Close Brothers Group Asset Management Division Presentation to Investors and Analysts 22 April 2009

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Close Brothers Group

Asset Management Division

Presentation to Investors and Analysts

22 April 2009

Page 2

Cautionary statement

Certain statements included in this presentation may constitute "forward-looking statements" in respect of the Group’s operations, performance, prospects and/or financial condition. By their nature, forward looking statements involve a number of risks, uncertainties and assumptions and actual results or events may differ materially from those expressed or implied by those statements. Accordingly, no assurance can be given that any particular expectation will be met and reliance should not be placed on any forward-looking statement. Additionally, forward-looking statements regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. No responsibility or obligation is accepted to update or revise any forward-looking statement resulting from new information, future events or otherwise. Nothing in this presentation should be construed as a profit forecast.

This presentation does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase any shares in the Company, nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any contract or commitment or investment decisions relating thereto, nor does it constitute a recommendation regarding the shares of the Company. Past performance cannot be relied upon as a guide to future performance.

Information in this presentation reflects the knowledge and information available at the time of its preparation.Not intended for distribution to retail customers.

Regarding information in this presentation

Page 3

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Page 4

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Page 5

Introduction

• The Asset Management Division developed via acquisitions over 20+ years

• Encompassed a diverse range of autonomous businesses and capabilities

• Generated significant profit growth to 2007

• Restructuring to improve focus and deliver improved results

Page 6

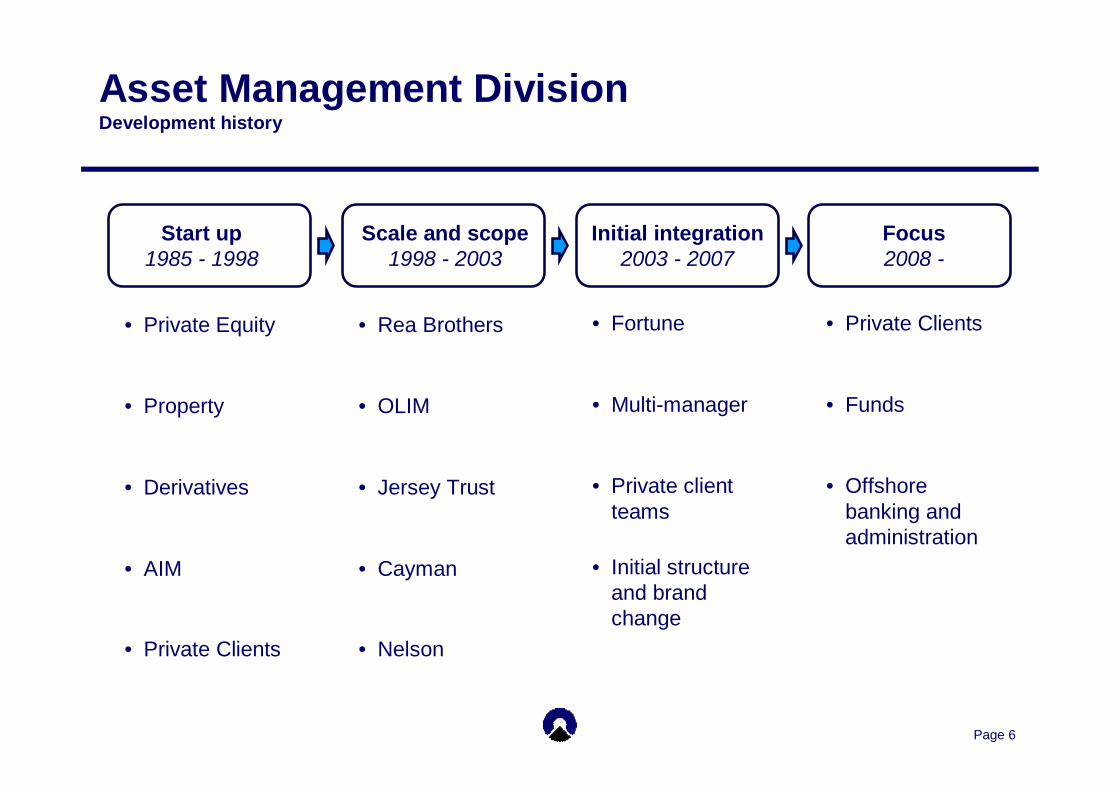

Asset Management DivisionDevelopment history

• Private Equity

• Property

• Derivatives

• AIM

• Private Clients

Start up1985 - 1998

Scale and scope1998 - 2003

Initial integration2003 - 2007

Focus2008 -

• Rea Brothers

• OLIM

• Jersey Trust

• Cayman

• Nelson

• Fortune

• Multi-manager

• Private client teams

• Initial structure and brand change

• Private Clients

• Funds

• Offshore banking and administration

Page 7

Asset Management DivisionSummary

Private Clients Funds Banking and Administration

Wealth and discretionary investment management for private clients, onshore and offshore

Range of specialist investment management capabilities for retail and institutional clients

Range of banking and administration capabilities in Cayman, UK offshore islands and South Africa

Asset Management Division

• Retain business diversification• Increase focus on 3 core areas

• Restructure and integrate internally to improve efficiency and growth

Page 8

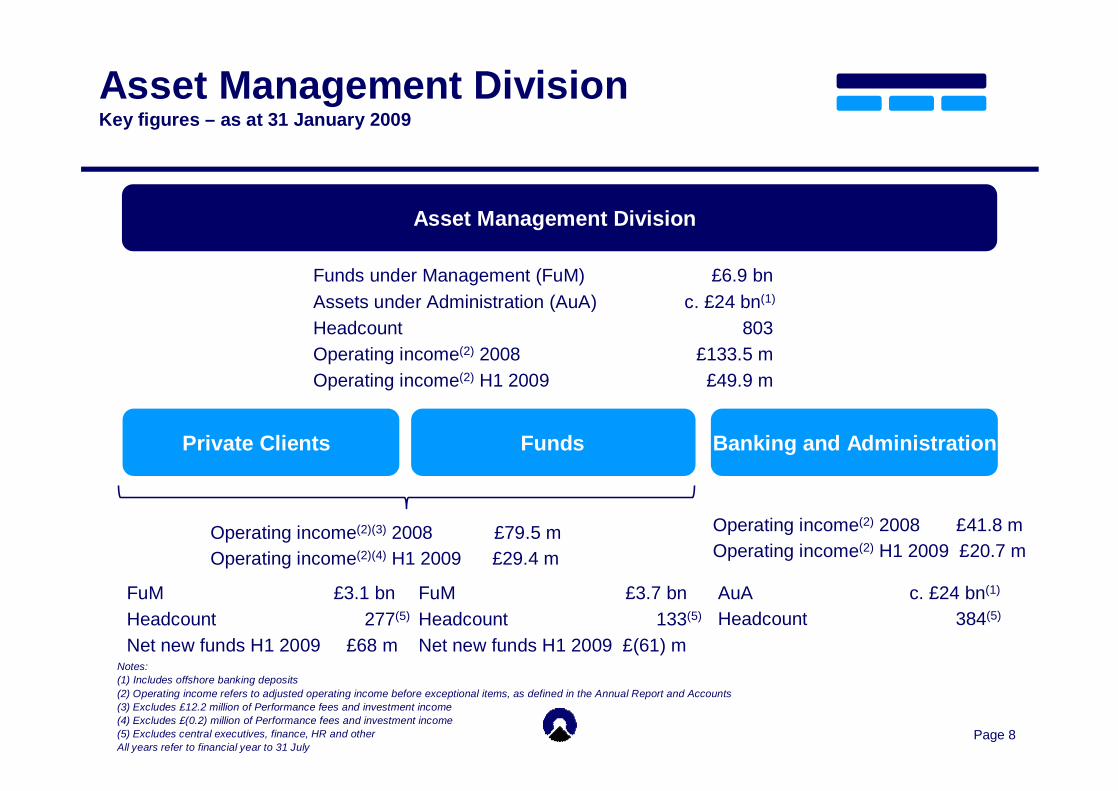

Asset Management DivisionKey figures – as at 31 January 2009

Private Clients Funds Banking and Administration

Asset Management Division

Funds under Management (FuM) £6.9 bnAssets under Administration (AuA) c. £24 bn(1)

Headcount 803Operating income(2) 2008 £133.5 mOperating income(2) H1 2009 £49.9 m

FuM £3.1 bnHeadcount 277(5)

Net new funds H1 2009 £68 m

FuM £3.7 bnHeadcount 133(5)

Net new funds H1 2009 £(61) m

AuA c. £24 bn(1)

Headcount 384(5)

Operating income(2) 2008 £41.8 mOperating income(2) H1 2009 £20.7 m

Operating income(2)(3) 2008 £79.5 mOperating income(2)(4) H1 2009 £29.4 m

Notes: (1) Includes offshore banking deposits(2) Operating income refers to adjusted operating income before exceptional items, as defined in the Annual Report and Accounts(3) Excludes £12.2 million of Performance fees and investment income(4) Excludes £(0.2) million of Performance fees and investment income(5) Excludes central executives, finance, HR and otherAll years refer to financial year to 31 July

