CPE 15: CPE 15: Budget and Tax Update – Budget and Tax Update – 2006 2006 “This is the year of plenty, when all South Africans will reap the fruits of economic growth.” Trevor Manual

CPE 15: Budget and Tax Update – 2006 “This is the year of plenty, when all South Africans will reap the fruits of economic growth.” Trevor Manual.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CPE 15:CPE 15:

Budget and Tax Budget and Tax Update – 2006Update – 2006

“This is the year of plenty, when all South Africans will reap the fruits of economic

growth.”Trevor Manual

2

Objectives

To obtain and understanding of the 2006 budget reforms and its impact on the taxation of individuals and

companies in South Africa

3

Contents Module 1:Module 1: 2006 Budget Review2006 Budget Review Module 2:Module 2: Income Tax for individualsIncome Tax for individuals Module 3:Module 3: Fringe benefitsFringe benefits Module 4:Module 4: Capital Gains Tax, Capital Gains Tax,

Donations Tax & Estate Donations Tax & Estate DutyDuty

Module 5:Module 5: Company TaxCompany Tax Module 6:Module 6: Value Added TaxValue Added Tax Module 7:Module 7: Capital AllowancesCapital Allowances Module 8:Module 8: Sundry Tax MattersSundry Tax Matters

4

Module 1

Budget Review: 2006

5

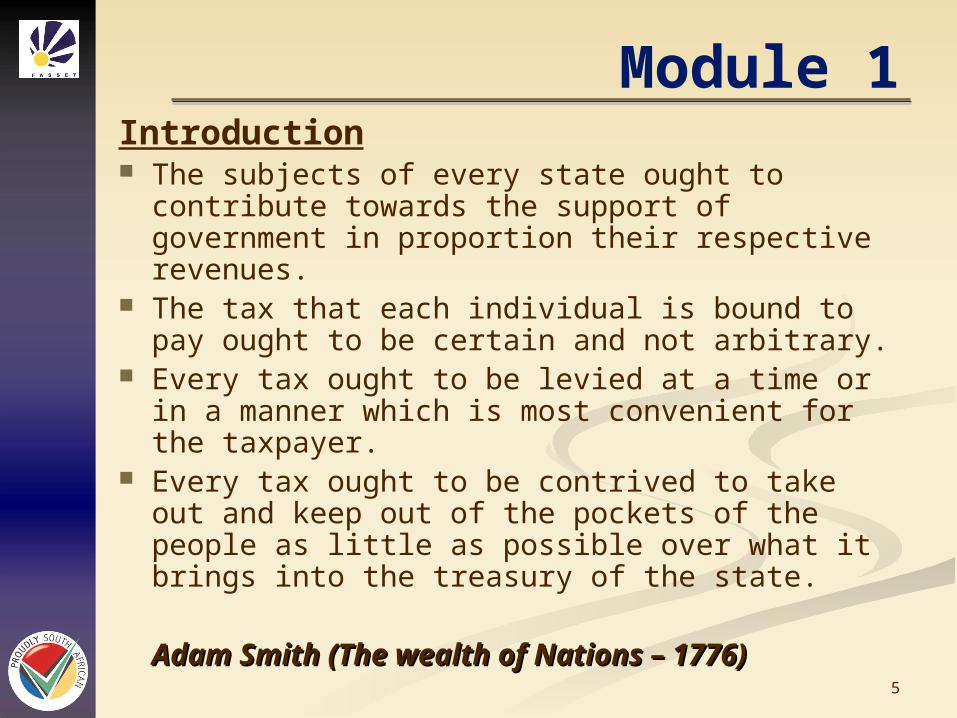

Module 1Introduction The subjects of every state ought to

contribute towards the support of government in proportion their respective revenues.

The tax that each individual is bound to pay ought to be certain and not arbitrary.

Every tax ought to be levied at a time or in a manner which is most convenient for the taxpayer.

Every tax ought to be contrived to take out and keep out of the pockets of the people as little as possible over what it brings into the treasury of the state.

Adam Smith (The wealth of Nations – 1776)Adam Smith (The wealth of Nations – 1776)

6

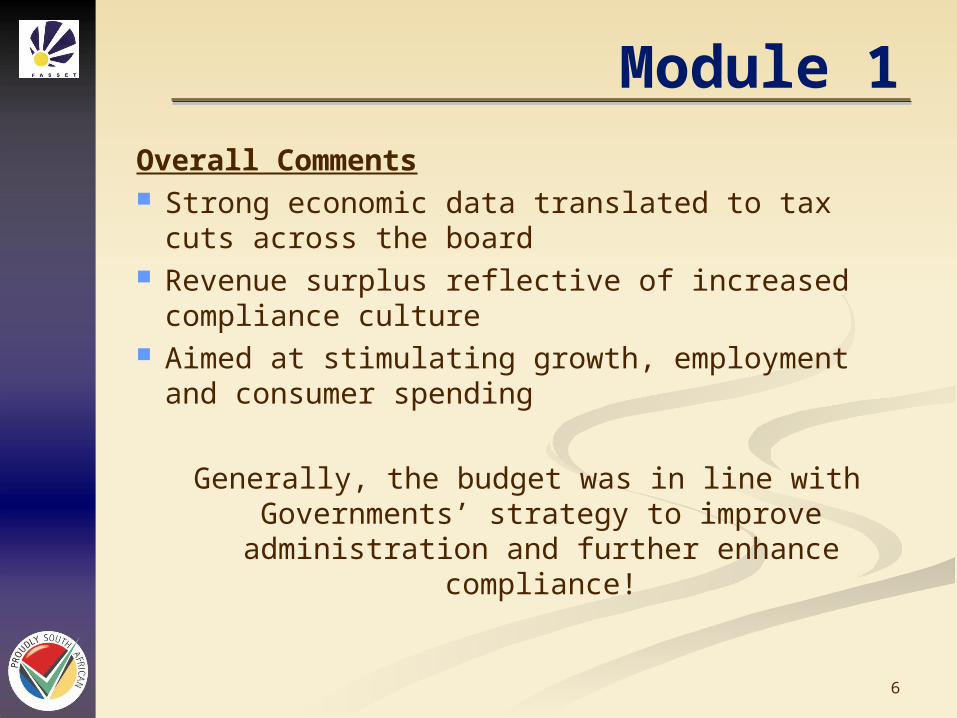

Module 1Overall Comments Strong economic data translated to tax cuts

across the board Revenue surplus reflective of increased

compliance culture Aimed at stimulating growth, employment and

consumer spending

Generally, the budget was in line with Governments’ strategy to improve

administration and further enhance compliance!

7

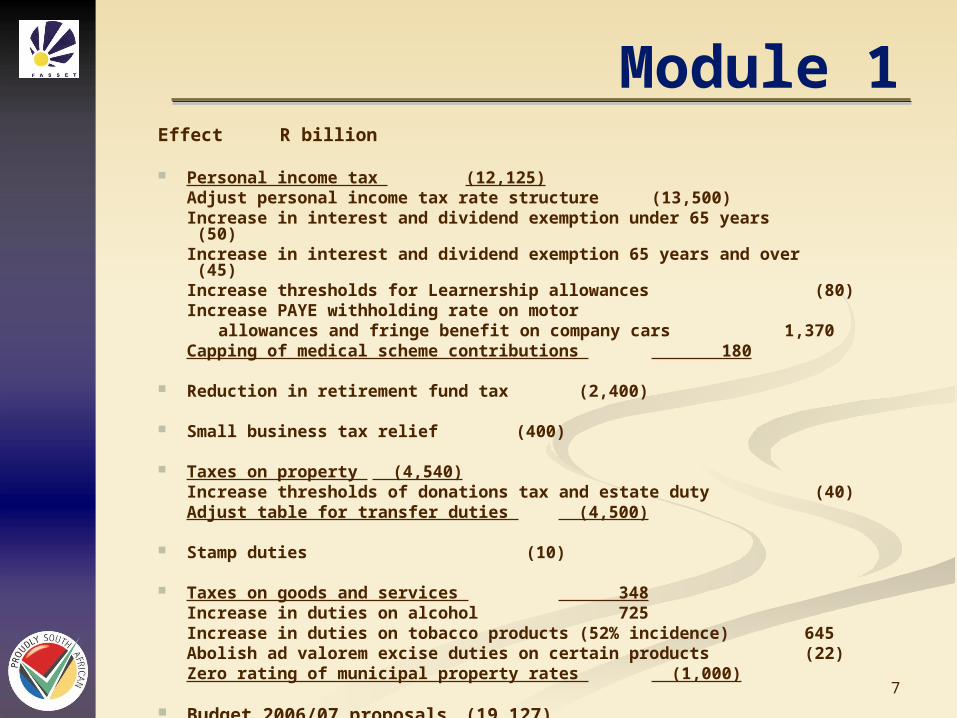

Module 1Effect R billion

Personal income tax (12,125)Adjust personal income tax rate structure (13,500)Increase in interest and dividend exemption under 65 years (50)Increase in interest and dividend exemption 65 years and over (45)Increase thresholds for Learnership allowances (80)Increase PAYE withholding rate on motor

allowances and fringe benefit on company cars 1,370Capping of medical scheme contributions 180

Reduction in retirement fund tax (2,400)

Small business tax relief (400)

Taxes on property (4,540)Increase thresholds of donations tax and estate duty (40)Adjust table for transfer duties (4,500)

Stamp duties (10)

Taxes on goods and services 348Increase in duties on alcohol 725Increase in duties on tobacco products (52% incidence) 645Abolish ad valorem excise duties on certain products (22)Zero rating of municipal property rates (1,000)

Budget 2006/07 proposals (19,127)

8

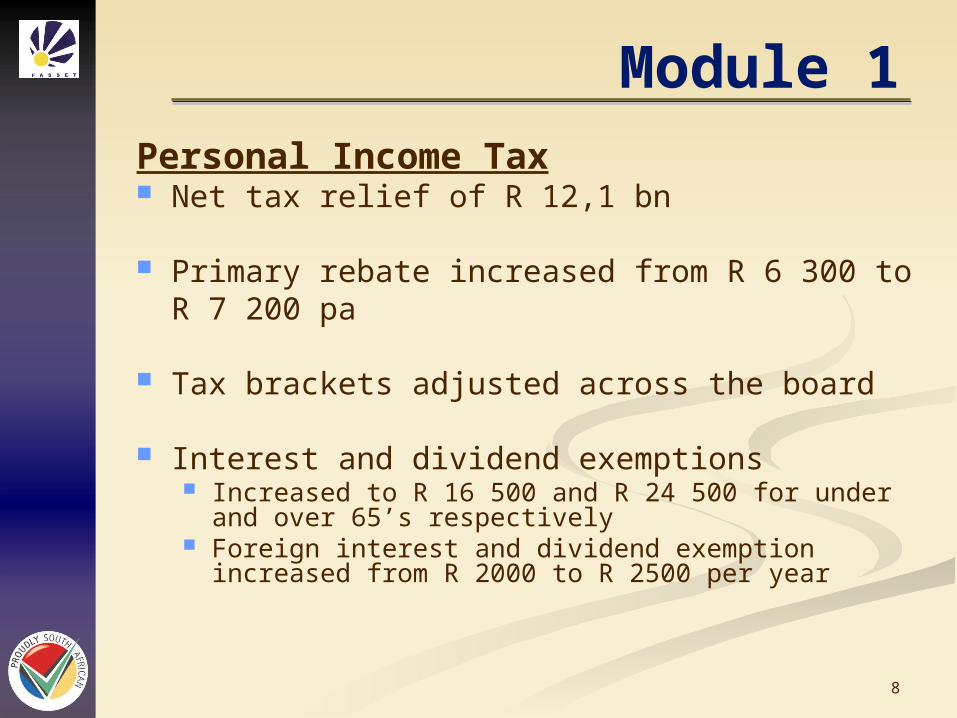

Module 1Personal Income Tax Net tax relief of R 12,1 bn

Primary rebate increased from R 6 300 to R 7 200 pa

Tax brackets adjusted across the board

Interest and dividend exemptions Increased to R 16 500 and R 24 500 for under and

over 65’s respectively Foreign interest and dividend exemption increased

from R 2000 to R 2500 per year

9

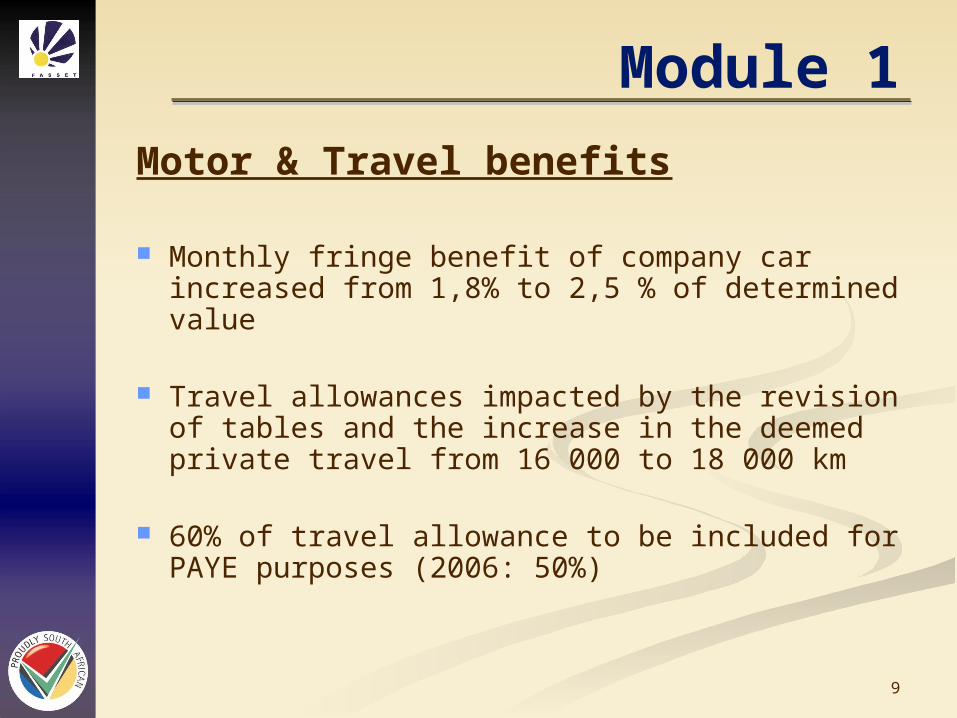

Module 1

Motor & Travel benefits

Monthly fringe benefit of company car increased from 1,8% to 2,5 % of determined value

