January 2012 Yale School of Management Global Social Entrepreneurship Team: Courtney Drake, Jiaxin Liu, Dan Peck, Jonathan Shafer, Richa Sharda Rickshaw Bank Pradip Sarmah Final Report for Rickshaw Bank Project

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

January 2012

Yale School of Management Global Social Entrepreneurship Team: Courtney Drake, Jiaxin Liu, Dan Peck, Jonathan Shafer, Richa Sharda Rickshaw Bank Pradip Sarmah

Final Report for Rickshaw Bank Project

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

2 | P a g e

Table of Contents Executive Summary ...................................................................................................................................... 4

Yale SOM/GSE Program .............................................................................................................................. 5

Rickshaw Bank Overview ............................................................................................................................. 5

Mission ...................................................................................................................................................... 5

Description ................................................................................................................................................ 5

Impact ....................................................................................................................................................... 5

Business Model ......................................................................................................................................... 6

Sources of revenue .................................................................................................................................... 7

Rickshaw Bank’s Goals and Challenges ....................................................................................................... 8

Scope of Work .............................................................................................................................................. 9

Methodology ................................................................................................................................................. 9

Research Findings ....................................................................................................................................... 12

Expansion ................................................................................................................................................ 12

Financial Clarity...................................................................................................................................... 12

Inefficiency in Collection and Repayment Process ................................................................................ 13

Funding Needs in Status Quo and Expansion Scenarios ........................................................................ 15

Recommendations ....................................................................................................................................... 18

1. Adopting Weekly Collection Schedule ............................................................................................... 18

2. Adopting Electronic Loan Tracking System ....................................................................................... 18

3. Redefining and Enforcing Collection Policies .................................................................................... 19

4. Developing Financial Monitoring and Budgeting Process ................................................................. 20

Conclusions ................................................................................................................................................. 21

Appendix ..................................................................................................................................................... 22

Exhibit 1: Application Process Flow Chart and Possible Improvement ............................................. 22

Exhibit 2: Detailed Financial Model Methodology ............................................................................ 23

Exhibit 3: Summary of Operations Activities Scorecard .................................................................... 26

Exhibit 4: Operations Activities Scorecard ......................................................................................... 26

Exhibit 5: EBIT & Net Income over Time.......................................................................................... 27

Exhibit 6: Revenue Composition over Time ....................................................................................... 27

Exhibit 7: Profit Margins .................................................................................................................... 28

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

3 | P a g e

Exhibit 8: Profit Margin per Rickshaw Calculation ............................................................................ 28

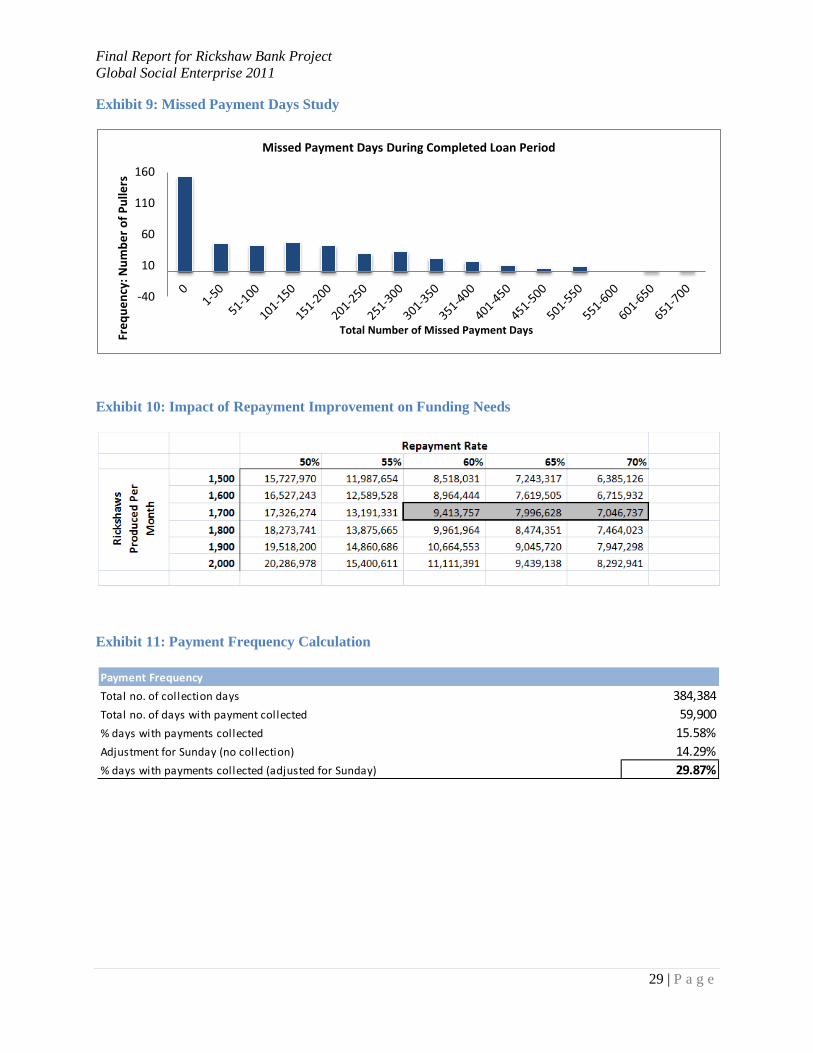

Exhibit 9: Missed Payment Days Study .............................................................................................. 29

Exhibit 10: Impact of Repayment Improvement on Funding Needs .................................................. 29

Exhibit 11: Payment Frequency Calculation ...................................................................................... 29

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

4 | P a g e

Executive Summary

This report contains analysis and recommendations for Rickshaw Bank to improve its current loan collection operations and prepare itself to approach banks for funding. Rickshaw Bank is an internal program of Center for Rural Development (CRD) based in Guwahati, Assam. The mission of Rickshaw Bank is to improve rickshaw pullers’ lives through asset ownership.

We were initially presented with the question of how Rickshaw Bank should expand its operations. However, through our research and analysis, we concluded that the essential first step to expansion is to understand and potentially improve Rickshaw Bank’s current operations. As a relatively young organization, Rickshaw Bank has yet to develop a systematic analysis of its profitability and operational efficiency. Consequently, we analyzed Rickshaw Bank’s financial statements and studied its operations through a variety of approaches, with primary emphasis on its collection practices, as the collection process has the most direct impact on RB’s financial viability.

Our findings suggest that Rickshaw Bank’s business model can be financially viable but it needs to make several concrete changes to its collection process. In addition, in order to grow its production and repay loans that are maturing in the next year, Rickshaw Bank needs Rs 6.6 million additional financing before March 2015.

We recommend that Rickshaw Bank make the following changes to better serve the rickshaw pullers:

1. Adopt a weekly collection schedule

2. Use an electronic loan tracking system

3. Stricter enforcement of collection policies

4. Develop a financial monitoring and budgeting process

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

5 | P a g e

Yale SOM/GSE Program

The mission of the Yale School of Management (SOM) is to educate leaders for business and society. The Global Social Entrepreneurship (GSE) class is an elective course offered at SOM that teaches students the important issues concerning mission driven social enterprises. This course connects teams of students at Yale SOM to selected social enterprises in India. Together, teams of students and the social enterprises address challenges faced by the enterprises and students apply class concepts to give recommendations.

Rickshaw Bank Overview

Mission

Rickshaw Bank’s mission is to empower and improve the lives of rickshaw pullers in India by providing them access to asset ownership through the issuance of micro leases on rickshaws and other pedal carts.

Description

Based in Guwahati, Assam and founded in 2004 as an internal program of the Center for Rural Development, the Rickshaw Bank is a unique rickshaw micro-leasing program that provides vulnerable and marginalized rickshaw pullers access to the necessary financing to purchase their own rickshaws and improve the quality of their lives. Since inception, the organization has manufactured and distributed nearly 4,000 of its uniquely designed rickshaws to pullers in the state of Assam. To maintain a holistic service, Rickshaw Bank provides insurance, registration and identity card, uniform and sandals, and training to the pullers. As a result of the Rickshaw Bank’s interventions, rickshaw pullers throughout Assam have been able to attain a greater level of financial independence, send their children to school, and provide higher quantity and quality of food for their families.

Impact

The impact of Rickshaw Bank’s work can be tremendous. It is estimated that there are 8 million rickshaw pullers in India. However, less than 10% of these rickshaw pullers own their rickshaws. The vast majority of them pay a daily rental fee between Rs. 25 and Rs. 40 to a local rickshaw leaser for their entire career. With Rickshaw Bank’s model, the rickshaw pullers can pay a similar daily rate for a fixed period of time and eventually own the rickshaw.

Rickshaw Bank believes that, by providing the Rickshaw pullers asset ownership, they can improve pullers’ standards of living; once they gain ownership, pullers will no longer be forced to pay daily rental fees for their rickshaws, leaving them with higher disposable income in the future. Asset ownership also brings other intangible benefits to these rickshaw pullers and their families. Rickshaw Bank has observed that pullers gain a sense of dignity and self-confidence that they lacked prior to participating in the program.

So far, Rickshaw Bank has impacted the lives of approximately 4,000 rickshaw pullers and their families in Assam.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

6 | P a g e

Business Model

Rickshaw Bank’s business model consists of two components – manufacturing and leasing.

