FEASIBILITY STUDY FOR A PROPOSED HOTEL IN SOUTH LAKE TAHOE, CALIFORNIA A Thesis Presented to the Faculty of California State University, Stanislaus In Partial Fulfillment of the Requirements for the Degree of Master of Business Administration By Caleb Flora October 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FEASIBILITY STUDY FOR A PROPOSED HOTEL IN

SOUTH LAKE TAHOE, CALIFORNIA

A Thesis Presented to the Faculty

of

California State University, Stanislaus

In Partial Fulfillment

of the Requirements for the Degree

of Master of Business Administration

By

Caleb Flora

October 2020

CERTIFICATION OF APPROVAL

FEASIBILITY STUDY FOR A PROPOSED HOTEL IN

SOUTH LAKE TAHOE, CALIFORNIA

by

Caleb Flora

Dr. Yili Lian, Faculty Advisor

Associate Professor of Finance

Ms. Katrina Kidd, Director

Graduate Business Programs

Dr. Tomas Gomez-Arias, Dean

College of Business Administration

Date

Date

Date

Signed Certification of Approval page

is on file with the University Library

© 2020

Caleb Flora

ALL RIGHTS RESERVED

iv

DEDICATION

I wish to dedicate this project to the following people:

My parents, whose love, unselfish support, and example over many years laid

the foundations for the discipline and application necessary to complete this work.

My wife, whose steadfast love, unwavering support, and never-ending

patience has allowed me to dedicate the time necessary to complete this work.

My son, who inspires me every day to strive to be the best version of myself.

v

ACKNOWLEDGEMENTS

This project has become reality with the kind support and help of many

individuals. I would like to extend my sincere appreciation to all of them.

First and foremost, I must acknowledge and thank God for His provisions and

grace in my life and for granting me the opportunity to pursue a graduate degree in

business administration. My goal is to use the knowledge gained in this program, to

be a humble and effective servant leader not only in my professional and business

dealings, but also in my family and my community.

I would like to express my gratitude to my family for their encouragement

which helped me in the completion of this paper and ultimately, this program. My

amazing and supportive wife, who has supported and encouraged me through both

undergraduate studies and now graduate school, is the primary reason I did not give

up when the going got tough. To my son, I love you. News of your addition to our

family was the final push I needed to enroll in graduate school.

I would like to express my sincere gratitude to my advisor, Dr. Yili Lian for

imparting his knowledge and expertise in this study.

My thanks and appreciation also go to my colleagues and others who have

willingly helped out with their abilities throughout this study and throughout the

entirety of the graduate program.

vi

TABLE OF CONTENTS

PAGE

Dedication ............................................................................................................... iv

Acknowledgements ................................................................................................. v

List of Tables .......................................................................................................... viii

List of Figures ......................................................................................................... ix

Abstract ................................................................................................................... x

Introduction ............................................................................................................. 1

Project Scope .............................................................................................. 1

Vision .......................................................................................................... 2

Mission ........................................................................................................ 2

Supply and Demand ................................................................................................ 3

Potential Volume ........................................................................................ 3

Seasonal Attractions.................................................................................... 7

SWOT Analysis .......................................................................................... 10

Market Analysis ...................................................................................................... 11

Competition................................................................................................. 11

Target Market.............................................................................................. 13

Rates ............................................................................................................ 13

Seasonal Occupancy Rates ......................................................................... 16

Pro Forma Financials .............................................................................................. 17

Balance Sheet .............................................................................................. 17

Income Statement........................................................................................ 19

Cash Flow Statement .................................................................................. 21

Initial Investment .................................................................................................... 24

Purchase and Renovate ............................................................................... 24

Ground Up Construction ............................................................................. 27

vii

Financials ................................................................................................................ 28

Breakeven Analysis .................................................................................... 28

Fixed and Variable Costs ............................................................................ 29

Revenue....................................................................................................... 30

Profit Margin ............................................................................................... 31

Valuation ................................................................................................................. 33

Cost to Run ................................................................................................. 33

Net Present Value ....................................................................................... 37

Product Mix ................................................................................................ 40

Conclusion .............................................................................................................. 41

Project Limitations ...................................................................................... 41

Next Steps ................................................................................................... 42

References ............................................................................................................... 44

Appendices

A. South Lake Tahoe TOT Zone Map ............................................................. 47

B. Expanded Balance Sheet ............................................................................. 48

C. Expanded Income Statement....................................................................... 49

D. Expanded Cash Flow Statement ................................................................. 50

viii

LIST OF TABLES

TABLE PAGE

1. Lodging Supply, Demand, and Occupancy Rate for Past 3 Years ................... 4

2. Lodging Revenue, Occupancy, and ADR by Quarter for 2019 ........................ 5

3. Hotel Comp Set Overview (Room Count, Location, and Rating) .................... 11

4. Visitation by City and Demographics of City................................................... 13

5. Occupancy and ADR of Comp Set ................................................................... 14

6. Average Daily Rate Assumptions for the Subject Property.............................. 16

7. Occupancy Assumptions for the Subject Property ........................................... 16

8. Balance Sheet – 5 Year Overview .................................................................... 17

9. Balance Sheet – 2021 to 2025 Detail ................................................................ 17

10. Income Statement – 5 Year Overview .............................................................. 19

11. Income Statement – 2021 to 2025 Detail .......................................................... 20

12. Cash Flow Statement – 5 Year Overview ......................................................... 22

13. Cash Flow Statement – 2021 to 2025 Detail .................................................... 22

14. Guestroom Renovation Cost Breakdown.......................................................... 25

15. Guest Bathroom Renovation Cost Breakdown ................................................. 26

16. Total Renovation Cost Estimate ....................................................................... 27

17. Expenses Year-to-Year Breakdown .................................................................. 29

18. Profit Margin ..................................................................................................... 31

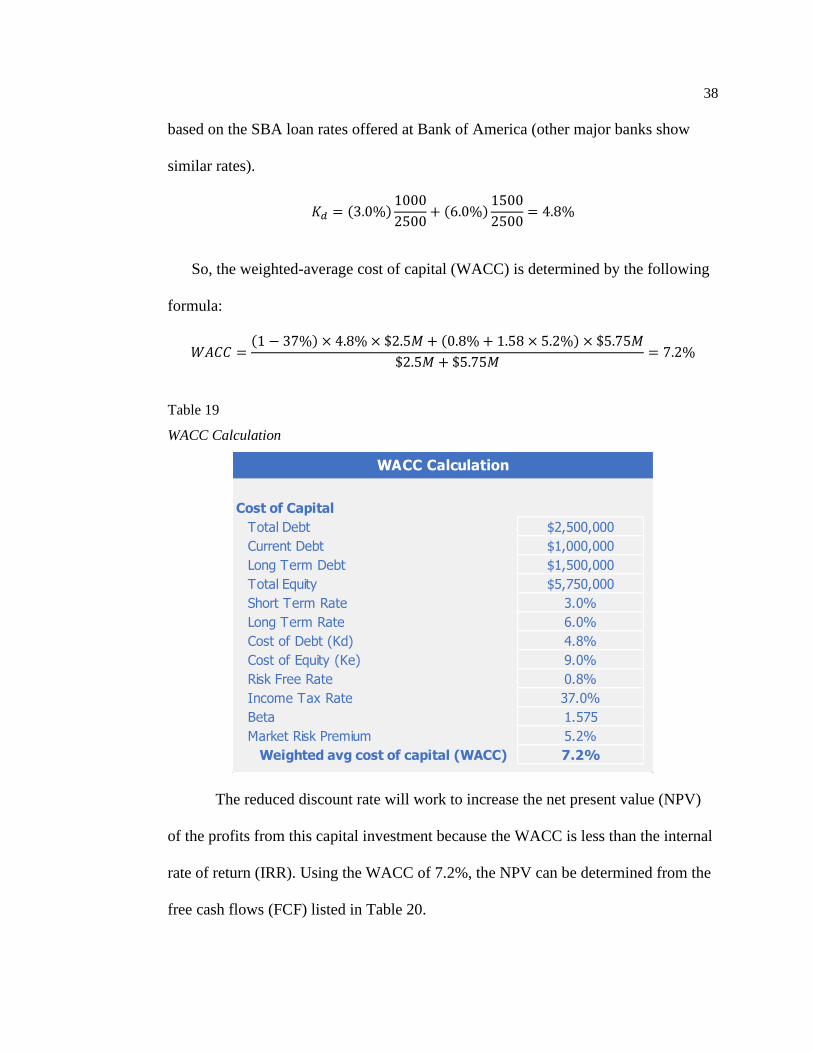

19. WACC Calculation ........................................................................................... 38

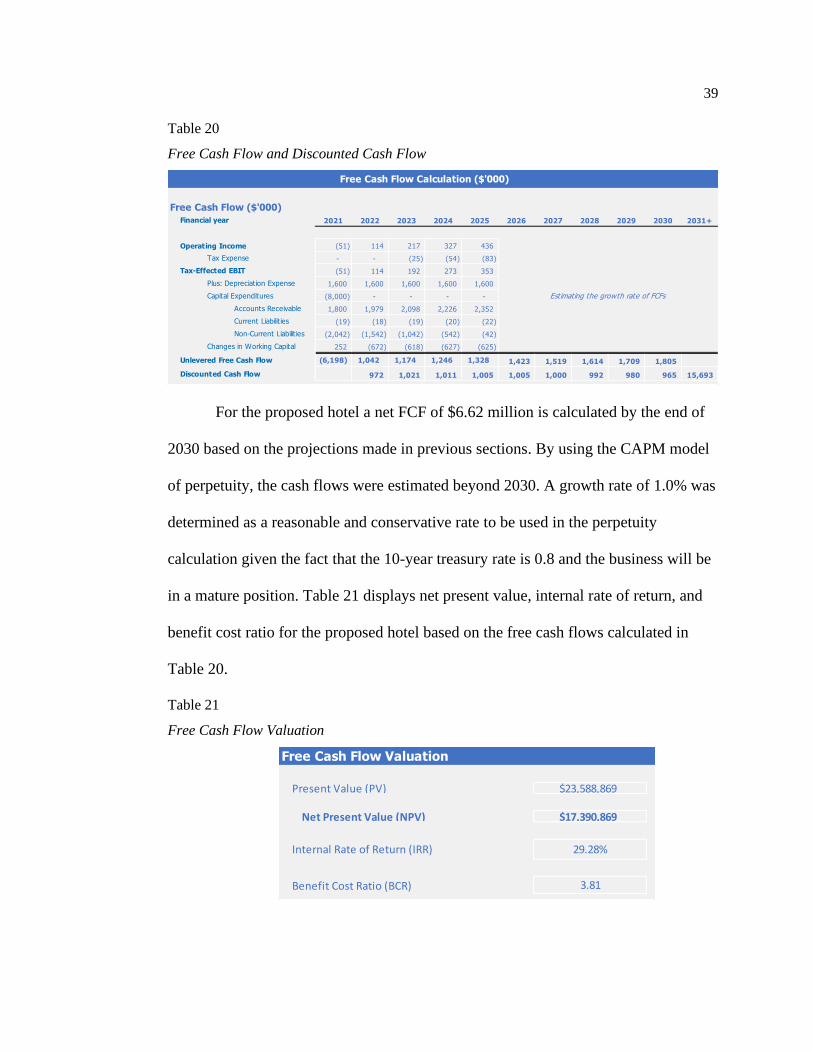

20. Free Cash Flow and Discounted Cash Flow ..................................................... 39

21. Free Cash Flow Valuation ................................................................................ 39

ix

LIST OF FIGURES

FIGURE PAGE

1. Proximity to high population cities. .................................................................. 3

2. Lodging supply and demand. ............................................................................ 5

3. Proposed multi-purpose event center. ............................................................... 6

4. Average temperature and precipitation. ............................................................ 7

5. Access to demand generators. ........................................................................... 8

6. SWOT analysis. ................................................................................................ 10

7. Occupancy and ADR trend. .............................................................................. 15

8. Subject property listing. .................................................................................... 24

9. Break even chart. .............................................................................................. 28

10. Revenue summary. ............................................................................................ 30

11. Top 5 expense categories. ................................................................................. 33

ABSTRACT

The purpose of this paper was to develop and articulate a feasibility study to

purchase and operate a 35 to 65 room hotel in California’s Lake Tahoe area. South

Lake Tahoe is in the midst of a rebirth of new or updated hotels, eateries, and

breweries. Hotels are being renovated to give a modern, elegant feel while

maintaining the history of the buildings and sense of adventure that so many people

visit Tahoe for. The paper begins by reviewing the area of South Lake Tahoe and

hospitality businesses that are currently operating in the area. Past visitation,

surrounding cities and demographics, and nearby attractions are presented as a

foundation for a proposed hotel in the subject city. The framework for the feasibility

analysis is set by reviewing past occupancy rates and average daily rates statistics for

the South Lake Tahoe area and then projecting these figures into the future for a

proposed hotel. Furthermore, expenses are estimated to complete proforma financial

statements in order to paint a picture of what revenues, expenses, profitability are

expected to be year to year and even month to month. A very rough estimation is

made to purchase and renovate an existing hotel property. Finally, a conclusion is

made on the feasibility of the proposed hotel and next steps, should the project be

pursued further.

x

1

INTRODUCTION

Project Scope

The goal of this project is to conduct, formulate, and then concisely present, a

feasibility study to acquire and operate a full service, boutique lodging facility in

South Lake Tahoe California. This report will make a conclusion of the feasibility of

the endeavor by reviewing data and projections related to market demand, local

seasonal attractions, future growth plans for the area, current hospitality market

analysis, purchase and renovation estimates, and pro forma financial projections. The

report focuses on acquiring and renovating a 22,794 sq ft vintage motel for sale in the

Tourist Core Area of South Lake Tahoe and consisting of 58 lodging rooms.

However, the data report is compiled in such a way that it could be quickly updated to

input new information based on a new property that becomes available.

It is necessary, first, to briefly introduce the subject city – South Lake Tahoe.

The city, located on the southern shore of Lake Tahoe in California’s Sierra Nevada

mountains, is known for being surrounded by stunningly beautiful, natural scenery. It

sits on the California–Nevada border and is primarily geared toward tourism thanks to

the beautiful scenery in addition to year-round attractions that will be covered in more

detail throughout this paper. The city is directly adjacent to the census-designated

place of Stateline, Nevada, known for its world class casinos with big name

entertainment.

2

South Lake Tahoe is a vibrant mountain community with a population of

residents and visitors who enjoy exploring beautiful outdoor locations. Lake Tahoe’s

South Shore is in the midst of a revival – old motels are transforming into trendy

lodgings, a growing craft brewery scene has emerged, new restaurants are popping up

and luxury condos are being built on the lake front. Technology is attracting business

owners and workers who are devoted to fostering a unique, active lifestyle centered

around the Sierra Nevada mountains and the largest alpine lake in North America –

an unparalleled combination that has South Lake Tahoe dubbed “the outdoor capital

of the world.”

Vision

The vision of this hotel project is to leverage the growing trend of revitalized,

midcentury motels into a style-conscious and contemporary experience that caters to

the values of the millennial adventurer.

Mission

The mission of our hotel is to provide outstanding lodging facilities and

services to our guests with a focus on providing the opportunity to experience unique

social connections and interactions with other guests in our common gathering areas.

We emphasize high quality standards in our rooms and food and beverage divisions.

We seek to provide a fair return on investment for our owners and recognize that this

cannot be done without well trained, motivated, and enthusiastic team members.

3

SUPPLY AND DEMAND

Potential Volume

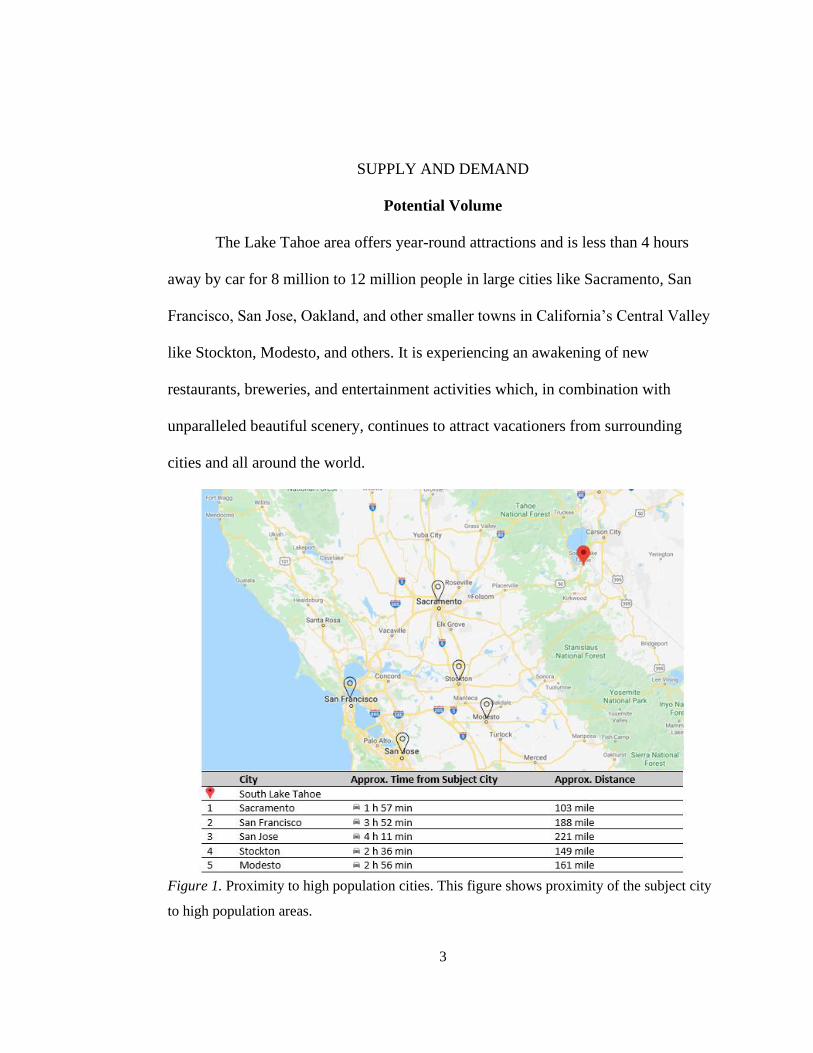

The Lake Tahoe area offers year-round attractions and is less than 4 hours

away by car for 8 million to 12 million people in large cities like Sacramento, San

Francisco, San Jose, Oakland, and other smaller towns in California’s Central Valley

like Stockton, Modesto, and others. It is experiencing an awakening of new

restaurants, breweries, and entertainment activities which, in combination with

unparalleled beautiful scenery, continues to attract vacationers from surrounding

cities and all around the world.

Figure 1. Proximity to high population cities. This figure shows proximity of the subject city

to high population areas.

