(Wholly owned subsidiary of Bank of Baroda) Exhibit 1: Financial summary (Rs mn) Year end: March FY13 FY14 FY15 FY16e FY17e FY18e Net sales 1,614 1,747 1,683 2,289 3,548 5,890 Growth (%) 29.1 8.3 -3.7 36.0 55.0 66.0 Operating margin (%) 4.7 5.9 1.9 7.3 8.2 10.0 PAT 53 77 9 115 209 433 Adjusted PAT 53 77 9 115 209 433 EPS (Rs) 1.9 2.8 0.3 4.2 7.5 15.7 Growth (%) -19.8 44.3 -88.4 1182.1 81.9 107.6 P/E(x) 64.9 36.8 499.5 39.5 21.7 10.5 ROE (%) 6.5 7.1 0.8 8.8 13.4 23.1 ROCE (%) 7.5 8.4 1.3 9.4 13.8 23.3 Debt/equity (x) 0.12 0.01 0.00 0.00 0.00 0.00 P/Bv (x) 3.3 2.5 3.9 3.1 2.7 2.2 Source: Company, BOBCAPSe EPC Industrie Ltd. (Mahindra & Mahindra Group Co.) If there is any company which can benefit out of Pradhan Mantri Krishi Sinchhayi Yojana (PMKSY) then its Mahindra’s EPC; initiate with BUY The government under the Pradhan Mantri Krishi Sinchayi Yojana (PMKSY) launched mega irrigation scheme worth Rs 500bn which will give a boost to irrigation sector as a whole. EPC Industrie (EPC) presently has 5.5% market share in the micro irrigation space. We initiate coverage on EPC with a BUY rating and a price target of Rs 313 implying 91% upside. We expect EPC’s revenue/earnings to grow at a CAGR of ~52%/264% respectively over FY15-18e led by 1) PMKSY scheme of Rs 500bn over five years, 2) ~2600 dealers network spread over 17 states 3) strong parentage of M&M, 4) well established product portfolio. Huge opportunities laying; as Govt launches mega irrigation scheme of Rs 500bn under PMKSY: The union cabinet under the Pradhan Mantri Krishi Sinchayi Yojana (PMKSY) launched mega irrigation scheme worth Rs 500bn (spent over next five years; for FY16 the allocation is of Rs 53bn). This scheme will focus on improving irrigation in non-rain-fed areas as well as strive to improve water efficiency through the country. India is a second largest country under crop cultivation (~142 mn ha.). Even though ~60% of the cultivated land is still dependent on the monsoons for the cultivation. The PMKSY aims to ensure access to some means of protective irrigation to all agricultural farms in the country, to produce 'per drop more crop'. Higher Scope for expansion in market share, profitability: At present Jain Irrigation is a market leader with ~55% market share followed by private player Netafim India (~20% market share). We believe, going forward EPC can easily expand its market share (~5.5% to ~15%) and profitability (~ led by 1) strong support from the parent company (M&M), 2) EPC can also use M&M’s agri business network for its own expansion, 3) EPS has better debtors days and Debt to Equity ratios than its peers, we further believe, EPC can improve upon its margin once economies of scale take place. (Market leader Jain Irrigation enjoys~12% EBITDA margins.) Consumers reach through strong network of channel partners: EPC currently has ~2600 channel partners spread in ~17 states. MIS sales are driven by strong demand in states like Gujarat, Rajasthan, Madhya Pradesh Maharashtra, Karnataka, Andhra Pradesh, Tamil Nadu, Rajasthan and Haryana. The strong network with the help of parent company M&M can help EPC to expand its reach pan India level. Valuation: At CMP of Rs 164, the stock trades at PE of 37.8x/20.8x/10x of FY16/17/18e respectively. We initiate the stock with a BUY rating and a target price of Rs 313. (20x of FY18e). Vaishali Parkar Kumar | [email protected] | +91 22 6138 9381 Price Price Target Up/Down (%) Rs. 164 Rs. 313 * Listed on BSE only Bloomberg Code EPC. IN Share Holding (%) Promoters 54.78 FII 1.64 DIIs 1.28 Stock Data Nifty 8,485 Sensex 28,093 52 week high/low 237/128 Maket Cap (Rs. bn) 4.52 Face value 10 Price performance (%) 1M 3M 6M 1Y Absolute 25.7 0.5 7.4 -23.9 Relative to Sensex 21.5 2.7 4.1 -31.2 Relative Performance 91 EPCI.BO. Reuters Code As on 31st Mar, 2015 50 100 150 200 250 Jul-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Mar-11 Apr-11 May-11 Jun-11 BSE Sensex EPC Industries Source:-Bloomberg Sector: PLASTIC PRODUCT 6 th July, 2015 Initiating coverage BUY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

(Wholly owned subsidiary of Bank of Baroda)

Exhibit 1: Financial summary (Rs mn)

Year end: March FY13 FY14 FY15 FY16e FY17e FY18e

Net sales 1,614 1,747 1,683 2,289 3,548 5,890

Growth (%) 29.1 8.3 -3.7 36.0 55.0 66.0

Operating margin (%) 4.7 5.9 1.9 7.3 8.2 10.0

PAT 53 77 9 115 209 433

Adjusted PAT 53 77 9 115 209 433

EPS (Rs) 1.9 2.8 0.3 4.2 7.5 15.7

Growth (%) -19.8 44.3 -88.4 1182.1 81.9 107.6

P/E(x) 64.9 36.8 499.5 39.5 21.7 10.5

ROE (%) 6.5 7.1 0.8 8.8 13.4 23.1

ROCE (%) 7.5 8.4 1.3 9.4 13.8 23.3

Debt/equity (x) 0.12 0.01 0.00 0.00 0.00 0.00

P/Bv (x) 3.3 2.5 3.9 3.1 2.7 2.2

Source: Company, BOBCAPSe

$Com panyName$

EPC Industrie Ltd. (Mahindra & Mahindra Group Co.)

