud

b th Accoutig ad Auditig Orgaisatio or IslamicFiacial Istitutios (AAOIFI), th Shari’a Ruls ad

Pricipls as dtrmid b th Shari’a Suprvisor Board o th Group, th Bahrai Commrcial Compais Law, thCtral Bak o Bahrai ad Fiacial Istitutios Law. Iaccordac with th rquirmts o AAOIFI, or mattrs or

which o AAOIFI stadard xists, th Group uss th rlvat Itratioal Fiacial Rportig Stadards (th IFRSs).

exhii 3: exac, 2009 aa p Ihmaa bakb.s.C., bahai15

Basis o prparatio

Th cosolidatd acial statmts o th Group arprpard i accordac with ad compl with ItratioalFiacial Rportig Stadards (IFRS) as issud b th

Itratioal Accoutig Stadards Board (IASB). Thcosolidatd acial statmt compris th cosolidatd

statmt o acial positio, cosolidatd icom

statmt, cosolidatd statmt o comprhsivicom, cosolidatd statmt o chags i quit,cosolidatd statmt o cash fows ad th ots. Th

cosolidatd acial statmts ar prpard udr thhistorical cost covtio as modid b th rvaluatio o availabl-or-sal acial assts, tradig scuritis,

drivativ istrumts ad ivstmt proprt.

15. In April 2010, ollowing an approve restructure b the nancial

regulator, Central Bank o Bahrain (CBB), Ithmaar Bank aopte AAOIFI

stanars with immeiate eect.

exhii 4: exac, 2009 aa p uicIm bak b.s.C., bahaiStatmt o compliac

Th cosolidatd acial statmts o th Group havb prpard i accordac with th Fiacial Accoutig Stadards (FAS) issud b th Accoutig ad Auditig

Orgaisatio or Islamic Fiacial Istitutios (AAOIFI) adItratioal Fiacial Rportig Stadards (IFRS), ad ar i

coormit with th Bahrai Commrcial Compais Law adth Ctral Bak o Bahrai ad Fiacial Istitutios Law.

exhii 5: exac, 2008 aa p A rahi akiga im cpai, sai Aaiaa) Basis o prstatio

Th cosolidatd acial statmts ar prpard iaccordac with th Accoutig Stadards or FiacialIstitutios promulgatd b th Saudi Arabia Motar

Agc (SAMA) ad Itratioal Fiacial Rportig Stadards (IFRS). Th Bak also prpars its cosolidatd

acial statmts to compl with th Bakig Cotrol Law ad th Rgulatios o Compais i th Kigdom o Saudi

Arabia.

exhii 6: exac, 2009 aa p bak IamMaaia bha, Maaia(a) Statmt o compliac

Th acial statmts o th Group ad o th Bak havb prpard i accordac with th applicabl FiacialRportig Stadards (FRS) issud b th Malasia

Accoutig Stadards Board (MASB) as modid b Bak ngara Malasia Guidlis, th provisios o th Compais

Act, 1965 ad Shariah rquirmts.

exhii 7: exac, 2008 aa p Iamic bak biai PlC, uK (a) Statmt o compliacThs acial statmts hav b prpard iaccordac with Itratioal Fiacial Rportig Stadards

(IFRSs) as adoptd b th eU ad approvd b th dirctors.

Appix 1: bai ppaai facia am Iamic

fac iii, c

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 20/24

20

exhii 8: exac, 2009 aa p Kai FiacH K.s.C., KaiBasis o prparatio

Th cosolidatd acial statmts hav b prpard iaccordac with th rgulatios o th Govrmt o Kuwait or acial srvics istitutios rgulatd b th Ctral

Bak o Kuwait. Ths rgulatios rquir adoptio o allItratioal Fiacial Rportig Stadards (IFRS) xcpt or

th IAS 39 rquirmt or collctiv provisio, which hasb rplacd b th Ctral Bak o Kuwait’s rquirmt or a miimum gral provisio as dscribd udr th

accoutig polic or impairmt o acial assts.

exhii 9: exac, 2009 aa p Ma baklimi, PakiaStatmt o compliac

4.1 Ths acial statmts hav b prpard iaccordac with th approvd accoutig stadards as

applicabl i Pakista. Approvd accoutig stadardscompris o such Itratioal Fiacial Rportig Stadardsissud b th Itratioal Accoutig Stadards Board adIslamic Fiacial Accoutig Stadards issud b th

Istitut o Chartrd Accoutats o Pakista, as ar otidudr th Compais Ordiac, 1984, provisios o addirctivs issud udr th Compais Ordiac, 1984, ad

th Bakig Compais Ordiac, 1962, ad th dirctivsissud b th Stat Bak o Pakista (SBP). I cas thrquirmts o provisios ad dirctivs issud udr th

Compais Ordiac, 1984, ad th Bakig CompaisOrdiac, 1962, ad th dirctivs issud b SBP dir, thprovisios o ad th dirctivs issud udr th Compais

Ordiac, 1984, ad th Bakig Compais Ordiac,1962, ad th dirctivs issud b SBP shall prvail.4.2 SBP through its BSD Circular no. 10 datd August 26,

