COST MANAGEMENT COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning. Cengage Learning and South-Western are trademarks used herein under license. 1 Guan ▪ Hansen ▪ Mowen Chapter 2 Basic Cost Management Concepts

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COST MANAGEMENT

COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning.Cengage Learning and South-Western are trademarks used herein under license.

1

Guan ▪ Hansen ▪ Mowen

Chapter 2Basic Cost Management

Concepts

2

Study Objectives

1. Explain the cost assignment process.

2. Define tangible and intangible products, and explain why there are different product cost definitions.

3. Prepare income statements for manufacturing and service organizations.

4. Explain the differences between traditional and contemporary cost management systems.

3

Cost Assignment: Direct Tracing, Driver Tracing and Allocation

• A cost object is any item, such as products, customers, departments, projects, activities, and so on, for which costs are measured and assigned.– Example: A bicycle is a cost object when you are

determining the cost to produce a bicycle.

• An activity is a basic unit of work performed within an organization. – Example: Setting up equipment, moving materials,

maintaining equipment, designing products, etc.

4

Cost Assignment: Direct Tracing, Driver Tracing and Allocation

• Traceability means that costs can be assigned easily and accurately, using a causal relationship.

• Methods of tracing:– Direct tracing: relies on physical observance of

causal relationships to assign costs to cost objects.– Driver tracing: relies on drivers as causal factors to

assign costs to cost objects.

5

Cost Assignment Methods

6

Examples of Product Cost Definitions

7

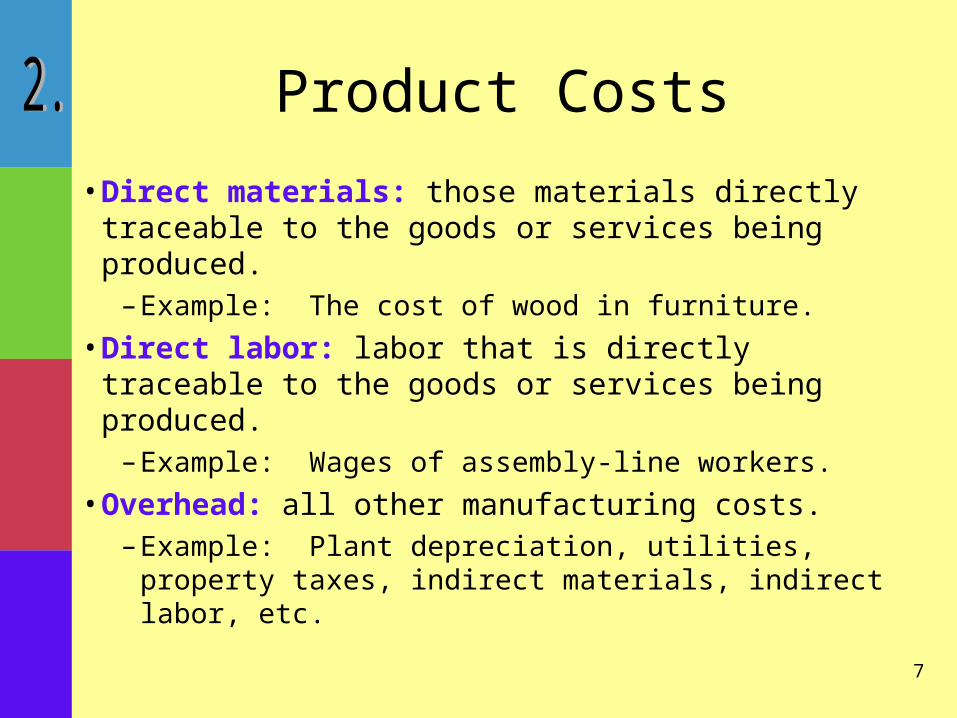

Product Costs

• Direct materials: those materials directly traceable to the goods or services being produced.

– Example: The cost of wood in furniture.

• Direct labor: labor that is directly traceable to the goods or services being produced.

– Example: Wages of assembly-line workers.

• Overhead: all other manufacturing costs.– Example: Plant depreciation, utilities, property

taxes, indirect materials, indirect labor, etc.