4

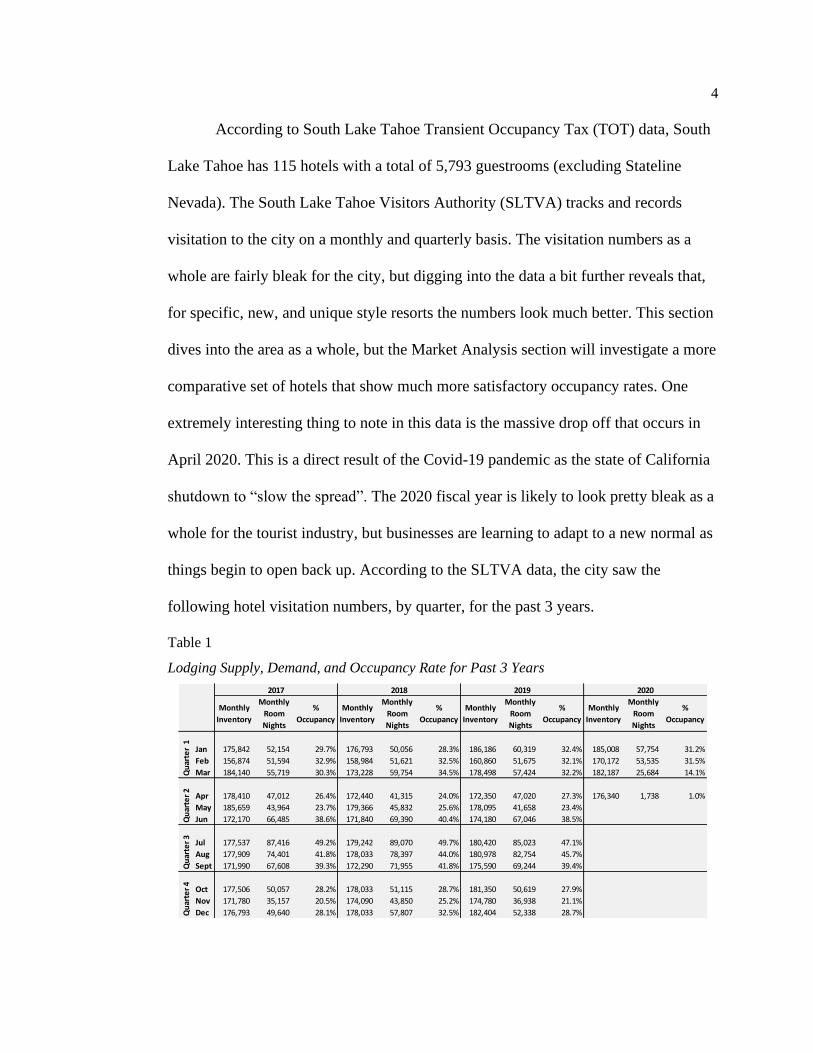

According to South Lake Tahoe Transient Occupancy Tax (TOT) data, South

Lake Tahoe has 115 hotels with a total of 5,793 guestrooms (excluding Stateline

Nevada). The South Lake Tahoe Visitors Authority (SLTVA) tracks and records

visitation to the city on a monthly and quarterly basis. The visitation numbers as a

whole are fairly bleak for the city, but digging into the data a bit further reveals that,

for specific, new, and unique style resorts the numbers look much better. This section

dives into the area as a whole, but the Market Analysis section will investigate a more

comparative set of hotels that show much more satisfactory occupancy rates. One

extremely interesting thing to note in this data is the massive drop off that occurs in

April 2020. This is a direct result of the Covid-19 pandemic as the state of California

shutdown to “slow the spread”. The 2020 fiscal year is likely to look pretty bleak as a

whole for the tourist industry, but businesses are learning to adapt to a new normal as

things begin to open back up. According to the SLTVA data, the city saw the

following hotel visitation numbers, by quarter, for the past 3 years.

Table 1

Lodging Supply, Demand, and Occupancy Rate for Past 3 Years

Monthly

Inventory

Monthly

Room

Nights

%

Occupancy

Monthly

Inventory

Monthly

Room

Nights

%

Occupancy

Monthly

Inventory

Monthly

Room

Nights

%

Occupancy

Monthly

Inventory

Monthly

Room

Nights

%

Occupancy

Jan 175,842 52,154 29.7% 176,793 50,056 28.3% 186,186 60,319 32.4% 185,008 57,754 31.2%

Feb 156,874 51,594 32.9% 158,984 51,621 32.5% 160,860 51,675 32.1% 170,172 53,535 31.5%

Mar 184,140 55,719 30.3% 173,228 59,754 34.5% 178,498 57,424 32.2% 182,187 25,684 14.1%

Apr 178,410 47,012 26.4% 172,440 41,315 24.0% 172,350 47,020 27.3% 176,340 1,738 1.0%

May 185,659 43,964 23.7% 179,366 45,832 25.6% 178,095 41,658 23.4%

Jun 172,170 66,485 38.6% 171,840 69,390 40.4% 174,180 67,046 38.5%

Jul 177,537 87,416 49.2% 179,242 89,070 49.7% 180,420 85,023 47.1%

Aug 177,909 74,401 41.8% 178,033 78,397 44.0% 180,978 82,754 45.7%

Sept 171,990 67,608 39.3% 172,290 71,955 41.8% 175,590 69,244 39.4%

Oct 177,506 50,057 28.2% 178,033 51,115 28.7% 181,350 50,619 27.9%

Nov 171,780 35,157 20.5% 174,090 43,850 25.2% 174,780 36,938 21.1%

Dec 176,793 49,640 28.1% 178,033 57,807 32.5% 182,404 52,338 28.7%

Qu

arte

r 1

Qu

arte

r 2

Qu

arte

r 3

Qu

arte

r 4

2020201920182017

5

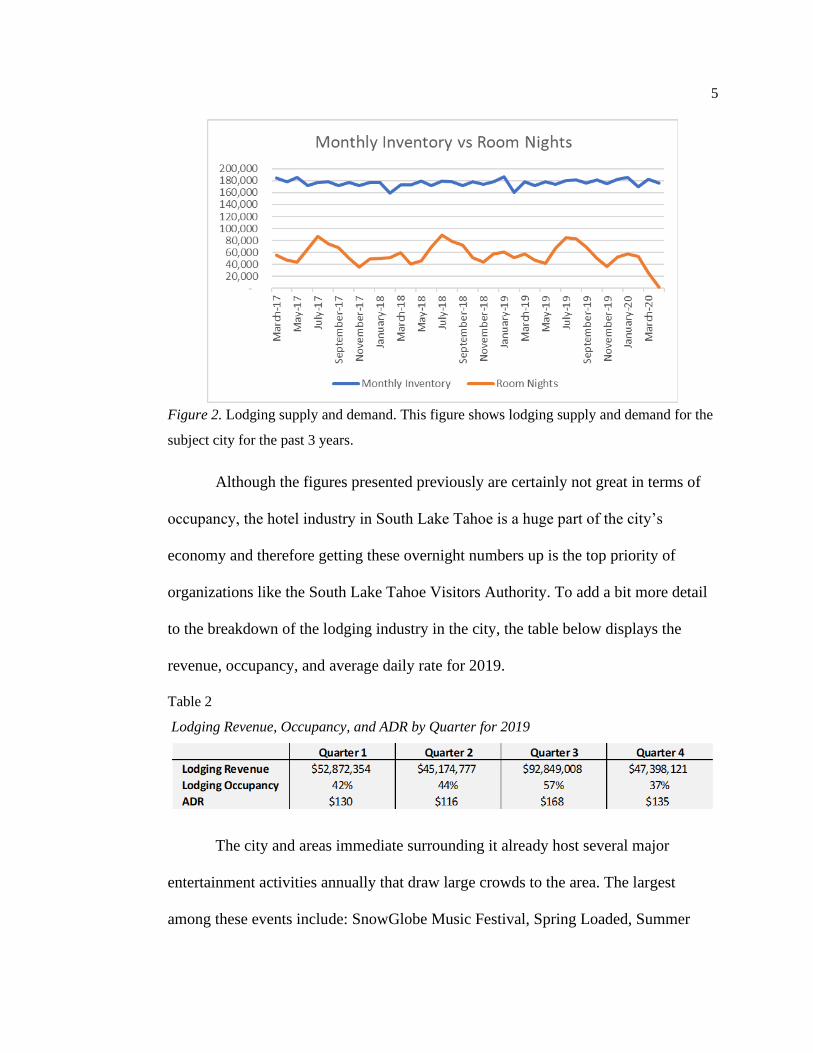

Figure 2. Lodging supply and demand. This figure shows lodging supply and demand for the

subject city for the past 3 years.

Although the figures presented previously are certainly not great in terms of

occupancy, the hotel industry in South Lake Tahoe is a huge part of the city’s

economy and therefore getting these overnight numbers up is the top priority of

organizations like the South Lake Tahoe Visitors Authority. To add a bit more detail

to the breakdown of the lodging industry in the city, the table below displays the

revenue, occupancy, and average daily rate for 2019.

Table 2

Lodging Revenue, Occupancy, and ADR by Quarter for 2019

The city and areas immediate surrounding it already host several major

entertainment activities annually that draw large crowds to the area. The largest

among these events include: SnowGlobe Music Festival, Spring Loaded, Summer

6

Concert Series, Lights on the Lake Fireworks, American Century Celebrity Golf

Championship, and Fall Fish Festival. The SLTVA is fully aware of the direct impact

that entertainment events have on the room night count and so they have successfully

spearheaded the design and approval for a new 5,000-plus person event center slated

to break ground this year and be completed by late Summer 2022. As mentioned, the

resort market is historically soft during shoulder seasons (April, May and October,

November). A multiuse event center provides a venue to attract concerts, corporate

meetings, conventions, trade shows, sporting events, and more – all of which would

be sure to generate more room nights for local hotels.

Figure 3. Proposed multi-purpose event center. This figure shows a rendering of the proposed

multi-purpose center in the subject city.

One cannot talk about potential volume and events that draw people to the

area without briefly mentioning the five large casinos on the Nevada side of the

border. Several of these casino’s host outdoor summer concert series 12 to 15 nights

7

during the summer months and according to the LTVA, have demonstrated that

entertainment is a significant room night generator.

Seasonal Attractions

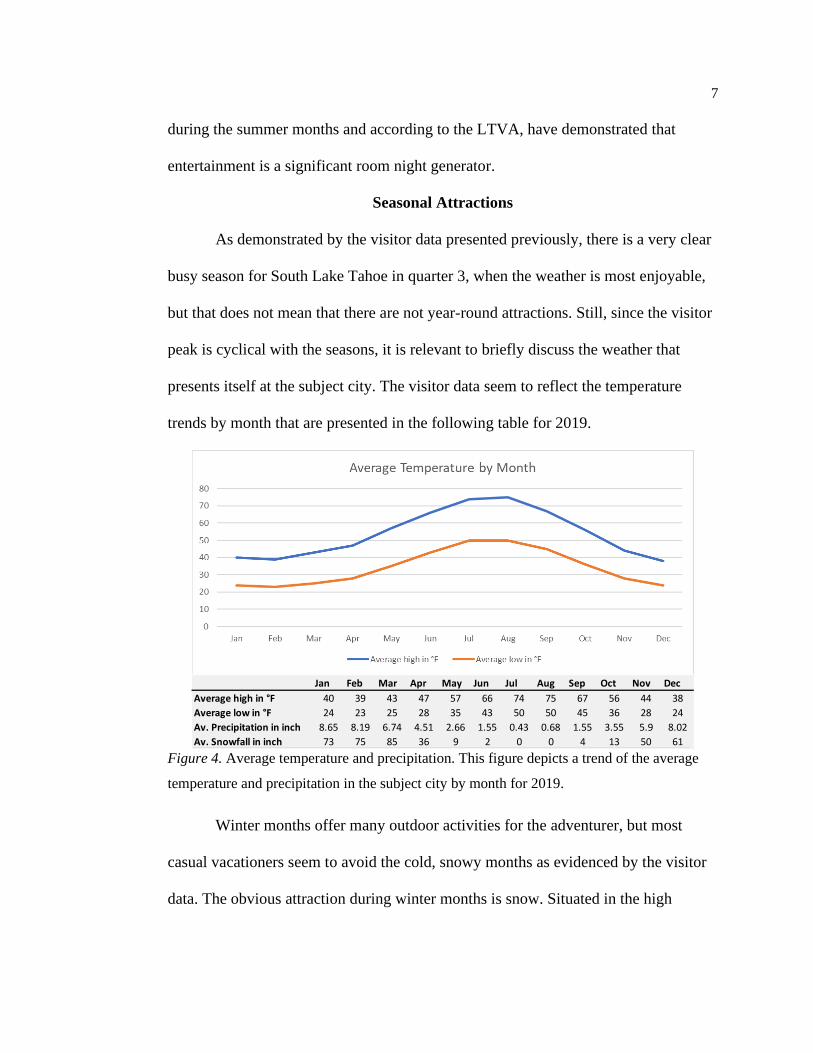

As demonstrated by the visitor data presented previously, there is a very clear

busy season for South Lake Tahoe in quarter 3, when the weather is most enjoyable,

but that does not mean that there are not year-round attractions. Still, since the visitor

peak is cyclical with the seasons, it is relevant to briefly discuss the weather that

presents itself at the subject city. The visitor data seem to reflect the temperature

trends by month that are presented in the following table for 2019.

Figure 4. Average temperature and precipitation. This figure depicts a trend of the average

temperature and precipitation in the subject city by month for 2019.

Winter months offer many outdoor activities for the adventurer, but most

casual vacationers seem to avoid the cold, snowy months as evidenced by the visitor

data. The obvious attraction during winter months is snow. Situated in the high

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Average high in °F 40 39 43 47 57 66 74 75 67 56 44 38

Average low in °F 24 23 25 28 35 43 50 50 45 36 28 24

Av. Precipitation in inch 8.65 8.19 6.74 4.51 2.66 1.55 0.43 0.68 1.55 3.55 5.9 8.02

Av. Snowfall in inch 73 75 85 36 9 2 0 0 4 13 50 61

8

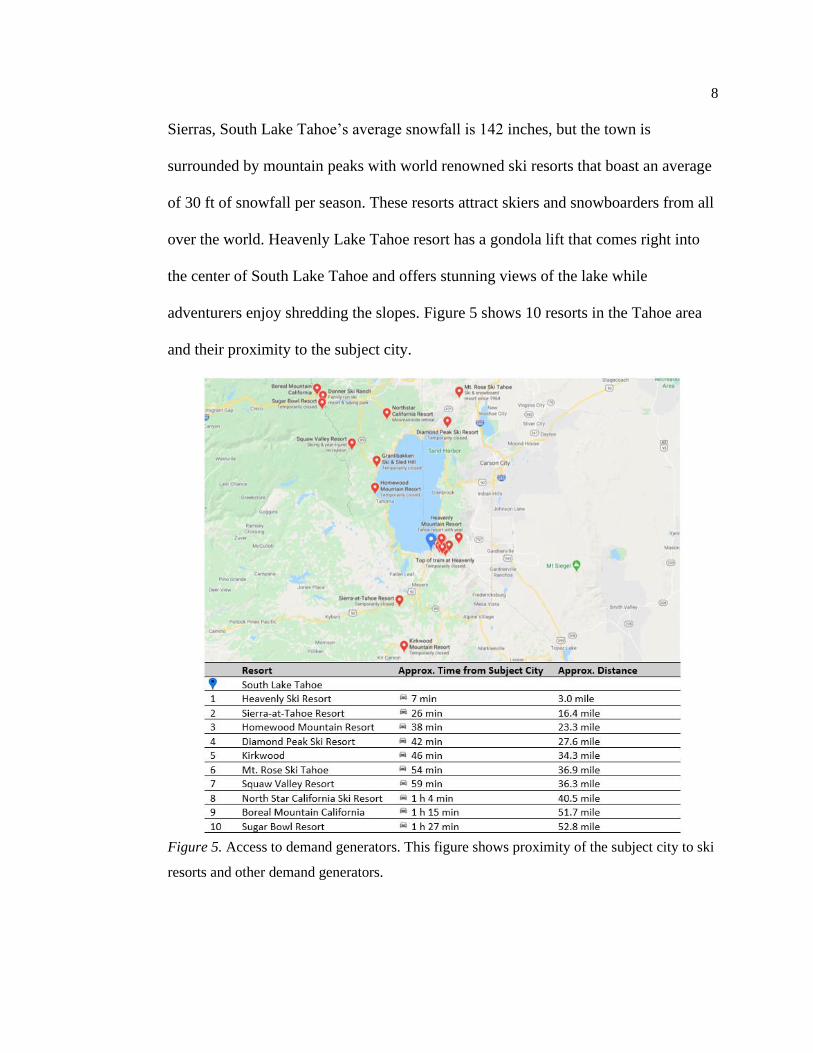

Sierras, South Lake Tahoe’s average snowfall is 142 inches, but the town is

surrounded by mountain peaks with world renowned ski resorts that boast an average

of 30 ft of snowfall per season. These resorts attract skiers and snowboarders from all

over the world. Heavenly Lake Tahoe resort has a gondola lift that comes right into

the center of South Lake Tahoe and offers stunning views of the lake while

adventurers enjoy shredding the slopes. Figure 5 shows 10 resorts in the Tahoe area

and their proximity to the subject city.

Figure 5. Access to demand generators. This figure shows proximity of the subject city to ski

resorts and other demand generators.

9

Downhill skiing and snowboarding are far from the only attraction during

winter months. Cross country skiing and snow shoeing are fantastic ways to escape

the heavily populated areas, see spectacular views, and get some exercise in the fresh

mountain air. Just south of town, Hope Valley Recreation Area offers skiers and

hikers more than 60 miles of trails through valleys and meadows and up mountain

trails. Snowmobile tours are a great option for a fast-paced trip through the mountain

trails and the snow-covered trees of South Lake Tahoe. Zephyr Cove Snowmobile

Center offers adventurers a trip through trails that reach elevations of almost 9,000 ft

with stunning panoramic views of the lake. Tubing and sledding are simple and fun

activities for the entire family. You can go to one of the many resorts that offer

facilities for this activity or find your own hill that you can enjoy all to yourself. For a

truly unique wintertime experience guests may charter an old-fashioned sleigh and

take a ride through the snow-covered mountain landscape to the sound of jingling

bells. After all the adventuring (or if you are not the adventuring type), enjoy a cup of

hot chocolate or a mug of mulled cider, the warmth of an open fireplace, and hours of

conversation at one of the many hotels or local eateries.

Spring and Fall offer many of the same activities with the exception of

beautiful scenery and changing colors in the Fall. Go for a hike on one of the many

marked trails of wide-ranging difficulty levels. Take a bike ride along the lake or if

you are feeling very adventurous, go downhill biking at one of the nearby ski resorts.

Take a boat ride to Emerald Bay on the MS Dixie II, the 500-passenger award

winning paddle wheeler and the largest cruising vessel in South Lake Tahoe.

10

The Summer months see by far the highest number of visitors compared to

any other season. All the same activities of the Spring and Fall months can still be

enjoyed as well as additional lake activities available because of warmer weather.

South Lake Tahoe has some beautiful sandy beaches that are perfect for just relaxing

with a good book or playing with the family on the beach or in the water. Rent a

kayak or a paddle board for a relaxing cruise on the lake or a ski boat or jet ski for a

bit more speed. Go scuba diving at Emerald Bay Underwater State Park.