Page 9

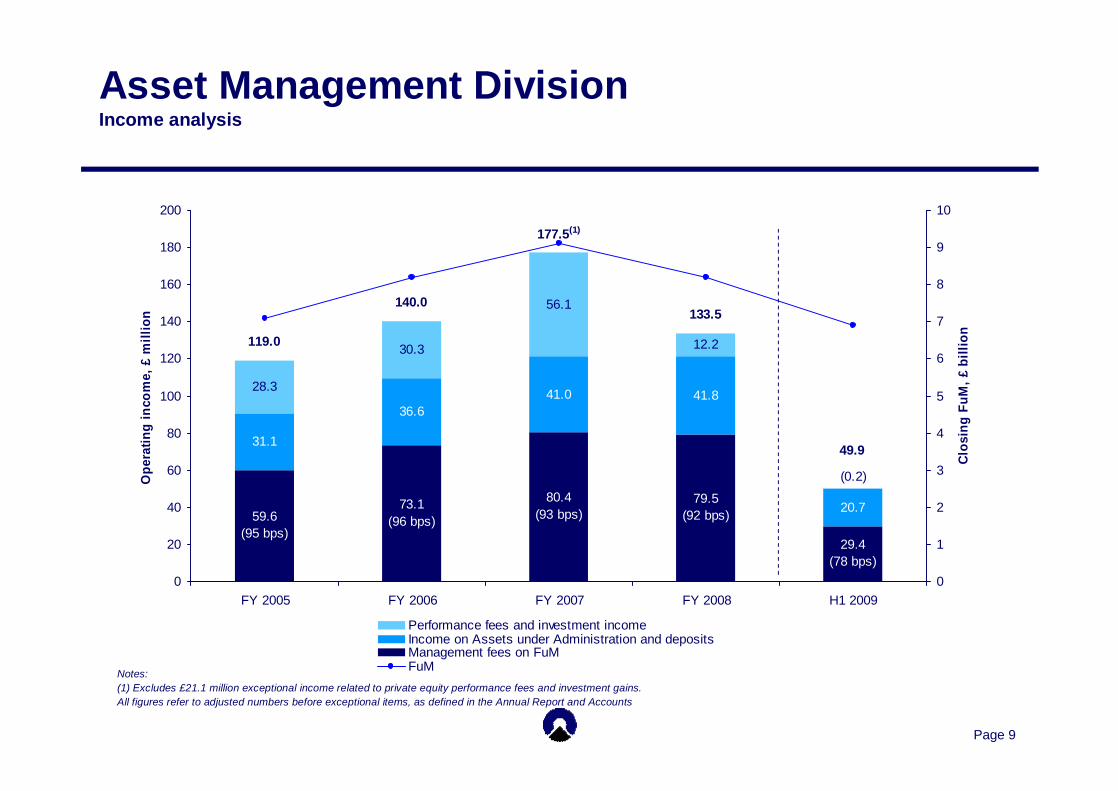

31.1

36.641.0 41.8

20.7

28.3

30.3

56.1

12.2

59.6(95 bps)

73.1(96 bps)

29.4(78 bps)

79.5(92 bps)

80.4(93 bps)

(0.2)

133.5

177.5(1)

119.0

140.0

49.9

0

20

40

60

80

100

120

140

160

180

200

FY 2005 FY 2006 FY 2007 FY 2008 H1 2009

Ope

ratin

g in

com

e, £

mill

ion

0

1

2

3

4

5

6

7

8

9

10

Clos

ing

FuM

, £ b

illio

n

Column 4Performance fees and investment incomeIncome on Assets under Administration and depositsManagement fees on FuMFuM

Asset Management DivisionIncome analysis

Notes:(1) Excludes £21.1 million exceptional income related to private equity performance fees and investment gains.All figures refer to adjusted numbers before exceptional items, as defined in the Annual Report and Accounts

Page 10

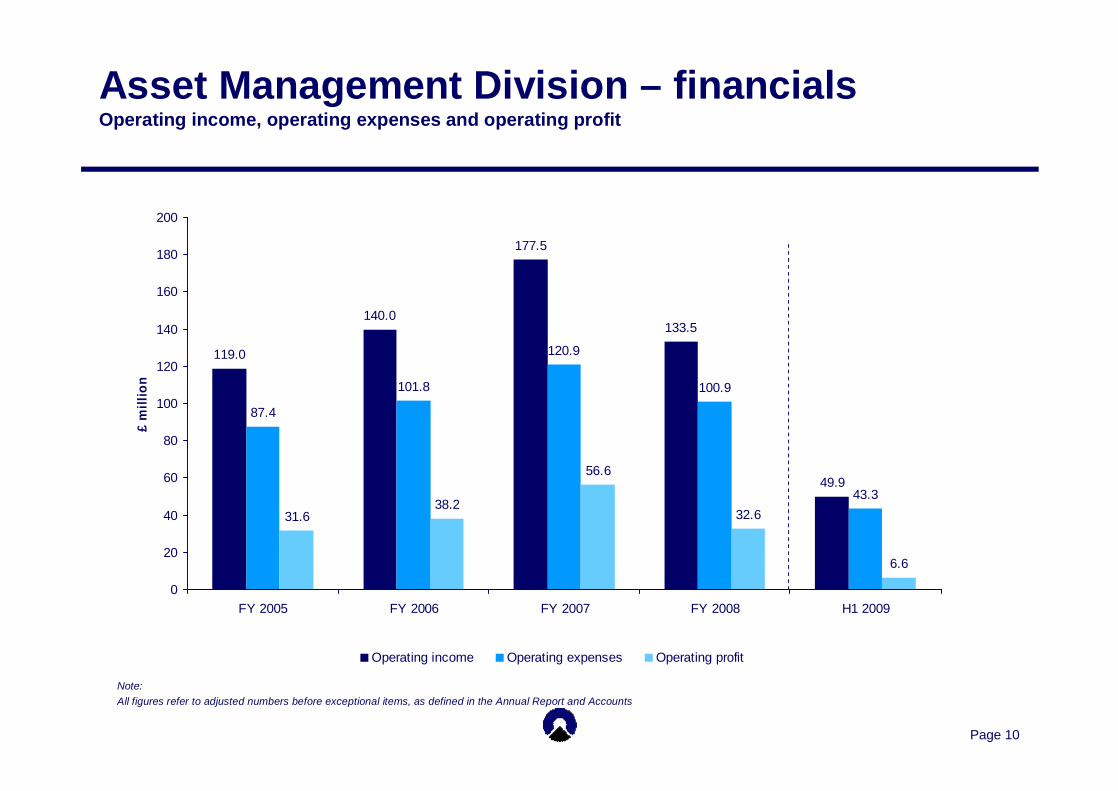

119.0

140.0

177.5

133.5

49.9

87.4

101.8

120.9

100.9

43.3

31.638.2

56.6

32.6

6.6

0

20

40

60

80

100

120

140

160

180

200

FY 2005 FY 2006 FY 2007 FY 2008 H1 2009

£ m

illio

n

Operating income Operating expenses Operating profit

Asset Management Division – financialsOperating income, operating expenses and operating profit

Note: All figures refer to adjusted numbers before exceptional items, as defined in the Annual Report and Accounts

Page 11

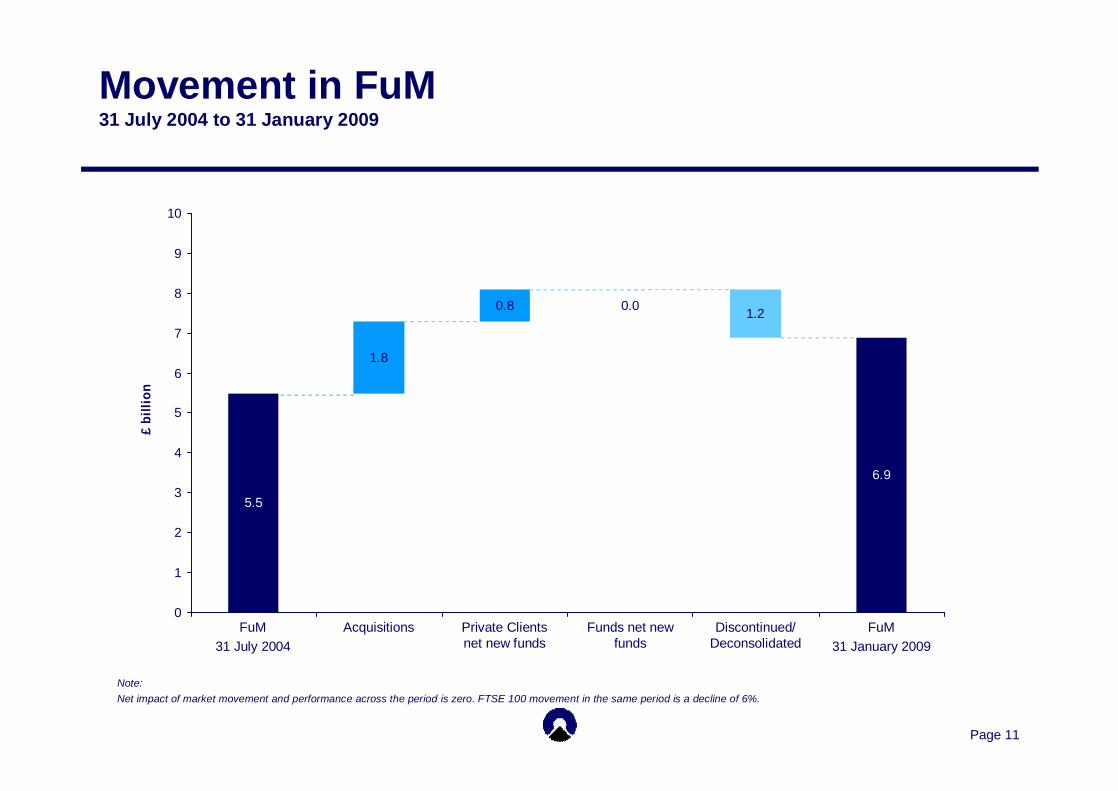

0.0

5.5

1.8

0.8 1.2

6.9

0

1

2

3

4

5

6

7

8

9

10

£ b

illio

n

Movement in FuM31 July 2004 to 31 January 2009

Discontinued/ Deconsolidated

FuM31 January 2009

Funds net new funds

Private Clients net new funds

AcquisitionsFuM31 July 2004

Note: Net impact of market movement and performance across the period is zero. FTSE 100 movement in the same period is a decline of 6%.

