FEASIBILITY STUDY Proposed Extended- StayHotel MARICOPA, ARIZONA SUBMITTED TO:Ms. Denyse Airheart 39700 W Civic Center Plaza Maricopa, Arizona, 85239 +1 (520) 316-6992 PREPARED BY: HVS Consulting & Valuation Division of TS Worldwide, LLC 221 East Indianola Avenue Phoenix, Arizona, 85012 +1 (608) 658-0587 February-2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FEASIBILITY STUDY

ProposedExtended-StayHotel MARICOPA, ARIZONA

SUBMITTED TO:PR OPOSED

Ms. Denyse Airheart 39700 W Civic Center Plaza Maricopa, Arizona, 85239 +1 (520) 316-6992

PREPARED BY:

HVS Consulting & Valuation Division of TS Worldwide, LLC 221 East Indianola Avenue Phoenix, Arizona, 85012 +1 (608) 658-0587

February-2018

March 2, 2018 Ms. Denyse Airheart 39700 W Civic Center Plaza Maricopa, Arizona, 85239

Re: Proposed Extended-Stay Hotel Maricopa, Arizona HVS Reference: 2017022183

Dear Ms. Airheart: Pursuant to your request, we herewith submit our feasibility study pertaining to the above-captioned property. We have inspected the real estate and analyzed the hotel market conditions in the Maricopa, Arizona area. We have studied the proposed project, and the results of our fieldwork and analysis are presented in this report. We have also reviewed the proposed improvements for this site. Our report was prepared in accordance with the Uniform Standards of Professional Appraisal Practice (USPAP), as provided by the Appraisal Foundation. We hereby certify that we have no undisclosed interest in the property, and our employment and compensation are not contingent upon our findings. This study is subject to the comments made throughout this report and to all assumptions and limiting conditions set forth herein.

Sincerely, TS Worldwide, LLC

Ryan Wall, Director [email protected], +1 (608) 658-0587 State Appraiser License (AZ) 32100

HVS PHOENIX - LOS ANGELES OFFICE

221 East Indianaola Avenue Phoenix, Arizona, 85012 +1 (608) 658-0587 +1 (415) 896-0516 FAX

www.hvs.com

Superior results through unrivaled hospitality intelligence. Everywhere.

Table of Contents

SECTION TITLE PAGE

1. Executive Summary 1 Ownership, Franchise, and Management Assumptions 1 Summary of Hotel Market Trends 2 Summary of Forecast Occupancy and Average Rate 6 Summary of Forecast Income and Expense Statement 6 Feasibility Conclusion 9

2. Description of the Site and Neighborhood 12 Physical Characteristics 12 Access and Visibility 13 Airport Access 15 Neighborhood 15 Flood Zone 17 Zoning 19

3. Market Area Analysis 20 Workforce Characteristics 24 Radial Demographic Snapshot 28 Unemployment Statistics 30 Major Business and Industry 31 Office Space Statistics 34 Convention Activity 34 Airport Traffic 37 Tourist Attractions 39

4. Supply and Demand Analysis 46 Definition of Subject Hotel Market 46 National Trends Overview 46 Historical Supply and Demand Data 50 Seasonality 53

Patterns of Demand 56 Primary Competition 59 Secondary Competitors 68 Supply Changes 70 Demand Analysis Using Market Segmentation 71 Base Demand Growth Rates 73 Latent Demand 74 Accommodated Demand and Market-wide Occupancy 76

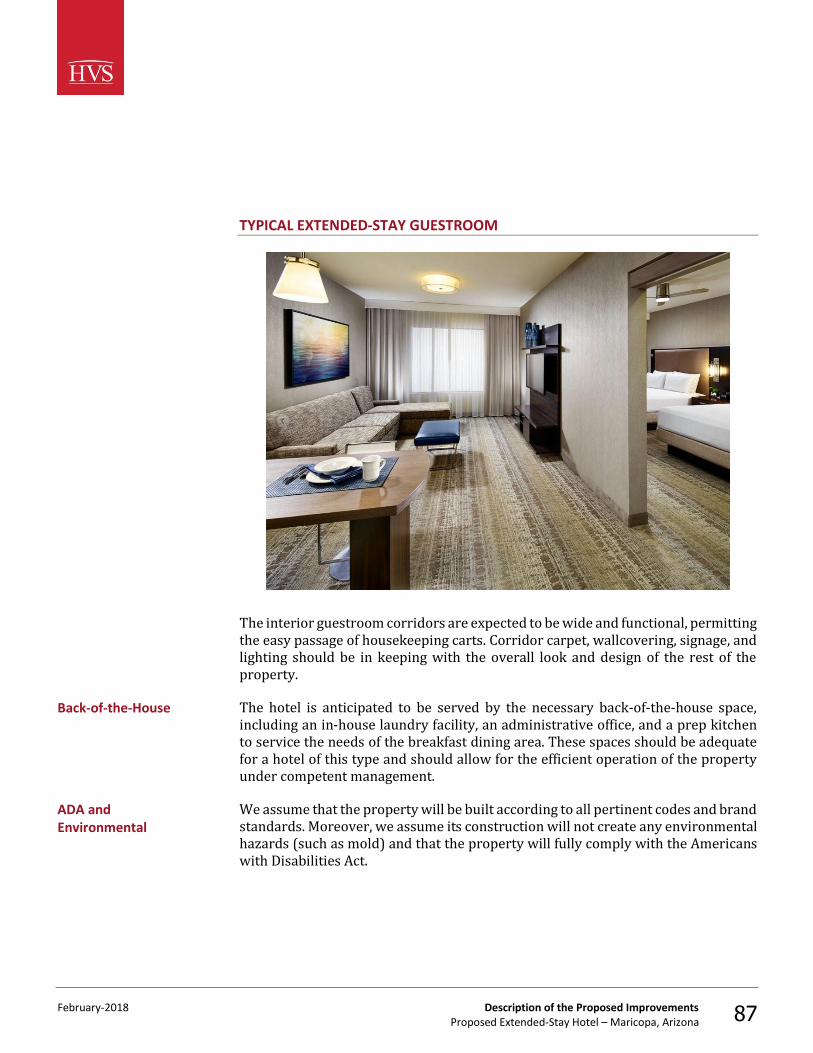

5. Description of the Proposed Improvements 78 Project Overview 78 Summary of the Facilities 81 Site Improvements and Hotel Structure 82 Public Areas 83 Guestrooms 85 Construction Budget 88 Conclusion 88

6. Projection of Occupancy and Average Rate 89 Historical Penetration Rates by Market Segment 89 Forecast of Subject Property’s Occupancy 90 Average Rate Analysis 93 Competitive Position 93

7. Projection of Income and Expense 99 Comparable Operating Statements 99 Forecast of Revenue and Expense 103 Rooms Revenue 106 Other Operated Departments Revenue 106 Miscellaneous Income 106 Rooms Expense 107 Other Operated Departments Expense 107 Administrative and General Expense 108 Information and Telecommunications Systems Expense 108

Marketing Expense 108 Franchise Fee 109 Property Operations and Maintenance 109 Utilities Expense 110 Management Fee 111 Property Taxes 111 Insurance Expense 115 Reserve for Replacement 115 Forecast of Revenue and Expense Conclusion 116

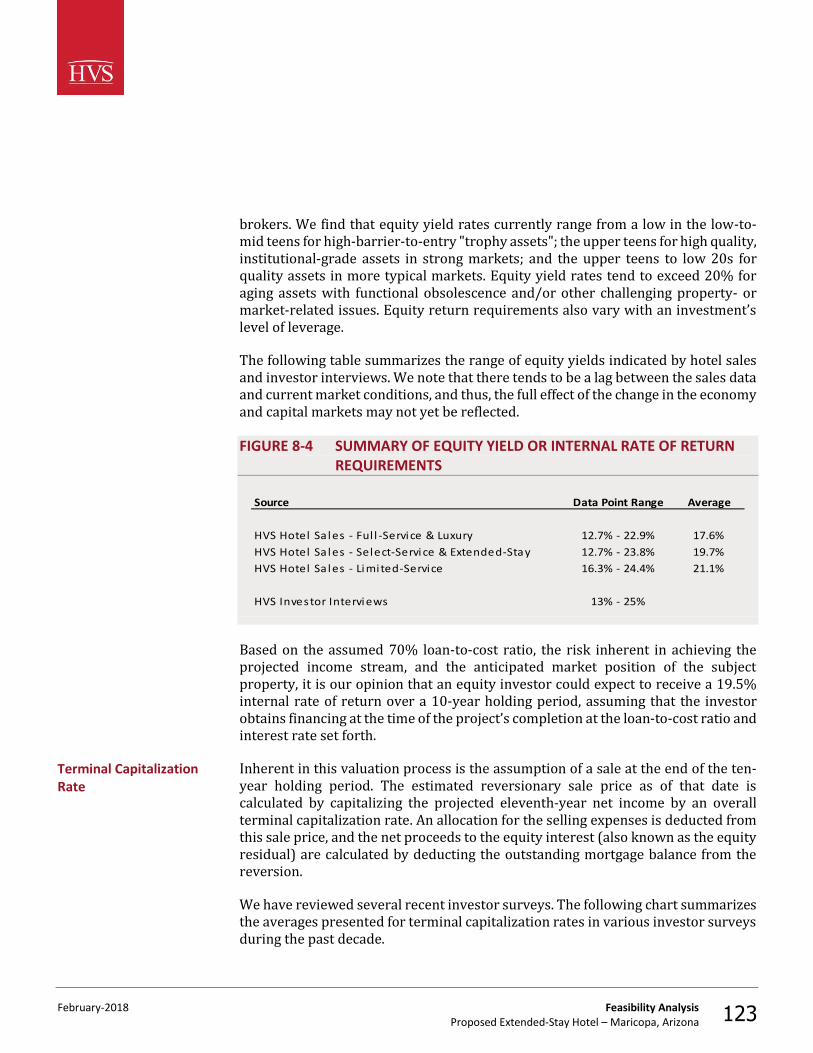

8. Feasibility Analysis 117 Construction Cost Estimate 117 Mortgage Component 118 Equity Component 120 Terminal Capitalization Rate 123 Mortgage-Equity Method 125 Conclusion 127

9. Statement of Assumptions and Limiting Conditions 129 10. Certification 132

Addenda

Qualifications Copy of Appraisal License(s)

Flood Zone Map with Base Flood Elevation Determinations

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 1

1. Executive Summary

We have analyzed the potential performance for a nationally branded, extended-stay hotel that is anticipated to be located along the State Route 347 corridor in Maricopa, Arizona. The property, which is expected to open on July 1, 2020, is recommended to feature 100 rooms, a breakfast dining area, 450 square feet of meeting space, an outdoor pool and whirlpool, a fitness room, a lobby workstation, a market pantry, a guest laundry room, and an outdoor patio and barbecue area. The hotel should also contain the appropriate parking capacity (surface) and all necessary back-of-the-house space. The Maricopa market area does not contain any non-casino, overnight lodging accommodations. Although primarily a residential community, greater Maricopa is home to automotive proving grounds, a USDA research facility, a first-class event center, top recreational facilities, and a growing retail/restaurant sector, including the soon-to-be-completed Edison Pointe shopping complex. While a particular brand has yet to be determined for the proposed subject property, our study assumes that the proposed subject hotel will operate as a nationally branded, upper-midscale to upscale, extended-stay hotel. This hotel is expected to enjoy a location along State Route 347, a major thoroughfare connecting Maricopa to the greater Phoenix region and Pinal County. The subject site’s location is anticipated to be along the State Route 347 corridor in Maricopa, Arizona. The effective date of the report is March 2, 2018. The subject market and select prospective sites were inspected by Ryan M. Wall on November 30, 2017. We note that a specific site for hotel development in the City of Maricopa has not been selected at this time. Several available sites exist along State Route 347 and are considered suitable for hotel development, including a city-owned site next to the Copper Sky Recreational Complex. The forecast and assumptions outlined in this report assume that the proposed hotel will be located favorably within the State Route 347 corridor, which offers easy access to transportation linkages, ancillary commercial uses (retail, restaurant, and entertainment), and demand generators in/around the City of Maricopa. Any deviation from these site assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. Details pertaining to management terms were not yet determined at the time of this report; however, we assume that the proposed hotel will be managed by a professional hotel-operating company, with fees deducted at rates consistent with

