Closing State Corporate Tax Loopholes Michael Mazerov ([email protected]) Center on Budget & Policy Priorities AFL-CIO Workers’ Voice Conference San Francisco, California July 20, 2003

Closing State Corporate Tax Loopholes Michael Mazerov ([email protected]) Center on Budget & Policy Priorities AFL-CIO Workers’ Voice Conference San Francisco,

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Closing State Corporate Tax Loopholes

Michael Mazerov ([email protected]) Center on Budget & Policy Priorities

AFL-CIO Workers’ Voice Conference San Francisco, CaliforniaJuly 20, 2003

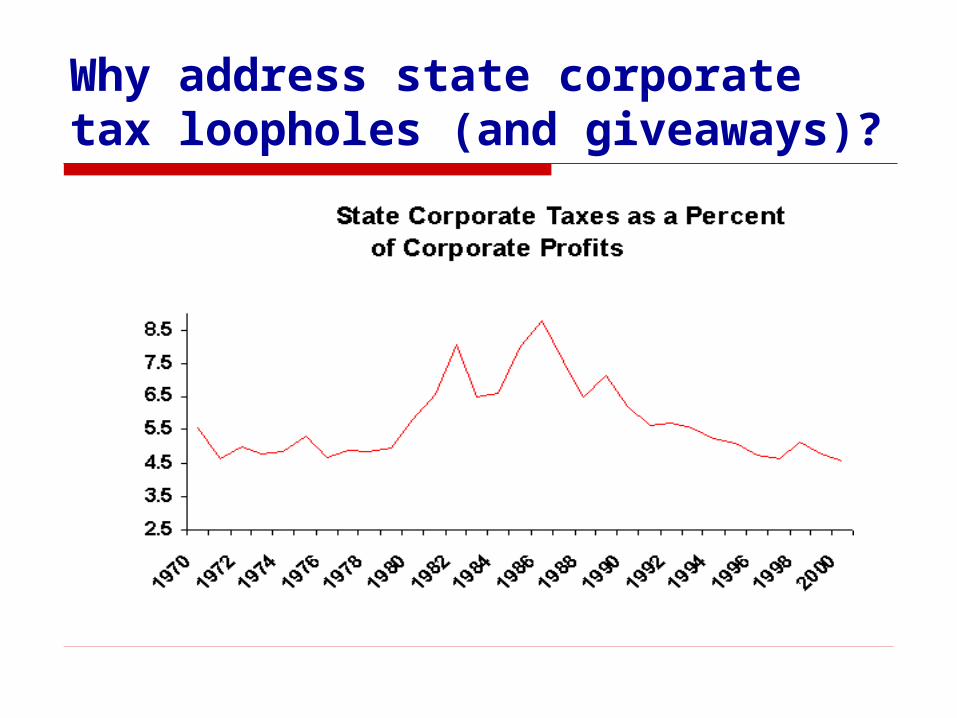

Why address state corporate tax loopholes (and giveaways)?

Share of Total State Taxes Contributed by Corporate Income Taxes

(States with Corporate Income Taxes)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1979 1989 2000

Why address state corporate tax loopholes (and giveaways)?

Why address state corporate tax loopholes (and giveaways)?

Annual Growth in CorporateIncome Taxes, 1995-2000

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Federal State

Ann

ual P

erce

nt G

row

th

Why address state corporate tax loopholes (and giveaways)?

State Corporate Income Tax Revenues: Actual FY00 and FY00 If Same Share of Total State Taxes As in FY79

$32.5

$54.5

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

Actual FY00 If same share of total state taxes as in '79

$ b

illio

ns

First, DO NO HARM;Stop New Revenue Losses From:

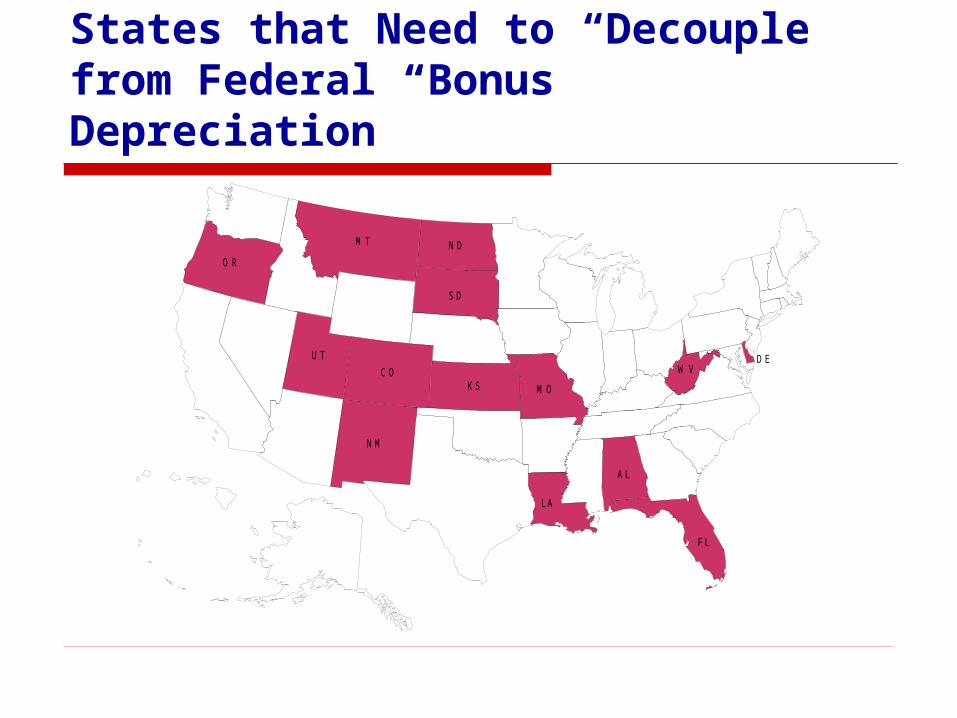

State corporate income tax coupling to federal deduction for “bonus depreciation” in 2002 and 2003 federal tax cut bills

States can “decouple” their laws; 31 have already

States that Need to “Decouple” from Federal “Bonus Depreciation”

W VU T

S D

O R

N M

N DM T

M O

L A

K S

F L

D EC O

A L

First, DO NO HARMStop New Revenue Losses From:

New economic development giveaways.

Still proliferating (e.g., “single sales factor” corporate tax formula enacted this year in Wisconsin)

First, DO NO HARMStop New Revenue Losses From: Proposed federal legislation restricting

state corporate tax powers Known as “business activity tax” (BAT)

“nexus” bill Would require a corp. to have a

“substantial physical presence” in a state before that state could tax its profits

Higher nexus threshold than required at present, so states would lose $ rapidly

Opens up all kinds of new tax shelters

First, DO NO HARM; Block Proposed BAT Nexus Bill to Avoid Revenue Losses

NCSL considering resolution to endorse proposed BAT nexus bill

Corporate America demanding this bill as quid pro quo for empowering states to tax Internet sales