Page 12

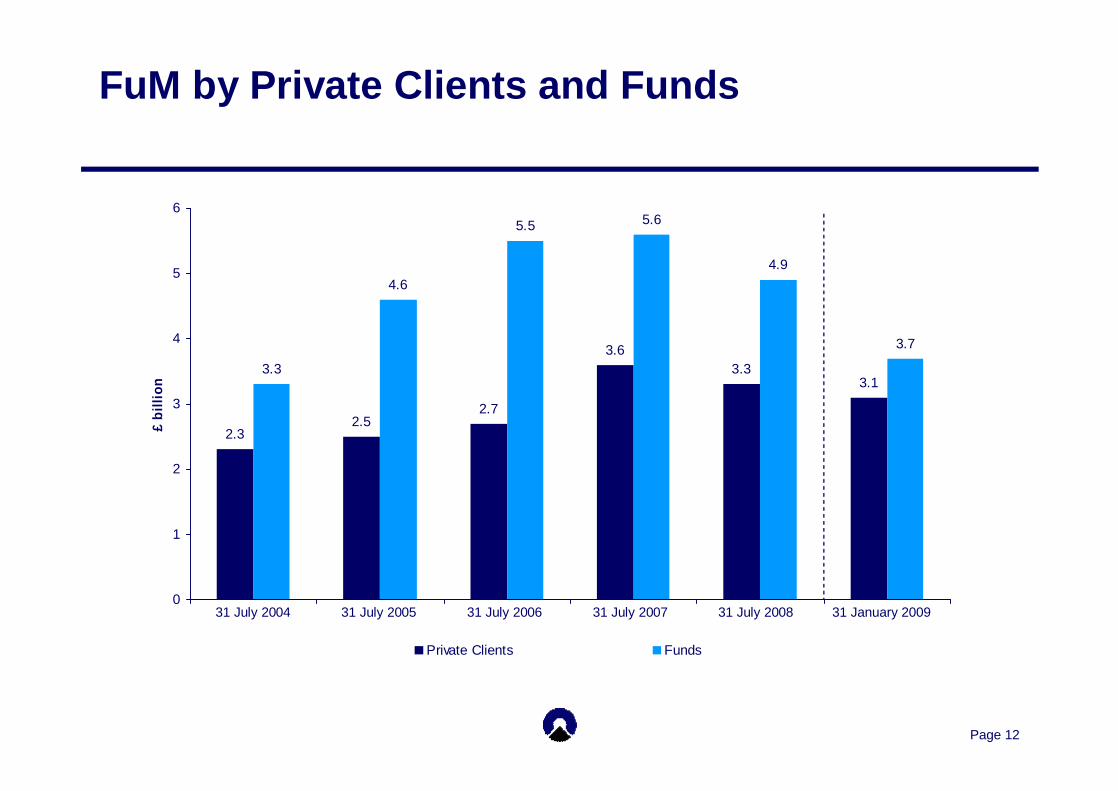

FuM by Private Clients and Funds

2.32.5

2.7

3.63.3

3.13.3

4.6

5.5 5.6

4.9

3.7

0

1

2

3

4

5

6

31 July 2004 31 July 2005 31 July 2006 31 July 2007 31 July 2008 31 January 200

£ bi

llion

Private Clients Funds

31 July 2007 31 January 200931 July 200831 July 200631 July 200531 July 2004

Page 13

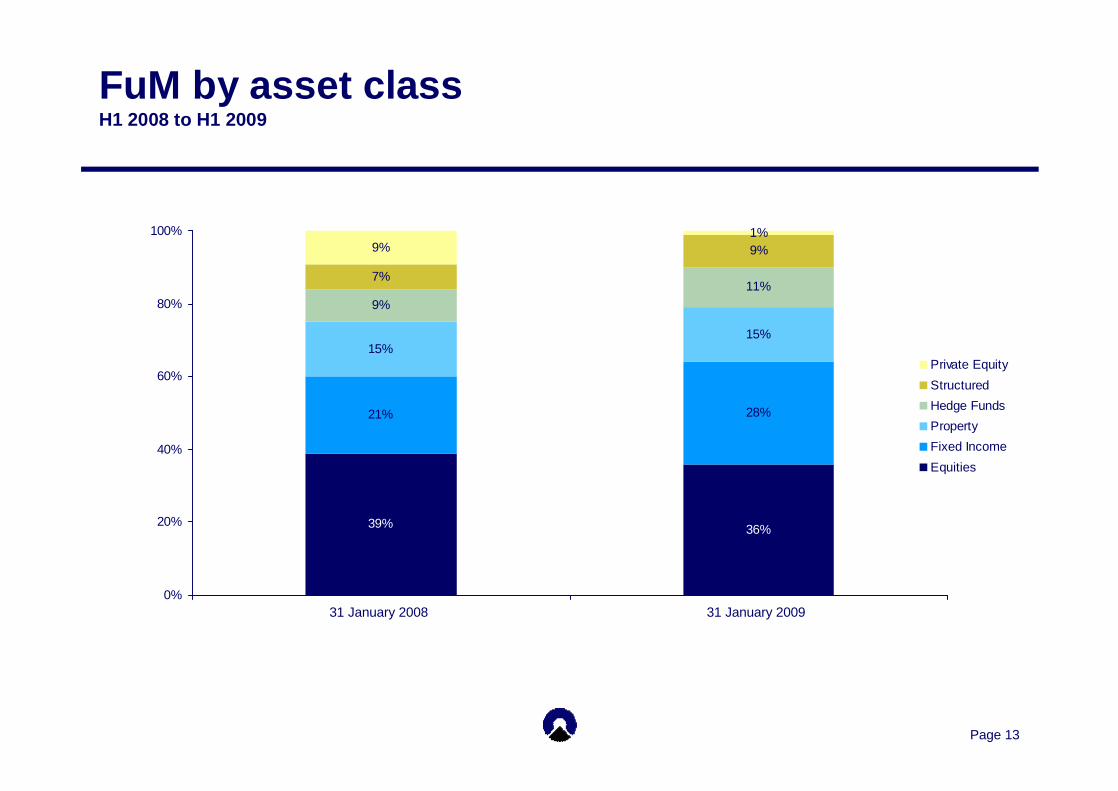

FuM by asset classH1 2008 to H1 2009

39% 36%

21% 28%

15%15%

9%11%

7%

9%9%1%

0%

20%

40%

60%

80%

100%

2008 2009

Private EquityStructuredHedge FundsPropertyFixed IncomeEquities

31 January 200931 January 2008

Page 14

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Page 15

Private Clients and FundsOverall themes

• Integration for efficiency, scalability and growth

• Primary focus on UK individual investors

• Dual channel distribution

• Secondary focus on institutions and international

• Primary focus on multi-asset “Managed Solutions”

• Secondary focus on specialist propositions

Page 16

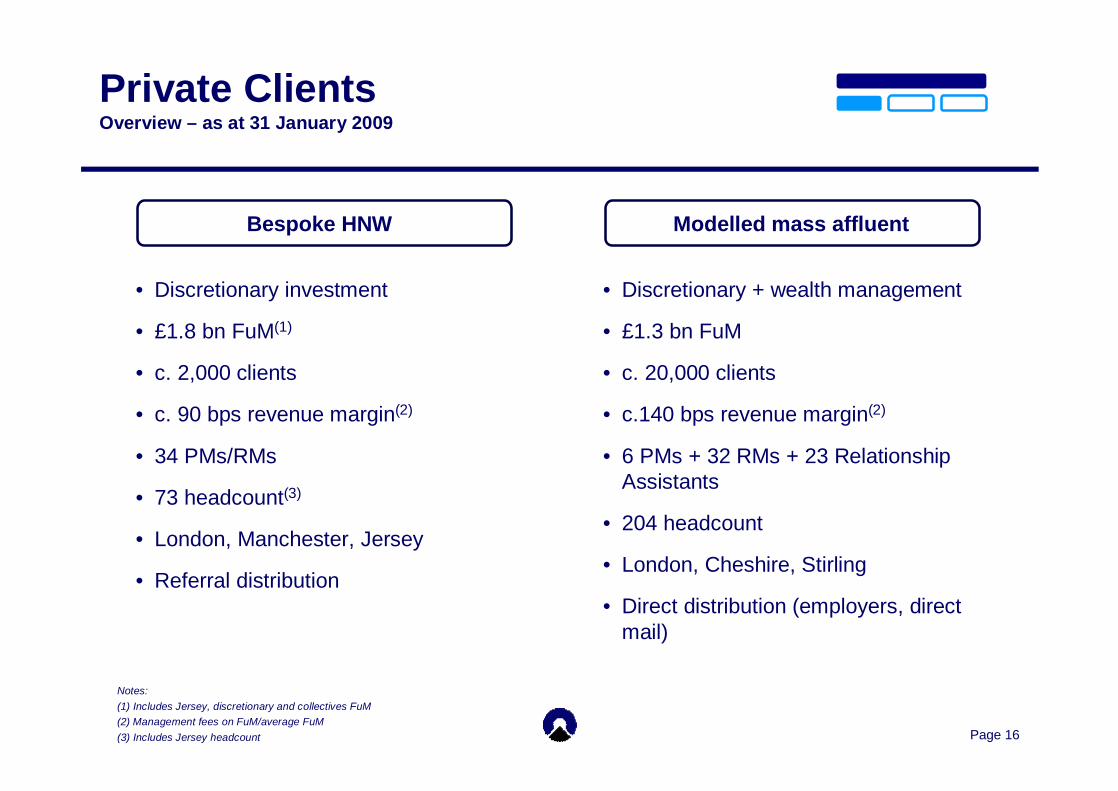

Private ClientsOverview – as at 31 January 2009

• Discretionary investment

• £1.8 bn FuM(1)