8

Prime and Conversion Costs

Direct Direct Prime+ =Materials Labor Costs

Direct Overhead Conversion+ =Materials Costs Costs

9

Nonproduction Costs

• Amount and timing of benefit cannot be reasonably estimated

• Period costs– Not inventoried– Expensed as incurred

• Examples– Research and development– Marketing costs– Administrative costs

10

Production and Nonproduction Costs

11

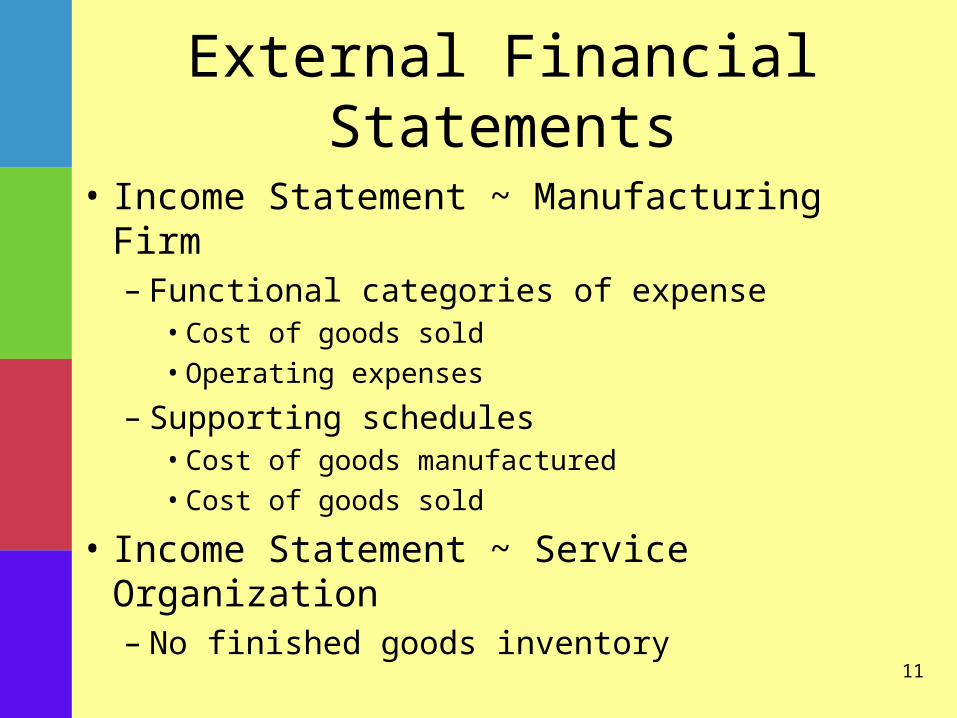

External Financial Statements

• Income Statement ~ Manufacturing Firm– Functional categories of expense

• Cost of goods sold• Operating expenses

– Supporting schedules• Cost of goods manufactured• Cost of goods sold

• Income Statement ~ Service Organization– No finished goods inventory

12

Income Statement: Manufacturing Firm

Sales 2,000,000$ Less: Cost of Goods Sold 1,300,000

Gross margin 700,000$ Less operating expenses:

Research and development 100,000$ Selling 300,000 Administrative 150,000 550,000

Operating income 150,000$

Manufacturing OrganizationIncome Statement

For the Year Ended December 31, 2009

From the Cost of Goods Sold Schedule

13

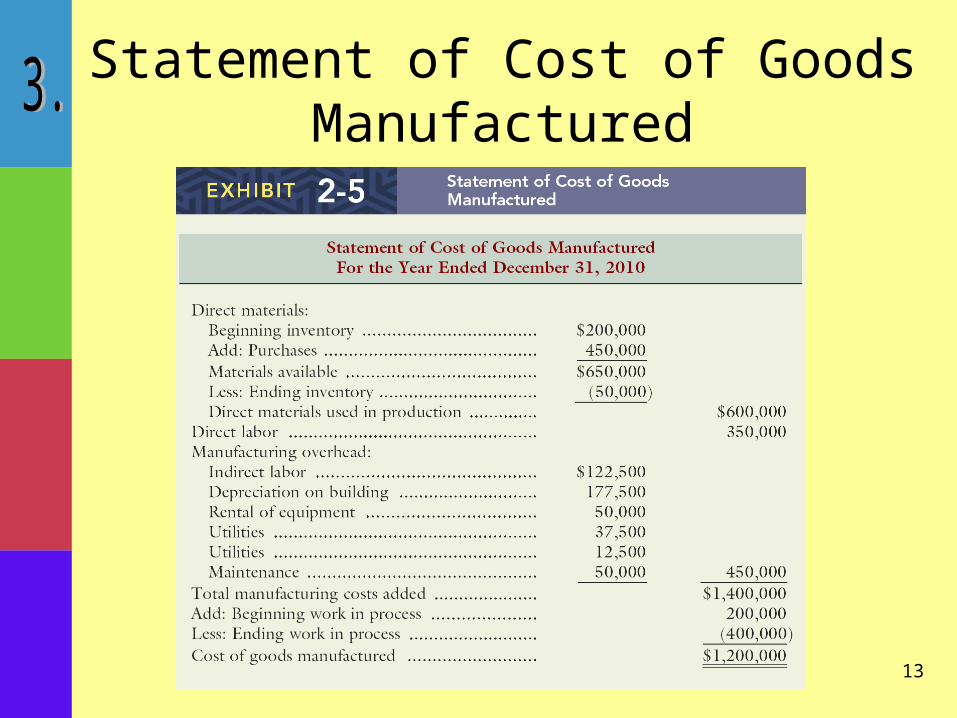

Statement of Cost of Goods Manufactured

14

Cost of Goods Sold Schedule

15

Cost Management Systems

• Functional-Based– Assumes a linear production cost behavior– Assigns costs to organizational units

• Activity-Based– Emphasizes tracing over allocation– Identifies non-unit-based activity drivers

16

Functional-BasedCost Management

• Unit-based drivers • Allocation-intensive• Narrow and rigid product costing• Focus on managing costs• Sparse activity information• Maximization of individual unit

performance• Uses financial measures of performance

17

Activity-BasedCost Management

• Unit- and non-unit-based drivers• Tracing intensive• Broad, flexible product costing• Focus on managing activities• Detailed activity information• System-wide performance maximization• Uses both financial and nonfinancial

measures of performance

18

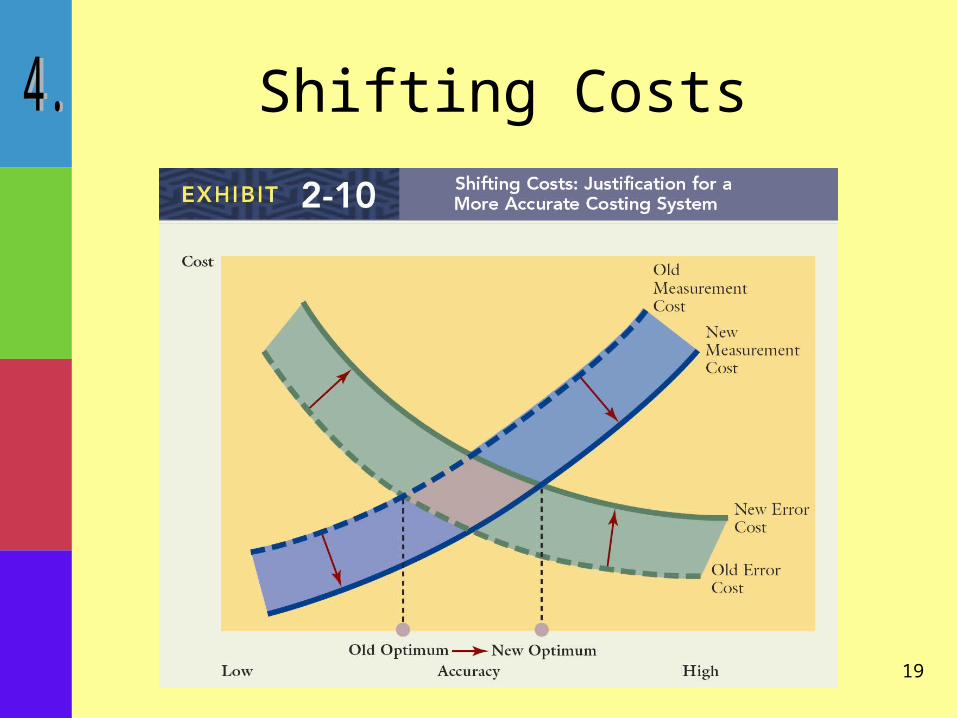

Trade-Off between Measurement Costs and Error Costs

19

Shifting Costs

COST MANAGEMENT

COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning.Cengage Learning and South-Western are trademarks used herein under license.

20

Guan ▪ Hansen ▪ Mowen

End Chapter 2

Related Documents