2002, has drrd th implmtatio o Itratioal Accoutig Stadard (IAS) 39 – ‘Fiacial Istrumts:Rcogitio ad Masurmt’ ad IAS 40 – ‘Ivstmt

Proprt’ or baks i Pakista. Accordigl, thrquirmts o thos IASs hav ot b cosidrd iprparatio o ths acial statmts.

exhii 10: exac, 2009 aa p qaa Iamicbak (s.A.q), qaaBasis o prparatio

Th cosolidatd acial statmts o th Bak ad its subsidiaris (togthr ‘th Group’) ar prpard udr thhistorical cost covtio as modid or masurmt at

air valu o acial ivstmts, i accordac withFiacial Accoutig Stadards (FAS) issud b th

Accoutig ad Auditig Orgaisatio or Islamic FiacialIstitutios (AAOIFI), Itratioal Fiacial Rportig Stadards (IFRS); whr AAOFI guidac is ot availabl,

rlatd rgulatios o Qatar Ctral Bak ad applicablprovisios o th Qatar Commrcial Compa’s Law.

exhii 11: exac, 2009 aa p dai Iamicbak PjsC, uAeStatmt o compliac

Th cosolidatd acial statmts hav b prpard iaccordac with Itratioal Fiacial Rportig Stadards

(IFRS) issud b th Itratioal Accoutig StadardsBoard (IASB), itrprtatios issud b th ItratioalFiacial Rportig Itrprtatios Committ (IFRIC) adapplicabl rquirmts o th Laws o th UAe.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 21/24

HARMONISING FINANCIAL REPORTING OF ISLAMIC FINANCE 21

AAOIFI Accounting an Auiting Organisation or Islamic Financial Institutions

AOSSG Asian-Oceanic Stanars Setters group

FAS Financial Accounting Stanars (issue b AAOIFI)

GAAP Generall Accepte Accounting Principles

IASB International Accounting Stanars Boar

IASCF16 International Accounting Stanars Committee Founation

ICAP Institutions o Chartere Accounts o Pakistan

IFAS Islamic Financial Accounting Stanar (issue b ICAP)

IFI Islamic nancial institutions

IFRIC International Financial Reporting Interpretation Committee

IFRS International Financial Reporting Stanars (issue b IASB)

IFSB Islamic Financial Services Boar

IRR Investment risk reserve

MASB Malasian Accounting Stanars Boar

PER Prot equalisation reserve

SFA Statement o Financial Accounting (issue b AAOIFI)

URIA Unrestricte investment account

16. With eect rom 1 Jul 2010, the IASCF was rename the IFRS Founation.

Appix 2: Aiai a acm i hi p

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 22/24

22

Ijara a lease contract

Ijara mutahia bittamlk a lease contract where the lessee has the option to acquire ownership o the asset at an time

Ijara wa iqtia a lease contract where the lessee has the option to acquire ownership o the asset at en olease perio

Istisa’a contract to manuacture, where the eliver is eerre – the sale price ma be paable atspot or eerre

Mudaraba partnership agreement where one partner (Rab al maal) provies the capital an the other(Mudarib) provies the work/management

Murabaha sale o goos at an agree mark-up

Musharaka partnership arrangement

Riba literall excess, reerring to unair gain: usuall snonmous with interest

Salam a contract where avance pament is mae or ene goos to be elivere later at a xeate

Shari’a (or Shariah) the rules an unerling principles o Islamic law

Appix 3: Aaic m i hi p

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 23/24

sAMer HIjAzI

Samer is a irector in KPMG’s FinancialServices Auit practice. Samer iscurrentl irector on the StanarChartere auit team responsible orthe auit o the Wholesale Bank anIslamic nance. He also works with anumber o Islamic retail aninvestment banking entities in the UK

where he has provie accounting anavisor services or the past six ears.Samer has also provie accounting an qualit assuranceavice on Islamic nancial proucts an operations toseveral leaing conventional global nancial institutionswith Islamic winows in Lonon.

AzIz tAyyebI

Aziz is the nancial reporting ocerat ACCA an is a leaing contributorto ACCA’s commentar an policpositions on global an nationalevelopments in nancial reporting.As secretar to ACCA’s FinancialReporting Committee, Aziz preparesposition papers on ke evelopments

in nancial reporting, as well aseveloping ACCA’s ormal responsesto relevant consultative ocuments. He also heas ACCA’sthought leaership in the el o Islamic nance,contributing articles an iscussion papers on thesubject.

Iiai cmm

This report raises a number o important questions about the uture irection o nancial reporting o Islamic nance.The roun-table iscussions with ke stakeholers, ue to be hel in Bahrain, Kuala Lumpur an Lonon, will seek toevelop answers to man o these questions.

ACCA an KPMG are keen to hear rom all stakeholers intereste in this subject. I ou woul like to comment on an othe issues raise in this paper please contact either Aziz Taebi or Samer Hijazi who are leaing this project or ACCAan KPMG respectivel.

8/8/2019 Financial Reporting Tech Af Hfrif

http://slidepdf.com/reader/full/financial-reporting-tech-af-hfrif 24/24

TECH-AF-HFRIF

Related Documents