CAPITAL BUDGETING

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CAPITAL BUDGETING

QUESTION (A)What is capital

budgeting?

•Analysis of potential projects.•Long-term decisions; involve large expenditures.

•Very important to firm’s future.•Evaluate & select long term investment, align with the goal of the firm, maximize s/holder wealth.

QUESTION (B)What is the difference between independent

and mutually exclusive projects?

Projects are:

Independent, if the cash flows of one are unaffected by the acceptance of the other.

Mutually exclusive, if the cash flows of one can be adversely impacted by the acceptance of the other.

QUESTION C (1)What is the payback

period? Find the paybacks for Franchises L and S.

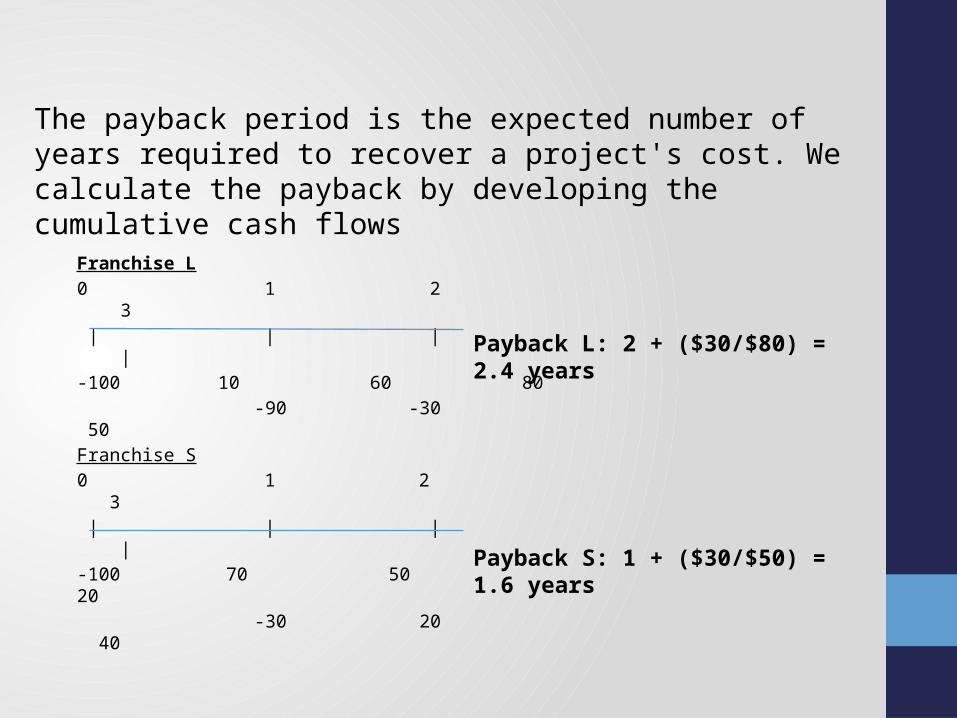

Franchise L0 1 2 3 | | | |-100 10 60 80 -90 -30 50Franchise S0 1 2 3 | | | |-100 70 50 20 -30 20 40

The payback period is the expected number of years required to recover a project's cost. We calculate the payback by developing the cumulative cash flows

Payback L: 2 + ($30/$80) = 2.4 years

Payback S: 1 + ($30/$50) = 1.6 years

QUESTION C (2)What is the rational for the payback method? According to the payback

criterion, which franchises should be accepted if the firm’s maximum

acceptable payback is 2 years, and if franchises L and S are independent? If

they are mutually exclusive?

• Payback represents a type of "breakeven"

analysis: the payback period tells us when the

project will break even in a cash flow sense.

• With a required payback of 2 years, franchise S

is acceptable, but franchise L is not.

• Whether the two projects are independent or

mutually exclusive makes no difference in this

case.

QUESTION C (3)What is the difference

between the regular and discounted payback

periods?

Payback period Discounted payback period

• A capital budgeting procedure

used to determine the profitability

of a project.

• Provides the overall value of a

project, a discounted payback

period gives the number of years it

takes to break even from

undertaking the initial expenditure.

• the payback period only measure

how long it take for the initial cash

outflow to be paid back, ignoring

the time value of money

QUESTION C (3)What is the main disadvantage of

discounted payback? Is the payback method of any real

usefulness in capital budgeting decisions?

• Time value of money is not considered when you

calculate payback period.

• lack of consideration of cash flows beyond the

payback period.

• discounted payback period does not really give the

financial manager or business owner a solid decision

criterion upon which to make an investment decision.

• However, payback is not generally used as the

primary decision tool. Rather, it is used as a rough

measure of a project's liquidity and riskiness.

