ECIA CONFERENCE - Investors panel - 5th June 2013

Mar 06, 2016

Â

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

What do European investors look for in the CCIs?

18:00h19:00h

What do European investors look for in the CCIs? The entrepreneurs are more than ever being required the capacity of detecting different typologies of investors and being able to identify their interlocutor’s profile, what are their priorities, fears and uncertainities. What do investors look for in the creative industries? How can I adapt my project to the different type of investor, either a business angel or an equity fund or a bank representative? An european survey on this issue will be presented, as well as a round table with the point of view of different european investors. Moderator: Jenny Tooth, Managing Director of Angel Capital Innovations and Chief Executive of UK Business Angels Association [email protected]

Jenny Tooth, since July 2012 has taken the role of part-‐time CEO of the UK Business Angels Association which has superseded the British Business Angels Association, the trade body for angel and early stage investing. Jenny has been providing strategic support to BBAA since its establishment in 2004, supporting both policy and interfacing with Government, as well as developing the trade body’s major annual events. Jenny has over 20 years’ experience of supporting SMEs access to investment, both in the UK and internationally. She ran her own consultancy, including spending nine years based in Brussels, working closely with the EC. She has operated a wide range of investment readiness programmes, including projects supported by national and EU funding. She has also participated in a number of expert groups on access to finance and chaired the EC Knowledge Intensive Services group under DG Enterprise. In 2006 she took on the role of Business Development Director at GLE Growth Capital and in 2009 she co-‐founded Angel Capital Group where she has been acting as MD of Angel Capital Innovations focusing on demand side issues and angel investment, operating projects on ICT; nano technology and Mobile services and applications. She has also been a frequent judge at business plan competitions and acted as an assessor for the

Technology Strategy Board for innovation grant applications. Jenny is an experienced speaker, both in the UK and across Europe. She has an MSc in Economics from London School of Economics and Political Science. PANELISTS § Antoinette Godin, European Projects Officer of St’Art Antoinette.GODIN@start-‐invest.be

Antoinette is the European Projects Officer at St’art. St’art investment fund is a unique financial instrument in Brussels and Wallonia supportingthe development of the creative economy.

St’art is aimed at small and medium companies, including non-‐for-‐profit organisations. The fund contributes to the creation of companies and the development of existing structures in order, for example, to undertake new projects, create new products and win new markets. The fund provides financing in the form of loans and investments.

The objective is also to influence banks and private investors. St’art will work closely with public bodies and regional investment funds. Therefore St’art complements and not replaces other existing financial mechanisms and possible public subsidies.

To implement that objective, St’art is also involved in two European projects: C-‐I factor aiming to develop access to finance to creative industries and Wallonia European Creative Districtexploring creative economy in the Wallonia Region.

§ Jose María Pina, Entrepreneurship Director, Keiretsu Forum Barcelona [email protected]

§ Anthony Clarke, MD of London Business Angels [email protected]

Anthony is the co-‐founder and CEO of Angel Capital Group which includes London Business Angels where he has the role of Managing Director.

Anthony qualified as a Chartered Accountant and Chartered Secretary with Deloitte Haskins & Sells (now PWC) in 1980. Thereafter, he worked on a full time basis as Finance Director and Chief Executive of a number of privately owned SME companies and since 1995 he has been a business angel investor/non-‐executive director of over 20 start-‐up/early stage businesses. Between 2002 and 2009 Anthony was Managing Director of GLE Growth Capital and also sat on the main Board of GLE.

Anthony has been involved with London Business Angels for 18 years and took on the role of MD of LBA when it became part of GLE Growth Capital in 2002. He is also a co-‐founder and currently sits on the advisory Board of Seraphim Capital-‐ the UK’s first £30m Enterprise Capital Fund. He was Chairman of the UK Business Angels Association (UKBAA) from August 2004 to July 2012 and remains on its Board. He is President Emeritus of European Business Angels Network (EBAN) having been its President from 2004-‐2009. Anthony also sits on the Venture Capital Committee of the BVCA. § Núria Bosch Balada -‐ Board of Directors member at Baring Private Equity Partners [email protected]

Ms. Bosch began her professional career as a risk analyst at Banque National de Paris, where she later became Associate Regional Manager. In 1992, she joined RBA Editores as Controller. During the period 1994-‐97, she was a shareholder and director of the university-‐level school EUROAULA, after which time she returned to the financial field as a Private Wealth Manager at Andorra Private Banking. She later worked in the area of investment capital in Catalonia as Director of Financing and Entrepreneurship at the CIDEM (Generalitat de Catalunya), where she represented the Catalonian Government at investment fund board meetings. She joined Baring Private Equity Partners in January 2007. Ms. Bosch holds a Business Management degree and MBA from ESADE University.

Moderator: Jenny Tooth, Managing Director of Angel Capital Innovations and Chief Executive of UK Business Angels Association

C-I Factor Research Study| 08.01.2013 | peacefulfish

The Views of Investors, both traditional and alternative Finance

Sources in Financing Creative Industries

Jenny Tooth, MD, Angel Capital Innovations ,

CEO UK Business Angels Association Barcelona 5th June 2013

C-I Factor Research Study| 08.01.2013 | peacefulfish

Background to the Research

Many studies look at the Demand side- not enough info on the Views of the Finance Supply Side

Research Focus on Investors C-I Factor Partner countries:

UK, Netherlands, Belgium, France, Germany: June to October 2012

1. Review of Online profiles of existing CI Investors: 594 2. Online Survey: ~1200 invited to participate

231 Investors participated 3. Interview series: 25 participated (July-October 2012) 4. Case Studies: 5 active CI Finance funders

5. Report with Key findings and Recommendations for CI

Factor Partners - December 2012

C-I Factor Research Study| 08.01.2013 | peacefulfish

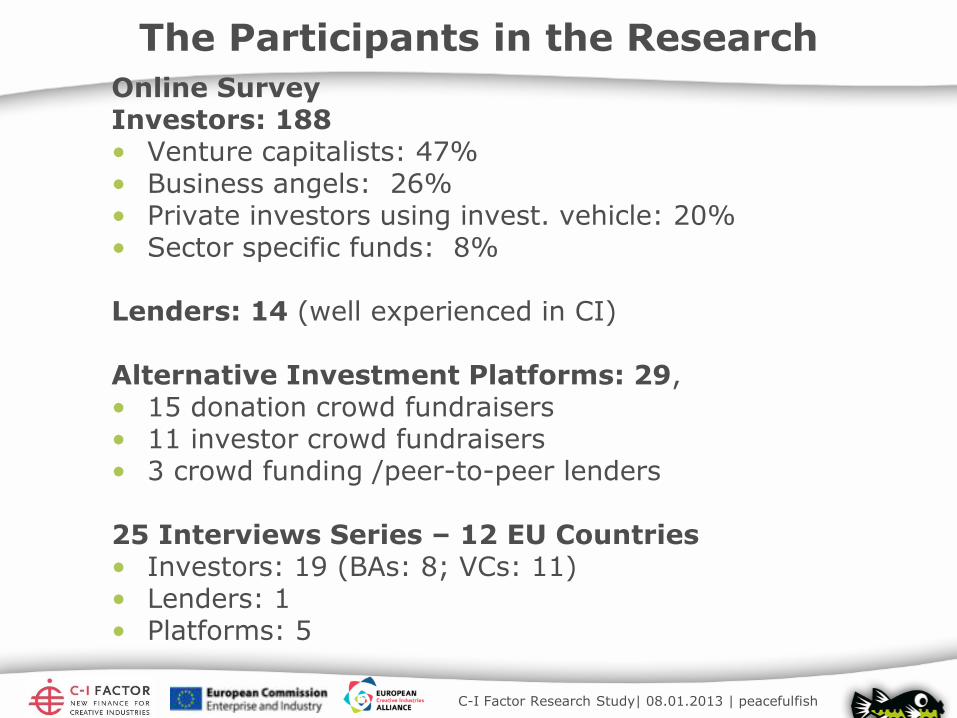

The Participants in the Research

Online Survey Investors: 188 • Venture capitalists: 47% • Business angels: 26% • Private investors using invest. vehicle: 20% • Sector specific funds: 8% Lenders: 14 (well experienced in CI) Alternative Investment Platforms: 29, • 15 donation crowd fundraisers • 11 investor crowd fundraisers • 3 crowd funding /peer-to-peer lenders