Manufacturing

Rickshaw Bank has an internal manufacturing facility that is currently staffed by eighteen full-time workers. Rickshaw Bank’s rickshaw model is uniquely designed by IIT Guwahati, a major engineering school in India, and has been modified by students from MIT in Cambridge, Massachusetts. The design lowers the center of gravity and hence gives pullers better stability when operating the rickshaws. Although the capacity of the manufacturing facility is 125 rickshaws per month, Rickshaw Bank has been producing at about 75 rickshaws per month in the most recent months. Rickshaw Bank is producing below its capacity because of the following reasons:

a. Lack of funding – Rickshaw Bank does not have enough funds to invest to produce at capacity b. Lack of power – without a generator, the manufacturing facility faces major power cuts and

therefore cannot operate to produce at capacity.

Leasing

Rickshaw Bank obtains loans from financial institutions to manufacture rickshaws and then leases the manufactured rickshaws to local rickshaw pullers.

To qualify for a rickshaw lease, a rickshaw puller must complete an application that includes the following required documents:

• Residency document • Residency certificate from village leaders • Indian citizenship number • Field Collector Verification Form • Agreement signed by the puller and guarantor

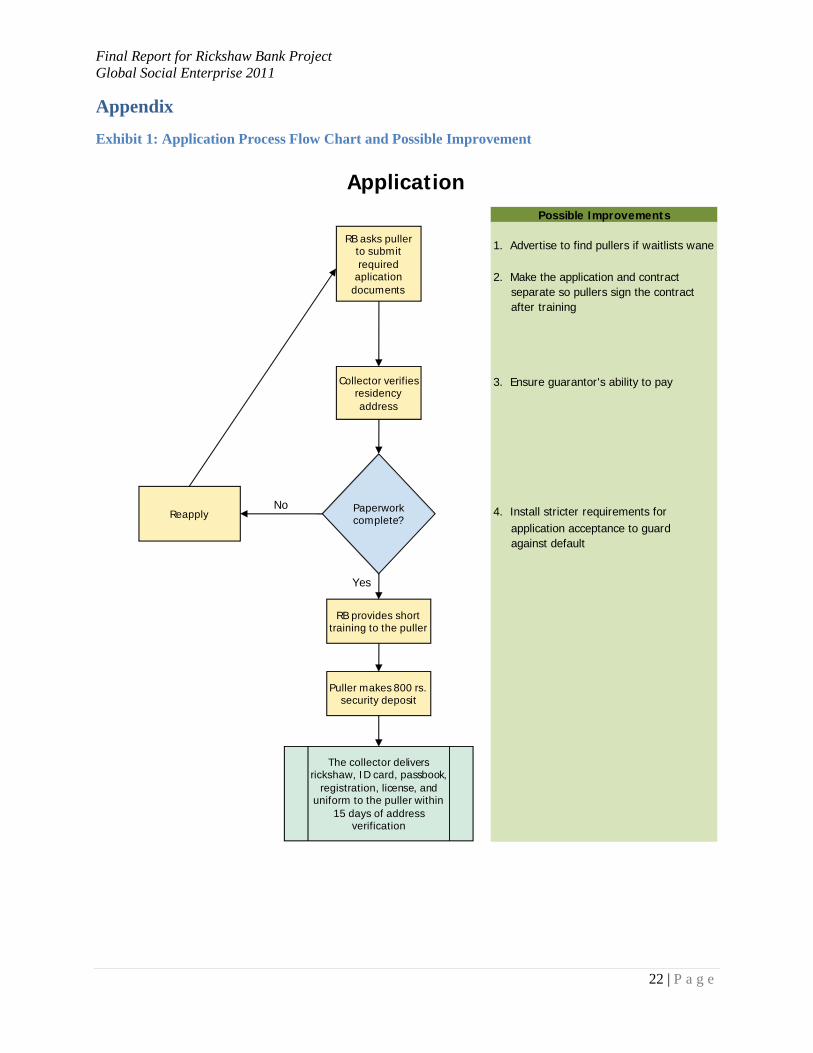

After Rickshaw Bank employees ensure all the required documents are present, RB approves loans for the lease of rickshaws. Each puller receives a rickshaw, along with a license, an ID card, insurance for the rickshaw asset and a uniform and sandals. As of August 2011, Rickshaw bank charges Rs 14,000 for the entire package. The contracted repayment term is 350 days in the form of Rs 40 daily payments (Exhibit 1).

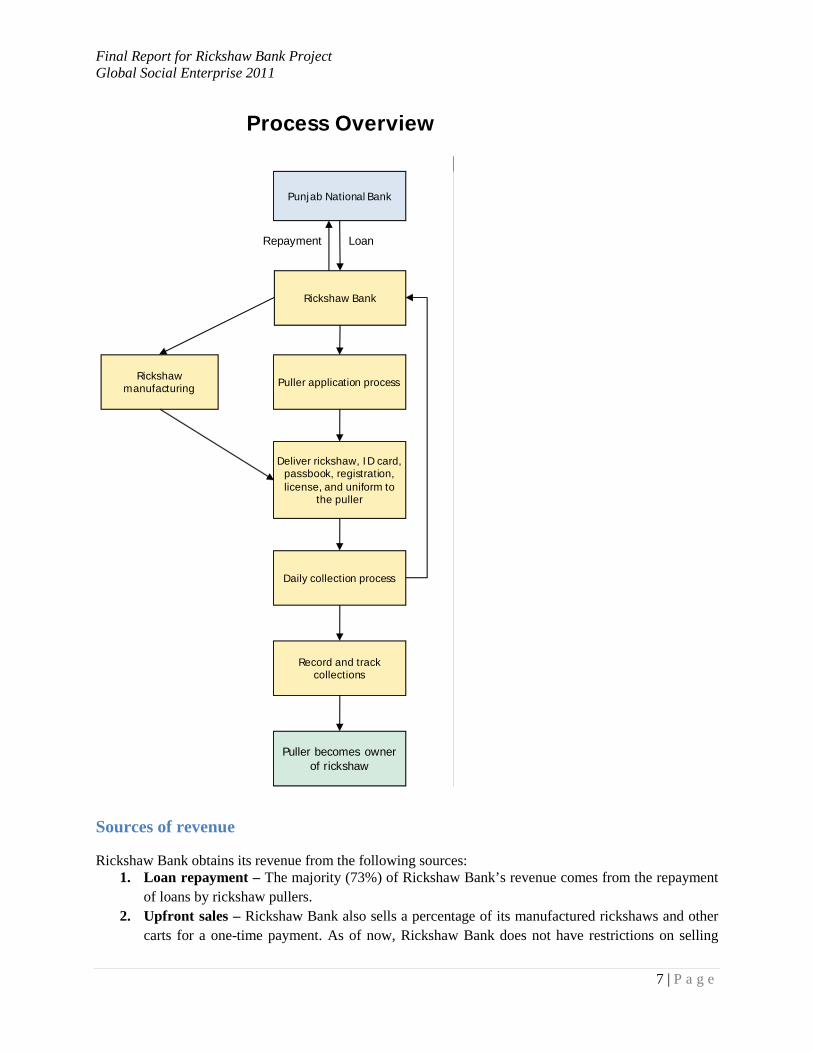

Pullers are assigned to a group of 25 based on their residential location, and each loan collector is assigned five groups of rickshaw pullers, called garages. The collector goes to each garage daily to collect payments from his assigned group of rickshaw pullers. Once a rickshaw puller has completed all his payments, he is issued a certificate of ownership. A broad overview of RB’s operational process is presented below.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

7 | P a g e

Sources of revenue

Rickshaw Bank obtains its revenue from the following sources: 1. Loan repayment – The majority (73%) of Rickshaw Bank’s revenue comes from the repayment

of loans by rickshaw pullers. 2. Upfront sales – Rickshaw Bank also sells a percentage of its manufactured rickshaws and other

carts for a one-time payment. As of now, Rickshaw Bank does not have restrictions on selling

Repayment Loan

Rickshaw Bank

Punjab National Bank

Puller application processRickshaw manufacturing

Deliver rickshaw, ID card, passbook, registration, license, and uniform to

the puller

Daily collection process

Record and track collections

Puller becomes owner of rickshaw

Process Overview

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

8 | P a g e

more than one rickshaw to the same person. Upfront sales currently account for 27% of Rickshaw Bank’s revenue.

3. Other revenue – A very small percentage of Rickshaw Bank revenue also comes from non-core businesses such as fees paid by rickshaw pullers to apply for loans and sales of scrap and excess spare parts.

4. Late payment charges – Pullers who do not make payments on time without valid excuses are charged a late payment fee. The fee is 2% of the balance outstanding at the end of one month or 45 days. However, this fee has been an insignificant source of revenue for Rickshaw Bank as the fee itself is small, and few pullers are charged the fee.

5. Advertising revenue – In its early years, Rickshaw Bank received advertising funding from companies such as Indian Oil Corporation. Advertisements of these companies are placed at the back of the rickshaw. Although Rickshaw Bank has not actively pursued advertisement revenue in the past few years, the organization considers exploring this option in future.

Rickshaw Bank’s Goals and Challenges

Rickshaw Bank has successfully transitioned from a mere idea to a fully operational, high-impact social enterprise, and it is now considering expanding beyond Assam and spreading the model to other cities. As the Yale GSE team sought to assist Rickshaw Bank to explore options to expand, we realized that there were many challenges that were crucial to address before expansion.

