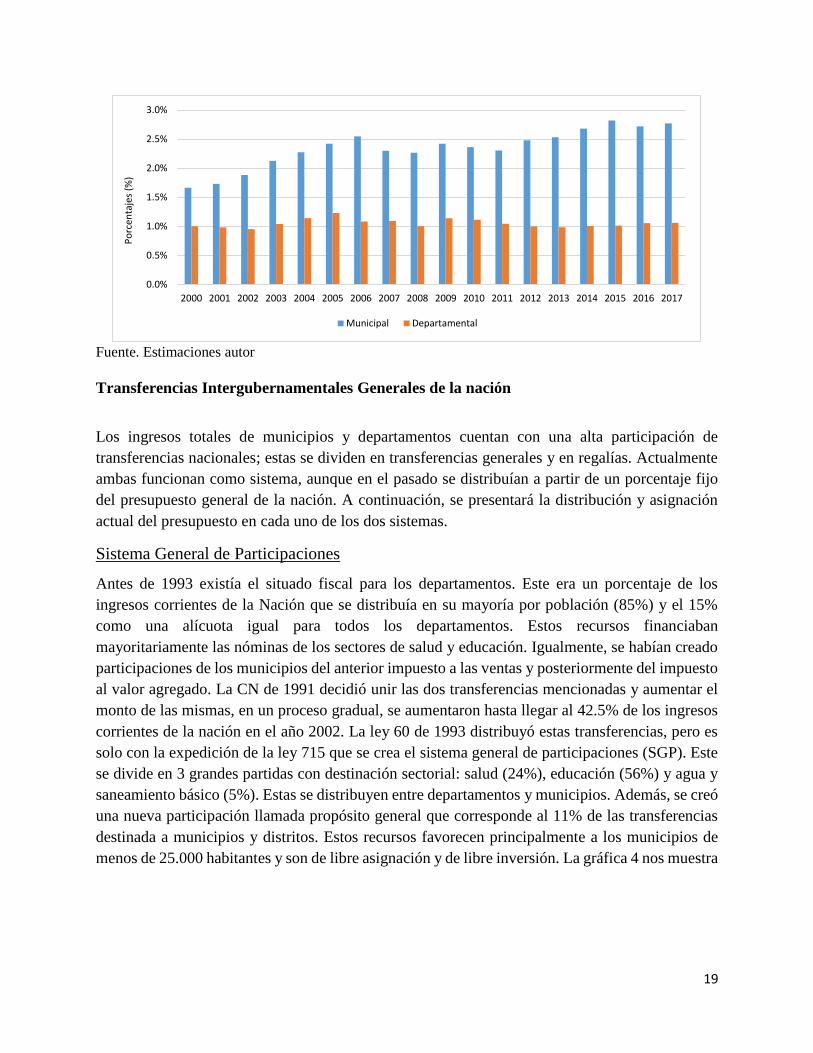

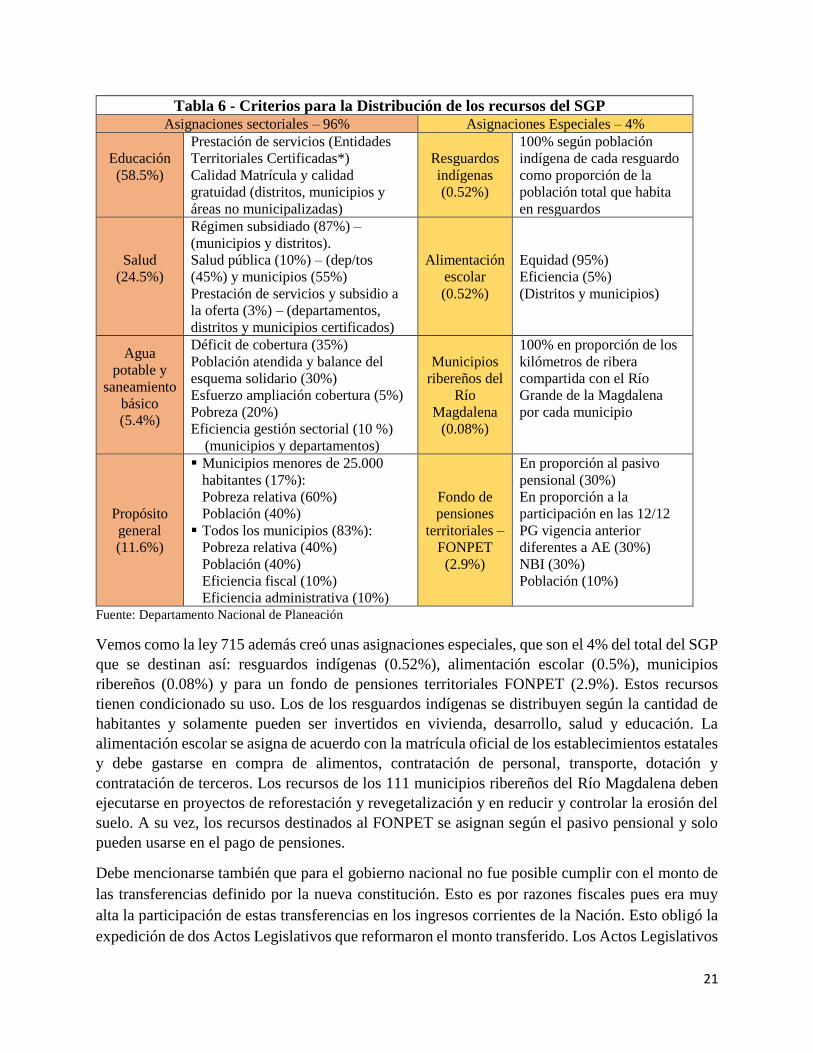

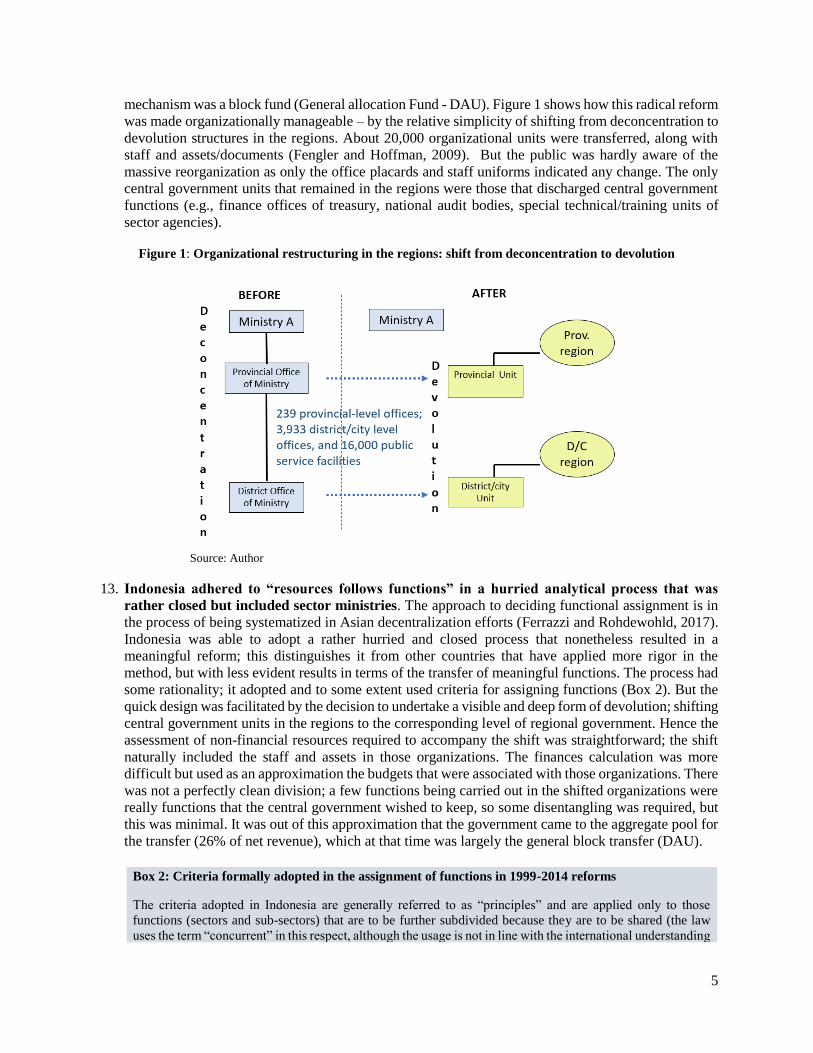

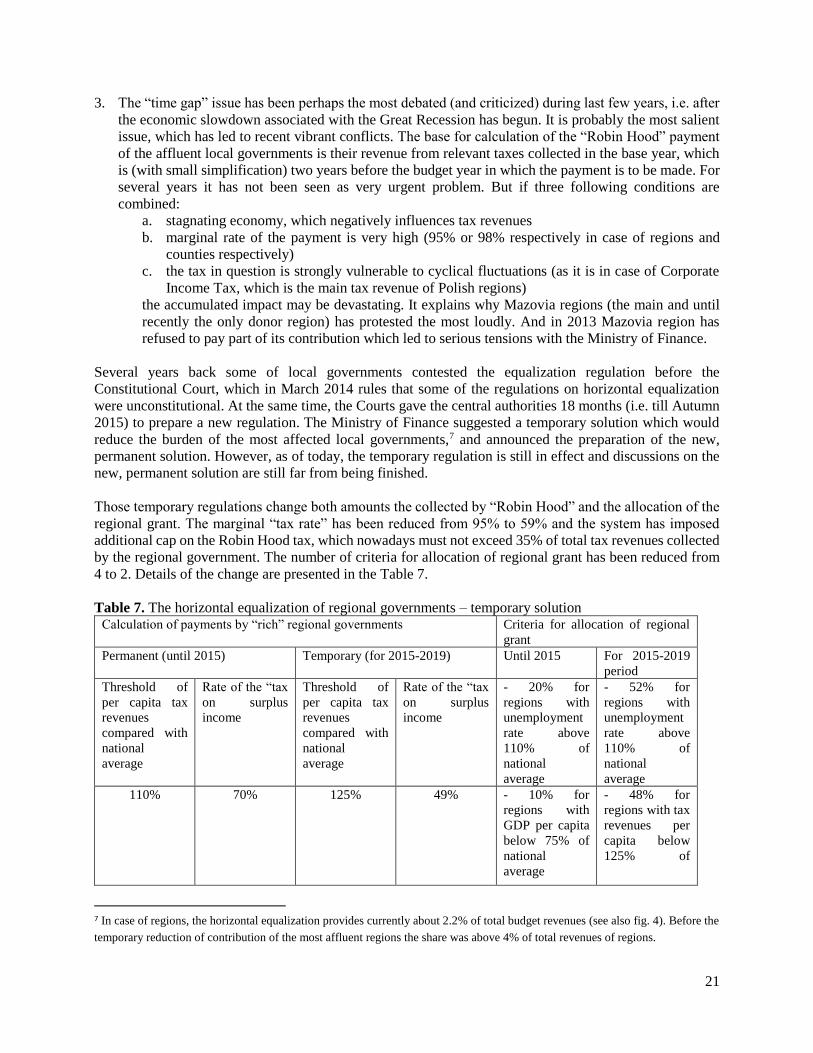

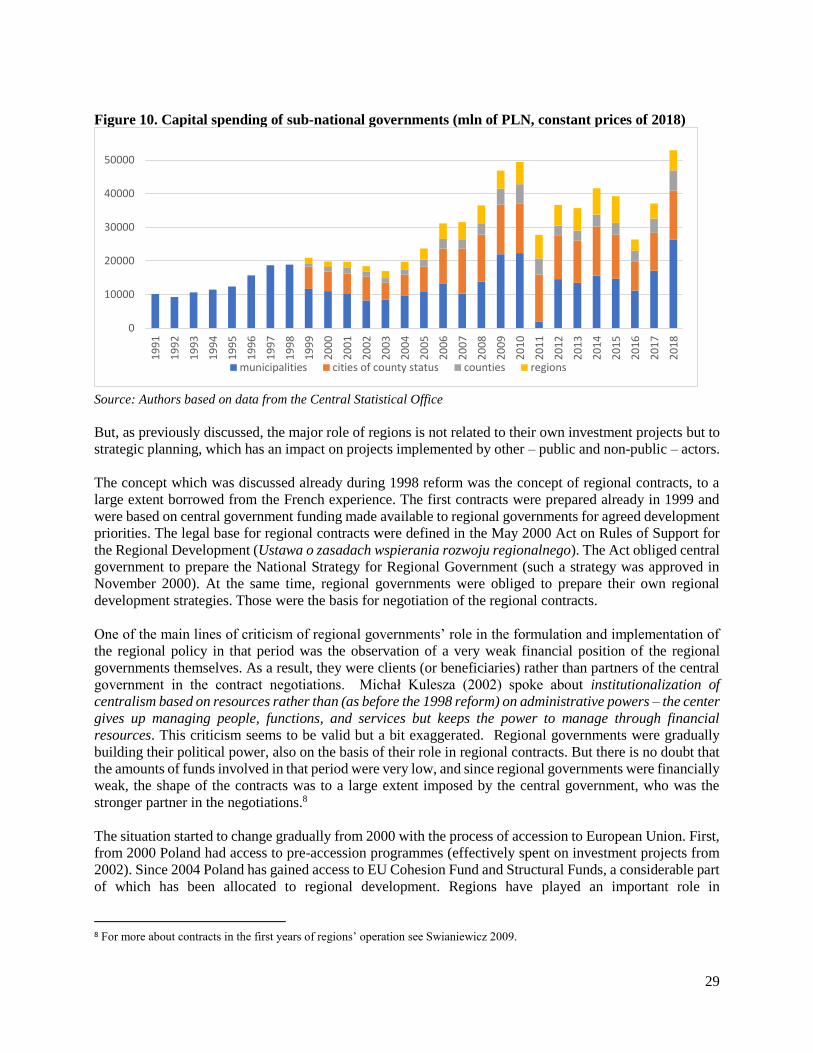

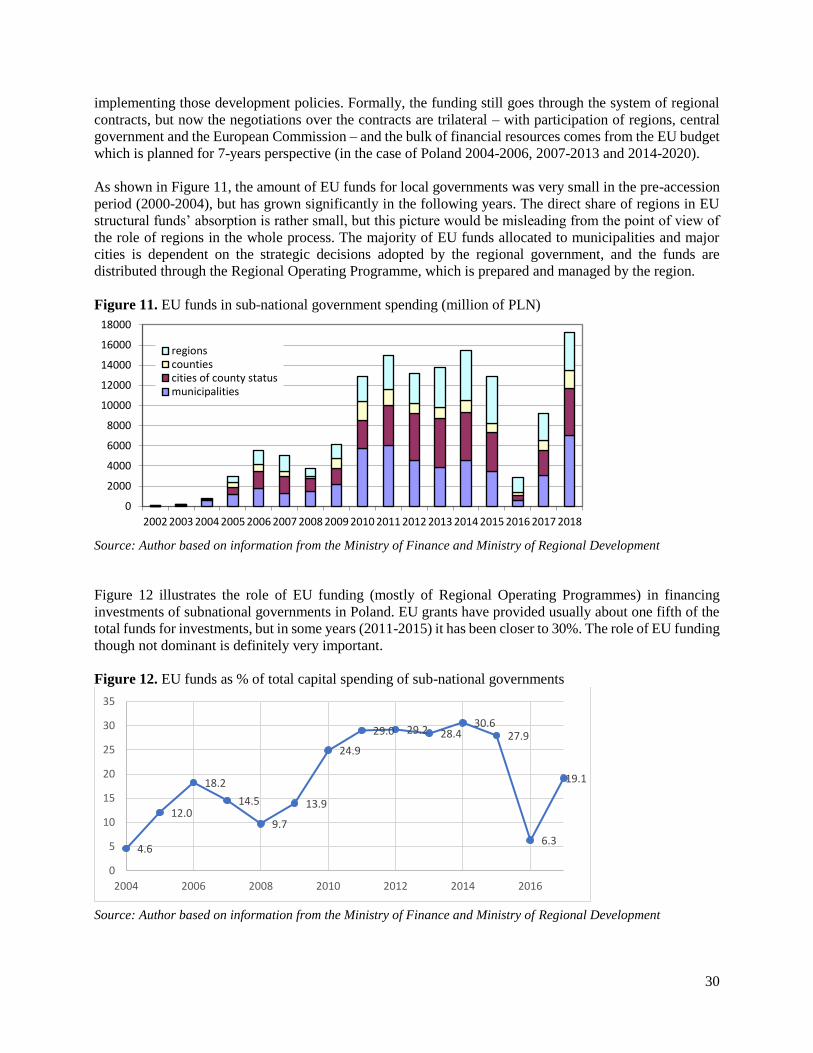

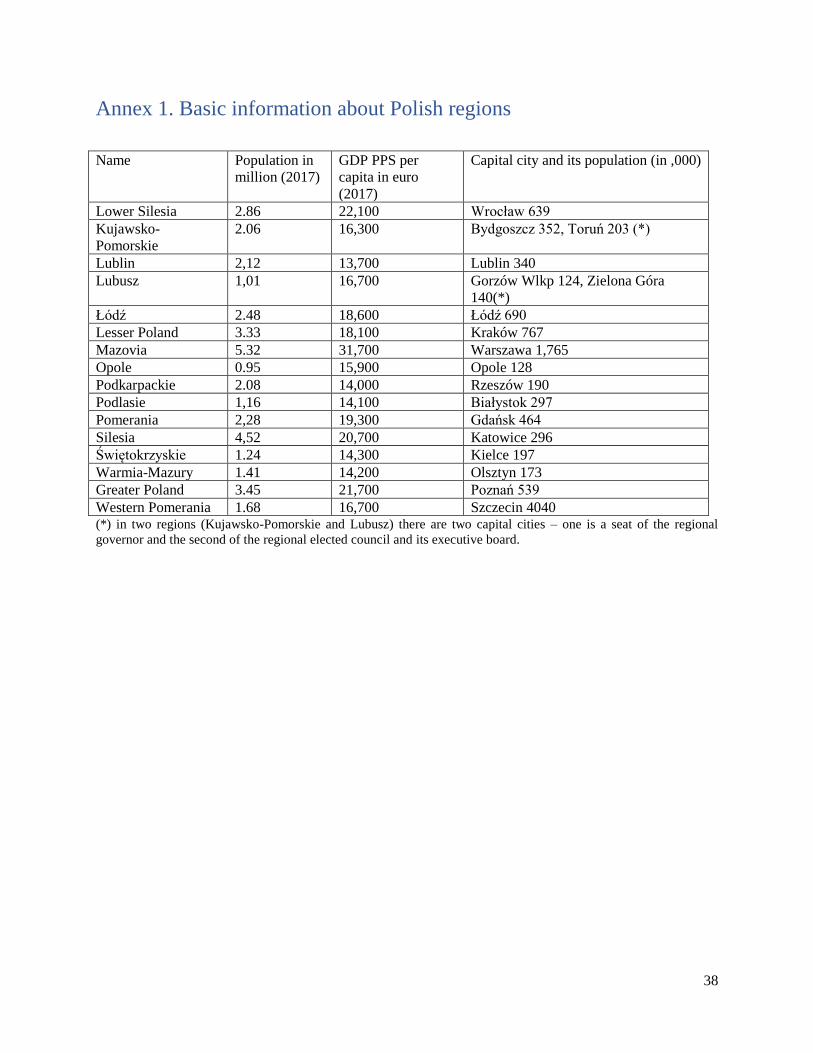

1 Lessons from International Experience on Fiscal Decentralization for Regional Governments Volume II: Overview and Case Studies: Colombia, Indonesia, Poland and Spain prepared under the World Bank Partnership RAS for Chile 1 1 The Overview Chapter was written by Ewa Korczyc and Natalia Campora under the supervision of Jorge Martinez-Vazquez. Case studies were authored by country experts: Colombia - Juan Gonzalo Zapata; Indonesia - Gabriele (Gabe) Ferrazzi; Poland- Pawel Swianiewicz; and Spain - Santiago Lago-Peñas. The work benefitted from comments by Pedro L. Rodriguez. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

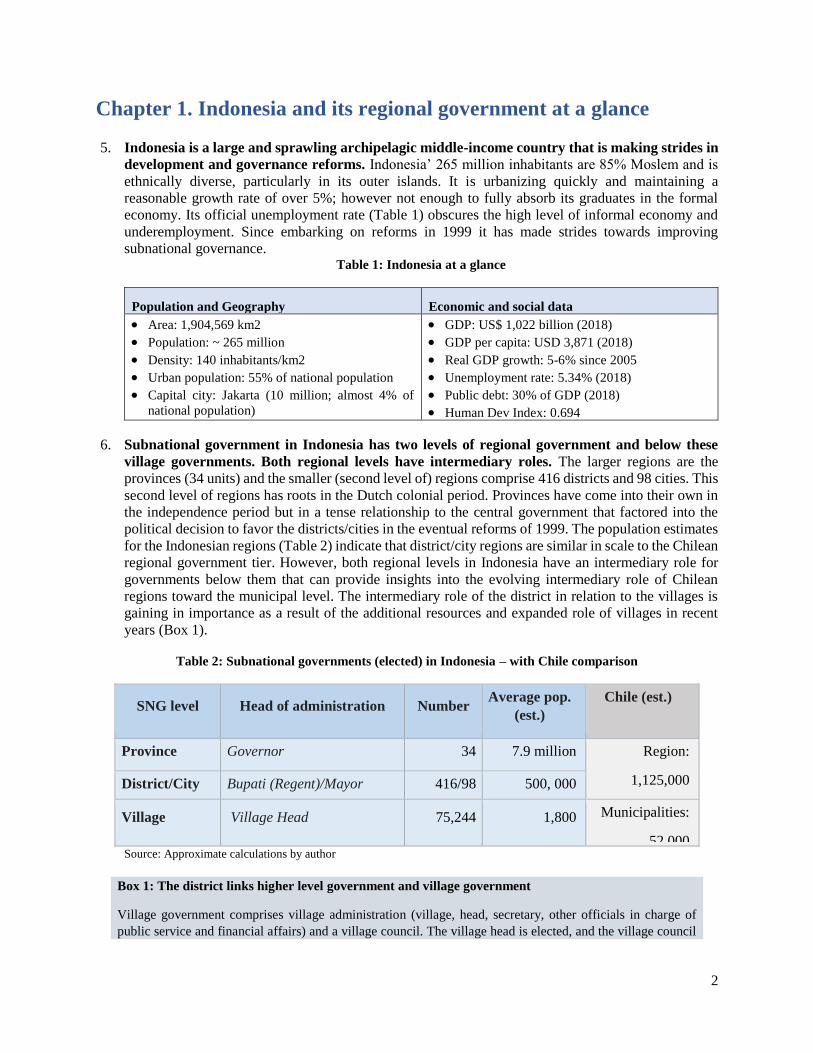

Lessons from International Experience on

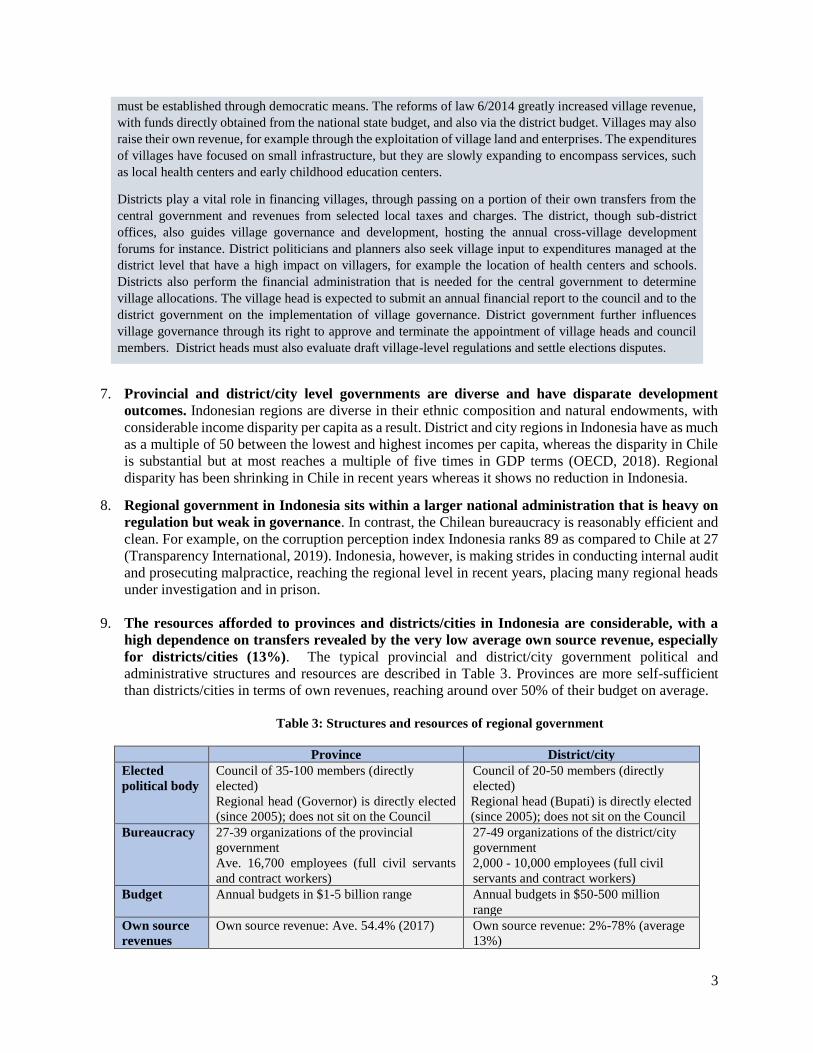

Fiscal Decentralization for Regional

Governments

Volume II: Overview and Case Studies:

Colombia, Indonesia, Poland and Spain

prepared under the World Bank Partnership RAS for Chile1

1 The Overview Chapter was written by Ewa Korczyc and Natalia Campora under the supervision of Jorge Martinez-Vazquez.

Case studies were authored by country experts: Colombia - Juan Gonzalo Zapata; Indonesia - Gabriele (Gabe) Ferrazzi; Poland-

Pawel Swianiewicz; and Spain - Santiago Lago-Peñas. The work benefitted from comments by Pedro L. Rodriguez.