If there is any company which can benefit out of Pradhan Mantri Krishi Sinchhayi Yojana (PMKSY) then its Mahindra’s EPC; initiate with BUY

The government under the Pradhan Mantri Krishi Sinchayi Yojana

(PMKSY) launched mega irrigation scheme worth Rs 500bn which will

give a boost to irrigation sector as a whole. EPC Industrie (EPC)

presently has 5.5% market share in the micro irrigation space. We

initiate coverage on EPC with a BUY rating and a price target of Rs 313

implying 91% upside. We expect EPC’s revenue/earnings to grow at a

CAGR of ~52%/264% respectively over FY15-18e led by 1) PMKSY

scheme of Rs 500bn over five years, 2) ~2600 dealers network spread

over 17 states 3) strong parentage of M&M, 4) well established product

portfolio.

Huge opportunities laying; as Govt launches mega irrigation scheme of

Rs 500bn under PMKSY: The union cabinet under the Pradhan Mantri Krishi

Sinchayi Yojana (PMKSY) launched mega irrigation scheme worth Rs 500bn (spent

over next five years; for FY16 the allocation is of Rs 53bn). This scheme will focus

on improving irrigation in non-rain-fed areas as well as strive to improve water

efficiency through the country. India is a second largest country under crop

cultivation (~142 mn ha.). Even though ~60% of the cultivated land is still

dependent on the monsoons for the cultivation. The PMKSY aims to ensure access

to some means of protective irrigation to all agricultural farms in the country, to

produce 'per drop more crop'.

Higher Scope for expansion in market share, profitability: At present Jain

Irrigation is a market leader with ~55% market share followed by private player

Netafim India (~20% market share). We believe, going forward EPC can easily

expand its market share (~5.5% to ~15%) and profitability (~ led by 1) strong

support from the parent company (M&M), 2) EPC can also use M&M’s agri

business network for its own expansion, 3) EPS has better debtors days and Debt

to Equity ratios than its peers, we further believe, EPC can improve upon its

margin once economies of scale take place. (Market leader Jain Irrigation

enjoys~12% EBITDA margins.)

Consumers reach through strong network of channel partners: EPC

currently has ~2600 channel partners spread in ~17 states. MIS sales are driven

by strong demand in states like Gujarat, Rajasthan, Madhya Pradesh Maharashtra,

Karnataka, Andhra Pradesh, Tamil Nadu, Rajasthan and Haryana. The strong

network with the help of parent company M&M can help EPC to expand its reach

pan India level.

Valuation: At CMP of Rs 164, the stock trades at PE of 37.8x/20.8x/10x of

FY16/17/18e respectively. We initiate the stock with a BUY rating and a target

price of Rs 313. (20x of FY18e).

Vaishali Parkar Kumar | [email protected] | +91 22 6138 9381

Price Price Target Up/Down (%)

Rs. 164 Rs. 313

* Listed on BSE only

Bloomberg Code

EPC. IN

Share Holding (%)

Promoters 54.78

FII 1.64

DIIs 1.28

Stock Data

Nifty 8,485

Sensex 28,093

52 week high/low 237/128

Maket Cap (Rs. bn) 4.52

Face value 10

Price performance (%) 1M 3M 6M 1Y

Absolute 25.7 0.5 7.4 -23.9

Relative to Sensex 21.5 2.7 4.1 -31.2

Relative Performance

91

EPCI.BO.

Reuters Code

As on 31st Mar, 2015

50

100

150

200

250

Jul-

10

Jul-

10

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

BSE Sensex EPC Industries

Source:-Bloomberg

Sector: PLASTIC PRODUCT

6th July, 2015

Initiating coverage

BUY

EPC Industrie Ltd. | 7 July 2015

| Equity research | 2

(Wholly owned subsidiary of Bank of Baroda)

Industry outlook

Scope of Irrigation industry in India

India being the 2nd largest land under cultivation (~142 mn ha) has a huge scope especially

when the 65% of cultivated land is dependent on monsoons. Irrigation can help to 1)reduce

over dependence on monsoons, 2) advanced agricultural productivity, 3) bringing more land

under cultivation, 4) reducing instability in output levels, 5) creation of job opportunities, 6)

electricity and transport facilities, 7)control of floods and prevention of droughts.

The Task Force on Micro Irrigation set up by the Central Government has stated that more

areas can be brought under irrigation if modern methods of irrigation are adopted. It

estimates the total potential in India to be around 69.5 Million Hectares. Only around ~10%

of this potential has been tapped so far in India. Hence there is tremendous opportunity for

micro irrigation business in the years to come. The Indian Micro Irrigation Industry had been

growing at a CAGR of ~20% prior to FY13.

Scarcity of water; may create problems for highly populated country like India

Water is becoming increasingly scarce in many parts of the world and thereby limiting

agricultural development. The capacity of large countries like India to efficiently develop and

manage water resources is likely to be a key determinant for global food security in 21st

century.