QUESTION D(1)Define the term net present value (NPV). What is each

franchise’s NPV?

NPV compares the value of a dollar today to the value of that same

dollar in the future. If the NPV of a prospective project is positive, it

should be accepted and vice versa.

Franchise L’s NPV is = $18.79

0 1 2 3

| | | |

(100.00) 10 60 80

9.09

49.59

60.11

18.79 = NPV L

Franchise S’s NPV is = $19.99

0 1 2 3

| | | |

(100.00) 70 50 20

63.64

41.32

15.03

19.99 = NPV S

QUESTION D (2)What is the rationale behind the NPV

method? According to NPV, which franchise or franchises should be accepted if they are independent?

Mutually exclusive?

• If the NPV of any project is zero then it means that the return from

the project is equal to the outflow of the project. There is no chance

of making a profit from the project.

• A positive NPV indicates that project earns more than its cash

outflow and is profitable. In the case of negative NPV, the implication

is vice-versa.

• If franchises L and S are independent, then both should be

accepted, because they both add to shareholders' wealth, hence to

the stock price.

• If the franchises are mutually exclusive, then franchise S should be

chosen over L, because S adds more to the value of the firm.

QUESTION D(3)Would the NPVs change if the cost of

capital changed?

The NPV of a project is dependent

on the cost of capital used. Thus, if

the cost of capital changed, the

NPV of each project would change.

NPV declines as r increases, and

NPV rises as r falls.

QUESTION E(1) (2)Define the term Internal Rate of

Return (IRR). What is each franchise's IRR?

How is the IRR on a project related to the YTM on a bond?

Internal Rate of Return (IRR) is the discount rate that will equate the present value of the outflows with the present value of the inflows.

By using Financial Calculator, we get IRRL = 18.1% and IRRS = 23.6%.

e. (2) How is the IRR on a project related to the YTM on a bond?

IRR to a capital project is like YTM to a bond. IRR is the expected rate of return on the project, just as YTM is the promised rate of return on a bond.

QUESTION E(3)What is the logic behind the IRR method? According to

IRR, which franchises should be accepted if they are independent? Mutually

exclusive?

IRR measures a project's profitability in the rate of return sense.

If IRR = k : cash flows are just sufficient to provide investors with their required rates of return.

If IRR > k : economic profit, which accrues to the firm's shareholders.

If IRR < k : economic loss, or a project that will not earn enough to cover its cost of capital.

If S and L are independent, accept both. IRRs > r = 10%.

If S and L are mutually exclusive, accept S because IRRS nor IRRL .

QUESTION E(4)Would the franchises'

IRR change if the cost of capital changed?

IRR are independent of the cost of capital.

Therefore, neither IRRS nor IRRL would change if k changed.

However, the acceptability of the franchises could change; L would be rejected if k was above 18.1%, and S would also be rejected if k was above 23.6%.

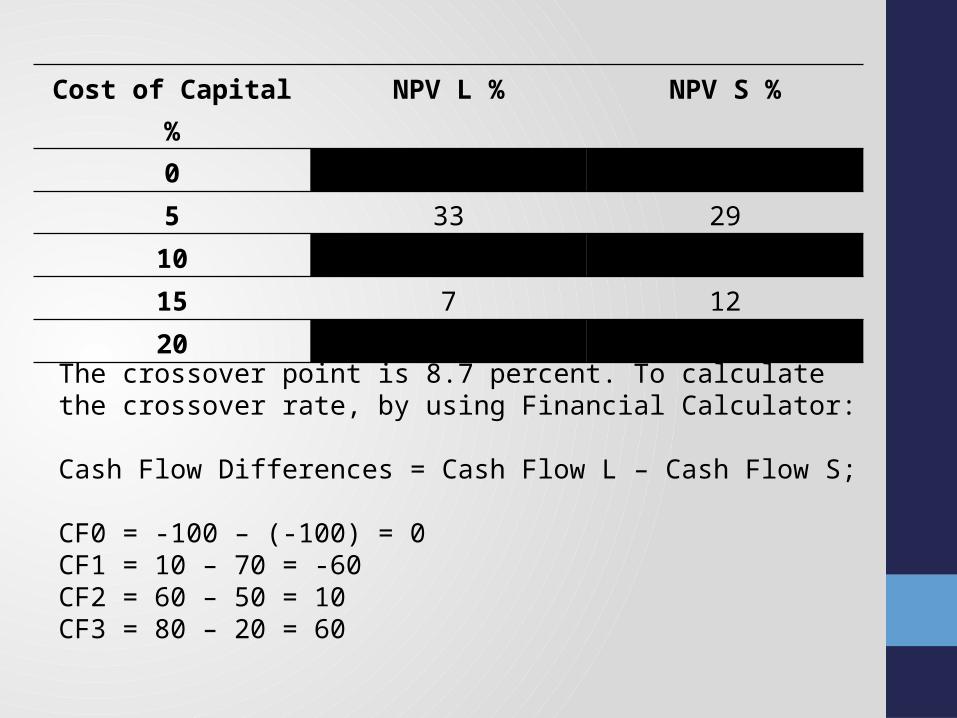

QUESTION F(1)

Draw NPV profiles for franchises L and S. At what discount rate do the profiles

cross?