NCSL (rightfully) wants this; but too high a price to pay

Need to block any NCSL resolution on BAT nexus at this time

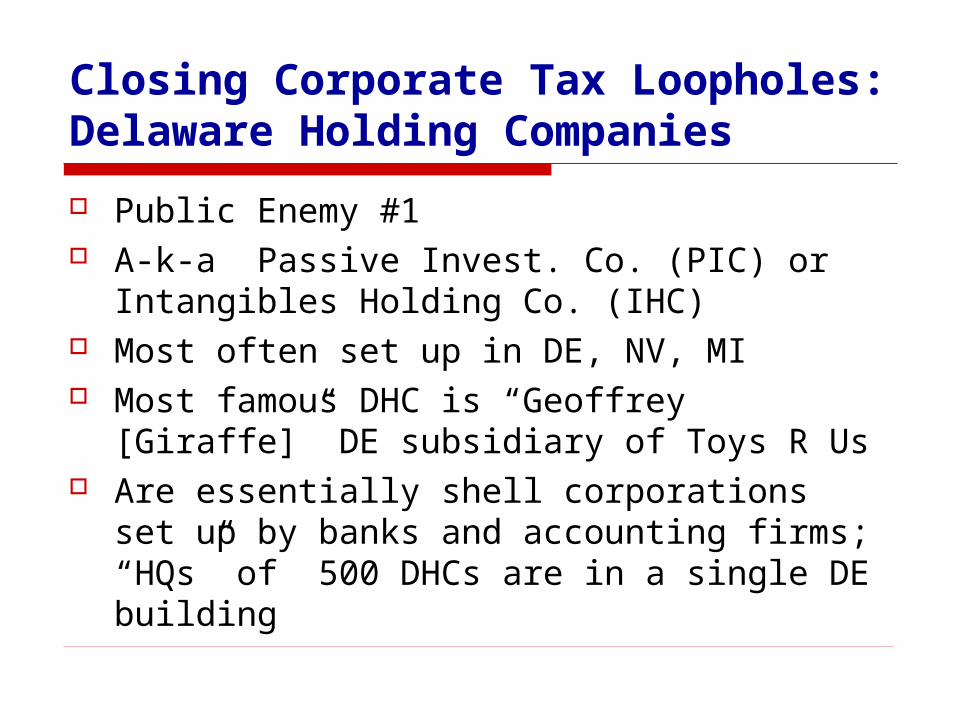

Closing Corporate Tax Loopholes: Delaware Holding Companies

Public Enemy #1 A-k-a Passive Invest. Co. (PIC) or

Intangibles Holding Co. (IHC) Most often set up in DE, NV, MI Most famous DHC is “Geoffrey [Giraffe]”

DE subsidiary of Toys R Us Are essentially shell corporations set up

by banks and accounting firms; “HQs” of 500 DHCs are in a single DE building

How the DHC game works

Step 1: Parent corporation sets up DHC in state without corporate income tax (NV) or that doesn’t tax corps whose only income is from intangible assets (DE, MI)

Step 2: Parent transfers to DHC its patents, trademarks, “know-how,” etc.

Step 3: DHC licenses back to parent the right to use patents, trademarks, etc. in exchange for tax-deductible royalties

Result: payment of royalties reduces (perhaps eliminates) taxable profit of parent, while DHC is not subject to tax on its profit

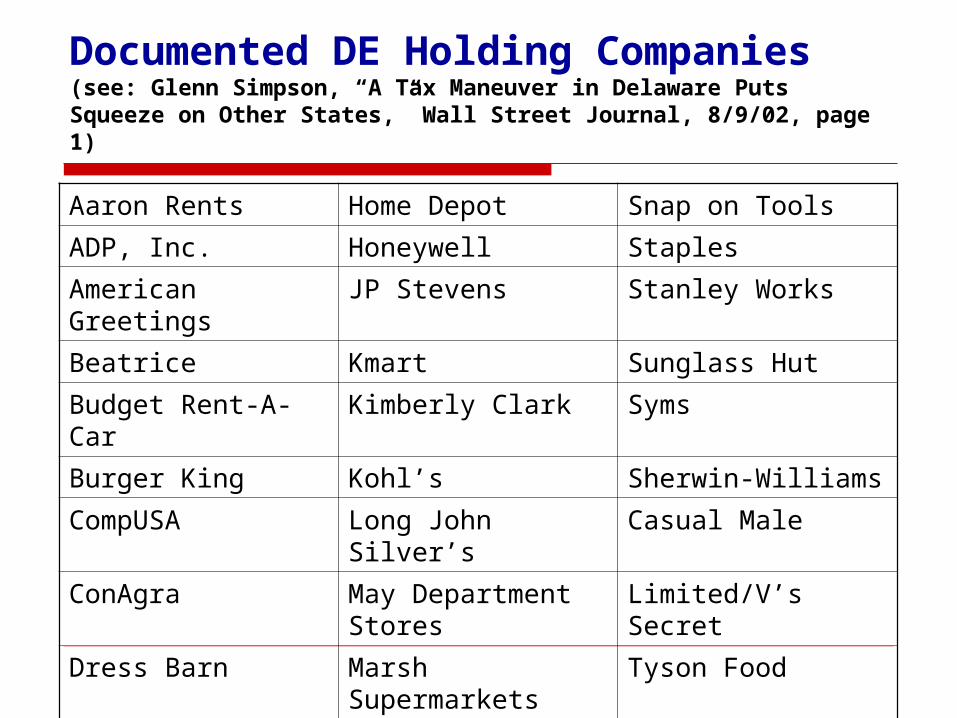

Documented DE Holding Companies(see: Glenn Simpson, “A Tax Maneuver in Delaware Puts Squeeze on Other States,” Wall Street Journal, 8/9/02, page 1)

