15-1 CHAPTER 15 Capital Structure and Leverage

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

15-1

CHAPTER 15Capital Structure and Leverage

15-2

Optimal capital structure : a firm’s capital structure that maximizes its firm value (or Minimizes the WACC)

Target capital structure : the mix of debt, preferred stock and common equity with which the firm plans to raise capital

Capital Structure

15-3

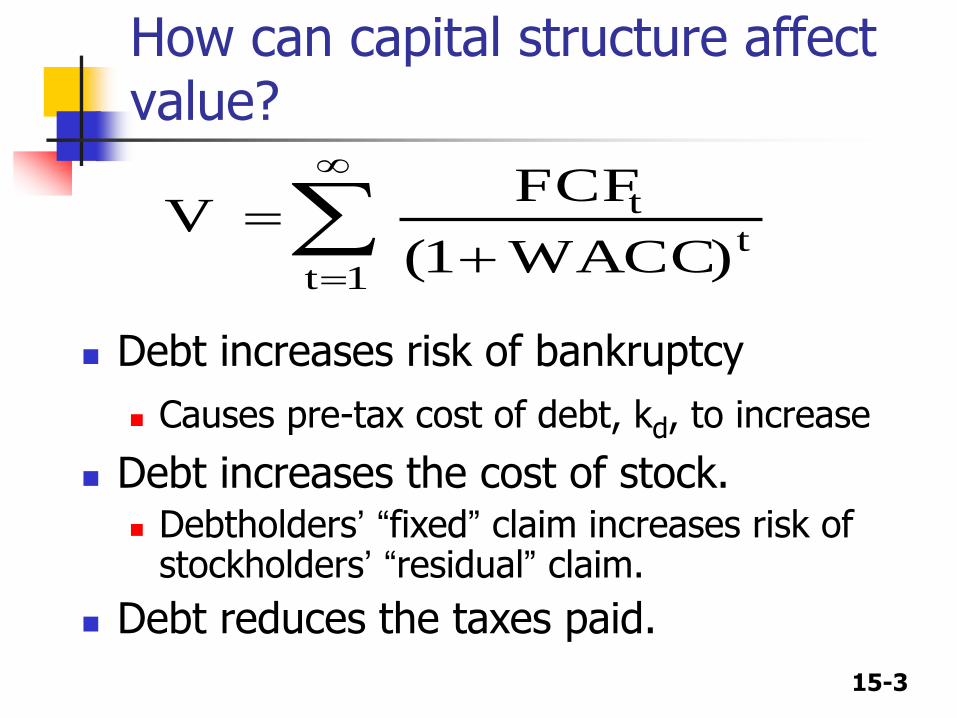

How can capital structure affect value?

1t

tt

)WACC1(

FCFV

Debt increases risk of bankruptcy

Causes pre-tax cost of debt, kd, to increase

Debt increases the cost of stock. Debtholders’ “fixed” claim increases risk of

stockholders’ “residual” claim.

Debt reduces the taxes paid.

15-4

How can capital structure affect value? (cont’d)