We believe that Rickshaw Bank first needs to ensure that its current processes and collections operations are efficient and financially viable. To this end, our team identified the following challenges that the organization needs to address before considering expansion:

Lack of Financial Clarity

Rickshaw Bank has yet to systematically analyze its financial position and the factors that drive profitability. This is partially because over the seven years in operations, Rickshaw Bank’s financial reporting has been part of Center for Rural Development, its parent nonprofit, and most of the revenue and costs are embedded in the larger CRD. Without knowing its current profitability and financing needs, it would be difficult for Rickshaw Bank to present the viability of its business model to potential funders.

Inefficiency in Leasing and Collection Process

Repayment of loans by the rickshaw pullers and the collection of these loans constitute major parts of the Rickshaw Bank activities. Although Rickshaw Bank has developed collection policies and procedures, we observed that the organization had little clarity on how effective these policies are and how well the policies are enforced. Specifically, we identified the following key metrics that needed to be evaluated:

a. Effective interest rate charged to rickshaw pullers b. On-time repayment rate c. Frequency of repayment d. Late payment e. Issuance

Understanding Funding Needs

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

9 | P a g e

In order for Rickshaw Bank to expand, it requires funding from financial institutions like Punjab National Bank. To be able to approach a bank, Rickshaw Bank must have a clear understanding of its current business and know the exact amount of funds needed to reach that level of expansion.

Scope of Work

Based on the challenges above, we defined the scope of work for the project to give Rickshaw Bank recommendations for strengthening current operations. We aimed to use a broad range of approaches to help Rickshaw Bank address the challenges. Specifically, we did the following analyses:

Financial Analysis. The GSE Team studied Rickshaw Bank’s current and future profitability by consolidating and analyzing all cash payments and receipts for the past three years..

Analysis on Collection and Repayment. The team amalgamated daily payment information for all Guwahati rickshaw pullers in the past three years. We studied rickshaw pullers’ repayment behavior and benchmarked Rickshaw Bank’s collection process with comparable microfinance institutions (MFIs) in India. We also analyzed the rickshaw issuance pattern and its corresponding revenue impact on the organization.

Funding Needs. Building on the results obtained from the financial analysis and repayment data analysis, the team created a financial model to project the future financials of rickshaw bank, thus calculating its funding needs under two scenarios:

a. Production at current level b. Expansion at various output levels

Expansion. Rickshaw Bank is considering two opportunities to expand: within Assam through its current set up and manufacturing facility, and beyond Assam to other states of India. We developed a self-evaluation scorecard and broadly determined the strengths and weaknesses of each operating segment. As explained above, Rickshaw Bank needs to address its current challenges. Therefore, for this project the Yale GSE team focused primarily on resolving these challenges and strengthening Rickshaw Bank’s current position so that it can be better prepared for future expansion.

Methodology

In-person Client Interviews

Two members from the GSE team travelled to India in August 2011, where they conducted interviews with RB and observed their operations. Later in September, the Rickshaw Team visited Yale. During this period, the other team members had a chance to understand the enterprise and the client better and together the two teams finalized the scope of work.

After structuring the project and coming up with more detailed questions about finances, accounting and the collection process, a third team member visited Rickshaw Bank in October and conducted in-depth interviews.

These in-person client interactions, in addition to regular phone calls, enabled the GSE team to work closely with RB, ensuring timely communication and regular progress updates.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

10 | P a g e

Process Mapping

The information obtained through interviews from the first visit was translated into process maps of Rickshaw Bank’s operations. This helped us scope our project when the Rickshaw Bank team visited Yale and helped us address the most important issues for the Rickshaw Bank.

Analysis of Rickshaw Bank’s historical cash flow statements

As CRD does not have separate accounting for its rickshaw operations, and does not use accrual accounting, we developed monthly income statements based on cash receipts and payments for the past three years.

Puller Payment Data Analysis

Our analysis is based on 1,105 rickshaw pullers’ daily payment data at Rickshaw Bank’s Guwahati branch from April 1, 2008 to August 31, 2011. The loan portfolio is broken into two segments:

• Legacy portfolio: expected loan repayment before August 31, 2011 • Active portfolio: expected loan repayment after August 31, 2011

Financial Modeling

The key findings of the above analyses were used to create a financial model to project Rickshaw Bank’s future financial performance and funding needs under different scenarios. The model was based on the following assumptions:

• The last three years’ Rickshaw Puller Data and Financial Data provided by Rickshaw Bank is accurate and complete

• There is sufficient demand for lease-to-own rickshaws in the future • There are no manufacturing capacity constraints as long as additional funding and workers are

available • Prices of inputs are largely constant, growing only at the rate of inflation in India • Expenses on Rickshaw Bank’s cash flow statements represent an accurate relationship between

expenses and revenue; hence an average of the last three years’ relationship is a good assumption for the status quo scenario for future projections

A more detailed description of the model methodology is attached in the Appendix (Exhibit 2).

Benchmarking rickshaw bank’s collection process against other MFIs

We compared Rickshaw Bank’s collection process with 70 similarly sized Indian microfinance institutions. While RB is not an MFI, its lending and collection operations closely resemble MFIs in India and provide a suitable benchmark. In selecting comparable MFIs, we only included those with individual lending practices.

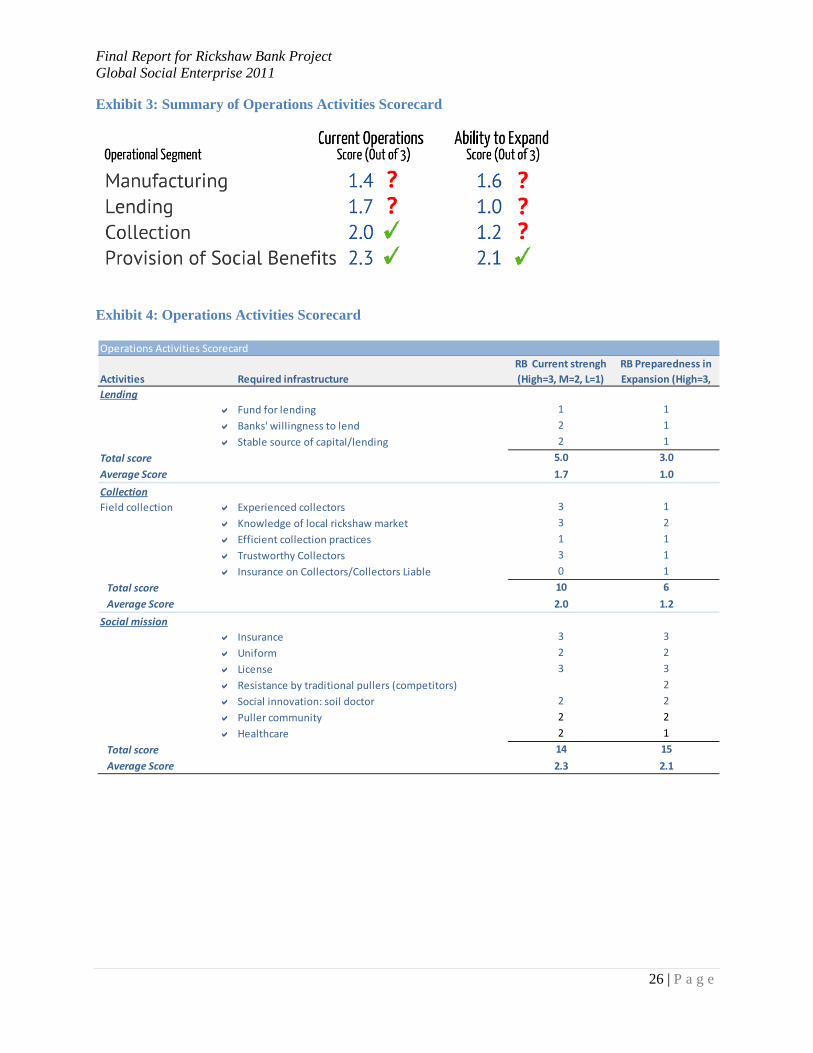

Operations Activities Scorecard

The Team used a self-reported scoring system to help Rickshaw Bank determine the strengths and weaknesses of its operations currently as well as in an expansion scenario. A list of key infrastructure

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

11 | P a g e

were identified for each important business activity at Rickshaw Bank and senior management gave a score for each infrastructure item on a scale of 1 to 3 (3 being the highest). An average of the total score was taken to determine the strength of the four main business activities: manufacturing, lending, collection and social security measures.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

12 | P a g e

Research Findings

Expansion

Based on the self-evaluation done by Rickshaw Bank’s key staff members, we assessed the organization’s key business activities. With the exception of social benefit-related activities, Rickshaw Bank’s leadership believes it needs to improve most of its core business activities in order to be ready for expansion (Exhibit 3 and 4).

For the purpose of the project, we focused on lending and collection process as they have the most significant impact on Rickshaw Bank’s profitability.

