cJJ9Ndr.l, &do$ :- rgd: doaoo$d *oe4d eo. sJ.?"ro?iedo6 C:a6o$d)d .add 201 5-16 de EoOn eJE, dod.roeduo ddo E9$d d)od). **{i*,1 1993 d dNlr€3d #ozooJ:dd doe36 erQ Oo$d) dc)o 246(1) do_ {d{rod eQEidd *€dri edt doaroo$,go$ dNr.2015-16 de xood e3d* d&eio$&4 dultood: doo 246(5) d {iEDd ddao$$d dr d)rosd dd)3"x*,6derond. ddao$g og d-oeo.xd erd*ed#otribu aorto el3id:ddd$d iodar sd:!ds'o ddao$$4 3 ,9o?id.,ognon edt goe)Jo3d roo$r&aordd eQ6"0ri9) qdo?i ioior geicrond. dFEFo.3d ,dE?d ( ooa, dd* dod,oedd d.* dd* !o;oerDd/dd/2 016-17 / n3d: doasoo3:d €oe4d EE.:aJ.!.DiieEsE d:&60$$d. qeo$$1 d)aoeJcenaiodl diEbn-oR ,Orcrond dgi .asoej ) b0o$ e,ldode rddd: 49cof, sid* dod.o€ds! NQqlel I erdd:ejd. daoiro ddQ. asro$c))d. deo$$1 deo 246(5) d €i'od ejd+ doeh ddaoi,ooari Elobroa"rdd sQE"o?i$r soo,oEo do?5oo$d ,aocg $.a:adc-oB q#O?i drobgnoR 6"d,o dozroo$go$ daa 246(7) d d:edzl (J€ (ddd9?i cr$idr5o ddao3:d:o god$el dd* *od d 5 6*nie)) €-oeod. e .!-..)- o \ .9^J.l ^ gcogl c.JE .qca(J {rcliJe !,vrr ,,1;v$a*J Eeo6$ srJd&de Frdd:. de* 49Qob eJdr dodJoed-" 8*tro *oa.sioou, eoe4d

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

cJJ9Ndr.l,

&do$ :- rgd: doaoo$d *oe4d eo. sJ.?"ro?iedo6

C:a6o$d)d .add 201 5-16 de EoOn eJE,

dod.roeduo ddo E9$d d)od).**{i*,1

1993 d dNlr€3d #ozooJ:dd doe36 erQ Oo$d) dc)o 246(1) do_

{d{rod eQEidd *€dri edt doaroo$,go$ dNr.2015-16 de xood e3d*

d&eio$&4 dultood: doo 246(5) d {iEDd ddao$$d dr d)rosd dd)3"x*,6derond.

ddao$g og d-oeo.xd erd*ed#otribu aorto el3id:ddd$d iodar sd:!ds'oddao$$4 3 ,9o?id.,ognon edt goe)Jo3d roo$r&aordd eQ6"0ri9) qdo?iioior geicrond.

dFEFo.3d ,dE?d( ooa, dd* dod,oedd d.* dd*

!o;oerDd/dd/2 016-17 /

n3d: doasoo3:d €oe4dEE.:aJ.!.DiieEsE d:&60$$d.

qeo$$1 d)aoeJcenaiodldiEbn-oR ,Orcrond

dgi .asoej )b0o$ e,ldode rddd:

49cof, sid* dod.o€ds!NQqlel I

erdd:ejd. daoiro ddQ.

asro$c))d.

deo$$1 deo 246(5) d €i'od ejd+ doeh ddaoi,ooari Elobroa"rddsQE"o?i$r soo,oEo do?5oo$d ,aocg $.a:adc-oB q#O?i drobgnoR 6"d,odozroo$go$ daa 246(7) d d:edzl (J€ (ddd9?i cr$idr5o ddao3:d:o god$el

dd* *od d 5 6*nie)) €-oeod.

e .!-..)- o \ .9^J.l ^ gcogl c.JE .qca(J

{rcliJe !,vrr

,,1;v$a*JEeo6$ srJd&de Frdd:.

de* 49Qob eJdr dodJoed-"

8*tro *oa.sioou, eoe4d

duor[Jd iE-oFd

5oJ.ro€di *6 eJE 5s___ _:. _ _t -- _,

g*ood:4dd-e/nlda / €Adda / 2016 -11 /

iao$drd.

e"oo$ srDd&deFddd dqJeo,

!eeo! c.i* Eod,oedo-oadNc.r qJeI I

od"d&/&6Ln3d) doeroo$g

&do$ : D.sDdc-EG Eo$Jod e,@eJEd rts* dosroo$co$ 2015-l6de

-."- "e- '3d-oreuo -68 Eelid Dri.

*++++*duo-63d Sosroqld EozEs erQ&ob* 1993d d{a56 246(6)d c{oji &6ob&d *el-o$

?r.0lEzie-o6 EEe.oSd 8-@CtOd rB$ dotiooi.go$ 2015-16de rEOd dd* dodJocduo

-o6or&d * SgdJooA?i C)fig?' 6q:b4cro^d.ldd c*Qzi ejdd d0i.rded6to $e*dod: ddr a,odtr d.o.1000=00dd&d dddg ?,!J*

d,o. r1,000/-(dd.o4o& Eoad)rid$d * d.rodei * t$nd dd+ 5f&rdd dcrE sD.rod

a?io$$ddg qjdlED d5Ee aioF6 d.go$$r * ddcod 2"dni$ E& 6&niDdd.

