A STUDY ON FINANCIAL PERFORMANCE ANALYSIS OF PONNI SUGAR (ERODE) LIMITED Submitted by S.PRAVEENKUMAR (REG .NO.211414631142) Of PANIMALAR ENGINEERING COLLEGE PROJECT REPORT Submitted to the FACULTY OF MANAGEMENT STUDIES In partial fulfilment of the requirements For the award of the degree 1

Financial performance analysis in ponni sugar (erode) limited

Feb 22, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A STUDY ON FINANCIAL PERFORMANCE

ANALYSIS OF PONNI SUGAR (ERODE) LIMITED

Submitted by

S.PRAVEENKUMAR

(REG .NO.211414631142)

Of

PANIMALAR ENGINEERING COLLEGE

PROJECT REPORT

Submitted to the

FACULTY OF MANAGEMENT STUDIES

In partial fulfilment of the requirementsFor the award of the degree

Of

MASTER OF BUSINESS ADMINISTRATION

OCTOBER-2015

PANIMALAR ENGINEERING COLLEGE(A CHRISTIAN MINORITY INSTITUTION)

1

JAISAKTHI EDUCATIONAL TRUSTBANGALORE TRUNK RECORD

VARADARAJAPURAM, NASARATHPETTAIPOONAMALLEE, CHENNAI – 602 102

DEPARTMENT OF MANAGEMENT STUDIES

CERTIFICATE

This is to certify that this project report titled, “A STUDY ON FINANCE PERFORMANCE ANALYSIS OF PONNI SUGAR (ERODE) LTD, AT SUGAR FACTORY” is the bonafide work of S.PRAVEENKUMAR who carried out the research under my supervision. Certified further, that to the best of my knowledge the work reported herein does not form part of any other project report or dissertation on the basis of which a degree or award was conferred on earlier occasion on this or any other candidate.

Internal Guide Head of the Department

ACKNOWLEDGEMENT

2

I would like to express my sincere gratitude to Our Chairman Dr. JEPPIAR

M.A.,B.L.,Ph.D., for providing excellent environment and infrastructure and for his valuable

support throughout the course of study.

I express my deep sense of gratitude and thanks to Our Secretary and

Correspondent Dr.P.CHINNADURAI M.A.,PH.D., and I express my sincere thanks to

Our Directors Mrs. C. VIJAYA RAJESHWARI, Mr. C.SAKTHIKUMAR, M.E.,

M.Phil. I also express my gratitude to my Principal Dr. K.MANI M.E.,Ph.D. for providing

all the required facilities for the successful completion of this work.

I take this opportunity to express my gratitude to the Dean & Head of the

Department of Management studies, Dr. V.MAHALAKSHMI M.L., M.B.A., Ph.D., for

providing me an opportunity and MR.I.YABESH ABRAHAM DURAIRAJ MBA., who

has given me guidance to do this work.

I express my deep sense of gratitude to Dr.V.MAHALAKSHMI M.L., M.B.A.,

Ph.D for giving me the opportunity to undertake my project in his esteemed concern and

guiding me throughout the entire work period.

I would like to thank other faculty members of M.B.A. Department for their

valuable guidance. Last but not least, I thank the almighty and my parents for their blessings

in successful completion of the project

(S.PRAVEENKUMR)

TABLE OF CONTENT

3

S.NO PARTICULARS PAGE NO

LIST OF TABLES

LIST OF CHART

ABSTRACT

V

VII

IX

1

1.1

1.2

1.3

1.4

CHAPTER-1 INTRODUCTION

INTRODUCTION

STATEMENT OF PROBLEM

COMPANY PROFILE

PRODUCT PROFILE

1

2

3

3

6

2

2.1

2.2

2.3

2.4

2.5

CHAPTER-2 DEVELOPMENT OF MAIN THEME

NEED OF THE STUDY

OBJECTIVE OF THE STUDY

SCOPE OF THE STUDY

LIMITATIONS OF THE STUDY

REVIEW OF LITRATURE

7

8

9

10

11

12

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

CHAPTER-3 ANALYSIS AND INTERPRETATION

RESEARCH METHODOLOGY

RESEARCH DESIGN

SOURCE OF DATA

TOOLS OF FINANCIAL PERFORMANCE ANALYSIS

PERIOD OF STUDY

ANALYSIS AND INTERPRETATION

FINDING AND SUGGESTIONS

CONCLUSION

16

17

17

18

19

19

20

71

76

APPENDIX

BALANCE SHEET (2011-2015)

THE STATEMENT OF PROFIT AND LOSS

BIBLOGRAPHY

78

79

81

83

LIST OF TABLES

TABLE

NO PARTICULARS PAGE .NO

4

3.6.1 Current ratio 28

3.6.2 Quick asset ratio 30

3.6.3 Cash position ratio 32

3.6.4 Inventory turnover ratio 34

3.6.5 Fixed asset turnover ratio 36

3.6.6 Working capital turnover ratio 38

3.6.7 Fixed asset ratio 40

3.6.8 Proprietary ratio 42

3.6.9 Return on total asset 44

3.6.10 Net profit ratio 46

3.6.11 Gross profit ratio 48

3.6.12 The comparative balance sheet 2010-11 50

3.6.13 The common size balance sheet 2010-11 52

3.6.14 The comparative balance sheet 2011-12 54

3.6.15 The common size balance sheet 2011-12 57

3.6.16 The comparative balance sheet 2012-13 59

3.6.17 The common size balance sheet 2012-13 61

3.6.18 The comparative balance sheet 2013-14 63

3.6.19 The common size balance sheet 2013-14 65

3.6.20 The comparative balance sheet 2014-15 67

3.6.21 The common size balance sheet 2014-15 69

LIST OF CHART

TABLE

NO

PARTICULARS PAGE NO

3.6.1 The Chart of current ratio 29

3.6.2 The Chart of quick asset ratio 31

5

3.6.3 The Chart of cash position ratio 33

3.6.4 The Chart of inventory turnover ratio 35

3.6.5 The Chart of fixed asset turnover ratio 37

3.6.6 The Chart of working capital turnover ratio 39

3.6.7 The Chart of fixed asset ratio 41

3.6.8 The Chart of proprietary ratio 43

3.6.9 The Chart of return on total asset 45

3.6.10 the chart of net profit ratio 47

3.6.11 The chart of gross profit ratio 49

ABSTRACT

6

In this project, titled “A STUDY ON FINANCIAL PERFORMANCE OF PONNI

SUGAR (ERODE) LTD”. This aim is to analysis the liquidity and profitability position of

the company using the financial tools.

This study based on financial statements such as Ratio Analysis, Comparative

balance sheet and common size balance sheet. By using this tools combined it enables to

determine in an effective manner.

The study is made to evaluate the financial position, the operational results as well as

financial progress of a business concern.

This study explains ways in which ratio analysis can be of assistance in long-range

planning, budgeting and asset management to strengthen financial performance and help

avoid financial difficulties.

The study not only throws on the financial position of a firm but also serves as a

stepping stone to remedial measures for ponni sugar (erode) limited.

This project helps to identify and give suggestion the area of weaker position of

business transaction in “PONNI SUGAR (ERODE) LIMITED”.

7

CHAPTER -1

INTRODUCTION

1.1INTRODUCTION

The word ‘Performance is derived from the word ‘par fourmen’, which means

8

‘to do’, ‘to carry out’ or ‘to render’. It refers the act of per forming; execution,

accomplishment, fulfillment, etc. In border sense, performance refers to the

accomplishment of a given task measured against preset standards of accuracy,

completeness, cost, and speed. In other words, it refers to the degree to which

an achievement is being or has been accomplished. In the words ofFrich Kohlar

“The performance is a general term applied to a part or to all the conducts of

activities of an organization over a period of time often with reference to past or

projected cost efficiency, management responsibility or accountability or the

like. Thus, not just the presentation, but the quality of results achieved refers to

the performance. Performance is used to indicate firm’s success, conditions,

and compliance.

Financial performance refers to the act of performing financial activity. In

broader sense, financial performance refers to the degree to which financial

objectives being or has been accomplished. It is the process of measuring the

results of a firm's policies and operations in monetary terms. It is used to

measure firm's overall financial health over a given period of time and can also

be used to compare similar firms across the same industry or to compare

industries or sectors in aggregation.

The financial performance analysis identifies the financial strengths and

weaknesses of the firm by properly establishing relationships between the items

of the balance sheet and profit and loss account.

1.1 STATEMENT OF THE PROBLEM

9

Financial performance are prepared to review the state of investment in a

business and result achieved during specific period, financial performance

analyses are also of great importance to the financial lenders. The financial

performances are useful and meaningful only when they are analyzed.

Sugar industries are of the developing industries in our country after

liberalization. The government has opened new opportunities for the century old

sugar industry. There is a vast home market and export potential for sugar

industry. The process of consolidation and rationalization in the industry will

continue. This will lead to greater challenges in matching the right companies

and their product making facilities to the right market. On account of these

facts, it is of considerable interest to study the sugar industry.

1.2 COMPANY PROFILE

Ponni Sugars (Erode) Ltd is an off spring of Ponni Sugars and Chemicals

Ltd (PSCL) under a Demerger Scheme sanctioned by the High Court of Madras

on 10th September 2001. In terms of the Scheme, the company took over the

business of Erode Under taking with concurrent transfer of major part of

stakeholders’ interest in PSCL to the company.

The Erode sugar mill was set up with 1250 TCD capacity in 1984 in a

record time of 12 months. It achieved full capacity crushing during the very first

year of its commercial operation that enabled declaration of a maiden dividend

of 10% in that very first year, a record in the annals of sugar industry. It was a

trendsetter in mobilizing surplus cane during its infancy stage from neighboring

sugar mills and extending crushing season to well above industry average. Its

capacity was expanded to 2500 TCD In 1994.

The Erode sugar mill has successfully implemented an innovative Lift

10

Irrigation Scheme by bringing in dry lands under cane cultivation, utilizing the

effluent discharge of the neighboring paper mill. This has helped secure

multitudinal benefits – providing a dependable and perennial source of

irrigation to farmers in the neighborhood, increase of land value manifold in the

region, transforming the livelihood of local rural population, resolving the raw

material needs of sugar and paper mills and addressing ecological corners in

effluent discharge.

