Mazda Motor Logistics Europe – Willebroek FD SEMINAR 18/06/2015 1 Christine Plasmans CFO

FDSeminar Wat wil de fiscus? Christine Plasmans - Mazda

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mazda Motor Logistics Europe – WillebroekFD SEMINAR 18/06/2015

1

Christine PlasmansCFO

OUR PRODUCTS:

2

CARS : 90% of turnover!

6 carlines

Spare parts (service & warranty) and Accessories

CX-5

3

Mazda 6

4

Stylish, insightful & spirited

Mazda 3

5

Mazda 2

6

Stylish, insightful & spirited

MX-5 Roadster Coupe

7

CX-3

8

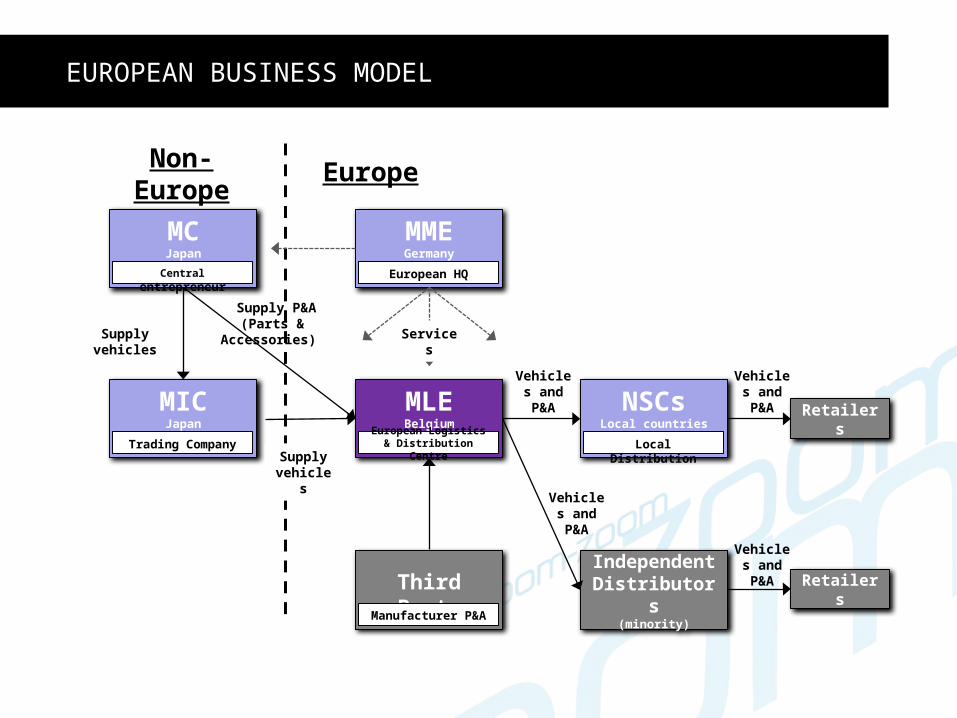

MCJapan

Central entrepreneur

Non-Europe

Europe

MICJapan

Trading Company

MMEGermany

European HQ

MLEBelgium

European Logistics & Distribution Centre

NSCsLocal countries

Local Distribution

Third Party

Manufacturer P&A

Independent Distributors

(minority)

Retailers

Retailers

Vehicles andP&A

Vehicles andP&A

Vehicles andP&A

Vehicles andP&A

ServicesSupply vehicles

Supply P&A (Parts &

Accessories)

