Asia-Pacific Oil & Gas January 23, 2013 Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741 Michael W. Parker (Senior Analyst) • [email protected] • +852-2918-5747 Mike Werner (Senior Analyst) • [email protected] • +852-2918-5748 Vanessa Lau (Senior Analyst) • [email protected] • +852-2918-5717 Lu Wang • [email protected] • +852-2918-5723 Ying Lou • [email protected] • +852-2918-5743 Hua Cheng • [email protected] • +852-2918-5721 Will Feng • [email protected] • +852-2918-5730 See Disclosure Appendix of this report for important disclosures and analyst certifications. China Economic & Energy Indicators - December 2012; Dragon Year Ends on a High as Energy Demand Heats Up Please see the Disclosure Appendix for the ratings and price targets of the companies covered in this report. Highlights ∑ 2012 ended with a strong finish despite a weak start. Real GDP growth in 4Q12 improved to 7.9%. Industrial production growth in December accelerated to 10.3%. Both refinery throughput and apparent oil demand surged to all time highs. Electricity production rebounded with 7.2% y-o-y growth in December. Gas demand remained strong with 10% y-o-y growth in November. Latest energy indicators continue to affirm China is on the road to economic recovery. ∑ Year-over-year real GDP growth for Q4 2012 came in at 7.9%, a 50bp improvement from the 7.4% growth reported in Q3 and 10bp above the market expectations of 7.8%. This represents the first time China's economic growth accelerated after 7 consecutive quarters of deceleration. December Industrial production growth improved 20bp m-o-m to 10.3% while the PMI figure was flat at 50.6, supporting the economic rebound in China as we enter 2013. ∑ The December headline loan growth figure came in at RMB 454 billion, 17% below market expectations. This marked the weakest month of loan growth since December 2009. Despite this, total credit formation (total bank loans and non-bank financing) was robust at RMB 1.61 trillion in December, 25% higher than year-to-date average as the issuance of corporate debt and trust loans remained strong. ∑ For December, China's CPI inflation figure (at 2.5%) increased sequentially by 50bp which was more driven by an increase in food price (+4.2%) while the non-food portion of the inflation (at 1.7%) stayed below 2.0% for the 13th consecutive month. Meanwhile, December PPI inflation was up 30bp m- o-m to -1.9%. This marks the third consecutive m-o-m increase to the nation's PPI inflation figure after declining the previous 14 months. ∑ Apparent oil demand surged by 9.1% y-o-y to an all time high of 44.8MT as Chinese refining throughput reached a new high in December. Apparent oil demand averaged 9.67Mbpd in 2012, which was up 4.0% y-o-y. We expect Chinese apparent oil demand will accelerate by 6% y-o-y to 10.3Mbpd, which is 0.3Mbpd higher than current IEA estimates (9.98Mbpd). Crude production improved by 5.6% y-o-y to 17.9MT in December on CNOOC's expanding offshore production and Penglai ramp up. Crude imports increased 8.0% y-o-y to 23.7MT. ∑ Natural gas demand in November increased by 10.2% y-o-y as demand from heating accelerates in winter. Gas imports accounted for 28% of gas demand. Pipeline gas imports from Central Asia increased by 0.34bcf/d (15% m-o-m) to 2.57bcf/d, offsetting LNG imports decrease as spot LNG markets tightened in winter. Natural gas production increased by 8.2% y-o-y to 11.5bcf/d in November. ∑ Electricity production in December was 432.7TWh, up 7.2% Y-o-Y and up 7.9% sequentially from November. The Y-o-Y power generation growth in December 2011 was 9.8%. Power production in 2012 was 4,771TWh up 4.2% Y-o-Y. This is the lowest annual production growth since 2005. ∑ Qinhuangdao spot coal price (5,500kcal/kg) has decreased by RMB15/ton to RMB620/ton since the end of November. Coal prices turned with the end of winter restocking at the end of October. We For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

Michael W. Parker (Senior Analyst) • [email protected] • +852-2918-5747

Mike Werner (Senior Analyst) • [email protected] • +852-2918-5748

Vanessa Lau (Senior Analyst) • [email protected] • +852-2918-5717

Lu Wang • [email protected] • +852-2918-5723

Ying Lou • [email protected] • +852-2918-5743

Hua Cheng • [email protected] • +852-2918-5721

Will Feng • [email protected] • +852-2918-5730

See Disclosure Appendix of this report for important disclosures and analyst certifications.

China Economic & Energy Indicators - December 2012; Dragon Year Ends on a High as Energy Demand Heats Up

Please see the Disclosure Appendix for the ratings and price targets of the companies covered in this report.

Highlights

∑ 2012 ended with a strong finish despite a weak start. Real GDP growth in 4Q12 improved to 7.9%. Industrial production growth in December accelerated to 10.3%. Both refinery throughput and apparent oil demand surged to all time highs. Electricity production rebounded with 7.2% y-o-y growth in December. Gas demand remained strong with 10% y-o-y growth in November. Latest energy indicators continue to affirm China is on the road to economic recovery.

∑ Year-over-year real GDP growth for Q4 2012 came in at 7.9%, a 50bp improvement from the 7.4% growth reported in Q3 and 10bp above the market expectations of 7.8%. This represents the first time China's economic growth accelerated after 7 consecutive quarters of deceleration. December Industrial production growth improved 20bp m-o-m to 10.3% while the PMI figure was flat at 50.6, supporting the economic rebound in China as we enter 2013.

∑ The December headline loan growth figure came in at RMB 454 billion, 17% below market expectations. This marked the weakest month of loan growth since December 2009. Despite this, total credit formation (total bank loans and non-bank financing) was robust at RMB 1.61 trillion in December, 25% higher than year-to-date average as the issuance of corporate debt and trust loans remained strong.

∑ For December, China's CPI inflation figure (at 2.5%) increased sequentially by 50bp which was more driven by an increase in food price (+4.2%) while the non-food portion of the inflation (at 1.7%) stayed below 2.0% for the 13th consecutive month. Meanwhile, December PPI inflation was up 30bp m-o-m to -1.9%. This marks the third consecutive m-o-m increase to the nation's PPI inflation figure after declining the previous 14 months.

∑ Apparent oil demand surged by 9.1% y-o-y to an all time high of 44.8MT as Chinese refining throughput reached a new high in December. Apparent oil demand averaged 9.67Mbpd in 2012, which was up 4.0% y-o-y. We expect Chinese apparent oil demand will accelerate by 6% y-o-y to 10.3Mbpd, which is 0.3Mbpd higher than current IEA estimates (9.98Mbpd). Crude production improved by 5.6% y-o-y to 17.9MT in December on CNOOC's expanding offshore production and Penglai ramp up. Crude imports increased 8.0% y-o-y to 23.7MT.

∑ Natural gas demand in November increased by 10.2% y-o-y as demand from heating accelerates in winter. Gas imports accounted for 28% of gas demand. Pipeline gas imports from Central Asia increased by 0.34bcf/d (15% m-o-m) to 2.57bcf/d, offsetting LNG imports decrease as spot LNG markets tightened in winter. Natural gas production increased by 8.2% y-o-y to 11.5bcf/d in November.

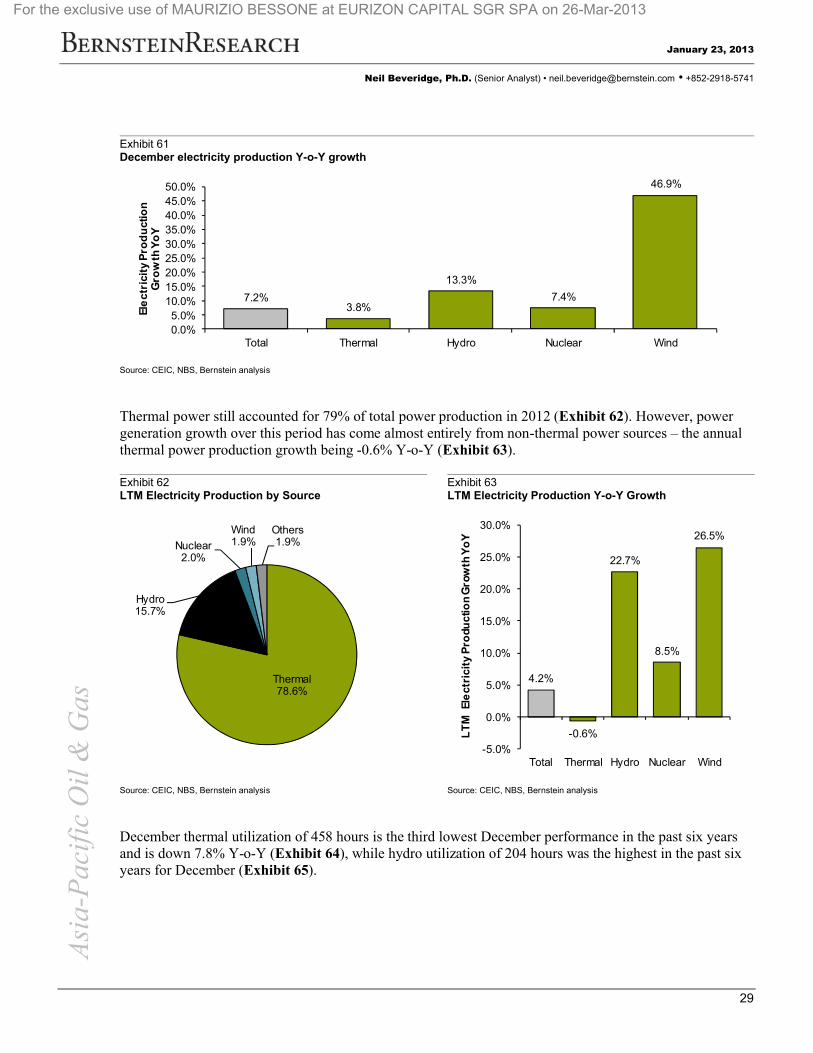

∑ Electricity production in December was 432.7TWh, up 7.2% Y-o-Y and up 7.9% sequentially from November. The Y-o-Y power generation growth in December 2011 was 9.8%. Power production in 2012 was 4,771TWh up 4.2% Y-o-Y. This is the lowest annual production growth since 2005.

