EUROPE 2020 1 European Semester 20

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EUROPE 2020

1

European Semester 2012

EUROPE 2020

2

Annual Growth Survey 2012

EUROPE 2020

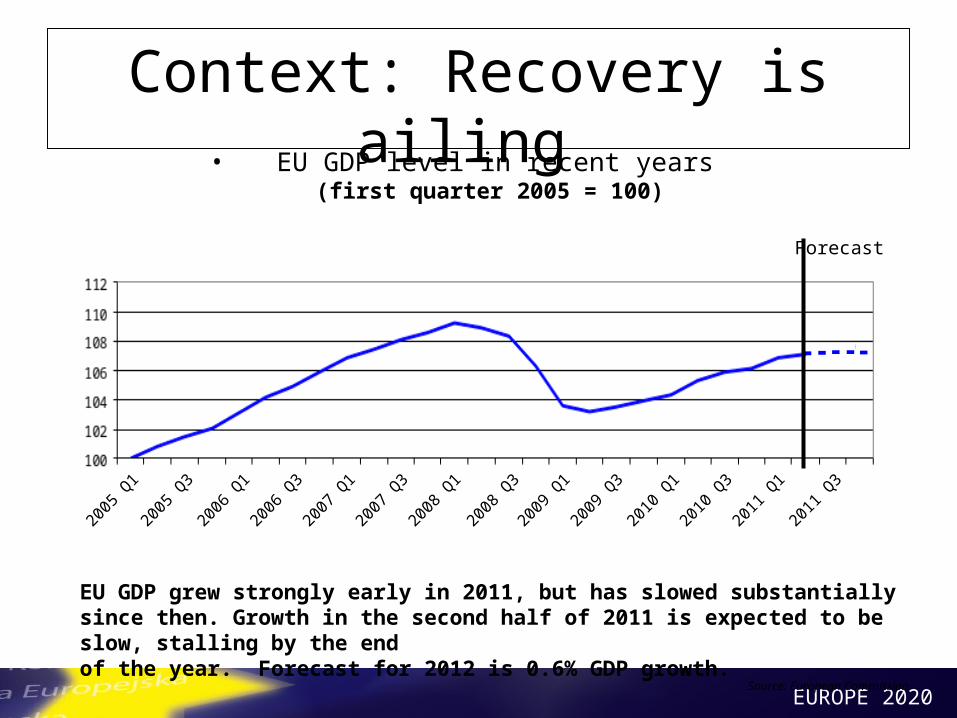

3Context: Recovery is ailing

• EU GDP level in recent years(first quarter 2005 = 100)

Source: European Commission

EU GDP grew strongly early in 2011, but has slowed substantially since then. Growth in the second half of 2011 is expected to be slow, stalling by the end of the year. Forecast for 2012 is 0.6% GDP growth.

Forecast

2005

Q1

2005

Q3

2006

Q3

2006

Q1

2007

Q3

2007

Q1

2008

Q1

2008

Q3

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

EUROPE 2020

4Unemployment is reaching high

levels•Unemployment rates in the EU, Euro Area, US

and Japan

23 million people are now unemployed in the EU (10% of the working age population) and 16 million in the euro area (9.5%). The slight improvement since 2010 has come to an halt.

Source: European Commission

2005

2006

2007

2008

2009

2010

2011

Japan EU Euro area US

%

EUROPE 2020

5Young people are particularly hit

Source: European Commission

•Youth unemployment rates in the EU, Euro Area and US

(under 25 year-olds)

Unemployment is twice as high for young people. It has increased sharply due to the crisis and is now over 20%.

EU Euro area US

2005

2006

2007

2008

2009

2010

2011

%

EUROPE 2020

6Confidence has been shaken…

Source: European Commission

Investors are still holding back, and household savings rates reflect caution, limiting overall economic demand.