Supply vehicles

EUROPEAN BUSINESS MODEL

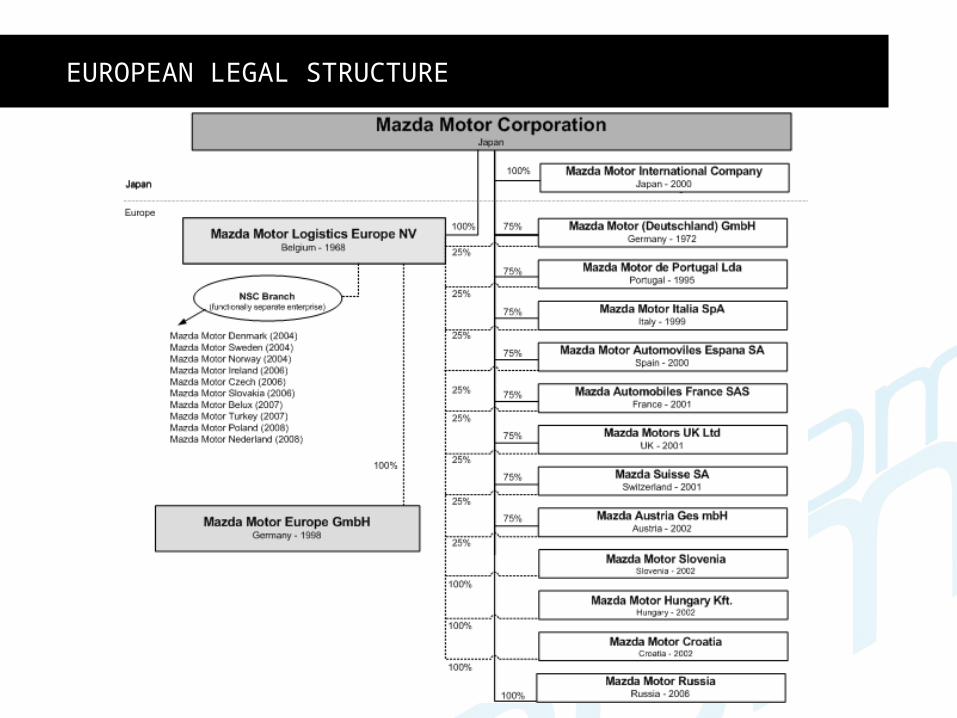

EUROPEAN LEGAL STRUCTURE

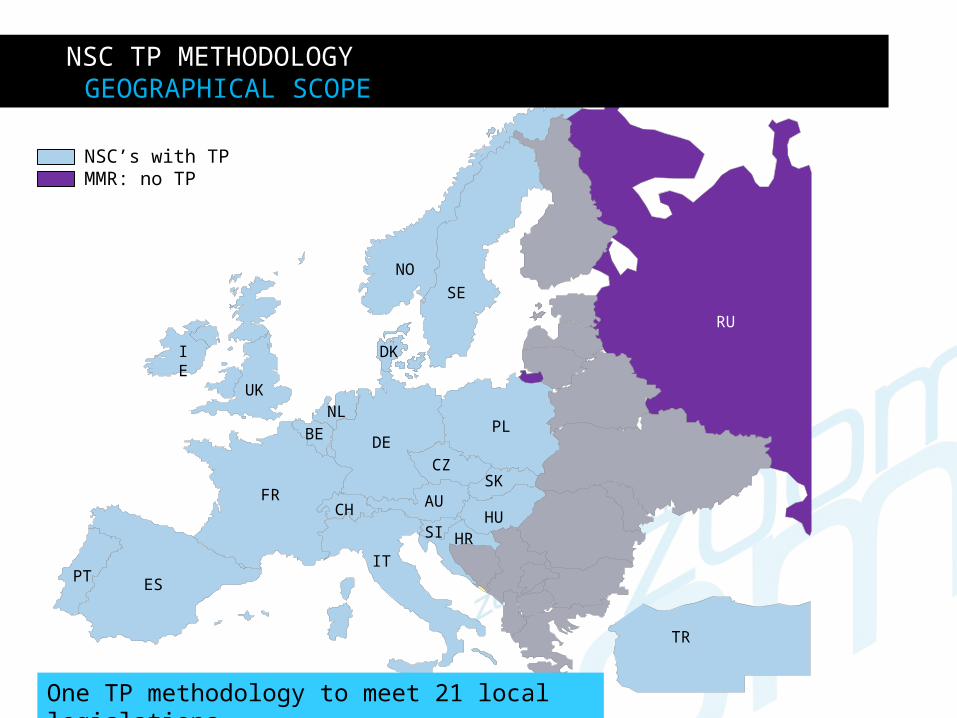

NSC’s with TPMMR: no TP

NSC TP METHODOLOGYGEOGRAPHICAL SCOPE

ES

IE

UK

PT

FR

BE

NL

DK

DE

RU

IT

CH AU

SI HR

PL

CZSK

HU

TR

NO

SE

One TP methodology to meet 21 local legislations

12

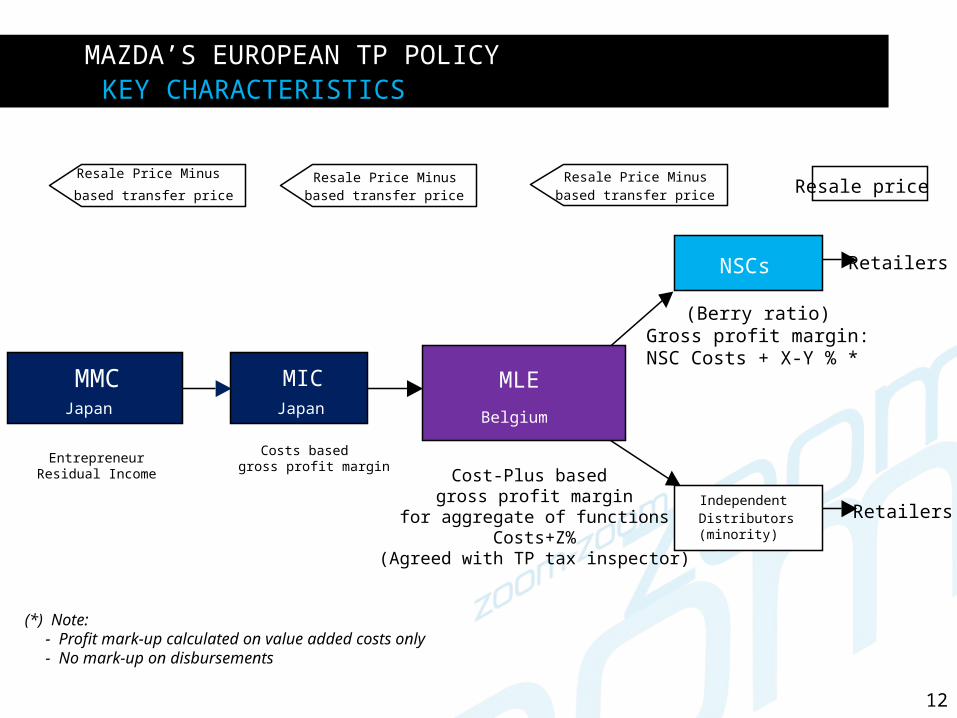

MAZDA’S EUROPEAN TP POLICY KEY CHARACTERISTICS

MMCJapan

IndependentDistributors(minority)

NSCs Retailers

Retailers

MICJapan

Resale Price Minusbased transfer price

Resale Price Minusbased transfer price

Resale Price Minus

based transfer price Resale price

Cost-Plus based gross profit margin

for aggregate of functionsCosts+Z%

(Agreed with TP tax inspector)

(Berry ratio)Gross profit margin:

NSC Costs + X-Y % *

Belgium

MLE

Costs based gross profit margin

EntrepreneurResidual Income

(*) Note: - Profit mark-up calculated on value added costs only - No mark-up on disbursements