Subject of the Feasibility Study

Pertinent Dates

Ownership, Franchise, and Management Assumptions

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 2

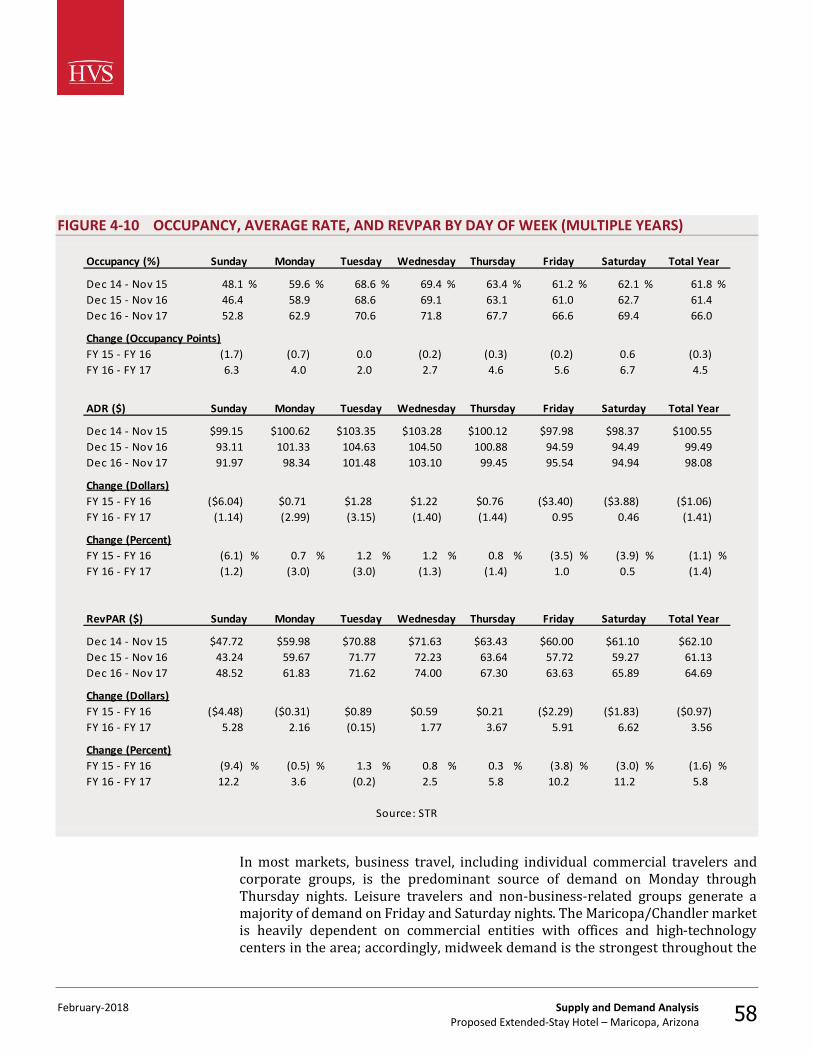

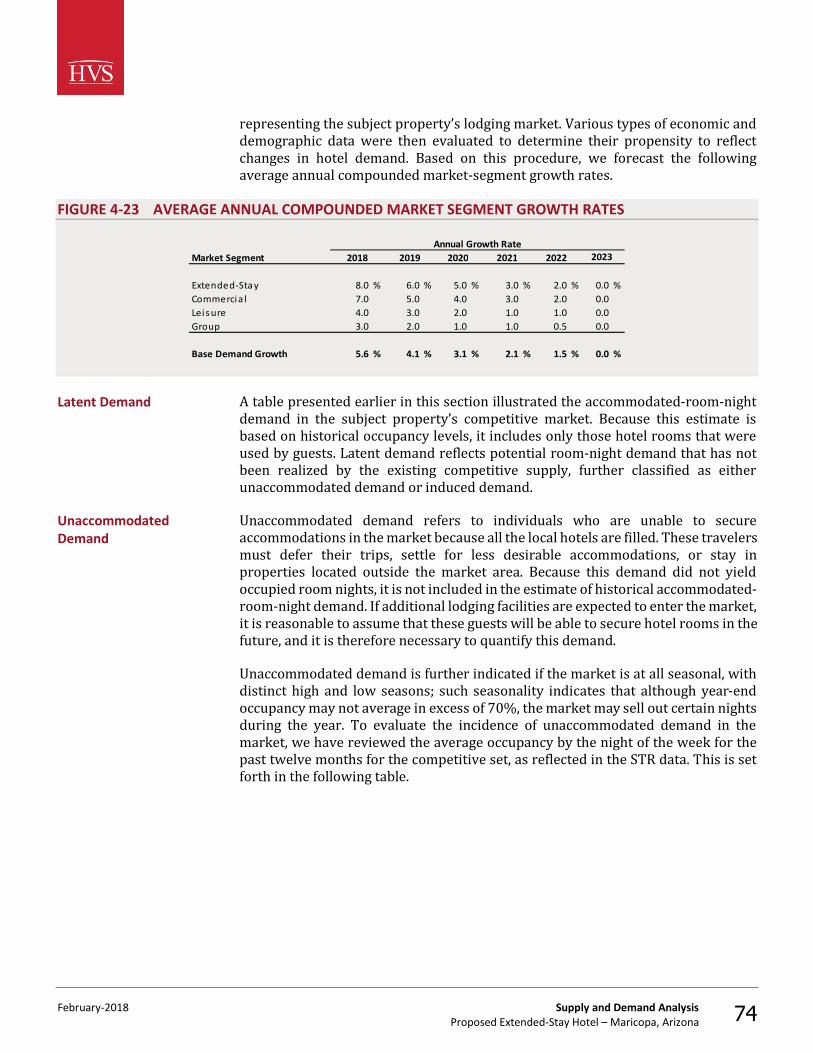

current market standards. We have assumed a market-appropriate total management fee of 3.0% of total revenues in our study. We recommend that the proposed subject property operate as an upper-midscale to upscale, extended-stay hotel. While we have placed heavy consideration on the Home2 Suites by Hilton, Staybridge Suites, and TownePlace Suites by Marriott brands, a specific franchise affiliation and/or brand has yet to be finalized. Our projections reflect a nationally branded, upper-midscale to upscale, extended-stay hotel. Based on our review of the agreement’s terms or expected terms, a typical franchise fee for the aforementioned brands is reflected in our forecasts with a royalty fee of 5.0% of rooms revenue, and a marketing assessment of 3.0% of rooms revenue. Following the Great Recession, RevPAR rose 18.0% in 2011, as increased economic activity along Chandler's nearby Price Road Corridor allowed the greater Chandler submarket to recover at a quicker pace than the rest of region that year. Nonetheless, the majority of the selected competitive set is located along the Interstate 10 Corridor in Chandler, set back from the main concentration of commercial demand in the Price Road Corridor. We note that hotels along the Interstate 10 Corridor in Chandler have historically received compression-related room nights during peak periods of demand given the proximity. However, increased commercial demand along the Price Road Corridor from 2012 through 2014 led to increases in new, non-competitive hotel supply that limited the number of compression-related room nights received for the competitive set. This dynamic led to minimal overall RevPAR growth from 2012 through 2014 for the competitive hotels. In 2015, increased demand associated with Super Bowl XLIX in Phoenix helped area hotels to achieve strong average rate (ADR) growth. However, stronger demand growth, coinciding with improvements in the local and state economies, was not enough to offset the modest post-Super Bowl ADR correction and the openings of the Home2 Suites by Hilton and Best Western Plus in 2016. Strong demand growth continued in the year-to-date 2017 period, with the market realizing a 5.6% increase in overall RevPAR. We note that several of the competitive hotels along the Interstate 10 Corridor in Chandler are older structures that feature dated interiors in some instances. Therefore, these hotels have realized modest ADR erosion in the year-to-date period as they seek to provide a more cost-effective alternative to newer hotels opening in the greater Chandler market. The outlook for this market is cautiously optimistic, despite a large amount of new supply, given major office developments and expansions of high-technology firms, such as Intel and Orbital ATK. The following table provides a historical perspective on the supply and demand trends for a selected set of hotels, as provided by STR.

Summary of Hotel Market Trends

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 3

FIGURE 1-1 HISTORICAL SUPPLY AND DEMAND TRENDS (STR)

YearAverage Daily Room Count

Available Room Nights Change

Occupied Room Nights Change Occupancy

Average Rate Change RevPAR Change

2007 597 217,905 — 161,938 — 74.3 % $108.13 — $80.36 — 2008 597 217,905 0.0 % 141,656 (12.5) % 65.0 112.83 4.3 % 73.35 (8.7) %2009 597 217,905 0.0 115,541 (18.4) 53.0 94.67 (16.1) 50.20 (31.6)2010 597 217,905 0.0 121,624 5.3 55.8 84.30 (10.9) 47.05 (6.3)2011 597 217,905 0.0 139,112 14.4 63.8 86.99 3.2 55.54 18.02012 597 217,905 0.0 129,892 (6.6) 59.6 91.13 4.8 54.32 (2.2)2013 596 217,540 (0.2) 135,871 4.6 62.5 91.71 0.6 57.28 5.42014 596 217,540 0.0 133,929 (1.4) 61.6 93.26 1.7 57.41 0.22015 596 217,540 0.0 135,036 0.8 62.1 100.37 7.6 62.31 8.52016 696 254,035 16.8 157,201 16.4 61.9 99.15 (1.2) 61.35 (1.5)

Year-to-Date Through November2016 685 228,956 — 141,768 — 61.9 % $100.54 — $62.26 — 2017 809 270,206 18.0 % 179,329 26.5 % 66.4 99.10 (1.4) % 65.77 5.6 %

Average Annua l Compounded Change:2007 - 2010 0.0 % (9.1) % (8.0) % (16.3) %2010 - 2016 2.6 4.4 2.7 4.5

Hotels Included in Sample

Fa irfie ld Inn & Suites Phoenix Chandl er Upper Mids ca le Cla s s Primary 64 Dec 1995 Dec 1995Hampton Inn Phoenix Chandler Upper Mids ca le Cla s s Primary 101 Ma y 1997 Ma y 1997Homewood Suites Phoenix Chandler Upsca le Cla s s Primary 83 Apr 1998 Apr 1998La Quinta Inns & Sui tes Phoenix Chandler Mids cale Cla ss Secondary 117 Jun 1998 Jun 1998Hol iday Inn Expres s & Sui tes Phoenix Cha ndler Upper Mids ca le Cla s s Primary 125 Oct 1998 Oct 1998Hol iday Inn & Suites Phoeni x Chandl er Upper Mids ca le Cla s s Secondary 106 Mar 2004 Ma r 2004Home2 Suites Phoenix Chandler Upper Mids ca le Cla s s Primary 126 Jul 2016 Jul 2016Bes t Western Plus Chandler Hotel & Suites Upper Mids ca le Cla s s Secondary 87 Aug 2016 Aug 2016

Total 809

Source: STR

ClassNumber

of RoomsYear

OpenedCompetitive Year

Status Affiliated

The following tables reflect our estimates of operating data for hotels on an individual basis. These trends are presented in detail in the Supply and Demand Analysis chapter of this report.