25 Interviews Series – 12 EU Countries • Investors: 19 (BAs: 8; VCs: 11) • Lenders: 1 • Platforms: 5

C-I Factor Research Study| 08.01.2013 | peacefulfish

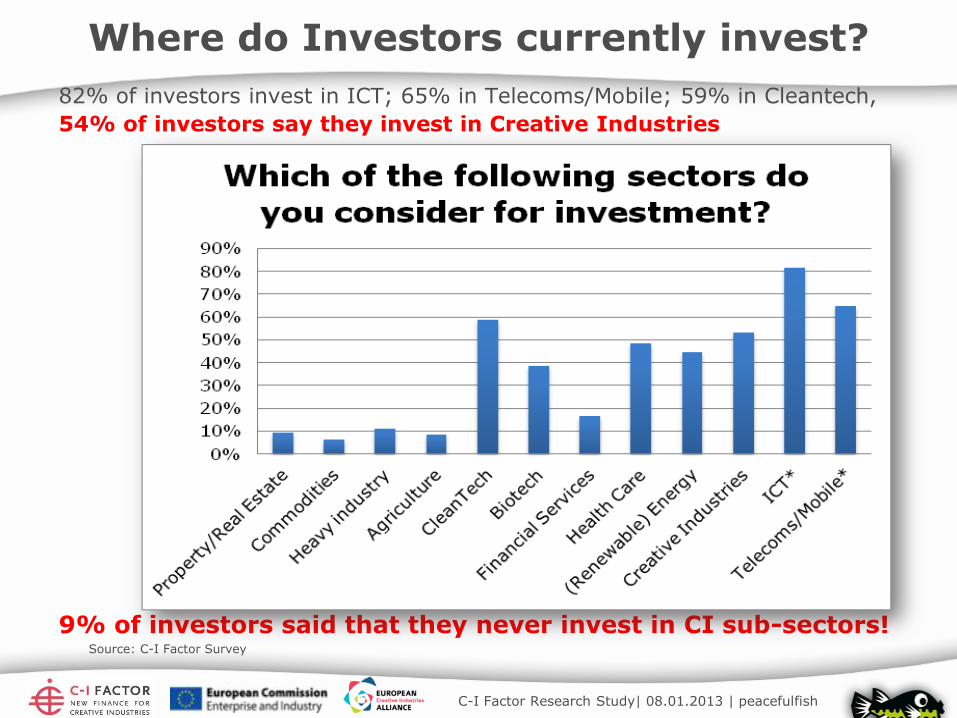

Where do Investors currently invest?

82% of investors invest in ICT; 65% in Telecoms/Mobile; 59% in Cleantech,

54% of investors say they invest in Creative Industries

9% of investors said that they never invest in CI sub-sectors!

Source: C-I Factor Survey

C-I Factor Research Study| 08.01.2013 | peacefulfish

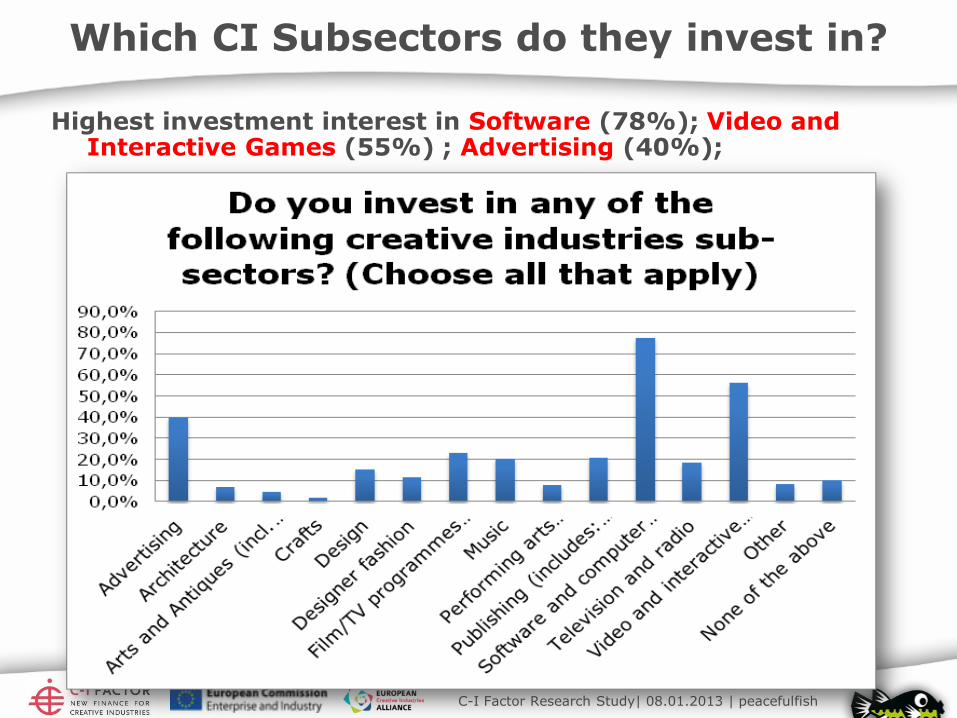

Which CI Subsectors do they invest in?

Highest investment interest in Software (78%); Video and Interactive Games (55%) ; Advertising (40%);

Source: C-I Factor Survey

C-I Factor Research Study| 08.01.2013 | peacefulfish

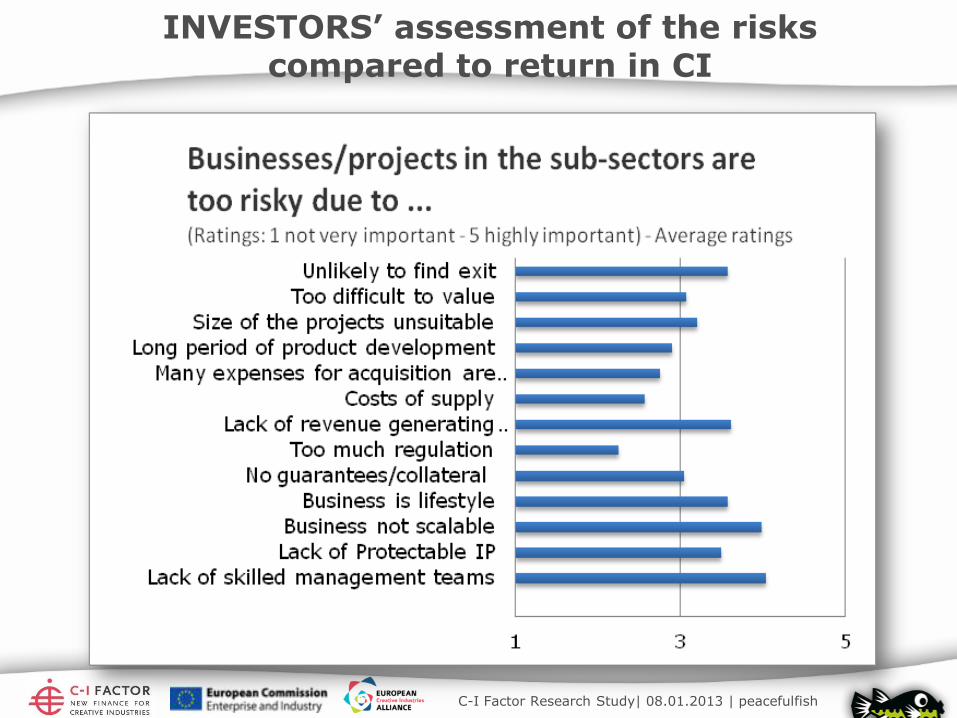

INVESTORS’ assessment of the risks

compared to return in CI

C-I Factor Research Study| 08.01.2013 | peacefulfish

Biggest Risks for Investors in CI

Investors identify what are 4 biggest risks in CI

1.Lack of Skilled Management Teams

2.Business lacks clear revenue generating model

3.Business not scalable

4.Unlikely to find Exit

C-I Factor Research Study| 08.01.2013 | peacefulfish

Survey: What attracts Investors to CI?