Aaron Rents Home Depot Snap on Tools

ADP, Inc. Honeywell Staples

American Greetings JP Stevens Stanley Works

Beatrice Kmart Sunglass Hut

Budget Rent-A-Car Kimberly Clark Syms

Burger King Kohl’s Sherwin-Williams

CompUSA Long John Silver’s Casual Male

ConAgra May Department Stores Limited/V’s Secret

Dress Barn Marsh Supermarkets Tyson Food

Gap Payless Shoesource Toys R Us

Gore[tex] Industries Radio Shack Urban Outfitters

States Still Losing Revenue to the “DE Holding Company” Tax Shelter

W V

W I

V T

V A

T X

T N

S D

S C

R I

P A

O K

N Y

N M

M O

M D

L A

K Y

I N

I A

G A

F L

D E

D C

A R

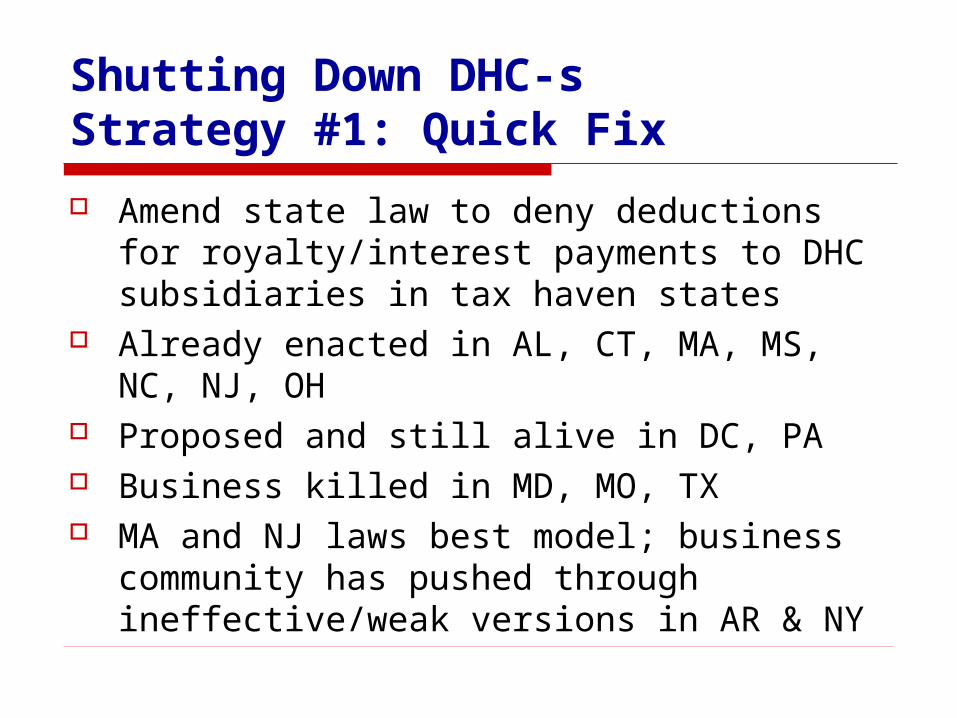

Shutting Down DHC-sStrategy #1: Quick Fix

Amend state law to deny deductions for royalty/interest payments to DHC subsidiaries in tax haven states