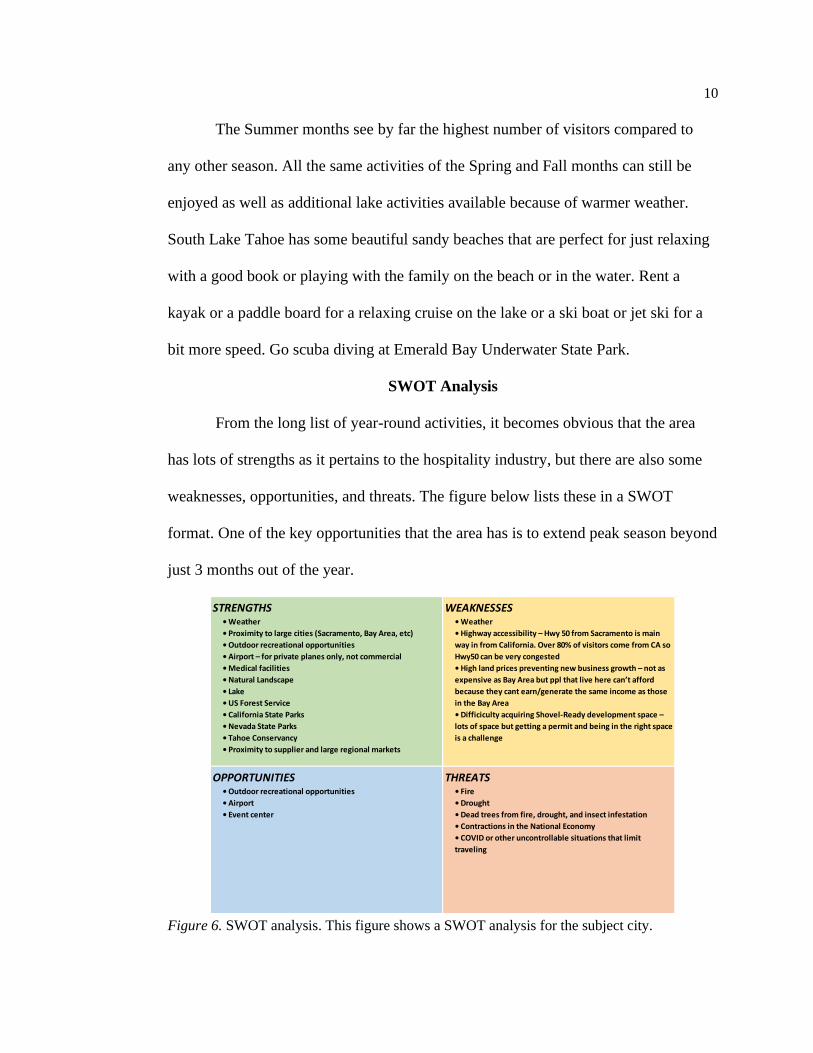

SWOT Analysis

From the long list of year-round activities, it becomes obvious that the area

has lots of strengths as it pertains to the hospitality industry, but there are also some

weaknesses, opportunities, and threats. The figure below lists these in a SWOT

format. One of the key opportunities that the area has is to extend peak season beyond

just 3 months out of the year.

Figure 6. SWOT analysis. This figure shows a SWOT analysis for the subject city.

STRENGTHS WEAKNESSES• Weather

• Proximity to large cities (Sacramento, Bay Area, etc)

• Outdoor recreational opportunities

• Airport – for private planes only, not commercial

• Medical facilities

• Natural Landscape

• Lake

• US Forest Service

• California State Parks

• Nevada State Parks

• Tahoe Conservancy

• Proximity to supplier and large regional markets

• Weather

• Highway accessibility – Hwy 50 from Sacramento is main

way in from California. Over 80% of visitors come from CA so

Hwy50 can be very congested

• High land prices preventing new business growth – not as

expensive as Bay Area but ppl that live here can’t afford

because they cant earn/generate the same income as those

in the Bay Area

• Difficiculty acquiring Shovel-Ready development space –

lots of space but getting a permit and being in the right space

is a challenge

OPPORTUNITIES THREATS• Outdoor recreational opportunities

• Airport

• Event center

• Fire

• Drought

• Dead trees from fire, drought, and insect infestation

• Contractions in the National Economy

• COVID or other uncontrollable situations that limit

traveling

11

MARKET ANALYSIS

Competition

Since the economy of South Lake Tahoe is almost exclusively tourism, there

is plenty of competition to be found for the hotel industry within the city limits.

Between hotels, Airbnbs, VRBOs (vacation rental by owner), and others, there is no

shortage of options for tourists looking for a place to stay.

According to South Lake Tahoe Transient Occupancy Tax (TOT) data there

are 115 different lodging options inside the city limits. These combined lodging

options bring the grand total of available rooms to 5,793 with an average occupancy

percentage of 53.5%. However, for a like comparison, the author has selected a group

of hotels that will be primary competitors based on factors such as location within the

city, style, and rating. This study was conducted, and the following list was compiled.

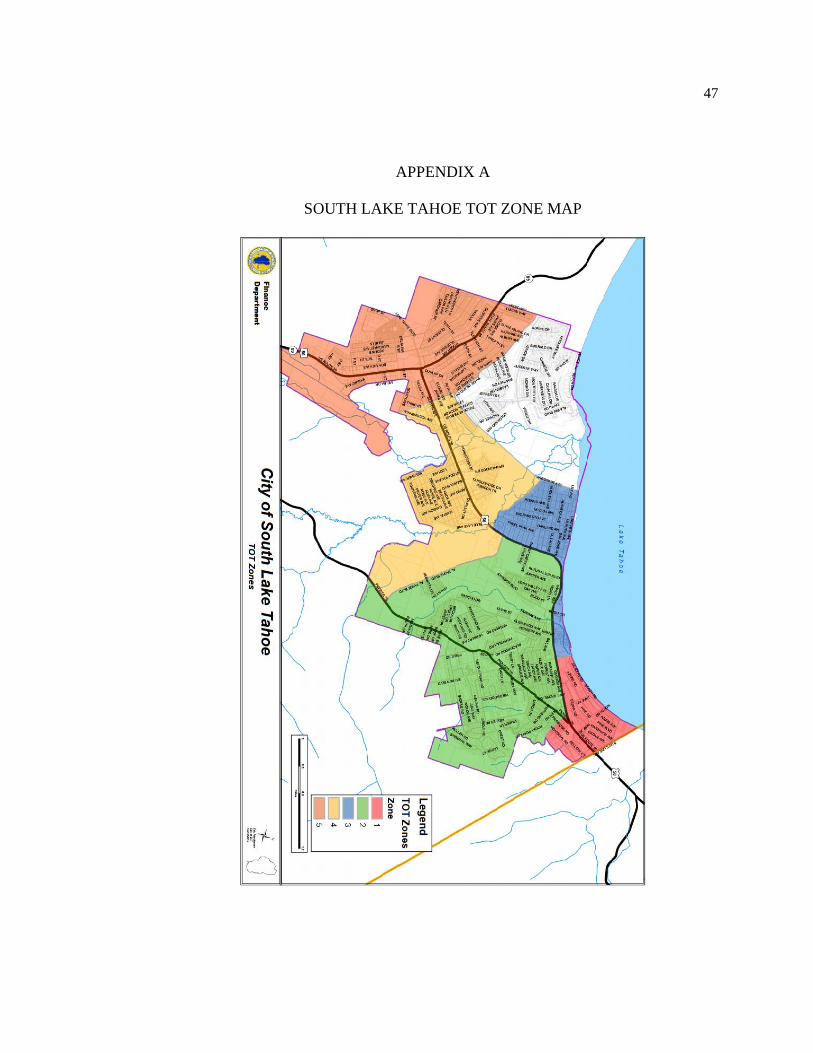

The table displays the hotel name, number of rooms, zone (reference Zone map in

Appendix A), and rating. A subsequent subsection will go over occupancy and rates

of this comp set.

Table 3

Hotel Comp Set Overview (Room Count, Location, and Rating)

Hotels Included in Sample

Number

of Rooms Zone

Rating

(stars)

3 Peaks Resort & Beach Club 62 1 3

Hotel Azure Tahoe 99 2 3

BaseCamp Hotel 51 1 3

Hotel Becket, Trademark Collection by Wyndham 167 1 3

The Coachman Hotel 38 1 4

Forest Suites Resort at Heavenly Village 119 1 3

Holiday Inn Express South Lake Tahoe 89 1 3

Tahoe Lakeshore Lodge & Spa 50 3 3

Station House Inn 98 1 3

Total 773

Source: City of SLT TOT and TID Report

12

A comp set is an important set of data for a hotel to use to compare against

similar, nearby competing hotels. The selection criteria for this comp set includes but

is not necessarily limited to the following: scale and quality, geographical location

and accessibility, and leisure facilities. One of the primary selection criteria is the

style and feel of the hotel. All of these, with the exception of the Holiday Inn Express,

are boutique hotels which sets them uniquely apart from traditional hotels. This type

of hotel is furnished in a central theme and offers unique character, a personalized

touch, and value-added service that meet customers’ lifestyles (Ahmad, Hemdi, &

Othman, 2017). Lim and Endean (2009) describe the boutique hotel as “the

combination of service quality characteristics, individual design, location, and

facilities.” From a different perspective, Teo and Chang (2009) consider that central

to the concept of the boutique hotel “is the importance of the touristic experience of

place histories and cultural identities.” According to Van Hartesvelt (2006), the

defining characteristics of boutique hotels are that they typically range from 20–150

rooms, are at least four stars, have a successful restaurant on the premises, are

exclusive, and are typically “housed in older, unique structures that have been

converted from another use”. The conclusion of the overview of Aggett (2007) of

international definitions of boutique hotels was that “boutique hotels are

contemporary design-led hotels with up to 100 bedrooms, which offer unique levels

of personalized service and high-tech facilities.”

13

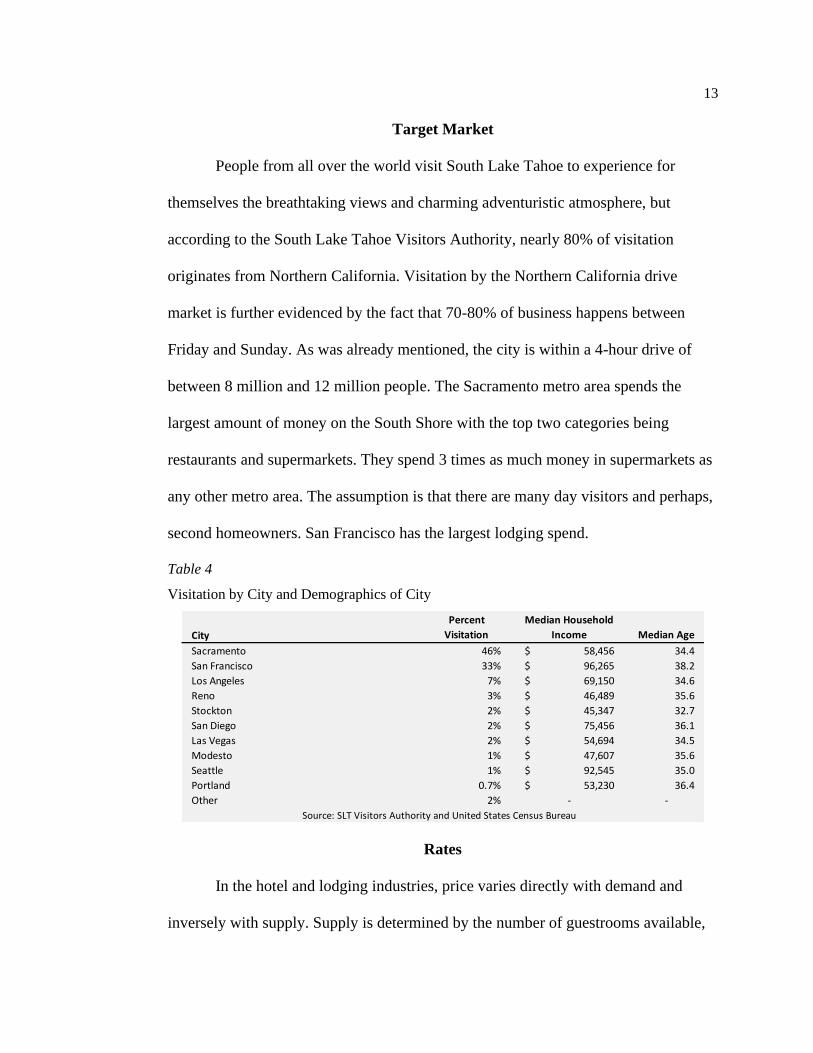

Target Market

People from all over the world visit South Lake Tahoe to experience for

themselves the breathtaking views and charming adventuristic atmosphere, but

according to the South Lake Tahoe Visitors Authority, nearly 80% of visitation

originates from Northern California. Visitation by the Northern California drive

market is further evidenced by the fact that 70-80% of business happens between

Friday and Sunday. As was already mentioned, the city is within a 4-hour drive of

between 8 million and 12 million people. The Sacramento metro area spends the

largest amount of money on the South Shore with the top two categories being

restaurants and supermarkets. They spend 3 times as much money in supermarkets as

any other metro area. The assumption is that there are many day visitors and perhaps,

second homeowners. San Francisco has the largest lodging spend.

Table 4

Visitation by City and Demographics of City

Rates

In the hotel and lodging industries, price varies directly with demand and

inversely with supply. Supply is determined by the number of guestrooms available,

City

Percent

Visitation

Median Household

Income Median Age

Sacramento 46% 58,456$ 34.4

San Francisco 33% 96,265$ 38.2

Los Angeles 7% 69,150$ 34.6

Reno 3% 46,489$ 35.6

Stockton 2% 45,347$ 32.7

San Diego 2% 75,456$ 36.1

Las Vegas 2% 54,694$ 34.5

Modesto 1% 47,607$ 35.6

Seattle 1% 92,545$ 35.0

Portland 0.7% 53,230$ 36.4

Other 2% - -

Source: SLT Visitors Authority and United States Census Bureau

14

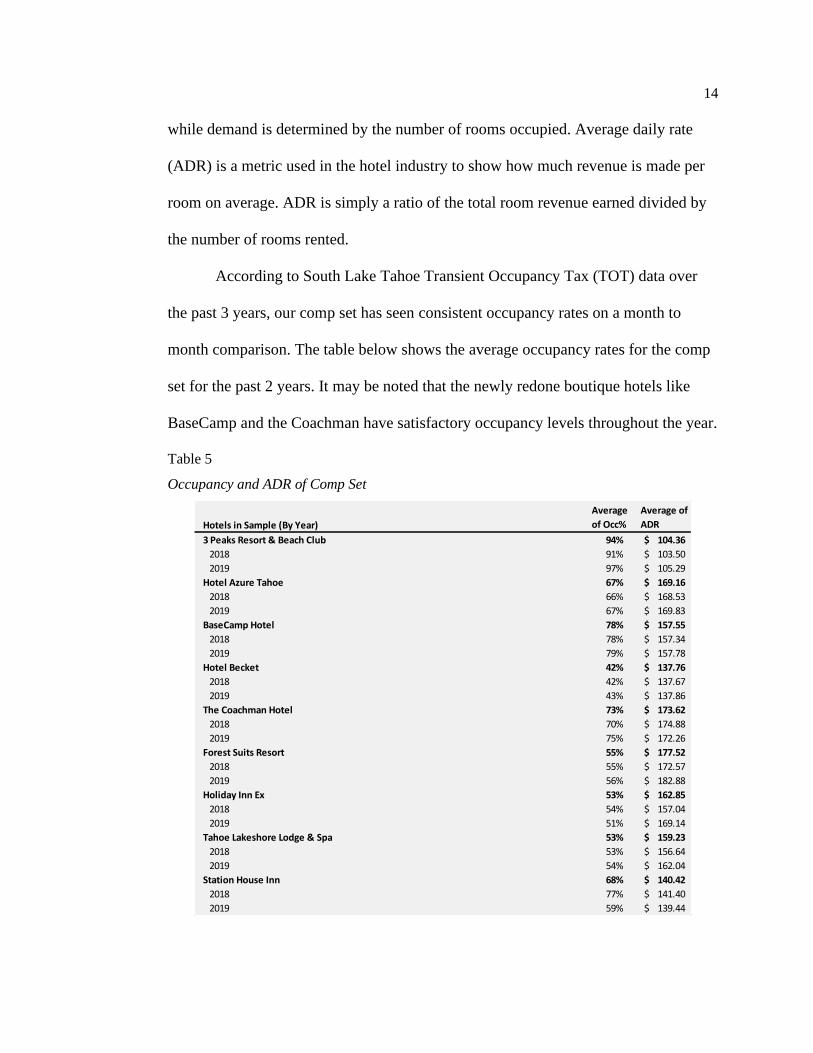

while demand is determined by the number of rooms occupied. Average daily rate

(ADR) is a metric used in the hotel industry to show how much revenue is made per

room on average. ADR is simply a ratio of the total room revenue earned divided by

the number of rooms rented.

According to South Lake Tahoe Transient Occupancy Tax (TOT) data over

the past 3 years, our comp set has seen consistent occupancy rates on a month to

month comparison. The table below shows the average occupancy rates for the comp

set for the past 2 years. It may be noted that the newly redone boutique hotels like

BaseCamp and the Coachman have satisfactory occupancy levels throughout the year.

Table 5

Occupancy and ADR of Comp Set

Hotels in Sample (By Year)

Average

of Occ%

Average of

ADR

3 Peaks Resort & Beach Club 94% 104.36$

2018 91% 103.50$

2019 97% 105.29$

Hotel Azure Tahoe 67% 169.16$

2018 66% 168.53$

2019 67% 169.83$

BaseCamp Hotel 78% 157.55$

2018 78% 157.34$

2019 79% 157.78$

Hotel Becket 42% 137.76$

2018 42% 137.67$

2019 43% 137.86$

The Coachman Hotel 73% 173.62$

2018 70% 174.88$

2019 75% 172.26$

Forest Suits Resort 55% 177.52$

2018 55% 172.57$

2019 56% 182.88$

Holiday Inn Ex 53% 162.85$

2018 54% 157.04$

2019 51% 169.14$

Tahoe Lakeshore Lodge & Spa 53% 159.23$

2018 53% 156.64$

2019 54% 162.04$

Station House Inn 68% 140.42$

2018 77% 141.40$

2019 59% 139.44$

15

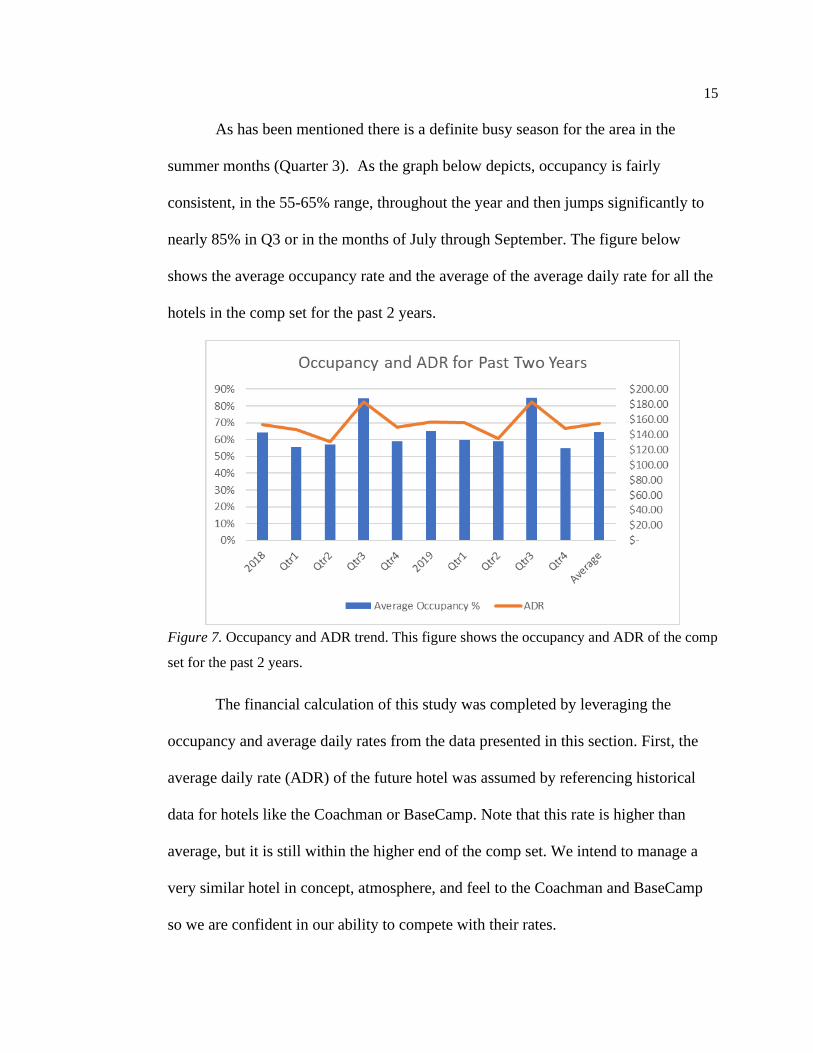

As has been mentioned there is a definite busy season for the area in the

summer months (Quarter 3). As the graph below depicts, occupancy is fairly

consistent, in the 55-65% range, throughout the year and then jumps significantly to

nearly 85% in Q3 or in the months of July through September. The figure below

shows the average occupancy rate and the average of the average daily rate for all the

hotels in the comp set for the past 2 years.

