CHAPTER III FINANCIAL POLICIES 1. DPE/Guidelines/III/1 Holding of shares in Government Companies in the names of the President of India and the Governor of a State. The undersigned is directed to refer to this Department’s Office Memorandum No.15/32/65-IGC dated the 13th October, 1965 on the above subject and to state that certain Ministries of the Government of India and State Governments have, on receipt of the above communication, raised a query as to whether the President or the Governor of a State will be deemed to be a corporation sole for purposes of holding shares in Government companies. This matter has, therefore, been examined in detail and the clarification as under is given for information and guidance of all concerned. 2. This Department had advised in the above Office Memorandum that shares in a Government company can not be registered in the name of a public office which is not a corporation sole as understood in law. Thus the shares in a Company can not be held in the name of the Collector of Central Excise or a Secretary to the Government of India, etc. This position may be followed in the case of holders of all public offices save as mentioned below. 3. The President or the Governor of a State functioning under the Constitution is not a corporated sole, just as the Administrator-General constituted under the Administrators General Act 1963, is. As provided by Article 77(1) and 166(1)of the Constitution, all executive action of the Government of India or the Government of a State shall be expressed to be taken in the name of the President or the Governor, as the case may be. "Executive action" or "executive power" has been broadly stated to be "the residue of Governmental functions that remain after legislative and judicial functions are taken away." Further it appears that the said articles are confined to cases where the executive action is required to be expressed in the shape of a formal order or notification or any other instrument. When an executive decision affects an outsider or is required to be officially notified or communicated, it should be normally expressed in the form mentioned in these Articles, that is, in the name of the President or the Governor, as the case may be. 4. The acquisition or holding of shares in a company by the Government of India or a State Government is "executive action" as contemplated by Articles 77(1) and 166(1) of the Constitution and can, therefore, be made in the name of the President of India or the Governor of the State, as the case may be. 5. In view of the above, shares in a Government company can be held in the name of the President of India or the Governor of a State. 6. The clarification as above is brought to the notice of all Ministries of the Government of India and State Governments for their information and guidance. (D/o Company Affairs No.15/32/65-IGC dated 30th September, 1966) ***

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER III FINANCIAL POLICIES

1. DPE/Guidelines/III/1 Holding of shares in Government Companies in the names of the President of India and the Governor of a State.

The undersigned is directed to refer to this Department’s Office Memorandum No.15/32/65-IGC dated the 13th October, 1965 on the above

subject and to state that certain Ministries of the Government of India and State Governments have, on receipt of the above communication,

raised a query as to whether the President or the Governor of a State will be deemed to be a corporation sole for purposes of holding shares

in Government companies. This matter has, therefore, been examined in detail and the clarification as under is given for information and

guidance of all concerned.

2. This Department had advised in the above Office Memorandum that shares in a Government company can not be registered in the name

of a public office which is not a corporation sole as understood in law. Thus the shares in a Company can not be held in the name of the

Collector of Central Excise or a Secretary to the Government of India, etc. This position may be followed in the case of holders of all public

offices save as mentioned below.

3. The President or the Governor of a State functioning under the Constitution is not a corporated sole, just as the Administrator-General

constituted under the Administrators General Act 1963, is. As provided by Article 77(1) and 166(1)of the Constitution, all executive action of

the Government of India or the Government of a State shall be expressed to be taken in the name of the President or the Governor, as the

case may be. "Executive action" or "executive power" has been broadly stated to be "the residue of Governmental functions that remain after

legislative and judicial functions are taken away." Further it appears that the said articles are confined to cases where the executive action is

required to be expressed in the shape of a formal order or notification or any other instrument. When an executive decision affects an

outsider or is required to be officially notified or communicated, it should be normally expressed in the form mentioned in these Articles, that

is, in the name of the President or the Governor, as the case may be.

4. The acquisition or holding of shares in a company by the Government of India or a State Government is "executive action" as

contemplated by Articles 77(1) and 166(1) of the Constitution and can, therefore, be made in the name of the President of India or the

Governor of the State, as the case may be.

5. In view of the above, shares in a Government company can be held in the name of the President of India or the Governor of a State.

6. The clarification as above is brought to the notice of all Ministries of the Government of India and State Governments for their information

and guidance.

(D/o Company Affairs No.15/32/65-IGC dated 30th September, 1966)

***

CHAPTER III

FINANCIAL POLICIES

2. DPE/Guidelines/III/2

Guarantees by Central Government

The undersigned is directed to say that the question of laying down formally the criteria and

procedures to be followed while giving Central Government guarantees in respect of the

borrowings etc. of Public Sector and Private Institutions has been considered. The Public

Accounts Committee has also from time to time, made recommendations in this regard. After

taking these into account and also the existing practices, it has been decided to prescribe the

following criteria and procedures for considering proposals for guarantees by Central

Government:

(i) Any proposal for guarantee by Government must be justified by public interest.

Public interest can not be precisely defined. However, the following may be considered to be an

illustrative list:

a. borrowings by public sector institutions for approved developmental purposes e.g., from

foreign lending agencies and public sector financial institution if so required by their

charters and from banks of public in order to enable the institutions to borrow on

reasonable terms;

b. borrowings by public sector undertakings from banks for working capital purposes e.g. in

respect of margin money for cash credit accommodation or before commencement of

production when hypothecation for cash credit may be somewhat difficult – the Bureau

of Public Enterprises have already laid down certain guidelines in this regard vide their

OM No.2(32) F1 dated 16th March, 1967 sometimes counter-guarantees against

guarantees given by banks to foreign suppliers against deferred payment facilities may

also become necessary; and

c. borrowings of non-public sector institutions if justified on broad policy and similar

consideration e.g. borrowings for approved developmental purposes from foreign lending

agencies or public sector financial institutions by private concerns, if so required by the

charters of the concerned agencies or institutions: financial requirements of sugar Mills,

Sate Cooperative Banks in Union Territories or Central Land Mortgage Banks, in

pursuance of policy decisions: financial requirements of textile mills and the like, facing

closure or other difficulties, which are to be supported in pursuance of policy decisions,

etc.

(ii) The proposal for a guarantee, which amounts to undertaking a contingent liability, should be

examined in the same manner as proposal for a loan. This would mean that the proposal should

be examined in the concerned administrative Ministry with reference to:

a. the public interest which the guarantee will serve;

b. the credit-worthiness of the borrowed in order to see whether any undue risk would be

taken by giving the guarantee;

c. the terms of the borrowings in the case of market borrowings and negotiated loans from

financial institutions to see that they are not out of line with those approved by the

Reserve Bank; and

d. the conditions, if any, which should be made by Government while giving the guarantee

e.g. period of guarantee, levy of a fee to cover the risk, representation for Government on

the Board of Management, mortgage or lien on the assets, submission to Government of

periodical reports and accounts, right to get the accounts audited on behalf of

Government, etc. In general these questions will arise only in the case of non-public

sector institutions and even if fee, representation and mortgage are not considered

necessary, the right to verify the continued credit-worthiness of the borrower should be

ensured.

Thereafter the proposal should be referred to the Associate Finance Division for concurrence.

The latter should consult the Internal Finance Division (Banking Section) of the Economic

Affairs Department where borrowings from banks are proposed. Budget Division where market

borrowings or negotiated loans from financing institutions are proposed and External Finance

Division where borrowings from foreign lending agencies or counter guarantees to banks for

guarantees given to foreign lending agencies or suppliers are involved. Where guarantees to

public sector financing institution are involved the Internal Finance Division (Corporation

Branch) should be consulted.

As a rule the amounts involved will be large and it is necessary that the decision to give a

guarantee is taken at a sufficiently high level. In so far as public sector institutions are concerned,

individual cases involving less than Rs.50 lakhs may be decided at Joint Secretary’s level and

those in excess of this limit at Secretary’s level—both in the administrative Ministry and in the

Expenditure Department. Insofar as private institutions are concerned, however, all cases of

guarantees may be preferably got approved by Minister and those involving amounts exceeding

Rs.10 lakhs each case (each institution or group of institutions if the same party is connected

with it)—the limit being applied after taking into account the guarantees already given in respect

of the institution or group of institutions—may be considered for being submitted to the Cabinet

for approval.