Cost of Capital % NPV L % NPV S %

0 50 40

5 33 29

10 19 20

15 7 12

20 (4) 5

The crossover point is 8.7 percent. To calculate the crossover rate, by using Financial Calculator:

Cash Flow Differences = Cash Flow L – Cash Flow S;

CF0 = -100 – (-100) = 0 CF1 = 10 – 70 = -60 CF2 = 60 – 50 = 10 CF3 = 80 – 20 = 60

QUESTION F(2)Look at your NPV profile graph without referring to the actual NPVs and IRRs. Which franchise or franchises should be accepted if they are independent? Mutually exclusive? Explain. Are your answers correct at any cost of capital

less than 23.6 percent?

NPV and IRR always lead to the same accept/reject decision for independent projects;

k < IRR and NPV > 0 : Accept

k > IRR and NPV < 0 : Reject

However, for mutually exclusive projects;

K < 8.7 : NPVL > NPVS , IRRS > IRRL ; Conflict

K > 8.7 : NPVs > NPVL , IRRS > IRRL ; No Conflict

QUESTION G(1)What is the underlying

cause of ranking conflicts between NPV and IRR?

• A conflict exists if the cost of capital is less than the crossover rate.

• Two basic condition: When project size (or scale)

differences exist When timing differences

exist

QUESTION G(2)What is the

“reinvestment rate assumption,” and how does it affect the NPV versus IRR conflict?

The underlying cause of ranking conflicts is the reinvestment rate assumption

• Assumed that a project will cost some money up front, and then produce cash flow returns over a period of time

• Assumed that these cash flows will be reinvested by the firm

• NPV assumes that the cash flows will be reinvested at the firm's cost of capital (WACC)

• IRR assumes that cash flows are reinvested at the IRR rate.

QUESTION G (3)Which method is the

best? Why?

• The best assumption :

The project’s cash flows can be reinvested at the cost of capital

• NPV method is more reliable• More realistic in real world

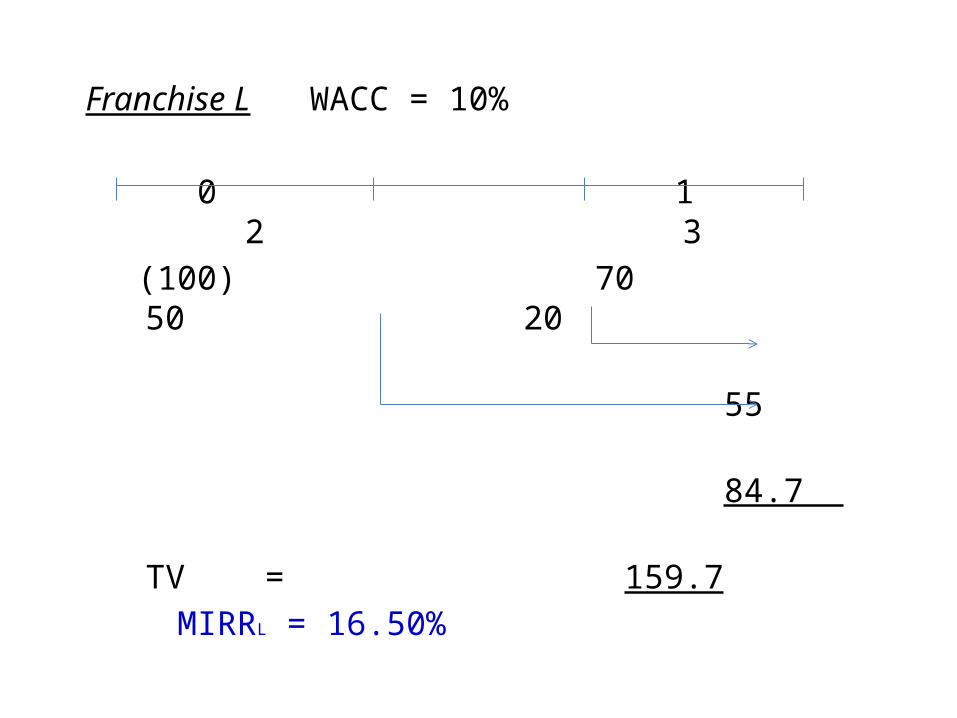

QUESTION H(1)Define the term modified

IRR (MIRR). Find the MIRRs for Franchise L and S

The discount rate that causes a project’s cost (or cash outflows) to

equal the present value of the project’s terminal value.