Figure 7. Occupancy and ADR trend. This figure shows the occupancy and ADR of the comp

set for the past 2 years.

The financial calculation of this study was completed by leveraging the

occupancy and average daily rates from the data presented in this section. First, the

average daily rate (ADR) of the future hotel was assumed by referencing historical

data for hotels like the Coachman or BaseCamp. Note that this rate is higher than

average, but it is still within the higher end of the comp set. We intend to manage a

very similar hotel in concept, atmosphere, and feel to the Coachman and BaseCamp

so we are confident in our ability to compete with their rates.

16

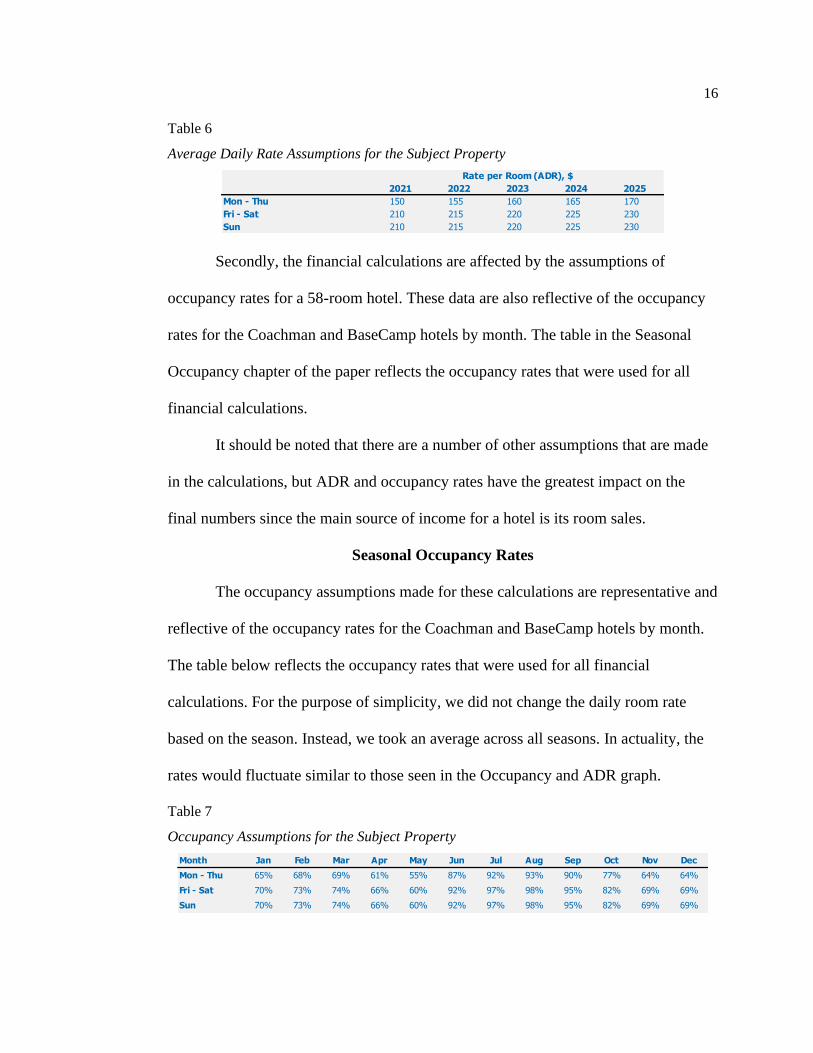

Table 6

Average Daily Rate Assumptions for the Subject Property

Secondly, the financial calculations are affected by the assumptions of

occupancy rates for a 58-room hotel. These data are also reflective of the occupancy

rates for the Coachman and BaseCamp hotels by month. The table in the Seasonal

Occupancy chapter of the paper reflects the occupancy rates that were used for all

financial calculations.

It should be noted that there are a number of other assumptions that are made

in the calculations, but ADR and occupancy rates have the greatest impact on the

final numbers since the main source of income for a hotel is its room sales.

Seasonal Occupancy Rates

The occupancy assumptions made for these calculations are representative and

reflective of the occupancy rates for the Coachman and BaseCamp hotels by month.

The table below reflects the occupancy rates that were used for all financial

calculations. For the purpose of simplicity, we did not change the daily room rate

based on the season. Instead, we took an average across all seasons. In actuality, the

rates would fluctuate similar to those seen in the Occupancy and ADR graph.

Table 7

Occupancy Assumptions for the Subject Property

2021 2022 2023 2024 2025

Mon - Thu 150 155 160 165 170

Fri - Sat 210 215 220 225 230

Sun 210 215 220 225 230

Rate per Room (ADR), $

Month Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mon - Thu 65% 68% 69% 61% 55% 87% 92% 93% 90% 77% 64% 64%

Fri - Sat 70% 73% 74% 66% 60% 92% 97% 98% 95% 82% 69% 69%

Sun 70% 73% 74% 66% 60% 92% 97% 98% 95% 82% 69% 69%

17

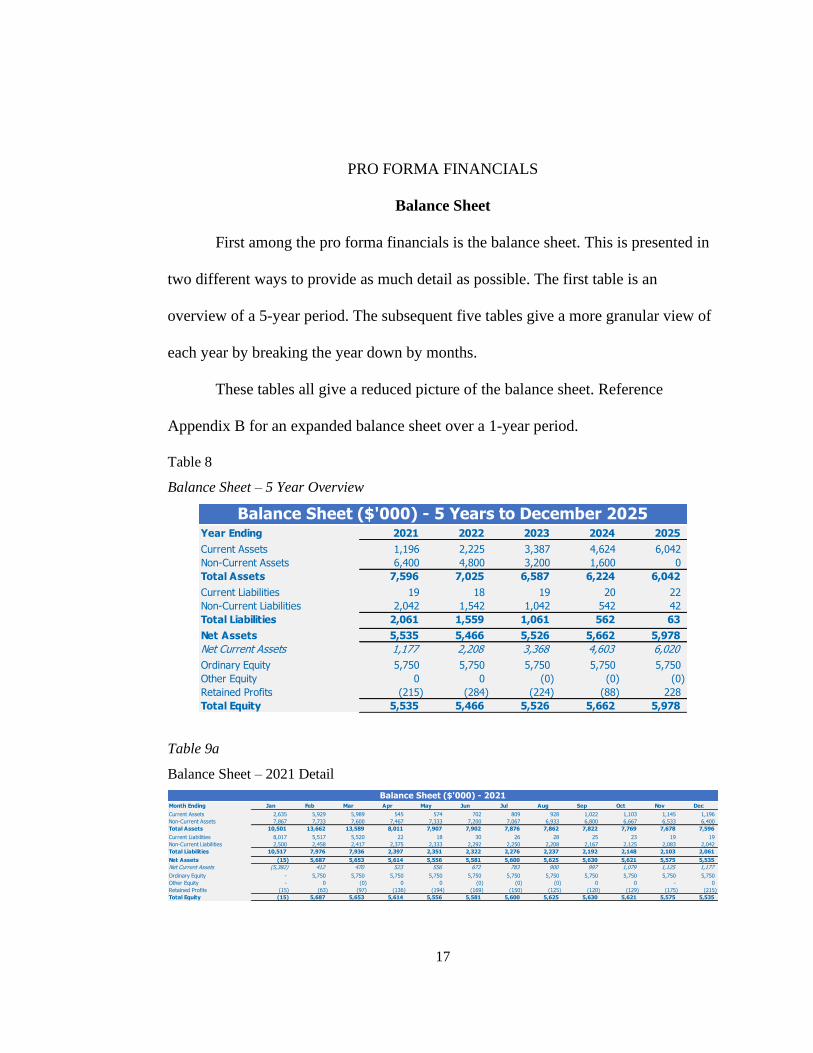

PRO FORMA FINANCIALS

Balance Sheet

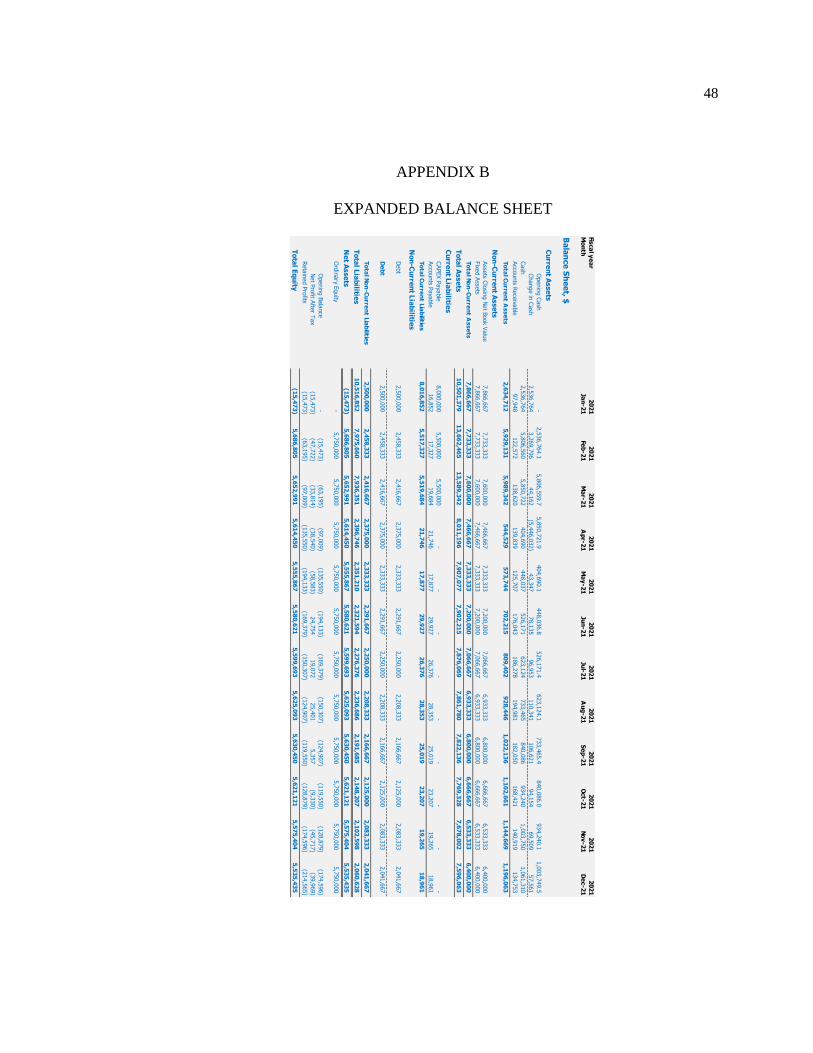

First among the pro forma financials is the balance sheet. This is presented in

two different ways to provide as much detail as possible. The first table is an

overview of a 5-year period. The subsequent five tables give a more granular view of

each year by breaking the year down by months.

These tables all give a reduced picture of the balance sheet. Reference

Appendix B for an expanded balance sheet over a 1-year period.

Table 8

Balance Sheet – 5 Year Overview

Table 9a

Balance Sheet – 2021 Detail

Year Ending 2021 2022 2023 2024 2025

Current Assets 1,196 2,225 3,387 4,624 6,042

Non-Current Assets 6,400 4,800 3,200 1,600 0

Total Assets 7,596 7,025 6,587 6,224 6,042

Current Liabilities 19 18 19 20 22

Non-Current Liabilities 2,042 1,542 1,042 542 42

Total Liabilities 2,061 1,559 1,061 562 63

Net Assets 5,535 5,466 5,526 5,662 5,978

Net Current Assets 1,177 2,208 3,368 4,603 6,020

Ordinary Equity 5,750 5,750 5,750 5,750 5,750

Other Equity 0 0 (0) (0) (0)

Retained Profits (215) (284) (224) (88) 228

Total Equity 5,535 5,466 5,526 5,662 5,978

Balance Sheet ($'000) - 5 Years to December 2025

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Current Assets 2,635 5,929 5,989 545 574 702 809 928 1,022 1,103 1,145 1,196

Non-Current Assets 7,867 7,733 7,600 7,467 7,333 7,200 7,067 6,933 6,800 6,667 6,533 6,400

Total Assets 10,501 13,662 13,589 8,011 7,907 7,902 7,876 7,862 7,822 7,769 7,678 7,596

Current Liabilities 8,017 5,517 5,520 22 18 30 26 28 25 23 19 19

Non-Current Liabilities 2,500 2,458 2,417 2,375 2,333 2,292 2,250 2,208 2,167 2,125 2,083 2,042

Total Liabilities 10,517 7,976 7,936 2,397 2,351 2,322 2,276 2,237 2,192 2,148 2,103 2,061

Net Assets (15) 5,687 5,653 5,614 5,556 5,581 5,600 5,625 5,630 5,621 5,575 5,535

Net Current Assets (5,382) 412 470 523 556 672 783 900 997 1,079 1,125 1,177

Ordinary Equity - 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750

Other Equity - 0 (0) 0 0 (0) (0) (0) 0 0 - 0

Retained Profits (15) (63) (97) (136) (194) (169) (150) (125) (120) (129) (175) (215)

Total Equity (15) 5,687 5,653 5,614 5,556 5,581 5,600 5,625 5,630 5,621 5,575 5,535

Balance Sheet ($'000) - 2021

18

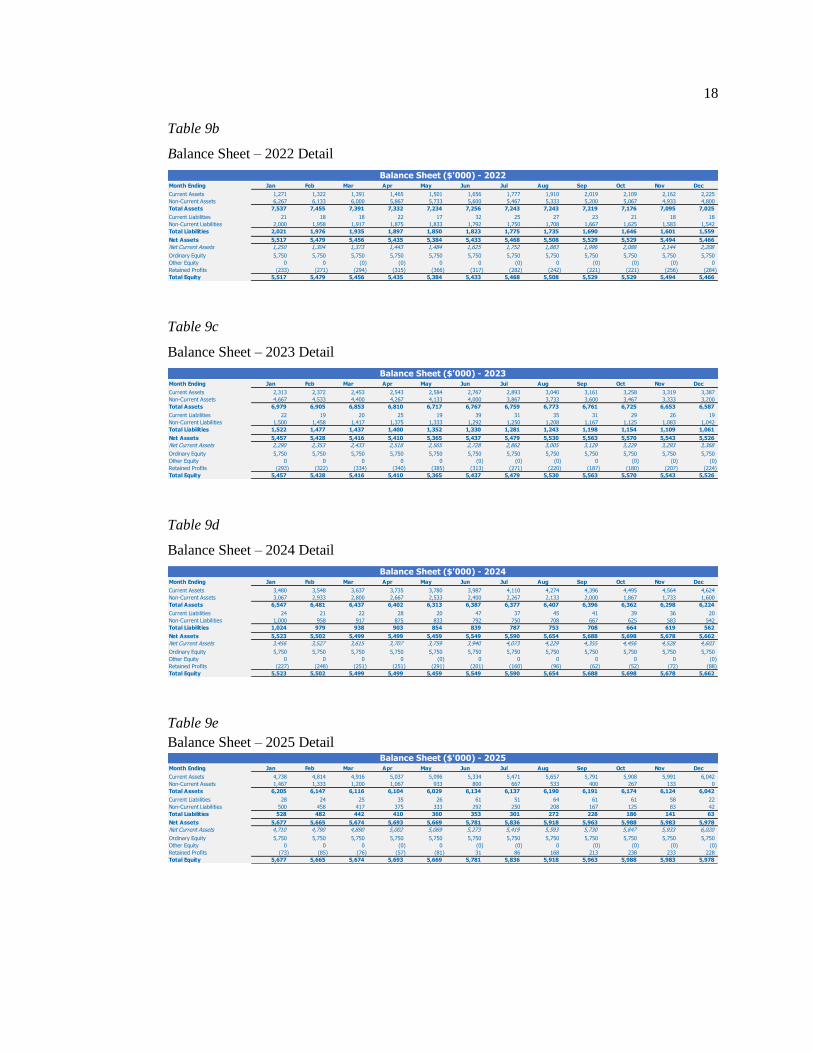

Table 9b

Balance Sheet – 2022 Detail

Table 9c

Balance Sheet – 2023 Detail

Table 9d

Balance Sheet – 2024 Detail

Table 9e

Balance Sheet – 2025 Detail

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Current Assets 1,271 1,322 1,391 1,465 1,501 1,656 1,777 1,910 2,019 2,109 2,162 2,225

Non-Current Assets 6,267 6,133 6,000 5,867 5,733 5,600 5,467 5,333 5,200 5,067 4,933 4,800

Total Assets 7,537 7,455 7,391 7,332 7,234 7,256 7,243 7,243 7,219 7,176 7,095 7,025

Current Liabilities 21 18 18 22 17 32 25 27 23 21 18 18

Non-Current Liabilities 2,000 1,958 1,917 1,875 1,833 1,792 1,750 1,708 1,667 1,625 1,583 1,542

Total Liabilities 2,021 1,976 1,935 1,897 1,850 1,823 1,775 1,735 1,690 1,646 1,601 1,559

Net Assets 5,517 5,479 5,456 5,435 5,384 5,433 5,468 5,508 5,529 5,529 5,494 5,466

Net Current Assets 1,250 1,304 1,373 1,443 1,484 1,625 1,752 1,883 1,996 2,088 2,144 2,208

Ordinary Equity 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750

Other Equity 0 0 (0) (0) 0 0 (0) 0 (0) (0) (0) 0

Retained Profits (233) (271) (294) (315) (366) (317) (282) (242) (221) (221) (256) (284)

Total Equity 5,517 5,479 5,456 5,435 5,384 5,433 5,468 5,508 5,529 5,529 5,494 5,466

Balance Sheet ($'000) - 2022

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Current Assets 2,313 2,372 2,453 2,543 2,584 2,767 2,893 3,040 3,161 3,258 3,319 3,387

Non-Current Assets 4,667 4,533 4,400 4,267 4,133 4,000 3,867 3,733 3,600 3,467 3,333 3,200

Total Assets 6,979 6,905 6,853 6,810 6,717 6,767 6,759 6,773 6,761 6,725 6,653 6,587

Current Liabilities 22 19 20 25 19 39 31 35 31 29 26 19

Non-Current Liabilities 1,500 1,458 1,417 1,375 1,333 1,292 1,250 1,208 1,167 1,125 1,083 1,042

Total Liabilities 1,522 1,477 1,437 1,400 1,352 1,330 1,281 1,243 1,198 1,154 1,109 1,061

Net Assets 5,457 5,428 5,416 5,410 5,365 5,437 5,479 5,530 5,563 5,570 5,543 5,526

Net Current Assets 2,290 2,353 2,433 2,518 2,565 2,728 2,862 3,005 3,129 3,229 3,293 3,368

Ordinary Equity 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750

Other Equity 0 0 0 0 0 (0) (0) (0) 0 (0) (0) (0)

Retained Profits (293) (322) (334) (340) (385) (313) (271) (220) (187) (180) (207) (224)

Total Equity 5,457 5,428 5,416 5,410 5,365 5,437 5,479 5,530 5,563 5,570 5,543 5,526

Balance Sheet ($'000) - 2023

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Current Assets 3,480 3,548 3,637 3,735 3,780 3,987 4,110 4,274 4,396 4,495 4,564 4,624

Non-Current Assets 3,067 2,933 2,800 2,667 2,533 2,400 2,267 2,133 2,000 1,867 1,733 1,600

