Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Steel Insights, February 2014 3

Dear readers,

The year 2014 has brought with it some “good news” and also some “not so good news” for the steel industry. Let’s take a peek at the good news first! Subdued domestic demand and favourable currency exchange rate have made India a net exporter of steel during the first nine months of the current fiscal, after a gap of six years. India exported 4.14 million tons (mt) of steel during April-December, a 9.5 percent year-on-year growth. Experts say the trend will continue this fiscal unless there is quick recovery in domestic demand. Experts, however, also noted that it does not indicate any structural change yet as most steelmakers wanted to ship excess stocks.

Looking at this trend, an industry stalwart said it is important for a country to direct its steel in nation building in the development stage and hence it should focus more on the domestic market. While steel players like JSW Steel, Essar Steel and Steel Authority of India took an advantage of sharp rupee depreciation over August-September period and aggressively increased their exports, Tata Steel chose to focus on the domestic market. Now it needs to be seen how the industry plans its moves in a stable currency situation.

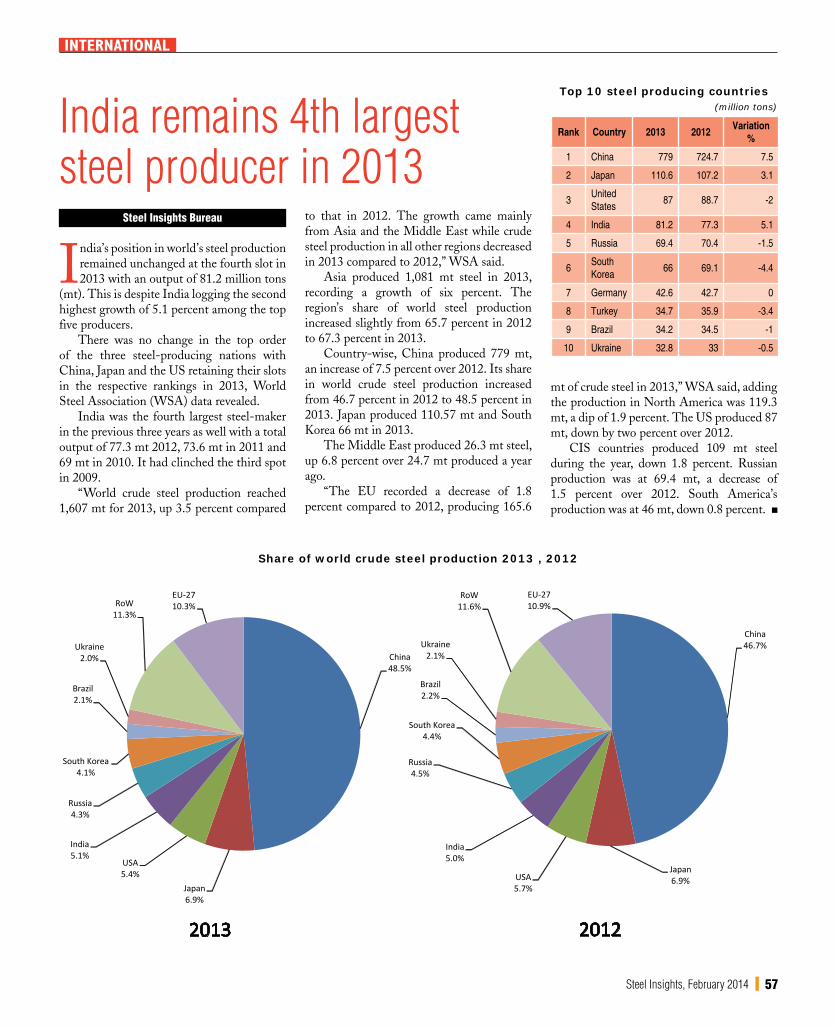

Next “the not so good news”! Steel consumption in India picked up by meagre 1.8 percent (April-December) year-on-year to 53.7 mt as major steel consuming sectors – from automobiles and capital goods through to infrastructure – are facing tough times, reflecting a slowdown in the economy. Also, India’s position in world steel production remained unchanged at the fourth slot in 2013 with an output of 81.2 mt. This is despite India logging the second highest growth of 5.1 percent among the top five producers. There was no change in the order of the top three steel producing nations with China, Japan and the US retaining their slots (in that order) in 2013. India was the fourth largest steel maker in the previous three years as well with a total output of 77.3 mt (2012), 73.6 mt in (2011) and 69 mt in (2010), respectively. It had clinched the third spot in 2009.

Meanwhile, the steel ministry is preparing a blueprint to expand India’s steel capacity to 300 mt from 96 mt at present. But capacity enhancement will only make sense if demand improves. The government also constituted a task force to prepare a blueprint for promoting research and development in the steel sector in a bid to help India treble its steel production capacity.

In the current edition of Steel Insights, we have tried to analyse market voices after government imposed 5 percent export duty on pellets. As India braces to treble capacity, beneficiation of low grade ore and pelletisation become the need of the hour. A balanced approach towards the sector is required; otherwise investments will dry up in the long run. The edition also tried to capture market voices from the forging and foundry sectors.

Happy reading!

(Rakesh Dubey)

EDITORIAL

Copyright: All rights reserved. No part of Steel Insights can be reproduced or copied in any form or by any means without the prior permission of mjunction services limited. Please inform us if any copyright has been inadvertently infringed.

Disclaimer: This document is for information purpose only. Certain information herein has been acquired from various external sources believed to be reliable. While we have taken reasonable care to compile this report, we in no way assume any responsibility for any error or discrepancy in regards to information contained herein. Readers are requested to make appropriate judgment without any prejudice or compulsion.

Registered Officemjunction services limited, Tata Centre, 43 J L Nehru Rd, Kolkata 700 071

Website: www.mjunction.in

Corporate Head Quarters: Godrej Waterside, 3rd Floor, Tower 1, Plot V, Block DP, Sector V, Salt Lake, Kolkata 700091, Tel: +91 33 6610 6100, Fax: +91 33 6610 6187 Bhilai: Room 321, 3rd Floor, Ispat Bhavan, Bhilai Steel Plant, Bhilai 490001, Tel: +91 788 6451066, Tele/Fax: +91 788 2221071 Bokaro: Room 19, Old Admin Bldg., Bokaro Steel Plant, Bokaro 827001, Tel/Fax: +91 654 2226132 Burnpur: SAIL - IISCO Steel Plant, Materials Building, Order Department, Ground Floor, Burnpur 713325, Telfax: +91 341 2240107 Chennai: Basement, Begum Ispahani Complex, New No 91, Old No 44, Armenian Street, Chennai 600 001, Tel: +91 44 64624733-35, Fax: +91 44 25216536 Durgapur: Room 618, Ispat Bhavan, Durgapur Steel Plant, Durgapur 713203, Tel: +91 343 6510185, Tele/Fax: +91 343 2586946 Jamshedpur: Kashi Kunj, Ground Floor, Road No. 02, Contractors Area, Bistupur, Jamshedpur 831001, Tel: +91 657 6519985/86/90/91, Fax: +91 657 2230040 Mumbai: Jolly Bhavan II, 403, 4th Floor, 7 New Marine Lines, Mumbai 400020, Tel: +91 22 66510663, Tele/Fax: +91 22 66510662 New Delhi: C127, 2nd Floor, A One Plaza, Naraina Industrial Area, Phase I, New Delhi 110028, Tel: +91 11 65661774/65413288, Tele/Fax: +91 11 25897000 Noamundi: C/o TATA Steel Limited, Mines Purchase Cell, PO: Noamundi, Singbhum (West), Jharkhand 833 217, Tel: +91 9204791638/9234368606 Rourkela: Administrative Bldg., Room 624, 6th Flr, Rourkela Steel Plant, Rourkela 769011, Tel: +91 661 6514142/6511412

Chief EditorRakesh Dubey, Tel: +91 91633 48159, E-mail: [email protected]

Executive EditorTamajit Pain, Tel: +91 91633 48065, E-mail: [email protected]

Editorial BoardDr Abhirup Sirkar, Professor Economics, Indian Statistical Institute (ISI)Dr Amit Chatterjee, Consultant and former Advisor to MD, Tata Steel LtdJayant Acharya, Director (Commercial & Marketing), JSW Steel LtdK Ranganath, former CMD, KIOCLVikram Amin, ED (Strategy and Business Development), Essar Steel LtdRana Som, Former CMD, NMDC Ltd

AdvertisingSoumitra Bose, Tel: +91 92310 00232, Email: [email protected] Jalan, Tel: +91 91633 48243, Email: [email protected]

SubscriptionRachita Das, Tel: +91 91633 48045, Email: [email protected] Free No.: 1800 4192 000 1. Press 8 for publicationEmail: [email protected]

DesignDebal Ray, Sobhan Jas

For suggestions, feedback and queries, please write to [email protected]

mjunction believes that all junctionites, customers, suppliers, partners, etc should practice the highest ethical standards in their daily operations.

Report a concern to [email protected]

4 Steel Insights, February 2014

COnTEnTs

50 | INTERVIEW ‘Foundry needs a parent in the government’IIF working for bringing industry under ambit of Ministry of Small & Medium Enterprises (MSME).

46 | INTERVIEW Vikrant forges a secure future Vikrant Forge bullish on Indian market and feel it will grow at a faster clip in next two years.

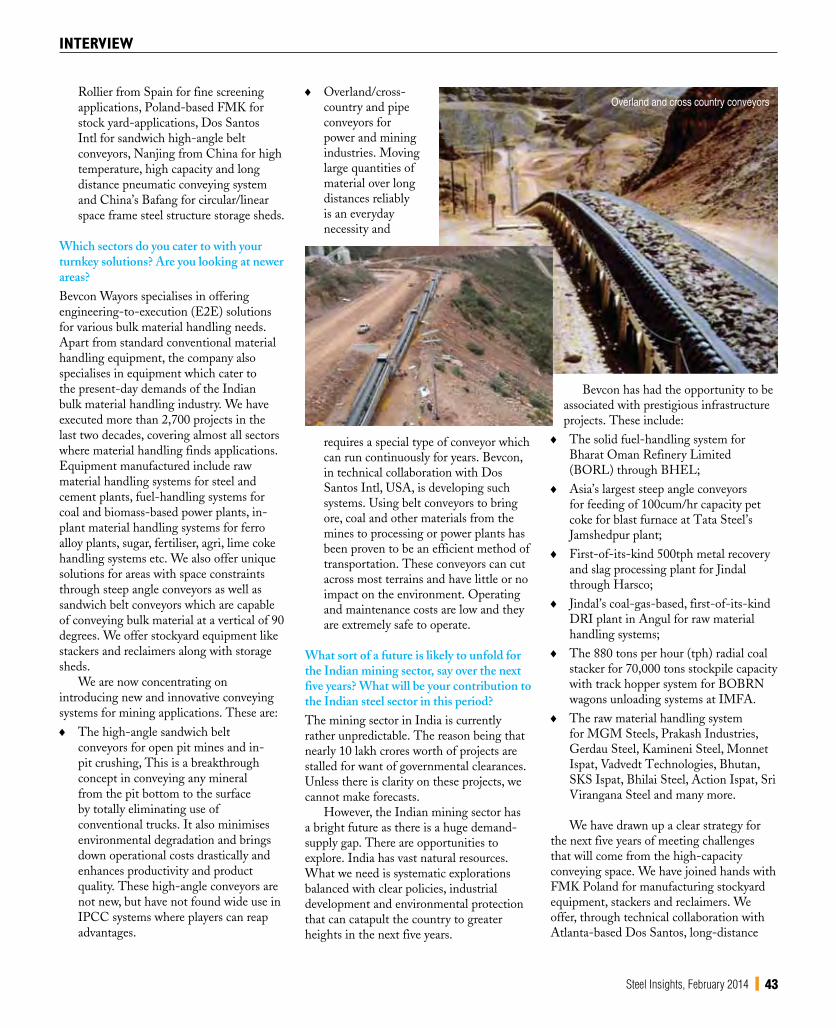

41 | INTERVIEW ‘Our focus is innovative conveying systems for mining applications’Bevcon has drawn a clear strategy for next 5 years for high capacity conveying space.

