COST TERMS AND PURPOSES © 2012 Pearson Prentice Hall. All rights reserved.

COST TERMS AND PURPOSES © 2012 Pearson Prentice Hall. All rights reserved.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COST TERMS AND PURPOSES

© 2012 Pearson Prentice Hall. All rights reserved.

© 2012 Pearson Prentice Hall. All rights reserved.

Class Announcement

See SCC for information on accounting recruitment information sessions

Assignment #1 due September 19th

Business Society Golf Tournament (Daily Schwartz on Facebook) Date: Saturday Sept 21st (Colin MacInnis, at x2010qbn) Time: tee off times begin at 12:00pm Location: Antigonish Golf & Country Club (87 Cloverville road) Team size: 4 Fee: $50/team member

Invest-X Initial Meeting on Monday September 16th in SCHW 152

2

© 2012 Pearson Prentice Hall. All rights reserved.

Class Objectives

1. Different costs for different decisions2. Various cost classification approaches3. Match information need with cost

classification approach

© 2012 Pearson Prentice Hall. All rights reserved.

Cost Accounting and Cost Management

1. Calculating the cost of products, services, and other cost objects

2. Obtaining information for planning and control, and performance evaluation

3. Analyzing the relevant information for making decisions

© 2012 Pearson Prentice Hall. All rights reserved.

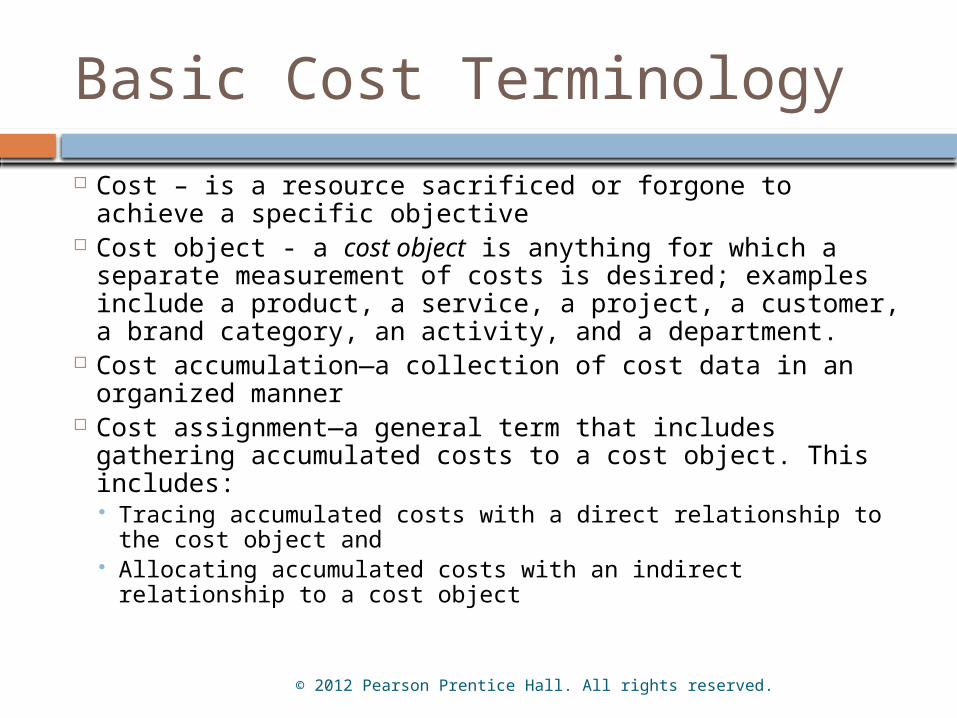

Basic Cost Terminology

Cost – is a resource sacrificed or forgone to achieve a specific objective

Cost object - a cost object is anything for which a separate measurement of costs is desired; examples include a product, a service, a project, a customer, a brand category, an activity, and a department.

Cost accumulation—a collection of cost data in an organized manner

Cost assignment—a general term that includes gathering accumulated costs to a cost object. This includes: Tracing accumulated costs with a direct relationship to the

cost object and Allocating accumulated costs with an indirect relationship to

a cost object

© 2012 Pearson Prentice Hall. All rights reserved.

Cost Classification

Costs assignment can vary in relationship to many different cost drivers.

Cost Classification is dependent on decision being made

Cost Classifications: 1) Direct and Indirect 2) Variable and Fixed 3) Manufacturing Cost Type 4) Period and Product Costs 5) Controllable and Uncontrollable 6) Other Classifications

© 2012 Pearson Prentice Hall. All rights reserved.

Cost Classification

© 2012 Pearson Prentice Hall. All rights reserved.

1) Direct and Indirect Costs

Direct costs can be conveniently and economically traced (tracked) to a cost object. See http://www.youtube.com/watch?v=vBA87iakRLI

Indirect costs cannot be conveniently or economically traced (tracked) to a cost object. Instead of being traced, these costs are allocated to a cost object in a rational and systematic manner.

Factors Affecting Direct/Indirect Cost Classification Cost materiality Availability of information-gathering technology Operational design

© 2012 Pearson Prentice Hall. All rights reserved.

1) Direct and Indirect Costs

© 2012 Pearson Prentice Hall. All rights reserved.

2) Fixed and Variable Costs

Variable costs—changes in total in proportion to changes in the related level of activity or volume.

Fixed costs—remain unchanged in total regardless of changes in the related level of activity or volume.

Costs are fixed or variable only with respect to a specific activity or a given time period.

© 2012 Pearson Prentice Hall. All rights reserved.

2) Fixed and Variable Costs

© 2012 Pearson Prentice Hall. All rights reserved.

