In t h ebookso f aC om pan y C ost Sheet for t h e p er i oden d ed …….. U n i t s P r od uced ….. N ame of t h e p r od u ct unit sold …. P a rt i cu lars To tal cost Rs. U nit Cost Rs. O p eni n g st ock rawmateri al s A dd P u rchases o f RawMa t e r i a l s A dd: E x p e n se s on P u rchases of Raw M a t eria l s (oct r oi & d u t y) L ess:Closi n gs t ock of r aw materials L ess: Sale o f scra p or d efecti ves of r aw ma teri a ls = Cost of mater i al s con su med A dd: P r oductive La b ou r A dd: Outstandin g l abour A d d : Direc t E x pe n ses ( arc h itec t ’s f ee s) = Pri me cost A dd: Facto r y o v e r heads A d d : Openingstoc k o f W or k -in- p rog r ess L ess:C l osi n g st ock of Wor k- in-progress L ess: Sale o f scrap or d ef ecti ves of W or k- i n - progress = F act ory cost

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 1/16

In the books of a Company

Cost Sheet for the period ended……..

Units Produced…..

Name of the product unit sold….

Particulars Total cost

Rs.

Unit

Cost

Rs.

Opening stock raw materials

Add Purchases of Raw Materials

Add: Expenses on Purchases of RawMaterials (octroi & duty)

Less:Closing stock of raw materials

Less:Sale of scrap or defectives of raw

materials

= Cost of materials consumed

Add: Productive Labour

Add: Outstanding labour

Add: Direct Expenses( architect’s fees)

= Prime cost

Add: Factory overheads

Add: Opening stock of Work-in-progress

Less:Closing stock of Work-in-progress

Less:Sale of scrap or defectives of Work-in-

progress

= Factory cost

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 2/16

Add: Office overheads

= Cost of Production

Add: Opening Stock of Finished Goods

Less:Closing Stock of Finished Stock

= Cost of Goods Sold

Add: Selling & Distribution Overheads

= Total cost

Add ProfitLess Loss

= Sales

Statement showing distribution of overheads

Particulars Factory Office Selling &

distribution

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 3/16

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 4/16

Non cost items

ie. Items to be excluded from cost.

1.Financial Incomes:

Capital profits, dividend received, brokerage &

commission received, share transfer fees, interest on

investments, rent received , bad debts recovery, interest

on loan given.

2.Financial charges

capital losses, cash discount , trade discount, penalties &

fines, share transfer fees paid, interest on debentures,

preliminary expenses, underwriting commission,

discount on issue of shares and debentures, loss on

investment, capital expenses, interest on capital, salaryor commission paid to partner, income tax, wealth tax,

interest on debentures, reconstruction expenses,

development expenses.

3.Appropriations:

Bad debts reserve, dividends paid, charitable donations,

transfer to reserve, sinking fund, debenture redumption

fund, machinery replacement fund, investment

fluctuation fund.4.Abnormals:

Abnormal wastage, abnormal idle time, loss by fire, loss

by theft, loss of stock, insurance premium.