13

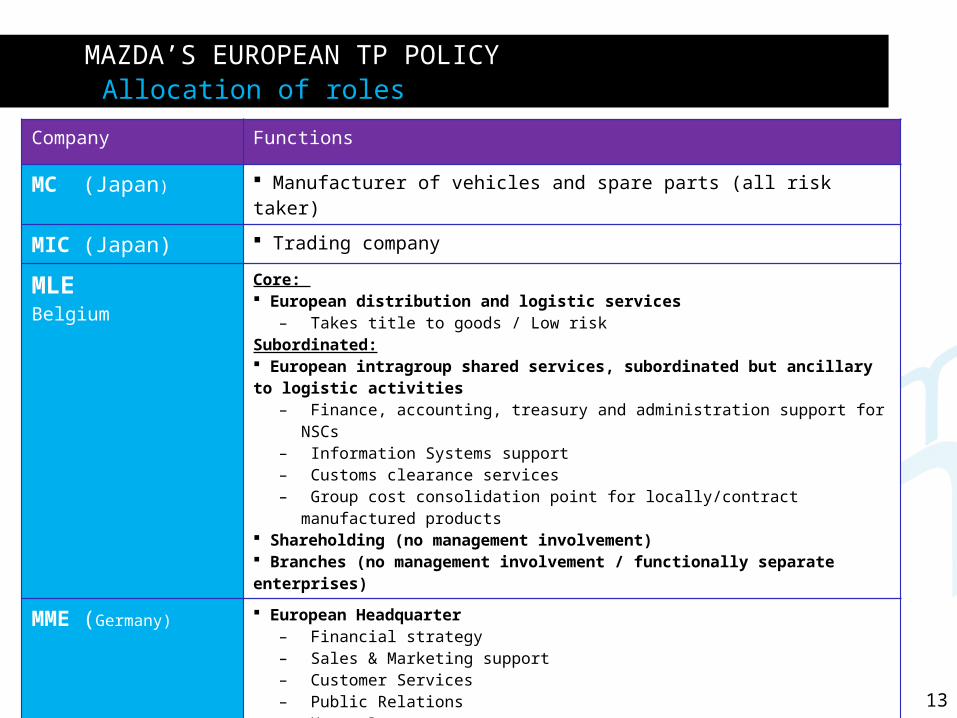

MAZDA’S EUROPEAN TP POLICY Allocation of roles

Company Functions

MC (Japan) Manufacturer of vehicles and spare parts (all risk taker)

MIC (Japan) Trading company

MLEBelgium

Core: European distribution and logistic services

– Takes title to goods / Low risk Subordinated: European intragroup shared services, subordinated but ancillary to logistic activities

– Finance, accounting, treasury and administration support for NSCs– Information Systems support– Customs clearance services– Group cost consolidation point for locally/contract manufactured products

Shareholding (no management involvement) Branches (no management involvement / functionally separate enterprises)

MME (Germany) European Headquarter – Financial strategy– Sales & Marketing support– Customer Services– Public Relations– Human Resources support– Legal support

European Research & development

NSCsVarious countries

Local distribution and sales– Local sales, marketing and branding support– Coordination and supervision of retailer network