(iii) Each case of guarantee should be periodically (at least annually) reviewed to see that the

need for guarantee continues and that Government’s interest continues to be safe/safeguarded.

For this purpose, the published accounts of the borrower should be scrutinised and periodical

reports etc. called for from the borrower as also from the Government representative on the

Board of Management, if any. Wherever necessary or justified, action to withdraw the guarantee

should be taken.

(iv) All cases of guarantees (whether given or withdrawn) should be reported to the Budget

Division for Central record. All payments made in pursuance of the guarantees given should also

likewise be reported for record. The proforma in which this information should be furnished is at

Annexure. The first return should cover guarantees given and outstanding as on 31st March,

1969 as also the information for the month of April 1969. The returns should reach the Budget

Division by the 15th of the month following that to which they pertain.

2. It is requested that the requirements of this Office memorandum may be scrupulously

observed in future.

(Deptt. of Economic Affairs No. F.18(1)W&M/69 dated 3rd May, 1969)

***

CHAPTER III

FINANCIAL POLICIES

3. DPE/Guidelines/III/3

Issue of Guarantee and Performance Bond

Kindly refer to the O.M. No.BPE/1(4)/Adv (Fin) 68 dated 19th April, 1969 in which

Government have agreed to the L.I.C. having pari passu charge with the Government on the

fixed assets of the enterprises for considering the request from Public Enterprises for the issue of

guarantee and performance bonds. In this connection, recently the following questions have been

raised for clarifications:–

a. If provision of the O.M. dated 19.4.69 would imply generally clearance from the

President, according permission to LIC having pari passu charge on the fixed assets of

the undertakings or a separate communication granting such permission in each case

would be necessary; and

b. If such a communication is necessary whether a reference to Associate Finance and the

Budget Division and Bureau are called for.

2. The matter has been considered in the Finance Ministry and it has been decided that as and

when it becomes necessary to have LIC a pari passu charge with the Government on the fixed

assests of the Public Enterprises, it would be necessary for an enterprise to make a specific

reference to the Administrative Ministry who will accord a specific approval in consultation with

the Associate Finance. It may not be necessary to refer each case individually to the Budget

Division and the Bureau of Public Enterprises for specific approval. However, copies of the

permissions issued in favour of LIC having a pari passu charge be endorsed to both the Budget

Division and the Bureau of Public Enterprises.

3. The Ministry of Industrial Development etc. are requested to bring the contents of this OM to

the notice of Public enterprises under their control.

(DPE No. BPE/1(4)/Adv.(F)/69 dated 30th May, 1970)

ANNEXURE

PROFORMA

No.

Government of India

Ministry/Department of

Statement showing guarantees given/withdrawn by the Central Government during the

month of ………………..

1. Name of the institution in respect of which guarantee

given/withdrawn Public/Private Sector

2. Name of the institution to/from whom guarantee

given/withdrawn

3. No. and date of the letter in which guarantee given/withdrawn

4. Level at which decision to give/withdraw guarantee taken

5. Details of the guarantee given:

a) Precise purpose

a. *Maximum Amount of guarantee (In rupees)

b. Guarantee valid upto

c. *Sums guaranteed outstanding at the end of the month

d. Steps taken to safeguard Government interest

e. Conditions, if any, on which guarantee given (e.g. pledging

of securities as a set off against the guarantee, fees levied

etc.)

f. Rate of interest involved, if any (Per cent per annum)

6. Amount if any paid by Govt. against the guarantee and the steps

taken to recover the same from the institution concerned.

7. No. and date of the previous return.

Note :

1. Where more than one guarantee has been given in respect of an institution, details

of each guarantee should be furnished separately.

2. If no guarantee has been given/withdrawn during a month, a ‘nil’ return need not

be sent.

* In the case of guarantees given in foreign currencies, the amount in foreign currency

should be shown in brackets.

CHAPTER III FINANCIAL POLICIES

4. DPE/Guidelines/III/4 Guarantees by Central Government

The undersigned is directed to invite a reference to this Ministry’s O.M. No. F.18(1)-W&M/69 of 3rd May, 1969 on the subject mentioned

above. In accordance with the procedure prescribed therein, the administrative Ministries, after satisfying themselves of the need for giving a

guarantee, should refer the proposal to their Associate Finance Division for concurrence. The latter are required to consult the Department of

Banking where the proposal involves borrowings from banks or guarantees to financial institutions in the Public Sector. Similarly where the

proposal involves market borrowings or negotiated loans from financing institutions, the Budget Division of this Department, and where it

involves borrowings from foreign lending agencies or where it is proposed to give a counter-guarantee to Banks against their guarantees to

foreign suppliers, the E.F. Division of this Department, are to be consulted.

2. The working of the above procedure has been reviewed in the light of the experience gained so far and it has been found that in some

cases, consultations with various Departments by the Associate Finance Divisions result in avoidable delays. It has, therefore, been decided

that henceforth the following revised procedure should be adopted in examining proposals for guarantees by Government:

(i) Every proposal should first be examined in the Administrative Ministry concerned in the manner indicated in this Ministry’s O.M. dated

3.5.1969.

(ii) Thereafter the proposal should be referred to the Associate Finance Division for concurrence. That Division will take action as follows:

a. Proposals involving borrowings from Banks/guarantees to Public Sector Financial Institutions

If the Associate Finance Division are satisfied about the proposal they may themselves concur in the proposal. However, if the proposal

discloses some unusual features, a reference to the Department of Banking may be made at the discretion of the Associate Finance Division.

b.Proposals involving borrowing from foreign lending agencies

If the Associate Finance Division are satisfied about the merits of the case they may concur in the proposal. However, if the case presents

any unusual feature, the concerned Division of the Department of Economic Affairs may be consulted.

c. Proposal for counter-guarantees to banks against their guarantees to foreign suppliers

Normally, Public Sector Undertakings should approach banks for guarantees and it is only in exceptional cases e.g. where the banks are not

satisfied about the liability or finances of the projects and, therefore, a bank guarantee will not be available, that a proposal for counter-

guarantee by Government is likely to be made. In such cases, there would be no particular advantage in giving counter-guarantees by

Government. The preferable course would be for Government to give straight guarantees to the foreign lending agencies/suppliers, provided

the agencies/suppliers find this arrangement acceptable. No consultation with the E.F.Division is normally necessary in such cases.

d. Proposals involving market borrowing/negotiated loans

Such proposals may continue to be referred to the Budget Division with the recommendations of the Associate Finance Division.

3. The other conditions and procedure to be observed in connection with the grant of guarantees, in particular the level at which the decision

is to be taken, as laid down in this Ministry’s O.M. dated the 3rd May, 1969 remain unchanged and will continue to be observed.

4. The Administrative Ministry should undertake a consolidated review of all the Government guarantees given during a financial year and

such reviews after being seen by the Associate Finance Division may be referred to the Department of Banking or the concerned E.F.

Division as the case may be, as also the Bureau of Public Enterprises. Such reviews would help to assess the actual performance of the

guarantees and would enable a decision to be taken whether any modification in the criteria already laid down is necessary.

5. All cases of guarantees (whether given or withdrawn) should be reported by the Associate Finance Division to the Budget Division. All

payments made in pursuance of such guarantees should also be reported by the Associate Finance Division to the Budget Division.

(Deptt. of Economic Affairs No. F.7(6)-PD/70 dated 27th June, 1970)

***

CHAPTER III FINANCIAL POLICIES

5. DPE/Guidelines/III/5 Issue of Bank Guarantee in respect of advances paid by the Central Government Departments to the State level enterprises—Clarifications.

Reference is invited to BPE’s O.M. No. BPE/19(2)/Adv.(F)/83 dated the 27th October, 1983, regarding the question of obtaining guarantees

from the State Governments in respect of advances paid by central public enterprises to State level public enterprises. As central public

enterprises were expected to observe normal business principles and undertake profitable operations, it was clarified therein that they had

the discretion to take a view in this regard.