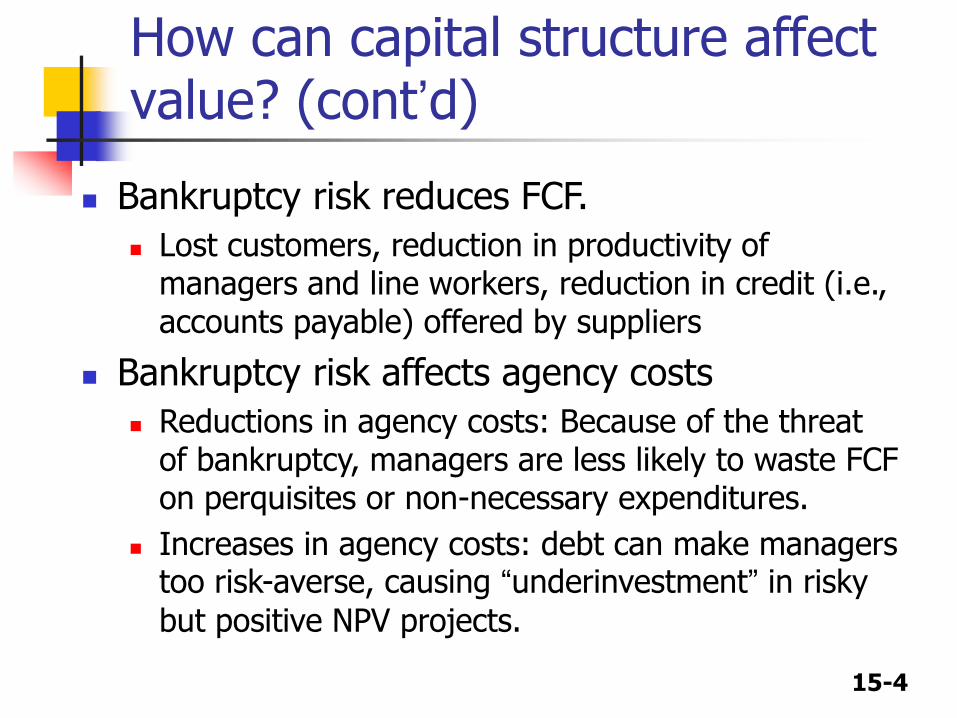

Bankruptcy risk reduces FCF.

Lost customers, reduction in productivity of managers and line workers, reduction in credit (i.e., accounts payable) offered by suppliers

Bankruptcy risk affects agency costs

Reductions in agency costs: Because of the threat of bankruptcy, managers are less likely to waste FCF on perquisites or non-necessary expenditures.

Increases in agency costs: debt can make managers too risk-averse, causing “underinvestment” in risky

but positive NPV projects.

15-5

How can capital structure affect value? (cont’d)

Asymmetric Information and Signaling

Managers know the firm’s future prospects better than investors.

Managers would not issue additional equity if they thought the current stock price was less than the true value of the stock (given their inside information).

Hence, investors often perceive an additional issuance of stock as a negative signal, and the stock price falls.

15-6

Capital Structure Theory

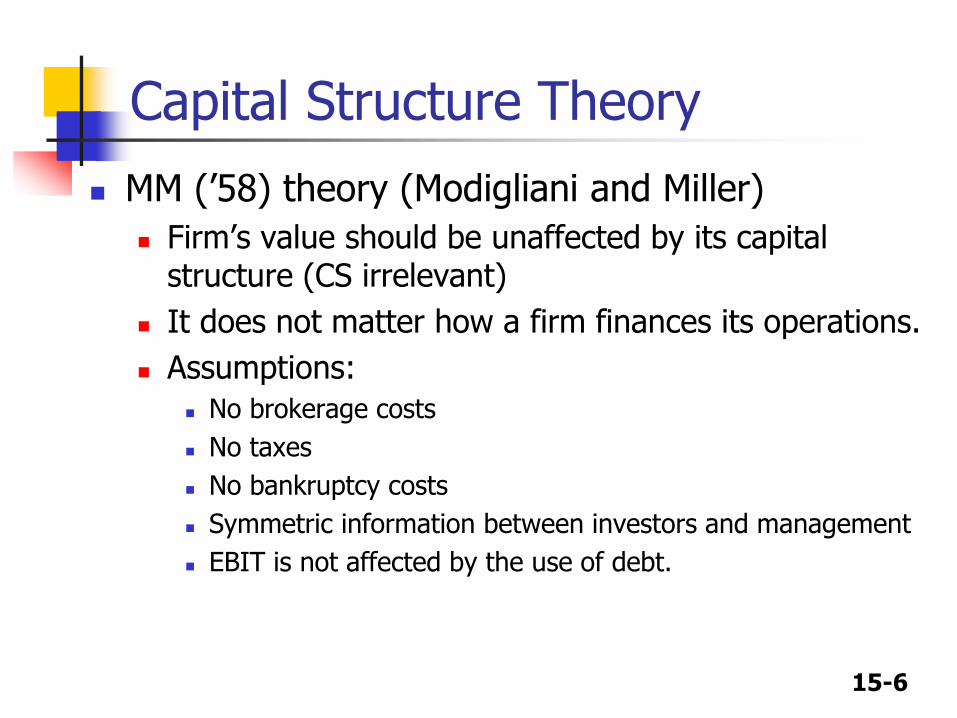

MM (’58) theory (Modigliani and Miller)

Firm’s value should be unaffected by its capital structure (CS irrelevant)

It does not matter how a firm finances its operations.

Assumptions:

No brokerage costs

No taxes

No bankruptcy costs

Symmetric information between investors and management

EBIT is not affected by the use of debt.

