International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online), Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME 1 CAPITAL STRUCTURE AND ECONOMIC PERFORMANCE OF THE FIRM: EVIDENCE FROM ITALY PASQUALE DE LUCA PhD, Researcher, Faculty of Economics at Sapienza University in Rome (Italy) ABSTRACT Financing choices are one of the most critical decision for management by influencing the firm’s behaviour as well as its economic performance and value. Based on the researches of Abor (2005) and Gill, Biger and Mathur (2011) the paper is a moderate attempt to understand the relationship between capital structure and economic performance of Italian large, medium and small firms in manufacturing and service industry listed in Italian Stock Exchange in a period of 5 years (from 2007 to 2011). The analysis found a significant relationship between economic performance of the firm and its financial debt but with non-unique direction. A positive correlation was found in the medium manufacturing firms (between i) ROE and total, long-term and short-term financial debt to total assets; ii) ROA and total and short-term financial debt to total assets; iii) ROI and short-term financial debt to total assets), in the large service firms (between i) ROA and total financial debt to total assets; ii) ROI and long-term financial debt to total assets) and in the small service firms (between ROE and total and short-term financial debt to total assets). Differently a negative correlation was found in the large manufacturing firms (between i) ROE, ROA and short-term financial debt to total assets; ii) ROI and total and long-term financial debt to total assets), in the small manufacturing firms (between ROE and total and short-term financial debt to total assets) and in the large and small service firms (between ROI and short-term financial debt to total assets). In medium service firms were not found correlations. 1. INTRODUCTION The capital structure choices are relevant for the firm not only in order to maximize the returns on equity, but also because they have effects on firm’s ability to deal to its competitive environmental. The financing choices can influence the firm’s behaviour as well as its performance, survivability, business perspectives and market value. Thus, they are one of the most critical decision for management. The capital structure basically refers to the combination of equity and debt a firm uses to INTERNATIONAL JOURNAL OF MANAGEMENT (IJM) ISSN 0976-6502 (Print) ISSN 0976-6510 (Online) Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME: www.iaeme.com/ijm.asp Journal Impact Factor (2014): 7.2230 (Calculated by GISI) www.jifactor.com IJM © I A E M E

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

1

CAPITAL STRUCTURE AND ECONOMIC PERFORMANCE OF THE FIRM:

EVIDENCE FROM ITALY

PASQUALE DE LUCA

PhD, Researcher, Faculty of Economics at Sapienza University in Rome (Italy)

ABSTRACT

Financing choices are one of the most critical decision for management by influencing the

firm’s behaviour as well as its economic performance and value.

Based on the researches of Abor (2005) and Gill, Biger and Mathur (2011) the paper is a

moderate attempt to understand the relationship between capital structure and economic performance

of Italian large, medium and small firms in manufacturing and service industry listed in Italian Stock

Exchange in a period of 5 years (from 2007 to 2011).

The analysis found a significant relationship between economic performance of the firm and

its financial debt but with non-unique direction. A positive correlation was found in the medium

manufacturing firms (between i) ROE and total, long-term and short-term financial debt to total

assets; ii) ROA and total and short-term financial debt to total assets; iii) ROI and short-term

financial debt to total assets), in the large service firms (between i) ROA and total financial debt to

total assets; ii) ROI and long-term financial debt to total assets) and in the small service firms

(between ROE and total and short-term financial debt to total assets). Differently a negative

correlation was found in the large manufacturing firms (between i) ROE, ROA and short-term

financial debt to total assets; ii) ROI and total and long-term financial debt to total assets), in the

small manufacturing firms (between ROE and total and short-term financial debt to total assets) and

in the large and small service firms (between ROI and short-term financial debt to total assets). In

medium service firms were not found correlations.

1. INTRODUCTION

The capital structure choices are relevant for the firm not only in order to maximize the

returns on equity, but also because they have effects on firm’s ability to deal to its competitive

environmental. The financing choices can influence the firm’s behaviour as well as its performance,

survivability, business perspectives and market value. Thus, they are one of the most critical decision

for management.