2. The question whether the Central Government Departments should insist on guarantees from State Governments in respect of advances

paid by these Departments to State level public enterprises, has been examined and it has been decided that Departments may treat State

Government undertakings on par with Central public enterprises depending on the circumstances of the case.

(DPE No. BPE/19(2)/Adv.(F)/83 dated 2nd July, 1984)

***

CHAPTER III

FINANCIAL POLICIES

6. DPE/Guidelines/III/6

Banking arrangements of Central Government Public Enterprises.

Reference is invited to this office Memorandum No.BPE/1(86)/ Adv(F)/72 dated 7th May 1973

and OM No. BPE/1(24)/87-Fin (PPU) dated 10th April, 1987 on the subject cited (copy

enclosed) above. The extant policy that Public Sector Enterprises should have banking

arrangements only with public sector banks has since been reviewed and it has now been decided

that Central Public Sector Enterprises can undertake normal banking transactions with any bank

of their choice including foreign/private sector banks.

Enclosure: Copy of OM No. BPE/1(24)/87-Fin.(PPU) dt. 10th April, 1987

Regarding: Banking arrangements and financing of working capital requirements of Public

Sector Enterprises.

A reference is invited to this office O.M. No. BPE/1(86)/Adv.(F)/72 dated 7th May, 1973 on the

subjected cited above (copy enclosed).

1. Subsequent to the issue of the above instructions, six more banks were nationalized in

1980. These six Banks, namely Andhra Bank, Corporation Bank, New Bank of India,

Oriental Bank of Commerce, Punjab & Sind Bank and Vijaya Bank would be in a

position to provide adequate banking facilities to any public undertaking which is

desirous of having banking arrangements with these banks. Public Sector Undertakings

can have dealings with these banks also according to their needs and commercial

judgements.

2. Administrative Ministries/Departments are requested to bring these instructions to the

notice of all Public Sector Undertakings under their control for information and necessary

action.

Enclosure: Copy of OM No.BPE/1(86)/Adv.(F)/72 dated 7th May 1973

Regarding: Banking arrangements and financing of working capitals requirements of public

sector enterprises.

A reference is invited to O. M. No. F.7(4)/BOIII/72 dated the 22nd May, 1972, from the

Department of Banking and O.M. No. BPE/1(49)/Adv.(F)/71 dated the 24th July, 1971, from the

Bureau of Public Enterprises as the subject indicated above.

2. The provisions of the O.M’s require inter alia that:–

i. All public sector enterprises should maintain their accounts only with the State Bank of

India including its subsidiaries or with any of the 14 Nationalized Banks;

ii. If any existing undertaking needs additional working Capital requirement it should in the

first instance approach its principal banker and if that bank finds it difficult to provide

additional requirement from its own resources, it will in consultation with the

undertaking, initiate arrangements for participation with the public sector banks.

3. According to a review made by the Bureau, certain enterprises are still maintaining banks

arrangements and cash credit facilities with non-nationalized banks.

4. Ministry of Commerce, etc., are requested to examine the necessity for continuing the banking

account with non-nationalized banks which some of the public sector undertakings are operating

at present.

(DPE O.M. No. DPE/14(19)/ 90-Fin dated 3rd January, 1992)

***

CHAPTER III

FINANCIAL POLICIES

7. DPE/Guidelines/III/7

Schemes for dividend, bonus shares etc., in respect of PSU shares disinvested in 1991-92 &

1992-93.

The Government of India had disinvested shares of some of the PSEs to various financial

institutions/mutual funds and merchant banks in 1991-92 and 1992-93. As per the procedure

followed for transfer of shares from the name of President of India to these institutions, all the

financial institutions/ mutual funds and merchant banks were required to submit duly completed

and stamped transfer deeds in Form 7B with the respective administrative Ministries. Thereafter,

the administrative Ministries/Departments were to sign on the transfer documents on behalf of

President of India and to send the same to the respective PSUs for transfer of the shares in favour

of the buying financial institution/mutual fund and merchant bankers. On receipt of duly signed,

executed and stamped transfer deed in Form 7B, the PSUs were required to transfer the shares in

the name of the buying institutions.

2. It has been brought to the notice of Department of Public Enterprises that the above procedure

for transfer of shares from President of India to the respective buying institution has taken

considerable time. Meanwhile, some of these PSUs have declared dividends, bonus shares etc.,

for the year

1991-92 and 1992-93 in respect of the shares disinvested by Government of India.

3. The Department of Public Enterprises has received a number of references from various

financial institutions and Ministries regarding entitlements of the financial institutions to

dividends, bonus shares etc., declared in respect of shares disinvested for the year 1991-92 and

1992-93.

4. It has been decided in consultation with the Ministry of Finance that any benefit on the shares

declared by the companies after the date the buyers paid the purchase consideration should be

viewed as constructively accruing to them. Since the prices at which these institutions had bid for

the shares were based on the company’s book values, which got diluted with any subsequent

bonus and other benefits, it is necessary that the benefits should logically belong to the buyers.

5. In view of the above, the Ministries/Departments of Government of India are requested to

instruct the concerned PSUs under their administrative control wherein disinvestment has taken

place during 1991-92 and 1992-93 to transfer to the buyers the dividends and other benefits after

the date the respective buyers had paid the purchase consideration to Government of India.

(DPE O.M. No. DPE/12(4)/91-Fin. dated 25th February, 1994)

***

CHAPTER III FINANCIAL POLICIES

8. DPE/Guidelines/III/8 Renunciation of Right Issues of PSUs.

Several Central Public Sector Undertakings (PSUs) are coming up with proposals regarding Right Issues in order to augment their capital

base and get additional funds by way of premium. In such cases, the administrative Ministries would have to decide whether Rights should

be renounced or subscribed. The matter has been considered carefully by the Government and the following procedures have been

prescribed in the case of renunciation of the shares by the President.

(i) The decision to renounce the rights or not is a substantive decision which will be taken by the concerned Ministry with the concurrence of

Ministry of Finance.

(ii) Upon taking a decision to renounce, the Ministry should advise the PSU to arrange with the merchant banker retained to manage the

rights issue to invite mutual funds/financial institutions (both private and public sector) and other agencies which in the opinion of the

merchant banker will be interested in buying the renunciation to submit bids.

(iii) The bids to be addressed to the PSU will be evaluated by the PSU and the merchant bank in the descending order of the renunciation

premium offered. Thereafter the administrative Ministry will issue an acceptance based on which the PSU will collect the amount from one or

more successful buyers and credit the amount to the designated account of GOI.

(iv) No fees will be payable to the merchant banker by the Government for the above service which should be part of the package to manage

the PSU’s right issue.

(v) The reserve price for renunciation of Rights would be decided by the concerned Administrative Ministry in consultation with the merchant

banker taking all factors including market conditions into account. This will be the minimum price at which the Right could be renounced by

the administrative Ministry on behalf of the President in the auction method to be handled by the same merchant banker who is entrusted

with the Rights Issues management. In case some rights of the President could not be sold in the auction, the merchant banker can be

offered first these unsold Rights at the reserve price. On his acceptance at this price, these Rights may also be renunciated.

(vi) All steps required for selling the Rights issue of Government on renunciation will be undertaken by the merchant banker as per instruction

from the administrative Ministries in accordance with the provisions of Company Law, SEBI guidelines rules in force.

(vii) However, the administrative Ministry can take a decision with the concurrence of Ministry of Finance whether the Government could still

subscribe for the unsold Rights before offering them to the merchant banker at the reserve price or in case the merchant banker is not

interested in accepting the same fully or partially.

(viii) The merchant banker is required to manage all actions in connection with renunciation of Rights.

These instructions may be brought to the notice of all the PSUs for necessary action.

(DPE O.M. No. DPE/12(19)/93-Fin. dated 15th March, 1994)

***

CHAPTER III

FINANCIAL POLICIES

9. DPE/Guidelines/III/9

Investment of surplus funds, procedures of investments, banking transactions,

responsibilities of Board of Directors, etc.—Recommendations of the Joint Parliamentary

Committee.