Right from its inception, Ponni was structured on the concept of total

diversion of bagasse for paper. Accordingly it installed a coal fired boiler and

later added a multi fuel boiler in place of conventional bagasse fired boilers. It

has a bagasse tie up arrangement with Seshasayee Paper and Boards Ltd for a

mutually beneficial and rewarding long term relationship.

Ponni is an efficient and quality producer of sugar, catering to both domestic

and international markets. It is a venerable partner for villagers growing

sugarcane in its neighborhood. It enjoys cordial relationship with employees. It

firmly believes in transparent and fair dealings with all its stakeholders by

following sound corporate governance norms both in letter and spirit.

11

A COMPANY WITH A DIFFERENCE

Innovative structuring as backward integration to paper.

First to commit bagasse for paper and derive value

addition.

Pioneered long sugar season.

Implemented a unique effluent irrigation scheme converting

waste to wealth.

ISO 9001:2008 certified for Quality Management system.

ISO 14001:2004 certified for Environmental Management system.

VISION

To excel as trusted socially responsible and customer driven organization

providing maximum value to all stakeholders.

MISSION

To manufacture quality products at competitive cost through technology and teamwork.

VALUES

Ethical practices Customer focus Commitment and transport management Empowerment and accountability Adaptability to “change” Innovation and creativity Emphasis on human resources development, cost reduction, productivity

enhancement and resource conservation.

12

FACTORY FACTSHEET

Year of Establishment 1984

Initial Capacity (TCD) 1250

Present Capacity (TCD) 3500

Factory Area (acres) 33.51

Colony Area (acres) 9.10

No of EmployeesRegular - 232

327Seasonal – 95

No. of Employee Quarters 145

No. of Cultivators 7475

Annual Cane Area under 21300Registration (acres)

1.3 PRODUCT PROFILE

Ponni Sugars (Erode) Limited is an India-based company. The Company is

engaged in the manufacture of sugar and its by-products. The Company’s products

include sugar, bagasse and molasses. During the fiscal year ended March31, 20015

(fiscal 2015), the Company crushed 745,644 tons of cane and produced 76464 tons

of sugar. The Company’s plant is located in Namakkal District, Tamil Nadu.

13

CHAPTER-2

DEVELOPMENT OF MAIN THEME

14

2.1CONCEPT OF THE STUDY

FINANCIAL PERFORMANCE:

Finance is the life blood of a business. Finance is one of the basic

foundations of all kinds of economic activities. Like any other functional

management in a firm (such as production, making, sales etc.,) “finance” is a vit al

functional organization of the firm. If the finance function does not operate will,

the whole organizational activity will be collapsed. The subject matter of financial

management has been defined in many ways depending upon the study of the

subject.

The level of performance of a business over a specified period of time,

expressed in terms of overall profits and losses during that time. Evaluating the

financial performance of a business allows decision-makers to judge the results of

business strategies and activities in objective monetary terms.

Financial performance is prepared primarily for decision making. It plays a

dominant role in setting the frame work of managerial decisions. But the

information provided in Financial performance is not an end in itself as no

meaningful conclusions can be drawn from these statements alone.

2.2 NEED FOR STUDY:

15

The financial performance analysis of overview sugar industry for financial strength and weakness of position in industry. Every business needs to view the financial performance analysis.

The study of financial data like to balance sheet and profit & loss a/c for past five years.

The study of effectiveness of operational and financial performance of ponni sugar (erode) limited is conducted to measure the overall performance of company. The financial strength the industry to make best use and to be able to spot out financial weakness of the industry to state suitable corrective action.

The study aims at analyzing the financial performance of the company by using various financial tools like comparative analysis, common size statement analysis and ratio analysis.

In recent year almost all industries have been facing a challenging scenario due to global competition, increase in input prices and overall economic slowdown which has imposed severe pressures on growth and profitability.

The sugar industry has also been facing weather agriculture farmers work rise sugar cane and increase profit. That is low of stage loss. It is based different weather of year to year.

16

2.3 OBJECTIVE OF THE STUDY:

Primary objective:

To study the financial performance analysis of ponni sugar (erode) limited.

Secondary objective:

To compare and analysis the financial statement for the past five financial years.

To know the profitability, liquidity, activities and solvency position of company.

To comparative and interpret financial statement of the ponni sugar (erode) limited with comparative and common size.

To forecast future sales of ponni sugar (erode) limited. To provide suggestions for improving the overall financial performance of

company.

17

2.4 SCOPE OF THE STUDY:

The data of the past five years are taken into a/c for the study. The performances compared within those periods. This study finds out the areas where ponni sugar factory can improve to increase the efficiency of its asst and funds employed.

The financial statements are analyzed for finding out the various aspects ranging from a simple analysis of the firm to a comprehensive management of the firm in various areas.

The study of financial performance will help the management in the decision making process. The concern is to understand its own position overtime.

Finance is the life blood of company. The study of the financial performance helps the company to understand their

overall profitability position, liquidity position, solvency position and activities long term financial performance of company.

The study gives practical experience researcher to analyzing performance of company.

The financial performance is analysis whether the company attains satisfactory level or not.

18

2.5 LIMITATIONS OF STUDY:

The data collected is not sufficient detailed study of project. The study is mainly based the sources of annual report of the company. The duration of the project work was also barriers to conduct details study. The study related with ponni sugar (erode) limited and project department only. Analysis of ratio can also be done with the help of alternative formulae. Changes in accounting procedures by firm may often financial analysis

misleading. Financial performance statement prepared on the basic certain accounting

concept and conventions. The financial performance analysis is based on monetary information are non

monetary information ignored. The calculation has been on the figures provided the published financial

statement hence, the study is subject to limitations inherited to financial accounting.

19

2.6 REVIEW OF LITERATURE:

1. “G. Malyadri, and B. Sudheer Kumar (2013) found 15 at Indian sugar

industry ishighly stragmented with organize and unorganized players. The

unorganized players mainly produce gur and khandsari, the fess refined forms

sugar. The sector has a number of transformational opportunities. These

opportunities have remained largely untapped. The industry has the potential to

cater to the large and growing domestic sugar consumption and emerge as a

significant carbon credit and power producer. Further, the industry can improve its

cost competitiveness through higher farm productivity and by managing the

domestic production variation through international trade with a focus on countries

in the Indian Ocean. Thus, transformed sector would be fess cyclical with greater

alignment between sugar cane and sugar prices, and will have stable diversified

sources of revenue. This study we have used analysis of Indian Sugar Industry

from Ratio’s Port Of View, Profitability Ratio, Turnover Ratio.”

2.“Miss paravathiin her financial analysis of Hindustan photo films, Ooty for the

years (2009). The researcher concluded that the gross profit has shown an

increasing trend. However the net profit shown a decreasing trend, due to steep rise

in operations cost. The long term solvency, debt equity ratio, proprietary ratio were

not satisfactory. It has been recommended that an increase in long term debts will

take advantage of debt capital.”

3. “Mr. vasanthamani (2006) has studied the financial performance of L.G

Balakrishnan & bros Itd. For the year 2003-2008, the tools used by him were the

ratio analysis, fund flow statement, cash flow statement and the working capital

analysis. It concluded that the financial position of the company was not steady;

20

the rate of return had decline trend till 2000. He found that company in spite of

earning huge gross profit of comparatively very low because of high operating

cost.”

4. “D.I Bhashyam (2003) financial statement analysis is largely a study of

relationship among various financial factors. The analysis and interpretation of

financial statement forecasting future earning ability to pay interest & debt matures

& profitability.”

5. “I M Pandey (financial management 9th edition) comparative statement

analysis is a simple method of tracing periodic changes in the financial

performance of to prepare comparatives statement. Comparative financial

statement will contain items at least for two period changes increased and

decreased in income statement and balance sheet.”

6. “S.K Khatik and P.K Singh made an effort to analyze the working capital

management of IFFCO during the period of (2001-2002). It was found the working

capital ratio, acid test ratio, absolute test ratio and short term liquidity is very much

satisfactory.”

7. “Pandy (1991) has sought to identify factors which influence corporate

economic performance. Importance of industrial characteristics which have been

used by industrial organization researchers as the determinants of financial

21

performance are concentration. Market, share, industry growth, research and

development expenditure, advertisement intensity and size of firms in the industry.

These characteristics may allow firms to be in a better position to implement their

strategies successfully and profitability consequently firms may reflect better

performance on account of favorable characteristics.”

8. “Rachchh minaxi (2011) have suggested that the financial statement analysis

involves analyzing the financial statement to extract information that can be

facilitating decision making. It is the process of evaluating the relationship

between components parts of the financial statement to obtain better understanding

of an entity is position and performance.

9. “John myer, a renowned authority on financial statement analysis has

reference that in the initial year of 20th century the hankers and securities exchange

authority were extensively relying on the financial statement of the companies for

analysis monitoring and control of activities and performance of business. The

history principles and financial statement analysis has been referred by other

authority.

10.“Attwood, D. W. (1995) found the reasons why cooperative sugar factories

inMaharashtra, India are given: (1) successful are examined. Two contradictory

explanations are generally the cooperative spirit already prevalent in the village

communities provided a sound basis for formal cooperatives; (2) village life is

governed by a few wealthy and powerful leaders who also control the cooperatives.

Both explanations are rejected. It is argued that despite a high level of inequality in

the past and the present, informal cooperation has flourished in the villages. The

22

success of the sugar cooperatives rests on the long-standing habit forming selective

alliances to overcome serious technical obstacles in production. The large farmers

depend on the cane supplied by the small farmers to maintain full capacity

utilization, which enables the factories to pay high cane prices.”

23

CHAPTER-3

ANALYSIS AND INTERPRETACTION

3.1 RESEARCH MEHTODLOGY:24

Research is often described as an active, diligent and systematic process of

inquiry aimed at discovering, interpreting and revising facts. This intellectual

investigation produces a greater understanding of events, behaviors or theories and

makes practical applications through laws and theories. The term research is also

used to describe a collection of information about a particular subject, and is

usually associated with science and scientific method.

BASIC RESEARCH

Basic research is also called as fundamental or pure research. Its primary

objective is the advancement of knowledge and the theoretical understanding of

the relations among the variables. It is exploratory and often driven by researcher s

curiosity or interest. It is conducted without any practical end in mind. Basic

research often lays down the foundation for further applied research.

APPLIED RESEARCH

Applied research is done to solve specific, practical questions. Its primary

objective is not to gain knowledge for its own sake. It is usually descriptive in

nature. It is almost always done on the basis of basic research.