Investors identify what makes a good deal in CI

• scalability

• disruptive business models

• strong intangible assets

• “fit” with organisational & personal interests and current portfolio were also significant drivers

BAs and VCs prefer locating deals

• through direct contact from entrepreneurs

• and personal recommendations

• BAs rank pitching events combined with market intelligence higher than VCs

• crowdfunding and online networking platforms are the least favoured

•

C-I Factor Research Study| 08.01.2013 | peacefulfish

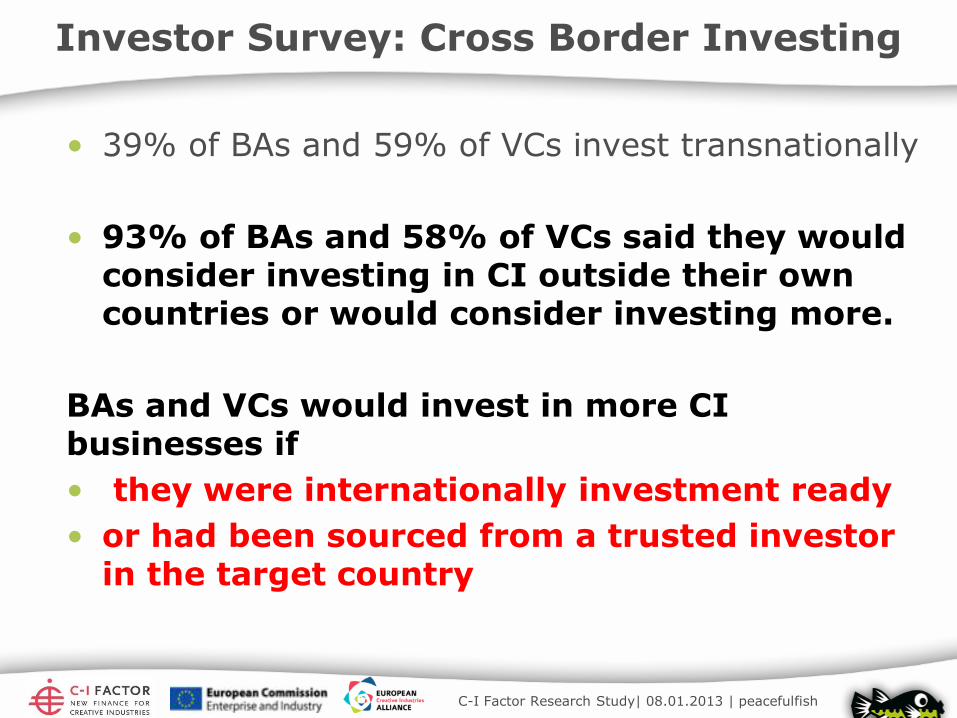

• 39% of BAs and 59% of VCs invest transnationally

• 93% of BAs and 58% of VCs said they would consider investing in CI outside their own countries or would consider investing more.

BAs and VCs would invest in more CI businesses if

• they were internationally investment ready

• or had been sourced from a trusted investor in the target country

Investor Survey: Cross Border Investing

C-I Factor Research Study| 08.01.2013 | peacefulfish

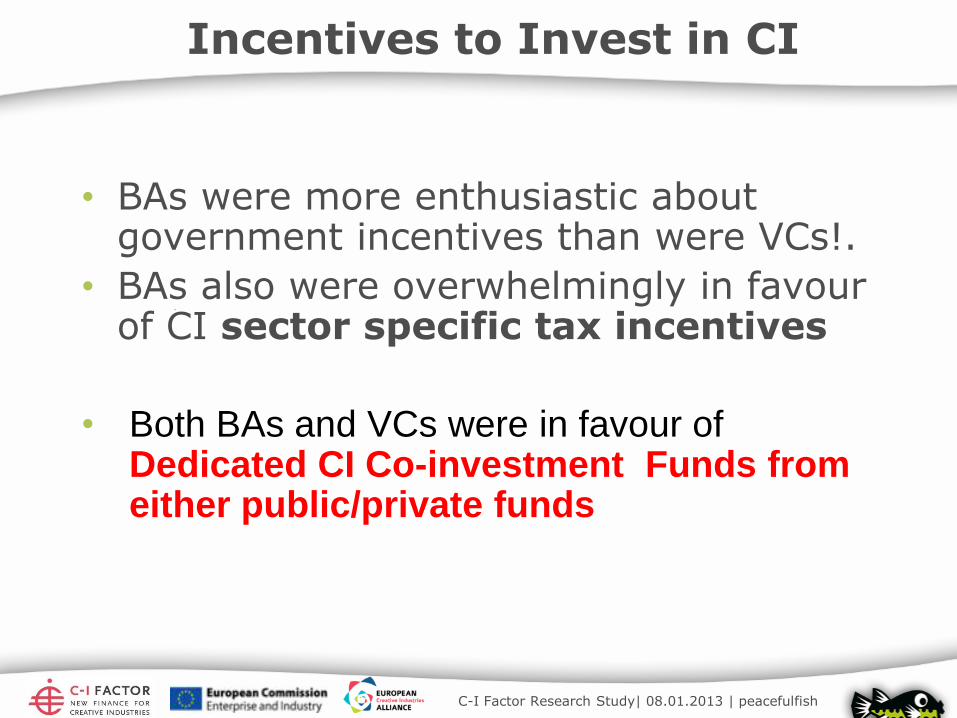

• BAs were more enthusiastic about government incentives than were VCs!.

• BAs also were overwhelmingly in favour of CI sector specific tax incentives

• Both BAs and VCs were in favour of Dedicated CI Co-investment Funds from either public/private funds

Incentives to Invest in CI

C-I Factor Research Study| 08.01.2013 | peacefulfish

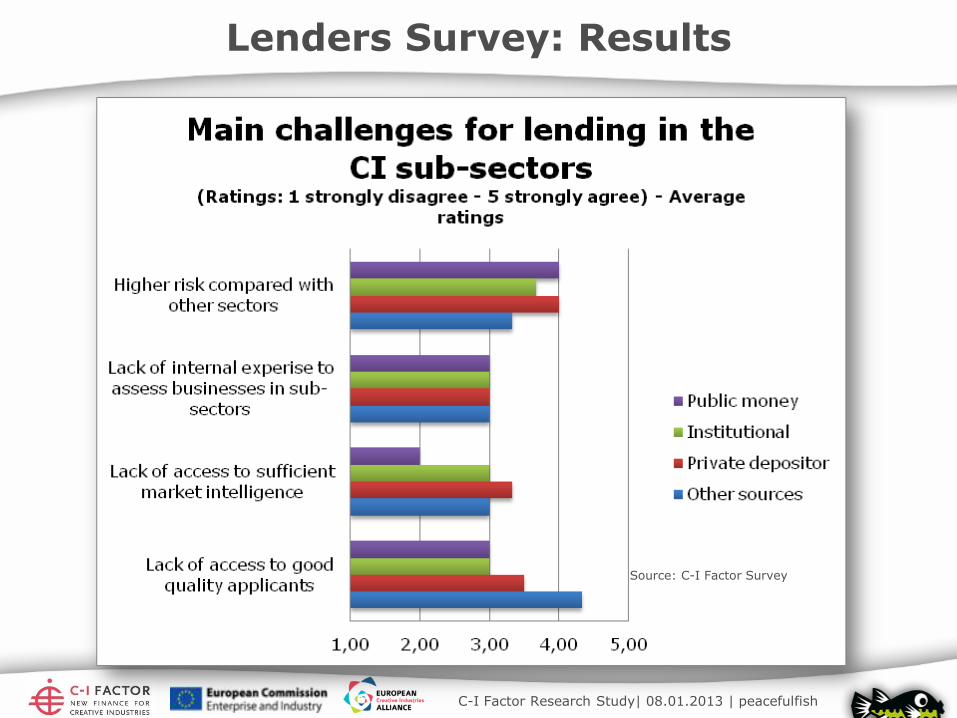

Lenders Survey: Results

Where do they invest?

71% of our sample lenders lend to the CI

43% lend to property/real estate sector

36% lend to the ICT sector

36% lend to the Telecoms/mobile sector

Top 3 CI sub-sectors in nearly all 4 lender categories in our sample

• Software

• Publishing

• Film

All bank groups in the sample consider CI higher risk compared with other sectors !.

