Expanding your business to Europe: Business location Bavaria Four Embarcadero Center (conference hall), San Francisco, California 94111 Thursday, Jun 16, 2011, 11:30 AM - 02:00 PM Jörg Kemkes, managing director, BridgehouseTax, Atlanta

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Expanding your business to Europe:

Business location Bavaria

Four Embarcadero Center (conference hall),

San Francisco, California 94111

Thursday, Jun 16, 2011, 11:30 AM - 02:00 PM

Jörg Kemkes, managing director,

BridgehouseTax, Atlanta

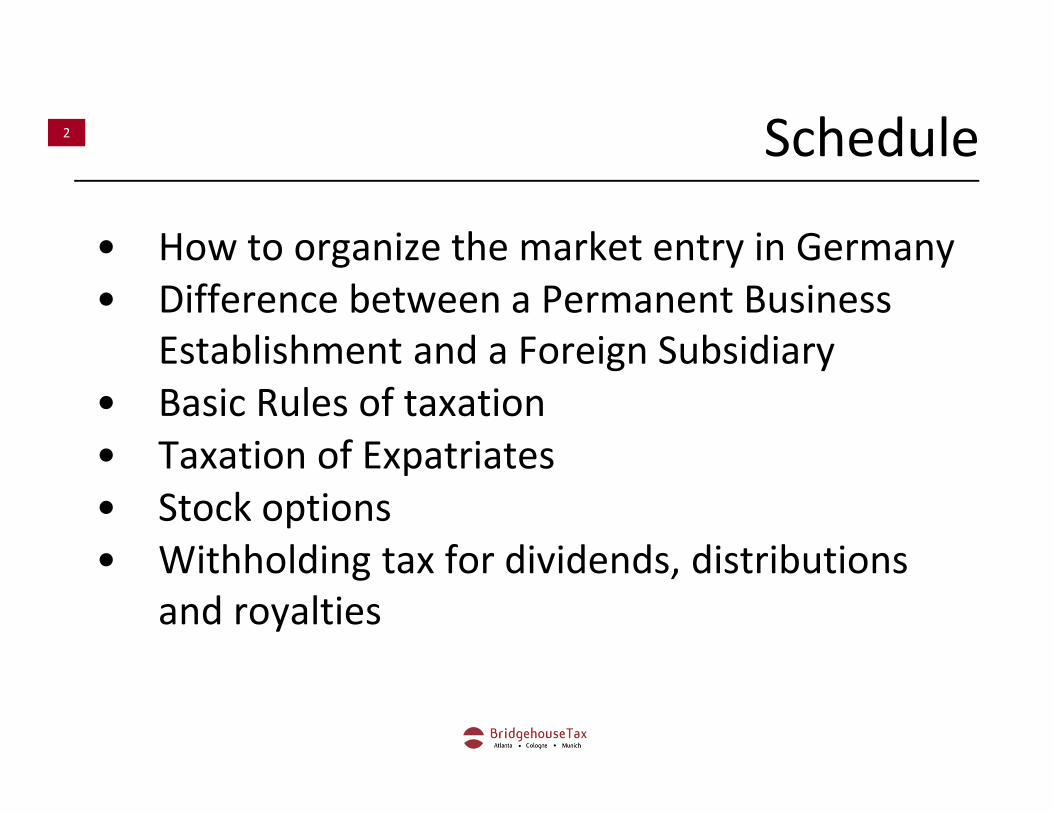

2 Schedule

• How to organize the market entry in Germany