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 5/16

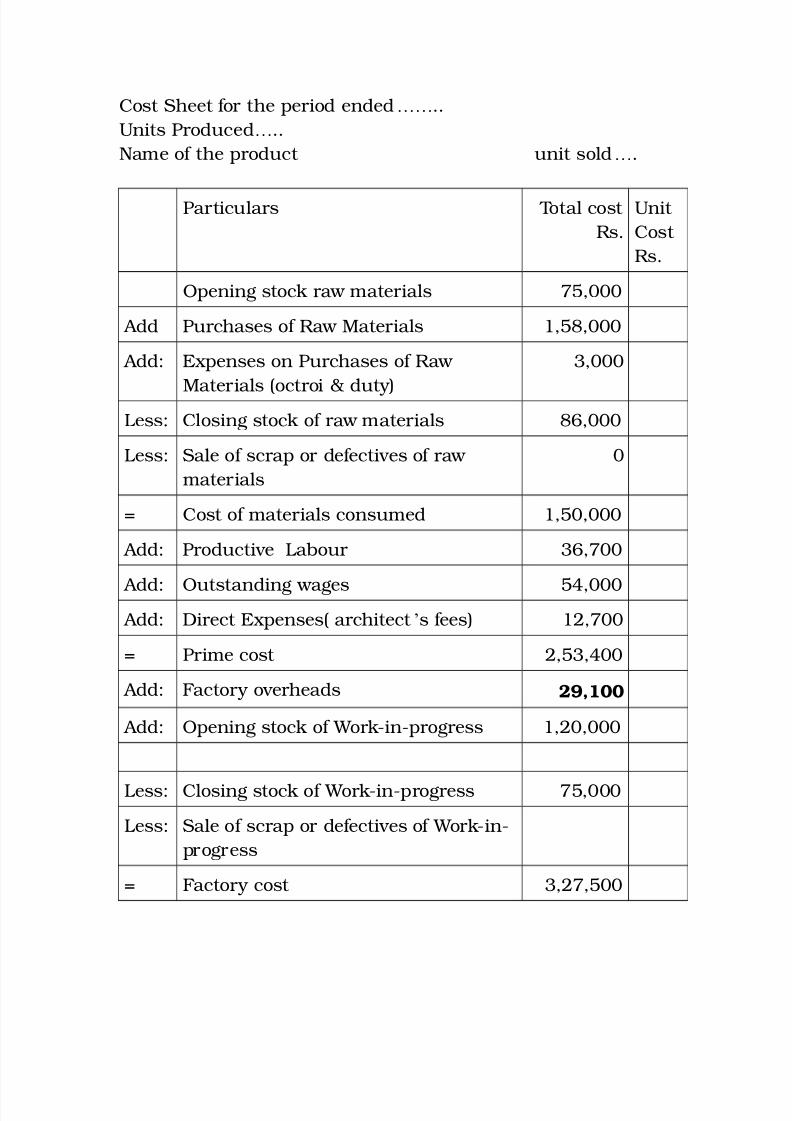

Q. 1) The cost accounts of A Ltd. Mumbai, for the year ended

31st March 2009 showed the following information.

Types of stock As on 1-4-2008 As on 31-3-2009

Raw materials 75,000 86,000

Work-in-progress 1,20,000 75,000

Finished stock 44,000 21,000

Underwriting commission 12,000

Purchase of raw material 1,58,000

Selling overheads 23,000

Drawing Office salaries 5,600

Productive Labour 36,700

Audit fees 13,900

Establishment on cost 36,000

Steam, gas and water 4,300

Sales 6,78,800

Rent 24,000

(factory 80%, office 20%)

Architect’s fees 12,700

Wages outstanding 54,000

Octroi and duty 3,000

Distribution on cost 12,800

Solution:

In the books of a Company

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 6/16

Cost Sheet for the period ended……..

Units Produced…..

Name of the product unit sold….

Particulars Total cost

Rs.

Unit

Cost

Rs.

Opening stock raw materials 75,000

Add Purchases of Raw Materials 1,58,000

Add: Expenses on Purchases of Raw

Materials (octroi & duty)