30 | COVER STORY Indian pellet-makers’ palette of woes Government’s imposition of 5% export duty on pellet has divided the steel industry.

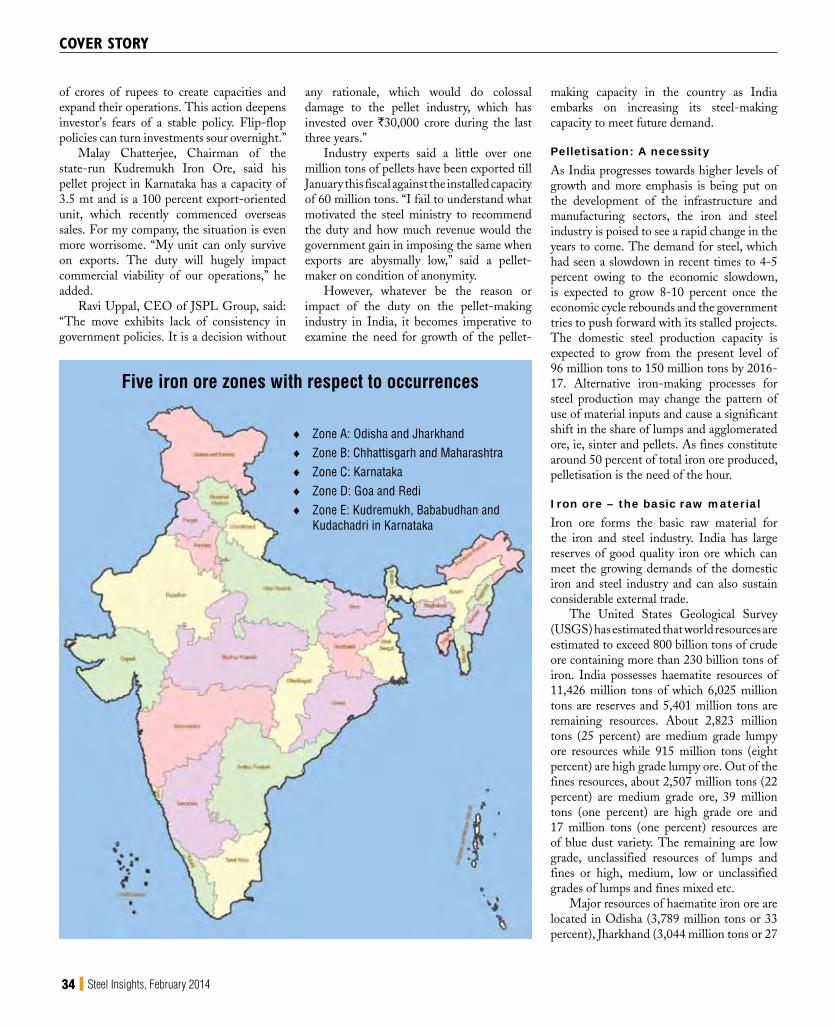

10 | SpECIAl FEATuREIron ore scarcity still hunts Analysts feel production to decline marginally in FY14 but rose 10-12% in FY15.

6 Iron ore exports to go up as Goa prepares for e-auction

14 Sponge iron expects demand sheen to return

16 Will green signal start Posco’s project 18 Two-wheelersegmentfindsthegoing

slightly easy 20 Construction industry outlook negative

for 2014 22 Negative sentiment, sticky prices put

pressure on realty sector 24 Coking coal continues ‘slide’ show in

January 26 Flat steel producers play on low import,

input costs 28 Longsteel,semi-finisheddemand

remain volatile 29 Tata Steel launches 2 branded ferro

alloys 39 RSP doubles production capacity with

slab caster from SMS Siemag 40 Siemens continuous caster starts

operation at JSPL 52 JSW Steel Q3 net drops 47.3% 53 RINL sales increase 12% in January

y-o-y 53 Outokumpu bags 700-tons order in India 53 JSPL Angul plant construction on track 54 Traffichandlingbymajorportsup1.91%

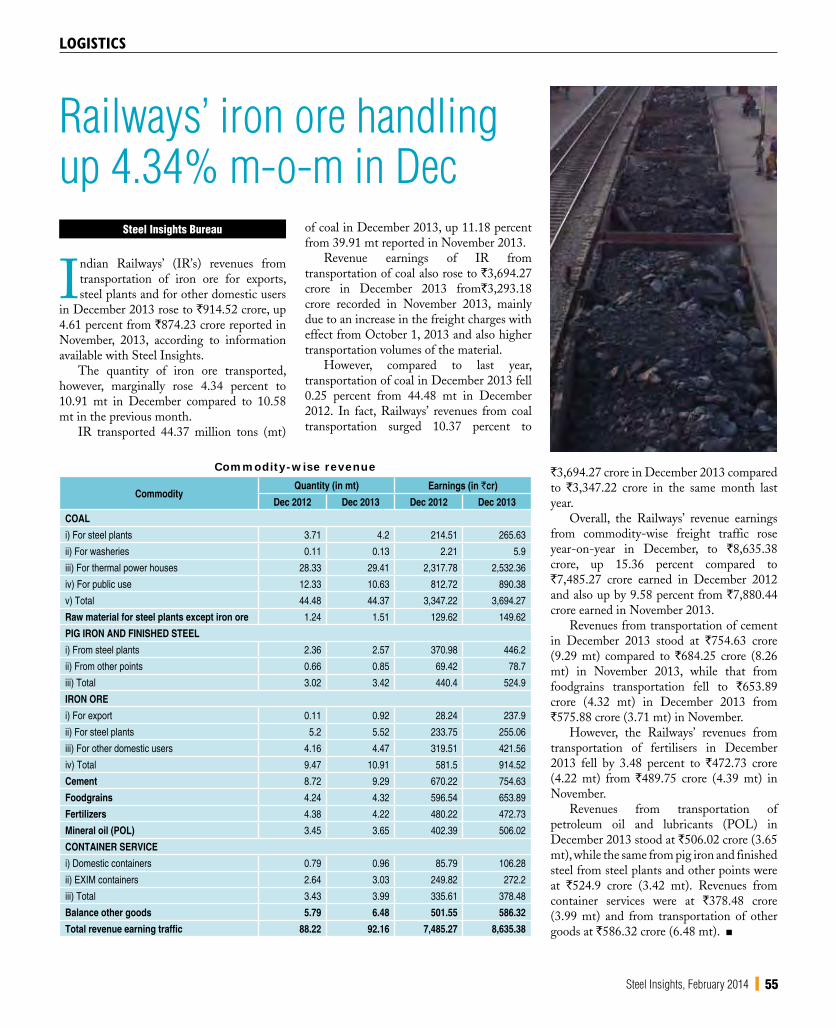

in April-December 55 Railways’ iron ore handling up 4.34%

m-o-m in Dec 56 Global crude steel output up 1.43% in

December m-o-m 57 India remains 4th largest steel producer

in 2013 58 Price data

6 Steel Insights, February 2014

sPECIAL fEATuRE

Iron ore exports to go up as Goa prepares for e-auction

Steel Insights Bureau

India’s iron ore exports are set to increase as Goa prepares to auction unsold stocks, following the easing of a ban on sales of

the steel-making raw material.“Bids will be invited for about 15 million

tons of inventory that will be offered through online sales starting next month,” Goa’s Mines Director Prasanna Acharya said. “The buyers will be allowed to ship the ore overseas or sell locally,” he said.

The Supreme Court, in November, had allowed sales of mined ore in Goa, while continuing the ban on extraction because of environmental concerns. Goa was the nation’s biggest iron ore exporter before the ban was imposed in September 2012.

Goa’s mines department has sought applications from prospective bidders and it is expected to have the first auction in February, Acharya said. There is no timeline for completing the sale of the entire quantity.

The revival in Goa’s exports comes as iron ore shipments from India are poised to tumble for a fourth year to less than 10 million tons in the year ending March from 18 million tons a year earlier.

Government curbs, mining bans and higher export taxes are prompting buyers to secure the raw material from other producers.

Sesa Sterlite Ltd, which owns its biggest iron ore mine in Goa, and rival miners mainly export their low-grade produce to China as steel-makers in India mostly lack the ability to process poor quality ore.

Steel firms register

Over a dozen steel firms, including Jindal Steel & Power (JSPL), Bhushan Steel and JSW Steel, have registered themselves with the Indian Bureau of Mines as the Goa government is all set to start the process of e-auctioning of around 15 million ton of iron ore lying idle in its stockyards.

Goa’s ore under auction could support 7million tons of steel capacity annually.

The Supreme Court appointed a three-member monitoring committee to oversee the e-auctioning process and said that the proceeds from the sale will be kept in a separate fixed deposit account by the Goa government till the apex court finally decides on the matter.

However, the base price will be decided on the basis of iron ore grades.

The auction will take place along similar lines of Karnataka. Goa’s ore has more than 55+Fe content, industry sources said.

The domestic steel mills have traditionally preferred ores with higher iron content but are now also developing technology to use the low-grade ore.

8 Steel Insights, February 2014

sPECIAL fEATuRE

Indian steel-makers are raising their iron ore beneficiation and pelletisation capacities as they seek to expand the range of ore that their plants can handle.

India has about 36 iron ore pelletisation plants operated by steel companies as well as standalone raw material companies such as KIOCL (formerly Kudremukh Iron Ore Company) with a combined capacity of around 62 million tons.

Goa used to be India’s top exporting state, with sales of more than 40 million tons a year, mostly to China. But it has not produced or exported any ore since the Supreme Court imposed a ban to curb illegal mining. Recently, the government imposed a five percent tax on the export of iron ore pellets that may put brakes on the expansion plans of the country’s pelletisation industry, worth around `50,000 crore.

