Credit Shocks in an Economy with Heterogeneous Firms and Default by Aubhik Khan, Tatsuro Senga and Julia K. Thomas Discussed by Urban Jermann

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Credit Shocks in an Economywith Heterogeneous Firms and

Defaultby Aubhik Khan, Tatsuro Senga and Julia K. Thomas

Discussed by Urban Jermann

Contribution

I Present GE model with heterogenous firms and default

I Similar objectives as Gomes and Schmid (2010),Arellano, Bai and Kehoe (2012)

I Solve & calibrate the model, and study TFP and creditshocks

I Credit shocks have persistent effects on N, I and GDP

I Slow recovery

I Fluctuations in entry and exit are important

Contribution

I Present GE model with heterogenous firms and defaultI Similar objectives as Gomes and Schmid (2010),Arellano, Bai and Kehoe (2012)

I Solve & calibrate the model, and study TFP and creditshocks

I Credit shocks have persistent effects on N, I and GDP

I Slow recovery

I Fluctuations in entry and exit are important

Contribution

I Present GE model with heterogenous firms and defaultI Similar objectives as Gomes and Schmid (2010),Arellano, Bai and Kehoe (2012)

I Solve & calibrate the model, and study TFP and creditshocks

I Credit shocks have persistent effects on N, I and GDP

I Slow recovery

I Fluctuations in entry and exit are important

Contribution

I Present GE model with heterogenous firms and defaultI Similar objectives as Gomes and Schmid (2010),Arellano, Bai and Kehoe (2012)

I Solve & calibrate the model, and study TFP and creditshocks

I Credit shocks have persistent effects on N, I and GDP

I Slow recovery

I Fluctuations in entry and exit are important

Contribution

I Present GE model with heterogenous firms and defaultI Similar objectives as Gomes and Schmid (2010),Arellano, Bai and Kehoe (2012)

I Solve & calibrate the model, and study TFP and creditshocks

I Credit shocks have persistent effects on N, I and GDPI Slow recovery

I Fluctuations in entry and exit are important

Contribution

I Present GE model with heterogenous firms and defaultI Similar objectives as Gomes and Schmid (2010),Arellano, Bai and Kehoe (2012)

I Solve & calibrate the model, and study TFP and creditshocks

I Credit shocks have persistent effects on N, I and GDPI Slow recovery

I Fluctuations in entry and exit are important

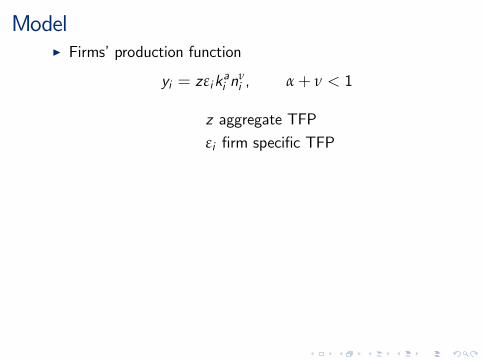

ModelI Firms’production function

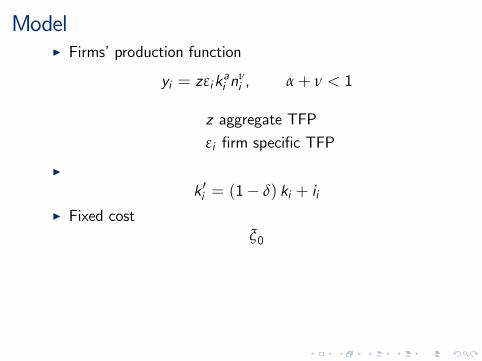

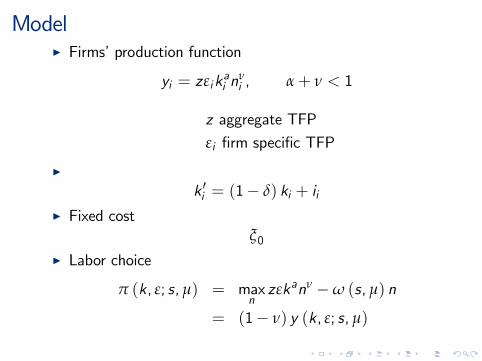

yi = zεikai n

νi , α+ ν < 1

z aggregate TFP

εi firm specific TFP

I

k ′i = (1− δ) ki + iiI Fixed cost

ξ0I Labor choice

π (k, ε; s, µ) = maxnzεkanν −ω (s, µ) n

= (1− ν) y (k, ε; s, µ)