Financial Clarity

1. Profitability

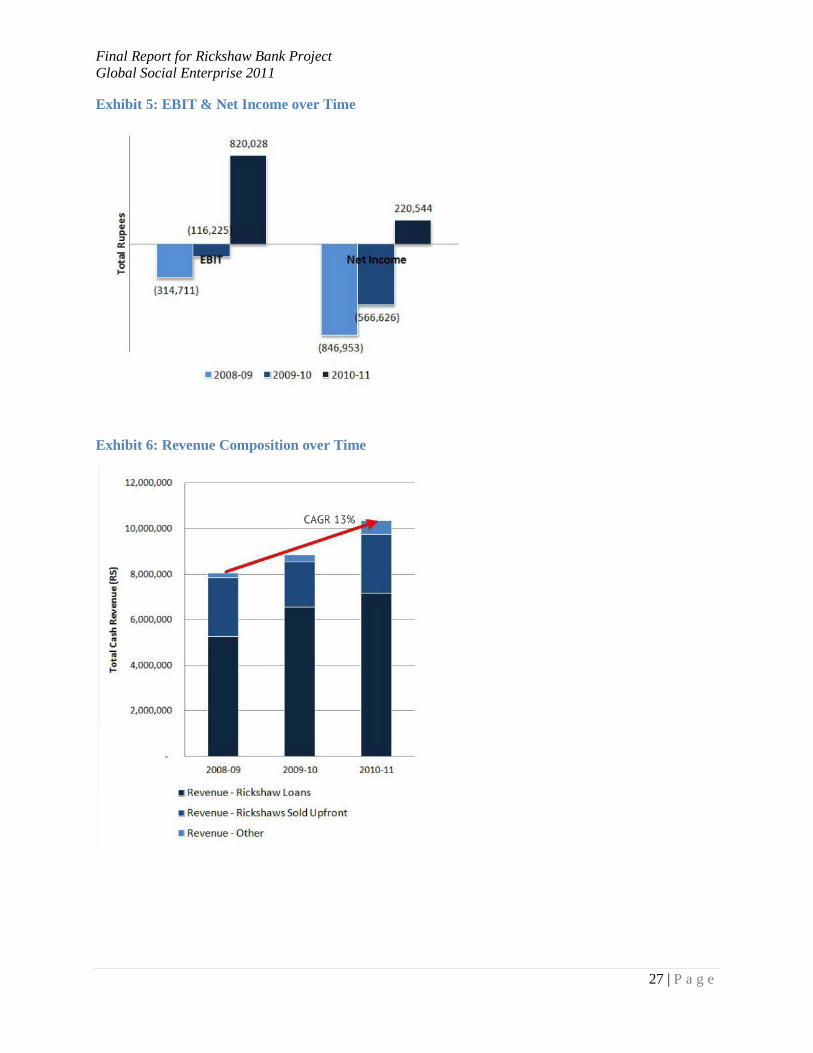

Based on the analysis of Rickshaw Bank’s historical financials, we found that their financial position has improved over the past three years. Revenue has grown by 13% since FY 2008, net income became positive in 2010, gross profit margin improved from 11% to 13% over the past three years, and production cost as a percentage of revenue decreased by 10%. The growth is largely due to increased rickshaw issuance (including upfront sales). Upfront rickshaw sales grew at around 30% during the last year while traditional rickshaw loan sales group by around 6%. The aforementioned margin improvements were the result of the growth in the lower cost (lower selling, general, and administrative costs) upfront rickshaw sales, thus explaining the decline in production costs as a percentage of total revenues. With total rickshaw loan and upfront sales growing faster than raw material and selling/general costs, profitability margins improved during the period (Exhibit 5, 6 and 7).

2. Ownership Issue

We observed that a significant portion of the organization’s revenue comes from the upfront sales of rickshaws and other carts. In 2010 alone, upfront sales accounted for 27% of total revenue, which is a 30% increase from the previous year. While this helps improve profitability, given that it does not require loan collections, Rickshaw Bank risks diverting too much of its limited funding and resources to business activities that are not closely aligned with its social mission. Rickshaw Bank’s goal is to offer asset ownership to pullers who are traditionally unable to own rickshaws. However, the upfront sales inevitably require the organization to serve an entirely different set of client – pullers that are already able to purchase the rickshaws. Such trend is further supported by the pullers’ data for Guwahati branch. Out of the 1,105 rickshaws issued in Guwahati between 2008 and 2010, only 70% of the rickshaws are issued to unique pullers. A number of pullers own more than one rickshaw; some purchased as many as six rickshaws from Rickshaw Bank. Therefore, we suggest that Rickshaw Bank should improve profitability from its regular rickshaw leasing program so as to reduce its reliance on upfront sales.

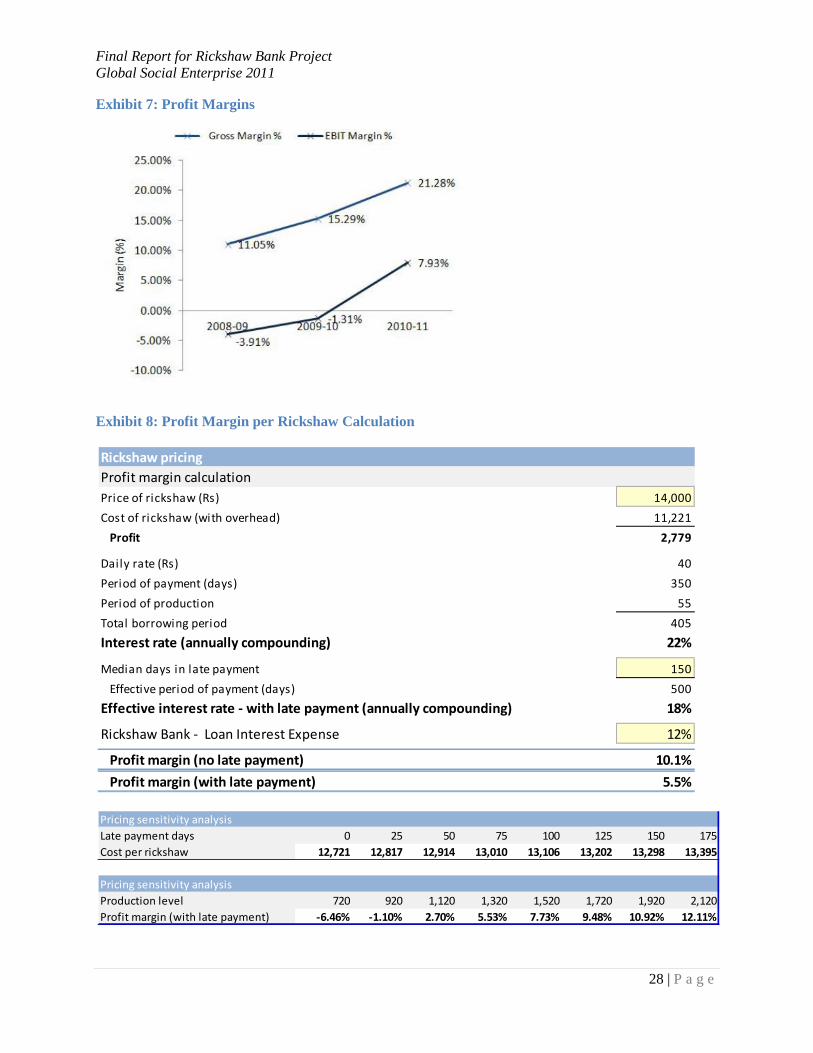

3. Profit Margin per Rickshaw

Based on the price and cost of rickshaws in Fiscal Year 2011, the implied profit margin per rickshaw is 10.1%. However, this rate is not indicative of Rickshaw Banks’ actual profitability as the actual profit earned is negatively impacted by late payments and production level. When pullers take longer to pay loans back, Rickshaw Bank has to pay more interest on loans from Punjab National Bank, therefore driving up the cost of capital. If Rickshaw Bank factors in 150 average days of late payments per puller,

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

13 | P a g e

the profit margin adjusts downward to 5.5%. This profit margin per rickshaw may further decrease to as much as -6.5% if Rickshaw Bank were to drop annual production level to 720 rickshaws.

10.1% profit margin per rickshaw that the organization charges is reasonable, but Rickshaw Bank needs to be aware that this ratio is highly sensitive to late repayment and production level. (Exhibit 8)

Inefficiency in Collection and Repayment Process

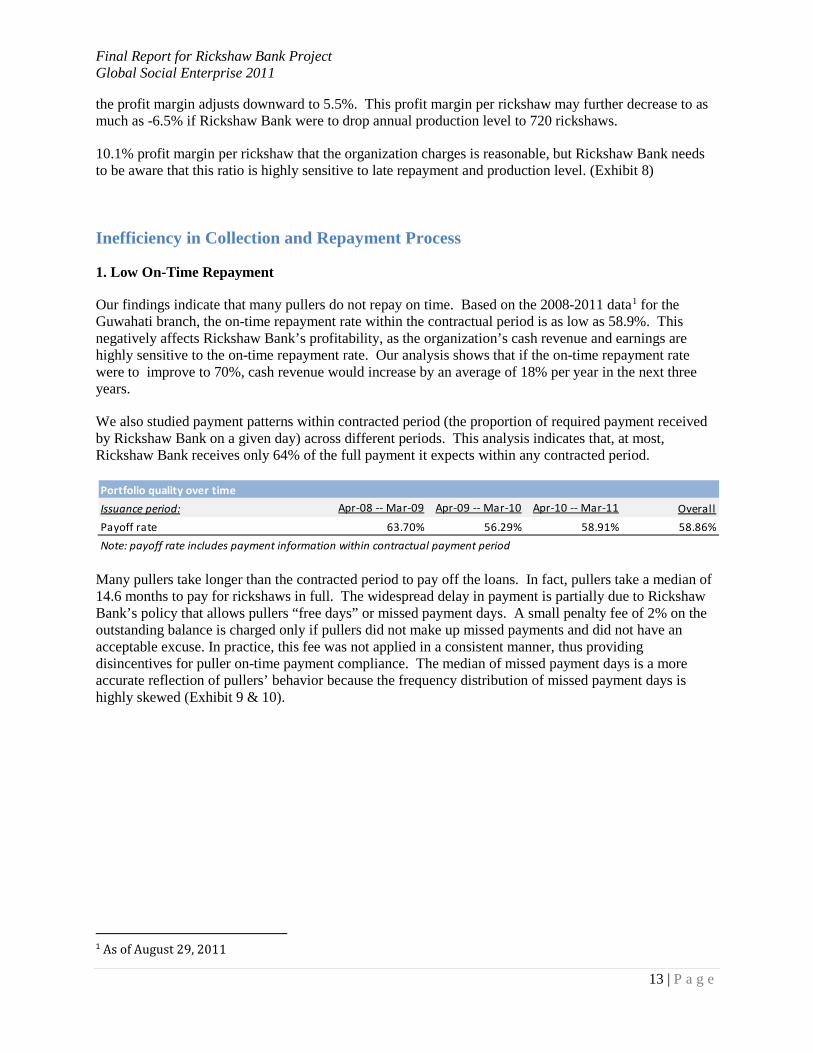

1. Low On-Time Repayment

Our findings indicate that many pullers do not repay on time. Based on the 2008-2011 data1 for the Guwahati branch, the on-time repayment rate within the contractual period is as low as 58.9%. This negatively affects Rickshaw Bank’s profitability, as the organization’s cash revenue and earnings are highly sensitive to the on-time repayment rate. Our analysis shows that if the on-time repayment rate were to improve to 70%, cash revenue would increase by an average of 18% per year in the next three years.