Franchise L WACC = 10%

0 1 2 3 (100) 70 50 20 55 84.7 TV = 159.7 MIRRL = 16.50%

Franchise S WACC = 10%

0 1 2 3 (100) 10 60 80 66 12.1 TV = 158.1 MIRRS = 16.89%

QUESTION H(2)What are the MIRR’s

advantages and disadvantages vis-a-vis the regular IRR?

• MIRR assumes that cash flows from all the firm’s projects are reinvested at the cost of capital.

• MIRR is a better indicator of a project’s true profitability.

• MIRR solves the multiple IRR problems, as a set of cash flows can have but one MIRR.

What are the MIRR’s advantages and disadvantages vis-a-vis the NPV?

• MIRR does not always lead to the same decision as NPV when mutually exclusive projects are being considered

• NPV remains the single best decision rule• NPV also does provides the best indication of

how much each project will add to the value of the firm.

QUESTION I

As a separate project (project P), you are considering sponsoring a pavilion at the upcoming world's fair. The pavilion would cost $800,000, and it is expected to result in $5 million of incremental cash inflows during its 1 year of operation. However, it would then take another year, and $5 million of costs, to demolish the site and return it to its original condition. Thus, project P's expected net cash flows look like this (in millions of dollars):

Year Net Cash Flows

0 ($0.8) 1 5.0 2 (5.0)

The project is estimated to be of average risk, so its cost of capital is 10 percent.

(1) What are normal and non-normal cash flows? • Normal cash flows begin with a negative or a series of negative cash flows, switch to positive cash flows and then remain positive and vice versa. •They have only one change in sign. •Non-normal cash flows have more than one sign change. For example, they may start with negative cash flows, switch to positive, and then switch back to negative.

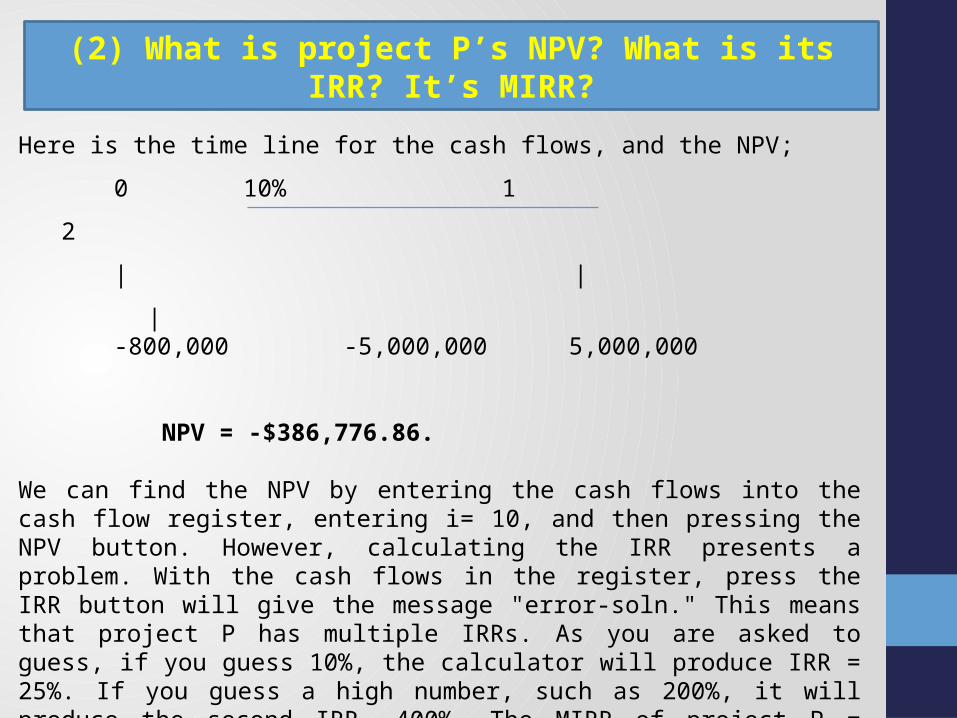

(2) What is project P’s NPV? What is its IRR? It’s MIRR?

Here is the time line for the cash flows, and the NPV;

0 10% 1 2

| | | -800,000 -5,000,000 5,000,000

NPV = -$386,776.86.