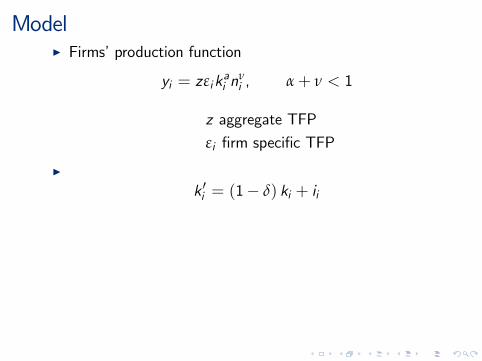

ModelI Firms’production function

yi = zεikai n

νi , α+ ν < 1

z aggregate TFP

εi firm specific TFP

I

k ′i = (1− δ) ki + ii

I Fixed costξ0

I Labor choice

π (k, ε; s, µ) = maxnzεkanν −ω (s, µ) n

= (1− ν) y (k, ε; s, µ)

ModelI Firms’production function

yi = zεikai n

νi , α+ ν < 1

z aggregate TFP

εi firm specific TFP

I

k ′i = (1− δ) ki + iiI Fixed cost

ξ0

I Labor choice

π (k, ε; s, µ) = maxnzεkanν −ω (s, µ) n

= (1− ν) y (k, ε; s, µ)

ModelI Firms’production function

yi = zεikai n

νi , α+ ν < 1

z aggregate TFP

εi firm specific TFP

I

k ′i = (1− δ) ki + iiI Fixed cost

ξ0I Labor choice

π (k, ε; s, µ) = maxnzεkanν −ω (s, µ) n

= (1− ν) y (k, ε; s, µ)