• Difference between a Permanent Business

Establishment and a Foreign Subsidiary

• Basic Rules of taxation

• Taxation of Expatriates

• Stock options

• Withholding tax for dividends, distributions

and royalties

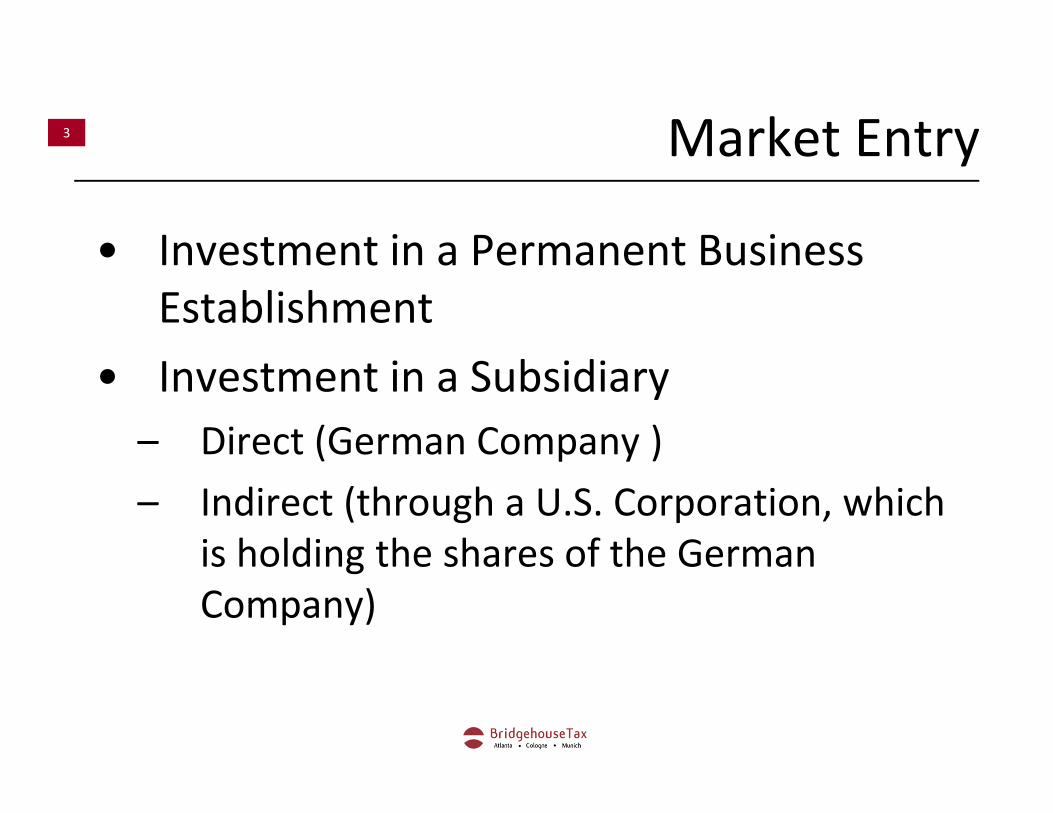

3 Market Entry

• Investment in a Permanent Business

Establishment

• Investment in a Subsidiary

– Direct (German Company )

– Indirect (through a U.S. Corporation, which

is holding the shares of the German

Company)

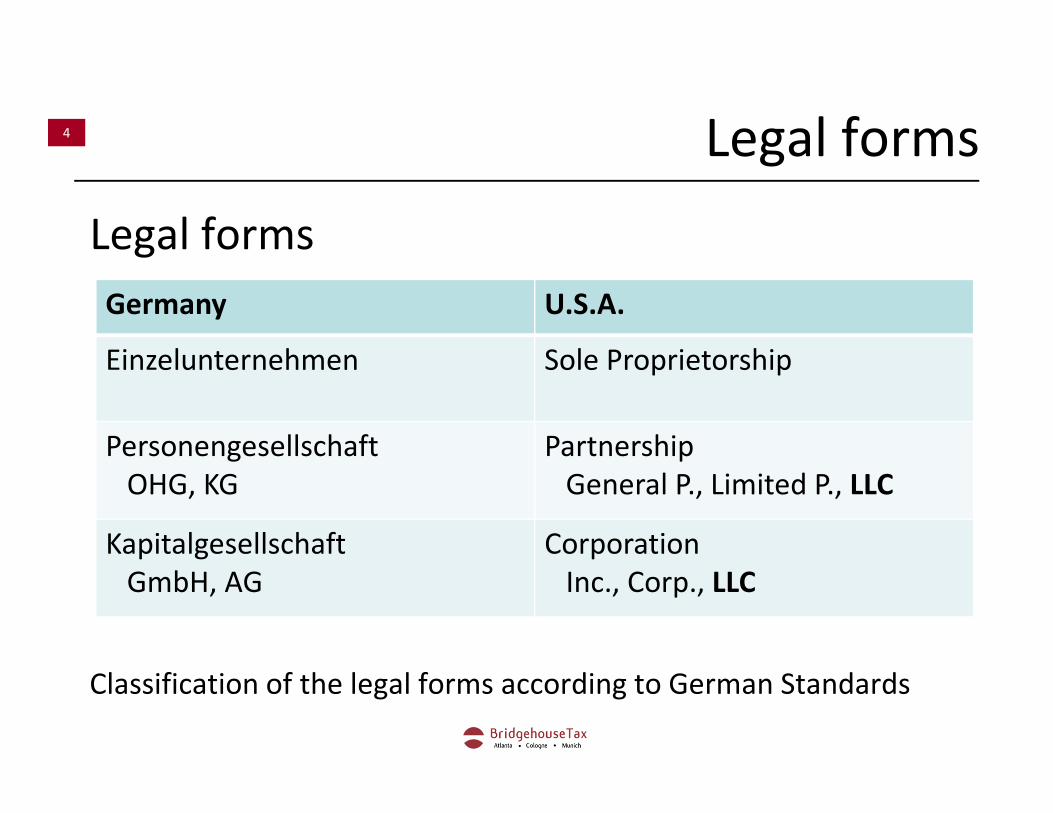

4 Legal forms

Legal forms

Classification of the legal forms according to German Standards

Germany U.S.A.