Travel allowances impacted by the revision of tables and the increase in the deemed private travel from 16 000 to 18 000 km

60% of travel allowance to be included for PAYE purposes (2006: 50%)

10

Module 1

Medical expenses

Monthly caps introduced for medical aid contributions:- R 500 pm for member- R 500 pm for 1st dependent- R 300 pm for each further dep.Any excess above the threshold is taxed as a fringe benefit

Medical expenses may only be claimed to the extent that it exceeds 7,5% of taxable income (previously 5%)

11

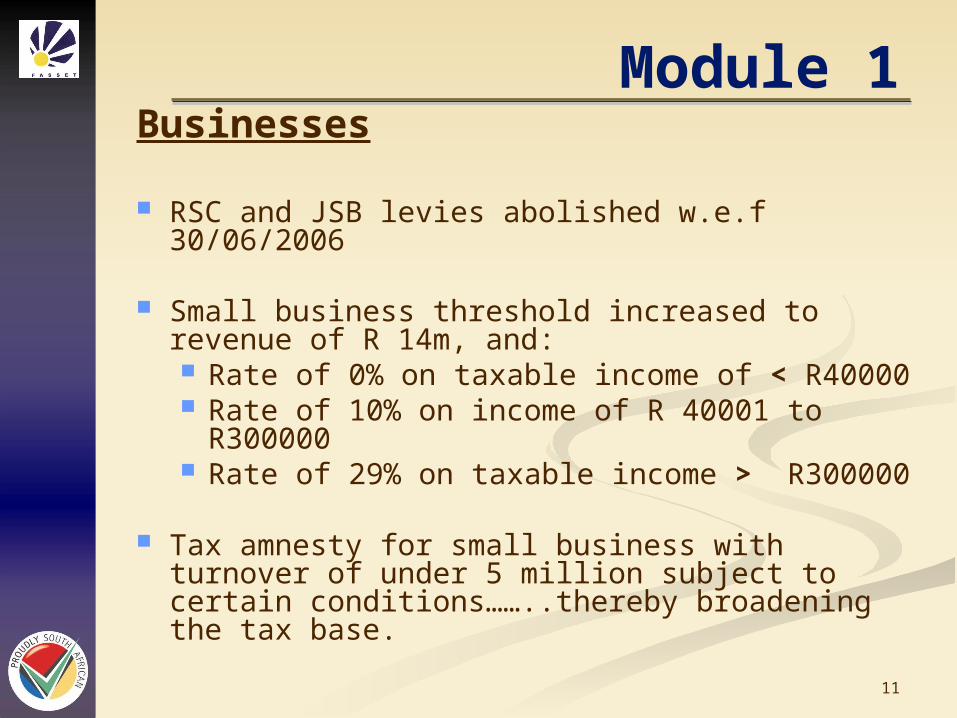

Module 1Businesses

RSC and JSB levies abolished w.e.f 30/06/2006

Small business threshold increased to revenue of R 14m, and: Rate of 0% on taxable income of < R40000 Rate of 10% on income of R 40001 to

R300000 Rate of 29% on taxable income > R300000

Tax amnesty for small business with turnover of under 5 million subject to certain conditions……..thereby broadening the tax base.

12

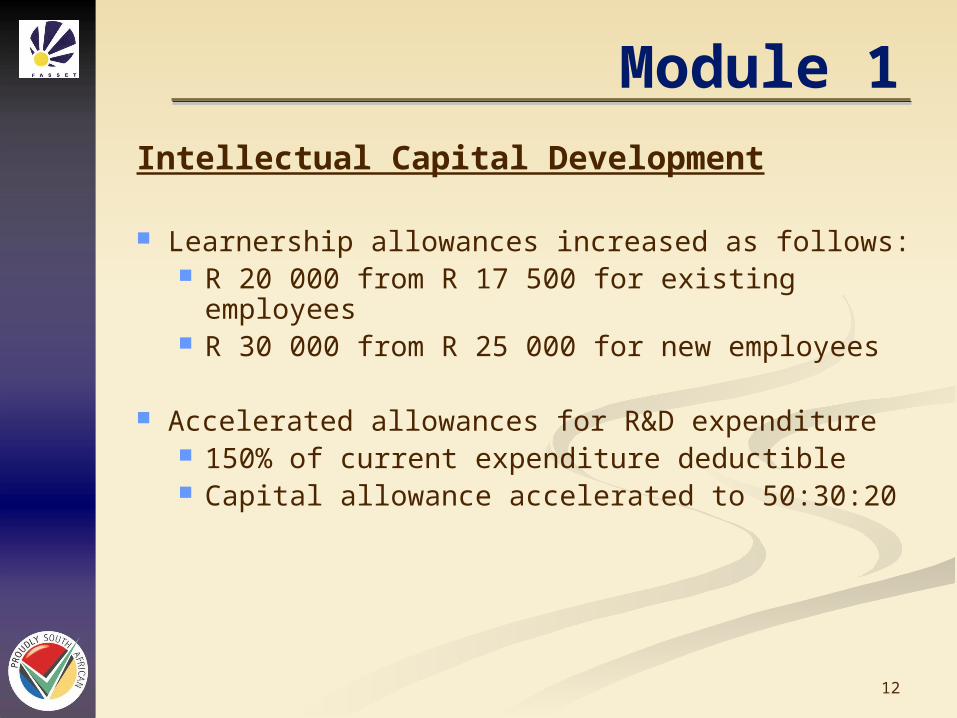

Module 1Intellectual Capital Development

Learnership allowances increased as follows: R 20 000 from R 17 500 for existing

employees R 30 000 from R 25 000 for new employees

Accelerated allowances for R&D expenditure 150% of current expenditure deductible Capital allowance accelerated to 50:30:20

13

Module 1

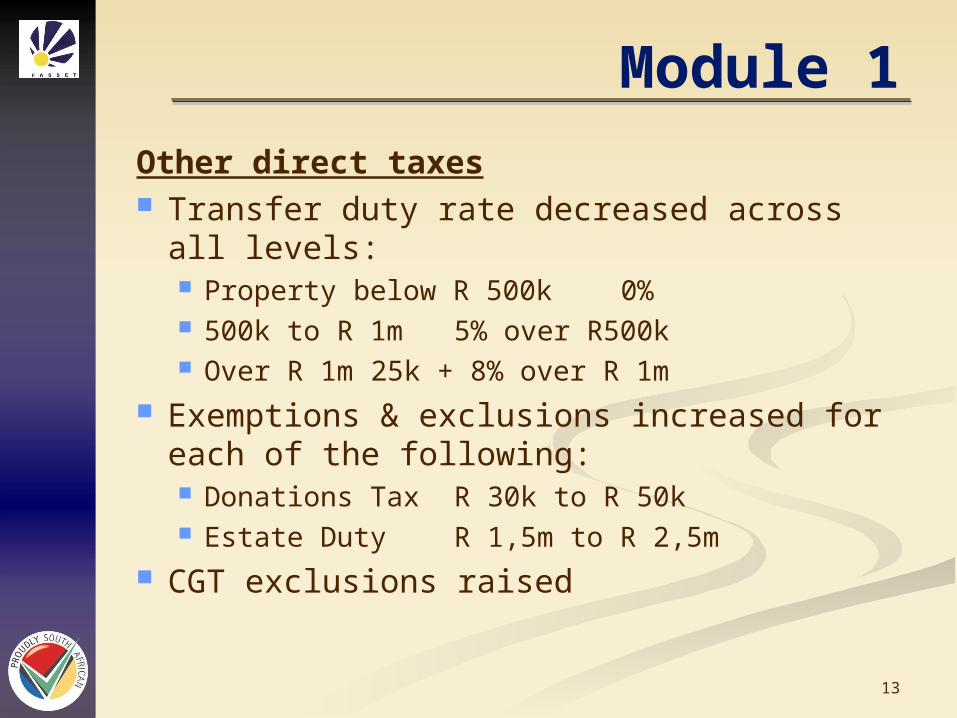

Other direct taxes Transfer duty rate decreased across all

levels: Property below R 500k 0% 500k to R 1m 5% over R500k Over R 1m 25k + 8% over R 1m

Exemptions & exclusions increased for each of the following: Donations Tax R 30k to R 50k Estate Duty R 1,5m to R 2,5m

CGT exclusions raised

14

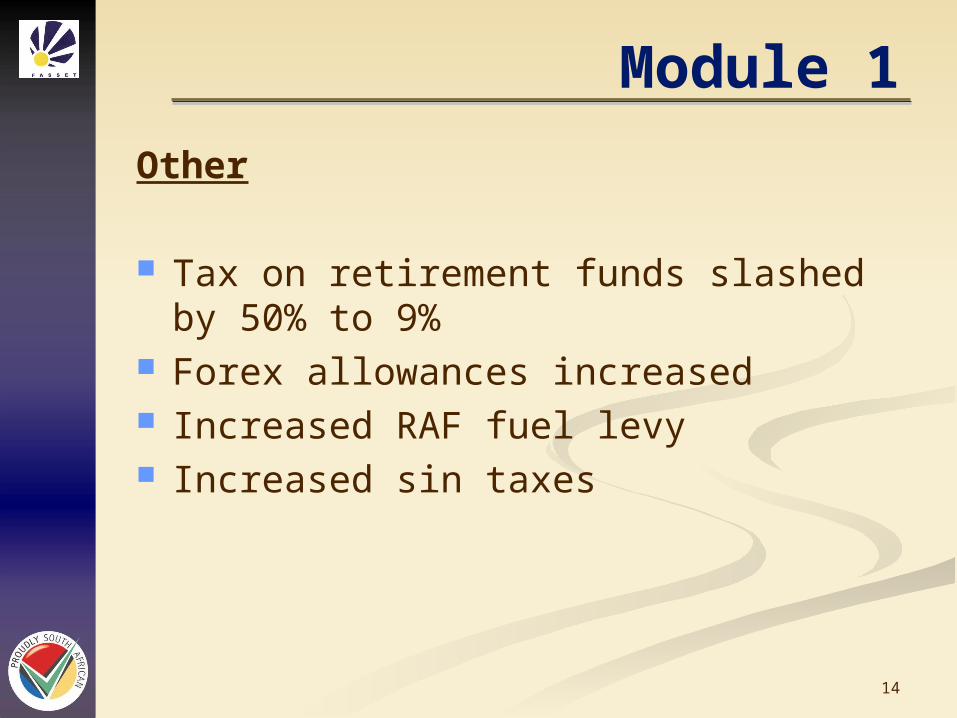

Module 1

Other

Tax on retirement funds slashed by 50% to 9%

Forex allowances increased Increased RAF fuel levy Increased sin taxes

15

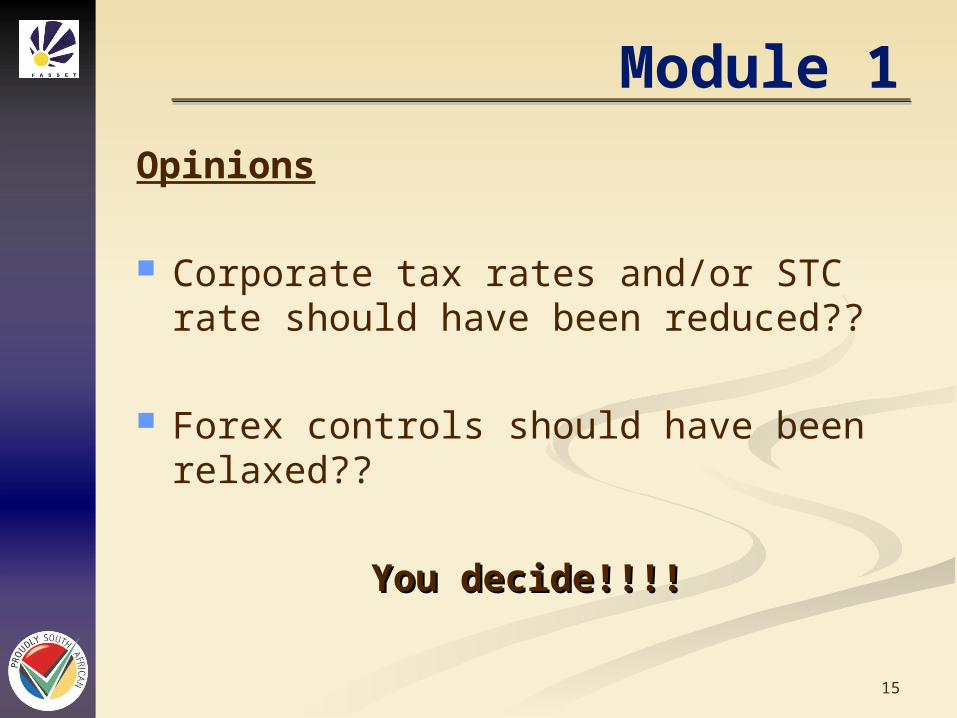

Module 1

Opinions

Corporate tax rates and/or STC rate should have been reduced??