Total Assets 6,547 6,481 6,437 6,402 6,313 6,387 6,377 6,407 6,396 6,362 6,298 6,224

Current Liabilities 24 21 22 28 20 47 37 45 41 39 36 20

Non-Current Liabilities 1,000 958 917 875 833 792 750 708 667 625 583 542

Total Liabilities 1,024 979 938 903 854 839 787 753 708 664 619 562

Net Assets 5,523 5,502 5,499 5,499 5,459 5,549 5,590 5,654 5,688 5,698 5,678 5,662

Net Current Assets 3,456 3,527 3,615 3,707 3,759 3,940 4,073 4,229 4,355 4,456 4,528 4,603

Ordinary Equity 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750

Other Equity 0 0 0 0 (0) 0 0 0 0 0 0 (0)

Retained Profits (227) (248) (251) (251) (291) (201) (160) (96) (62) (52) (72) (88)

Total Equity 5,523 5,502 5,499 5,499 5,459 5,549 5,590 5,654 5,688 5,698 5,678 5,662

Balance Sheet ($'000) - 2024

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Current Assets 4,738 4,814 4,916 5,037 5,096 5,334 5,471 5,657 5,791 5,908 5,991 6,042

Non-Current Assets 1,467 1,333 1,200 1,067 933 800 667 533 400 267 133 0

Total Assets 6,205 6,147 6,116 6,104 6,029 6,134 6,137 6,190 6,191 6,174 6,124 6,042

Current Liabilities 28 24 25 35 26 61 51 64 61 61 58 22

Non-Current Liabilities 500 458 417 375 333 292 250 208 167 125 83 42

Total Liabilities 528 482 442 410 360 353 301 272 228 186 141 63

Net Assets 5,677 5,665 5,674 5,693 5,669 5,781 5,836 5,918 5,963 5,988 5,983 5,978

Net Current Assets 4,710 4,790 4,890 5,002 5,069 5,273 5,419 5,593 5,730 5,847 5,933 6,020

Ordinary Equity 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750 5,750

Other Equity 0 0 0 (0) 0 (0) (0) 0 (0) (0) (0) (0)

Retained Profits (73) (85) (76) (57) (81) 31 86 168 213 238 233 228

Total Equity 5,677 5,665 5,674 5,693 5,669 5,781 5,836 5,918 5,963 5,988 5,983 5,978

Balance Sheet ($'000) - 2025

19

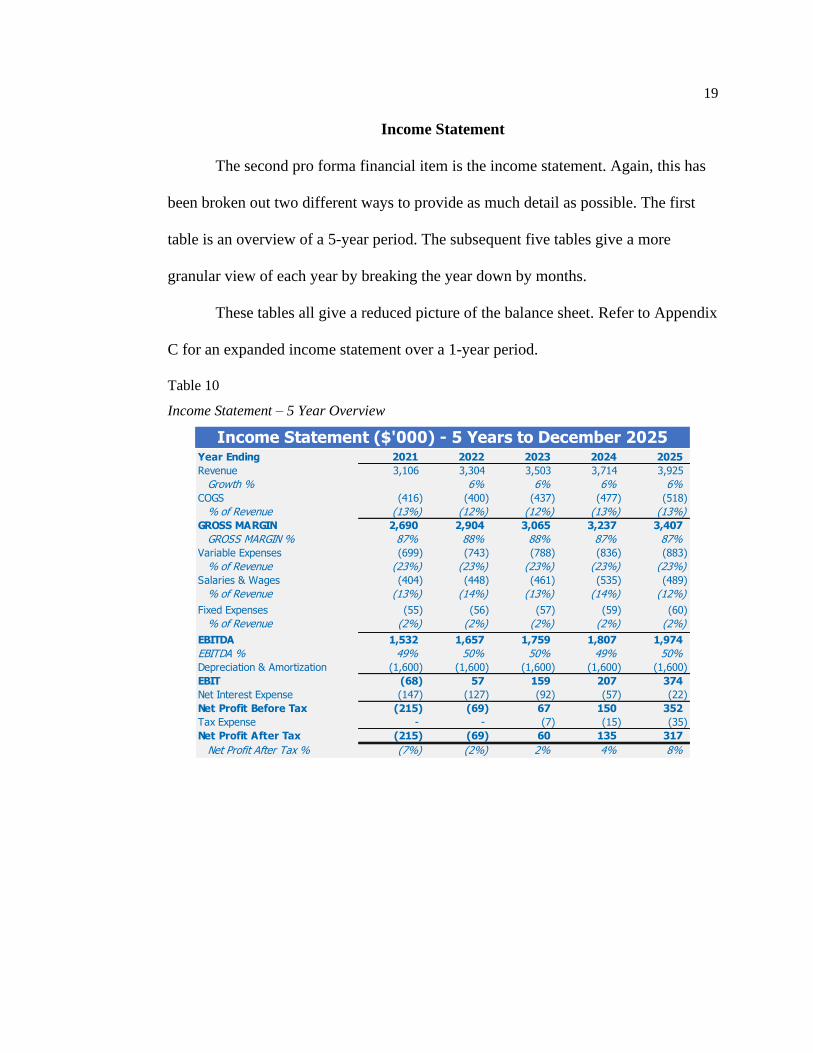

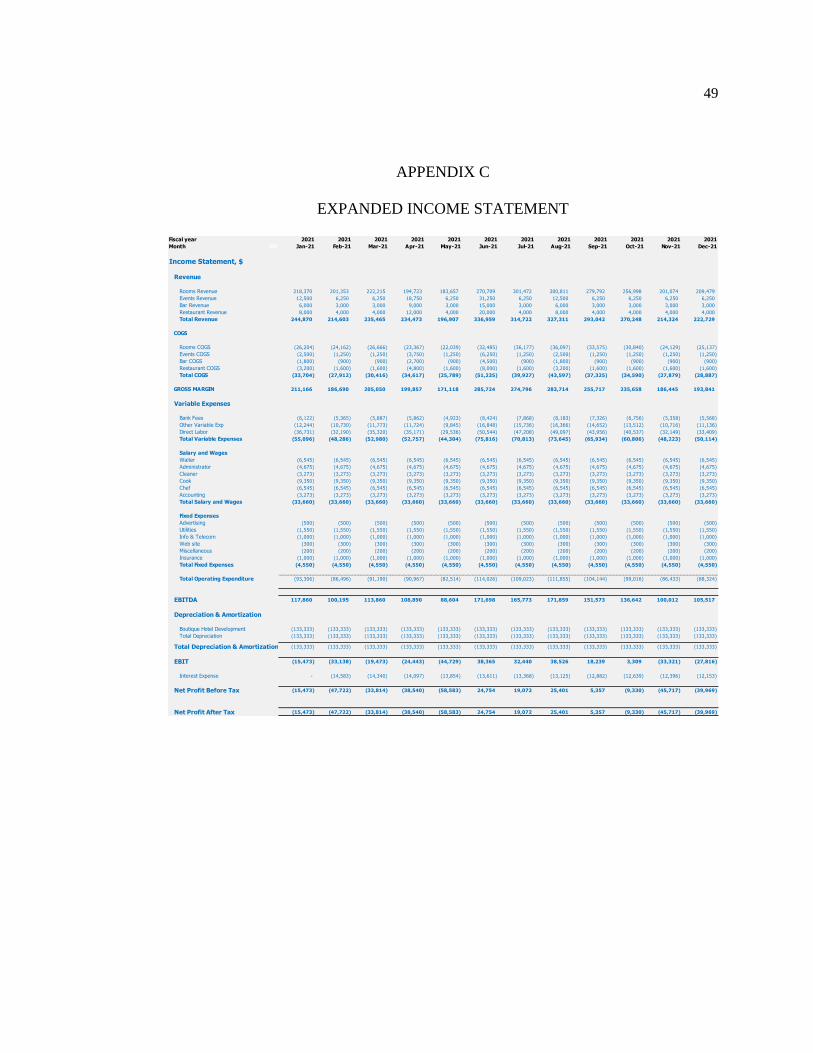

Income Statement

The second pro forma financial item is the income statement. Again, this has

been broken out two different ways to provide as much detail as possible. The first

table is an overview of a 5-year period. The subsequent five tables give a more

granular view of each year by breaking the year down by months.

These tables all give a reduced picture of the balance sheet. Refer to Appendix

C for an expanded income statement over a 1-year period.

Table 10

Income Statement – 5 Year Overview

Year Ending 2021 2022 2023 2024 2025

Revenue 3,106 3,304 3,503 3,714 3,925

Growth % 6% 6% 6% 6%

COGS (416) (400) (437) (477) (518)

% of Revenue (13%) (12%) (12%) (13%) (13%)

GROSS MARGIN 2,690 2,904 3,065 3,237 3,407

GROSS MARGIN % 87% 88% 88% 87% 87%

Variable Expenses (699) (743) (788) (836) (883)

% of Revenue (23%) (23%) (23%) (23%) (23%)

Salaries & Wages (404) (448) (461) (535) (489)

% of Revenue (13%) (14%) (13%) (14%) (12%)

Fixed Expenses (55) (56) (57) (59) (60)

% of Revenue (2%) (2%) (2%) (2%) (2%)

EBITDA 1,532 1,657 1,759 1,807 1,974

EBITDA % 49% 50% 50% 49% 50%

Depreciation & Amortization (1,600) (1,600) (1,600) (1,600) (1,600)

EBIT (68) 57 159 207 374

Net Interest Expense (147) (127) (92) (57) (22)

Net Profit Before Tax (215) (69) 67 150 352

Tax Expense - - (7) (15) (35)

Net Profit After Tax (215) (69) 60 135 317

Net Profit After Tax % (7%) (2%) 2% 4% 8%

Income Statement ($'000) - 5 Years to December 2025

20

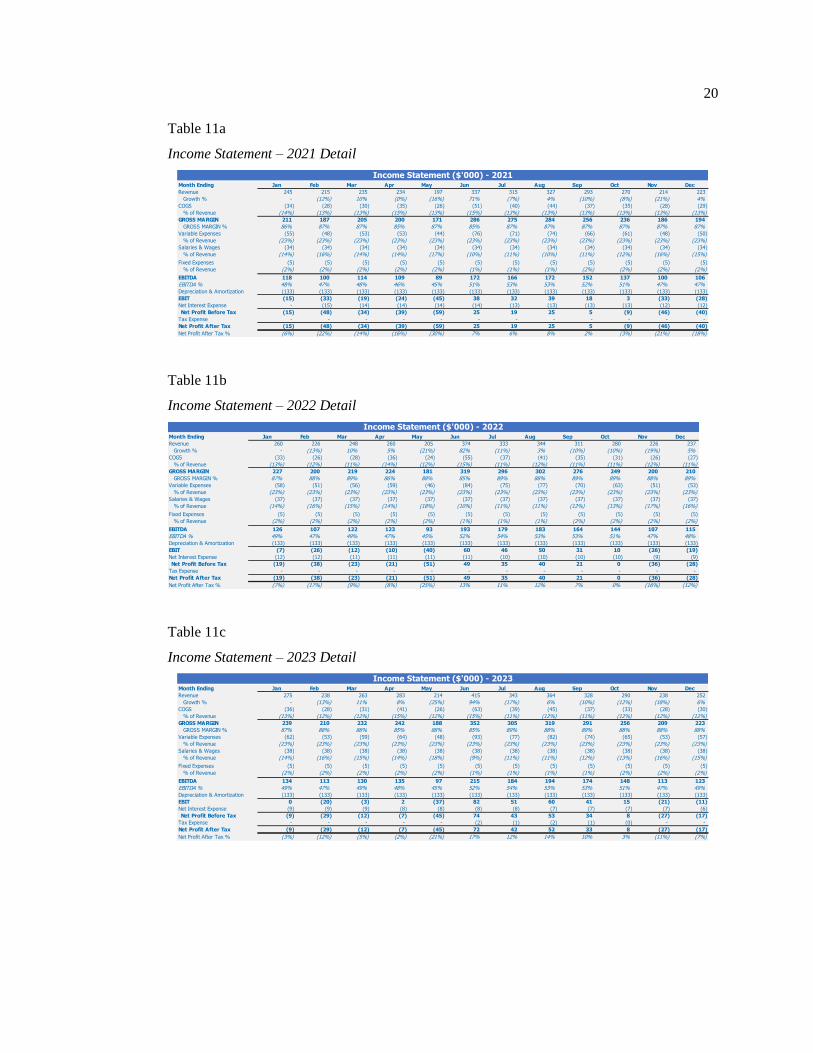

Table 11a

Income Statement – 2021 Detail

Table 11b

Income Statement – 2022 Detail

Table 11c

Income Statement – 2023 Detail

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Revenue 245 215 235 234 197 337 315 327 293 270 214 223

Growth % - (12%) 10% (0%) (16%) 71% (7%) 4% (10%) (8%) (21%) 4%

COGS (34) (28) (30) (35) (26) (51) (40) (44) (37) (35) (28) (29)

% of Revenue (14%) (13%) (13%) (15%) (13%) (15%) (13%) (13%) (13%) (13%) (13%) (13%)

GROSS MARGIN 211 187 205 200 171 286 275 284 256 236 186 194

GROSS MARGIN % 86% 87% 87% 85% 87% 85% 87% 87% 87% 87% 87% 87%

Variable Expenses (55) (48) (53) (53) (44) (76) (71) (74) (66) (61) (48) (50)

% of Revenue (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%)

Salaries & Wages (34) (34) (34) (34) (34) (34) (34) (34) (34) (34) (34) (34)

% of Revenue (14%) (16%) (14%) (14%) (17%) (10%) (11%) (10%) (11%) (12%) (16%) (15%)

Fixed Expenses (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5)

% of Revenue (2%) (2%) (2%) (2%) (2%) (1%) (1%) (1%) (2%) (2%) (2%) (2%)

EBITDA 118 100 114 109 89 172 166 172 152 137 100 106

EBITDA % 48% 47% 48% 46% 45% 51% 53% 53% 52% 51% 47% 47%

Depreciation & Amortization (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133)

EBIT (15) (33) (19) (24) (45) 38 32 39 18 3 (33) (28)

Net Interest Expense - (15) (14) (14) (14) (14) (13) (13) (13) (13) (12) (12)

Net Profit Before Tax (15) (48) (34) (39) (59) 25 19 25 5 (9) (46) (40)

Tax Expense - - - - - - - - - - - -

Net Profit After Tax (15) (48) (34) (39) (59) 25 19 25 5 (9) (46) (40)

Net Profit After Tax % (6%) (22%) (14%) (16%) (30%) 7% 6% 8% 2% (3%) (21%) (18%)

Income Statement ($'000) - 2021

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Revenue 260 226 248 260 205 374 333 344 311 280 226 237

Growth % - (13%) 10% 5% (21%) 82% (11%) 3% (10%) (10%) (19%) 5%

COGS (33) (26) (28) (36) (24) (55) (37) (41) (35) (31) (26) (27)

% of Revenue (13%) (12%) (11%) (14%) (12%) (15%) (11%) (12%) (11%) (11%) (12%) (11%)

GROSS MARGIN 227 200 219 224 181 319 296 302 276 249 200 210

GROSS MARGIN % 87% 88% 89% 86% 88% 85% 89% 88% 89% 89% 88% 89%

Variable Expenses (58) (51) (56) (59) (46) (84) (75) (77) (70) (63) (51) (53)

% of Revenue (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%)

Salaries & Wages (37) (37) (37) (37) (37) (37) (37) (37) (37) (37) (37) (37)

% of Revenue (14%) (16%) (15%) (14%) (18%) (10%) (11%) (11%) (12%) (13%) (17%) (16%)

Fixed Expenses (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5)

% of Revenue (2%) (2%) (2%) (2%) (2%) (1%) (1%) (1%) (2%) (2%) (2%) (2%)

EBITDA 126 107 122 123 93 193 179 183 164 144 107 115

EBITDA % 49% 47% 49% 47% 45% 52% 54% 53% 53% 51% 47% 48%

Depreciation & Amortization (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133)

EBIT (7) (26) (12) (10) (40) 60 46 50 31 10 (26) (19)

Net Interest Expense (12) (12) (11) (11) (11) (11) (10) (10) (10) (10) (9) (9)

Net Profit Before Tax (19) (38) (23) (21) (51) 49 35 40 21 0 (36) (28)

Tax Expense - - - - - - - - - - - -

Net Profit After Tax (19) (38) (23) (21) (51) 49 35 40 21 0 (36) (28)

Net Profit After Tax % (7%) (17%) (9%) (8%) (25%) 13% 11% 12% 7% 0% (16%) (12%)

Income Statement ($'000) - 2022

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Revenue 275 238 263 283 214 415 343 364 328 290 238 252

Growth % - (13%) 11% 8% (25%) 94% (17%) 6% (10%) (12%) (18%) 6%

COGS (36) (28) (31) (41) (26) (63) (39) (45) (37) (33) (28) (30)

% of Revenue (13%) (12%) (12%) (15%) (12%) (15%) (11%) (12%) (11%) (12%) (12%) (12%)

GROSS MARGIN 239 210 232 242 188 352 305 319 291 256 209 223

GROSS MARGIN % 87% 88% 88% 85% 88% 85% 89% 88% 89% 88% 88% 88%

Variable Expenses (62) (53) (59) (64) (48) (93) (77) (82) (74) (65) (53) (57)

% of Revenue (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%)

Salaries & Wages (38) (38) (38) (38) (38) (38) (38) (38) (38) (38) (38) (38)

% of Revenue (14%) (16%) (15%) (14%) (18%) (9%) (11%) (11%) (12%) (13%) (16%) (15%)

Fixed Expenses (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5)

% of Revenue (2%) (2%) (2%) (2%) (2%) (1%) (1%) (1%) (1%) (2%) (2%) (2%)

EBITDA 134 113 130 135 97 215 184 194 174 148 113 123

EBITDA % 49% 47% 49% 48% 45% 52% 54% 53% 53% 51% 47% 49%

Depreciation & Amortization (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133)

EBIT 0 (20) (3) 2 (37) 82 51 60 41 15 (21) (11)

Net Interest Expense (9) (9) (9) (8) (8) (8) (8) (7) (7) (7) (7) (6)

Net Profit Before Tax (9) (29) (12) (7) (45) 74 43 53 34 8 (27) (17)

Tax Expense - - - - - (2) (1) (2) (1) (0) - -

Net Profit After Tax (9) (29) (12) (7) (45) 72 42 52 33 8 (27) (17)

Net Profit After Tax % (3%) (12%) (5%) (2%) (21%) 17% 12% 14% 10% 3% (11%) (7%)