Einzelunternehmen Sole Proprietorship

Personengesellschaft

OHG, KG

Partnership

General P., Limited P., LLC

Kapitalgesellschaft

GmbH, AG

Corporation

Inc., Corp., LLC

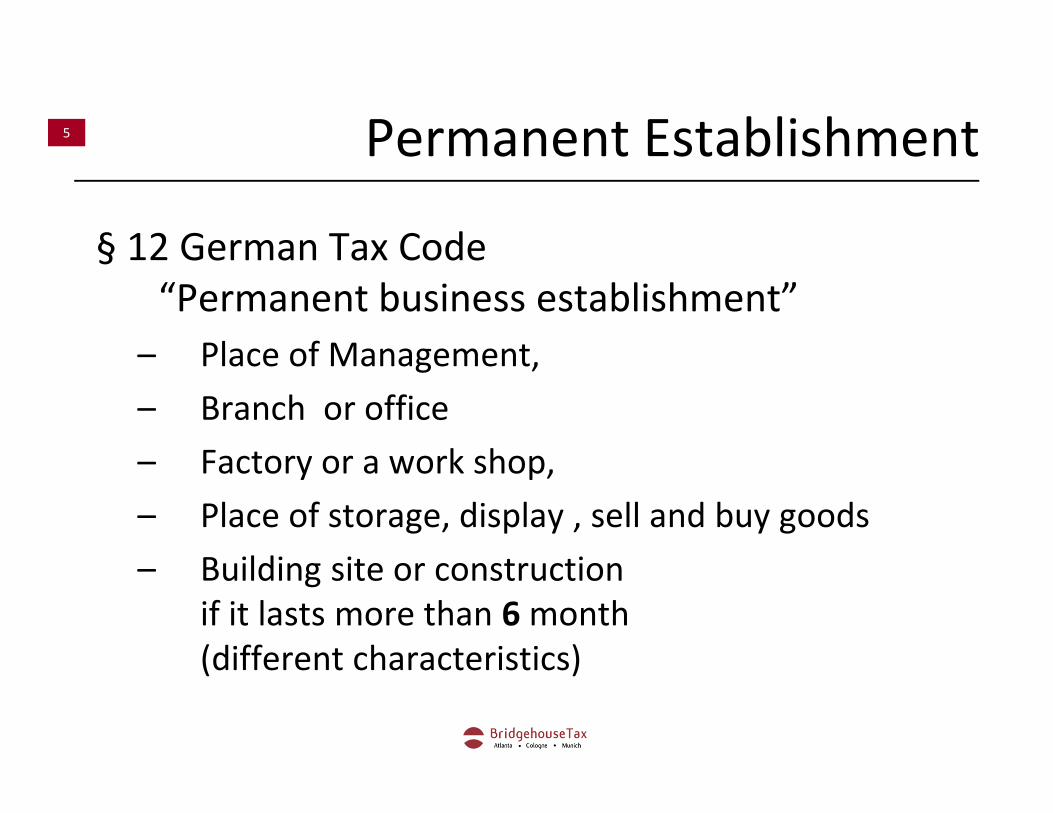

5 Permanent Establishment

§ 12 German Tax Code

“Permanent business establishment”

– Place of Management,

– Branch or office

– Factory or a work shop,

– Place of storage, display , sell and buy goods

– Building site or construction

if it lasts more than 6 month

(different characteristics)

6 Permanent Establishment

Permanent establishment

Art. 5 DTA versus § 12 German Tax code

– DTA:

more detailed

positive and negative catalog of cases

� Review every single case separately

7 Foreign subsidiary

= corporation, which is

separate and distinct from its owners

and a legally recognized person

• In Germany:

mainly GmbH

= Gesellschaft mit beschränkter Haftung

= company with limited liability

(always a corporation, no “check the box”)

8 Differences

• A permanent establishment located in

Germany: the profit of the company earned

by the permanent establishment will be taxed

in Germany (limited taxation)

Main problem: how to split the profit

• A German Corporation with either their

management or their registered office in

Germany is to be taxed in Germany with their

world income (unlimited taxation)