70 eEdc eJd9g nfddgi60 eddr B€d?19)

110 iE-oro eJi+ doglo(dd-o &e.))*

0 eJl dor"o€c -o $9)+01 rrosid erd+ dg qc'oeJ

d i dod"ocd o ddBo$gd doG8deri EEoiro$ JddF6 246(6)d edo$ e&rdF.oddao$$4 dr,od) .ao?i$lddmn E"o$r O-?FdFoQroodd) edoii dq.blDd* ddac$de)&ddd eedd.g B*)8oien d"orderoRd.

toerod

vv49.-{r^FrAli e.\i5rlF-!ilrlr

d% 4efo$ dd+ dodJoeCN" doo$dBro dod!c$d' €.o(Dd.

dda 5i3oi:ib;-

1) E?obr&-oadFoQEoo?iC) 6oc).,od doasoobd e.sDzi( oB edorl d6o0roe do?^rooig6

does6 eQ&obdr-246(6)d{on 3 go?idJoesnoR o$ndd ddojndd:. oJ5Edde

diJocro,g eC-o z106 erD9d)e,oo&&d ei{eddriezi i*SdF gr$ ttJodeAdgdoe-roobse o-0.E6 eeQno$dr ddd.0-240(7) drgl 2a0(8)d EiEod g;1, te)e/o*raa*.

2) drodocjesroEDe& (D&o*D) (o&q) 1&2, diroFt^3d, zJo?id,o&.

Sooo$ err)d&derdd6,dr* 49f o$ ddd dodJoedda

dcjo$ i?;o$$d

The statement showing the major shorlcomings found in 2015-16 years audit enquiry of Gram panchayat

Kolhar tq. B bagewadi , DistVijaypur.

Sl.no. NoteNo.

Short comins details in brief

1 03 Previous \ears audit report. compliance not iubmitred.2 05 Grant register ot maintained.

08 Budget statement not produced.

4 09 Classifi cation register to maintained5 10 Impodant Register not maintained6 l8 Asset register not maintained1 2l Important Register not maintained

8 25 SupDlmeltry not deposited to soven]ment9 Labouers revised list not Dresneted

*DesdQ6o0ddtd*ro doz.Eoi)d, €Joerad.

Dist Local Auditing Circle

VIJAYPUR.

\Jtyb-\e/"Assistant Controler

Gram panchayat KOLHAR tq. B bagewadi, DistVijaypur.

Statement showing objection and recovery suggested amount details in audit enquiry for 2015-16

Assistant Controler

Dist Local Auditing Circle

VIJAYPUR.

sl.No

Note No. Objection in Brief Amount kept in

Objection

Amountsuggested

for receipt

1 25 Supplmentry not deposited to govemment 62469

2 31 Audit fees to be deposited 1000

3 31 Income tax, sales ta\, and Royalty not deposited

to gowerrment

65520

Total 128989

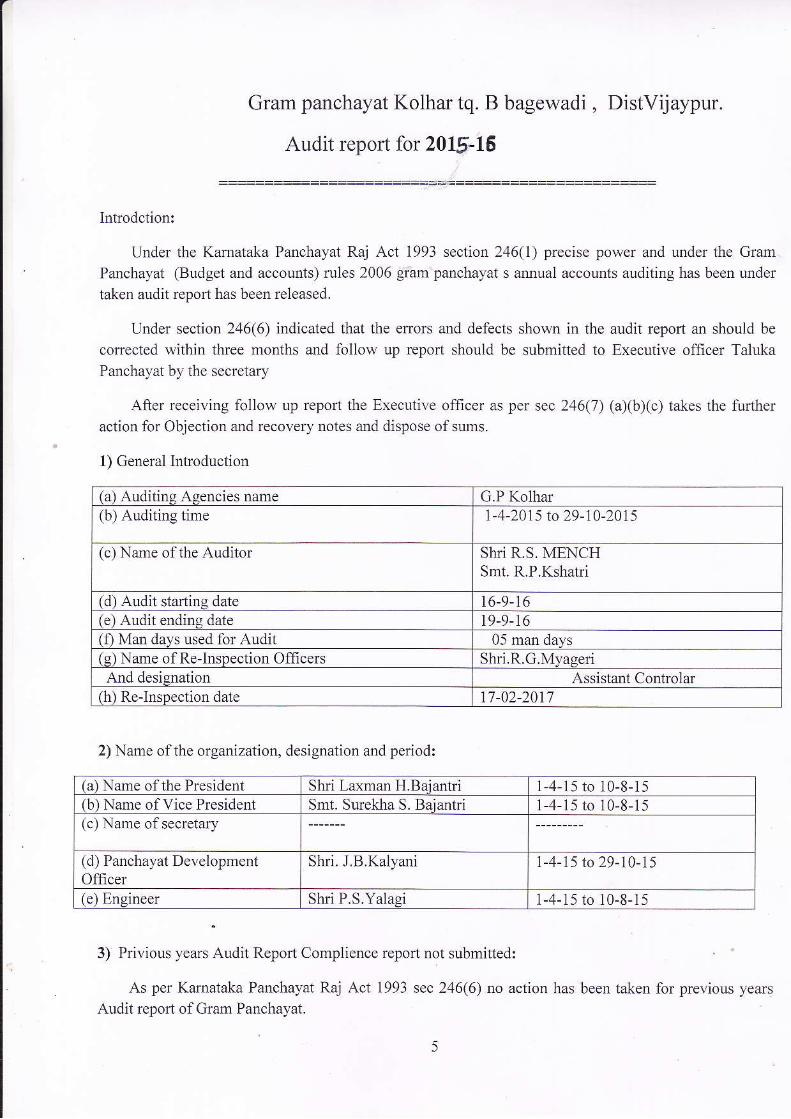

Gram panchayat Kolhar tq. B bagewadi , DistVijaypur.