We can find the NPV by entering the cash flows into the cash flow register, entering i= 10, and then pressing the NPV button. However, calculating the IRR presents a problem. With the cash flows in the register, press the IRR button will give the message "error-soln." This means that project P has multiple IRRs. As you are asked to guess, if you guess 10%, the calculator will produce IRR = 25%. If you guess a high number, such as 200%, it will produce the second IRR, 400%. The MIRR of project P = 5.6%, and is found by computing the discount rate that equates the terminal value ($5.5 million) to the present value of cost ($4.93 million).

i. (3) Does project P have normal or non-normal cash flows? Should this project be accepted?

• Project P has non-normal cash flows because it has more than one change of signs in the cash flows. Besides it has two IRRs at 25% and at 400%, multiple IRRs is only possible in non-normal cash flow pattern.

• Since project P's NPV is negative, the project should be rejected, even though both IRRs (25% and 400%) are greater than the project's 10 % of capital. The MIRR of 5.6% also supports the decision that the project should be rejected.

QUESTION (J)

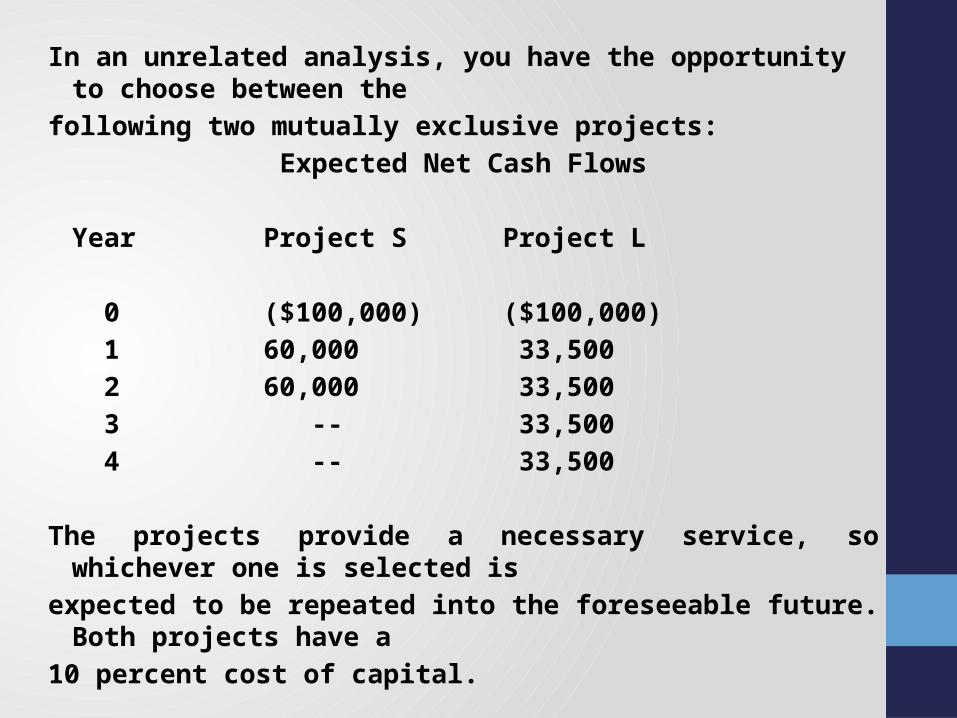

In an unrelated analysis, you have the opportunity to choose between the following two mutually exclusive projects:

Expected Net Cash Flows

Year Project S Project L

0 ($100,000) ($100,000) 1 60,000 33,500 2 60,000 33,500 3 -- 33,500 4 -- 33,500

The projects provide a necessary service, so whichever one is selected is expected to be repeated into the foreseeable future. Both projects have a 10 percent cost of capital.

