Chapter Overview of Security Types McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 3

Chapter Overview of Security Types McGraw-Hill/IrwinCopyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 3.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter

Overview of Security Types

McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

3

3-2

Learning Objectives

Price quotes for all types of investments are easy to find, but what do they mean? Learn the

answers for:

1. Various types of interest-bearing assets.

2. Equity securities.

3. Futures contracts.

4. Option contracts.

3-3

Security Types

• Our goal in this chapter is to introduce the different types of securities that investors routinely buy and sell in financial markets around the world.

• For each security type, we will examine:

– Its distinguishing characteristics– Its potential gains and losses– How its prices are quoted in the financial press.

3-4

Classifying Securities

Basic Types Major Subtypes

Interest-bearing Money market instruments

Fixed-income securities

Equities Common stock Preferred stock

Derivatives Futures Options

3-5

Interest-Bearing Assets

• Money market instruments are short-term debt obligations of large corporations and governments.

– These securities promise to make one future payment.– When they are issued, their lives are less than one

year.

• Fixed-income securities are longer-term debt obligations of corporations and governments.

– These securities promise to make fixed payments according to a pre-set schedule.

– When they are issued, their lives exceed one year.

3-6

Money Market Instruments

• Examples: U.S. Treasury bills (T-bills), bank certificates of deposit (CDs), corporate and municipal money market instruments.

• Potential gains/losses: A known future payment, except when the borrower defaults (i.e., does not pay).

• Price quotations: Usually, the instruments are sold on a discount basis, and only the interest rates are quoted.

• Therefore, investors must be able to calculate prices from the quoted rates.

3-7

Fixed-Income Securities

• Examples: U.S. Treasury notes, corporate bonds, car loans, student loans.

• Potential gains/losses:

– Fixed coupon payments and final payment at maturity, except when the borrower defaults.

– Possibility of gain (loss) from fall (rise) in interest rates– Depending on the debt issue, illiquidity can be a problem.

Illiquidity means that you might not be able to sell securities

quickly for their current market value.

3-8

Quote Example: Fixed-Income Securities

• Price Quotations from www.wsj.com—the online version of The Wall Street Journal (some columns are self-explanatory):

You will receive 2.20% of the bond’s face value each year in 2 semi-annual payments.

The price (per $100 face) of the bond when it last traded.

The Yield to Maturity (YTM) of the bond.

3-9

Equities

• Common stock: Represents ownership in a corporation. A part owner receives a pro rated share of whatever is left over after all obligations have been met in the event of a liquidation.

• Preferred stock: The dividend is usually fixed and must be paid before any dividends for the common shareholders. In the event of a liquidation, preferred shares have a particular face value.

3-10

Common Stock

• Examples: IBM shares, Microsoft shares, Intel shares, Dell shares, etc.

• Potential gains/losses:

– Many companies pay cash dividends to their shareholders. However, neither the timing nor the amount of any dividend is guaranteed.

– The stock value may rise or fall depending on the prospects for the company and market-wide circumstances.

3-11

Common Stock Price Quotes

3-12

Common Stock Price Quotes Onlineat http://finance.yahoo.com

First, enter symbol.

Resulting Screen

3-13

Preferred Stock• Information is a bit harder to find for preferred stock versus common stock.

• Example: Bank of America (BAC) preferred stock • Find all the BAC preferred stock issues via a Google search—one source

is: quantumonline.com.• One issue has a ticker of: BAC-J (BAC-PJ is its symbol at Yahoo!)

• Potential gains/losses:

– Dividends are “promised.” However, there is no legal requirement that the dividends be paid, as long as no common dividends are distributed.

– The stock value may rise or fall depending on the prospects for the company and market-wide circumstances.

3-14

Option Contracts, I.

• A call option gives the owner the right, but not the obligation, to buy something, while a put option gives the owner the right, but not the obligation, to sell something.

• The “something” can be an asset, a commodity, or an index.

• The price you pay today to buy an option is called the option premium.

• The specified price at which the underlying asset can be bought or sold is called the strike price, or exercise price.

3-15

Option Contracts, II.• An American option can be exercised anytime up to and

including the expiration date, while a European option can be exercised only on the expiration date.

• Options differ from futures in two main ways:

– Holders of call options have no obligation to buy the underlying asset.

– Holders of put options have no obligation to sell the underlying asset.

– To avoid this obligation, buyers of calls and puts must pay a price today. Holders of futures contracts do not pay for the contract today.

3-16

Option Contracts, III.

• Potential gains and losses from call options:

– Buyers:• Profit when the market price minus the strike price is greater than the option

premium. • Best case, theoretically unlimited profits.• Worst case, the call buyer loses the entire premium.

– Sellers:• Profit when the market price minus the strike price is less than the option

premium.• Best case, the call seller collects the entire premium.• Worst case, theoretically unlimited losses.

– Note that, for buyers, losses are limited, but gains are not.

3-17

Option Contracts, IV.

• Potential gains and losses from put options:

– Buyers:• Profit when the strike price minus the market price is greater than the option

premium. • Best case, market price (for the underlying) is zero. • Worst case, the put buyer loses the entire premium.

– Sellers:• Profit when the strike price minus the market price is less than the option

premium.• Best case, the put seller collects the entire premium.• Worst case, market price (for the underlying) is zero.

