Chapter 21

Chapter 21. Learn why managers use budgets Develop strategy PlanActControl 3Copyright 2009 Prentice Hall. All rights reserved.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 21

Learn why managers use budgets

3Copyright 2009 Prentice Hall. All rights reserved.

Copyright 2009 Prentice Hall. All rights reserved. 4

Understand the components of the master budget

Set of budgeted financial statements and supporting schedules

Three types:◦ Operating◦ Capital expenditures◦ Financial

Copyright 2009 Prentice Hall. All rights reserved. 6

Sales budget

Operating expenses budget

Purchases and cost of goods sold budget

Inventory budget

Budgeted income statement

Copyright 2009 Prentice Hall. All rights reserved. 7

8

Budgeted income statement

Cash budget

Budgeted balance

sheet

Budgeted statement of cash flows

Capital expenditures

budget

Financial budget

Copyright 2009 Prentice Hall. All rights reserved.

Prepare an operating budget

Forecast of sales revenues Cornerstone of master budget

◦ Level of sales affects all elements

10Copyright 2009 Prentice Hall. All rights reserved.

Budgeted total sales

Sales priceExpected number of units sold

11

Purchases = Cost of goods sold + Ending inventory – Beginning inventory

Copyright 2009 Prentice Hall. All rights reserved.