∑ Qinhuangdao spot coal price (5,500kcal/kg) has decreased by RMB15/ton to RMB620/ton since the end of November. Coal prices turned with the end of winter restocking at the end of October. We

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

2

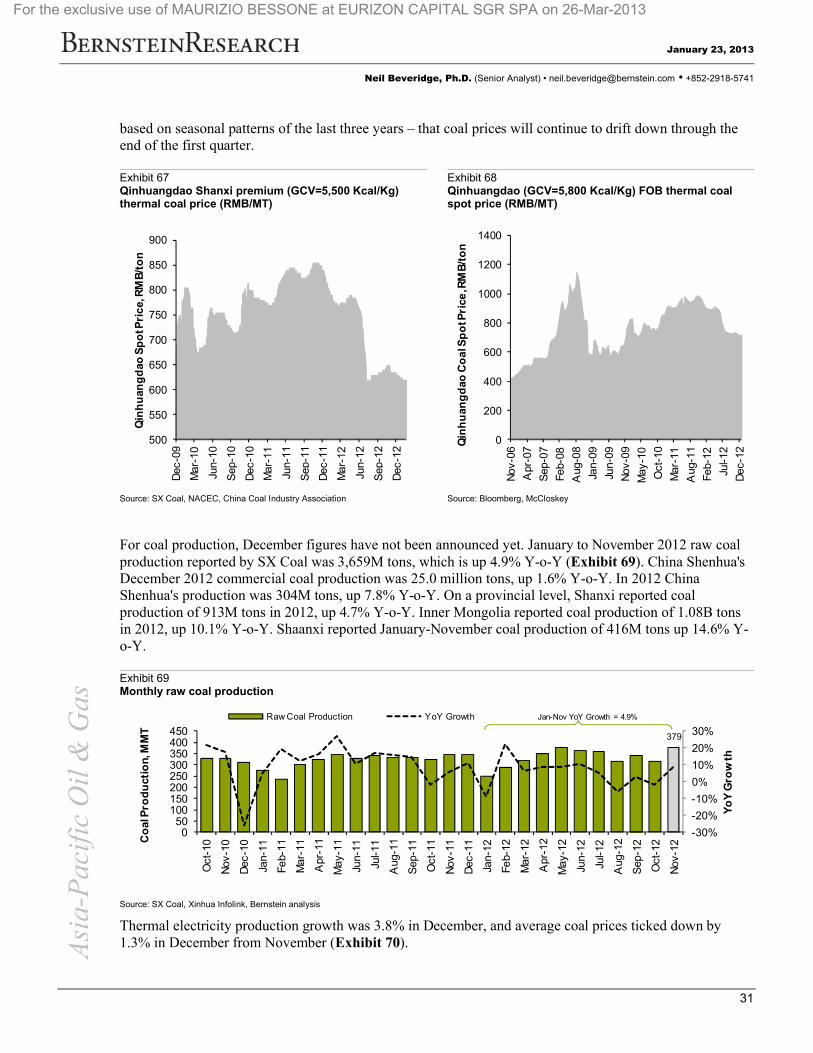

anticipate – based on seasonal patterns of the last three years – that coal prices will continue to drift down through the end of the first quarter. Coal price is down 26% since last December. The average coal price was RMB699/ton in 2012 down 15% from RMB821/ton in 2011. The coal price was down 24% for the fourth quarter Y-o-Y.

∑ Crude steel production in December was 59.5 million tons, up 14% YoY due to low production in December 2011. 2012 full year saw crude steel production of ~711 million tons i.e. 3.8% growth, only slightly higher than the 2.1% seen in 2008 when the financial crisis hit. Steel prices saw a moderate rebound from mid-September, with China HRC spot price ending the year at RMB3,974 per ton. Despite the rise, this is still 6% lower than the price at the start of 2012.

∑ Aluminum LME price saw a rebound in mid-November, ending the year at US$2,040 per ton, close to where the year started. Alumina price was less volatile than LME price, and only saw a moderate increase to US$331 per ton, averaging at 15.9% of LME price for 2012, which is above what we would see as the more "normal" range of 13-15%.

∑ Within China's energy sector, gas distributors, power companies and oil services outperformed regional index over the last 12 months while steel and coal companies underperformed. Natural gas continues to be the fastest growing component of China's energy complex. With slower electricity growth resulting in lower coal prices, power producers continue to outperform over coal names.

Investment Conclusion

The economic recovery which started in September 2012 continued to gather pace in December. Total energy consumption growth in 4Q reached 7.4%, the highest reading since 1Q12 while GDP growth rebounded to 7.9%. Sectors with a high beta to a recovery in China growth such as steel, cement, refining and petrochemicals are all benefiting from the turnaround in growth in the near term. While China oil demand exceeded 10Mbpd in 4Q12 for the first time ever, strong non-OPEC production continues to put a cap on oil prices which is limiting the benefit to integrated oils and E&Ps. The key question remains how sustainable this recovery will prove. While most expect positive momentum in the first half of 2013, there remains uncertainty beyond this. Policy announcements over the coming months as the new government takes shape could set the tone for how the rest of 2013 pans out.

Our top picks within Chinese energy sector are Huaneng (902.HK; TP HK$8.0) and CR Power (836.HK, TP HK$20.0), Sinopec (386.HK; TP HK$10.0) and CNOOC (883.HK; TP HK$21.7) which we rate as outperform.

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

3

Details

In this note, we review energy and economic statistics published for December 2012, which highlights recent trends in the economic and energy data in China.

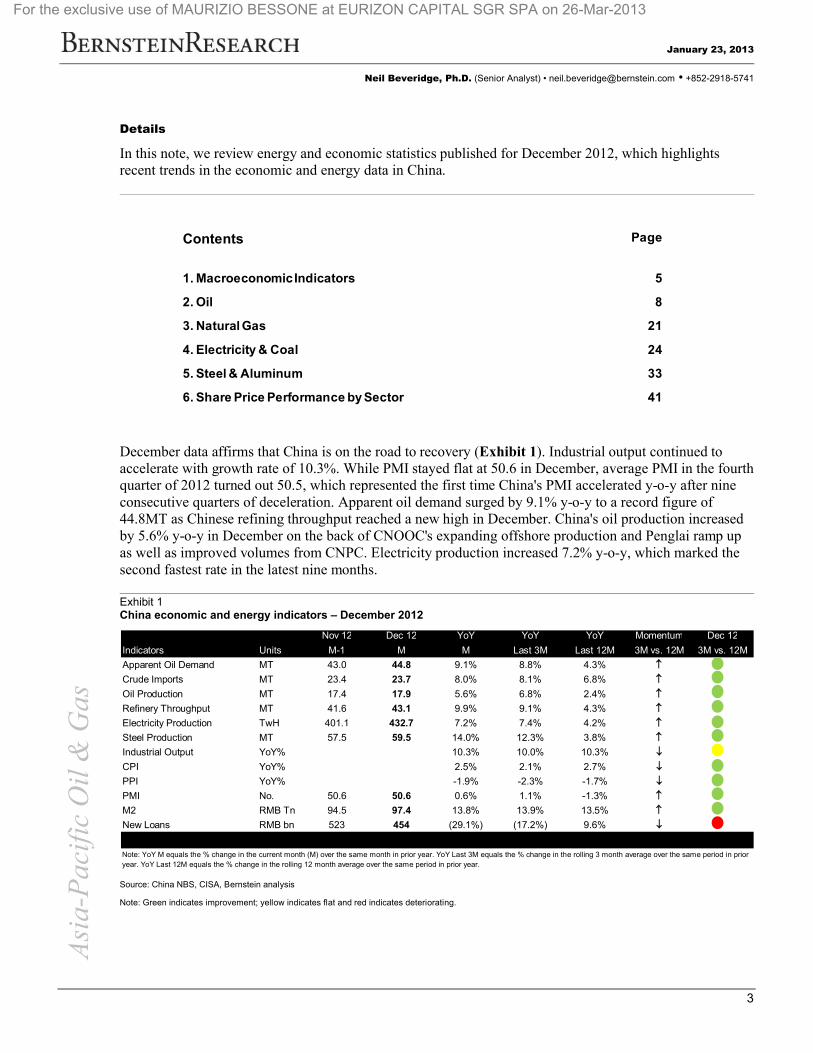

December data affirms that China is on the road to recovery (Exhibit 1). Industrial output continued to accelerate with growth rate of 10.3%. While PMI stayed flat at 50.6 in December, average PMI in the fourth quarter of 2012 turned out 50.5, which represented the first time China's PMI accelerated y-o-y after nineconsecutive quarters of deceleration. Apparent oil demand surged by 9.1% y-o-y to a record figure of 44.8MT as Chinese refining throughput reached a new high in December. China's oil production increased by 5.6% y-o-y in December on the back of CNOOC's expanding offshore production and Penglai ramp upas well as improved volumes from CNPC. Electricity production increased 7.2% y-o-y, which marked the second fastest rate in the latest nine months.

Exhibit 1China economic and energy indicators – December 2012

Source: China NBS, CISA, Bernstein analysis

Note: Green indicates improvement; yellow indicates flat and red indicates deteriorating.

Contents Page

1. Macroeconomic Indicators 5

2. Oil 8

3. Natural Gas 21

4. Electricity & Coal 24

5. Steel & Aluminum 33

6. Share Price Performance by Sector 41

Nov 12 Dec 12 YoY YoY YoY Momentum Dec 12

Indicators Units M-1 M M Last 3M Last 12M 3M vs. 12M 3M vs. 12M

Apparent Oil Demand MT 43.0 44.8 9.1% 8.8% 4.3% ≠Crude Imports MT 23.4 23.7 8.0% 8.1% 6.8% ≠Oil Production MT 17.4 17.9 5.6% 6.8% 2.4% ≠Refinery Throughput MT 41.6 43.1 9.9% 9.1% 4.3% ≠Electricity Production TwH 401.1 432.7 7.2% 7.4% 4.2% ≠Steel Production MT 57.5 59.5 14.0% 12.3% 3.8% ≠Industrial Output YoY% 10.3% 10.0% 10.3% ØCPI YoY% 2.5% 2.1% 2.7% ØPPI YoY% -1.9% -2.3% -1.7% ØPMI No. 50.6 50.6 0.6% 1.1% -1.3% ≠M2 RMB Tn 94.5 97.4 13.8% 13.9% 13.5% ≠New Loans RMB bn 523 454 (29.1%) (17.2%) 9.6% Ø

Note: YoY M equals the % change in the current month (M) over the same month in prior year. YoY Last 3M equals the % change in the rolling 3 month average over the same period in prior year. YoY Last 12M equals the % change in the rolling 12 month average over the same period in prior year.

