www.eurexchange.com Evolution and behaviour of European volatility: VSTOXX® January 2018 Evolution and behaviour of European volatility: VSTOXX® Megan Morgan Email: [email protected] Twitter: @meganbeausang

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

Evolution and behaviour of European volatility: VSTOXX®Megan MorganEmail: [email protected]: @meganbeausang

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• Eurex recognized the US volatility market as a strategic area of growth upon receiving no action relief for the VSTOXX® futures in 2012

• Shortly thereafter, the exchange put in place a strategy to grow liquidity based upon changing market structure to open up the VSTOXX® market to US participants.

– Step One: Grow the liquidity in the VSTOXX® futures – Step Two: Convert the VSTOXX® Options to Options on Futures for CFTC-approval– Step Three: Work with a ETP provider to list a VSTOXX® ETN on a US-based exchange

• US participants have been keen to trade VSTOXX® to access European volatility – The index is constructed in a similar fashion as the VIX– The VSTOXX® is more reactive to European-specific events– The VSTOXX®/VIX spread is mean reverting

2

VSTOXX® and the US market

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

3

A path to liquidity: VSTOXX® market structure initiatives

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

4

FVS ADV

2012 ADV 15,000

2013 ADV 21,000

2014 ADV 27,500

2015 ADV 29,500

2016 ADV 38,200

2017 ADV 52,205

Orderbook volume growth 2012 vs 2017

FVS 2012 2017

Order book 71.93% 84.67%

A path to liquidity: grow liquidity in the underlying

• August 1, 2012: VSTOXX® futures received CFTC no-action relief. Volume doubled from month to month as Eurex saw an inflow of volume from US-based customers previously restricted from the contract

• March 1, 2015: Extend VSTOXX® futures market hours to overlap US trading hours• November 1, 2015: Eurex revamped the VSTOXX® futures market making program adding six new

market making participants improving order book liquidity.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000FVS - ADV By Expiry

Expiry 1 Expiry 2 Expiry 3 Expiry 4 Expiry 5 Expiry 6 Expiry 7 Expiry 8

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

0.0000

0.1000

0.2000

0.3000

0.4000

0.5000

0.6000

0.7000

0.8000

0.00

50.00

100.00

150.00

200.00

250.00

insi

de m

arke

t spr

ead

insi

de m

arke

t vol

ume

The effect of new market makers on order book liquidity

average size bid average size ask average spread(r.h.scale)