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 4

FIGURE 1-2 PRIMARY COMPETITORS – OPERATING PERFORMANCE

Est. Segmentation Estimated 2015 Estimated 2016

Property Occ. RevPAR RevPAROccupancy Penetration

Yield Penetration

Homewood Sui tes by Hi l ton Phoenix Chandler 83 35 % 40 % 20 % 5 % 83 65 - 70 % $115 - $120 $75 - $80 83 70 - 75 % $115 - $120 $80 - $85 110 - 120 % 110 - 120 %

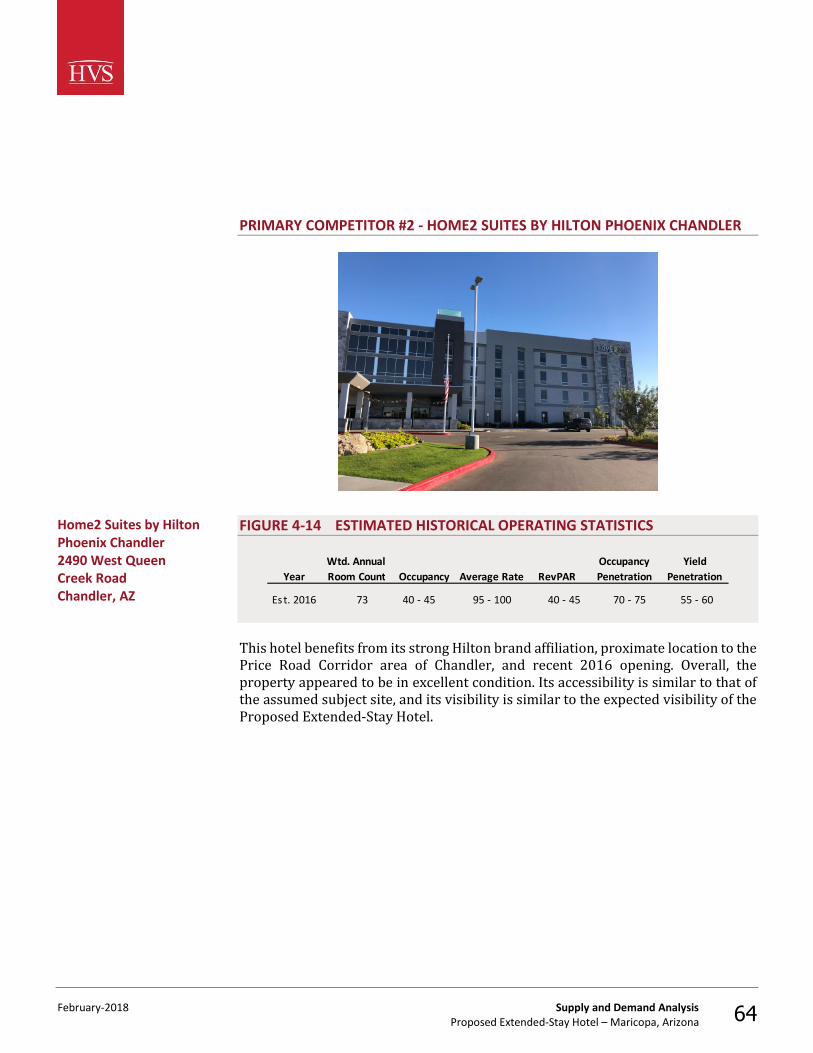

Home2 Sui tes by Hi l ton Phoenix Chandler 126 50 30 15 5 0 — — — 73 40 - 45 95 - 100 40 - 45 70 - 75 55 - 60

Hampton Inn Phoenix Chandler 101 15 50 25 10 101 65 - 70 105 - 110 65 - 70 101 65 - 70 105 - 110 70 - 75 100 - 110 100 - 110

Fa i rfie ld Inn by Marriott Phoenix Chandler 64 15 50 25 10 64 60 - 65 90 - 95 55 - 60 64 60 - 65 90 - 95 55 - 60 100 - 110 80 - 85

Hol iday Inn Express Hotel & Sui tes Phoenix Chandler

125 15 50 25 10 125 60 - 65 90 - 95 60 - 65 125 60 - 65 90 - 95 55 - 60 100 - 110 80 - 85

Sub-Totals/Averages 499 28 % 43 % 21 % 8 % 373 65.6 % $101.97 $66.89 446 62.9 % $101.24 $63.73 101.1 % 90.8 %

Secondary Competi tors 810 7 % 26 % 36 % 30 % 428 60.0 % $129.57 $77.78 475 61.6 % $123.80 $76.30 99.0 % 108.7 %

Totals/Averages 1,309 18 % 35 % 28 % 19 % 801 62.6 % $116.12 $72.71 921 62.3 % $112.75 $70.21 100.0 % 100.0 %

* Specific occupancy and average rate data were utilized in our analysis, but are presented in ranges in the above table for the purposes of confidentiality.

Weighted Annual Room Count

Weighted Annual Room Count Average RateEx

tend

ed-S

tay

Com

mer

cial

Leisu

re

Grou

pNumber of Rooms Average Rate Occ.

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 5

FIGURE 1-3 SECONDARY COMPETITORS – OPERATING PERFORMANCE

Est. Segmentation Estimated 2015 Estimated 2016

Weighted Weighted

Exte

nded

-Sta

y

Com

mer

cial

PropertyNumber of

Rooms Occ. Average Rate RevPAR Occ. Average Rate RevPAR

Best Western Pl us Chandler Hotel & Suites 87 10 % 45 % 35 % 10 % 80 % 0 — % — — 46 60 - 65 % $85 - $90 $50 - $55

La Quinta Inn & Suites Phoeni x Chandl er 117 10 40 40 10 80 94 60 - 65 80 - 85 50 - 55 94 60 - 65 80 - 85 50 - 55

Hol iday Inn & Suites Phoeni x Chandl er 106 10 30 55 5 80 85 45 - 50 115 - 120 55 - 60 85 55 - 60 115 - 120 65 - 70

Sheraton Wi l d Horse Pass Resort & Spa 500 5 15 30 50 50 250 60 - 65 150 - 160 90 - 95 250 60 - 65 140 - 150 90 - 95

Totals/Averages 810 7 % 26 % 36 % 30 % 61 % 428 60.0 % $129.57 $77.78 475 61.6 % $123.80 $76.30

* Specific occupancy and average rate data was utilized in our analysis, but is presented in ranges in the above table for the purposes of confidentiality.

Grou

p

Total Competitive

Level

Weighted Annual Room Count

Weighted Annual Room CountLe

isure

Exte

nded

-Sta

y

Com

mer

cial

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 6

Based on our analysis presented in the Projection of Occupancy and Average Rate chapter, we have chosen to use a stabilized occupancy level of 70% and a base-year rate position of $103.00 for the proposed subject hotel. The following table reflects a summary of our market-wide and proposed subject hotel occupancy and average rate projections.

FIGURE 1-4 MARKET AND SUBJECT PROPERTY AVERAGE RATE FORECAST

Calendar Year 2017 2018 2019 2020 2021 2022 2023 2024 2025

Market ADR $110.84 $111.94 $114.18 $117.61 $121.14 $124.77 $128.51 $132.37 $136.34Projected Ma rket ADR Growth Ra te — 1.0% 2.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

Proposed Subject Property ADR (As-If Stabi l ized) $103.00 $104.03 $106.11 $109.29 $112.57 $115.95 $119.43 $123.01 $126.70ADR Growth Rate — 1.0% 2.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

Proposed Subject Stabi l ized ADR Penetra tion 93% 93% 93% 93% 93% 93% 93% 93% 92.9%

Fiscal Year 2020/21 2021/22 2022/23 2023/24 2024/25 2025/26

Proposed Subject Property Average Ra te $110.92 $114.25 $117.67 $121.21 $124.84 $128.59Opening Discount 2.0% 1.0% 0.0% 0.0% 0.0% 0.0%

Average Rate After Discount $108.70 $114.25 $117.67 $121.21 $124.84 $128.59

Real Avera ge Ra te Growth — 5.1% 3.0% 3.0% 3.0% 3.0%

Market ADR $119.36 $122.94 $126.63 $130.43 $134.34 $138.37Proposed Subject ADR Penetra tion (After Discount) 91% 93% 93% 93% 93% 93%

ADR Expressed in Ba se-Year Dol lars Deflated @ Inflation Rate $100.45 $102.50 $102.50 $102.50 $102.50 $102.50

Our positioning of each revenue and expense level is supported by comparable operations or trends specific to this market. Our forecast of income and expense is presented in the following table.

Summary of Forecast Occupancy and Average Rate

Summary of Forecast Income and Expense Statement

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 7

FIGURE 1-5 DETAILED FORECAST OF INCOME AND EXPENSE

2020/21 Begins July 2021/22 Stabilized 2023/24 2024/25

Number of Rooms: 100 100 100 100 100Occupancy: 62% 67% 70% 70% 70%Average Rate: $108.70 $114.25 $117.67 $121.21 $124.84RevPAR: $67.39 $76.55 $82.37 $84.84 $87.39Days Open: 365 365 365 365 365Occupied Rooms: 22,630 %Gross PAR POR 24,455 %Gross PAR POR 25,550 %Gross PAR POR 25,550 %Gross PAR POR 25,550 %Gross PAR POR OPERATING REVENUERooms $2,460 97.6 % $24,600 $108.71 $2,794 97.8 % $27,940 $114.25 $3,007 97.8 % $30,070 $117.69 $3,097 97.8 % $30,970 $121.21 $3,190 97.8 % $31,900 $124.85Other Operated Departments 34 1.3 339 1.50 36 1.2 357 1.46 37 1.2 372 1.46 38 1.2 383 1.50 39 1.2 395 1.55Miscellaneous Income 27 1.1 271 1.20 29 1.0 285 1.17 30 1.0 298 1.17 31 1.0 307 1.20 32 1.0 316 1.24 Total Operating Revenues 2,521 100.0 25,210 111.40 2,858 100.0 28,582 116.88 3,074 100.0 30,740 120.31 3,166 100.0 31,660 123.91 3,261 100.0 32,611 127.63DEPARTMENTAL EXPENSES *Rooms 568 23.1 5,679 25.10 602 21.6 6,025 24.64 631 21.0 6,314 24.71 650 21.0 6,503 25.45 670 21.0 6,698 26.22Other Operated Departments 30 87.1 295 1.30 31 85.8 306 1.25 32 85.0 316 1.24 33 85.0 326 1.28 34 85.0 336 1.31 Total Expenses 597 23.7 5,974 26.40 633 22.1 6,331 25.89 663 21.6 6,630 25.95 683 21.6 6,829 26.73 703 21.6 7,034 27.53DEPARTMENTAL INCOME 1,924 76.3 19,235 85.00 2,225 77.9 22,251 90.99 2,411 78.4 24,110 94.36 2,483 78.4 24,831 97.19 2,558 78.4 25,577 100.10UNDISTRIBUTED OPERATING EXPENSESAdministrative & General 223 8.9 2,231 9.86 235 8.2 2,350 9.61 245 8.0 2,447 9.58 252 8.0 2,520 9.86 260 8.0 2,596 10.16Info & Telecom Systems 27 1.1 266 1.17 28 1.0 280 1.14 29 0.9 291 1.14 30 0.9 300 1.17 31 0.9 309 1.21Marketing 153 6.1 1,530 6.76 148 5.2 1,477 6.04 140 4.5 1,398 5.47 144 4.5 1,440 5.64 148 4.5 1,483 5.81Franchise Fee 197 7.8 1,968 8.70 224 7.8 2,235 9.14 241 7.8 2,406 9.42 248 7.8 2,478 9.70 255 7.8 2,552 9.99Prop. Operations & Maint. 85 3.4 850 3.76 101 3.5 1,007 4.12 117 3.8 1,165 4.56 120 3.8 1,200 4.70 124 3.8 1,236 4.84Utilities 96 3.8 956 4.23 101 3.5 1,007 4.12 105 3.4 1,049 4.10 108 3.4 1,080 4.23 111 3.4 1,113 4.35 Total Expenses 780 31.1 7,802 34.48 836 29.2 8,358 34.18 876 28.4 8,756 34.27 902 28.4 9,018 35.30 929 28.4 9,289 36.36GROSS HOUSE PROFIT 1,143 45.2 11,434 50.52 1,389 48.7 13,894 56.81 1,535 50.0 15,354 60.09 1,581 50.0 15,813 61.89 1,629 50.0 16,288 63.75Management Fee 76 3.0 756 3.34 86 3.0 857 3.51 92 3.0 922 3.61 95 3.0 950 3.72 98 3.0 978 3.83INCOME BEFORE NON-OPR. INC. & EXP. 1,068 42.2 10,677 47.18 1,304 45.7 13,036 53.31 1,443 47.0 14,432 56.48 1,486 47.0 14,863 58.17 1,531 47.0 15,309 59.92NON-OPERATING INCOME & EXPENSEProperty Taxes 126 5.0 1,262 5.58 159 5.6 1,590 6.50 171 5.6 1,711 6.69 184 5.8 1,840 7.20 190 5.8 1,895 7.42Insurance 27 1.1 275 1.21 28 1.0 283 1.16 29 0.9 291 1.14 30 0.9 300 1.17 31 0.9 309 1.21Reserve for Replacement 50 2.0 504 2.23 86 3.0 857 3.51 123 4.0 1,230 4.81 127 4.0 1,266 4.96 130 4.0 1,304 5.11 Total Expenses 204 8.1 2,041 9.02 273 9.6 2,730 11.17 323 10.5 3,231 12.65 341 10.7 3,407 13.33 351 10.7 3,509 13.73EBITDA LESS RESERVE $864 34.1 % $8,637 $38.16 $1,031 36.1 % $10,306 $42.14 $1,120 36.5 % $11,200 $43.84 $1,146 36.3 % $11,456 $44.84 $1,180 36.3 % $11,801 $46.19