3.2 RESEARCH DESIGN:

A research design is simply the framework or plan for a study that is used as guide

in collecting and analyzing the data. It is a blueprint that is following in

completing study.

Descriptive research

25

Descriptive research includes surveys and fact-finding enquiries of different

kinds. The major purpose of descriptive research is descriptive of the state of

affairs as it exists at present. In social science and business research we quite often

use the term. Example post facto research for descriptive research studies. The

main characteristic of this method is that the researcher has no control over the

variables; he can only report what has happened or what is happening.

3.3 SOURCE OF DATA:

1. Primary data.

2. Secondary data.

PRIMARY DATA:

Interviewing primary and secondary data have been source of data. The

study derives its data mainly from primary source of information from finance

employee of the company and the major source of secondary data was annual

report of ponni sugar (erode) limited for years 2010-11, 2011-12, 2012-13, 2013-

14 and 2014-15 from of the balance sheet and profit and loss account of company.

SECONDARY DATA:

There are source containing data which have been collected complied for another

purpose. The secondary source consists of reality available compendia and already

complied statistical statement and reports whose data may be used by researchers

for their studies e.g, census report, statistical statement, annual report and financial

statement of companies, reports of government departments, annual report on

currency and finance published by reserve bank of India.

3.4 TOOLS AND TECHNIQUES OF FINANCIAL PERFORMANCE ANALYSIS:

26

1. Ratio analysis2. Comparative analysis3. Common size analysis

3.5 PERIOD OF STUDY:

The study covers the period of 2011 to 2015 in ponni sugar (erode) limited.

3.6ANALYSIS AND INTERPRECTION:

FINANCIAL PERFORMANCE EVALUATION USING RATIO ANALYSIS:

Ratio analysis is a powerful tool of financial analysis. A ratio is defined as “The

Indicated Quotient of Two Mathematical Expressions” and as “The Relationship

between Two or More Things”. In financial analysis, a ratio is used as a

benchmark for evaluating the financial position and performance of firm. The

absolute accounting figures reported in the financial statement do not provide a

meaningful understanding of the performance and financial position of a firm. The

relationship between two accounting figures, expressed mathematically is known

as a financial ratio. Ratios help to summaries large quantities of financial data and

to make qualitative about the firm’s financial performance.

The point to note is that a ratio reflecting a quantitative relationship helps to

form a qualitative judgment. Such is the nature of all financial ratios.

Significance of Using Ratios:

The significance of a ratio can only truly be appreciated when:

1. It is compared with other ratios in the same set of financial statements.

2. It is compared with the same ratio in previous financial statements (trend

analysis).

3. It is compared with a standard of performance (industry average). Such a

standard may be either the ratio which represents the typical performance of

27

the trade or industry, or the ratio which represents the target set by

management as desirable for the business.

Types of Ratios

Liquidity Ratios

Liquidity refers to the ability of a firm to meet its short-term financial

obligations when and as they fall due.

The main concern of liquidity ratio is to measure the ability of the firms to

meet their short-term maturing obligations. Failure to do this will result in

the total failure of the business, as it would be forced into liquidation.

A. Current Ratio

The Current Ratio expresses the relationship between the firm’s current

assets and its current liabilities. Current assets normally include cash,

marketable securities, accounts receivable and inventories. Current liabilities

consist of accounts payable, short term notes payable, short-term loans,

current maturities of long term debt, accrued income taxes and other accrued

expenses (wages).

Current ratio = current asset / current liabilities

B. Quick asset ratio:

The ratio is also called ‘Liquidity assets or Acid test ratio. It is calculated by comparing the quick asset with current liabilities. Quick or liquid asset refers to assets which are quickly convertible into cash. Current asset other then stock and prepaid expenses are considered as quick assets.

28

Formula:

Liquid ratio= quick asset or liquid asset ------------------------------- Current liabilities

Liquid liabilities= current liabilities-bank O.D

C. Cash position ratio:

The ratio is also called ‘absolute liquidity ratio ‘or ‘super quick ratio’. This is a variation of quick ratio. This ratio is calculated when liquidity is highly restricted in terms of cash and cash equivalents. This ratio measures liquidity in terms of cash and near cash items and short term current liabilities.

Formula:

Cash position ratio= cash and bank balance + marketable securities

-------------------------------------------------------

Current liabilities

Activity Ratio:

If a business does not use its assets effectively, investors in the business would

rather take their money and place it somewhere else. In order for the assets to be

used effectively, the business needs a high turnover.

Unless the business continues to generate high turnover, assets will be idle as it is

impossible to buy and sell fixed assets continuously as turnover changes. Activity

ratios are therefore used to assess how active various assets are in the business.

A. Inventory turnover ratio:

29

This ratio measures the stock in relation to turnover in order to determine how

often the stock turns over in the business. It indicates the efficiency of the firm in

selling its product. It is calculated by dividing the cost of goods sold by the average

inventory.

Formula:

Inventory turnover ratio= cost of goods sold

----------------------------

Average inventory

Average inventory= opening stock + closing stock

-----------------------------------------

2

B. Fixed asset turnover ratio:

The fixed assets turnover ratio measures the efficiency with which the firm has

been using its fixed assets to generate sales. It is calculated by dividing the firm’s

sales by its net fixed assets as follows.

Formula:

Fixed asset turnover ratio= sales

-------------------

Net fixed asset

C. Working capital turnover ratio:

This ratio shows the number of times the working capital results in sales. In other

words, this ratio indicates the efficiency or otherwise in the utilization of short

term funds in making sales. Working capital means the excess of current assets

over current liabilities. In fact, in the short run, it is the current assets and current

liabilities which pay a major role. A careful handling of the short term assets and

30

funds will mean a reduction in the amount of capital employed, thereby improving

turnover. The following formula is used to measure this ratio:

Working capital turnover ratio= sales

-----------------------------

Net working capital

Long term solvency ratio:

a. Fixed asset ratio:

The ratio establishes the relationship between fixed assets and long-term funds. The objectives of calculating this ratio is to ascertain the proportion of long term funds invested in fixed assets.

Formula:

Fixed assets ratio= fixed assets ---------------------- Long term funds

b. Proprietary ratio:

.This ratio is also known as ‘Owners fund ratio’ (or) ‘Shareholders equity ratio’

(or) ‘Equity ratio’ (or) ‘Net worth ratio’. This ratio establishes the relationship

between the proprietors’ fund and total tangible assets. The formula for this

ratio may be written as follows.

Shareholders fund

Proprietary ratio = ---------------------------

Total tangible asset

Profitability Ratios

31

Profitability is the ability of a business to earn profit over a period of time.

Although the profit figure is the starting point for any calculation of cash flow, as

already pointed out, profitable companies can still fail for a lack of cash.

A company should earn profits to survive and grow over a long period of

time.

Profits are essential, but it would be wrong to assume that every action

initiated by management of a company should be aimed at maximizing

profits, irrespective of social consequences.

The ratios examined previously have tendered to measure management efficiency

and risk.

A. Gross Profit Margin

Normally the gross profit has to rise proportionately with sales.

It can also be useful to compare the gross profit margin across similar

businesses although there will often be good reasons for any disparity.

Gross profit margin= gross profit ---------------- *100 Net sales

B. Net Profit Margin

This is a widely used measure of performance and is comparable across companies

in similar industries. The fact that a business works on a very low margin need not

cause alarm because there are some sectors in the industry that work on a basis of

high turnover and low margins, for examples supermarkets and motorcar dealers.

32

What is more important in any trend is the margin and whether it compares well

with similar businesses.

Net profit margin= net profit

--------------- *100

Sales

C. Return on total assets

This ratio is also known as the profit-to-assets ratio. This ratio establishes the

relationship between net profits and assets. As these two terms have conceptual

differences, the ratio may be calculated taking the meaning of the terms according

to the purpose and intent of analysis. Usually, the following formula is used to

determine the return on total assets ratio.

Return on total assets = (Net profit after taxes and interest / Total assets) * 100

Comparative analysis:

Comparative study of financial statement is the comparison of the financial

statement of the business with the previous year’s financial statements and with the

performance of other competitive enterprises, so that weaknesses may be identified

and remedial measures applied.

Comparative statements can be prepared for both types of financial statements

i.e., Balance sheet as well as profit and loss account. The comparative profits and

loss account will present a review of operating activities of the business. The

comparative balance shows the effect of operations on the assets and liabilities that

change in the financial position during the period under consideration.

33

Comparative analysis is the study of trend of the same items and computed

items into or more financial statements of the same business enterprise on different

dates.The presentation of comparative financial statements, in annual and other

reports, enhances the usefulness of such reports and brings out more clearly the

nature and trends of current changes affecting the enterprise.

While the single balance sheet represents balances of accounts drawn at the end

of an accounting period, the comparative balance sheet represent not nearly the

balance of accounts drawn on two different dates, but also the extent of their

increase or decrease between these two dates. The single balance sheet focuses on

the financial status of the concern as on a particular date, the comparative balance

sheet focuses on the changes that have taken place in one accounting period. The

changes are the direct outcome of operational activities, conversion of assets,

liability and capital form into others as well as various interactions among assets,

liability and capital.

Common size analysis:

The common size statements indicate the relationship of various items with some

common items (expressed as percentage of the common items). In the income

statements, the sales figure is taken as basis and all other figures are expressed as

percentage of sales. Similarity, in the balance sheet the total assets and liabilities is

taken as base and all other figures are expressed as percentage of this total.

The percentages so calculated are compared with corresponding

percentage in other period or other firms and meaningful conclusions are drawn.

Generally, a common size income statement and common size balance sheet is

prepared.

34

TABLE-3.6.1

LIQUDITY MEASUREMENT RATIO

35

CURRENT RATIO

Year Current asset Current liabilities Current ratio 2011 9296 4017 2.312012 7794 7124 1.09 2013 10582 10251 1.032014 9463 7601 1.242015 9750 8521 1.14

FINDING:

Initially in financial year 2010-11 the current ratio is 2.31:1 which means there was ideal capital but there was decrease in the current ratio in 2011-12 to 2012-13 which was 1.09:1 and 1.03:1. The dramatically there was particle decrease in the current ratio 2013-14 1.24:1. This means there was ideal capital in 2014-15 there was decrease in current ratio 1.14:1.

INFERENCE:

The ideal current ratio is 2:1. As observed from the table current ratio shows average of 2:1 only during the year 2010-11. The following of year less than ideal ratio 2012 to 2015. It is lack of liquidity and shortage of working capital.