India’s annual precipitation (rainfall & snowfall) is around 4000 BCM (Billion Cubic Meters) (or

4000 lakh crore litres). Out of this, close to 80% either gets washed away into the sea or is

subject to evaporation and percolation in the ground. Only about 20% or 800 BCM is currently

available for use. 80% of this usable water is utilized for Agriculture. India is currently on the

verge of being water stressed (< 1500 Cu m per capita) and it is estimated that by the year

2050,led by growing population and the pressure that it puts on agriculture, India will be on

the brink of becoming a water scarce country (< 1000 Cu m per capita).

Since agriculture is the major water-consuming sector in India, demand management in

agriculture is crucial to reduce the demand for water to match the available future supplies. A

number of demand management strategies and programmes have been introduced to save

water and increase the existing water use efficiency in Indian agriculture. One such method

introduced in Indian agriculture is micro-irrigation, which includes both drip and sprinkler

method of irrigation.

Exhibit 2: Water availability in India

433 231 202

690

403 287

-

200

400

600

800

1,000

1,200

Utilizable Present use Available

Billio

n Cubic

Mete

r (B

CM

)/A

nnum

Ground water Surface water

Source: BOBCAPSe, Government of India (PMKSY presentation)

EPC Industrie Ltd. | 7 July 2015

| Equity research | 3

(Wholly owned subsidiary of Bank of Baroda)

Micro-irrigation - today’s requirement

Micro-irrigation (MI) has proved to be an efficient method in saving water and increasing

water use efficiency as compared to the conventional surface method of irrigation. Micro-

irrigation was introduced primarily to save water and increase the water use efficiency in

agriculture. However, it also delivers many other economic and social benefits.

Reduction in water consumption due to drip irrigation systems over the surface irrigation

varies from 30 to 70% for different crops. Productivity gain due to use of micro-irrigation is

estimated to be in the range of 20 to 90% for different crops. It also reduces weed problems,

soil erosion and cost of cultivation substantially, especially in labour-intensive operations. The

reduction in water consumption in micro-irrigation also reduces the energy use (electricity)

that is required to lift water from irrigation wells. Micro-irrigation can also be adopted in all

kind of lands, which is not generally possible through flood irrigation method.

Research suggests that Drip Irrigation systems are not only suitable for those areas that are

presently under cultivation, but can also be operated efficiently in undulating terrain, rolling

topography, hilly areas, barren land and areas which have shallow soils. Given the population

growth and increasing requirement of agricultural commodities, there is a need to increase

the area under cultivation. Micro-irrigation can be one of the viable options for expanding area

under cultivation. Investment in Micro Irrigation also appears to be economically viable, even

without availing State subsidy.

Exhibit 3: Reasons for Micro Irrigation System

0% 10% 20% 30% 40% 50% 60% 70%

Subsidy

Reduced labour dependency

Access to credit

Long term cost reduction

Higher productivity

Source: BOBCAPSe, Company

EPC Industrie Ltd. | 7 July 2015

| Equity research | 4

(Wholly owned subsidiary of Bank of Baroda)

Investment rationale

The government under the Pradhan Mantri Krishi Sinchayi Yojana (PMKSY) launched

mega irrigation scheme worth Rs 500bn (spent over next five years; for FY16 the

allocation is of Rs 53bn), which will give a boost to irrigation sector as a whole. EPC

presently has 5.5% market share in the micro irrigation space. Since, business is in

pretty nascent stages, the profitability is low and benefits of operating leverage will

take a while to play out.

We believe EPC with the PMSKY project and strong parentage of M&M can achieve

market share upwards of 15-20% with EBITDA margins of 15%+ over next 2-3-5

years.

We are quite confident that over next 5 years, EPC will grow at a CAGR of 51% We

feel the way application of agro chemicals is increasing , limited cultivable land and

importance of water usage increasing, growth in micro irrigation business can be

quite exponential in the times to come.

Huge opportunities laying; as Govt launches mega irrigation scheme of Rs 500bn under PMKSY

The union cabinet under the Pradhan Mantri Krishi Sinchayi Yojana (PMKSY) launched mega

irrigation scheme worth Rs 500bn. This scheme will focus on improving irrigation in non-rain-

fed areas as well as strive to improve water efficiency through the country.

India is a second largest country under crop cultivation (~142 mn ha.). Even though ~65% of

the cultivated land is still dependent on the monsoons for the cultivation. The PMKSY aims to

ensure access to some means of protective irrigation to all agricultural farms in the country,

to produce 'per drop more crop'. This initiative of the Government will help to boost

productivity, improve crop quality and help farmers upgrade to modern methods of farming.

This scheme will give boost to irrigation manufacturers; we believe EPC with strong product

portfolio and strong support from M&M will be the highest beneficiary going forward.

Exhibit 4: Governments policy under PMSKY project

Need for Gap Filling

Water Sources

Distribution Management

Accelerated Irrigation Benefit

Programme (AIBP) Integrated Watershed

Management Programme

(IWMP), MGNREGS, NMSA

Command Area Development

(CAD)

National Mission for Sustainable

Agriculture (NMSA) : Drip-

sprinkler irrigation, Moisture

conservation

Fragmented approach rather than ‘end to end’ solution

Source: BOBCAPSe, Government of India (PMKSY presentation)

EPC Industrie Ltd. | 7 July 2015

| Equity research | 5

(Wholly owned subsidiary of Bank of Baroda)

Strong parentage of “Mahindra & Mahindra Group”

Mahindra & Mahindra acquired EPC in 2011. Mahindra & Mahindra has presence in the tractor and farm equipment business and the agriculture domain through Mahindra Samriddhi centers across the country. Mahindra & Mahindra group has strong desires in Agriculture space. It is clear that as the agricultural business vertical of Mahindra and Mahindra complements EPC’s business, it provides scope for exploiting synergies to create value for both businesses. Mahindra’s Farm Equipment sector’s management bandwidth and competence in marketing and operations will augur well for EPC.

