Dr. Alex White Ag & Applied Economics [email protected] 540-231-3132 http://faculty.agecon.vt.edu/ alexwhite/

Dr. Alex White Ag & Applied Economics [email protected] 540-231-3132

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Why you need financial statements What financial statements you need Construction of statements

◦ Start-up capital exercise◦ Labor cost exercise◦ Balance sheet exercise

Breakeven analysis Ratio Analysis

Applying for loans◦ Start-up loans, operating loans/lines, etc.

◦ Typical loan application (“loan app”) 2-3 years of balance sheets, income statements

Historical, projected

◦ Impress your lender with: Cash flow statement and breakevens Best/worst case scenarios

Powerful management tools◦ Compare the business to the industry averages◦ Identify strengths/weaknesses of the business◦ Identify trends within the business◦ Identify strategies to improve◦ Enterprise analysis!! (woo hoo!!)

Helps with tax preparation◦ Improved recordkeeping

Balance sheet◦ Listing of what you own and how you paid for it

Assets = Liabilities + Net Worth Value of Assets = Debt financing + “Owner

financing”

◦ Tells lender Liquidity and solvency position Outstanding debts, creditors Assets available for collateral

◦ Not a useful day-to-day tool for managers

Income Statement◦ Shows the economic profit for the period (year)

Revenues – COGS – Overhead = EBT

◦ Cash vs accrual accounting

◦ Lenders & managers use to assess: Profitability, Repayment ability, and Financial

efficiency Breakevens, sensitivity analysis

◦ Retail operations usually do a weekly income statements

Cash Flow Statement (Budget)◦ Shows all cash coming in/going out and the timing

◦ Helps the lender and manager: Estimate cash surplus/deficits for each period Shift the timing of cash flows Determine when to schedule loan payments Determine operating loan needs and terms

◦ IMO – the most powerful statement for managers

Calculate ratios and measures

Compare to benchmarks (RMA, S&P, etc.)◦ Available at libraries

Usually at the reference desk Robert Morris Associates – Annual Statement Studies

Look for trends over time◦ Compare years side-by-side

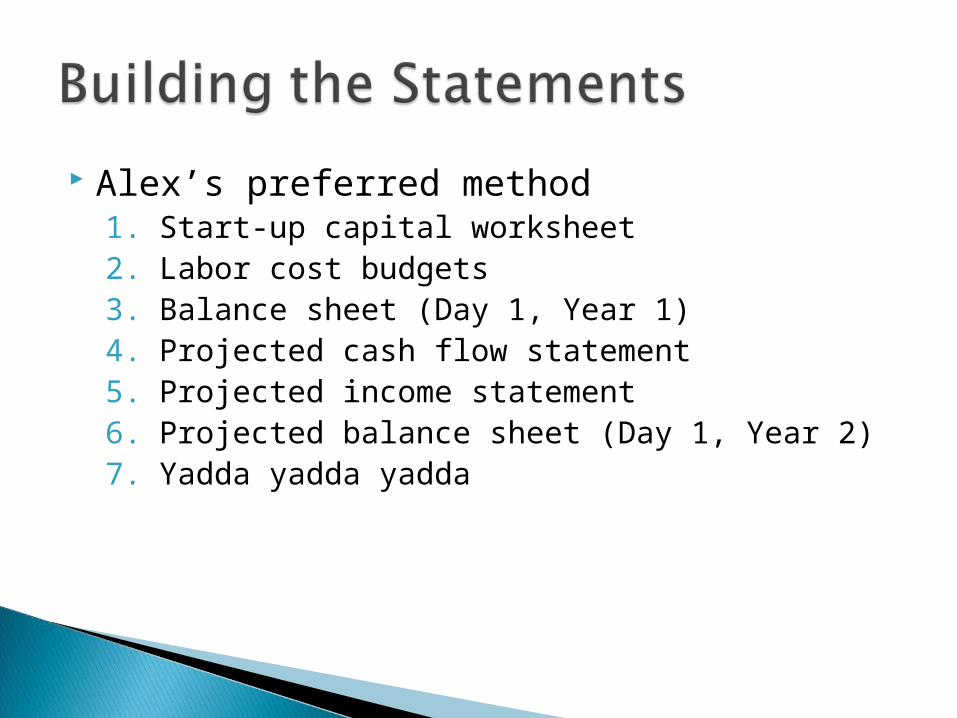

Alex’s preferred method1. Start-up capital worksheet2. Labor cost budgets3. Balance sheet (Day 1, Year 1)4. Projected cash flow statement5. Projected income statement6. Projected balance sheet (Day 1, Year 2)7. Yadda yadda yadda