Pub

lic D

iscl

osur

e A

utho

rized

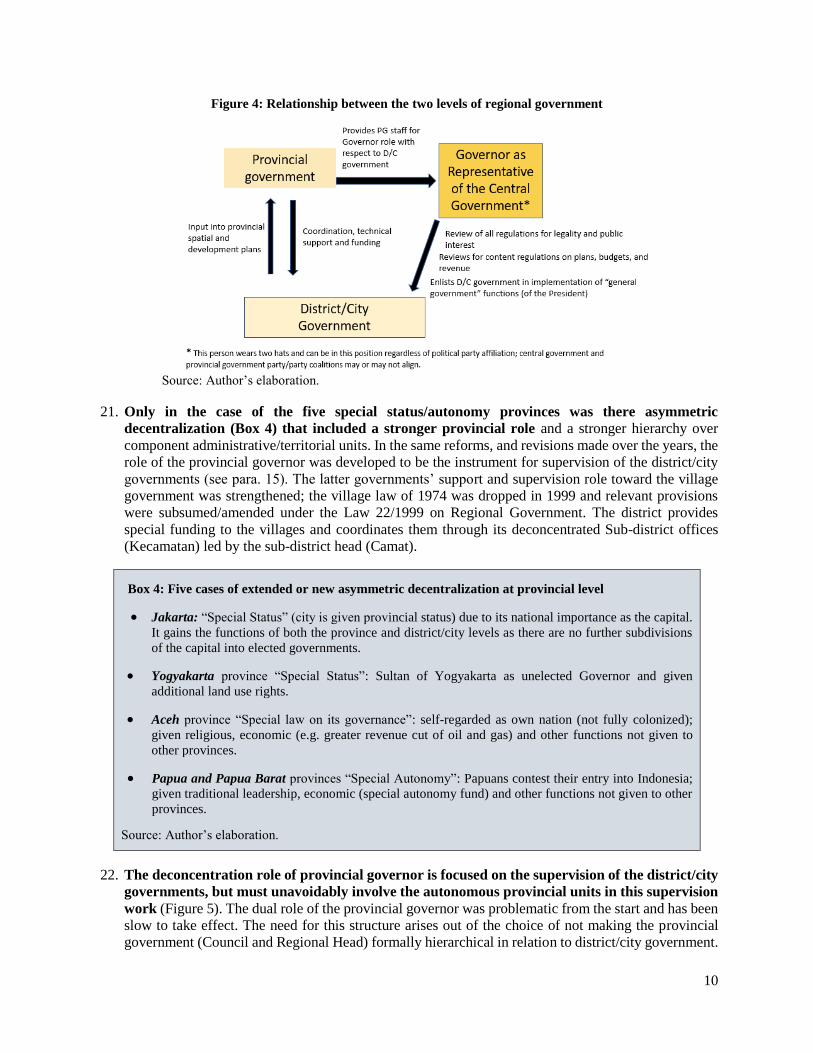

Pub

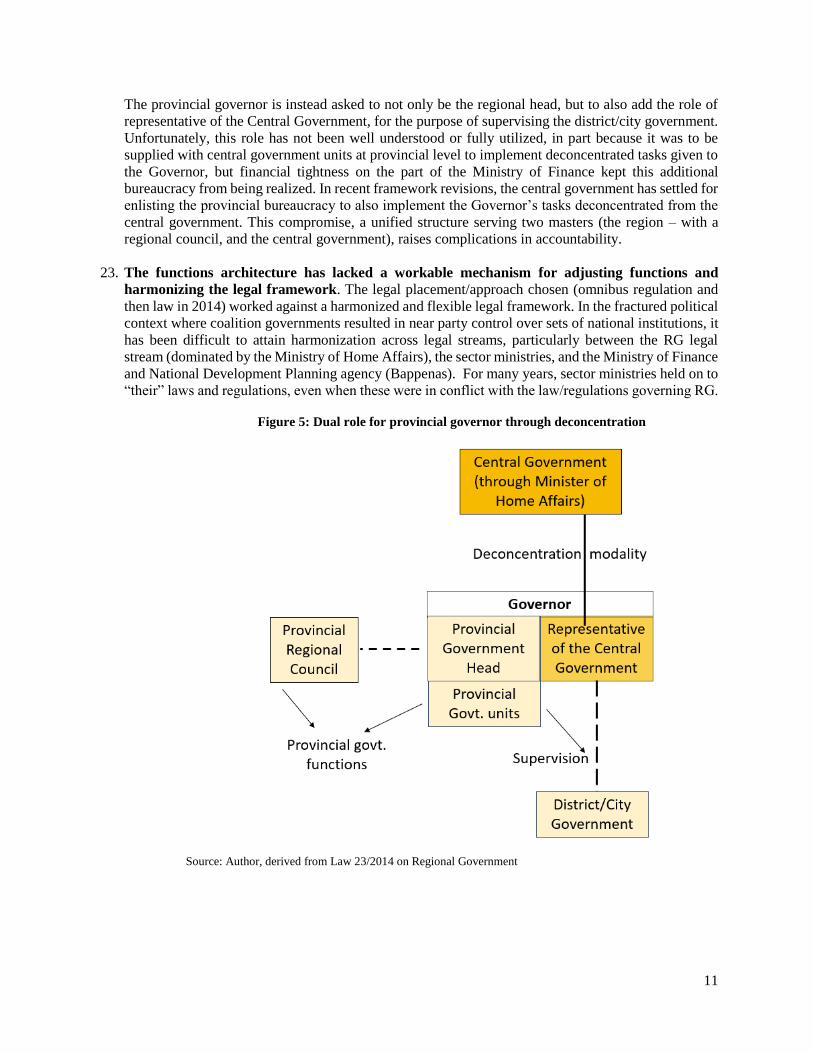

lic D

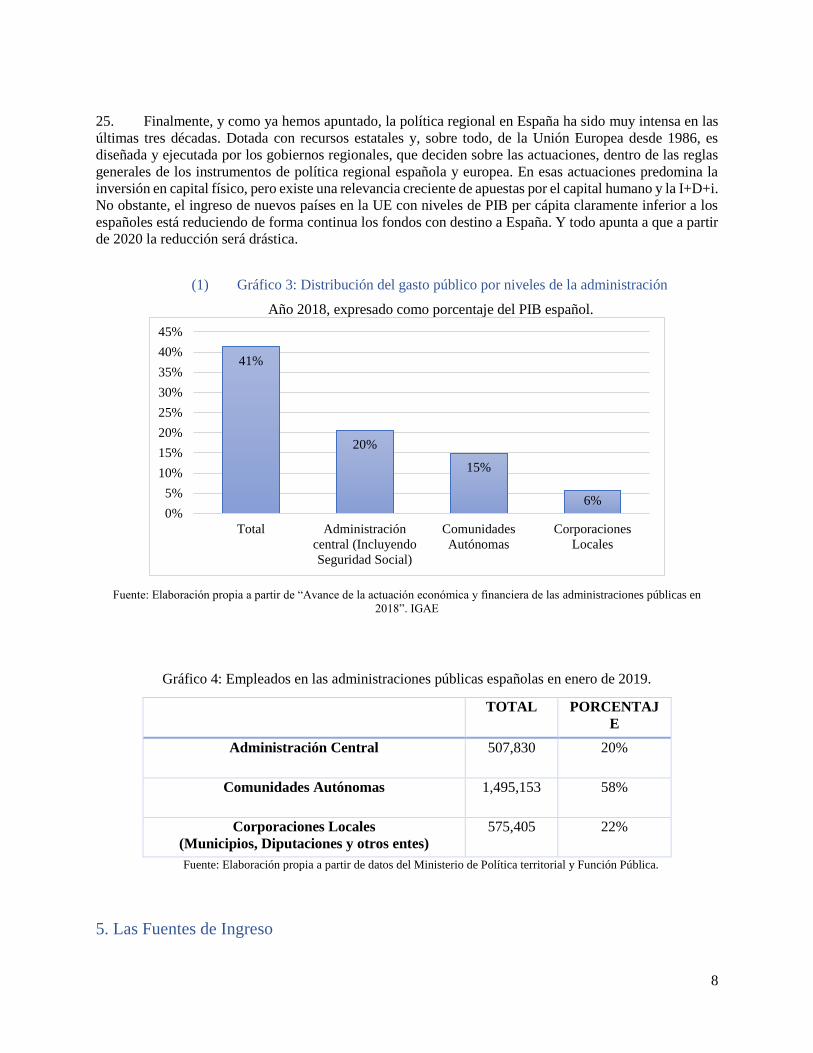

iscl

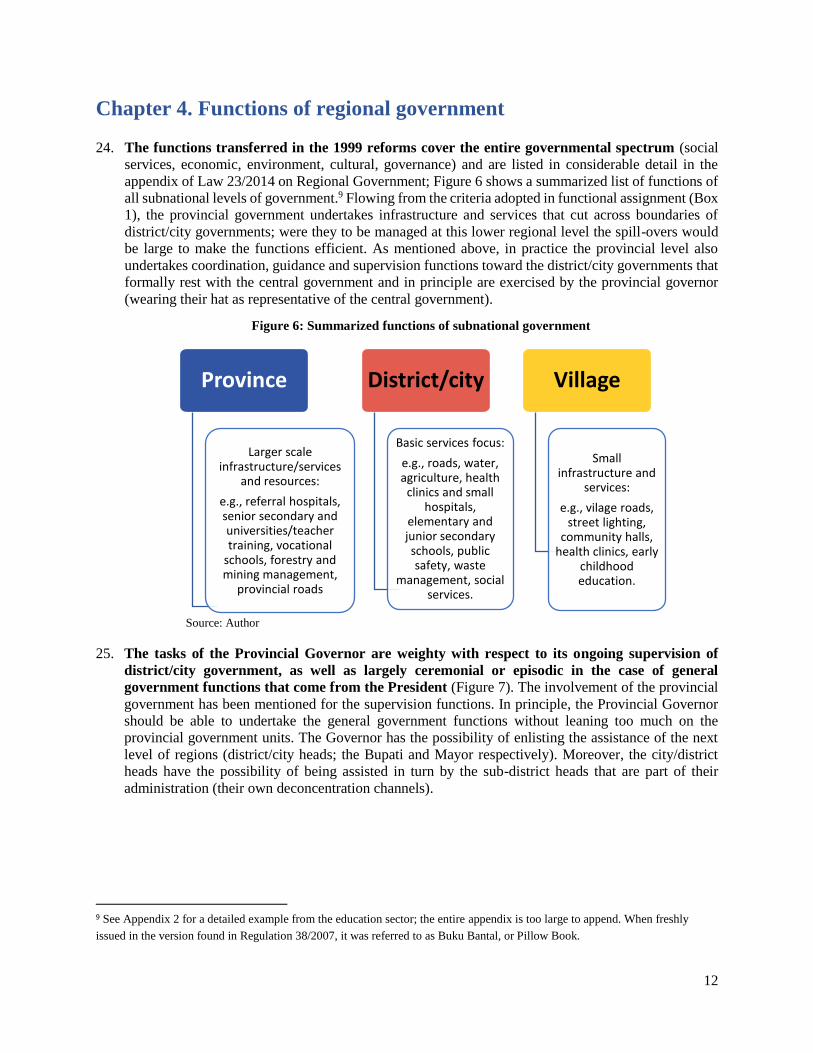

osur

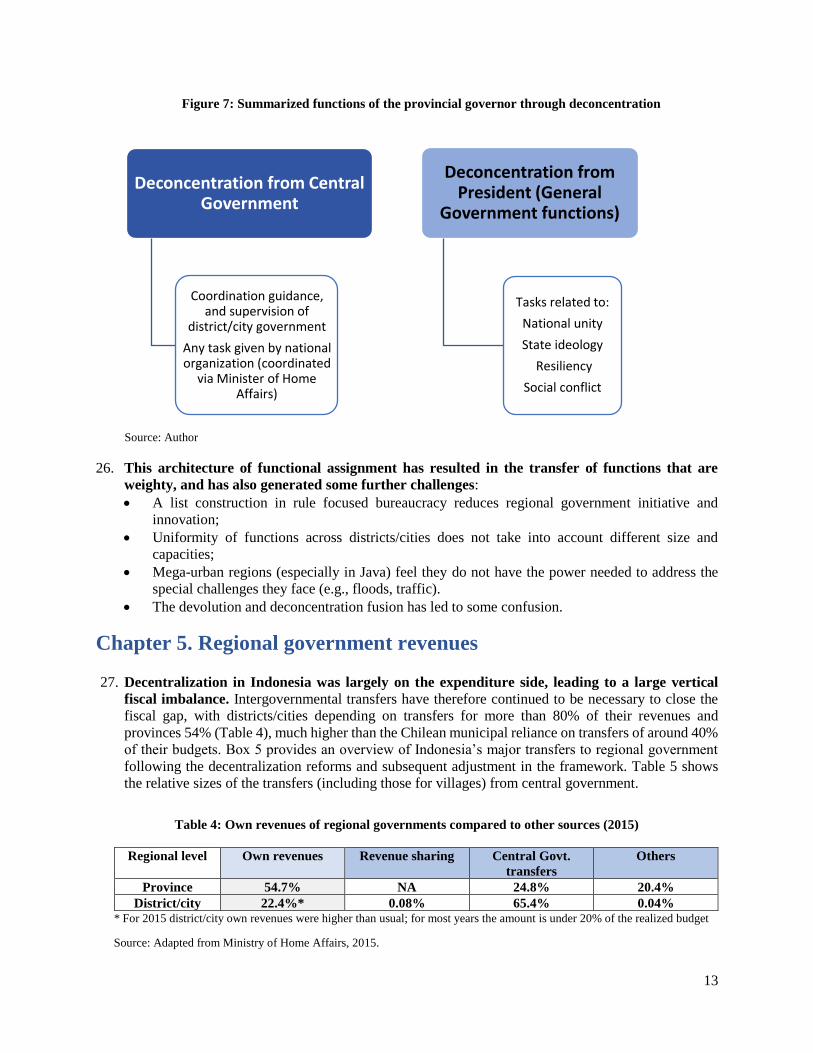

e A

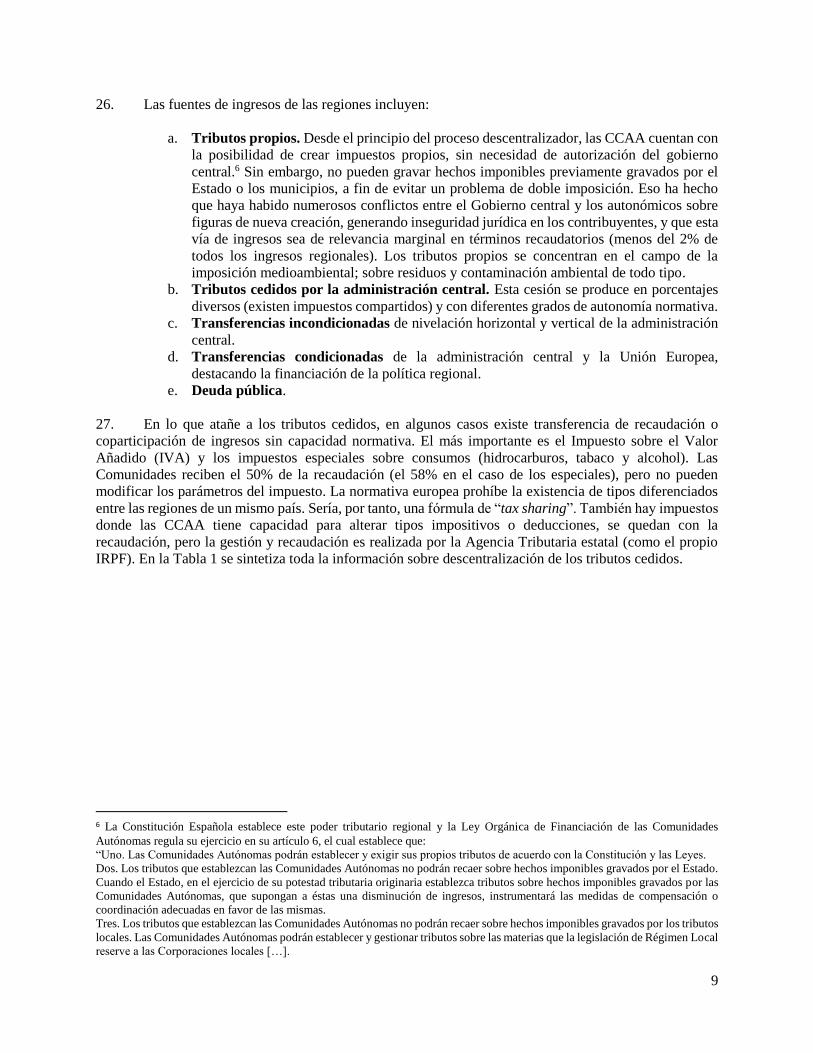

utho

rized

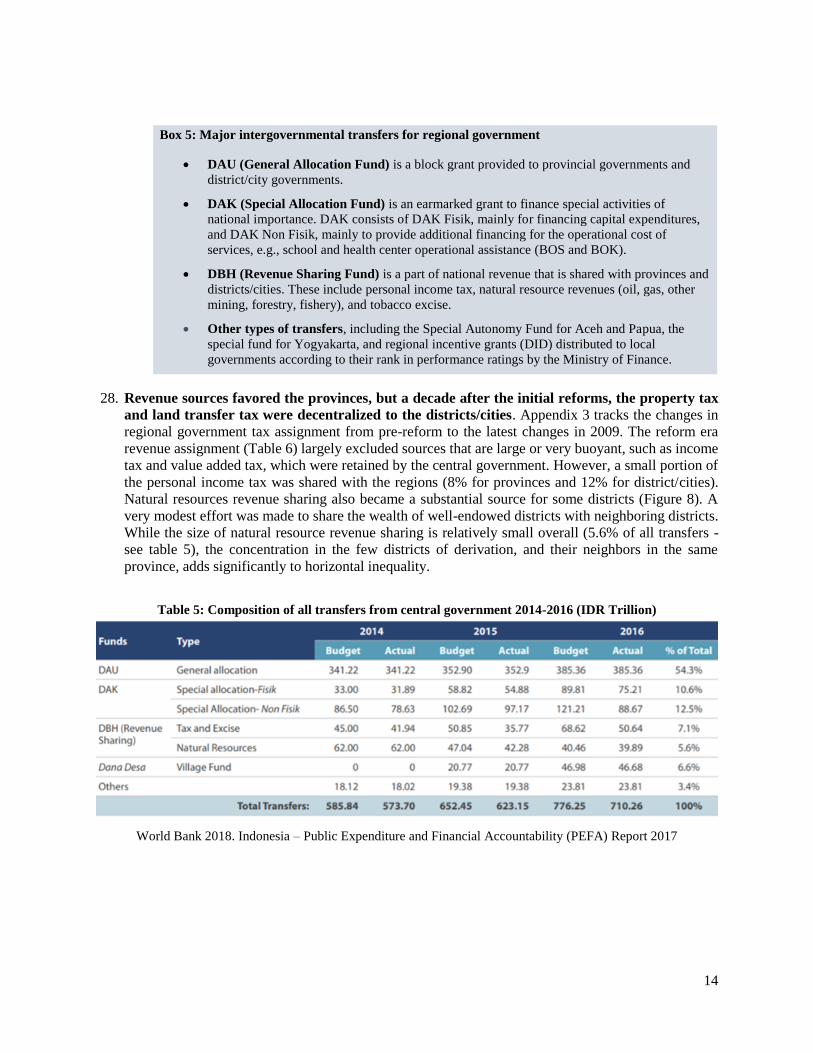

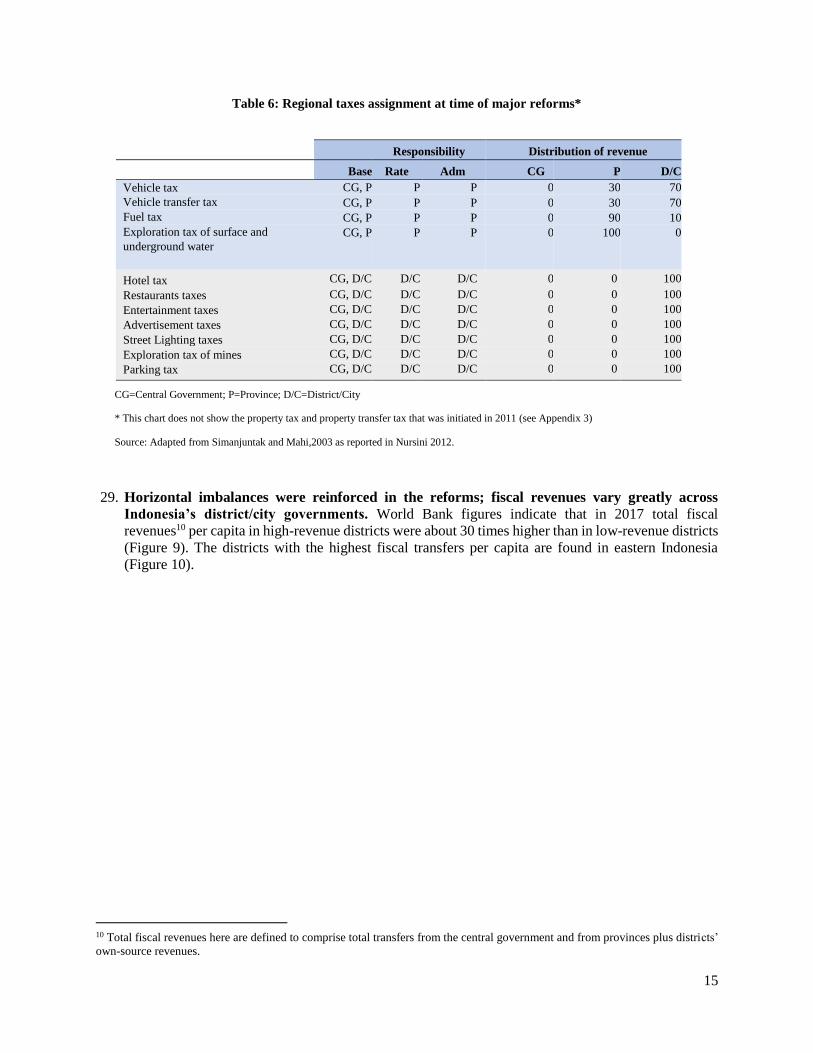

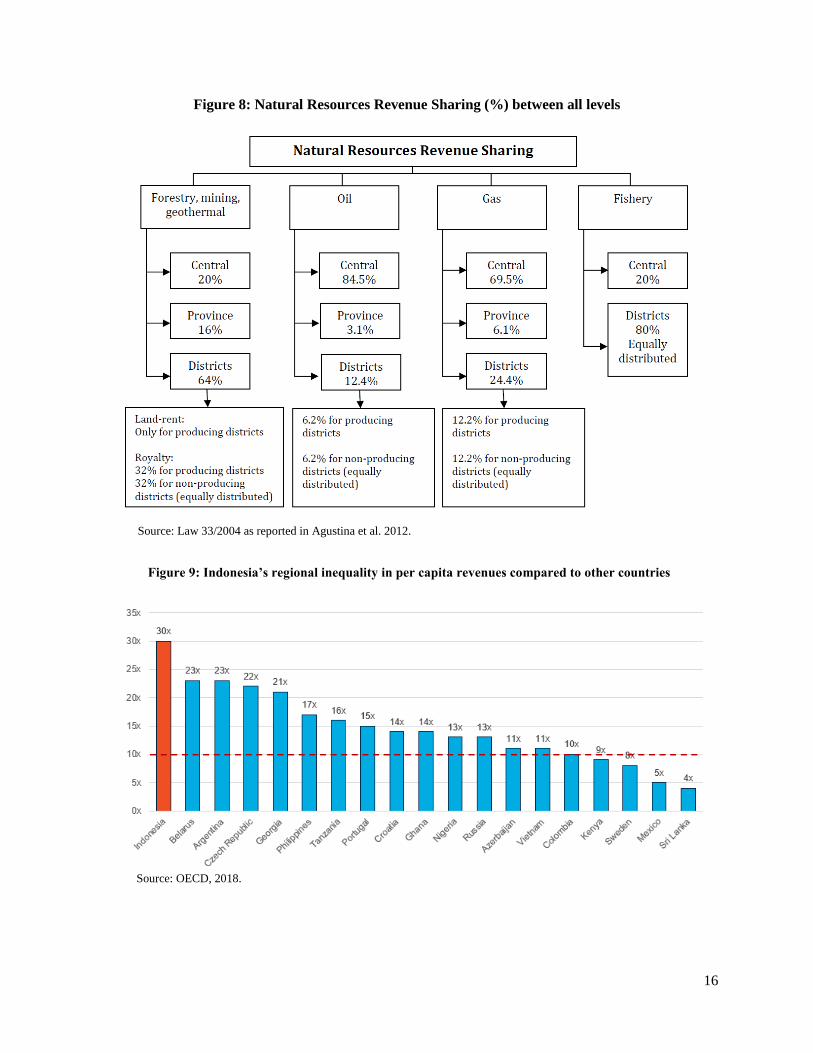

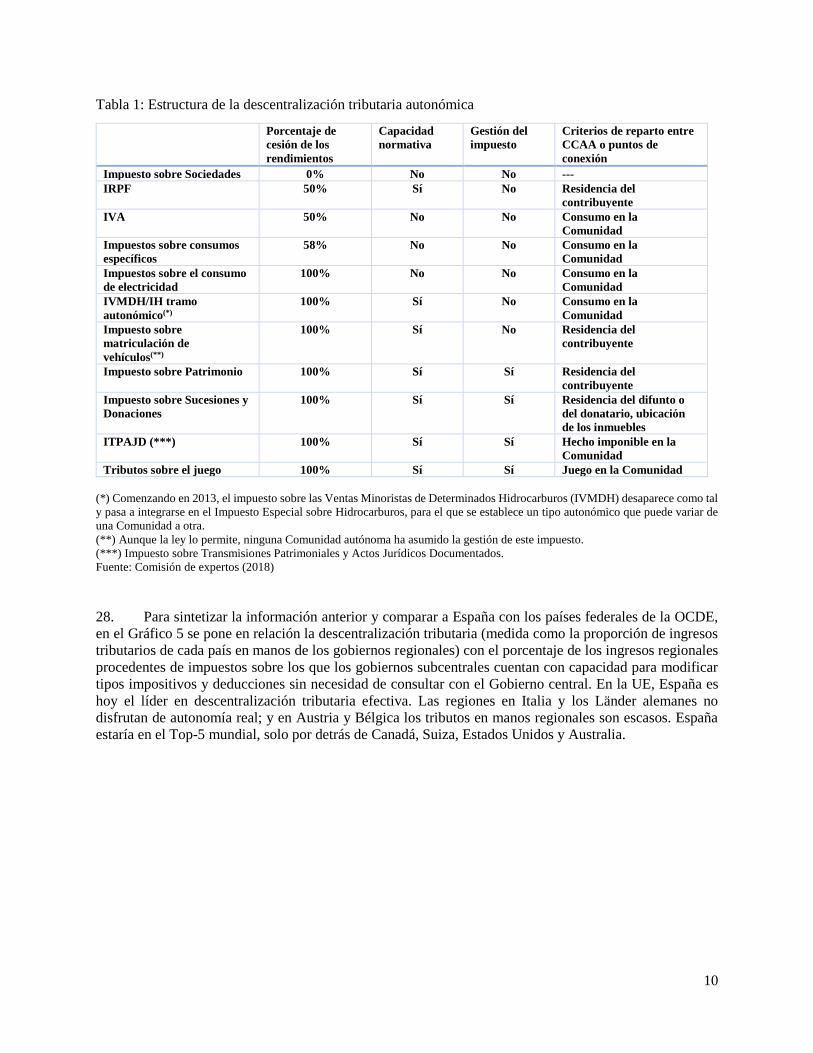

Pub

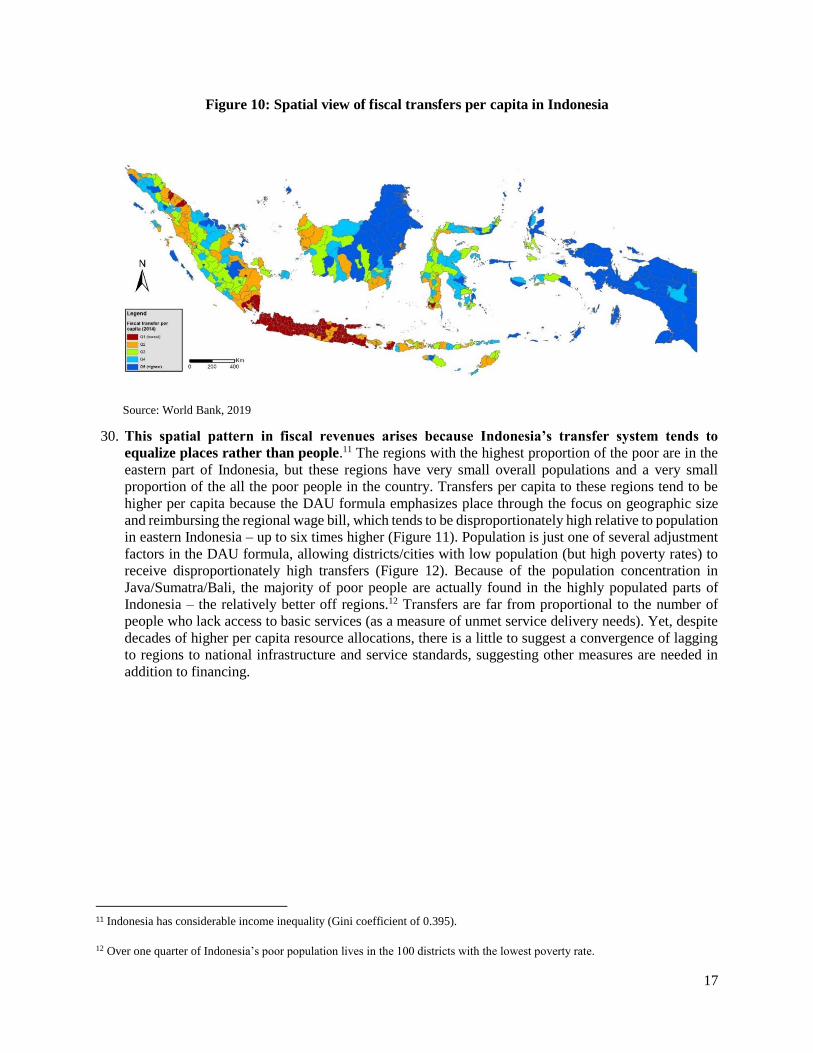

lic D

iscl

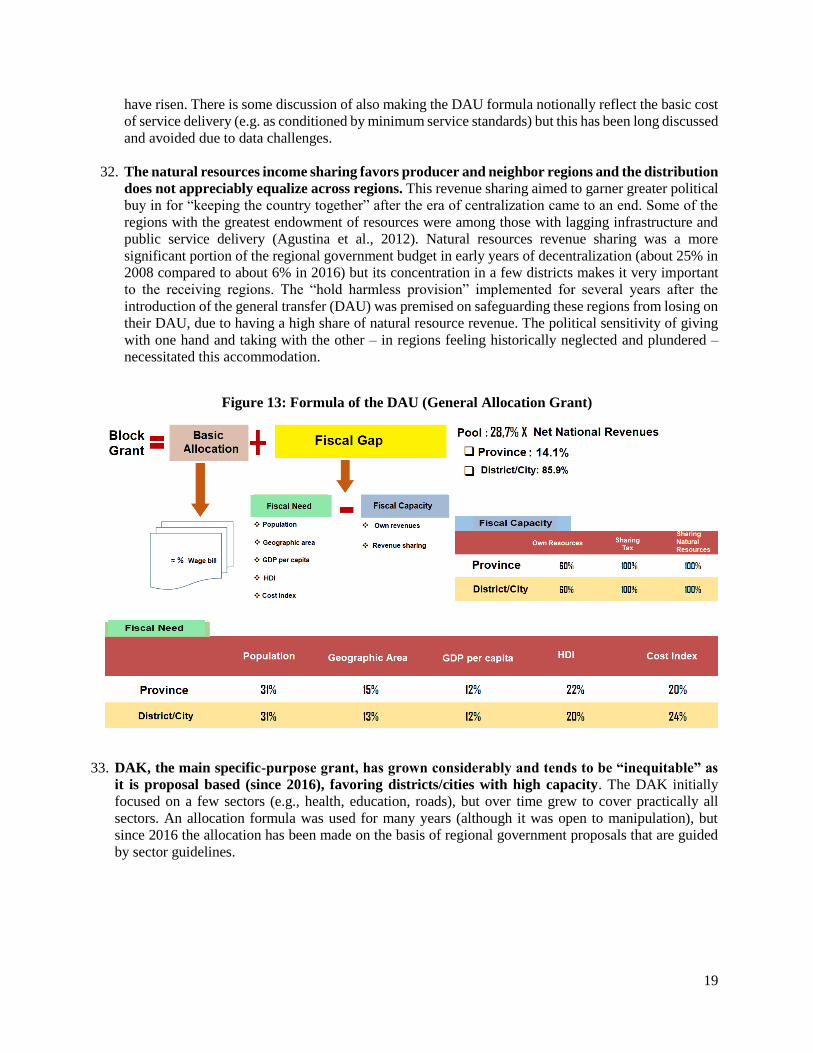

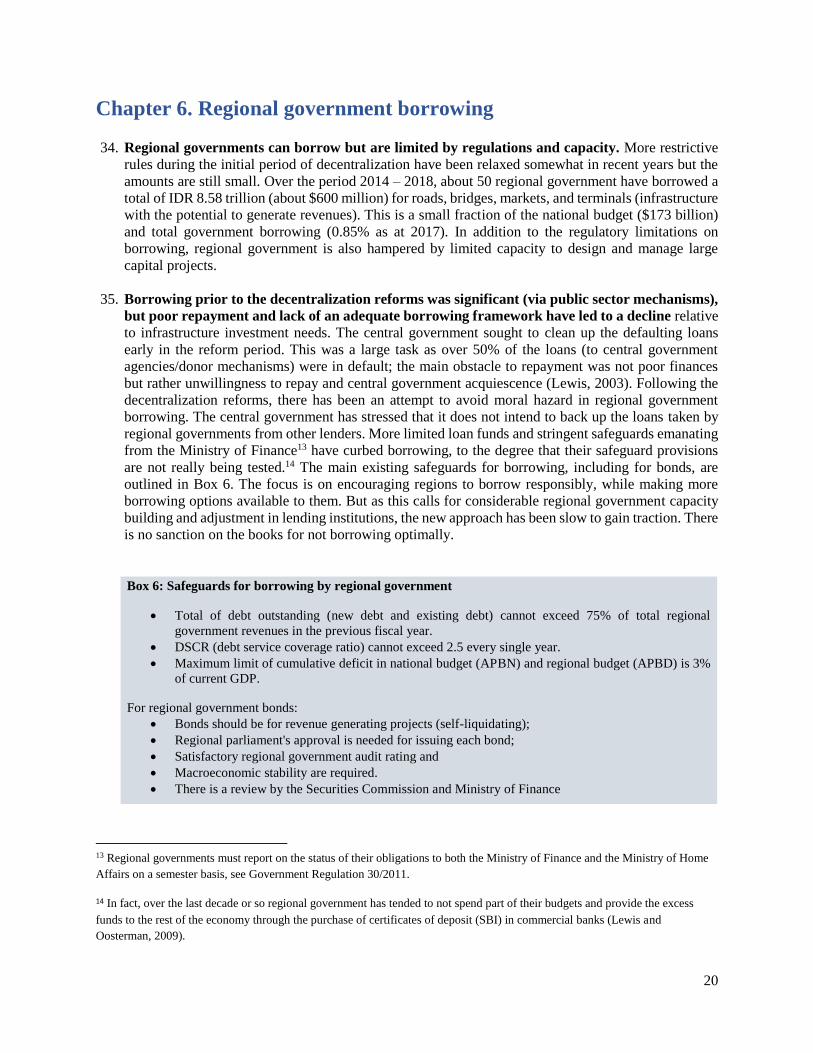

osur

e A

utho

rized

Pub

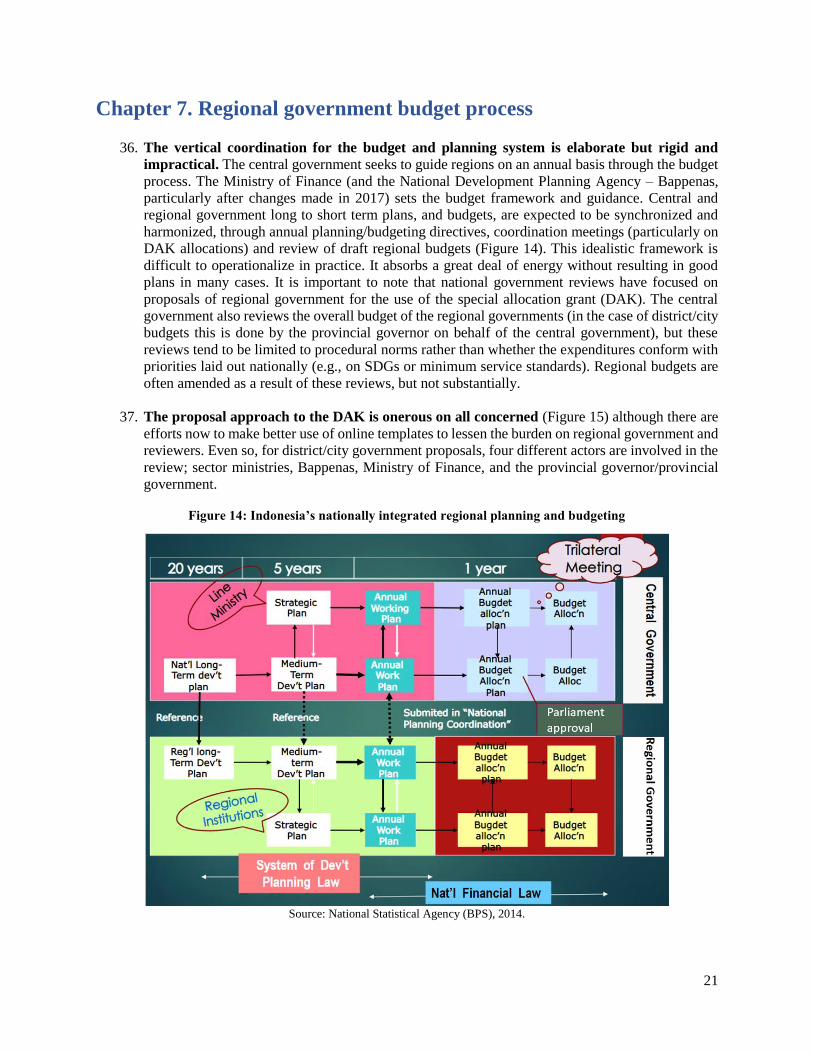

lic D

iscl

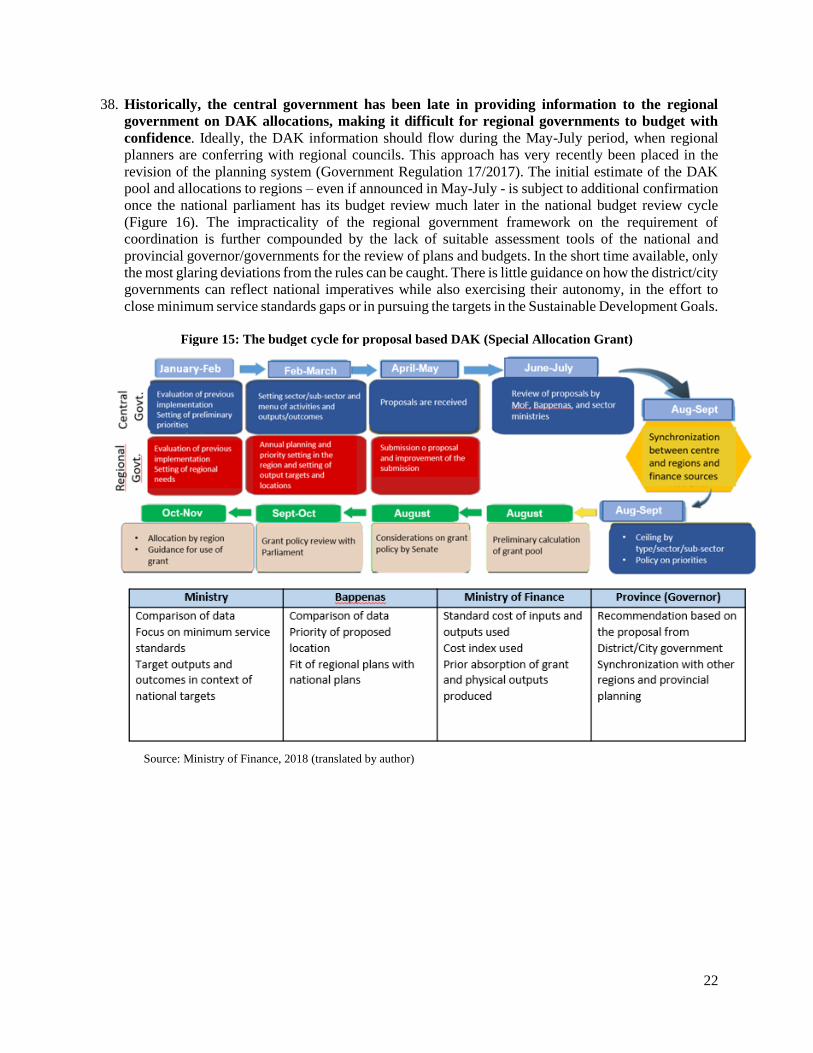

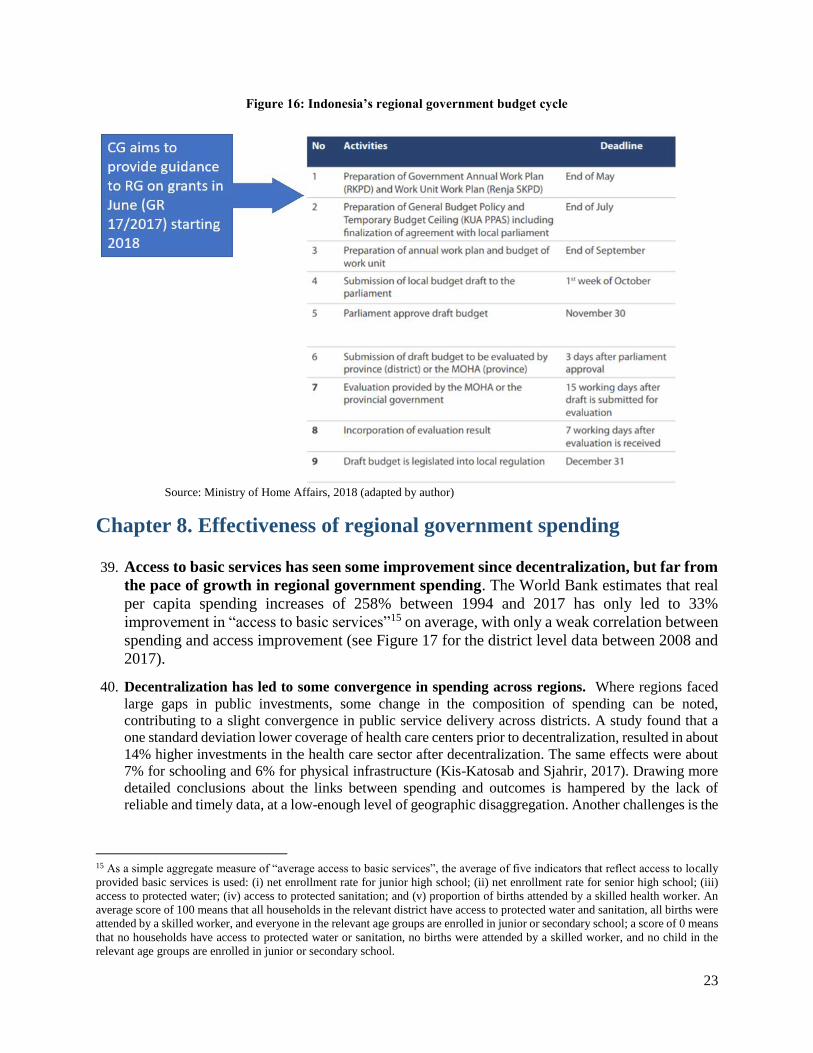

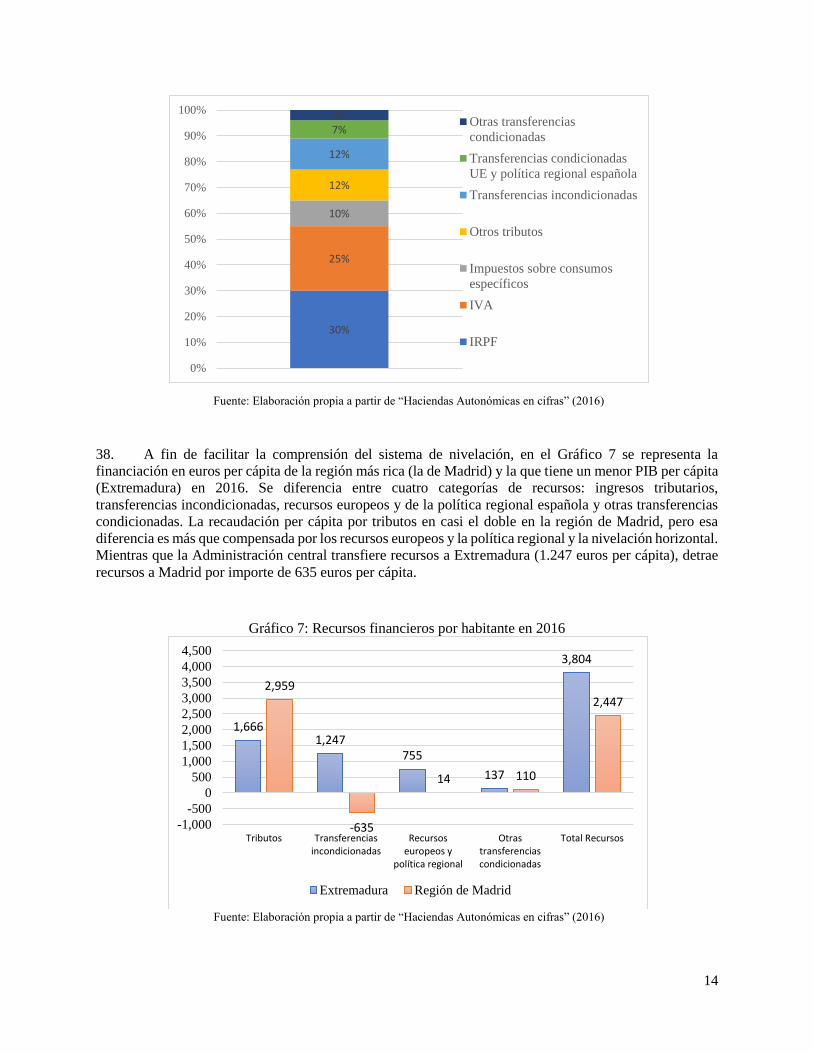

osur

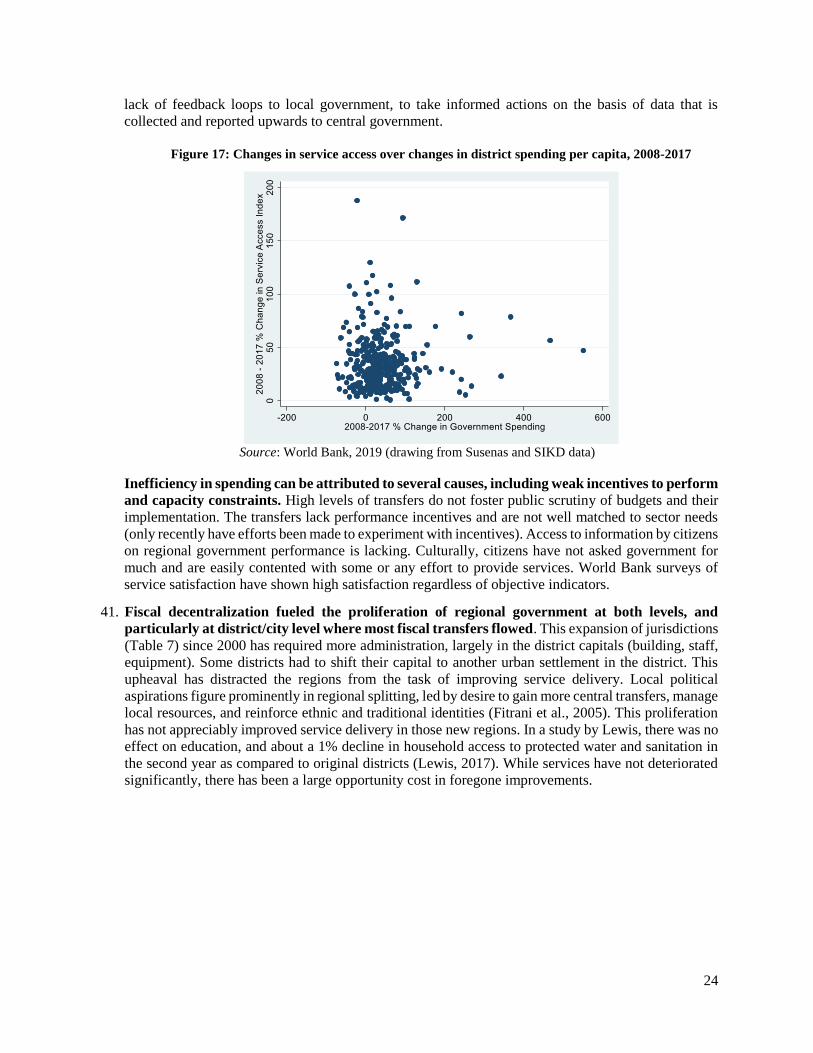

e A

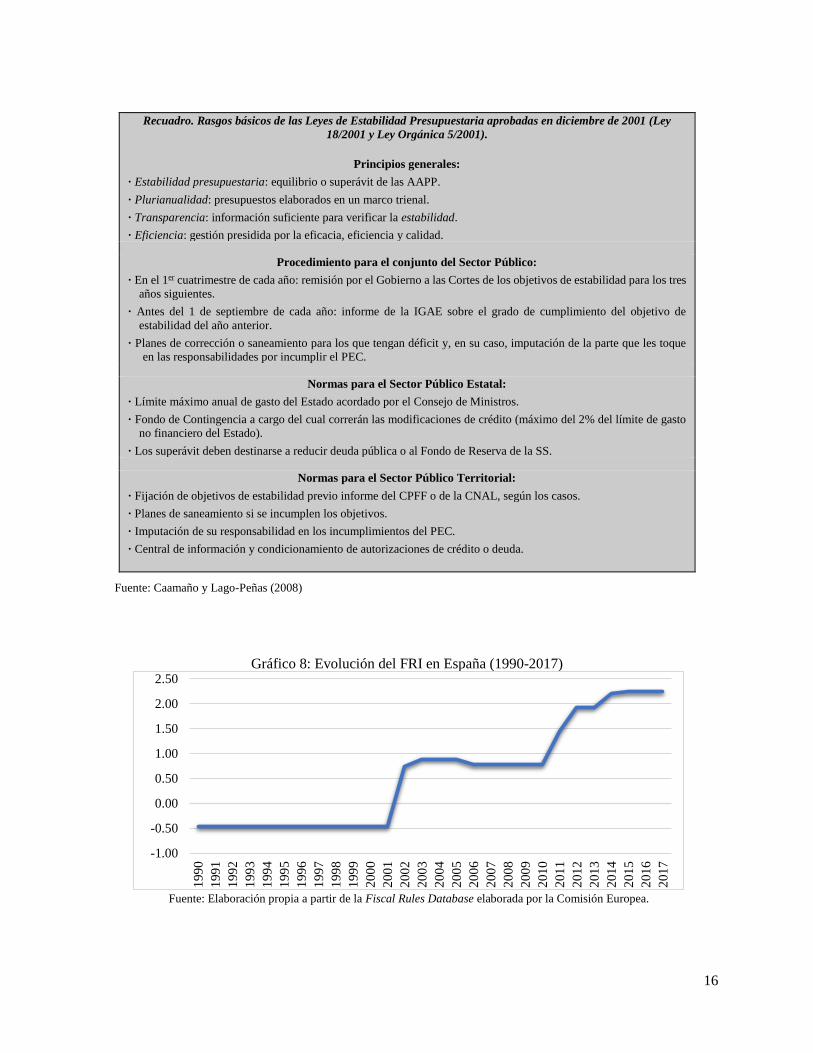

utho

rized

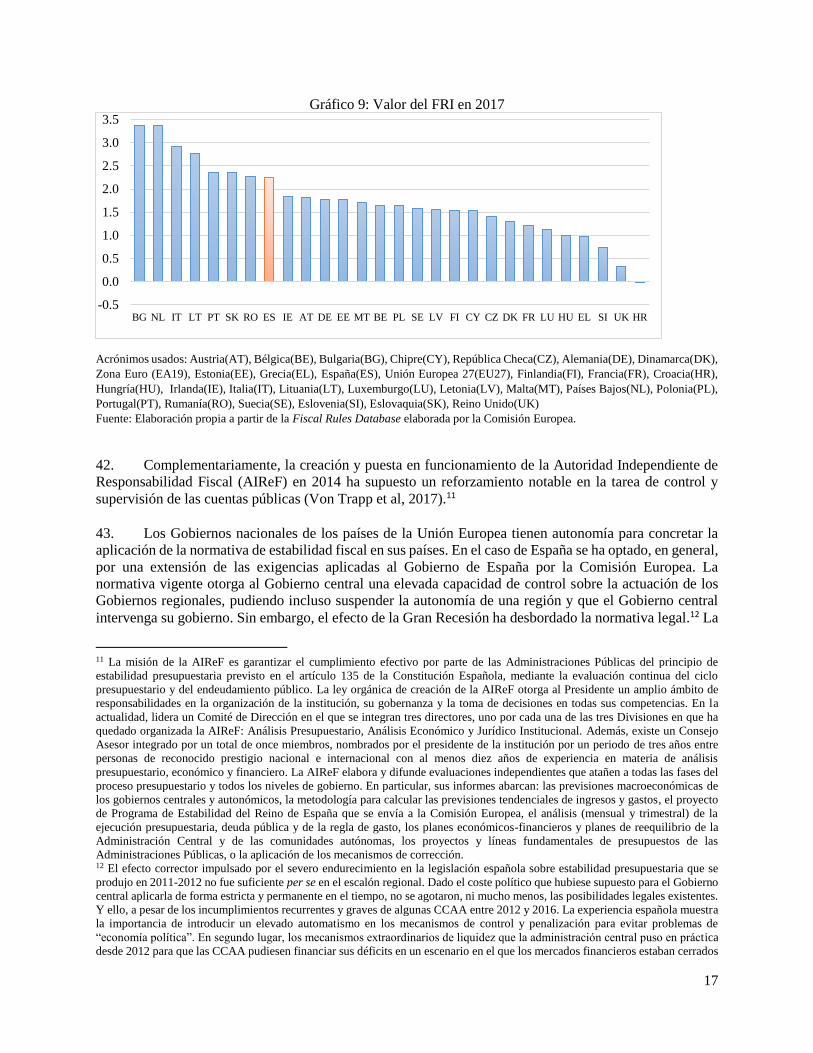

2

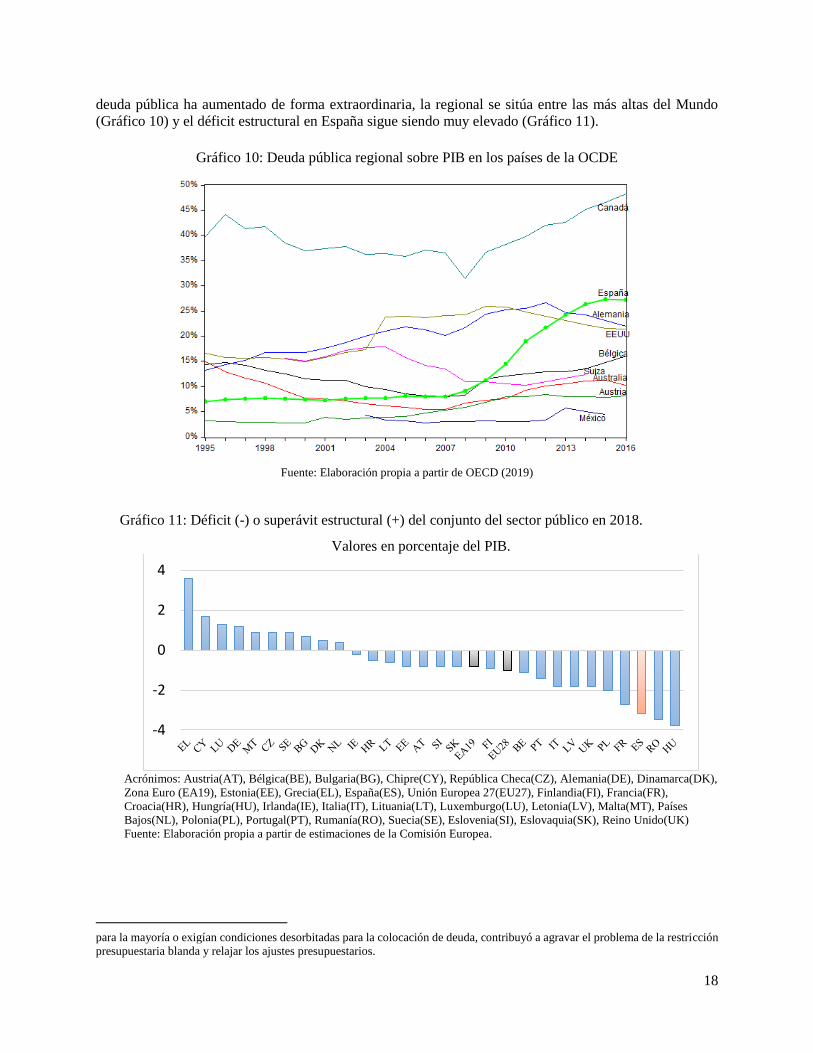

Foreword:

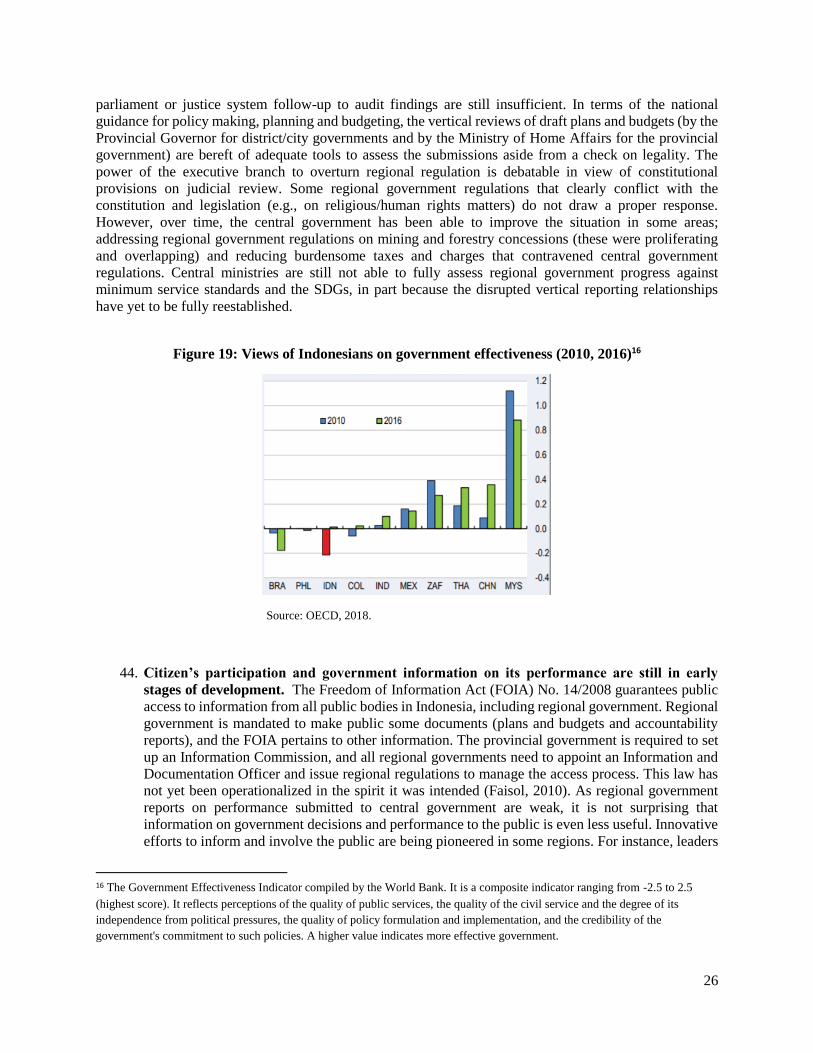

The World Bank has been requested to accompany the Chilean government in conducting a comprehensive

analysis of international experience with fiscal decentralization processes for regional level of subnational

governments. Such analysis will provide lessons and recommendations that can assist the Ministry of

Finance in designing and implementing the fiscal decentralization framework for regional governments in

Chile.

This work is aligned with the Government’s decentralization strategy which places the regionalization

process, in particular democratically elected self-governing regions with resources and responsibilities, at

the center of the reform effort.

This work is very timely, as Chile - confronted with social unrest towards the end of 2019 - will hold a

referendum regarding the current constitution and is embarking on a national debate to redefine the