Forex controls should have been relaxed??

You decide!!!!You decide!!!!

16

Module 2

Income tax for individuals

•Tax rates and rebates

•Deductions & exemptions

•Employees’ and Provisional Tax

•Personal Service Companies & Trusts

17

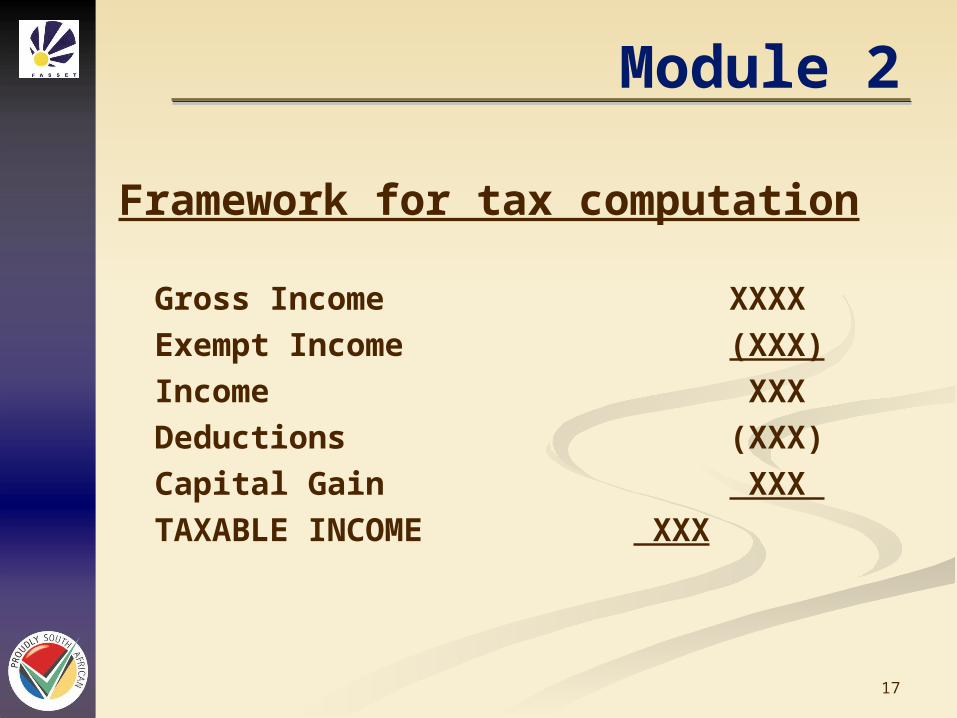

Module 2

Framework for tax computation

Gross Income XXXXExempt Income (XXX)Income XXXDeductions (XXX)Capital Gain XXX TAXABLE INCOME XXX

18

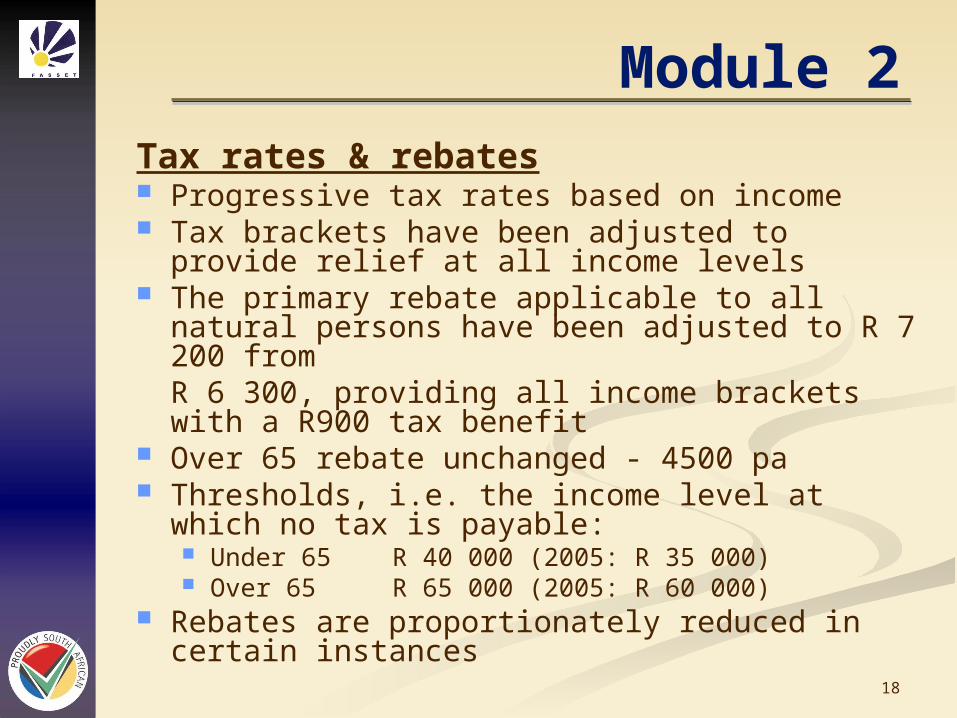

Module 2Tax rates & rebates Progressive tax rates based on income Tax brackets have been adjusted to provide

relief at all income levels The primary rebate applicable to all natural

persons have been adjusted to R 7 200 from R 6 300, providing all income brackets with a R900 tax benefit

Over 65 rebate unchanged - 4500 pa Thresholds, i.e. the income level at which no

tax is payable: Under 65 R 40 000 (2005: R 35 000) Over 65 R 65 000 (2005: R 60 000)

Rebates are proportionately reduced in certain instances

19

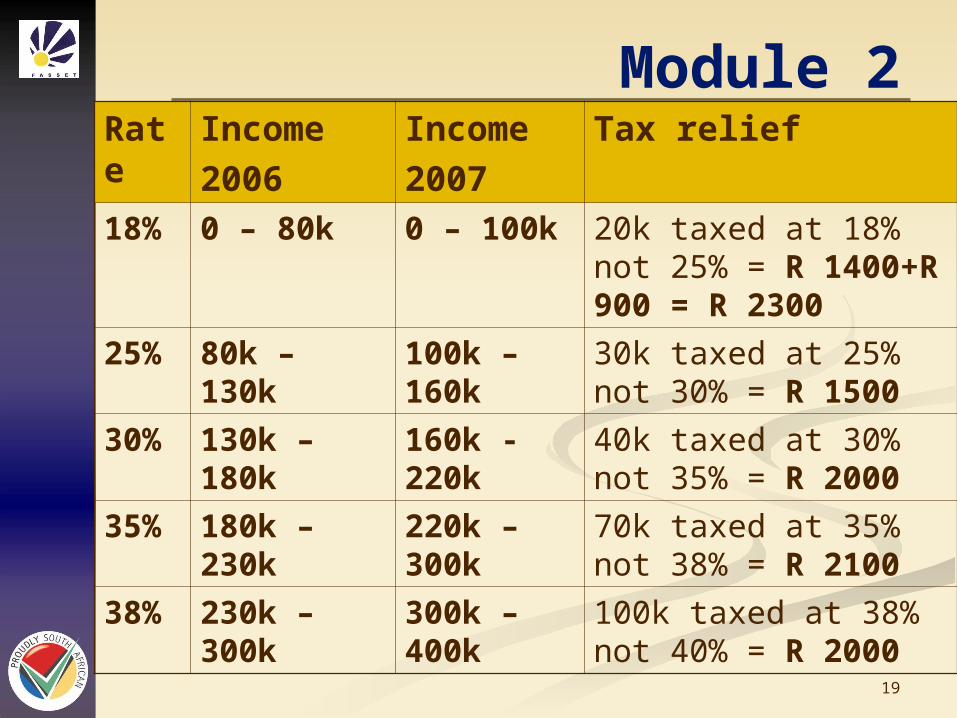

Module 2Rate

Income 2006

Income2007

Tax relief

18% 0 – 80k 0 – 100k 20k taxed at 18% not 25% = R 1400+R 900 = R 2300

25% 80k – 130k

100k – 160k

30k taxed at 25% not 30% = R 1500

30% 130k – 180k

160k - 220k

40k taxed at 30% not 35% = R 2000

35% 180k – 230k

220k – 300k

70k taxed at 35% not 38% = R 2100

38% 230k – 300k

300k – 400k

100k taxed at 38% not 40% = R 2000

20

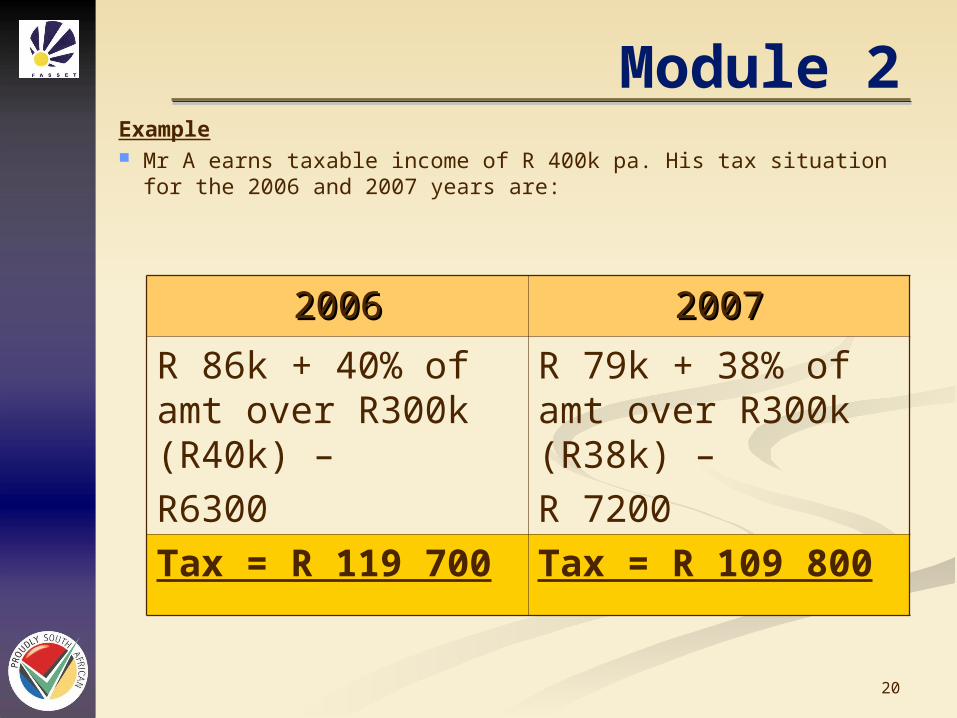

Module 2Example Mr A earns taxable income of R 400k pa. His tax situation for the

2006 and 2007 years are:

20062006 20072007

R 86k + 40% of amt over R300k (R40k) – R6300

R 79k + 38% of amt over R300k (R38k) –R 7200

Tax = R 119 700 Tax = R 109 800

21

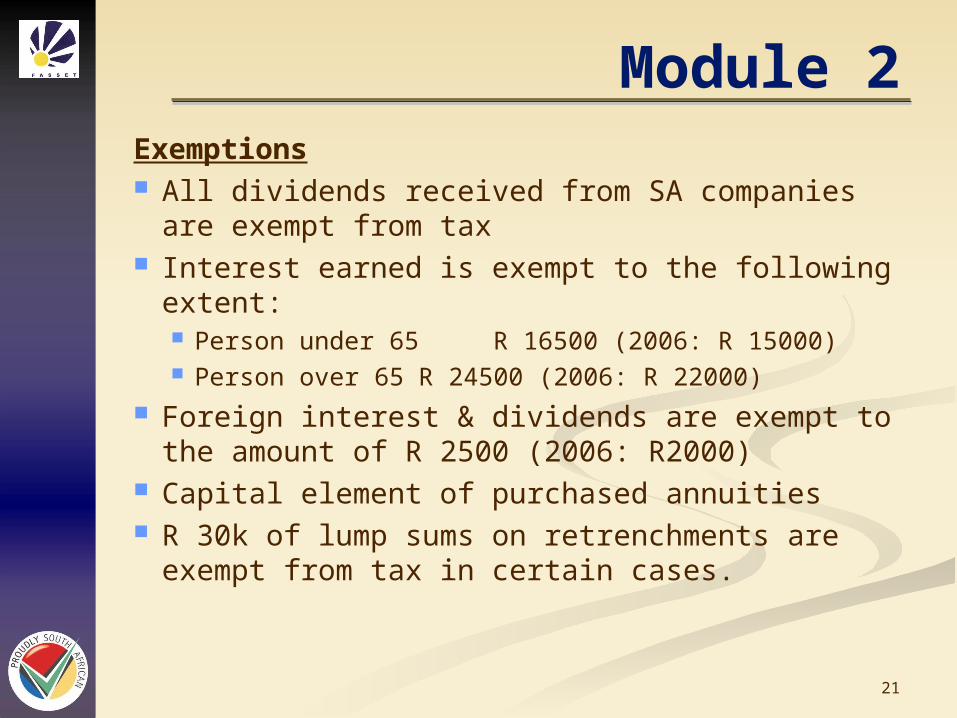

Module 2Exemptions All dividends received from SA companies are

exempt from tax Interest earned is exempt to the following

extent: Person under 65 R 16500 (2006: R 15000) Person over 65 R 24500 (2006: R 22000)

Foreign interest & dividends are exempt to the amount of R 2500 (2006: R2000)

Capital element of purchased annuities R 30k of lump sums on retrenchments are

exempt from tax in certain cases.

22

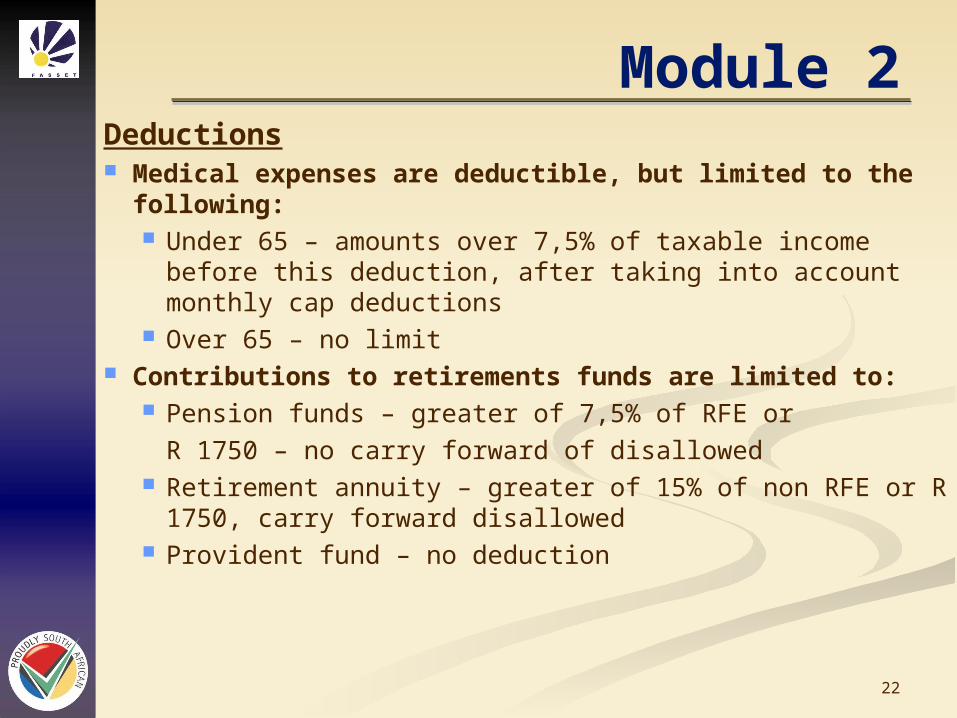

Module 2Deductions Medical expenses are deductible, but limited to the

following: Under 65 – amounts over 7,5% of taxable income before

this deduction, after taking into account monthly cap deductions

Over 65 – no limit Contributions to retirements funds are limited to:

Pension funds – greater of 7,5% of RFE or R 1750 – no carry forward of disallowed

Retirement annuity – greater of 15% of non RFE or R 1750, carry forward disallowed

Provident fund – no deduction

23

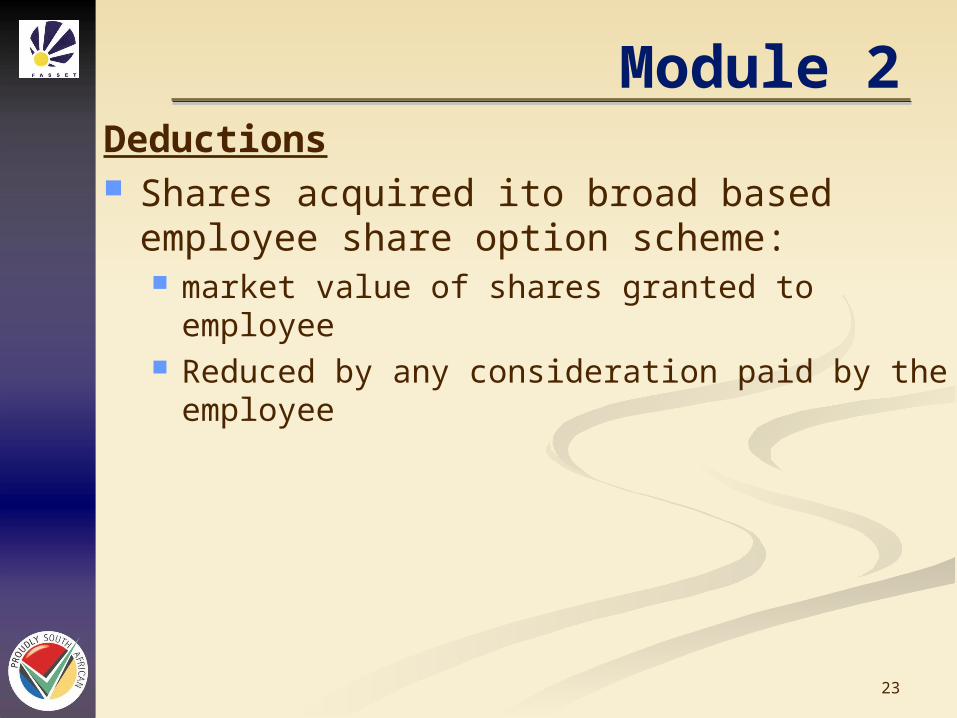

Module 2Deductions Shares acquired ito broad based employee

share option scheme: market value of shares granted to employee Reduced by any consideration paid by the

employee

24

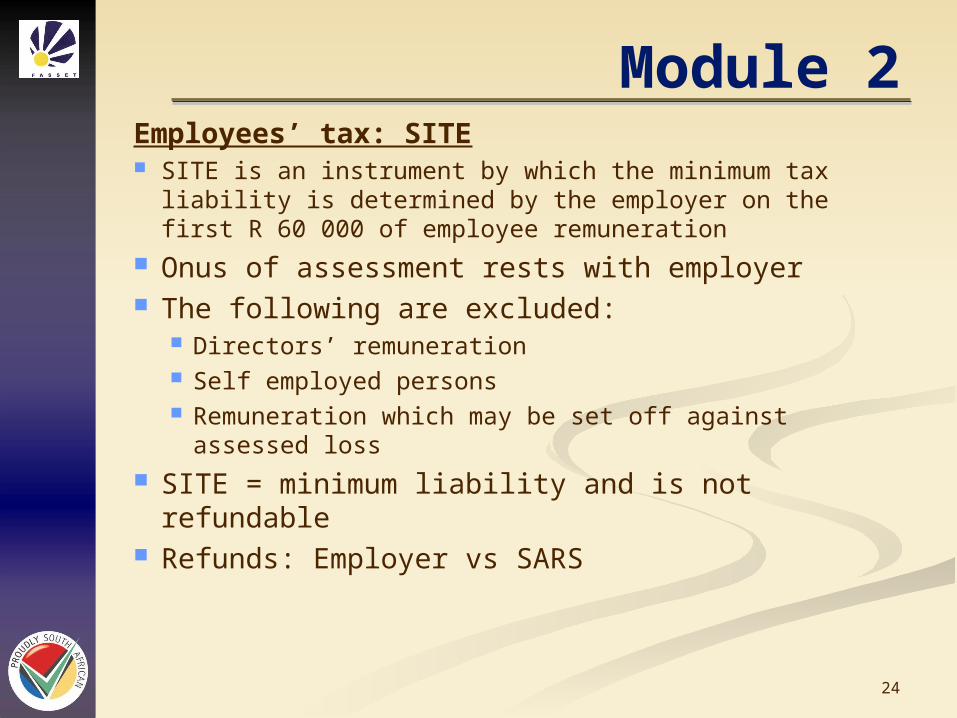

Module 2Employees’ tax: SITE SITE is an instrument by which the minimum tax

liability is determined by the employer on the first R 60 000 of employee remuneration

Onus of assessment rests with employer The following are excluded:

Directors’ remuneration Self employed persons Remuneration which may be set off against

assessed loss SITE = minimum liability and is not refundable Refunds: Employer vs SARS

25

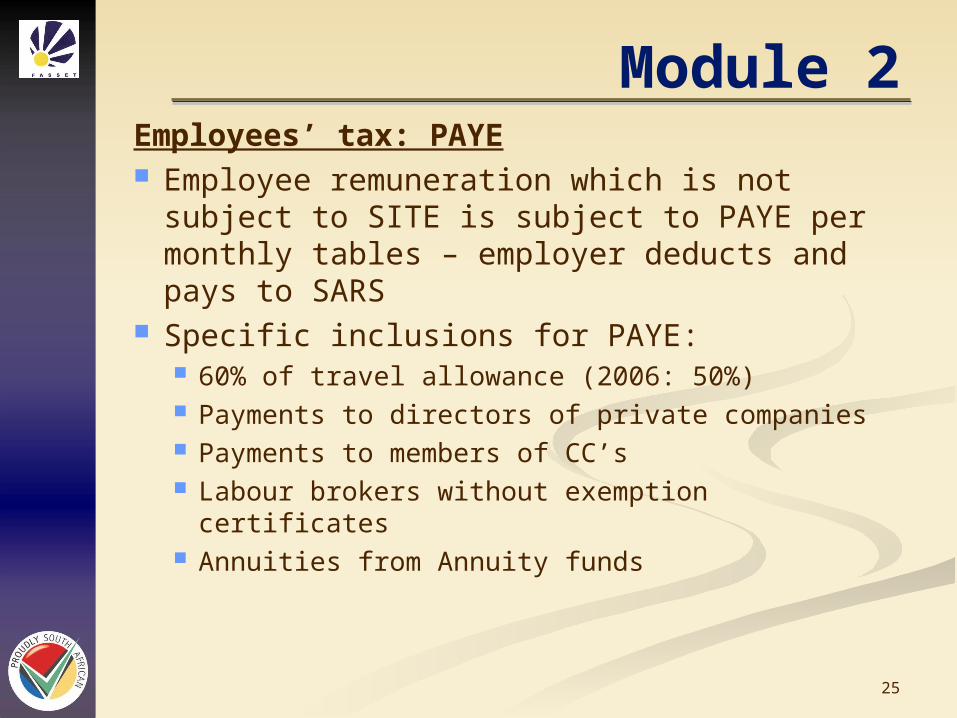

Module 2Employees’ tax: PAYE Employee remuneration which is not

subject to SITE is subject to PAYE per monthly tables – employer deducts and pays to SARS

Specific inclusions for PAYE: 60% of travel allowance (2006: 50%) Payments to directors of private companies Payments to members of CC’s Labour brokers without exemption certificates Annuities from Annuity funds

26

Module 2Casual / Part time employmentPAYE must be deducted at a rate of 25%in

respect of employees who: Work for an employer for less than 22 hours

per week OR Who work for an employer without reference

to a period.

Exemptions: Employee works regularly for less than 22

hours per week and provide written undertaking that they do not render services to another employer.

