Corporate Financial Policy 2007-2008 WACC Professor André Farber Solvay Business School Université Libre de Bruxelles

Corporate Financial Policy 2007-2008 WACC Professor André Farber Solvay Business School Université Libre de Bruxelles.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Corporate Financial Policy2007-2008WACC

Professor André Farber

Solvay Business School

Université Libre de Bruxelles

Advanced Finance 2008 03 WACC |2April 18, 2023

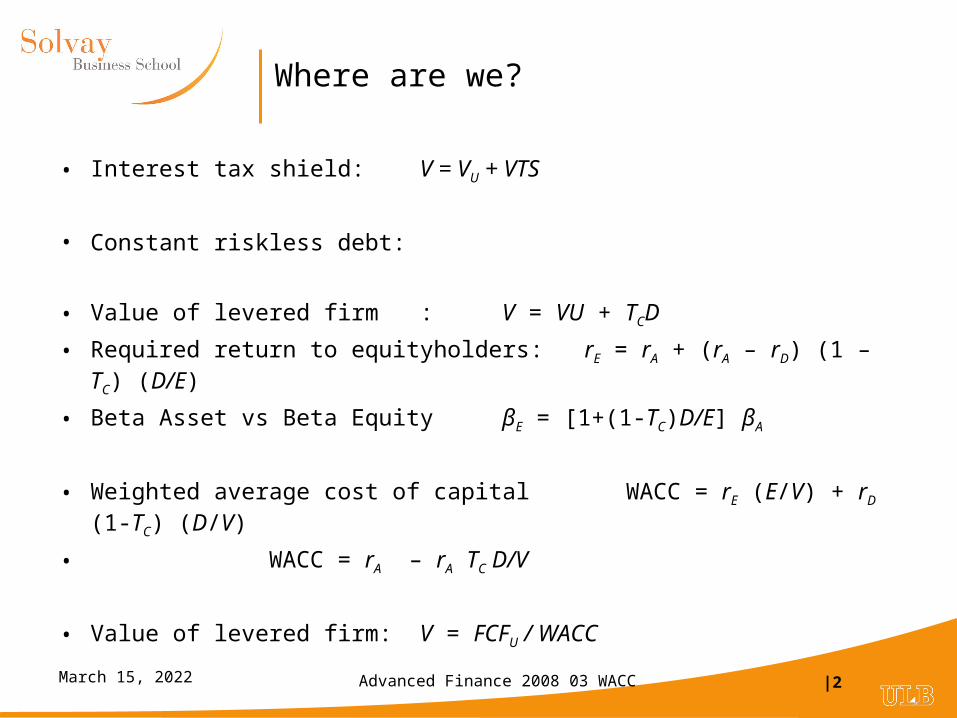

Where are we?

• Interest tax shield: V = VU + VTS

• Constant riskless debt:

• Value of levered firm : V = VU + TCD

• Required return to equityholders: rE = rA + (rA – rD) (1 – TC) (D/E)

• Beta Asset vs Beta Equity βE = [1+(1-TC)D/E] βA

• Weighted average cost of capital WACC = rE (E/V) + rD (1-TC) (D/V)

• WACC = rA – rA TC D/V

• Value of levered firm: V = FCFU / WACC

Advanced Finance 2008 03 WACC |3April 18, 2023

How to value a levered company?

• Value of levered company: V = VU + VTS = E + D

• In general, WACC changes over time

)1(1

1

1

1,11

t

tD

t

ttEtttCDt V

Dr

V

ErVVDTrFCF

)1(

))1(1(

1

1

1

1

1,1

tt

t

tCD

t

ttEttt

WACCV

V

DTr

V

ErVVFCF

Rearrange:

Solve:

t

ttt WACC

VFCFV

11

Expected payoff =Free cash flow unlevered

+ Interest Tax Shield+ Expected value

Expected return for debt and equity investors

Advanced Finance 2008 03 WACC |4April 18, 2023

Comments

• In general, the WACC changes over time. But to be useful, we should have a constant WACC to use as the discount rate. This can be obtained by restricting the financing policy.

• 2 possible financing rules:

• Rule 1: Debt fixed

• Borrow a fraction of initial project value

» Interest tax shields are constant. They are discounted at the cost of debt.

• Rule 2: Debt rebalanced

• Adjust the debt in each future period to keep it at a constant fraction of future project value.

» Interest tax shields vary. They are discounted at the opportunity cost of capital (except, possibly, for next tax shield –cf Miles and Ezzel)