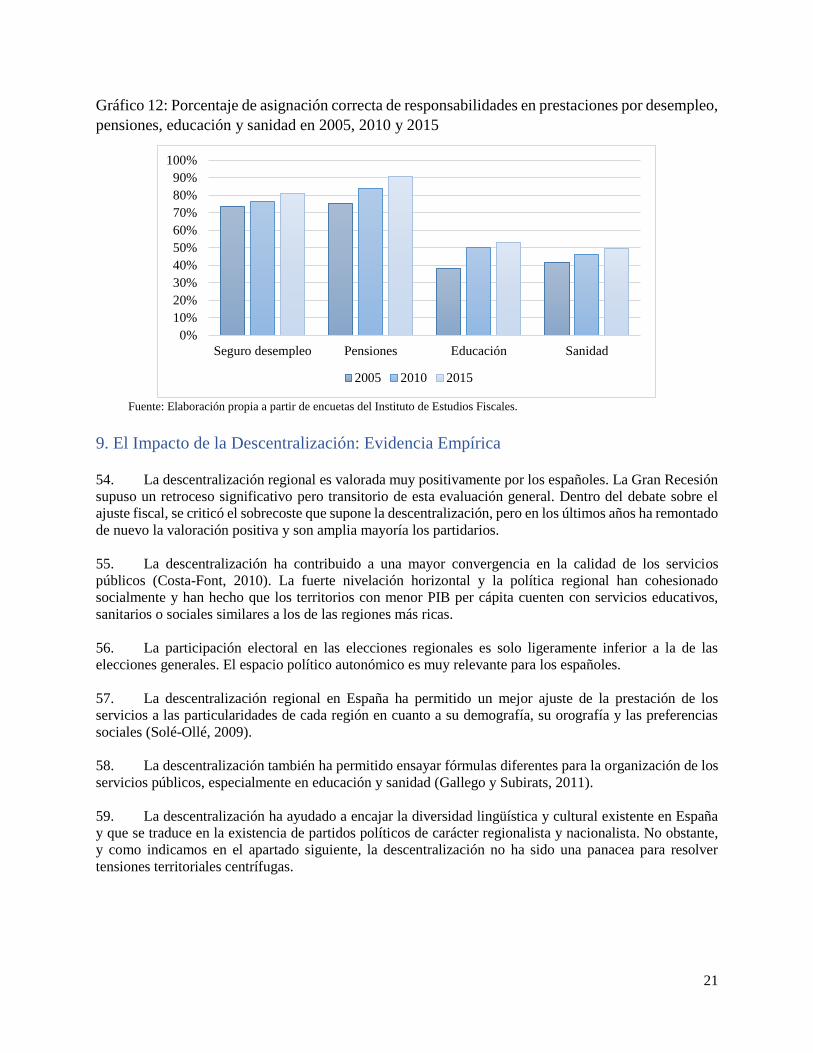

fundamental principles of state organization.

The study is comprised of two volumes.

Volume I provides a systematic review of the relevant international experience in fiscal decentralization for

the mid-level of government. The work focuses primarily on the aspects of fiscal decentralization from the

fiscal discretion angle, specifically expenditure responsibilities, revenue assignments, transfers and

subnational borrowing. This work is supplemented with a brief overview of selected aspects of fiscal

accountability related to the budget process, audit and control; as well as transparency and citizen

engagement.

Volume II includes in-depth case studies with descriptions and analyses of decentralization processes in

four selected countries: Colombia, Indonesia, Poland and Spain. This volume is prefaced by an overview

that summarizes the main issues and draws relevant lessons from the experience of these four countries.

The case studies for the report were selected jointly with the Government of Chile. The following criteria

were applied in selecting the case study countries:

• “unitary constitution” (rather than a federal structure);

• income per capita similar to that of Chile;

• decentralization experiences and insights are relevant and interesting in terms of both achievements

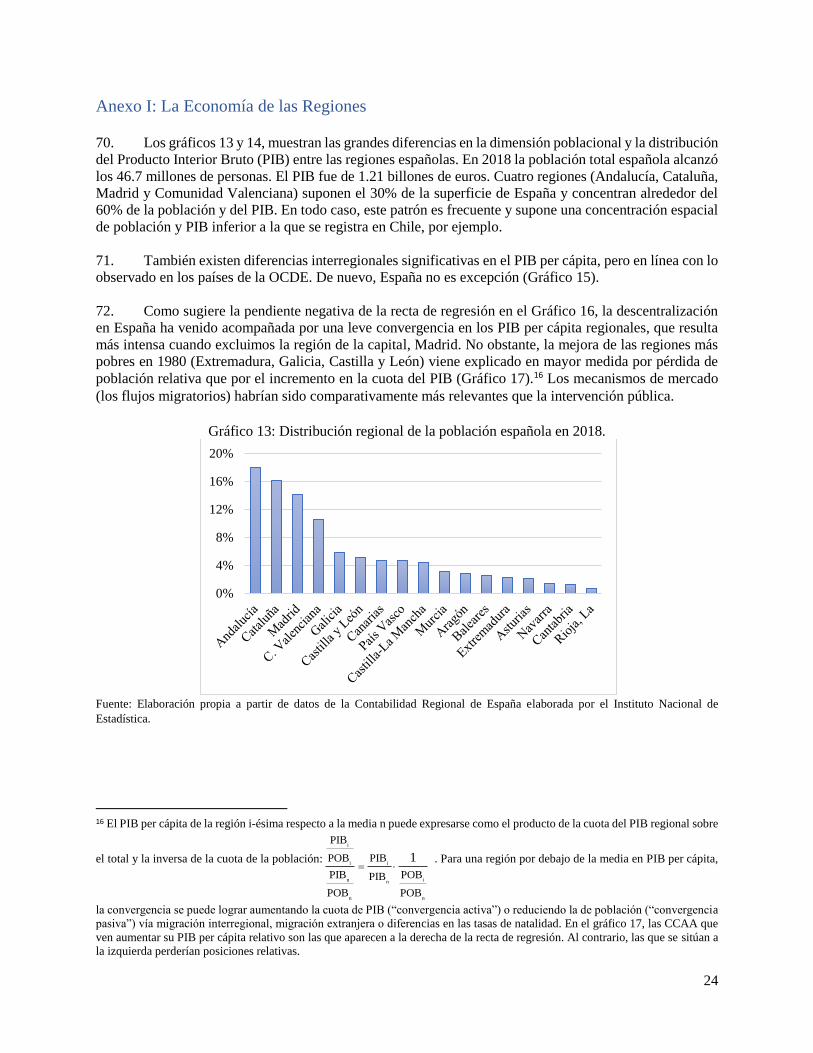

and failures; and

• existence of relevant “in-house” experience at the World Bank.

All case studies follow a similar structure – they provide a brief history of the decentralization process in

the respective country and describe major adjustments to the decentralization model. Next, they provide a

detailed analysis of the expenditure assignments and sources of funding (revenue assignments) for the

intermediate level of subnational governments. Each report also includes a discussion about subnational

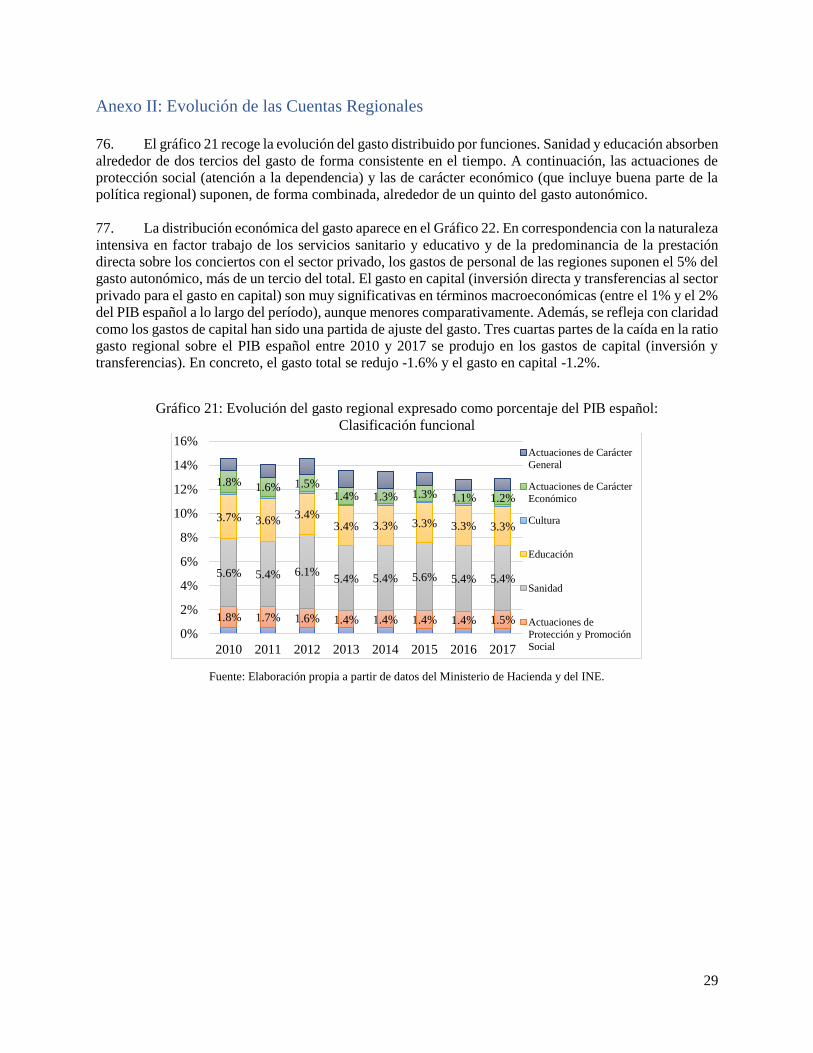