36

CHART -3.6.1

CURRENT RATIO

37

2011 2012 2013 2014 20150

0.5

1

1.5

2

2.5

Current ratio

Current ratio

TABLE-3.6.2

LIQUIDITY OR ACID TEST RATIO

year Liquid assets Current liabilities Liquid ratio

2011 2638 4017 0.656 2012 3100 7124 0.435 2013 3199 10251 0.312 2014 2249 7601 0.295 2015 2500 8521 0.293

FINDING:

Initially in the financial year 2010-11 the quick ratio is 0.656:1. This means there was no ideal capital but there was decrease in 2011-12 to 2012-13.which was 0.312:1 and dramatically there was decrease on the quick ratio 2013-14. This means there was ideal capital in 2014-15 there was decrease in quick ratio 0.293:1

INFERENCE:

The ideal quick ratio is 1:1. As observed from the table quick ratio not possible. Because all years no ideal ratio and less than ideal ratio. It is not better short term financial position of company.

CHART-3.6.2

38

LIQUIDITY OR ACID TEST RATIO

39

2011 2012 2013 2014 20150

0.1

0.2

0.3

0.4

0.5

0.6

0.7

liquidity ratio

liquidity ratio

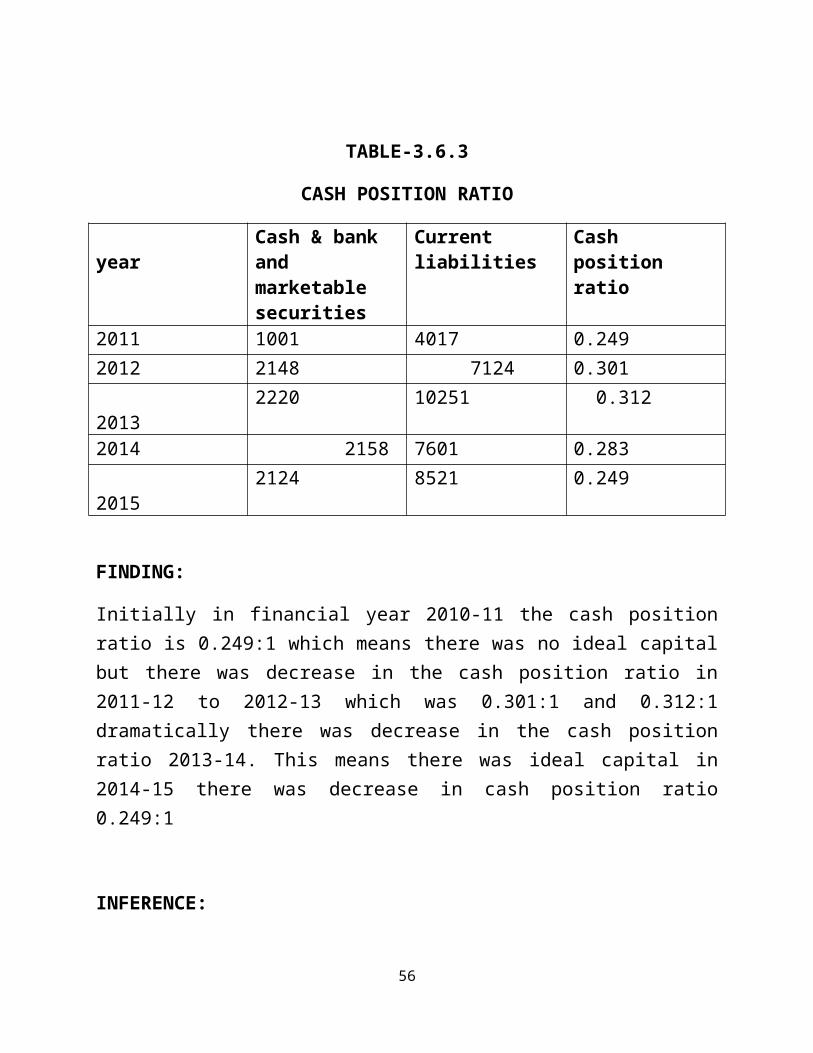

TABLE-3.6.3

CASH POSITION RATIO

year Cash & bank and marketable securities

Current liabilities Cash position ratio

2011 1001 4017 0.2492012 2148 7124 0.301 2013 2220 10251 0.3122014 2158 7601 0.283 2015 2124 8521 0.249

FINDING:

Initially in financial year 2010-11 the cash position ratio is 0.249:1 which means there was no ideal capital but there was decrease in the cash position ratio in 2011-12 to 2012-13 which was 0.301:1 and 0.312:1 dramatically there was decrease in the cash position ratio 2013-14. This means there was ideal capital in 2014-15 there was decrease in cash position ratio 0.249:1

INFERENCE:

40

The ideal cash position ratio is 0.75:1. As observed from the table cash position ratio no average ideal ratio. It is less than ideal ratio of all years. Thereis not better cash position of company .

CHART-3.6.3

CASH POSITION RATIO

2011 2012 2013 2014 20150

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Cash position ratio

Cash position ratio

41

TABLE-3.6.4

TURNOVER MEASUREMENT RATIO

a) INVENTORY TURNOVER RATIO

year Cost of goods sold

Average inventory

Inventory turnover ratio

2011 26948 3329 8.092012 26562 2347 11.312013 21248 3691.5 5.752014 16878 3607 4.672015 15876 3635 4.37

FINDING:

Initially in financial year 2010-11 the inventory turnover ratio is 8.09:1 which means there was increase in the inventory turnover ratio in 2011-12 which was 11.31:1 and dramatically there was decrease in the inventory turnover ratio

42

2012-13 to 2013-14 in 5.75:1 and 4.67:1 which means there was sales decrease in inventory turnover ratio 4.37:1

INFERENCE:

The inventory turnover ratio higher sales and lower inventory. It is higher inventory turnover ratio and better position of company. As observed table inventory turnover ratio shows that 11.31:1 only during the year 2011-12 over sales and low inventory and next 3 years decrease sales and high inventory.

CHART-3.6.4

INVENTORY TURNOVER RATIO

2011 2012 2013 2014 20150

2

4

6

8

10

12

inventoy turnover ratio

inventoy turnover ratio

43

TABLE-3.6.5

FIXED ASSET TURNOVER RATIO

Year Sales Net fixed assets Fixed asset turnover ratio

2011 26948 4521 5.960 2012 26893 12834 2.095 2013 21248 13336 1.590 2014 16878 13406 1.258 2015 15876 12789 1.241

FINDING:

Initially in financial year 2010-11 the fixed assets turnover ratio is 5.960:1 which means there was decrease in the fixed assets turnover ratio in 2011-12 to 2012-13 in 2.095:1 and 1.590:1. The dramatically decrease fixed asset turnover ratio 2013-14 in 1.258:1 which means there was no increase fixed asset turnover ratio 2014-15 in 1.241:1.

INFERENCE:

44

The fixed asset turnover ratio is increase any year and compared with all year rise or fall ratio. This ratio is higher better utilization fixed asset of company and fall ratio no efficiently used of asset. As on observed table show that 2010-2011 5.960:1 and compared all year of fall ratio and no efficiently use asset of company.

CHART-3.6.5

FIXED ASSETS TURNOVER RATIO

45

2011 2012 2013 2014 20150

1

2

3

4

5

6

7

Fixed asset turnover ratio

Fixed asset turnover ratio

TABLE-3.6.6

WORKING CAPITAL TURNOVER RATIO

Year Sales Net working capital

Working capital turnover ratio

2011 26948 5279 5.102012 26893 670 40.132013 21248 331 64.192014 16878 1862 9.062015 15876 1229 12.91

FINDING:

Initially in financial year 2010-11 the working capital turnover ratio is 5.10:1

which means there was increase working capital turnover ratio in 2011-12 to 2012-

2013 of 40.13:1 and 64.19:1 which means there was dramatically decrease 2013-14

to 2014-15 in 9.06:1 and 12.91:1.

46

INFERENCE:

The working capital turnover ratio is higher than efficiently use of company and

low working capital turnover ratio under utilization of company. As on observed

from the table shows that 64.19:1 in 2012-13 this year efficient use of company in

working capital turnover ratio and next two years low working capital ratio for

under utilization of company.

CHART -3.6.6

WORKING CAPITAL TURNOVER RATIO

2011 2012 2013 2014 20150

10

20

30

40

50

60

70

Working capital turnover ratio

Working capital turnover ratio

47

TABLE-3.6.7

DEBT MEASUREMENT RATIO

a) FIXED ASSETS RATIO

Year Fixed assets Long term funds Fixed asset ratio2011 4521 11270 0.4012012 12834 14831 0.8652013 13336 15914 0.8382014 13406 17302 0.7742015 12789 16249 0.787

FINDING:

Initially in financial year 2010-11 the fixed asset ratio is 0.40:1 which means

there was no ideal ratio but there was increase in the fixed asset ratio in 2011-12 to

2012-13 which was 0.865:1 and 0.838:1. The dramatically there was decrease on

48

the fixed asset ratio 2013-14 in 0.774:1 which means there was ideal capital in

2014-15 there was fixed asset ratio partly increase 0.787:1.

INFEENCE:

The ideal fixed asset ratio is 0.67:1. As observed from the table fixed asset

ratio shows that 2010-11decrease ideal ratio 0.404:1 and following next four years

increase ideal ratio. If ratio less than it indicate that a portion working capital has

been financing by long term funds on following year and not more than ideal ratio.

CHART-3.6.7

FIXED ASSETS RATIO

2011 2012 2013 2014 20150

0.10.20.30.40.50.60.70.80.9

1

Fixed asset ratio

Fixed asset ratio

49

TABLE-3.6.8

PROPRIETORY RATIO

Year Share holder funds

Total tangible asset

Proprietary ratio

2011 4521 11270 0.4902012 11154 22760 0.4902013 12914 26275 0.4912014 12376 25210 0.4902015 12011 24899 0.482

FINDING:

Initially in financial year 2010-2011 proprietary ratio is 0.490:1 which

means there was no ideal capital but there was constant of proprietary ratio in

2011-12 and 2013-14 which was 0.491:1 dramatically increase proprietary ratio in

2012-13 which means there was no ideal capital in 2014-15 there was decrease in

proprietary ratio 0.482:1.