We also studied payment patterns within contracted period (the proportion of required payment received by Rickshaw Bank on a given day) across different periods. This analysis indicates that, at most, Rickshaw Bank receives only 64% of the full payment it expects within any contracted period.

Many pullers take longer than the contracted period to pay off the loans. In fact, pullers take a median of 14.6 months to pay for rickshaws in full. The widespread delay in payment is partially due to Rickshaw Bank’s policy that allows pullers “free days” or missed payment days. A small penalty fee of 2% on the outstanding balance is charged only if pullers did not make up missed payments and did not have an acceptable excuse. In practice, this fee was not applied in a consistent manner, thus providing disincentives for puller on-time payment compliance. The median of missed payment days is a more accurate reflection of pullers’ behavior because the frequency distribution of missed payment days is highly skewed (Exhibit 9 & 10).

1 As of August 29, 2011

Portfolio quality over timeIssuance period: Apr-08 -- Mar-09 Apr-09 -- Mar-10 Apr-10 -- Mar-11 OverallPayoff rate 63.70% 56.29% 58.91% 58.86%Note: payoff rate includes payment information within contractual payment period

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

14 | P a g e

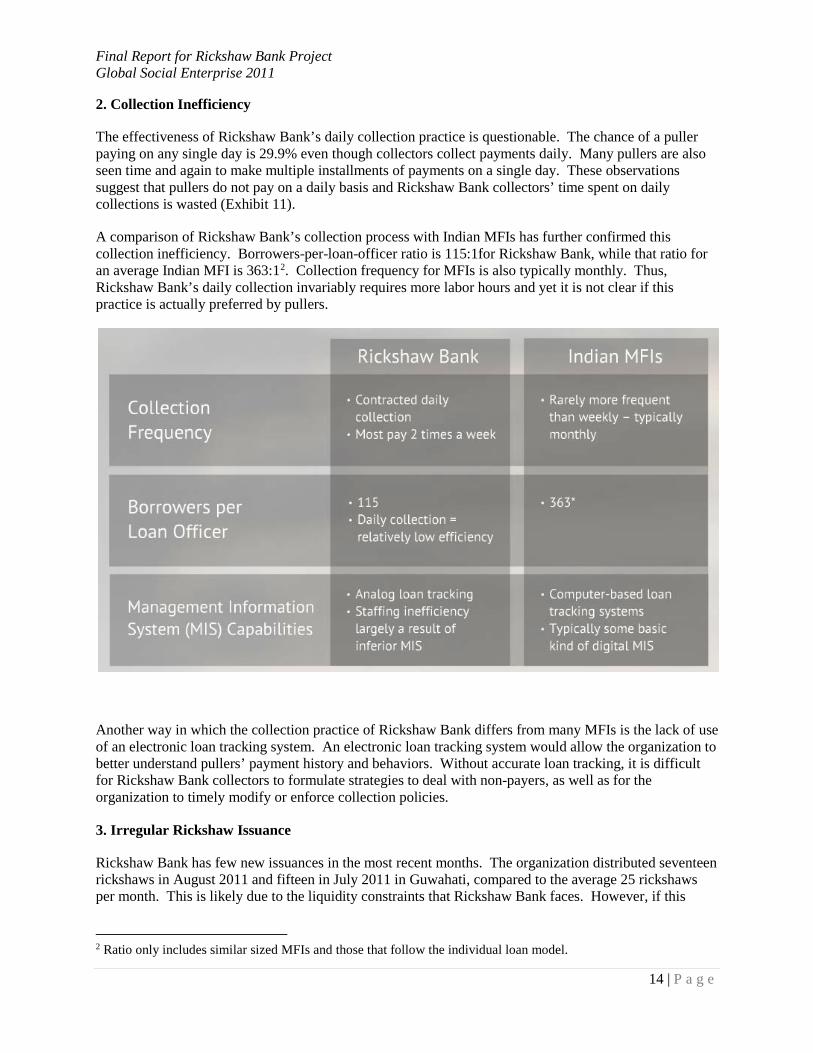

2. Collection Inefficiency

The effectiveness of Rickshaw Bank’s daily collection practice is questionable. The chance of a puller paying on any single day is 29.9% even though collectors collect payments daily. Many pullers are also seen time and again to make multiple installments of payments on a single day. These observations suggest that pullers do not pay on a daily basis and Rickshaw Bank collectors’ time spent on daily collections is wasted (Exhibit 11).

A comparison of Rickshaw Bank’s collection process with Indian MFIs has further confirmed this collection inefficiency. Borrowers-per-loan-officer ratio is 115:1for Rickshaw Bank, while that ratio for an average Indian MFI is 363:12. Collection frequency for MFIs is also typically monthly. Thus, Rickshaw Bank’s daily collection invariably requires more labor hours and yet it is not clear if this practice is actually preferred by pullers.

Another way in which the collection practice of Rickshaw Bank differs from many MFIs is the lack of use of an electronic loan tracking system. An electronic loan tracking system would allow the organization to better understand pullers’ payment history and behaviors. Without accurate loan tracking, it is difficult for Rickshaw Bank collectors to formulate strategies to deal with non-payers, as well as for the organization to timely modify or enforce collection policies.

3. Irregular Rickshaw Issuance

Rickshaw Bank has few new issuances in the most recent months. The organization distributed seventeen rickshaws in August 2011 and fifteen in July 2011 in Guwahati, compared to the average 25 rickshaws per month. This is likely due to the liquidity constraints that Rickshaw Bank faces. However, if this

2 Ratio only includes similar sized MFIs and those that follow the individual loan model.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

15 | P a g e

trend continues, Rickshaw Bank’s revenue from daily collection may significantly decline in the near future with a decreasing number of new clients.

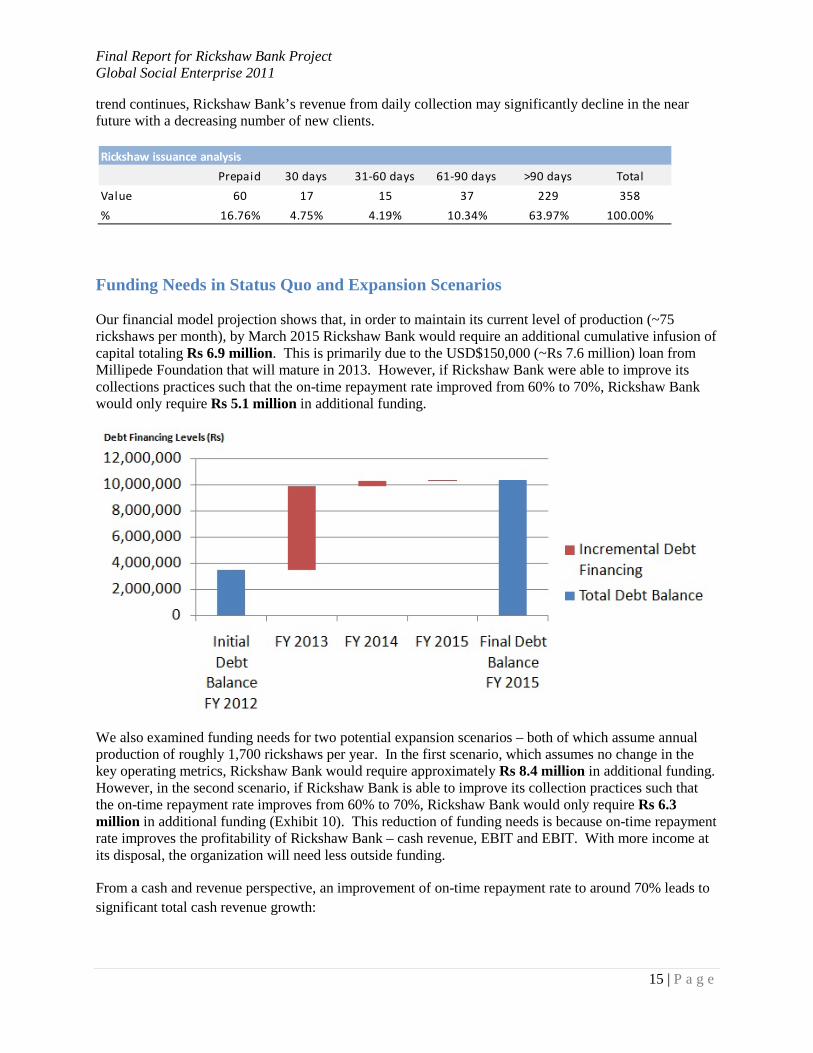

Funding Needs in Status Quo and Expansion Scenarios Our financial model projection shows that, in order to maintain its current level of production (~75 rickshaws per month), by March 2015 Rickshaw Bank would require an additional cumulative infusion of capital totaling Rs 6.9 million. This is primarily due to the USD$150,000 (~Rs 7.6 million) loan from Millipede Foundation that will mature in 2013. However, if Rickshaw Bank were able to improve its collections practices such that the on-time repayment rate improved from 60% to 70%, Rickshaw Bank would only require Rs 5.1 million in additional funding.