5

A path to liquidity: grow liquidity in the underlying

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

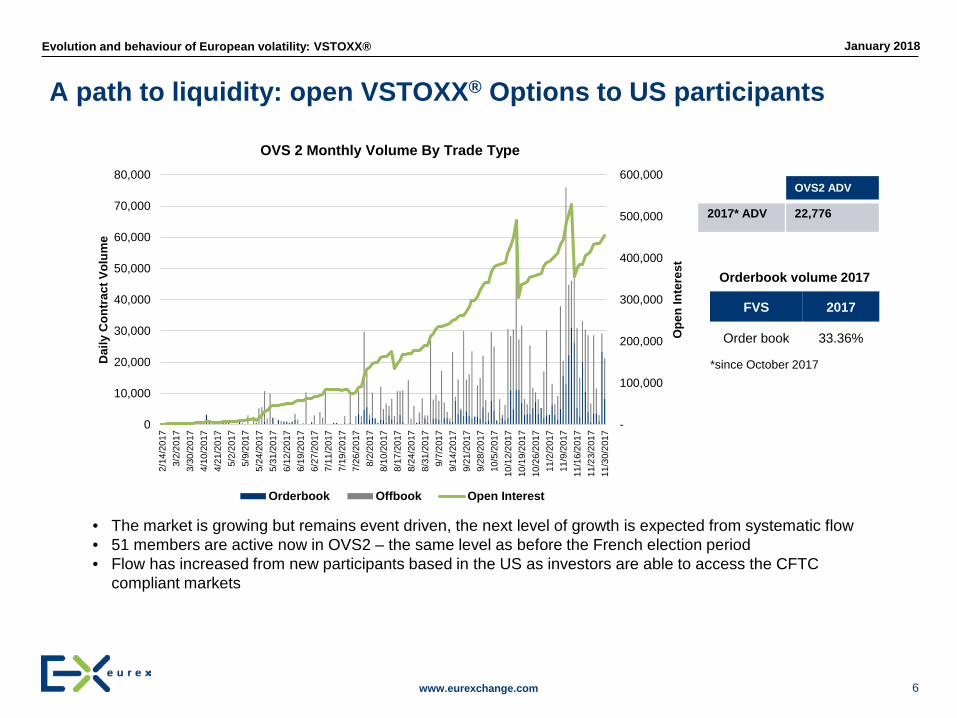

A path to liquidity: open VSTOXX® Options to US participants

• The market is growing but remains event driven, the next level of growth is expected from systematic flow• 51 members are active now in OVS2 – the same level as before the French election period• Flow has increased from new participants based in the US as investors are able to access the CFTC

compliant markets

6

-

100,000

200,000

300,000

400,000

500,000

600,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,0002/

14/2

017

3/2/

2017

3/30

/201

74/

10/2

017

4/21

/201

75/

2/20

175/

9/20

175/

24/2

017

5/31

/201

76/

12/2

017

6/19

/201

76/

27/2

017

7/11

/201

77/

19/2

017

7/26

/201

78/

2/20

178/

10/2

017

8/17

/201

78/

24/2

017

8/31

/201

79/

7/20

179/

14/2

017

9/21

/201

79/

28/2

017

10/5

/201

710

/12/

2017

10/1

9/20

1710

/26/

2017

11/2

/201

711

/9/2

017

11/1

6/20

1711

/23/

2017

11/3

0/20

17

Ope

n In

tere

st

Dai

ly C

ontr

act V

olum

e

OVS 2 Monthly Volume By Trade Type

Orderbook Offbook Open Interest

OVS2 ADV

2017* ADV 22,776

Orderbook volume 2017

FVS 2017

Order book 33.36%

*since October 2017

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

Evolution and behaviour of European volatility: VSTOXX®Mark Shore, Shore Capital Research LLCEmail: [email protected]

www.shorecapmgmt.comTwitter: @shorecap

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• Past performance is not necessarily indicative of future results.

• There is risk of loss when investing in futures and options.

• Futures & options can be a volatile and risky investment; only use appropriate risk capital; this investment is not for everyone.

• The opinions expressed are solely those of the author and are only for educational purposes. Please talk to your financial advisor before making any investment decisions.

Evolution and behaviour of European volatility: VSTOXX®

8

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• Over 30 years experience in the futures markets/ alternative investments

• Undergrad DePaul University; MBA University of Chicago; Doctoral candidate in applied research

• Former COO of VK Capital (a wholly owned $300 million AUM CTA subsidiary of Morgan Stanley)

• Former Head of Risk at Octane Research, $1.1 billion AUM

• Adjunct Professor, DePaul University

• Contributing Author to two Wiley & Sons books on hedge funds & commodities

• Contributing Writer: Eurex, CBOE, CBOE Futures, MicroCap Review, Swiss Derivatives Review, Seeking

Alpha, Prime Meridian Capital Management, Coquest Advisors

• Board Member Arditti Center for Risk Mgmt; PRMIA Chicago Steering Committee, NIBA Board of

Directors, QWAFAFEW Chicago Steering Committee

• Director of Educational Research, Coquest Advisors LLC

• Hosted an internet talk show on alternative investments “Skewing Your Diversification”

• Founded consulting/research firm Shore Capital Research LLC• Research of markets & trading strategies• Due diligence of managers • Business development of alternative investments• Educational workshops• Research & expert witness testimony for capital market litigation

Mark Shore’s bio

9

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• VSTOXX® Spot (V2X)

• VSTOXX® Futures (FVS)

• VSTOXX® Options (OVS) – ended in Sept 2017

• (New) Options on VSTOXX® Futures (OVS2) – began Feb 2017

VSTOXX® volatility index derivatives

10

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

VSTOXX® Futures (Eurex)

30 Day Forward Yes

Annualized Implied Volatility of EURO STOXX 50® Index

Ticker Symbol for Spot & Futures V2X (spot) & FVS (futures)

Currency Euro

Futures Began Trading (trades 8 expirations) 2009

Average Daily Trading Volume (As of November 2017) **

52,580

Long negative volatility of underlying Market Yes

Mean Reverting Yes

Top range 45 to 50

Median* 22.8

Bottom range 13 to 17

*Spot price 1/4/1999 to 8/14/17** Eurex website

VSTOXX® spot and futures

11

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• STOXX Limited formed in 1997. A leading index specialist based in Zurich, Switzerland (stoxx.com)

• EURO STOXX 50® Index “represents the performance of the 50 largest companies in terms of free-float market cap” of up to 11 Eurozone countries.

• Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain

• Composition is reviewed every September

• A smaller and less diversified index than S&P 500

• Heavily weighted by financial stocks ~(25%)

Source: www.stoxx.com, as of Oct 31, 2017

STOXX®

12

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

Sector Weighting Country Weighting

Banks 15.5% France 36.5%

Industrial Good & Services 10.8% Germany 33.1%

Personal Household Goods 9.2% Spain 10.4%

Chemicals 9.0% Netherlands 10.1%

Technology 7.3% Italy 4.7%

Healthcare 7.2% Belgium 3.1%

Insurance 6.9% Ireland 1.1%

Oil & Gas 6.2% Finland 1.0%

Utilities 5.2%

Automobiles & Parts 5.1%

Food & Beverage 4.9%

Telecommunications 4.8%

Construction & Materials 4.1%

Retail 2.2%

Media 0.9%

Real Estate 0.9%

Total 100% Total 100%

Source: https://www.stoxx.com/document/Bookmarks/CurrentFactsheets/SX5GT.pdfAs of October 31, 2017

EURO STOXX 50® index sector weightings

13

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

0

10,000

20,000

30,000

40,000

50,000

60,000

2010 2011 2012 2013 2014 2015 2016 2017

Ope

n in

tere

st

Aver

age

Dai

ly V

olum

e

Avg Daily Volume Open interest

VSTOXX® volume & open interest (2010 to November 2017)

14

Source: Eurex website

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

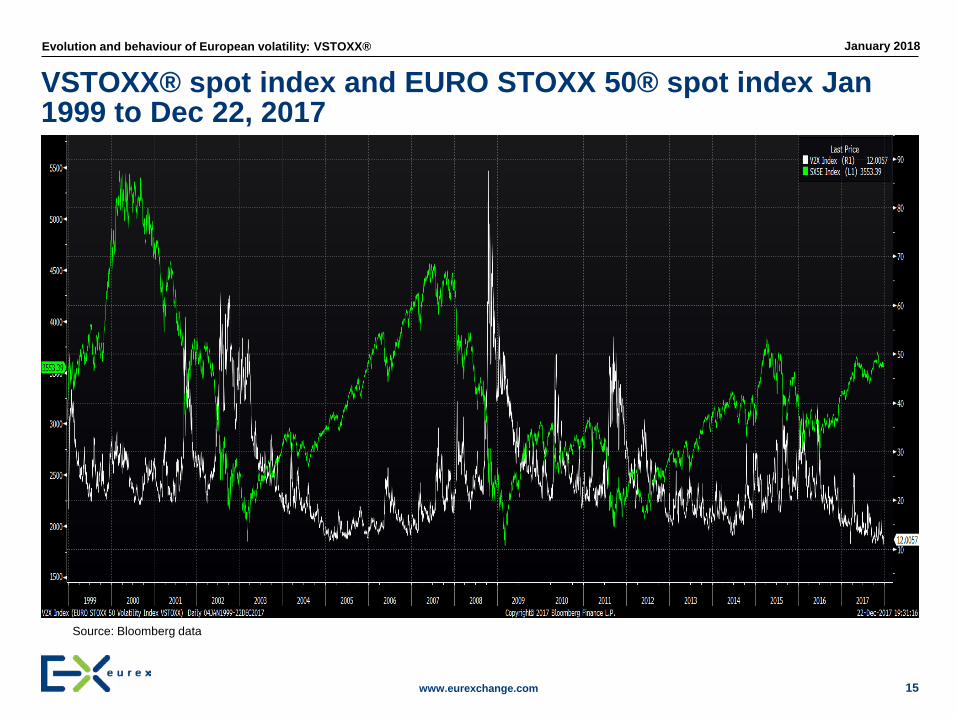

VSTOXX® spot index and EURO STOXX 50® spot index Jan 1999 to Dec 22, 2017

15

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• Hedging

• Directional trading

• Intra-market spreads = term structure

• VSTOXX® Futures / VIX futures spreads (relative value trading)