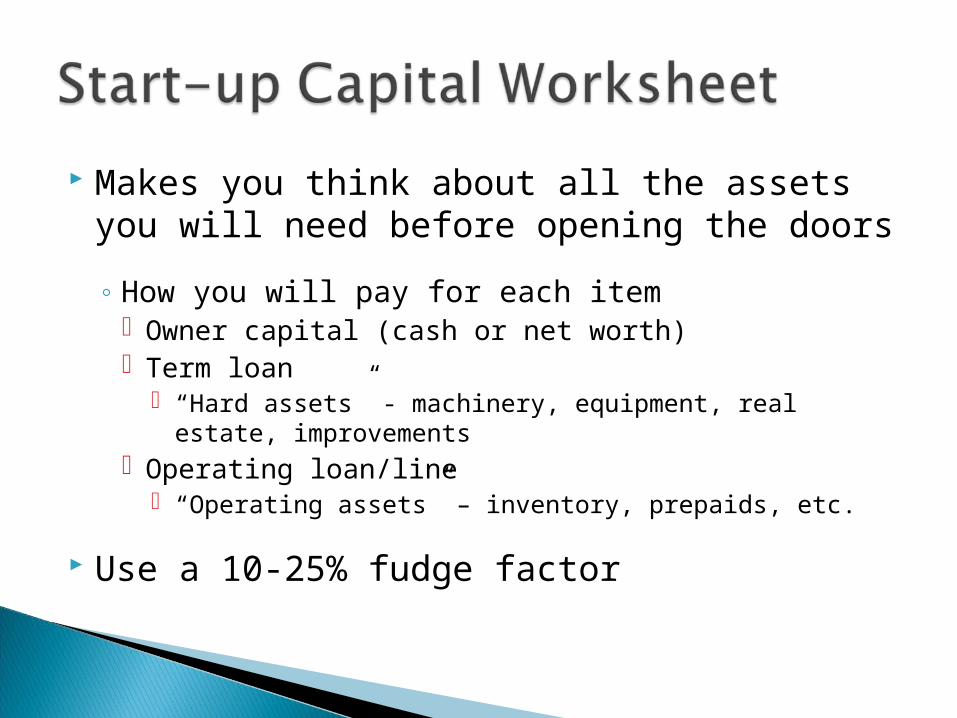

Makes you think about all the assets you will need before opening the doors

◦ How you will pay for each item Owner capital (cash or net worth) Term loan

“Hard assets” - machinery, equipment, real estate, improvements

Operating loan/line “Operating assets” – inventory, prepaids, etc.