C-I Factor Research Study| 08.01.2013 | peacefulfish

Lenders Survey: Results

Source: C-I Factor Survey

C-I Factor Research Study| 08.01.2013 | peacefulfish

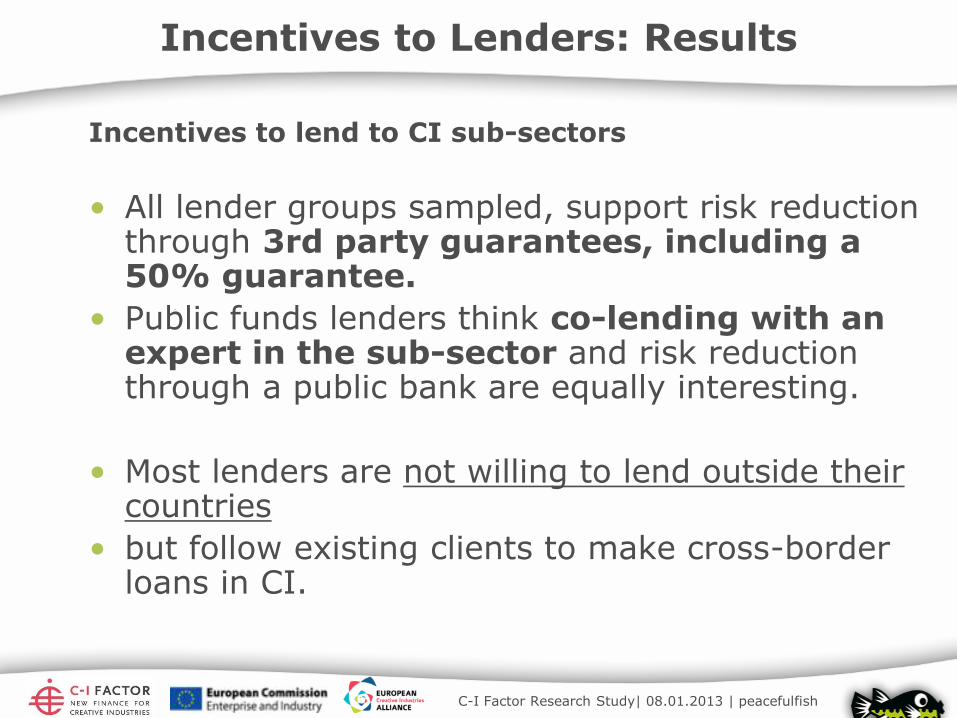

Incentives to Lenders: Results

Incentives to lend to CI sub-sectors

• All lender groups sampled, support risk reduction through 3rd party guarantees, including a 50% guarantee.

• Public funds lenders think co-lending with an expert in the sub-sector and risk reduction through a public bank are equally interesting.

• Most lenders are not willing to lend outside their countries

• but follow existing clients to make cross-border loans in CI.

C-I Factor Research Study| 08.01.2013 | peacefulfish

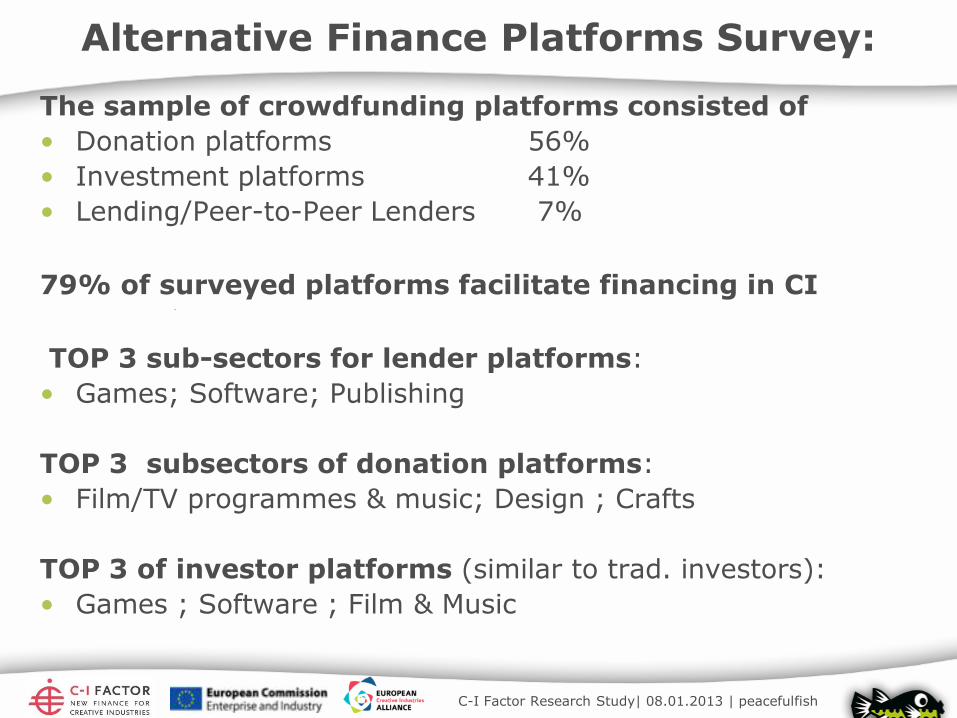

Alternative Finance Platforms Survey:

The sample of crowdfunding platforms consisted of

• Donation platforms 56%

• Investment platforms 41%

• Lending/Peer-to-Peer Lenders 7%

79% of surveyed platforms facilitate financing in CI

TOP 3 sub-sectors for lender platforms:

• Games; Software; Publishing

TOP 3 subsectors of donation platforms:

• Film/TV programmes & music; Design ; Crafts

TOP 3 of investor platforms (similar to trad. investors):

• Games ; Software ; Film & Music

C-I Factor Research Study| 08.01.2013 | peacefulfish

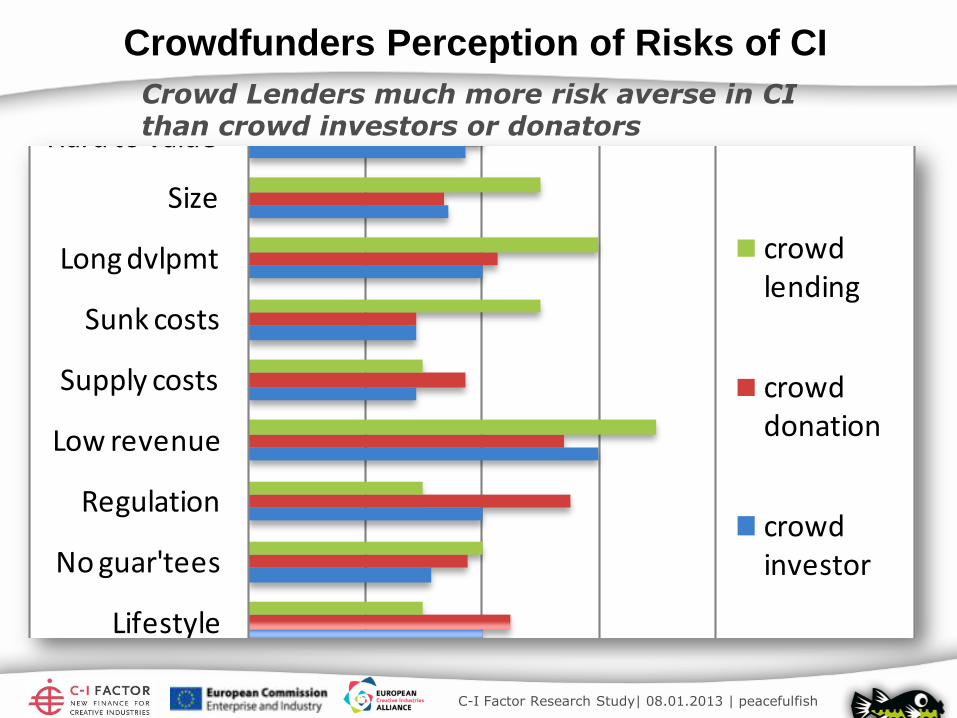

Crowdfunders Perception of Risks of CI

1,00 2,00 3,00 4,00 5,00

Mgmt teams

Lack of IP

Not scalable

Lifestyle

No guar'tees

Regulation

Low revenue

Supply costs

Sunk costs

Long dvlpmt

Size

Hard to value

Unlikely exit

Sub-sectors too risky due to(Ratings: 1 not very important - 5 highly important) -

Average ratings

crowd lending

crowd donation

crowd investor

Crowd Lenders much more risk averse in CI than crowd investors or donators

C-I Factor Research Study| 08.01.2013 | peacefulfish

CI Factor

Develop a Knowledge Centre of CI Market Intelligence- success stories, deals done; exits etc:

Market Intelligence at CI Pitching and showcasing events

Create an online CI Investor community – sharing intelligence and deals creating better connectivity between all finance sources

Develop an integrated programme of finance awareness and investment readiness dedicated to CI and subsector specific- incl a new Serious Game for investors and CI SMEs

Create database of CI finance sources: investors, lenders , platforms interactive information Tools for accessing CI Finance

Actions at EU Level

Support Development of the new Bank Guarantee Fund for CI

Support Development of new CI Co-investment Fund of Funds

Support an integrated overall EU Policy agenda for financing CI

What Could be Done?