• c. 2,000 clients

• c. 90 bps revenue margin(2)

• 34 PMs/RMs

• 73 headcount(3)

• London, Manchester, Jersey

• Referral distribution

• Discretionary + wealth management

• £1.3 bn FuM

• c. 20,000 clients

• c.140 bps revenue margin(2)

• 6 PMs + 32 RMs + 23 Relationship Assistants

• 204 headcount

• London, Cheshire, Stirling

• Direct distribution (employers, direct mail)

Bespoke HNW Modelled mass affluent

Notes:(1) Includes Jersey, discretionary and collectives FuM(2) Management fees on FuM/average FuM(3) Includes Jersey headcount

Page 17

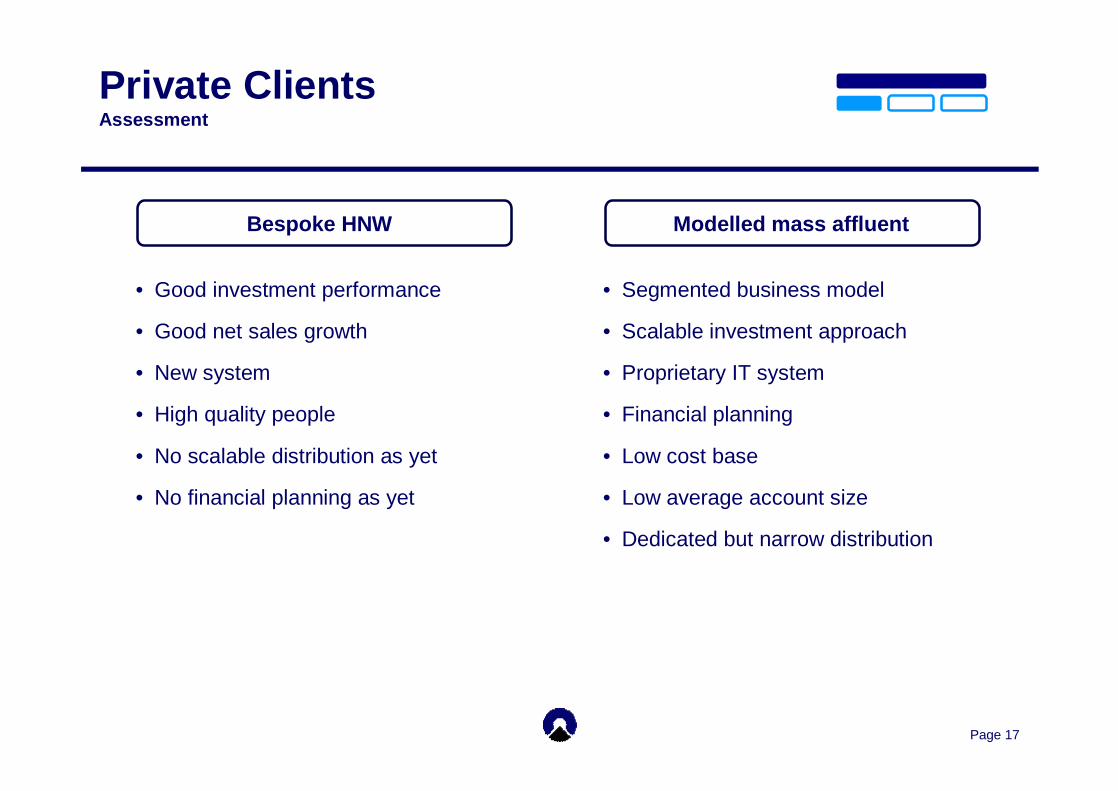

Private ClientsAssessment

• Good investment performance

• Good net sales growth

• New system

• High quality people

• No scalable distribution as yet

• No financial planning as yet

• Segmented business model

• Scalable investment approach

• Proprietary IT system

• Financial planning

• Low cost base

• Low average account size

• Dedicated but narrow distribution

Bespoke HNW Modelled mass affluent

Page 18

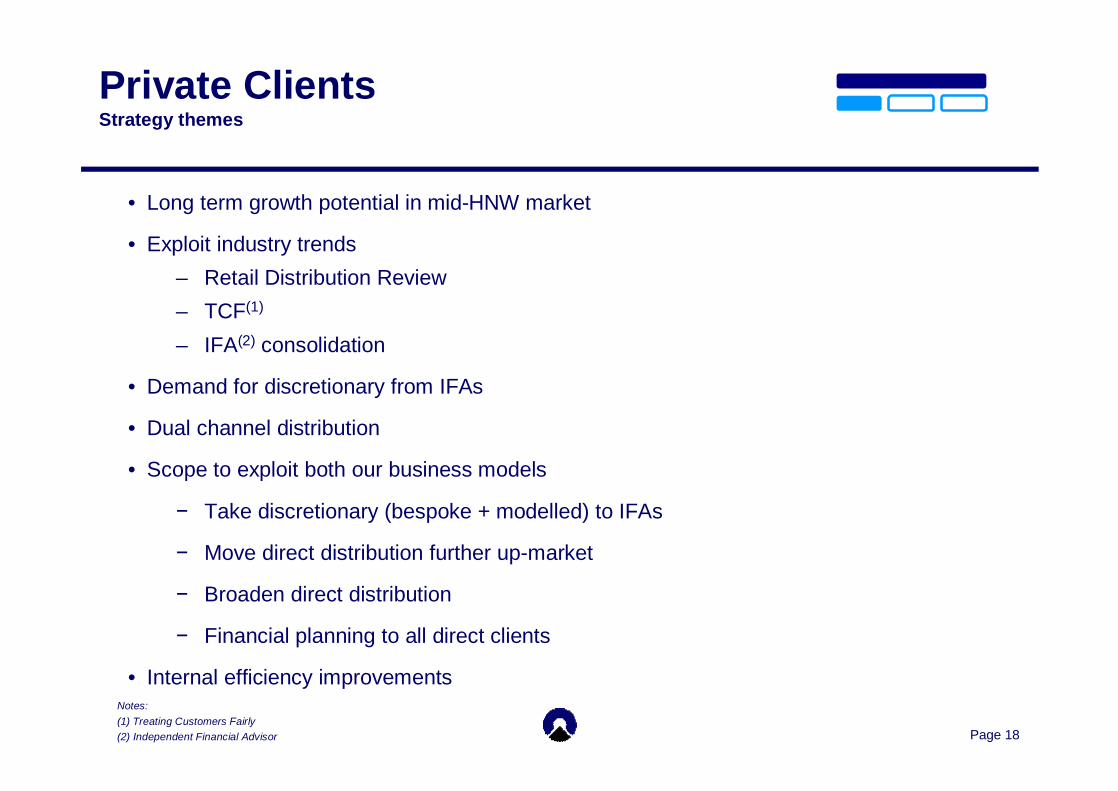

Private ClientsStrategy themes

• Long term growth potential in mid-HNW market

• Exploit industry trends– Retail Distribution Review – TCF(1)

– IFA(2) consolidation

• Demand for discretionary from IFAs

• Dual channel distribution

• Scope to exploit both our business models

− Take discretionary (bespoke + modelled) to IFAs

− Move direct distribution further up-market

− Broaden direct distribution

− Financial planning to all direct clients

• Internal efficiency improvementsNotes:(1) Treating Customers Fairly(2) Independent Financial Advisor