The undersigned is directed to say that the Joint Parliamentary Committee (JPC) in their report

on "irregularities in securities and banking transactions" have made a number of

recommendations covering the areas mentioned above. These recommendations have been

considered by the Government. The decisions of the Government on these recommendations are

given below for information and necessary action by the respective administrative Ministries and

the public sector enterprises.

i. It was noted by the Committee that while the Government permitted PSUs to have

banking transactions with foreign banks, it was not monitored properly. The Government

have decided that the administrative Ministries dealing with particular PSU should

monitor adherence to all guidelines issued by the Government. The PSUs should report to

the administrative Ministry in case of inability to comply with particular guidelines and

the Ministry will consider condonation or enforcement by issue of a Presidential

directive. In this connection, attention is also invited to the Department of Public

Enterprises OM No. 6/6/88-Coord. dated 8.4.91 wherein it is indicated that the Boards of

Directors of the PSUs will have the discretion not to adopt these guidelines for reasons to

be recorded in writing. 'The Board Resolution on the subject given the reasons therein

should be forwarded both to the administrative Ministries as well as to the DPE. The

valid reasons should be fully rendered in speaking orders/ resolutions.

ii. On an observation of the Committee about the policies and procedures followed by the

public sector undertakings in respect of the investments of their surplus funds, the

Government have taken note of the fact that the policies and procedures followed by the

PSUs in many cases were not in conformity with the guidelines and did not satisfy

acceptable norms. The administrative Ministries are requested to take appropriate action

to demarcate the responsibilities of the Government in its different

Ministries/Departments and their nominee Directors as well as the Board of the Public

Sector Undertakings, the whole time Directors and its top managers. By effective

performance of their respective functions, these agencies should ensure laying down the

correct policies and procedures and monitor their faithful implementation.

iii. The Committee have raised the question of the duty and responsibility for ensuring,

implementation of guidelines. It is the primary responsibility of the PSU itself to abide by

Governmental guidelines. Government recognizes that the prime duties of a Government

nominee on the Board of Directors of a PSU are to safeguard the interest of the

shareholders, contribute to the efficient functioning of the PSUs and report back the same

regularly to the Government. The Department of Public Enterprises and the Cabinet

Sectt. had earlier issued instructions in this regard. DPE OM No. 18/1/84-GM dated 19th

September, 1984 and Cabinet Sectt. D.O. Letter No. 6/l/7/92-CAB dated 30th September,

1992, addressed to the Secretaries of administrative Ministries may be referred to this

matter . The administrative ministries are requested to take action in order to ensure that

the nominee Directors comply with the responsibility cast on them and the instructions

issued already on the subject are reiterated.

iv. With regard to investment of surplus funds, the Committee have suggested that the

policies should be clear-cut and transparent. Administrative Ministries are requested to

lay down guidelines for different types of PSUs under their control indicating the

destination and procedures of investment of their surplus funds. Administrative

Ministries are also requested to direct the Boards of Directors of their PSUs to the effect

that instructions regarding investment of fund shall be transparent and taken only by the

delegated authority and that exercise of such authority shall be monitored by the Board.

The administrative Ministries are also desired to lay down guidelines for the PSU under

their control in the matter of regular reporting of financial transactions to the Board

having regard to the nature of its business, size of financial transactions and the level to

which the financial powers have been delegated.

v. Boards of Directors of all non-financial PSUs should ensure that decisions regarding

investments of funds are transparent and taken only by the delegated authority, and that

the proper exercise of such authority is monitored by the Board. Boards of all PSUs are

directed to lay down clear policies on investment of surplus funds, establish transparent

procedures, review delegation of authority and prescribe regular reporting of investments

to the Board. The streamlining of policies and procedures is to be with the knowledge of

the administrative Ministry and as and when required, the Board will be given guidance

by the administrative Ministry. The latter will include the performance of the company in

this sphere as one of the items to be considered in its periodic reviews. The administrative

Ministry, in turn, will seek the guidance of the DPE and the Ministry of Finance and

follow up closely the implementation of the policies on investment laid down by these

Ministries. Administrative Ministries are requested to ensure that this course of section is

carefully followed by all concerned.

vi. The administrative Ministries and the Public Enterprises are advised to keep the decisions

of the Government on these various recommendations of the JPC in view and take

appropriate measures in accordance with the Government decision indicated above. The

Ministries may, in turn, issue suitable instructions to the enterprises for strict compliance.

The action taken in this matter may be intimated to the Department of Public Enterprises.

(DPE O.M. No.DPE/4/3/92-Fin. dated 27th June, 1994)

***

CHAPTER III FINANCIAL POLICIES

10. DPE/Guidelines/III/10 Guidelines for Investment of Surplus Funds by Public Sector Enterprises

The Joint Parliamentary Committee [JPC] which enquired into the irregularities in securities transactions had adversely commented on

certain investment decisions made by certain PSEs. The Committee had desired that Government should lay down clear guidelines

governing investment of surplus funds by Public Sector Enterprises to avoid recurrence of instances of misuse of funds.

Principles concerning investments

2. The Government have considered the observations of the Committee. The undersigned is directed to advise that PSEs should observe the

following guidelines in regard to investment of surplus funds:

i. Investments should be made only in instruments with maximum safety.

ii. There should be no element of speculation on the yield obtaining from the investment.

iii. There should be a proper commercial appreciation before any investment decision of surplus funds is taken. The surplus

availability may be worked out for a period of minimum one year at any point of time.

iv. Funds should not be invested by the PSE at a particular rate of interest for a particular period of time while the PSE is resorting to

borrowing at an equal or higher rate of interest for its requirements for the same period of time.

v. Investment decision should be based on sound commercial judgement. The availability should be worked out based on cash flow

estimates taking into account working capital requirements, replacement of assets and other foreseeable demands.

vi. The remaining period of maturity of any instrument of investment should not exceed one year from the date of investment where

the investment is made in an instrument already issued. Where investment is made in an instrument newly issued, the final

maturity of the instrument should not exceed one year. However, only in the case of term deposits with banks, it can be up to

three years.

Eligible Investments

3. Investments may be made in one or more of the following instruments, subject to principles outlined in the previous paragraph:

i. Term deposits with any scheduled commercial bank [i.e., banks incorporated in India] and with a paid up capital of atleast Rs. 100

Crores, fulfilling the capital adequacy norms as prescribed by the R.B.I. from time to time. These adequacy norms should be

reflected in the last published balance sheet.

ii. Instruments which have been rated by an established Credit Rating Agency and have been accorded the highest credit rating

signifying highest safety e.g. certificates of deposits, deposits schemes or similar instruments issued by scheduled commercial

banks/term lending institutions including their subsidiaries, as well as commercial paper of corporates.

iii. Inter-corporate loans are permissible to be lent only to Central PSEs, which have obtained highest credit rating awarded by one of

the established Credit Rating Agencies for borrowings for the corresponding period.

iv. Any debt instrument, which has obtained highest credit rating from an established Credit Rating Agency.

4. Authority Competent to Invest

i. Decisions on investment of surplus funds shall be taken by the Public Sector PSU Board. However, decisions involving investing

short-term surplus funds up to one year maturity may be delegated up to prescribed limits of investment, to a designated group of

Director[s], which should invariably include CMD & Director (Finance)/Head of Finance internally. Where such delegation is made,

the delegation order should spell out the levels of approval and the powers of each official, which should be strictly observed.

Where such delegation is exercised, there should be a proper system of automatic internal reporting to the Board at its next

meeting in all cases.

ii. PSEs should ensure that all investment decisions are in accordance with the regulations as per the Company Law & Government

of India instructions and any other relevant legislation and rules as applicable. Any investment already made, which is not in

conformity with the above guidelines should not be renewed after maturity.

5. Every PSE should arrange to place the above guidelines at its next Board Meeting and evolve a suitable procedure to cover investment of

surplus funds to be followed by company.