Advanced Finance 2008 03 WACC |5April 18, 2023

A general framework

Value of all-equity firm

Value of tax shield

Value of equity

Value of debt

V = VU + VTS = E + D

rE

rD

rA

rTS

V

Dr

V

Er

V

VTSr

V

Vr DETS

UA

Advanced Finance 2008 03 WACC |6April 18, 2023

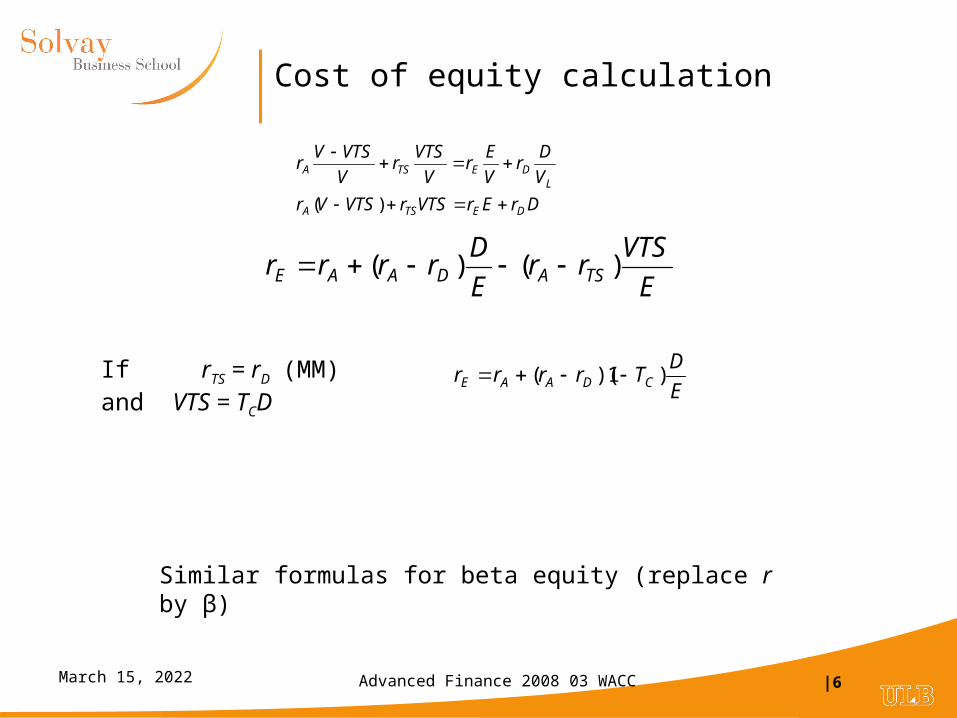

Cost of equity calculation

DrErVTSrVTSVr

V

Dr

V

Er

V

VTSr

V

VTSVr

DETSA

LDETSA

)(

E

DTrrrr CDAAE )1)(( If rTS = rD (MM)

and VTS = TCD

Similar formulas for beta equity (replace r by β)

E

VTSrr

E

Drrrr TSADAAE )()(

Advanced Finance 2008 03 WACC |7April 18, 2023

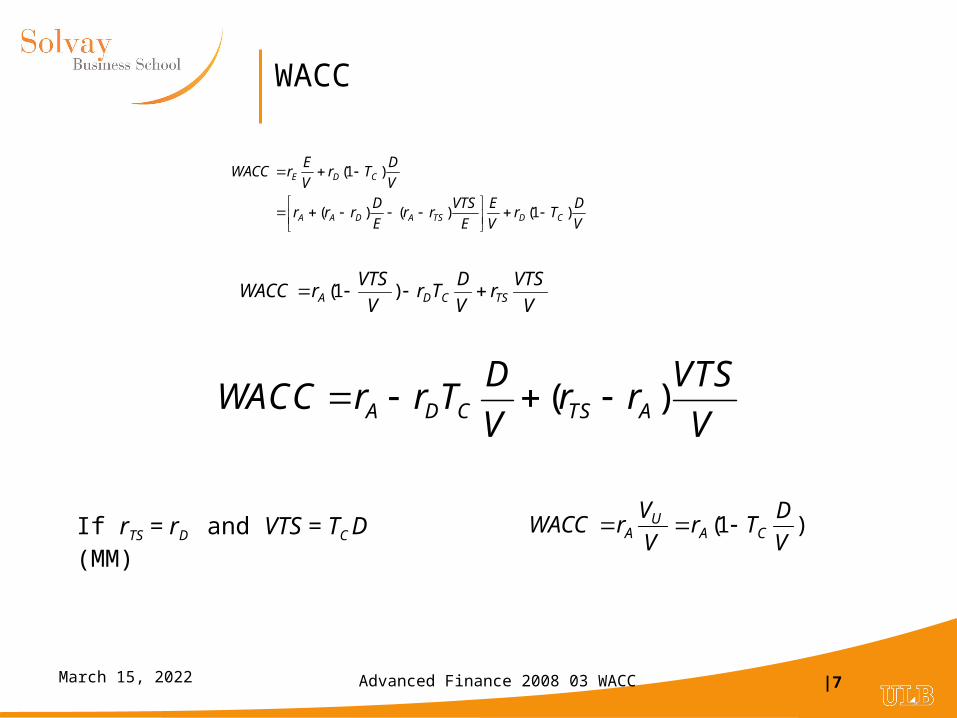

WACC

V

DTr

V

E

E

VTSrr

E

Drrr

V

DTr

V

ErWACC

CDTSADAA

CDE

)1()()(

)1(

)1(V

DTr

V

VrWACC CA

UA

V

VTSr

V

DTr

V

VTSrWACC TSCDA )1(

If rTS = rD and VTS = TC D (MM)