3,000

Less:Closing stock of raw materials 86,000

Less:Sale of scrap or defectives of raw

materials

0

= Cost of materials consumed 1,50,000

Add: Productive Labour 36,700

Add: Outstanding wages 54,000

Add: Direct Expenses( architect’s fees) 12,700

= Prime cost 2,53,400

Add: Factory overheads 29,100

Add: Opening stock of Work-in-progress 1,20,000

Less:Closing stock of Work-in-progress 75,000

Less:Sale of scrap or defectives of Work-in-

progress

= Factory cost 3,27,500

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 7/16

Add: Office overheads 54,700

= Cost of Production 3,82,200

Add: Opening Stock of Finished Goods 44,000

Less:Closing Stock of Finished Stock 21,000

= Cost of Goods Sold 4,05,200

Add: Selling & Distribution Overheads 35,800

= Total cost 4,41,000

Add Profit 2,37,800

Less Loss

= Sales 6,78,800

Statement showing distribution of overheads

Particulars Factory

Overheads

Office

Overheads

Selling &

distributionOverheads

Selling overheads 23,000

Drawing office salaries 5,600

Audit fees 13,900

Establishment on cost 36,000

Steam ,gas and water 4,300

Rent 19,200 4,800

Distribution on cost 12,800

Total 29,100 54,700 35,800

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 8/16

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 9/16

Problems

Q.2) The expenditure incurred in the manufacturing and

selling of product‘ A’for the three months ended 31st march

2008 is given as below: Rs.

Direct material cost 30,000

Engineers fees 1,000

Power & fuel 7,000

Wages payable 2,000

Office salary 5,000

Trade discount 500

Direct expenses 4,000

Haulage 3,000

General on cost 1,000

Catalogue expenses 1,500

Process & operating wages 13,000

Time-keeping expenses 2,000

Electricity charges 2,000

Donations 1,000

Tendering expenses 1,000

Commission on sales 2,500

Tons manufactured & sold 900

Prepare cost sheet of XYZ Ltd., Pune, showing the cost of each

element, the total cost per ton and the profits if selling price is

Rs. 120 per ton.

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 10/16

Q. 3) From the following particulars relating to M/S Shah

Brothers, prepare a simple cost sheet showing,

a.prime cost

b.works cost

c.cost of production

d.cost of sales

e.profit or loss for the period for six months ended

31.3.2009 Rs.

Cost of materials consumed 2,30,000

Oil and waste 3,000

Operating labour 32,000

Wages of foreman 44,500

Direct expenses 3,900

Stock keeper wages 40,000

Sales cash and credit 100Commission to partner 9,000

Electric power 1,000

Salary to partner 2,000

Consumable stores 500

Direct wages payable 1,00,000

Lighting

i)Factory plant 200

ii) office establishment 650

Carriage outward 1,000

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 11/16

Rent

i)factory plant 1,000

ii) machinery 2,000

iii) office premises 3,000

iv) warehouse 4,000

Interest on bank overdraft 5,500

Advertising 3,450

Depreciation

i) office building 2,000ii) machinery 4,280

Traveling expenses 6,000

Office manager’s salary 12,000

Salesman’s commission 22,000

Director’s fees 40,000

Printing & stationery 5,200

Telephone charges 6,500

Postage 3,320

Bad debts 2,900

0.

Q. 4) from the following particulars of Maharasttra Traders,

prepare a cost sheet for the year 2008-2009

Sale of scrap of raw material 500

Works overheads 45,000

Stock of raw materials as on 1-4-2008 40,000

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 12/16

Selling and distribution expenses 71,500

Wages due but not paid 4,500

Costom duty on purchases 5,500

Share transfer fees paid 1,500

Purchases of raw materials 1,50,000

Office on cost 32,500

Share transfer fees received 2,500

Stock of raw materials as on 31-3-2009 15,000

Direct wages 95,500

The company has to send a tender for the manufacture of a

machine in the year 2009-10. As per the judgment of costing

department materials of Rs. 80,000 will be required and wages

will be Rs. 50,000. The factory expenses bears the same

percentage on direct wages, office expenses bears the same

percentage on works cost and selling & distribution expenses

bear the same percentage on the cost of production as that ofthe year 2008-09. The tender is to be made at a profit of 25 %

on market price.

Q. 5) Prepare a cost sheet with the help of the following

information. Give statement of cost and profit valuing closing

stock on the basis of LIFO, FIFO AND Weighted average cost

separately.

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 13/16

Opening stock:

• Raw materials:

• Work in

progress:

• Finished goods:

(1000 units)

Purchase of raw

material

Direct labour

Direct power

Indirect power

Indirect material

Other factory

expenses

10,000

30,000

80,000

1,00,000

3,00,000

20,000

6,000

24,000

30,000

Show room expenses

Selling commission

@ 5 % on sales

Other selling

expenses

Office & Admn.