• Sentiment indicator

• Trading CFTC – certified options on the futures contracts

Utilizing VSTOXX® derivatives

16

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

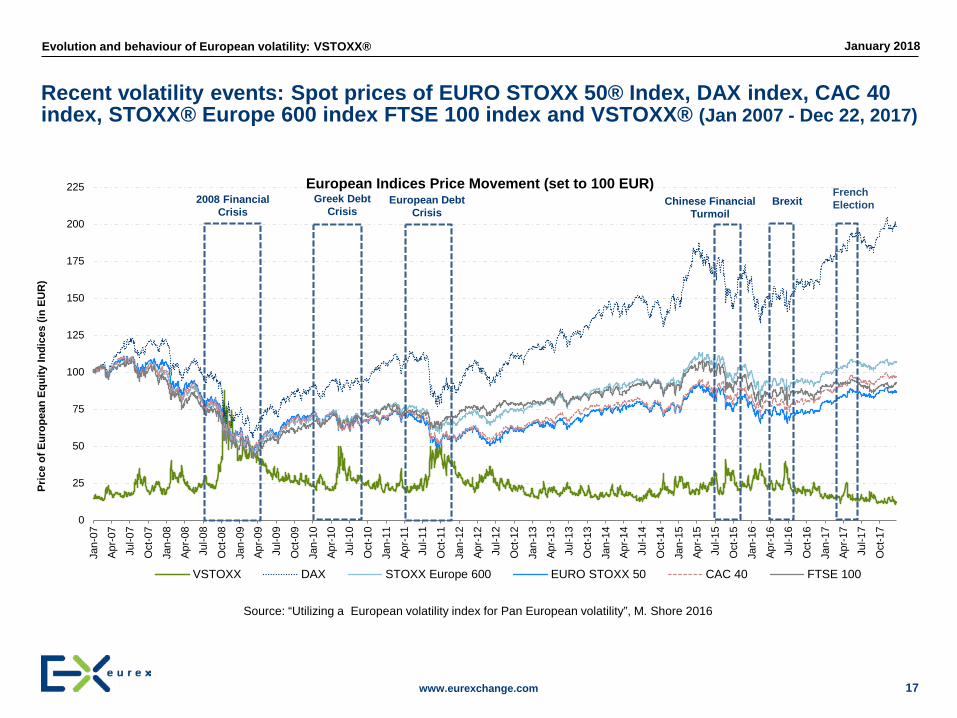

Recent volatility events: Spot prices of EURO STOXX 50® Index, DAX index, CAC 40 index, STOXX® Europe 600 index FTSE 100 index and VSTOXX® (Jan 2007 - Dec 22, 2017)

17

Source: “Utilizing a European volatility index for Pan European volatility”, M. Shore 2016

0

25

50

75

100

125

150

175

200

225

Jan-

07Ap

r-07

Jul-0

7

Oct

-07

Jan-

08Ap

r-08

Jul-0

8

Oct

-08

Jan-

09Ap

r-09

Jul-0

9

Oct

-09

Jan-

10Ap

r-10

Jul-1

0

Oct

-10

Jan-

11Ap

r-11

Jul-1

1

Oct

-11

Jan-

12Ap

r-12

Jul-1

2

Oct

-12

Jan-

13Ap

r-13

Jul-1

3

Oct

-13

Jan-

14Ap

r-14

Jul-1

4

Oct

-14

Jan-

15Ap

r-15

Jul-1

5

Oct

-15

Jan-

16Ap

r-16

Jul-1

6

Oct

-16

Jan-

17Ap

r-17

Jul-1

7

Oct

-17

Pric

e of

Eur

opea

n Eq

uity

Indi

ces

(in E

UR

)

European Indices Price Movement (set to 100 EUR)

VSTOXX DAX STOXX Europe 600 EURO STOXX 50 CAC 40 FTSE 100

European Debt Crisis

Chinese Financial Turmoil

Greek Debt Crisis

Brexit2008 Financial Crisis

French Election

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

VSTOXX® EURO STOXX 50® Index CAC 40 FTSE 100 DAX STOXX®

Europe 600

VSTOXX® 1.00 -0.77 -0.76 -0.67 -0.74 -0.76

EURO STOXX 50® Index 1.00 0.98 0.85 0.95 0.96

CAC 40 1.00 0.87 0.93 0.97

FTSE 100 1.00 0.82 0.94

DAX 1.00 0.93

STOXX® Europe 600 1.00

Can you apply VSTOXX® derivatives to other European equity indices?