Exhibit 5: Revenue growth trend after M&M’s acquisition

-20

0

20

40

60

80

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY12

FY13

FY14

FY15

FY16e

FY17e

FY18e

(%)

Rs.

Mn

Revenue Growth %

Source: BOBCAPSe, Company

Synergy with M&M finance can work wonders

M&M finance is the subsidiary of M&M which is working in the NBFC space ( with a vision to

transform rural and semi-urban India into a self-reliant), along with ~1,000 branches. M&M

can use synergy between EPC and M&M finance to expand EPC’s network under PMKSY

scheme.

The way business can happen between M&M Financials and EPC can be better understood

with the help of following example based on Gujarat model:

M&M is in sweet spot having an agri NBFC, Irrigation company+ strong dealers network across state, due to PMKSY scheme, this model can work wonders for EPC

EPC approaches farmers who has desires to buy irrigation equipment

Farmers puts Rs 5,000 to buy the irrigation equipment

M&M Finance can give loan upto Rs 20,000

Product purchase from EPC Industrie worth Rs 25,000

Farmers apply to govt. for subsidy through DBT (Direct Bank Transfer)

Govt. Transfer subsidy ~Rs 20,000 to ESCROW A/c through farmer to M&M

M&M Finance receives money

Farmer is debt free

Farmer desires to buy the irrigation equipment of ~Rs25,000

EPC Industrie Ltd. | 7 July 2015

| Equity research | 6

(Wholly owned subsidiary of Bank of Baroda)

Higher Scope for expansion in market share, profitability

India has a second largest land under cultivation (~142mn. Ha) out of which ~60% cultivable

land is still dependent on the monsoon. So far ~70mn ha land has got covered under

irrigation system, out of which only ~6mn land is under MIS (Micro-irrigation system). The

government of India is also giving the importance for micro- irrigation under PMKSY scheme.

We believe EPC has a huge potential to grow under this scheme along with its ~2600 dealers

spread across 17states, which they can further expand through M&M’s agri business network.

Exhibit 6: Industry size and opportunity for EPC to grow

10,767

6,250 4,922

3,354 2,983

2,008 1,864 1,850 1,038 1,084 547

0.20%

2.2%13%

0.7% 9% 26% 22% 0 28% 12% 51% -

2,000

4,000

6,000

8,000

10,000

12,000

Utt

ar

Pra

desh

MP

Raja

sth

an

Punja

b

Guja

rat

Mahara

shtr

a

Hary

ana

Bhira

Karn

ata

ka

Wst

Bengal

Andhra

Pra

desh

Are

a (

x 1

000 H

a)

Potential Penetration

Source: BOBCAPSe, Company’s 4QFY15 presentation

At present Jain Irrigation is a market leader with ~55% market share followed by private

player Netafim India (~20% market share). We believe, going forward EPC can easily expand

its market share and profitability led by 1) strong support from the parent company (M&M), 2)

EPC can also use M&M’s agri business network for its own expansion, 3) EPS is a zero debt

and better debtors days company than its peers, we further believe, EPC can improve upon its

margin once economies of scale take place (Market leader Jain Irrigation enjoys ~12%

EBITDA margins).

Exhibit 7: Market share distribution in irrigation sector

Jain Irrigation, 55%

Netafim India, 20%

EPC Industries,

5.5%

Others, 20%

Source: BOBCAPSe, Company

Exhibit 8: Peer comparison

Jai Irrigation Netafim India EPC Industrie

Dealers Network 4000 1500 2600

Market Share 55% 20% 5.5%

Rvenue (Rs Mn) 60508 7588* 1683

EBITDA margin 12% 5.4%* 1.9%

Debtors Day (Avg. 3 years) 143 113* 107

Debt to Equity ratio 1.21 0.54* 0.004

Source: BOBCAPSe, Company

*(Netafim India’s nos. based on FY14)

EPC Industrie Ltd. | 7 July 2015

| Equity research | 7

(Wholly owned subsidiary of Bank of Baroda)

Well established brand with superior quality

EPC has been in the business of manufacturing MIS for over 30 years (since 1986). It has

developed technical expertise for providing reliable and quality products. This quality of the

hardware delivered to the farmer is the most crucial aspect in determining the performance of

the MIS as regards to the yield of the crop, quantity of water applied, quantity of fertilizers

delivered to the plant, energy consumption etc. EPC is considered to be one among the very few

quality brands in MIS.

Exhibit 9: EPC’s Product Portfolio

Product Portfolio: Drip irrigation

Online Drippers Round Inline drippers Flat Inline drippers Irrigation laterals

Drip Fittings

Drip filters

Fertigation Equipment

Product Portfolio: Sprinkler Irrigation

Sprinkler Irrigation pipes Pipe fittings

Sprinkler Nozzles

Source: BOBCAPSe, Company

EPC Industrie Ltd. | 7 July 2015

| Equity research | 8

(Wholly owned subsidiary of Bank of Baroda)

Consumers reach through strong network of channel partners

EPC currently has ~2600 channel partners spread in ~17 states. MIS sales are driven by

strong demand in states like Gujarat, Rajasthan, Madhya Pradesh Maharashtra, Karnataka,

Andhra Pradesh, Tamil Nadu, Rajasthan and Haryana in India. Being a Mahindra group

company, EPC has presence in most of these states through a network of sales/branch offices

supported by its channel partners which can help EPC to expand its reach pan India level.