Audit report for 2015-16

Intrcdction:

Under the Karnataka Panchayat Raj Act 1993 section 246(1) precise power and under the Gram

Panchayat (Budget and accounts) n es 2006 gram panchayat s annual accounts auditing has been r-rnder

taken audit report has been released.

Under section 246(6) indicated that the erors and defects shown in the audit repot an should be

co ected within three months and follow up repofi should be submitted to Executive officer TalukaPanchayat by thc secretary

After receiving follow up repofl the Executive officer as per sec 216(7) (axbxc) takes the l'urther

action for Obiection and recovery notes and dispose ofsums.

1) General Intoduction

2) Name ofthe organization, designation and pe od:

3) Privious years Audit Report Complience report not submitted:

As per Kamataka Panchayat Raj Act 1993 sec 246(6) no action has been taken for previous years

Audir repon olGram Panchalat.

(a) Auditins Asencies name G.P Kolhar(b) Auditing time l-4-2015 to29-10-2015

(c) Name ofthe Auditor Shri R.S. MENCHSmt. R.P.Kshatd

(d) Audii starting date 16-9-16(e) Audit endins date l9-9-16(1) Man days used for Audit 05 mcn days(s) Name ofRe-lnsoection Office$ Shri.R.G.M\,al]eriAnd desiEnation Assistant Controlar

(h) Re-InsDection dale 17 -02-201',7

(a) Name ofthe President Shri Laxman H.Baiantri 1,4-15 to 10-8-t 5

(b.) Name of Vice President Smt. Surekla S. Baiantri 1-4-15 to 10-8-15(c) Name of secretary

(d) Panchayat DevslopmentOflicer

Shri. J.B.Kalyani 1-4-15 to 29-10-15

(e) Engineer Shri P.S.Yalaei 1-4-15 to 10-8- l5

As per Sec 246(8) of Kamataka Panchyat Raj the Executive officer

Taluka Panchayat, no case of issue ofdebts and exhaust found.

Therefore. the executive officer and gram, panchalt secretary are asked to take action

under section 246(6) and (8) ofKarnataka Panchayat Raj Act.

'fhe renraining objection and recovery suggesied amounts are as follows:

4) Financial Position:

For 2015-16 financial position of Class 1 is prepared in annexure 1 And comprehensivefinancial position is prepared in annexur 2 and enclosed at the end ofthe audit report.

9) Gmnts:

As per sec 87 of Kamataka Panchayat Raj Act 1995 Gmnt registe. is 11ot prepared. Suggested toprepare and produce.

As per cuffent pass book and cash book details ofgrant are found as follows.

6

S1.No Audit year NoteNo

Objectionamotmt

NoteNo

Suggested ofreceiDt sum

1 1994-95 04 15102 05 6000, 1995-96 15 66076 10 '7523

1996-97 04 23815 03 285 5

I 1997-98 04 5979 02 t7705 1998-99 t0 53321 03 247 5

6 1999-2000 02 47009 04 t4t967 2000-01 02 24480 01 )5258 2001-02 03 t2565 02 9129 2002-03 02 1002010 2003-04 04 62783 02 554I 2004-05 69649 01 I97,1812 2005-06 04 118234 04 106843'll 2006-07 02 80628 02 20040511 2007-08 04 1152',72 03 1289015 2008-09 04 12397416 2009-10 03 1i5638 0t 3031517 2010-t I 03 10889018 2011-12 006 127011t9 2012-13 0) 983 86 01 1947120 2013-14 1 5058402t 2014-15 02 7065t

Total 83 t9912t2 44 s10002Added i[ curretlt vear( 14-15 ) 03 128989

Total 86 2t2U0t 510002Balance on 3l-3-16 86 2t2020t 44 s10002

Sl.No Name of the schemes for grantreleased

Released Grant Deduction

Amountcredited

Credited vear

1 Il"'financial YotLiana t3'15614 t3756t4 2015-16

2 Water management 10048 10048 Do3 StaffSalary 6t23',7 t 61237t Do4 Ra.U.Kia vo 14836!, 1,18364 Do5 73300 73800 Do

Total 2220t9',1 2220t97

6) Investments:

According to Karnataka Gram Pancha)ats (balarce sheet and accountirg management) Act 2006

rule 95, formate 'l l invenstment register is Dot maintained. Instructed to maintain according to the rule

maintained.

7) Deposits:

According to Kamataka Gram Panchayats (balance sheet and accounting management) Act 2006

rule 100, fonnate-,17 deposite register is not mairtained. Because ofthat details ofdeposits cannot be

conformed. Instructed to maintaiD deposit register as pe. the rule.

8) Budget:

Duing 2015-16 audits work approved Budget for cu ent year not produced. Because ofthatcrment estimated income, expenditure and 20o% reseNe amounts infomation could not be found. Witlroutbudget approval, on what base Gram panchayat's transactions are to be done? Therefore, instructed tobudget approval is to be taken first.