2) Fixed and Variable Costs

Total Dollars Cost per Unit

Variable Costs

Change in proportion with

outputMore output = More cost

Fixed CostsUnchanged in

relation to output

Change inversely with output

More output = lower cost per unit

Total Dollars Cost Per Unit

Variable CostsChange in

proportion with output

More output = More cost

Unchanged in relation to output

Fixed Costs Unchanged in relation to output

Change inversely with

outputMore output = lower cost

per unit

© 2012 Pearson Prentice Hall. All rights reserved.

2) Fixed and Variable Costs

Unit costs should be used cautiously. Because unit costs change with a different level of output or volume, it may be more prudent to base decisions on a total dollar basis. Unit costs that include fixed costs should

always reference a given level of output or activity.

Unit costs are also called average costs. Managers should think in terms of total

costs rather than unit costs.

© 2012 Pearson Prentice Hall. All rights reserved.

2) Fixed and Variable Costs

Cost driver—a variable that causally affects costs over a given time span

Relevant range—the band of normal activity level (or volume) in which there is a specific relationship between the level of activity (or volume) and a given cost For example, fixed costs are considered

fixed only within the relevant range.

© 2012 Pearson Prentice Hall. All rights reserved.

3) Manufacturing Costs

Direct materials—acquisition costs of all materials that will become part of the cost object.

Direct labor—compensation of all manufacturing labor that can be traced to the cost object.

Indirect manufacturing—factory costs that are not traceable to the product in an economically feasible way. Examples include lubricants, indirect manufacturing labor, utilities, and supplies. Includes indirect labour Office, security, and management salaries Payroll fringe benefits Rework labour Idle time – wages related to unproductive time Overtime premium - – wages paid in excess of regular

wage rate

© 2012 Pearson Prentice Hall. All rights reserved.

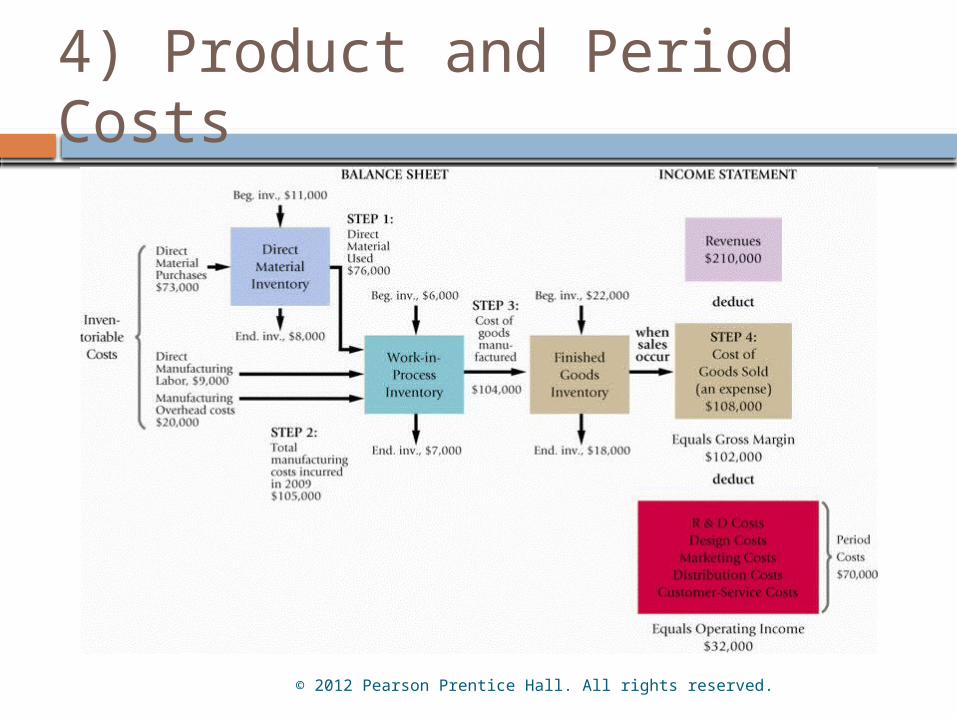

4) Product and Period Costs

Product (Inventoriable) costs—product manufacturing costs. These costs are capitalized as assets (inventory) until they are sold and transferred to Cost of Goods Sold.

Period costs—have no future value and are expensed in the period incurred(i.e., all costs other than Cost of Goods Sold).

Inventories: Raw materials—resources in-stock and available for use Work-in-process (or progress)—products started but not

yet completed, often abbreviated as WIP Finished goods—products completed and ready for sale

© 2012 Pearson Prentice Hall. All rights reserved.

4) Product and Period Costs

© 2012 Pearson Prentice Hall. All rights reserved.

5) Controllable and Uncontrollable Costs (chpt 16)

Assessing controllability of costs assists in performance measurement and evaluation

Controllable costs costs over which a manger has influence

Uncontrollable costs costs over which a manger has no

influence

© 2012 Pearson Prentice Hall. All rights reserved.

6) Prevention and Appraisal Costs (chpt 19)

Prevention Costs

Support activities whose purpose is to

reduce the number of defects

Appraisal Costs

Incurred to identify defective products

before the products are shipped

Internal Failure Costs

Incurred as a result of identifying defects

before they are shipped

External Failure Costs

Incurred as a result of defective products being delivered to

customers

© 2012 Pearson Prentice Hall. All rights reserved.

7) Other Cost Classifications (chpt 11)

Opportunity cost - benefit foregone Sunk cost - cannot be changed by future

decisions Differential cost- difference between two

decisions Marginal cost - cost of one additional unit Committed costs - long-term obligations, difficult

to change in the short term. Discretionary costs – costs that can be changed

in the short term

© 2012 Pearson Prentice Hall. All rights reserved.

Multiple Classification of Costs

Related Documents