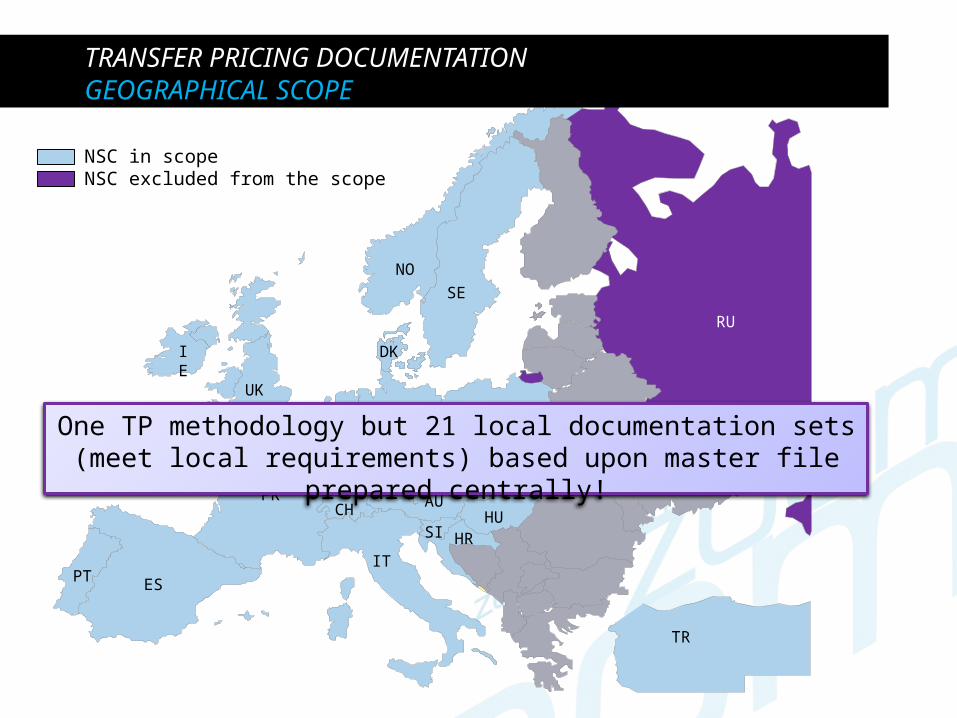

NSC in scopeNSC excluded from the scope

TRANSFER PRICING DOCUMENTATIONGEOGRAPHICAL SCOPE

ES

IE

UK

PT

FR

BE

NL

DK

DE

RU

IT

CH AU

SI HR

PL

CZSK

HU

TR

NO

SE

One TP methodology but 21 local documentation sets (meet local requirements) based upon master file prepared centrally!

15

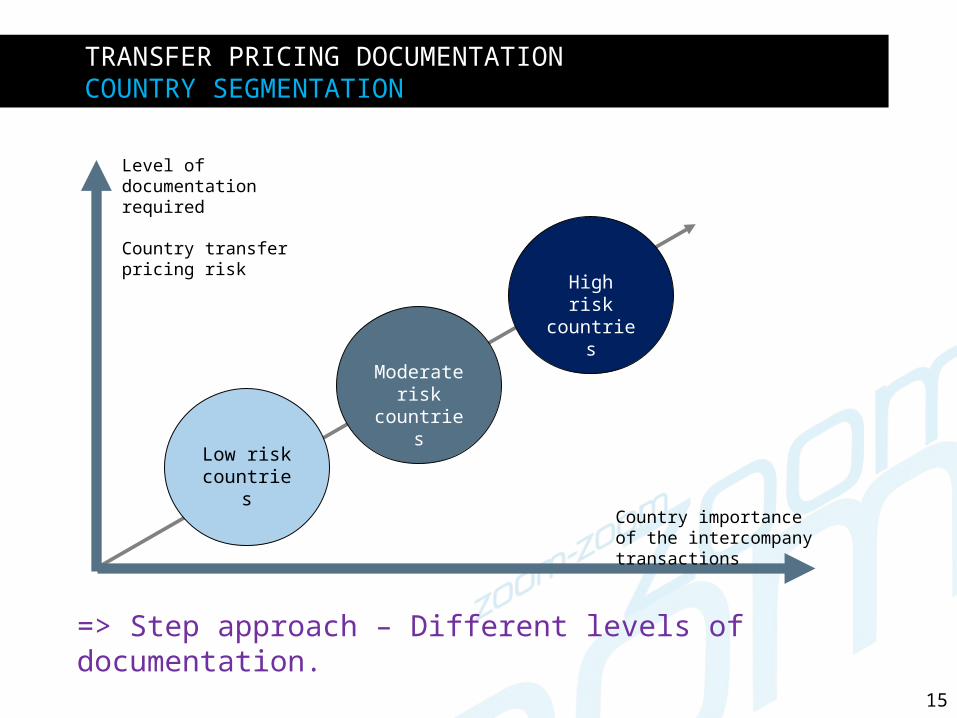

TRANSFER PRICING DOCUMENTATIONCOUNTRY SEGMENTATION

Low risk countries

Moderate risk

countries

High risk countries

Level of documentation required

Country transfer pricing risk

Country importance of the intercompany transactions

=> Step approach – Different levels of documentation.