The capital structure basically refers to the combination of equity and debt a firm uses to

INTERNATIONAL JOURNAL OF MANAGEMENT (IJM)

ISSN 0976-6502 (Print)

ISSN 0976-6510 (Online)

Volume 5, Issue 3, March (2014), pp. 01-20

© IAEME: www.iaeme.com/ijm.asp

Journal Impact Factor (2014): 7.2230 (Calculated by GISI)

www.jifactor.com

IJM © I A E M E

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

2

finance its operations and investments. Equityholders and debtholders have different level of the risk,

benefit and control. Debtholder bears the default risk, earns a fixed rate of return, and exerts a lower

and indirect control on firm's activities. Differently equityholder bears the most of the risk, his gain

are uncertainly and variables depending to the firm’s performance and its self-financing perspectives,

and exerts a full control on the firm's activities.

More than 50 years later Modigliani and Miller’s (1958) celebrate paper and despite the

theoretical models and empirical researches developed over the following years, the problem of

“optimal” capital structure is still open. Researchers continue to analyse capital structure trying to

determinate whether “optimal” capital structure exists, what are the determinates and in which way

they combine. Theories and empirical researches seem to explain some aspects under certain

condition of the firm’s behaviour. Actually there is still no theory can fully explain the firm’s

behaviour on capital structure decision or, even more, be able to define the optimal capital structure.

The problem is still open.

In this paper the relationship between capital structure and economic performance of the firm

was investigated by integrating studies and researches in strategic management and corporate finance

inside in the framework of the economic theoretical premises.

Traditionally strategic management and corporate finance are considered separately. It is argued they

are based on different paradigms not related and sometimes in opposition with difficulty for manager

to find a linkages (Bettis, 1983; Ward and Grundy, 1996).

Today, the high complexity of the firm and the relationship with its dynamic environment

require a strong integration between skills in corporate strategy and in corporate finance. Finance

plays central role in the government strategic of the firm. It is a relevant player in all business

decisions and influences the system of strategies. Every decision, operational or strategic, has

financial implications that relate to its size. Finance, therefore, has full and rightful place in the

strategic government of the firm. One of the most critical decision for finance in its role of relevant

player in the strategic government of the firm are the capital structure choices. The optimization of

capital structure is relevant since that good performances, the future survivability and business

prospects of the firm depend also on financing decisions. The leverage has an impact on competitive

strategy of the firm and therefore on its economic performance (Barton and Gordon, 1987 and 1988;

Hitt et al., 1991; Kester and Luehrman, 1992; Balakrishnan and Fox, 1993; Short, 1994; Barclay and

Smith, 1995; Kochhar, 1996; Stohs and Mauer, 1996; Shleifer and Vishny, 1997; Kochhar and Hitt,

1998; Simerly and Mingfang Li, 2000; Ozkan, 2002).

The relationship between capital structure and economic performance of the firm is

confirmed by several empirical researches although with non-unique results. Under different

perspectives and assumptions, some researches found a positive relationship while others found a

negative relationship.

The aim of this paper is a moderate attempt to understand the relationship between capital

structure and economic performance of the Italian large, medium and small firms in manufacturing

and services industry listed in Italian Stock Exchange in a period of 5 years (from 2007 to 2011).

Although there have been several researches on the relationship between capital structure and firm

performance, this paper is interesting by considering the particularity of the Italian firms and their

economic and environmental system. In this sense it is sufficient to consider three mainly aspects.

First, the Italian production is made up by small and medium firms run mostly family. Second, the

capital market is largely inefficient and profoundly bank-oriented. Third, there is a high corruption

and illegality at all level.