EPC has ~5.5% market share with ~2600 dealer’s network which is near to the competitors,

which gives us comfort that EPC can easily increase its revenue. Also with the strong

parentage like M&M and its agriculture network will work as a booster for the expansion in

revenue.

Exhibit 10: Peer comparison; Revenue vs Dealers network

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1,000 2,000 3,000 4,000 5,000

Rs

Mn

No. of Dealers

Netafim

EPC Industries

Jain Irrigation

*Netafim Revenue based on FY14 and Jain Irrigation and EPC Industrie revenue based on FY15

Source: BOBCAPSe, Company

EPC Industrie Ltd. | 7 July 2015

| Equity research | 9

(Wholly owned subsidiary of Bank of Baroda)

Key risk

Raw Material price risk The major raw material for EPC is high, medium and linear low density

polyethylene. Naturally it is exposed to fluctuations in the price of raw material for the

manufacture of MIS products. The manufacture of these raw materials is dependent on crude oil

and the price of crude oil globally determinates the prices of these raw materials. Any fluctuation

in the price of crude oil have significant implications on the financials of the company.

Government’s subsidy scheme – a major influencing factor. EPC’s MIS products are

significantly dependent on the government policies regarding subsidies. Delay in receipt of the

subsidy component would adversely impact its margins. Since the product is subsidized

government withdrawing or reducing subsidy to the farmers and the horticulturists, would

discourage them as they may not be in a position to afford micro irrigation systems.

Growth dependant on Government policies Government is the main force behind this

industry growth so far. Any reduction in government budgetary outlays for agriculture or

irrigation could impact the sector. However with the current policy under PMKSY has opened up

huge opportunity for this sector. MI has gained traction among the farmer community due to the

proven benefits like Water savings and crop yield improvements when compared to traditional

irrigation methods.

Competition –Presently the market is dominated by Jain irrigation followed by Netafim. There

are other players like finolex and recently Godrej industries have made a foray in to the market.

While this augurs well for the growth of the sector, it also poses a threat to the margins of

established players. No corporate governance issue with company unlike its established

competitors.

EPC Industrie Ltd. | 7 July 2015

| Equity research | 10

(Wholly owned subsidiary of Bank of Baroda)

Valuation:

We believe with the PMKSY project, the government is planning to open an

opportunity of Rs 500bn for irrigation sector. Even though EPC retain its current

market share of 5.5% can get an opportunity of Rs 27.5bn which is a huge potential

for the company.

At CMP of Rs 164, the stock trades at PE of 37.8x/20.8x/10x of FY16/17/18e

respectively. We initiate the stock with a BUY rating and a target price of Rs 313.

(20x of FY18e).

Exhibit 11: One year forward PE

0

50

100

150

200

250

300

5-J

ul-10

5-O

ct-

10

5-J

an-1

1

5-A

pr-

11

5-J

ul-11

5-O

ct-

11

5-J

an-1

2

5-A

pr-

12

5-J

ul-12

5-O

ct-

12

5-J

an-1

3

5-A

pr-

13

5-J

ul-13

5-O

ct-

13

5-J

an-1

4

5-A

pr-

14

5-J

ul-14

5-O

ct-

14

5-J

an-1

5

5-A

pr-

15

(x)

PE(x) Avg

6 yr mean = 58.2xCurrent = 17x

Source: BOBCAPSe, Bloomberg

Exhibit 12: Peer comparison- key financials and margins

Companies Sales PAT EBITDA margin (%) EPS

Rs (mn) Rs (mn) FY15 FY16e FY17e FY15 FY16e FY17e

Jain Irrigation 60508 55 12.77 13.63 13.99 1.21 4.36 6.83

EPC Industrie 1,683 9 1.9 7.3 8.2 0.3 4.2 7.5

Source: BOBCAPSe, Bloomberg

Exhibit 13: Peer comparison – key valuation metrics

Companies Price Mkt. cap PE (x) ROE (%)

Rs/share Rs (bn) FY15 FY16e FY17e FY15 FY16e FY17e

Jain Irrigation 71 6.6 58.8 16.3 10.4 2.6 8.6 12.4

EPC Industrie 163 4.5 503.2 39.3 21.6 0.8 8.8 13.4

Source: BOBCAPSe, Bloomberg

EPC Industrie Ltd. | 7 July 2015

| Equity research | 11

(Wholly owned subsidiary of Bank of Baroda)