An employee who is in standard employment. Pensions paid to pensioners

27

Module 2Employer’s Responsibility Where employer fails to deduct full employees’ tax:

Employer becomes personally liable SARS may absolve employer where SARS believes

that there is a prospect of recovering from employee, if satisfied as to intent

If employer not absolved, then may recover from employee and hold back tax certificate until recovered

Employer liability is deemed to be a penalty and not deductible for tax purposes

SARS could levy penalty of up to twice the unpaid tax.

28

Module 2Provisional Tax Provisional tax is a method of paying tax due during a

year based on ‘basic amount’ or estimated income for that year.

1st payment for 50% of the estimated tax liability is due 6 months before year end and the 2nd payment of 50% at year end.

Total provisional tax paid should be based on latest assessment or estimated income and should not be less than 90% of final tax due.

Provisional tax is reduced by the amount of employees’ tax paid during the period

Optional 3 payment could be made within 6 months from end of year – (7 mths for Feb year ends)

29

Module 2Provisional Tax - Individuals Any capital gain previously assessed is

excluded from the basic amount for provisional tax purposes

Taxable portion of lump sum is excluded from the basic amount for provisional tax purposes

Interest and penalties1st pmt – No penalty for late submission,

only for late payment2nd pmt - 20% for late submission, 10% for

late paymentIn addition where estimate is less than 90% of actual

income, a penalty of 20% is levied on the diff of the actual tax and the tax paid on the estimate

30

Module 2Personal Service Companies & Trusts Any entity which renders services by a person

connected to the company & one of the following apply: The person would be an employee but for the

entity; Person is subject to the supervision of client ito

work; Payments regularly – like remuneration 80% of earning derived from one company

Entity not PSC if 3 or more employees for full year

31

Module 2Personal Service Companies &

Trusts Any remuneration earned by Personal

Service subject to 34% PAYE. Deductions in determining income is

limited to remuneration paid to member, director and employees of entity.

32

Module 2Ring-Fencing Assessed Losses Sec 20A effective years ending on or after 1

March 2004. Applies to individuals whose taxable income

before setting off assessed loss is equal to or exceeds the level at which maximum rate of tax is applicable. (2007 : R400k /2006 : R300k)

Applies in 1 of 2 situations: The taxpayer has during a five year period incurred

a loss in the relevant trade in at least three years OR

The trade in respect of which the assessed loss is incurred is included in the list stipulated in the act.

Does not apply if the trade constitutes a business in which there is a reasonable prospect of deriving taxable income within a reasonable period.

33

Module 3

Fringe benefits•Traveling allowances

•Employer owned vehicles

•Medical aid contributions

•Holiday accommodation

•Local and overseas travel

•Broad based share option scheme

34

Module 3Travel Allowances Beware of excessive allowances!! – deemed salary

and PAYE is to be deducted. 60% (2006:50%) of fixed travel allowances are

included in remuneration and subject to PAYE – the full allowance is disclosed

Re-imbursive travel is not subject to PAYE on the following conditions: Total mileage does not exceed 8000km pa The rate per km does not exceed 246c per km

(2006: 238c) Reimbursement for actual travel is not subject to

PAYE

35

Module 3Travel Allowances The taxable fringe benefit is calculated by

reducing the benefit received by a rate per km in respect of business mileage travelled

The fixed rate per km is reduced of not for full year

Where no log book is maintained, the first 18 000 of travel is deemed to be private with the balance deemed to be business subject to a maximum of 14 000 km – all deemed figures are apportioned for part of a year

The rate per km is determined by SARS and is influenced by the value of the vehicle, limited to a maximum of R 360 000.

36

Module 3Employer owned vehicles The employee is taxed on 2,5% per month (2006:

1,8%) of the ‘value’ of the vehicle and 4% per month on the 2nd vehicle if two vehicles are provided: Reduced by the value paid by the employee for use

‘Value’ of vehicle is reduced by 15% for each 12 month period, where second hand

The benefit is reduced if responsible for any cost as follows: All private fuel used 0,22% monthly Maintenance costs 0,18% monthly

Exclusions: The vehicle is available to all employees and

private use is negligible and incidental Required for employee’s work after hours

37

Module 3Employer owned vehicles Where travel allowance is received in addition

to company car: Company car is taxed at 4% No portion of consideration paid by employee may

be deducted, if not for actual business travel

Where private travel is less than 10 000km and accurate records are kept, SARS may reduce the value placed on private use

38

Module 3Medical Aid Contributions The contribution by the employer to the

employees’ medical aid is taxable insofar as the contribution exceeds R 500 for the first 2 beneficiaries and R 300 for each other beneficiary

For 2006, the benefit was the deemed to be the excess of two thirds of the employees medical aid cost i.e. where 50% was paid by the employer, no fringe benefit accrued

No value contributions: Employee retired from employer due to ill health or

other infirmity Dependents of an employee who died and was

employed at time of death or of a deceased retired employee

39

Module 3Holiday Accommodation The fringe benefit to the employee is the

prevailing market rate if the accommodation is owned by the employer

actual rental if the accommodation is rented

Subsistence Allowances: Local Travel

Where an allowance is paid to an employee, the employee must travel within 1 month to avoid PAYE being deducted from that allowance

Deemed allowances include: R60 per day or part thereof for incidentals R196 per day for meals and incidentals

40

Module 3Subsistence Allowances: Overseas Where an allowance is paid to an employee,

the employee must travel within 1 month to avoid PAYE being deducted from that allowance

Deemed allowances include: $ 190 for meals and incidentals outside the

Republic

General Fringe benefits are generally the difference

between the market value of the benefit provided to the employee and the consideration paid by the employee

VAT implications for employer

41

Module 3Share options – Section 8A

Any gain obtained by exercise, cession or release of any right to acquire any marketable security

As a consequence of services as a director or employee

Gives rise to a tax liability on the date that the right is exercised

Taxable gain is the difference between the market value at date right or option is exercised and the consideration paid for the right/share

Relief is provided to the taxpayer where the restrictions in respect of disposal of shares

42

Module 3Broad based employee share plan – S

8B S 8B introduced from 26 October 2004. Purpose: To encourage long-term empowerment

of employees through the receipt of shares at less than market value without adverse tax consequences.

Applicable to any “qualifying equity shares” as defined.

Any gain from the disposal of any qualifying equity share which is disposed of within 5 yrs from date of grant must be included in income, except: Disposals on death and insolvency or qualifying

equity shares exchanged for other qualifying equity shares

43

Module 3Broad-based employee share plan

(BBESP) BBESP is a plan in terms of which:

Equity shares in that employer are acquired by employees for a consideration not exceeding the minimum required by the Co’s Act.

If employees participate in any other share plan of the employer, then not allowed to participate in the BBESP and at least 90% of other employees entitled to participate.

The persons acquiring these shares have full voting rights and dividends.

No restrictions must be placed on disposal of shares, except:

That shares may not be disposed of for at least five years from date of grant

44

Module 3Broad based employee share options –

S 8B Furthermore, the initial receipt of those shares are tax exempt.

Loans to employees to buy such shares are not subject to fringe benefits tax.

If the employee is no longer a resident within 5 years of being granted those shares, the shares are deemed not to have been disposed of

If the employee dies and the executor sells the shares, section 25 does not apply to tax the estate or heir on the proceeds.

45

Module 3Broad based employee share options –

S 8B Employer companies may issue shares up to a limit of R9 000 per employee in current tax year and immediate preceding two tax years.

A tax deduction up to R3 000 per employee per annum for 3 years will be allowed.

Where the employee holds those shares for at least 5 years, there will be no tax consequences except for CGT.

46

Module 4

•Capital Gains Tax

•Donations Tax

•Estate Duty

47

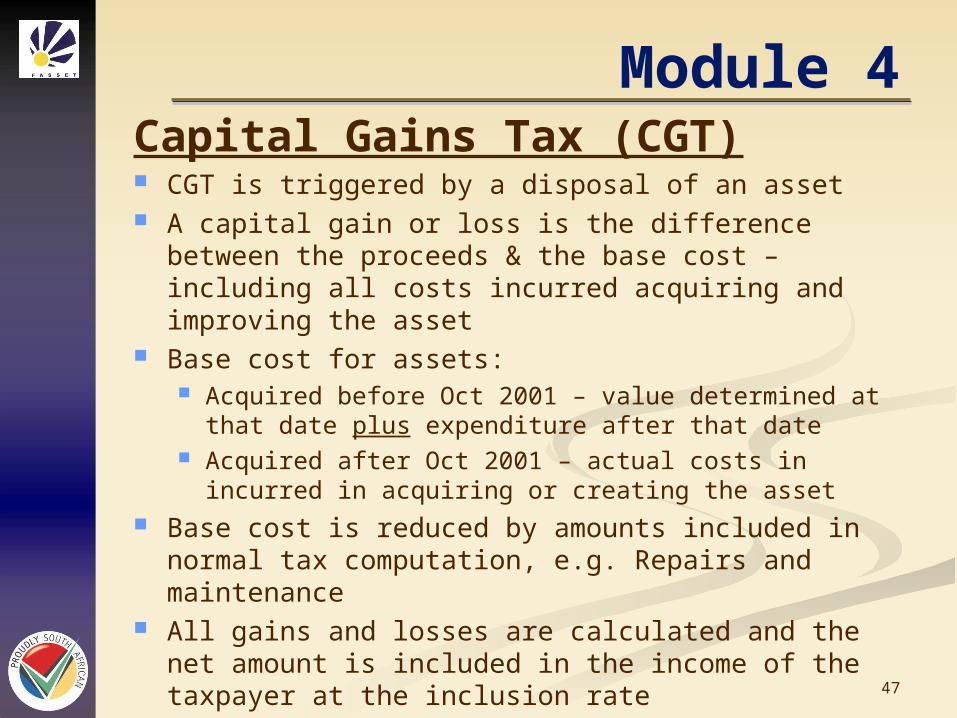

Module 4Capital Gains Tax (CGT) CGT is triggered by a disposal of an asset A capital gain or loss is the difference between the

proceeds & the base cost – including all costs incurred acquiring and improving the asset

Base cost for assets: Acquired before Oct 2001 – value determined at

that date plus expenditure after that date Acquired after Oct 2001 – actual costs in incurred in

acquiring or creating the asset Base cost is reduced by amounts included in

normal tax computation, e.g. Repairs and maintenance

All gains and losses are calculated and the net amount is included in the income of the taxpayer at the inclusion rate

48

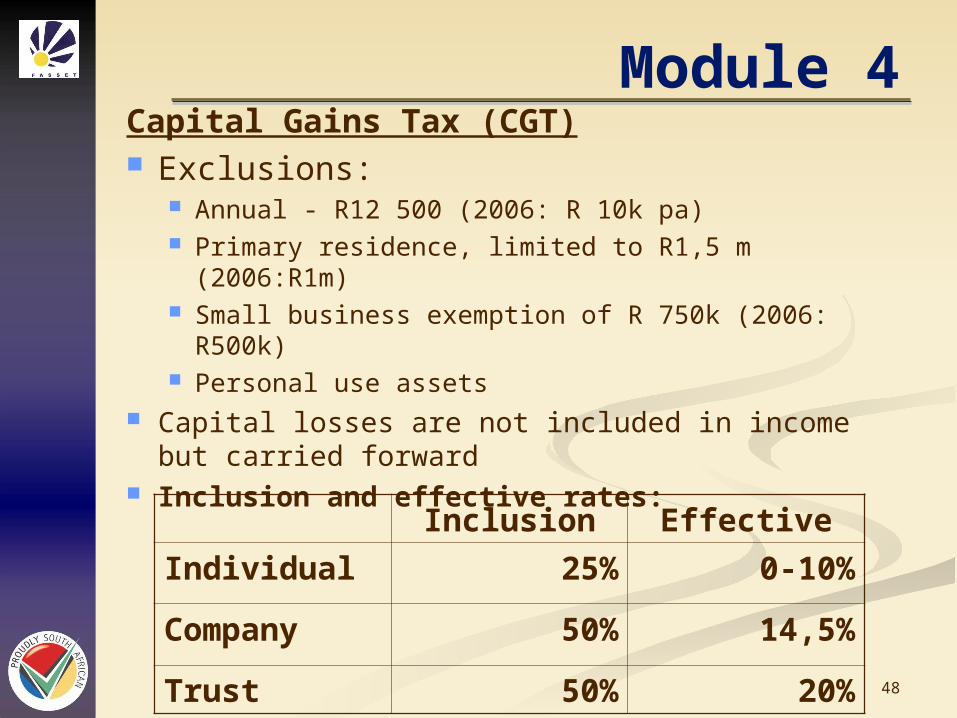

Module 4Capital Gains Tax (CGT) Exclusions:

Annual - R12 500 (2006: R 10k pa) Primary residence, limited to R1,5 m (2006:R1m) Small business exemption of R 750k (2006:

R500k) Personal use assets

Capital losses are not included in income but carried forward

Inclusion and effective rates:Inclusion Effective

Individual 25% 0-10%

Company 50% 14,5%

Trust 50% 20%

49

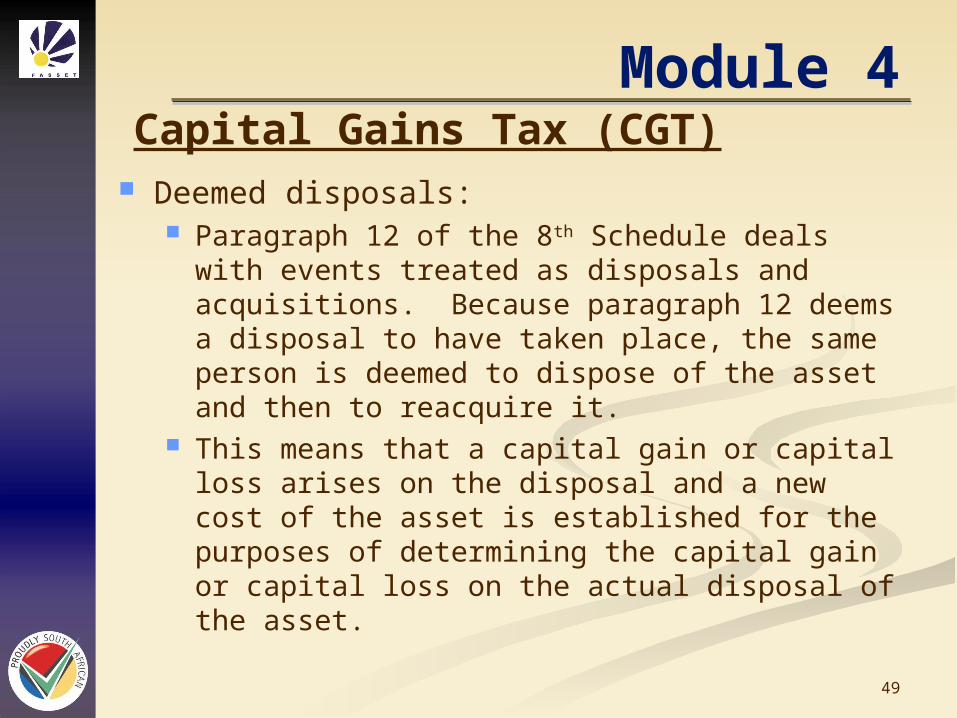

Module 4Capital Gains Tax (CGT)

Deemed disposals: Paragraph 12 of the 8th Schedule deals with

events treated as disposals and acquisitions. Because paragraph 12 deems a disposal to have taken place, the same person is deemed to dispose of the asset and then to reacquire it.

This means that a capital gain or capital loss arises on the disposal and a new cost of the asset is established for the purposes of determining the capital gain or capital loss on the actual disposal of the asset.

50

Module 4Capital Gains Tax (CGT)

Deemed disposals: A person ceases to be a resident of South

Africa An asset of a non-resident become part of

(deemed acquisition) or ceases to be part of (deemed disposal) a South African permanent establishment of a non-resident

A capital asset becomes trading stock Personal use assets become capital assets and

vice versa

51

Module 4Rollover relief Rollover relief applies by using two different

methods Roll-over relief means that recognition of the

capital gain is deferred until a future date. Most common instances:

Transfer of assets between spouses Involuntary disposals Reinvestment in replacement assets

Where rollover is elected, so much of the gain as relates to any allowances claimed on the replacement assets should be recognised

52

Module 4Donations Tax Tax of 20% levied on property

gratuitously disposed of, except: Donations by natural persons < R50k

pa (2006: R30k) Donations by private companies < R

10k Donations between spouses Donations by public companies (tax

purposes) Donations to PBO’s

53

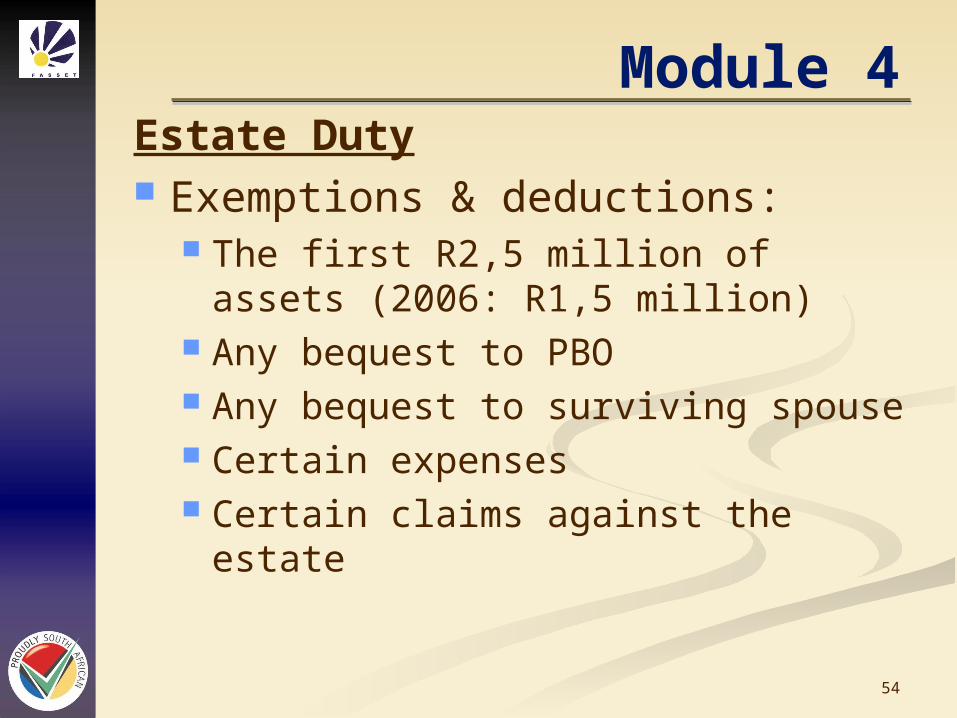

Module 4Estate Duty Payable on net value of property

at time of death Levied at the rate of 20% Certain property is deemed to be

property of the deceased: Insurance policies on life of deceased Property which deceased could have

disposed of at time of death

54

Module 4Estate Duty Exemptions & deductions:

The first R2,5 million of assets (2006: R1,5 million)

Any bequest to PBO Any bequest to surviving spouse Certain expenses Certain claims against the estate

55

Module 5

•Company & CC Tax

- Normal tax

- Small Businesses

- STC

56

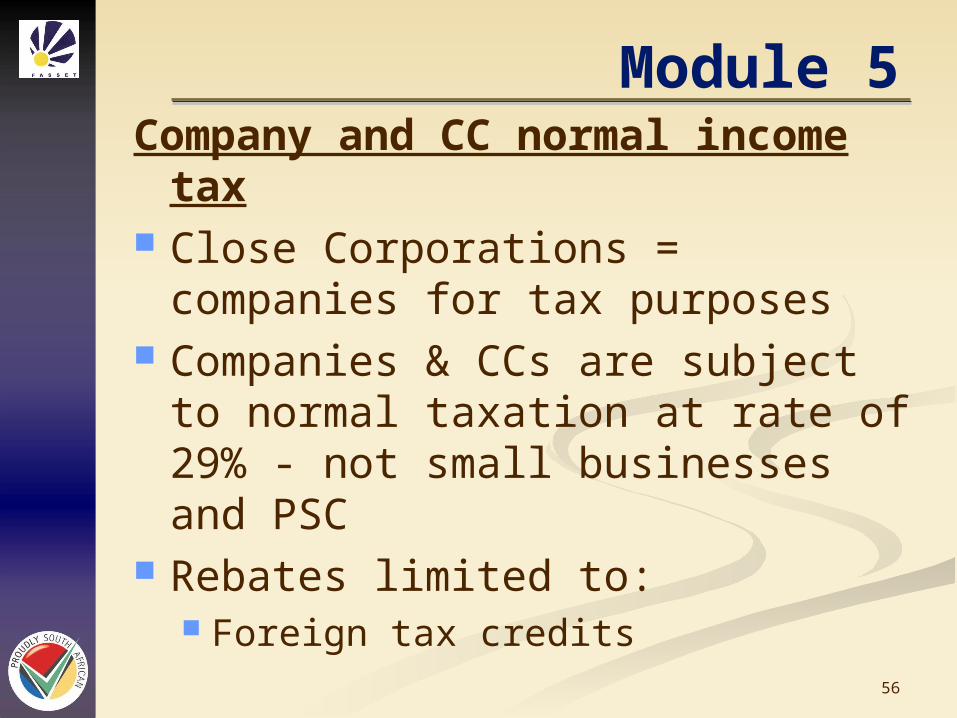

Module 5Company and CC normal income

tax Close Corporations = companies

for tax purposes Companies & CCs are subject to

normal taxation at rate of 29% - not small businesses and PSC

Rebates limited to: Foreign tax credits

57

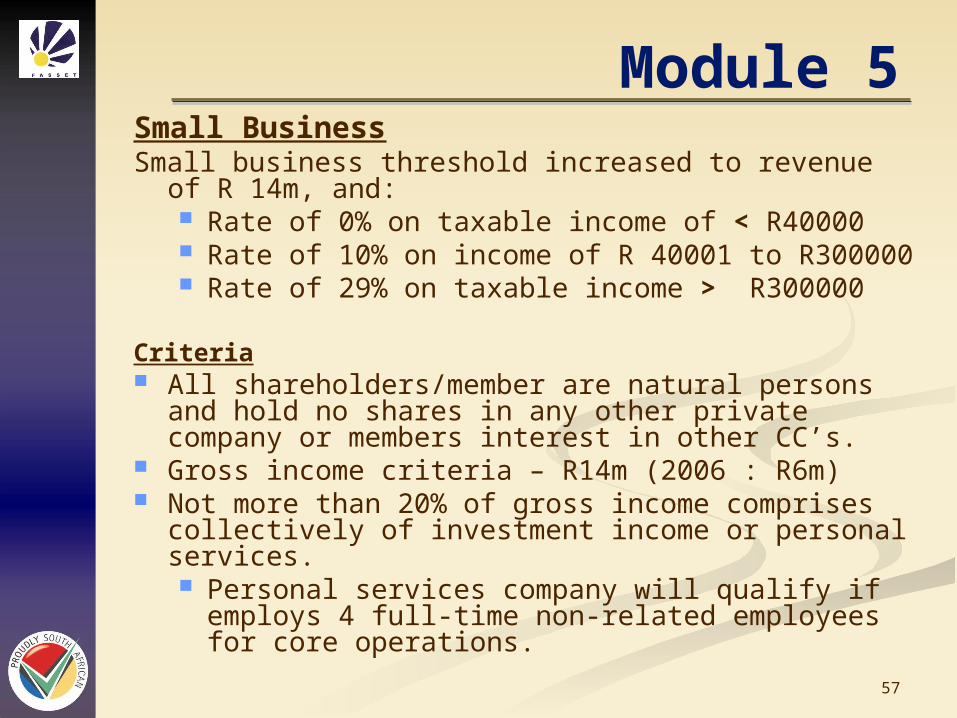

Module 5Small BusinessSmall business threshold increased to revenue of R

14m, and: Rate of 0% on taxable income of < R40000 Rate of 10% on income of R 40001 to R300000 Rate of 29% on taxable income > R300000

Criteria All shareholders/member are natural persons and

hold no shares in any other private company or members interest in other CC’s.

Gross income criteria – R14m (2006 : R6m) Not more than 20% of gross income comprises

collectively of investment income or personal services. Personal services company will qualify if

employs 4 full-time non-related employees for core operations.