Use a 10-25% fudge factor

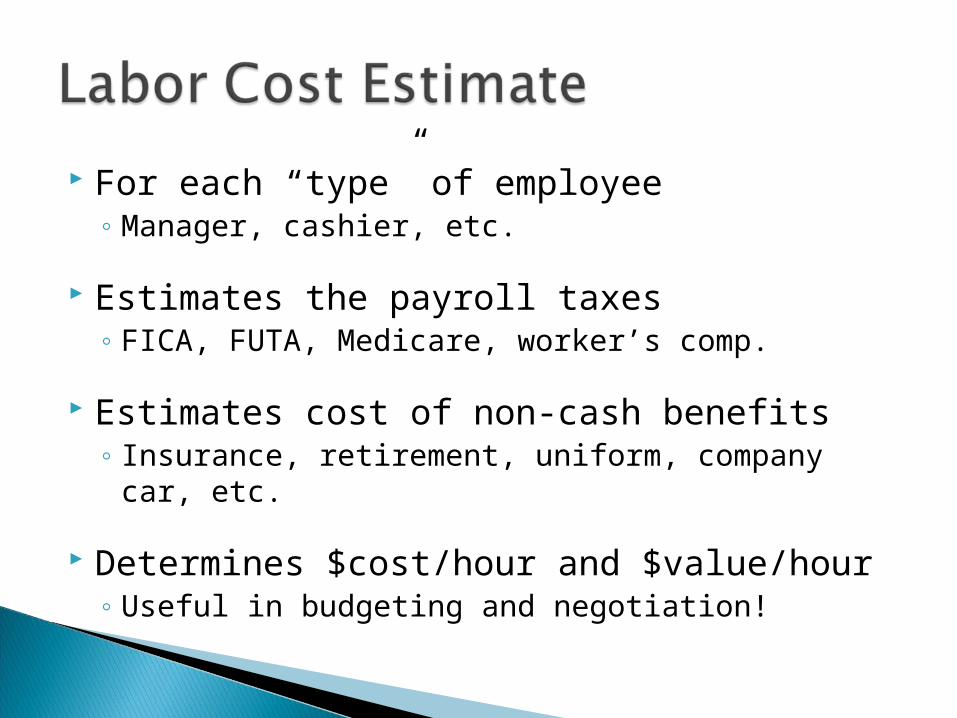

For each “type” of employee◦ Manager, cashier, etc.

Estimates the payroll taxes◦ FICA, FUTA, Medicare, worker’s comp.

Estimates cost of non-cash benefits◦ Insurance, retirement, uniform, company car, etc.

Determines $cost/hour and $value/hour◦ Useful in budgeting and negotiation!

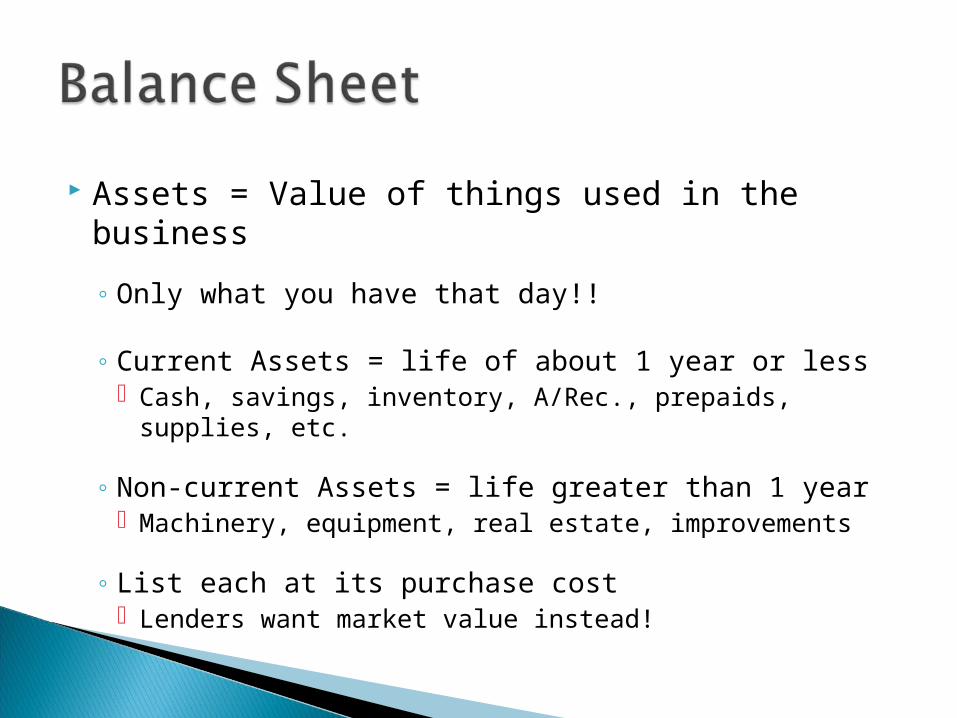

Assets = Value of things used in the business

◦ Only what you have that day!!

◦ Current Assets = life of about 1 year or less Cash, savings, inventory, A/Rec., prepaids, supplies,

etc.

◦ Non-current Assets = life greater than 1 year Machinery, equipment, real estate, improvements

◦ List each at its purchase cost Lenders want market value instead!

Liabilities = what you owe as of that day◦ Current Liabilities = owed within 1 year

Operating loan, A/Pay., principal due, accrued interest ◦ Non-current liabilities = owed AFTER 1 year

Remaining principal balances

◦ List the actual dollar amount owed as of that day

Net Worth = owner’s investment as of that day◦ Original cash invested – withdrawals + additions◦ Retained Earnings ~ net income from previous years