6. Necessary instructions may be issued for strict compliance of these guidelines.

7. These guidelines issue in consultation with the Ministry of Finance.

(DPE O.M. No.4/6/94-Fin. dated 14th December, 1994)

***

CHAPTER III

FINANCIAL POLICIES

12. DPE/Guidelines/III/12

Issue of Bonus Shares by Public Sector Undertakings simplifying the Procedures.

It has come to the notice of the Govt. that a number of Central Govt. Public Sector Undertakings are carrying substantial reserves in their

balance sheets against a relatively small paid up capital base. The question of the need for these enterprises to capitalize a portion of their

reserves by issuing Bonus Shares to the existing shareholders has been under consideration of the Govt.

2. The issue of Bonus Shares helps in bringing about at proper balance between paid up capital and accumulated reserves, elicit good public

response to equity issues of the public enterprises and helps in improving the market image of the company.

3. Therefore, the Government has decided that the public enterprises, which are carrying substantial reserves in comparison to their paid up

capital sold issue Bonus Shares to capitalize the reserves for which the following norms/conditions and criteria may be followed and fulfilled.

4. SEBI guidelines may be followed in deciding the correct proportion of reserves to be capitalized by issuing Bonus Shares. A copy of the

bonus issue guidelines of SEBI is enclosed.

5. For the purpose of determining the quantum of bonus issue, PSUs should be guided by the following factors:

(i) Likely increase in capital base from fresh public issues by PSUs in the next two to three years (which will dilute the GOI’s equity).

(ii) PSUs should prepare profit projections for the next three years on realistic basis as projected by them in their corporate plan and estimate

their ability to service the enlarged equity after taking into account any fresh equity issue they expect to make for their

expansion/diversification needs.

6. PSUs are at liberty to engage public/private sector merchant bankers to determine the quantum of bonus and provide advice on related

matters. The mode of selection of merchant bankers and any fee payable for their services may be decided by PSU Boards.

7. While recommending proposals for capitalizing reserves, PSUs should also consider the need for increasing their authorized capital to

accommodate the release of bonus shares and any subsequent public issues and recommend increase in the capital where necessary.

8. PSUs should ensure that after making the bonus there are enough reserves left which together with future plough-back of profit will be

sufficiently large to inspire confidence and support from existing and potential shareholders. This is necessary to remain as an attractive scrip

in the market.

9. Each administrative Ministry may direct the enterprises under their control that PSUs having reserves in excess of three times their paid-

up capital should immediately consider the scope for issuing bonus shares to GOI (and pro-rata to other existing shareholders if partial

disinvestment had occurred so far). PSUs having large reserves may be allowed to make any public issue only after examining the scope for

capitalizing a portion of reserves.

10. Ministries/Departments should expeditiously examine and approve bonus issue proposals if the quantum of bonus and profit projections

are found to be properly assessed and the PSUs certify that the proposals are in conformity with the SEBI guidelines.

11. Bonus issue proposals need not be referred to Ministry of Finance (MoF) for approval unless there are special reasons to do so. Likewise

proposals involving increase in authorized capital need not be referred to MoF. It has been clarified earlier that increase in authorized capital

does not require Cabinet approval.

12. Ministries should keep the Department of Public Enterprises informed about bonus issue proposals and authorized capital increases

approved by them.

13. The above conditions shall cut down the procedural delays in obtaining the approval for bonus shares besides enabling the PSUs to

finalize public issue plans quickly and tap the capital market when conditions are favourable.

14. The Financial Advisers in the administrative Ministries shall keep a control over the fulfillment of various conditions/criteria as mentioned

above before agreeing to the bonus issues.

(DPE O.M. No. DPE/12(6)/95-Fin. dated 10th November, 1995)

ENCLOSURE

Copy of Securities and Exchange Board of India (SEBI)’ s guidelines dated 13th April, 1994 for Disclosure and Investor

Protection—Bonus Issue Guidelines.

In keeping with current pace of liberalization and reforms in the Primary Market, the Board of SEBI has decided to modify the extant

guidelines for bonus shares, forming Section M of the Guidelines for Disclosure and Investor Protection issued by SEBI on June 11, 1992.

SEBI believes that the Board of Directors of the companies wishing to make bonus issues will take into due consideration the relevant

financial factors while deciding on bonus issues and observe the following guidelines.

Section M

(i) These guidelines are applicable to existing listed companies who shall forward a certificate duly signed by the issuer and duly

countersigned by its statutory auditor or by a company secretary in practice to the effect that the terms and conditions for issue of bonus

shares as laid down in these guidelines, have been complied with.

(ii) Issue of bonus shares after any public/right issue is subject to the condition that no bonus issue shall be made which will dilute the value

or rights of the holders of debentures, convertible fully or partly.

In other words, no company shall, pending conversion of FCDs/PCDs, issue any shares by way of bonus unless similar benefit is extended

to the holders of such FDCs/PCDs, through reservation of shares in proportion to such convertible part of FCDs or PCDs. The shares so

reserved may be issued at the time of conversion(s) of such debentures on the same terms on which the bonus issues were made.

(iii) The bonus issue is made out of free reserves built out of the genuine profits or share premium collected in cash only.

(iv) Reserves created by revaluation of fixed assets are not capitalized.

(v) The declaration of bonus issue, in lieu of dividend, is not made.

(vi) The bonus issue is not made unless the partly-paid shares, if any existing, are made fully paid-up.

(vii) The Company –

1. has not defaulted in payment of interest or principal in respect of fixed deposits and interest on existing debentures or principal on

redemption thereof and.

2. has sufficient reason to believe that it has not defaulted in respect of the payment of statutory dues of the employees such as contribution

to provident fund, gratuity bonus etc.

(viii) A company, which announces bonus issue after the approval of the Board of Directors must implement the proposals within a period of

six months from the date of such approval and shall not have the option of changing the decision.

(ix) There should be a provision in the Articles of Association of the company for capitalization of reserves, etc. and if not, the company shall

pass a Resolution at its General Body Meeting making provisions in the Articles of Association for capitalization.

(x) Consequent to the issue of bonus shares if the subscribed and paid-up capital exceed the authorized capital, a Resolution shall be

passed by company at its General Body Meeting for increasing the authorized capital.

ENCLOSURE

Copy of Securities and Exchange Board of India (SEBI)’s RMB (DIP Series) Circular No. 2(94-95) dated 15th April, 1994 – Guidelines

for Disclosure and Investor Protection.

In tune with the process of liberalization and reforms in the primary market, it has been decided to modify the extant guidelines for issue of

bonus shares contained in Section M of the guidelines for Disclosure and Investor Protection issued by SEBI on June 11, 1992. The revised

guidelines have done away with certain requirements relating to issue of bonus, namely profitability Test, Residual Reserves Test etc.

A copy of the Press Release dated April 13, 1994 issued by SEBI in this connection is enclosed for your information.

CHAPTER III

FINANCIAL POLICIES

12. DPE/Guidelines/III/12

Issue of Bonus Shares by Public Sector Undertakings simplifying the Procedures.

It has come to the notice of the Govt. that a number of Central Govt. Public Sector Undertakings are carrying substantial reserves in their

balance sheets against a relatively small paid up capital base. The question of the need for these enterprises to capitalize a portion of their

reserves by issuing Bonus Shares to the existing shareholders has been under consideration of the Govt.

2. The issue of Bonus Shares helps in bringing about at proper balance between paid up capital and accumulated reserves, elicit good public

response to equity issues of the public enterprises and helps in improving the market image of the company.

3. Therefore, the Government has decided that the public enterprises, which are carrying substantial reserves in comparison to their paid up

capital sold issue Bonus Shares to capitalize the reserves for which the following norms/conditions and criteria may be followed and fulfilled.

4. SEBI guidelines may be followed in deciding the correct proportion of reserves to be capitalized by issuing Bonus Shares. A copy of the

bonus issue guidelines of SEBI is enclosed.

5. For the purpose of determining the quantum of bonus issue, PSUs should be guided by the following factors:

(i) Likely increase in capital base from fresh public issues by PSUs in the next two to three years (which will dilute the GOI’s equity).

(ii) PSUs should prepare profit projections for the next three years on realistic basis as projected by them in their corporate plan and estimate

their ability to service the enlarged equity after taking into account any fresh equity issue they expect to make for their

expansion/diversification needs.