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

4

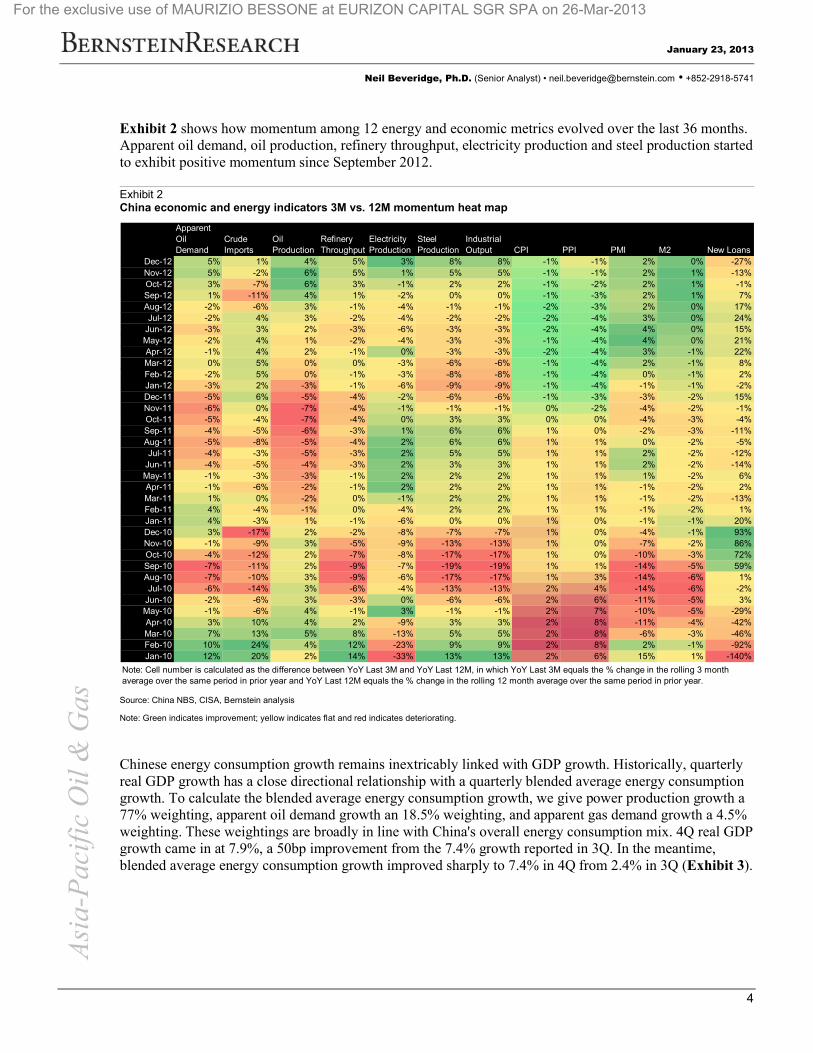

Exhibit 2 shows how momentum among 12 energy and economic metrics evolved over the last 36 months. Apparent oil demand, oil production, refinery throughput, electricity production and steel production started to exhibit positive momentum since September 2012.

Exhibit 2China economic and energy indicators 3M vs. 12M momentum heat map

Source: China NBS, CISA, Bernstein analysis

Note: Green indicates improvement; yellow indicates flat and red indicates deteriorating.

Chinese energy consumption growth remains inextricably linked with GDP growth. Historically, quarterly real GDP growth has a close directional relationship with a quarterly blended average energy consumption growth. To calculate the blended average energy consumption growth, we give power production growth a 77% weighting, apparent oil demand growth an 18.5% weighting, and apparent gas demand growth a 4.5% weighting. These weightings are broadly in line with China's overall energy consumption mix. 4Q real GDP growth came in at 7.9%, a 50bp improvement from the 7.4% growth reported in 3Q. In the meantime, blended average energy consumption growth improved sharply to 7.4% in 4Q from 2.4% in 3Q (Exhibit 3).

Apparent Oil Demand

Crude Imports

Oil Production

Refinery Throughput

Electricity Production

Steel Production

Industrial Output CPI PPI PMI M2 New Loans

Dec-12 5% 1% 4% 5% 3% 8% 8% -1% -1% 2% 0% -27%Nov-12 5% -2% 6% 5% 1% 5% 5% -1% -1% 2% 1% -13%Oct-12 3% -7% 6% 3% -1% 2% 2% -1% -2% 2% 1% -1%Sep-12 1% -11% 4% 1% -2% 0% 0% -1% -3% 2% 1% 7%Aug-12 -2% -6% 3% -1% -4% -1% -1% -2% -3% 2% 0% 17%Jul-12 -2% 4% 3% -2% -4% -2% -2% -2% -4% 3% 0% 24%

Jun-12 -3% 3% 2% -3% -6% -3% -3% -2% -4% 4% 0% 15%May-12 -2% 4% 1% -2% -4% -3% -3% -1% -4% 4% 0% 21%Apr-12 -1% 4% 2% -1% 0% -3% -3% -2% -4% 3% -1% 22%Mar-12 0% 5% 0% 0% -3% -6% -6% -1% -4% 2% -1% 8%Feb-12 -2% 5% 0% -1% -3% -8% -8% -1% -4% 0% -1% 2%Jan-12 -3% 2% -3% -1% -6% -9% -9% -1% -4% -1% -1% -2%Dec-11 -5% 6% -5% -4% -2% -6% -6% -1% -3% -3% -2% 15%Nov-11 -6% 0% -7% -4% -1% -1% -1% 0% -2% -4% -2% -1%Oct-11 -5% -4% -7% -4% 0% 3% 3% 0% 0% -4% -3% -4%Sep-11 -4% -5% -6% -3% 1% 6% 6% 1% 0% -2% -3% -11%Aug-11 -5% -8% -5% -4% 2% 6% 6% 1% 1% 0% -2% -5%Jul-11 -4% -3% -5% -3% 2% 5% 5% 1% 1% 2% -2% -12%

Jun-11 -4% -5% -4% -3% 2% 3% 3% 1% 1% 2% -2% -14%May-11 -1% -3% -3% -1% 2% 2% 2% 1% 1% 1% -2% 6%Apr-11 -1% -6% -2% -1% 2% 2% 2% 1% 1% -1% -2% 2%Mar-11 1% 0% -2% 0% -1% 2% 2% 1% 1% -1% -2% -13%Feb-11 4% -4% -1% 0% -4% 2% 2% 1% 1% -1% -2% 1%Jan-11 4% -3% 1% -1% -6% 0% 0% 1% 0% -1% -1% 20%Dec-10 3% -17% 2% -2% -8% -7% -7% 1% 0% -4% -1% 93%Nov-10 -1% -9% 3% -5% -9% -13% -13% 1% 0% -7% -2% 86%Oct-10 -4% -12% 2% -7% -8% -17% -17% 1% 0% -10% -3% 72%Sep-10 -7% -11% 2% -9% -7% -19% -19% 1% 1% -14% -5% 59%Aug-10 -7% -10% 3% -9% -6% -17% -17% 1% 3% -14% -6% 1%Jul-10 -6% -14% 3% -6% -4% -13% -13% 2% 4% -14% -6% -2%

Jun-10 -2% -6% 3% -3% 0% -6% -6% 2% 6% -11% -5% 3%May-10 -1% -6% 4% -1% 3% -1% -1% 2% 7% -10% -5% -29%Apr-10 3% 10% 4% 2% -9% 3% 3% 2% 8% -11% -4% -42%Mar-10 7% 13% 5% 8% -13% 5% 5% 2% 8% -6% -3% -46%Feb-10 10% 24% 4% 12% -23% 9% 9% 2% 8% 2% -1% -92%Jan-10 12% 20% 2% 14% -33% 13% 13% 2% 6% 15% 1% -140%

Note: Cell number is calculated as the difference between YoY Last 3M and YoY Last 12M, in which YoY Last 3M equals the % change in the rolling 3 month average over the same period in prior year and YoY Last 12M equals the % change in the rolling 12 month average over the same period in prior year.

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

5

Exhibit 3China energy consumption growth and real GDP growth

Source: China NBS, Bernstein analysis and estimates

Part 1 - Macroeconomic Indicators

Consumer inflation was 2.5% for December, up 50bp from the previous month's readings and 20bp above market expectations (see Exhibit 4). China's 2012 full-year CPI inflation rate averaged 2.65%, well below the central bank's full-year target of 4.0%. China's December PPI inflation of -1.9% was up 30bp from November levels but was 10bp below market expectations of -1.8%. This marks the third consecutive MoM increase to China's PPI inflation figure as PPI inflation is now 170bp higher than the 35-month low levels reported in September. As the PPI tends to be a leading indicator to CPI in China, we believe the data supports the view that consumer price inflation will remain moderate in the coming 6 months (though food prices may continue to rise in the short-term).

Exhibit 4China's y-o-y CPI growth

Source: CEIC, NBS, Bernstein analysis

Including the December data, China's economic indicators have exhibited an upward trend over the past 3-4 months that was highlighted by the rebound in the country's Q4 2012 real GDP growth of 7.9%. This

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

4Q20

12

3Q20

12

2Q20

12

1Q20

12

4Q20

11

3Q20

11

2Q20

11

1Q20

11

4Q20

10

3Q20

10

2Q20

10

1Q20

10

4Q20

09

3Q20

09

2Q20

09

1Q20

09

4Q20

08

3Q20

08

2Q20

08

1Q20

08

4Q20

07

3Q20

07

2Q20

07

En

erg

y C

on

sum

pti

on G

row

th

Rea

l GD

P G

row

th

Real GDP Growth (YoY) Energy Consumption Growth (YoY)

Dec CPI = 2.5%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Jan

-05

Apr

-05

Jul

-05

Oc

t-0

5

Jan

-06

Apr

-06

Jul

-06

Oc

t-0

6

Jan

-07

Apr

-07

Jul

-07

Oc

t-0

7

Jan

-08

Apr

-08

Jul

-08

Oc

t-0

8

Jan

-09

Apr

-09

Jul

-09

Oc

t-0

9

Jan

-10

Apr

-10

Jul

-10

Oc

t-1

0

Jan

-11

Apr

-11

Jul

-11

Oc

t-1

1

Jan

-12

Apr

-12

Jul

-12

Oc

t-1

2

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

6

marked an improvement of 50bp off the 7.4% reported in Q3 2012 and represented the first QoQ improvement in nearly 2 years.