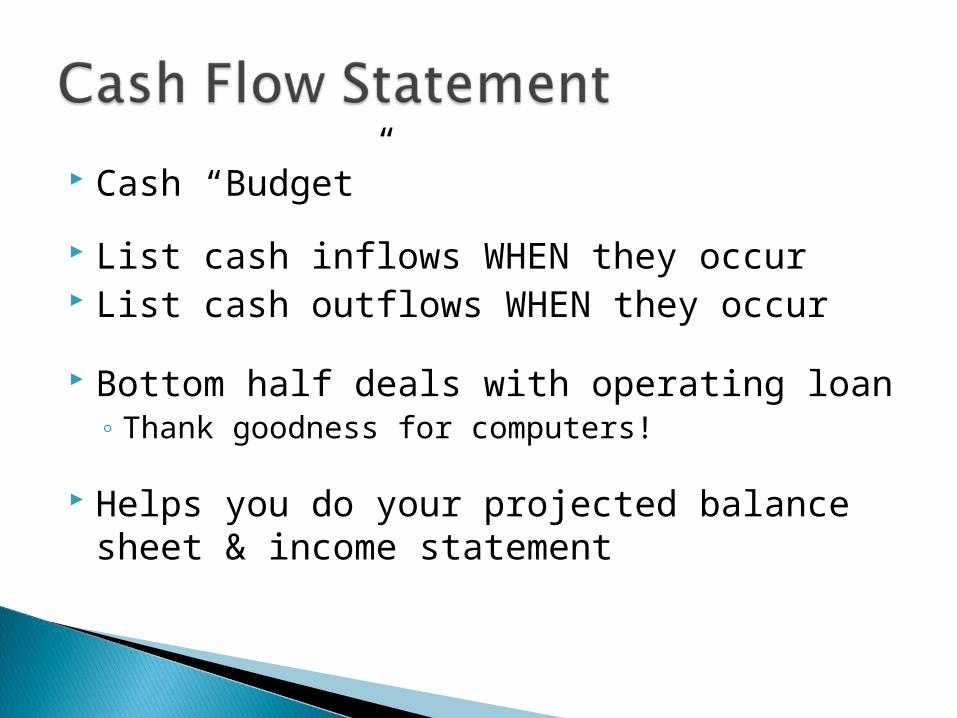

Cash “Budget”

List cash inflows WHEN they occur List cash outflows WHEN they occur

Bottom half deals with operating loan◦ Thank goodness for computers!

Helps you do your projected balance sheet & income statement

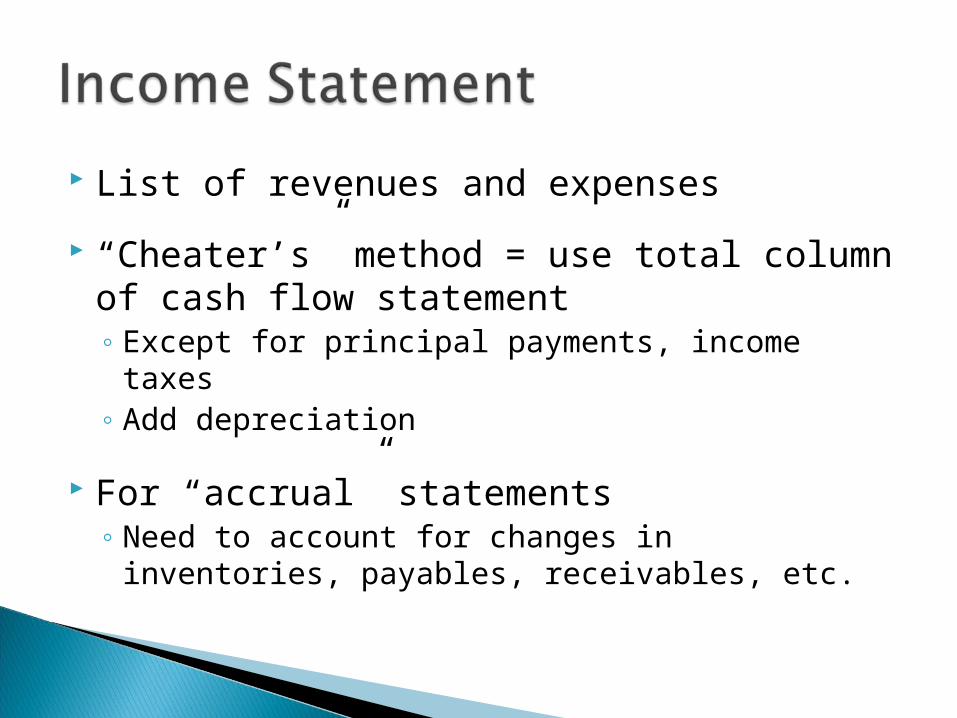

List of revenues and expenses

“Cheater’s” method = use total column of cash flow statement◦ Except for principal payments, income taxes◦ Add depreciation

For “accrual” statements◦ Need to account for changes in inventories,

payables, receivables, etc.