( )A D C TS A

D VTSWACC r r T r r

V V

Advanced Finance 2008 03 WACC |8April 18, 2023

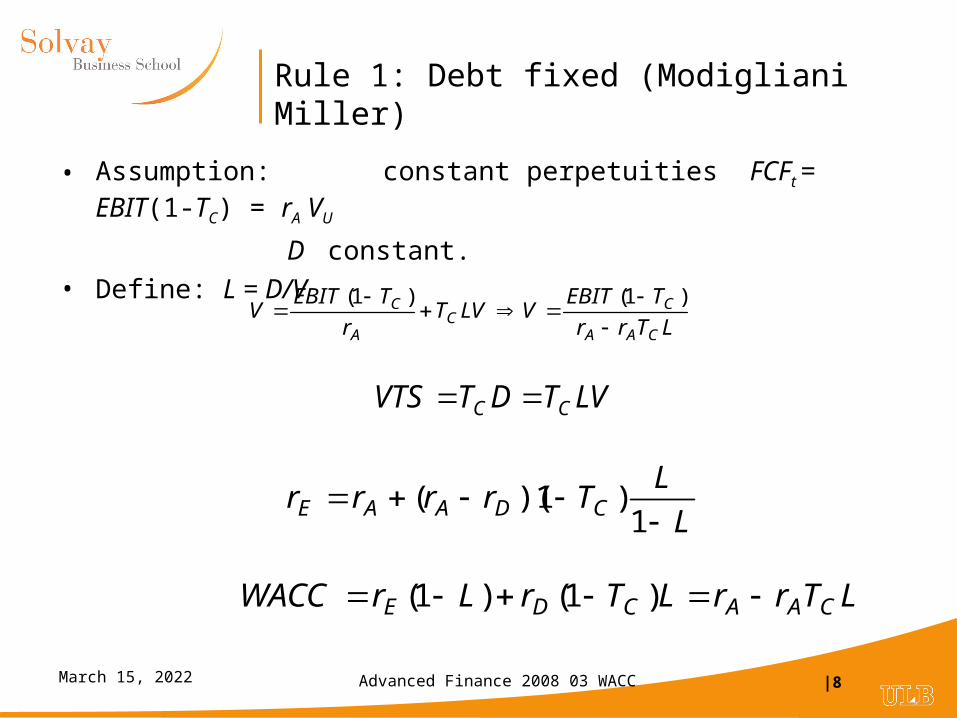

Rule 1: Debt fixed (Modigliani Miller)

• Assumption: constant perpetuities FCFt = EBIT(1-TC) = rA VU

D constant.

• Define: L = D/V

LTrr

TEBITVLVT

r

TEBITV

CAA

CC

A

C

)1()1(

LTrrLTrLrWACC CAACDE )1()1(

L

LTrrrr CDAAE

1

)1)((

LVTDTVTS CC

Advanced Finance 2008 03 WACC |9April 18, 2023

Rule 2a: Debt rebalanced (Miles Ezzel)

D

ACDA

ttt

D

tCD

A

ttt

r

rLTrr

VFCFV

r

LVTr

r

VFCFV

1

1111

111

D

ACDACDE r

rLTrrLTrLrWACC

1

1)1()1(

D

ACDA

ttU

CD

CDt

r

rLTrr

VTSV

LTr

LTrVTS

1

11)1(1

1,

Assumption: any cash flowsDebt rebalanced Dt/Vt = L ( a constant)

L

L

r

rrTrrrr

D

DACDAAE

1

)]1

1([

Advanced Finance 2008 03 WACC |10April 18, 2023

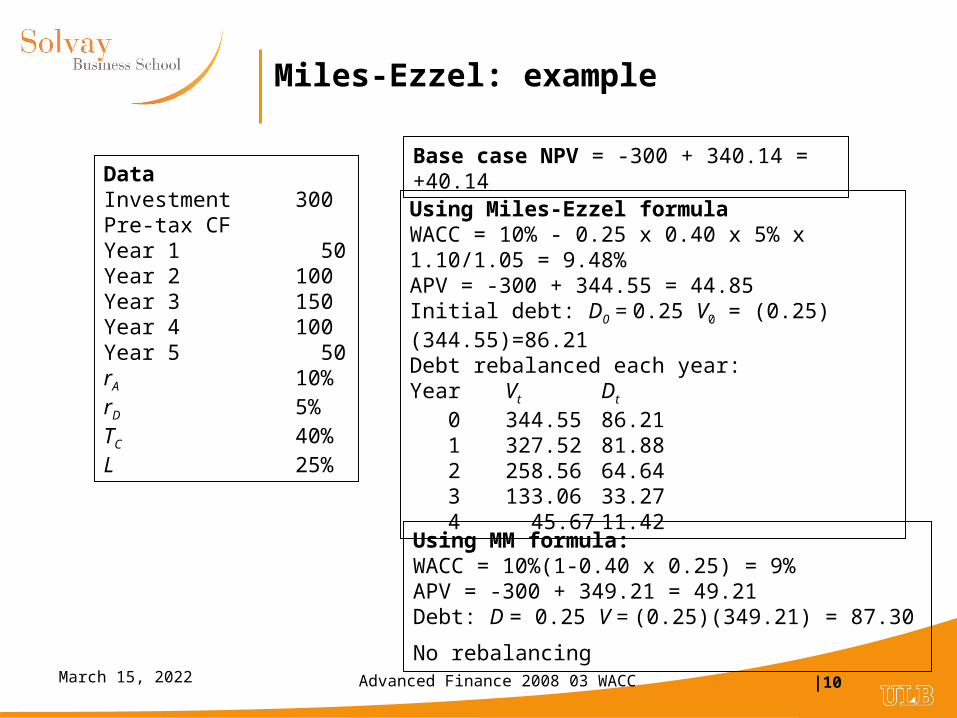

Miles-Ezzel: example

DataInvestment 300Pre-tax CFYear 1 50Year 2 100Year 3 150Year 4 100Year 5 50rA 10%rD 5%TC 40%L 25%