C-I Factor Research Study| 08.01.2013 | peacefulfish

• How does this research compare with your views

on financing of CI businesses?

• How much investment are you making in which CI

subsectors - and what are you looking for?

• Is the problem with the CI Businesses not being

Investment ready, or not investor attractive?

• Or the lack of awareness/interest of investors in

financing CI businesses?

• What are the right measures to take for the supply

and demand side?

Questions for Discussion

Antoinette Godin, European Projects Officer of St’Art

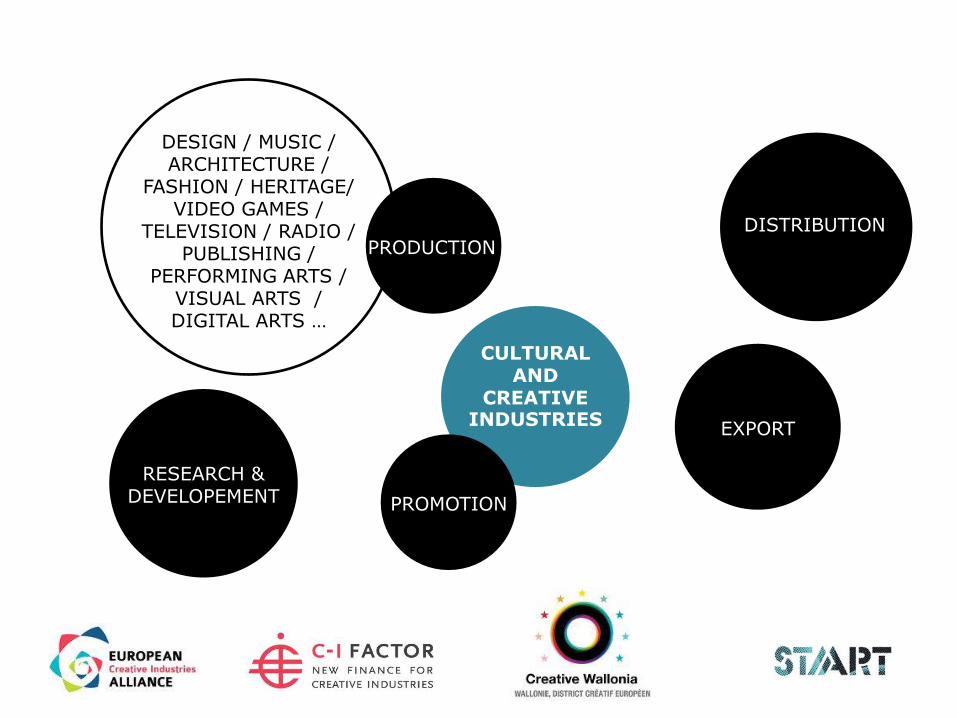

THE INVESTMENT FUND FOR CULTURAL AND CREATIVE INDUSTRIES

ANTOINETTE GODIN – EUROPEAN PROJECT OFFICER

A FEW WORDS ABOUT

…

ECIA Conference on Access to Finance - Barcelona- 5th June 2013

WALLONIA

BRUSSELS

SME’S

CULTURAL AND

CREATIVE INDUSTRIES

16 MILLION EUROS

DESIGN / MUSIC / ARCHITECTURE /

FASHION / HERITAGE/ VIDEO GAMES /

TELEVISION / RADIO / PUBLISHING /

PERFORMING ARTS / VISUAL ARTS / DIGITAL ARTS …

PROMOTION

PRODUCTION

EXPORT

RESEARCH & DEVELOPEMENT

DISTRIBUTION

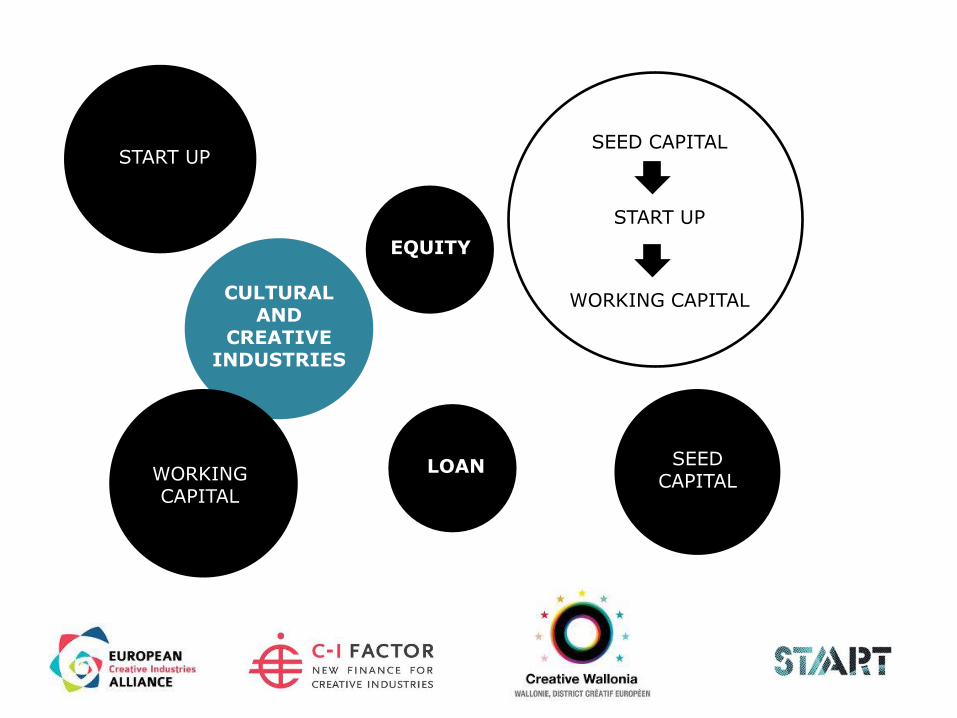

CULTURAL AND