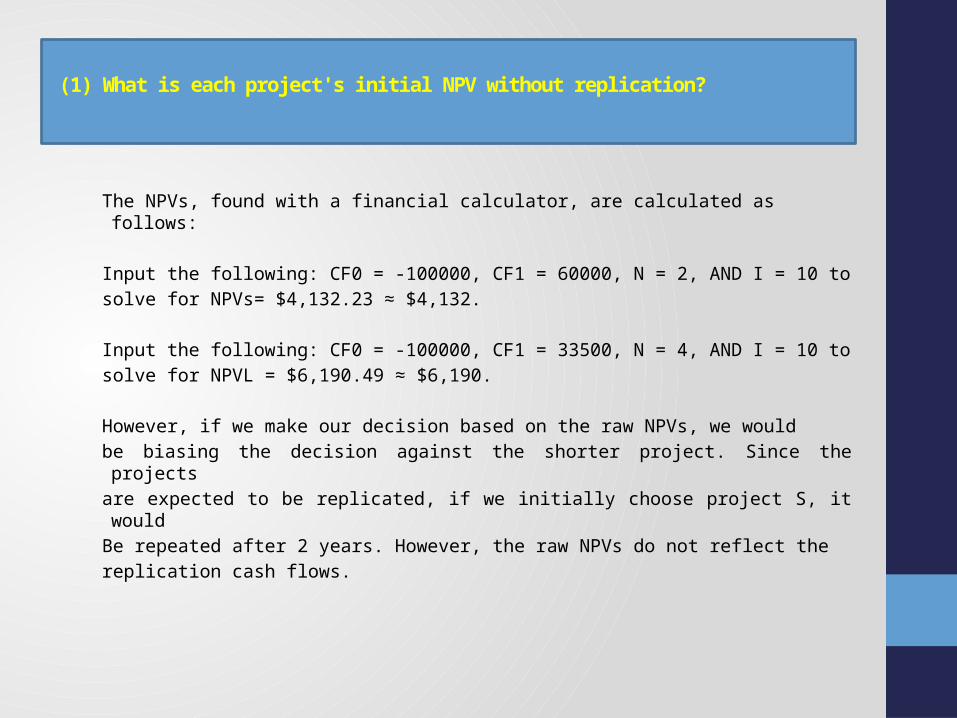

(1) What is each project's initial NPV without replication?

The NPVs, found with a financial calculator, are calculated as follows: Input the following: CF0 = -100000, CF1 = 60000, N = 2, AND I = 10 to solve for NPVs= $4,132.23 ≈ $4,132. Input the following: CF0 = -100000, CF1 = 33500, N = 4, AND I = 10 to solve for NPVL = $6,190.49 ≈ $6,190. However, if we make our decision based on the raw NPVs, we would be biasing the decision against the shorter project. Since the projects are expected to be replicated, if we initially choose project S, it would Be repeated after 2 years. However, the raw NPVs do not reflect the replication cash flows.

(2) Now apply the replacement chain approach to determine the projects’ extended NPVs. Which project should be chosen?

The simple replacement chain approach assumes that the projects will be replicatedout to a common life. Since project S has a 2-year life and L has a 4-year life, the shortest common life is 4 years.

Project L's common life NPV is its raw NPVL = $6,190 (since actual duration = 4 years)

However, project S would be replicated in year 2, and if we assume that the replicated

project's cash flows are identical to the first set of cash flows, then the replicated NPV is also $4,132, but it "comes in" in year 2. We can put project S's cash flow situation

on a time line: 0 10% 1 2 3 4

| | | | |

4132 41323,4157,547 7547

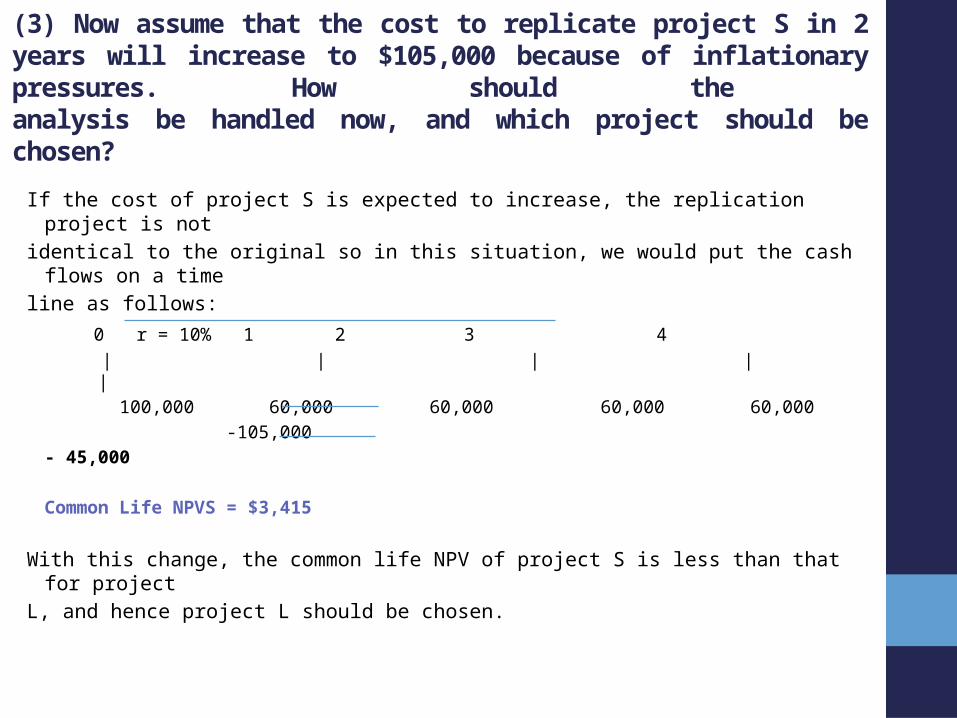

(3) Now assume that the cost to replicate project S in 2 years will increase to $105,000 because of inflationary pressures. How should the analysis be handled now, and which project should be chosen?