Income Statement ($'000) - 2023

21

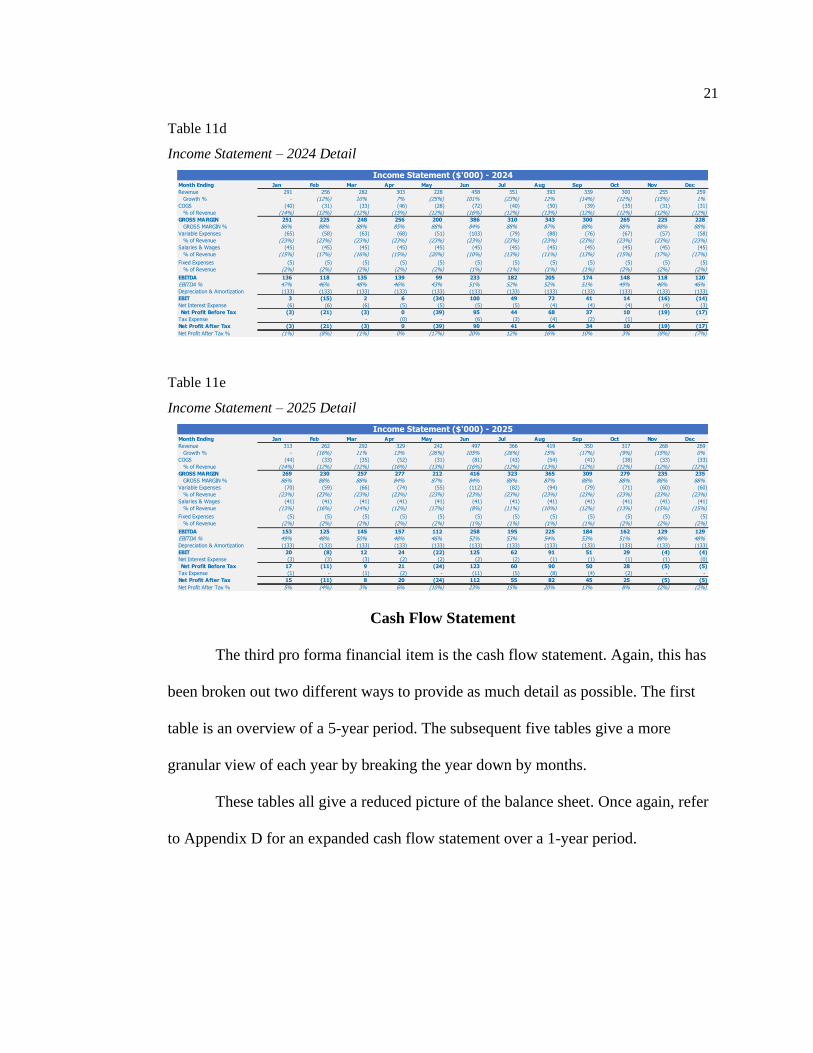

Table 11d

Income Statement – 2024 Detail

Table 11e

Income Statement – 2025 Detail

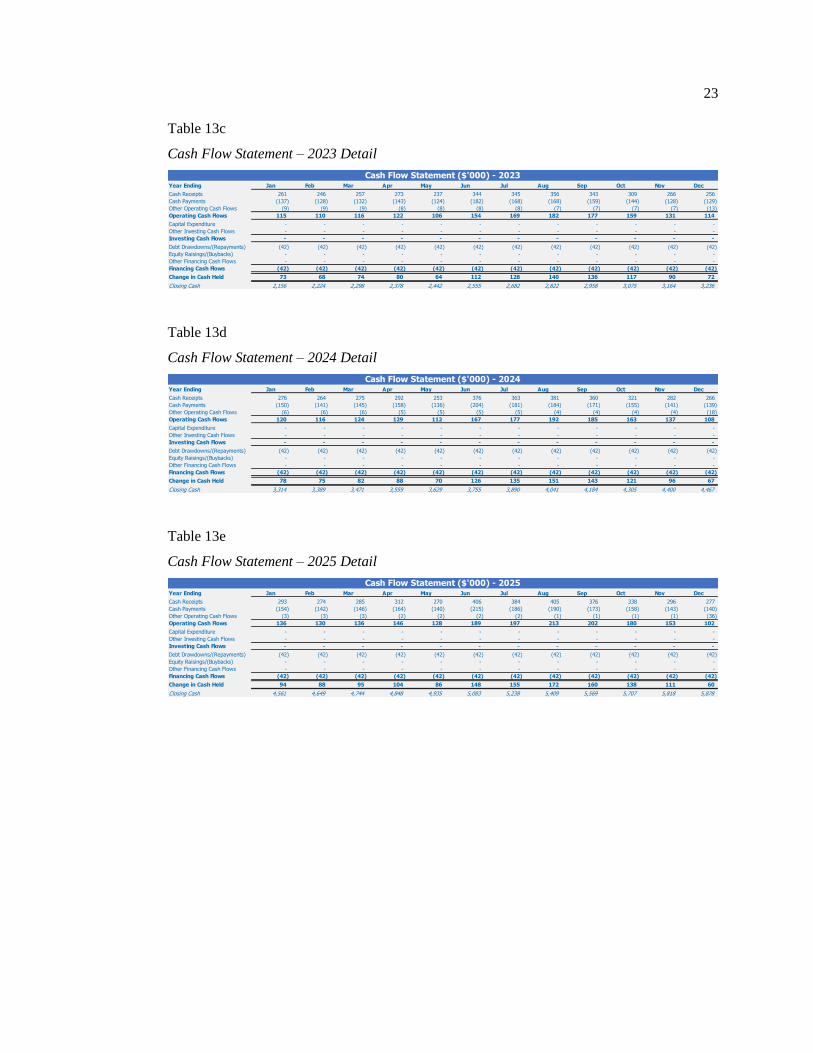

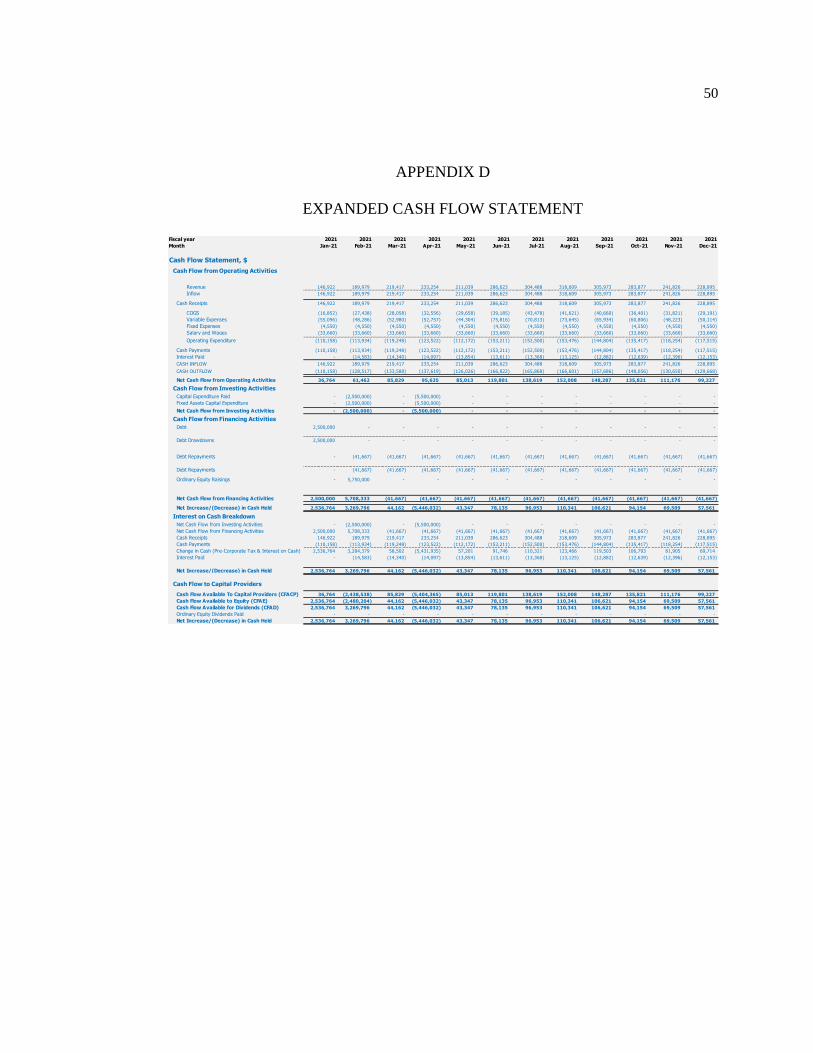

Cash Flow Statement

The third pro forma financial item is the cash flow statement. Again, this has

been broken out two different ways to provide as much detail as possible. The first

table is an overview of a 5-year period. The subsequent five tables give a more

granular view of each year by breaking the year down by months.

These tables all give a reduced picture of the balance sheet. Once again, refer

to Appendix D for an expanded cash flow statement over a 1-year period.

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Revenue 291 256 282 303 228 458 351 393 339 300 255 259

Growth % - (12%) 10% 7% (25%) 101% (23%) 12% (14%) (12%) (15%) 1%

COGS (40) (31) (33) (46) (28) (72) (40) (50) (39) (35) (31) (31)

% of Revenue (14%) (12%) (12%) (15%) (12%) (16%) (12%) (13%) (12%) (12%) (12%) (12%)

GROSS MARGIN 251 225 248 256 200 386 310 343 300 265 225 228

GROSS MARGIN % 86% 88% 88% 85% 88% 84% 88% 87% 88% 88% 88% 88%

Variable Expenses (65) (58) (63) (68) (51) (103) (79) (88) (76) (67) (57) (58)

% of Revenue (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%)

Salaries & Wages (45) (45) (45) (45) (45) (45) (45) (45) (45) (45) (45) (45)

% of Revenue (15%) (17%) (16%) (15%) (20%) (10%) (13%) (11%) (13%) (15%) (17%) (17%)

Fixed Expenses (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5)

% of Revenue (2%) (2%) (2%) (2%) (2%) (1%) (1%) (1%) (1%) (2%) (2%) (2%)

EBITDA 136 118 135 139 99 233 182 205 174 148 118 120

EBITDA % 47% 46% 48% 46% 43% 51% 52% 52% 51% 49% 46% 46%

Depreciation & Amortization (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133)

EBIT 3 (15) 2 6 (34) 100 49 72 41 14 (16) (14)

Net Interest Expense (6) (6) (6) (5) (5) (5) (5) (4) (4) (4) (4) (3)

Net Profit Before Tax (3) (21) (3) 0 (39) 95 44 68 37 10 (19) (17)

Tax Expense - - - (0) - (6) (3) (4) (2) (1) - -

Net Profit After Tax (3) (21) (3) 0 (39) 90 41 64 34 10 (19) (17)

Net Profit After Tax % (1%) (8%) (1%) 0% (17%) 20% 12% 16% 10% 3% (8%) (7%)

Income Statement ($'000) - 2024

Month Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Revenue 313 262 292 329 242 497 366 419 350 317 268 269

Growth % - (16%) 11% 13% (26%) 105% (26%) 15% (17%) (9%) (15%) 0%

COGS (44) (33) (35) (52) (31) (81) (43) (54) (41) (38) (33) (33)

% of Revenue (14%) (12%) (12%) (16%) (13%) (16%) (12%) (13%) (12%) (12%) (12%) (12%)

GROSS MARGIN 269 230 257 277 212 416 323 365 309 279 235 235

GROSS MARGIN % 86% 88% 88% 84% 87% 84% 88% 87% 88% 88% 88% 88%

Variable Expenses (70) (59) (66) (74) (55) (112) (82) (94) (79) (71) (60) (60)

% of Revenue (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%) (23%)

Salaries & Wages (41) (41) (41) (41) (41) (41) (41) (41) (41) (41) (41) (41)

% of Revenue (13%) (16%) (14%) (12%) (17%) (8%) (11%) (10%) (12%) (13%) (15%) (15%)

Fixed Expenses (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5) (5)

% of Revenue (2%) (2%) (2%) (2%) (2%) (1%) (1%) (1%) (1%) (2%) (2%) (2%)

EBITDA 153 125 145 157 112 258 195 225 184 162 129 129

EBITDA % 49% 48% 50% 48% 46% 52% 53% 54% 53% 51% 48% 48%

Depreciation & Amortization (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133) (133)

EBIT 20 (8) 12 24 (22) 125 62 91 51 29 (4) (4)

Net Interest Expense (3) (3) (3) (2) (2) (2) (2) (1) (1) (1) (1) (0)

Net Profit Before Tax 17 (11) 9 21 (24) 123 60 90 50 28 (5) (5)

Tax Expense (1) - (1) (2) - (11) (5) (8) (4) (2) - -

Net Profit After Tax 15 (11) 8 20 (24) 112 55 82 45 25 (5) (5)

Net Profit After Tax % 5% (4%) 3% 6% (10%) 23% 15% 20% 13% 8% (2%) (2%)

Income Statement ($'000) - 2025

22

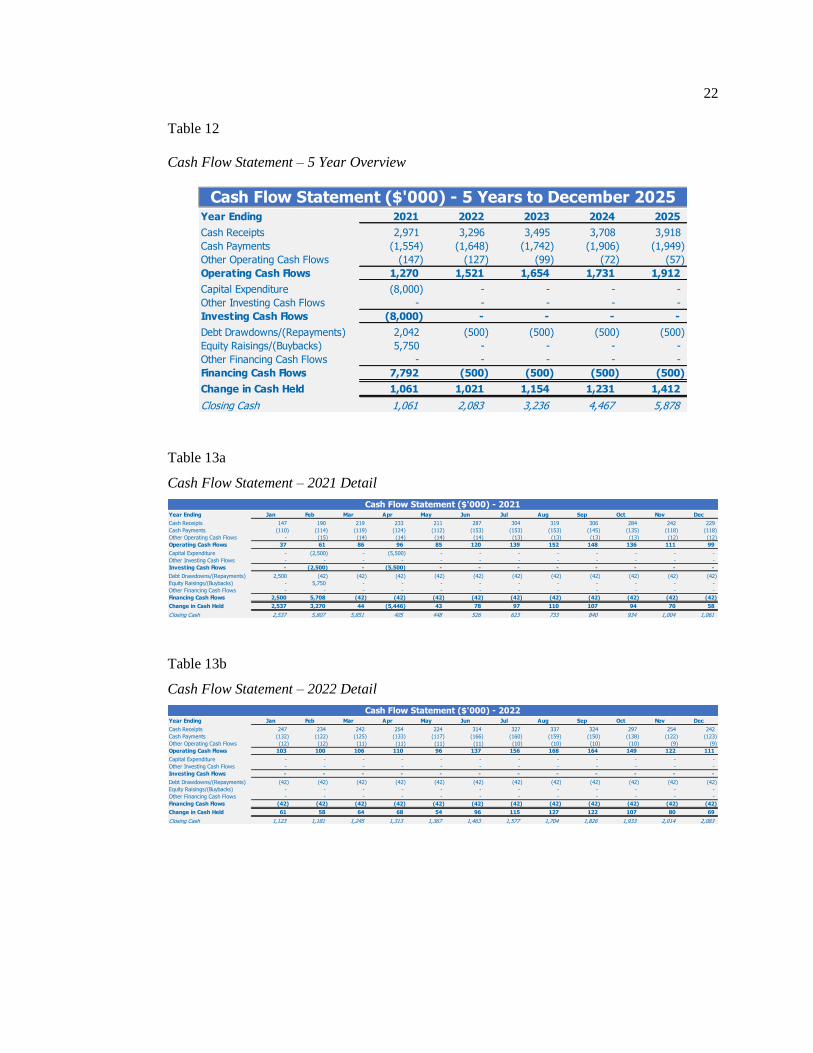

Table 12

Cash Flow Statement – 5 Year Overview

Table 13a

Cash Flow Statement – 2021 Detail

Table 13b

Cash Flow Statement – 2022 Detail

Year Ending 2021 2022 2023 2024 2025

Cash Receipts 2,971 3,296 3,495 3,708 3,918

Cash Payments (1,554) (1,648) (1,742) (1,906) (1,949)

Other Operating Cash Flows (147) (127) (99) (72) (57)

Operating Cash Flows 1,270 1,521 1,654 1,731 1,912

Capital Expenditure (8,000) - - - -

Other Investing Cash Flows - - - - -

Investing Cash Flows (8,000) - - - -

Debt Drawdowns/(Repayments) 2,042 (500) (500) (500) (500)

Equity Raisings/(Buybacks) 5,750 - - - -

Other Financing Cash Flows - - - - -

Financing Cash Flows 7,792 (500) (500) (500) (500)

Change in Cash Held 1,061 1,021 1,154 1,231 1,412

Closing Cash 1,061 2,083 3,236 4,467 5,878

Cash Flow Statement ($'000) - 5 Years to December 2025

Year Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash Receipts 147 190 219 233 211 287 304 319 306 284 242 229

Cash Payments (110) (114) (119) (124) (112) (153) (153) (153) (145) (135) (118) (118)

Other Operating Cash Flows - (15) (14) (14) (14) (14) (13) (13) (13) (13) (12) (12)

Operating Cash Flows 37 61 86 96 85 120 139 152 148 136 111 99

Capital Expenditure - (2,500) - (5,500) - - - - - - - -

Other Investing Cash Flows - - - - - - - - - - - -

Investing Cash Flows - (2,500) - (5,500) - - - - - - - -

Debt Drawdowns/(Repayments) 2,500 (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Equity Raisings/(Buybacks) - 5,750 - - - - - - - - - -

Other Financing Cash Flows - - - - - - - - - - - -

Financing Cash Flows 2,500 5,708 (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Change in Cash Held 2,537 3,270 44 (5,446) 43 78 97 110 107 94 70 58

Closing Cash 2,537 5,807 5,851 405 448 526 623 733 840 934 1,004 1,061

Cash Flow Statement ($'000) - 2021

Year Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash Receipts 247 234 242 254 224 314 327 337 324 297 254 242

Cash Payments (132) (122) (125) (133) (117) (166) (160) (159) (150) (138) (122) (123)

Other Operating Cash Flows (12) (12) (11) (11) (11) (11) (10) (10) (10) (10) (9) (9)

Operating Cash Flows 103 100 106 110 96 137 156 168 164 149 122 111

Capital Expenditure - - - - - - - - - - - -

Other Investing Cash Flows - - - - - - - - - - - -

Investing Cash Flows - - - - - - - - - - - -

Debt Drawdowns/(Repayments) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Equity Raisings/(Buybacks) - - - - - - - - - - - -

Other Financing Cash Flows - - - - - - - - - - - -

Financing Cash Flows (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Change in Cash Held 61 58 64 68 54 96 115 127 122 107 80 69

Closing Cash 1,123 1,181 1,245 1,313 1,367 1,463 1,577 1,704 1,826 1,933 2,014 2,083

Cash Flow Statement ($'000) - 2022

23

Table 13c

Cash Flow Statement – 2023 Detail

Table 13d

Cash Flow Statement – 2024 Detail

Table 13e

Cash Flow Statement – 2025 Detail

Year Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash Receipts 261 246 257 273 237 344 345 356 343 309 266 256

Cash Payments (137) (128) (132) (143) (124) (182) (168) (168) (159) (144) (128) (129)

Other Operating Cash Flows (9) (9) (9) (8) (8) (8) (8) (7) (7) (7) (7) (13)

Operating Cash Flows 115 110 116 122 106 154 169 182 177 159 131 114

Capital Expenditure - - - - - - - - - - - -

Other Investing Cash Flows - - - - - - - - - - - -

Investing Cash Flows - - - - - - - - - - - -

Debt Drawdowns/(Repayments) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Equity Raisings/(Buybacks) - - - - - - - - - - - -

Other Financing Cash Flows - - - - - - - - - - - -

Financing Cash Flows (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Change in Cash Held 73 68 74 80 64 112 128 140 136 117 90 72

Closing Cash 2,156 2,224 2,298 2,378 2,442 2,555 2,682 2,822 2,958 3,075 3,164 3,236

Cash Flow Statement ($'000) - 2023

Year Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash Receipts 276 264 275 292 253 376 363 381 360 321 282 266

Cash Payments (150) (141) (145) (158) (136) (204) (181) (184) (171) (155) (141) (139)

Other Operating Cash Flows (6) (6) (6) (5) (5) (5) (5) (4) (4) (4) (4) (18)

Operating Cash Flows 120 116 124 129 112 167 177 192 185 163 137 108

Capital Expenditure - - - - - - - - - - - -

Other Investing Cash Flows - - - - - - - - - - - -

Investing Cash Flows - - - - - - - - - - - -

Debt Drawdowns/(Repayments) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Equity Raisings/(Buybacks) - - - - - - - - - - - -

Other Financing Cash Flows - - - - - - - - - - - -

Financing Cash Flows (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Change in Cash Held 78 75 82 88 70 126 135 151 143 121 96 67