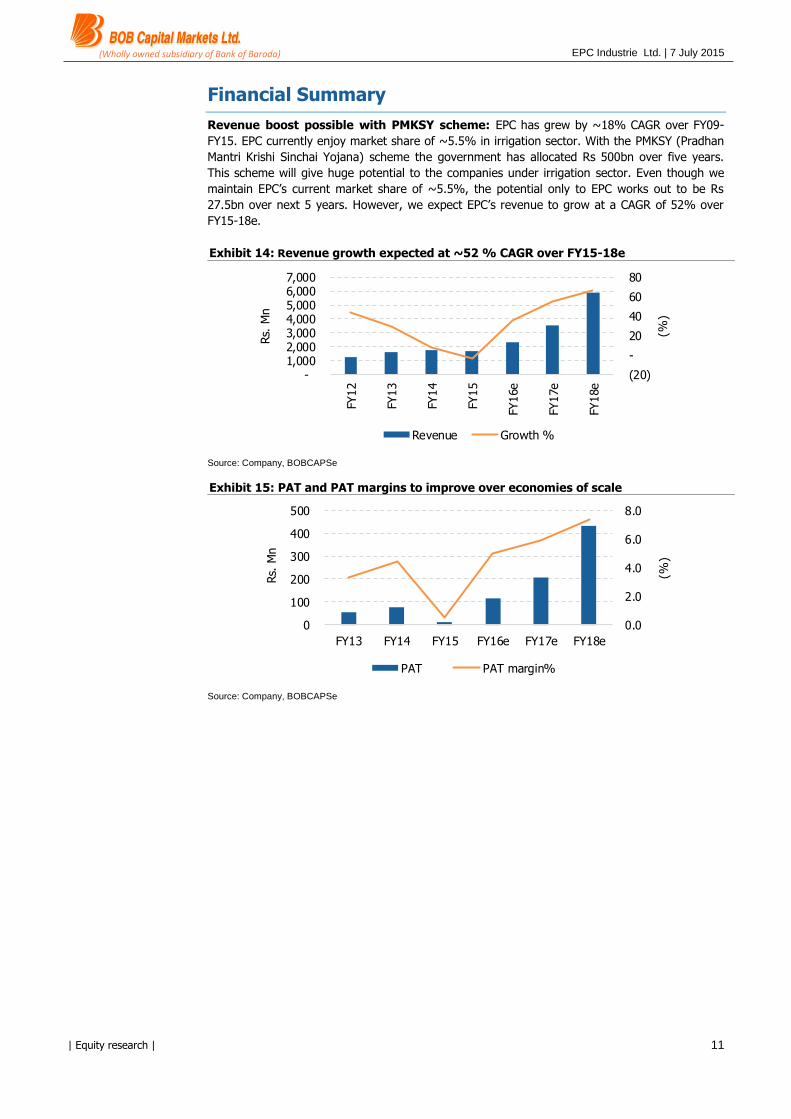

Financial Summary

Revenue boost possible with PMKSY scheme: EPC has grew by ~18% CAGR over FY09-

FY15. EPC currently enjoy market share of ~5.5% in irrigation sector. With the PMKSY (Pradhan

Mantri Krishi Sinchai Yojana) scheme the government has allocated Rs 500bn over five years.

This scheme will give huge potential to the companies under irrigation sector. Even though we

maintain EPC’s current market share of ~5.5%, the potential only to EPC works out to be Rs

27.5bn over next 5 years. However, we expect EPC’s revenue to grow at a CAGR of 52% over

FY15-18e.

Exhibit 14: Revenue growth expected at ~52 % CAGR over FY15-18e

(20)

-

20

40

60

80

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

FY12

FY13

FY14

FY15

FY16e

FY17e

FY18e

(%)

Rs.

Mn

Revenue Growth %

Source: Company, BOBCAPSe

Exhibit 15: PAT and PAT margins to improve over economies of scale

0.0

2.0

4.0

6.0

8.0

0

100

200

300

400

500

FY13 FY14 FY15 FY16e FY17e FY18e

(%)

Rs.

Mn

PAT PAT margin%

Source: Company, BOBCAPSe

EPC Industrie Ltd. | 7 July 2015

| Equity research | 12

(Wholly owned subsidiary of Bank of Baroda)

EBITDA margins to expand by 661bps: EPC posted ~1.9% EBITDA margin in FY15 (down

by ~400 bps over FY14) led by change from NMMI (National Mission on Micro Irrigation) to

NMSA (National Mission for Substantial Agriculture) which had a lack of policy clarity across many

states. However, with the PMKSY initiative by the government, we expect EPC to expand its

margin by ~661bps over FY15-18e (Market leader Jain Irrigation enjoys ~12% EBITDA

margins).

Exhibit 16: Margin expansion by ~661 bps over FY15-18e

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

FY13 FY14 FY15 FY16e FY17e FY18e

(%)

Rs.

Mn

EBITDA EBITDA margin %

Source: Company, BOBCAPSe

Return ratios to improve: We expect return ratios to improve to 20% led by

revenue/earnings to grow at a CAGR ~51%/245% respectively over FY15-18e.

Exhibit 17: Improving ROE & ROCE

0

5

10

15

20

25

%

ROE ROCE

Source: Company, BOBCAPSe

EPC Industrie Ltd. | 7 July 2015

| Equity research | 13

(Wholly owned subsidiary of Bank of Baroda)

WCC to remain high due to nature of business: EPC’s WCC was high in FY15 to 120 days

led by change from NMMI (National Mission on Micro Irrigation) to NMSA (National Mission for

Substantial Agriculture) which had a lack of policy clarity across many states. However, EPCs

average WCC remained high (avg. 91 days over FY10-15) as the company works closely with

farmers and the state government. We believe, going forward EPCs WCC will remain in the range

of 80 day due to nature of business.

Exhibit 18: WCC to remain high due to nature of business

-10

20

50

80

110

140

FY13 FY14 FY15 FY16e FY17e FY18e

No fo D

ays

Debtors Days Inventory Days Creditors Days WCC

Source: Company, BOBCAPSe

EPC Industrie Ltd. | 7 July 2015

| Equity research | 14

(Wholly owned subsidiary of Bank of Baroda)

Company Profile

EPC Industrie is one the pioneers in the Micro Irrigation industry in India backed by the strong

parent M&M Ltd., (M&M acquired 38% equity stake in EPC Industrie in February 2011 and in

June 2012 it raised its stake to 54.8%). EPC is in to manufacturing and sales of Micro Irrigation

System (MIS) consisting of Drip Irrigation System (online drippers, inline drip laterals, plain

laterals, drip fittings, filters, and fertigation equipments) and Sprinkler Irrigation System

(sprinkler irrigation pipes, pipe fittings and sprinkler nozzles. As part of project market sales it

undertakes supply, installation and provision of agronomical services to farmers) It also

manufactures specialized pipes for water and gas distribution as well as pipes required for

industrial and agricultural purposes with complete fitting and installation tools. EPC has 2600

channel partners. It is registered in 17 states of India as approved manufacturer of MIS with

respective state government authorities under the National Mission on Micro Irrigation and Micro

Irrigation Scheme.