*Departmental expenses are expressed as a percentage of departmental revenues.

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 8

FIGURE 1-6 TEN-YEAR FORECAST OF INCOME AND EXPENSE

2020/21 2021/22 2022/23 2023/24 2024/25 2025/26 2026/27 2027/28 2028/29 2029/30

Number of Rooms: 100 100 100 100 100 100 100 100 100 100Occupied Rooms: 22,630 24,455 25,550 25,550 25,550 25,550 25,550 25,550 25,550 25,550Occupancy: 62% 67% 70% 70% 70% 70% 70% 70% 70% 70%Average Rate: $108.70 % of $114.25 % of $117.67 % of $121.21 % of $124.84 % of $128.59 % of $132.44 % of $136.42 % of $140.51 % of $144.73RevPAR: $67.39 Gross $76.55 Gross $82.37 Gross $84.84 Gross $87.39 Gross $90.01 Gross $92.71 Gross $95.49 Gross $98.36 Gross $101.31OPERATING REVENUERooms $2,460 97.6 % $2,794 97.8 % $3,007 97.8 % $3,097 97.8 % $3,190 97.8 % $3,285 97.8 % $3,384 97.8 % $3,485 97.8 % $3,590 97.8 % $3,698 97.8 %Other Operated Departments 34 1.3 36 1.2 37 1.2 38 1.2 39 1.2 41 1.2 42 1.2 43 1.2 44 1.2 46 1.2Miscellaneous Income 27 1.1 29 1.0 30 1.0 31 1.0 32 1.0 33 1.0 34 1.0 35 1.0 36 1.0 37 1.0 Total Operating Revenues 2,521 100.0 2,858 100.0 3,074 100.0 3,166 100.0 3,261 100.0 3,358 100.0 3,459 100.0 3,563 100.0 3,670 100.0 3,780 100.0DEPARTMENTAL EXPENSES *Rooms 568 23.1 602 21.6 631 21.0 650 21.0 670 21.0 690 21.0 711 21.0 732 21.0 754 21.0 777 21.0Other Operated Departments 30 87.1 31 85.8 32 85.0 33 85.0 34 85.0 35 85.0 36 85.0 37 85.0 38 85.0 39 85.0 Total Expenses 597 23.7 633 22.1 663 21.6 683 21.6 703 21.6 724 21.6 746 21.6 769 21.6 792 21.6 815 21.6DEPARTMENTAL INCOME 1,924 76.3 2,225 77.9 2,411 78.4 2,483 78.4 2,558 78.4 2,634 78.4 2,713 78.4 2,794 78.4 2,878 78.4 2,965 78.4UNDISTRIBUTED OPERATING EXPENSESAdministrative & General 223 8.9 235 8.2 245 8.0 252 8.0 260 8.0 267 8.0 275 8.0 284 8.0 292 8.0 301 8.0Info & Telecom Systems 27 1.1 28 1.0 29 0.9 30 0.9 31 0.9 32 0.9 33 0.9 34 0.9 35 0.9 36 0.9Marketing 153 6.1 148 5.2 140 4.5 144 4.5 148 4.5 153 4.5 157 4.5 162 4.5 167 4.5 172 4.5Franchise Fee 197 7.8 224 7.8 241 7.8 248 7.8 255 7.8 263 7.8 271 7.8 279 7.8 287 7.8 296 7.8Prop. Operations & Maint. 85 3.4 101 3.5 117 3.8 120 3.8 124 3.8 127 3.8 131 3.8 135 3.8 139 3.8 143 3.8Utilities 96 3.8 101 3.5 105 3.4 108 3.4 111 3.4 115 3.4 118 3.4 122 3.4 125 3.4 129 3.4 Total Expenses 780 31.1 836 29.2 876 28.4 902 28.4 929 28.4 957 28.4 985 28.4 1,015 28.4 1,045 28.4 1,077 28.4GROSS HOUSE PROFIT 1,143 45.2 1,389 48.7 1,535 50.0 1,581 50.0 1,629 50.0 1,677 50.0 1,728 50.0 1,779 50.0 1,833 50.0 1,888 50.0Management Fee 76 3.0 86 3.0 92 3.0 95 3.0 98 3.0 101 3.0 104 3.0 107 3.0 110 3.0 113 3.0INCOME BEFORE NON-OPR. INC. & EXP. 1,068 42.2 1,304 45.7 1,443 47.0 1,486 47.0 1,531 47.0 1,576 47.0 1,624 47.0 1,672 47.0 1,723 47.0 1,775 47.0NON-OPERATING INCOME & EXPENSEProperty Taxes 126 5.0 159 5.6 171 5.6 184 5.8 190 5.8 195 5.8 201 5.8 207 5.8 213 5.8 220 5.8Insurance 27 1.1 28 1.0 29 0.9 30 0.9 31 0.9 32 0.9 33 0.9 34 0.9 35 0.9 36 0.9Reserve for Replacement 50 2.0 86 3.0 123 4.0 127 4.0 130 4.0 134 4.0 138 4.0 143 4.0 147 4.0 151 4.0 Total Expenses 204 8.1 273 9.6 323 10.5 341 10.7 351 10.7 361 10.7 372 10.7 383 10.7 395 10.7 407 10.7EBITDA LESS RESERVE $864 34.1 % $1,031 36.1 % $1,120 36.5 % $1,146 36.3 % $1,180 36.3 % $1,215 36.3 % $1,252 36.3 % $1,289 36.3 % $1,328 36.3 % $1,368 36.3 %

1 1 1 1 1 1 1 1 1 1*Departmental expenses are expressed as a percentage of departmental revenues.

% ofGross

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 9

As illustrated, the hotel is expected to stabilize at a profitable level. Please refer to the Forecast of Income and Expense chapter of our report for a detailed explanation of the methodology used in deriving this forecast. The Feasibility Analysis chapter of this report converts these cash flows into a net present value indication assuming set-forth debt and equity requirements. The conclusion of this analysis indicates that an equity investor contributing $3,471,000 (roughly 30% of the $11,600,000 development cost) could expect to receive a 20.3% internal rate of return over a ten-year holding period, assuming that the investor obtains financing at the time of the project’s completion at the loan-to-value ratio and interest rate set forth. The proposed subject hotel has an opportunity to serve an unrepresented niche in the market because the Maricopa area remains underserved by non-casino lodging facilities. Based on our market analysis, there is sufficient market support for the proposed upper-midscale to upscale, extended-stay hotel. Our conclusions are based primarily on the long-term strength of this hotel market. The greater market continues to absorb new supply, and the forecasts related to strong demand and ADR growth indicate that the market should successfully absorb the new supply, including the proposed subject hotel. Our review of investor surveys indicates equity returns ranging from 14.2% to 23.8%, with an average of 19.7%. Based on these parameters, the calculated return to the equity investor, 20.3%, is above the average yet within the range of market-level returns given the anticipated cost of $11,600,000. Based on these parameters, the feasibility of the subject project is confirmed. “Extraordinary Assumption” is defined in USPAP as follows:

An assumption, directly related to a specific assignment, as of the effective date of the assignment results, which, if found to be false, could alter the appraiser’s opinions or conclusions. Comment: Extraordinary assumptions presume as fact otherwise uncertain information about physical, legal, or economic characteristics of the subject property; or about conditions external to the property, such as market conditions or trends; or about the integrity of data used in an analysis.1

The analysis is based on the extraordinary assumption that the described improvements have been completed as of the stated date of opening. The reader should understand that the completed subject property does not yet exist as of the date of this report. Our feasibility study does not address unforeseeable events that could alter the proposed project and/or the market conditions reflected in the analyses; we assume that no significant changes, other than those anticipated and 1 The Appraisal Foundation, Uniform Standards of Professional Appraisal Practice, 2016–2017 ed.

Feasibility Conclusion

Assignment Conditions

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 10

explained in this report, shall take place between the date of inspection and stated date of opening. The use of this extraordinary assumption may have affected the assignment results. We have made no other extraordinary assumptions specific to this feasibility study. However, several important general assumptions have been made that apply to this feasibility study and our studies of proposed hotels in general. These aspects are set forth in the Assumptions and Limiting Conditions chapter of this report. We have assumed the hypothetical condition that the subject site, which has yet to be selected, would be located favorably along the State Route 347 corridor, offering easy access to transportation linkages, ancillary commercial uses (retail, restaurant, and entertainment), and demand generators in/around the City of Maricopa. The reader should understand that the specific subject site has not been chosen, and that any deviation from these site assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. We have assumed no other significant hypothetical conditions. Furthermore, we have not made any jurisdictional exceptions to the Uniform Standards of Professional Appraisal Practice in our analysis or report. This feasibility report is being prepared for use in the development of the proposed subject hotel. The client for this engagement is City of Maricopa. This report is intended for the addressee firm, and may not be distributed to or relied upon by other persons or entities. The methodology used to develop this study is based on the market research and valuation techniques set forth in the textbooks authored by Hospitality Valuation Services for the American Institute of Real Estate Appraisers and the Appraisal Institute, entitled The Valuation of Hotels and Motels,2 Hotels, Motels and Restaurants: Valuations and Market Studies,3 The Computerized Income Approach to Hotel/Motel Market Studies and Valuations,4 Hotels and Motels: A Guide to Market

2 Stephen Rushmore, The Valuation of Hotels and Motels. (Chicago: American Institute of Real Estate Appraisers, 1978). 3 Stephen Rushmore, Hotels, Motels and Restaurants: Valuations and Market Studies. (Chicago: American Institute of Real Estate Appraisers, 1983). 4 Stephen Rushmore, The Computerized Income Approach to Hotel/Motel Market Studies and Valuations. (Chicago: American Institute of Real Estate Appraisers, 1990).