India’s exports languish

Meanwhile, India’s iron ore exports have gone down by 28.16 percent during April-December of the current fiscal to 11.17 million tons as gloom continues to hang over the sector due to the present regulatory scenario, according to the mineral industries body, the Federation of Indian Mineral Industries (FIMI).

India, once the third-largest exporter of iron ore, had exported 15.55 million tons of the mineral in the corresponding period of last fiscal, according to FIMI data.

“We expect the situation to continue as long as the government policy does not change. There is total gloom in the sector… no ray of hope,” FIMI Secretary General R K Sharma said.

He added that this year’s iron ore exports are expected to come down by 20 percent to about 14-15 million tons from the levels of 18.37 million tons in 2012-13.

Paradip (4 million tons), Vizag (3.84 million tons) and Haldia (1.58 million tons) are the major ports from where exports of the minerals were taking place, FIMI data showed.

Indian iron ore exports have been badly hurt badly in the last few years due to mining bans in Goa and Karnataka, which led to a drastic fall in domestic production as well.

Increase in the export duty to 30 percent on both types of iron ore, lumps and fines, in December 2012, had also impacted the sector.

At present, low grade iron ore (or fines) are being exported from Odisha, Jharkhand, Rajasthan and Madhya Pradesh as mining is still banned in Goa. Export of the mineral is not permitted from Karnataka at present.

A few days back, the Goa government had issued a notification to sell about 15 million tons of iron ore through exports, as per a Supreme Court order. Industry is estimating that India’s total iron ore production in the present fiscal will be around 130-140 million tons, almost the same as last year.

Rusty global outlook

Iron ore may have outperformed other commodities last year, but the price of the metal used in making steel looks set to decline this year as China’s growth slows.

China’s continued heavy spending on subways, bridges and other infrastructure kept demand for iron ore high last year. Exports to China from Port Hedland, Australia’s main shipment point for the metal, increased by 34 percent to 256 million tons. Overall, shipments of iron ore – including to Japan and South Korea – rose 26 percent to 318 million tons. Exports of the commodity reached record levels in December.

Many analysts and traders have been surprised by the way iron-ore prices, buoyed by record Chinese demand, held up throughout 2013. Prices of other industrial commodities, such as nickel and coal, have tumbled, but iron ore has largely remained above $130 a ton.

Although prices are still about a third lower than their all-time peak three years ago, they remain well above the sub-$90-a-ton level they sank to in 2012 as China’s economy stuttered.

But a less bright outlook for China’s economy this year, coupled with new iron-ore mines going online in Australia, is threatening to drag down prices this year. A decline would dampen the outlook for companies at a time when exports from India may see some uptick with the auctioning of stockpiles in Goa.

Sesa Sterlite to resume sales

Steel Insights Bureau

Sesa Sterlite Ltd, which restarted its iron ore mines in southern India last month, will shortly resume sales of the steel-making ingredient from the region after a halt of more than two years.

The company plans to start auctioning iron ore mined in the state of Karnataka shortly, officials said.

The company, which was the biggest Indian exporter of the commodity until the court-ordered ban, may sell about 100,000 tons of ore in its first offering, industry sources said.

Sesa Sterlite, controlled by billionaire Anil Agarwal, saw revenues from its iron ore business collapse after the nation’s courts ordered mining bans in Goa in October 2012 and Karnataka in August 2011, as part of probes into illegal mining and environmental degradation.

Iron ore mining accounted for 98 percent of earnings at Sesa Goa Ltd, which, in August, merged with sister company and zinc, copper and aluminium producer Sterlite Industries (India) Ltd to form Sesa Sterlite.

Mining in Goa is still suspended although companies have been allowed to sell inventory. The resumption in Karnataka will help ease shortages faced by local steel-makers.

The company, owned by London-listed Vedanta Resources plc, has approval to produce as much as 2.29 million tons (mt) of iron ore a year, industry sources said, adding that output in the first three months of 2014 may reach 1.2 mt-1.5 mt from the restarted Karnataka mines.

10 Steel Insights, February 2014

bidder has to bid over and above the base price and is liable to pay 10 percent royalty and 12 percent forest development tax, unlike other places where it is borne by mining companies,” KISMA said.

The Bangalore Chamber of Industry & Commerce (BCIC) has also joined the protest along with the Association of Indian Mini Blast Furnaces. In a letter to Karnataka Chief Secretary H V Harish, President, BCIC, said: “This arbitrary way of putting abnormally high base prices is resulting in huge profiteering for the lessees.”

Miners hit back The ongoing blame game between Karnataka’s iron ore producers and their clients reached a new pitch with the mine-owners launching a counter tirade against the steel companies.

Mining industry body Federation of Indian Mineral Industries (FIMI) denied that a mining cartel was selling ore at high prices in the state or causing short supply of ore. On the contrary, it alleged that three to four steel majors had formed a cartel and had artificially kept iron ore prices low in the Karnataka auctions.

FIMI Vice-President Basant Poddar and Managing Director of Sesa Sterlite (formerly Sesa Goa) Prasun K Mukherjee rubbished steel companies’ allegations against mining firms and said the prices were market driven.

“The quantities fixed by the Supreme Court for each mine lease (are too) insignificant for any one mining company to dictate prices or think of cartelisation. Moreover, the mine owners have been fixing the reserve price after clearance from the Supreme Court and all approvals from government.

“It is astonishing to see this weird allegation when 70 percent of the iron ore in the e-auction is being supplied by the National Minerals Development Corporation, a Government of India company (whose) reserve price is abysmally low compared to private mine owners.”

“The steel industry is selectively targeting Karnataka mine owners,” Poddar and Mukherjee said. In the last two years, some steel plants had bought two million tons of ore from the eastern states at high prices; whereas a similar quantity of ore lumps and fines of private mines and NMDC remained unsold in the Karnataka auctions.

Iron ore scarcity still hunts India

Tamajit Pain

India’s Minister of Steel, Beni Prasad Verma, recently said production of iron ore in the country has been above the

domestic requirements during the last three years.

In a written reply in the Rajya Sabha, Verma said the decision regarding imports of iron ore is taken by the individual steel producers based on their requirements.

The fact that iron ore is still scarce is evident from the ongoing spat between large steel players and miners.

Large steel players like JSW Steel, Mukand Steel, Kalyani Steels, Kirloskar Ferrous and BMM Ispat are up in arms against alleged price fixation of iron ore in Karnataka. The companies have come together and are preparing to file an affidavit in the Supreme Court against private miners for allegedly forming a cartel and jacking up ore prices.

With general elections round the corner, steel companies under the Karnataka Iron & Steel Manufacturers’ Association (KISMA) have joined forces with the Karnataka Sponge Iron Manufacturers’ Association (KSIMA) to keep the pressure on the state and central government, given the politically sensitive nature of the mining industry. Together, they are also planning to protest in a big way through public demonstrations and advertising campaigns.

“It is a helpless situation for the steel industry. The ore pricing in Karnataka is simply unviable. The January price of `5,000 per ton is historically the highest-ever, up from

`2,250 to `2,475 in September 2013. Even in 2008, when prices went up to $180 per ton, ore prices did not reach this level. Except for state-owned NMDC, other miners have formed a cartel and are increasing the base prices of ore in the e-auctions,” said Seshagiri Rao, Joint Managing Director (MD) and Chief Financial Officer (CFO) of JSW Steel, which is the largest steel plant in the state.

While state-owned NMDC, the country’s largest miner, decides on the base price for the ore it produces, the Supreme Court has allowed the base price, quantity, quality etc to be decided by the lessees.

S Shah, Joint MD of Mukund Steel, which is operating at barely 60-70 percent of its current capacity, said it is extremely unfortunate that the steel industry has had to go through such a crisis after investing nearly `80,000 crore in the state.

Steel companies are planning to file an application with the Competition Commission of India (CCI) against alleged cartelisation by private mine owners. They will also demand setting up of an immediate regulator to keep a close eye on and monitor sharp movement in the e-auction prices of iron ore.

Due to the ore crisis, a number of sponge iron units too have closed down in Karnataka, while the rest are operating at only 15-20 percent capacity.

K Satya Prasad, Secretary, KSIMA, said: “Some of the lessees have formed a cartel with the base prices nearly 70-80 percent over NMDC prices, even as ore prices are stagnant in Odisha and have fallen by 13 percent internationally.” To add to it, “the

Production, export, consumption of iron ore in million tons

Year Iron ore production

Domestic Consumption/ Requirement (e)

Iron Ore Import *

Iron Ore Export *

Share of Export with production

2010-11 207.16 107.22 1.87 97.66 47.1%

2011-12 168.58 100.57 0.97 61.74 36.6%

2012-13* 136.02 103.40 3.05 18.37 13.5%Source: Production/Consumption - Indian Bureau of Mines, Ministry of Mines; Import/Export - MMTC, Ministry of Commerce; * Provisional; e Estimated

sPECIAL fEATuRE

12 Steel Insights, February 2014

sPECIAL fEATuRE

They alleged that currently only 21 of the 115 mines in the non-C category were operational in the state. Of the 12 million tons produced since April 1, 2013, the cartel of three to four private steel majors bought almost 75 percent of Karnataka’s ores through the e-auctions and artificially depressed the prices of ore sold by NMDC.

“Any cartelisation is on the buying side,” Mukherjee said, adding the artificially low price in the absence of a large number of buyers subverted the very objective of e-auctions. The government was also losing some of the revenue due to it as royalty and taxes. Iron ore productionAs per the report of the Working Group on the Steel Industry for the 12th Five-Year Plan, the iron ore requirement for the year 2013-14 is 149.43 million tons. However, requirement had been much below expectations till the last fiscal.

Analysts feel that India’s iron ore production will witness a minor decline in the fiscal ending March 2014. But it is set to witness a moderate growth of 10-12 percent to touch a level of 150 million tons in 2014-15. The growth in production during the next year is likely to come from Karnataka and Goa, while production cap in Odisha will restrict further growth.

According to miners and analysts tracking the sector, the majority of growth will be seen in Karnataka, where several mines are in the final stages of securing regulatory approvals.

The biggest among all, Sesa Sterlite, started production towards the end of December 2013. Other mines like NMDC are gearing up to increase production and companies like Mineral Enterprises Limited are awaiting renewal of their mining leases.

“Unless Goa restarts mining, though

partially, we cannot expect a big jump in iron ore production next fiscal. Many more mines are set to restart in Karnataka and the total production is unlikely to exceed 20 million tons. There is a big suspense over production caps in Odisha based on the Shah Commission recommendations. In total, we can expect around 150 million tons of production next fiscal,” Basant Poddar, Vice-President, FIMI, said.

Production of iron ore in 2013-14 is likely to remain flat at around 135 million tons, same as the previous year, or it might even decline by 3-5 percent, said analysts.

The output will be flat on a year-on-year basis in 2013-14 as Goa was out of business. Jharkhand and Chhattisgarh have more or less remained flat in the current year till now. In Karnataka too, production is yet to pick up as many leases are still awaiting clearances, sources said.