Already enacted in AL, CT, MA, MS, NC, NJ, OH

Proposed and still alive in DC, PA Business killed in MD, MO, TX MA and NJ laws best model; business

community has pushed through ineffective/weak versions in AR & NY

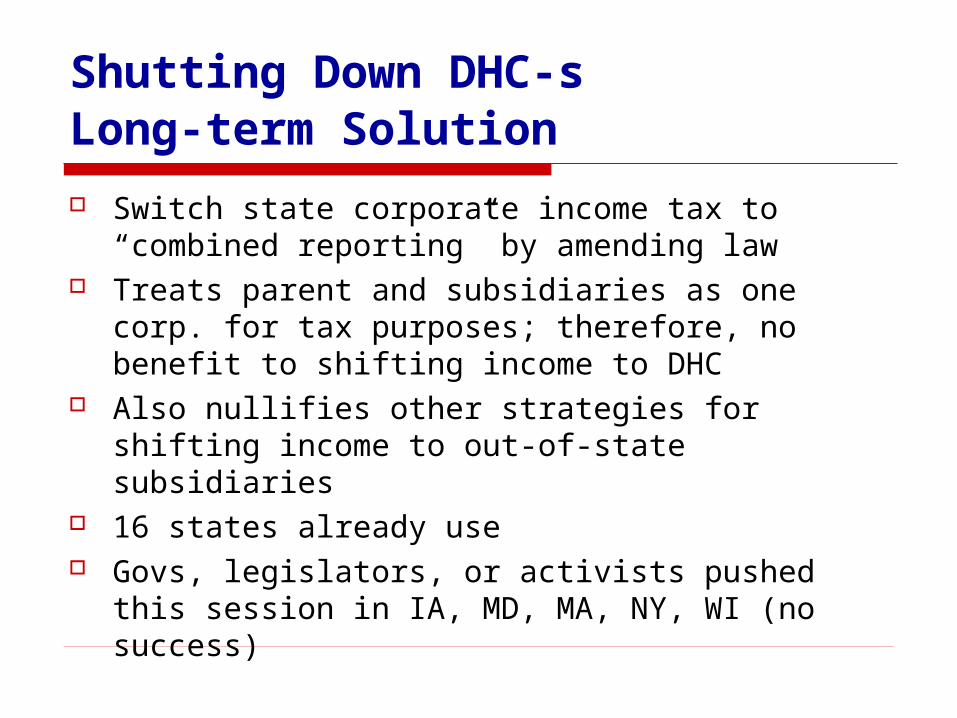

Shutting Down DHC-sLong-term Solution

Switch state corporate income tax to “combined reporting” by amending law

Treats parent and subsidiaries as one corp. for tax purposes; therefore, no benefit to shifting income to DHC

Also nullifies other strategies for shifting income to out-of-state subsidiaries

16 states already use Govs, legislators, or activists pushed this

session in IA, MD, MA, NY, WI (no success)

States that Need to Adopt “Combined Reporting”

W V

W I

V T

V A

T X

T N

S D

S C

R I

P A

O K

O H

N Y

N M

N J

N C

M S

M O

M D

M A

L A

K Y

I N

I A

G A

F L

D E

D C

C T

A R

A L

Closing Corporate Loopholes:“Nowhere Income” Problem: Corporations can make sales in

states in which they don’t cross taxability threshold — “have nexus”

Solution: enact “throwback” or “throwout” rule

Ensures that corps. are taxed on profits they earn in states where they aren’t taxable — home state taxes profit instead

NJ enacted 2002; MD 2003 (Gov vetoed)

States that Need to Adopt “Throwback Rule”

V A

T N

S C

R IP A

O H

N Y

N E

N C

M N

M D

M A

L A

K Y

I A

G A

F L

D E

C T

A Z

Eliminate Unwarranted Corporate Tax Giveaways

Repeal “single sales factor formula” Giveaway to corps. that sell most of

what they produce out of state — especially manufacturers

Big business still actively seeking in AZ, CA, NJ, NY, PA, RI (be on guard)

Repeal being pushed in IL, MA, MO

States that Need to Repeal “Single Sales Factor Formula” (and Similar Giveaway)