Intended Use of the Feasibility Study

Identification of the Client and Intended User(s)

Scope of Work

February-2018 Executive Summary Proposed Extended-Stay Hotel – Maricopa, Arizona 11

Analysis, Investment Analysis, and Valuations,5 and Hotels and Motels – Valuations and Market Studies.6

1. All information was collected and analyzed by the staff of TS Worldwide, LLC. Information was supplied by the client and/or the property’s development team.

2. The subject site has yet to be selected. However, a potential site located along the State Route 347 corridor has been evaluated from the viewpoint of its physical utility for the future operation of a hotel, as well as access, visibility, and other relevant factors.

3. The subject property's proposed improvements have been reviewed for their expected quality of construction, design, and layout efficiency.

4. The surrounding economic environment, on both an area and neighborhood level, has been reviewed to identify specific hostelry-related economic and demographic trends that may have an impact on future demand for hotels.

5. Dividing the market for hotel accommodations into individual segments defines specific market characteristics for the types of travelers expected to utilize the area's hotels. The factors investigated include purpose of visit, average length of stay, facilities and amenities required, seasonality, daily demand fluctuations, and price sensitivity.

6. An analysis of existing and proposed competition provides an indication of the current accommodated demand, along with market penetration and the degree of competitiveness. Unless noted otherwise, we have inspected the competitive lodging facilities summarized in this report.

7. Documentation for an occupancy and average rate projection is derived utilizing the build-up approach based on an analysis of lodging activity.

8. A detailed projection of income and expense made in accordance with the Uniform System of Accounts for the Lodging Industry sets forth the anticipated economic benefits of the subject property.

9. A feasibility analysis is performed, in which the market equity yield an investor would expect is compared to the equity yield an investor must accept.

5 Stephen Rushmore, Hotels and Motels: A Guide to Market Analysis, Investment Analysis, and Valuations (Chicago: Appraisal Institute, 1992). 6 Stephen Rushmore and Erich Baum, Hotels and Motels – Valuations and Market Studies. (Chicago: Appraisal Institute, 2001).

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 12

2. Description of the Site and Neighborhood

The suitability of the land for the operation of a lodging facility is an important consideration affecting the economic viability of a property and its ultimate marketability. Factors such as size, topography, access, visibility, and the availability of utilities have a direct impact on the desirability of a particular site. We note that a specific site for hotel development in the City of Maricopa has not been selected at this time. Several available sites exist along State Route 347 and are considered suitable for hotel development, including a city-owned site next to the Copper Sky Recreational Complex. The forecast and assumptions outlined in this report assume that the proposed hotel will be located favorably along the State Route 347 corridor, which offers easy access to transportation linkages, ancillary commercial uses (retail, restaurant, and entertainment), and demand generators in/around the City of Maricopa. Any deviation from these site assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. AERIAL PHOTOGRAPH (STATE ROUTE 347 CORRIDOR)

Physical Characteristics

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 13

For the purposes of this study and our forecast, we assume that the topography of the selected site will be generally flat, and that the shape will permit efficient use of the site for building and site improvements, including ingress and egress. We note that a specific site has not been selected yet, and any deviation from our topography and site assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. Upon completion of construction, the subject site is expected to not contain any significant portion of undeveloped land that could be sold, entitled, and developed for alternate use. It is expected that the site will be developed fully with building and site improvements, thus contributing to the overall profitability of the hotel. It is important to analyze the site with respect to regional and local transportation routes and demand generators, including ease of access. The subject site is expected to be readily accessible to a variety of local and county roads, as well as state and interstate highways.

Topography and Site Utility

Access and Visibility

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 14

MAP OF REGIONAL ACCESS ROUTES

Primary regional access through the area is provided by east/west Interstate 10, which extends to such cities as Tucson to the southeast and Los Angeles, California, to the west. North/south Interstate 17 is another major highway, which provides access to Flagstaff to the north and has its southern terminus in Phoenix. State Route 202, or Loop 202/Santan Freeway, forms a beltway around the cities of Tempe, Chandler, Mesa, and Gilbert. State Route 101, or Loop 101, intersects with Loop 202/Santan Freeway in Chandler and in the northeast corner of Tempe; this freeway forms a beltway around the northern cities of Scottsdale, Phoenix, Glendale, and Peoria. State Route 347 connects the City of Maricopa with Interstate 10 to the north and Interstate 8 (via State Route 84) to the south. The subject market is served by a variety of additional local highways, which are illustrated on the map. For the purposes of this study and our forecast, we assume that the chosen site will be accessible via a main arterial roadway and will be relatively simple to locate from the nearest major intersection and highway. The proposed subject hotel is anticipated to have adequate signage at the street, as well as on its façade. We

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 15

assume that the selected site will benefit from very good to excellent accessibility; the proposed hotel is expected to enjoy very good to excellent visibility from within its local neighborhood. Any deviation from our access and visibility assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. The proposed subject hotel will be served by the Sky Harbor International Airport, which is located approximately 30 miles to the north of the assumed area for the subject site, as described previously. Furthermore, we note that the Ak-Chin Regional Airport is a privately owned, public-use airport located approximately 10 miles to the southeast of Maricopa. The neighborhood surrounding a lodging facility often has an impact on a hotel's status, image, class, style of operation, and sometimes its ability to attract and properly serve a particular market segment. This section of the report investigates the subject neighborhood and evaluates any pertinent location factors that could affect its future occupancy, average rate, and overall profitability. The neighborhood that surrounds the assumed area of the subject site is generally defined as the State Route 347 corridor between Smith Enke Road to the north and Farrell Road to the south. The corridor is characterized by a multi-use sports complex, casino resort and entertainment complex, restaurants, and retail shopping centers along the primary thoroughfares, with residential areas located along the secondary roadways. Some specific businesses and entities in the area include Copper Sky Recreational Complex, Harrah’s Ak-Chin Casino Resort, and the Maricopa Amtrak station. Furthermore, restaurants located in this neighborhood include Culver's, Chipotle, and Barros's Pizza; the proximity of these restaurants is considered supportive for the operation of an extended-stay lodging property. While no hotels are currently located within the Maricopa city limits, the Harrah’s Ak-Chin Casino Resort is located in the Ak-Chin Indian Community directly south of Maricopa. In general, this neighborhood is in the growth stage of its life cycle. Notable changes in this neighborhood include increased retail and restaurant development due to the growing population in Maricopa. Vintage Partners began construction on Edison Pointe, a 130,000-square-foot retail development at the northeast corner of Edison Road and State Route 347, in 2017. Tenants include Ross Dress for Less, Burger King, Brakes Plus, Goodwill, Planet Fitness, and Dunkin Donuts; the project is slated to open in early 2018. Work is expected to begin in 2018 on a new road realignment and bridge over the Union Pacific Railroad tracks on the south side of State Route 347. The $55-million project is expected to relieve traffic congestion and encourage development in the southern portion of Maricopa.

Airport Access

Neighborhood

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 16

MAP OF NEIGHBORHOOD

The proposed subject hotel's opening should be a positive influence on the area; the hotel is expected to be in character with and to complement surrounding land uses. Overall, the supportive nature of the development in the immediate area is considered appropriate for and conducive to the operation of a hotel.

The subject site will reportedly be served by all necessary utilities. For the purposes of this study and our forecast, we assume that no extraordinary soil conditions will exist at the selected development site. However, geological and soil reports will need to be conducted to verify these surface conditions once a site is chosen. Any deviation from our soil and subsoil condition assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm.

Utilities

Soil and Subsoil Conditions

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 17

For the purposes of this study and our forecast, we assume that there will not be any site-specific nuisances or hazards, including any ground contaminants. However, a hazardous waste inspection will need to be conducted to verify that no nuisances or hazards exist once a site is chosen. Any deviation from our nuisance and hazard assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. According to the Federal Emergency Management Agency map illustrated below, the assumed subject site is expected to be located in Flood Zone AE.

Nuisances and Hazards

Flood Zone

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 18

COPY OF FLOOD MAP AND COVER

The flood zone definition for the AE designation is as follows: areas of 100-year flood; base flood elevations and flood hazard factors not determined (flood insurance required; refer to FEMA for more specific information on A codes).

February-2018 Description of the Site and Neighborhood Proposed Extended-Stay Hotel – Maricopa, Arizona 19

Additional flood zone information provided by the City of Maricopa has been included in the addenda of this report. Officials at the City of Maricopa Planning Division revealed that a new zoning code was adopted in December 2014. However, the previous zoning districts are recognized as existing zoning within the City, with the new zoning code largely comprising of new overlay details. Based on a review of existing zoning along the State Route 347 corridor, the subject property will likely be in a Commercial Zone or, which could encompass any of the following commercial zoning districts: Neighborhood Commercial (NC), General Commercial (GC), Shopping Center (SC), or General Office (GO). We note that hotel and motel use is allowed in General Commercial and Shopping Center base zoning districts. Additionally, the General Office zoning district requires an administrative use permit before hotel and motel use is permitted, while it is prohibited under the Neighborhood Commercial zoning district. It was mentioned that the State Route 347 corridor falls under the Transportation Corridor overlay, which is not prohibitive to the development of a lodging facility, however, does require additional design standards, such as massing and placement location of building(s). For the purposes of this study and our forecast, we assume that all necessary permits and approvals have been secured (including the appropriate liquor license if applicable) and that the subject property was constructed in accordance with local zoning ordinances, building codes, and all other applicable regulations. Our zoning analysis should be verified before any physical changes are made to the hotel. For the purposes of this study and our forecast, we assume that there will not be any easements attached to the property that would significantly affect the utility of the site or marketability of this project. Any deviation from our easement and encroachment assumptions could potentially alter the feasibility of this project; however, additional analysis would be required to confirm. We have made general assumptions on the issues of size, topography, access, visibility, and the availability of utilities. The subject site is assumed to be located within the State Route 347 corridor, which is the main roadway connecting Maricopa to the surrounding area. Our forecast assumes that the site will be well suited for future hotel use, with acceptable access, visibility, and topography for an effective operation.

Zoning

Easements and Encroachments

Conclusion

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 20

3. Market Area Analysis

The economic vitality of the market area and neighborhood surrounding the subject site is an important consideration in forecasting lodging demand and future income potential. Economic and demographic trends that reflect the amount of visitation provide a basis from which to project lodging demand. The purpose of the market area analysis is to review available economic and demographic data to determine whether the local market will undergo economic growth, stabilize, or decline. In addition to predicting the direction of the economy, the rate of change must be quantified. These trends are then correlated based on their propensity to reflect variations in lodging demand, with the objective of forecasting the amount of growth or decline in visitation by individual market segment (e.g., commercial, meeting and group, and leisure). The market area for a lodging facility is the geographical region where the sources of demand and the competitive supply are located. The subject site is located in the city of Maricopa, the county of Pinal, and the state of Arizona. Maricopa is part of the greater Phoenix MSA economic base. Phoenix is the capital and largest city in the state of Arizona, comprising 15 urban villages that include well-known neighborhoods or districts. Greater Phoenix serves as a hub for aerospace, high-tech, bioscience, advanced business services, and sustainable technologies companies. Forbes Magazine named Phoenix the 15th fastest-growing city in the nation for 2016; however, CBS News recently ranked Phoenix as the third fastest-growing city given the substantial employment increase in the technology industry. Additionally, Realtor.com ranked Phoenix first in the U.S.'s "10 Hottest Housing Markets to Watch in 2017." Tourism is an especially vital part of the economy. With more than 16 million visitors from throughout the United States and Canada annually visiting for the warm weather and sunshine in the Valley of the Sun, Phoenix is an important resort and regional meeting destination. The suburb of Maricopa, home to over 50,000 residents, was incorporated as a city in 2003; today, it features high-capacity utilities, a well-educated workforce, and attractive neighborhoods. As a maturing community on the edge of Metropolitan Phoenix, Maricopa has begun to evolve beyond its bedroom community roots to support growth within the automotive, agri-tech, healthcare, and retail business sectors, further solidifying its growing economic influence in the Pinal County area.