ASSOCHAM calls for review of e-auction systemMeanwhile, apex industry body ASSOCHAM has urged the government to review e-auctioning of iron ore and provide long-term iron ore linkages to protect the interest of the domestic iron and steel industry.

‘’The e-auction of iron ore has to provide relief to India’s iron and steel industry. Otherwise, there will be an adversely effect, more so as lack of raw material would be a major cause for tardy progress of both greenfield and brown-field steel capacity expansion projects,’’ highlighted The Associated Chambers of Commerce and Industry of India (ASSOCHAM) in a communication addressed to R H Khwaja, Secretary, Ministry of Mines.

‘’There is a need to adopt a holistic development approach for ensuring smooth

supply of iron ore, thereby harnessing the growth of the iron and steel industry,’’ said D S Rawat, Secretary General of ASSOCHAM.

Iron ore production in FY2013 was 136 million tons, out of which 42 million tons was captive production while 18.4 million tons had been exported and about 76 million tons of total iron

ore was available for the relevant market for non-captive steel producers.

Supply of an important raw material like iron ore is required for non-captive users as well and they cannot be ignored, noted ASSOCHAM.

It also noted that in case of e-auctioning, the quality of raw material cannot be assured and it will always remain fluctuating as each time it would come from multiple sources and create problems in the operations of blast furnaces and steel melting furnaces, thereby leading to high coal and energy consumption.

Besides, ASSOCHAM also shared its concerns over the inflow of new investments in the domestic steel sector as setting up of integrated steel plants involves huge finances.

‘’It is almost impossible to commit large financial resources without having security of iron ore supply which is a critical raw material for operating steel plants,’’ highlighted ASSOCHAM. ‘’Besides, in India, even banks do not provide financial closure to projects without secure sources of raw materials.’’

Will India resolve iron ore scarcity issue?Now the big question is whether India will be able to solve the iron ore scarcity problem as the country increases its steel production capacity to over 100 million tons in a year’s time.

All eyes are also on what action would be taken on the Shah Commission report on Odisha.

The Shah Commission, while arguing for preservation of minerals like iron ore, had mentioned that China, despite having 200 billion tons of iron ore reserves, was importing ore from India and other places to shore up its stocks. The commission feared that, if allowed to be exploited at the present rate, the iron ore reserves in Odisha would be exhausted in 30 years. Hence, it favoured capping the iron ore production to below 55 million tons and also putting restrictions on exports.

Odisha is the largest producer and supplier of iron ore in the country. In 2012-13, it accounted for nearly 45 percent of India’s total iron ore production.

Similarly, the proposal to restrict export of iron ore has been opposed by the Union commerce ministry on the plea that it would affect foreign exchange earnings adversely.

State-wise production of iron ore(in million tons)

2009-10 2010-11 2011-12 2012-13 2013-14*

Chhattisgarh 26.21 29.32 30.45 27.94 30

Goa 38.13 35.56 33.37 10.57 11

Jharkhand 22.54 22.28 18.94 17.97 19

Karnataka 43.16 38.98 13.18 11.22 15

Odisha 80.89 76.12 67.01 64.19 50

Others 7.62 4.89 4.33 3.96 4

Total 218.55 207.15 167.28 135.85 129* Industry projections Source: Federation of Indian Mineral Industries

IRC GroupIRC House | 1 Sunyat Sen Street | Kolkata 700012Tel: 033 2236 5110 (5 lines) | Fax: 033 2225 5936 | Email: [email protected] | Website: www.irclgroup.com

Warehousing

Material HandlingMaterial Handling

Plantation

Education

Manufacturing

Ash Management

Transportation

Construction

Mining

Ash Export

Record Management

Bauxite Mine Guinea

Mining Warehousing

A h E t

R d M Transportation

IRC Natural Resources Pvt Ltd

New Light Construction Pvt Ltd

IRC Limited

IRC Infra & Realty Pvt Ltd

IRC FISHCO Pvt Ltd

IRC Logistics Ltd

Indian Roadways Corporation Ltd

Transworld Minerals LLC, Oman

Greengold Plantations Pvt Ltd

Promining SARL, Guinea

Ed ti

Always Ahead

14 Steel Insights, February 2014

fEATuRE

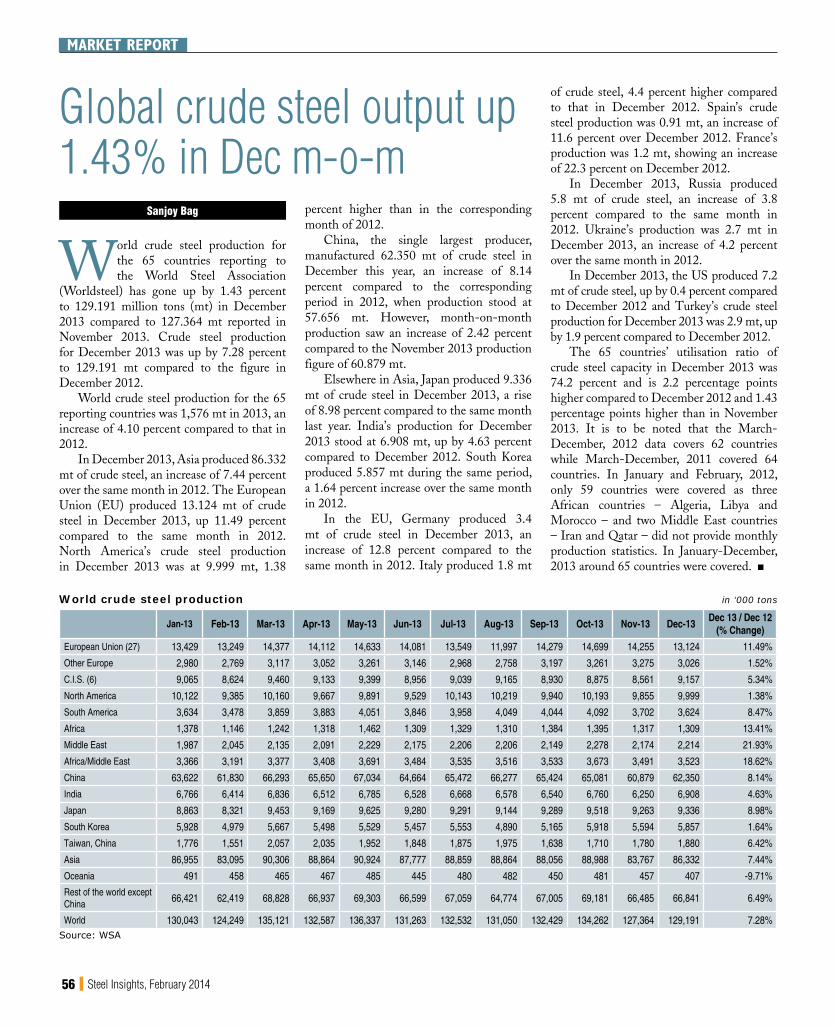

range-bound between $125 and $135 a ton, coal and other energy costs have gone up.

Steel mills have decided to pass on the rise to consumers with a proportionate increase in their product prices with immediate effect.

“With the lowering of capacity since June, sponge-iron inventory has dried completely. Any upsurge in demand will benefit makers with a proportionate increase in margins,” said a sponge iron maker based out of Chhattisgarh. Steel demand in the past month has risen seven percent.

Many mills in the north have shut down their plants due to lack of electricity. Now they have gradually started coming on stream with the restoration in power supply. So, sponge-iron demand will continue its rising momentum, said Sharma.

Meanwhile, the government has proactively intervened (through the Cabinet Committee on Investment) to clear major investment projects, which is key to reviving the investment cycle. With expected commencement of investments in industrial and infrastructure projects post-general elections, Indian steel demand is expected to improve in FY15.

Sponge iron expects demand sheen to return

Steel Insights Bureau

The sponge iron industry expects demand to revive after its first increase in January after a period of

seven months of drawdown. The sector, expected to be of the size

of `40,000-crore with many small players operating within its ambit, has seen signs of revival in January with producers having seen a spurt in demand from steel mills.

The past seven months have seen the worst phase on non-availability of iron ore due to the mining ban in Goa and lower mining production in Karnataka.

Used as a raw material for steel-making, the demand for sponge iron has reduced due

to fewer projects announced for construction. As a result, producers have reduced utilisation to 30-35 percent in seven months. With 18.7 million tons of production, the sector recorded 50 percent utilisation during FY’13 compared to 20.6 million and 58 percent of utilisation a year ago.

“Demand has revived suddenly, in a month. Therefore, makers have raised prices by 3-5 percent this month,” said V R Sharma, President of the Sponge Iron Manufacturers Association and Deputy Managing Director of Jindal Steel and Power (JSPL).

Sponge iron is quoted in the range of `19,000-20,500 a ton. The price of pig iron, also used for steel-making, moved up to `25,500 a ton. While ore prices have been

Sponge iron sector figures(in million tons)

particulars 2011-12 2012-13 % change

Output 20.56 18.67 -9.18

Installed capacity

35.31 37.31 5.66

Capacity utilization (%)

58.22 50.05 0

Sponge iron prices on Jan 31, 2014

place 31-Jan m-o-m

Durgapur 20500 -200

Raigarh 20000 300

Raipur 21000 700

Rourkela 19200 800

Basic price (ED and Taxes extra)

16 Steel Insights, February 2014

fEATuRE

environmental clearance, the environment ministry has delinked the port from the steel plant. The company had received an environment clearance for the captive port in May, 2007. But the five-year validity of the permission has expired. Though the Odisha government has submitted the coastal regulation zone (CRZ) compliance report according to the revised guidelines, the renewal of environment clearance of the port project is yet to pass the environment ministry’s scrutiny.

Some industry experts feel the captive port is crucial for the start of work on the POSCO plant as the company will bring heavy equipment through this port. Besides, the sand dredged from Jatadhari Muhan (the location of the port) will be used to raise the ground level of the plant site, which is very shallow. In other words, building of the port will precede the steel plant. So, with no environment clearance for the port as of now it is difficult to start work on the steel plant.

The company is also in a quandary over the direction of the environment ministry to spend five percent of the project cost on social commitments in the site area. This is expected to push up the project cost by about `2,600 crore.

The Odisha government last year had asked POSCO to spend about `250 crore to upgrade the socio-economic infrastructure in the site area. However, the company had evaded the task on the plea that it will be difficult to get the board’s approval for such a large amount when it was not assured of land and mines to take the project forward.

Some industry sources feel it would be difficult for the company to spend ten times of that amount without any substantial change in the status of the project. All eyes are now on the clarity on the issue and framing of necessary policy guidelines by the government.

The Odisha government’s MoU with POSCO expired in June 2010, but it has not been renewed yet. With the law department opining against renewal post-facto, the state government had decided to enter into a tripartite agreement with POSCO India and its Seoul-based parent, which will replace the earlier MoU. Though the negotiation for this pact ended more than two years ago, the document is yet to be inked.