Base case NPV = -300 + 340.14 = +40.14

Using Miles-Ezzel formulaWACC = 10% - 0.25 x 0.40 x 5% x 1.10/1.05 = 9.48%APV = -300 + 344.55 = 44.85Initial debt: D0 = 0.25 V0 = (0.25)(344.55)=86.21Debt rebalanced each year:Year Vt Dt

0 344.55 86.21 1 327.52 81.88 2 258.56 64.64 3 133.06 33.27 4 45.67 11.42

Using MM formula:WACC = 10%(1-0.40 x 0.25) = 9%APV = -300 + 349.21 = 49.21Debt: D = 0.25 V = (0.25)(349.21) = 87.30

No rebalancing

Advanced Finance 2008 03 WACC |11April 18, 2023

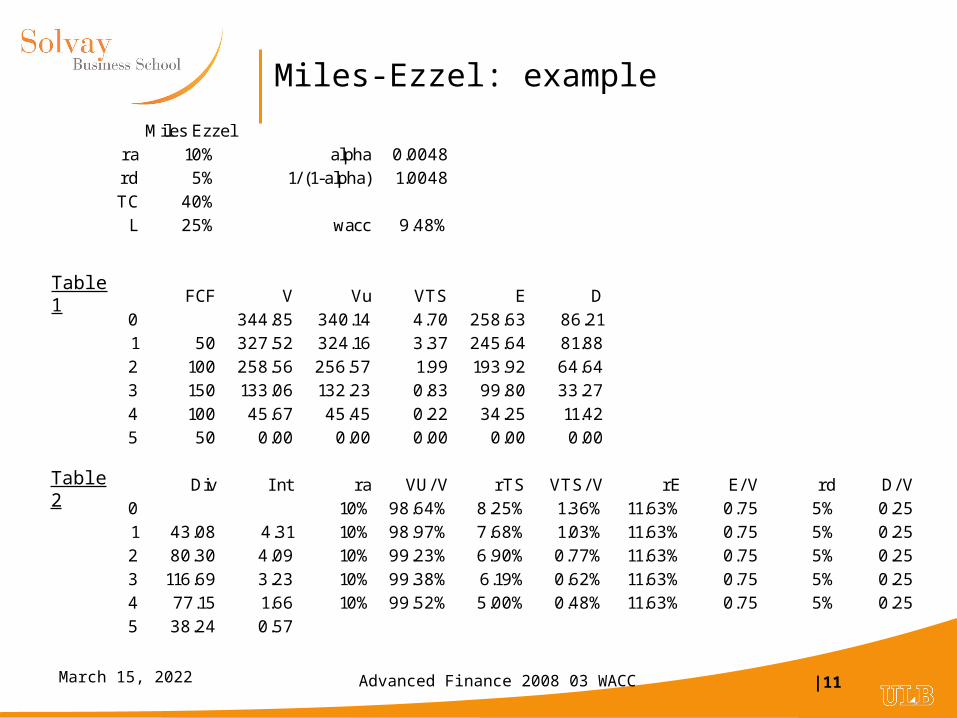

Miles-Ezzel: example

Miles Ezzelra 10% alpha 0.0048rd 5% 1/ (1-alpha) 1.0048TC 40%

L 25% wacc 9.48%

FCF V Vu VTS E D0 344.85 340.14 4.70 258.63 86.211 50 327.52 324.16 3.37 245.64 81.882 100 258.56 256.57 1.99 193.92 64.643 150 133.06 132.23 0.83 99.80 33.274 100 45.67 45.45 0.22 34.25 11.425 50 0.00 0.00 0.00 0.00 0.00

Div I nt ra VU/ V rTS VTS/ V rE E/ V rd D/ V0 10% 98.64% 8.25% 1.36% 11.63% 0.75 5% 0.251 43.08 4.31 10% 98.97% 7.68% 1.03% 11.63% 0.75 5% 0.252 80.30 4.09 10% 99.23% 6.90% 0.77% 11.63% 0.75 5% 0.253 116.69 3.23 10% 99.38% 6.19% 0.62% 11.63% 0.75 5% 0.254 77.15 1.66 10% 99.52% 5.00% 0.48% 11.63% 0.75 5% 0.255 38.24 0.57

Table 1

Table 2

Advanced Finance 2008 03 WACC |12April 18, 2023

Rule 2b: Debt rebalanced (Harris & Pringle)

LTrrLTrLrWACC CDACDE )1()1(

L

Lrrrr DAAE

1

)(

Any free cash flows – debt rebalanced continously Dt = L Vt

The risk of the tax shield is equal to the risk of the unlevered firm

rTS = rA

LTrr

VTSV

LTr

LTrVTS

CDA

ttU

CA

CDt

1)1(11

,

Advanced Finance 2008 03 WACC |13April 18, 2023

Harris-Pringle: exampleHarris Pringle

ra 10% alpha 0.0045rd 5% 1/ (1-alpha) 1.0046TC 40%

L 25% wacc 9.50%

FCF V Vu VTS E D0 344.63 340.14 4.49 258.47 86.161 50 327.37 324.16 3.21 245.53 81.842 100 258.47 256.57 1.90 193.85 64.623 150 133.02 132.23 0.79 99.77 33.264 100 45.66 45.45 0.21 34.25 11.425 50 0.00 0.00 0.00 0.00 0.00