18

Source: “Utilizing a European volatility index for Pan European volatility”, M. Shore 2016

• Pan-European Correlation Spot Prices (2 Jan 2007 to 30 Sept 2016 in EUR)

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

-60%

-40%

-20%

0%

20%

40%

60% 5-Day Rolling Return of European Equity Index Futures (2 April 2016 to 1 July 2016)

VSTOXX DAX STOXX Europe 600 CAC 40 EURO STOXX 50

European equity front months future returns vs VSTOXX® futures front month returns

19

Source: Utilizing a European volatility index for Pan European volatility”, M. Shore 2016

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

Why VSTOXX® is a better proxy for European volatility

20

0

100

200

300

400

500

600

700

800

900-1

.00

-0.9

5-0

.90

-0.8

5-0

.80

-0.7

5-0

.70

-0.6

5-0

.60

-0.5

5-0

.50

-0.4

5-0

.40

-0.3

5-0

.30

-0.2

5-0

.20

-0.1

5-0

.10

-0.0

50.

000.

050.

100.

150.

200.

250.

300.

350.

400.

450.

500.

550.

600.

650.

700.

750.

800.

850.

900.

951.

00

Freq

uenc

y

Correlation

Frequency of 5-Day Rolling Correlation of VSTOXX® Spot & VIX Spot to EURO STOXX 50® Index January 1999 to December 2013

VIX Correlation VSTOXX Correlation

Average Maximum Minimum5 Day Rolling PeriodVSTOXX ® spot correlation -0.85 0.57 -1.0VIX spot correlation -0.51 1.0 -1.0One-Month Rolling PeriodVSTOXX ® spot correlation -0.83 -0.28 -0.97VIX spot correlation -0.51 0.27 -0.87

Correlations of VSTOXX® spot and VIX spot to EURO STOXX 50® during -2% or greater equity market corrections

Source: “Noisy short-term correlations in global volatility index futures: why trading one regional index futures market may not be enough”, M. Shore 2014

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

12

14

16

18

20

22

24

26

28

30

32

1 2 3 4 5 6 7 8 9

19/6/2014 19/9/2014 6/10/2014 10/10/2014 16/10/2014

Contango to Backwardation: evolution of the volatility regime shift of VSTOXX® spot and VSTOXX® futures

21

• VSTOXX® is in contango 70% of the time since 2011: source Eurex Exchange

Source: “An analysis of why volatility indexes are relevant”, M. Shore 2014

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

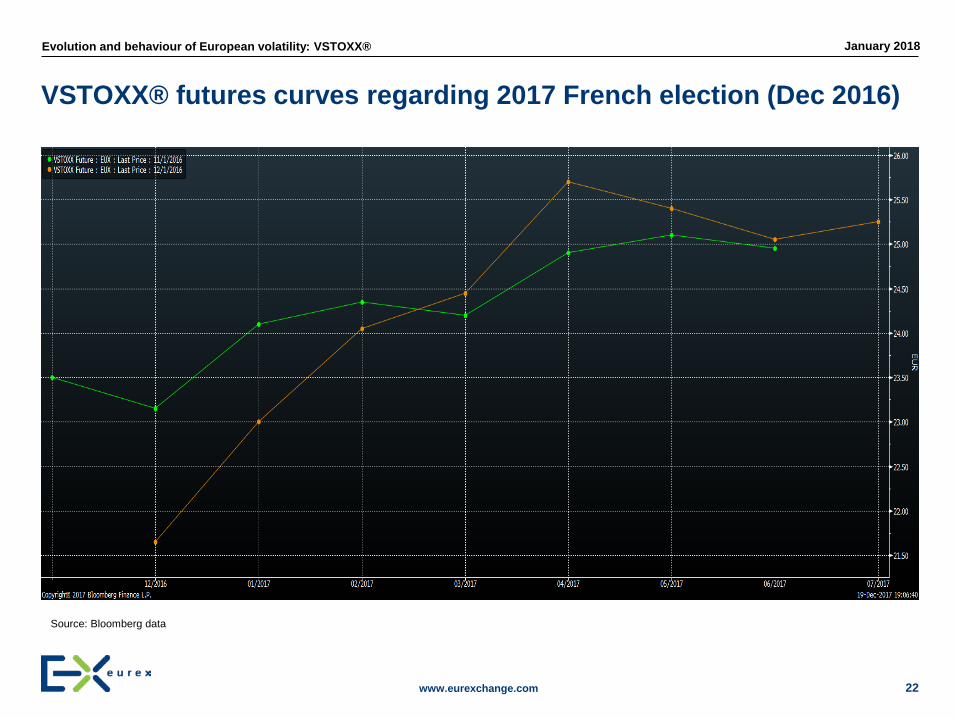

VSTOXX® futures curves regarding 2017 French election (Dec 2016)