15-7

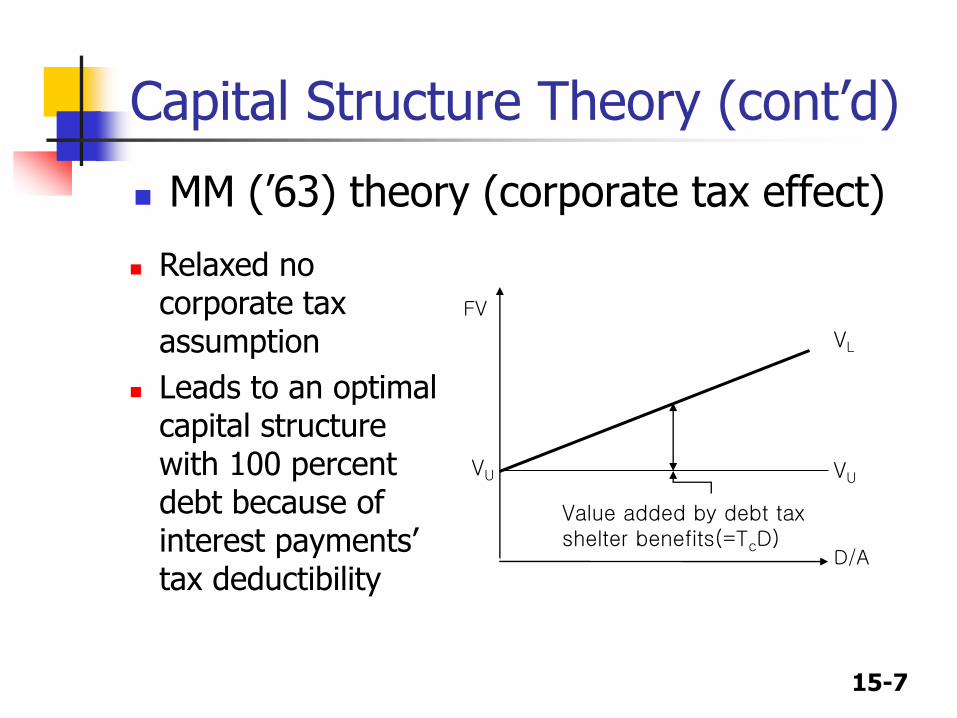

Capital Structure Theory (cont’d)

MM (’63) theory (corporate tax effect)

D/A

FV

VUVU

VL

Value added by debt tax shelter benefits(=TcD)

Relaxed no corporate tax assumption

Leads to an optimal capital structure with 100 percent debt because of interest payments’ tax deductibility

15-8

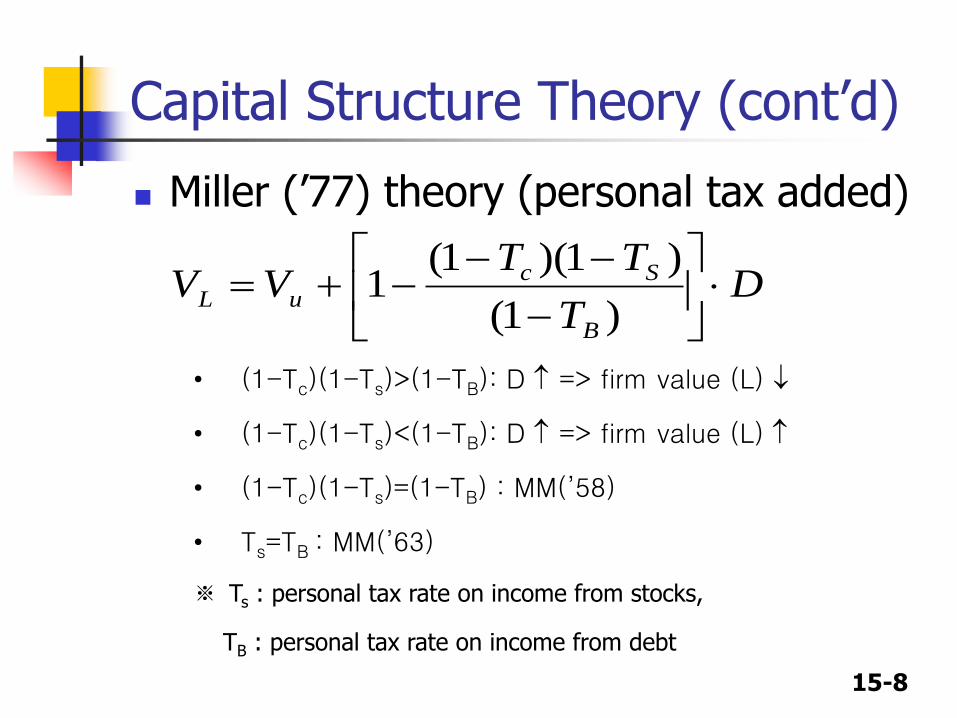

Capital Structure Theory (cont’d)