Thus, for POSCO, the long journey to producing steel in Odisha isn’t over yet.

Will Green signal start POSCO’s project?

Steel Insights Bureau

Prime Minister Manmohan Singh recently said work on the long-delayed integrated steel plant of POSCO in

Odisha will begin in a few weeks. Singh also assured South Korean President Park Gyun-hye in New Delhi on similar lines. His statement might have brought some cheer to the visiting Korean delegation and contributed to the success of the bilateral trade talks, but those on the ground know there are still large hurdles ahead.

The Prime Minister’s optimism was based on the recent revalidation of the environment clearance of the project by the Union Ministry of Environment and Forests (MoEF) and the fresh recommendation by the state government to the Centre for granting prospecting licence to POSCO for the Khandadhar iron ore mines. Industry sources say getting land or the environment clearance is not a big issue but the company should be more bothered about the raw material for the project.

Ever since it signed a memorandum of understanding with Odisha in 2005, the South Korea-headquartered steel-maker has stuck to its position of “no mine, no project”.

Though the Odisha government has submitted a fresh request to the Centre for the Khandadhar mines, getting the mining rights is still fraught with a lot of problems. While disposing of a case related to the prospecting licence for the Khandadhar mines in May last year, the Supreme Court had asked the Union mines ministry to take up POSCO’s case but with the rider that the ministry would have to consider “all objections raised by various parties”. It may be noted there were 226 claimants of these mines before the matter went to court. So, the process of eliminating objections and allotting the prospecting licence to POSCO may take a long time, point out analysts. There is also the possibility of some dissatisfied claimants going to court and stalling the process again.

Layers of clearanceEven if POSCO gets the prospecting licence, the next stage of getting a mining lease will be more arduous as then forest and environment issues will come into play. Khandadhar being a scheduled area and with a precedent like Niyamgiri, the forest diversion and environment issues are likely to be decided through gram sabhas (village committees).

Already, local protests are building up in Khandadhar to POSCO’s proposed mining plan. These will only get shriller once the gram sabhas take up the matter, hurting POSCO’s chances to start mining iron ore.

Typically in India, from the grant of a prospecting licence to the start of mining, it takes eight to nine years. So POSCO has to look for raw material linkage from alternative sources before it can operate its own mines if it builds the plant in the next three to four years, industry analysts say.

The company has held preliminary discussions on sourcing raw material from state-owned Odisha Mining Corporation in the event of a delay in operating its captive mine. But POSCO may be sceptical about depending solely on the state-owned miner.

To add to POSCO’s woes, there have been persistent strikes by local villagers at the plant site. Earlier, it was the protracted agitation by the POSCO Pratirodh Sangram Samiti that delayed land acquisition for the project. Now, the villagers of Gadakujang and Nuagaon panchayats, hitherto known to be supporters of the project, have demanded fresh compensation and raised livelihood issues.

Thousands of villagers, including those to be displaced in Polang, Noliasahi and Bhuyianpal villages, were on mass dharna recently, threatening to bring down the boundary wall that is being constructed around the acquired land.

Hurdles more complicated After captive mines, the next roadblock is the captive port. While revalidating the

18 Steel Insights, February 2014

fEATuRE

volumes in the LCV segment contracted by 24.5 percent during the same period. “In terms of market share, Tata Motors has gained some its lost market in the M&HCV (goods) segment in the first nine months of 2013-14, while its market position has weakened in the LCVs (goods) segment as slowdown has caught up with the sub-2 tons category where it commands a strong market share. In contrast, the 2-3.5 tons segment has witnessed strong growth where M&M has relatively strong market position with its wide portfolio of pick-up trucks,” the ICRA report added.

Raw material prices a concern

Raw martial prices, meanwhile, continued to be a matter of concern for the industry as most of the companies procure raw material through import. In most cases, the automobile companies tried to balance the costs by passing the hike to customers. Despite this, it continued to impact the financials of the companies.

For example, higher raw material prices impacted the earnings before interest, taxes, depreciation and amortisation (EBIDTA) of Hero MotoCorp Limited during the third quarter of 2013-14 at 13.06 percent.

Pawan Munjal, Managing Director and Chief Executive Officer of Hero MotoCorp Limited, said in a statement, “Despite better sales and increasing net profits during the quarter, our EBIDTA has been affected due to partial recovery of rising raw material costs and currency fluctuation.”

It is the same story at MSIL and General Motors India who procure a large portion of their raw materials through imports. For GM, the amount is almost 70 percent.

In this scenario, the companies do not rule out the possibility of procuring steel from the domestic market. “We can procure steel from the domestic market if the pricing is right and the quality of steel is up to the mark,” an official from MSIL told Steel Insights.

General Motor believes in a wait-and-watch policy, as P Balendran, Vice-President, General Motor India told Steel Insights, the company may increases its local steel sourcing from a present 30 percent share depending on economic conditions.

Two-wheeler segment finds the going slightly easy

Priyalina Basu

Early trends in the January 2014 sales for the automobile sector show that the journey for car manufacturers

continued to be bumpy, though the two-wheeler segment had an easy ride. Complete segment-wise sales report for the month of January 2014, however, is yet to be published by the Society of Indian Automobile Manufacturers (SIAM).

During January 2014, most of the leading car manufacturers such as Maruti-Suzuki India Limited (MSIL), Hyundai Motor India Limited (HMIL), Mahindra and Mahindra Limited posted a dip in sales due to subdued market conditions in India and abroad though Honda Cars India Limited (HCIL) posted a three-fold increase in sales on the back of strong demand for Honda City and Honda Amaze. On the other hand, most of the leading two-wheeler manufacturer such as Hero MotoCorp Limited, TVS Motors, Yamaha Motor India reported a surge in their January 2014 sales on a year-on-year basis, except Bajaj Auto.

In December 2013, the two-wheeler segment posted volume-wise growth for five consecutive months, said a report from ICRA and for the first nine months, two-wheeler sales registered growth of 5.40 percent over April-December, 2012, said data from SIAM.

The reason for the increase in sales in the two-wheeler segment is a surge in demand for scooters. According to an ICRA report, during the first nine months (April-December) of the current financial year (2013-14), the scooter segment expanded its share by 24 percent in the total two-wheelers volume.

The motorcycle segment, however, received lukewarm response during the period and has undergone a change in the

growth dynamics. According to ICRA, growth of the 125cc segment, the fastest growing sub-segment even a year ago (2012-13), contracted 22.7 percent y-o-y in December 2013 alone as the entry-level 100 cc continued to get better response.

According to the report, MSIL increased its market share in the domestic passenger car segment during the first nine months of the current financial year to 41.3 percent compared to 39.1 percent on the back of steady volumes of Alto, Swift DZire, Swift and WagonR. MSIL is followed by HCIL and HMIL. In comparison, Tata Motors, Mahindra & Mahindra Limited and Toyota have been the biggest market share losers during the period under review.

Commercial vehicles: Blues continue

For the commercial vehicles segment, slowdown continued even faster as demand for light commercial vehicles (LCVs) came off the cliff during December 2013. The domestic commercial vehicles (CV) industry ended with another month of depressed sales volumes as reflected by a decline of 25.5 percent y-o-y in December 2013. In comparison to the first nine months of the previous year (2012-13), slowdown in 2013-14 was sharper as small commercial vehicles (SCVs) also came under the grips of a cyclical slowdown, following almost five years of strong growth, due to saturation of demand across metros and tier II and tier III cities.

Of the commercial vehicle segments, the medium and heavy commercial vehicles (M&HCV) segment sales continued to decline for almost two years in a row, reflecting the impact of weak economic activity, subdued industrial activity and low freight and cargo availability.

The M&HCV segment contracted 27.9 percent during December 2013, while sales

All Trade Marks Acknowledged

Some of our esteemed clients:

BHUSHAN

20 Steel Insights, February 2014

fEATuRE

spending on construction and infrastructure have had come to rescue in times of a crisis. This sector has a strong multiplier effect. The government should look into the obstacles,” said an analyst with a broking firm.

Current woesFor the majority of companies, aggressive bidding at low margins has reduced surpluses from operations. This coupled with increased input costs (labour, cement, sand) and lower revenue growth has resulted in under-absorption of fixed costs. In many cases, EBITDA margins have deteriorated and operational cash flows have become negative.

“Aggressive bidding leading to low EBITDA margins has squeezed liquidity, especially where a significant portion of

the order value, close to the EBITDA margin, is locked up as retention money,” said a report by India Ratings.

As mentioned, these factors together have slowed down order execution. There have been a significant slowdown in execution since 2013 and the industry expects the trend to continue in 2014.

“Order execution will continue to be sluggish in

FY15 due to reduced ability of companies to fund working capital and delays in statutory clearances. Consequently, the aggregate revenue growth of the sector will continue to decline, with some companies facing a fall in revenue,” the report said.

RemediesAccording to analysts, the government needs to pay immediate attention to the stagnated order execution in the construction sector. “This sector is a major employer and this fact should be kept in mind during a slowdown.”

To improve fund availability, the government needs to encourage investments in the sector by framing investor friendly policies and removing hurdles. A major concern is the delay in project clearances. There is hope that clearances may be expedited following a change of guard at the Ministry of Environment and Forests (MoEF). Also, the Supreme Court’s verdict on de-linking environmental clearance from forest clearance will help start execution in non-forest land and provide temporary momentum in the roads sector.

“Overall, the revival in the construction sector will depend largely on the economic recovery. The government needs to continue reforms and take pro-growth measures by removing procedural hurdles. That said, we don’t see much action on this front till the elections in May,” the analyst said.