Regarding the specific factors we track, retail sales and industrial production growth accelerated in December from November levels while the December PMI figures remained above 50 (indicating economic expansion) – see Exhibit 5 and Exhibit 6. Retail sales for the month were 15.2%, 20bp higher than expected and 30bp higher than November. China's PMI Industrial production came in at 50.6 for December, inline with November levels which themselves marked a 7-month high. The only deceleration we saw from a major indictor was on YTD fixed-asset investment where December YTD growth fell 10bp from November levels to 20.6%.

Exhibit 5China PMI and Industrial Production Growth

Source: NBS, CEIC, Bernstein analysis

Exhibit 6YoY Growth of Key Components to China's GDP Growth

Source: Bloomberg, Bernstein analysis & estimates

On the export side, China reported a trade surplus of US$31.6 billion in December, the third highest level for 2012 as exports rose 14.1% YoY, up sharply from the 2.9% growth reported in November and well above the year-to-date average of 7.9% (see Exhibit 7).

In light of improving economic data over the past 3-4 months as well as the rising CPI inflation, we'd be surprised to see the central bank cut interest rates again in the coming months, despite the fact that M2

50.6

8%

10%

12%

14%

16%

18%

46474849505152535455

De

c-1

0

Jan

-11

Fe

b-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul

-11

Au

g-1

1

Se

p-1

1

Oc

t-1

1

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul

-12

Au

g-1

2

Se

p-1

2

Oc

t-1

2

No

v-1

2

De

c-1

2

Ind

us

try

Pro

du

cti

on

Gro

wth

PM

Il

Manufacturing PMI Industry Production Growth

20%

21%

22%

23%

24%

25%

26%

27%

10%

12%

14%

16%

18%

20%

Oc

t-1

0

No

v-1

0

De

c-1

0

Jan-

11

Fe

b-1

1

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul

-11

Au

g-1

1

Se

p-1

1

Oc

t-1

1

No

v-1

1

De

c-1

1

Jan-

12

Fe

b-1

2

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul

-12

Au

g-1

2

Se

p-1

2

Oc

t-1

2

No

v-1

2

De

c-1

2

FA

I Yo

Y G

row

th

Re

tail

Sa

les

Yo

Y G

row

th

Retail Sales Fixed Asset Investment (YTD)

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

7

money supply growth missed the central bank's target of 14.0% last year (December M2 growth was 13.8%).

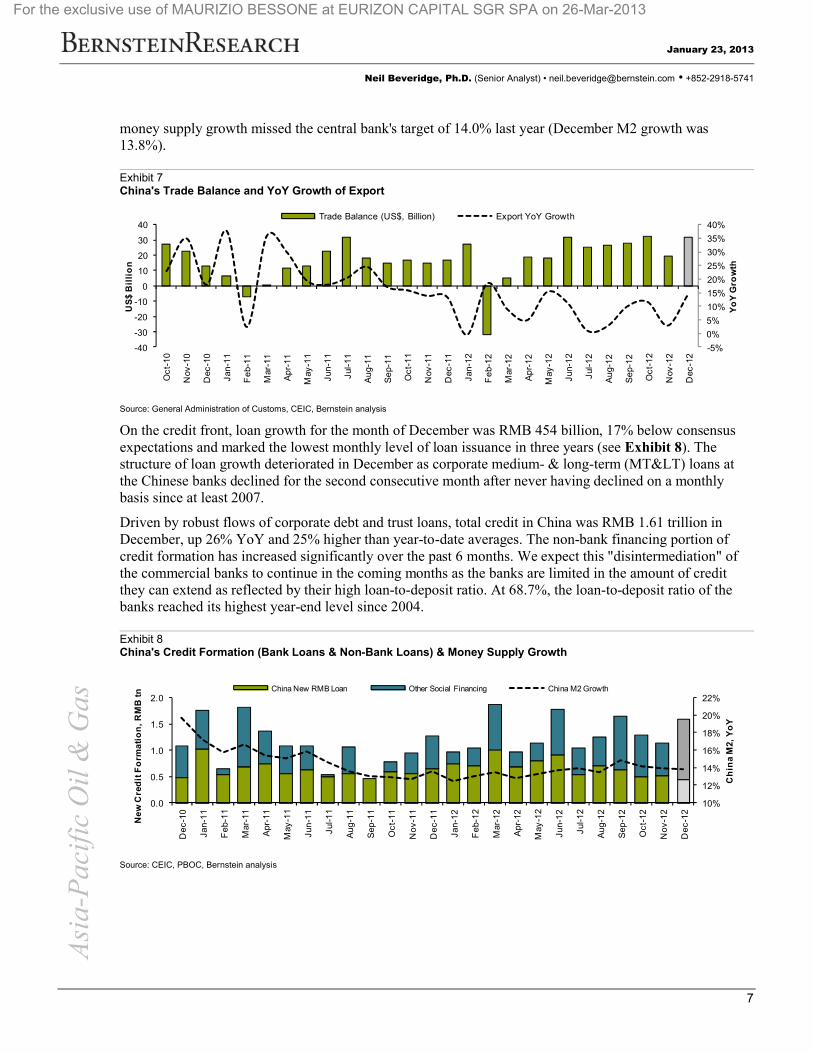

Exhibit 7China's Trade Balance and YoY Growth of Export

Source: General Administration of Customs, CEIC, Bernstein analysis

On the credit front, loan growth for the month of December was RMB 454 billion, 17% below consensus expectations and marked the lowest monthly level of loan issuance in three years (see Exhibit 8). The structure of loan growth deteriorated in December as corporate medium- & long-term (MT<) loans at the Chinese banks declined for the second consecutive month after never having declined on a monthly basis since at least 2007.

Driven by robust flows of corporate debt and trust loans, total credit in China was RMB 1.61 trillion in December, up 26% YoY and 25% higher than year-to-date averages. The non-bank financing portion of credit formation has increased significantly over the past 6 months. We expect this "disintermediation" ofthe commercial banks to continue in the coming months as the banks are limited in the amount of credit they can extend as reflected by their high loan-to-deposit ratio. At 68.7%, the loan-to-deposit ratio of the banks reached its highest year-end level since 2004.

Exhibit 8China's Credit Formation (Bank Loans & Non-Bank Loans) & Money Supply Growth

Source: CEIC, PBOC, Bernstein analysis

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

-40

-30

-20

-10

0

10

20

30

40

Oc

t-1

0

Nov

-10

Dec

-10

Jan

-11

Fe

b-1

1

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul

-11

Au

g-11

Se

p-11

Oc

t-1

1

Nov

-11

Dec

-11

Jan

-12

Fe

b-1

2

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul

-12

Au

g-12

Se

p-12

Oc

t-1

2

Nov

-12

Dec

-12

Yo

Y G

row

th

US

$ B

illi

on

Trade Balance (US$, Billion) Export YoY Growth

10%

12%

14%

16%

18%

20%

22%

0.0

0.5

1.0

1.5

2.0

De

c-1

0

Jan-

11

Fe

b-1

1

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul

-11

Aug

-11

Sep

-11

Oc

t-11

No

v-1

1

De

c-1

1

Jan-

12

Fe

b-1

2

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul

-12

Aug

-12

Sep

-12

Oc

t-12

No

v-1

2

De

c-1

2

Ch

ina

M2,

Yo

Y

Ne

w C

red

it F

orm

ati

on

, R

MB

tn China New RMB Loan Other Social Financing China M2 Growth

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

8

Part 2 - Oil

Oil Demand

Apparent oil demand (crude runs plus net product imports) in December increased by 9.1% y-o-y with a record-high daily demand of 10.64 Mbpd (Exhibits 9).

Exhibit 9China apparent oil demand

Source: China NBS, Bernstein analysis

Note: China apparent oil demand is defined as crude runs plus net product imports

Crude imports in December increased 8.0% y-o-y to 23.7MT on higher demand (Exhibit 10).

Exhibit 10Chinese crude imports

Source: China NBS, Bernstein analysis

During 2Q12 and 3Q12, demand for oil slumped in China along with industrial production and passenger vehicle sales growth. Since 4Q however there has been a dramatic increase in apparent oil demand, increasing at 9.9% y-o-y in November and 9.1% y-o-y in December as economic conditions improved. This improving trend has been evident in the bottoming out of industrial production growth (Exhibit 11).

44.8

-2%0%2%4%6%8%10%12%14%16%18%20%

25

30

35

40

45

50

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Dec

-12

Gro

wth

, Yo

Y

Ap

par

ent O

il D

eman

d,

MM

T

Apparent Oil Demand YoY Growth

23.7

-20%

-10%0%10%20%

30%40%

9111315171921232527

Dec

-10

Jan

-11

Feb

-11

Ma

r-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Ma

r-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Dec

-12

Cru

de

Imp

ort

s G

wth

. Yo

Y

Ch

ina

Cru

de

Imp

ort

s, M

MT

China Crude Imports Crude Imports

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

9

Exhibit 11Industrial output growth vs. apparent oil demand growth

Source: China NBS, Bernstein analysis

China's oil market is dominated by growth in demand for transportation fuels. Over the past decade, demand for transportation fuels has more than doubled and now accounts for 54% of total demand. In December, passenger car sales increased by 6.9% y-o-y as Chinese consumers bought 1.46 million cars (Exhibit 12) highlighting continued growth in automobile and transport fuel demand.

Exhibit 12Passenger car sales in China

Source: China NBS, Bernstein analysis

Given that industrial demand and transport demand are the two dominant factors which drive oil demand, we use PMI and passenger car sales (both 1 quarter lagged and weighted by 80% PMI and 20% car sales) as

5%

8%

11%

14%

17%

20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%M

ar-0

5

Jun-

05

Sep

-05

Dec

-05

Mar

-06

Jun-

06

Sep

-06

Dec

-06

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Ind

us

tria

l Ou

tpu

t G

row

th

Ap

par

en

t O

il D

ema

nd

Gro

wth

Apparent Oil Demand Growth Industrial Output Growth

December apparentoil demand growth

is 9.1%

1.5

-30%

-20%

-10%

0%

10%

20%

30%

0.00.20.40.60.81.01.21.41.61.8

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Yo

Y G

wth

Sal

es V

olu

me

, MM

un

its

Passenger Car Sales Volume YoY Growth

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

10

leading indicators in forecasting China oil demand growth. Our near term projection for China oil demand are shown in Exhibit 13, Exhibit 14.