Miller (’77) theory (personal tax added)

• (1-Tc)(1-Ts)>(1-TB): D => firm value (L)

• (1-Tc)(1-Ts)<(1-TB): D => firm value (L)

• (1-Tc)(1-Ts)=(1-TB) : MM(’58)

• Ts=TB : MM(’63)

※ Ts : personal tax rate on income from stocks,

TB : personal tax rate on income from debt

DT

TTVV

B

Sc

uL

)1(

)1)(1(1

15-9

CS Theory : Trade-off Theory

The trade-off theory states that firms trade off the tax benefits of debt financing against problems caused by potential bankruptcy.

The possibility of bankruptcy, not just bankruptcy per se, has a negative effect on the value of the firm.

Direct Costs: directly associated with bankruptcy proceeding

Legal and administrative costs (ex. Enron, $1bil.)

Indirect Costs: associated indirectly with bankruptcy potential

Impaired ability to conduct business (e.g., sales drops, worker turnover, increases in cost of capital )

15-10

CS Theory : potential bankruptcy

Firm value

VU

VL* (Max.

FV)

VL=Vu + corp. tax shield

Value reduced by bankruptcy-related costs

D/A* D/A

VL=Vu+CTS–bankruptcy-

related costs

Value added by debt tax shelter benefits

15-11

CS Theory : signaling theory

Based on information asymmetry assumption: Managers have better

information about a firm’s long-run value than outside investors.

What can managers be expected to do?

Issue stock if they think stock is overvalued: a firm with unfavorable

prospects wants to finance with stock to share the losses with new

investors

Issue debt if they think stock is undervalued: a firm with favorable

prospects wants to finance with debt not to share the profits

As a result, investors view a stock offering negatively that managers

think stock is overvalued.

Need to maintain a reserve borrowing capacity for future good

investment opportunity => Firms use more equity and less debt than is

suggested by optimal capital structure in normal times.

15-12

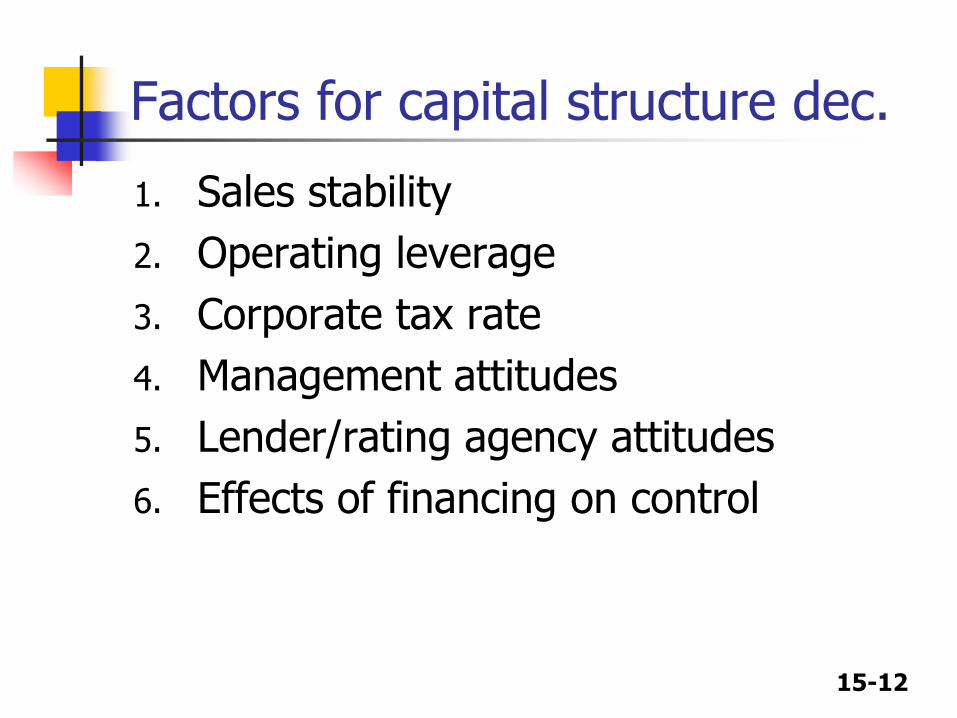

Factors for capital structure dec.