Cost of goods sold = Beginning inventory + Purchases – Ending inventory

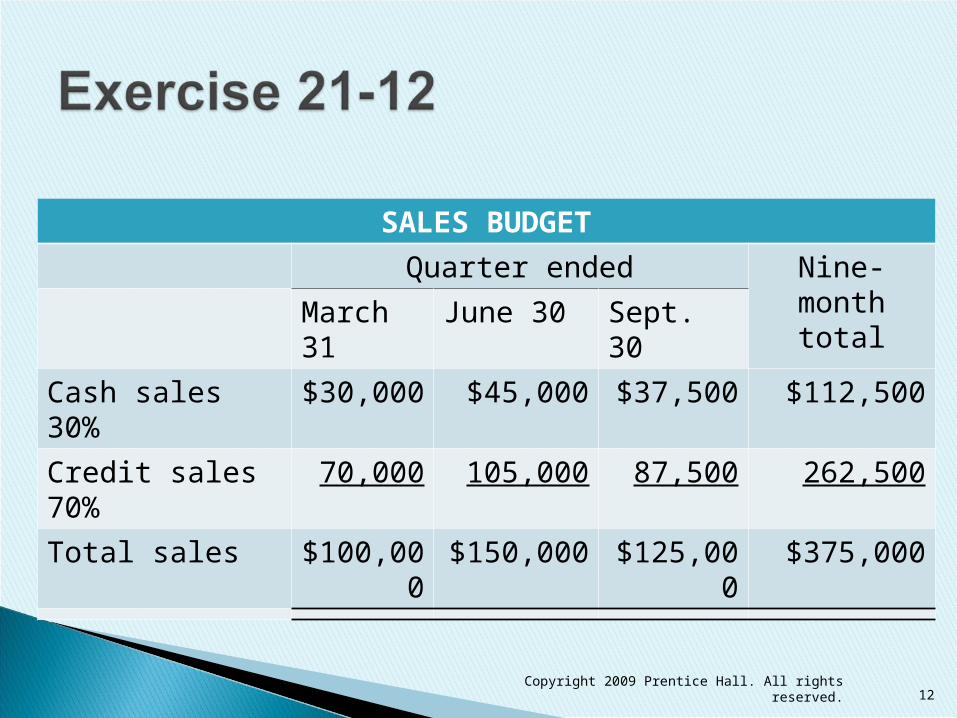

SALES BUDGET

Quarter ended Nine-month total

March 31

June 30 Sept. 30

Cash sales 30% $30,000 $45,000 $37,500 $112,500

Credit sales 70%

70,000 105,000 87,500 262,500

Total sales $100,000

$150,000 $125,000

$375,000

Copyright 2009 Prentice Hall. All rights reserved. 12

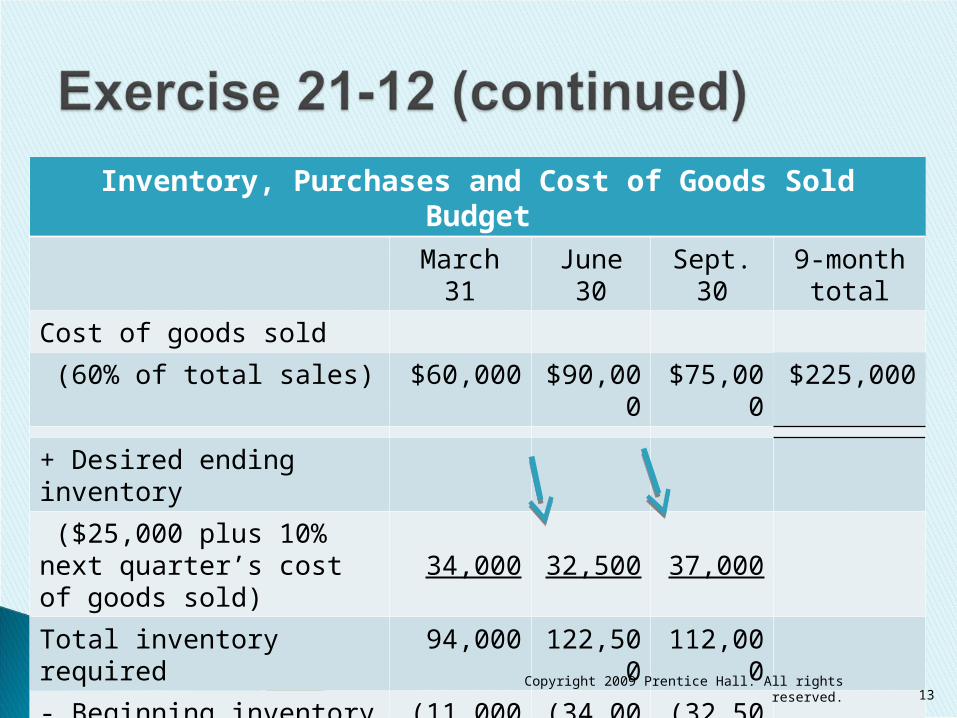

Inventory, Purchases and Cost of Goods Sold BudgetMarch

31June 30 Sept.

309-month

total

Cost of goods sold

(60% of total sales) $60,000 $90,000

$75,000

$225,000

+ Desired ending inventory

($25,000 plus 10% next quarter’s cost of goods sold)

34,000 32,500 37,000

Total inventory required 94,000 122,500

112,000

- Beginning inventory (11,000) (34,000)

(32,500)

= Budgeted purchases $83,000 $88,500

$79,500

Copyright 2009 Prentice Hall. All rights reserved. 13

Expenses can be either fixed or variable Includes items such as:

◦ Salaries◦ Rent◦ Insurance◦ Advertising

Copyright 2009 Prentice Hall. All rights reserved. 14

Prepare a financial budget

Copyright 2009 Prentice Hall. All rights reserved. 16

Details how the business expects to go from the beginning cash balance to the desired ending balance

Four major parts:◦ Cash collections from customers◦ Cash payments for purchases◦ Cash payments for operating expense◦ Cash payments for capital expenditures

17Copyright 2009 Prentice Hall. All rights reserved.

Cash collections from customers◦ Cash sales from the sales budget◦ Collections of previous month’s credit sales

Accounts receivable Cash payments for purchases

◦ Payment of current month purchases from the purchases budget

◦ Payment of prior month purchases Accounts payable

18Copyright 2009 Prentice Hall. All rights reserved.

Payments for operating expense◦ Use data from operating expense budget◦ Do not include noncash expenses such as

depreciation Payments for capital expenditures

◦ Use budgeted data

19Copyright 2009 Prentice Hall. All rights reserved.

Copyright 2009 Prentice Hall. All rights reserved. 20

Beginning cash balance 10$ 4$ Cash collections 8 12 Cash available 18 16 Cash payments:

Purchases of inventory 10 8 Operating expenses 2 2 Capital expenditures 4 1

Total cash payments 16 11 Ending cash balance before financing 2 5

Less: minimum cash balance (4) (4) Cash excess (deficiency) (2) 1 Financing of cash deficiency Borrowing 2 Payments (1)

Total effects of financing 2 (1) Ending cash balance 4$ 4$

Cash Budget

Copyright 2009 Prentice Hall. All rights reserved. 21

(a)

Book value of equipment:

Cost $22,000

Less: Accumulated depreciation

(7,000)