Div I nt ra VU/ V rTS VTS/ V rE E/ V rd D/ V0 10% 98.70% 10.00% 1.30% 11.67% 0.75 5% 0.251 43.10 4.31 10% 99.02% 10.00% 0.98% 11.67% 0.75 5% 0.252 80.32 4.09 10% 99.27% 10.00% 0.73% 11.67% 0.75 5% 0.253 116.70 3.23 10% 99.40% 10.00% 0.60% 11.67% 0.75 5% 0.254 77.16 1.66 10% 99.55% 10.00% 0.45% 11.67% 0.75 5% 0.255 38.24 0.57

Advanced Finance 2008 03 WACC |14April 18, 2023

Summary of Formulas

Modigliani Miller Miles Ezzel Harris-Pringle

Operating CF Perpetuity Finite or Perpetual Finite of Perpetual

Debt level Certain Uncertain Uncertain

First tax shield Certain Certain Uncertain

WACC

L = D/V

rE(E/V) + rD(1-TC)(D/V)

rA (1 – TC L) rA – rD TC L

Cost of equity rA+(rA –rD)(1-TC)(D/E) rA+(rA –rD) (D/E)

Beta equity βA+(βA – βD) (1-TC) (D/E) βA +( βA – βD) (D/E)

D

ACDA r

rLTrr

1

1

Source: Taggart – Consistent Valuation and Cost of Capital Expressions With Corporate and Personal Taxes Financial Management Autumn 1991

E

D

r

rrTrrr

D

DACDAA )]

11([

D

CDA r

LTr

E

D

1

)1(1)1(

Advanced Finance 2008 03 WACC |15April 18, 2023

Constant perpetual growth

• Which formula to use if unlevered free cash flows growth at a constant rate?

gWACC

FCFV

1

0

Growth 5%

Risk f ree rate 6%

Unlevered beta 1

Equity premium 4%

Beta debt 0.25

Tax rate 40%

Total asset 2,000

I nitial debt 500

I nitial f ree cash flow if g=0 192

Unlevered cost of equity 10.0%

Cost of debt 7.00%

I nitial f ree cash flow 92

Value of unlevered company 1,840

MM Miles-Ezzel Harris-Pringle Fernandez

L 23.50% 23.58%

Value of tax shield 700 288 280 400

Value of levered company 2,540 2,128 2,120 2,240

Debt 500 500 500 500

Equity 2,040 1,628 1,620 1,740

WACC 8.62% 9.32% 9.34% 9.11%

Cost of equity 9.71% 10.90% 10.93% 10.52%

Cost of tax shield 7.00% 9.86% 10.00% 8.50%

Advanced Finance 2008 03 WACC |16April 18, 2023

Varying debt levels

• How to proceed if none of the financing rules applies?

• Two important instances:

• (i) debt policy defined as an amount of borrowing instead of as a target percentage of value

• (ii) the amount of debt changes over time

• Use the Capital Cash Flow method suggested by Ruback

• (Ruback, Richard A Note on Capital Cash Flow Valuation, Harvard Business School, 9-295-069, January 1995)