1. Sales stability

2. Operating leverage

3. Corporate tax rate

4. Management attitudes

5. Lender/rating agency attitudes

6. Effects of financing on control

15-13

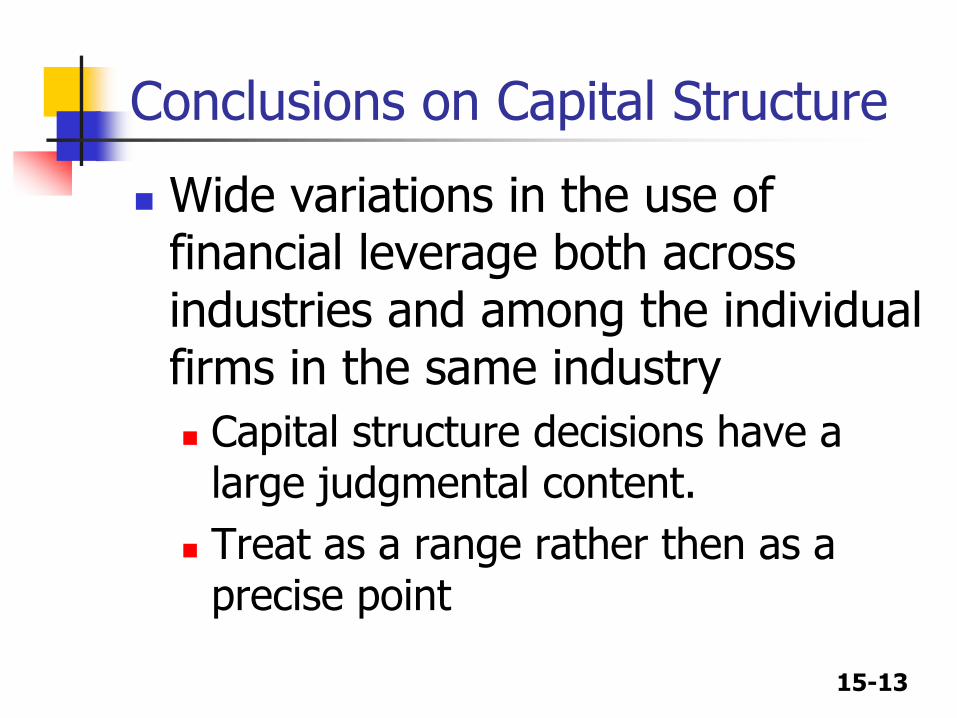

Conclusions on Capital Structure

Wide variations in the use of financial leverage both across industries and among the individual firms in the same industry

Capital structure decisions have a large judgmental content.

Treat as a range rather then as a precise point

15-14

Risk inherent in the firm’s operating activities. Uncertainty about future operating income (EBIT), i.e.,

how well can we predict operating income?

Riskiness of the firm’s value if it uses no debt. Business risk does not include financing effects.

※ What is business risk?

Probability

EBITE(EBIT)0

Low risk

High risk

15-15

※ What determines business risk?

Sales Risk Uncertainty about demand (sales).

Uncertainty about sales prices.

Uncertainty about input costs. Ability to adjust prices for changes in input costs

Ability to develop new products in a timely, cost-effective manner

Operating Risk The extent to which costs are fixed:

Operating leverage.