EPC ‘s business model is manly categorized into two division 1) open market 2)

project market sales

Open market sales: Sales through open market secures receipt of a majority of the sale

proceeds of MIS upfront from the (intermediaries) channel partners. The channel partners in turn

sell the MIS to the customer/ farmer whereby subsidy disbursement exposure is taken by the

channel partners or the customers. Consequently, a majority of inventory costs and working

capital requirements is funded by its channel partners under the open market sales model.

Project market sales: EPC operates under the project market model in the states of Gujarat,

Andhra Pradesh and Tamil Nadu. As per the requirement of nodal agencies in the states of

Gujarat, Andhra Pradesh and Tamil Nadu, EPC enters into an agreement with the farmers, nodal

agencies and with banks, wherever applicable. After the loan tie ups and subsidy eligibility is

approved by the nodal agency in these states, EPC installs MIS and submit its claim for payment

to the nodal agency. Consequently, in the project market, the exposure of subsidy disbursement

is taken by EPC.

Exhibit 19: Key Management

Subhash Modak COO He holds a bachelors’ degree in mechanical engineering

from College of Engineering, University of Pune. He is on

deputation since September, 2011 and is responsible for

supervision over manufacturing, supply chain

management, product development, sourcing, industrial

relations and quality control. He has vast experience of

over 33 years

Sunil Johnson VP, sales and

marketing

He holds a bachelors’ degree in agriculture technology

from University of Allahabad in 1986 and Diploma in

Marketing from All India Management Association in

1998. He has experience of over 25 years and is

responsible for domestic and international sales, channel

development and agronomical services.

Anant Kshirsagar Head- Finance,

Accounts and IT

He holds Masters degree in commerce from University of

Pune. He is also a fellow member of the Institute of

Chartered Accountants of India. He has experience of

over 32 years and in finance and accounts functions

Source: Company, BOBCAPSe

EPC Industrie Ltd. | 7 July 2015

| Equity research | 15

(Wholly owned subsidiary of Bank of Baroda)

Exhibit 20: Income Statement

Y/E Mar (Rsmn) FY13 F14 F15 F16e F17e F18e

Net sales 1,614 1,747 1,683 2,289 3,548 5,890

growth (%) 29.1 8.3 (3.7) 36.0 55.0 66.0

COGS 1,057 1,143 1,075 1,442 2,217 3,592

Staff Cost 151 181 197 268 416 691

R&D Cost - - - - - -

SG&A Cost 330 320 380 412 625 1,019

EBITDA 76 103 31 167 290 588

growth (%) (23) 36 (69) 430 74 103

Depreciation 25 28 27 29 31 32

EBIT 50 75 4 137 260 556

Other income 28 26 26 28 31 34

Interest paid 25 24 12 13 13 13

Extraordinary/Exceptional items

- - - - - -

PBT 53 77 18 153 278 578

Tax - - 9 38 70 144

Minority interest - - - - - -

PAT 53 77 9 115 209 433

Non-recurring items - - - - - -

Adjusted PAT 53 77 9 115 209 433

growth (%) (20) 44 (88) 1,182 82 108

Exhibit 21: Balance Sheet

Y/E Mar (Rsmn) FY13 F14 F15 F16e F17e F18e

Cash & Bank balances 381 242 270 527 513 336

Other Current assets 692 1,003 891 1,009 1,407 2,310

Investments 0 0 0 0 0 0

Net fixed assets 314 322 302 297 292 285

Goodwill - - - - - -

Other non-current assets 88 95 61 59 59 59

Total assets 1,475 1,662 1,524 1,893 2,270 2,990

Current liabilities 253 481 359 420 587 872

Borrowings 130 8 4 4 4 4

Other non-current liabilities

37 43 16 18 20 22

Total liabilities 420 532 380 442 611 898

Share capital 276 276 276 276 276 276

Reserves & surplus 779 854 868 1,174 1,382 1,815

Shareholders' funds 1,056 1,130 1,144 1,451 1,659 2,092

Total liabilities 1,475 1,662 1,524 1,893 2,270 2,990

Source: Company, BOBCAPSe

EPC Industrie Ltd. | 7 July 2015

| Equity research | 16

(Wholly owned subsidiary of Bank of Baroda)

Exhibit 22: Cash Flow Statement

Y/E Mar (Rsmn) FY13 F14 F15 F16e F17e F18e

Profit after tax 53 77 9 115 209 433

Depreciation 27 30 27 29 31 32

Chg in working capital (104) (84) (2) (53) (229) (616)

Total tax paid - - - - - -

Cash flow from operations

(24) 23 34 91 11 (151)

Capital expenditure (52) (38) (8) (25) (25) (25)

Change in investments 0 0 - - - -

Cash flow from investments

(52) (38) (8) (25) (25) (25)

Free cash flow (76) (15) 26 66 (14) (176)

Issue of shares 104 0 0 - - -

Net inc/dec in debt (99) (122) (4) - - -

Dividend (incl. tax) - - - (1) (1) (1)

Other financing activities 300 (2) 5 192 0 0

Cash flow from financing

305 (124) 1 192 (0) (0)

Inc/(Dec) in Cash & Bank bal.