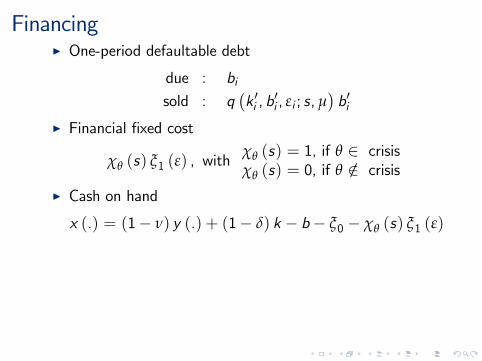

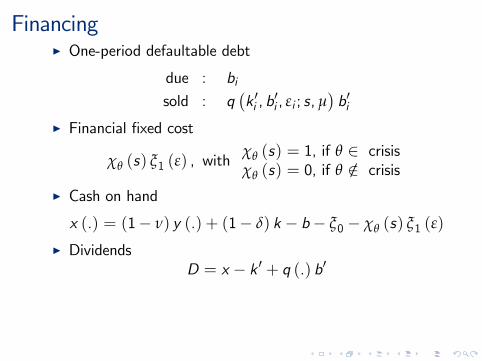

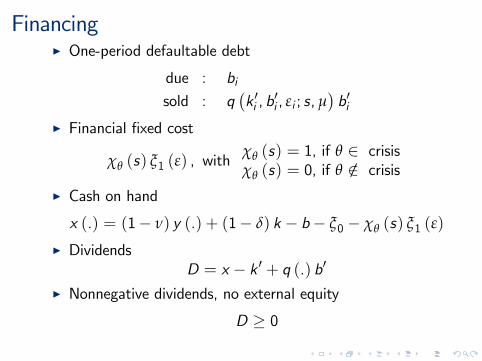

FinancingI One-period defaultable debt

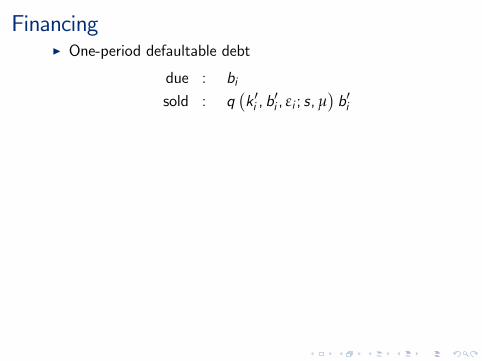

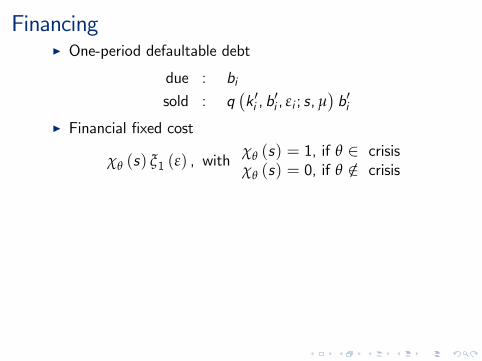

due : bisold : q

(k ′i , b

′i , εi ; s, µ

)b′i

I Financial fixed cost

χθ (s) ξ1 (ε) , withχθ (s) = 1, if θ ∈ crisisχθ (s) = 0, if θ /∈ crisis

I Cash on hand

x (.) = (1− ν) y (.) + (1− δ) k − b− ξ0 − χθ (s) ξ1 (ε)

I DividendsD = x − k ′ + q (.) b′

I Nonnegative dividends, no external equity

D ≥ 0

FinancingI One-period defaultable debt

due : bisold : q

(k ′i , b

′i , εi ; s, µ

)b′i

I Financial fixed cost

χθ (s) ξ1 (ε) , withχθ (s) = 1, if θ ∈ crisisχθ (s) = 0, if θ /∈ crisis

I Cash on hand

x (.) = (1− ν) y (.) + (1− δ) k − b− ξ0 − χθ (s) ξ1 (ε)

I DividendsD = x − k ′ + q (.) b′

I Nonnegative dividends, no external equity

D ≥ 0

FinancingI One-period defaultable debt

due : bisold : q

(k ′i , b

′i , εi ; s, µ

)b′i

I Financial fixed cost

χθ (s) ξ1 (ε) , withχθ (s) = 1, if θ ∈ crisisχθ (s) = 0, if θ /∈ crisis

I Cash on hand

x (.) = (1− ν) y (.) + (1− δ) k − b− ξ0 − χθ (s) ξ1 (ε)

I DividendsD = x − k ′ + q (.) b′

I Nonnegative dividends, no external equity

D ≥ 0

FinancingI One-period defaultable debt

due : bisold : q

(k ′i , b

′i , εi ; s, µ

)b′i

I Financial fixed cost

χθ (s) ξ1 (ε) , withχθ (s) = 1, if θ ∈ crisisχθ (s) = 0, if θ /∈ crisis

I Cash on hand

x (.) = (1− ν) y (.) + (1− δ) k − b− ξ0 − χθ (s) ξ1 (ε)

I DividendsD = x − k ′ + q (.) b′

I Nonnegative dividends, no external equity

D ≥ 0

FinancingI One-period defaultable debt

due : bisold : q

(k ′i , b

′i , εi ; s, µ

)b′i

I Financial fixed cost

χθ (s) ξ1 (ε) , withχθ (s) = 1, if θ ∈ crisisχθ (s) = 0, if θ /∈ crisis

I Cash on hand

x (.) = (1− ν) y (.) + (1− δ) k − b− ξ0 − χθ (s) ξ1 (ε)