•EU business investment ratios and households savings Business investment rate

(% of gross added value)

Households' saving rate (% of disposable income)

EUROPE 2020

7

- A Communication from the Commission - with an annex :EU specific proposals with substantial growth potential and indicative timelines

- 4 annexes

1. Progress report on Europe 2020 strategy2. Macro-economic report3. Joint employment report4. Growth friendly tax policies in Member States and better tax coordination in the EU.

2012 Annual Growth Survey: structure

EUROPE 2020

8

- Implementing the outcome of the 2011 European Semester is so far below expectations => strong emphasis on implementation in 2012 AGS

- Five priority areas for action:

1. Pursuing differentiated growth- friendly fiscal consolidation

2. Restoring normal lending to the economy3. Promoting growth and competitiveness for today and

tomorrow4. Tackling unemployment and the social consequences of

the crisis5. Modernising public administration

2012 Annual Growth Survey: Key messages

EUROPE 2020

9

1. Pursuing differentiated growth- friendly fiscal consolidation

-Differentiated strategies depending on the situation of MS (under financial assistance, with excessive deficit or without)

- Priority to be given on growth-friendly expenditure: education, research, innovation and energy. Reinforce employment services and active labour market policies.

- Continue the reform and modernisation of the pension system- respecting national traditions of social dialogue

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

10

Improve the contribution of the revenue side to fiscal consolidation:

For example by

- Broadening the tax base of certain taxes, reducing distortions (ex: VAT exemptions, environmentally harmful subsidies)

- Shifting taxation away from labour towards taxation less detrimental to growth: consumption, environment, wealth

- Improving the efficiency of tax collection and tackling tax evation

- Coordinating MS efforts through enhanced dialogue at EU level.