58

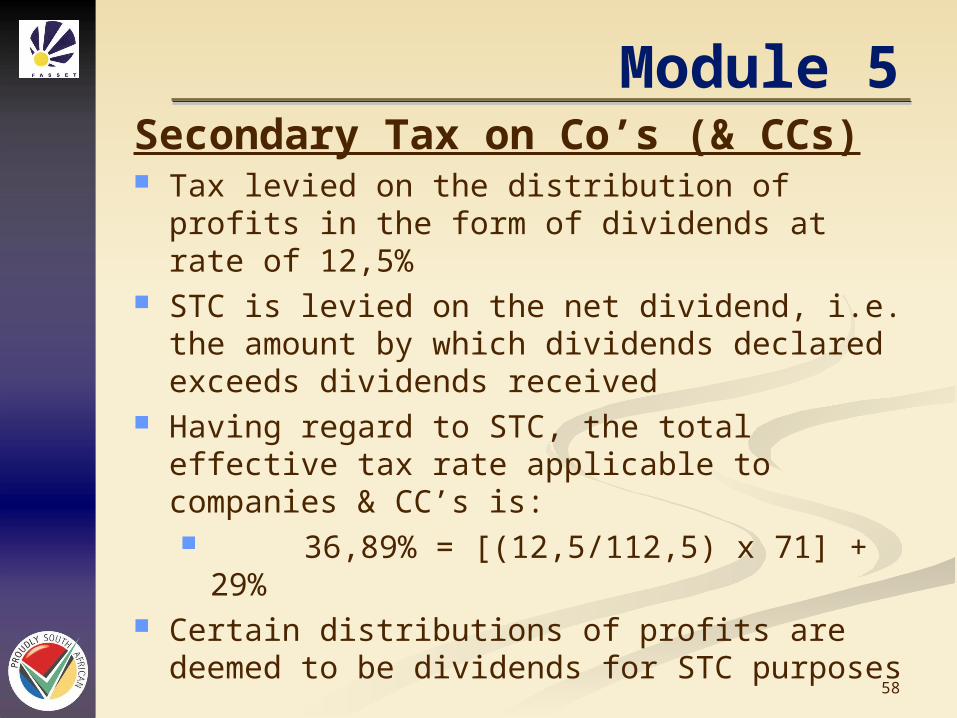

Module 5Secondary Tax on Co’s (& CCs) Tax levied on the distribution of profits in the

form of dividends at rate of 12,5% STC is levied on the net dividend, i.e. the

amount by which dividends declared exceeds dividends received

Having regard to STC, the total effective tax rate applicable to companies & CC’s is: 36,89% = [(12,5/112,5) x 71] + 29%

Certain distributions of profits are deemed to be dividends for STC purposes

59

Module 6

•Value Added Tax

60

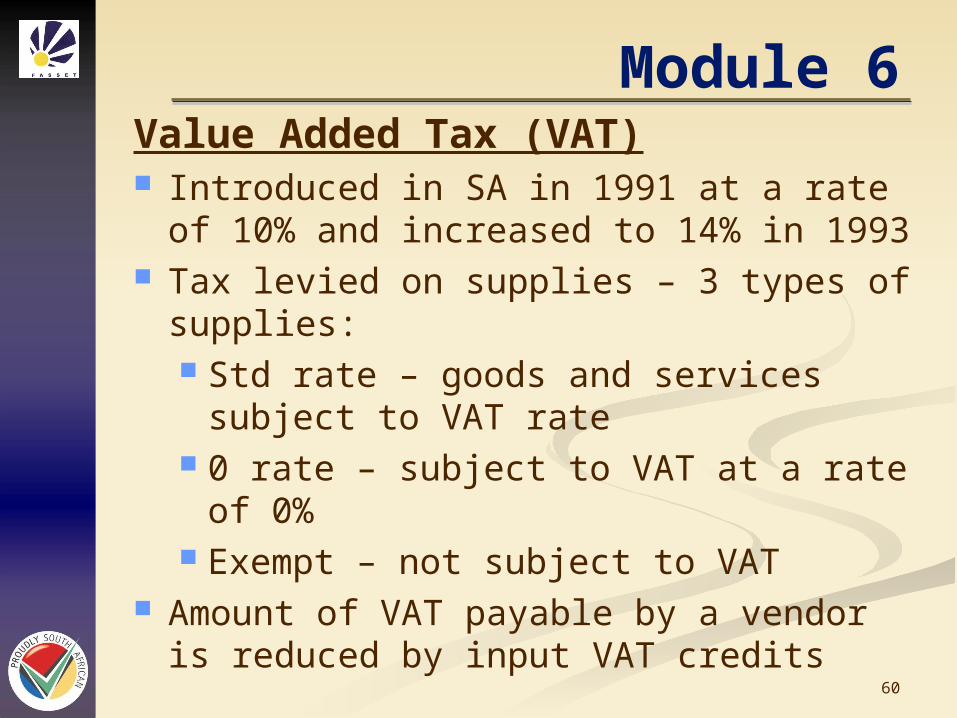

Module 6Value Added Tax (VAT) Introduced in SA in 1991 at a rate of

10% and increased to 14% in 1993 Tax levied on supplies – 3 types of

supplies: Std rate – goods and services subject

to VAT rate 0 rate – subject to VAT at a rate of

0% Exempt – not subject to VAT

Amount of VAT payable by a vendor is reduced by input VAT credits

61

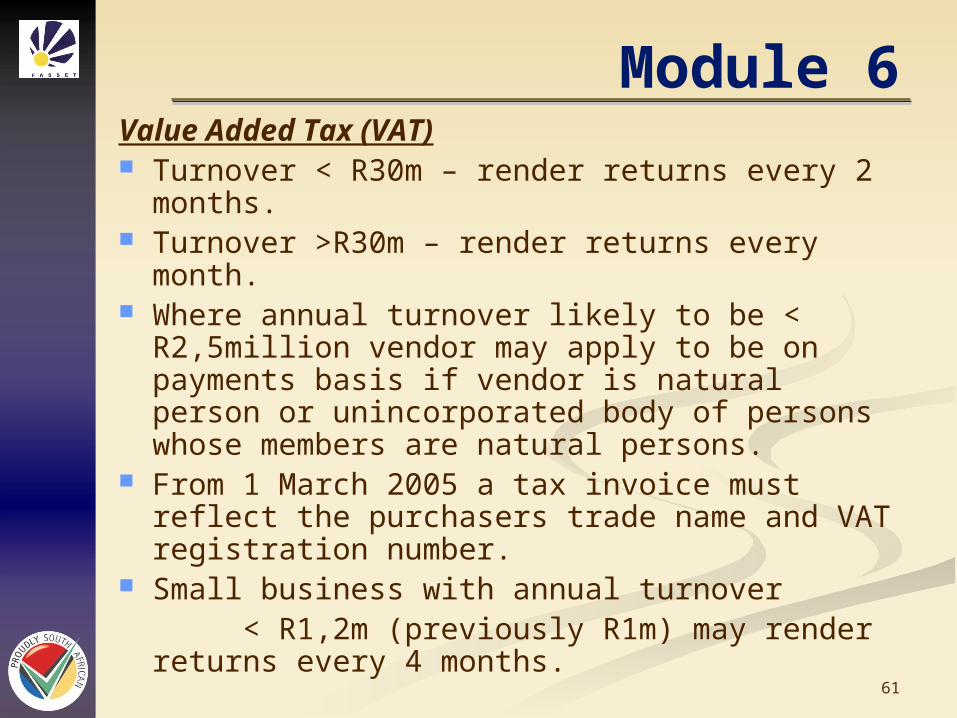

Module 6Value Added Tax (VAT) Turnover < R30m – render returns every 2

months. Turnover >R30m – render returns every

month. Where annual turnover likely to be <

R2,5million vendor may apply to be on payments basis if vendor is natural person or unincorporated body of persons whose members are natural persons.

From 1 March 2005 a tax invoice must reflect the purchasers trade name and VAT registration number.

Small business with annual turnover < R1,2m (previously R1m) may render returns

every 4 months.

62

Module 6

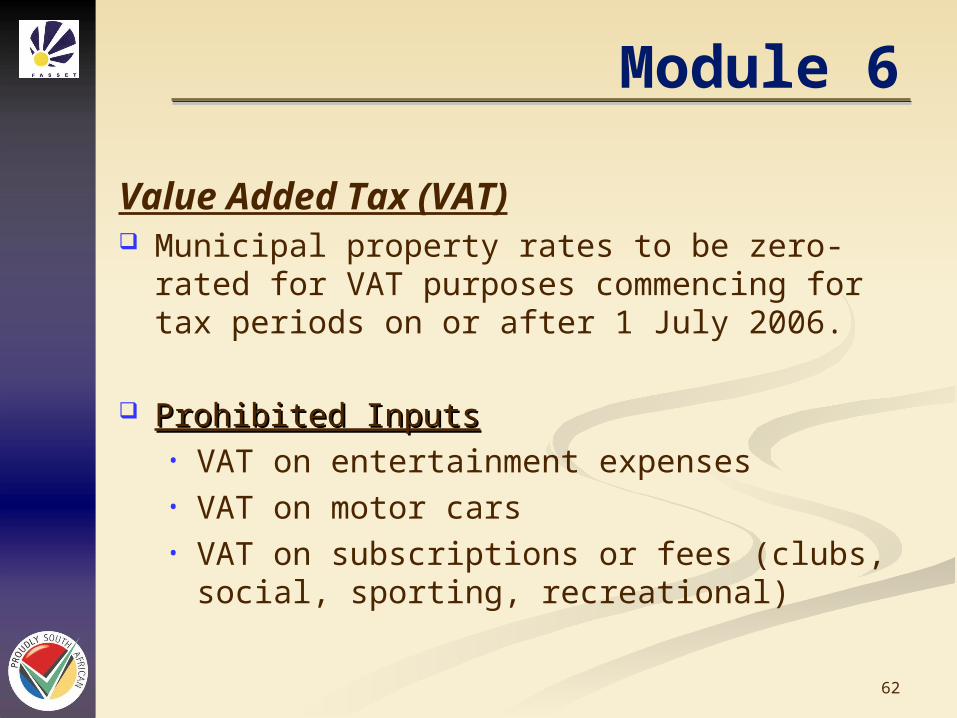

Value Added Tax (VAT) Municipal property rates to be zero-rated for

VAT purposes commencing for tax periods on or after 1 July 2006.

Prohibited InputsProhibited Inputs• VAT on entertainment expenses• VAT on motor cars• VAT on subscriptions or fees (clubs, social,

sporting, recreational)

63

Module 7

•Capital allowances

64

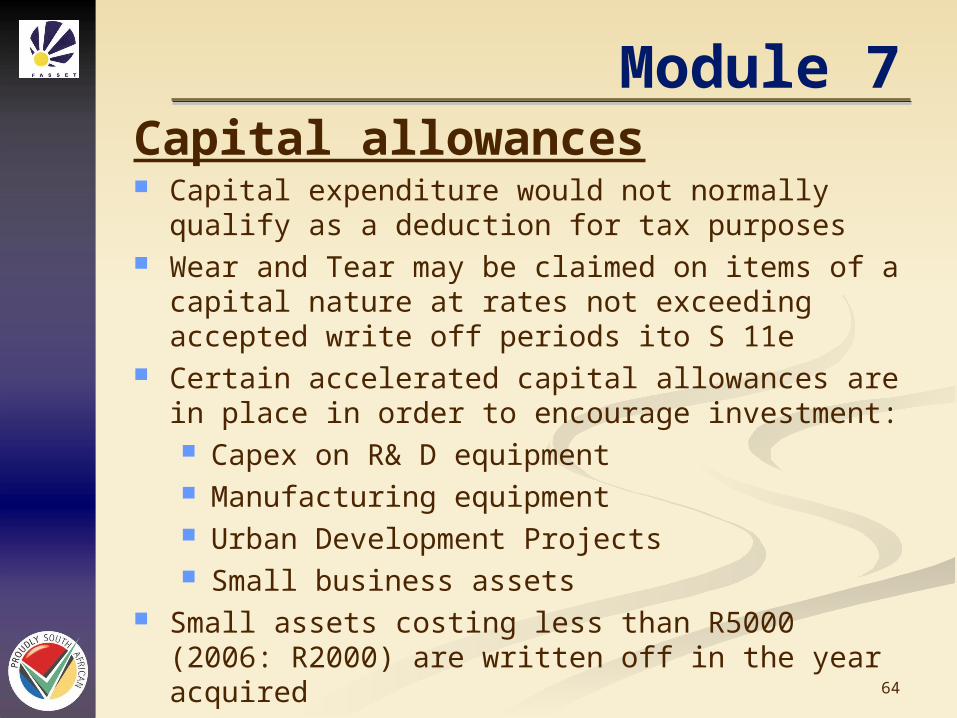

Module 7Capital allowances Capital expenditure would not normally qualify as

a deduction for tax purposes Wear and Tear may be claimed on items of a

capital nature at rates not exceeding accepted write off periods ito S 11e

Certain accelerated capital allowances are in place in order to encourage investment: Capex on R& D equipment Manufacturing equipment Urban Development Projects Small business assets

Small assets costing less than R5000 (2006: R2000) are written off in the year acquired