borrowing and fiscal rules. A separate section is dedicated to issues related to accountability, budget process

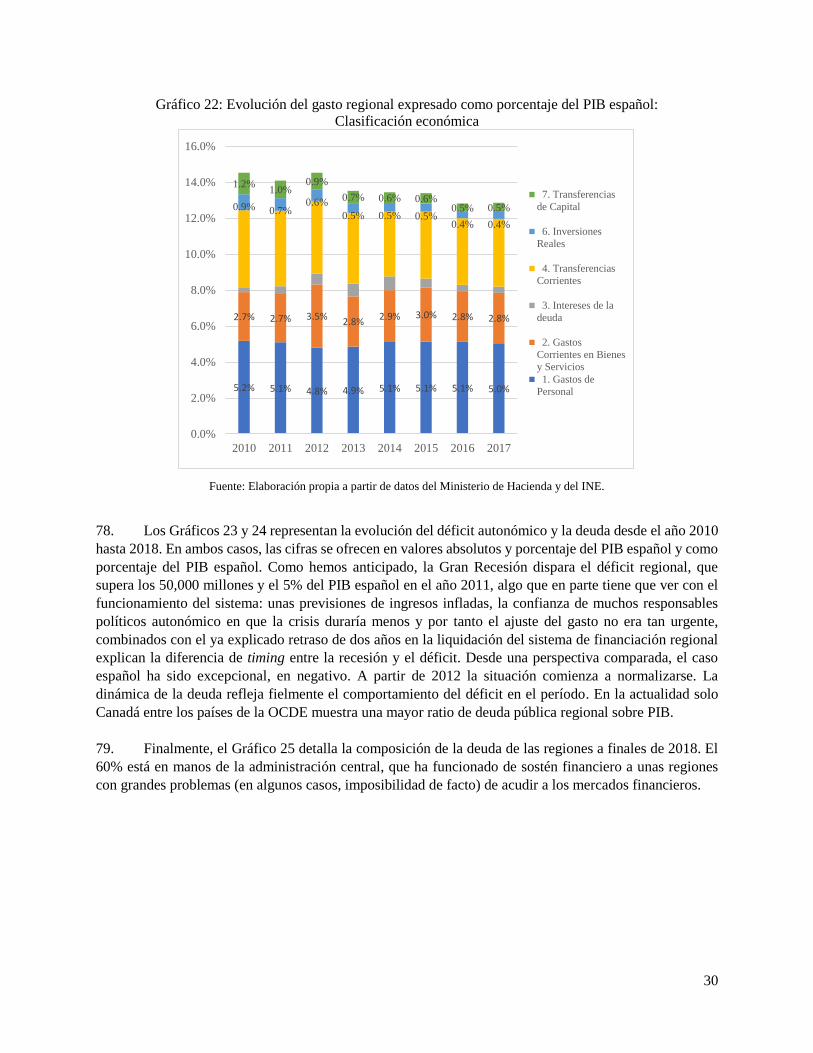

and control mechanism. Each report ends with a summary of the key lessons and their applicability to Chile.

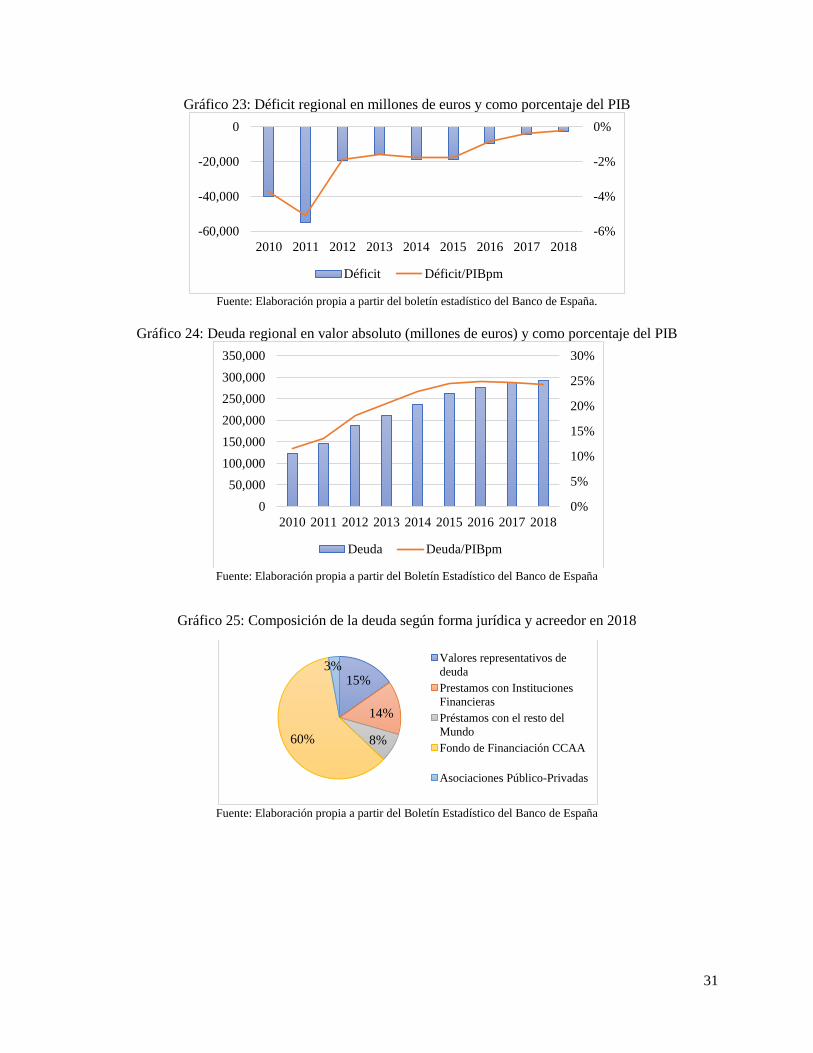

3

Overview

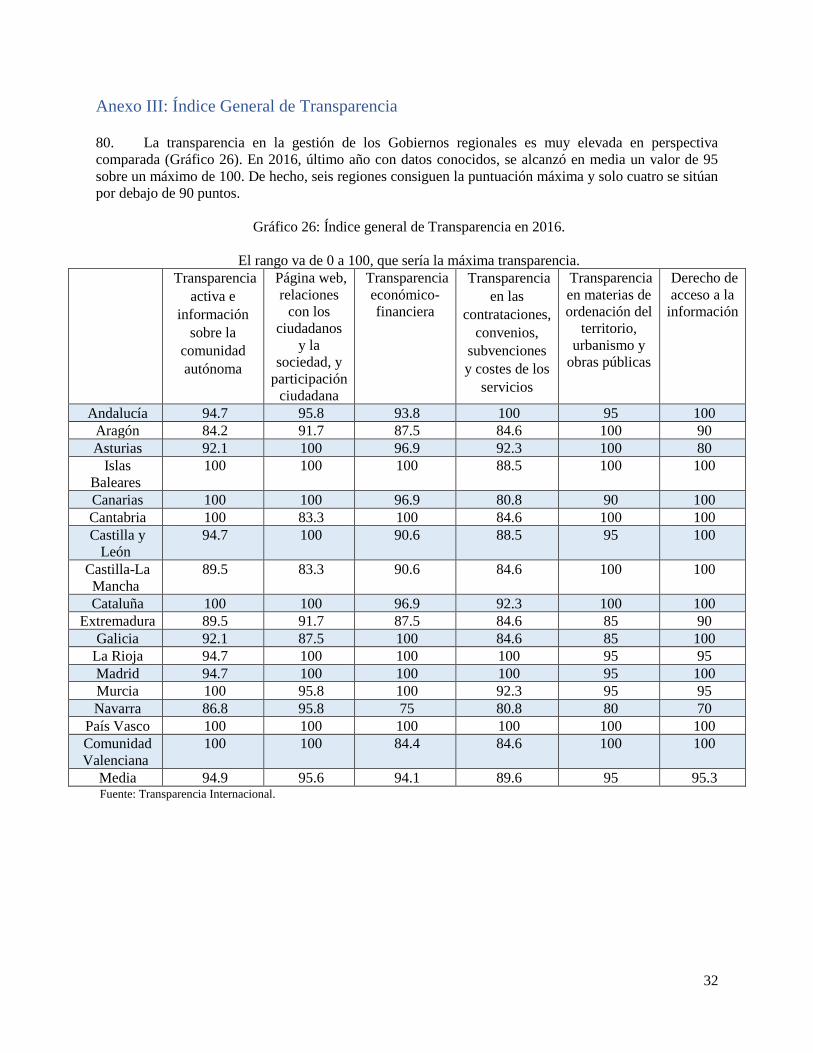

Decentralization process and its drivers

The case studies show that the process of decentralization is closely linked to specific circumstances

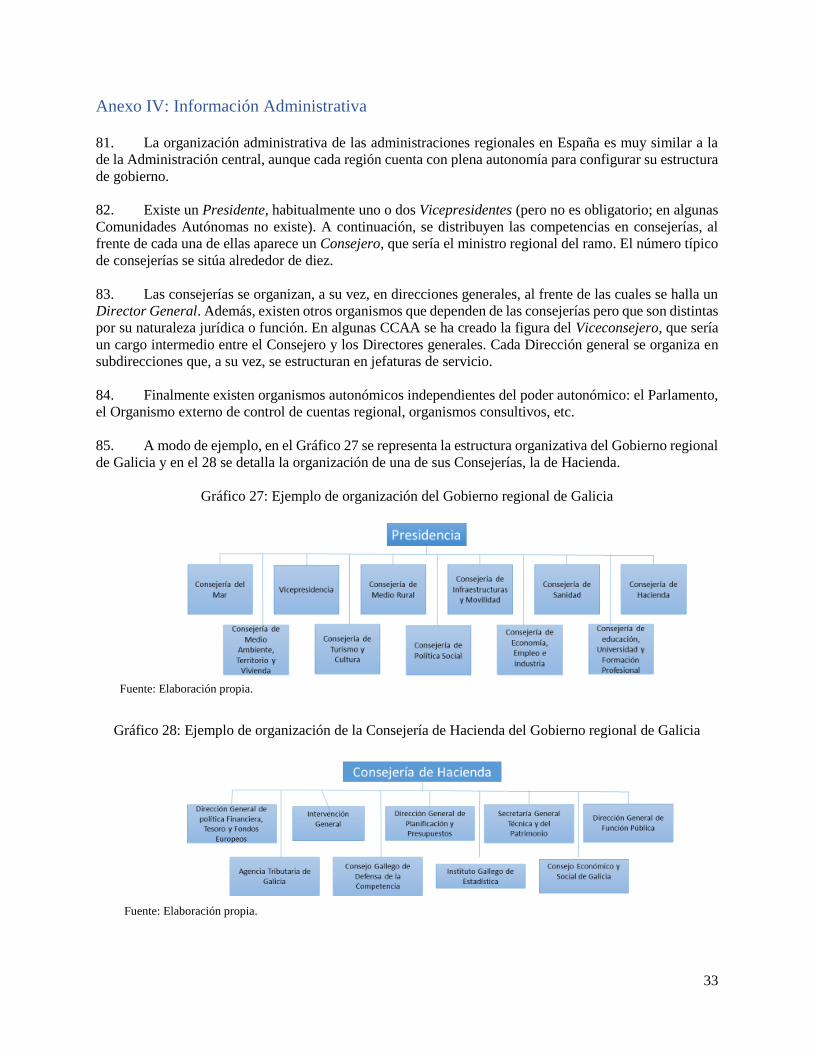

of the individual countries. The decentralization process in Indonesia is known in the literature as “big

bang”, as most of the decentralization reforms were completed within a short period of two years. In 1998,

the effects of the Asian Financial Crisis and the ensuing political turmoil provided Indonesia with the fertile

ground for decentralization reforms, which were generally driven by long-standing grievances regarding

limited democracy, concentration of wealth and political centralization. Without the benefit of a longer

period of preparation, Indonesia enacted several laws and the central government suddenly transferred

political authorities, responsibilities and financial resources to the districts and villages, but much less so

to the intermediate level, the provinces. In contrast, the process of decentralization in Colombia has been

evolving for decades. The early decentralization efforts in Colombia date back to the mid-19th century but

it was only in the 1980s that Colombia finally achieved fiscal, political and administrative decentralization

by assigning fiscal resources to the municipalities, allowing the election of mayors, and by transferring

functions from the central government to the subnational governments. For Colombia, in contrast to the

case of Indonesia, the decentralization process was gradual and comprehensive, as the policies were

oriented simultaneously to decentralize functions, resources and political responsibilities.