The paper is organized as follows. The Section-2 presents a review of literature. The Section-

3 discusses the research methodology by defining the data collection, the variables, the hypothesis

and the empirical analysis model. The Section-4 discuss empirical results. Finally Section-5

summarizes the finding of the research and concludes the discussion.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

3

2. LITERATURE REVIEW

2.1. Capital structure theories The relationship between capital structure and firm’s performance is the subject of

considerable debate. It is focused on the question about the real existence of the “optimal” capital

structure as the mix of equity and debt that maximizes the firm’s market value.

The Modigliani-Miller’s theory (1958) is considered the starting point of the modern theory

of the capital structure. Based on strong restrictive assumptions structured on perfect capital market,

MM argued that capital structure choices has irrelevant both on the value of the firm than on its cost

of capital (Proposition I and II).

The MM’s Propositions was based on very restrictive assumptions and do not hold in the real

word. Over the years many theories and empirical researches have been developed by removing the

restrictions assumptions used by MM.

The introductions in the models of many variables lead to postulate the relevance of capital

structure on firm’s performance and its market value. Thus it is possible to postulate the existence of

“optimal” capital structure as the mix of equity and debt that minimizes the cost of capital while

maximizing firm's value.

The main theoretical models about capital structure are the trade-off, the agency costs and the

pecking order.

The trade-off theory (Kraus and Litzenberger, 1973) tries to find “optimal” capital structure

balancing benefits and costs of debt as derived by taxation and financial distress and bankruptcy

costs.

Taxation generates a positive effect of debt on firm performance in order to the tax shield.

They were just Modigliani and Miller (1963), in a subsequent paper, to revise their earlier

Propositions (1958) by incorporating corporate tax other Proposition’s assumptions fixed. They

argued that under capital market imperfection where interest rate on debt are tax deductible, firm

value increases with higher financial leverage. Miller (1977), in a subsequent further study,

introduces the personal tax imposed to individuals in addition to corporate taxation on the firm.

Based on USA tax legislation, Miller identifies three taxes rate that could impact on firm’s value in

order to the relative level and connections: corporate tax rate, shareholders tax rate (imposed on the

income of the dividends) and debholders tax rate (imposed on the income of interest inflows).

In presence of default risk, debt can generate financial distress and bankruptcy costs (Myers,

1984; 2001; Ross, 1977). The use of the debt, above certain levels, increase the operational and

financial risk of the firm, increasing its default probability and bankruptcy and reduce the firm’s

value. Thus it has a negative effect on firm performance and profitability (Johnson, 1997; Bradley et

al., 1984; Titman and Wessels, 1988; Friend and Lang, 1988; MacKie-Mason, 1990; Kale et al.,

1991; Kim et al., 1998; Jordan et al., 1998; Michaelas et al., 1999; Wald, 1999; Esperanca et al.,

2003).

The risk of financial distress is mainly due to the fact that firm might not be able to generate

enough profits to repay interest on debt and return back the debt. Greater is the earning volatility of

the firm, greater is the probability of reduction of the cash flow, greater is the probability of inability

of the firm to fulfil the commitments on debt. Firm with a high business risk has less capacity to

sustain financial risks and has to use less debt (Kim and Sorensen, 1986; Titman, 1984).

Trade-off theory claims that the optimal capital structure is the point at which the marginal cost of

debt, due its negative effects, is equal to its marginal benefits due to its positive effects. At this debt

level the levered firm value is maximized.

The agency costs theory can be use to investigate the effect of debt on performance of the

firm (Jensen and Meckling, 1976; Jensen, 1986).

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

4

Considering agency costs of equity and debt, the effect of debt on firm performance is non-unique.

Debt has positive effect on agency cost of equity reducing the conflicts between shareholders and

management due to difference in their utility functions, with consequently different behaviour,

targets, information and operating decisions. While the first want to maximize equity value, the

second have incentive to maximize firm value because it increases their control of the resources,

their power and their compensation. Debt has a discipline function for managers (Jensen, 1986)

because it increase the default risk in order to the cash-out relate debt payment, requiring to

maximize efficiency, thus increasing equity value (Amihud and Lev, 1981; Jensen, 1986; Friend and

Hasbrouck, 1988; Stulz, 1990; Harris and Raviv, 1990 and 1991; Bethel and Liebeskind, 1993;

Hoskisson et al., 1994; Bergh, 1995; Noe and Rebello, 1996; Lane et al., 1998).