Advanced Finance 2008 03 WACC |17April 18, 2023

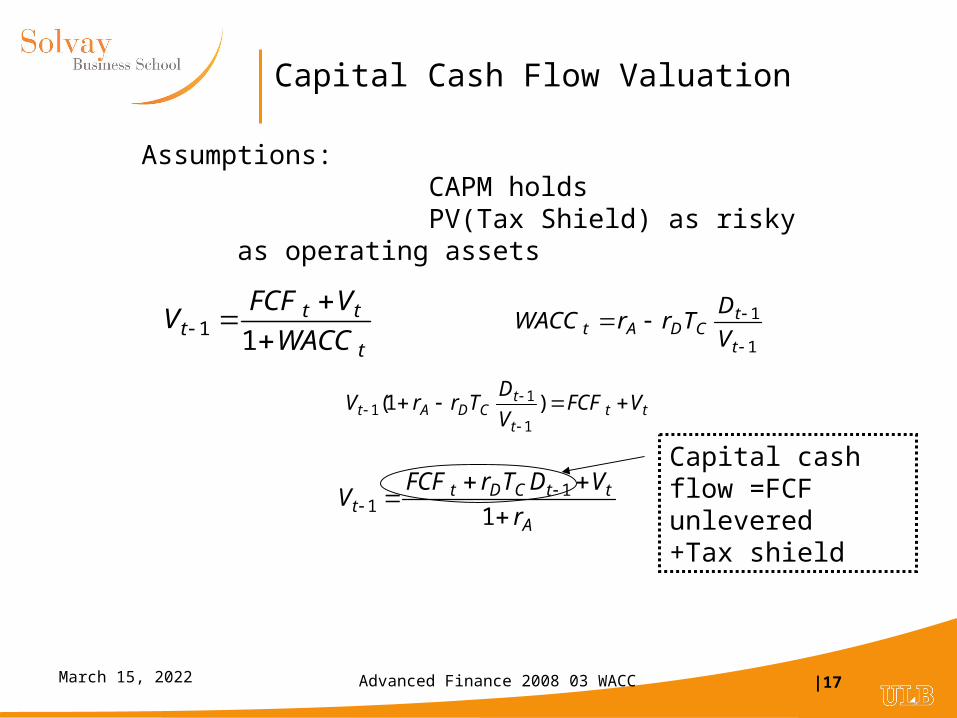

Capital Cash Flow Valuation

t

ttt WACC

VFCFV

11

Assumptions:CAPM holdsPV(Tax Shield) as risky as operating

assets

1

1

t

tCDAt V

DTrrWACC

ttt

tCDAt VFCF

V

DTrrV

)1(

1

11

A

ttCDtt r

VDTrFCFV

1

11

Capital cash flow =FCF unlevered+Tax shield

Advanced Finance 2008 03 WACC |18April 18, 2023

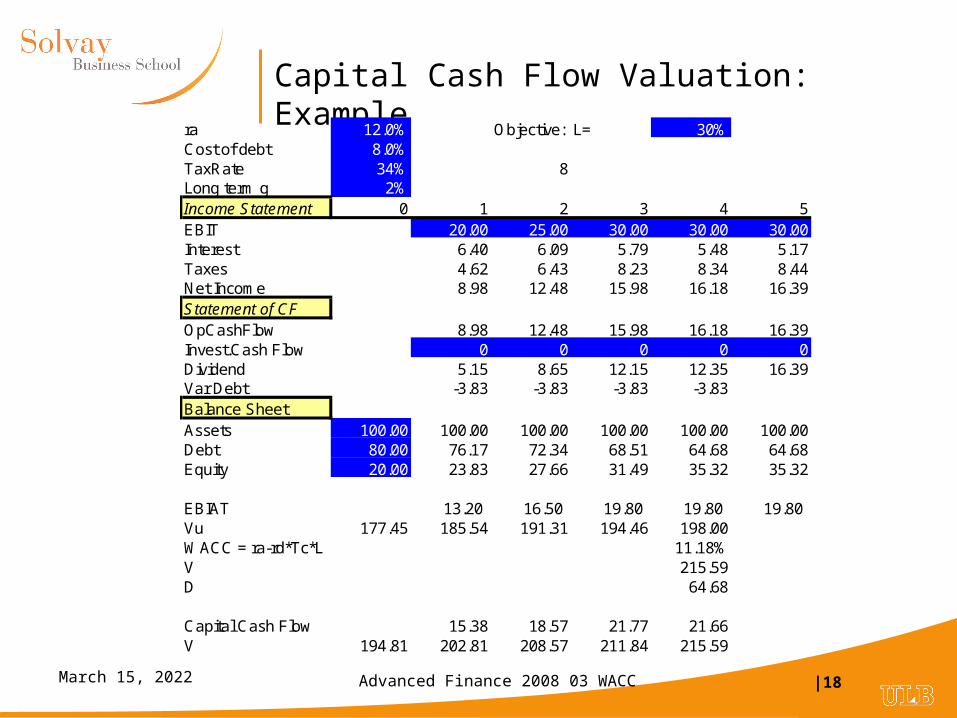

Capital Cash Flow Valuation: Example

ra 12.0% Objective: L= 30%Cost of debt 8.0%TaxRate 34% 8Long term g 2%Income Statement 0 1 2 3 4 5EBIT 20.00 25.00 30.00 30.00 30.00Interest 6.40 6.09 5.79 5.48 5.17Taxes 4.62 6.43 8.23 8.34 8.44Net Income 8.98 12.48 15.98 16.18 16.39Statement of CFOpCashFlow 8.98 12.48 15.98 16.18 16.39Invest.Cash Flow 0 0 0 0 0Dividend 5.15 8.65 12.15 12.35 16.39Var Debt -3.83 -3.83 -3.83 -3.83Balance SheetAssets 100.00 100.00 100.00 100.00 100.00 100.00Debt 80.00 76.17 72.34 68.51 64.68 64.68Equity 20.00 23.83 27.66 31.49 35.32 35.32

EBIAT 13.20 16.50 19.80 19.80 19.80 Vu 177.45 185.54 191.31 194.46 198.00WACC = ra-rd*Tc*L 11.18%V 215.59D 64.68