9) Ilcome and expendilure statement:

According to Kamataka Gram Panchayats (balance sheet and accounting) rules 1995 rule 30

incomes and expenditure classification register not mailtained. Tlis register is most essential so,

prcpared and presented.

As per Kamataka Panchayat Raj Act 1993 sec 244 araual accounts are not approved from grum

panchayat and submitted to zila panchayat.

The income and expenditue details given by the organization and on the bases cash book,

voucher confomred. The said statement given in annexure 1.

As per Kamataka Panchayat Raj Accounts rules 1995 sec 42(2) montfiy accounts ate not ceftifiedby ChiefAccountant Z.P. in fomat 9. Therefor informed to produce cefiified accounts10) Important RegisteN not maintained:

According to Kamataka Gram Panchayat Raj (Gram Panchayat balance sheet and accounting)

rules 2006, Accormts rules 2006 the following impotant registeN according to their rules not maintained.

Instructed to prepare the important registers in proper forms and produce in next audit.

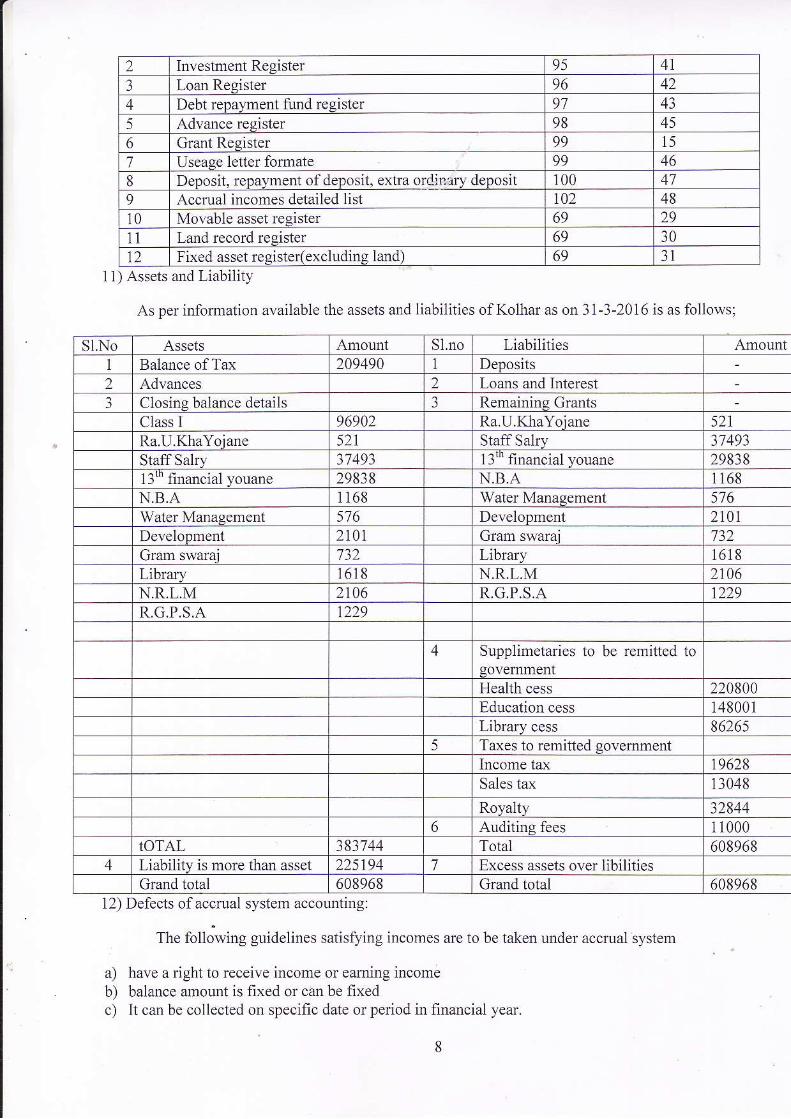

Sl.No Not maintained Registers Rule No Fomate No1 Work complited Register 92 40

2 Investment Register 95 41

Loan Register 96 12

4 Debt reDayment fund register 97 43

5 Advauce register 98 45

6 Grant Register 99 t5,1 Usease letter fomate 99 46

8 Deposit, repayment ofdeposit, extra ordicery deposit r00 47

9 Accrual incomes detailed list t02 48

10 Mo\able asset Iegister 69 29

11 Land record register 69 30

12 Fixed asset resister(excludinc land) 69 31

11) Assets and Liability

As per infomration available the assets and liabilities of Kolhar as on 31-3-2016 is as follows:

Sl.No Assets Sl.no Liabilities AmountBalance of Ta,r 20949C) I Deposits

2 Advances 2 Loans and InterestClosins balance details 3 Remainin,:I CrantsClass I 96902 Ra.U.ICnYoiane 521

Ra.U.KhaYoiane s21 Staff SaIIY 37493

staffsalr\ 37493 13"'financial youane 29838I3'" financial vouane 29838 N.B,A 1168

N.B-A 1i68 Water Manasement 5',76

Water Management 5',76 Develooment 2101DeveloDment 210 t Gram swarai '732

Gram swarai 732 Librarv 1618

Librarv 161 8 N.R,L.M 2106N.R,L,M 2106 R.G.P.S.A t229R,G,P,S.A t229

4 Supplimetaries to be remitted togoveIIlmentHealih cess 220800Education cess r 48001Library cess 86265

5 Ta\es to remitted govemment

Income tirx 19628Sales ta,\ I3048

Royalty 328446 Auditing fees 1 1000

TOTAL 3837 41 Total 6089684 l,iabilitv is rnore than asset 225194 7 Excess assets over libililies

Grand total 608968 Grand total 60896812) Defects ofaccrual system accounting:

The following guidelines satisfying incomes are to be taken under accrual system

a) ha\ e a right to recei\e incomeoreaming incomeb) balance amounl is fixed or can be fixedc) It cau be collected on specific date or period in hnancial year.