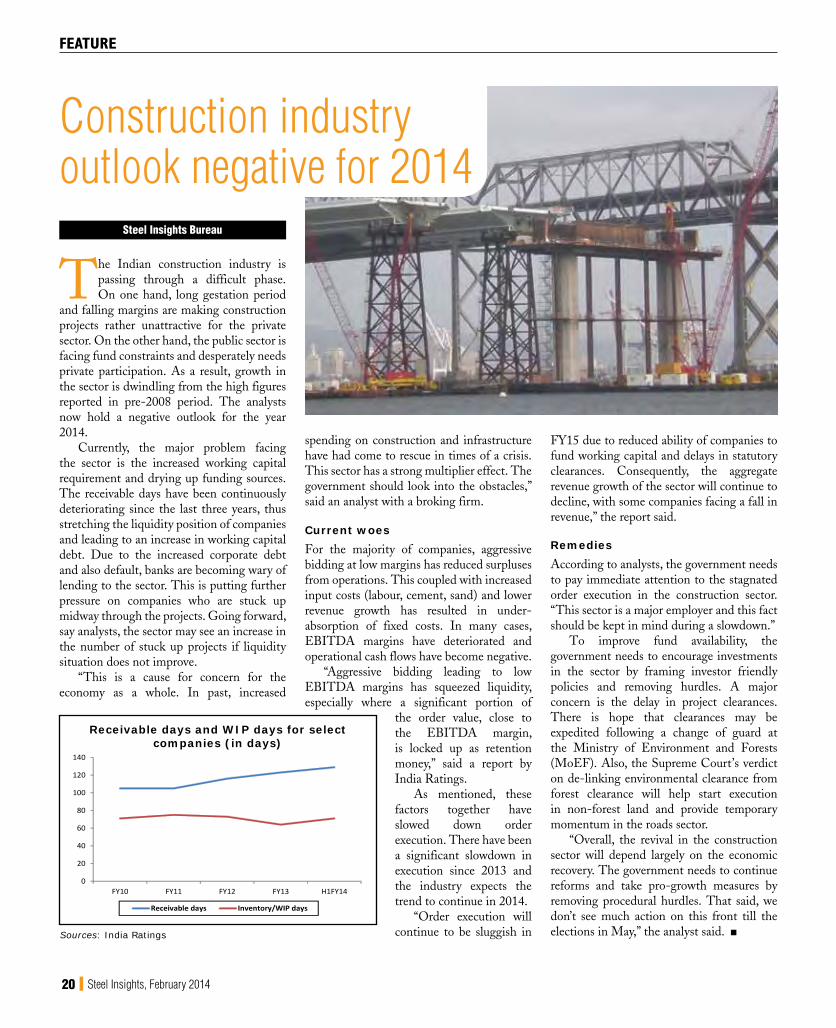

Steel Insights Bureau

The Indian construction industry is passing through a difficult phase. On one hand, long gestation period

and falling margins are making construction projects rather unattractive for the private sector. On the other hand, the public sector is facing fund constraints and desperately needs private participation. As a result, growth in the sector is dwindling from the high figures reported in pre-2008 period. The analysts now hold a negative outlook for the year 2014.

Currently, the major problem facing the sector is the increased working capital requirement and drying up funding sources. The receivable days have been continuously deteriorating since the last three years, thus stretching the liquidity position of companies and leading to an increase in working capital debt. Due to the increased corporate debt and also default, banks are becoming wary of lending to the sector. This is putting further pressure on companies who are stuck up midway through the projects. Going forward, say analysts, the sector may see an increase in the number of stuck up projects if liquidity situation does not improve.

“This is a cause for concern for the economy as a whole. In past, increased

Sources: India Ratings

0

20

40

60

80

100

120

140

FY10 FY11 FY12 FY13 H1FY14

Receivable days Inventory/WIP days

Receivable days and WIP days for select companies (in days)

Construction industry outlook negative for 2014

22 Steel Insights, February 2014

speculative factor in the market, but this is often underestimated,” he said.

In fact, prices have been on a steady rise since 2008-09. Neither the global recession and industrial slowdown, nor the higher interest rates and tight monetary policy of the Reserve Bank of India (RBI) could dent the bloated prices. As a result, the margins of the realty firms have remained protected despite adverse market conditions.

“In 2014, we don’t see any massive change in that equation. A price correction has been a talking point, but we need to appreciate that so long as speculative demand stays, the market would survive the falling end use demand,” the expert added.

Margins are stable There are many odds, as mentioned, for the players in the realty market. However,

the firm prices have saved the day for them in 2013, despite an increase in raw material costs, the general inflationary pressure and high borrowing costs.

According to a report by India Ratings & Research, while revenues were stagnant for most of the major players, the EBITDA margins were stable in 2013.

DLF Ltd reported a net profit of Rs 83 crore in the quarter ended September 2013, compared to a loss of Rs 19.5 crore in the year ago period. Similarly, Ansal Properties recorded a 17.9 percent growth in net profit for the first half of 2013-14 over the same period previous year. Barring the exception of Unitech Group, most other leading players saw a positive growth in margins during the April-September 2013 period.

As a result of stable margins, the outlook on individual companies remains stable even though the sector specific outlook is somewhat negative.

Election may be a game-changer While much of the industry expects to see continued slowdown in demand in 2014, there is a consensus that the general elections in May could bring fresh blood into the market.

“If there is a strong verdict in favour of any party, the market should receive a boost. We expect to see some activity post-elections,” an analyst said.

However, the impact is not likely to be prompt and would come only with a lag. The commercial property segment would be the first to get a boost before the residential segment sees a recovery in demand, he added.

“There is a risk too,” he said, “if the elections fail to give any clear verdict the market could respond with an adverse movement. And in this case, the impact would be rather prompt.”

Arindam Bandyopadhyay

Expect the expected in the Indian real estate industry, say analysts. Low demand, high prices, increased

debt. Overall, a negative outlook is what the industry is assigned for calendar 2014 and also for fiscal 2014-15.

Blame it on the inflexible prices, the analysts say, for the stagnated sales, but don’t blame the market players doing a tight rope walking between increased debt and increased investment inflow, at the same time.

“There is sort of a paradox in the realty market today. On one hand, there is perceptible downward trend in sale of new units over the last one year. On the other hand, prices remain firm despite low economic growth and falling disposable income,” said an industry expert.

“Prices showed some weakening in the first half of 2013-14, but the trend reversed thereafter. One reason of this could be the NRI funds which switched to realty following the imposition of import duties on gold last year. Actually, there is a strong investor or

0

20

40

60

80

100

120

140

DLF NationalBldg Const

Sobha Dev PrestigeEstates

HDIL MahindraLifestyle

SamruddhiRealty

OPM NPM

Profit margins for select realty cos in Q2, FY14 (%)

Source: BSE

fEATuRE

Realty check for 2014

Negative sentiment, sticky prices put pressure on realty sector

24 Steel Insights, February 2014

fEATuRE

Steel Insights Bureau

The sea-borne coking coal market continued its downward rally in January as demand remained

sluggish and there was little interest for fresh procurement. According to market sources, prices softened in the absence of Chinese buyers who were busy preparing for their New Year holidays starting January 31.

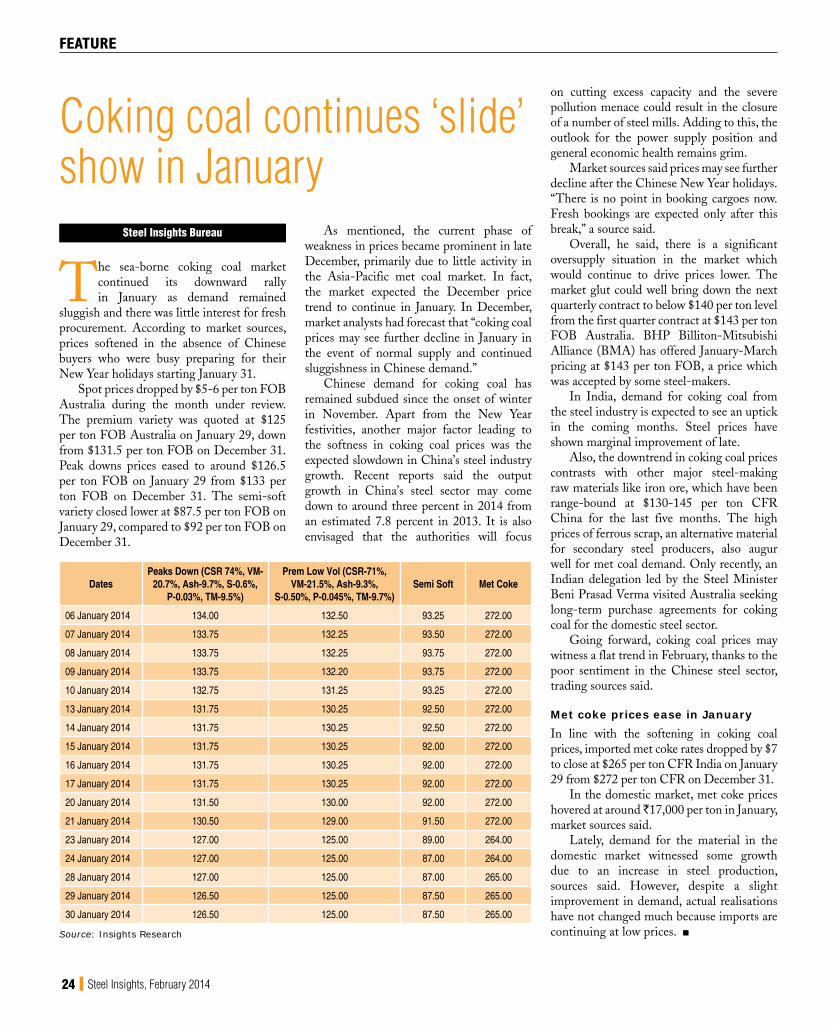

Spot prices dropped by $5-6 per ton FOB Australia during the month under review. The premium variety was quoted at $125 per ton FOB Australia on January 29, down from $131.5 per ton FOB on December 31. Peak downs prices eased to around $126.5 per ton FOB on January 29 from $133 per ton FOB on December 31. The semi-soft variety closed lower at $87.5 per ton FOB on January 29, compared to $92 per ton FOB on December 31.

As mentioned, the current phase of weakness in prices became prominent in late December, primarily due to little activity in the Asia-Pacific met coal market. In fact, the market expected the December price trend to continue in January. In December, market analysts had forecast that “coking coal prices may see further decline in January in the event of normal supply and continued sluggishness in Chinese demand.”

Chinese demand for coking coal has remained subdued since the onset of winter in November. Apart from the New Year festivities, another major factor leading to the softness in coking coal prices was the expected slowdown in China’s steel industry growth. Recent reports said the output growth in China’s steel sector may come down to around three percent in 2014 from an estimated 7.8 percent in 2013. It is also envisaged that the authorities will focus

Coking coal continues ‘slide’ show in January

on cutting excess capacity and the severe pollution menace could result in the closure of a number of steel mills. Adding to this, the outlook for the power supply position and general economic health remains grim.

Market sources said prices may see further decline after the Chinese New Year holidays. “There is no point in booking cargoes now. Fresh bookings are expected only after this break,” a source said.

Overall, he said, there is a significant oversupply situation in the market which would continue to drive prices lower. The market glut could well bring down the next quarterly contract to below $140 per ton level from the first quarter contract at $143 per ton FOB Australia. BHP Billiton-Mitsubishi Alliance (BMA) has offered January-March pricing at $143 per ton FOB, a price which was accepted by some steel-makers.

In India, demand for coking coal from the steel industry is expected to see an uptick in the coming months. Steel prices have shown marginal improvement of late.

Also, the downtrend in coking coal prices contrasts with other major steel-making raw materials like iron ore, which have been range-bound at $130-145 per ton CFR China for the last five months. The high prices of ferrous scrap, an alternative material for secondary steel producers, also augur well for met coal demand. Only recently, an Indian delegation led by the Steel Minister Beni Prasad Verma visited Australia seeking long-term purchase agreements for coking coal for the domestic steel sector.

Going forward, coking coal prices may witness a flat trend in February, thanks to the poor sentiment in the Chinese steel sector, trading sources said.