6. PSUs are at liberty to engage public/private sector merchant bankers to determine the quantum of bonus and provide advice on related

matters. The mode of selection of merchant bankers and any fee payable for their services may be decided by PSU Boards.

7. While recommending proposals for capitalizing reserves, PSUs should also consider the need for increasing their authorized capital to

accommodate the release of bonus shares and any subsequent public issues and recommend increase in the capital where necessary.

8. PSUs should ensure that after making the bonus there are enough reserves left which together with future plough-back of profit will be

sufficiently large to inspire confidence and support from existing and potential shareholders. This is necessary to remain as an attractive scrip

in the market.

9. Each administrative Ministry may direct the enterprises under their control that PSUs having reserves in excess of three times their paid-

up capital should immediately consider the scope for issuing bonus shares to GOI (and pro-rata to other existing shareholders if partial

disinvestment had occurred so far). PSUs having large reserves may be allowed to make any public issue only after examining the scope for

capitalizing a portion of reserves.

10. Ministries/Departments should expeditiously examine and approve bonus issue proposals if the quantum of bonus and profit projections

are found to be properly assessed and the PSUs certify that the proposals are in conformity with the SEBI guidelines.

11. Bonus issue proposals need not be referred to Ministry of Finance (MoF) for approval unless there are special reasons to do so. Likewise

proposals involving increase in authorized capital need not be referred to MoF. It has been clarified earlier that increase in authorized capital

does not require Cabinet approval.

12. Ministries should keep the Department of Public Enterprises informed about bonus issue proposals and authorized capital increases

approved by them.

13. The above conditions shall cut down the procedural delays in obtaining the approval for bonus shares besides enabling the PSUs to

finalize public issue plans quickly and tap the capital market when conditions are favourable.

14. The Financial Advisers in the administrative Ministries shall keep a control over the fulfillment of various conditions/criteria as mentioned

above before agreeing to the bonus issues.

(DPE O.M. No. DPE/12(6)/95-Fin. dated 10th November, 1995)

ENCLOSURE

Copy of Securities and Exchange Board of India (SEBI)’ s guidelines dated 13th April, 1994 for Disclosure and Investor

Protection—Bonus Issue Guidelines.

In keeping with current pace of liberalization and reforms in the Primary Market, the Board of SEBI has decided to modify the extant

guidelines for bonus shares, forming Section M of the Guidelines for Disclosure and Investor Protection issued by SEBI on June 11, 1992.

SEBI believes that the Board of Directors of the companies wishing to make bonus issues will take into due consideration the relevant

financial factors while deciding on bonus issues and observe the following guidelines.

Section M

(i) These guidelines are applicable to existing listed companies who shall forward a certificate duly signed by the issuer and duly

countersigned by its statutory auditor or by a company secretary in practice to the effect that the terms and conditions for issue of bonus

shares as laid down in these guidelines, have been complied with.

(ii) Issue of bonus shares after any public/right issue is subject to the condition that no bonus issue shall be made which will dilute the value

or rights of the holders of debentures, convertible fully or partly.

In other words, no company shall, pending conversion of FCDs/PCDs, issue any shares by way of bonus unless similar benefit is extended

to the holders of such FDCs/PCDs, through reservation of shares in proportion to such convertible part of FCDs or PCDs. The shares so

reserved may be issued at the time of conversion(s) of such debentures on the same terms on which the bonus issues were made.

(iii) The bonus issue is made out of free reserves built out of the genuine profits or share premium collected in cash only.

(iv) Reserves created by revaluation of fixed assets are not capitalized.

(v) The declaration of bonus issue, in lieu of dividend, is not made.

(vi) The bonus issue is not made unless the partly-paid shares, if any existing, are made fully paid-up.

(vii) The Company –

1. has not defaulted in payment of interest or principal in respect of fixed deposits and interest on existing debentures or principal on

redemption thereof and.

2. has sufficient reason to believe that it has not defaulted in respect of the payment of statutory dues of the employees such as contribution

to provident fund, gratuity bonus etc.

(viii) A company, which announces bonus issue after the approval of the Board of Directors must implement the proposals within a period of

six months from the date of such approval and shall not have the option of changing the decision.

(ix) There should be a provision in the Articles of Association of the company for capitalization of reserves, etc. and if not, the company shall

pass a Resolution at its General Body Meeting making provisions in the Articles of Association for capitalization.

(x) Consequent to the issue of bonus shares if the subscribed and paid-up capital exceed the authorized capital, a Resolution shall be

passed by company at its General Body Meeting for increasing the authorized capital.

ENCLOSURE

Copy of Securities and Exchange Board of India (SEBI)’s RMB (DIP Series) Circular No. 2(94-95) dated 15th April, 1994 – Guidelines

for Disclosure and Investor Protection.

In tune with the process of liberalization and reforms in the primary market, it has been decided to modify the extant guidelines for issue of

bonus shares contained in Section M of the guidelines for Disclosure and Investor Protection issued by SEBI on June 11, 1992. The revised

guidelines have done away with certain requirements relating to issue of bonus, namely profitability Test, Residual Reserves Test etc.

A copy of the Press Release dated April 13, 1994 issued by SEBI in this connection is enclosed for your information.

CHAPTER III FINANCIAL POLICIES

13. DPE/Guidelines/III/13 Guidelines on investment of surplus funds by PSUs.

Reference is invited to the OM of even number dated 14.12.94 and the subsequent clarifications issued by DPE vide O.M. dated 1.11.95 on

the above mentioned subject. Through these OMs the PSUs were advised that the investment of surplus funds in UTI and other public and

private sector mutual funds should not be made as they are inherently risky. The PSUs were further advised that the existing holdings or the

enterprises in UTI or other similar schemes or various other mutual funds be disinvested to fall in line with these guidelines and such

liquidation of holdings be phased out without running the risk of capital loss.

2. The matter has been further examined by the Government and it has now been decided that the existing holdings of PSUs in various

schemes of UTI and similar mutual funds schemes of other public sector and private sector mutual funds may be phased out over a period of

three years.

3. The administrative Ministries/Departments are requested to suitably advise the public enterprises under their administrative control to

strictly comply with these guidelines.

4. These guidelines are issued in consultation with Ministry of Finance.

(DPE No. DPE/4(6)/94-Fin. dated 11th March, 1996)

***

CHAPTER III FINANCIAL POLICIES

14. DPE/Guidelines/III/14 Investment of Surplus Fund by PSUs.

The Government had vide OM of even number dated 14th December, 1994 and OM dated 1.11.95 issued detailed guidelines on investment

of surplus funds by the PSUs. A reference was received by the Government on the applicability of these guidelines to the finance sector

PSUs. The matter has been examined in consultation with Ministry of Finance and it is clarified that the finance sector PSUs are by and large

development financial institution set up under Section 4(9) of the Companies Act as public Financial Institutions. These companies are

governed by the RBI directives for non-banking finance companies. Such of these companies which are already registered with RBI are

guided by RBI directive for maintenance of liquid assets in India in the form of deposit/investments in Central or State Govt. Securities or

Govt. guaranteed bonds at a level higher than those which are not registered with RBI.

2. In view of the above, it has been decided that the finance sector PSUs, get registered with RBI as NBFCs, in case where it is not already

done and completely falls in line with the directive/monitoring process of RBI. The NBFCs in Public Sector registered with RBI will be outside

the purview of the above referred guidelines issued by DPE.

3. The Administrative Ministries/Departments are requested to suitably advise the Public Enterprises under their Administrative control to

strictly comply with the guidelines.