Page 19

Private ClientsBusiness model and Managed Solutions

Private Individuals£0.3 m – £3 m

Direct Intermediated

Close IFA

Bespoke Modelled

Discretionary Investment Propositions

Target market

Client acquisition and relationship management

Provider of advice and relationship manager

Consistent range of Managed Solutions

Page 20

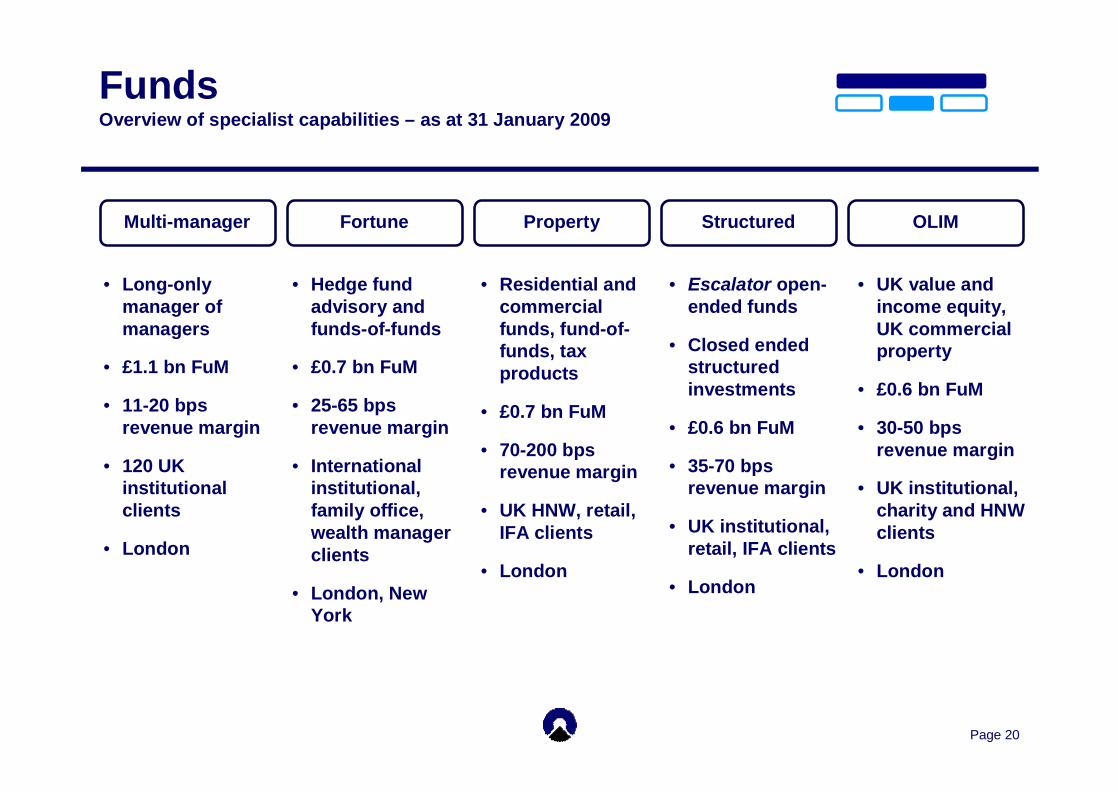

FundsOverview of specialist capabilities – as at 31 January 2009

• Long-only manager of managers

• £1.1 bn FuM

• 11-20 bps revenue margin

• 120 UK institutional clients

• London

Multi-manager

• UK value and income equity, UK commercial property

• £0.6 bn FuM

• 30-50 bps revenue margin

• UK institutional, charity and HNW clients

• London

OLIM

• Escalator open-ended funds

• Closed ended structured investments

• £0.6 bn FuM

• 35-70 bps revenue margin

• UK institutional, retail, IFA clients

• London

Structured

• Residential and commercial funds, fund-of-funds, tax products

• £0.7 bn FuM

• 70-200 bps revenue margin

• UK HNW, retail, IFA clients

• London

Property

• Hedge fund advisory and funds-of-funds

• £0.7 bn FuM

• 25-65 bps revenue margin

• International institutional, family office, wealth manager clients

• London, New York

Fortune

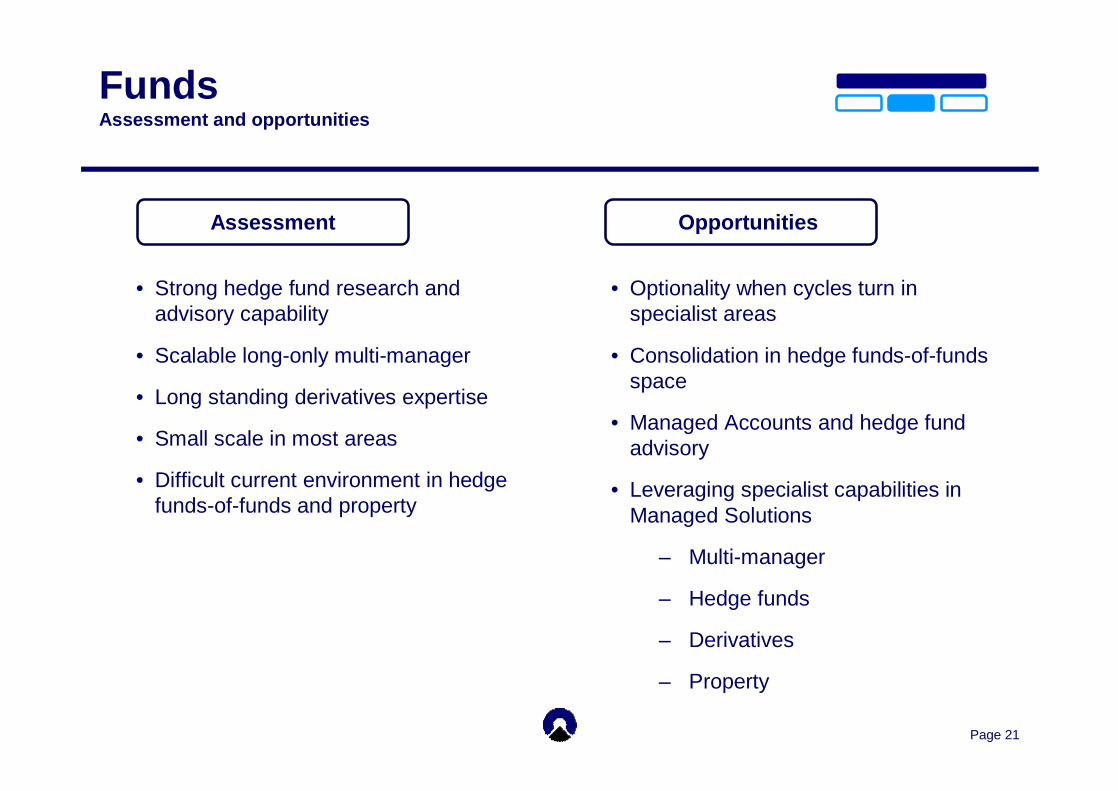

Page 21

• Strong hedge fund research and advisory capability

• Scalable long-only multi-manager

• Long standing derivatives expertise

• Small scale in most areas

• Difficult current environment in hedge funds-of-funds and property

Assessment

FundsAssessment and opportunities

• Optionality when cycles turn in specialist areas

• Consolidation in hedge funds-of-funds space

• Managed Accounts and hedge fund advisory

• Leveraging specialist capabilities in Managed Solutions

– Multi-manager

– Hedge funds

– Derivatives

– Property

Opportunities

Page 22

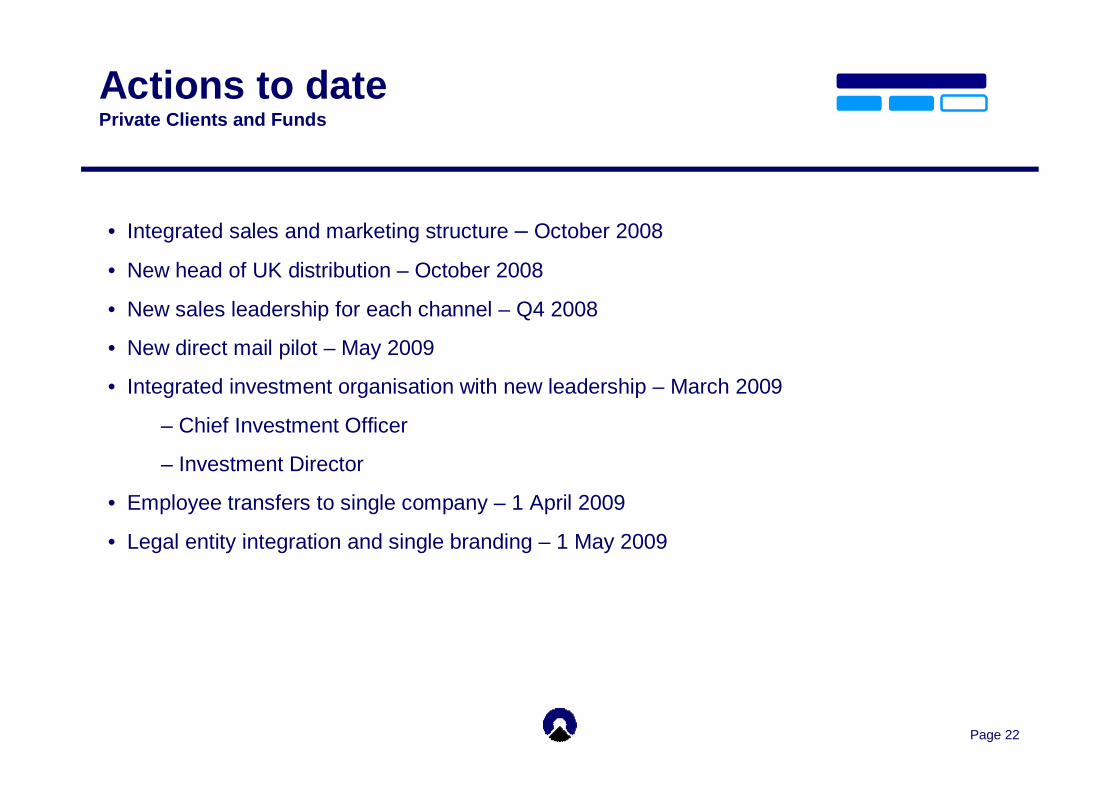

Actions to datePrivate Clients and Funds

• Integrated sales and marketing structure – October 2008

• New head of UK distribution – October 2008

• New sales leadership for each channel – Q4 2008

• New direct mail pilot – May 2009

• Integrated investment organisation with new leadership – March 2009

– Chief Investment Officer

– Investment Director

• Employee transfers to single company – 1 April 2009