Closing Cash 3,314 3,389 3,471 3,559 3,629 3,755 3,890 4,041 4,184 4,305 4,400 4,467

Cash Flow Statement ($'000) - 2024

Year Ending Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cash Receipts 293 274 285 312 270 406 384 405 376 338 296 277

Cash Payments (154) (142) (146) (164) (140) (215) (186) (190) (173) (158) (143) (140)

Other Operating Cash Flows (3) (3) (3) (2) (2) (2) (2) (1) (1) (1) (1) (36)

Operating Cash Flows 136 130 136 146 128 189 197 213 202 180 153 102

Capital Expenditure - - - - - - - - - - - -

Other Investing Cash Flows - - - - - - - - - - - -

Investing Cash Flows - - - - - - - - - - - -

Debt Drawdowns/(Repayments) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Equity Raisings/(Buybacks) - - - - - - - - - - - -

Other Financing Cash Flows - - - - - - - - - - - -

Financing Cash Flows (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42) (42)

Change in Cash Held 94 88 95 104 86 148 155 172 160 138 111 60

Closing Cash 4,561 4,649 4,744 4,848 4,935 5,083 5,238 5,409 5,569 5,707 5,818 5,878

Cash Flow Statement ($'000) - 2025

24

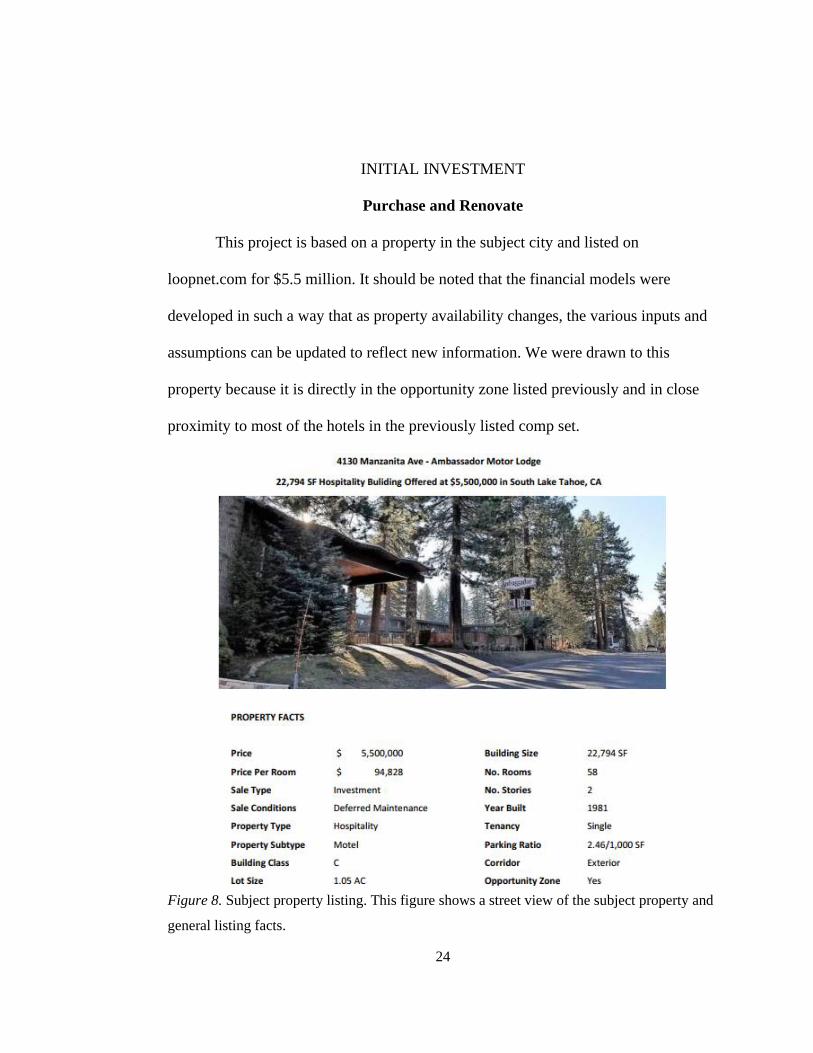

INITIAL INVESTMENT

Purchase and Renovate

This project is based on a property in the subject city and listed on

loopnet.com for $5.5 million. It should be noted that the financial models were

developed in such a way that as property availability changes, the various inputs and

assumptions can be updated to reflect new information. We were drawn to this

property because it is directly in the opportunity zone listed previously and in close

proximity to most of the hotels in the previously listed comp set.

Figure 8. Subject property listing. This figure shows a street view of the subject property and

general listing facts.

25

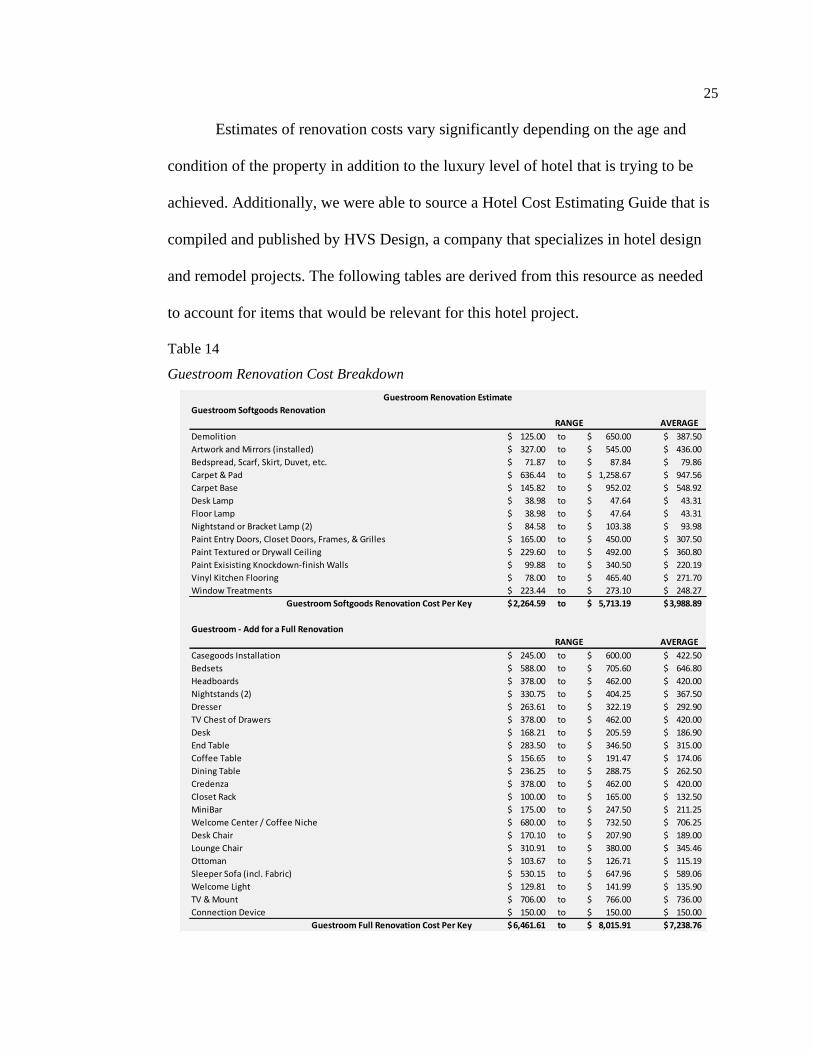

Estimates of renovation costs vary significantly depending on the age and

condition of the property in addition to the luxury level of hotel that is trying to be

achieved. Additionally, we were able to source a Hotel Cost Estimating Guide that is

compiled and published by HVS Design, a company that specializes in hotel design

and remodel projects. The following tables are derived from this resource as needed

to account for items that would be relevant for this hotel project.

Table 14

Guestroom Renovation Cost Breakdown

Guestroom Softgoods Renovation

AVERAGE

Demolition 125.00$ to 650.00$ 387.50$

Artwork and Mirrors (installed) 327.00$ to 545.00$ 436.00$

Bedspread, Scarf, Skirt, Duvet, etc. 71.87$ to 87.84$ 79.86$

Carpet & Pad 636.44$ to 1,258.67$ 947.56$

Carpet Base 145.82$ to 952.02$ 548.92$

Desk Lamp 38.98$ to 47.64$ 43.31$

Floor Lamp 38.98$ to 47.64$ 43.31$

Nightstand or Bracket Lamp (2) 84.58$ to 103.38$ 93.98$

Paint Entry Doors, Closet Doors, Frames, & Grilles 165.00$ to 450.00$ 307.50$

Paint Textured or Drywall Ceiling 229.60$ to 492.00$ 360.80$

Paint Exisisting Knockdown-finish Walls 99.88$ to 340.50$ 220.19$

Vinyl Kitchen Flooring 78.00$ to 465.40$ 271.70$

Window Treatments 223.44$ to 273.10$ 248.27$

Guestroom Softgoods Renovation Cost Per Key 2,264.59$ to 5,713.19$ 3,988.89$

Guestroom - Add for a Full Renovation

AVERAGE

Casegoods Installation 245.00$ to 600.00$ 422.50$

Bedsets 588.00$ to 705.60$ 646.80$

Headboards 378.00$ to 462.00$ 420.00$

Nightstands (2) 330.75$ to 404.25$ 367.50$

Dresser 263.61$ to 322.19$ 292.90$

TV Chest of Drawers 378.00$ to 462.00$ 420.00$

Desk 168.21$ to 205.59$ 186.90$

End Table 283.50$ to 346.50$ 315.00$

Coffee Table 156.65$ to 191.47$ 174.06$

Dining Table 236.25$ to 288.75$ 262.50$

Credenza 378.00$ to 462.00$ 420.00$

Closet Rack 100.00$ to 165.00$ 132.50$

MiniBar 175.00$ to 247.50$ 211.25$

Welcome Center / Coffee Niche 680.00$ to 732.50$ 706.25$

Desk Chair 170.10$ to 207.90$ 189.00$

Lounge Chair 310.91$ to 380.00$ 345.46$

Ottoman 103.67$ to 126.71$ 115.19$

Sleeper Sofa (incl. Fabric) 530.15$ to 647.96$ 589.06$

Welcome Light 129.81$ to 141.99$ 135.90$

TV & Mount 706.00$ to 766.00$ 736.00$

Connection Device 150.00$ to 150.00$ 150.00$

Guestroom Full Renovation Cost Per Key 6,461.61$ to 8,015.91$ 7,238.76$

RANGE

RANGE

Guestroom Renovation Estimate

26

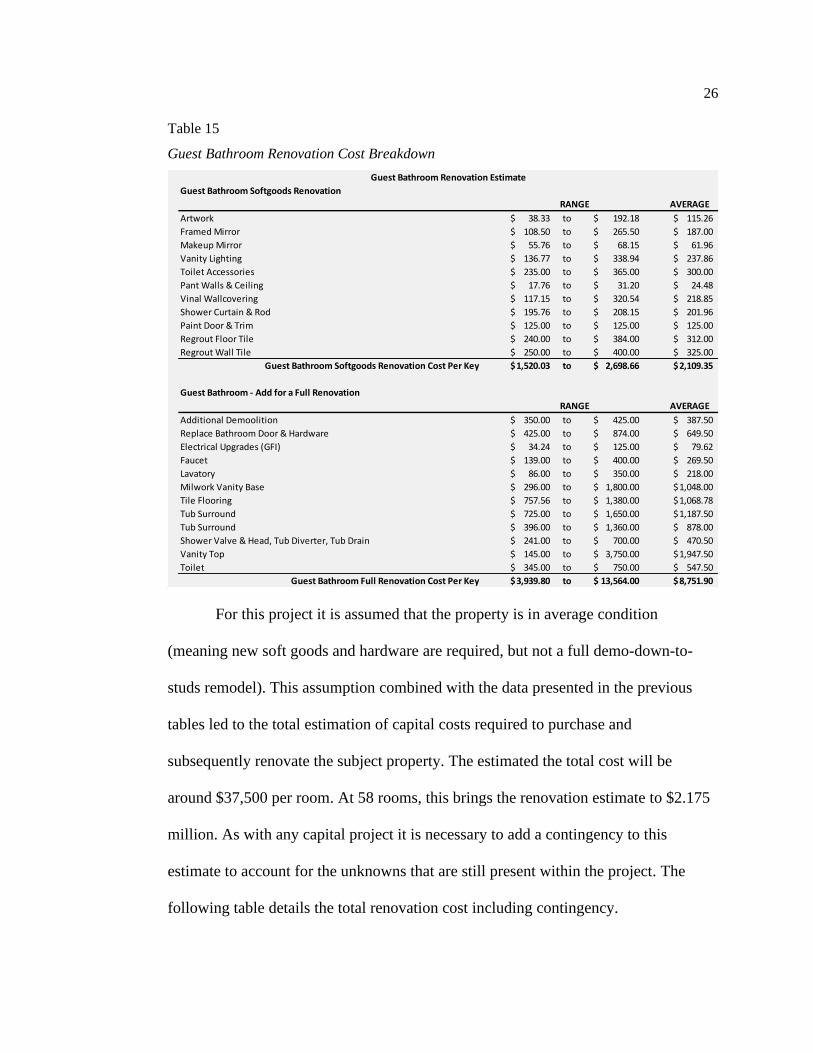

Table 15

Guest Bathroom Renovation Cost Breakdown

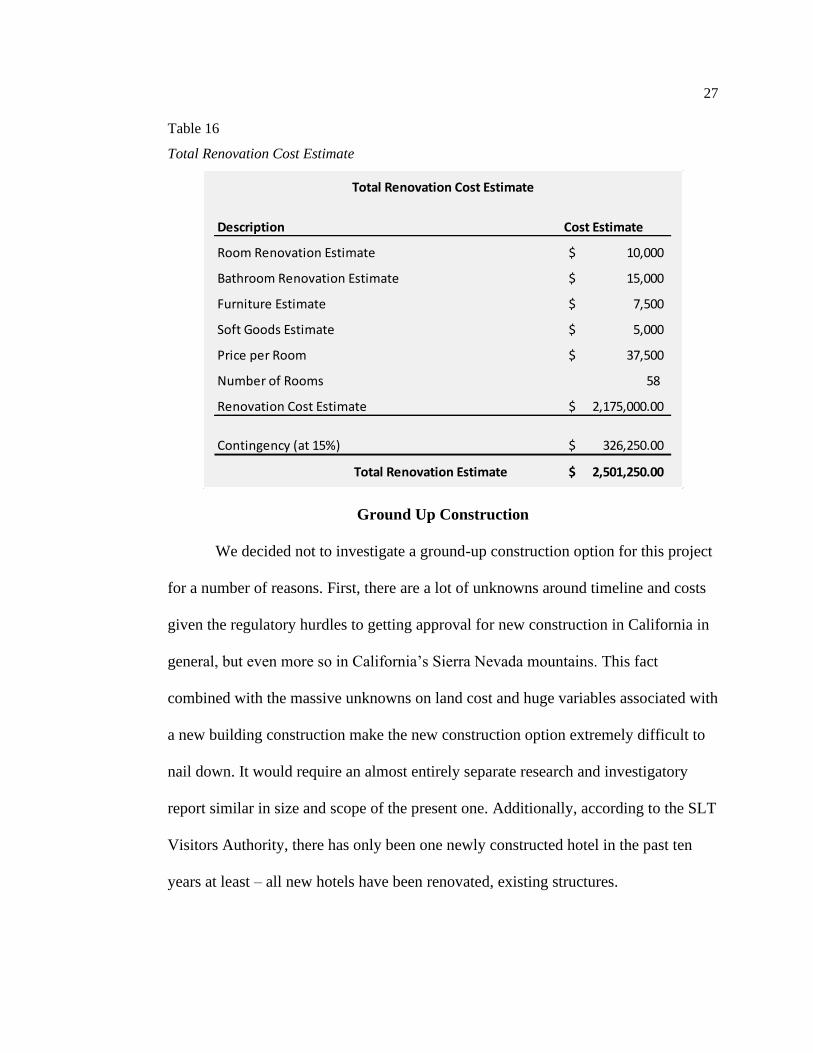

For this project it is assumed that the property is in average condition

(meaning new soft goods and hardware are required, but not a full demo-down-to-

studs remodel). This assumption combined with the data presented in the previous

tables led to the total estimation of capital costs required to purchase and

subsequently renovate the subject property. The estimated the total cost will be

around $37,500 per room. At 58 rooms, this brings the renovation estimate to $2.175

million. As with any capital project it is necessary to add a contingency to this

estimate to account for the unknowns that are still present within the project. The

following table details the total renovation cost including contingency.

Guest Bathroom Softgoods Renovation

AVERAGE

Artwork 38.33$ to 192.18$ 115.26$

Framed Mirror 108.50$ to 265.50$ 187.00$

Makeup Mirror 55.76$ to 68.15$ 61.96$

Vanity Lighting 136.77$ to 338.94$ 237.86$

Toilet Accessories 235.00$ to 365.00$ 300.00$

Pant Walls & Ceiling 17.76$ to 31.20$ 24.48$

Vinal Wallcovering 117.15$ to 320.54$ 218.85$

Shower Curtain & Rod 195.76$ to 208.15$ 201.96$

Paint Door & Trim 125.00$ to 125.00$ 125.00$

Regrout Floor Tile 240.00$ to 384.00$ 312.00$

Regrout Wall Tile 250.00$ to 400.00$ 325.00$

Guest Bathroom Softgoods Renovation Cost Per Key 1,520.03$ to 2,698.66$ 2,109.35$

Guest Bathroom - Add for a Full Renovation

AVERAGE

Additional Demoolition 350.00$ to 425.00$ 387.50$

Replace Bathroom Door & Hardware 425.00$ to 874.00$ 649.50$

Electrical Upgrades (GFI) 34.24$ to 125.00$ 79.62$

Faucet 139.00$ to 400.00$ 269.50$

Lavatory 86.00$ to 350.00$ 218.00$

Milwork Vanity Base 296.00$ to 1,800.00$ 1,048.00$

Tile Flooring 757.56$ to 1,380.00$ 1,068.78$

Tub Surround 725.00$ to 1,650.00$ 1,187.50$

Tub Surround 396.00$ to 1,360.00$ 878.00$

Shower Valve & Head, Tub Diverter, Tub Drain 241.00$ to 700.00$ 470.50$

Vanity Top 145.00$ to 3,750.00$ 1,947.50$

Toilet 345.00$ to 750.00$ 547.50$

Guest Bathroom Full Renovation Cost Per Key 3,939.80$ to 13,564.00$ 8,751.90$

RANGE

RANGE

Guest Bathroom Renovation Estimate

27

Table 16

Total Renovation Cost Estimate

Ground Up Construction

We decided not to investigate a ground-up construction option for this project

for a number of reasons. First, there are a lot of unknowns around timeline and costs

given the regulatory hurdles to getting approval for new construction in California in

general, but even more so in California’s Sierra Nevada mountains. This fact

combined with the massive unknowns on land cost and huge variables associated with

a new building construction make the new construction option extremely difficult to

nail down. It would require an almost entirely separate research and investigatory

report similar in size and scope of the present one. Additionally, according to the SLT

Visitors Authority, there has only been one newly constructed hotel in the past ten

years at least – all new hotels have been renovated, existing structures.