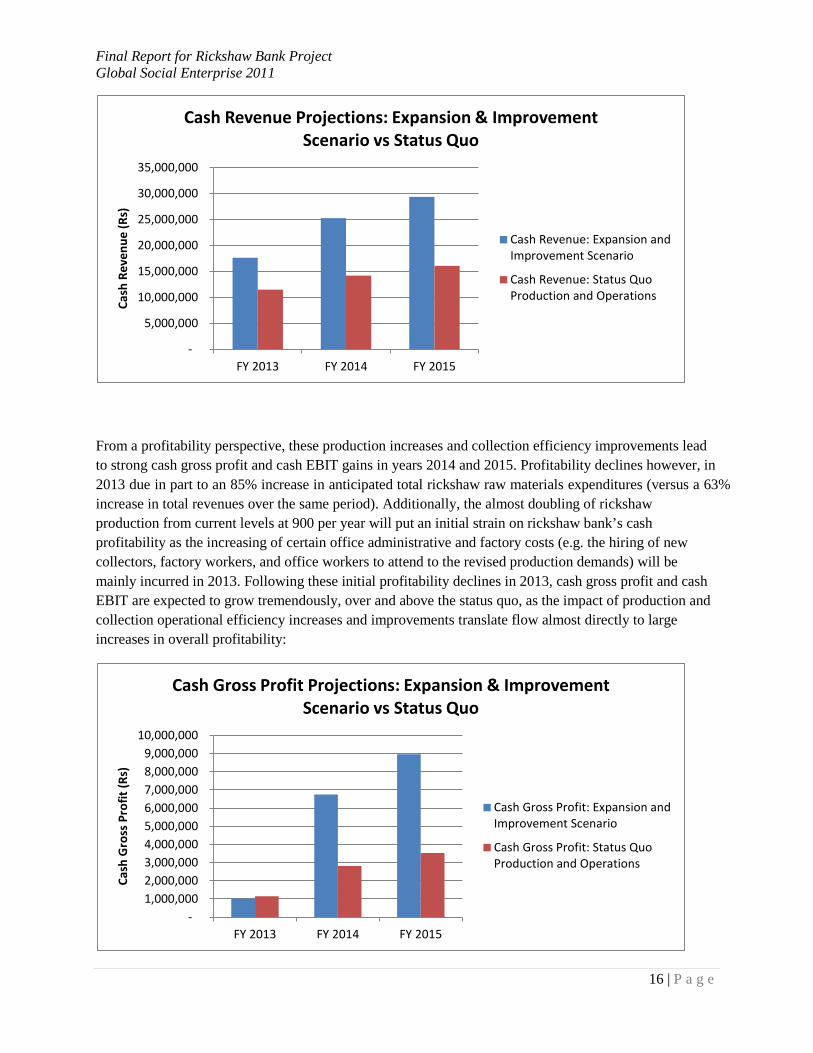

We also examined funding needs for two potential expansion scenarios – both of which assume annual production of roughly 1,700 rickshaws per year. In the first scenario, which assumes no change in the key operating metrics, Rickshaw Bank would require approximately Rs 8.4 million in additional funding. However, in the second scenario, if Rickshaw Bank is able to improve its collection practices such that the on-time repayment rate improves from 60% to 70%, Rickshaw Bank would only require Rs 6.3 million in additional funding (Exhibit 10). This reduction of funding needs is because on-time repayment rate improves the profitability of Rickshaw Bank – cash revenue, EBIT and EBIT. With more income at its disposal, the organization will need less outside funding.

From a cash and revenue perspective, an improvement of on-time repayment rate to around 70% leads to significant total cash revenue growth:

Rickshaw issuance analysisPrepaid 30 days 31-60 days 61-90 days >90 days Total

Value 60 17 15 37 229 358% 16.76% 4.75% 4.19% 10.34% 63.97% 100.00%

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

16 | P a g e

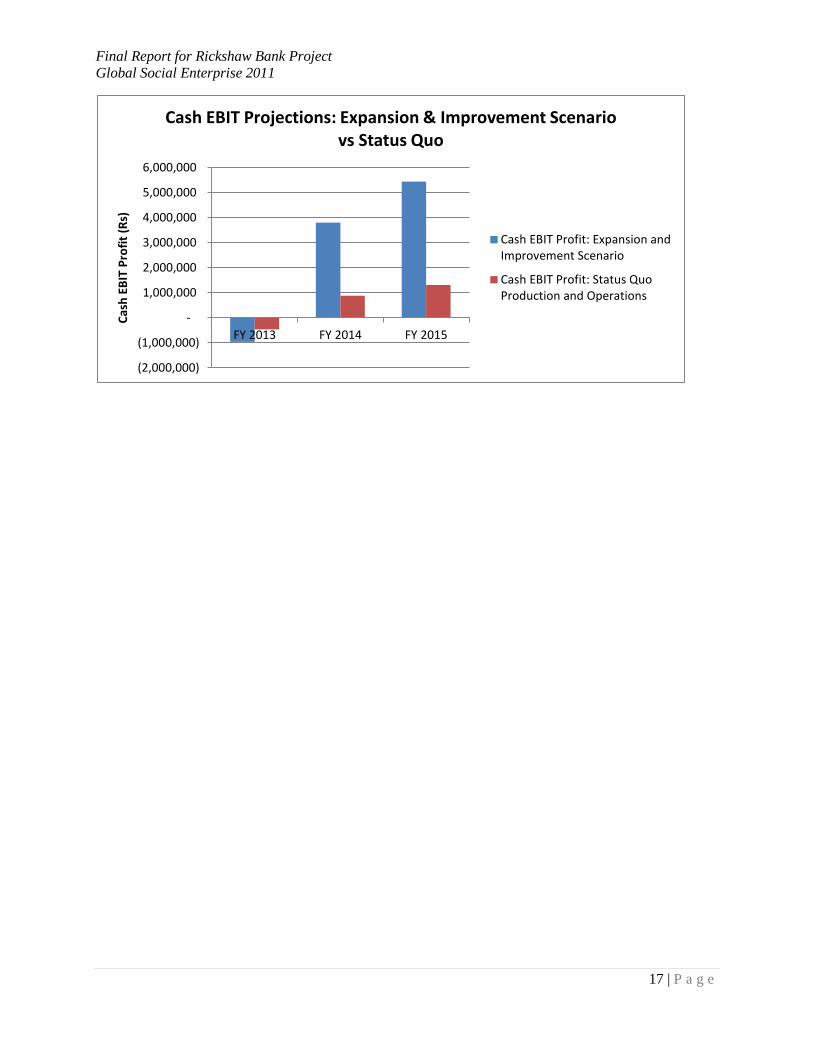

From a profitability perspective, these production increases and collection efficiency improvements lead to strong cash gross profit and cash EBIT gains in years 2014 and 2015. Profitability declines however, in 2013 due in part to an 85% increase in anticipated total rickshaw raw materials expenditures (versus a 63% increase in total revenues over the same period). Additionally, the almost doubling of rickshaw production from current levels at 900 per year will put an initial strain on rickshaw bank’s cash profitability as the increasing of certain office administrative and factory costs (e.g. the hiring of new collectors, factory workers, and office workers to attend to the revised production demands) will be mainly incurred in 2013. Following these initial profitability declines in 2013, cash gross profit and cash EBIT are expected to grow tremendously, over and above the status quo, as the impact of production and collection operational efficiency increases and improvements translate flow almost directly to large increases in overall profitability:

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

FY 2013 FY 2014 FY 2015

Cash

Rev

enue

(Rs)

Cash Revenue Projections: Expansion & Improvement Scenario vs Status Quo

Cash Revenue: Expansion andImprovement Scenario

Cash Revenue: Status QuoProduction and Operations

- 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000 7,000,000 8,000,000 9,000,000

10,000,000

FY 2013 FY 2014 FY 2015

Cash

Gro

ss P

rofit

(Rs)

Cash Gross Profit Projections: Expansion & Improvement Scenario vs Status Quo

Cash Gross Profit: Expansion andImprovement Scenario

Cash Gross Profit: Status QuoProduction and Operations

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

17 | P a g e

(2,000,000)

(1,000,000)

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

FY 2013 FY 2014 FY 2015

Cash

EBI

T Pr

ofit

(Rs)

Cash EBIT Projections: Expansion & Improvement Scenario vs Status Quo

Cash EBIT Profit: Expansion andImprovement Scenario

Cash EBIT Profit: Status QuoProduction and Operations

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

18 | P a g e

Recommendations

To address the challenges faced by Rickshaw Bank, the GSE team made four recommendations that are most crucial for the Rickshaw Bank.