Similarly, the drivers behind the decentralization process varied considerably among the four

countries. In the case of Poland, the process of fiscal decentralization was part of a broader reform package,

as the country moved from a central planning system to a market economy. The prospect of the European

Union accession and the important role of subnational governments in other European Union countries

were important factors supporting decentralization reforms in Poland. In fact, Poland -as well as Colombia-

has had a long history of decentralization, but it was not until the 1990s, when comprehensive

decentralization reforms were launched. Political events also prompted decentralization in Spain, where a

phase of transition towards democracy coincided with death of General Franco in 1975. By 1977, the first

Autonomous Communities (Regional Governments) were established, and the decentralization process was

officially launched. The new Constitution of 1978 incorporated three governmental levels: Central

Administration; the regions called Autonomous Communities; and the Local Corporations, which include

the municipalities and the provincial councils.

Expenditure assignments

The experiences of case study countries show that most sectoral competencies are overlapping,

although central government tends to play a leading role in regulatory framework, while

implementation is devolved to subnational governments. For example, in Colombia, the 1991

Constitution granted the central government responsibilities related to the design of sectoral policies, while

their implementation was delegated to the subnational level. Initially the financing of these policies was

provided with resources from the National Budget; however, the system evolved with the introduction of a

system of intergovernmental transfer systems and the strengthening of own revenue sources for subnational

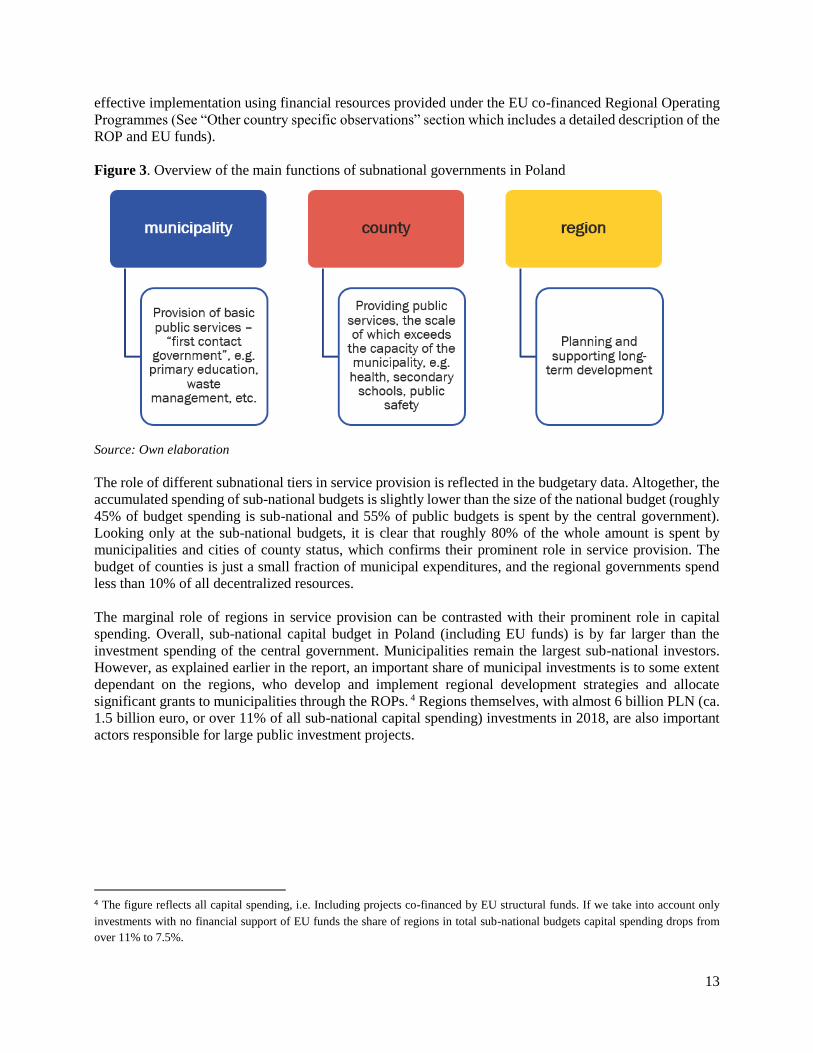

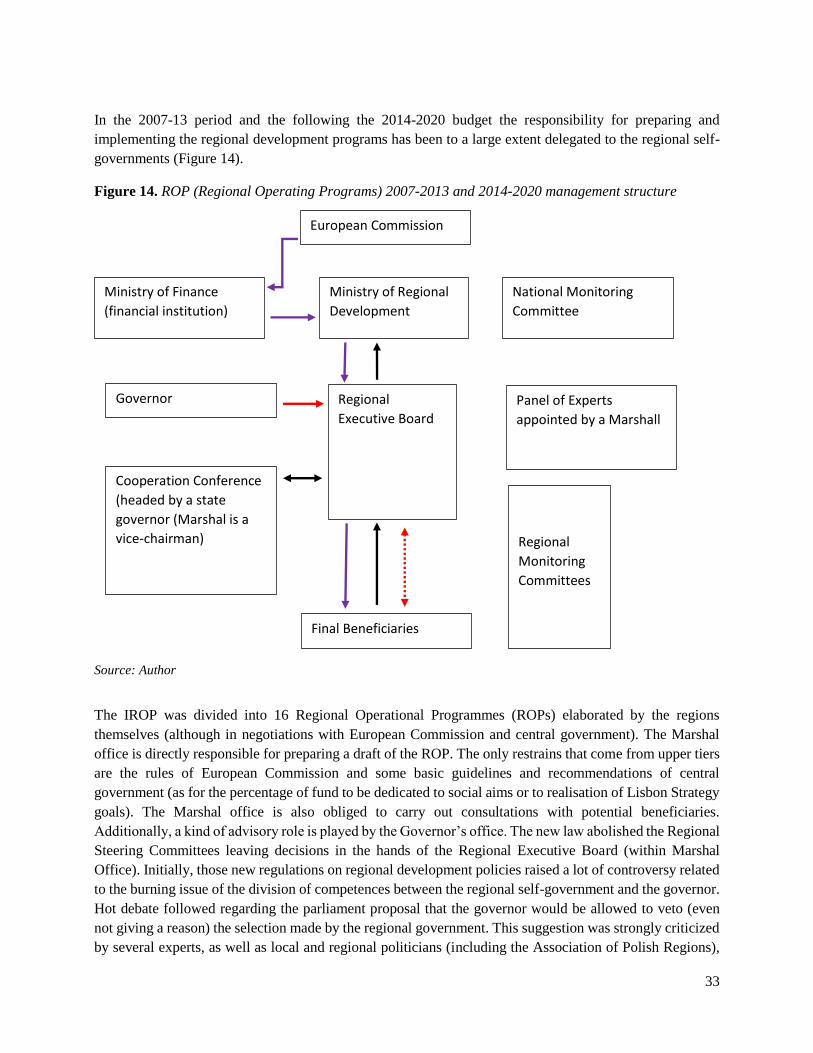

governments. In Poland, regional governments have just a few specific service delivery functions that are

related to sectoral competencies, and their primary role is with regards to the programming of regional

development policies, especially in the context of the significant European Union structural funds. Regional

governments also play a much more pronounced role in public investment than other layers of subnational

governments, which helps to exploit existing economies of scale. The case of Spain shows much more

emphasis on delegating functions to the intermediate level of subnational governments. Regional

governments in Spain share many regulatory functions with the central government, especially with respect

to territorial management, culture, environment, R & D policy, transport infrastructure, etc. And there some

4

hierarchical relationship in the sense that regional governments can decide on the organization of

municipalities and provinces within their regional territory.

Among case studies, there are examples of both uniform and asymmetric decentralization models.

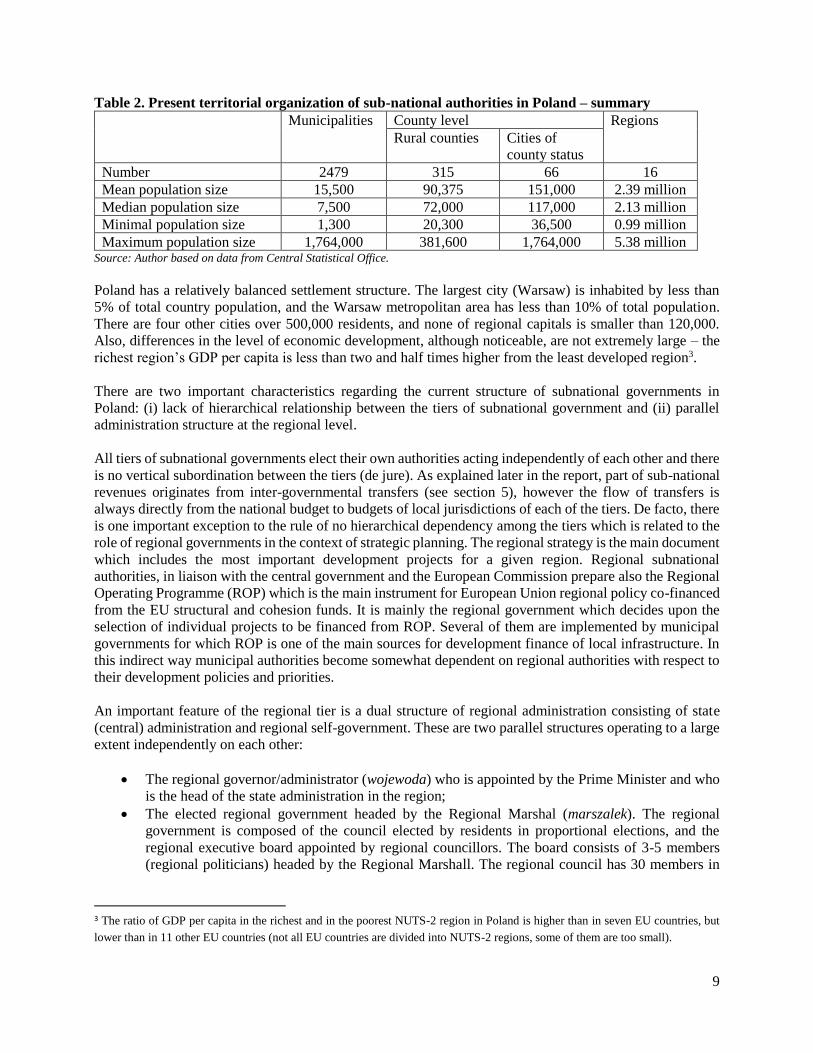

For example, in the three-tier structure of subnational governments in Poland, each tier has its specific

functions defined in the legal framework. All subnational governments belonging to the same subnational

tier, have the same set of responsibilities, hence there is no asymmetric decentralization. In contrast, in

Indonesia, Colombia and Spain, the process of decentralization was asymmetric with regards to political,

fiscal and administrative/management function. For example, 5 regions in Indonesia are granted a stronger

role in selected aspects of management or economic policy. In Colombia, political asymmetry in

decentralization is present through the special rights of indigenous peoples to manage their own territory or

special metropolitan status of Bogota. Special administrative and management functions have also been

granted to six other metropolitan areas. Finally, in Spain, at the regional level, decentralization is

asymmetric, with two distinct regimes: the common regime (15 ACs) and the “foral” regime (Basque

Country and Navarra), with this latter characterized by an almost complete spending and revenue autonomy.

In addition, ACs of the common regime each have their specific statute, allowing for some distinctive

features, especially since the 2000s (several statutes have been reformed case by case).

In some of the countries the decentralized subnational governments coexist with the deconcentrated

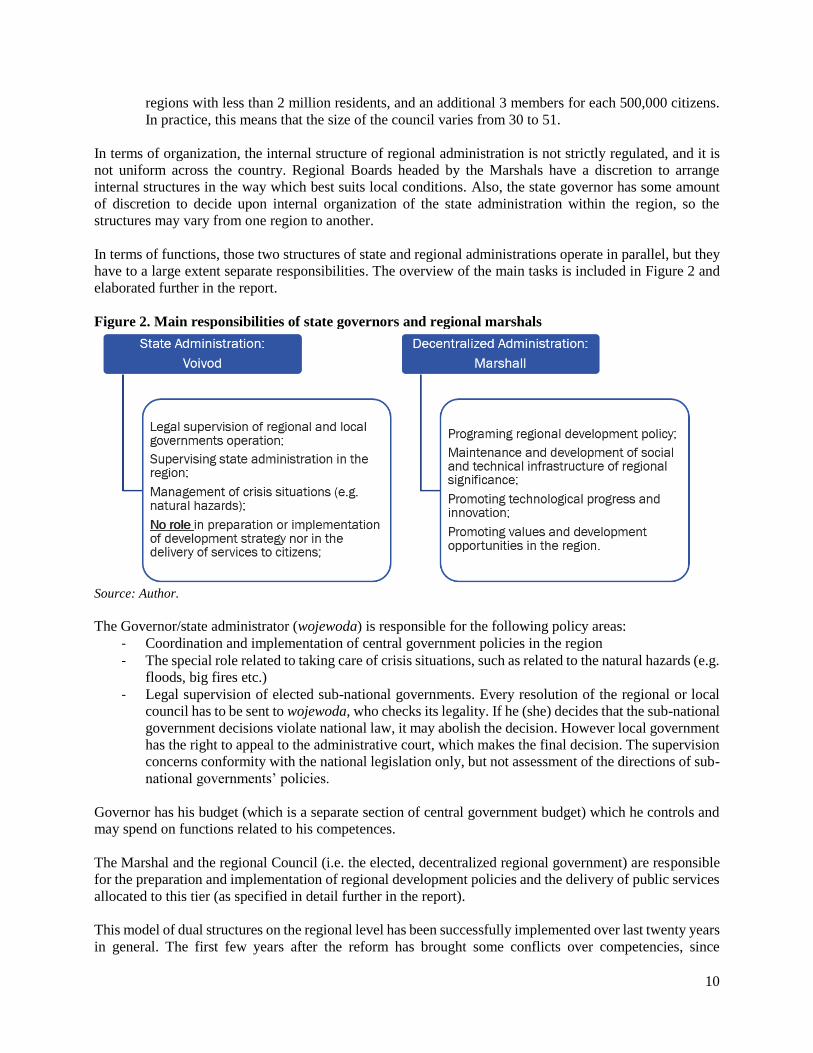

central government units. Poland’s case is interesting as at the regional level there are two parallel

structures operating to a large extent independently of each other: the regional governor/administrator

(wojewoda) who is appointed by the Prime Minister and who is the head of the state administration in the

region; and the elected regional government, headed by the Regional Marshal (marszalek). While at the

beginning of such dual system there were some conflicts over competencies, the model has been

successfully implemented over last twenty years and currently there are no conflicts between the two

structures even when the subnational authorities represent different political views than the central

administration holding office. However, in the case of Indonesia, the dual role of provincial governor as a

regional head and a representative of the Central Government for the purpose of supervising the district/city

governments, has not been well understood or fully utilized leading to complications with public

accountability. In the case of Spain, there are territorialized agencies of the central administration and a

“delegate” of the central government in each region, but the regional administrations (CAs) function

entirely in a separate and autonomous way.

Revenue sources

In most cases analyzed subnational tax autonomy is rather limited. The subnational regional

governments in Poland have virtually no own revenues, except for small revenues from fees and property

constituting less than 5 percent of regional budgets. Even though the legislation in Spain allows that the

Autonomous Communities create their own taxes within the regional borders, in practice there are many

impediments and as a result the role of own taxes in the revenue structure of regional governments at 2

percent is rather insignificant. However, the so called “ceded” central taxes, including 50 percent of the

central personal income tax and others, and for which regional governments can select rates and tax base,

provide much higher levels of revenue autonomy. In the case of the Basque Country and Navarra e

autonomy is still much higher, as these regional governments benefit from all taxes except import duties,

payroll taxes, VAT and excise duties. In Colombia, the central government retained the main sources of

public revenues including the income tax, the value-added tax and taxes on international trade, and

subnational governments have limited taxing autonomy and little discretion over tax rates and bases.

Several taxes are earmarked for specific use defined by the law. Taxes represent around 20 percent of

revenues for departments and include receipts from the excise taxes (beer, tobacco, liquor), vehicle tax,

register tax and gasoline tax.

5

Regional governments seem to receive quite substantial resources from tax sharing arrangements

with the central government. While there are different types of tax sharing arrangements, it seems that

regional governments in Spain have somewhat larger fiscal leeway whereby they participate in sharing of

major taxes (PIT, VAT, excise) and also have autonomy over the wealth tax, inheritance and gift tax, tax

on capital transfers, gambling tax, vehicle excise and hydrocarbons retail sales tax. In Poland, tax sharing

arrangements include PIT and CIT, the latter being particularly problematic both in terms of its sharing

formula and high volatility leading to large horizontal disparities among regions and cyclical swings in their

revenue base.

Different transfers play an important role in subnational financing and help achieve important

objectives within the fiscal decentralization process.

• In Poland, the general grant (non-earmarked) constitutes the most important grant. It is made up of

several shares, including the education share, the equalization share, the balancing share and the

regional share. The education share is by far the largest, and it aims at covering educational

expenses, including teacher’s salaries, but it is not earmarked. The equalization share is allocated

to all SNGs with below-average tax capacities. The regional share is calculated for each region

based on several criteria (demography, unemployment, GDP per capital, roads, etc.). Earmarked

transfers include specific transfers for central government delegated tasks (e.g. social spending),

capital expenditure, etc.

• In Spain, Basque Country and Navarra do not receive transfers from the central government but,

on the contrary, they transfer funds to central government to participate to national general

expenses. Other ACs (in the common regime) receive general unconditional equalization grants

and conditional grants. There are two main funds: (i) the Guarantee of Basic Public Services Fund,

non-earmarked, which is intended to ensure equal funding for basic public services (health care,

education and social services), and (ii) the Global Sufficiency Fund, which is based on the

assessment of the fiscal gap between expenditure needs and fiscal capacity. In addition, regions

receive conditional grants aimed at fostering regional development, such as the compensation fund.

• In Colombia, the General System of Transfers (Sistema General de Participaciones, SGP) is the

most important central government transfer. SGP funds are earmarked for the most part, and their

distribution between key sectors (education, health and water supply and sewerage) is determined

by law according to a formula based on a combination of population coverage, social equity and

efficiency criteria.

• In Indonesia, transfers from the central government consist of three major components: the general

allocation fund, the revenue-sharing fund and the specific purpose fund. The general allocation

fund (Dana Alokasi Umum, DAU) is an equalization transfer system aiming at reducing fiscal

imbalances between sub-national governments. Transfers are formula-based, consisting of a base

allocation (equal to the amount of spending on personal) and a fiscal gap allocation (which can be

positive or negative). The shared revenue fund (Dana Bagi Hasil, DBH) is sub-divided in two

categories. The DBH from taxes is a shared tax system, based on receipts from the personal income

tax, etc. The DBH from natural resources is based on revenues derived from forestry, mining, oil,

etc. Last, the special allocation fund (Dana Alokasi Khusus, DAK) is a transfer system to fund

responsibilities that are considered as national priorities and are mostly earmarked capital transfers.

6

Subnational borrowing and fiscal rules

The case studies underscore the need for ensuring fiscal stability at the subnational level by putting

in place borrowing rules. In Colombia, the subnational entities suffered significant financial problems.

During the decade of the 1990s, many departments and large cities became excessively indebted and could

not meet their payment obligations. That prompted the national government to bail out those subnational

governments. To avoid the situation from re-occurring, a robust regulatory framework was issued imposing

borrowing restrictions on subnational governments, in order to encourage fiscal sustainability. In Indonesia,

subnational borrowing prior to the decentralization reforms used to be significant. The central government

sought to clean up the defaulting loans early in the reform period. Nowadays, regional governments can

borrow but are limited by regulations and capacity to design and manage large capital projects. The

subnational governments in Poland have a right to take loans or issue bonds to borrow in the financial

market without asking for central government prior permission, although, they are subject to regulations

and ex-post controls. If the sub-national entities have problems for servicing their debt, they need to approve

a recovery program. It often includes fiscal adjustment programs in exchange for a low-interest loan from

the central administration.

Subnational borrowing is often embedded in the subnational fiscal rules and supervised through

independent bodies or the central government:

• In Spain, the subnational debt has significantly increased after the 2008 global financial crisis. This

situation led to profound reforms regarding fiscal rules. A constitutional reform was adopted in

2011 to underpin the fiscal consolidation targets for all Spanish administrations from 2020 onward.

Moreover, an Organic Law on Budgetary Stability and Financial Sustainability passed in 2012

introduced a structural balanced budget rule and debt ceilings for all levels of governments, as well

as expenditure rules for SNGs. The regional Liquidity Fund (FLA) was also temporarily established

in 2012 to support heavily indebted regions with difficulties borrowing in open markets. Finally,

an independent authority for Fiscal Responsibility was set up to monitor and report on compliance

of all levels of government.

• In Poland, the 2011 Public Finance Act stipulated to balance local current budgets and strengthened

debt limitations requiring that the sum of loan instalments and interest payments must not exceed

15% of total debt. From 2014 onwards, the mode of calculation for debt ratios is changed in order

to reduce subnational debt.

• In Indonesia, sub-national debt must not exceed 75% of the previous year’s budget revenues. Sub-

national governments are not allowed to borrow internationally; those with outstanding arrears on

government loans are prohibited from borrowing. A cumulative lending limit for subnational loans

is set by the ministry of finance.

• In the case of Colombia, recourse to borrowing is regulated by strict prudential rules, established

in 1997 (“Traffic Light Law” or Ley de Semáforo); in addition, in 2000 and in 2003 the Law on

Fiscal Transparency and Responsibility curbed the growing subnational government indebtedness

observed during the 1990’s. In addition, since 2003, departments and large municipalities must

obtain satisfactory credit ratings from international rating agencies before they can borrow.

7

Challenges and lessons

The case studies show that the decentralization process is a continuous effort that has to be carefully

sequenced and managed. Challenges are multiple:

• The decentralization process is unlikely to succeed if it is only partial -political decentralization. If

these reforms are not accompanied by fiscal and administrative decentralization the overall

outcome can in fact have detrimental effects on the quality and effectiveness of governance in the

country.

• Accountability becomes complicated and diffused when there are overlapping competencies or

when these responsibilities are not well-defined, which also increases the likelihood of political

conflicts.

• Politically it is much easier to decentralize expenditure responsibilities than revenue sources.

However, insufficient revenue decentralization and financial autonomy is a significant threat to

accountability and the overall efficiency of the decentralized system.

• Local fiscal accountability and citizens’ participation on subnational governments’ affairs represent

a difficult challenge in the decentralization process of any country, but they are key to successful

decentralization.

Case studies also offer many lessons to other countries embarking on decentralization reforms:

• While decentralization processes are very country specific, they need to be informed by fiscal

federalism principles and the ample international experience on what has worked and what has not

work in other countries.

• Decentralization is not an effortless and simple process, on the contrary, it requires a significant

planning effort and political leadership in its execution.

• Supporting newly created subnational governments is a core responsibility of the central

government in the evolved decentralized intergovernmental architecture.

• Macroeconomic and fiscal stability are core objectives that the fiscal decentralization architecture

must support and respect. Subnational governments, even when they have autonomy in their fiscal

matters, must still be subject to the rules and regulations that are necessary to ensure economic

stability.

What can Chile learn from the case studies?

Articulate a vision. Decentralization reforms are too complicated to be planned and implemented on ad

hoc basis and only with a partial view. While they can be spread over years, it is important to have a clear

vision or roadmap in mind.

All stakeholders must get involved in the process. Chile is not in a rush, thereby, all kind of stakeholders

should get involved in the process to converge as much as possible on goals, concepts, terminology and key

options.

Good planning is essential. For expenditure responsibilities, it is important to identify and asses which is

the lowest organizational level of government at which functions can be done efficiently and successfully.