Overheads

Sales ( 12,000 units)

Closing Stock:

• Raw materials:

• Work in

progress:

• Finished goods:

(4000 units )

40,000

15,000

60,000

15,000

18,000

Selling price Rs. 100 per unit.

Q. 6) The books & records of AB manufacturing company,

present the following data for the month of January 2009:

Direct Labour cost :Rs. 16,000 (160 % of factory overheads)

Cost of Goods sold : Rs. 56,000

Inventory accounts showed these opening and closing

balances:

January 1 January 31

Raw materials Rs. 8,000 Rs. 8,600

Work-in-progress 8,000 12,000

Finished goods 14,000 18,000

Other data: selling Expenses Rs. 3,400; General Expenses

Rs.2,600; Sales for the month Rs. 75,000. You are required to

prepare a statement showing cost of goods manufactured and

sold and profit earned.

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 14/16

Q. 7) The following data pertains to Mr. Y for the month of

March 2009:

Direct material used

Opening finished

goods stock

Closing finished stock

Direct manufacturing

labour

Rs.

847

?

94

389

Manufacturing

overhead

Cost of goods

manufactured

Cost of goods sold

Cost of goods

available for sale

Rs.

?

1,878

?

1,949

Find out the missing items and the statement of cost for

March 2009.

Q. 8) Raw materials‘ X’costing Rs. 100 per KG and‘ Y’costing

Rs. 60 per KG are mixed in equal proportions for making

product‘ A’. The loss of materials in processing works out to

25 % of the output. The production expenses are allocated at

50 % of direct material cost. The end product is priced with a

margin of 33 % over the total cost. Material‘ Y’is not easily

available and substitute material‘Z’has been found for‘ y’

costing Rs. 50 per KG. It is required to keep the proportion of

this substitute material in the mixture as low as possible and

the same time maintain the selling price of the end product at

existing levels and ensure the same quantum of profit as at

present.

Q.9) The following details are available from the books of Ram

products Ltd. for the year ending 31st March 2007:

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 15/16

Direct wages 6,00,000Printing &

stationery

12,000

Purchase of

materials

7,20,000Counting house

salary

12,000

Other materials 36,000Carriage outwards 8,640

Wages of foremen

and stores keeper

48,000Other indirect

wages

6,000

Cost of research

and experiments

30,000Office manager’s

salary

72,000

Power fuel and

haulage

54,000Drawing office

salary

36,000

Closing stock of -

Raw materials

Work in progress

Finished goods

( 12,000 units)

1,33,440

96,000

1,95,000

Opening stock of -

Raw materials

Work in progress

Finished goods

(6,000 units)

1,20,000

28,800

97,500

Sales 18,00,000Income tax

Donations

22,000

5,000

Selling and distribution expenses are to be charged at Re. 1

per unit sold. During this year total units produced were

96,000. Prepare a cost sheet showing different elements of cost

and the profit.

Q. 10) The following are the details of 14 H.P. motor cars

produced by Zen & Co Ltd. for the year ending 31st March

2007:

Opening stock of Raw materials Rs. 50,000

Works overheads Rs. 1, 96,000

Purchases Rs. 12, 00,000

Establishment charges Rs 1, 49,170

8/9/2019 Cost Sheet Examples

http://slidepdf.com/reader/full/cost-sheet-examples 16/16

Carriage Rs. 60,000

Wages Rs. 7, 00,000

Closing stock of Raw materials Rs. 75,000

1.Find out the works cost & the total cost of motor cars,percentage the works overheads bears to wages and

percentage that establishment charges bears to works

cost.

2.Work out what price a co should quote for a motor car,

which is estimated will require on expenditure of Rs.5,500

in raw material and Rs. 4,000 in wages, so that it would

yield a profit of 25% on quotation price.

Related Documents