Met coke prices ease in JanuaryIn line with the softening in coking coal prices, imported met coke rates dropped by $7 to close at $265 per ton CFR India on January 29 from $272 per ton CFR on December 31.

In the domestic market, met coke prices hovered at around ̀ 17,000 per ton in January, market sources said.

Lately, demand for the material in the domestic market witnessed some growth due to an increase in steel production, sources said. However, despite a slight improvement in demand, actual realisations have not changed much because imports are continuing at low prices.

Datespeaks Down (CSR 74%, VM-

20.7%, Ash-9.7%, S-0.6%, p-0.03%, TM-9.5%)

prem low Vol (CSR-71%, VM-21.5%, Ash-9.3%,

S-0.50%, p-0.045%, TM-9.7%)Semi Soft Met Coke

06 January 2014 134.00 132.50 93.25 272.00

07 January 2014 133.75 132.25 93.50 272.00

08 January 2014 133.75 132.25 93.75 272.00

09 January 2014 133.75 132.20 93.75 272.00

10 January 2014 132.75 131.25 93.25 272.00

13 January 2014 131.75 130.25 92.50 272.00

14 January 2014 131.75 130.25 92.50 272.00

15 January 2014 131.75 130.25 92.00 272.00

16 January 2014 131.75 130.25 92.00 272.00

17 January 2014 131.75 130.25 92.00 272.00

20 January 2014 131.50 130.00 92.00 272.00

21 January 2014 130.50 129.00 91.50 272.00

23 January 2014 127.00 125.00 89.00 264.00

24 January 2014 127.00 125.00 87.00 264.00

28 January 2014 127.00 125.00 87.00 265.00

29 January 2014 126.50 125.00 87.50 265.00

30 January 2014 126.50 125.00 87.50 265.00

Source: Insights Research

26 Steel Insights, February 2014

fEATuRE

Flat steel producers play on low import, input costs

Steel Insights Bureau

Flat steel product makers relied on low imports and rising input costs to raise their prices even as demand failed to

cheer them. JSW Steel, a major producer of flat steel

products, announced a price hike of `1,000-1,200 per ton effective from February, 2014. Rising input costs are posing a challenge for the flat steel major.

Industry experts are still sceptical of any major revival in domestic demand for flat products. But, lower levels of imports of flat products have given JSW elbow room to raise prices amidst a dull demand scenario the economy.

Industry sources believe that JSW Steel has booked orders till March 31, 2014. Moreover, it has been able to find a lucrative overseas market. JSW has more than doubled its exports, which has helped in better realisations.

The flat steel industry is witnessing a pricing strategy wherein increase in prices by one major player triggers other manufacturers to raise prices. Last month, the price hike

from JSW Steel was followed by SAIL and other primary manufacturers.

This month, Essar Steel is also planning to raise its prices for flat steel products by `1,000-1,200 per ton, according to Essar Steel sources.

Industry sources say SAIL too plans to raise prices of flat steel products by `750-1,200 per ton.

Some industry analysts say high procurement prices of iron ore for JSW, which does not have any captive iron ore block, has led to frequent increase in prices.

A comparison of flat steel production and iron ore procurement prices is shown below.

Meanwhile, trading sources said markets in Mumbai also remained weak. An importer based in Mumbai expressed pessimism owing to a dull demand in this region. Mumbai, which is often considered a key hub for trading in flat steel products, has not seen any revival in demand either.

A slowdown in the number of projects and lack of demand from the automobile industry are to be blamed for poor demand in this region. Demand from pre-engineering and fabrication units has not seen any improvement either.

The automobile sector, one of the major

JSW Steel flat steel production vs iron ore procurement prices

Steel Insights, February 2014 27

consumers of flat steel products, has not seen any significant improvement in demand. The automobile industry consumes 19 percent of total flat steel production in India.

An overview of the consumption pattern of flat steel products across different sectors is shown below.

Mixed numbers for auto sectorThe latest numbers from the auto industry

association, Society of Indian Automobile Manufacturers (SIAM), reveals that production has seen a modest growth of 2.1 percent between the period of April 2013-December 2013 when compared to the same period last year. SIAM believes that the two-wheelers segment has

seen a good growth in this period and, in fact, has c o n t r i b u t e d to the overall growth.

Passenger vehicles sales

declined 5.7 percent and commercial vehicles sales declined 18.4 percent. Medium and heavy commercial vehicles encountered a de-growth of 26.9 percent, whereas light commercial vehicles registered a decline in sales by 13.9 percent during this period. The slowdown in sales of commercial vehicles is because of lack of mining activities and stalled infrastructure projects.

fEATuRE

Belt Cleaners | Transfer Point Components | Air Cannons | Vibration | Dust Managment | Safety Solutions

MARTIN ENGINEERING COMPANY INDIA PVT. LTD. | call +91 2135 674000 | fax +91 2135 674012 | email [email protected] | visit martin-eng.inU Turn Industrial Hub, Shed No. 5 | Gat No. 301, Kharabwadi, Chakan Tal-Khed | Dist – Pune – 410 501, Maharashtra, India

The steel industry is vital to our economy because of its broad range of applications—including renewable energy infrastructure, machinery and equipment, defense, transportation and infrastructure. Steel is also the most recycled material in the world.

Martin Engineering is there to help facilitate the process from coke oven to blast furnace to the steel refining facility. Our products are used in every part of the process.

As the worldwide leader in bulk materials handling solutions, Martin has the experience and expertise to make your steel plant as efficient and productive as possible.

0

0.1

0.2

0.3

0.4

0.5

0.6

April

May

June July

Augu

st

Sept

embe

r

Oct

ober

Nov

embe

r

Dece

mbe

r

Qty (in million tons)

Month wise import of flat steel products in 2013-14

Source: Insights Research

28%

19%

18%

15%

9%6% 5%

Capital goods Automobiles PipelinesConstruction Consumer durables OthersOil & Gas

Sector wise consumption of flat steel products

28 Steel Insights, February 2014

During the month of January, the government and private companies started their construction projects, which resulted in improvement in demand.

Few major brands based in Raipur have supplied around 2,500 tons of average quantities of beams to Chhattisgarh State Electricity Board (CSEB).

Some industry players said the rise in structure demand did not lead to a concomitant rise in prices as rates of scraps, the input material, fell in the main trading centre of Alang.

In line with the other structure brands, wire rod demand also remained stable.

Sources at RINL said the stable market led to a rise in wire rod offers by `600 per ton by the state-owned steel company. Sources

said SAIL has also raised wire rod prices by `500 per ton.

“In the beginning only pending orders were cleared but now we are receiving new orders on new rates,” said an industry player.

Semi finished demand volatile

Demand for semi-finished MS ingots and billets remained volatile in line with the end products.

However, re-bar production growth supported the volatility in demand to some extent. “Any further improvement in prices is not expected from this position as the construction sector, which is the major buyer of finished steel, is witnessing slower activities,” said an ingot buyer.

NINL keeps offers unchanged

Neelachal Ispat Nigam Limited (NINL), which has an integrated plant with a capacity of around 1.1 million tons and a steel plant at Kalinga Nagar Industrial complex, Jajpur (Odisha), kept its MS billet prices unchanged at `27,600 per ton (ex-plant).

The company is offering 9,635 tons of Concast billets of grade IS 2830 in an open sale offer on first-come-first-serve basis, according to company sources.

Long steel, semi finished demand remain volatile

Steel Insights Bureau

Long steel product demand remained volatile with marginal ups and downs but market players were confident

that demand would remain stable in the near future with construction and infrastructure sectors being the major platforms of growth for the economy.

In case of re-bars, market demand remained stable and, according to participants, there will be no major correction in re-bar demand and it would be stable in the near term on the back of ongoing construction and infrastructure projects.

While market participants see good demand in the western, central and northern regions of the country, a re-bar manufacturer in Rourkela said, “The conversion cost of MS ingot to re-bar has increased. Stable demand has led to the clearance of stock and plants operating at full capacity. I am of the view that the market will sustain in this pace.”

In south India, demand remained good but re-bar supplies to Bangalore went down owing to a halt in construction activity due to a strike by the sand traders.

But demand will pick up as soon as there is an upswing in construction activities, said traders.

Structural demand strong

Structural demand in central and western India increased as expected by market players.

Consumption of non-alloy finished steel in April-December 2013-14(in '000 tons)

particulars Total production Imports Exports Availability Variation

in stock

Consumption Variation %2013-14 2012-13

Bars & rods 22196 254 465 21985 -226 22211 21587 2.9

Structurals 5014 33 53 4994 -22 5016 4691 6.9

Rly Materials 659 4 1 662 -19 681 694 -1.9

Total 27869 291 519 27641 -267 27908 26972 3.5

fEATuRE

Steel Insights, February 2014 29

fEATuRE

Steel Insights Bureau

Tata Steel has launched two new products, Tata Ferromag (branded ferro manganese) and Tata Tiscrome

(branded ferro chrome). These products were launched by Tata Steel’s Ferro Alloys & Minerals Division.

Speaking on the occasion, D B Sundara Ramam, Executive-In-Charge, Ferro Alloys & Minerals, said, “As part of our promise to deliver innovative quality products to the market, we are proud to announce the launch of Tata Ferromag & Tata

Tiscrome. These brands fulfill the long-felt market need of committed availability to customers along with product consistency and guaranteed chemistry, weight and size of alloy. Authorised distributors across the country will ensure that customers have the convenience of purchasing the product when they want it, how they want it and where they want it.”

The products will be sold in branded 50 kg & 1 million ton (mt) HDPE bags which have tear-proof labels ensuring bag-wise traceability across the value chain. Tata Steel is targeting a market size of 300,000 mt a year in India for both Tata Tiscrome and

MMTC aims to export chrome ore in Q4, eyes tie-up with MOIL

Steel Insights Bureau

MMTC Ltd expects to sell around 40,000 tons of chrome ore in the export market after tendering in the January-March quarter (Q4) of 2013-14, a source said.

“The company has sold a total of 150,000 tons of chrome ore during the first nine months of 2013-14 and another 40,000 tons are expected to be sold in the fourth quarter,” the source added.

MMTC has set a target to achieve an export turnover of `300 crore from chrome ore in 2013-14 and is most likely to achieve the target. Besides chrome ore, MMTC is also trying for export of high carbon ferro chrome, the source added. MMTC Ltd is also planning to enter into a tie-up with South African miners for import of fixed quantities of manganese ore, a source said.

“No one gives manganese ore on long-term price basis contracts, but MMTC is trying to enter into some long-term contracts for fixed quantities,” the source added.

Meanwhile, a consignment of 5,000 tons of manganese ore from MMTC is likely to arrive at Paradip Port in March.

The company is also trying to tie up with Manganese Ore India Ltd (MOIL) for exporting the latter’s ore.

A final agreement is yet to be reached, but it is understood that MOIL has given the go- ahead to MMTC to tie up with buyers and, based on the responses of the tie-ups or number of buyers, the miner will take a call on the prices for exports. MOIL is already selling manganese ore through e-auction to domestic buyers.