4Q12 apparent oil demand achieved a record high of over 10.3Mbpd giving an average apparent demand for 2012 of 9.7Mbpd (4% higher y-o-y). We estimate apparent oil demand in 1Q13 will grow by 7.5% y-o-y to 10.3Mbpd. We estimate Chinese oil demand in 2013 will reach 10.3Mbpd (Exhibit 13), which remains 0.3Mbpd above the IEA estimates despite of IEA's recent upside revision. We expect the IEA to make a number of further positive demand revisions this year.

Exhibit 13Chinese oil demand estimate

Source: China NBS, Bernstein analysis and estimates

Exhibit 14We estimate China oil demand growth using PMI and car sales growth as leading indicators

Source: China NBS, Bernstein analysis

Oil Supply

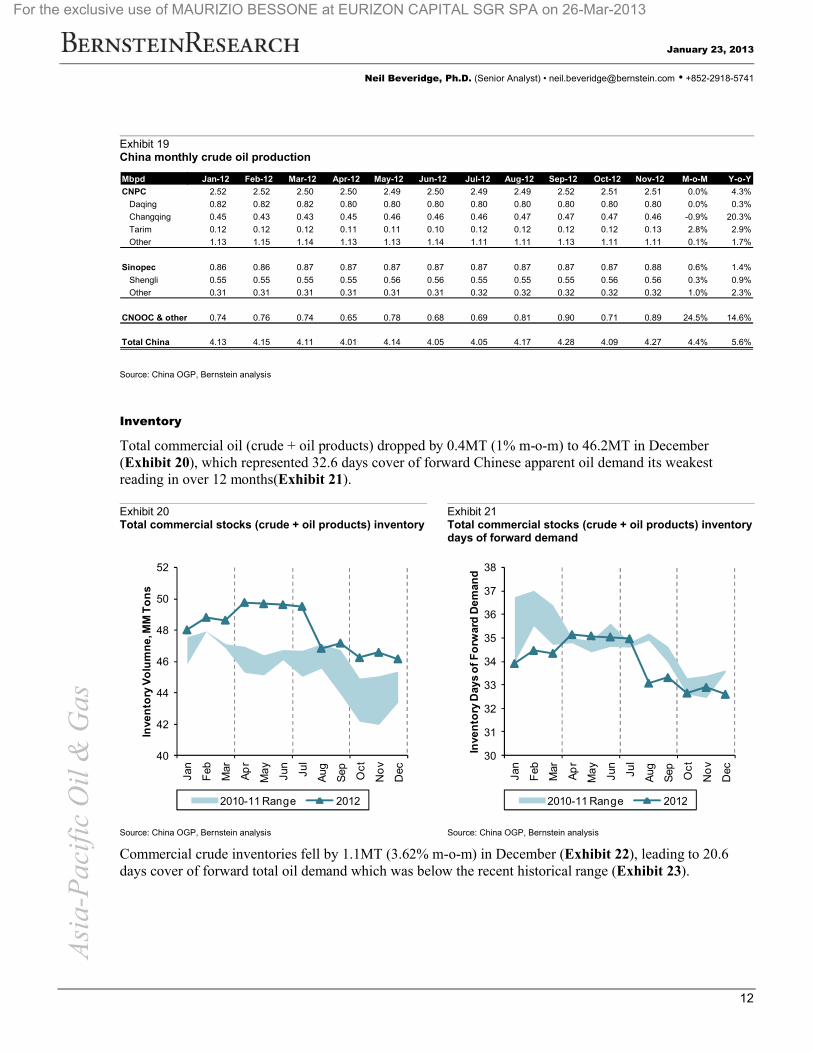

Oil production in December increased by 5.6% y-o-y to 17.9MT (Exhibit 15). PetroChina and Sinopec continued to increase production gradually (Exhibit 16, Exhibit 17). CNOOC delivered exceptionally strong growth in oil production on the back expanding offshore production and Penglai ramp up although we now expect this growth to level off (Exhibit 18).

Chinese Oil Demand Summary 1Q12 2Q12 3Q12 4Q12 2012 1Q13E 2Q13E 3Q13E 4Q13E 2013E

Mbpd

PMI 51.53 51.30 49.70 50.47 50.75 50.70 51.30 50.80 50.70 50.88

YoY change -2.5% -1.2% -2.4% 1.1% -1.3% -1.6% 0.0% 2.2% 0.5% 0.2%

Car sales 3.77 3.84 3.65 4.22 15.49 4.06 4.15 3.89 4.51 16.63

YoY change -1.8% 16.6% 6.7% 7.4% 6.9% 7.5% 7.9% 6.5% 6.9% 7.4%

PMI and car sales index growth 0.2% 1.6% 3.1% 1.7% 1.7%

China apparent oil demand 9.69 9.30 9.37 10.33 9.67 10.31 9.83 9.94 11.02 10.28

YoY change 3.3% 0.2% 3.5% 8.8% 4.0% 6.4% 5.7% 6.1% 6.6% 6.2%

Refining throughput 9.31 9.01 9.14 9.99 9.36 9.90 9.52 9.70 10.65 9.94

Net product import 0.38 0.29 0.23 0.35 0.31 0.41 0.31 0.24 0.37 0.33

China oil demand - IEA - Jan 13 9.59 9.26 9.40 10.12 9.60 9.95 9.81 9.87 10.30 9.98

YoY change 3.1% -0.4% 4.4% 7.7% 3.9% 3.8% 5.9% 5.0% 1.8% 4.0%

Delta (SCB - IEA) 0.10 0.04 (0.03) 0.21 0.07 0.36 0.02 0.07 0.72 0.30

-5%

0%

5%

10%

15%

20%

25%

4Q

13

3Q

13

2Q

13

1Q

13

4Q

12

3Q

12

2Q

12

1Q

12

4Q

11

3Q

11

2Q

11

1Q

11

4Q

10

3Q

10

2Q

10

1Q

10

4Q

09

3Q

09

2Q

09

1Q

09

4Q

08

3Q

08

2Q

08

1Q

08

4Q

07

3Q

07

2Q

07

1Q

07

4Q

06

Yo

Y C

han

ge

Actual oil demand growth Estimate by blended index

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

11

Exhibit 15Chinese oil production

Source: China NBS, Bernstein analysis

Exhibit 16PetroChina oil production

Exhibit 17Sinopec oil production

Exhibit 18CNOOC and others oil production

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis

Exhibit 19 summarizes China monthly crude oil production by key fields. CNPC's Changqing oil field achieved 20.3% y-o-y growth in November and contributed 18.5% of CNPC's overall production. This is largely driven by the growth in tight oil fraccing in Central China. CNOOC and others' production increased sharply by 14.6% in November as Peng Lai volumes continued to ramp up. While offshore China oilfields (Fanyu 4-2/5-1 and Liuhua 4-1) started production in December 2012, we expect production will start to flatten off in the near term.

17.9

-8%

-3%

2%

7%

12%

12.5

13.5

14.5

15.5

16.5

17.5

18.5D

ec-1

0

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Yo

Y G

row

th

Oil

Pro

du

ctio

n, M

MT

Oil Production YoY Growth

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jul-

09S

ep-0

9N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-

11S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-1

2

Yo

Y G

row

th

mm

bp

d

Daqing Changqing

Tarim Other

YoY Growth

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jul-

09S

ep-0

9N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-

11S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-1

2

Yo

Y G

row

th

mm

bp

d

Shengli Other YoY Growth

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jul-

09S

ep-0

9N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-

11S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-1

2

Yo

Y G

row

th

mm

bp

d

CNOOC & Others YoY Growth

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

12

Exhibit 19China monthly crude oil production

Source: China OGP, Bernstein analysis

Inventory

Total commercial oil (crude + oil products) dropped by 0.4MT (1% m-o-m) to 46.2MT in December(Exhibit 20), which represented 32.6 days cover of forward Chinese apparent oil demand its weakest reading in over 12 months(Exhibit 21).

Exhibit 20Total commercial stocks (crude + oil products) inventory

Exhibit 21Total commercial stocks (crude + oil products) inventory days of forward demand

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis

Commercial crude inventories fell by 1.1MT (3.62% m-o-m) in December (Exhibit 22), leading to 20.6 days cover of forward total oil demand which was below the recent historical range (Exhibit 23).

Mbpd Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 M-o-M Y-o-Y

CNPC 2.52 2.52 2.50 2.50 2.49 2.50 2.49 2.49 2.52 2.51 2.51 0.0% 4.3%

Daqing 0.82 0.82 0.82 0.80 0.80 0.80 0.80 0.80 0.80 0.80 0.80 0.0% 0.3%

Changqing 0.45 0.43 0.43 0.45 0.46 0.46 0.46 0.47 0.47 0.47 0.46 -0.9% 20.3%

Tarim 0.12 0.12 0.12 0.11 0.11 0.10 0.12 0.12 0.12 0.12 0.13 2.8% 2.9%

Other 1.13 1.15 1.14 1.13 1.13 1.14 1.11 1.11 1.13 1.11 1.11 0.1% 1.7%

Sinopec 0.86 0.86 0.87 0.87 0.87 0.87 0.87 0.87 0.87 0.87 0.88 0.6% 1.4%

Shengli 0.55 0.55 0.55 0.55 0.56 0.56 0.55 0.55 0.55 0.56 0.56 0.3% 0.9%

Other 0.31 0.31 0.31 0.31 0.31 0.31 0.32 0.32 0.32 0.32 0.32 1.0% 2.3%

CNOOC & others 0.74 0.76 0.74 0.65 0.78 0.68 0.69 0.81 0.90 0.71 0.89 24.5% 14.6%

Total China 4.13 4.15 4.11 4.01 4.14 4.05 4.05 4.17 4.28 4.09 4.27 4.4% 5.6%

40

42

44

46

48

50

52

Jan

Feb

Mar

Ap

r

Ma

y

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry V

olu

mn

e, M

M T

on

s

2010-11 Range 2012

30

31

32

33

34

35

36

37

38

Jan

Feb

Mar

Ap

r

Ma

y

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry D

ays

of

Fo

rwar

d D

em

and

2010-11 Range 2012

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

13

Exhibit 22Commercial crude inventory

Exhibit 23Commercial crude inventory days of forward demand

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis

The commercial oil products inventory grew by 0.88MT (4.15% m-o-m) to in December (Exhibit 24), implying 12.3 days cover of forward apparent oil demand (Exhibit 25) which was in line with seasonal averages

Exhibit 24Commercial oil products inventory

Exhibit 25Commercial oil products inventory days of forward demand

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis

Gasoline inventory accounted for 44% of total oil products inventory. In December, gasoline inventory increased by 0.59MT (8.54% m-o-m) (Exhibit 26), leading to 30.7 days cover of forward apparent gasoline demand which was in line with the historical range (Exhibit 27).