50

INFERENCE:

The ideal proprietary ratio is 0.50:1. As observed from the table proprietary

ratio shows below .50 of all years the creditors since them to lose heavily in the

event of company’s liquidation. It is ratio shows that soundness of company.

CHART-3.6.8

PROPRIETORY RATIO

2011 2012 2013 2014 20150.476

0.478

0.48

0.482

0.484

0.486

0.488

0.49

0.492

Proprietary ratio

Proprietary ratio

51

TABLE-3.6.9

PROFITABILITY MEASUREMENT RATIO

a) RETURN ON TOTAL ASSETS

Year Profit after tax and interest

Total assets Return on total assets

2011 2009 12104 16.59%2012 1898 22760 8.33%2013 2269 26275 8.63%2014 1149 16878 6.80%2015 877 15876 5.52%

FINDING:

Initially in financial year 2010-11 the return on total asset is 16.59% which

means higher return on total asset is profit but there was decrease in the return on

total asset in 2011-12 to 2012-13 which was 8.33% and 8.63% dramatically there

52

was decrease in the proprietary ratio 2013-14 which means there was low return on

total asset in 2014-15 there was decrease in return on total asset 5.52%

INFERENCE:

The return on total asset higher than profit of business. As on observed from

the table return on total asset shows average 16.59% only during the year 2010-11

and next 4 years lower of return on total asset.

CHART-3.6.9

RETURN ON TOTAL ASSETS

2011 2012 2013 2014 20150.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

Return on total assets

Return on total assets

53

TABLE-3.6.10

NET PROFIT RATIO

Year Net profit Net sales Net profit ratio

2011 1861 26948 6.90%2012 1779 26562 6.69%2013 1911 21248 8.99%2014 478 16878 2.83%2015 365 15876 2.29%

FINDING:

Initially in financial year 2010-11net profit ratio is 6.90 which means no higher

profit but there was partly increase in the net profit ratio in 2011-12which was

6.69% and dramatically there was increase in the net profit ratio 2012-13 in 8.99%

which means there was decrease in net profit ratio 2013-14 and 2014-15 2.83 to

2.29%.

54

INFERENCE:

The net profit ratio is higher than and profit of business and lowers than a loss

of business. As on observed from table that shows average 8.99% in 2012-13 and

lower 2.29% in 2014-15.

CHART-3.6.10

NET PROFIT RATIO

2011 2012 2013 2014 20150.00%1.00%2.00%3.00%4.00%5.00%6.00%7.00%8.00%9.00%

10.00%

Net profit ratio

Net profit ratio

55

TABLE-3.6.11

GROSS PROFIT RATIO

Year Gross profit Net sales Gross profit ratio2011 1810 25016 7.25%2012 3272 26893 12.16%2013 2928 21428 13.66%2014 674 16878 3.99%2015 358 15876 2.25%

FINDING:

Initially in financial year 2010-2011gross profit ratio is 7.25% which means

there was higher ratio preferable higher profitability but there was increase gross

profit ratio in 2011-12 to 2012-13 which was 13.66% and dramatically there was

decrease in the gross profit ratio in 2013-14 3.99% and also decrease gross profit

ratio 2.25% in 2014-15.

56

INFERENCE:

The gross profit ratio higher profit ratio preferable for indicates of higher

profitability of business and low gross profit ratio losses of business. As on

observed from the table show that higher gross profit is 2012-13 in 13.66 and

lower gross profit ratio is 2.25 in 2014-2015.

CHART-3.6.11

GROSS PROFIT RATIO

2011 2012 2013 2014 20150.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Gross profit ratio

Gross profit ratio

57

TABLE-3.6.12

PONNI SUGAR (ERODE) LIMITED

COMPARATIVE BALANCE SHEET AS ON 31ST MARCH 2010 AND 2011

particular 2010 Rs. In lakh

2011Rs. In lakh

(+) increase and (-) decreaseAmount Rs.

Percentage %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Sundry debtorsc. Cash & bankd. Loan & advances

8,969 1,227 306 1,333

6,658 352 172 2,114

-2,311 -875 -134 +781

25.76 71.31 43.79 58.58

A. TOTAL CURRENT ASSETS

11,835 9,296 -2,539 21.45

2. FIXED ASSETS:a. Gross blockb. (-) depreciation

7,095 2,392

7,168 2,647

+73 -255

1.028 10.660

c. Net block 4,703 4,521 -182 3.869

58

d. Capital WISe. Cogon project

_ _

18 1,457

+18 +1,457

0 0

B. TOTAL FIXED ASSETS 4,703 5,996 +1,475 31.36

3. INVESTMENT 829 829 _ _4. CURRENT

LIABILITIESa. Current

liabilityb. Provision

3,595 2,035

3,817 200

-222 +1,875

6.175 90.170

C. TOTAL CURRENT LIABILITIES

5,630 4,017 +1,613 28.650

TOTAL ASSETS (A+B-C)

11,737 12,104 367 3.126

LIABILITIES:a. Share capitalb. Reserve &

surplusc. Secured loand. Deferred tax

860 7,104

3,430 343

860 8,765

1,645 834

_ +1,661

-1,785 +491

20.85

52.04 143.41

TOTAL LIABILITIES 11,835 12,104 367 3.126

FINDING:

The total current asset on 2010 Rs.11, 835(in lakh) and 2011 Rs.9, 296(in lakh). It was decrease of 2010 to 2011 -2539 based for decrease of inventory, sundry debtors, and cash& bank in 2011.

The total fixed asset on 2011 Rs 4, 703(in lakh) and 2010 Rs.5, 996(in lakh). It was increase of 2010 to 2011 +1475 based for increase capital work in progress , cogon project , and gross block in 2011

The total current liabilities is deducted in total asset on 2010 Rs.5, 630(in lakh) and 2011 Rs.4, 017(in lakh) increased of 2010 to 2011 +1,613 based for increase provision in 2011.

59

The long term liabilities on 2010 Rs.11, 835(in lakh) and 2011 Rs.12, 104(in lakh) based for increased reserve & surplus and deferred tax in 2011.

The total assets Rs. 11, 737(in lakh) in 2010 and increased asset Rs. 12, 104 (in lakh)in 2011.There was increase asset in 2010 to 2011 growing of company.

TABLE-3.6.12

PONNI SUGAR (ERODE) LIMITED

COMMON SIZE BALANCE SHEET AS ON 31ST MARCH 2010 AND 2011

Particular 2010 % 2011 %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Sundry debtorsc. Cash & bankd. Loans &

advances

8,969 1,227 306

1,333

76.41 10.45 2.60

11.35

6,658 352 172

2,114

55 2.90 1.42

17.46A. TOTAL

CURRENT ASSETS:

11,835 100.81 9,296 76.78

2. FIXED ASSETS:a. Gross blockb. (-) depreciation

7,095 2,392

60.44 20.38

7,168 2,647

59.22 21.86

c. Net block 4,703 40.06 4,521 31.26

60

d. Capital WISe. Cogon project

_ _

_ _

18 1,457

0.148 12.00

B. TOTAL FIXED ASSETS 4,703 40.06 5,996 49.53

3. INVESTMENT 829 7.063 829 6.844. CURRENT

LIABILITIES(-)a. Current liabilitiesb. Provision

3,595 2,035

30.62 17.33

3,817 200

31.53 1.65

C. TOTAL CURRENT LIABILITIES

5,630 47.96 4,017 33.19

TOTAL ASSETS (A+B-C)

11,737 100 12,104 100

LIABILITIES:a. Share capitalb. Reserve & surplusc. Secured loand. Deferred tax

860 7,104 3,430 343

7.32 60.52 29.22 2.92

860 8,765 1,645 834

7.10 72.41 13.59 6.81

TOTAL LIABILITIES 11,737 100% 12,104 100

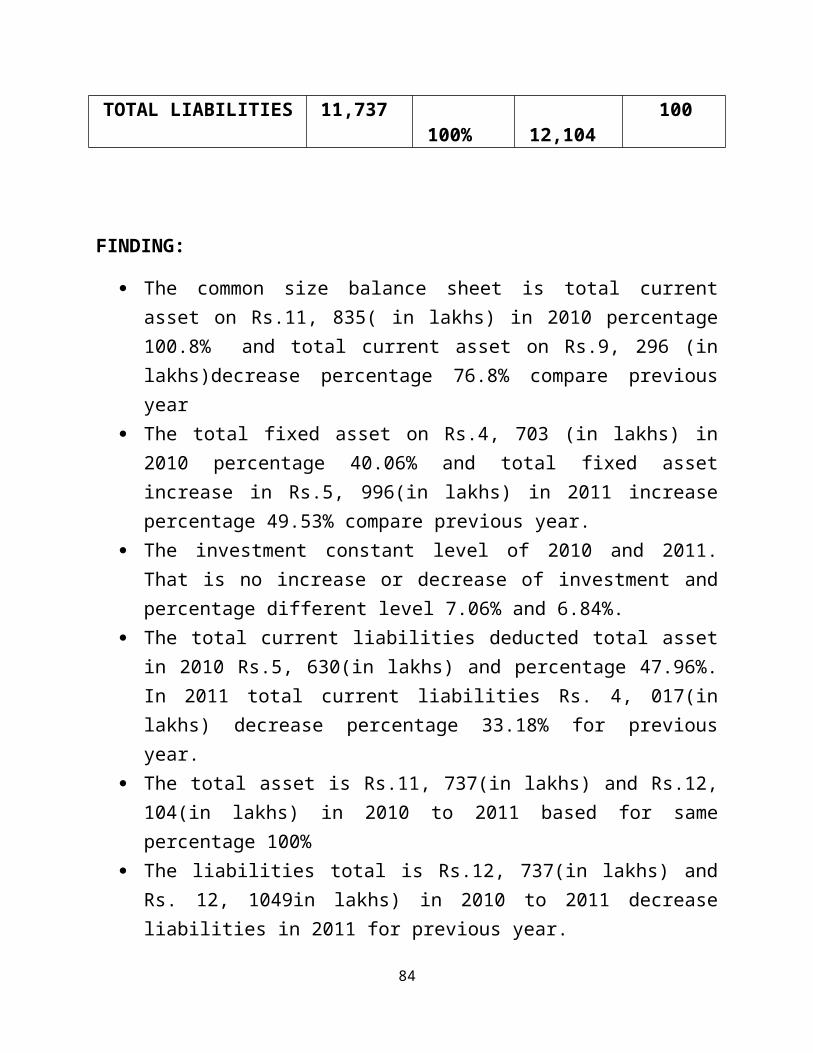

FINDING:

The common size balance sheet is total current asset on Rs.11, 835( in lakhs) in 2010 percentage 100.8% and total current asset on Rs.9, 296 (in lakhs)decrease percentage 76.8% compare previous year

The total fixed asset on Rs.4, 703 (in lakhs) in 2010 percentage 40.06% and total fixed asset increase in Rs.5, 996(in lakhs) in 2011 increase percentage 49.53% compare previous year.