1. Adopting Weekly Collection Schedule

The current daily collection requires a large amount of time and effort from collectors. The benefit of the frequent collection schedule is also not clear, as the on-time payment rate is low. We recommend that Rickshaw Bank reduce the collection frequency to weekly, given that pullers make multiple payments at a time and often do not pay on all collection days. These observations suggest that weekly collection would require less personnel effort and align more closely with pullers’ payment behavior. From the cost side of things, a movement from daily to weekly collections could potentially lead to an 83% cost savings from collector salaries.

2. Adopting Electronic Loan Tracking System

Rickshaw Bank currently uses paper forms to record loan payment information. This is time consuming and limits the organization’s ability to analyze repayment information. An electronic loan tracking system would allow the collectors to track each puller’s payment pattern. This will help collectors to easily examine each puller’s payment history, and have stricter enforcement on pullers that have not been paying on time. The organization as a whole will also benefit from having a clear understanding of measures that are essential to assess the organization’s performance, such as loan repayment rates. Rickshaw Bank will also be able to adjust or enforce collection policies in a timely manner to improve collection. A number of suitable systems are available on the market – many at little or no cost. An Excel-based spreadsheet, assuming it is updated regularly, may also be sufficient.

To effectively evaluate the proper system to acquire, Rickshaw Bank should consider the following characteristics:

• Cost • Functionality • Scalability • Level of Sophistication

Indian microfinance institutions require similar functionality and face similar constraints, and thus, the systems available to them will likely be the most useful to Rickshaw Bank. Cost

The cost of an electronic system ranges from free (Excel-based and open-source systems) to hundreds of thousands of dollars (full featured and customized systems). Given Rickshaw Bank’s current lack of readily available funding, it will need to look for a system near the lower end of the cost spectrum. Functionality

There is a large range available to the Rickshaw Bank when it comes to the functionality that an electronic system can provide. The most basic systems will do no more than tracking payer data based on the manual inputs of employees with no integration to the accounting system. Alternatively, the top of the line systems are completely automated with full integration that includes accounting system. Rickshaw Bank’s accounting software –Tally, is more than sufficient and thus does not require inclusion

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

19 | P a g e

into the electronic system it acquires. Again, the organization should look for a system near the lower end of the functionality spectrum. Scalability

A prime consideration when selecting an electronic system will be its ability to expand in scale and scope with the expected growth of the organization. For example, an Excel-based system, while better than today’s paper system, may soon be outdated and actually hinder future growth as the number of active clients increases. On the other hand, a full electronic system, while more expensive, may be better suited to grow alongside the Rickshaw Bank. Level of Sophistication

Large MFIs and other financial institutions employ large teams of IT professionals dedicated to the installation and management of the company’s electronic systems. Rickshaw Bank does not currently have the luxury of employing individuals with this skill set. With that in mind, it must acquire a system with a relatively low level of sophistication and potentially low-cost external assistance from the manufacturer. In sum, Rickshaw Bank should acquire an inexpensive, relatively low functioning, expandable, and relatively unsophisticated system. This combination of characteristics may be rare in the MFI software world, but one system stands out as a distinct possibility for Rickshaw Bank. Mifos, developed by the Grameen Bank, is a free and open source software package that was specifically designed for institutions, such as Rickshaw Bank, that lacked the necessary capital required to purchase a ‘real’ electronic system. We recommend that Rickshaw Bank contact the Mifos team at Grameen to begin exploring the feasibility of installing the software at the main Guwahati office. Alternatively, as expressed at the recent conference in Mumbai, ZMQ has offered to outfit Rickshaw Bank with its own proprietary MFI electronic tracking software. Rickshaw Bank would be well served to follow up on this offer and explore the feasibility of implementation.

3. Redefining and Enforcing Collection Policies

We believe that Rickshaw Bank needs to redefine its “free payment day” and “late payment” policies to achieve higher on-time repayment rate. Although “free payment day” policy relieves the financial burden of pullers with genuine needs, such policy opens the floodgates to other pullers who are simply not paying. The 2% late payment fee (equivalent to less than 1 rupee per day) seems insufficient to deter late payment. An appropriate limit of maximum free payment days should be set for all pullers and late payment fee needs to be increased. We suggest Rickshaw Bank to set its late payment fee to 12%, which is the same rate that the organization pays for its loan from Punjab National Bank. This will encourage pullers to pay and at the same time cover the organization additional finance.ng cost due to late payment.

Rickshaw Bank will also need to enforce its collection policies more strictly. As evidenced by the payment data from Guwahati Branch, some pullers who have had their rickshaws issued in 2008 still have not paid back in full. Collection targets can be set for all collectors to achieve stricter enforcement of collection policies.

As Rickshaw Bank seeks to improve collections, it should consider training and incentives for both collectors and pullers:

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

20 | P a g e

Collector Training

Rickshaw Bank should evaluate how it trains and motivates collectors to adhere to policies. Case studies of Asian MFIs that have similar collection processes to Rickshaw Bank highlight the importance of investing resources and time in training and aligning incentives for collectors.3 Possible strategies include:

• Rickshaw Bank can provide training for collectors on how to enforce policies: when pullers have proper excuses for missed payments, and when pullers should pay late fees. Training can serve two purposes: 1) it will empower collectors to do their jobs better; and 2) it will further educate collectors on the population they serve and intrinsically motivate them to dedicate themselves to their work.

• Rickshaw Bank should also determine whether collector salaries are high enough to motivate them to work hard to enforce policies.

• Rickshaw Bank could consider the merits of performance pay. Financial rewards for on-time collections daily, weekly or monthly may encourage dishonestly or harsh enforcement, so a better measure of performance could be the number of pullers who attain ownership under a collector. It could give bonuses to collectors who demonstrated their ability to support pullers to pay loans back in full and in a reasonable period of time.

Puller Training

When Rickshaw Bank issues a loan, pullers are required to attend a short training. Rickshaw Bank should invest more in this initial training to ensure borrowers understand the requirements of their loan and expectations for payment. Rickshaw Bank already has some positive incentives in place, such as access to non-rickshaw loans. It should consider other ways to reward pullers for on-time repayment. While the rickshaw itself serves as collateral to miss payments, Rickshaw Bank can also use some of the following strategies to align incentives:

• Stronger supervision by collectors or regular reminders about loan terms

• Require character references from village headmen to deter pullers from paying late

• Require pullers who intend to buy second rickshaw to achieve a certain on-time repayment rate while paying off their first rickshaw

• Reserve the right to take a rickshaw back if a puller does not pay for a certain period of days

4. Developing Financial Monitoring and Budgeting Process

The GSE team has developed a financial model, which should be used by the Rickshaw Bank management team as a planning tool for both internal budgeting and external funding needs. The primary purpose of the model is to illustrate the profitability, cash flow, and required external funding for a targeted level of annual production under a series of operational scenario assumptions. The model should 3 Hulme, David, and Paul Mosley. "The Management of Financial Institutions for the Poor."Finance against Poverty. London: Routledge, 1996. 157-79. Print.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

21 | P a g e

be used to gain a better understanding of the funding needs of the organization. As the knowledge of one’s current financial status as well as projected financial viability is a prerequisite for raising additional stable capital financing, the model may be used as a tool to prepare the rickshaw bank for anticipated profitability and expansion financing questions from potential funding partners. Hitherto, the Rickshaw Bank has had difficulties in quantitatively articulating its current financial status and future expansionary vision to potential funding partners. The financial model will aid them in lifting this veil of quantitative uncertainty. Additionally, the model will help the management team estimate the effects of various operational changes on the organization’s profitability and ultimate viability.

For Rickshaw Bank to be able to keep track of its financial status, it is important to create an accounting book for Rickshaw Bank, independent of the CRD. As of now, Rickshaw Bank’s financial data is not separated from CRD. This makes analyzing the performance of the rickshaw operation difficult. Therefore, we recommend that the Rickshaw Bank takes the following steps:

• Create monthly statements that include the revenues, expenses and interest related to Rickshaw Bank activities only

• Allocate shared overhead costs (between Rickshaw Bank and other CRD projects) on the basis of percentage of time spent on Rickshaw Bank activities

• Compare actual performance to projections in the financial model and analyze the variances

Conclusions

The impact of Rickshaw Bank’s work on many rickshaw pullers’ lives is clearly significant. Although the organization has a financially viable business model, it is yet to achieve its full potential due to issues such as low on-time repayment rate. Should Rickshaw Bank make concrete steps to improve operational efficiency, we believe that the organization will be positioned to apply for additional funding for future expansion, and to reach more underserved rickshaw pullers in Assam and beyond.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

22 | P a g e

Appendix

Exhibit 1: Application Process Flow Chart and Possible Improvement

1. Advertise to find pullers if waitlists wane

2. Make the application and contract separate so pullers sign the contract after training

3. Ensure guarantor's ability to pay

4. Install stricter requirements for application acceptance to guard against default

Possible Improvements

RB asks puller to submit required

aplication documents

The collector delivers rickshaw, ID card, passbook,

registration, license, and uniform to the puller within

15 days of address verification

Collector verifies residency address

Reapply

RB provides short training to the puller

Paperwork complete?