It will be necessary to find a balance between the subsidiarity principle and economies of scale. Then, a

timely and relevant capacity development plan must be prepared that recognizes critical and urgent

transition issues, but which also incorporates a longer-term perspective.

8

Create a dynamic and flexible system. The architecture and typology of functions scheme must provide

a dynamic and creative system. Chile should provide certainty to the subnational level in order to undertake

the new functions but must guarantee that there is room for changes and improvements, of course, under

the central government’s guidance and control, when needed.

Focus on establishing a comprehensive role for the intermediate level of government. Overriding

political considerations shapes the choice of intermediary roles and mechanisms. Chile may have the option

(with only one level in play) to create from the beginning an integral but at the same time transparent

intermediate level of government.

Design an efficient accountability mechanism. Lack of accountability mechanisms may generate a slow

progress on service improvement and innovation. Lack of accountability will also lead to the inefficient

and unresponsive provision of public services, and ultimate to the waste of public resources. Chile has the

chance to design good mechanisms (especially in terms of the use of the information) which are not

burdensome and involve all stakeholders more meaningfully.

Match revenues to needs. To ensure accountability, revenue should be matched as closely as possible to

expenditure needs that is: “finance follows function.” In addition, tax instruments intended to further

specific policy goals should be assigned to the tier of government which is in charge of providing that

service.

Manage increases on aggregate national expenditures. While in theory decentralization could be

considered neutral in terms of expenditures, in practice Chile should be prepared for an increase in overall

national public expenditures. This is specially the case if decentralization implies funding underprovided

key public services in lagging areas. Chile needs to find its own boundaries and priorities in implementing

a fiscal decentralization plan at the intermediate level of government.

1

Fiscal decentralization of regional

governments – the case of Colombia

prepared under the World Bank TA RAS for Chile1

1 The note for Colombia was written by Juan Gonzalo Zapata

2

Índice

Contexto y breve revisión histórica ........................................................................................................... 3

Descentralización en Colombia .................................................................................................................. 5

Competencias de departamentos y municipios ........................................................................................ 9

Transferencias Intergubernamentales Generales de la nación ............................................................. 19

Sistema General de Participaciones ........................................................................................................ 19

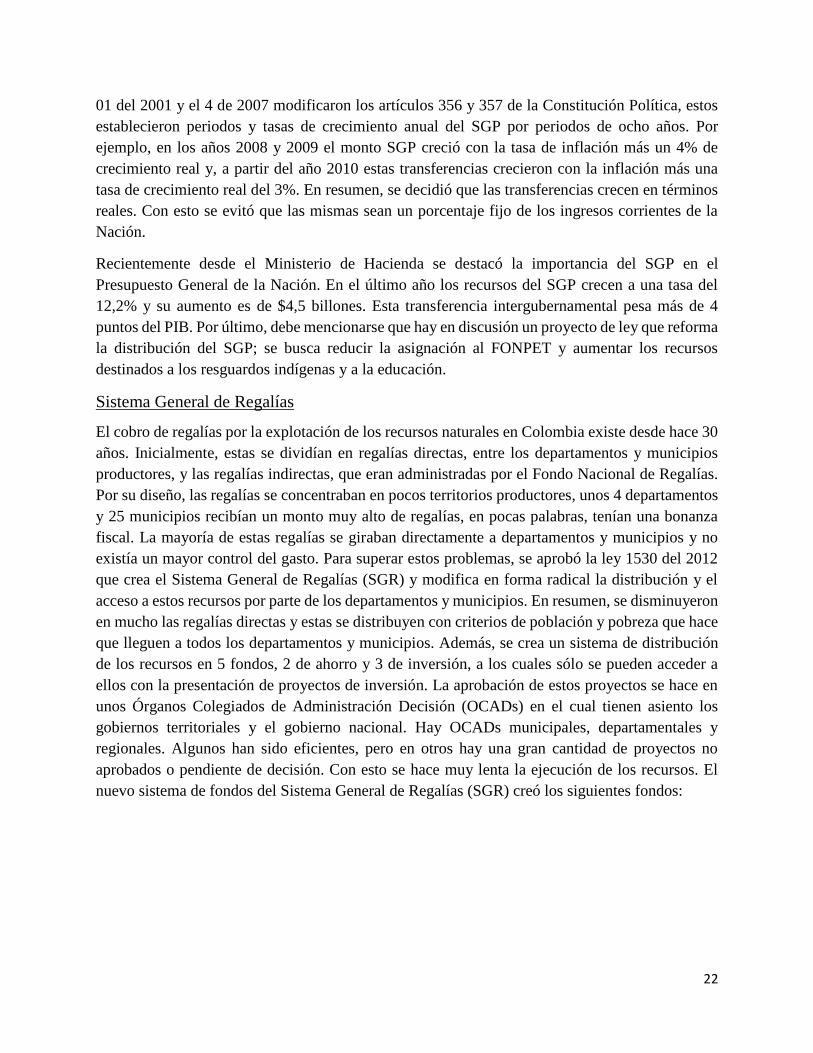

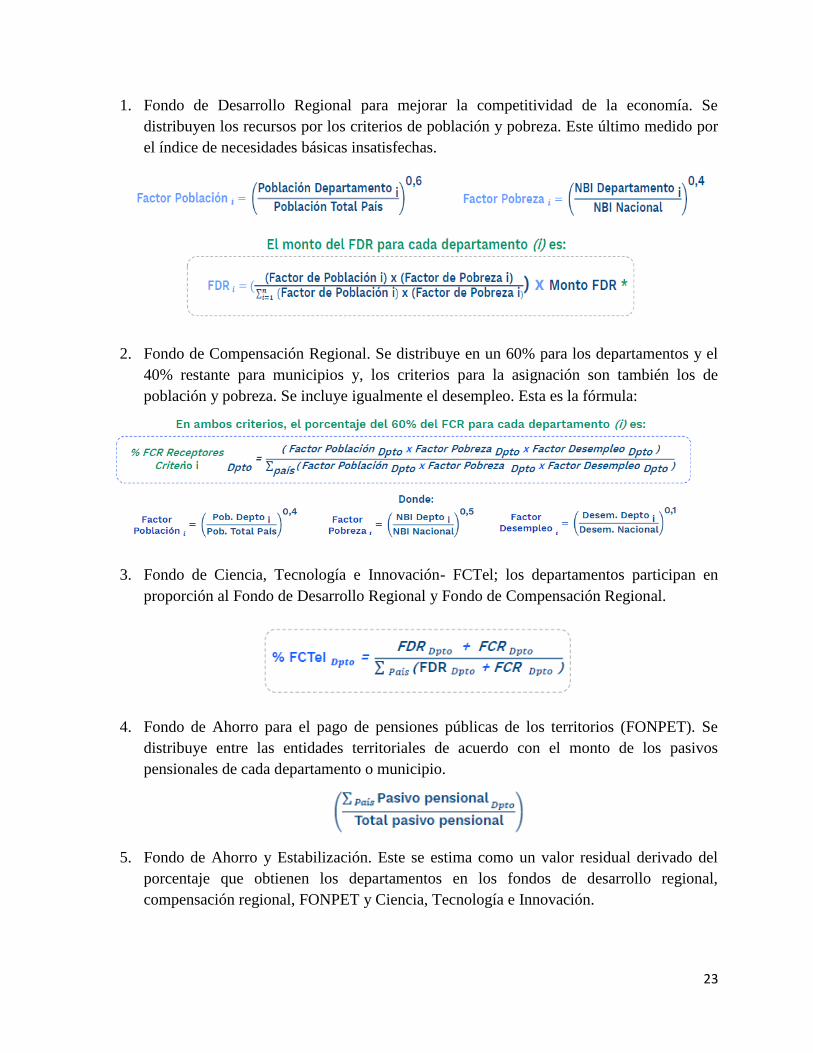

Sistema General de Regalías ................................................................................................................... 22

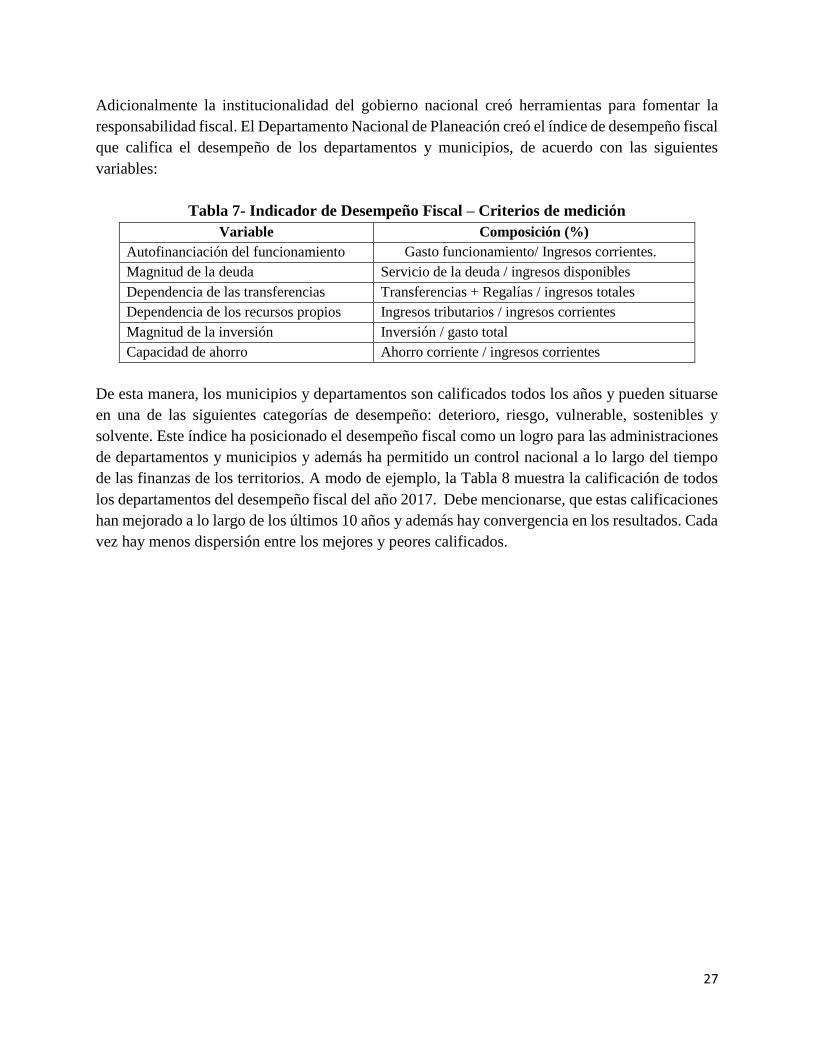

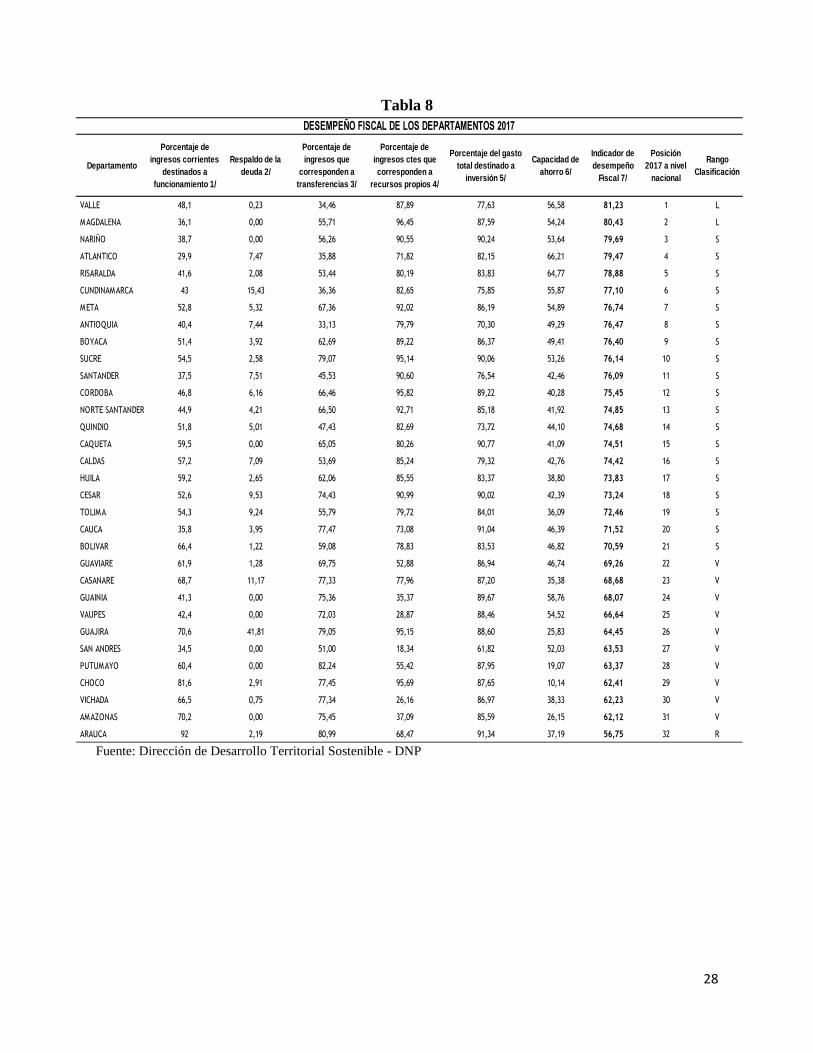

Deuda y sostenibilidad fiscal .................................................................................................................... 26

Balance de la Descentralización en Colombia: Ajustes sobre la marcha ............................................. 29

3

Contexto y breve revisión histórica

Desde mediados del siglo XIX los niveles intermedios de gobierno en Colombia han sido

importantes en términos fiscales y han tenido autotomía administrativa y política. Esto se explica

porque, si bien este país ha sido marcadamente centralista, tuvo un periodo largo en donde,

inspirado en ideas liberales, se abrió el camino para la expedición de tres constituciones de corte

federal. Las constituciones de 1853, 1858 y 1863, en un proceso lento pero persistente, crearon en

total 9 estados. Estos estados se crearon a partir de las anteriores provincias heredadas del largo

periodo colonial. En la década de los años 50 del siglo XIX las 42 provincias se agruparon y se les

dio autonomía plena en los ámbitos políticos, económicos y sociales.2

Ya para la década de los años sesenta, en el marco de la Constitución de Rionegro de 1863, que

funda los Estados Unidos de Colombia, los anteriores estados se convierten en estados soberanos

en donde cada uno tenía su asamblea legislativa, tenía su ejército, creaba sus propios impuestos y

priorizaba el gasto público que ejecutaba, entre muchas funciones más. Era un modelo federal muy

cercano a una confederación. La autonomía de estos estados era muy amplia; por ejemplo, algunos

de ellos deciden abolir la pena de muerte con una pena máxima de 10 años. Por esto, las relaciones

con el gobierno nacional eran complejas pues cada estado tenía un voto para la elección

presidencial y gran parte del poder se ejercía desde el Congreso, en donde los estados tenían una

alta representación. Además, cada estado nombraba su presidente, tenía asamblea legislativa y en

algunos de ellos nombraban sus mandatarios locales por voto calificado. Si bien no es del caso

mencionar las duras confrontaciones entre conservadores y liberales, es necesario recordar que la

agenda pública estaba signada por el papel de la religión, por la reforma educativa, por la

distribución de algunos impuestos nacionales con los mencionados estados; por ejemplo, la renta

de la producción y comercialización de las salinas, y por la difícil puesta en marcha de proyectos

nacionales. El mejor ejemplo de esto último fueron los intentos de construir ferrocarriles y otros

numerosos esfuerzos adelantados tanto por los estados soberanos como por el gobierno nacional.

De otro lado, la independencia de España no cambió la estructura tributaria existente. La mayoría

de los impuestos al consumo se mantuvieron e inclusive buena parte de los monopolios coloniales

aún estaban en la lista de los gravámenes departamentales vigentes. Esto es bien importante, puesto

que el monopolio del aguardiente, los ingresos por juegos de suerte y azar y del degüello mayor y

menor, entre otros, han sido importantes para las finanzas departamentales desde que estos fueron

creados. A pesar de todos los cambios políticos producto de las guerras civiles y nuevas

constituciones, estos impuestos se han mantenido en el tiempo. Es más, a finales de siglo XIX

cuando los estados soberanos se degradan y se convierten en departamentos, varios de sus tributos

mencionados los incorpora el gobierno nacional y su peso dentro del total de ingresos fue

importante.

2 Zapata, G. J.G. Reforma radical en el Estado de Santander, 1850-1885. Bogotá: Universidad del Rosario, 2015.

4

Aunque es conocido que este periodo federal termina con la expedición de la constitución de 1886,

que era muy centralista, buena parte del desarrollo institucional que se adelantó durante el periodo

federal se mantuvo en los años siguientes. Los estados soberanos pasaron a ser departamentos, los

gobernadores eran designados por el gobierno nacional, y estos a su vez nombraban a los alcaldes.

Si bien la autonomía política del modelo federal murió, se mantuvo la misma estructura de las

secretarías (ministerios) sectoriales (salud, educación, vías, etc.). Por supuesto, los ejércitos de los

estados se acabaron y las asambleas no tenían funciones legislativas mayores, ya que no expedían

leyes sino ordenanzas con un alcance mucho más limitado.

Es el momento de mencionar que el primer esfuerzo de descentralización en Colombia fue a

mediados del siglo XIX. Se dio durante el gobierno de José Hilario López, cuando en 1850 su

secretario Manuel Murillo Toro descentralizó en favor de las provincias varios de los impuestos

nacionales. Esto con el fin de agilizar su cobro y darles más autonomía y poder a los mandatarios

territoriales. Desde lo fiscal, se buscaba además que el gobierno nacional se concentrara en el

cobro de pocos impuestos y, que las provincias pusieran en marcha el cobro del impuesto directo.

Por explicarlo en forma resumida, este impuesto era una combinación de impuesto de renta y de

impuesto a la propiedad de acuerdo con parámetros actuales. Por ejemplo, en el estado de

Santander, la autoridad entregaba una declaración de bienes a la persona llamada riqueza gravada,

y a partir de esta declaración se le aplicaba una tarifa cercana al 1% anual. Era un sistema de cobro

elaborado pues la persona podía solicitar una revisión de la declaración de su riqueza gravada y

existía una autoridad encargada de dicha revisión. Además, las alcaldías, llamadas en Santander

distritos, decidían la tarifa a aplicar sobre la riqueza gravada, ver Zapata (2016).3 En este impuesto

muchos de los líderes del partido liberal que apoyaban el modelo federal, centraron muchas de las

esperanzas de autonomía fiscal de los gobiernos federales.

Más adelante, durante el gobierno del general Rafael Reyes a comienzos del siglo XX, varios

departamentos se escindieron, con lo cual se crearon nuevos departamentos. Se llegó así, a un total

de 15 y casi al mismo tiempo se crearon las intendencias y comisarias para los territorios nacionales

poco poblados y alejados del centro. Estos fueron administrados desde el nivel central por una

entidad pública y un departamento administrativo nacional. Ya durante el siglo XX los

departamentos encontraron en el monopolio de los licores y en sus loterías sus principales fuentes

de recursos. Luego, la explotación del chance y el impuesto a los vehículos automotores, entre

otros tributos tomaron relevancia. Se ha criticado que estos impuestos al ocio son regresivos, que

tienen cuño colonial y que sus bases gravables son poco dinámicas. Este tema, sin embargo, por

lo pronto lo dejaremos de lado.

De lo anterior queda en claro que, desde el siglo XIX, los departamentos son importantes en la

vida fiscal y financiera del sector público colombiano. También que estos siempre han tenido

fuentes propias de recursos y han tenido claridad en las funciones que les competían. A pesar de

lo anterior, a lo largo del siglo XX los departamentos pierden relevancia al interior de la vida

3 Zapata, J. G. (2015). Caps. 2 y 3. Ibid.

5

pública por varias razones. Primero, sus fuentes de recursos propias perdieron fuerza; segundo, los

impuestos nacionales crecieron notablemente y desplazaron en términos relativos a los impuestos

territoriales. Tercero, la descentralización, que comenzó en la década de los años noventa del siglo

XX, inicialmente se concentró en los municipios y el marco legal que se desarrolló favoreció su

financiamiento, tanto sus recursos propios como transferidos.

Descentralización en Colombia

En los años ochenta del siglo XX, una serie larga de paros cívicos eran la expresión de las regiones.

La mayoría de estos paros no tenían reivindicaciones políticas y eran más sociales, en especial por

la falta de servicios públicos. Acueductos, interconexión eléctrica y vías eran los principales temas

(Maldonado: 2012).4 En este sentido la descentralización fue en gran parte, la respuesta política a

las demandas que comenzaron en las regiones. Las demandas venían desde abajo pues se

identificaban como malos o inoperantes a los alcaldes elegidos directamente por los gobernadores.

El descredito de la vida política local era muy alto. Sin embargo, con la posterior elección popular

de alcaldes los paros cívicos disminuyeron rápidamente.

De otra parte, el proceso de descentralización tuvo antecedentes técnicos importantes en los años

80, antes de los cambios normativos centrales. El informe Bird- Wiesner, una misión de expertos

nacionales e internacionales presentó sus resultados en 1979, demostró que el 84.6% de los

ingresos del Estado estaban concentrados en el nivel central, mientras que solo 9.7% en los

departamentos, intendencias y comisarias.5 Con este muy bajo nivel de gasto territorial era muy

difícil responder a las demandas locales. Una de las recomendaciones del informe fue de fortalecer

las fuentes de recursos territoriales. Es así como se expiden varias leyes que fortalecen los fiscos

municipales; la Ley 14 de 1983 mejoró el recaudo de impuestos como el de timbre nacional,

licores, cigarrillos. Esta ley lo que hizo fue aumentar las tasas y las bases gravables. Mas adelante

en 1995, se crea la sobretasa a la gasolina y los municipios eran los encargados de decidir su tarifa;

sin embargo, la legislación posterior volvió obligatorio el cobro del 20% en todos los municipios.

También en 1998 con la expedición de la ley 488 se creó el impuesto a los vehículos automotores

que reemplazó al de Circulación y Transito, el de timbre sobre vehículos automotores y el impuesto

unificado de vehículos que había creado Bogotá. Con esto se aumentó la base gravable y es el

ministerio del transporte el que decide el precio de los vehículos nuevos y usados (base gravable)

para su cobro. Su recaudo se destina mayoritariamente a los departamentos. A su vez, más

adelante, con la creación del Impuesto al Valor Agregado (IVA), que reemplazó al anterior

impuesto a las ventas, aumentó al mismo tiempo la transferencia en favor de los municipios.

Debe mencionarse que un artículo transitorio de la Constitución Nacional obliga la expedición de

un nuevo estatuto tributario territorial; sin embargo, después de 28 años este estatuto aún no se ha

4 Maldonado, A. Los límites de la descentralización territorial: el caso de Colombia 1991- 2008. Tesis de Doctorado. Universidad

Complutense. Madrid. 2011. 5 DNP (1981). Las finanzas intergubernamentales en Colombia: informe de la Misión Wiesner-Bird de finanzas

intergubernamentales. Bogotá.

6

expedido. El gobierno nacional ha utilizado las reformas tributarias nacionales para mejorar, poco

a poco, el recaudo de los ingresos corrientes o propios de departamentos y municipios al incluir

siempre algunos artículos al respecto. Por ejemplo, la ley 1943 incluyó un aumento importante en

la tarifa del impuesto a los cigarrillos. Esta tarifa se triplica en un periodo de sólo 3 años. Una de

las últimas reformas tributarias nacionales, la mencionada ley 1943 de 2018, creo la Comisión de

Estudio del Sistema Tributario Territorial. Esta comisión se reúne desde el mes de junio y se espera

que sus recomendaciones estén para mediados del 2020. Estas recomendaciones, no obligan su

adopción o la presentación de un proyecto de ley, pero es la primera vez que una comisión de este

tipo se concentra en analizar los ingresos territoriales.

Un paso importante para la descentralización política se dio con el Acto Legislativo 1 de 1986 que

estableció la elección de alcaldes, anteriormente eran funcionarios de libre nombramiento y

remoción por parte de los gobernadores. Esta decisión contribuyó a ampliar la democracia

representativa en el país. Para este mismo año hubo un cambio importante en la distribución de

funciones de las entidades territoriales, especialmente de los municipios. La Ley 12 de 1986, al

mismo tiempo que aumentó la participación de los municipios del recién creado impuesto al valor

agregado (IVA), se les asignó más competencias en la administración de servicios en el sector

salud, educación, desarrollo agropecuario, desarrollo urbano y saneamiento básico. Este salto no

fue exento de críticas pues no se crearon planes o mecanismos claros de implementación que

ayudaran a los territorios a asumir estas funciones. Adicionalmente, se criticó que no se

diferenciaran las funciones de acuerdo con criterios como el número de habitantes, nivel de

ruralidad o generación de recursos propios, entre muchos más. La mayoría de las funciones

descentralizadas pasaron del nivel nacional al municipal, en especial en el sector salud. En esta

coyuntura no se entregaron funciones a los departamentos.

El proceso de descentralización se volvió más integral con la expedición de la Constitución

Nacional de 1991. Esta constitución permitió que los departamentos lograran desarrollarse como

entidades autónomas en lo político, lo administrativo y lo fiscal en forma paralela a como se hizo

con los municipios. Se decidió que las autoridades departamentales se eligieran por voto popular.

Hay que tener presente que durante los debates de la Asamblea Constituyente se expresaron dos

líneas sobre la elección popular de gobernadores. Los que querían que la descentralización fuera

únicamente municipal y los que querían un tercer nivel de gobierno fuerte. Los principales reparos

para extender la descentralización a los departamentos eran fiscales; se entendía que no se disponía

de los recursos necesarios para financiar tres niveles de gobierno. Sin embargo, las realidades

políticas, los departamentos siempre han tenido presencia en la vida nacional, permitieron que esta

decisión no tuviera fuerte oposición en la Asamblea Constituyente. Como veremos, esta decisión

explica el gran aumento de las transferencias intergubernamentales en favor de departamentos y

municipios.

La elección de gobernadores por voto popular se entendió como un complemento de la elección

municipal. Además, las anteriores intendencias y comisarías se volvieron departamentos con

iguales funciones y responsabilidades. Se llegó así a un total de 32 departamentos, con lo cual en

7

Colombia se formalizó un proceso de descentralización con tres niveles de gobierno fuertes. Falleti

argumenta que en Colombia se dio muy fácil la descentralización política pero que la cesión de

funciones y recursos fue mucho más lenta.6 Esto generó problemas en las relaciones entre el

gobierno nacional y los mandatarios de los territorios.7 El proceso de descentralización fue

complejo pues el gobierno nacional cerró varias entidades descentralizadas nacionales para

seguidamente ceder las funciones a los territorios. En especial se debe mencionar al sector agua

potable y saneamiento en donde una entidad era la encargada de construir los acueductos. Esta

entidad, el Instituto de Fomento Municipal (INSFOPAL) tenía muy malos resultados. Hay ejemplo

en el sector agrícola y en la construcción de vías, etc. El proceso de cesión de funciones y recursos

tuvo con la Constitución Nacional de 1991 un salto cualitativo pues la descentralización fue uno

de los temas ganadores con la nueva carta fundamental.