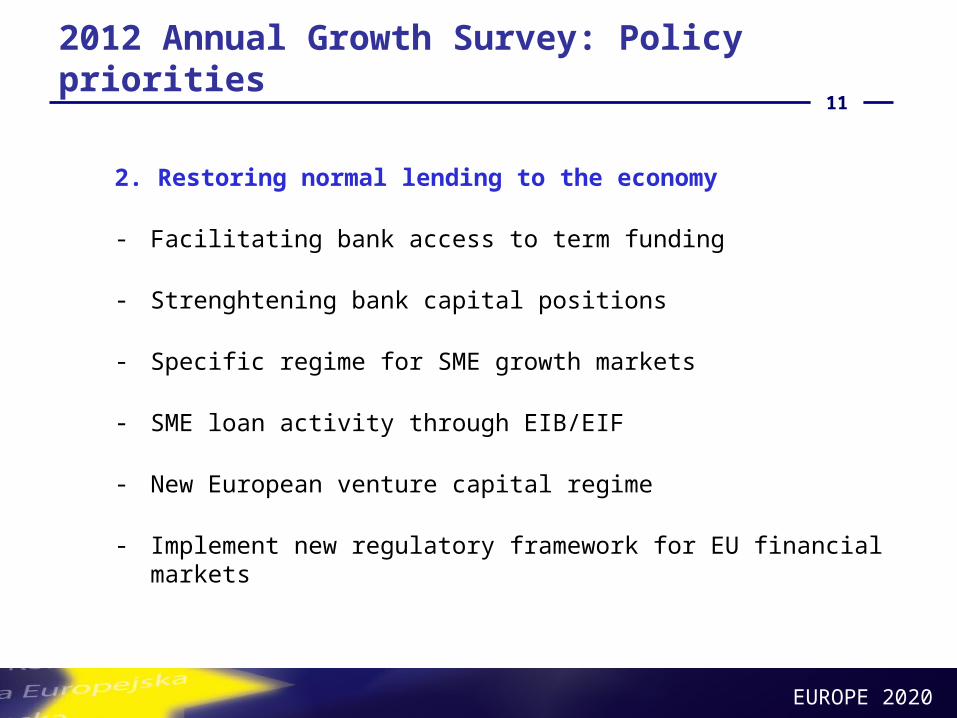

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

11

2. Restoring normal lending to the economy

- Facilitating bank access to term funding

- Strenghtening bank capital positions

- Specific regime for SME growth markets

- SME loan activity through EIB/EIF

- New European venture capital regime

- Implement new regulatory framework for EU financial markets

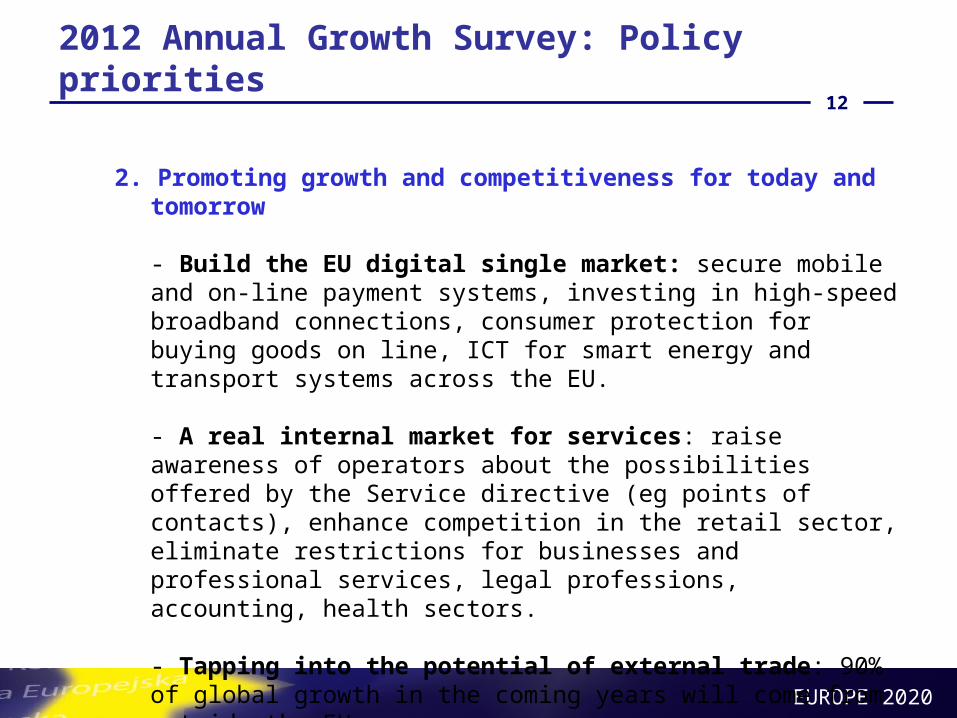

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

12

2. Promoting growth and competitiveness for today and tomorrow

- Build the EU digital single market: secure mobile and on-line payment systems, investing in high-speed broadband connections, consumer protection for buying goods on line, ICT for smart energy and transport systems across the EU.

- A real internal market for services: raise awareness of operators about the possibilities offered by the Service directive (eg points of contacts), enhance competition in the retail sector, eliminate restrictions for businesses and professional services, legal professions, accounting, health sectors.

- Tapping into the potential of external trade: 90% of global growth in the coming years will come from outside the EU.