15-16

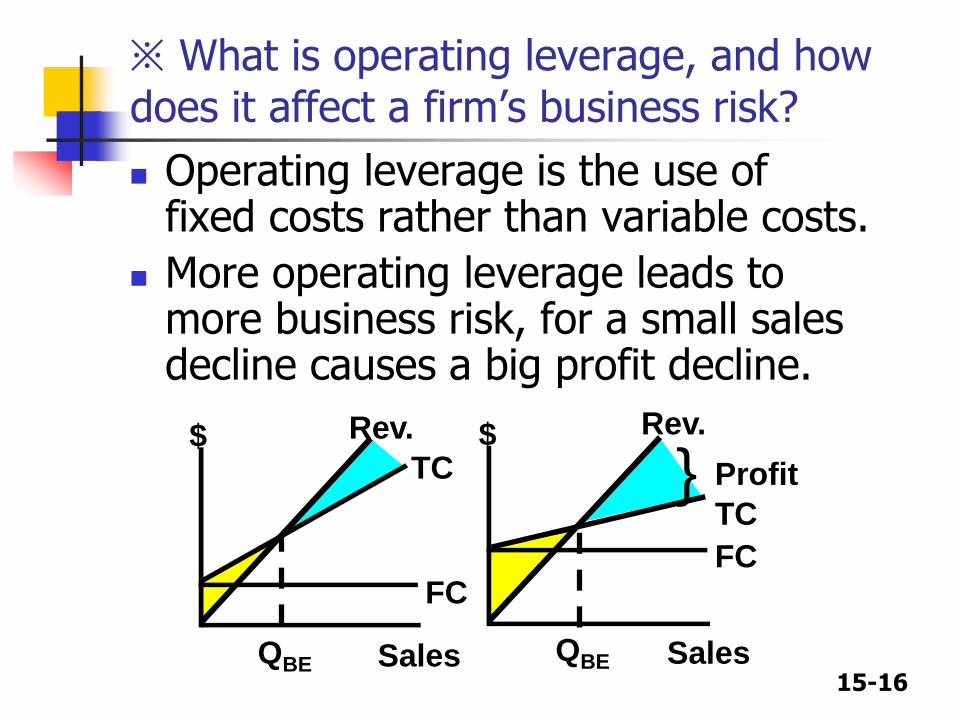

※ What is operating leverage, and how does it affect a firm’s business risk?

Operating leverage is the use of fixed costs rather than variable costs.

More operating leverage leads to more business risk, for a small sales decline causes a big profit decline.

Sales

$ Rev.

TC

FC

QBE Sales

$ Rev.

TC

FC

QBE

} Profit

15-17

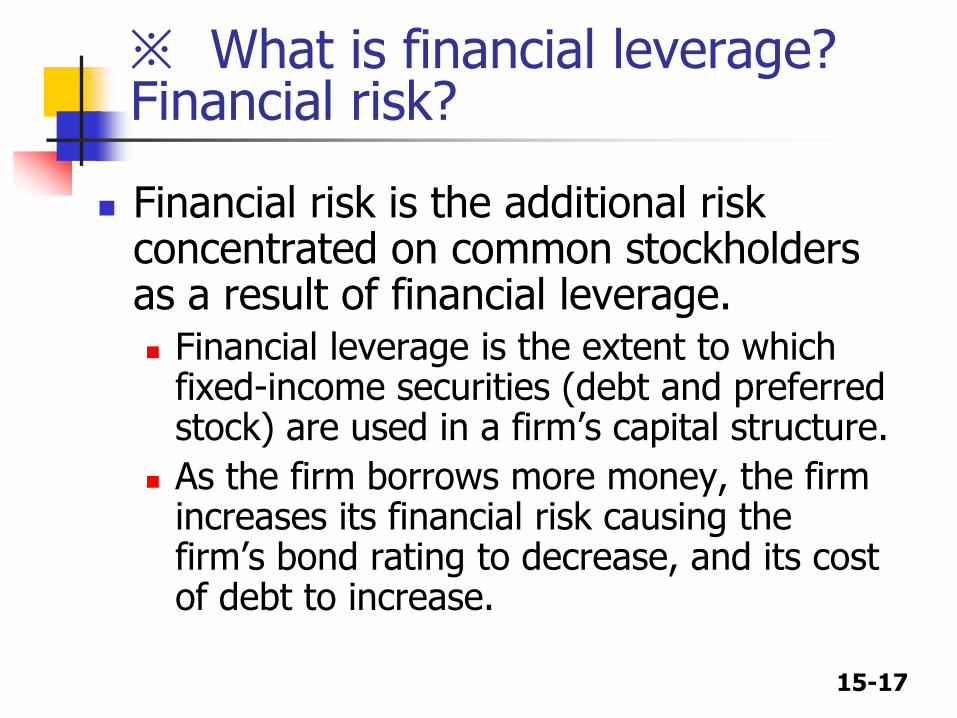

※ What is financial leverage?Financial risk?