Este cambio constitucional hizo que el aumento de las transferencias intergubernamentales, junto

con el de las regalías por la explotación de recursos naturales no renovables, tuvieran en cuenta a

los dos niveles de gobierno territoriales. La distribución de estos recursos favoreció a los gobiernos

subnacionales. De esta manera se reconoció el gasto social como prioritario, así como la

destinación condicionada de los recursos de inversión en sectores como salud, educación y

saneamiento básico. En pocas palabras los territorios y la descentralización fueron los ganadores

con el nuevo marco normativo producto de la CN de 1991. Se desarrolló igualmente una nueva

institucionalidad por parte del gobierno nacional encargada de administrar los recursos

transferidos, de hacer seguimiento de la planeación en los territorios e intervenir mediante

convenios de desempeño en las entidades territoriales con problemas financieros críticos, ley 358

junto con la ley 550 de 1999, que es una ley de quiebras que tiene su capítulo para el sector público.

Esta ley permite reestructurar sus pasivos. Cuando un gobierno territorial, departamento o

municipio, tiene problemas financieros puede acogerse a cualquiera de estas dos leyes. Para esto

debe firmar un convenio de desempeño o un acuerdo de reestructuración con la Dirección de

Apoyo Fiscal (DAF) del Ministerio de Hacienda. Estos convenios y acuerdos son ortodoxos,

puesto que obligan a que el gobierno subnacional mejore sus ingresos, controle sus gastos de

funcionamiento o generales, limite la inversión en infraestructura y, cierre o reorganice sus

empresas de servicios públicos o cualquier entidad de su jurisdicción. Las metas son anuales y se

hace un seguimiento de ellas permanente. A su vez la firma y el cumplimiento de los convenios

de desempeño les permite acceder a recursos frescos de los bancos para refinanciarse. Sin la firma

de los convenios de desempeño no es posible acceder al crédito, ver Caja 1.

Caja 1 - Reestructuración de Pasivos y Convenios de Desempeño de los Territorios

Los departamentos y municipios se encuentran en programas de Saneamiento Fiscal y Financiero,

siempre y cuando tengan suscritos convenios o planes de desempeño en el marco de la ley 358 de

6 Falletti, T. A sequential theory of decentralization and its effects on the intergovernmental balance of power: latin american cases

in comparative perspective. Working Paper # 314. Kellog Institute. July 2004. 7 En este trabajo cuando se utiliza la palabra territorios se debe entender que son al tiempo los departamentos y municipios. Así los

mandatarios territoriales son los alcaldes y gobernadores.

8

1997 o suscriban acuerdos de reestructuración de pasivos, ley 550 de 1999. Estos programas de

saneamiento deben contar con el concepto favorable del Ministerio de Hacienda y Crédito, ley 617

de 2000, y es la dirección de Apoyo Fiscal (DAF) del Ministerio de Hacienda la encargada de

cumplir con la reestructuración o con los convenios. Veamos un resumen de estas dos figuras de

ajuste financiero para auxiliar a los territorios con problemas financieros.

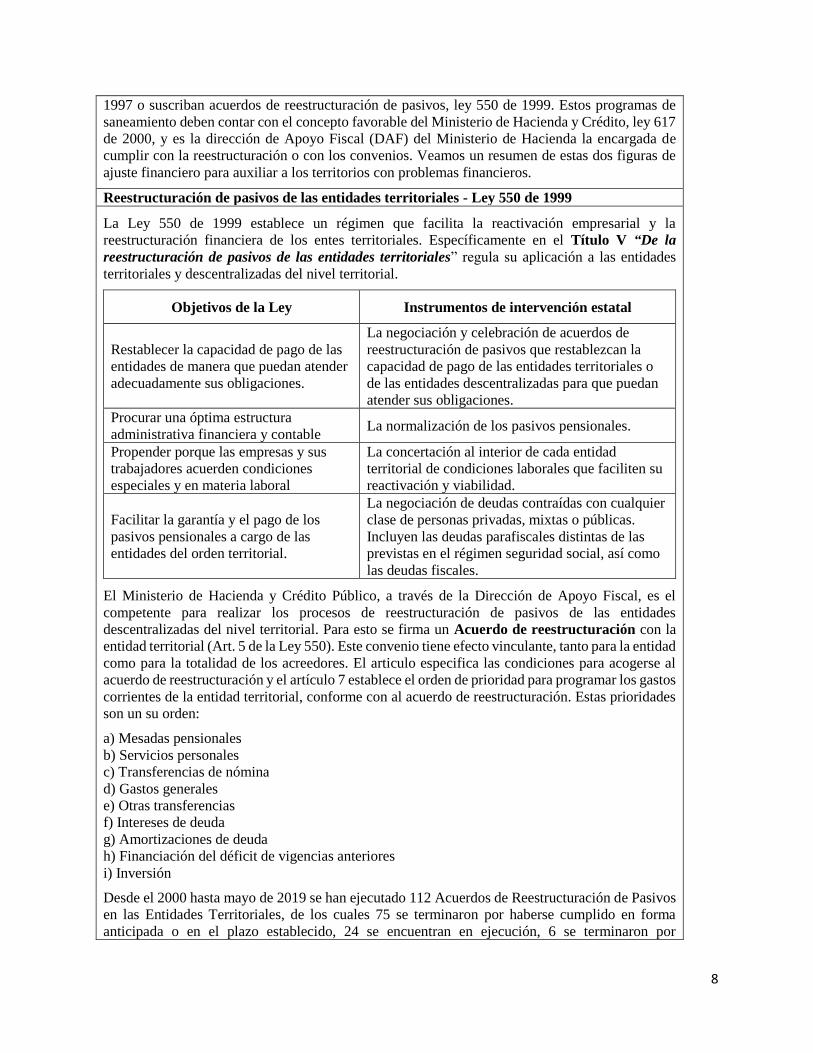

Reestructuración de pasivos de las entidades territoriales - Ley 550 de 1999

La Ley 550 de 1999 establece un régimen que facilita la reactivación empresarial y la

reestructuración financiera de los entes territoriales. Específicamente en el Título V “De la

reestructuración de pasivos de las entidades territoriales” regula su aplicación a las entidades

territoriales y descentralizadas del nivel territorial.

Objetivos de la Ley Instrumentos de intervención estatal

Restablecer la capacidad de pago de las

entidades de manera que puedan atender

adecuadamente sus obligaciones.

La negociación y celebración de acuerdos de

reestructuración de pasivos que restablezcan la

capacidad de pago de las entidades territoriales o

de las entidades descentralizadas para que puedan

atender sus obligaciones.

Procurar una óptima estructura

administrativa financiera y contable La normalización de los pasivos pensionales.

Propender porque las empresas y sus

trabajadores acuerden condiciones

especiales y en materia laboral

La concertación al interior de cada entidad

territorial de condiciones laborales que faciliten su

reactivación y viabilidad.

Facilitar la garantía y el pago de los

pasivos pensionales a cargo de las

entidades del orden territorial.

La negociación de deudas contraídas con cualquier

clase de personas privadas, mixtas o públicas.

Incluyen las deudas parafiscales distintas de las

previstas en el régimen seguridad social, así como

las deudas fiscales.

El Ministerio de Hacienda y Crédito Público, a través de la Dirección de Apoyo Fiscal, es el

competente para realizar los procesos de reestructuración de pasivos de las entidades

descentralizadas del nivel territorial. Para esto se firma un Acuerdo de reestructuración con la

entidad territorial (Art. 5 de la Ley 550). Este convenio tiene efecto vinculante, tanto para la entidad

como para la totalidad de los acreedores. El articulo especifica las condiciones para acogerse al

acuerdo de reestructuración y el artículo 7 establece el orden de prioridad para programar los gastos

corrientes de la entidad territorial, conforme con al acuerdo de reestructuración. Estas prioridades

son un su orden:

a) Mesadas pensionales

b) Servicios personales

c) Transferencias de nómina

d) Gastos generales

e) Otras transferencias

f) Intereses de deuda

g) Amortizaciones de deuda

h) Financiación del déficit de vigencias anteriores

i) Inversión

Desde el 2000 hasta mayo de 2019 se han ejecutado 112 Acuerdos de Reestructuración de Pasivos

en las Entidades Territoriales, de los cuales 75 se terminaron por haberse cumplido en forma

anticipada o en el plazo establecido, 24 se encuentran en ejecución, 6 se terminaron por

9

incumplimiento, 2 se encuentran en negociación y 5 no se suscribieron porque no se obtuvo la

votación requerida, fracaso la negociación o por no tener facultades del concejo municipal.

Convenios de Desempeño

Estos planes o convenios de desempeño son programas de ajuste fiscal, financiero y administrativo

que buscan restablecer la solidez económica y financiera de la entidad territorial. Buscan garantizar

la capacidad de pago de largo plazo y el mejoramiento de los indicadores de endeudamiento de las

entidades territoriales (artículo 7 – ley 358). Estos planes de desempeño incluyen medidas de

racionalización del gasto y el fortalecimiento de los ingresos propios. También obligan a tomar

decisiones como el cierre o la mejora de la gestión de las entidades descentralizadas del

departamento o municipio.

Los planes son ortodoxos, pue se hace un seguimiento periódico de las metas acordadas. Por esto

las entidades territoriales deberán enviar trimestralmente la información de la evolución de los

planes de desempeño a la DAF. Esta dirección evalúa el cumplimiento de dichos planes. Las

entidades que incumplan esta medida quedarán sujetas a las sanciones pertinentes. Estos planes

son de largo plazo y los mismos se mantienen vigentes hasta que la entidad territorial registre un

nivel de intereses/ahorro operacional menor o igual al 40%.

Sin el cumplimiento de los planes de desempeño, los departamentos y municipios no pueden

acceder a los recursos del crédito.

A continuación, se presentará el desarrollo que ha tenido este proceso en la definición de las

competencias asignadas a los departamentos y municipios; el comportamiento de las finanzas

públicas en los últimos 20 años; el funcionamiento de los sistemas de transferencias y, el

desempeño fiscal y al endeudamiento de las entidades territoriales. Como veremos, la legislación

que se expidió abarcó a los dos gobiernos subnacionales.

Competencias de departamentos y municipios

De acuerdo con lo señalado con anterioridad, la asignación de competencias a los departamentos

y municipios tuvo cambios importantes durante la década de los años 80. En general, la mayoría

de las funciones son compartidas entre los tres niveles de gobierno, en especial en los sectores de

salud y educación en donde se movilizan los mayores recursos y las nóminas públicas son muy

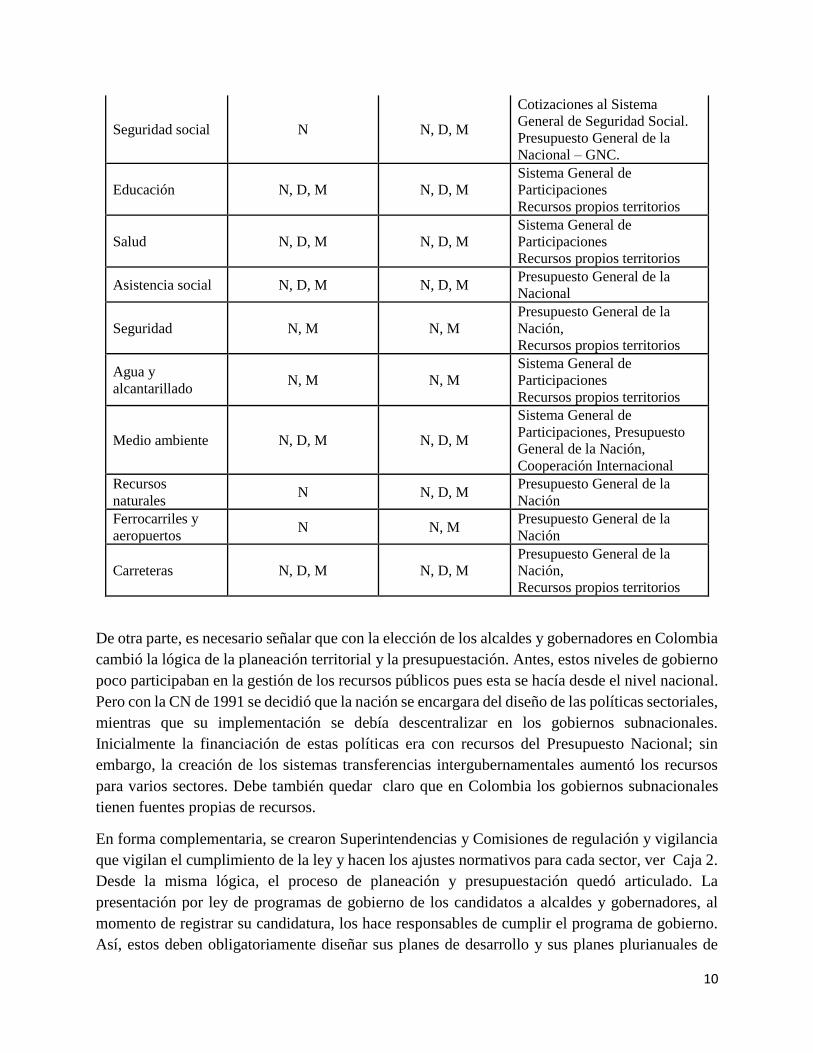

grandes; por ejemplo, en Colombia hay más de 300 mil maestros públicos. La tabla 1 nos muestra

la competencia de los gobiernos por sectores del gasto. La lógica que hay al compartir

responsabilidades es que el gobierno nacional es el encargado de diseñar las políticas sectoriales

y los gobiernos subnacionales los encargados de ejecutarlas. Sin embargo, dado que en Colombia

se demoró 20 años la expedición de la Ley Orgánica de Ordenamiento Territorial (LOOT),

estipulada en la CN de 1991, lo que se dio fue un proceso en donde las leyes sectoriales, al tiempo

que distribuían las funciones y recursos, creaban su propio ordenamiento territorial sectorial.

Tabla 1 – Funciones y responsabilidades por sectores del Gasto

Función Responsabilidad de

política y control

Responsabilidad

de provisión

Financiación

10

Seguridad social N N, D, M

Cotizaciones al Sistema

General de Seguridad Social.

Presupuesto General de la

Nacional – GNC.

Educación N, D, M N, D, M

Sistema General de

Participaciones

Recursos propios territorios

Salud N, D, M N, D, M

Sistema General de

Participaciones

Recursos propios territorios

Asistencia social N, D, M N, D, M Presupuesto General de la

Nacional

Seguridad N, M N, M

Presupuesto General de la

Nación,

Recursos propios territorios

Agua y

alcantarillado N, M N, M

Sistema General de

Participaciones

Recursos propios territorios

Medio ambiente N, D, M N, D, M

Sistema General de

Participaciones, Presupuesto

General de la Nación,

Cooperación Internacional

Recursos

naturales N N, D, M

Presupuesto General de la

Nación

Ferrocarriles y

aeropuertos N N, M

Presupuesto General de la

Nación

Carreteras N, D, M N, D, M

Presupuesto General de la

Nación,

Recursos propios territorios

De otra parte, es necesario señalar que con la elección de los alcaldes y gobernadores en Colombia

cambió la lógica de la planeación territorial y la presupuestación. Antes, estos niveles de gobierno

poco participaban en la gestión de los recursos públicos pues esta se hacía desde el nivel nacional.

Pero con la CN de 1991 se decidió que la nación se encargara del diseño de las políticas sectoriales,

mientras que su implementación se debía descentralizar en los gobiernos subnacionales.

Inicialmente la financiación de estas políticas era con recursos del Presupuesto Nacional; sin

embargo, la creación de los sistemas transferencias intergubernamentales aumentó los recursos

para varios sectores. Debe también quedar claro que en Colombia los gobiernos subnacionales

tienen fuentes propias de recursos.

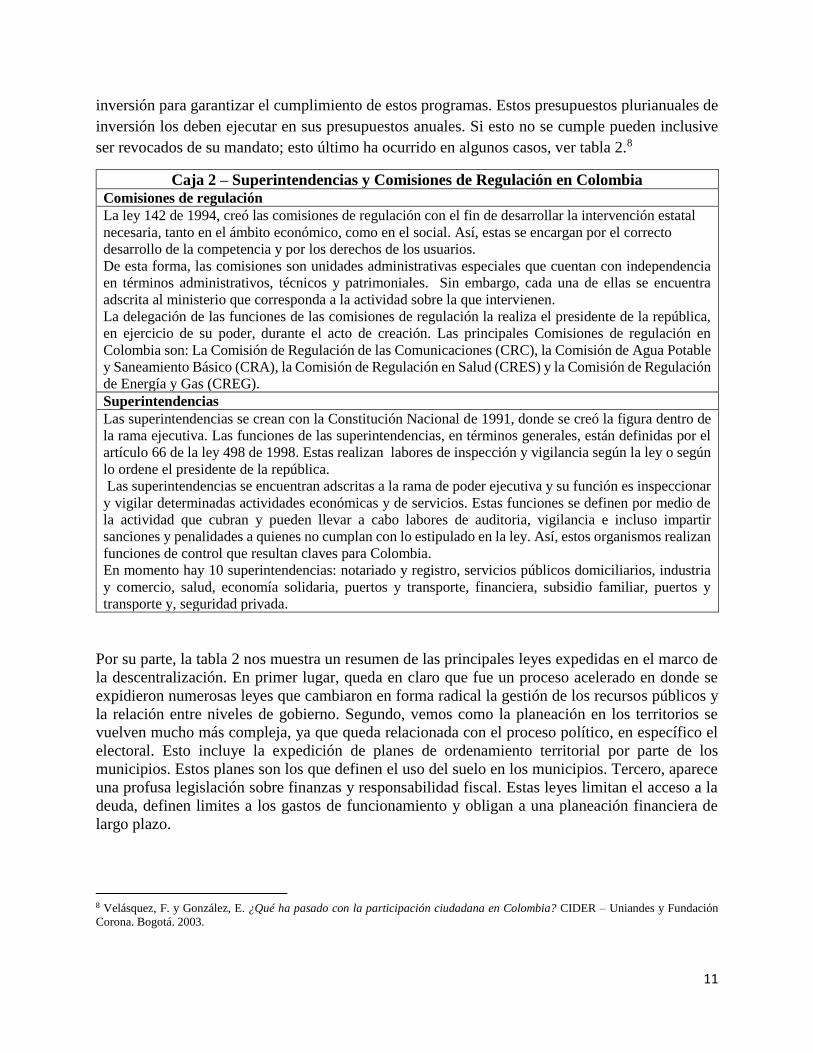

En forma complementaria, se crearon Superintendencias y Comisiones de regulación y vigilancia

que vigilan el cumplimiento de la ley y hacen los ajustes normativos para cada sector, ver Caja 2.

Desde la misma lógica, el proceso de planeación y presupuestación quedó articulado. La

presentación por ley de programas de gobierno de los candidatos a alcaldes y gobernadores, al

momento de registrar su candidatura, los hace responsables de cumplir el programa de gobierno.

Así, estos deben obligatoriamente diseñar sus planes de desarrollo y sus planes plurianuales de

11

inversión para garantizar el cumplimiento de estos programas. Estos presupuestos plurianuales de

inversión los deben ejecutar en sus presupuestos anuales. Si esto no se cumple pueden inclusive

ser revocados de su mandato; esto último ha ocurrido en algunos casos, ver tabla 2.8

Caja 2 – Superintendencias y Comisiones de Regulación en Colombia Comisiones de regulación

La ley 142 de 1994, creó las comisiones de regulación con el fin de desarrollar la intervención estatal

necesaria, tanto en el ámbito económico, como en el social. Así, estas se encargan por el correcto

desarrollo de la competencia y por los derechos de los usuarios.

De esta forma, las comisiones son unidades administrativas especiales que cuentan con independencia

en términos administrativos, técnicos y patrimoniales. Sin embargo, cada una de ellas se encuentra

adscrita al ministerio que corresponda a la actividad sobre la que intervienen.

La delegación de las funciones de las comisiones de regulación la realiza el presidente de la república,

en ejercicio de su poder, durante el acto de creación. Las principales Comisiones de regulación en

Colombia son: La Comisión de Regulación de las Comunicaciones (CRC), la Comisión de Agua Potable

y Saneamiento Básico (CRA), la Comisión de Regulación en Salud (CRES) y la Comisión de Regulación

de Energía y Gas (CREG).

Superintendencias

Las superintendencias se crean con la Constitución Nacional de 1991, donde se creó la figura dentro de

la rama ejecutiva. Las funciones de las superintendencias, en términos generales, están definidas por el

artículo 66 de la ley 498 de 1998. Estas realizan labores de inspección y vigilancia según la ley o según

lo ordene el presidente de la república.

Las superintendencias se encuentran adscritas a la rama de poder ejecutiva y su función es inspeccionar

y vigilar determinadas actividades económicas y de servicios. Estas funciones se definen por medio de

la actividad que cubran y pueden llevar a cabo labores de auditoria, vigilancia e incluso impartir

sanciones y penalidades a quienes no cumplan con lo estipulado en la ley. Así, estos organismos realizan

funciones de control que resultan claves para Colombia.

En momento hay 10 superintendencias: notariado y registro, servicios públicos domiciliarios, industria

y comercio, salud, economía solidaria, puertos y transporte, financiera, subsidio familiar, puertos y

transporte y, seguridad privada.

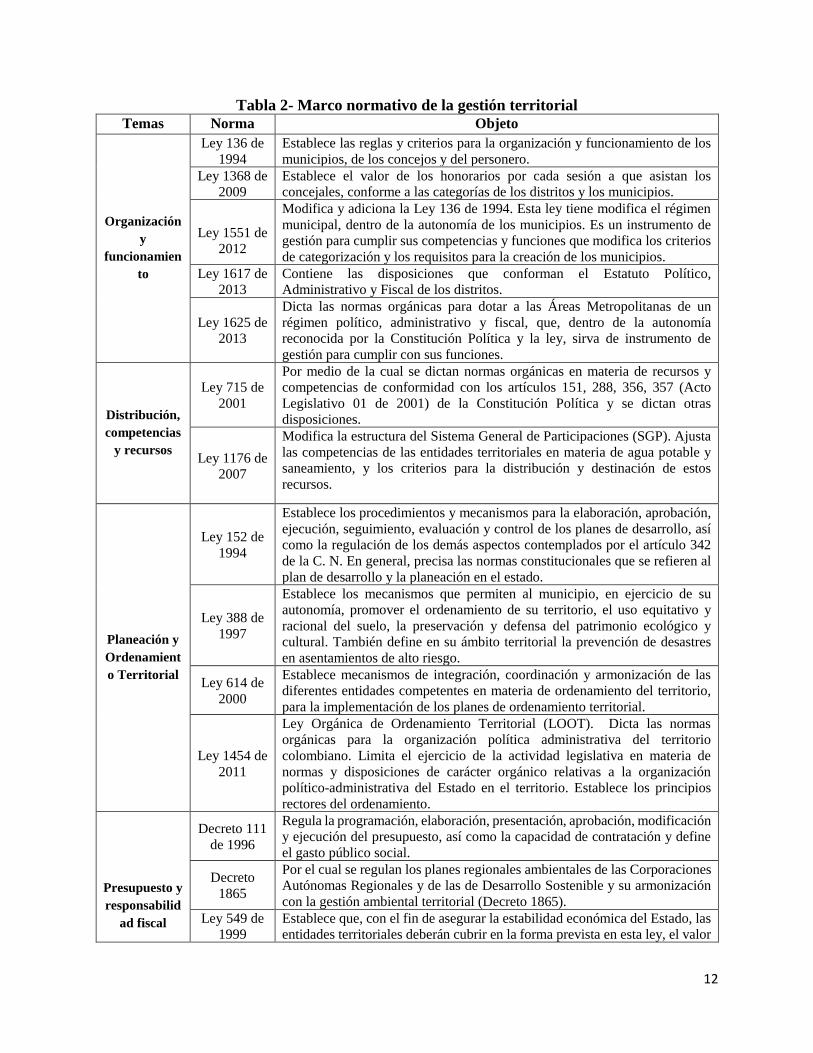

Por su parte, la tabla 2 nos muestra un resumen de las principales leyes expedidas en el marco de

la descentralización. En primer lugar, queda en claro que fue un proceso acelerado en donde se

expidieron numerosas leyes que cambiaron en forma radical la gestión de los recursos públicos y

la relación entre niveles de gobierno. Segundo, vemos como la planeación en los territorios se

vuelven mucho más compleja, ya que queda relacionada con el proceso político, en específico el

electoral. Esto incluye la expedición de planes de ordenamiento territorial por parte de los

municipios. Estos planes son los que definen el uso del suelo en los municipios. Tercero, aparece

una profusa legislación sobre finanzas y responsabilidad fiscal. Estas leyes limitan el acceso a la

deuda, definen limites a los gastos de funcionamiento y obligan a una planeación financiera de

largo plazo.

8 Velásquez, F. y González, E. ¿Qué ha pasado con la participación ciudadana en Colombia? CIDER – Uniandes y Fundación

Corona. Bogotá. 2003.

12

Tabla 2- Marco normativo de la gestión territorial

Temas Norma Objeto

Organización

y

funcionamien

to

Ley 136 de

1994

Establece las reglas y criterios para la organización y funcionamiento de los

municipios, de los concejos y del personero.

Ley 1368 de

2009

Establece el valor de los honorarios por cada sesión a que asistan los

concejales, conforme a las categorías de los distritos y los municipios.

Ley 1551 de

2012

Modifica y adiciona la Ley 136 de 1994. Esta ley tiene modifica el régimen

municipal, dentro de la autonomía de los municipios. Es un instrumento de

gestión para cumplir sus competencias y funciones que modifica los criterios

de categorización y los requisitos para la creación de los municipios.

Ley 1617 de

2013

Contiene las disposiciones que conforman el Estatuto Político,

Administrativo y Fiscal de los distritos.

Ley 1625 de

2013

Dicta las normas orgánicas para dotar a las Áreas Metropolitanas de un

régimen político, administrativo y fiscal, que, dentro de la autonomía

reconocida por la Constitución Política y la ley, sirva de instrumento de

gestión para cumplir con sus funciones.

Distribución,

competencias

y recursos

Ley 715 de

2001

Por medio de la cual se dictan normas orgánicas en materia de recursos y

competencias de conformidad con los artículos 151, 288, 356, 357 (Acto

Legislativo 01 de 2001) de la Constitución Política y se dictan otras

disposiciones.