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

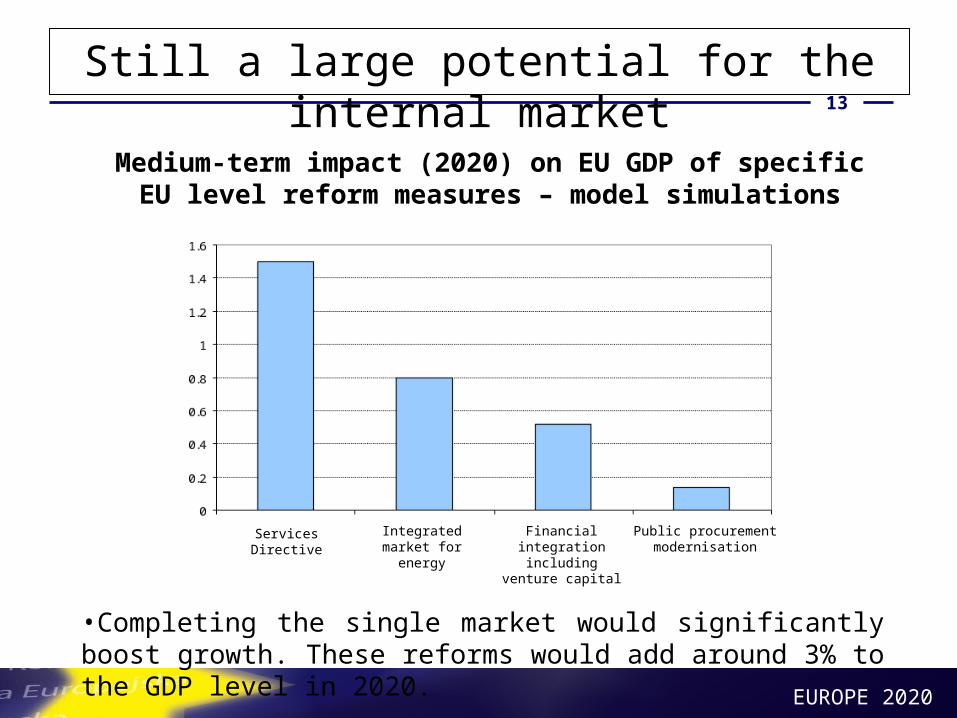

13

Still a large potential for the internal market

Medium-term impact (2020) on EU GDP of specific EU level reform measures – model simulations

•Completing the single market would significantly boost growth. These reforms would add around 3% to the GDP level in 2020.

Services Directive Integrated market for energy

Financial integration including venture

capital

Public procurement modernisation

EUROPE 2020

14

- Mobilise the EU budget for growth and competitiveness

- Using the potential of the EU structural funds

- Room for using or re-programming available funds: ex: support apprenticeship for young people with the ESF or energy efficiency investments programmes for household and firms

- Agree Commission proposal to increase the co-financing rates

-> Annex indentifying EU level decisions which can give an immediate boost to growth.