On the contrary debt has a negative effect on agency cost of debt increasing the conflicts

between shareholders and debtholders in order to the different claims on the firm (Jensen, 1986).

Equity offers to holders residual claim on firm’s cash flow; debt offer to holders a fixed claim over a

borrowing firm’s cash flow. Thus, it is possible shareholders’ moral hazard and asset-substitutions

(Jensen and Meckling, 1976; Diamond, 1989; Harris and Raviv, 1991). Debtholder try to anticipate

the shareholder’s opportunistic behaviour by lending less debt or increasing its cost.

The packing order theory (Myers, 1984; Myers and Majluf, 1984; Fama and French, 1998 and 2002)

based on asymmetric information in a market and postulates a hierarchy of the finance sources and

not define a “optimal” capital structure.

In asymmetric information contest, insiders are assumed to possess private information about

the firm. The presence of private information influence the perception of the investors about the

firm’s risk with consequent impact on the cost of capital. Thus, the costs of finance vary among

different financial sources (Myers, 1977 and 1984; Brennan and Kraus, 1987; Noe, 1988;

Constantinides and Grundy, 1989; Rajan and Zingales, 1995; Chittenden et al., 1996; Abor, 2005).

The direction of the relationship between capital structure choices and asymmetric information is not

clear (Harris and Raviv, 1991). On one hand, it has been hypothesized that the capital structure

choices can mitigate inefficiencies in the firm’s investment policy due to asymmetric information

reducing over-under investment problems (Myers and Majluf 1984; Myers, 1984; Narayanan, 1988;

Heinkel and Zechner, 1990; Brennan and Kraus, 1987; Noe, 1988; Constantinides and Grundy,

1989). On the other hand, it has been hypothesized that the capital structure choices signals to

investors private information about firm perspectives reducing asymmetric information (Ross, 1977;

Leland and Pyle, 1977; Heinkel, 1982; Poitevin, 1989).

The pecking order theory does not define a “optimal” capital structure but assume that firm

defines its capital structure basing on a finance sources hierarchy.

The theory suggests that firm prefers internal sources of finance instead of external source.

Firm prefers first internal source of finance due to self-finance adapting the dividend policy (payout

ratio) to the investment opportunities. If external source of finance are required, the firm prefers to

resort first to the debt, then hybrid instruments and only finally to equity. Thus there are two kinds of

equity: internal, regarding self-financing, that is at the top of the packing order; external, regarding

the issue of new shares, that is at the bottom of the packing order.

2.2. Capital structure and economic performance of the firm The empirical researches have highlighted other determinants, in addition to the models, that

could affect the capital structure choices. Among these the main are profit, age, size, growth,

industry, asset structure, managerial characteristics and ownership, institutional and macroeconomic

environment of the firm. In this paper the attention was focused on the firm profitability by

investigating the relationship between capital structure choices and economic performance of the

firm.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

5

This relationship was confirmed by several empirical researches although with discordant

results. Based on different point of view, some researches found a positive relationship between

firm's performance and its capital structure.

Roden and Lewell (1995) in a study of leveraged buyout transactions that took place in the

Unites State in a period 1981-1990, found evidence about a systemic relationship between the

proportion and the characteristics of the debt in the buyout financing package and the target firm’s

earnings rate, earnings variability, growth prospects, and its tax and liquidity position.

Nimalathasan and Valeriu (2010) in a study of 13 random selected on 31 listed manufacturing

companies in Sri Lanka for a period 2003-2007, found a positive relationship between capital

structure and firm’s profitability measured by gross profit ratio, operating profit ratio, net profit ratio

of the firm.

Majumdar and Sen (2010) in a study of Indian corporate firms in a period 1988-1993, found

that firms which rely on arm’s-length debt have better performance and are more likely to engage in

advertising and diversification than firms which rely on borrowing from institutional lenders such as

term-lending institutions.