22

24

26

28

30

32

34Ja

n

Feb

Ma

r

Ap

r

May

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry V

olu

mn

e, M

M T

on

s

2010-11 Range 2012

18

19

20

21

22

23

24

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry D

ays

of

Fo

rwar

d D

em

and

2010-11 Range 2012

10

12

14

16

18

20

22

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Aug

Sep Oct

No

v

Dec

Inve

nto

ry V

olu

mn

e, M

M T

on

s

2010-11 Range 2012

10

11

12

13

14

15

16

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Aug

Sep Oct

No

v

Dec

Inve

nto

ry D

ays

of

Fo

rwar

d D

eman

d

2010-11 Range 2012

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

14

Exhibit 26Gasoline inventory

Exhibit 27Gasoline inventory days of forward demand

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis and estimates

Diesel inventories accounted for 48% of total oil products inventory. In December the diesel inventory increased slightly by 0.88MT (1.90% m-o-m) (Exhibit 28), implying 16.7 days cover of forward apparent diesel demand (Exhibit 29) which was in line with seasonal trends.

Exhibit 28Diesel inventory

Exhibit 29Diesel inventory days of forward demand

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis and estimates

4

5

6

7

8

9

10Ja

n

Feb

Mar

Ap

r

May

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry V

olu

mn

e, M

M T

on

s

2010-11 Range 2012

20

22

24

26

28

30

32

34

36

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry D

ays

of

Fo

rwar

d D

em

and

2010-11 Range 2012

0

2

4

6

8

10

12

14

Jan

Feb

Mar

Ap

r

Ma

y

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry V

olu

mn

e, M

M T

on

s

2010-11 Range 2012

12

14

16

18

20

22

24

26

28

Jan

Feb

Mar

Ap

r

Ma

y

Jun

Jul

Aug

Sep Oc

t

No

v

Dec

Inve

nto

ry D

ays

of

Fo

rwar

d D

em

and

2010-11 Range 2012

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

15

Refining

Refining throughput surged by 9.9% y-o-y in December to all time high amount of 43.1MT (Exhibit 30). We expect high refining throughput growth to continue as Chinese refiners add 1.2Mblsd of additional refining capacity in 2013.

Exhibit 30Chinese refinery throughput

Source: China NBS, Bernstein analysis and estimates

Net products imports were 1.6MT for December, which marked the highest reading over the last nine months as seasonal demand for fuel oil and diesel increased (Exhibit 31).

Exhibit 31Chinese net products imports

Source: China NBS, Bernstein analysis and estimates

Apparent gasoline demand in November was 7.7MMT, up 17.6% y-o-y (Exhibit 32) and diesel demand increased by 3.2% y-o-y to 14.7MMT (Exhibit 33). Again this highlights the importance in transportation demand over industrial demand in driving overall oil demand in China.

43.1

-2%0%2%4%6%8%10%12%14%

25

30

35

40

45

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Dec

-12

Th

rou

gh

t Gw

th, Y

oY

Th

rou

gh

put

, MM

T

Refinery Throughput YoY

1.6

-100%

-50%

0%

50%

100%

150%

200%

0.0

0.5

1.0

1.5

2.0

2.5

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Dec

-12

Th

rou

gh

t Gw

th, Y

oY

Net

pro

du

cts

imp

ort

s, M

MT Net products imports YoY

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

16

Exhibit 32China gasoline demand

Source: China NBS, Bernstein analysis

Exhibit 33China diesel demand

Source: China NBS, Bernstein analysis

Since the introduction of the NDRC's current retail pricing mechanism in 2009 there have been 14 upward adjustments to product prices and 9 downward adjustments (Exhibit 34). China's NDRC announced the fourth fuel price reduction this year on November 15th, cutting retail gasoline and diesel prices by 3.2% and 3.4% respectively.

7.7

-5%

0%

5%

10%

15%

20%

25%

4.04.55.05.56.06.57.07.58.0

Dec

-10

Jan

-11

Feb

-11

Ma

r-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Ma

r-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Yo

Y G

row

th

Ap

par

ent G

aso

line

Dem

and

(M

MT

)

Apparent Gasoline Demand yoy %

14.7

-5%

0%

5%

10%

15%

20%

9

10

11

12

13

14

15

16

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Yo

Y G

row

th

Ap

par

ent D

iese

l Dem

and

(M

MT

)

Apparent Diesel Demand yoy %

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

17

Exhibit 34NDRC retail fuel price changes have lagged crude prices on since the start of the current pricing system

Source: Company reports, Bloomberg, Bernstein analysis and estimates

Despite the price cut, refining margins should still remain positive for Sinopec. Gasoline & diesel/crude price ratios correlate strongly with Sinopec's refining margins. The ratio between gasoline/diesel prices and crude bottomed out in 2Q12, which should mean that 2Q12 was probably the low point for refining margins this year. The improvement in refining margins going into 3Q and 4Q is a major positive for Sinopec given the scale of their refining division (Exhibit 35). We believe that in 2013, the government could take steps to reform product pricing to a shorter time window for pricing adjustment, a lower threshold for changes and an agency outside of NDRC to announce changes.

40

50

60

70

80

90

100

110

120

5

7

9

11

Jan-

09Fe

b-09

Mar

-09

Apr

-09

May

-09

Jun-

09Ju

l-09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10Fe

b-10

Mar

-10

Apr

-10

May

-10

Jun-

10Ju

l-10

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11Fe

b-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12Fe

b-12

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

$/b

bl

RM

B/L

China Gaso93 (RMB/L) China Diesel (RMB/L) Dubai Crude ($/bbl)

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

18

Exhibit 35Sinopec refining margins have tracked the price ratio of retail fuels and crude

Source: Company reports, Bloomberg, Bernstein analysis and estimates

Strategic Petroleum Reserves (SPR)

China does not release SPR fill on a regular basis. In addition, there is limited data to track the SPR fill. We estimate monthly SPR change and commercial inventory level change (Exhibit 36) through the difference between total oil demand (China crude production and net imports) and apparent oil demand (refining throughput and net products imports).

Exhibit 36Implied monthly change in China's commercial crude and products inventory and SPR level

Source: China NBS, Bernstein analysis

Note: Implied commercial crude and products inventory and SPR is calculated as the difference between total oil demand and apparent oil demand

-5

0

5

10

15

20

1.0x

1.4x

1.8x

2.2x

2.6x

3.0xJa

n-0

9F

eb-0

9M

ar-

09A

pr-

09M

ay-0

9Ju

n-0

9Ju

l-09

Aug

-09

Sep

-09

Oct

-09

No

v-09

Dec

-09

Jan

-10

Feb

-10

Ma

r-10

Ap

r-10

May

-10

Jun

-10

Jul-

10A

ug-1

0S

ep-1

0O

ct-1

0N

ov-

10D

ec-1

0Ja

n-1

1F

eb-1

1M

ar-

11A

pr-

11M

ay-1

1Ju

n-1

1Ju

l-11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Ma

r-12

Ap

r-12

May

-12

Jun

-12

Jul-

12A

ug-1

2S

ep-1

2O

ct-1

2N

ov-

12D

ec-1

2

SN

P re

po

rted

GR

M, $

/bb

l

Rat

io o

f ret

ail p

rice

s (a

dju

ste

d fo

r co

nsu

mp

tion

tax)

ov

er c

rud

e p

ric

es

Gaso / Dubai Diesel / Dubai SNP Reported GRM

-1.6

70

80

90

100

110

120

130

-3-2-1012345

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Bre

nt,

US

$/b

bl

Inve

nto

ry C

han

ge,

MM

T

on

s

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

19

Exhibit 37Implied monthly change in China's SPR level

Source: China NBS, Bernstein analysis

Note: Implied SPR level change is calculated as the difference between total oil demand and apparent oil demand minus commercial crude and products inventory change.

Through monitoring implied SPR level change every month (Exhibit 37), we estimate that China SPR level by December 2012 was close to 280mmbbls (Exhibit 38), indicating that Phase 2 SPR has been filled.Beyond Phase 2, China will begin the construction of Phase 3 storage bases this year with a total capacity of 28.2 cubic meters. We expect 200mbd of demand outside of 'apparent demand' for the filling of this capacity.