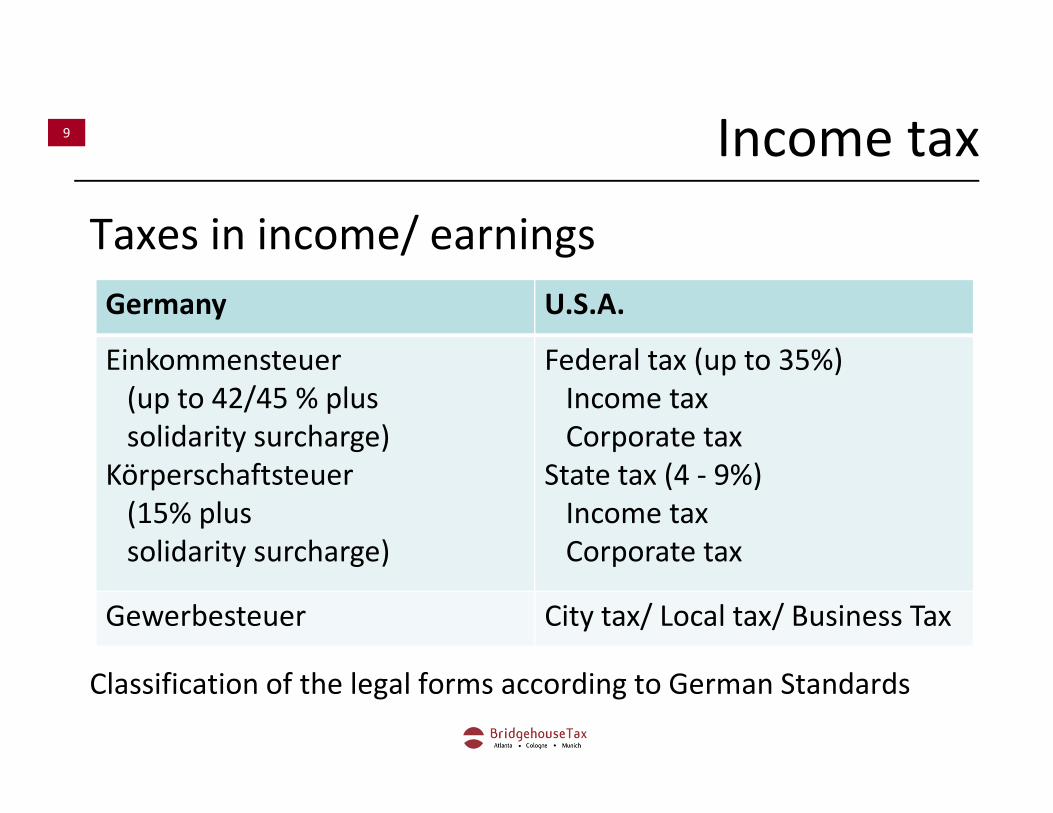

9 Income tax

Taxes in income/ earnings

Classification of the legal forms according to German Standards

Germany U.S.A.

Einkommensteuer

(up to 42/45 % plus

solidarity surcharge)

Körperschaftsteuer

(15% plus

solidarity surcharge)

Federal tax (up to 35%)

Income tax

Corporate tax

State tax (4 - 9%)

Income tax

Corporate tax

Gewerbesteuer City tax/ Local tax/ Business Tax

10 Value added tax

VAT in Germany

• is borne by the end costumer

(private individual)

• not borne by the company

11 Value added tax

Basics about VAT in Germany

• imposed on assets and services in Germany as

well as on imports into Germany

• standard value added tax rate: 19%.

• reduced rate of 7% (food, books…)

• input VAT will be credited

• tax reports: monthly or quarterly

(tax authoities are very strict)

12 Taxation of Expatriates

three Scenarios:

Employee takes residence in Germany

1. and fully abandons the U.S. residence

2. and does not fully abandon the U.S. residence

and

a) preserves the centre of life in the U.S.

or

b) shifts of the centre of life to Germany

13 Taxation of Expatriates

„183-day-Rule“ (Country of residence versus State of work)

How are calculated the 183 days?

• Physical presence

• A couple of minutes per day are already

enough

• During one calendar year

• Caution: spending holidays in the state of

work

14 Participation in stocks

Differentiate three main cases:

• Employees stock purchase plan

(ESPP)

• Restricted stock unit (RSU)