CREATIVE INDUSTRIES

LOAN

EQUITY

SEED CAPITAL WORKING

CAPITAL

START UP

CULTURAL AND

CREATIVE INDUSTRIES

SEED CAPITAL

START UP

WORKING CAPITAL

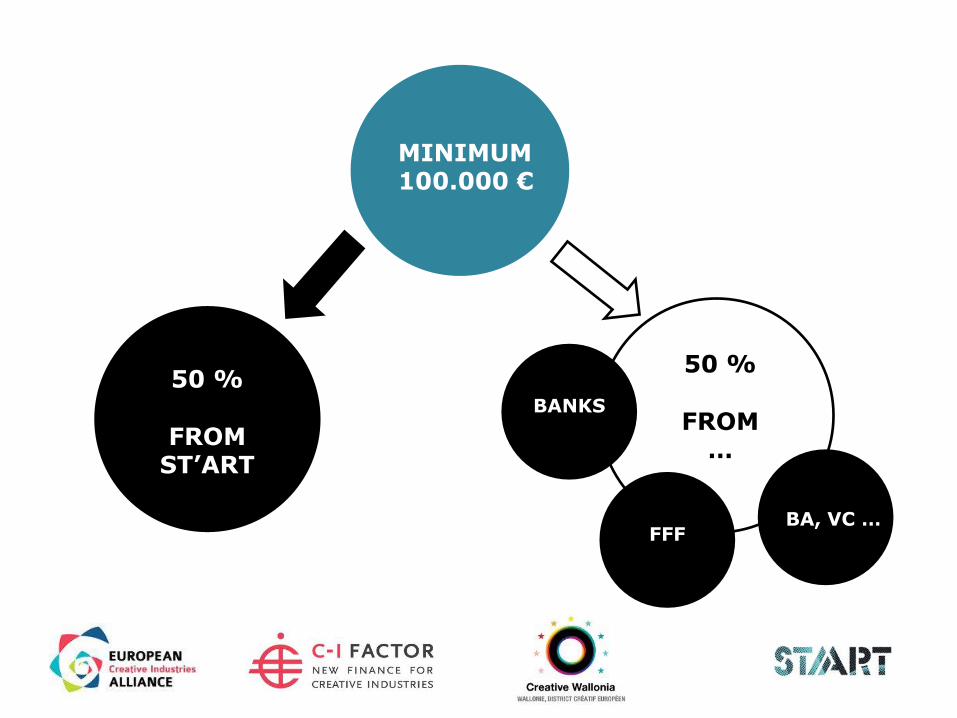

MINIMUM 100.000 €

50 %

FROM ST’ART

50 %

FROM …

BANKS

FFF BA, VC …

EXAMPLES OF

COMPANIES FINANCED BY ST’ART…

COMMUNITY PLATFORM FOR

OMIC PUBLISHING

Productions

du Dragon &

Dragone

Costumes

Sector:

performing

Date:

2001

Fishing Cactus

Sector:

Leisure

Software

Date:

2008

Fishing Cactus

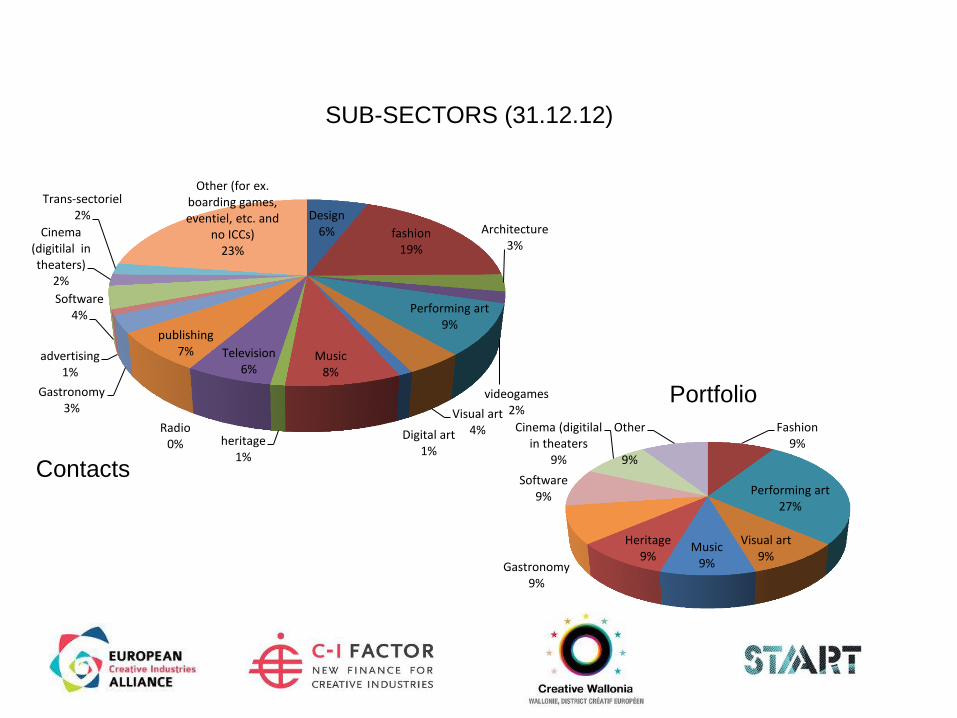

Design 6% fashion

19%

Architecture 3%

videogames 2%

Performing art 9%

Visual art 4% Digital art

1%

Music 8%

heritage 1%

Television 6%

Radio 0%

publishing 7%

Gastronomy 3%

advertising 1%

Software 4%

Cinema (digitilal in theaters)

2%

Trans-sectoriel 2%

Other (for ex. boarding games, eventiel, etc. and

no ICCs) 23%

Fashion 9%

Performing art 27%

Visual art 9%

Music 9%

Heritage 9%

Gastronomy 9%

Software 9%

Cinema (digitilal in theaters

9%

Other

9% Contacts

Portfolio

SUB-SECTORS (31.12.12)

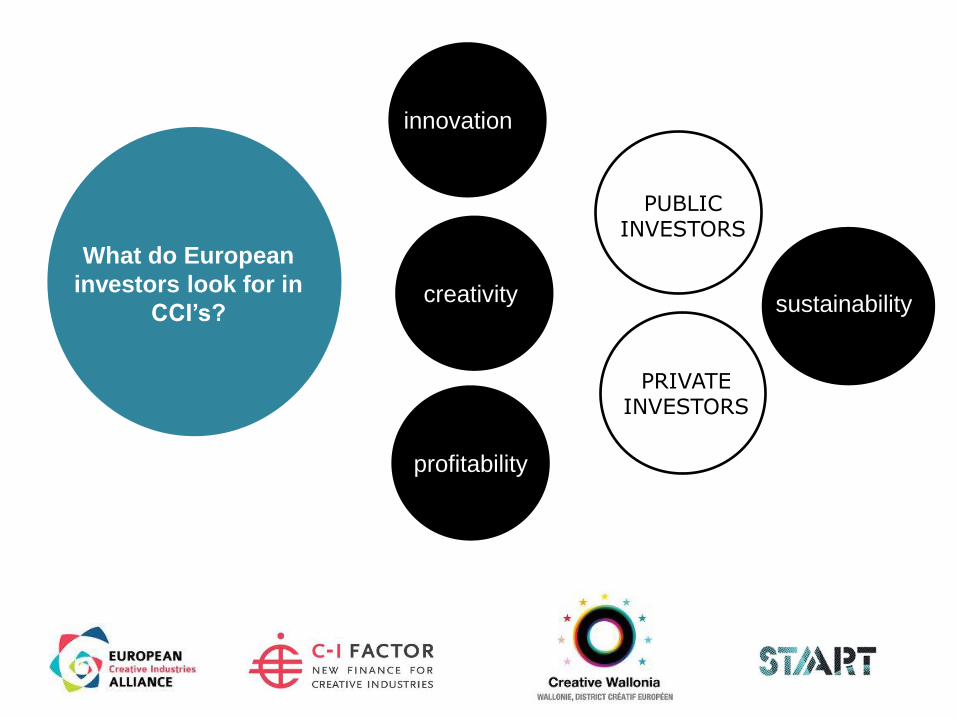

What do European

investors look for in

CCI’s?