If the cost of project S is expected to increase, the replication project is not identical to the original so in this situation, we would put the cash flows on a time line as follows: 0 r = 10% 1 2 3 4 | | | | | 100,000 60,000 60,000 60,000 60,000

-105,000- 45,000

Common Life NPVS = $3,415

With this change, the common life NPV of project S is less than that for project L, and hence project L should be chosen.

QUESTION K

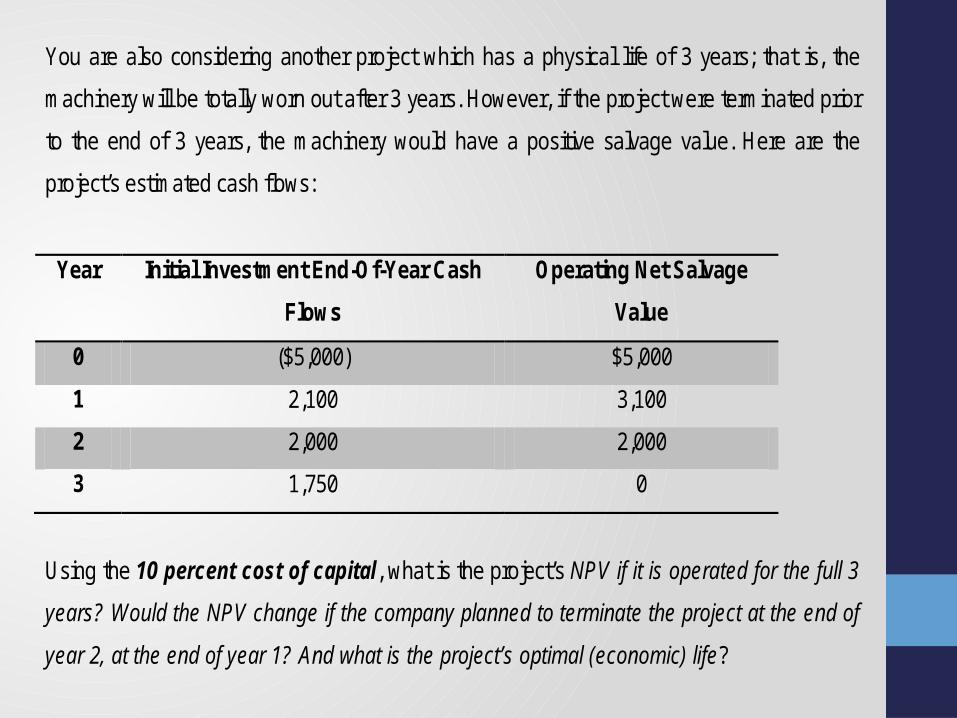

You are also considering another project which has a physical life of 3 years; that is, the

machinery will be totally worn out after 3 years. However, if the project were terminated prior

to the end of 3 years, the machinery would have a positive salvage value. Here are the

project’s estimated cash flows:

Year Initial Investment End-Of-Year Cash

Flows

Operating Net Salvage

Value

0 ($5,000) $5,000

1 2,100 3,100

2 2,000 2,000

3 1,750 0

Using the 10 percent cost of capital, what is the project’s NPV if it is operated for the full 3

years? Would the NPV change if the company planned to terminate the project at the end of

year 2, at the end of year 1? And what is the project’s optimal (economic) life?