• Stock options

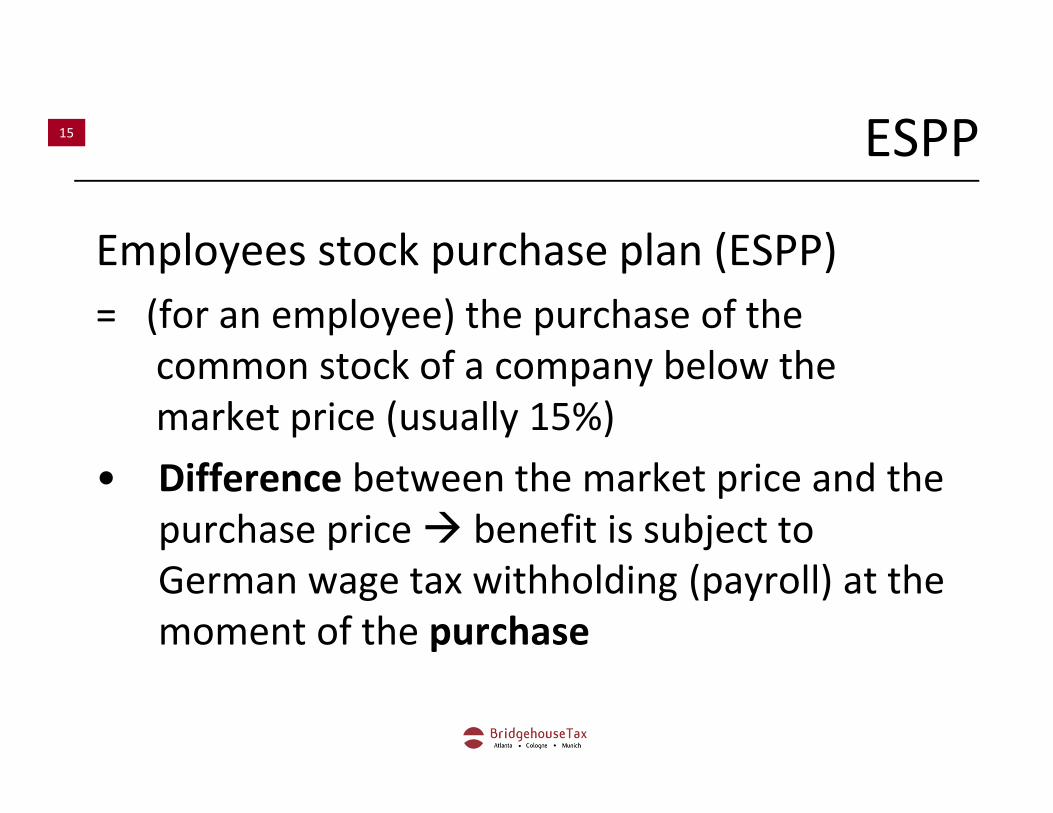

15 ESPP

Employees stock purchase plan (ESPP)

= (for an employee) the purchase of the

common stock of a company below the

market price (usually 15%)

• Difference between the market price and the

purchase price � benefit is subject to

German wage tax withholding (payroll) at the

moment of the purchase

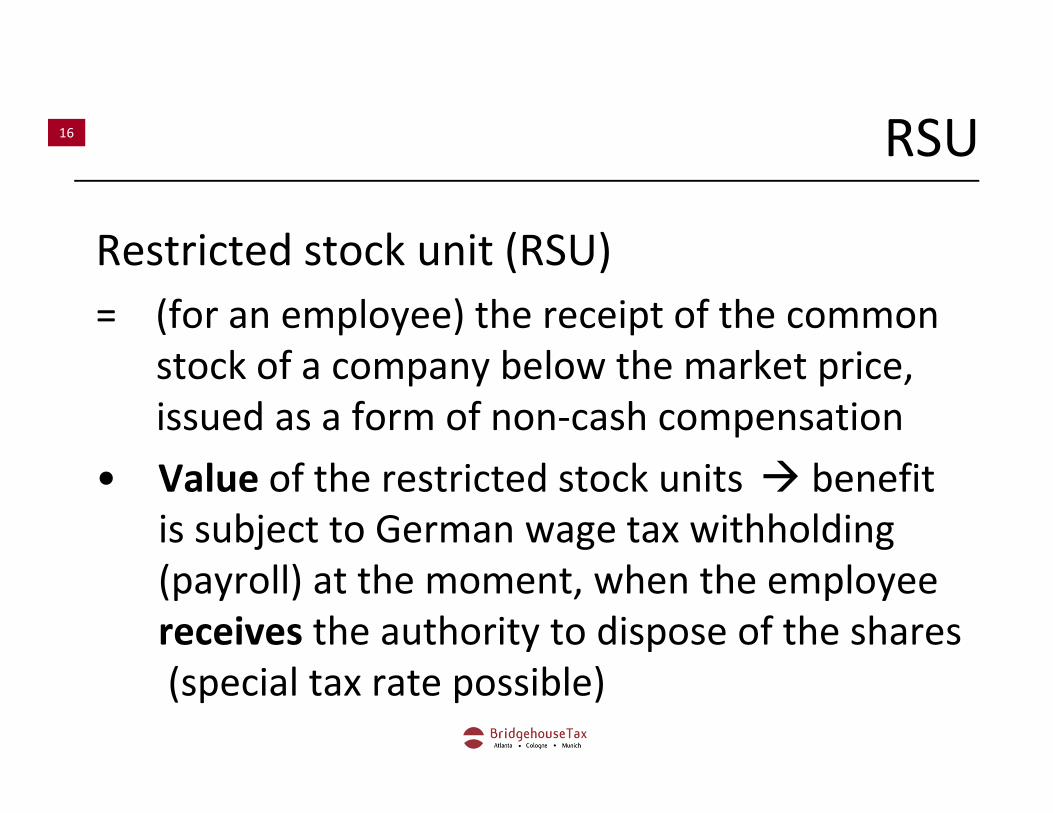

16 RSU

Restricted stock unit (RSU)