innovation

creativity

profitability

PUBLIC INVESTORS

PRIVATE INVESTORS

sustainability

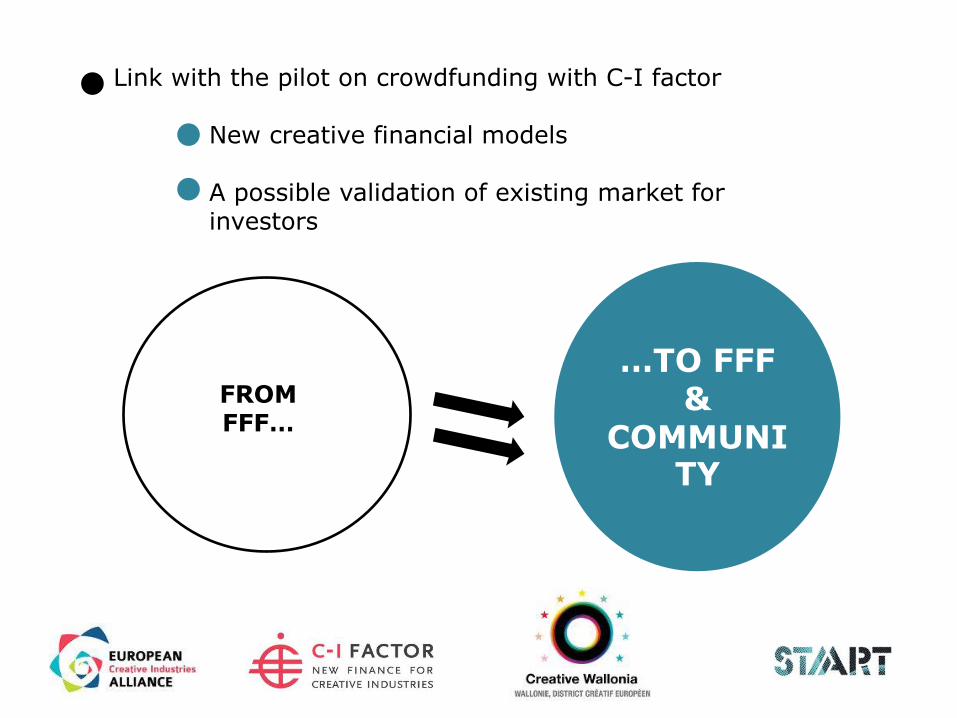

…TO FFF &

COMMUNITY

FROM FFF…

Link with the pilot on crowdfunding with C-I factor New creative financial models A possible validation of existing market for investors

THANKS!

Jose María Pina, Entrepreneurship Director, Keiretsu Forum Barcelona

Anthony Clarke, MD of London Business Angels

Creative Industries: Early Stage Investment

Anthony Clarke

CEO: London Business Angels ( LBA) Director : UKBAA

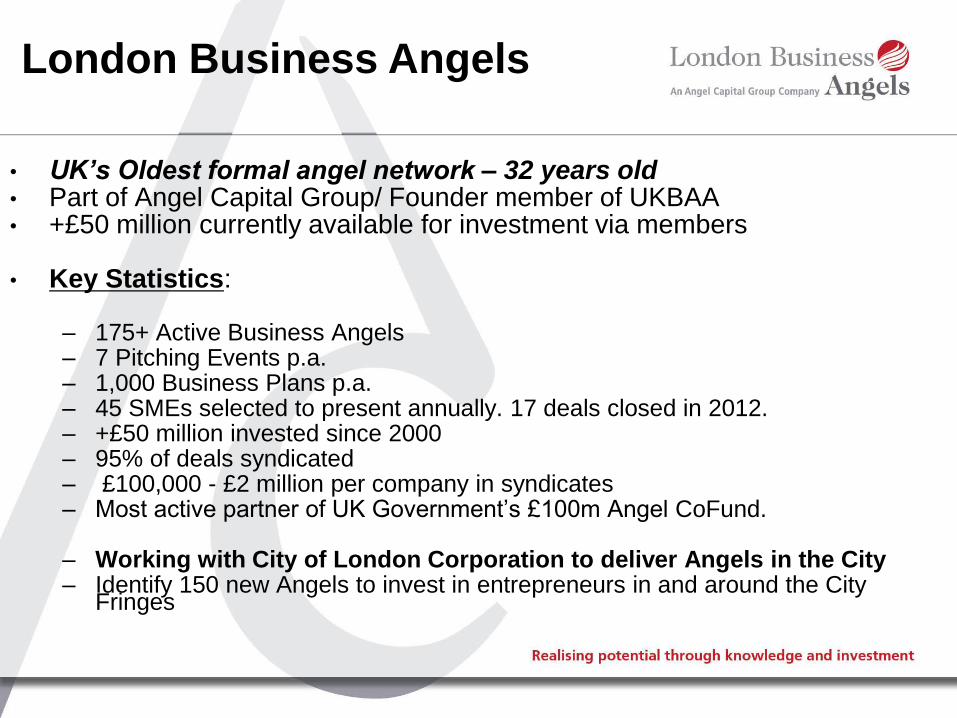

London Business Angels

• UK’s Oldest formal angel network – 32 years old • Part of Angel Capital Group/ Founder member of UKBAA • +£50 million currently available for investment via members

• Key Statistics:

– 175+ Active Business Angels – 7 Pitching Events p.a. – 1,000 Business Plans p.a. – 45 SMEs selected to present annually. 17 deals closed in 2012. – +£50 million invested since 2000 – 95% of deals syndicated – £100,000 - £2 million per company in syndicates – Most active partner of UK Government’s £100m Angel CoFund.

– Working with City of London Corporation to deliver Angels in the City – Identify 150 new Angels to invest in entrepreneurs in and around the City

Fringes

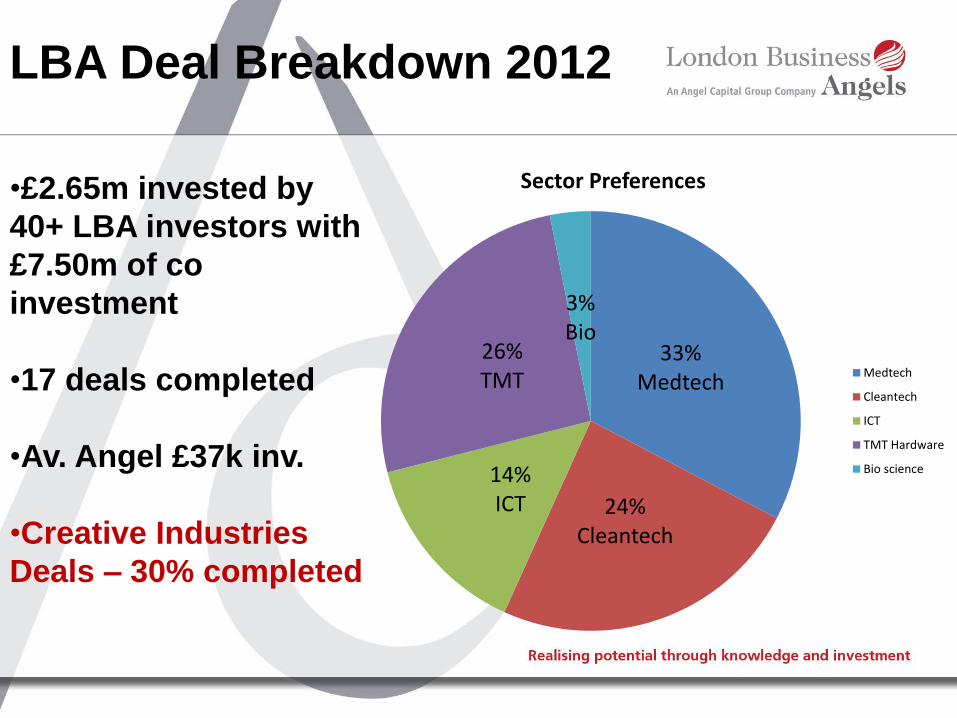

LBA Deal Breakdown 2012

•£2.65m invested by

40+ LBA investors with

£7.50m of co

investment

•17 deals completed

•Av. Angel £37k inv.