Capital Cash Flow 15.38 18.57 21.77 21.66V 194.81 202.81 208.57 211.84 215.59

Advanced Finance 2008 03 WACC |19April 18, 2023

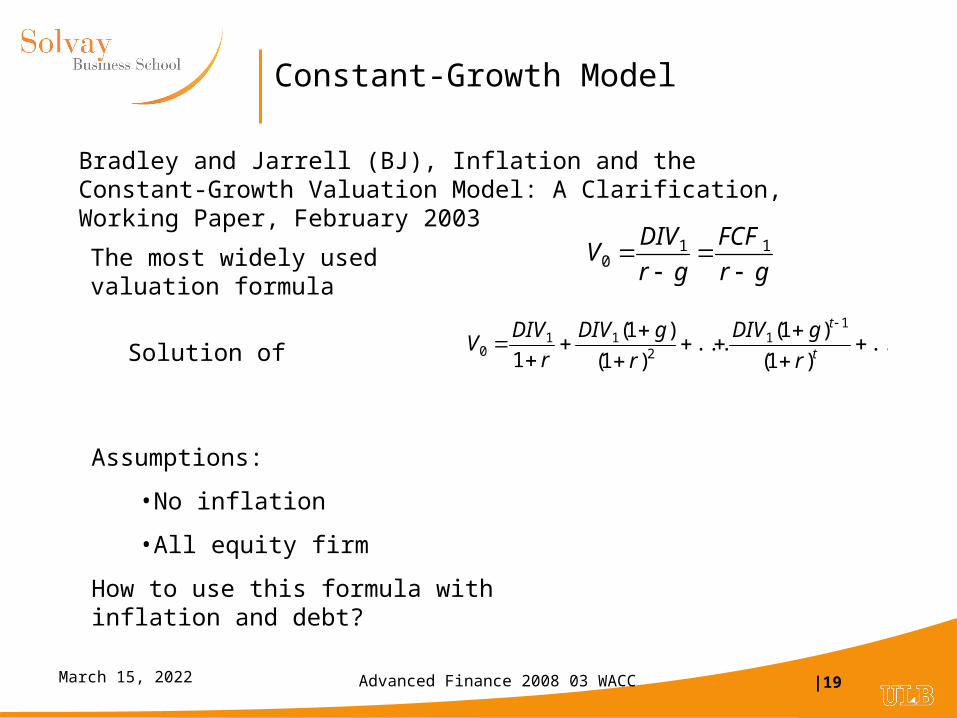

Constant-Growth Model

gr

FCF

gr

DIVV

11

0

...)1(

)1(...

)1(

)1(

1

11

211

0

t

t

r

gDIV

r

gDIV

r

DIVV

The most widely used valuation formula

Solution of

Assumptions:

•No inflation

•All equity firm

How to use this formula with inflation and debt?

Bradley and Jarrell (BJ), Inflation and the Constant-Growth Valuation Model: A Clarification, Working Paper, February 2003

Advanced Finance 2008 03 WACC |20April 18, 2023

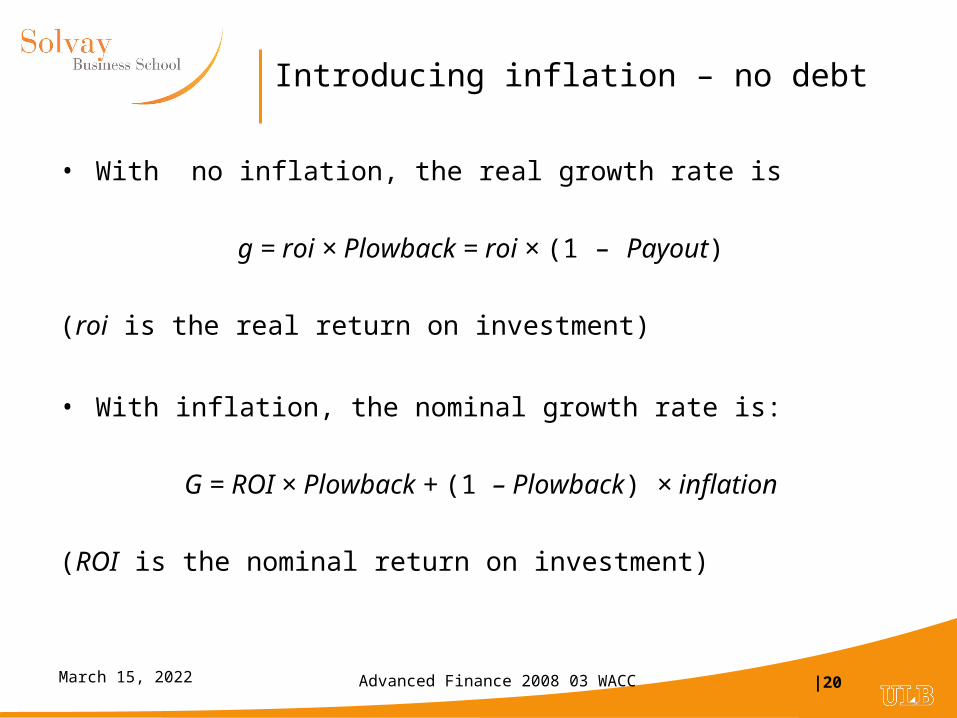

Introducing inflation – no debt

• With no inflation, the real growth rate is

g = roi × Plowback = roi × (1 – Payout)

(roi is the real return on investment)

• With inflation, the nominal growth rate is:

G = ROI × Plowback + (1 – Plowback) × inflation

(ROI is the nominal return on investment)

Advanced Finance 2008 03 WACC |21April 18, 2023

Growth in nominal earnings - details

)1(1 iroiKEBIAT tt

ttttt WCRCAPEXiDepKK )1)(( 11

)1(1 iDepREX tt

)1()()1( 1 iroiWCRNNIKiroiiEBIAT tttt

)1( iroiPlowbackiG

BJ(16)

BJ(17)

BJ(20)

BJ(23)

iPlowbackROIPlowbackG )1(BJ(27)