= (for an employee) the receipt of the common

stock of a company below the market price,

issued as a form of non-cash compensation

• Value of the restricted stock units � benefit

is subject to German wage tax withholding

(payroll) at the moment, when the employee

receives the authority to dispose of the shares

(special tax rate possible)

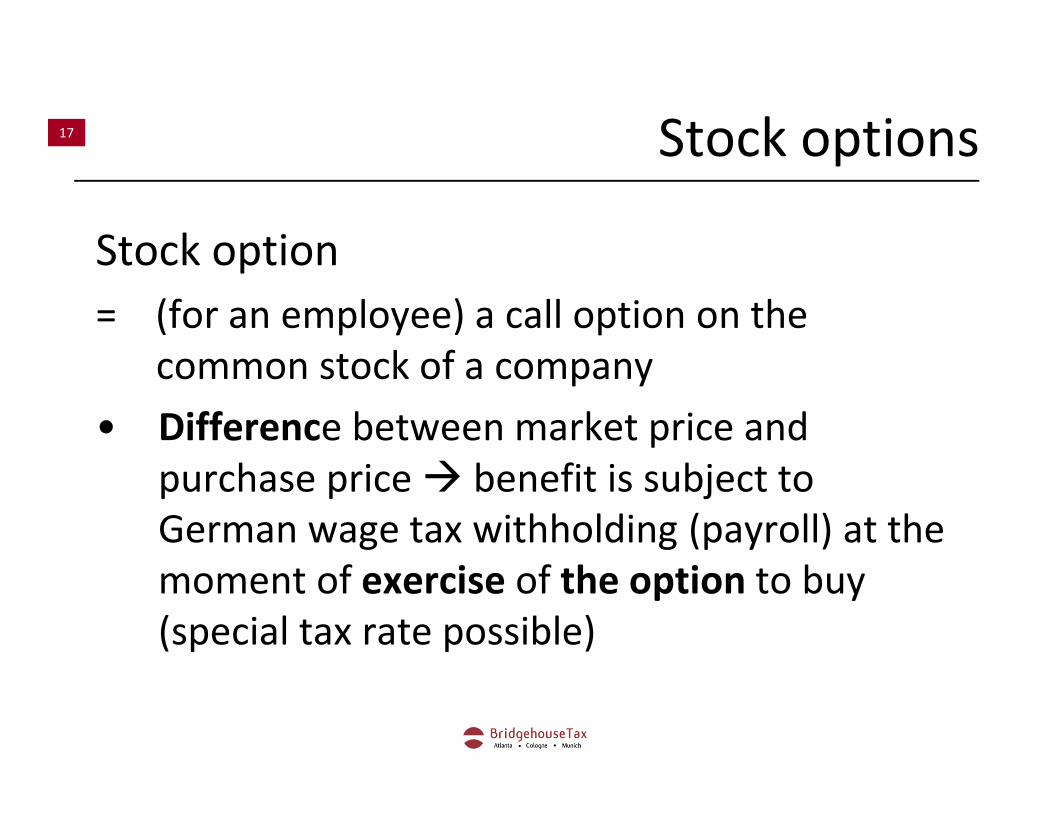

17 Stock options

Stock option

= (for an employee) a call option on the

common stock of a company

• Difference between market price and

purchase price � benefit is subject to

German wage tax withholding (payroll) at the

moment of exercise of the option to buy

(special tax rate possible)

18 Participation in stocks

Problems

What will happen, if

• the employee leaves the company?

• the employee leaves the country to work in

another country?

19 Participation in stocks

• Employee leaves the company

– Company has to claim the payroll tax from the

former employee or (if not successful)

– Company sends a special notice to the company‘s

tax office and the tax authority will claim the

payroll tax directly from the employee

– In cases of high taxable benefit it is advisable to

withhold 51,08 % of the stock gain to cover the

maximum payroll tax. The correct personal tax then

would be calculated with the next payroll.