On the contrary several studies found a negative relationship between capital structure and

firm performance.

Friend and Lang (1988) in a study of 984 firms listed in a New York Stock Exchange in a

period 1979-1983 in order to test whether capital structure choices are at least in part motivated by

managerial self interest, found that the level of debt is negatively related to the level of management

investment. Also they found that if the firm has large non-managerial investors, the average debt

ratio is significantly higher than in those with no principal stockholders.

Rajan and Zingales (1995), analysing the determinants of the capital structure choices of the

non-financial corporations of the G-7 countries in period 1987-1991, with regarding to the

relationship between debt and firm’s profitability, found a negative relationship. Similar conclusions

were found by Wald (1999) analysing the factors correlated with capital structure in different

countries.

Gleason, Mathur and Mathur (2000), in a study of 198 retailers in 14 European country

retailers for 1994, found a negative relationship between capital strucurre and firm’s performance

mainly due to agency conflict.

Booth, Aivazian, Demirguc-Kant and Maksimovic (2001), analysing the capital structure

choices of firms in 10 developing countries in comparison with developed countries, found a

negative relationship between debt and firm’s profitability.

Huang and Song (2006), analysing the determinants of capital structure choices of Chinese

listed company, found a negative relationship between debt and firm profitability.

Zeitun and Tian (2007), in a study of 167 Jordanian industrial firms (of which 47 were defaulted

firms in the following year) listed in Amman Stock Exchange in 16 sectors in a period 1989-2003,

found that a significantly negative relationship between capital structure and firm’s performance

measures in both the accounting and market measures.

Gi Shian Su and Hong Tam Vo (2010), in a study of listed firms in Vietnam, found a

significantly negative relationship between return on equity and debt ratio. They show that combined

effect of corporate strategy and capital structure explain well for the difference in firm performance.

Bistrova, Lace and Peleckiene (2011), in a study of 36 blue-chip firms listed on the Baltic Stock

Exchanges in a period 2007-2010, found that the firm pursues conservative capital management

policy. They found that firms having lower debt levels on their accounts are able to demonstrate

higher profitability. Thus, there is a negative relationship between debt and capital profitability.

Gupta, Srivastava and Sharma (2011), in a study of 100 firms listed on National Stock

Exchange of India in period 2006-2010, found a negatively correlation between firm performance

and financial leverage. The firm that has high profitability and good performance have less debt.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

6

Muzir (2011), in a study based on 114 firms listed at the Istanbul Stock Exchange in a period

1994-2003, found that asset expansions through debt may contribute much to firms’ risk exposure in

spite of tax benefits expected especially during economic downturns.

Norvaisiene (2012) in a study of 70 non-financial listed Baltic firms (28 Lithuanian firms, 14

Estonian firms, 28 Latvian firms) for a period 2002-2011, found a negative correlation between debt

level and profitability indicators for Lithuanian and Estonian firms and absence of correlation for

Latvian firms. For firms in Baltic countries higher level of debt leads to lower profitability indicators

and lower current solvency.

Tsuji (2013), in a studies based on Japanese machinery industries firms listed on the Tokyo

Stock Exchange in a period 1981-2011, found a negative relationship between capital structure and

corporate profitability.

Still other empirical researches found contemporary negative and positive relationship

between capital structure and firm performance.

Siemrly and Li (2000), in a study of 700 large U.S. firms in a variety of industry contexts

integrating elements from agency theory and transaction cost economics with strategic management,

found that environmental dynamism moderate the relationship between leverage and performance of

the firm. Leverage produces either positive and negative effects on performance depending on

whether the firm is in stable or dynamic environments. Particularly the high leverage has a positive

impact on performance for firms in stable environments while a negative impact in dynamic

environments.

Mesquita and Lara (2003), in a study on 70 Brazilian firms, found a positive correlation

between short-term debt and firm profitability and a negative relationship between long-term debt

and firm profitability.