1) Generally as demand, collection and fees accounts land and building tax income, vehicle tax, taxon advertisement board, water mtes, rent on pabchayat assets, linces, etc are included rurderaccrual system.

2) Demand on account and accrued illcome included statement in prepared in formate 48. On thatbases gram panchayat secretary/ P.D,O.prepare income receivable account regarding whole yearincome. Fomate 48 showing detailed list nol prepared and presented to auditor.

3) On the collection balances othem incomes are faken iD account4) On the base of format 48, G.P secretary shouid debit the the incomes received by general

voucherc to income accounts ( sepa-rate gene.al iedger format 52 rule (107), collected incomeshould be accured. Some incomes does not include previous financial year balance information.

5) All coliected incomes as they are accepted added to .eceivable income account. It should beshown il the Balance Sheet as receivabk account as out standing. It obseNed that some incomesarc not included.

6) Incon1es not coming under cash base income or accrual base income are taken into accoultt only\r'hen they a-re actually received or accepted.Accrual expenditure:1) All expelNes whether they are paid or not paid they are considered as expenditures. The

paymenl made tbtough gram panchayat f,mds, every welfare u,ork should be verified withwork order/supply order/ demand bill. If they are in p.oper order accued through generalvoucher. In the current year works account to be included general voucher not accuredobseNed in auditing.

2) Such expenditures accmal a.e considered at the year end along with staff/ administionexpenditure works order and contactors bill,ifthey are related to goods and services storebills. Such expenditures accrual should be shown in the Balance Sheet as payableexpenditur.es. It is obseNed in the audit that restoration ofu,orks is consideted.

3) Said years paid all expenditures (excluding balance receipt) ca.not be justified whether thataccounts are based absolutely real bills. Acceptanace and bills are of previous yearl currentyear and next year c.innot bejustigied patactically at initial stages.

14) Short comings in Cash Book Management:

Cash book is maintained according to Karnatata Panchayat Rai (Budget and Accounts)rule 2006 sec 104 states in fomat 49. Next financial year the following instructions to maintain cashbook and related other docunents to be considered.

Cash book having cash and bank colunm should be maintained as given in fomat 49. Cash andt.easure/bank tansaction of panchayat should be recorded in iLcram panchayats receipts and paymentstasactions should be recorded in related colrl1nn. Banl account debit / incomes (credit) should berecorded at the left hand side of cash book. Cash book should be recorded on the bases of receiptbook.(day book collection), cheque receipt register records and bant deposit challan, and paid vouchersand cheque paid register records. It is inst.ucted to maintain Cash book to be as following:

1) Cash book should be in printed form and machanised page number should give. Current cashbook does not have machanised page numbers.

2) Confim that the pages are conect in the cash book, fo. that oD the first page ofthe page numbershould be mentioned and cerfied by secretary.

3) Cash book should be closed daily. Acutual cash and book balance should tally. Such tally amountrecorded in the book and certified is necessary

4) The details of closing balance such as collected amount not deposited within the specified day,undistributed salary, advance amount,etc. I1ot recorded.