Financial risk is the additional risk concentrated on common stockholders as a result of financial leverage. Financial leverage is the extent to which

fixed-income securities (debt and preferred stock) are used in a firm’s capital structure.

As the firm borrows more money, the firm increases its financial risk causing the firm’s bond rating to decrease, and its cost of debt to increase.

15-18

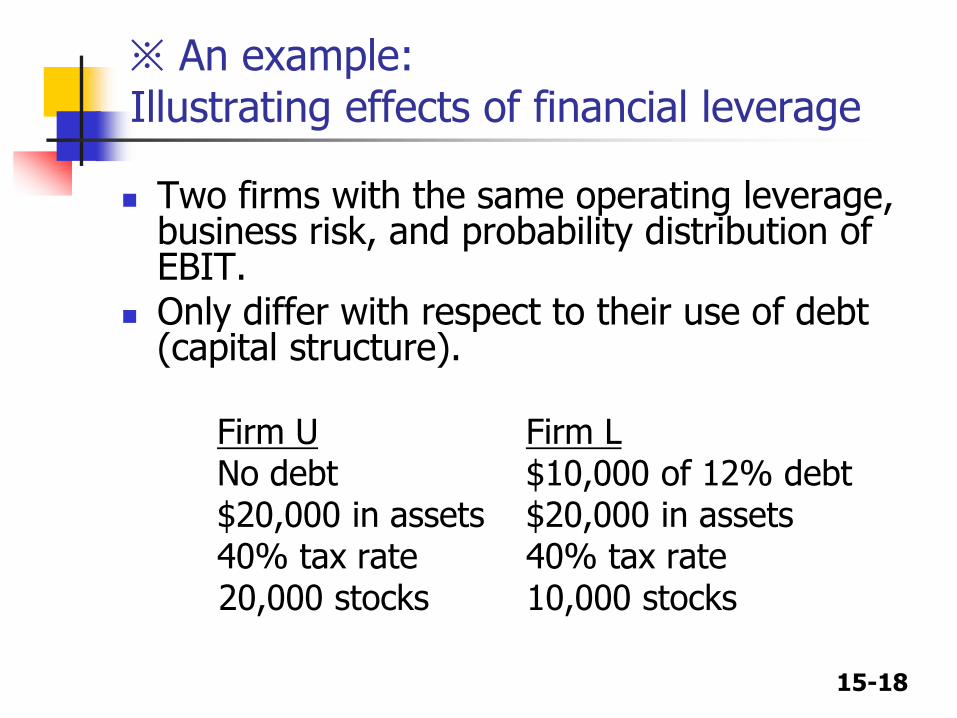

※ An example:Illustrating effects of financial leverage

Two firms with the same operating leverage, business risk, and probability distribution of EBIT.

Only differ with respect to their use of debt (capital structure).

Firm U Firm LNo debt $10,000 of 12% debt$20,000 in assets $20,000 in assets40% tax rate 40% tax rate20,000 stocks 10,000 stocks