– Note that, for buyers and sellers, gains and losses are limited.

3-18

Option Contracts: Online Price Quotesfor Nike (NKE) options

Source: www.finance.yahoo.com

3-19

The New Method to Decode Option Symbols

• The method of decoding option symbols had been in place for years. – Seasoned option traders would recognize the symbol “NKELN”

as a December Nike call option with a strike of 70.– Note that Yahoo! Appends “.X” to this symbol.

• In 2010, the exchanges introduced a new option symbol system.– The symbols expand from 5 letters to 20 letters and numbers. – The stated goal is to reduce confusion by explicitly stating:

• the underlying stock symbol• option expiration date• whether the option is a call or a put• the dollar part of the strike price• the decimal part of the strike price

– We do not know whether quadrupling the size of the ticker will reduce confusion .

– We do know that the symbol for the December Nike 70 call options will change from “NKELN” to “NIKE 091219C00070000”.

3-20

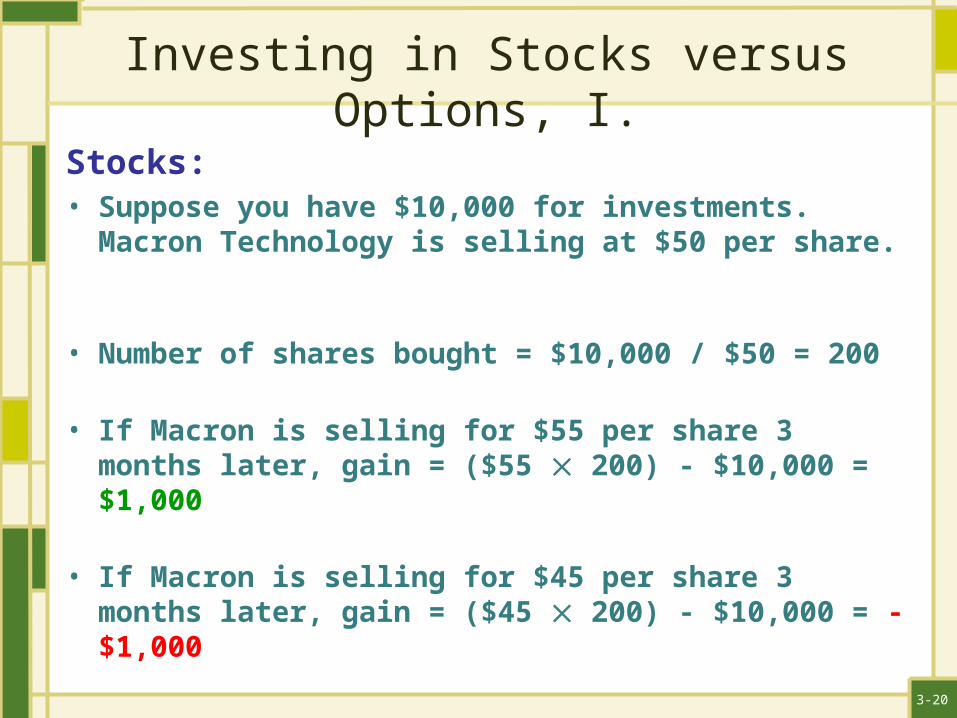

Investing in Stocks versus Options, I.

Stocks:• Suppose you have $10,000 for investments. Macron

Technology is selling at $50 per share.

• Number of shares bought = $10,000 / $50 = 200

• If Macron is selling for $55 per share 3 months later, gain = ($55 200) - $10,000 = $1,000

• If Macron is selling for $45 per share 3 months later, gain = ($45 200) - $10,000 = -$1,000

3-21

Investing in Stocks versus Options, II.Options:• A call option with a $50 strike price and 3 months to maturity is

also available at a premium of $4.

• Traded option contracts are on a bundle of 100 shares.

• One call contract costs $4 100 = $400, so number of contracts bought = $10,000 / $400 = 25 (for 25 100 = 2,500 shares)

• If Macron is selling for $55 per share 3 months later, gain = {($55 – $50) 2,500} - $10,000 = $2,500

• If Macron is selling for $45 per share 3 months later, loss = ($0 2,500) – $10,000 = -$10,000

3-22

Useful Internet Sites

• www.nasdbondinfo.com (current corporate bond prices)• www.investinginbonds.com (bond basics)• www.finra.com (learn more about TRACE)• www.fool.com (Are you a “Foolish investor”?)• www.stocktickercompany.com (reproduction stock tickers)• www.cmegroup.com (CME Group)• www.cboe.com (Chicago Board Options Exchange)• finance.yahoo.com (prices for option chains)• www.wsj.com (online version of The Wall Street Journal)

3-23

Chapter Review, I.

• Classifying Securities

• Interest-Bearing Assets

– Money Market Instruments– Fixed-Income Securities

• Equities

– Common Stock– Preferred Stock– Common and Preferred Stock Price Quotes

3-24

Chapter Review, II.

• Derivatives

– Futures Contracts– Futures Price Quotes– Gains and Losses on Futures Contracts

• Option Contracts

– Option Terminology– Options versus Futures– Option Price Quotes– Gains and Losses on Option Contracts– Investing in Stocks versus Options

Related Documents