Abor (2005), in a study of 22 firms listed in Ghana Stock Exchange during the period 1998-

2002, found a positive relationship between total and short-term debt and firm’s profitability. On the

contrary the results show a significantly negative relationship between long-term debt and firm’s

profitability.

San and Heng (2011), in a study of 49 construction firms listed in Main Board of Bursa

Malaysia in a period 2005-2008, found a positive relationship between return on capital and debt to

equity market value and between earnings per share and long-term debt to capital and a negative

relationship between earnings per share and debt to capital for big firms. Also they found a positive

relationship between operating margin and long-term debt to common equity for medium firms.

Finally they found a negative relationship between earnings per share and debt to capital for small

firms.

Gill, Biger and Mathur (2011), in a study on 272 American service and manufacturing firms

listed on New York Stock Exchange for a period of 3 years (2005-2007), found a positive

relationship between total and short-term debt and profitability of the firm in a service industry. Also

they found a positive relationship between total, long-term and short-term debt and profitability of

the firm in manufacturing industry.

Salehi and Manesh (2012), in a study based on 59 firms listed in Tehran Stock Exchange

during a period 2004-2011, found a negative relationship between profitability and firm growth with

capital structure and a positive relationship between firm size, market size, gross domestic product

growth and inflation rate with capital structure.

3. RESEARCH METHODOLOGY

3.1. Data collection

A database was built from selected firms, manufacturing and service, listed in the three main

Index (FTSE Mib, FTSE Mid Cap, FTSE Small Cap) of Italian Stock Exchange in a period of 5

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

7

years (2007-2011). Financial, insurance and real estate firms were excluded. The peculiarity of their

operations, assets structure and liabilities could distort the analysis. Also firms listed after 2007 and

firms which had made extraordinary operations during the observation period were excluded. Firms

selected are 120 of which 79 are manufacturing firms and 41 are service firms.

In this research book value was used. Data was obtained from balance sheet. Despite the market

value expresses the real value of the firm, the book value was used for three main reasons. First, the

market value of the firm is difficult to determinate, subject to the market volatility and the data

choice by reference to the market value is arbitrary. Managers tend to think in term of book value

rather than market value because it is more easily accessible, more accurately recorded and not

subject to market volatility. Second, the measurement of the firm economic performance are usually

based on income statements and the book value measure of leverage is considerate as best proxy of

market value (Rajan and Zingales, 1995; Gupta et al., 2011). Finally, the main cost of debt is the

expected cost of financial distress in the event of bankruptcy. In a financial distress situation, the

value of the firm is near to its book value. Also if bankruptcy occurs, the accurate measure of

debtholders’ liability is the book value of debt and not its market value.

3.2. Variables

The relationship between capital structure and the economic performance of the firm was

investigated by assuming the first as independent variable and the second as dependent variable.

Financial debt was used to examine the capital structure choices. It was measured by using

three indicators: total financial debt to total assets (TFD), short-term financial debt to total assets

(SFD) and long-term financial debt to total assets (LFD).

Economic performance of the firm was measured by using three classic indicators: return on

equity (ROE), return on assets (ROA) and return on investments (ROI).

Three control variables were used: firm size (SF), sales growth (SG) and firm industry (IF).

The firm size variables was defined by using the Index of Stock Market as a proxy. Therefore

all firms included in FTSE Mib (the index includes the top 40 firms by size and liquidity) were

considered large firms (SF-L); similarly all firms includes in FTSE Mid Cap (the index includes the

other 60 firms – excluding firms in FTES Mib – grater size, liquidity and capitalization) were

considered medium firms (SF-M); and finally all firms includes in FTSE Small Cap (the index includes

the other firms – excluding firms in FTSE Mib and FTSE Mid Cap – that meeting the minimum

requirement of liquidity and capitalization) were considered as small firms (SF-S).

The sales growth variable was defined by the percentage variation in revenue per year.