Tata Steel launches 2 branded ferro alloys

Tata Ferromag. In terms of market share, Tata Steel will target 38 percent share in the domestic market with Tata Tiscrome in FY’15 while Tata Ferromag is targeted at 10% in FY’15. The two newly-launched brands will be available across distribution centres in India. Tata Steel is rolling out the product in Gujarat, Maharashtra, NCR, Rajasthan, Odisha and West Bengal, which are the major consumption centres.

Ferro chrome and ferro manganese are ferro alloys widely used as alloying agents in the production of carbon and stainless steel. Ferro chrome provides corrosion resistance thus increasing the life of stainless steel, while ferro manganese provides the necessary toughness and hardness to steel. The introduction of the two brands will ensure customers are able to reduce on the inventory holding, get guaranteed quality, leading to minimal wastage of heat and customised sizes, leading to easier handling of the material, a Tata Steel release said.

IMFA Q3 net down 27% to `10.98 cr

Steel Insights Bureau

Indian Metals & Ferro Alloys (MFA) reported a 27 percent decline in net profit to `10.98 crore in the quarter

ended December 31, 2013. The company had reported a net profit of `15.06 crore in the same period last year.

The company said its revenues increased 17 percent to `364.06 crore in the quarter under review as compared to `311.50 crore in the same period last year.

EBIDTA (Earnings before interest, taxes, depreciation and amortisation) increased 44 percent to `87.13 crore as compared to `60.42 crore in the year-ago period.

"The quarterly performance is in line with our expectations with revenues rising 17 percent and operating profits by 44 percent which is better given the difficult circumstances. However, net profit has been impacted due to higher depreciation and finance costs on account of the recently commissioned captive power plants," Managing Director & Chief Executive Officer Subhrakant Panda said.

30 Steel Insights, February 2014

COvER sTORy

Indianpellet-makers’ palette of woesTamajit Pain

The government’s recent imposition of the 5% export duty on iron ore pellets has divided the steel industry.

Steel Insights, February 2014 31

COvER sTORy

The pellet industry, which had been slowly taking baby steps to bring in complete transformation of the steel-

making process in India, is in the limelight but for all the wrong reasons.

The Indian government has recently imposed a five percent tax on the export of iron ore pellets in response to demand from the domestic steel industry.

The Indian steel industry made representations to the government that a nil rate of duty on exports of iron ore pellets and a 30 percent tax on the export of iron-ore fines had led to a situation in which pellet exports were rising sharply through diversion of fines, leading to a shortage of raw material at the local steel mills.

The differential rate of duty on iron-ore fines and pellets was showing divergent trends in export of the critical raw material. Taking advantage of a nil rate of export duty, iron ore pellet shipments from the country increased 111 percent to 435,000 tons during April-October, 2013, compared to 40,000 tons during the corresponding period of the previous financial year, with the mining industry expecting that total pellet exports during 2013-14 would touch a whopping 800,000 tons or so.

During April-October, iron ore exports were estimated at 8.43 million tons, down 43.5 percent over the corresponding period of the previous year.

India has about 36 iron ore pelletisation plants operated by steel companies, as well as standalone raw material companies like KIOCL (formerly Kudremukh Iron Ore Company Limited), with a combined capacity of around 63 million tons.

The Indian government’s move came after the Associated Chamber of Commerce and Industry (ASSOCHAM), an industry representative body, wrote to Finance Minister P Chidambaram, pointing out the sharp rise in iron ore pellet exports, owing to the nil rate of tax, which had accentuated the shortage in the raw material faced by domestic steel companies at a time when several iron ore mines, in provinces such as Karnataka and Goa, continued to remain closed following investigations into illegal mining.

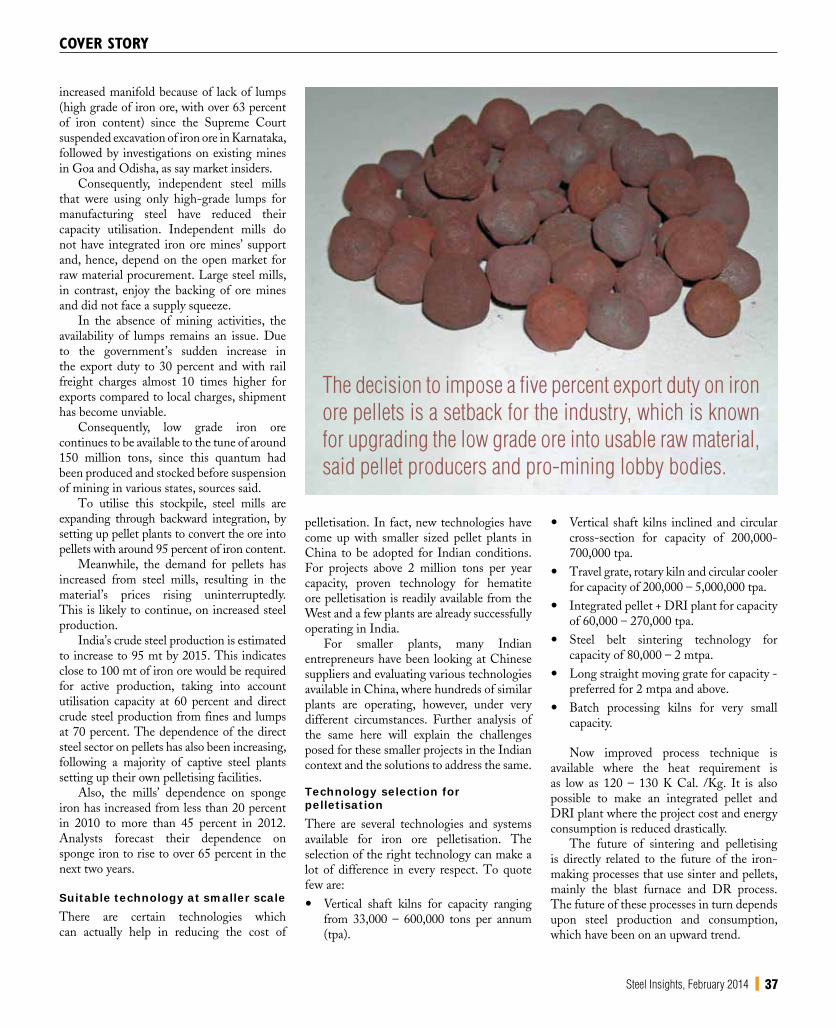

Decision a setbackThe decision to impose a five percent export duty on iron ore pellets is a setback for the

industry, which is known for upgrading the low grade ore into usable raw material, said pellet producers and pro-mining lobby bodies.

“It is a huge setback for the pellet industry because, as pellet producers, we have to pay excise duty and now the export duty comes as an additional burden,” said N D Rao, Managing Director of Brahmani River Pellet Ltd (BRPL), a unit of Stemcor that has a 4-million-tons-per-annum (mtpa) pellet plant in Odisha.

Taking advantage of the government’s incentives on import of pellet-making equipment and nil export duty, large capacities were added in the last two years, taking the total production capacity in the country to nearly 60 million ton from 28 million ton in 2010-11.

Till 2012-13, exports of iron ore pellets were negligible.

“However, in April-November, 2013, exports of iron ore pellets have risen sharply, causing an apprehension about shortage of iron ore in the country,” the finance ministry said in a statement.

According to trade estimates, so far, nearly one million tons of pellets have been exported, which is less than 1.5 percent of the total installed capacity. KIOCL tops the list as the lead exporter, followed by Jindal Steel & Power Ltd (JSPL). Essar Steel and BRPL also export pellets in limited quantities to South East Asian nations.

The mining lobby said the decision is skewed towards the steel-maker’s lobby. “The recent decision to impose the export duty on iron ore pellets shows that the Union government is influenced by the steel-makers’ lobby. This will hurt future investments in pelletisation capacity,” said R K Sharma, Secretary-General of the Federation of Indian Mineral Industries (FIMI).

Pellet producers said, since many large steel-makers have their own pellet plants and others do not have the facility to use domestically available blast furnace grade

pellets, it will affect the pellet manufacturers and lead to a curb on productions.

“Pellet manufacturers strongly feel the Union government is playing into the hands of a handful of steel-makers. We urge the government to reconsider its decision and exempt pellets from the export duty,” said S K Chatterjee, Secretary, Pellet Manufacturers’ Association of India (PMAI), in a statement.

Pellet-makers talk toughSome iron ore pellet producers said they may be compelled to shut operations if the government does not roll back the five percent duty imposed on exports of iron ore pellets. The shutdown would render futile nearly `35,000 crore of investments.

While recommending the duty, the steel ministry had argued that iron ore was being exported in the garb of pellets, which virtually amounted to exporting the scarce mineral.

It seems, the finance ministry imposed the duty despite objections raised by the commerce and industry ministry. In a letter dated January 7, the commerce ministry wrote to the revenue secretary, saying it does not support the export duty because pellet is a value-added product and it has been the ministry’s stance that there should be no export duty on the same.

However, the commerce ministry replied that, out of an installed capacity of over 60 mt, barely 25 mt is domestically consumed. The lack of low domestic demand has, in fact, compelled producers to cut down their capacity utilisation to less than 50 percent.

Leading pellet producers have told the finance ministry that while most plants would find it unviable to operate, bigger players may have to rethink on expanding the capacities unless the government addresses their concerns.

Firdose Vandrevala, Executive Vice-Chairman of Essar Steel, said: “The government hastily announced the five percent export duty on pellets, despite the fact that entrepreneurs have invested thousands

The demand for pellets has increased from steel mills, resulting in the material’s prices rising uninterruptedly. This is likely to continue, on increased steel production.

HORIZONTAL PUMP

HORIZONTAL PUMP

34 Steel Insights, February 2014

of crores of rupees to create capacities and expand their operations. This action deepens investor’s fears of a stable policy. Flip-flop policies can turn investments sour overnight.”

Malay Chatterjee, Chairman of the state-run Kudremukh Iron Ore, said his pellet project in Karnataka has a capacity of 3.5 mt and is a 100 percent export-oriented unit, which recently commenced overseas sales. For my company, the situation is even more worrisome. “My unit can only survive on exports. The duty will hugely impact commercial viability of our operations,” he added.

Ravi Uppal, CEO of JSPL Group, said: “The move exhibits lack of consistency in government policies. It is a decision without

any rationale, which would do colossal damage to the pellet industry, which has invested over `30,000 crore during the last three years.”

Industry experts said a little over one million tons of pellets have been exported till January this fiscal against the installed capacity of 60 million tons. “I fail to understand what motivated the steel ministry to recommend the duty and how much revenue would the government gain in imposing the same when exports are abysmally low,” said a pellet-maker on condition of anonymity.

However, whatever be the reason or impact of the duty on the pellet-making industry in India, it becomes imperative to examine the need for growth of the pellet-

making capacity in the country as India embarks on increasing its steel-making capacity to meet future demand.