22

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

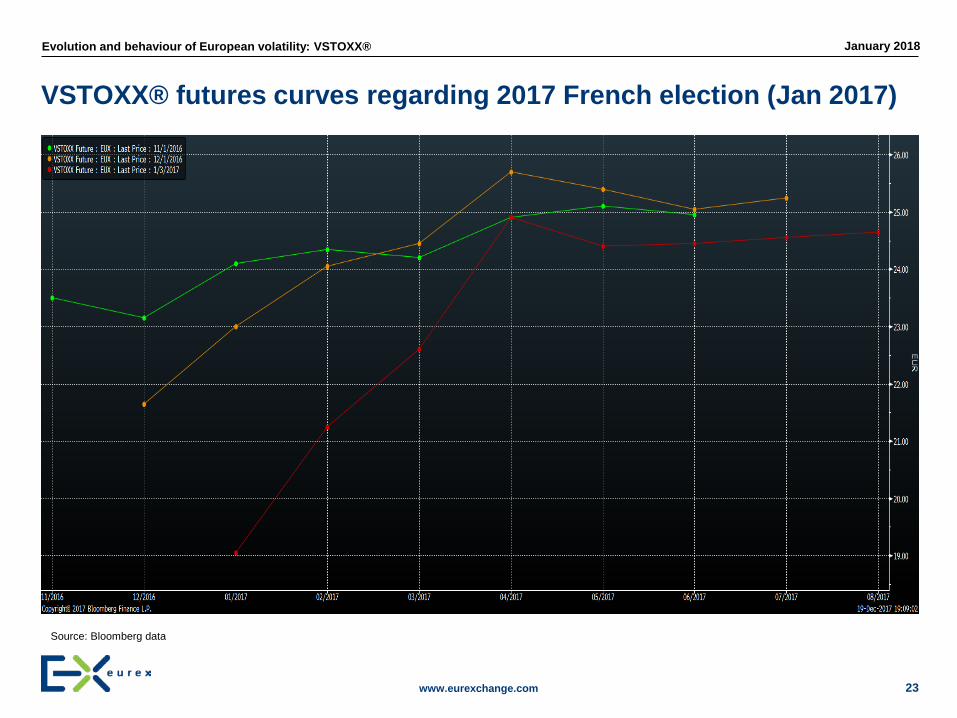

VSTOXX® futures curves regarding 2017 French election (Jan 2017)

23

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

VSTOXX® futures curves regarding 2017 French election (Feb 2017)

24

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

VSTOXX® futures curves regarding 2017 French election (Mar 2017)

25

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

VSTOXX® futures curves regarding 2017 French election (April 2017)

26

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

VSTOXX® futures curves regarding 2017 French election (May 2017)