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

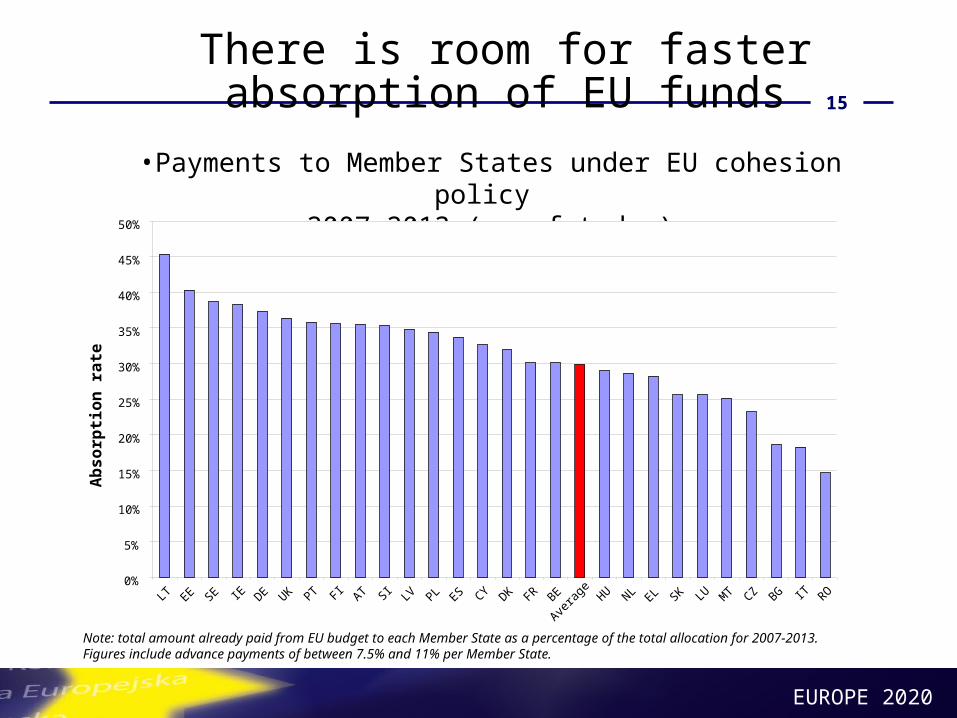

15

Note: total amount already paid from EU budget to each Member State as a percentage of the total allocation for 2007-2013. Figures include advance payments of between 7.5% and 11% per Member State.

There is room for faster absorption of EU funds

•Payments to Member States under EU cohesion policy 2007-2013 (as of today)

Ab

so

rpti

on

ra

te

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

LT EE SE IE DE UK PT FIAT SI

LV PL ES CY DK FR BE

Avera

ge HU NLEL SK LU M

T CZ BG IT RO

EUROPE 2020

16

4. Tackling unemployment and the social consequences of the crisis

Mobilising labour for growth:

- Enhance labour mobility by, for example, facilitating the recognition of professional qualifications and experience

- Implement recommendations on revision of wage-setting mechanisms

- Restricting access to early retirement schemes, support life-long learning

- Facilitate the development of sectors with high employment potential- including in the low-carbon economy, health and social sectors and digital economy.

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

17

Supporting employment of young people

- Target young people not in employment, education or training

- Engage with social partners to implement commitments to promote apprenticeships and traineeship contracts

- Reform employment protection legislation in consultation with social partners to reduce over-protection of workers with permanent contracts

- Adapt education and training to reflect labour market skills demand

- Review the quality and funding of universities

Protecting the vulnerable

- Improve the effectiveness of social protection systems- Implement active inclusion strategies- Ensure access to services supporting integration in the labour market (basic payment account, electricity supply, access to affordable housing)

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

18

5. Modernising public administration

- Minimise administrative burdens

- Increase administrative efficiency (e.g. through e-government)

- Implement the Small Business Act commitments to reduce time for starting up a company to 3 days by end 2012