T X

O R

N E

M O

M N

M I

M D

M A

I L

I A

C TW I

Eliminate Unwarranted Corporate Tax Giveaways

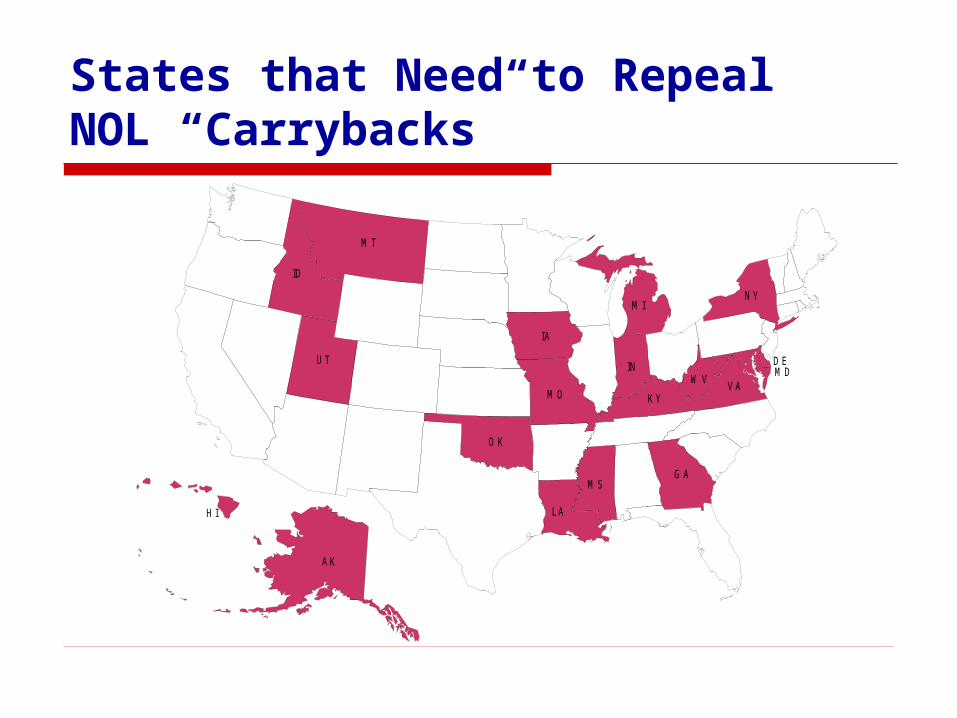

Repeal ability of corporations to “carry back” current losses to years in which they were profitable and obtain refunds of taxes paid in those years

Only minority of states still allow

States that Need to Repeal NOL “Carrybacks”

W VV A

U T

O K

N Y

M T

M S

M O

M I

M D

L A

K Y

I N

I D

I A

H I

G A

D E

A K

Other Current Corporate Tax Reform Efforts Legislation was introduced in TX to

close “Delaware Sub” loophole (use of limited partnerships to avoid franchise tax). Gov. supported; business killed.

NV Gov. Quinn proposed business gross receipts tax — OK, but CIT better. Business killed.

Other Corporate Tax Reform Options: Enact Corporate Minimum Taxes

Enact a second corporate tax not based on profits; corp. pays higher of profits tax or tax on other base

NJ enacted alternative minimum tax last year based on gross receipts

Another good model is NH’s alternative tax based on value added

Other Corporate Tax Reform Options: Stop Tax Avoidance from “Limited Liability Companies”

LLCs are businesses whose profits are taxed on the owners’ tax returns — whether owners are individuals or other businesses

Growing evidence that corps are using LLCs to avoid state profits taxes

Need to pass laws requiring LLC to withhold and pay tax due from out-of-state owners unless owners agree in writing to pay tax due on their pro-rata share of LLC income

Chipping Away at the Internet/ Catalog Sales Tax Loophole

Need federal law to ensure sales taxation of all Internet/catalog sales

But states can require their vendors to collect sales taxes (e.g. Dell Computer). AR, NC, SD do.

States can amend and then enforce laws to compel “dot-com” subsidiaries of retail store chains to charge sales tax (e.g. Barnes & Noble.com)

A recent column headline (and accompanying cartoon):

“It’s Time to Curb Corporate Tax Shenanigans”

From The Nation?Mother Jones?

No!

The Wall Street Journal (9/19/02)

Closing Corporate Tax Loopholes & Repealing Unwarranted Giveaways Time is ripe; take advantage of

current anger about phony financial reporting and aggressive tax sheltering to push reform

Can raise meaningful amounts of revenue now and help preserve state programs from budget cuts

Lays the groundwork for revitalization of corp. income tax as state revenue source; without it, CIT will steadily decline

Related Documents