•Creative Industries

Deals – 30% completed

33% Medtech

24% Cleantech

14% ICT

26% TMT

3% Bio

Sector Preferences

Medtech

Cleantech

ICT

TMT Hardware

Bio science

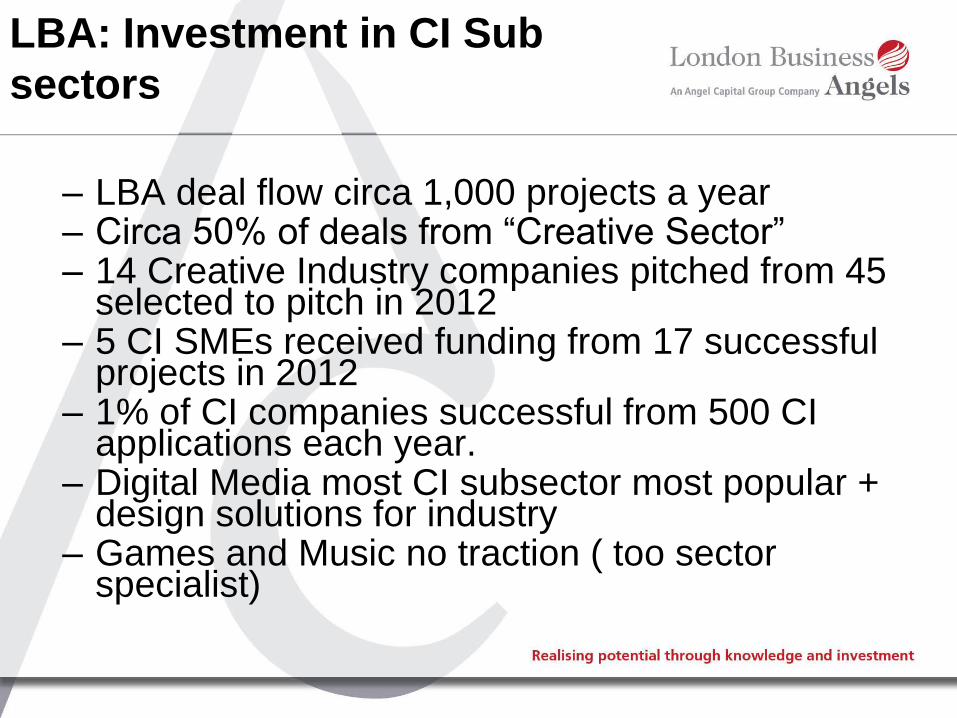

LBA: Investment in CI Sub

sectors

– LBA deal flow circa 1,000 projects a year – Circa 50% of deals from “Creative Sector” – 14 Creative Industry companies pitched from 45

selected to pitch in 2012 – 5 CI SMEs received funding from 17 successful

projects in 2012 – 1% of CI companies successful from 500 CI

applications each year. – Digital Media most CI subsector most popular +

design solutions for industry – Games and Music no traction ( too sector

specialist)

Investment Ready/Attractive?

• Both often a problem given investor “bias”

towards CI sector • Strong in human capital (often not productised) • Low barriers to entry? • Scalability? • Lack of defensive core IP? • Platform viability issues with growing revenues

not just growth in Users • Creative Innovators may lack skill sets to grow

a commercial business

Investors understanding of

Creative Sector?

• Lower initial capital needs of Creative Industry

Sector often not understood – Early Exists? • Early mover advantage • Trade Mark and other IP protection such as

copyright not always understood • Investors skills in strengthening and adding

value to the CI management team often ignored

• More case studies of successful early stage deals

Stimulating Demand/Supply

Side?....... BOTH!

• Sector Specific investment readiness

programmes delivered by industry experts with mentoring support

• More visibility in medis of successful Creative Industry projects from their seed/ early stage

• Angel capacity building focused more towards the CI sector

• Tax breaks for angel investment at seed ( e.g. 50% in the UK for all commercial sectors with 30% post seed)

• Specialist CI Angel Co Investment Funds

Recent CI Funding Case

Studies from LBA

• Orbel Health - £250k • Circalit - £140k • Style on Screen - £150k • Glopho - £150k • Gloople - £150k

Núria Bosch Balada - Board of Directors member at Baring Private Equity Partners

The Views of Investors, both traditional and alternative Finance Sources in Financing Creative Industries Round table - Nuria Bosch conclusions

# 1. How does this research compare with your views on financing of CI businesses? # 2. How much investment are you making in which CI subsectors -‐ and what are you looking for? # 3. Is the problem with the CI Businesses not being Investment ready, or not investor aEracFve? # 4. Or the lack of awareness/interest of investors in financing CI businesses? # 5. What are the right measures to take for the supply and demand side?

Questions for Discussion

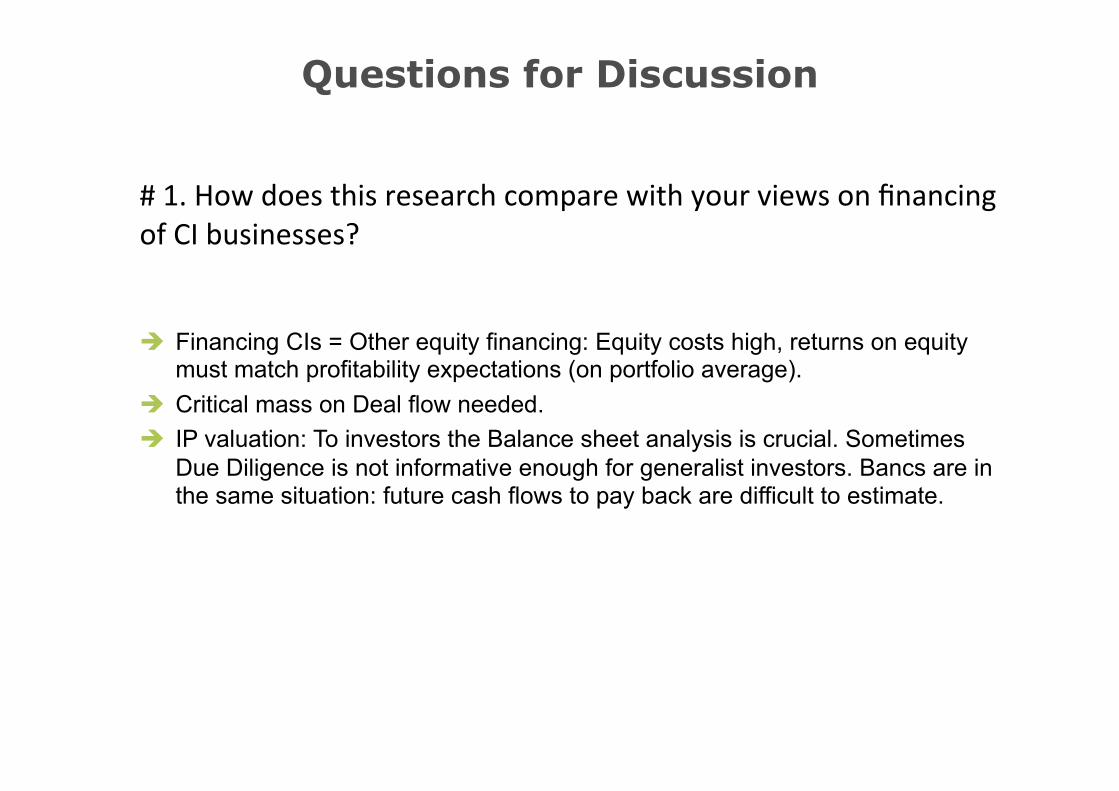

# 1. How does this research compare with your views on financing of CI businesses?

è Financing CIs = Other equity financing: Equity costs high, returns on equity must match profitability expectations (on portfolio average).

è Critical mass on Deal flow needed. è IP valuation: To investors the Balance sheet analysis is crucial. Sometimes

Due Diligence is not informative enough for generalist investors. Bancs are in the same situation: future cash flows to pay back are difficult to estimate.

Questions for Discussion

# 2. How much investment are you making in which CI subsectors -‐ and what are you looking for?

è We are looking for Companies having 3 to 5 m€ on EBITDA è We pay attention to leverage, in order not to enter to a Company with a

reduced value. è We like teams with certain corporate skills (in order to enable buy & build

projects)

Questions for Discussion

# 3. Is the problem with the CI Businesses not being Investment ready, or not investor aEracFve?

è If we could make a second disclosure on your #5 slide, showing Business Models in each sub-sector, probably we could find a certain correlation between non attractive sectors and the use of certain business models.

è Business models as Saas, Long tail, any product large scalability, etc. are interesting because of their profitability, being as growing exponentially.

è Investors try not to invest in one business highly dependent on one sole person, because of the inherent risks.

Questions for Discussion

# 4. Or the lack of awareness/interest of investors in financing CI businesses?

è Investors don’t have any prejudgement. Awareness or interest is raised deal by deal.

è Investors have the profitability pressure from LPs. è The most important amount on funds dedicated to CI as a vertical will come

from nowadays entrepreneurs, once the will exit their Companies.

Questions for Discussion

# 5. What are the right measures to take for the supply and demand side?

è Both sides + governments have to understand the risk – profitability binomial.

è Measures on tax saving always have a return: taxes avoided to investors will enter the system through new business created and unemployment reduction.

è Available spaces (real or virtual) to be able to share languages and increase trust.

Questions for Discussion

Related Documents