Exhibit 38China's SPR level and SPR capacity

Source: China NBS, Bernstein analysis

(1.3) (1.2)

70

80

90

100

110

120

130

-3-2-1012345

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Dec

-12

Bre

nt,

US

$/b

bl

SP

R L

evel

Ch

ang

e, M

M

To

ns

-

50

100

150

200

250

300

350

400

De

c-0

6F

eb

-07

Ap

r-0

7Ju

n-0

7A

ug

-07

Oct

-07

De

c-0

7F

eb

-08

Ap

r-0

8Ju

n-0

8A

ug

-08

Oct

-08

De

c-0

8F

eb

-09

Ap

r-0

9Ju

n-0

9A

ug

-09

Oct

-09

De

c-0

9F

eb

-10

Ap

r-1

0Ju

n-1

0A

ug

-10

Oct

-10

De

c-1

0F

eb

-11

Ap

r-1

1Ju

n-1

1A

ug

-11

Oct

-11

De

c-1

1F

eb

-12

Ap

r-1

2Ju

n-1

2A

ug

-12

Oct

-12

De

c-1

2F

eb

-13

Ap

r-1

3Ju

n-1

3A

ug

-13

Oct

-13

De

c-1

3

mm

bb

ls

SPR SPR Capacity

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

20

Petrochemicals

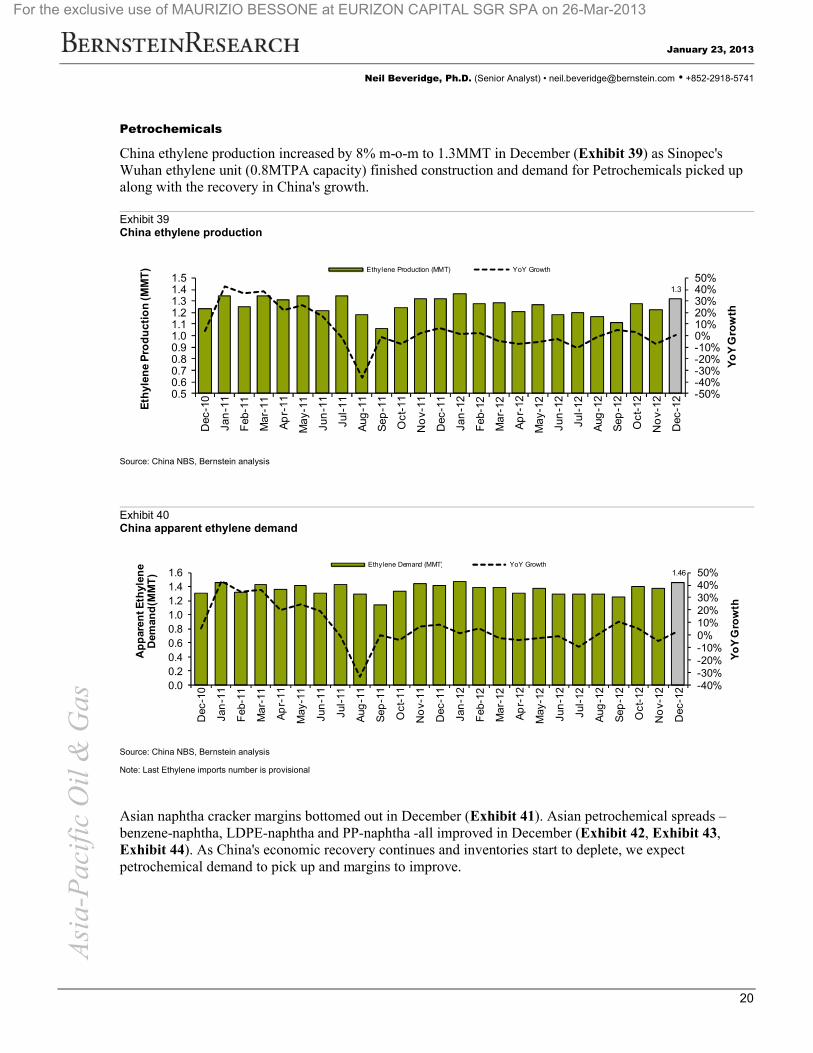

China ethylene production increased by 8% m-o-m to 1.3MMT in December (Exhibit 39) as Sinopec's Wuhan ethylene unit (0.8MTPA capacity) finished construction and demand for Petrochemicals picked up along with the recovery in China's growth.

Exhibit 39China ethylene production

Source: China NBS, Bernstein analysis

Exhibit 40China apparent ethylene demand

Source: China NBS, Bernstein analysis

Note: Last Ethylene imports number is provisional

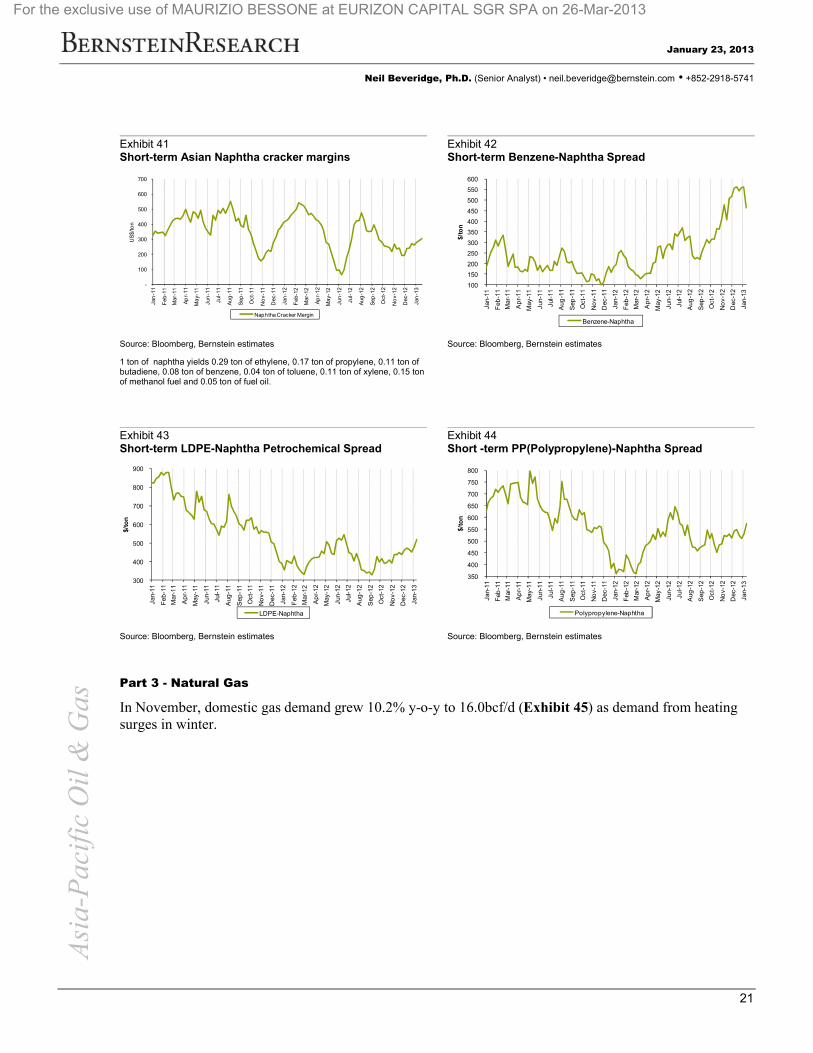

Asian naphtha cracker margins bottomed out in December (Exhibit 41). Asian petrochemical spreads –benzene-naphtha, LDPE-naphtha and PP-naphtha -all improved in December (Exhibit 42, Exhibit 43, Exhibit 44). As China's economic recovery continues and inventories start to deplete, we expect petrochemical demand to pick up and margins to improve.

1.3

-50%-40%-30%-20%-10%0%10%20%30%40%50%

0.50.60.70.80.91.01.11.21.31.41.5

Dec

-10

Jan

-11

Feb

-11

Ma

r-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Ma

r-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Yo

Y G

row

th

Eth

ylen

e P

rod

uc

tio

n (M

MT

) Ethylene Production (MMT) YoY Growth

1.46

-40%-30%-20%-10%0%10%20%30%40%50%

0.00.20.40.60.81.01.21.41.6

Dec

-10

Jan

-11

Feb

-11

Ma

r-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Ma

r-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Yo

Y G

row

th

Ap

par

ent E

thyl

ene

Dem

and

(MM

T)

Ethylene Demand (MMT) YoY Growth

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

21

Exhibit 41Short-term Asian Naphtha cracker margins

Exhibit 42Short-term Benzene-Naphtha Spread

Source: Bloomberg, Bernstein estimates

1 ton of naphtha yields 0.29 ton of ethylene, 0.17 ton of propylene, 0.11 ton of butadiene, 0.08 ton of benzene, 0.04 ton of toluene, 0.11 ton of xylene, 0.15 ton of methanol fuel and 0.05 ton of fuel oil.

Source: Bloomberg, Bernstein estimates

Exhibit 43Short-term LDPE-Naphtha Petrochemical Spread

Exhibit 44Short -term PP(Polypropylene)-Naphtha Spread

Source: Bloomberg, Bernstein estimates Source: Bloomberg, Bernstein estimates

Part 3 - Natural Gas

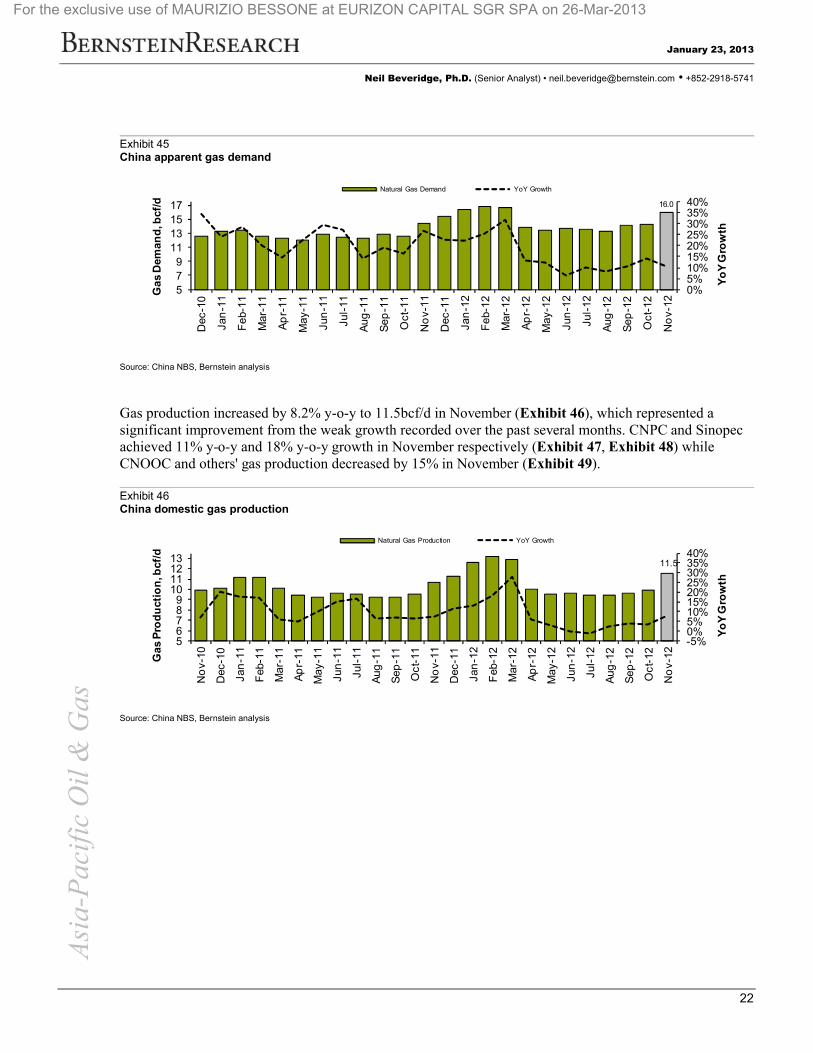

In November, domestic gas demand grew 10.2% y-o-y to 16.0bcf/d (Exhibit 45) as demand from heating surges in winter.