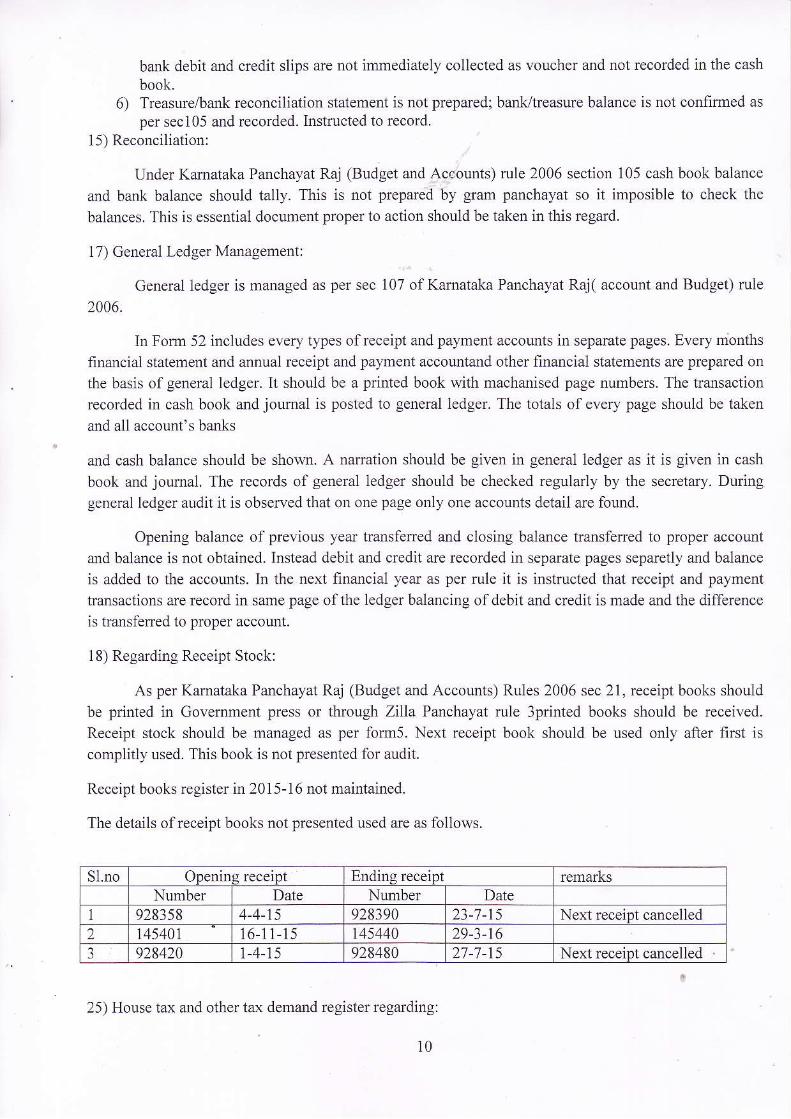

5) Debit and credit slips received ftom bank recorded accordilgly in the book. Comnission andinterest credited in pass bookd should be recorded in cash book. It is obserwed in auditing that

bank debit and credit slips are not immediately collected as voucher and not reco.ded in the cash

book.6) Treasure/bant reconciliation statement is not prepared; bank/treasue balance is not confirmed as

per sec105 and recorded. lnstructed to record.15) Reconciliation:

Under Kamataka Panchayat Raj (Budget and Accounts) rule 2006 section 105 cash book balance

and bank balance should tally. This is not prcpared by gram panchayat so it imposible to check the

baiances. This is essential document proper to action should be taken in this regard.

l7) General Ledger Ma[agement:

General ledger is managed as per sec 107 of Kamataka Panchayat Raj( account and Budget) rule

2006.

In Fonn 52 includes every types ofreceipt and payment accounts in separate pages. Every months

financial statement and annual receipt and payment accountand other financial statements are prepared on

the basis of general ledger. It should be a printed book with machanised page numbers. The t.amactiollrecorded in cash book and journa] is posted to general ledger. The totals of every page should be taken

and all account's bants

and cash balance should be shown. A naration should be given in general ledger as it is given in cash

book and joLrmal. The records of general ledger should be checked regularly by the secretary. Duringgeneral ledger audit it is observed that on one page only one accounts detail are fould.

Opening balance of previous year hansfered and closing balance transferred to proper accounl

and balance is not obtained. Instead debit and credit are recorded iI1 separate pages separetly and balance

is added to the accoullts. In the next financial year as per rule it is instructed that receipt and payment

tansactions are record in same page ofthe ledger balancing ofdebit and qedit is made and the difference

is tmnsllned 1() proper accorurt.

18) Regarding Receipt Stock:

As per Karnataka Panchayat Raj (Budget and Accounts) Ruies 2006 sec 2l, receipt books should

be printed in Govemment press or tfuough Zilla Pa[chayat rule 3printed books should be received.

Receipt stock should be managed as per fom5. Next receipt book should be used only afler first iscomplitly used. This book is not presented for audit.

Receipt books register in 2015-16 not maintained.

The details ofreceipt books not presented used are as follows.

Si.no ODenins receiDt Endin,:r recejpt rcmarksNumber Date Number Date

1 928358 1-4-15 928390 23-1-15 Next receiDt cancelled2 145401 16-11-15 145440 29-3-t6

928420 1-4-15 928480 27-1-15 Next receipt cancelled

25) House tax and other tax demand register regarding:

10

As per Kamataka Panchyat Raj Act 1995 sec 45 tax demand, collection, balance register not

produced for auditing. Therefore tax balance, demand and collection can not be found. It is instructed to

such essential register maintained colTectly posted, totaling made cerified and presented

The curent organization given the following details oftemporary t.Lx dema[d, recovery and balance

26) Tax Revision:

As per Kamataka Panchyat Raj Act 1993 Sec 199 schedule 4, taxes are to be revised in every,lyeals. It is not found in said period. It instructed to under take revision oftaxs.

27) The Government supplementary not deposited to government:

For the .vear 201,1-i 5 Govemment Supplmentaries are collected, but after deducting 10% ofamount collected balance 90o% not deposited to Govemment. Instructed to deposit the same

immediately. The details are as follows

Sl.no. particulars Health Cess EducationCess

Library Cess

Recovered in the vear 2015 16 33599 22399 134392 107o recoverv deducted 33 59 2239 t3433 Remaining 90% to be remitted to

Government30240 20160 12096

4 Balance of20l4-15 190560 127841 '74169

5 Iotalto be deposited 220800 148001 862656 Deposited with govenrment in2014-15

7 Balances 220800 148001 86265supplimentaries balances are more so insrrucled ro depo.it immedi culTentThe supplimentaries balances are more so instructed to deposit imme(

remittance amount Rs 0.00 is kept i1l objection until supplementary is deposited.year