Application

Yes

No

Puller makes 800 rs. security deposit

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

23 | P a g e

Exhibit 2: Detailed Financial Model Methodology The construction and analysis of a forward looking financial and operational model serves as an important valued added contribution of this project. Rickshaw Bank has struggled with not only developing a meaningful understanding of its own financial health and operational efficiency, but more importantly, planning for future growth and development. Now, with a robust and comprehensive financial and operational scenario model, the Rickshaw Bank has a tool that will aid efforts to shape their future as they seek to catalyze a new positive economic and social paradigm in the lives of improvised and maligned bicycle rickshaw pullers across Assam and beyond. The construction of this model followed a basic “bottom-up” approach, with structure and assumptions a derivative of existing Rickshaw Bank accounting statements, puller collection practices and data, and operational policies and procedures. Through close collaboration with the Rickshaw Bank, including their accountant, branch manager, board members and founder, Dr. Pradip Sarmah, the Yale team was able to coalesce around some basic structural and operational frameworks and assumptions that would serve as a basis for modeling Rickshaw Bank operational and financial performance over a 36 month future time horizon. Structurally, the model presented herein begins on the model outline pages where the model structure is visually articulated to the user. On this page, the various scenarios constructed within are explained and summarized, and the user as the option to use a “toggle switch” to “run” a particular scenario. On the various scenario case input pages, revenue and expense drivers sit alongside business operations drivers (e.g. number of pullers per collector, factory and office staff counts, etc.). Most importantly, each scenario pages provides monthly inputs for new rickshaws to be issued. The user has the opportunity to change any scenario inputs, but with the explicit understanding that many inputs are derived off of historical operational and financial relationships, to be kept constant ad infinitum. The aforementioned comprehensive analysis of rickshaw puller collection data was instrumental in the understanding of broader rickshaw bank collection processes (for use in the construction and modeling of future business operations) and more importantly, the establishment of scenario revenue and business operations drivers. Such inputs as monthly estimated “lease-to-own” percentage rates of the existing cohorts of pullers serve to guide scenario inputs surrounding similar percentage rates for the expected future cohorts of pullers. The data analysis provided additional insight into the development of scenario inputs for current cohort and future anticipated cohort puller monthly payment rates. Lastly, conclusions drawn from the puller collection data analysis aided in the understanding of puller collection operations (structure and patterns of collection). This basic understanding was incorporated into the business operations structure of the model, concurrently driving revenue, expense, bank loan, and cash flow projections within the model as well as business operations projections (e.g. puller ownership figures in the future, new collectors to be potentially hired to account for growth in the puller population, etc.). Information and conclusions gathered from the aforementioned historical financial analysis guided basic model assumptions surrounding such inputs as factory electricity expenditures as a % of revenue. We derived and utilized averages of such historical relationships between expenses and revenues to develop a status quo financial structure for the model, allowing us to model Rickshaw Bank expenses 36 months into the future. Through conversations with Rickshaw Bank employees, additional inputs such as rickshaw materials costs were derived. These original inputs within the scenarios are to be kept largely constant and expected to grow at an annualized rate of inflation that may be adjusted on the scenario pages as inflation rates in India adjust in the future.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

24 | P a g e

By toggling an individual scenario on the model outline page, the model automatically references the applicable scenario inputs, many of which flow directly into the business operations section of the model. The business operations section projects future puller numbers, existing puller ownership “graduations,” collector counts, factory employee counts (to increase depending on rickshaw production targets), etc. In essence, the business operations page is a representation of the inner operation processes and workings of the Rickshaw Bank, quantified and projected monthly for 36 months. It should be duly noted that the model (and specifically the business operations page) assumes no manufacturing capacity constraints. We exhaustively debated this simplification with our Yale and Morgan Stanley advisors, but came to the conclusion that it would have been incumbent upon us to conduct a time consuming operational study of all rickshaw bank manufacturing processes. Given the resource constraints of this project, this was not possible, as such, within this financial and operational model, it can be assumed that the Rickshaw Bank can produce an unlimited number of rickshaws each month, resulting only in increased hiring of factory, office, and collector employees as well as the need for increased bank financing. The model does not account for the efficiencies surrounding economies of scale (e.g. increased factory worker efficiency) arising with increased rickshaw production levels nor does it factor electricity, physical space, raw materials supply and manufacturing tools constraints within the current Rickshaw Bank manufacturing process. The user must take note of these limitations when revising scenario projections surrounding future rickshaw production. The model processes occurring within the business operations tab along with the applicable revenue and expense scenario inputs serve to project future revenues and expenses under the various scenarios. Under the revenue build up page in particular, the price (charged to pullers) of a rickshaw is calculated as a function of scenario expectations on % profit margin for Rickshaw Bank as well as accounting for the direct materials and labor costs of producing a rickshaw. The derived rickshaw price each month is expected to either remain flat or increase as materials and labor costs rise over time. Using this derived price as well as scenario input assumptions of total installment length as number of installment payments per month, contracted, effective and actual interest rates charged to pullers is calculated on a monthly basis moving forward. Loan payments (revenue) for the various cohorts of existing and anticipated new pullers are then calculated and modeled on a monthly basis. The expense page utilizes scenario expense inputs in the areas of raw materials, office salaries, etc. These expenses are typically a function of rickshaw production levels and are, like revenues, projected into the future. The revenue and expense modeled projections impact assumptions surrounding bank loan financing needs under each scenario. The bank loan page articulates and reflects Rickshaw Bank’s current financing/capital structure as well as the additional funding needs prescribed as a result of the various scenario projections surrounding future rickshaw production levels as well as other revenue, expense, and business operations assumptions. The projection of additional financing/funding needs is an important output of this financial model. It represents essentially the financing gap needed to be bridged prior to achieving rickshaw production goals. Lastly, the model utilizes the aforementioned revenue, expense, and bank loan projections to provide for a comprehensive cash sources and uses picture under the chosen scenario. The cash flow page allows to user to clearly visualize where the Rickshaw Bank utilizes cash and where it generates cash, breaking out cash generated from operations versus cash generated from bank financing. This page provides valuable insight into the expected health of Rickshaw Bank’s future monthly cash balances. In terms of final model outputs, the user is able to utilize the “dashboard” on the top of each model page in order to see how changes to various assumptions immediately impact particular output metrics. These metrics include the number of new rickshaws produced and delivered, active pullers within the system, loan balances, cash balances, rickshaws transferred to ownership, etc. These economic and operational

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

25 | P a g e

metrics are articulated in greater detail on the economic analysis metrics page as well as in the graphic analyses provided. These are tangible metrics for measuring the performance of Rickshaw Bank under various scenarios. This model is not designed to 100% anticipate or predict the future for Rickshaw Bank, but rather provide a basic view into what could be; what additional bank financing, changes in collection operations, and employee hiring would be needed in order to achieve Dr. Sarmah’s goal of bringing more rapid social and economic change to the bicycle rickshaw puller population of Eastern India.

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

26 | P a g e

Exhibit 3: Summary of Operations Activities Scorecard

Exhibit 4: Operations Activities Scorecard

Operations Activities Scorecard

Activities Required infrastructureRB Current strengh (High=3, M=2, L=1)

RB Preparedness in Expansion (High=3,

Lending Fund for lending 1 1 Banks' willingness to lend 2 1 Stable source of capital/lending 2 1

Total score 5.0 3.0Average Score 1.7 1.0CollectionField collection Experienced collectors 3 1

Knowledge of local rickshaw market 3 2 Efficient collection practices 1 1 Trustworthy Collectors 3 1 Insurance on Collectors/Collectors Liable 0 1

Total score 10 6Average Score 2.0 1.2

Social mission Insurance 3 3 Uniform 2 2 License 3 3 Resistance by traditional pullers (competitors) 2 Social innovation: soil doctor 2 2 Puller community 2 2 Healthcare 2 1

Total score 14 15Average Score 2.3 2.1

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

27 | P a g e

Exhibit 5: EBIT & Net Income over Time

Exhibit 6: Revenue Composition over Time

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

28 | P a g e

Exhibit 7: Profit Margins

Exhibit 8: Profit Margin per Rickshaw Calculation

Rickshaw pricingProfit margin calculationPrice of rickshaw (Rs) 14,000Cost of rickshaw (with overhead) 11,221

Profit 2,779

Daily rate (Rs) 40Period of payment (days) 350Period of production 55Total borrowing period 405Interest rate (annually compounding) 22%

Median days in late payment 150Effective period of payment (days) 500

Effective interest rate - with late payment (annually compounding) 18%

Rickshaw Bank - Loan Interest Expense 12%

Profit margin (no late payment) 10.1%Profit margin (with late payment) 5.5%

Pricing sensitivity analysisLate payment days 0 25 50 75 100 125 150 175Cost per rickshaw 12,721 12,817 12,914 13,010 13,106 13,202 13,298 13,395

Pricing sensitivity analysisProduction level 720 920 1,120 1,320 1,520 1,720 1,920 2,120Profit margin (with late payment) -6.46% -1.10% 2.70% 5.53% 7.73% 9.48% 10.92% 12.11%

Final Report for Rickshaw Bank Project Global Social Enterprise 2011

29 | P a g e

Exhibit 9: Missed Payment Days Study

Exhibit 10: Impact of Repayment Improvement on Funding Needs

Exhibit 11: Payment Frequency Calculation

-40

10

60

110

160

Freq

uenc

y: N

umbe

r of P

ulle

rs

Total Number of Missed Payment Days

Missed Payment Days During Completed Loan Period

Payment FrequencyTotal no. of collection days 384,384Total no. of days with payment collected 59,900% days with payments collected 15.58%Adjustment for Sunday (no collection) 14.29%% days with payments collected (adjusted for Sunday) 29.87%

Related Documents