-

100

200

300

400

500

600

700

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Jan

-13

US

$/to

n

Naphtha Cracker Margin

100

150

200

250

300

350

400

450

500

550

600

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun-

12

Jul-1

2

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Jan-

13

$/to

n

Benzene-Naphtha

300

400

500

600

700

800

900

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun-

12

Jul-1

2

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Jan-

13

$/to

n

LDPE-Naphtha

350

400

450

500

550

600

650

700

750

800

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun-

12

Jul-1

2

Aug

-12

Sep

-12

Oct

-12

No

v-12

Dec

-12

Jan-

13

$/to

n

Polypropylene-Naphtha

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

22

Exhibit 45China apparent gas demand

Source: China NBS, Bernstein analysis

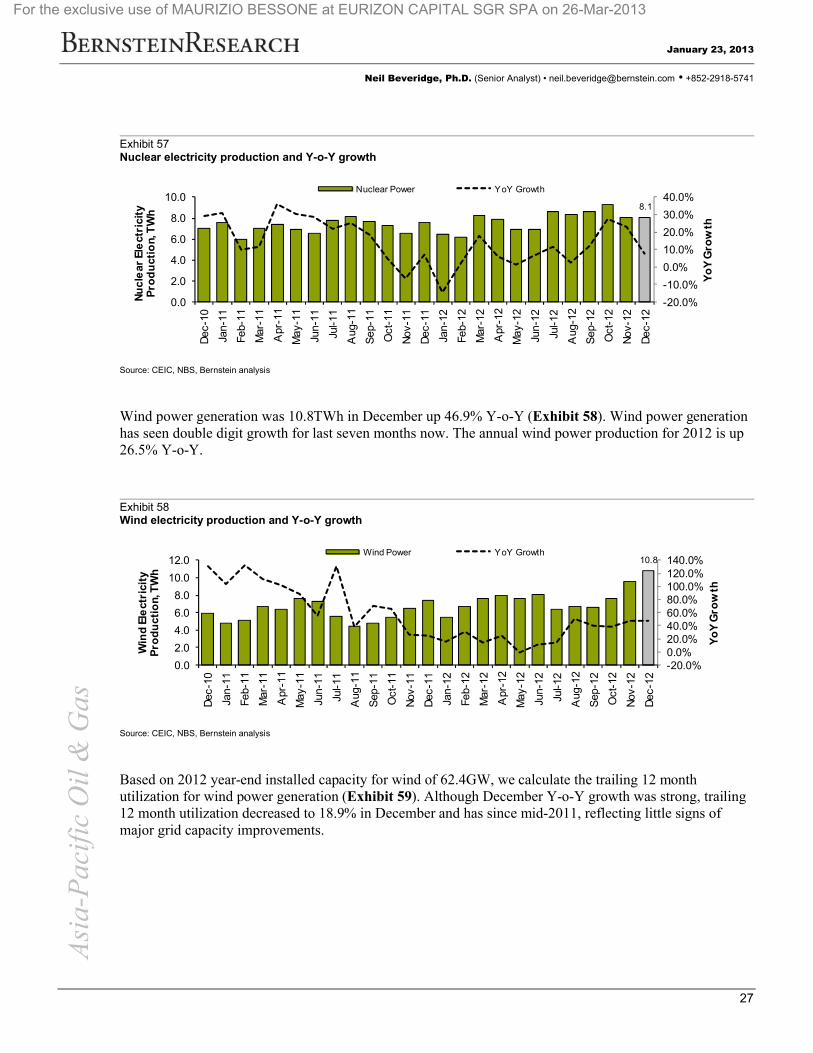

Gas production increased by 8.2% y-o-y to 11.5bcf/d in November (Exhibit 46), which represented a significant improvement from the weak growth recorded over the past several months. CNPC and Sinopec achieved 11% y-o-y and 18% y-o-y growth in November respectively (Exhibit 47, Exhibit 48) while CNOOC and others' gas production decreased by 15% in November (Exhibit 49).

Exhibit 46China domestic gas production

Source: China NBS, Bernstein analysis

16.0

0%5%10%15%20%25%30%35%40%

579

11131517

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Yo

Y G

row

th

Ga

s D

eman

d, b

cf/d

Natural Gas Demand YoY Growth

11.5

-5%0%5%10%15%20%25%30%35%40%

56789

10111213

No

v-10

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oc

t-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

May

-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oc

t-12

No

v-12

Yo

Y G

row

th

Ga

s P

rod

uct

ion

, bcf

/d

Natural Gas Production YoY Growth

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

23

Exhibit 47PetroChina gas production

Exhibit 48Sinopec gas production

Exhibit 49CNOOC and others gas production

Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis Source: China OGP, Bernstein analysis

Imports made up 28% of the total demand in November (Exhibit 50). Pipeline gas imports increased by 0.34bcf/d (15% m-o-m) to 2.57bcf/d (Exhibit 52), offsetting LNG imports decrease as spot LNG markets tightened in winter (Exhibit 51). Pipeline gas imports accounted for 58% of total gas imports in November. As China's second West-to-East gas pipeline became completely operational on December 30, 2012 and Myanmar pipeline will finish construction in May 2013, we expect pipeline gas imports continue to growthin 2013.

Exhibit 50China monthly gas supply and demand summary

Source: Bloomberg, China OGP, Bernstein analysis

-10%

-5%

0%

5%

10%

15%

20%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jul-

09S

ep-0

9N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-

11S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-1

2

Yo

Y G

row

th

bcf

/d

Total CNPC YoY Growth

0%

10%

20%

30%

40%

50%

60%

70%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jul-

09S

ep-0

9N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-

11S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-1

2

Yo

Y G

row

th

bcf

/d

Total Sinopec YoY Growth

-100%

-50%

0%

50%

100%

150%

200%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jul-

09S

ep-0

9N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-

11S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-1

2

Yo

Y G

row

th

bcf

/d

Total CNOOC & Others YoY Growth

Bcf/d Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 M-o-M Y-o-Y

Production 12.55 13.22 12.88 9.98 9.49 9.59 9.40 9.44 9.62 9.86 11.52 16.8% 8.2%

Imports 3.78 3.62 3.76 3.91 3.92 4.11 4.22 3.81 4.58 4.45 4.45 0.0% 16.0%

Pipeline gas 1.59 2.13 1.87 2.07 2.01 2.01 1.99 1.99 2.19 2.23 2.57 15.2% 61.7%

LNG 2.19 1.49 1.89 1.83 1.91 2.10 2.23 1.82 2.39 2.22 1.88 -15.4% -16.4%

Gas Demand 16.33 16.84 16.64 13.89 13.41 13.70 13.62 13.26 14.19 14.31 15.97 11.6% 10.2%Imports as % of demand 23% 21% 23% 28% 29% 30% 31% 29% 32% 31% 28%

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

24

Exhibit 51China LNG imports

Source: China NBS, Bernstein analysis

Exhibit 52China's pipeline gas imports

Source: China NBS, Bernstein analysis

Note: May data provisional

Part 4 - Electricity & Coal

Electricity production in December was 432.7TWh, up 7.2% Y-o-Y and up 7.9% sequentially from November. Power generation growth in December 2011 was 9.8% (Exhibit 53). Power production in 2012 was 4,771TWh up 4.2% Y-o-Y. This is the lowest annual production growth since 2005.

1.9

-40%

-20%

0%

20%

40%

60%

80%

100%

0.0

0.5

1.0

1.5

2.0

2.5

3.0O

ct-1

0

No

v-10

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-11

Ma

y-11

Jun

-11

Jul-

11

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-12

Ma

y-12

Jun

-12

Jul-

12

Aug

-12

Sep

-12

Oct

-12

No

v-12

Yo

Y G

row

th

LN

G Im

po

rts,

bcf

/d

Natural Gas Imports YoY Growth

2.6

0%

100%

200%

300%

400%

500%

600%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Oc

t-1

0

No

v-10

De

c-10

Jan

-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun

-11

Jul

-11

Au

g-1

1

Se

p-1

1

Oc

t-1

1

No

v-11

De

c-11

Jan

-12

Feb

-12

Mar

-12

Apr

-12

May

-12

Jun

-12

Jul

-12

Au

g-1

2

Se

p-1

2

Oc

t-1

2

No

v-12

Yo

Y G

row

th

Pip

ed G

as Im

po

rts

, bcf

/d

Piped Gas YoY Growth

For the exclusive use of MAURIZIO BESSONE at EURIZON CAPITAL SGR SPA on 26-Mar-2013

Asi

a-P

acif

ic O

il&

Gas

January 23, 2013

Neil Beveridge, Ph.D. (Senior Analyst) • [email protected] • +852-2918-5741

25

Exhibit 53Electricity production growth (Y-o-Y comparison – same month previous year)

Source: CEIC, NBS, Bernstein analysis

Using the average power production growth of 4.3% and GDP growth of 7.7% for 2012, we get a power multiplier of ~0.56x for 2012. We continue to believe the long-term power multiplier in China is roughly 1x real GDP growth (Exhibit 54). With increasing power production growth in the fourth quarter of 2012, the economy is moving back to this longer term trend.

Exhibit 54China power multiplier (power production growth / GDP growth)

Source: CEIC, NBS, Bernstein analysis

Thermal power generation was 355.4TWh in December, up 3.8% Y-o-Y and up 11.3% sequentially (Exhibit 55). This was the only second time thermal power generation growth was positive since March this year. 2012 thermal power production is down 0.6% Y-o-Y – the first time China has seen negative thermal production growth since 2005.

7.2%

-10%

0%

10%

20%

30%D

ec-1

0

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May