Ley 1176 de

2007

Modifica la estructura del Sistema General de Participaciones (SGP). Ajusta

las competencias de las entidades territoriales en materia de agua potable y

saneamiento, y los criterios para la distribución y destinación de estos

recursos.

Planeación y

Ordenamient

o Territorial

Ley 152 de

1994

Establece los procedimientos y mecanismos para la elaboración, aprobación,

ejecución, seguimiento, evaluación y control de los planes de desarrollo, así

como la regulación de los demás aspectos contemplados por el artículo 342

de la C. N. En general, precisa las normas constitucionales que se refieren al

plan de desarrollo y la planeación en el estado.

Ley 388 de

1997

Establece los mecanismos que permiten al municipio, en ejercicio de su

autonomía, promover el ordenamiento de su territorio, el uso equitativo y

racional del suelo, la preservación y defensa del patrimonio ecológico y

cultural. También define en su ámbito territorial la prevención de desastres

en asentamientos de alto riesgo.

Ley 614 de

2000

Establece mecanismos de integración, coordinación y armonización de las

diferentes entidades competentes en materia de ordenamiento del territorio,

para la implementación de los planes de ordenamiento territorial.

Ley 1454 de

2011

Ley Orgánica de Ordenamiento Territorial (LOOT). Dicta las normas

orgánicas para la organización política administrativa del territorio

colombiano. Limita el ejercicio de la actividad legislativa en materia de

normas y disposiciones de carácter orgánico relativas a la organización

político-administrativa del Estado en el territorio. Establece los principios

rectores del ordenamiento.

Presupuesto y

responsabilid

ad fiscal

Decreto 111

de 1996

Regula la programación, elaboración, presentación, aprobación, modificación

y ejecución del presupuesto, así como la capacidad de contratación y define

el gasto público social.

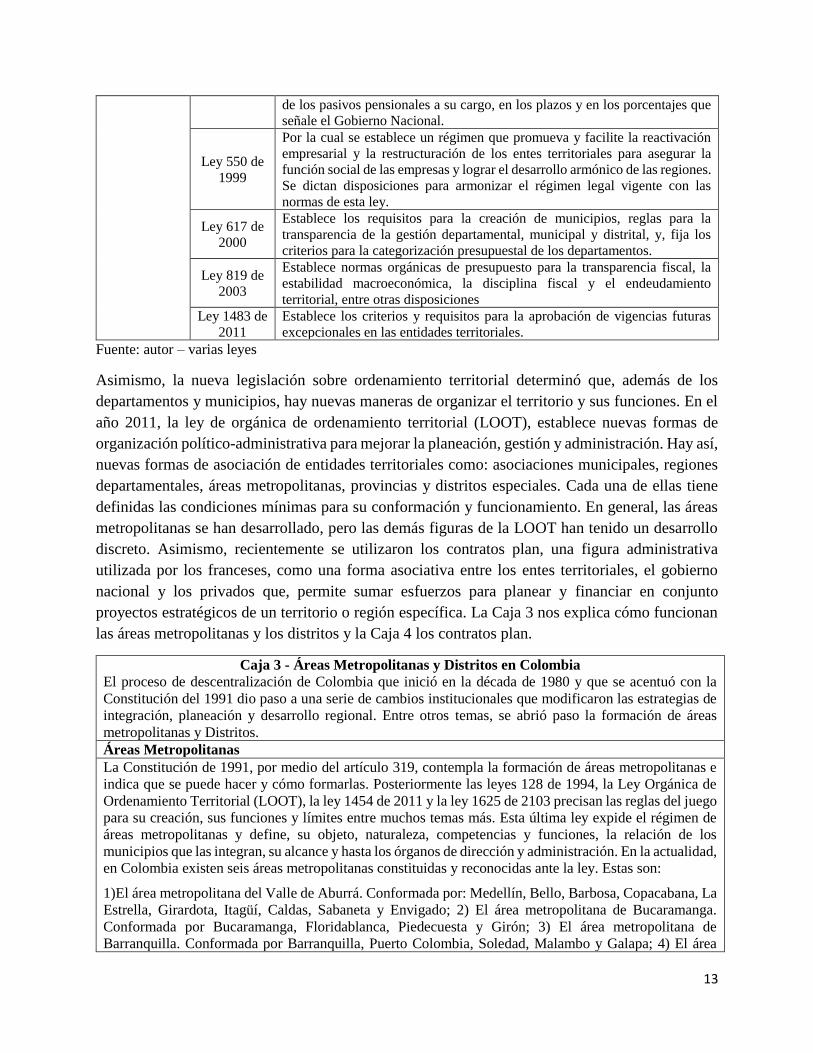

Decreto

1865

Por el cual se regulan los planes regionales ambientales de las Corporaciones

Autónomas Regionales y de las de Desarrollo Sostenible y su armonización

con la gestión ambiental territorial (Decreto 1865).

Ley 549 de

1999

Establece que, con el fin de asegurar la estabilidad económica del Estado, las

entidades territoriales deberán cubrir en la forma prevista en esta ley, el valor

13

de los pasivos pensionales a su cargo, en los plazos y en los porcentajes que

señale el Gobierno Nacional.

Ley 550 de

1999

Por la cual se establece un régimen que promueva y facilite la reactivación

empresarial y la restructuración de los entes territoriales para asegurar la

función social de las empresas y lograr el desarrollo armónico de las regiones.

Se dictan disposiciones para armonizar el régimen legal vigente con las

normas de esta ley.

Ley 617 de

2000

Establece los requisitos para la creación de municipios, reglas para la

transparencia de la gestión departamental, municipal y distrital, y, fija los

criterios para la categorización presupuestal de los departamentos.

Ley 819 de

2003

Establece normas orgánicas de presupuesto para la transparencia fiscal, la

estabilidad macroeconómica, la disciplina fiscal y el endeudamiento

territorial, entre otras disposiciones

Ley 1483 de

2011

Establece los criterios y requisitos para la aprobación de vigencias futuras

excepcionales en las entidades territoriales.

Fuente: autor – varias leyes

Asimismo, la nueva legislación sobre ordenamiento territorial determinó que, además de los

departamentos y municipios, hay nuevas maneras de organizar el territorio y sus funciones. En el

año 2011, la ley de orgánica de ordenamiento territorial (LOOT), establece nuevas formas de

organización político-administrativa para mejorar la planeación, gestión y administración. Hay así,

nuevas formas de asociación de entidades territoriales como: asociaciones municipales, regiones

departamentales, áreas metropolitanas, provincias y distritos especiales. Cada una de ellas tiene

definidas las condiciones mínimas para su conformación y funcionamiento. En general, las áreas

metropolitanas se han desarrollado, pero las demás figuras de la LOOT han tenido un desarrollo

discreto. Asimismo, recientemente se utilizaron los contratos plan, una figura administrativa

utilizada por los franceses, como una forma asociativa entre los entes territoriales, el gobierno

nacional y los privados que, permite sumar esfuerzos para planear y financiar en conjunto

proyectos estratégicos de un territorio o región específica. La Caja 3 nos explica cómo funcionan

las áreas metropolitanas y los distritos y la Caja 4 los contratos plan.

Caja 3 - Áreas Metropolitanas y Distritos en Colombia

El proceso de descentralización de Colombia que inició en la década de 1980 y que se acentuó con la

Constitución del 1991 dio paso a una serie de cambios institucionales que modificaron las estrategias de

integración, planeación y desarrollo regional. Entre otros temas, se abrió paso la formación de áreas

metropolitanas y Distritos.

Áreas Metropolitanas

La Constitución de 1991, por medio del artículo 319, contempla la formación de áreas metropolitanas e

indica que se puede hacer y cómo formarlas. Posteriormente las leyes 128 de 1994, la Ley Orgánica de

Ordenamiento Territorial (LOOT), la ley 1454 de 2011 y la ley 1625 de 2103 precisan las reglas del juego

para su creación, sus funciones y límites entre muchos temas más. Esta última ley expide el régimen de

áreas metropolitanas y define, su objeto, naturaleza, competencias y funciones, la relación de los

municipios que las integran, su alcance y hasta los órganos de dirección y administración. En la actualidad,

en Colombia existen seis áreas metropolitanas constituidas y reconocidas ante la ley. Estas son:

1)El área metropolitana del Valle de Aburrá. Conformada por: Medellín, Bello, Barbosa, Copacabana, La

Estrella, Girardota, Itagüí, Caldas, Sabaneta y Envigado; 2) El área metropolitana de Bucaramanga.

Conformada por Bucaramanga, Floridablanca, Piedecuesta y Girón; 3) El área metropolitana de

Barranquilla. Conformada por Barranquilla, Puerto Colombia, Soledad, Malambo y Galapa; 4) El área

14

metropolitana de Cúcuta. Conformada por: Cúcuta, Villar del Rosario, Los Patios y El Zulia; 5) El área

metropolitana de Centro Occidente. Conformada por Pereira y Dosquebradas y, 6) El área metropolitana

de Valledupar. Conformada por: Valledupar, Agustín Codazzi, La Paz, Manaure Balcón del Cesar y San

Diego.

Las áreas metropolitanas pueden ser integradas por municipios de un mismo departamento, municipios

de diferentes departamentos que limiten entre sí y, por municipios que no limitan entre sí, pero que

conservan una relación histórica en términos económicos y/o sociales.

Con estas áreas se integran las políticas públicas de los municipios y se logra una mejor coordinación en

términos económicos, políticos y de gobernanza territorial. Esto es muy positivo si se considera el hecho

de que los municipios siguen conservando su autonomía. Dado que cada municipio suele llevar a cabo su

propio Plan de Ordenamiento Territorial (POT) sin tener en cuenta las dificultades o los impactos causados

a los municipios vecinos. El área metropolitana soluciona esto por medio de la integración de la

gobernanza territorial en un solo POT. Se optimizan de una mejor manera los recursos, la capacidad de

gestión aumenta y se reducen las brechas económicas entre las regiones. Se pueden llevar a cabo proyectos

regionales.

Distritos9

Los distritos son una forma alternativa de organización y funcionamiento de los municipios. Solo pueden

ser distritos aquellos que cumplen una serie de características. Los distritos tienen un régimen legal,

administrativo, político y económico propio. En Colombia, hay varias categorías de distritos y esta guarda

relación con la actividad económica básica. Hay distritos turísticos, industriales, portuarios y culturales,

entre otros. También, existe la categoría de Distrito Capital, que se refiere a la ciudad capital del país,

Bogotá.

Es preciso señalar que la ley 1617 de 2013, por la cual se expide el régimen para los distritos especiales,

define los estatutos políticos, administrativos y fiscales de los distritos. En ella, se discute la creación, el

funcionamiento y los límites de los distritos, además de su organización política, administrativa y de

carácter territorial.

Actualmente, Colombia cuenta con los siguientes distritos:

1) Bogotá: Distrito Capital.

2) Barrancabermeja: Distrito especial, portuario, industrial, turístico y biodiverso.

3) Barranquilla: Distrito especial, industrial y portuario.

4) Buenaventura: Distrito especial, industrial, portuario, biodiverso y ecoturístico.

5) Cartagena: Distrito turístico y cultural.

6) Mompox: Distrito especial, turístico y cultural.

7) Riohacha: Distrito especial, turístico y cultural.

8) Santa Marta: Distrito turístico, cultural e histórico.

9) Turbo: Distrito portuario, logístico, turístico, industrial y comercial. Y,

10) Cali: Distrito especial, deportivo, empresarial y de servicios.

9 Gómez, L. (2017). Así nacieron las áreas metropolitanas. Revista Semana. Documento en línea, recuperado de:

https://www.semana.com/contenidos-editoriales/valle-de-aburra-sin-fronteras/articulo/historia-del-nacimiento-de-las-areas-

metropolitanas-de-colombia/544873.

Ley 1625 de 2013. Diario Oficial de la República de Colombia. Bogotá, Colombia, 29 de abril de 2013.

Ley 1617 de 2013. Diario Oficial de la República de Colombia. Bogotá, Colombia, 05 de febrero de 2013.

Zapata, O. (2017). Las provincias y las áreas metropolitanas en Colombia: Potencias para la integración y el desarrollo regional.

Revista Políticas Públicas. Vol. 10(2).

15

Caja 4 - Los Contratos Plan en Colombia

La 1454 de 2011, ley Orgánica de Ordenamiento Territorial (LOOT), entre otros objetivos, busca concertar

esfuerzos estatales para la planeación integral del desarrollo territorial con visión de largo plazo. Permite

que entidades u organismos del nivel nacional puedan firmar con entidades u organismos del nivel territorial

esquemas asociativos territoriales. Estos se conocen como los Contratos Plan (CP). Mas adelante, se utiliza

en los planes de desarrollo nacionales de 2010-2014 y 2014-2018 de la administración Santos. En mayo de

2016 los bautizó como Contratos Plan para la Paz. Estos son una herramienta de gestión de la inversión

pública que permite focalización y convergencia de los diferentes niveles de gobierno en la reconstrucción

de los territorios donde la violencia tuvo alto impacto. En estos contratos plan inclusive pueden participar

los privados.

Los Contratos Plan son un acuerdo de voluntades entre los diferentes niveles de gobierno. Estos identifican

los temas estratégicos para el desarrollo integral y mancomunado de una población y territorio en enfoque

de largo plazo. Lo más novedoso es permite la ejecución concertada de programas y proyectos de inversión,

la prestación de servicios públicos y el ejercicio de competencias y funciones que de manera conjunta

realicen los territorios. Debe quedar en claro que no es una nueva fuente de financiamiento para los

territorios; cada participante debe aportar sus recursos con las fuentes actualmente disponibles. No obstante,

sí implican mayor disponibilidad de recursos para los sectores y programas objeto del Contrato Plan ya

que, buena parte de los recursos provienen del Presupuesto Nacional. Se estima que la Nación contribuya

con un aporte máximo de hasta un 60% de las inversiones, al tiempo que las entidades territoriales deberán

concurrir con el 40% restante.

Inicialmente se hicieron 7 CP en su primera fase: Atrato Gran Darién, Boyacá, Santander, Sur del Tolima,

Cauca, Arauca y Nariño. Una evaluación de estos siete contratos dejo en evidencia que lo mejor no es hacer

múltiples proyectos, sino más bien concentrarse en iniciativas capaces de transformar la vida de las

comunidades. Es decir, proyectos de alto impacto. Por esta razón el Documento Conpes 3822 DNP permitió

aumentar en 10 el número de Contratos Plan y modificó la gestión de los recursos. Se creó así un Fondo

Regional para los Contratos Plan en el Plan Nacional de Desarrollo 2014-2018 Todos por un nuevo país.

Los Contratos Plan no pueden sustituir, ni entrar en competencia con los demás instrumentos de

priorización y gestión de la inversión; por lo contrario, deben ser complementarios. Su importancia es

concentrar en pocos años inversiones sociales y en mejora de la infraestructura de regiones o zonas

consideradas clave o estratégicas y que por diferentes razones no han tenido la atención del estado que

merecen. Estas son regiones con altos niveles de pobreza, malos indicadores sociales (salud, educación,

saneamiento básico, etc.), alejadas geográficamente o con un gran atraso en su infraestructura. Se estima

que una región en donde lleguen al tiempo y de manera coordinada inversiones de los tres niveles de

gobierno y del sector privado se logran sinergias definitivas.

Finalmente, se debe mencionar que el DNP es el encargado de la gestión y seguimiento de estos contratos.

Para esto se debe garantizar que las inversiones deberán ser verificables y, debe tener metas de gestión y

que son monitoreadas. También se busca mejorar la gestión de algunos territorios y para esto se incluyen

en las entidades territoriales institucionales. En el actual gobierno los Contratos Plan continúan, pero su

nuevo nombre es Pactos Territoriales. Muy en la línea del nombre del actual Plan de Desarrollo Nacional

Pacto por Colombia, pacto por la equidad.

Fuente: autor

16

Finanzas territoriales

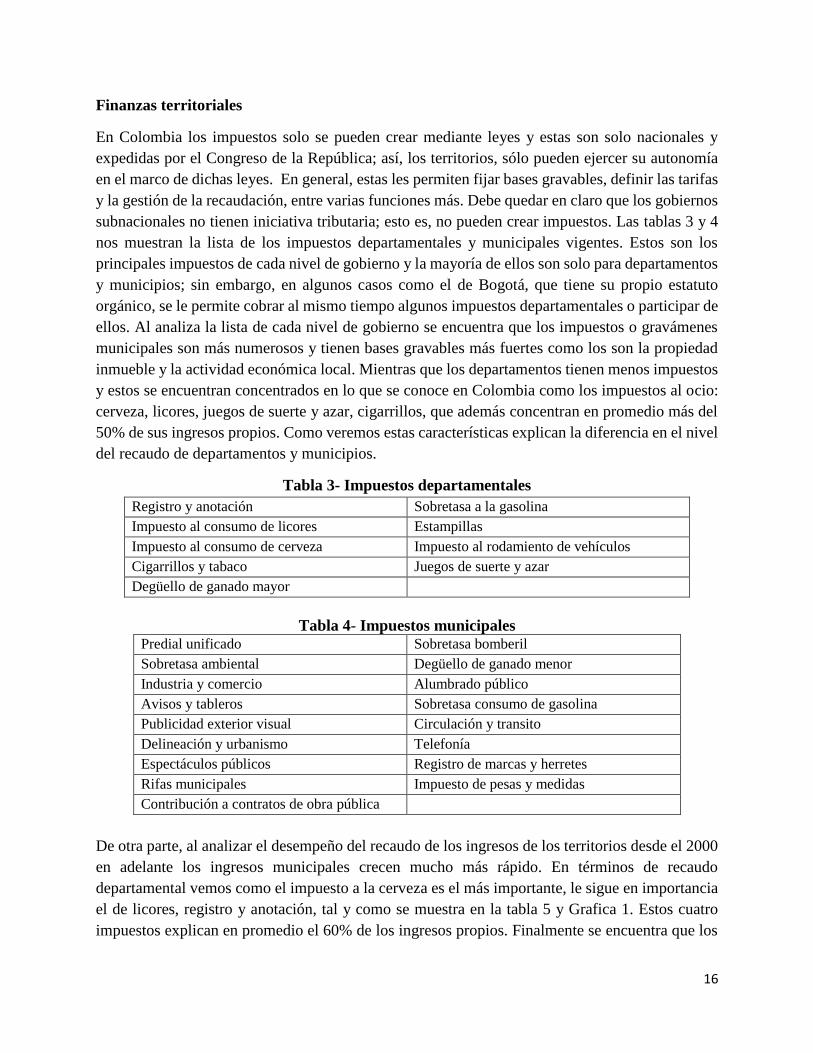

En Colombia los impuestos solo se pueden crear mediante leyes y estas son solo nacionales y

expedidas por el Congreso de la República; así, los territorios, sólo pueden ejercer su autonomía

en el marco de dichas leyes. En general, estas les permiten fijar bases gravables, definir las tarifas

y la gestión de la recaudación, entre varias funciones más. Debe quedar en claro que los gobiernos

subnacionales no tienen iniciativa tributaria; esto es, no pueden crear impuestos. Las tablas 3 y 4

nos muestran la lista de los impuestos departamentales y municipales vigentes. Estos son los

principales impuestos de cada nivel de gobierno y la mayoría de ellos son solo para departamentos

y municipios; sin embargo, en algunos casos como el de Bogotá, que tiene su propio estatuto

orgánico, se le permite cobrar al mismo tiempo algunos impuestos departamentales o participar de

ellos. Al analiza la lista de cada nivel de gobierno se encuentra que los impuestos o gravámenes

municipales son más numerosos y tienen bases gravables más fuertes como los son la propiedad

inmueble y la actividad económica local. Mientras que los departamentos tienen menos impuestos

y estos se encuentran concentrados en lo que se conoce en Colombia como los impuestos al ocio:

cerveza, licores, juegos de suerte y azar, cigarrillos, que además concentran en promedio más del

50% de sus ingresos propios. Como veremos estas características explican la diferencia en el nivel

del recaudo de departamentos y municipios.

Tabla 3- Impuestos departamentales

Registro y anotación Sobretasa a la gasolina

Impuesto al consumo de licores Estampillas

Impuesto al consumo de cerveza Impuesto al rodamiento de vehículos

Cigarrillos y tabaco Juegos de suerte y azar

Degüello de ganado mayor

Tabla 4- Impuestos municipales

Predial unificado Sobretasa bomberil

Sobretasa ambiental Degüello de ganado menor

Industria y comercio Alumbrado público

Avisos y tableros Sobretasa consumo de gasolina

Publicidad exterior visual Circulación y transito

Delineación y urbanismo Telefonía

Espectáculos públicos Registro de marcas y herretes

Rifas municipales Impuesto de pesas y medidas

Contribución a contratos de obra pública

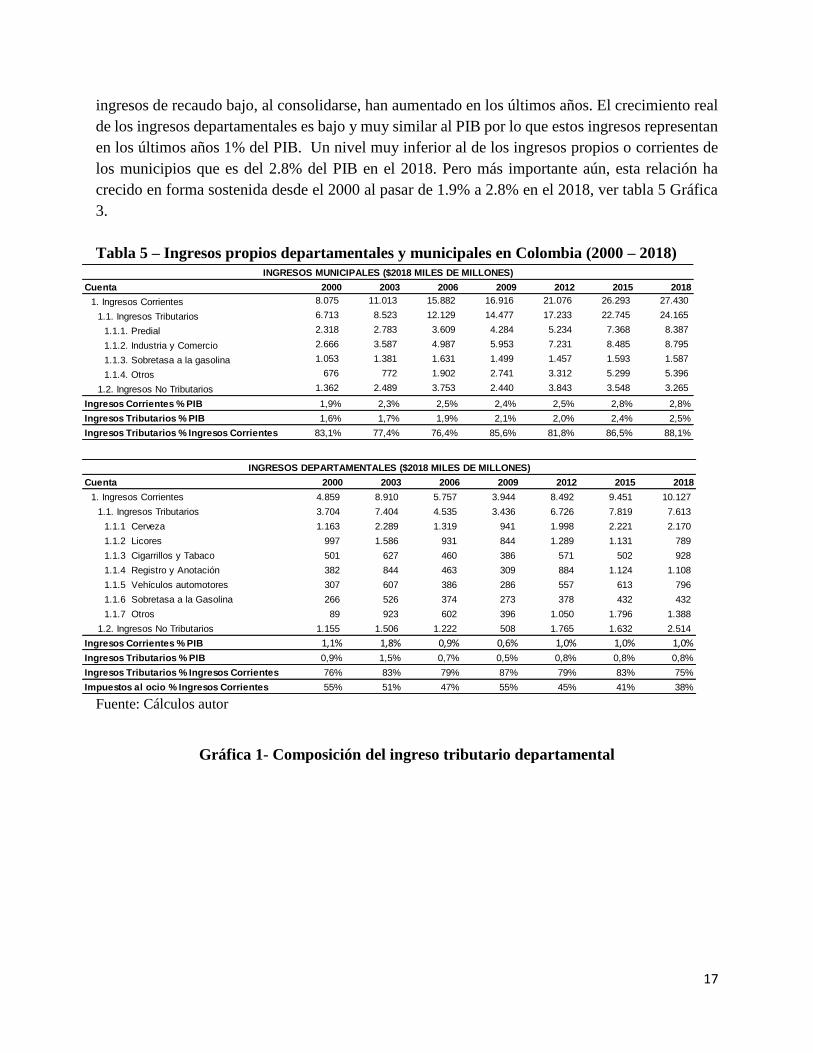

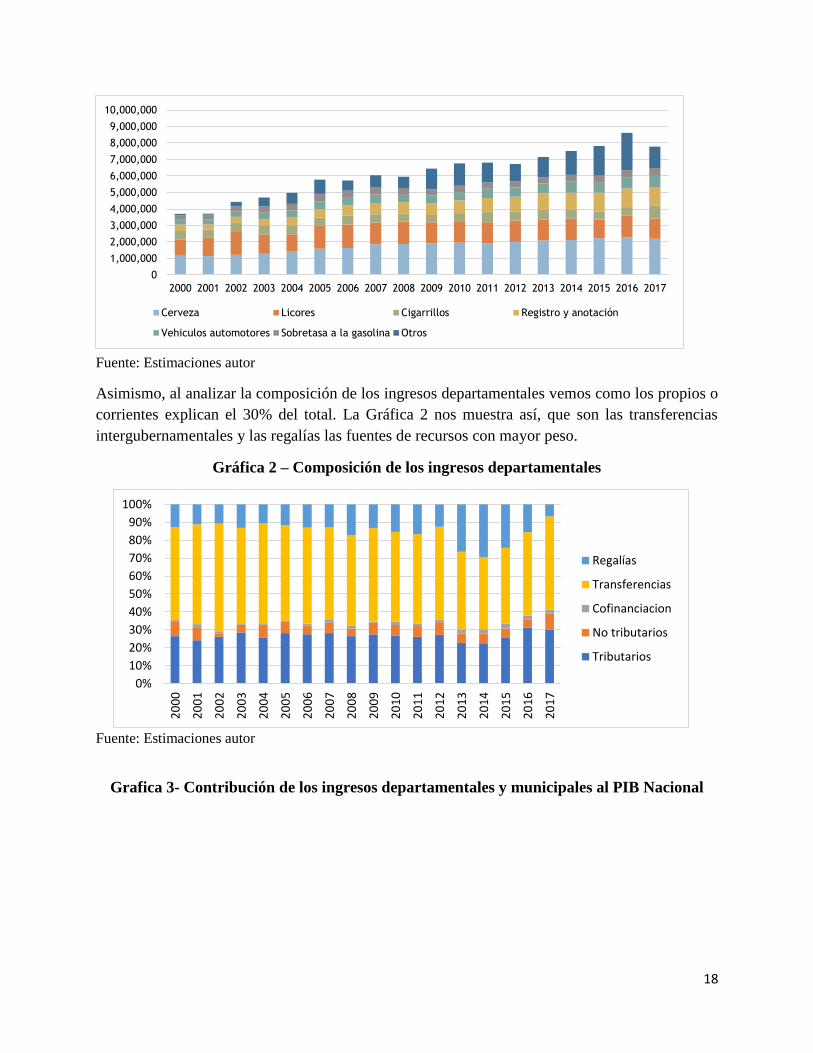

De otra parte, al analizar el desempeño del recaudo de los ingresos de los territorios desde el 2000

en adelante los ingresos municipales crecen mucho más rápido. En términos de recaudo

departamental vemos como el impuesto a la cerveza es el más importante, le sigue en importancia

el de licores, registro y anotación, tal y como se muestra en la tabla 5 y Grafica 1. Estos cuatro

impuestos explican en promedio el 60% de los ingresos propios. Finalmente se encuentra que los

17

ingresos de recaudo bajo, al consolidarse, han aumentado en los últimos años. El crecimiento real