From cash flow stmt◦ Cash balance◦ Operating loan balance & accrued interest

Adjust other asset values as needed◦ Add another year of depreciation on hard assets

From income statement◦ Net income helps determined retained earnings

4-step process for loans

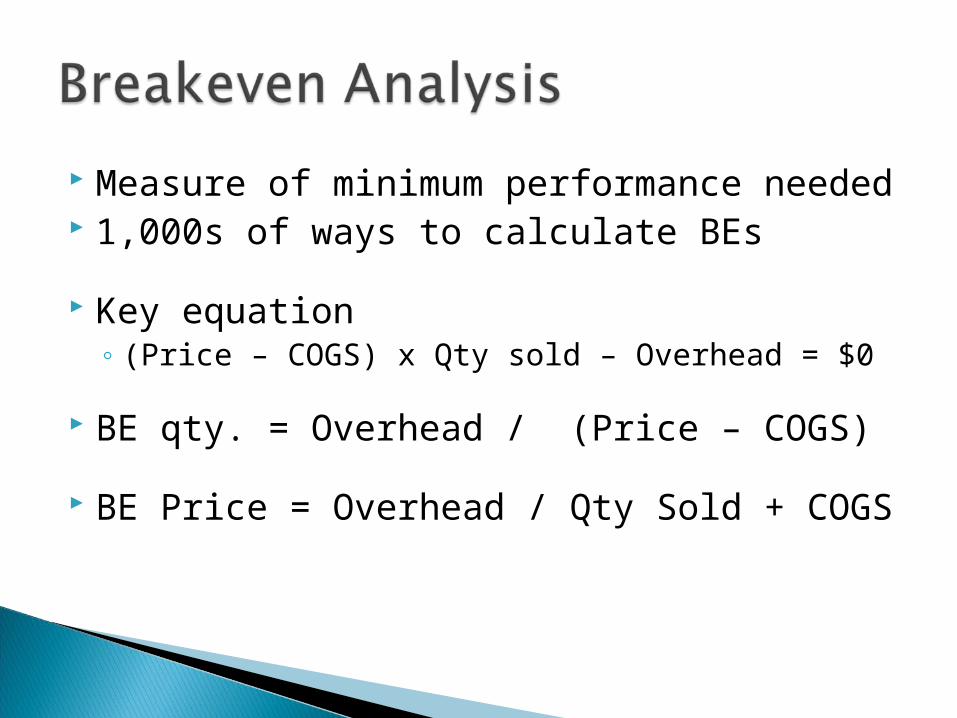

Measure of minimum performance needed 1,000s of ways to calculate BEs

Key equation◦ (Price – COGS) x Qty sold – Overhead = $0

BE qty. = Overhead / (Price – COGS)