The investment constant level of 2010 and 2011. That is no increase or decrease of investment and percentage different level 7.06% and 6.84%.

The total current liabilities deducted total asset in 2010 Rs.5, 630(in lakhs) and percentage 47.96%. In 2011 total current liabilities Rs. 4, 017(in lakhs) decrease percentage 33.18% for previous year.

61

The total asset is Rs.11, 737(in lakhs) and Rs.12, 104(in lakhs) in 2010 to 2011 based for same percentage 100%

The liabilities total is Rs.12, 737(in lakhs) and Rs. 12, 1049in lakhs) in 2010 to 2011 decrease liabilities in 2011 for previous year.

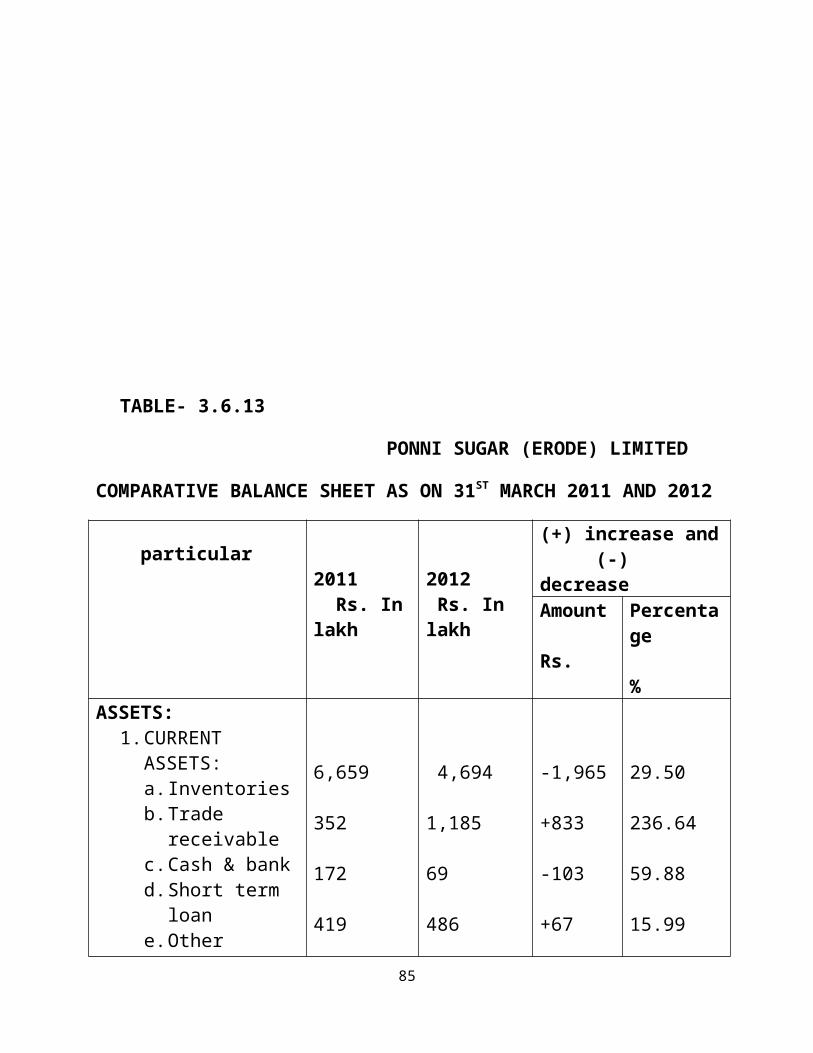

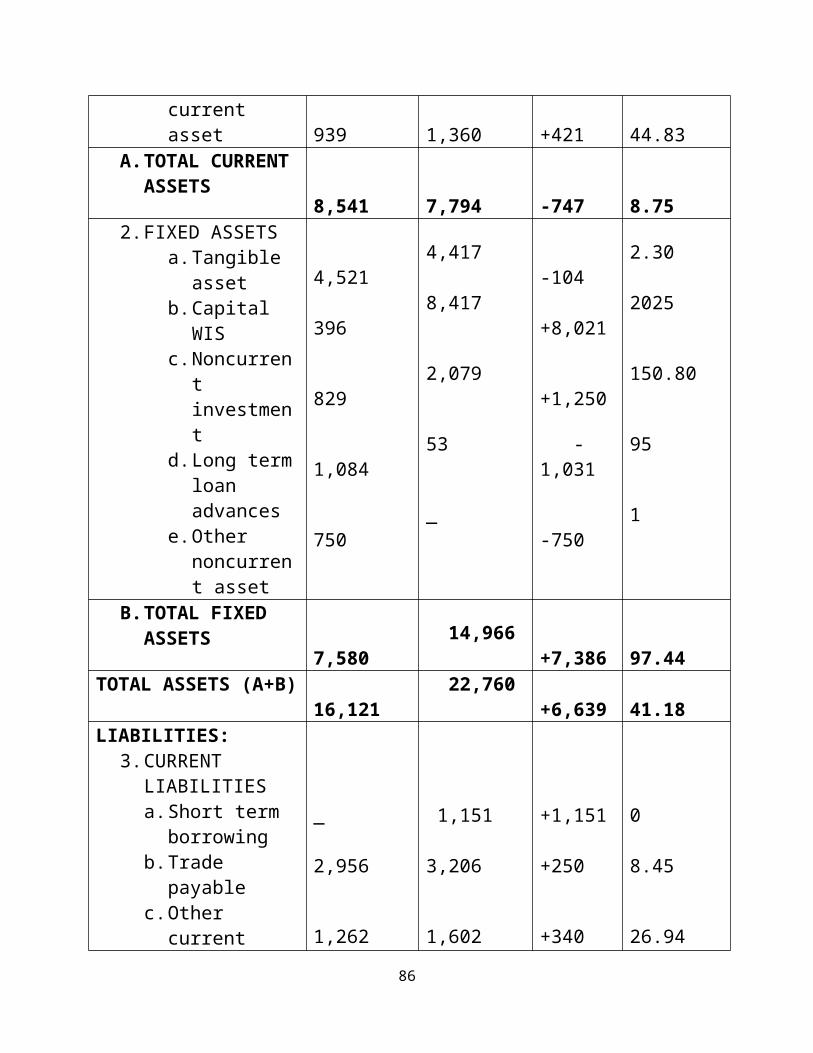

TABLE- 3.6.13

PONNI SUGAR (ERODE) LIMITED

COMPARATIVE BALANCE SHEET AS ON 31ST MARCH 2011 AND 2012

particular 2011 Rs. In lakh

2012 Rs. In lakh

(+) increase and (-) decreaseAmount Rs.

Percentage %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Trade receivablec. Cash & bankd. Short term loane. Other current

asset

6,659 352 172 419

939

4,694 1,185 69 486

1,360

-1,965 +833 -103 +67

+421

29.50 236.64 59.88 15.99

44.83A. TOTAL

CURRENT ASSETS

8,541 7,794 -747 8.75

2. FIXED ASSETS

62

a. Tangible assetb. Capital WISc. Noncurrent

investmentd. Long term

loan advancese. Other

noncurrent asset

4,521 396

829

1,084

750

4,417 8,417

2,079

53

_

-104 +8,021

+1,250

-1,031

-750

2.30 2025

150.80

95

1

B. TOTAL FIXED ASSETS 7,580 14,966 +7,386 97.44

TOTAL ASSETS (A+B) 16,121 22,760 +6,639 41.18LIABILITIES:

3. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilitiesd. Short term

provision

_ 2,956

1,262

589

1,151 3,206

1,602

1,165

+1,151 +250

+340

+576

0 8.45

26.94

97.92

C. TOTAL CURRENT LIABILITIES

4,807 7,124 +2,317 48.02

4. NONCURRENT LIABILITIESa. Long term

borrowingb. Deferred taxc. Share capitald. Reserve &

surplus

855 834 860

8,765

3,677 805 860

10,294

+2,822 -29 _

+1,529

330 3.47 0

17.44

D. TOTAL NON CURRENT 11,314 15,636 +4,322 181.66

63

LIABILITIES

TOTAL LIABILITIES(C+D)

16,121 22,760 +6,639 41.88

FINDING:

The total current asset is Rs. 8, 541( in lakhs) in 2011 and total current asset decrease Rs.7, 794 (in lakhs) 2012 based decrease of inventories, cash and bank -737 in current asset.

The total fixed asset is Rs. 7, 580 (in lakhs) in 2011 and total current asset increase Rs.14, 996(in lakhs) in 2012 based for increase capital work in progress, investment +7386 in fixed asset.

The total asset is Rs.16, 121 (in lakhs) and increase Rs.22, 760(in lakhs) in 2011 to 2012.

The total current liabilities is Rs.4, 807(in lakhs) in 2011 and increase current liabilities Rs.7, 124(in lakhs) in 2012 based for all current liabilities increase of previous year.

The total long term liabilities are Rs.11, 314(in lakhs) in 2011 and increase of current liabilities Rs.15, 636(in lakhs) in 2012 based for increase long term borrowing, reserve & surplus for previous year.

The total liability is Rs.16, 121(in lakhs) in 2011 and increase liabilities Rs. 22, 760(in lakhs) in 2012.