Market Area Definition

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 21

MARICOPA

The subject property’s market area can be defined by its Metropolitan Statistical Area (MSA): Phoenix-Mesa-Scottsdale, AZ MSA. The MSA is the most standard definition used in comparative studies of metropolitan areas. The federal government defines an MSA as a large population nucleus, which, together with adjacent counties, has a higher degree of social integration. The following exhibit illustrates the market area.

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 22

MAP OF MARKET AREA

A primary source of economic and demographic statistics used in this analysis is the Complete Economic and Demographic Data Source published by Woods & Poole Economics, Inc.—a well-regarded forecasting service based in Washington, D.C. Using a database containing more than 900 variables for each county in the nation, Woods & Poole employs a sophisticated regional model to forecast economic and demographic trends. Historical statistics are based on census data and information published by the Bureau of Economic Analysis. Projections are formulated by Woods & Poole, and all dollar amounts have been adjusted for inflation, thus reflecting real change. These data are summarized in the following table.

Economic and Demographic Review

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 23

FIGURE 3-1 ECONOMIC AND DEMOGRAPHIC DATA SUMMARY

Average AnnualCompounded Change

2000 2010 2016 2020 2000-10 2010-16 2016-20

Resident Population (Thousands)Pinal County 181.3 385.7 419.3 456.9 7.8 % 1.4 % 2.2 %Phoenix-Mesa-Scottsdale, AZ MSA 3,273.5 4,209.3 4,650.1 4,996.6 2.5 1.7 1.8State of Ari zona 5,160.6 6,412.0 6,948.7 7,415.5 2.2 1.3 1.6Uni ted States 282,162.4 309,347.1 324,506.9 336,690.4 0.9 0.8 0.9

Per-Capita Personal Income*Pinal County $21,096 $21,959 $24,510 $26,146 0.4 1.8 1.6Phoenix-Mesa-Scottsdale, AZ MSA 35,133 35,360 37,817 40,420 0.1 1.1 1.7State of Ari zona 31,942 33,629 35,985 38,485 0.5 1.1 1.7Uni ted States 36,812 39,622 43,613 46,375 0.7 1.6 1.5

W&P Wealth IndexPinal County 59.0 56.4 57.3 57.4 (0.4) 0.3 0.1Phoenix-Mesa-Scottsdale, AZ MSA 98.6 90.7 88.5 88.8 (0.8) (0.4) 0.1State of Ari zona 90.2 86.2 84.2 84.6 (0.5) (0.4) 0.1Uni ted States 100.0 100.0 100.0 100.0 0.0 0.0 0.0

Food and Beverage Sales (Millions)*Pinal County $113 $209 $262 $295 6.3 3.8 3.0Phoenix-Mesa-Scottsdale, AZ MSA 4,519 6,062 7,560 8,352 3.0 3.7 2.5State of Ari zona 6,682 8,764 10,897 11,984 2.7 3.7 2.4Uni ted States 368,829 447,728 562,999 602,635 2.0 3.9 1.7

Total Retail Sales (Millions)*Pinal County $1,227 $2,405 $2,769 $3,107 7.0 2.4 2.9Phoenix-Mesa-Scottsdale, AZ MSA 48,536 59,852 70,486 77,928 2.1 2.8 2.5State of Ari zona 71,246 85,453 99,155 109,013 1.8 2.5 2.4Uni ted States 3,902,830 4,130,414 4,846,834 5,181,433 0.6 2.7 1.7

* Inflation AdjustedSource: Woods & Poole Economics , Inc.

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 24

The U.S. population has grown at an average annual compounded rate of 0.8% from 2010 through 2016. The county’s population has grown at a quicker pace than the nation’s population; the average annual growth rate of 1.4% between 2010 and 2016 reflects a gradually expanding area. Following this population trend, per-capita personal income increased slowly, at 1.8% on average annually for the county between 2010 and 2016. Local wealth indexes have remained stable in recent years, registering a relatively low 57.3 level for the county in 2016. Food and beverage sales totaled $262 million in the county in 2016, versus $209 million in 2010. This reflects a 3.8% average annual change, which is weaker than the 6.3% pace recorded in the prior decade. Over the long term, the pace of growth is forecast to moderate to a more sustainable level of 3.0%, which is forecast through 2020. The retail sales sector demonstrated an annual increase of 7.0% registered in the decade 2000 to 2010, followed by an increase of 2.4% in the period 2010 to 2016. An increase of 2.9% average annual change is expected in county retail sales through 2020. The characteristics of an area's workforce provide an indication of the type and amount of transient visitation likely to be generated by local businesses. Sectors such as finance, insurance, and real estate (FIRE); wholesale trade; and services produce a considerable number of visitors who are not particularly rate-sensitive. The government sector often generates transient room nights, but per-diem reimbursement allowances often limit the accommodations selection to budget and mid-priced lodging facilities. Contributions from manufacturing, construction, transportation, communications, and public utilities (TCPU) employers can also be important, depending on the company type. The following table sets forth the county workforce distribution by business sector in 2000, 2010, and 2016, as well as a forecast for 2020.

Workforce Characteristics

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 25

FIGURE 3-2 HISTORICAL AND PROJECTED EMPLOYMENT (000S)

Average AnnualCompounded Change

Percent Percent Percent PercentIndustry 2000 of Total 2010 of Total 2016 of Total 2020 of Total

Farm 2.1 4.1 % 2.1 2.9 % 2.6 2.9 % 2.6 2.7 % 0.4 % 3.2 % 0.5 %Forestry, Fi shing, Related Activi ties And Other 0.7 1.4 0.6 0.8 0.6 0.6 0.6 0.6 (1.4) (1.0) 0.7Mining 1.3 2.6 1.5 2.0 1.7 1.8 1.7 1.7 1.5 1.6 0.3Uti l i ties 0.2 0.4 0.3 0.4 0.3 0.3 0.3 0.3 4.8 (0.9) 0.6Cons truction 2.1 4.2 2.8 3.8 4.1 4.6 4.8 4.8 3.0 6.4 3.7Ma nufacturing 3.1 6.1 3.5 4.7 4.4 4.8 4.5 4.6 1.4 3.6 0.8Tota l Trade 6.8 13.5 8.7 11.7 10.6 11.8 11.5 11.7 2.6 3.2 2.1 Wholesa le Tra de 1.2 2.4 1.3 1.8 1.5 1.7 1.5 1.6 0.9 2.4 0.2 Reta i l Trade 5.6 11.1 7.4 10.0 9.1 10.1 10.0 10.1 2.9 3.4 2.4Tra nsportation And Warehous ing 0.7 1.4 1.9 2.6 2.2 2.4 2.4 2.4 10.6 2.2 2.4Informa tion 0.4 0.7 0.8 1.0 1.1 1.2 1.2 1.2 8.0 5.9 1.8Finance And Insurance 0.9 1.9 2.5 3.3 3.2 3.5 3.8 3.8 10.1 4.1 4.4Real Esta te And Renta l And Leas e 1.6 3.1 3.6 4.8 5.2 5.7 5.7 5.8 8.7 6.1 2.4Tota l Services 14.3 28.4 25.3 33.9 32.3 35.9 36.0 36.6 5.9 4.2 2.8

Profes s ional And Technica l Services 1.1 2.2 2.1 2.9 2.7 3.0 2.9 3.0 6.6 4.0 1.9Ma nagement Of Compa nies And Enterpris es 0.2 0.4 0.3 0.4 0.4 0.5 0.5 0.5 5.2 4.9 2.3Administra tive And Waste Services 3.2 6.4 5.6 7.5 7.8 8.7 8.7 8.8 5.6 5.8 2.8Educational Services 0.2 0.5 1.1 1.5 1.8 2.0 2.2 2.3 16.8 8.7 4.9Heal th Care And Socia l Ass i s tance 3.4 6.8 5.9 7.9 6.5 7.2 7.2 7.3 5.5 1.6 2.9Arts , Enterta inment, And Recreation 0.7 1.4 1.5 2.1 1.9 2.1 2.1 2.2 8.0 3.6 2.7Accommodation And Food Services 2.8 5.5 4.4 5.9 5.1 5.7 5.5 5.6 4.8 2.3 2.1Other Services , Except Publ ic Admini stration 2.6 5.1 4.4 5.8 6.1 6.8 6.8 6.9 5.4 5.8 2.9

Tota l Government 16.2 32.2 20.8 27.9 21.8 24.3 23.4 23.8 2.5 0.8 1.8 Federa l Civi l ia n Government 0.9 1.8 1.7 2.3 1.8 2.0 2.0 2.0 6.8 0.7 2.6 Federa l Mi l i tary 0.4 0.8 0.8 1.1 0.8 0.9 0.8 0.9 6.7 0.9 0.1 State And Loca l Government 14.8 29.6 18.2 24.5 19.2 21.3 20.6 20.9 2.1 0.8 1.8

TOTAL 50.2 100.0 % 74.5 100.0 % 89.9 100.0 % 98.4 100.0 % 4.0 % 3.2 % 2.3 %

MSA 1,933.7 — 2,226.8 — 2,559.6 — 2,781.0 — 1.4 % 2.3 % 2.1 %U.S. 165,370.9 — 173,034.7 — 191,870.8 — 203,418.4 — 0.9 1.7 1.5

Source: Woods & Poole Economics , Inc.

2000-2010

2010-2016

2016-2020

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 26

Woods & Poole Economics, Inc. reports that during the period from 2000 to 2010, total employment in the county grew at an average annual rate of 4.0%. This trend was above the growth rate recorded by the MSA and also outpaced the national average. More recently, the pace of total employment growth in the county slowed to 3.2% on an annual average from 2010 to 2016. Of the primary employment sectors, Total Services recorded the highest increase in number of employees during the period from 2010 to 2016, increasing by 6,993 people, or 27.6%, and rising from 33.9% to 35.9% of total employment. Of the various service sub-sectors, administrative and waste services and health care and social assistance were the largest employers. Strong growth was also recorded in the total trade sector, as well as the real estate and rental and lease sector, which expanded by 21.0% and 23.8%, respectively, in the period 2010 to 2016. Forecasts developed by Woods & Poole Economics, Inc. anticipate that total employment in the county will change by 2.3% on average annually through 2020. The trend is above the forecast rate of change for the U.S. as a whole during the same period. The following table illustrates historical and projected employment, households, population and average household income data as provided by REIS for the overall Phoenix market.