The firm industry variable was defined by distinguishing all firms between manufacturing and

service industry. Therefore it was assigned value one to manufacturing firm (IF(1)) and value zero to

service firms (IF(0)).

3.3. Hypothesis and empirical analysis model

The aim of the paper is to investigate the relationship between financial debt, as a proxy of

capital structure choices and measured by TFD, LFD, SFD, and economic performance, measured by

ROE, ROA and ROI, for large, medium and small firms in manufacturing and service industry.

The basic hypothesis was that financial debt has effects (positive or negative) on the

economic performance of the firm.

This basic hypothesis can be explicated for the large, medium, small manufacturing and

service firms as following:

Hp 1: There is a significant relationship between economic performance (measured by ROE, ROA

and ROI) and the financial debt (measured by TFD, LFD, and SFD) in the large, medium and small

manufacturing firms;

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

8

Hp 2: There is a significant relationship between economic performance (measured by ROE, ROA

and ROI) and the financial debt (measured by TFD, LFD, and SFD) in the large, medium and small

service firms.

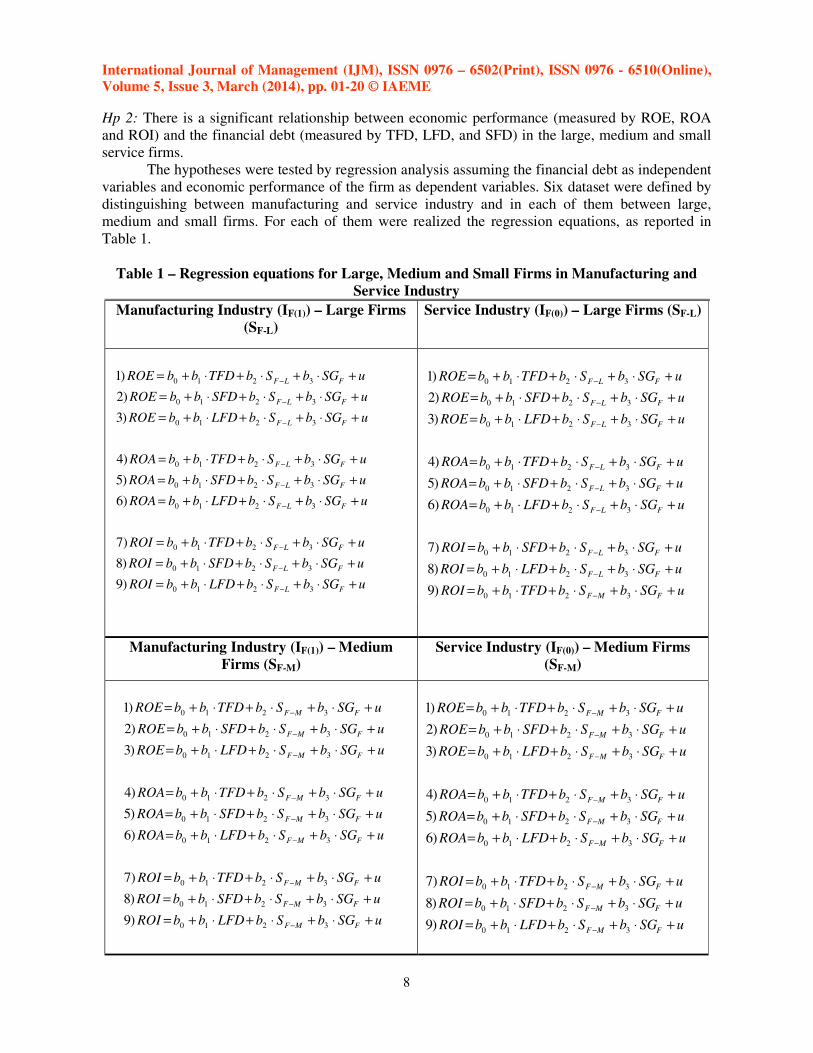

The hypotheses were tested by regression analysis assuming the financial debt as independent

variables and economic performance of the firm as dependent variables. Six dataset were defined by

distinguishing between manufacturing and service industry and in each of them between large,

medium and small firms. For each of them were realized the regression equations, as reported in

Table 1.