65

Module 8

•Sundry Issues

66

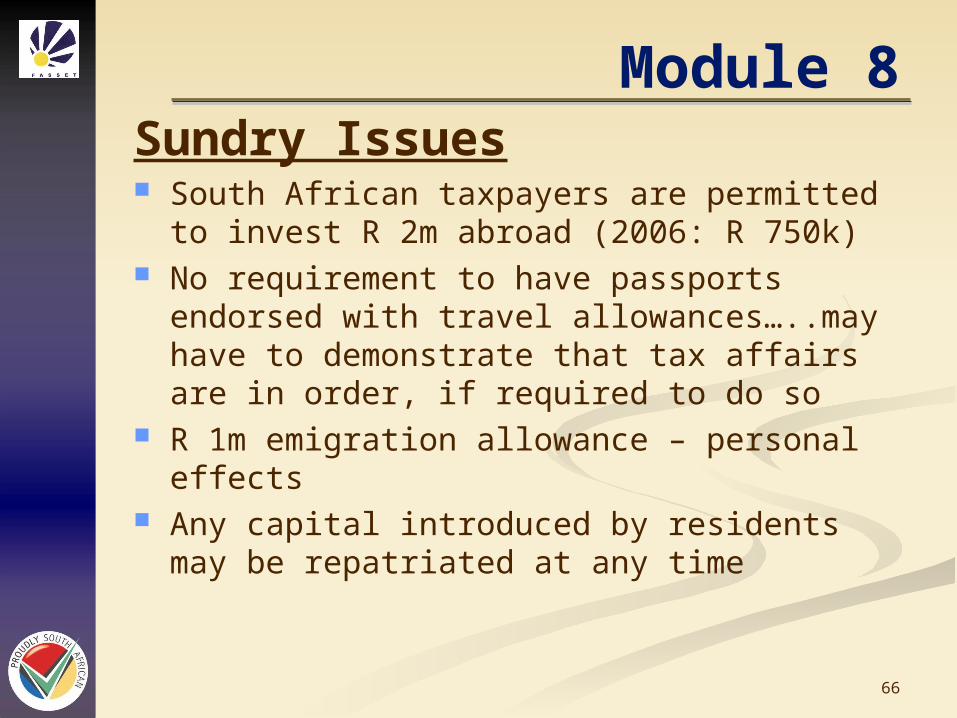

Module 8Sundry Issues South African taxpayers are permitted to

invest R 2m abroad (2006: R 750k) No requirement to have passports endorsed

with travel allowances…..may have to demonstrate that tax affairs are in order, if required to do so

R 1m emigration allowance – personal effects Any capital introduced by residents may be

repatriated at any time

67

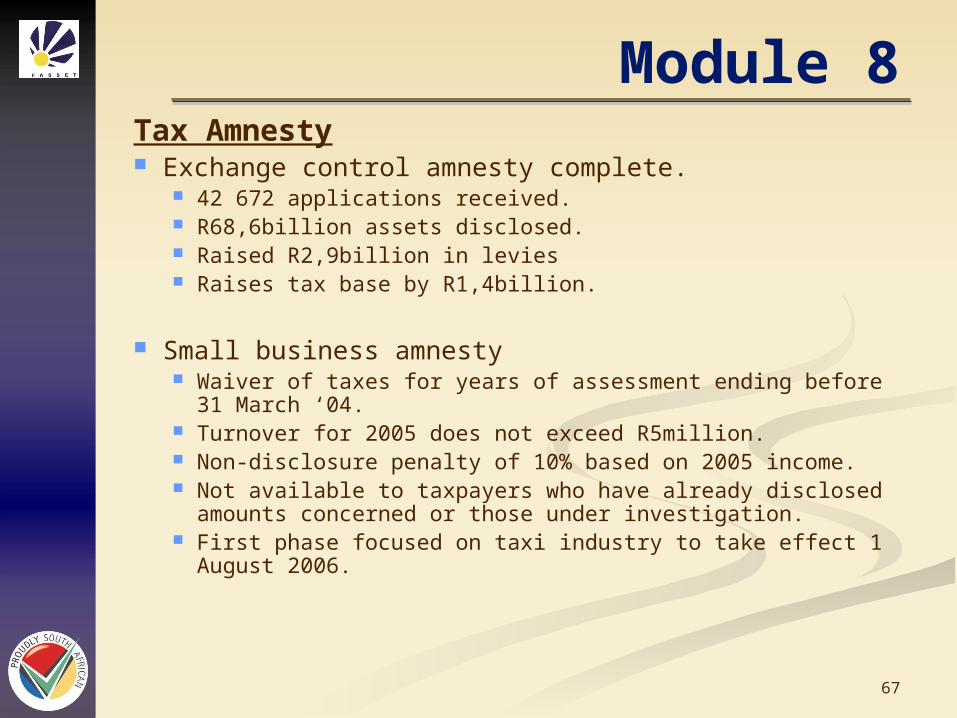

Module 8Tax Amnesty Exchange control amnesty complete.

42 672 applications received. R68,6billion assets disclosed. Raised R2,9billion in levies Raises tax base by R1,4billion.

Small business amnesty Waiver of taxes for years of assessment ending before 31

March ‘04. Turnover for 2005 does not exceed R5million. Non-disclosure penalty of 10% based on 2005 income. Not available to taxpayers who have already disclosed

amounts concerned or those under investigation. First phase focused on taxi industry to take effect 1 August

2006.

68

Module 8

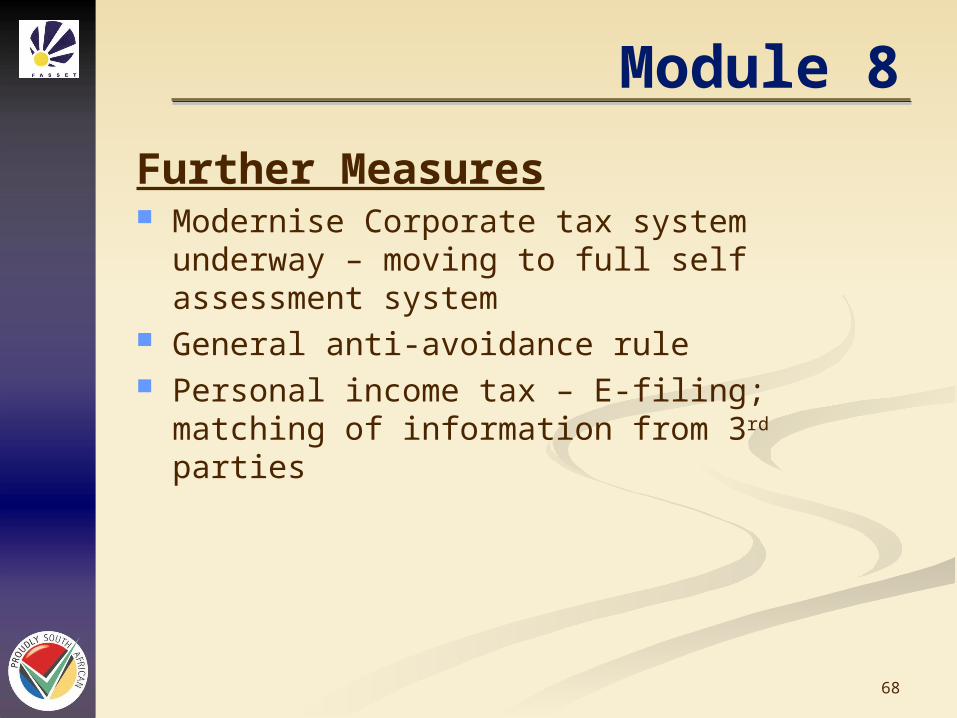

Further Measures Modernise Corporate tax system underway –

moving to full self assessment system General anti-avoidance rule Personal income tax – E-filing; matching of

information from 3rd parties

69

Module 8

Interest Rates

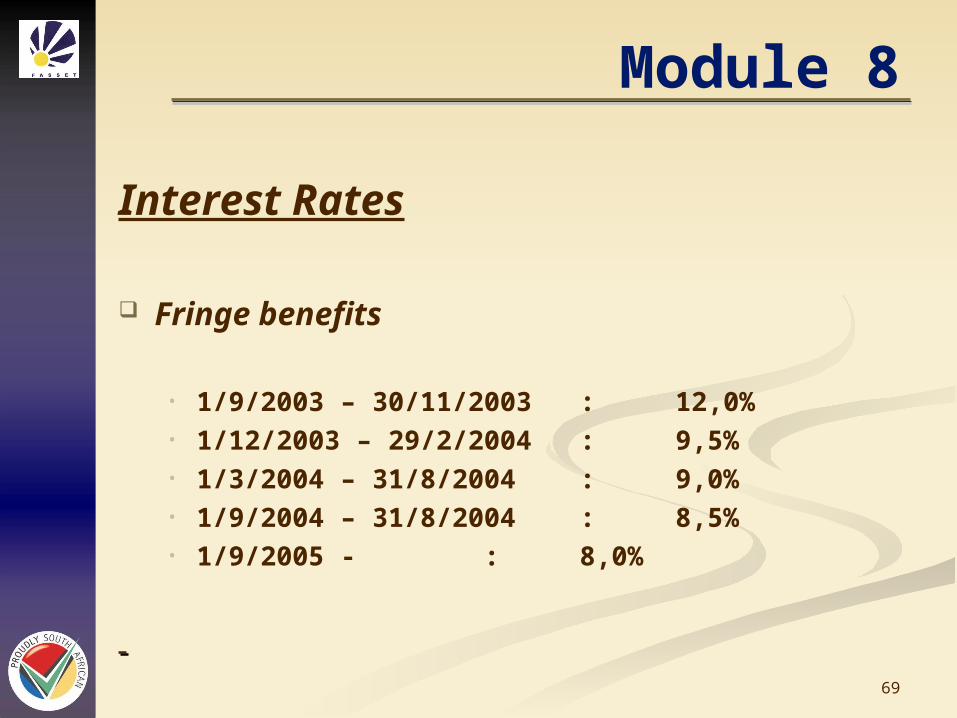

Fringe benefits

• 1/9/2003 – 30/11/2003 : 12,0%• 1/12/2003 – 29/2/2004 : 9,5%• 1/3/2004 – 31/8/2004 : 9,0%• 1/9/2004 – 31/8/2004 : 8,5%• 1/9/2005 - : 8,0%

70

Module 8

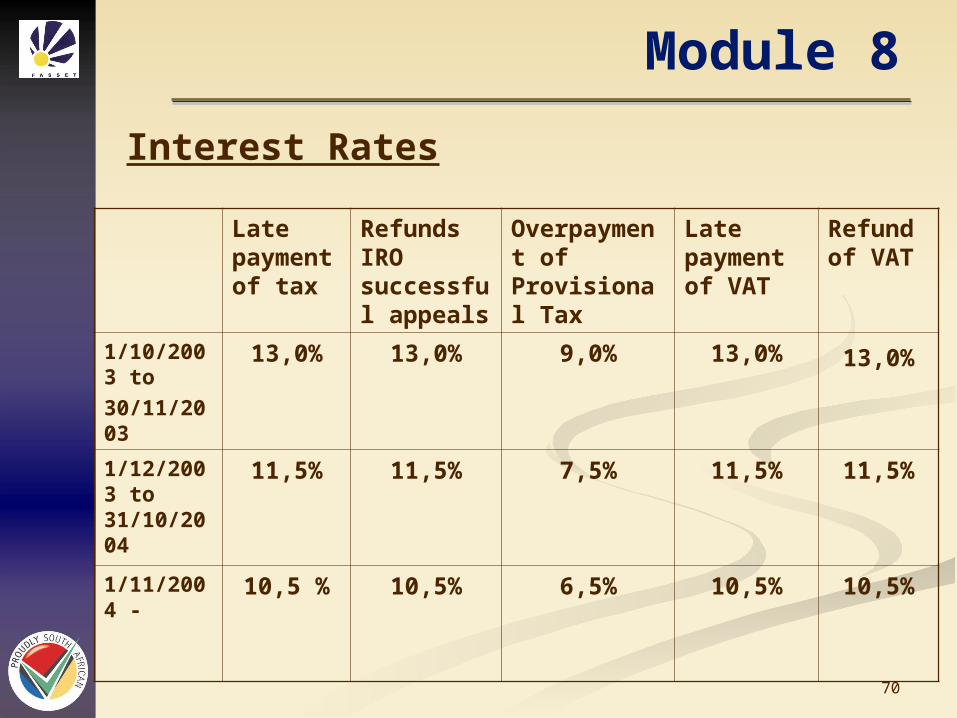

Late payment of tax

Refunds IRO successful appeals

Overpayment of Provisional Tax

Late payment of VAT

Refund of VAT

1/10/2003 to

30/11/2003

13,0% 13,0% 9,0% 13,0% 13,0%

1/12/2003 to 31/10/2004

11,5% 11,5% 7,5% 11,5% 11,5%

1/11/2004 - 10,5 % 10,5% 6,5% 10,5% 10,5%

Interest Rates

71

OtherRegistration of Tax Practitioners

All tax practitioners who provide tax advice or completes or assists in completing tax returns must have registered by 30 June 2005.

Exceptions:• Person who provide advice or completes a

return for no consideration.• Person who provides advice in anticipation or

in the course or litigation with taxpayer and SARS.

• Where advice is incidental to supply of goods or services.

• Person who provides tax services as full time employee to his employer or under the direct supervision of a registered practitioner.

• Where the tax services relate only to customs and excise.

72

Questions

Related Documents