15-19

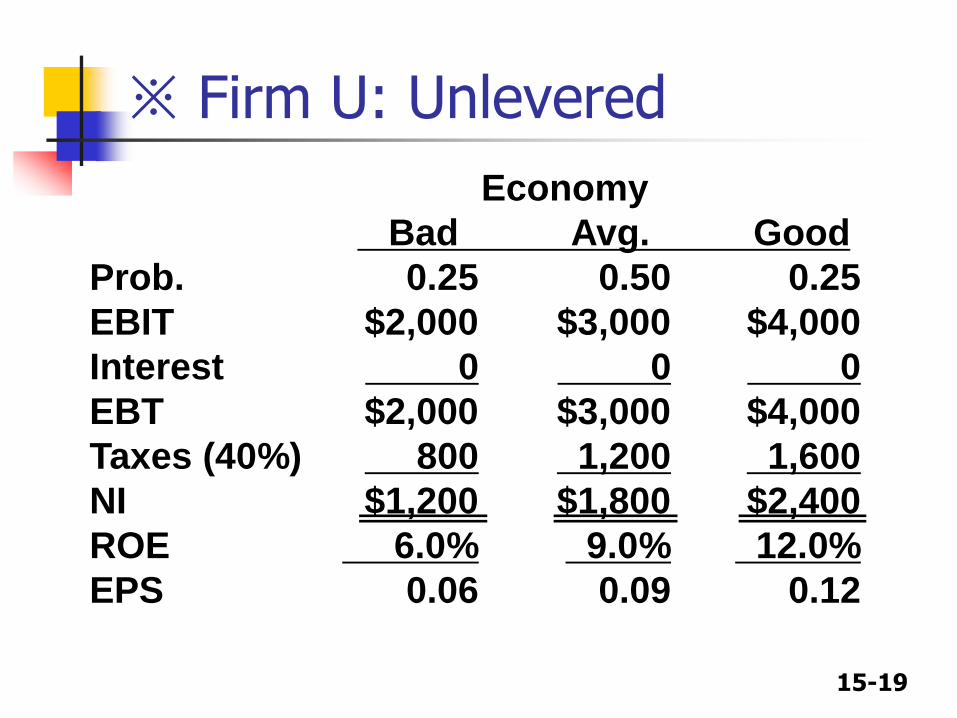

※ Firm U: Unlevered

Economy

Bad Avg. Good

Prob. 0.25 0.50 0.25

EBIT $2,000 $3,000 $4,000

Interest 0 0 0

EBT $2,000 $3,000 $4,000

Taxes (40%) 800 1,200 1,600

NI $1,200 $1,800 $2,400

ROE 6.0% 9.0% 12.0%

EPS 0.06 0.09 0.12

15-20

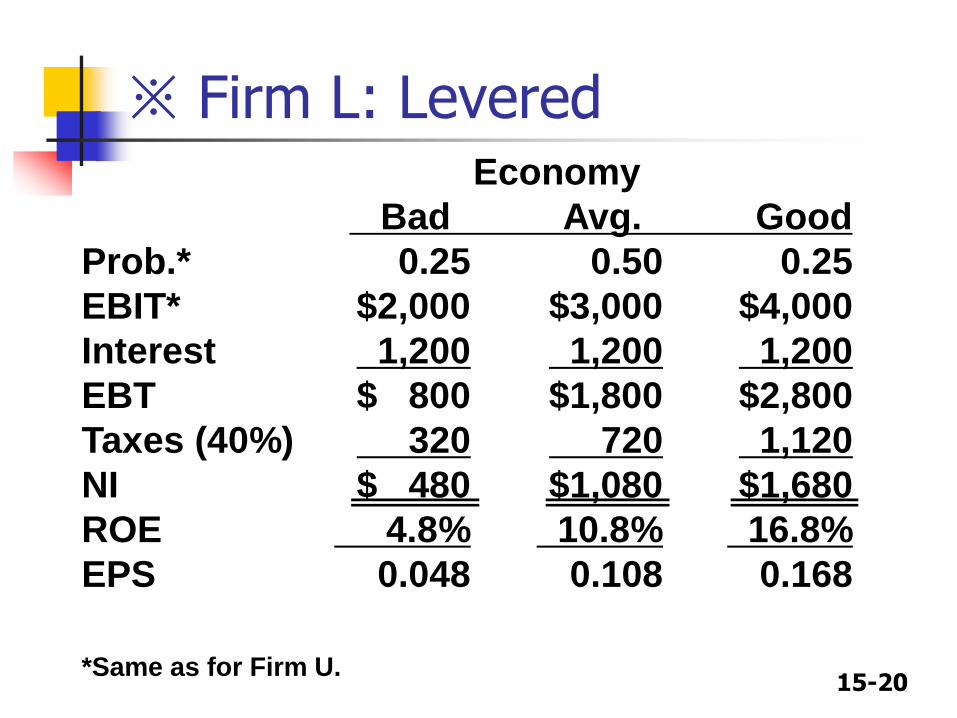

※ Firm L: LeveredEconomy

Bad Avg. Good

Prob.* 0.25 0.50 0.25

EBIT* $2,000 $3,000 $4,000

Interest 1,200 1,200 1,200

EBT $ 800 $1,800 $2,800

Taxes (40%) 320 720 1,120

NI $ 480 $1,080 $1,680

ROE 4.8% 10.8% 16.8%

EPS 0.048 0.108 0.168

*Same as for Firm U.

15-21

※ Risk and return for leveraged and unleveraged firms

Expected Values:Firm U Firm L

E(ROE) 9.0% 10.8%

Risk Measures:Firm U Firm L

σROE 2.12% 4.24%CVROE 0.24 0.39

L has much wider ROE (and EPS) swings because of

fixed interest charges. Its higher expected return is

accompanied by higher risk.

Related Documents