I DividendsD = x − k ′ + q (.) b′

I Nonnegative dividends, no external equity

D ≥ 0

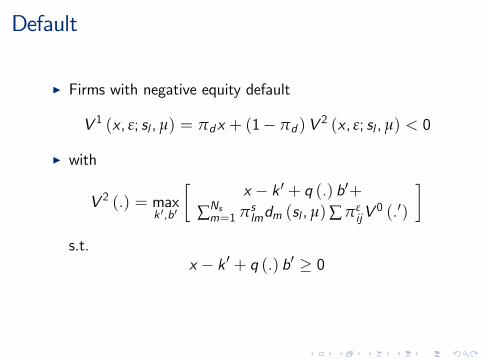

Default

I Firms with negative equity default

V 1 (x, ε; sl , µ) = πdx + (1− πd )V2 (x, ε; sl , µ) < 0

I with

V 2 (.) = maxk ′,b′

[x − k ′ + q (.) b′+

∑Nsm=1 πslmdm (sl , µ)∑ πε

ijV0 (.′)

]s.t.

x − k ′ + q (.) b′ ≥ 0

Default

I Firms with negative equity default

V 1 (x, ε; sl , µ) = πdx + (1− πd )V2 (x, ε; sl , µ) < 0

I with

V 2 (.) = maxk ′,b′

[x − k ′ + q (.) b′+

∑Nsm=1 πslmdm (sl , µ)∑ πε

ijV0 (.′)

]s.t.

x − k ′ + q (.) b′ ≥ 0

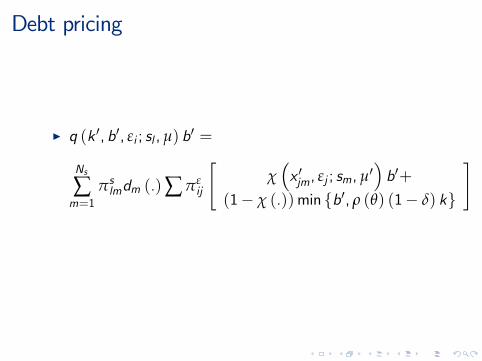

Debt pricing

I q (k ′, b′, εi ; sl , µ) b′ =

Ns

∑m=1

πslmdm (.)∑ πεij

[χ(x ′jm, εj ; sm, µ

′)b′+

(1− χ (.))min {b′, ρ (θ) (1− δ) k}

]

Frictions in the model

I Default cost

I Nonnegative dividends / no equity injectionI Financial (crisis) fixed cost χθ (s) ξ1 (ε)

I Exit & entry

Frictions in the model

I Default costI Nonnegative dividends / no equity injection

I Financial (crisis) fixed cost χθ (s) ξ1 (ε)

I Exit & entry

Frictions in the model

I Default costI Nonnegative dividends / no equity injectionI Financial (crisis) fixed cost χθ (s) ξ1 (ε)

I Exit & entry

Frictions in the model

I Default costI Nonnegative dividends / no equity injectionI Financial (crisis) fixed cost χθ (s) ξ1 (ε)

I Exit & entry

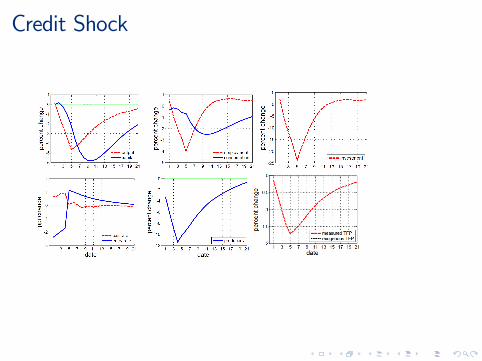

Credit Shock

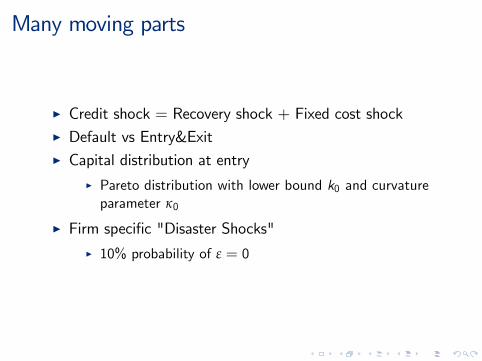

Many moving parts

I Credit shock = Recovery shock + Fixed cost shock

I Default vs Entry&ExitI Capital distribution at entry

I Pareto distribution with lower bound k0 and curvatureparameter κ0

I Firm specific "Disaster Shocks"