27

Source: Bloomberg data

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

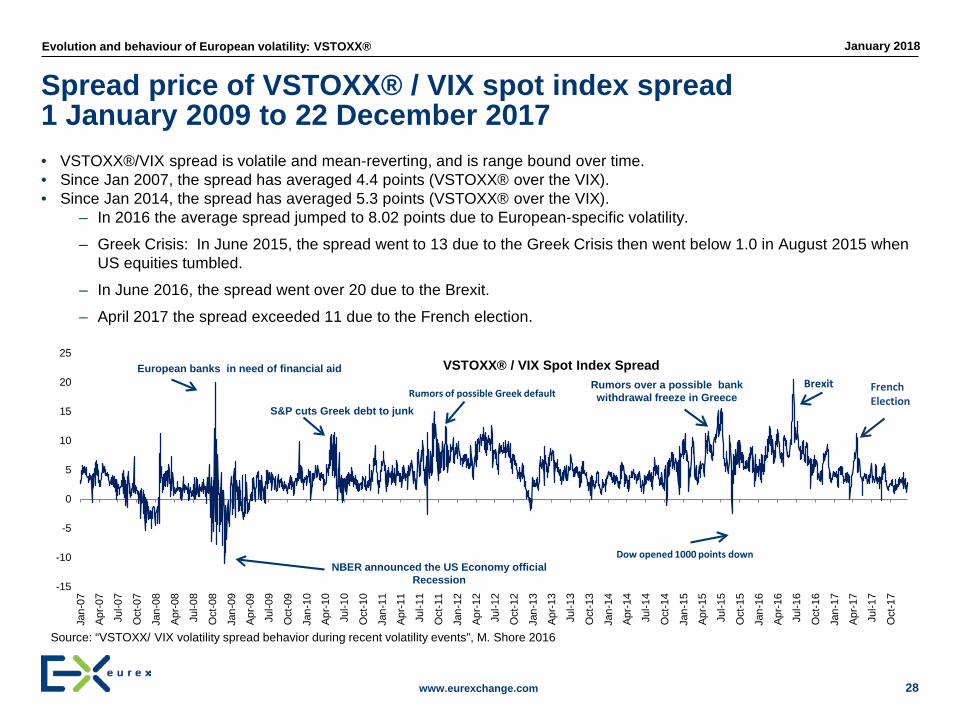

Spread price of VSTOXX® / VIX spot index spread 1 January 2009 to 22 December 2017

28

Source: “VSTOXX/ VIX volatility spread behavior during recent volatility events”, M. Shore 2016

• VSTOXX®/VIX spread is volatile and mean-reverting, and is range bound over time.• Since Jan 2007, the spread has averaged 4.4 points (VSTOXX® over the VIX).• Since Jan 2014, the spread has averaged 5.3 points (VSTOXX® over the VIX).

– In 2016 the average spread jumped to 8.02 points due to European-specific volatility.

– Greek Crisis: In June 2015, the spread went to 13 due to the Greek Crisis then went below 1.0 in August 2015 when US equities tumbled.

– In June 2016, the spread went over 20 due to the Brexit.

– April 2017 the spread exceeded 11 due to the French election.

-15

-10

-5

0

5

10

15

20

25

Jan-

07

Apr-0

7

Jul-0

7

Oct

-07

Jan-

08

Apr-0

8

Jul-0

8

Oct

-08

Jan-

09

Apr-0

9

Jul-0

9

Oct

-09

Jan-

10

Apr-1

0

Jul-1

0

Oct

-10

Jan-

11

Apr-1

1

Jul-1

1

Oct

-11

Jan-

12

Apr-1

2

Jul-1

2

Oct

-12

Jan-

13

Apr-1

3

Jul-1

3

Oct

-13

Jan-

14

Apr-1

4

Jul-1

4

Oct

-14

Jan-

15

Apr-1

5

Jul-1

5

Oct

-15

Jan-

16

Apr-1

6

Jul-1

6

Oct

-16

Jan-

17

Apr-1

7

Jul-1

7

Oct

-17

VSTOXX® / VIX Spot Index SpreadEuropean banks in need of financial aid

NBER announced the US Economy official Recession

S&P cuts Greek debt to junkRumors of possible Greek default

Dow opened 1000 points down

Rumors over a possible bank withdrawal freeze in Greece

Brexit French Election

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• The term structure of VSTOXX® Futures is frequently in contango (spot price is less than futures prices)

• When volatility begins to show up in the VSTOXX® index, it tends to experience greater moves in the spot, front and nearby futures months:

• If the market is in contango and an expectation of a larger move in the front month vs back months:– buy calls in the front month and buy puts in the back months– sell puts in the front month to receive some premium and the expectation the front month may move

higher

• If the market is expected to remain in contango:– buy puts in the back months as the price of the back months may decline as they move closer to

expiration

• If the futures term structure is in backwardation for an extended period of time: – determine to either buy puts or sell calls in the front month or nearby month with the perspective of

the VSTOXX® futures potentially moving lower

Potential ideas to think about regarding trading OVS2

29

Source: “Introduction on CFTC – certified Options on VSTOXX® Futures” M. Shore 2017

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

• Go to: http://www.eurexchange.com/exchange-en/products/vol/vstoxx

http://www.eurexgroup.com/group-en/newsroom/vstoxx-outlook

• Or to: http://www.shorecapmgmt.com/vstoxx-articles.html

For more information

30

www.eurexchange.com

Evolution and behaviour of European volatility: VSTOXX® January 2018

Thank You

31

Related Documents