Book value $15,000

Plus: Gain 4,000

Expected cash receipt $19,000

Copyright 2009 Prentice Hall. All rights reserved. 22

August September

Expected sales in units 7,800 9,100

Selling price $13 $13

Expected sales $101,400 $118,300

Cash sales (30%) 30,420 35,490

Credit sales (70%) 70,980 82,810

Cash sales $35,490

September credit sales collected

82,810 x ¾ 62,108

August credit sales collected

70,980 x ¼ 17,745

Expected cash collections in September

$115,343

Copyright 2009 Prentice Hall. All rights reserved. 23

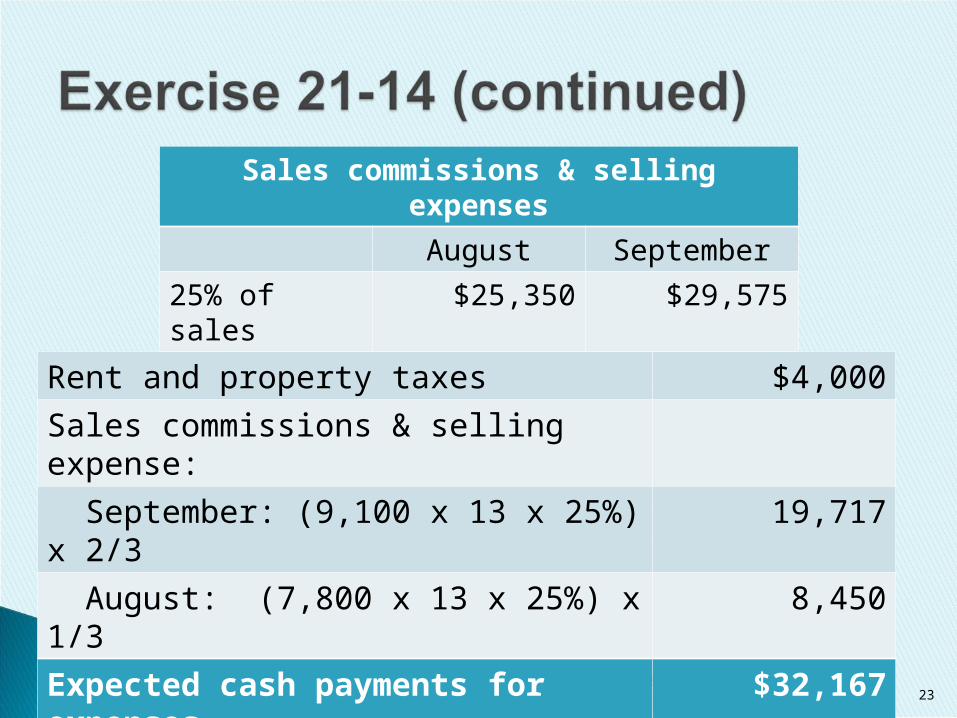

Rent and property taxes $4,000

Sales commissions & selling expense:

September: (9,100 x 13 x 25%) x 2/3

19,717

August: (7,800 x 13 x 25%) x 1/3 8,450

Expected cash payments for expenses

$32,167

Sales commissions & selling expenses

August September

25% of sales $25,350 $29,575

Use sensitivity analysis in budgeting

Actual results often differ from budgeted amounts

Sensitivity analysis◦ What-if technique that determines the result if

predicted amounts differ from those budgeted Spreadsheet programs used for budgeting

make sensitivity analysis cost-effective

25Copyright 2009 Prentice Hall. All rights reserved.

Copyright 2009 Prentice Hall. All rights reserved. 26

Company’s individual operating units roll up budgets to prepare company-wide budget

Budget management software used◦ Often part of Enterprise Resource Planning (ERP)

system Software allows managers to spend more

time analyzing data

Copyright 2009 Prentice Hall. All rights reserved. 27

Prepare performance reports for responsibility centers

Subunit of organization whose manager is accountable for specific activities

Four types:

29Copyright 2009 Prentice Hall. All rights reserved.

Cost center◦ Managers accountable for costs only

Goal – to control costs Revenue center

◦ Managers primarily accountable for revenues Goal – increase revenues

Profit center◦ Managers accountable for both revenues and

costs Goal – increase profits

Copyright 2009 Prentice Hall. All rights reserved. 30

Investment center◦ Managers accountable for investments, revenues,

and costs◦ Responsible for:

Generating sales Controlling expenses Managing investment needed to earn the income

◦ Goal – increase return on investment, residual income, or economic value added

Copyright 2009 Prentice Hall. All rights reserved. 31

Performance reports compare budgeted and actual amounts

Reporting at all levels:◦ Division (investment centers)◦ Product lines (profit centers)◦ Production (cost centers)◦ Sales (revenue centers)

Management by exception◦ Shows variances between actual and budgeted

amounts

32Copyright 2009 Prentice Hall. All rights reserved.

Related Documents