64

TABLE-3.6.14

PONNI SUGAR (ERODE) LIMITED

COMMON SIZE BALANCE SHEET AS ON 31ST MARCH 2011 AND 2012

Particular 2011Rs. In lakh %

2012 Rs. In lakh %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Trade receivablec. Cash & bankd. Short term loan

& advancese. Other current

liabilities

6,659 352 172

419

939

41.30 2.18 1.06

2.59

5.82

4,694 1,185 69

486

1,360

20.62 5.206 0.303

2.135

5.975A. TOTAL

CURRENT ASSETS

8,541 52.98 7,794 34.24

65

2. FIXED ASSETSa. Tangible assetb. Capital WISc. Noncurrent

investmentd. Long term loan

&advancese. Other noncurrent

asset

4,521 396

829

1,084

750

28.04 2.45

0.051

6.72

4.65

4,417 8,417

2,079

53

_

19.40 36.98

9.13

0.232

0

B. TOTAL FIXED ASSETS 8,580 47.00 14,966 65.75

TOTAL ASSETS (A+B) 16,121 100.00 22,760 100LIABILITIES:

1. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilitiesd. Short term

provision

_

2,956

1,262

589

0

18.33

7.82

3.65

1,151

3,206

1,602

1,165

5.05

14

7.03

5.11C. TOTAL

CURRENT LIABILITIES

4,807 29.81 7,124 31.30

2. NONCURRENT LIABILITIESa. Long term

borrowingb. Deferred taxc. Share capitald. Reserve and

surplus

855 834 860

8,765

5.30 5.17 5.33

54.37

3,677 805 860

10,294

16.15 3.53 3.77

45.22

D. TOTAL NON CURRENT LIAB LITIES

11,314 70.17 15,636 80.30

66

TOTAL LIABILITIES (C+D)

16,121 100 22,760 100

FINDING:

The total current asset is Rs.8, 541 (in lakhs) and percentage 52.98% in 2011. There was current asset is Rs.7, 794(in lakhs) decrease percentage 34.24% in2012.

The total fixed asset is Rs.8, 580 (in lakhs) and percentage 47.0% in 2011 and there was fixed asset is Rs.14, 966( in lakhs) increase percentage 65.75% in 2012.

The total asset is Rs.16, 121( in lakhs) 100%in 2011 and Rs.22, 760( in lakhs) increased 100% in 2012.

The total current liabilities is Rs.4, 807(in lakhs )of percentage 29.81% in 2011 and Rs.7, 124 (in lakhs) increase percentage 31.30% in 2012.

The total long term liabilities is Rs.9, 625 (in lakhs) of percentage 59.70% in 2011 and Rs.11, 154(in lakhs)decrease percentage in 2012.

The total liabilities Rs.16, 121(in lakhs) 100% in 2011 and increased Rs.22, 760 in lakhs 100% in 2012.

TABLE-3.6.15

PONNI SUGAR (ERODE) LIMITED

COMPARATIVE BALANCE SHEET AS ON 31ST MARCH 2012 AND 2013

Particular 2012Rs. In lakh

2013Rs. In lakh

(+) increase and (-) decrease Amount Rs.

Percentage %

ASSETS:1. CURRENT ASSETS:

a. Inventoriesb. Trade receivablec. Cash &bankd. Short term loan &

advancese. Other current asset

4,694 1,185 69

1,099 735

7,383 1,689 141

675 694

+2,689 +504 +72

-424 -41

57.28 42.53 104.34

38.58 5.57

A. TOTAL CURRENT

67

ASSETS 7,782 10,582 +2,800 35.982. FIXED ASSETS

a. Tangible assetsb. Capital WISc. Noncurrent

investmentd. Long term

loans&advances

4,417 8,417

2,079

65

13,309 27

2,079

278

+8,892 -8,390

_

+213

201 99.61

_

327.60B. TOTAL FIXED

ASSETS14,978 15,963 +715 4.773

TOTAL ASSETS (A+B) 22,760 26,275 +3,515 15.214LIABILITIES:

1. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilitiesd. Short term provision

1,151 3,162 1,646

1,165

5,031 2,762 1,526

932

+3,880 -400 -120

-233

337.98 12.65 7.29

20

C. TOTALCURRENT LIABLITIES 7,124 10,251 +3,127 43.89

2. NON CURRENT LIABILITIESa. Long term

borrowingb. Deferred taxc. Share capitald. Reserve & surplus

3,677 805 860 10,294

3,000 110 860 12,054

-677 -695 _ +1,760

18.41 86.33 _ 17.09

D. TOTAL NON CURRENT LIABILITES

15,636 16,024 388 46.38

TOTAL LIABILITIES (C+D) 22,760 26,275 +3,515 31.51

FINDING:

68

The total current asset is Rs.7, 782( in lakhs) in 2012 and increase current asset Rs.10, 582( in lakhs) in 2013 based for inventories, trade receivable and cash& bank +2800 for previous year.

The total fixed asset is Rs.14, 978( in lakhs) in 2012 and increase fixed asset Rs.15, 963 (in lakhs) in 2013 based for tangible asset and long term loans & advances +715 for previous year.

The total asset is Rs.22, 760( in lakhs) in 2012 and increase fixed asset Rs.26, 275( in lakhs) in 2013.

The total current liabilities is Rs.7, 124( in lakhs) in 2012 and increased current liabilities is Rs.10, 251( in lakhs) in 2013 based for short term borrowing +3127 for previous year.

The long term liabilities is Rs.15, 636( in lakhs) in 2012 and increase long term liabilities Rs.16, 024( in lakhs )in 2013 based for reserve & surplus for previous year.

The total liabilities are Rs.22, 760 (in lakhs) in 2012 and an increase liability is Rs.26, 275 (in lakhs) in 2013.

TABLE -3.6.16

PONNI SUGAR (ERODE) LIMITED

COMMON SIZE BALANCE SHEET AS ON 31ST MARCH 2012 AND 2013

Particular 2012 % 2013 %ASSETS:

1. CURRENT ASSETSa. Inventoriesb. Trade receivablec. Cash & bankd. Short term loane. Other current

assets

4,694 1,185 69 1,099

735

20.62 5.20 0.303 4.82

3.22

7,383 1,689 141 675

694

28 6.42 0.53 2.56

2.64A. TOTAL

CURRENT ASSETS

7,782 34.16 10,582 40.15

2. FIXED ASSETSa. Tangible assets 4,417 19.40 13,309 50.65

69

b. Capital WISc. Long noncurrent

investmentd. Long term loan

and advances

8,417 2,079

65

36.98 9.13

0.28

27 2,079

278

0.10 7.91

1.05

B. TOTAL FIXED ASSETS 14,978 65.79 15,693 59.71

TOTAL ASSETS(A+B) 22,760 100 26,275 100LIABILITIES

1. CURRENT LIABILITIES

a. Short term borrowing

b. Trade receivablec. Other current

liabilitiesd. Short term provision

1,151 3,162

1,646 1,165

5.05 13.89

7.23 5.11

5,031 2,762

1,526 932

19.14 10.57

5.80 3.84

C. TOTAL CURRENT LIABILITIES

7,124 31.28 10,251 38.99

2. NON CURRENT LIABILITIESa. Long term

borrowingb. Deferred tax

liabilitiesc. Share capitald. Reserve &

surplus

3,677

805 860

10,294

16.15

3.53 3.77

45.22

3,000

110 860

12,054

11.41

0.41 3.27

45.87D. TOTAL NON

CURRENT LIABILITES

15,636 68.67 16,024 60.96

TOTAL LIABILITES(C+D)

22,760 100 26,275 100

FINDING:

70

The total current asset is Rs.7, 782( in lakhs) of percentage on 34.16% in 2012 and increase current asset is Rs.10, 582( in lakhs) of percentage of 40.16% in 2013.

The total fixed asset is Rs.14, 978( in lakhs )of percentage on 65.79% in 2012 and increase fixed asset is Rs.15, 693( in lakhs) of percentage on 59.7% in 2013.

The total asset is Rs.22, 760( in lakhs) of 100% in 2012 and increase asset Rs.26, 275 (in lakhs) of 100% in 2013.

The total current liabilities is Rs.7, 124( in lakhs )percentage of 31.28% in 2012 and increase current liabilities Rs.10, 251( in lakhs) of percentage on 38.99% in 2013.

The long term liabilities is Rs.15, 636 (in lakhs) percentage on 68.67% in 2012 and increase long term liabilities Rs.16, 024( in lakhs) percentage on 60.96% in 2013.

The total liabilities is Rs.22, 760( in lakhs) 100% in 2012 and increase liabilities Rs.26, 275( in lakhs) 100% in 2013.

TABLE-3.6.17

COMPARATIVE BALANCE SHEET AS ON 31ST MARCH 2013 AND 2014

Particular 2013 Rs. In lakh

2014 Rs. In lakh

(+) increase and (-) decreaseAmount Rs.

Percentage %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Trade receivablec. Cash & bankd. Short term loan

and advancese. Other current

asset

7,383 1,689 141

675

694

7,214 1,156 79

299

715

-169 -533 -62

-376

+21

2.289 31.557 43.971

55.703

3.025A. TOTAL

CURRENT ASSETS

10,582 9,463 -1,119 10.574

71

2. FIXED ASSETS:a. Tangible assetsb. Capital WISc. Noncurrent

investmentd. Long term loan

& advances

13,309 27

2,079

278

13,339 67

2,079

262

+30 +40

_

-16

0.225 148.148

_

5.755B. TOTAL FIXED

ASSETS 15,693 15,747 +54 0.344TOTAL ASSETS (A+B) 26,275 25,210 -1065 -4.053LIABILITIES:

1. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilityd. Short term

provision

5,031 2,762

1,526

932

3,214 2,541

636

1,210

-1,817 -221

-890

+278

36.116 8.001

58.322

29.821A. TOTAL

CURRENT LIABILITIES

10,251 7,601 -2,650 25.850

2. NON CURRENT LIABILITIESa. Long term

borrowingb. Deferred tax

liabilityc. Capitald. Reserve &

surplus

3,000

110 860

12,054

4,926

307 860

11,516

+1,926

+197 -527

-538

64.20

179.09 3.944

4.463B. TOTAL NON

CURRENT LIABILITIES

16,024 17,609 1,585 8.11

TOTAL LIABILITIES (C+D)

26,275 25,210 -1,065 -4.053

FINDING:

72

The total current asset is Rs.10, 582 (in lakhs) in 2013 and decrease current asset based for inventories, trade receivable, cash & bank and short term loan and advances Rs.9, 463 (in lakhs)in 2014 -1119 for previous year.

The total fixed asset is Rs.15, 693 (in lakhs) on 2013 and increase fixed asset based for tangible asset and capital work in progress Rs.15, 747(in lakhs) on 2014 is +54 for previous year.

The total asset is Rs.26, 275 (in lakhs) in 2013 and decrease current asset is Rs.25, 210( in lakh) in 2014.

The total current liabilities is Rs.10, 251 (in lakhs) in 2013 and decrease of current liabilities based for trade payable, short term borrowing and other current liabilities Rs.7, 601 (in lakhs) in 2014 -2650 compare previous year.