I 10% probability of ε = 0

Many moving parts

I Credit shock = Recovery shock + Fixed cost shockI Default vs Entry&Exit

I Capital distribution at entry

I Pareto distribution with lower bound k0 and curvatureparameter κ0

I Firm specific "Disaster Shocks"

I 10% probability of ε = 0

Many moving parts

I Credit shock = Recovery shock + Fixed cost shockI Default vs Entry&ExitI Capital distribution at entry

I Pareto distribution with lower bound k0 and curvatureparameter κ0

I Firm specific "Disaster Shocks"

I 10% probability of ε = 0

Many moving parts

I Credit shock = Recovery shock + Fixed cost shockI Default vs Entry&ExitI Capital distribution at entry

I Pareto distribution with lower bound k0 and curvatureparameter κ0

I Firm specific "Disaster Shocks"

I 10% probability of ε = 0

Many moving parts

I Credit shock = Recovery shock + Fixed cost shockI Default vs Entry&ExitI Capital distribution at entry

I Pareto distribution with lower bound k0 and curvatureparameter κ0

I Firm specific "Disaster Shocks"

I 10% probability of ε = 0

Many moving parts

I Credit shock = Recovery shock + Fixed cost shockI Default vs Entry&ExitI Capital distribution at entry

I Pareto distribution with lower bound k0 and curvatureparameter κ0

I Firm specific "Disaster Shocks"I 10% probability of ε = 0

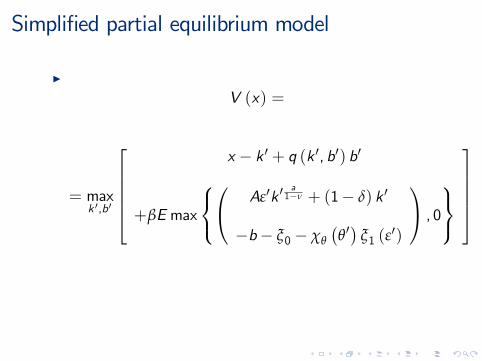

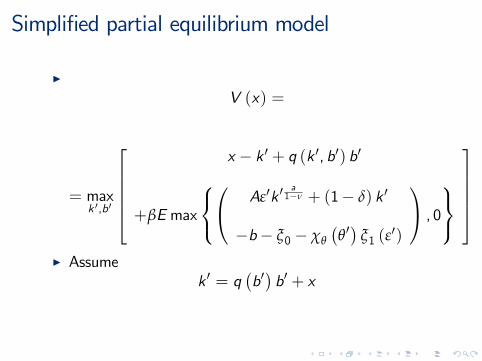

Simplified partial equilibrium model

I

V (x) =

= maxk ′,b′

x − k ′ + q (k ′, b′) b′

+βE max

Aε′k ′

a1−ν + (1− δ) k ′

−b− ξ0 − χθ

(θ′)

ξ1 (ε′)

, 0

I Assumek ′ = q

(b′)b′ + x

Simplified partial equilibrium model

I

V (x) =

= maxk ′,b′

x − k ′ + q (k ′, b′) b′

+βE max

Aε′k ′

a1−ν + (1− δ) k ′

−b− ξ0 − χθ

(θ′)

ξ1 (ε′)

, 0

I Assume

k ′ = q(b′)b′ + x

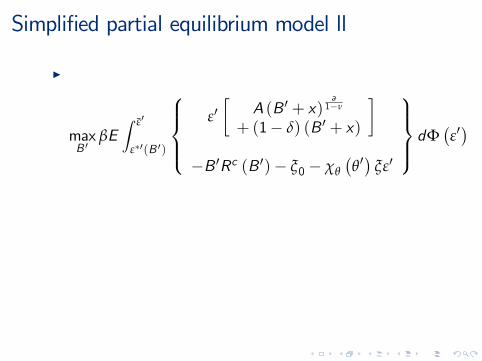

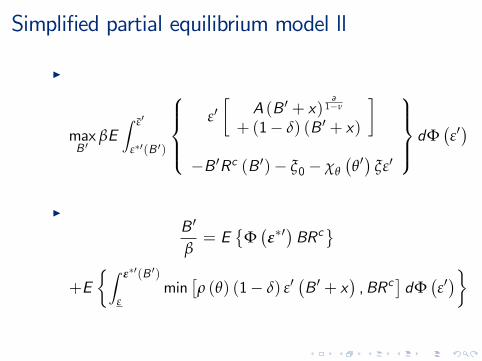

Simplified partial equilibrium model ll

I

maxB ′

βE∫ ε̄′

ε∗′(B ′)