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 27

FIGURE 3-3 HISTORICAL & PROJECTED EMPLOYMENT, HOUSEHOLDS, POPULATION, AND HOUSEHOLD INCOME STATISTICS

Year

2004 1,723,370 — 558,346 — 235,688 — 1,417,870 — 3,703,010 — $85,947 — 2005 1,827,300 6.0 % 588,681 5.4 % 244,202 3.6 % 1,475,590 4.1 % 3,847,880 3.9 % 92,844 8.0 %2006 1,902,170 4.1 615,154 4.5 249,376 2.1 1,505,230 2.0 3,968,720 3.1 100,277 8.02007 1,922,100 1.0 621,462 1.0 249,861 0.2 1,523,240 1.2 4,066,440 2.5 101,942 1.72008 1,824,470 (5.1) 596,529 (4.0) 236,857 (5.2) 1,537,000 0.9 4,132,070 1.6 98,433 (3.4)2009 1,689,400 (7.4) 557,971 (6.5) 214,204 (9.6) 1,540,710 0.2 4,179,490 1.1 94,334 (4.2)2010 1,696,070 0.4 560,552 0.5 211,154 (1.4) 1,545,730 0.3 4,225,060 1.1 96,659 2.52011 1,729,230 2.0 568,634 1.4 212,795 0.8 1,570,370 1.6 4,284,870 1.4 99,860 3.32012 1,778,330 2.8 586,535 3.1 216,120 1.6 1,601,110 2.0 4,360,950 1.8 104,939 5.12013 1,829,500 2.9 608,785 3.8 216,469 0.2 1,631,340 1.9 4,436,480 1.7 104,405 (0.5)2014 1,871,900 2.3 621,220 2.0 216,954 0.2 1,659,820 1.7 4,523,680 2.0 109,400 4.82015 1,939,130 3.6 642,504 3.4 219,100 1.0 1,682,860 1.4 4,613,480 2.0 112,920 3.22016 1,995,200 2.9 664,728 3.5 219,935 0.4 1,717,180 2.0 4,714,580 2.2 114,488 1.4

Forecasts2017 2,042,570 2.4 % 678,792 2.1 % 222,171 1.0 % 1,757,190 2.3 % 4,821,830 2.3 % $118,406 3.4 %2018 2,097,350 2.7 695,600 2.5 224,331 1.0 1,799,970 2.4 4,930,770 2.3 123,353 4.22019 2,128,520 1.5 704,218 1.2 224,794 0.2 1,842,110 2.3 5,040,670 2.2 127,453 3.32020 2,139,230 0.5 706,860 0.4 223,135 (0.7) 1,884,600 2.3 5,152,050 2.2 130,908 2.72021 2,168,390 1.4 717,408 1.5 222,917 (0.1) 1,928,290 2.3 5,267,980 2.3 134,874 3.0

Average Annual Compound Change2004 - 2016 1.2 % 1.5 % (0.6) % 1.6 % 2.0 % 2.4 %2004 - 2007 3.7 3.6 2.0 2.4 3.2 5.92007 - 2010 (4.1) (3.4) (5.5) 0.5 1.3 (1.8)2010 - 2016 2.7 2.9 0.7 1.8 1.8 4.3

Forecast 2017 - 2021 1.5 % 1.4 % 0.1 % 2.4 % 2.2 % 3.3 %

Household Avg. Income % Chg

Source: REIS Report, 3rd Quarter, 2017

Households % Chg PopulationIndustrial

Employment % ChgTotal

Employment % Chg % Chg% ChgOffice

Employment

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 28

For the Phoenix market, of the roughly 2,000,000 persons employed, 33% are categorized as office employees, while 11% are categorized as industrial employees. Total employment decreased by an average annual compound rate of -4.1% during the recession of 2007 to 2010, followed by an increase of 2.7% from 2010 to 2016. By comparison, office employment reflected compound change rates of -3.4% and 2.9%, during the same respective periods. Total employment is expected to expand by 2.4% in 2017, while office employment is forecast to expand by 2.1% in 2017. From 2017 through 2021, REIS anticipates that total employment will expand at an average annual compound rate of 1.5%, while office employment will expand by 1.4% on average annually during the same period. The number of households is forecast to expand by 2.4% on average annually between 2017 and 2021. Population is forecast to expand during this same period, at an average annual compounded rate of 2.2%. Household average income is forecast to grow by 3.3% on average annually from 2017 through 2021. The following table reflects radial demographic trends for our market area measured by three points of distance from the subject site.

Radial Demographic Snapshot

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 29

FIGURE 3-4 DEMOGRAPHICS BY RADIUS

Population2022 Projection 12,043 47,479 55,8132017 Estimate 10,818 42,788 50,2862010 Census 8,951 35,759 41,9052000 Census 337 1,007 1,895

Percent Change: 2017 to 2022 11.3% 11.0% 11.0%Percent Change: 2010 to 2017 20.9% 19.7% 20.0%Percent Change: 2000 to 2010 2556.1% 3451.0% 2111.4%

Households2022 Projection 3,546 14,794 17,4482017 Estimate 3,224 13,483 15,8772010 Census 2,769 11,724 13,7122000 Census 103 298 504

Percent Change: 2017 to 2022 10.0% 9.7% 9.9%Percent Change: 2010 to 2017 16.4% 15.0% 15.8%Percent Change: 2000 to 2010 2588.4% 3834.2% 2620.6%

Income2017 Est. Average Household Income $75,935 $76,880 $76,5412017 Est. Median Household Income 65,760 65,867 65,585

2017 Est. Civ. Employed Pop 16+ by OccupationArchi tecture/Engineering 146 539 637Arts/Des ign/Entertainment/Sports /Media 68 203 250Bui lding/Grounds Cleaning/Maintenance 77 503 590Busines s/Financia l Operations 180 690 780Community/Social Services 85 291 338Computer/Mathematica l 141 849 1,013Cons truction/Extraction 81 343 547Education/Training/Library 240 1,101 1,262Farming/Fishing/Fores try 175 356 395Food Preparation/Serving Related 245 973 1,178Heal thcare Practitioner/Technician 281 1,052 1,214Heal thcare Support 76 197 251Ins ta l la tion/Maintenance/Repai r 209 682 791Legal 6 134 154Li fe/Physical /Socia l Science 10 97 115Management 454 1,746 2,000Office/Adminis trative Support 739 3,048 3,602Production 206 1,015 1,159Protective Services 259 797 879Sa les /Related 474 2,122 2,480Persona l Care/Service 305 972 1,201Trans portation/Materia l Moving 164 1,101 1,414

0.00 - 1.00 miles 0.00 - 3.00 miles 0.00 - 5.00 miles

Source: Envi ronics Ana lytics

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 30

This source reports a population of 50,286 within a five-mile radius of the subject site, and 15,877 households within this same radius. Average household income within a five-mile radius of the subject site is currently reported at $76,541, while the median is $65,585. The following table presents historical unemployment rates for the proposed subject hotel’s market area. FIGURE 3-5 UNEMPLOYMENT STATISTICS

Year

2007 4.6 % 3.3 % 3.9 % 4.6 %2008 7.4 5.5 6.2 5.82009 12.3 9.3 9.9 9.32010 10.7 9.6 10.4 9.62011 9.8 8.6 9.5 8.92012 8.5 7.4 8.3 8.12013 8.1 6.7 7.7 7.42014 7.0 5.9 6.8 6.22015 6.3 5.2 6.0 5.32016 5.5 4.6 5.3 4.9

Recent Month - Dec2016 4.9 % 4.1 % 4.7 % 4.7 %2017 4.7 3.9 4.6 4.1

* Letters shown next to data points (i f any) reflect revised population controls and/or model re-estimation implemented by the BLS.

Source: U.S. Bureau of Labor Statis tics

MSACounty State U.S.

Current U.S. unemployment levels are now firmly below the annual averages of the last economic cycle peak of 2006 and 2007, when annual averages were 4.6%. National unemployment registered 4.1% in the final three months of 2017, roughly six points below the October 2009 peak of 10.0%. Total nonfarm payroll employment increased by 252,000 and 148,000 jobs in November and December of 2017, respectively. The highest gains were made in the professional and healthcare, manufacturing, and construction sectors. Unemployment has remained under the 5.0% mark since May 2016, reflecting a trend of relative stability and the overall strength of the U.S. economy. Locally, the unemployment rate was 5.5% in 2016; for this same area in 2017, the most recent month’s unemployment rate was registered at 4.7%, versus 4.9% for

Unemployment Statistics

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 31

the same month in 2016. Unemployment rose in 2008 as the region entered an economic slowdown, and this trend continued through 2010 as the height of the national recession took hold. However, unemployment declined in 2011 as the economy rebounded, a trend that continued through 2016. The most recent comparative period illustrates improvement, indicated by the lower unemployment rate in the latest available data. Economic development officials expect the county's unemployment rate to continue to fall, concurrent with the anticipated improvements in economic conditions through the near term and planned expansions at several major employers. Providing additional context for understanding the nature of the regional economy, the following table presents a list of the major employers in the subject property’s market. FIGURE 3-6 MAJOR EMPLOYERS

Number ofRank Firm Employees

1 Harrah's Ak-Chin Cas ino Resort 7702 Maricopa Uni fied School District 6503 Ci ty of Maricopa 3404 UltraStar Multi ta inment Center 2605 Walmart 2506 Volkswagen Proving Grounds 2007 Fry's Food Stores 2008 Pinal County Community Col lege 1869 USDA Arid-Land Research Center 9010 Bas ha 's 8511 Legacy Tradi tiona l School 8012 Native New Yorker 75

Source: Ci ty of Maricopa, 2017

The following bullet points highlight major demand generators for this market: • Volkswagen (VW) of America: VW’s Arizona proving grounds serve as a

worldwide, hot weather, testing location. VW test groups from around the world come to the facility for anywhere from a few days to weeks at a time, with the facility itself capable of hosting up to 150 individuals across multiple test teams. In 2017, it was estimated that the facility generated nearly 12,000 room nights for the competitive submarket. Given the facility’s specialization in hot-weather testing, room-night demand related to test teams is highest from mid-April

Major Business and Industry

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 32

through October. It was mentioned that test teams have the option to choose their own accommodations from a pre-approved list of lodging providers (across all brands). The most popular hotel selection from the list was reported to be the Sheraton Wild Horse Pass given its proximity to Maricopa and the number of associated retail, dining, and entertainment options nearby. Estimated room rates paid throughout the year were thought to be anywhere from $80 to $130 in the summer, and over $150 in the winter and spring. It was noted that the Sheraton can often accommodate these extended-stay room nights by offering a hospitality suite in the mornings and evenings, as well as an outdoor barbecue area for grilling.

• Nissan Technical Center North America - Arizona Testing Center: Similarly, Nissan’s Arizona proving grounds serve as a hot-weather test track for Nissan and its third-party automotive-part manufacturers. Officials with Nissan confirmed that the facility generates anywhere from 5,000 to 7,500 room nights annually, with demand highest from May through October, with June, July, and August being the busiest. The average length of stay was estimated to be one week, with some overseas travelers from Japan staying for two to three weeks. Travelers to the facility are encouraged by Nissan to choose overnight accommodations from a list of preferred hotels in the area (across all brands), including the Sheraton Wild Horse Pass, as well as limited-service and extended-stay hotels in Chandler along Interstate 10. It was mentioned that any planned hotel for the community should provide a complimentary breakfast, guestrooms with a microwave and a refrigerator, as well as good linkages to ancillary restaurants and entertainment options.

• Apex Motor Club: Currently under construction, the $25-million, 280-acre racetrack and motor club are expected to open near Maricopa in 2019. The facility will have indoor and outdoor restaurants, lounges, game rooms, a fitness center, a fuel station, and an auto shop. Two-hundred vehicle "condominiums," or garages, will also be available for those who want to store their rides at the track. Officials noted that the members-only club already has 66 members and is anticipated to cap out at a target membership base of 400. Most of the members are expected to be either full-time or part-time Phoenix area residents, which would largely preclude their need for overnight accommodations in Maricopa. However, Apex is in talks with several car manufacturers to bring a school to the site that would be open to the public. Often manufacturers of high-end sports cars will offer a free class to their customers as an incentive to purchase the vehicle. Since customers must travel for these classes, they often choose to expand the single free class to the full three- or four-day course. If such a facility were to open at the Apex in Maricopa, it was reported that anywhere from 5,000 to 10,000 students would be served annually.

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 33

• U.S. Arid Land Agricultural Research Center (USDA ARS): Management at the USDA ARS indicated that its room-night needs are minimal throughout the year. When accommodations are needed, it is typically for research scientists traveling to the area for anywhere from one day to a week at a time. It was noted that the University of Arizona (a collaborator at the facility) has an onsite dorm facility that will often house many of the people coming in to the facility. No changes were anticipated in terms of room-night demand because the federal discretionary programs that are used to support the facility have either experienced no growth or have declined in recent years.