Description Cost Estimate

Room Renovation Estimate 10,000$

Bathroom Renovation Estimate 15,000$

Furniture Estimate 7,500$

Soft Goods Estimate 5,000$

Price per Room 37,500$

Number of Rooms 58

Renovation Cost Estimate 2,175,000.00$

Contingency (at 15%) 326,250.00$

Total Renovation Estimate 2,501,250.00$

Total Renovation Cost Estimate

28

FINANCIALS

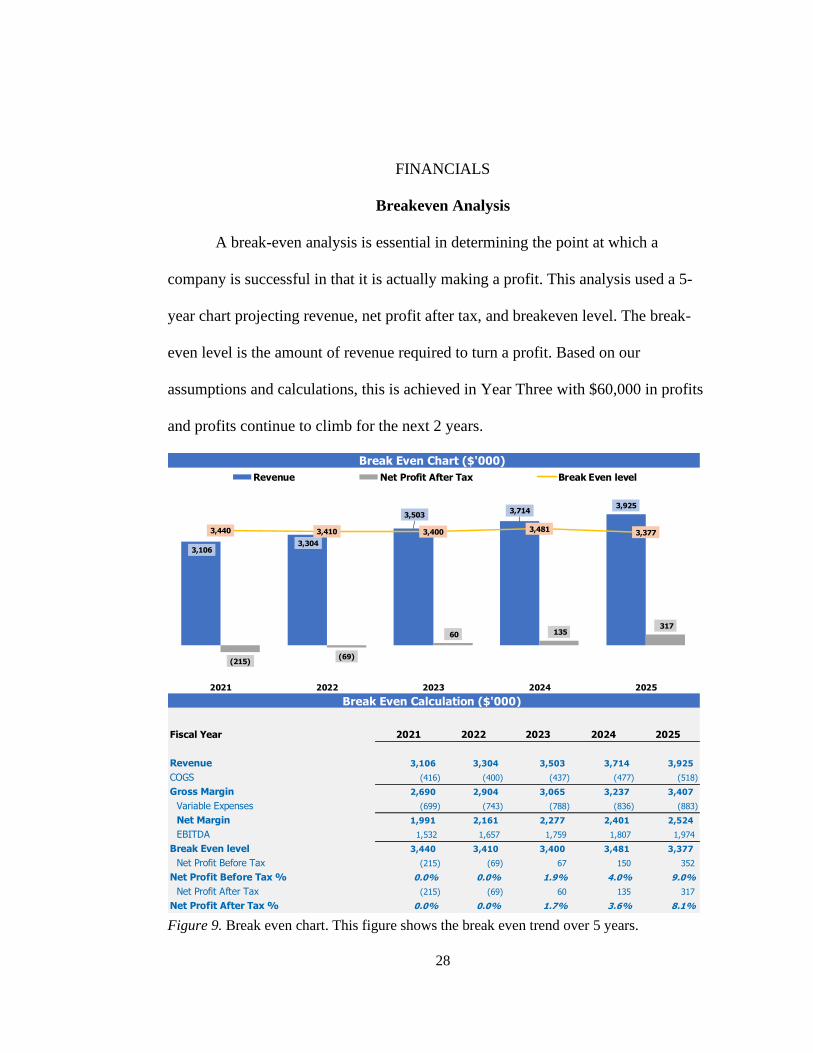

Breakeven Analysis

A break-even analysis is essential in determining the point at which a

company is successful in that it is actually making a profit. This analysis used a 5-

year chart projecting revenue, net profit after tax, and breakeven level. The break-

even level is the amount of revenue required to turn a profit. Based on our

assumptions and calculations, this is achieved in Year Three with $60,000 in profits

and profits continue to climb for the next 2 years.

Figure 9. Break even chart. This figure shows the break even trend over 5 years.

Fiscal Year 2021 2022 2023 2024 2025

Revenue 3,106 3,304 3,503 3,714 3,925

COGS (416) (400) (437) (477) (518)

Gross Margin 2,690 2,904 3,065 3,237 3,407

Variable Expenses (699) (743) (788) (836) (883)

Net Margin 1,991 2,161 2,277 2,401 2,524

EBITDA 1,532 1,657 1,759 1,807 1,974

Break Even level 3,440 3,410 3,400 3,481 3,377

Net Profit Before Tax (215) (69) 67 150 352

Net Profit Before Tax % 0.0% 0.0% 1.9% 4.0% 9.0%

Net Profit After Tax (215) (69) 60 135 317

Net Profit After Tax % 0.0% 0.0% 1.7% 3.6% 8.1%

Break Even Chart ($'000)

Break Even Calculation ($'000)

3,1063,304

3,5033,714

3,925

(215)(69)

60 135 317

3,440 3,410 3,400 3,481 3,377

2021 2022 2023 2024 2025

Revenue Net Profit After Tax Break Even level

29

Fixed and Variable Costs

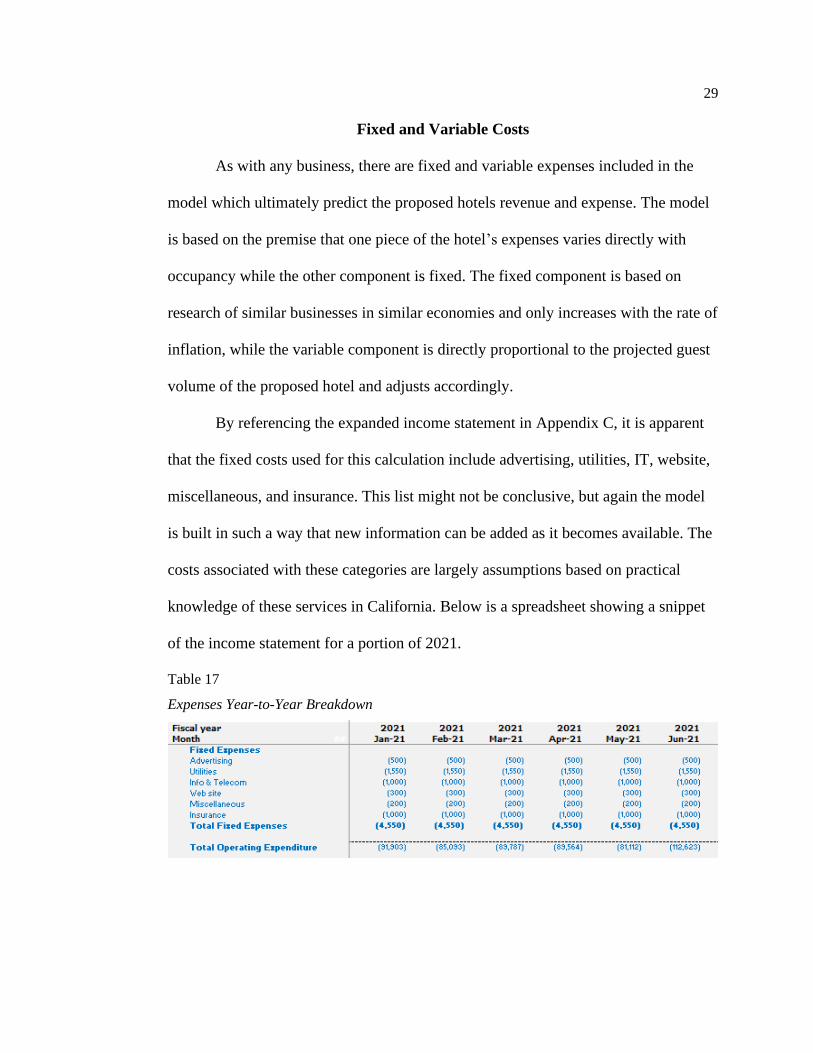

As with any business, there are fixed and variable expenses included in the

model which ultimately predict the proposed hotels revenue and expense. The model

is based on the premise that one piece of the hotel’s expenses varies directly with

occupancy while the other component is fixed. The fixed component is based on

research of similar businesses in similar economies and only increases with the rate of

inflation, while the variable component is directly proportional to the projected guest

volume of the proposed hotel and adjusts accordingly.

By referencing the expanded income statement in Appendix C, it is apparent

that the fixed costs used for this calculation include advertising, utilities, IT, website,

miscellaneous, and insurance. This list might not be conclusive, but again the model

is built in such a way that new information can be added as it becomes available. The

costs associated with these categories are largely assumptions based on practical

knowledge of these services in California. Below is a spreadsheet showing a snippet

of the income statement for a portion of 2021.

Table 17

Expenses Year-to-Year Breakdown

30

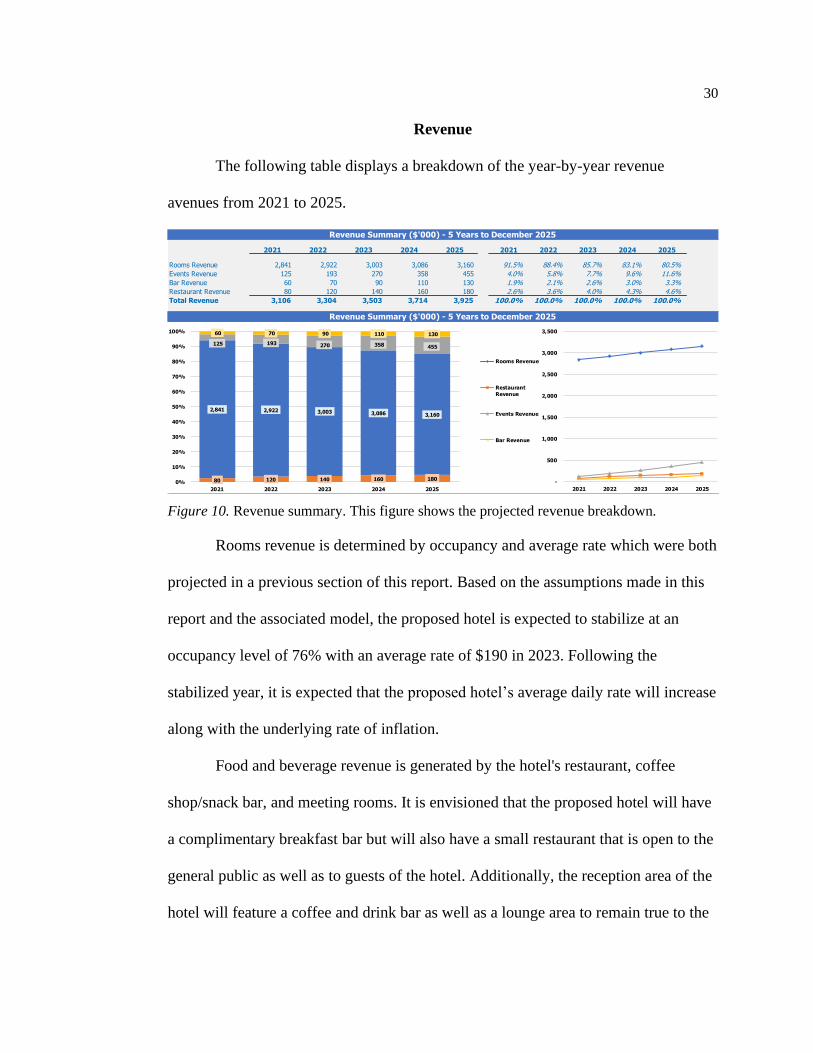

Revenue

The following table displays a breakdown of the year-by-year revenue

avenues from 2021 to 2025.

Figure 10. Revenue summary. This figure shows the projected revenue breakdown.

Rooms revenue is determined by occupancy and average rate which were both

projected in a previous section of this report. Based on the assumptions made in this

report and the associated model, the proposed hotel is expected to stabilize at an

occupancy level of 76% with an average rate of $190 in 2023. Following the

stabilized year, it is expected that the proposed hotel’s average daily rate will increase

along with the underlying rate of inflation.

Food and beverage revenue is generated by the hotel's restaurant, coffee

shop/snack bar, and meeting rooms. It is envisioned that the proposed hotel will have

a complimentary breakfast bar but will also have a small restaurant that is open to the

general public as well as to guests of the hotel. Additionally, the reception area of the

hotel will feature a coffee and drink bar as well as a lounge area to remain true to the

2021 2022 2023 2024 2025 2021 2022 2023 2024 2025

Rooms Revenue 2,841 2,922 3,003 3,086 3,160 91.5% 88.4% 85.7% 83.1% 80.5%

Events Revenue 125 193 270 358 455 4.0% 5.8% 7.7% 9.6% 11.6%

Bar Revenue 60 70 90 110 130 1.9% 2.1% 2.6% 3.0% 3.3%

Restaurant Revenue 80 120 140 160 180 2.6% 3.6% 4.0% 4.3% 4.6%

Total Revenue 3,106 3,304 3,503 3,714 3,925 100.0% 100.0% 100.0% 100.0% 100.0%

Revenue Summary ($'000) - 5 Years to December 2025

Revenue Summary ($'000) - 5 Years to December 2025

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2021 2022 2023 2024 2025

Rooms Revenue

Restaurant

Revenue

Events Revenue

Bar Revenue

80 120 140 160 180

2,841 2,922 3,003 3,086 3,160

125 193 270 358 455

60 70 90 110 130

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2021 2022 2023 2024 2025

31

hotels vision of providing an environment that is conducive to social interactions with

locals and other guests. Meeting rooms will be available to be rented by guests as

well as locals for busines retreats or general business meetings. It is the goal of the

proposed business to feature a large outdoor area that could be used for hosting

unique wedding venues and other celebrations. In addition to providing a source of

revenue, these outlets are expected to serve as an amenity that caters directly to the

intended customer that the proposed hotel seeks to serve.

Profit Margin

Profitability is a key metric that managers, investors, and stakeholders’ review

to determine whether or not a business is successful. There are a number of methods

and tools that may be used to determine the profitability of the proposed hotel. One of

the most reliable indicators of profitability is profit margin and as such, the following

is looking at the projected profit margin for the proposed hotel.

Table 18

Profit Margin

Year Ending 2021 2022 2023 2024 2025

Revenue 3,106 3,304 3,503 3,714 3,925

Growth % 6% 6% 6% 6%COGS (416) (400) (437) (477) (518)

% of Revenue (13%) (12%) (12%) (13%) (13%)

GROSS MARGIN 2,690 2,904 3,065 3,237 3,407

GROSS MARGIN % 87% 88% 88% 87% 87%Variable Expenses (699) (743) (788) (836) (883)

% of Revenue (23%) (23%) (23%) (23%) (23%)Salaries & Wages (387) (391) (403) (415) (427)

% of Revenue (12%) (12%) (11%) (11%) (11%)

Fixed Expenses (55) (56) (57) (59) (60)

% of Revenue (2%) (2%) (2%) (2%) (2%)

EBITDA 1,549 1,714 1,817 1,927 2,036

EBITDA % 50% 52% 52% 52% 52%Depreciation & Amortization (1,600) (1,600) (1,600) (1,600) (1,600)

EBIT (51) 114 217 327 436

Net Interest Expense (147) (127) (92) (57) (22)

Net Profit Before Tax (198) (13) 125 271 414

Tax Expense - - (13) (27) (41)

Net Profit After Tax (198) (13) 113 244 373

Net Profit After Tax % (6%) (0%) 3% 7% 9%

Income Statement ($'000) - 5 Years to December 2025

32

Profit margin is a measure of the fraction of each dollar of sales that makes its

way down through the income statement to profits. In essence, it is simply a reflection

on how efficient the proposed hotel will be in using its resources in its operations.

This is calculated using the data from the income statement. Gross margin is equal to

gross profit divided by gross sales. The Income Statement, shown in Table 18,

indicates that the proposed hotel is expected to have a gross margin in the upper 80%

range given the current operating assumptions.

33

VALUATION

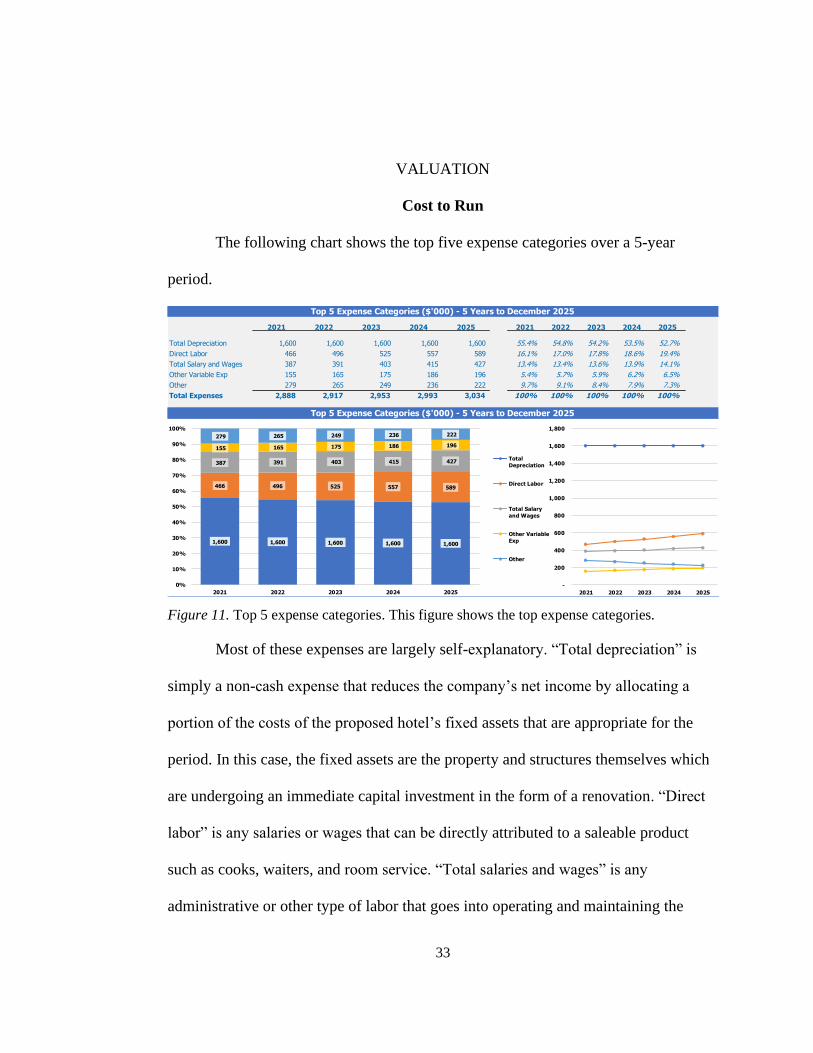

Cost to Run

The following chart shows the top five expense categories over a 5-year

period.

Figure 11. Top 5 expense categories. This figure shows the top expense categories.

Most of these expenses are largely self-explanatory. “Total depreciation” is

simply a non-cash expense that reduces the company’s net income by allocating a

portion of the costs of the proposed hotel’s fixed assets that are appropriate for the

period. In this case, the fixed assets are the property and structures themselves which

are undergoing an immediate capital investment in the form of a renovation. “Direct

labor” is any salaries or wages that can be directly attributed to a saleable product

such as cooks, waiters, and room service. “Total salaries and wages” is any

administrative or other type of labor that goes into operating and maintaining the

2021 2022 2023 2024 2025 2021 2022 2023 2024 2025

Total Depreciation 1,600 1,600 1,600 1,600 1,600 55.4% 54.8% 54.2% 53.5% 52.7%

Direct Labor 466 496 525 557 589 16.1% 17.0% 17.8% 18.6% 19.4%

Total Salary and Wages 387 391 403 415 427 13.4% 13.4% 13.6% 13.9% 14.1%

Other Variable Exp 155 165 175 186 196 5.4% 5.7% 5.9% 6.2% 6.5%

Other 279 265 249 236 222 9.7% 9.1% 8.4% 7.9% 7.3%

Total Expenses 2,888 2,917 2,953 2,993 3,034 100% 100% 100% 100% 100%

Top 5 Expense Categories ($'000) - 5 Years to December 2025

Top 5 Expense Categories ($'000) - 5 Years to December 2025

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2021 2022 2023 2024 2025

Total

Depreciation

Direct Labor

Total Salary

and Wages

Other Variable

Exp

Other

1,600 1,600 1,600 1,600 1,600

466 496 525 557 589

387 391 403 415 427

155 165 175 186 196

279 265 249 236 222

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2021 2022 2023 2024 2025

34