• Legal entity integration and single branding – 1 May 2009

Page 23

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Page 24

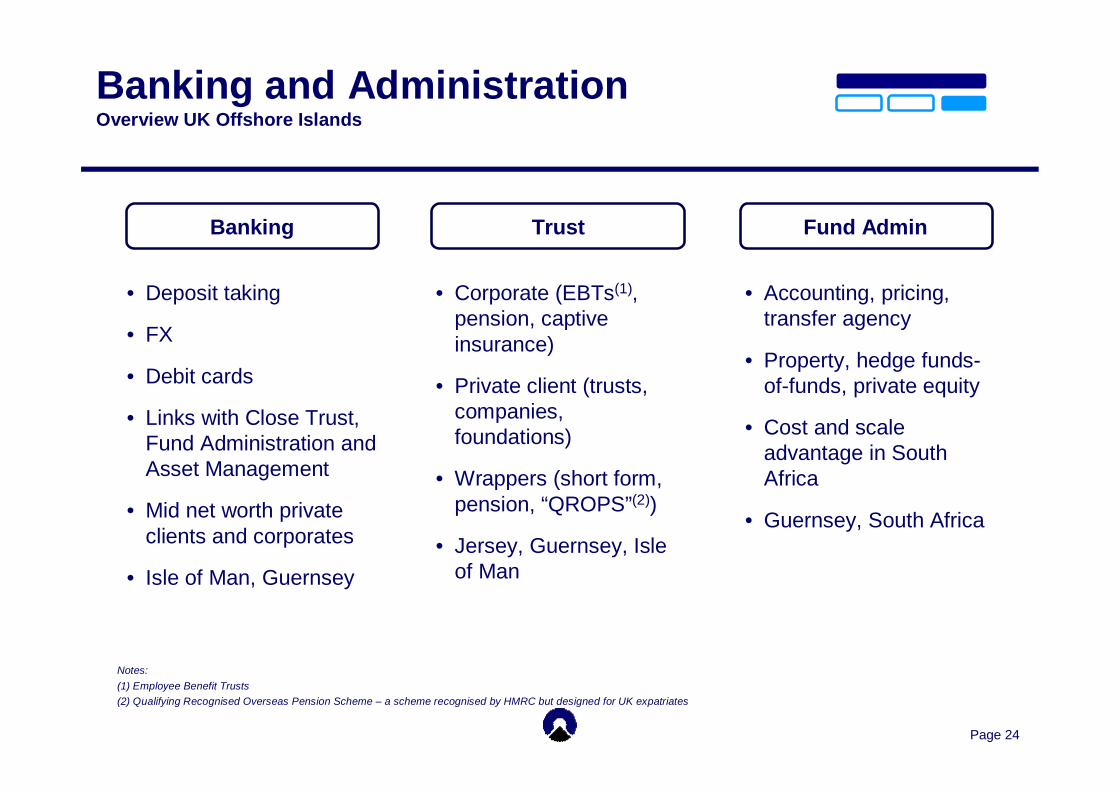

Banking and AdministrationOverview UK Offshore Islands

• Deposit taking

• FX

• Debit cards

• Links with Close Trust, Fund Administration and Asset Management

• Mid net worth private clients and corporates

• Isle of Man, Guernsey

Banking

• Accounting, pricing, transfer agency

• Property, hedge funds-of-funds, private equity

• Cost and scale advantage in South Africa

• Guernsey, South Africa

Fund Admin

• Corporate (EBTs(1), pension, captive insurance)

• Private client (trusts, companies, foundations)

• Wrappers (short form, pension, “QROPS”(2))

• Jersey, Guernsey, Isle of Man

Trust

Notes: (1) Employee Benefit Trusts(2) Qualifying Recognised Overseas Pension Scheme – a scheme recognised by HMRC but designed for UK expatriates

Page 25

Banking and AdministrationUK Offshore assessment and opportunities

• Links between businesses

• Revenue diversity

• Operational gearing in bank

• Fund administration capability in South Africa

• Uncertainty due to political rhetoric about offshore centres

• Market environment impact on fund administration

• Scalability in Trust

Assessment

• “QROPS(1)”

• “Manufacturing” in South Africa

• Fund administration consolidation

Opportunities

Note: (1) Qualifying Recognised Overseas Pension Scheme – a scheme recognised by HMRC but designed for UK expatriates

Page 26

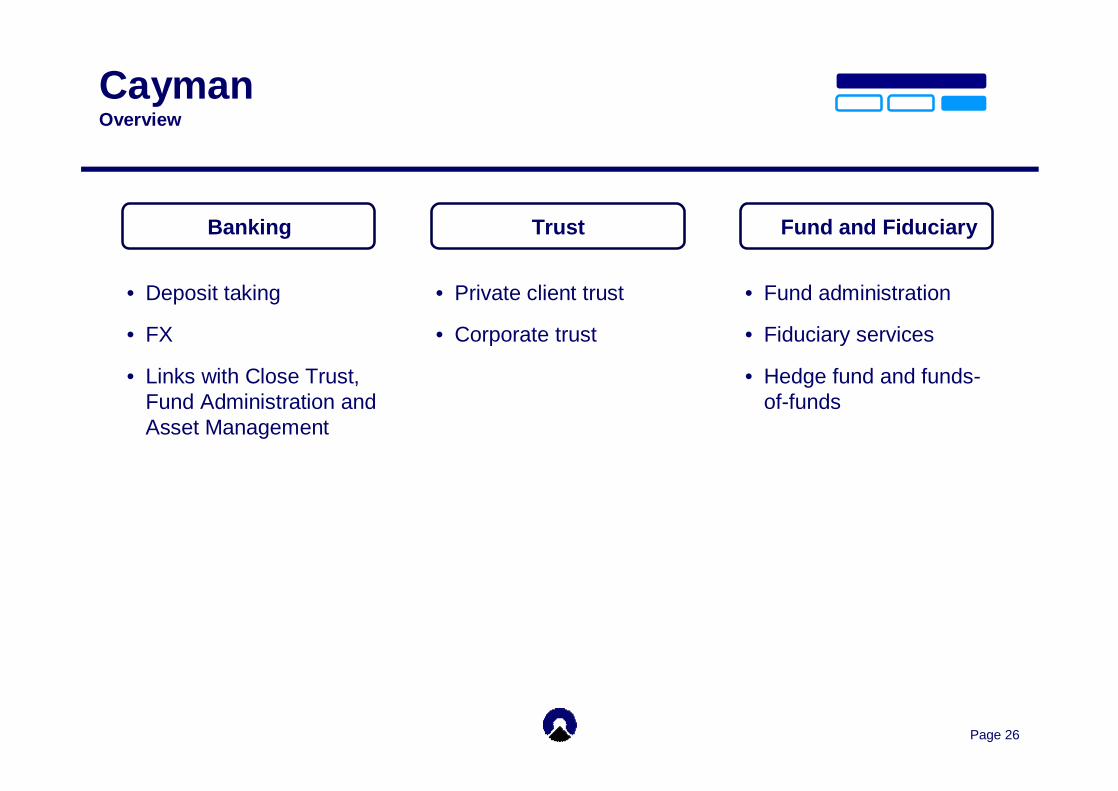

CaymanOverview

• Deposit taking

• FX

• Links with Close Trust, Fund Administration and Asset Management

Banking

• Fund administration

• Fiduciary services

• Hedge fund and funds-of-funds

Fund and Fiduciary

• Private client trust

• Corporate trust

Trust

Page 27

CaymanAssessment and opportunities

• Revenue diversity and low correlation to markets

• Acquisition record

• Uncertainty due to political rhetoric about offshore centres

• Hedge fund exposure

Assessment

• Further growth in core areas

• Latin America

Opportunities

Page 28

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Page 29

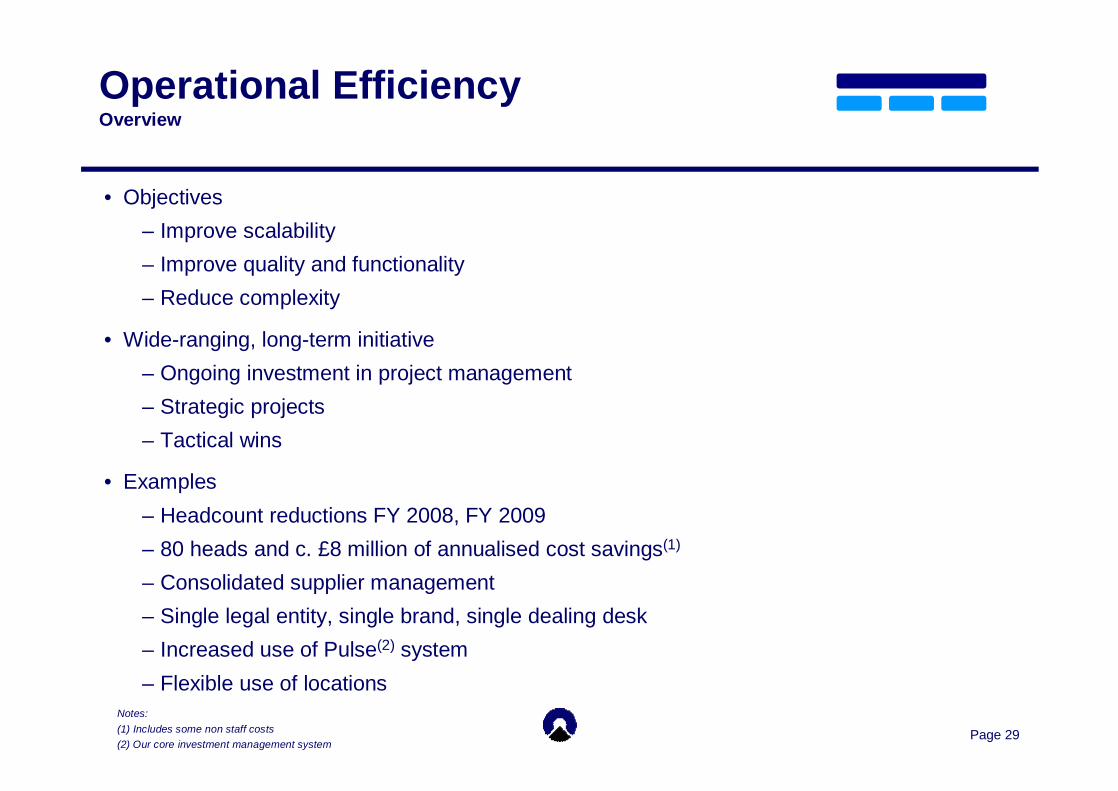

Operational EfficiencyOverview

• Objectives– Improve scalability– Improve quality and functionality– Reduce complexity