• Amtrak – Maricopa Station (MRC): The Maricopa Station is the closest Amtrak train station to the Phoenix Metropolitan Area. The station serves as a location for the Sunset Limited (tri-weekly Orlando-New Orleans-Tucson-Los Angeles) and Texas Eagle (daily Chicago-Dallas-San Antonio with through car service tri-weekly via the Sunset Limited to Los Angeles, with stops in Benson, Tucson, Maricopa, and Yuma) national rail networks. According to Amtrak’s 2017 Fiscal Year data, the Maricopa Station was the third busiest location in the state behind Flagstaff and Tucson.

FIGURE 3-7 AMTRAK SERVICE AND RIDERSHIP - ARIZONA

Fiscal Year 2017

Total*

* Up 2.4% from FY16

4,1872,036

111,242

WilliamsYumaWinslowBenson

39,80329,14611,8499,9449,6724,605

Flagstaff

Boardings & AlightingsCity

TucsonMaricopaKingman

The fast-developing Pinal County region of Metropolitan Phoenix, including Maricopa, has grown significantly over the past several years as a result of its diversifying economy and developments in the automotive, agri-tech, healthcare, and retail business sectors. Major companies such as Nissan and VW maintain a strong presence in Maricopa, while the retail sector further supports the local

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 34

economy. Additionally, according to the University of Arizona Economics and Business Research Center, economic indicators associated with the Phoenix metropolitan area are expected to register growth over the next few years. Trends in occupied office space are typically among the most reliable indicators of lodging demand, as firms that occupy office space often exhibit a strong propensity to attract commercial visitors. Thus, trends that cause changes in vacancy rates or occupied office space may have a proportional impact on commercial lodging demand and a less direct effect on meeting demand. The following table details office space statistics for the pertinent market area.

FIGURE 3-8 OFFICE SPACE STATISTICS – MARKET OVERVIEW

Submarket

1 North Centra l 57 3,506,000 2,794,300 20.3 % $22.622 East Centra l 47 2,797,000 1,974,700 29.4 24.133 Northwest 160 7,956,000 5,943,100 25.3 20.564 Tempe 166 10,267,000 8,357,300 18.6 23.865 Scottsda le 282 15,851,000 12,284,500 22.5 28.356 Mesa/Chandler 176 7,662,000 5,501,300 28.2 22.997 West 40 1,866,000 1,190,500 36.2 19.968 Uptown 85 9,549,000 7,123,600 25.4 21.889 Downtown 38 6,147,000 4,763,900 22.5 32.76

10 Camelback 149 9,811,000 7,789,900 20.6 27.80

Totals and Averages 1,200 75,412,000 57,723,100 23.5 % $25.21

Inventory Occupied Office Space

Vacancy Rate

Average Asking Lease RateBuildings Square Feet

Source: REIS Report, 3rd Quarter, 2017

The greater Phoenix market comprises a total of 75.4 million square feet of office space. For the 3rd Quarter of 2017, the market reported a vacancy rate of 23.5% and an average asking rent of $25.21. The subject property is located in the greater Mesa/Chandler submarket (as defined by REIS), which houses 7,662,000 square feet of office space. The submarket's vacancy rate of 28.2% is above the overall market average. The average asking lease rate of $22.99 is below the average for the broader market. A convention center serves as a gauge of visitation trends to a particular market. Convention centers also generate significant levels of demand for area hotels and serve as a focal point for community activity. Typically, hotels within the closest proximity to a convention center—up to three miles away—will benefit the most.

Office Space Statistics

Convention Activity

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 35

Hotels serving as headquarters for an event benefit the most by way of premium rates and hosting related banquet events. During the largest of conventions, peripheral hotels may benefit from compression within the city as a whole. Due to its location, geography, and climate, the greater Phoenix area is a major convention destination. Convention activity generated by the Phoenix Convention Center predominately affects the Downtown Phoenix submarket. Nevertheless, during peak periods and for citywide conventions generating more than 30,000 room nights, a marginal amount of overflow demand is directed to Scottsdale and other outlying areas of the greater metropolitan area. The $600-million expansion of the Phoenix Convention Center, which opened in January 2009, was a cooperative effort between the City of Phoenix and the State of Arizona that nearly tripled the size of the previous facility. The facility is now one of the 20 largest convention centers in the country. The western Executive Conference Center building received a LEED Silver Certification from the U.S. Green Building Council; the rooftop contains 732 thin-film solar panels. In addition to the Convention Center, events can be held at Symphony Hall, a 2,312-seat concert hall, and the 1,364-seat Orpheum Theatre. The METRO light rail operates a westbound line that runs in between the north and south buildings and an eastbound line along the southern boundary of the site; the METRO connects the Phoenix Convention Center to the Sky Harbor International Airport.

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 36

CONVENTION CENTER

The following table illustrates recent use statistics for this facility. FIGURE 3-9 CONVENTION CENTER STATISTICS

Percent PercentYear Change Change

2010 62 — 237,974 — 2011 52 (16.1) % 244,744 2.8 %2012 61 17.3 191,501 (21.8)2013 42 (31.1) 151,249 (21.0)2014 57 35.7 203,180 34.32015 66 15.8 248,678 22.42016 65 (1.5) 221,378 (11.0)

Source: Phoenix Convention Center

Number of Conventions

Number of Delegates

These data illustrate a strong 2009, following the expansion of the facility. However, the recession, negative press regarding corporate travel to luxury destinations, and

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 37

the controversial SB 1070 immigration law resulted in the cancelation of some group events, which led to a decline of the number of conventions and room nights in 2010 and 2011. While delegate attendance also decreased in 2010, a slight rebound occurred in 2011. Following a brief resurgence in the number of conventions in 2012, the number of delegates and events both declined in 2013, largely due to the continued fallout from the SB 1070 controversy, as many groups had decided in 2010 not to book future events in the Phoenix market. Statistics for 2014 and 2015 illustrate a strong rebound in both the number of events and delegates, as the impact of SB 1070 began to subside. Local convention officials also noted that the positive exposure from hosting major events related to Super Bowl XLIX in February 2015 allowed the downtown market to showcase itself on a national level. The number of conventions remained level in 2016, while total delegates decreased. Nonetheless, indications for 2017 point to growth in both conventions and delegates, as several large conventions are on the books, such as the Southern Baptist Convention, Berkshire Hathaway Sales Convention, and American Society for Microbiology. This positive momentum is expected to continue over the near term as local and national dynamics strengthen. Airport passenger counts are important indicators of lodging demand. Depending on the type of service provided by a particular airfield, a sizable percentage of arriving passengers may require hotel accommodations. Trends showing changes in passenger counts also reflect local business activity and the overall economic health of the area. Phoenix Sky Harbor International Airport (PHX) is the principal gateway for the Valley of the Sun region of Arizona, with major commercial airlines serving cities in the U.S., Canada, Mexico, and Europe. Growth of the airport has been spurred by a surge of population and job gains in the state over the last decade, as well as the successes of Dallas-based Southwest Airlines and Tempe-based US Airways, which merged with American Airlines in 2015. PHX Sky Train, an automated train stretching from 44th Street and Washington Street to the airport terminals and parking area, opened in 2013. The expansion of the Sky Train to the Rental Car Center is underway and will be operational in 2021. A $590-million Terminal Modernization Program of Terminal 3 began in March 2015. Phase I was completed in December 2016, which included a new security checkpoint, additional ticket counters, and baggage handling facilities. Phase II will add a new, 15-gate concourse with large seating areas and several food and retail concessions; this phase is in progress and expected to be completed in early 2019. Phase III is planned to add new food and beverage facilities and enhanced customer amenities with new finishes to the north concourse; this final phase is scheduled to be completed in 2020.

Airport Traffic

February-2018 Market Area Analysis Proposed Extended-Stay Hotel – Maricopa, Arizona 38

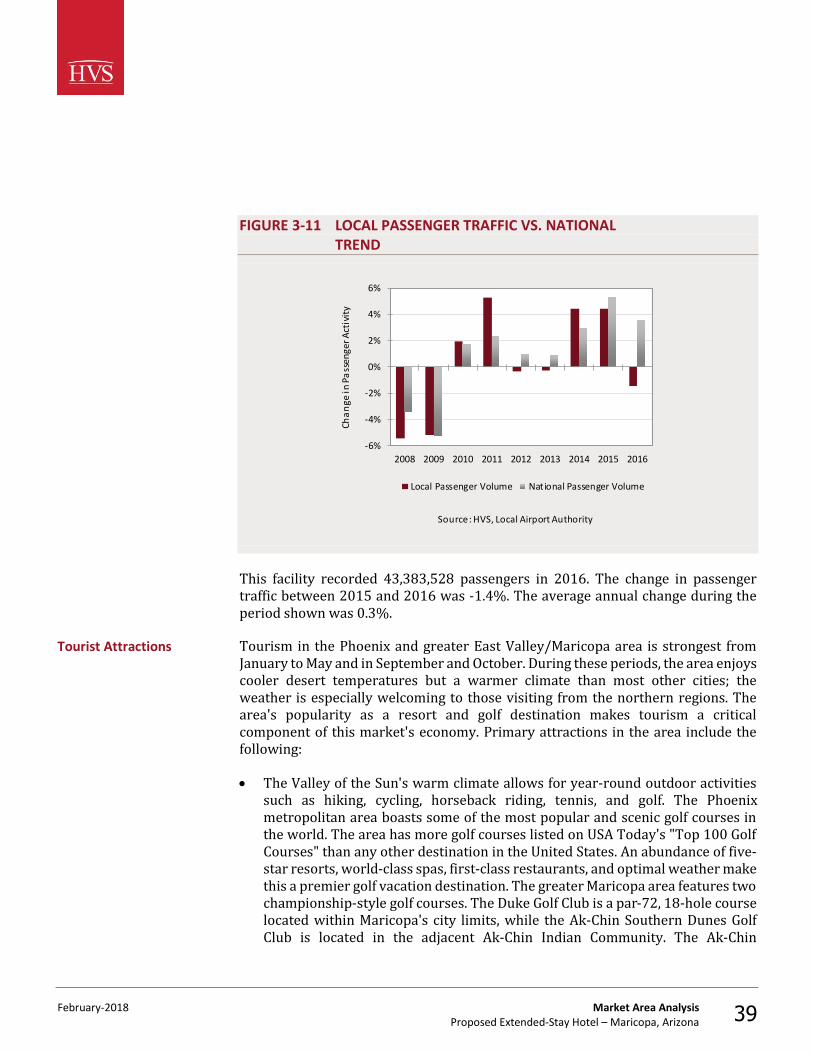

The following table illustrates recent operating statistics for the Phoenix Sky Harbor International Airport, which is the primary airport facility serving the proposed subject hotel’s submarket. FIGURE 3-10 AIRPORT STATISTICS - PHOENIX SKY HARBOR INTERNATIONAL

AIRPORT

Year

2007 42,184,174 — — 2008 39,891,193 (5.4) % (5.4) %2009 37,824,982 (5.2) (5.3)2010 38,554,530 1.9 (3.0)2011 40,592,295 5.3 (1.0)2012 40,448,932 (0.4) (0.8)2013 40,341,614 (0.3) (0.7)2014 42,134,662 4.4 (0.0)2015 44,003,840 4.4 0.52016 43,383,528 (1.4) 0.3

Year-to-date, Nov2016 39,726,167 — — 2017 40,200,418 1.2 % —

*Annual average compounded percentage change from the previous year**Annual average compounded percentage change from fi rs t year of data

Change**Passenger

Change*TrafficPercent Percent

Source: Phoenix Sky Harbor International Ai rport