(DPE O.M. No. 4/6/94-Fin dated 2nd July, 1996)

***

CHAPTER III FINANCIAL POLICIES

15. DPE/Guidelines/III/15

Investment of Surplus Funds by the Public Sector Enterprises

The Government vide OMs of even number dated 14th December, 1994, 1st November, 1995 and 11th March 1996 issued detailed

guidelines on investment of Surplus Funds by the Public Sector Undertakings. Para 2 of the guidelines dated 1.11.1995 mentioned “the

existing holdings of the enterprises in the UTI Schemes or similar schemes of various other Public Sector and Private Sector Mutual Funds

have to be disinvested to fall in line with these guidelines. Such investment may, however, be phased out without running the risk of capital

losses with due approval from the Boards of the Public Enterprises”. Further, the O.M. dated 11.3.96 advised that the existing holdings of

PSUs in various schemes of UTI and similar mutual fund schemes of other Public Sector and Private Sector Mutual Funds may be phased

out over a period of three years.

2. The Government have further reviewed the situation. Taking into account the various factors regarding the establishment and investment

activities of UTI and recognition of Units as eligible securities under the Indian Trusts Act, 1882, and the regulatory frame work of SEBI, it has

been decided to remove the existing restrictions on investment of surplus funds of PSEs in the Units/Schemes of UTI as contained in the

above mentioned guidelines.

3. The above clarifications may please be kept in view by the Boards of Public Sector Enterprises while taking decision to invest/disinvest in

the Units of UTI. The administrative Ministries may please advise suitably the PSUs under their administrative control.

(DPE O.M. No. 4/6/94-Fin dated 14th February, 1997)

***

CHAPTER III FINANCIAL POLICIES

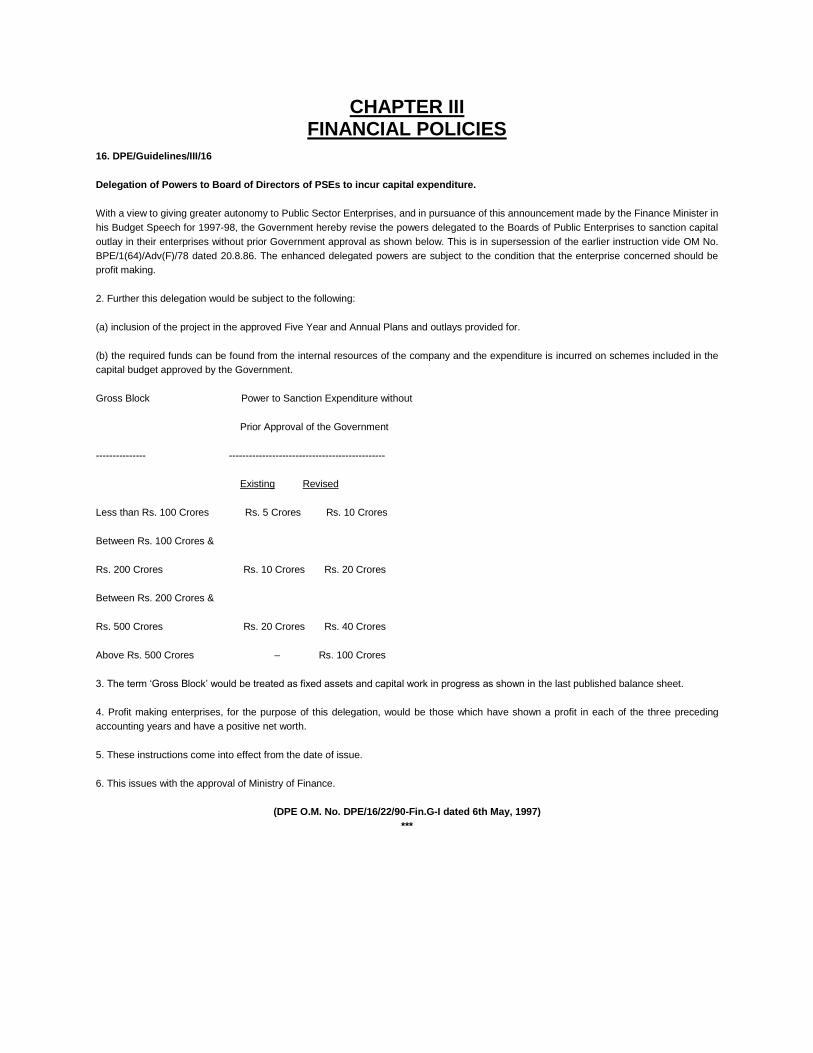

16. DPE/Guidelines/III/16

Delegation of Powers to Board of Directors of PSEs to incur capital expenditure.

With a view to giving greater autonomy to Public Sector Enterprises, and in pursuance of this announcement made by the Finance Minister in

his Budget Speech for 1997-98, the Government hereby revise the powers delegated to the Boards of Public Enterprises to sanction capital

outlay in their enterprises without prior Government approval as shown below. This is in supersession of the earlier instruction vide OM No.

BPE/1(64)/Adv(F)/78 dated 20.8.86. The enhanced delegated powers are subject to the condition that the enterprise concerned should be

profit making.

2. Further this delegation would be subject to the following:

(a) inclusion of the project in the approved Five Year and Annual Plans and outlays provided for.

(b) the required funds can be found from the internal resources of the company and the expenditure is incurred on schemes included in the

capital budget approved by the Government.

Gross Block Power to Sanction Expenditure without

Prior Approval of the Government

--------------- -----------------------------------------------

Existing Revised

Less than Rs. 100 Crores Rs. 5 Crores Rs. 10 Crores

Between Rs. 100 Crores &

Rs. 200 Crores Rs. 10 Crores Rs. 20 Crores

Between Rs. 200 Crores &

Rs. 500 Crores Rs. 20 Crores Rs. 40 Crores

Above Rs. 500 Crores – Rs. 100 Crores

3. The term ‘Gross Block’ would be treated as fixed assets and capital work in progress as shown in the last published balance sheet.

4. Profit making enterprises, for the purpose of this delegation, would be those which have shown a profit in each of the three preceding

accounting years and have a positive net worth.

5. These instructions come into effect from the date of issue.

6. This issues with the approval of Ministry of Finance.

(DPE O.M. No. DPE/16/22/90-Fin.G-I dated 6th May, 1997)

***

CHAPTER III

FINANCIAL POLICIES

17. DPE/Guidelines/III/17

Foreign companies entering into joint ventures in India and operate in India—to obey the

law of the land.

The Committee on Government Assurances, Rajya Sabha has recommended the following in its

41st and 42nd Report pertaining to MUL:

“The committee, therefore, recommends that while permitting the foreign companies to operate

in India or while entering in the joint ventures in India they should be told in unequivocal terms

that they shall have to obey the law of the land and there shall be no compromise or excuse for

the ignorance of the Indian legal system in any manner”.

2. The Government have accepted the recommendations of the Committee. The administrative

Ministries/Departments may please suitably advise the public enterprises under their

administrative control to ensure implementations of the above recommendations of the

Committee on Government Assurances, Rajya Sabha in all the joint venture cases where it is

applicable. The Financial Advisers of the Ministry shall monitor implementation of the above

recommendation from time to time.

(DPE O.M. No. DPE/4(9)/97-Fin. dated 15th July, 1997)

***

CHAPTER III FINANCIAL POLICIES

18. DPE/Guidelines/III/18 Delegation of Powers to Board of Directors of PSEs to incur capital expenditure.

Reference is invited to the Department of Public Enterprises O.M. of even number dated 6th May, 97 delegating powers to the Boards of the

public enterprises to incur capital expenditure without prior approval of the Govt. A copy of the O.M. is enclosed for ready reference.

The guidelines provided inter-alia that the public sector enterprises can exercise the enhanced financial powers subject to the proviso that

the required funds are found from the internal resources of the company. References have been received from different quarters seeking

clarification on whether the ‘internal resources’ of the company would include borrowings from the markets, like debts, bonds, ECB or

through any other instrument without any assistance from Govt. On this point it is now clarified that the enhanced delegation may be

applicable in respect of projects for which no budgetary support is envisaged, i.e. projects funded 100% from IEBR. The term IEBR (Internal

and Extra Budgetary Resources) for this purpose would include extra budgetary resources such as bonds, ECB and other similar

mobilization made on their own internal strength by the PSUs but excluding Govt. guaranteed borrowings.

The administrative Ministries/Departments are requested to suitably advise the public enterprises under their administrative control.