The total noncurrent liabilities is Rs.16, 024 (in lakhs) in 2013 and increase current liabilities based for long term borrowing and deferred tax Rs.17, 609 (in lakhs) in 2014 1585 for previous year.

The total liabilities is Rs.12, 914( in lakhs )in 2013 and decrease liabilities is Rs.12, 376 (in lakhs) in 2014.TABLE -3.6.18

PONNI SUGAR (ERODE) LIMITED

COMMON SIZE BALANCE SHEET AS ON 31ST MARCH 2013 AND 2014

Particular 2013 Rs. In lakh %

2014 Rs. In lakh %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Trade receivablec. Cash & bankd. Short term loane. Other current

asset

7,383 1,689 141 675

694

28.09 6.43 0.586 2.568

2.641

7,214 1,156 79 299

715

28.61 4.53 0.313 1.186

2.836A. TOTAL

CURRENT ASSETS

10,582 40.27 9,463 37.536

2. FIXED ASSETSa. Tangible asset 13,309 50.65 13,339 52.911

73

b. Capital WISc. Noncurrent asset

investmentd. Long term loan

& advances

27

2,079

278

0.102

7.912

1.058

67

2,079

262

0.265

8.246

1.039B. TOTAL FIXED

ASSETS 15,693 60.753 15,747 62.463TOTAL ASSETS (A+B) 26,275 100 25,210 100LIABILITIES:

1. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilityd. Short term

provision

5,031 2,762

1,526

932

19.14710.510

5.80

3.54

3,214 2,541

636

1,210

12.74 10.07

2.52

4.79C. TOTAL

CURRENT LIABILITIES

10,251 40.04 5,233 20.75

2. NON CURRENT LIABILITIESa. Long term

borrowingb. Deferred tax c. Share capitald. Reserve &

surplus

3,000 110 860

12,054

11.41 0.418 3.273

45.871

4,926 307 860

11,516

19.53 1.21 3.41

45.68D. TOTAL NON

CURRENT LIABILITES

16,024 60.985 17,609 49.09

TOTAL LIABLITIES (C+D)

26,275 100 25,210 100

FINDING:

74

The total current asset is Rs.10, 582(in lakhs) percentage on 40.27% in 2013 and decrease current asset is Rs.9, 463 percentages on 37.53% in 2014.

The total fixed asset is Rs.15, 693(in lakhs) percentage on 60.75% in 2013 and increase fixed asset is Rs.15, 747 (in lakhs) percentage on 62.42% in 2014.

The total asset is Rs.26, 275(in lakhs) 100% in 2013 and decrease asset Rs.25, 210 (in lakhs) 100% in 2014.

The total current liabilities is Rs.10, 251(in lakhs) percentage on 40.04% in 2013 and decrease current liabilities is Rs.5, 233( in lakhs )percentage on 20.75% in 2014.

The total noncurrent liabilities is Rs.16, 024(in lakhs) percentage on 60.98% in 2013 and increase noncurrent liabilities is Rs.17, 609 (in lakhs) percentage on 49.09% in 2014.

The total liability is Rs. 26, 275( in lakhs)100% in 2013 and decreased liabilities is Rs.25, 210( in lakhs) 100% in 2014.

TABLE-3.6.19

PONNI SUGAR (ERODE) LIMITED

COMPARATIVE BALANCE SHEET AS ON 31ST MARCH 2014 AND 2015

Particular 2014 Rs. In lakh

2015Rs. In lakh

(+) increase and (-) decreaseAmount Rs.

Percentage %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Trade receivablec. Cash & bankd. Short term loan

& advancese. Other current

7,214 1,156 79

299

7,250 1,504 45

260

+36 +348 -34

-39

0.49 30.70 43

13

75

asset 695 691 -4 0.57A. TOTAL

CURRENT ASSETS

9,443 9,750 +307 3.25

2. FIXED ASSETS:a. Tangible assetsb. Capital WISc. Noncurrent assetd. Long term loan

& advances

13,339 67 2,079

262

12,773 16 2,079

281

-566 -51 _

+19

4.24 76.11 _

7.25B. TOTAL FIXED

ASSETS 15,747 15,149 -598 3.79TOTAL ASSETS (A+B) 25,190 24,899 -291 1.15LIABILITIES:

1. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilitiesd. Short term

provision

3,214 2,541

616

1,210

3,438 3,175

749

1,159

+224 +634

+133

-51

6.96 24.95

21.54

4.21C. TOTAL

CURRENT LIABILITIES

7,581 8,521 +940 12.39

2. NONCURRENT LIABILITIES:

a. Long term borrowing

b. Deferred tax liability

c. Share capitald. Reserve & surplus

4,926 307 860 11,516

4,238 129 860 11,151

-688 -178 _ -365

13.96 57.98 _ 3.16

D. TOTAL NONCURRENT LIABILITIES

17,609 16,378 -1,231 19.48

TOTAL LIABILITIES (C+D)

25,190 24,899 -291 1.15

76

FINDING:

The total current asset is Rs.9, 443in lakhs in 2014 and increased current asset is Rs.9, 750 in lakhs based for inventories and trade receivable in 2015 +307 for previous year.

The total fixed asset is Rs.15, 747 in lakhs in 2014 and decrease fixed asset is Rs.15, 149in lakhs based for tangible asset and capital work in progress in 2015 -598 for previous year.

The total asset is Rs.25, 190 in lakhs in 2014 and decrease asset is Rs.24, 899 in lakhs in 2015.

The total current liabilities is Rs.7, 581 in lakhs in 2014 and increase current liabilities is Rs.8, 521 in lakhs based for short term borrowing, trade payable and other current liabilities in 2015 +940 for previous year.

The noncurrent liabilities is Rs.17, 609 in lakhs in 2014 and decrease noncurrent liabilities is Rs.16, 378 in lakhs based for all noncurrent liabilities in 2015 -1231 for previous year.

The total liabilities is Rs.25, 190 in lakhs in 2014 and decreased current liabilities Rs.24, 899 in lakhs in 2015. TABLE-3.6.20

PONNI SUGAR (ERODE) LIMITED

COMMON SIZE BALANCE SHEET AS ON 31ST MARCH 2014 AND 2015

Particular 2014 Rs. In lakh %

2015 Rs. In lakh %

ASSETS:1. CURRENT

ASSETS:a. Inventoriesb. Trade receivablec. Cash & bankd. Short term loane. Other current

asset

7,214 1,156 79 299

695

28.63 4.58 0.31 1.18

2.96

7,250 1,504 45 260

691

29.11 6 0.18 1

2.77A. TOTAL

CURRENT ASSETS

9,443 37.46 9,750 39.06

77

2. FIXED ASSETS:a. Tangible assetb. Capital WISc. Noncurrent

investmentd. Long term loan

& advances

13,339 67

2,079

262

52.95 0.26

8.25

1.04

12,773 16

2,079

281

51.29 0.06

8.34

1.12B. TOTAL FIXED

ASSETS 15,747 62.50 15,149 60.81TOTAL ASSETS (A+B) 25,190 100 24,899 100 LIABILITIES:

1. CURRENT LIABILITIESa. Short term

borrowingb. Trade payablec. Other current

liabilitiesd. Short term

provision

4,926 307

860

11,516

19.55 1.21

3.41

45.71

3,438 3,175

749

1,159

13.76 12.75

3

4.65C. TOTAL

CURRENT LIABILITIES

7,581 30 8,521 34.16

2. NONCURRENT LIABILITIES:a. Long term

borrowingb. Deferred tax

liabilityc. Share capitald. Reserve &

surplus

4,926

307 860

11,516

19.54

1.21 3.41

45.71

4,238

129 860

11,151

17

0.51 3.45

44.78D. TOTAL

NONCURRENT LIABILITIES

17,609 50.43 16,378 65.74

TOTAL LIABILITIES (C+D)

25,190 100 24,899 100

78

FINDING:

The total current asset is Rs.9, 443 (in lakhs)percentage on 37.46% in 2014 and increase current asset is Rs.9, 750 (in lakhs) percentage on 39.06% in 2015.

The total fixed asset is Rs.15, 747 (in lakhs) percentage on 62.40%in 2014 and decrease fixed asset is Rs.15, 149( in lakhs) percentage on 60.81% in 2015.

The total asset is Rs.25, 190 (in lakhs) 100% in 2014 and decrease asset Rs.24, 899 (in lakhs) 100% in 2015.

The total current liabilities is Rs.7, 581( in lakhs) percentage on 30% in 2014 and increase current liabilities is Rs.8, 521 (in lakhs) Percentage on 34.16% in 2015.

The total noncurrent liabilities is Rs.17, 609( in lakhs) percentage on 50.43% in 2014 and decrease noncurrent liabilities is Rs.16, 378( in lakhs ) percentage on 65.74% in 2015.

The total liabilities is Rs.25, 190( in lakhs )100% in 2014 and decrease current liabilities is Rs.24, 899( in lakhs) 100% in 2015.

FINDING AND SUGGESTION79

FINDINGS:

The current ratio is ideal ratio 2:1and highest current ratio 2.31:1 in 2010-11 the next following year decrease current ratio in 2012 to 2015.

The quick ratio is ideal ratio 1:1 and no ideal ratio in 2011to 2015 which means highest quick ratio is 0.645:1in 2010 -11 and lowest ratio 0.293:1 in 2014-15.

The cash position ratio is ideal ratio 0.75:1 and no ideal ratio in 2011 to 2015 which means highest ratio 0.312:1 in 2012-13 and lowest ratio is 0.249:1 in 2010-11 and 2014-15.

The inventory turnover ratio is highest sales and lower inventory of 11.31:1 in 2011-12 and lowest ratio 4.37:1 in 2014-15.

The fixed asset turnover ratio is highest ratio of 5.60:1 in 2010-11 and lowest ratio is 1.241:1in 2014-15.

The working capital turnover ratio is higher level of efficient use of company the highest ratio on 64.19:1 in 2012-13 and lowest ratio on 5.10:1 in 2010-11.

80

The fixed asset ratio is ideal capital 0.67:1 and there is highest ratio 0.868:1 in 2012-13 and lowest ratio is 0.404:1in 2010-11.

The proprietary ratio is ideal ratio 0.5:1 and there is no ideal ratio in 2011-15 which means highest ratio is 0.491:1 in 2012-13 and lowest ratio is 0.482:1 in 2014-15.