• Wide-ranging, long-term initiative– Ongoing investment in project management– Strategic projects– Tactical wins

• Examples– Headcount reductions FY 2008, FY 2009– 80 heads and c. £8 million of annualised cost savings(1)

– Consolidated supplier management– Single legal entity, single brand, single dealing desk– Increased use of Pulse(2) system– Flexible use of locations

Notes: (1) Includes some non staff costs(2) Our core investment management system

Page 30

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Page 31

Asset Management Division Summary

• 3 core areas representing blend of growth, stability and diversification

• Private Clients– Strong business position– Alignment to key changes in the industry– Scope to grow organically and inorganically

• Funds– Opportunistic development by acquisition– High-quality capabilities– Impact of current market environment– Optionality when cycle turns

• Banking and Administration– Resilient– Diversifier

Page 32

Agenda

1. Introduction – Jonathan Howell, Group Finance Director

2. Presentation on Asset Management Division – Martin Andrew, Chief Executive Asset Management

• Overview

• Private Clients and Funds

• Banking and Administration

• Operational Efficiency

• Summary

3. Q&A

Close Brothers Group

Asset Management Division

Presentation to Investors and Analysts

22 April 2009

Page 34

Appendix

• Fund performance summary

• Private client performance

• Senior management biographies

Page 35

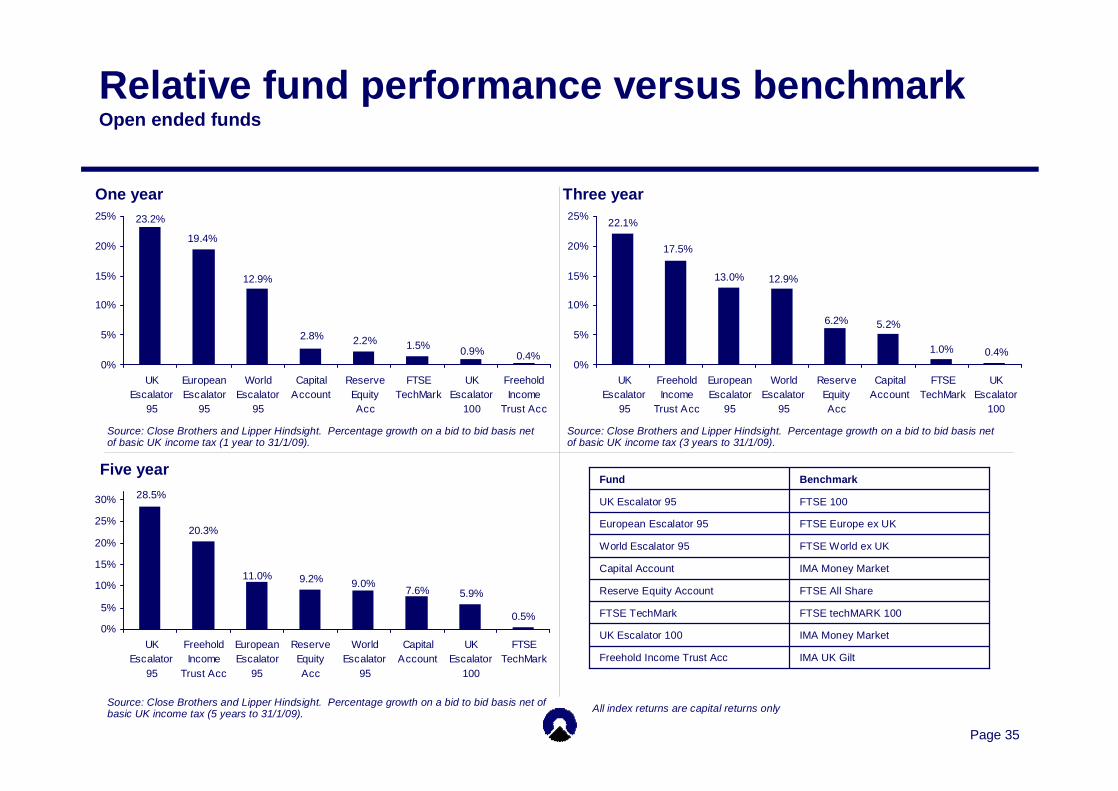

Three year

Relative fund performance versus benchmarkOpen ended funds

0.4%

2.8% 2.2% 1.5% 0.9%

12.9%

19.4%

23.2%

0%

5%

10%

15%

20%

25%

UKEscalator

95

EuropeanEscalator

95

WorldEscalator

95

CapitalAccount

ReserveEquityAcc

FTSETechMark

UKEscalator

100

FreeholdIncome

Trust Acc

0.5%

28.5%

20.3%

11.0%

5.9%7.6%9.0%9.2%

0%

5%

10%

15%

20%

25%

30%

UKEscalator

95

FreeholdIncome

Trust Acc

EuropeanEscalator

95

ReserveEquityAcc

WorldEscalator

95

CapitalAccount

UKEscalator

100

FTSETechMark

0.4%

22.1%

17.5%

13.0%

1.0%

5.2%6.2%

12.9%

0%

5%

10%

15%

20%

25%

UKEscalator

95

FreeholdIncome

Trust Acc

EuropeanEscalator

95

WorldEscalator

95

ReserveEquityAcc

CapitalAccount

FTSETechMark

UKEscalator

100

Five year

One year

Source: Close Brothers and Lipper Hindsight. Percentage growth on a bid to bid basis net of basic UK income tax (1 year to 31/1/09).

Source: Close Brothers and Lipper Hindsight. Percentage growth on a bid to bid basis net of basic UK income tax (3 years to 31/1/09).

Source: Close Brothers and Lipper Hindsight. Percentage growth on a bid to bid basis net of basic UK income tax (5 years to 31/1/09). All index returns are capital returns only

FTSE World ex UKWorld Escalator 95

FTSE Europe ex UKEuropean Escalator 95

FTSE 100UK Escalator 95

FTSE techMARK 100FTSE TechMark

FTSE All ShareReserve Equity Account

IMA UK GiltFreehold Income Trust Acc

IMA Money MarketUK Escalator 100

IMA Money MarketCapital Account

BenchmarkFund

Page 36

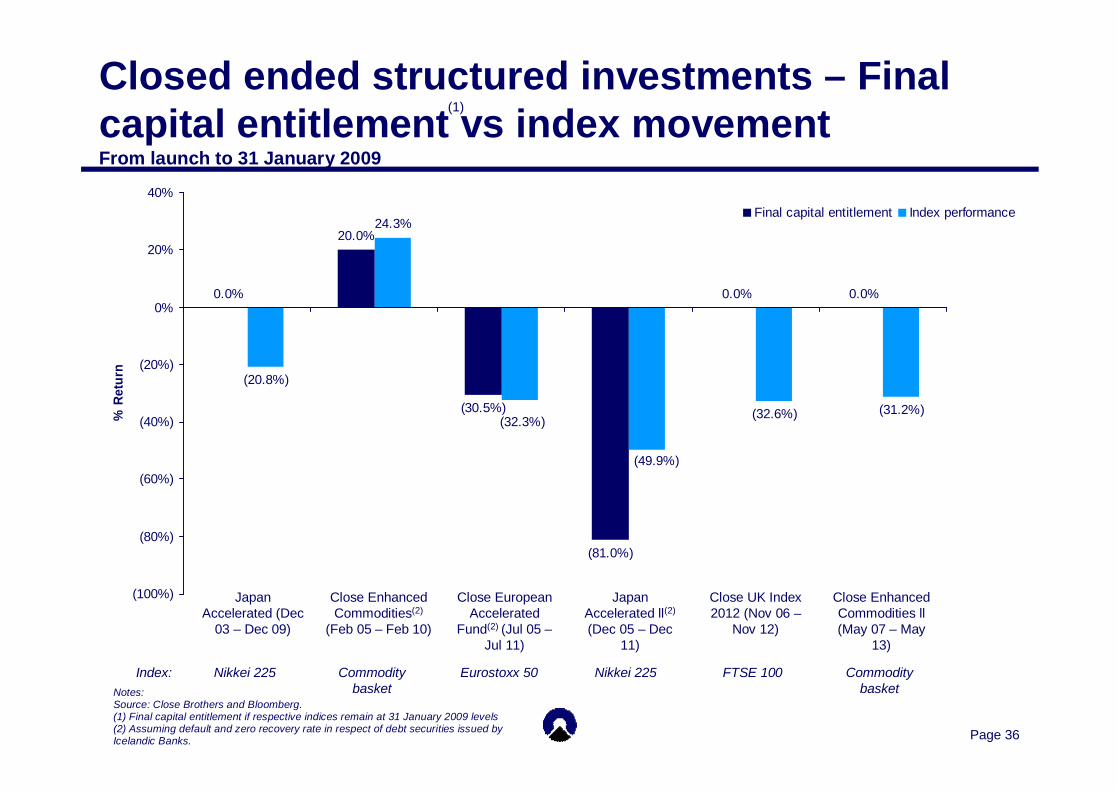

Closed ended structured investments – Final capital entitlement vs index movement From launch to 31 January 2009

0.0%

20.0%

(30.5%)

(81.0%)

0.0% 0.0%

(20.8%)

24.3%

(32.6%) (31.2%)

(49.9%)

(32.3%)

(100%)

(80%)

(60%)

(40%)

(20%)

0%

20%

40%

% R

etur

n

Final capital entitlement Index performance

Japan Accelerated ll(2)

(Dec 05 – Dec 11)

Close Enhanced Commodities ll(May 07 – May

13)

Close UK Index 2012 (Nov 06 –

Nov 12)

Close European Accelerated

Fund(2) (Jul 05 –Jul 11)

Close Enhanced Commodities(2)

(Feb 05 – Feb 10)

Japan Accelerated (Dec

03 – Dec 09)

Notes:Source: Close Brothers and Bloomberg. (1) Final capital entitlement if respective indices remain at 31 January 2009 levels(2) Assuming default and zero recovery rate in respect of debt securities issued by Icelandic Banks.

