Chapter 6 Moving from Day Books through the Ledgers to the Trial Balance

Chapter 6 Moving from Day Books through the Ledgers to the Trial Balance.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 6

Moving from Day Books

through the Ledgers to the Trial Balance

The Subsidiary Ledgers and the General Ledger

Every transaction must end up in the ledgers

There are three we will focus on:• Sales ledger • Purchases ledger • General ledger

Sales Ledger

This contains the "T" accounts of all the credit customers. Each "T" account here will tell the firm the exact amount due from each credit customer.

Sales Ledger

Look at the sales ledger accounts shown on the next slide so you can determine how much each customer owes

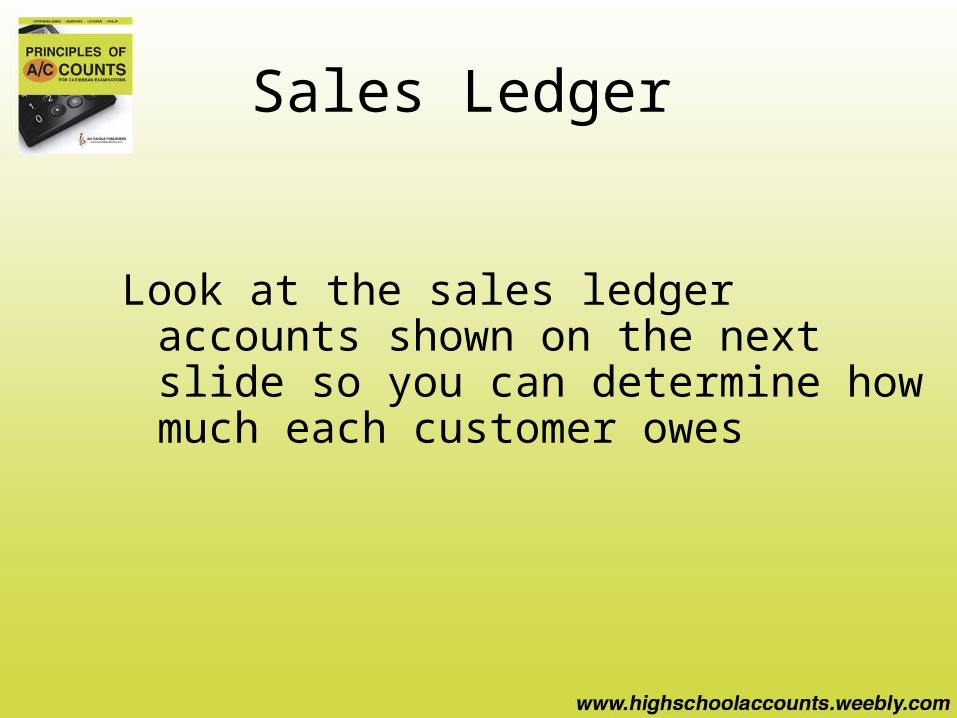

Sales Ledger

Date $ Date $Day3 4,000Day8 6,000

Date $ Date $Day4 5,000Day9 7,000

Customer C a/c

Details DetailsSalesSales

Customer D a/cDetails DetailsSalesSales

Sales Ledger

You should have determined the amounts owed by each debtor as:

• Customer C $ 10,000• Customer D $ 12,000

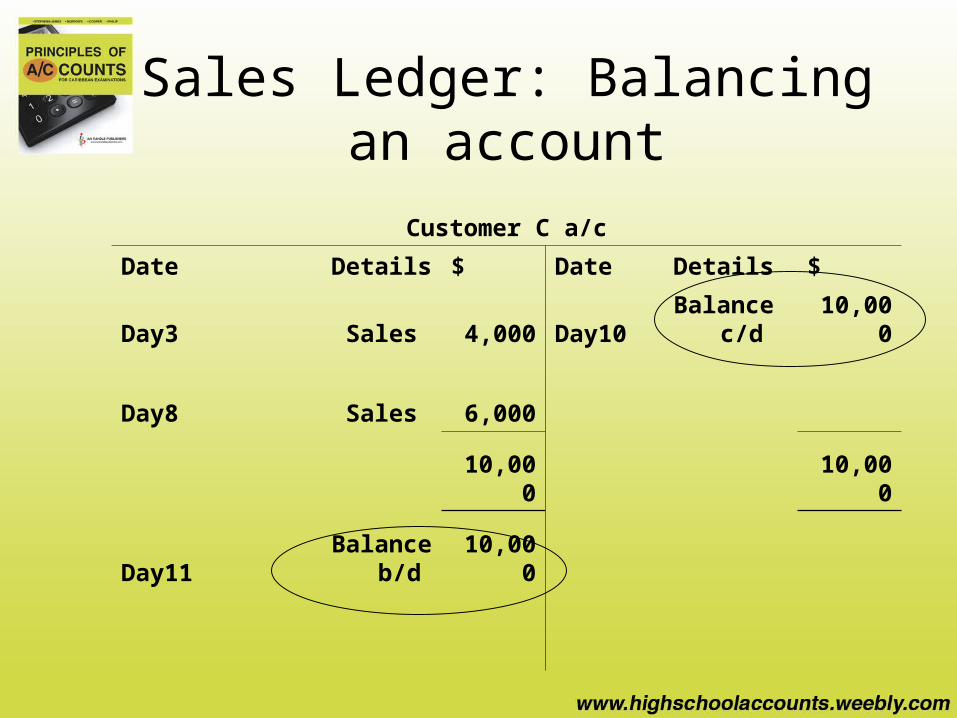

Sales Ledger: Balancing an account

Customer C a/c

Date Details $ Date Details $

Day3 Sales 4,000 Day10Balance

c/d 10,000

Day8 Sales 6,000

10,000 10,000

Day11Balance

b/d 10,000

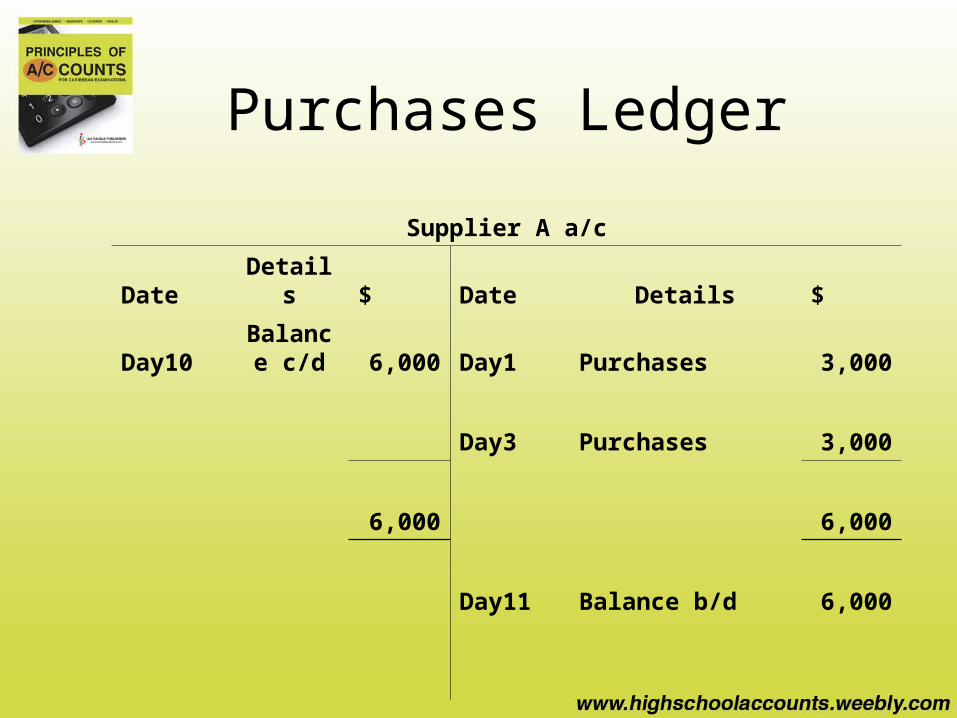

Purchases Ledger

Supplier A a/c

Date Details $ Date Details $

Day10Balance

c/d 6,000 Day1 Purchases 3,000

Day3 Purchases 3,000

6,000 6,000

Day11 Balance b/d 6,000

Purchases Ledger

This contains all the "T" accounts of all the credit suppliers. Each "T" account here will give the firm the exact amount payable to each supplier

Subsidiary ledgers

The sales ledger and the purchases ledger are examples of subsidiary ledgers. Other examples of subsidiary ledgers are a fixed asset ledger and a payroll ledger. The purpose of subsidiary ledgers is to reduce the amount of detail found in the general ledger.

The General Ledger

This contains real accounts (assets, liabilities, and capital) and nominal accounts (revenue and expenses). Real accounts are maintained over several accounting periods, but nominal accounts are closed each period. There will be no personal "T" accounts for customers or suppliers in the general ledger.

The Trial Balance

The trial balance is a listing of all the general ledger account balances at a particular date. Its main purpose is to ensure that all the debit and credit entries we made in the ledgers are the same. Remember that every time we put a debit entry in an account, we also put a credit entry, of an equal amount, into another account.

Example of a Trial Balance

A. Finch

Trial balance as at 30 Feb 2007

Dr Cr

Bank 328,000

Capital 500,000

Purchases 25,000

Sales 3,000

Delivery van 150,000

503,000 503,000

Related Documents