BE Price = Overhead / Qty Sold + COGS

RMA Annual Statement Studies◦ Indexed by NAICS codes

By Sales, by Assets, by Year◦ Top, middle, bottom quartiles

Compare ratios to benchmarks

Look for trends over time◦ That’s why lenders want 2-3 years of statements

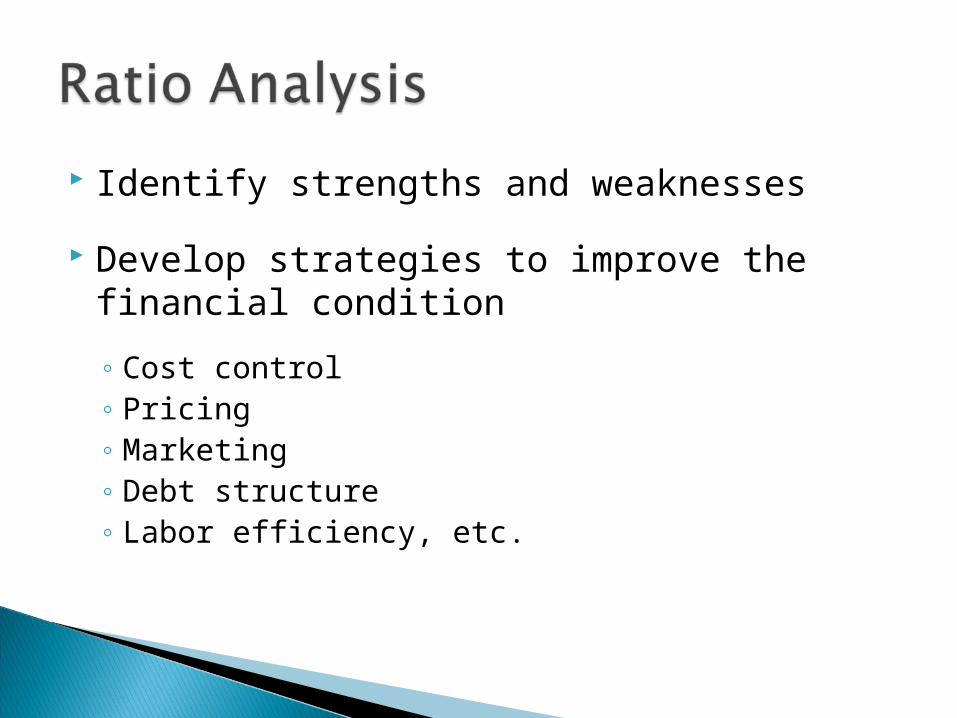

Identify strengths and weaknesses

Develop strategies to improve the financial condition

◦ Cost control◦ Pricing◦ Marketing◦ Debt structure◦ Labor efficiency, etc.

Liquidity – ability to meet current obligations

◦ Current Ratio current assets/current liabilities

◦ Quick Ratio (current asset – inventory)/cur. liab.

Solvency – ability to meet all debts

◦ Debt/Asset total liabilities/total assets

◦ Debt/Worth total liabilities/net worth

Repayment ability◦ EBIT/Interest

EBIT/Interest

◦ Debt Coverage Ratio(EBT + other income + Depreciation + Interest Expense

– Taxes & Family Living) / Annual P&I payments

Profitability◦ ROA EBT/Total Assets

◦ ROE EBT/Net Worth

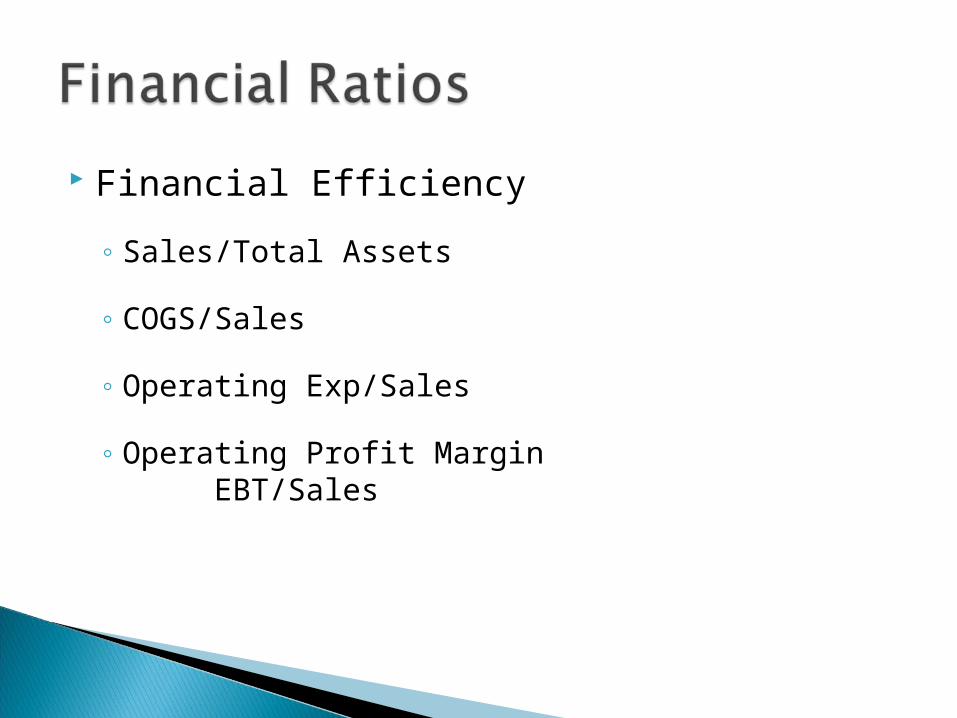

Financial Efficiency

◦ Sales/Total Assets

◦ COGS/Sales

◦ Operating Exp/Sales

◦ Operating Profit Margin EBT/Sales

http://faculty.agecon.vt.edu/alexwhite/

◦ Go to the Small Business tab

◦ Built as a teaching tool for start-up businesses Excel 2003

◦ Can be used for existing businesses

Related Documents