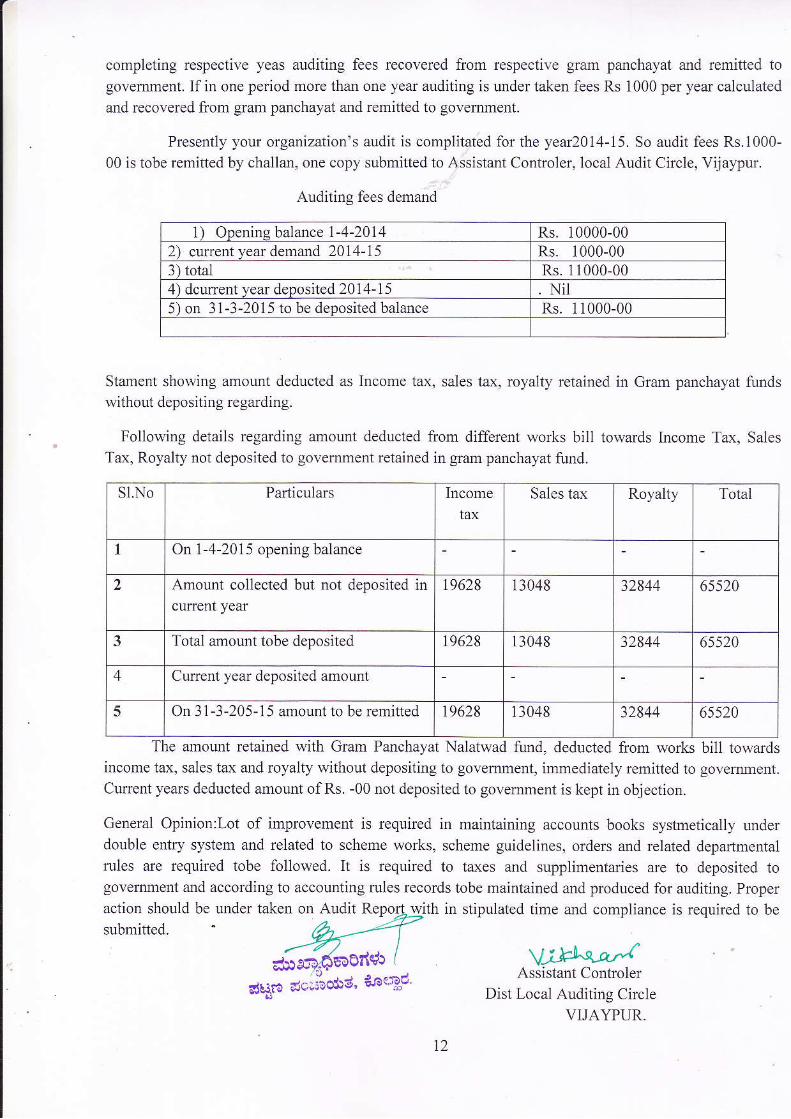

36) Audit fees

Under the Kamataka Panchayat Raj Accounts and Budget Rules 2005 sec 42(b) gram

panchayats one years audit fee is Rs. 1000 on1y. lt is instructed to said fees should be accounted and afler

1t

Sl.No. Tax pafiiculars Demand total Recovery inthe year 2014-15

Balance

balance cu1Tent

I House tax 1426',78 179804 322482 223997 98485

2 Water tax 38475 114870 153345 126561 26'184

3 Light tax 8791 1 122E74 210781 126560 84221

Total 269064 417544 686608 4771t8 209490

SupDlimentaryI Health Cess 85120 269',71 112091 33599 '78492 .

2 Ilducation Cess 5 8150 17980 76t30 22399 53731Library Cess 35695 10788 46483 13439 33044

Grand total 448029 4',73283 9213t2 546555 3747 5',7

completing respective yeas auditing fees recovered ftom respective gram panchayat and rcmitted to

govemment. If in one period more than one year auditing is under taken fees Rs 1000 per year calculated

and recovered from gaam panchayat and remitted to govemment.

Presently your organization's audit is complitated for the year2014-15. So audit fees Rs.1000-

00 is tobe remitted by challan, one copy submitted to Assistant Controler, loca1 Audit Circle, Vijaypur.

Auditing fees demand

l) Opening balance I -4-2014 Rs. 10000-002) current year demand 2014-i5 Rs. I000-003) total Rs. 1 1000-004) dcurent Year deposited 2014-15 . Nil5)on ll-3-2015 to be deposited balance Rs. 11000-00

Stament showing amount deducted as Income tax, sales tax, royalty retained il1 Gram panchayat funds

without depositing regarding.

Follo\i,ing details regarding amount deducted ftom different works bill towards Income Tax, Sales

Tax, Royalty not deposited to government retained in gram panchayat flurd.

Sl,NO Particulars Income

taxSales tax Royalty Total

1 On 1-4-2015 opening balance

2 Amount collected but not deposited incurent vear

t9628 13048 ))844 65520

Total amouDt tobe deposited t9628 13048 32844 6ss20

4 Cullent year deposited amount

5 On 31-3-205-15 amount to be rernitted 19628 13048 32844 6ss20

The amount retained with Gram Panchayat Nalatwad fund, deducted from works bill towardsincome tax, sales tax aDd royalty without depositing to govemment, immediately rcmitted to govemment.

Cun'ent yeals deducted amount ofRs. -00 not deposited to govemment is kept in objection.