EBIAT=EBIT(1 – TC)K = total capital (book value)CAPEX = REX + NNIREX = replacement expendituresNNI = net new investments

iroiiroiiroiROI 1)1)(1(

Advanced Finance 2008 03 WACC |22April 18, 2023

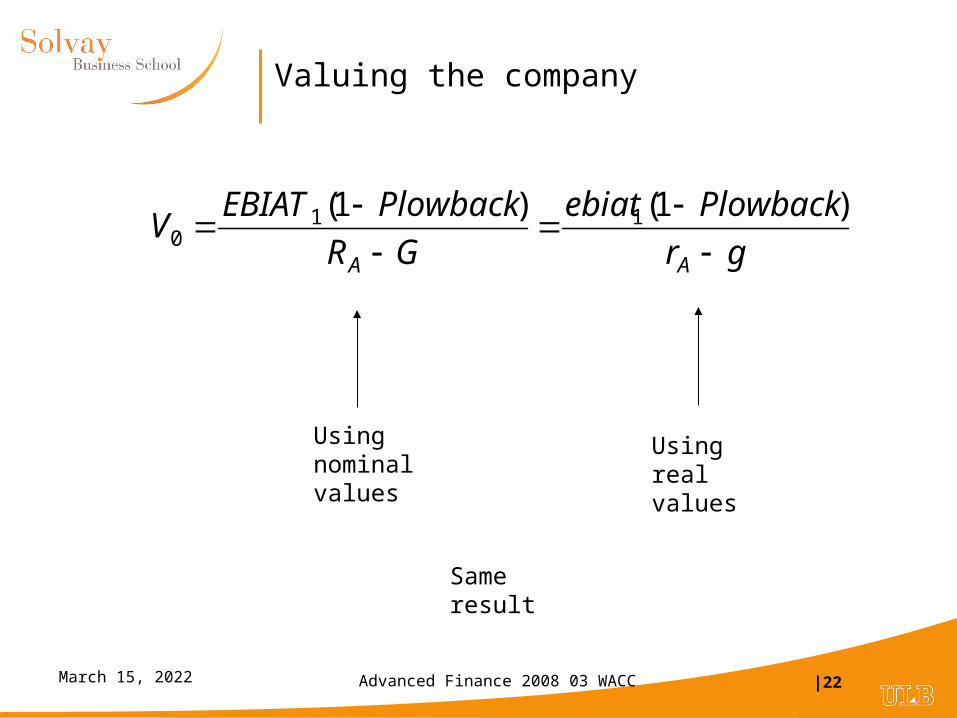

Valuing the company

gr

Plowbackebiat

GR

PlowbackEBIATV

AA

)1()1( 110

Using nominal values

Using real values

Same result

Advanced Finance 2008 03 WACC |23April 18, 2023

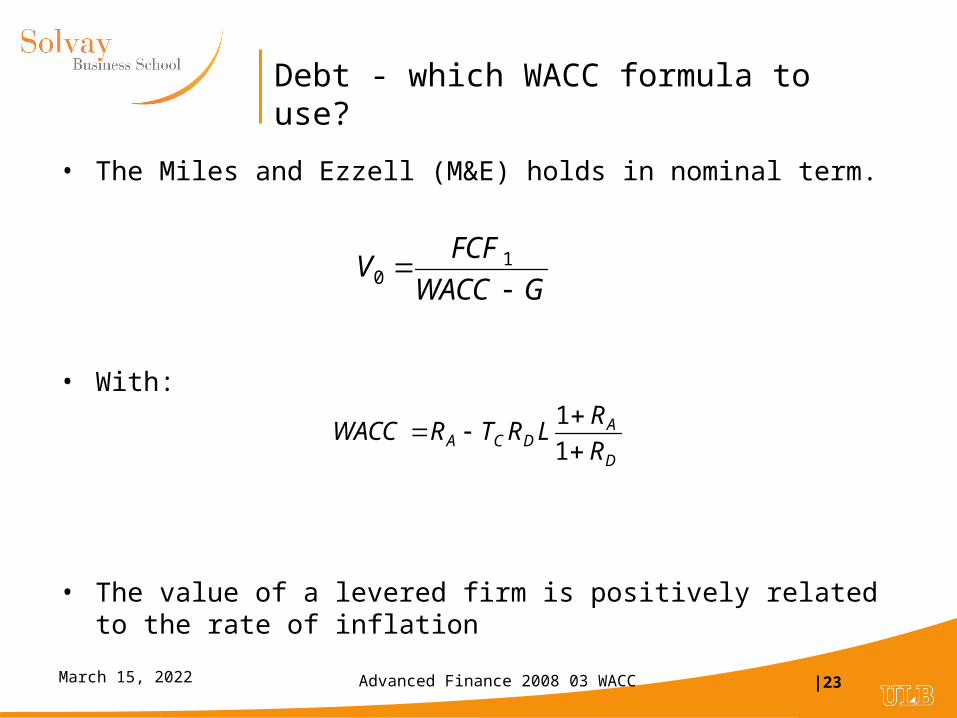

Debt - which WACC formula to use?

• The Miles and Ezzell (M&E) holds in nominal term.

• With:

• The value of a levered firm is positively related to the rate of inflation

GWACC

FCFV

1

0

D

ADCA R

RLRTRWACC

1

1

Advanced Finance 2008 03 WACC |24April 18, 2023

Interest tax shield and inflation

Borrow €1,000 for 1 yearReal cost of debt 3%Tax rate 40%1. Inflation 0%Interest year 1 €30Tax shield €122. Suppose inflation = 2%Nominal cost of debt 5.06%Nominal interest year 1 €50.60Nominal tax shield €20.24Real tax shield €19.84

Borrow RepayNominal €1,000.0 €1,000.0Real €1,000.0 €980.4Difference -€19.6

This difference is compensated by a higher interestNominal interest year 1 €50.6Real interest (adjusted for inflation) €30.60Repayment of real principal €20.00

Repayment of real principal is tax deductible→higher tax shield

Related Documents