This is issued in consultation with the Ministry of Finance.

(DPE O.M. No. DPE/16/22/90-Fin.G-I dated 8th October, 1998)

***

CHAPTER III FINANCIAL POLICIES

19. DPE/Guidelines/III/19 Holding Annual General Meeting and filing Annual Accounts with the Registrar of Companies—strict compliance of provisions of the Companies Act, 1956 regarding.

As per the Provisions of Section 166 of the Companies Act, 1956, the Annual General Meeting (AGM) of a Company is required to be held

once in every calendar year and not more than 15 months shall elapse between the date of one AGM and that of the next. Further, the

Section 210 of the Act stipulates that the audited Annual Accounts for the period ending with the day, which shall not precede the day of the

AGM by more than 6 months, have to be placed in the said AGM. Thereafter, the Companies are required to file the Annual Accounts with

the Office of the concerned Registrar of Companies within 30 days. However, it is observed that many of the Central Government

companies are not fully complying with the above provisions of the Companies Act, 1956.

2. The Comptroller & Auditor General of India (C&AG) has impressed the need to ensure necessary legal action under Companies Act, 1956

in cases of such delays. In view of this, the Department of Company Affairs has already issued necessary orders to the Registrar of the

Companies to file prosecution against such defaulting State Government undertakings. In one of such cases, filed by the Registrar of

Companies against M/s Kerala Ceramics Ltd., the Hon’ble High Court of Kerala has held that the offences were continuing offences, thereby

the offences committed day by day by the Managing Directors, who have joined the company subsequent to the commencement of first

offence till the offences were remedied, are also liable for offences.

3. All the administrative Ministries/Departments are, therefore, requested to bring this to the notice of the Government Companies falling

under their administrative control and advise them to strictly comply with the relevant provisions of the Companies Act, 1956 in the spirit of

the above judgement.

(DPE O.M. No. 13/9/99-Fin.G-VI dated 21st April, 1999)

CHAPTER III FINANCIAL POLICIES

20. DPE/Guidelines/III/20 Follow up action on the Reports of the Comptroller and Auditor General of India (Commercial)

The Committee on Public Undertakings (12th Lok Sabha) in their

2nd Report on follow up action on the Reports of the Comptroller and Auditor General of India (Commercial) noted that action taken notes on

a large number of audit paras were pending for a long time. The Committee noted that there was no strong and effective mechanism

available in the Ministries/Departments for coordinating and monitoring the submission of follow up action on the Reports of C&AG of India

(Commercial).

2. Keeping in view the huge pendency of follow up action on audit paragraphs, the Committee emphasized the need for evolving effective

monitoring mechanism in each Ministry to ensure timely submission of action taken notes on each report of C&AG presented to Parliament.

The Committee, therefore, recommended specific and immediate steps to be taken by the Government for setting up of Monitoring Cell in

each Ministry to monitor the submission of the follow up action on Audit Reports of C&AG of India (Commercial) on individual undertakings.

3. In this connection, attention is also invited to Lok Sabha Secretariat’s O.M. Nos.301(1)-PU/85 dated 16.7.1985 and 301(1)-PU/92 dated

17.2.1992 (copies enclosed) on the matter.

4. The above recommendation of COPU have been considered and accepted. All the administrative Ministries/Departments are requested to

take immediate steps for setting up monitoring cell for PSUs under their administrative control. They may also ensure timely submission of

follow up action taken notes duly vetted by the Audit to the Committee, on all relevant Reports/Paras of C&AG of India (Commercial)

presented to the Parliament, within six months from the date of presentation.

5. Submission of action taken notes to the Committee on audit paras pending for a long time may also be cleared by 21.10.99 positively.

6. Action taken in the matter may be intimated to DPE.

(DPE O.M. No.DPE/4(6)/99-Fin.G-X dated 19th August, 1999)

Copy of Lok Sabha Secretariat O.M.No.301(1)-PU/85 dated 16th July, 1985-Follow up action on the Reports of the Comptroller &

Auditor General of India

The undersigned is directed to invite attention of the Ministry of Agriculture and Cooperation etc. to the following recommendations of

the Committee on Public Undertakings contained in Para 19 (Part II) of

their 49th Report (1981-82) and the action taken by Government thereon

as reproduced on page 22 of the Committee’s 70th Action Taken Report (1982-83):

“Recommendation S.No.19 (para 19, Part-II) contained in the Forty-Ninth Report of C.P.U.

The C&AG’s Report (Commercial) is presented in several parts in addition to his comments on the accounts published in the Annual Reports

of the undertakings. There should be some automatic follow up action on these by the Ministries. These should be reviewed for suitable

action at the periodical performance review meetings and at the time of review of the working before laying of the Annual Reports before

parliament.

Reply of the Government vide page No.22 of Seventieth Report of C.P.U.

Government accept this recommendation. The administrative Ministries have been advised to take note of the recommendation while

conducting the periodical performance review meetings and before laying the annual reports of the Ministries before Parliament.

Ministry of Finance, Bureau of Public Enterprises, O.M.No.11(10)/82-BPE/(Parl.) dated 31st January, 1983.”

2. At their sitting held on 7th June, 1985, the Committee on Public Undertakings have decided that each Ministry/Department should be

requested to furnish a brief note each on their review of the follow up action taken on the Reports of the Comptroller and Auditor General of

India presented to Parliament during the period 1983-84 and 1984-85 and that the note should be got vetted by Audit before submission to

the Committee.

3. It is requested that the note in respect of all the public undertakings under your Ministry/Department, as desired by the Committee on

Public Undertakings, duly vetted by Audit, may kindly be furnished to this Secretariat by 20th August, 1985 for being placed before the

Committee.

4. Receipt of this O.M. may please be acknowledged.

Copy of the Lok Sabha Secretariat O.M.No.301/1-PU/92 dated 17th February, 1992-Follow-up action on the Reports of the Comptroller & Auditor General of India.

The undersigned is directed to invite attention to this Secretariat O.M.No.301(1)-PU/85 dated 16th July, 1985, wherein it was requested that

each Ministry/Department should, inter-alia, furnish a brief note each on their review of the follow up action taken on the Reports of the

Comptroller and Auditor General of India presented to parliament during the period 1983-84 and 1984-85, after getting the same vetted by

Audit before submission to the Committee.

2. At the sitting held on 5th February, 1992, the Committee on Public Undertakings have reiterated that each Ministry/Department should

furnish a brief note on the review of the follow up action taken on each of the Comptroller & Auditor General’s Reports presented to

Parliament after 1985. The note may be got vetted by audit before submission to the Committee.

3. It is requested that the note in respect of all P.U. under your Ministry/ Department, as desired by the Committee on Public Undertakings,

duly vetted by Audit, should be furnished to this Secretariat note later than 31st March, 1992 for being placed before the Committee.

4. Receipt of this O.M. may please be acknowledged.

CHAPTER III

FINANCIAL POLICIES

21. DPE/Guidelines/III/22

Guidelines for investment of surplus fund by Public Sector Enterprises.

Reference is invited to the Department of Public enterprises OM of even number dated 14th

December, 1994 detailing the guidelines for investment of surplus fund by public sector

enterprises, in the wake of Joint Parliamentary Committee Report which enquired into the

irregularities in security transactions noticed by the Committee in case of certain public

enterprises. These guidelines were followed by OM dated 1.11.95, 11.3.96, 2.7.96 and 14.2.97

indicating certain modifications in the policy and certain clarifications which were raised from

different quarters on the specific methods of investment of surplus funds.

There have been certain representations from public sector enterprises that the guidelines leave

no scope for the public enterprises to fully utilize their surpluses for a duration of less than 15

days, and that these enterprises may be permitted to invest their surpluses in the inter-bank call

money deposits on a day-to-day basis through the Discount and Finance House India Ltd.

(DFHI), a company jointly owned by RBI, nationalized banks and the financial institutions.

The above representations have been considered in consultation with the Ministry of Finance and

it has been decided that the public sector enterprises may be allowed to invest their surplus funds

in the call money deposits after taking individual approvals from the Reserve Bank of India.