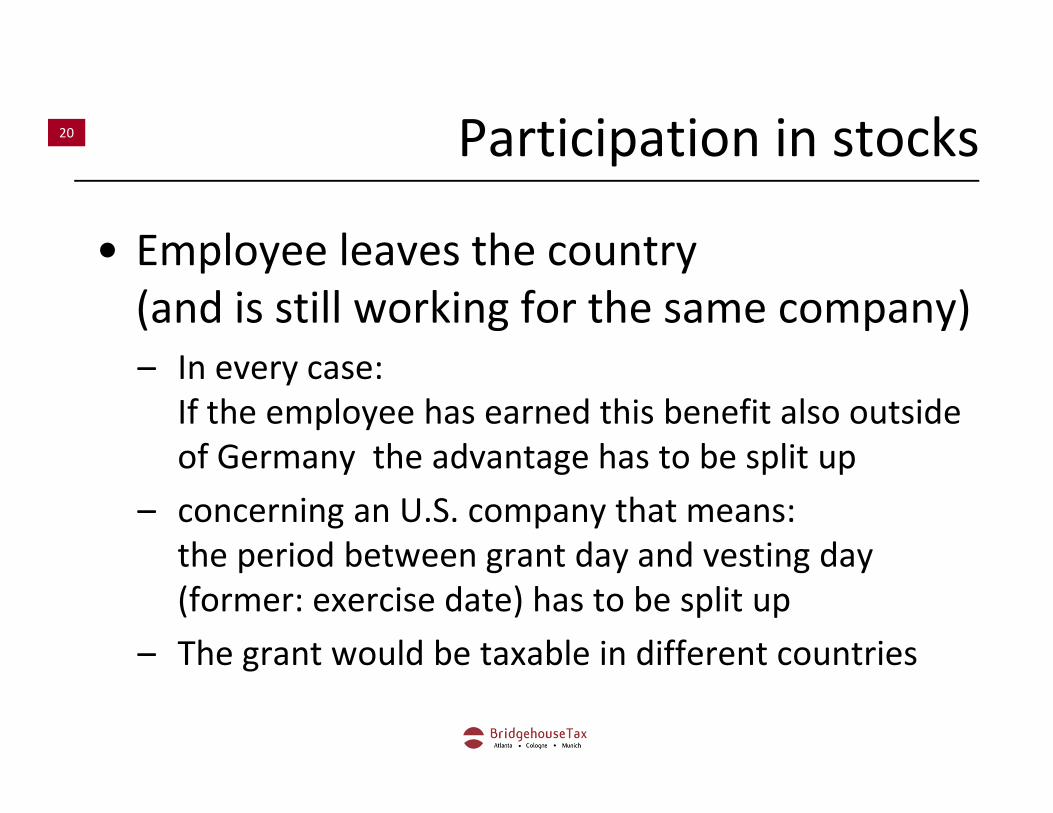

20 Participation in stocks

• Employee leaves the country

(and is still working for the same company)

– In every case:

If the employee has earned this benefit also outside

of Germany the advantage has to be split up

– concerning an U.S. company that means:

the period between grant day and vesting day

(former: exercise date) has to be split up

– The grant would be taxable in different countries

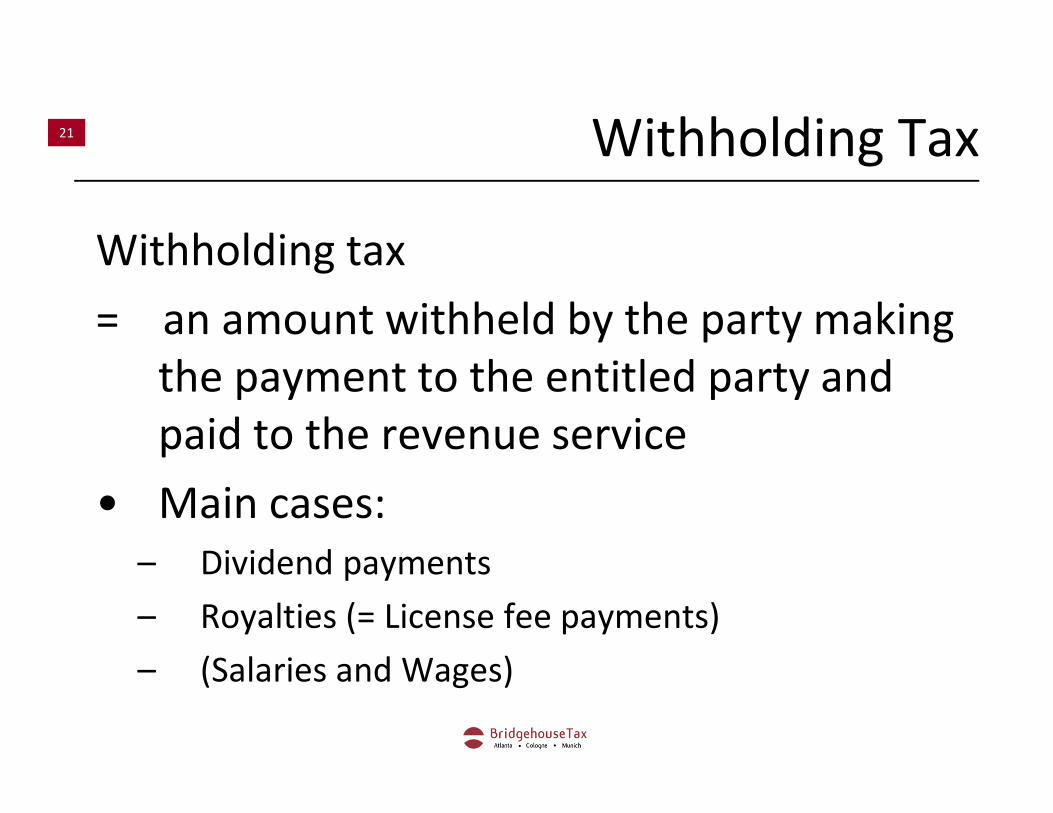

21 Withholding Tax

Withholding tax

= an amount withheld by the party making

the payment to the entitled party and

paid to the revenue service

• Main cases:

– Dividend payments

– Royalties (= License fee payments)

– (Salaries and Wages)

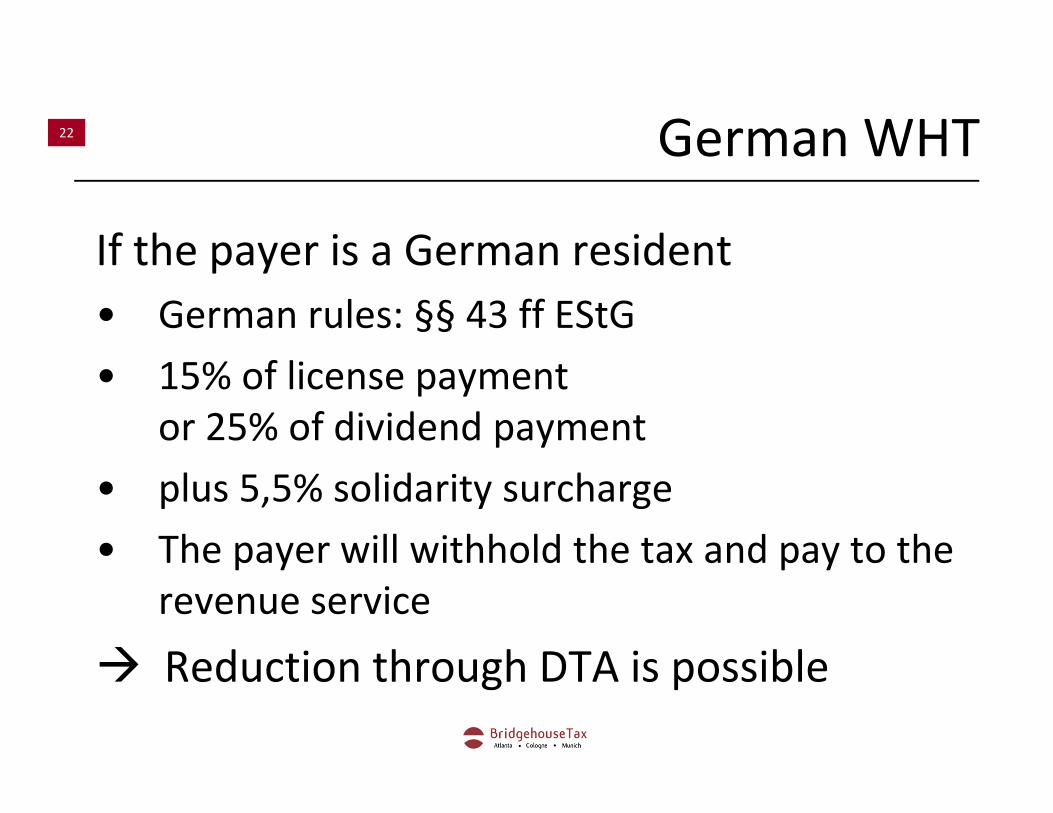

22 German WHT

If the payer is a German resident

• German rules: §§ 43 ff EStG

• 15% of license payment

or 25% of dividend payment

• plus 5,5% solidarity surcharge

• The payer will withhold the tax and pay to the

revenue service

� Reduction through DTA is possible

23 WHT in the DTA: dividends

Art. 10 par.2, 3 DTA:

Taxation in the source state:

• 5 % of the gross amount of the dividends if

the owner is a company that owns directly at

least 10 percent of the voting stock of the

paying company

• 0 % (Zero tax) is possible

difficult tests have to be made,

thorough examination is necessary

24 Definition: royalty

Art. 12 par.2 DTA: Royalty

= payments of any kind received as a consideration for

the use of, or the right to use

• any copyright of a literary, artistic, or scientific

work

• any patent, trademark, design or model, plan,

secret formula or process…

= also includes gains derived from the alienation of

any such right or property

25 WHT in the DTA: royalty

• the intellectual property is in the US and the

German subsidiary pays for the use of the

license

• 0 % (Zero tax) is possible

but the application for the exemption must be

applied and granted before payment

26 Kontakt

BridgehouseTax Atlanta

Jörg Kemkes

The Proscenium, Suite 1775

1170 Peachtree Street, NE

Atlanta, GA 30309-7675

U.S.A.

T +1 404 898 9122

F +1 404 506 9930

www.bridgehouestax.us

Related Documents