16

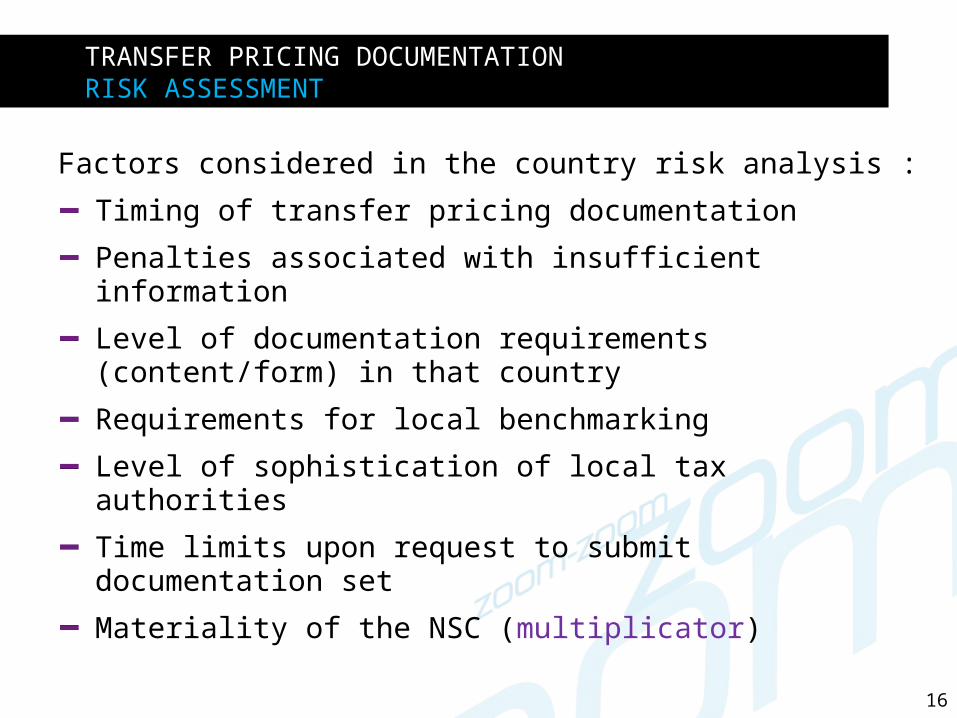

TRANSFER PRICING DOCUMENTATION RISK ASSESSMENT

Factors considered in the country risk analysis :

Timing of transfer pricing documentation

Penalties associated with insufficient information

Level of documentation requirements (content/form) in that country

Requirements for local benchmarking

Level of sophistication of local tax authorities

Time limits upon request to submit documentation set

Materiality of the NSC (multiplicator)