General Opinion:Lot of imprcvement is required in maintaining accounts books systmetically underdouble enty system and rclated to scheme works, scheme guidelines, orders and related departmentalrules are required tobe followed. It is required to ta\es and supplitnenta es are to deposited togovenlme[t and according to accounting rules records tobe maintained and produced for auditing. Properaction should be under taken on Audit with in stipulated time and compliance is required to be

U;!1l"s,w.fAssistant Controler

Dist Local Auditing CircleVI]AYPI]R

0d9:

suhmitted.

dsira daJio$d' nJoegd

12

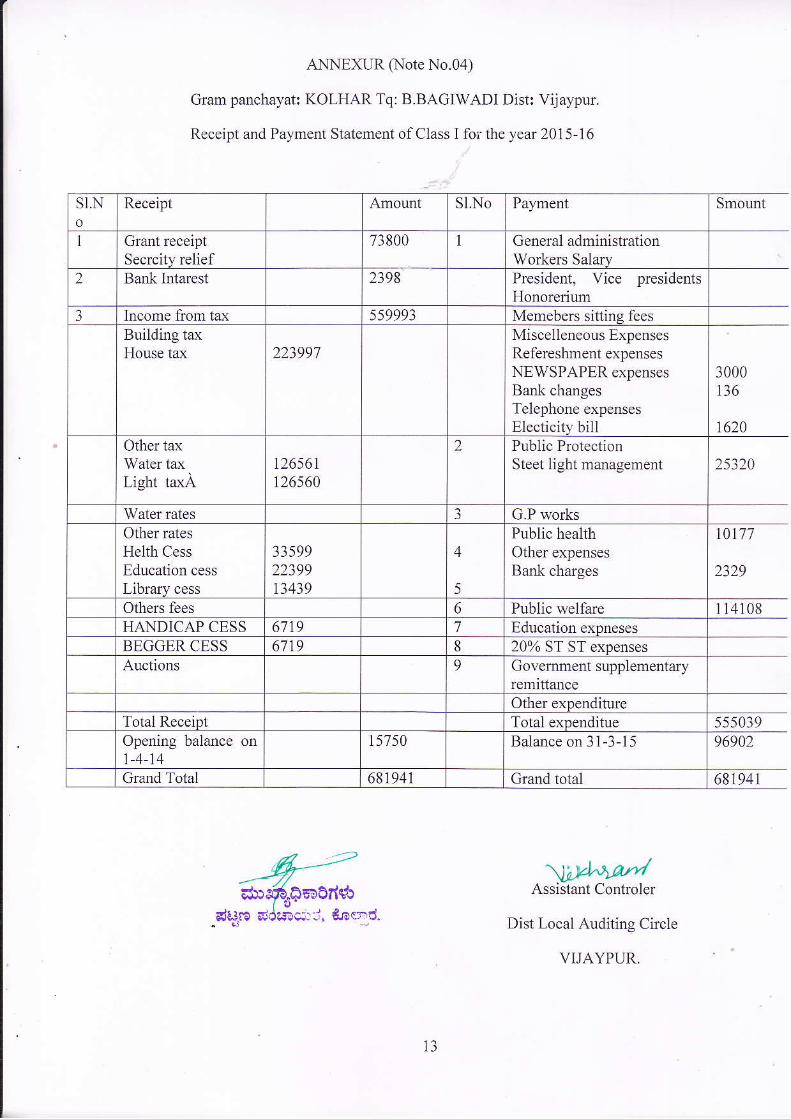

ANNEXUR (Note No.04)

Gram panchayat: KOLHAR Tq: B.BAGIWADT Dist: Vijaypur.

Receipt and Paymeflt Statement ofclass I for the year 2015-16

st.No

Receipt Amount SI,NO Payment Smount

Grant receiptSecrcity relief

73800 1 General adminishationWorkers Salarv

2 Bank Intarest 2398 President, Vice presidentsHonorerium

3 Tncome fronr tax 5s9993 Memebers sittins feesBuilding ta.x

House tax 22399'7Miscelleneous ExpensesRefereshment expensesNEWSPAPER expensesBark changesTelephone expensesElecticitv bill

3000136

t620Other taxWater ta\Light taxA

t2656tt26560

2 Public ProtectionSteet light management 25320

Water rates G.P worksOther ratesHelth Cess

Educatio11 cess

Library cess

33599223991:1,1:19

4

5

Public healthOther expensesBank charges

t0177

2329

a)thers fees 6 Public welfare I 14108HANDICAP CESS 6719 7 Education exDnesesBEGGER CESS 6719 8 20% ST ST expensesAuctions 9 Govemment supplementary

remitlanceOther e\penditure

Total Receipt Total expenditue 555039Opening balance on1-4-14

157 50 Balance on 3l -3-15 96902

Grand Total 681941 Crrand toial 681941

13

\9HwLw'.Assistant Controler

Dist Local Auditing Circle"driro s

VIJAYPUR.

ANNEXUR (NOTE NO )Format No 53

Gram panchayat: KOLHAR Tq B.BagewadiGram Swaraj Schemes Receipt and payment statement

For the oeriod 1-4-2015 to 3l -3-201 6

Administrative expenses

b) r.R.E.D/r.E.Cprograme

c) Printing/stationaryexpensE.M.D/F,S.D,

d) rvorks expenses

Solar battaries

aDnlication fomlManagerG.S.Y.Bengaluru

Deposiled to the Government

b) Bank interestreceived

b)Income tax

Ta-\ receiptsa)Sales 1ax

d) F.s.DE.M.D

b)lncorne tax Closins halance

c)Royalty

d)F.s.D

Totalexpnedityre

Iotal receipr

a5j'€6."eEoOnCr Assista nt Controler

Dist Local Auditing Circie

VIJAYPUR

dtiro dc?;c$d, & !d

11

Related Documents