2012 Annual Growth Survey: Policy priorities

EUROPE 2020

19

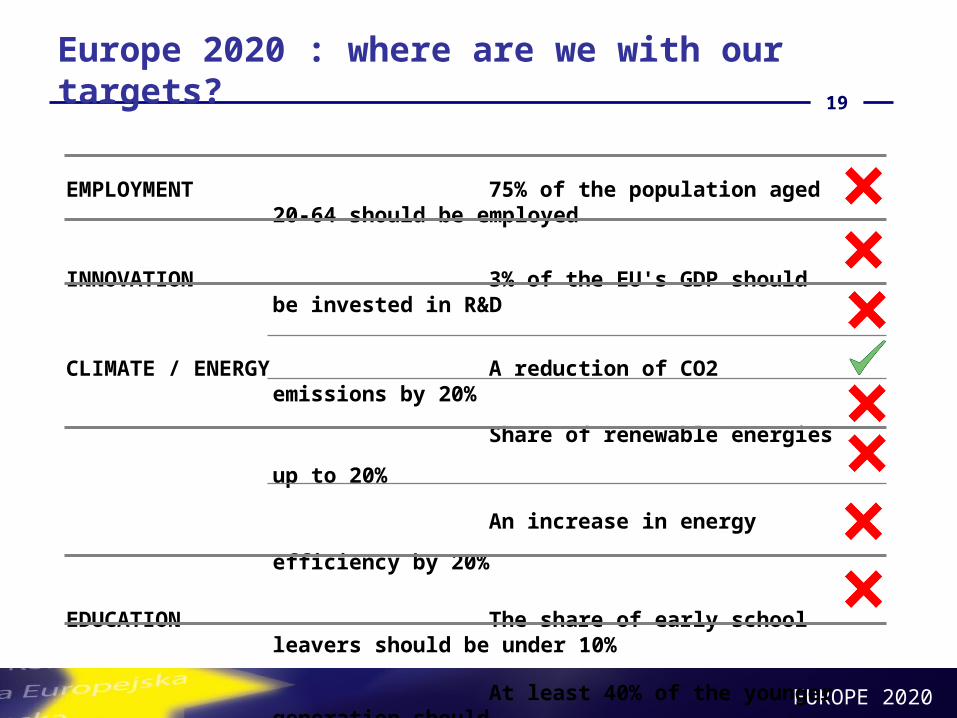

Europe 2020 : where are we with our targets?

EMPLOYMENT 75% of the population aged 20-64 should be employed

INNOVATION 3% of the EU's GDP should be invested in R&D

CLIMATE / ENERGY A reduction of CO2 emissions by 20%

Share of renewable energies up to

20%

An increase in energy efficiency

by 20%

EDUCATION The share of early school leavers should be under 10%

At least 40% of the younger generation should

have a degree or diploma

POVERTY 20 million fewer people should be at risk of poverty

EUROPE 2020

20

European Semester 2012: main steps

• AGS launched the 2012 European Semester for economic governance, 23/11/2011

• AGS to be examined by the Spring European Council on 1-2/3/2012

• Guidance to be incorporated in Member States’ updated NRP/SCP to be submitted in April 2012

• Commission to issue Country Specific Recommendations in view of European Council on 28-29/6/2012

• The new surveillance tools agreed as part of the 'Six Pack' will be used within the framework of the European Semester; possibility for sanctions in case of non compliance with CSRs

EUROPE 2020

21

Providing input to policy processes at national and EU level

- National level: Early input to the preparation and follow-up of NRPs

- EU-level:

• Feed-back on national NRP/Europe 2020 process: are you involved?

• Positions regarding the CSRs and planned actions by main social and economic stakeholders

• Your assessment of implementation of CSRs and other policy commitments (e.g. Euro plus pact, 2020 targets, flagships) at national level

• Timely EESC input feeding into Europe 2020 and the European semester

What is your role?

EUROPE 2020

22

Key role in implementation on the ground

• As underlined by the AGS: « The social partners will have an important role to play in implementing some of the recommendations. »

• In particular in mobilising employment for growth : revising wage-setting mechanisms, adapt unemployment benefits, combined with effective activation and training.

• And supporting employment: Promote quality apprenticeships and traineeships contracts

• Reform employment protection legislations, reduce the rigidities of permanent contracts, provide easier access to people left outside, particularly young people

What is your role?

EUROPE 2020

23

Documents and more information atwww.ec.europa.eu/europe2020

EUROPE 2020

24 2011 Recommendations for action at national level

NB: for EL, IE, LV, PT and RO, the only recommendation is to implement existing commitments under EU/IMF financial assistance programmes

Fiscalconsoli-dation

Long-term Sustain-

ability

Fiscalframework

TaxationWageSetting

Active Labour Market Policy

Labour market particip-

ation

EducationNetwork

industriesEnergy

efficiencyService sector

Business environ-

ment and SMEs

R&D and

innovation

Public services

and cohesion

policy

BankingHousing market

AT

BE

BG

CY

CZ

DE

DK

EE

ES

FI

FR

HU

IT

LT

LU

MT

NL

PL

SE

SI

SK

UKTotal number 22 16 10 6 8 11 17 9 7 5 10 6 2 7 5 3

Public finances Labour market Structural policies Financial stability

EUROPE 2020

25

E U R O P E 2 0 2 0

Related Documents