17

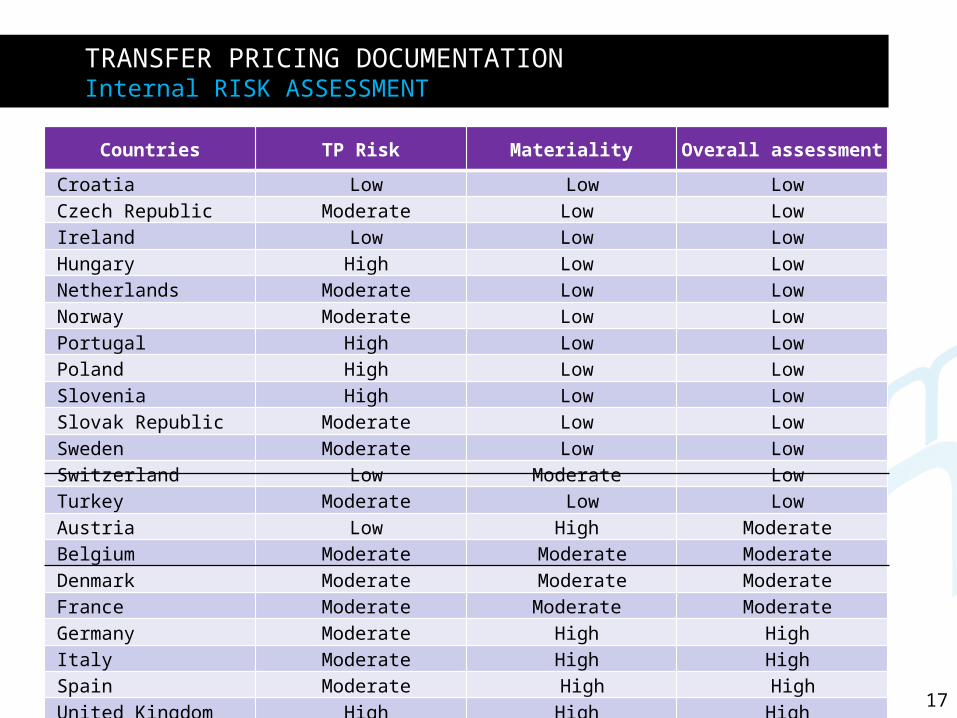

TRANSFER PRICING DOCUMENTATION Internal RISK ASSESSMENT

Countries TP Risk Materiality Overall assessment

Croatia Low Low LowCzech Republic Moderate Low LowIreland Low Low LowHungary High Low LowNetherlands Moderate Low LowNorway Moderate Low LowPortugal High Low LowPoland High Low LowSlovenia High Low LowSlovak Republic Moderate Low LowSweden Moderate Low LowSwitzerland Low Moderate LowTurkey Moderate Low LowAustria Low High ModerateBelgium Moderate Moderate ModerateDenmark Moderate Moderate ModerateFrance Moderate Moderate ModerateGermany Moderate High HighItaly Moderate High HighSpain Moderate High HighUnited Kingdom High High High