ε′[

A (B ′ + x)a1−ν

+ (1− δ) (B ′ + x)

]−B ′Rc (B ′)− ξ0 − χθ

(θ′)

ξε′

dΦ(ε′)

IB ′

β= E

{Φ(ε∗′)BRc

}+E

{∫ ε∗′(B ′)

εmin

[ρ (θ) (1− δ) ε′

(B ′ + x

),BRc

]dΦ

(ε′)}

Simplified partial equilibrium model ll

I

maxB ′

βE∫ ε̄′

ε∗′(B ′)

ε′[

A (B ′ + x)a1−ν

+ (1− δ) (B ′ + x)

]−B ′Rc (B ′)− ξ0 − χθ

(θ′)

ξε′

dΦ(ε′)

IB ′

β= E

{Φ(ε∗′)BRc

}+E

{∫ ε∗′(B ′)

εmin

[ρ (θ) (1− δ) ε′

(B ′ + x

),BRc

]dΦ

(ε′)}

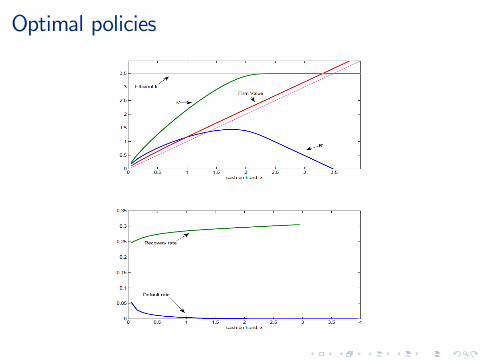

Optimal policies

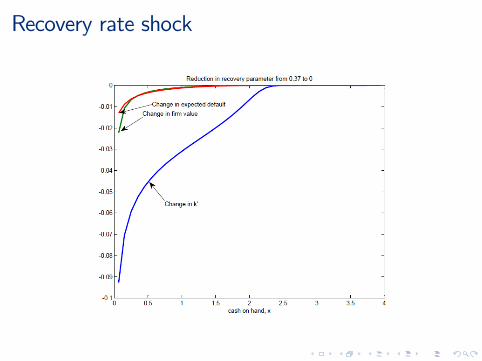

Recovery rate shock

Recovery rate shock with lower interest rate

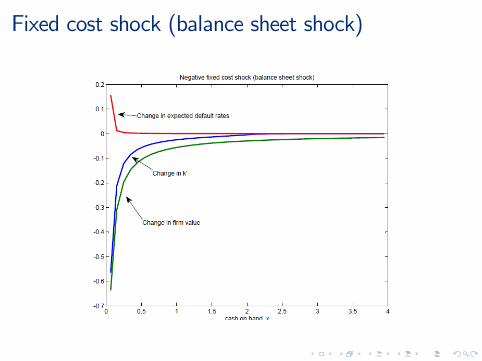

Fixed cost shock (balance sheet shock)

Conclusion

I Progress: GE with default and heterogenous firms

I I would like

I tighter calibration and more clarityI more explicit empirical evaluation

Conclusion

I Progress: GE with default and heterogenous firmsI I would like

I tighter calibration and more clarityI more explicit empirical evaluation

Conclusion

I Progress: GE with default and heterogenous firmsI I would like

I tighter calibration and more clarity

I more explicit empirical evaluation

Conclusion

I Progress: GE with default and heterogenous firmsI I would like

I tighter calibration and more clarityI more explicit empirical evaluation

Related Documents