229 (139) 28 257 (15) (176)

Exhibit 23: Ratio analysis

Y/E Mar FY13 F14 F15 F16e F17e F18e

Per share data (Rs)

EPS 1.9 2.8 0.3 4.2 7.5 15.7

CEPS 2.9 3.8 1.3 5.2 8.7 16.8

DPS - - - 0.0 0.0 0.0

BV 38.2 40.9 41.4 52.5 60.0 75.7

Profitability ratios (%)

Gross margins 25.2 24.2 24.4 25.3 25.8 27.3

Operating margins 4.7 5.9 1.9 7.3 8.2 10.0

Net margins 3.3 4.4 0.5 5.0 5.9 7.4

Valuation ratios (x)

PE 64.9 36.8 499.5 39.5 21.7 10.5

P/BV 3.3 2.5 3.9 3.1 2.7 2.2

EV/EBITDA 42.4 25.3 133.7 24.0 13.9 7.1

EV/Sales 2.0 1.5 2.5 1.7 1.1 0.7

RoE 6.5 7.1 0.8 8.8 13.4 23.1

RoCE 7.5 8.4 1.3 9.4 13.8 23.3

RoIC 5 6 (0) 10 18 28

Source: Company, BOBCAPSe

EPC Industrie Ltd. | 7 July 2015

| Equity research | 17

(Wholly owned subsidiary of Bank of Baroda)

Disclaimer BUY. We expect the stock to deliver >15% absolute returns. HOLD. We expect the stock to deliver 5-15% absolute returns. SELL. We expect the stock to deliver <5% absolute returns. Not Rated (NR). We have no investment opinion on the stock. “The BoB Capital Markets research team hereby certifies that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report."

BOB Capital Markets Ltd. generally prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. Additionally, BOB Capital Markets Ltd. generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. We are not soliciting any action based on this material. It is for the general information of clients of BOB Capital Markets Ltd.. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, clients should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. BOB Capital Markets Ltd. does not provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding any potential investment in certain transactions — including those involving futures, options, and other derivatives as well as non investment-grade securities —that give rise to substantial risk and are not suitable for all investors. The material is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed are our current opinions as of the date appearing on this material only. We endeavor to update on a reasonable basis the information discussed in this material, but regulatory, compliance, or other reasons may prevent us from doing so.

We and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance of this material, may from time to time have "long" or "short" positions in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein and may from time to time add to or dispose of any such securities (or investment). We and our affiliates may act as market maker or assume an underwriting commitment in the securities of companies discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or advisory services for or relating to those companies and may also be represented in the supervisory board or any other committee of those companies.

For the purpose of calculating whether BOB Capital Markets Ltd. and its affiliates hold, beneficially own, or control, including the right to vote for directors, 1% or more of the equity shares of the subject, the holding of the issuer of a research report is also included.

BOB Capital Markets Ltd. and its non-US affiliates may, to the extent permissible under applicable laws, have acted on or used this research to the extent that it relates to non-US issuers, prior to or immediately following its publication. Foreign currency denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of or income derived from the investment. In addition, investors in securities such as ADRs, the value of which are influenced by foreign currencies, affectively assume currency risk. In addition, options involve risks and are not suitable for all investors. Please ensure that you have read and understood the current derivatives risk disclosure document before entering into any derivative transactions. In the US, this material is only for Qualified Institutional Buyers as defined under rule 144(a) of the Securities Act, 1933.No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without BOB Capital Markets Ltd.’s prior written consent. No part of this document may be distributed in Canada or used by private customers in the United Kingdom.

Sales and Dealing Team

Purvesh Shelatkar – Senior Vice President & Head Equity +91-22-6138 9330 [email protected]

Anil Pawar – Senior Manager – Dealing +91-22-6138 9325 [email protected]

Sachin Sambare – Manager– Dealing +91-22-61389331/33 [email protected]

Ashwin Patil – Executive – Dealing +91-22-6138 9326 [email protected]

Research Team Sectors

Vaishali Parkar Kumar – Analyst Agri, Auto, Defence +91-22-6138 9382 [email protected]

Padmaja Ambekar – Analyst Auto Ancillary, Infra, Midcap +91-22-6138 9381 [email protected]

Akanksha Tripathi – Analyst Footwear, FMCG +91-22-6138 9383 [email protected]

Rishabh Mehta – Associate +91-22-6138 9384 [email protected]

Retail Research Team

Kshitij Kelkar +91-22-61389386 [email protected]

Kiran Sawardekar +91-22-61389385 [email protected]

Mohan Shinde +91-22-61389386 [email protected]

Debt Dealing Team

Minaxi Tiwari +91-22-61389336 [email protected]

UTI Tower, 3rd Floor, South Wing, Bandra-Kurla Complex, Bandra (E), Mumbai - 400 051. India.

Ph.: +91.22.6138.9300 || Fax: +91.22.6671.8535 ||

Email: [email protected]|| Web: www.bobcaps.in

NSE SEBI No. (CASH): INB231304537

NSE SEBI No. (DERIVATIVES): INF231304537

BSE SEBI No. : INB011304533

Related Documents

![[Industrie] secteur industrie](https://static.cupdf.com/doc/110x72/546d2ea1af795912528b6241/industrie-secteur-industrie.jpg)