18

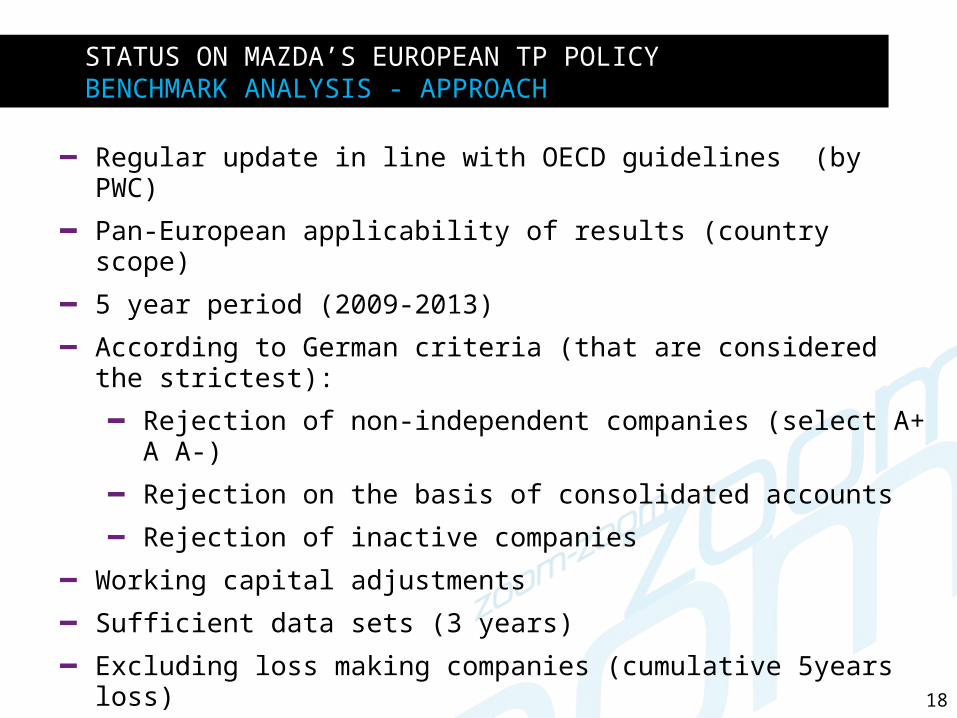

STATUS ON MAZDA’S EUROPEAN TP POLICY BENCHMARK ANALYSIS - APPROACH

Regular update in line with OECD guidelines (by PWC)

Pan-European applicability of results (country scope)

5 year period (2009-2013)

According to German criteria (that are considered the strictest):

Rejection of non-independent companies (select A+ A A-)

Rejection on the basis of consolidated accounts

Rejection of inactive companies

Working capital adjustments

Sufficient data sets (3 years)

Excluding loss making companies (cumulative 5years loss)

Manual exclusions and validation through web search (activity)

19

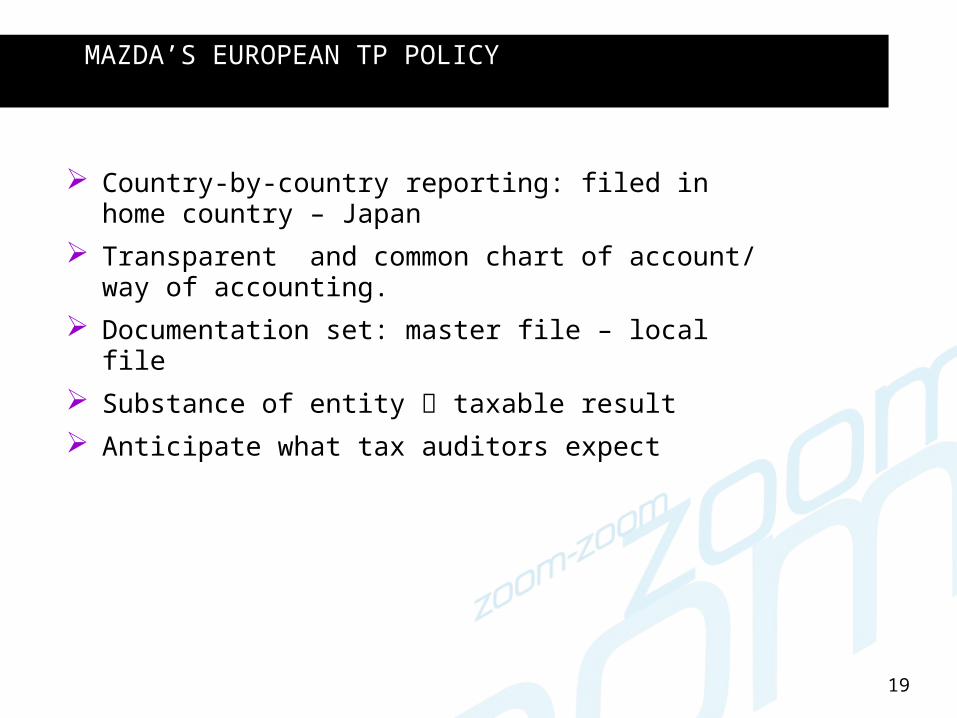

MAZDA’S EUROPEAN TP POLICY

Country-by-country reporting: filed in home country – Japan

Transparent and common chart of account/ way of accounting.

Documentation set: master file – local file

Substance of entity taxable result

Anticipate what tax auditors expect

20

MAZDA’S EUROPEAN TP POLICY

Related Documents