FTSE 100Eurostoxx 50 Commodity basket

Nikkei 225Commodity basket

Nikkei 225Index:

(1)

Page 37

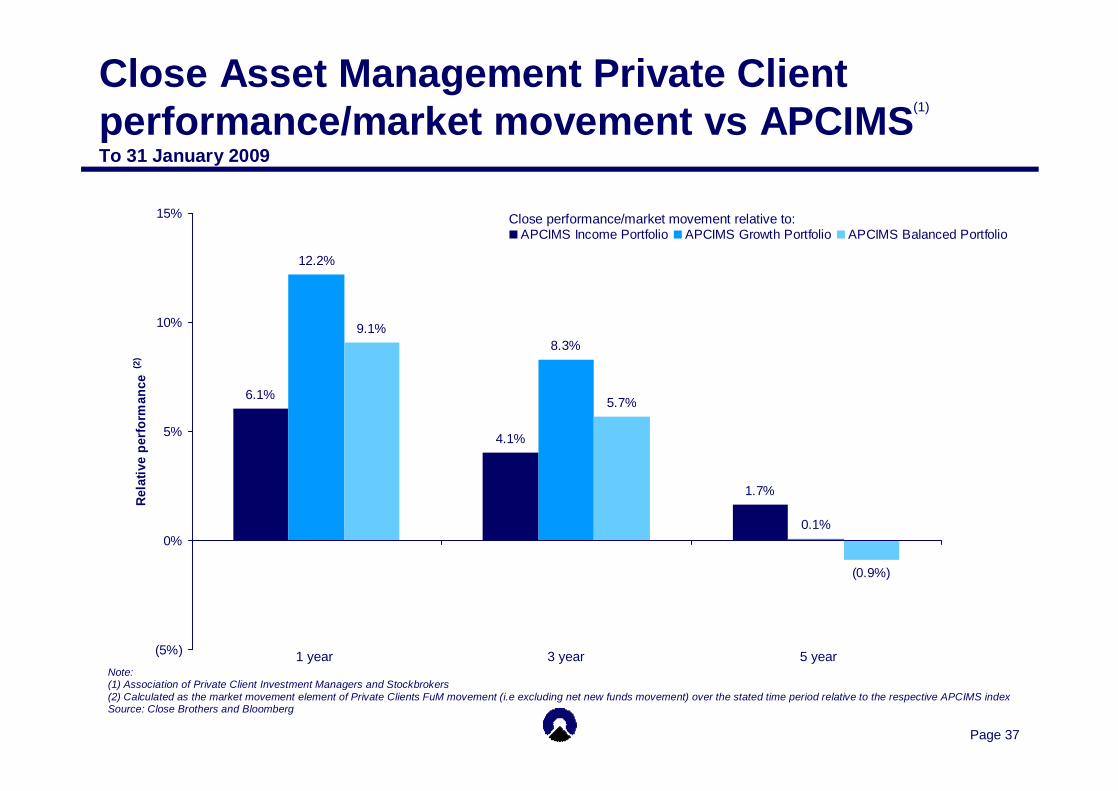

Close Asset Management Private Client performance/market movement vs APCIMS To 31 January 2009

6.1%

4.1%

1.7%

12.2%

8.3%

0.1%

9.1%

5.7%

(0.9%)

(5%)

0%

5%

10%

15%

Rela

tive

perf

orm

ance

(2)

APCIMS Income Portfolio APCIMS Growth Portfolio APCIMS Balanced Portfolio

5 year3 year1 yearNote:(1) Association of Private Client Investment Managers and Stockbrokers(2) Calculated as the market movement element of Private Clients FuM movement (i.e excluding net new funds movement) over the stated time period relative to the respective APCIMS indexSource: Close Brothers and Bloomberg

Close performance/market movement relative to:

(1)

Page 38

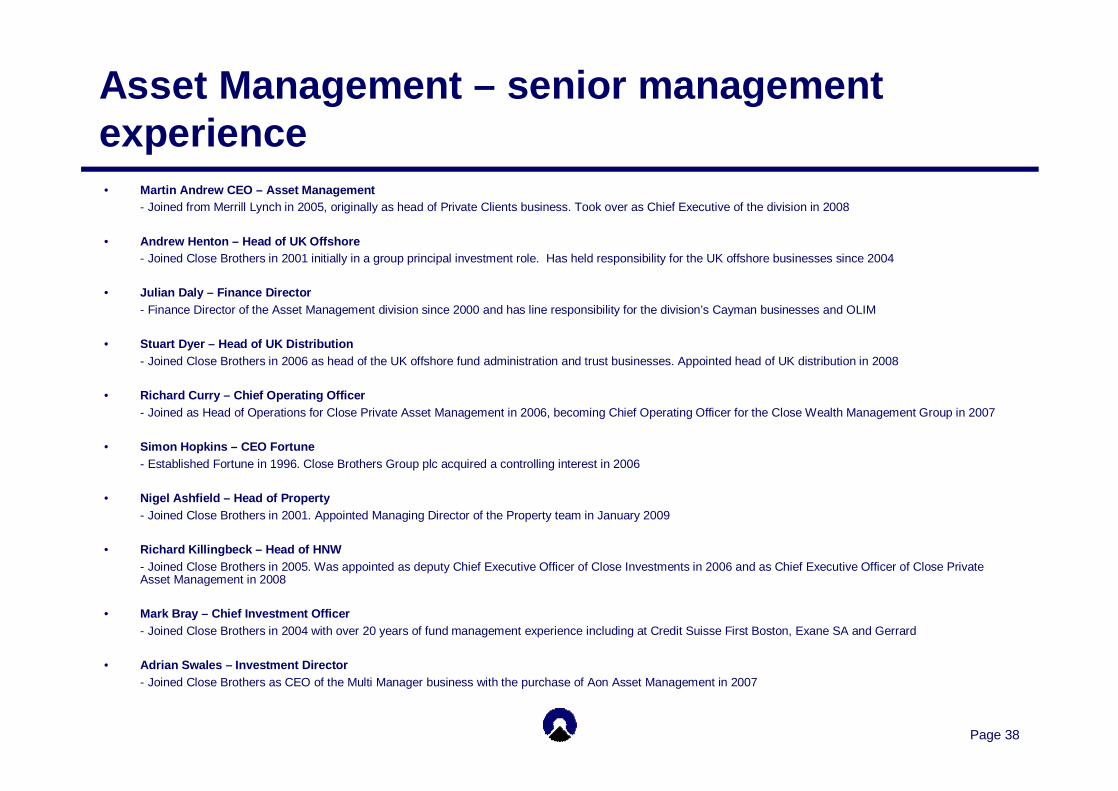

Asset Management – senior management experience• Martin Andrew CEO – Asset Management

- Joined from Merrill Lynch in 2005, originally as head of Private Clients business. Took over as Chief Executive of the division in 2008

• Andrew Henton – Head of UK Offshore- Joined Close Brothers in 2001 initially in a group principal investment role. Has held responsibility for the UK offshore businesses since 2004

• Julian Daly – Finance Director- Finance Director of the Asset Management division since 2000 and has line responsibility for the division’s Cayman businesses and OLIM

• Stuart Dyer – Head of UK Distribution- Joined Close Brothers in 2006 as head of the UK offshore fund administration and trust businesses. Appointed head of UK distribution in 2008

• Richard Curry – Chief Operating Officer- Joined as Head of Operations for Close Private Asset Management in 2006, becoming Chief Operating Officer for the Close Wealth Management Group in 2007

• Simon Hopkins – CEO Fortune- Established Fortune in 1996. Close Brothers Group plc acquired a controlling interest in 2006

• Nigel Ashfield – Head of Property- Joined Close Brothers in 2001. Appointed Managing Director of the Property team in January 2009

• Richard Killingbeck – Head of HNW- Joined Close Brothers in 2005. Was appointed as deputy Chief Executive Officer of Close Investments in 2006 and as Chief Executive Officer of Close Private Asset Management in 2008

• Mark Bray – Chief Investment Officer- Joined Close Brothers in 2004 with over 20 years of fund management experience including at Credit Suisse First Boston, Exane SA and Gerrard

• Adrian Swales – Investment Director- Joined Close Brothers as CEO of the Multi Manager business with the purchase of Aon Asset Management in 2007

Related Documents

![Untitled-1 [] news.pdf · bola voli futsal tenis meia kangmas & mbakyu pan brothers kangmas mbakyu pt. pan brothers group 2016 . pan brothers group olympic games 2016 pt. pan brothers](https://static.cupdf.com/doc/110x72/5a912f167f8b9af27f8e34c9/untitled-1-newspdfbola-voli-futsal-tenis-meia-kangmas-mbakyu-pan-brothers-kangmas.jpg)