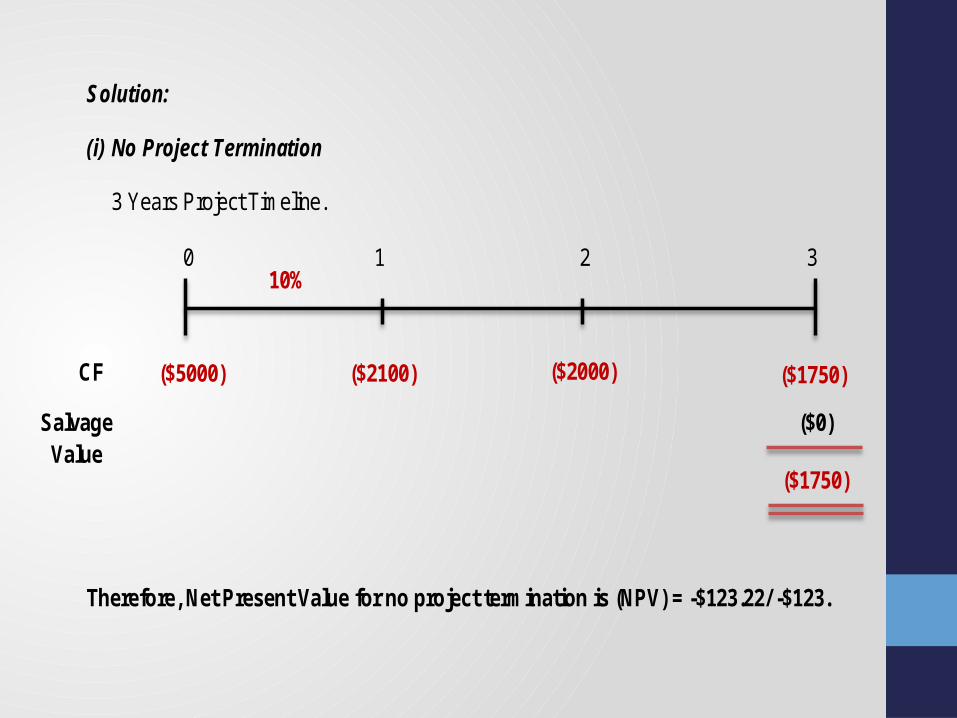

Solution:

(i) No Project Termination

3 Years Project Timeline.

Therefore, Net Present Value for no project termination is (NPV) = -$123.22/ -$123.

0 1 2 3 10%

($5000) ($2100) ($2000) ($1750) CF

Salvage Value

($0)

($1750)

(i) With Termination After 2 Years

2 Years Project Timeline.

Therefore, Net Present Value with project termination after 2 years is (NPV) = $214.88/ $215.

0 1 2 10%

($5000) ($2100) ($2000) CF

Salvage Value

($2000)

($4000)

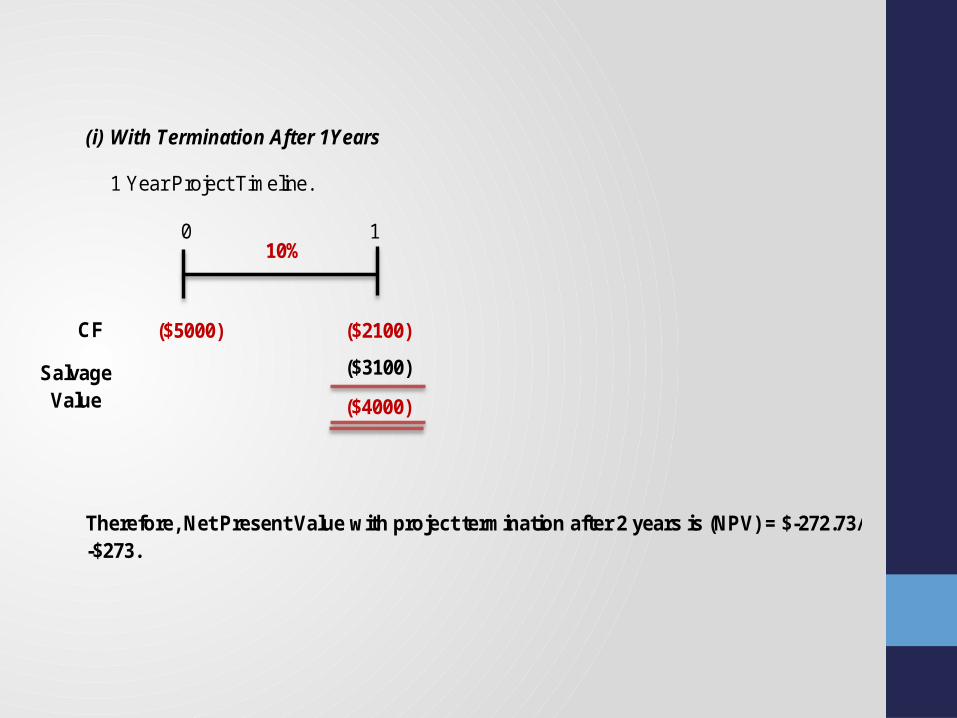

(i) With Termination After 1Years

1 Year Project Timeline.

Therefore, Net Present Value with project termination after 2 years is (NPV) = $-272.73/ -$273.

0 1 10%

($5000) ($2100) CF

Salvage Value

($3100)

($4000)

CONCLUSION:

Based on all NPV value from three different options

can be conclude that the optimal economic life is the

project should be terminate after years 2 where the

NPV value is positive ($215). Moreover, it also

indicated that a project engineering life does not

always equal to its economic life.

QUESTION L

After examining all the potential

projects, you discover that there

are many more projects this year

with positive NPVs than in a normal

year. What two problems might this

extra-large capital budget cause?

Increasing in Cost of Capital

• cause company to reject projects that they might otherwise accept

Capital Rationing

THANK YOUQ & A SESSION

Related Documents