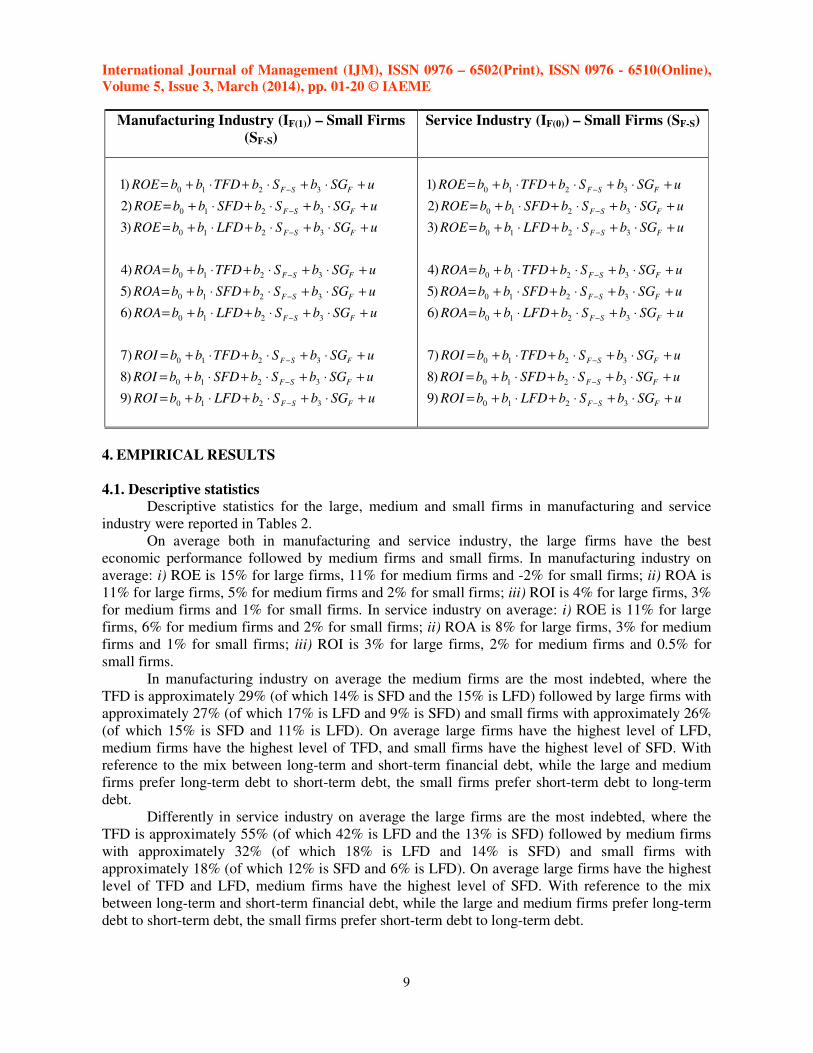

Table 1 – Regression equations for Large, Medium and Small Firms in Manufacturing and

Service Industry

Manufacturing Industry (IF(1)) – Large Firms

(SF-L)

Service Industry (IF(0)) – Large Firms (SF-L)

uSGbSbLFDbbROI

uSGbSbSFDbbROI

uSGbSbTFDbbROI

uSGbSbLFDbbROA

uSGbSbSFDbbROA

uSGbSbTFDbbROA

uSGbSbLFDbbROE

uSGbSbSFDbbROE

uSGbSbTFDbbROE

FLF

FLF

FLF

FLF

FLF

FLF

FLF

FLF

FLF

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

−

−

−

−

−

−

−

−

−

3210

3210

3210

3210

3210

3210

3210

3210

3210

)9

)8

)7

)6

)5

)4

)3

)2

)1

uSGbSbTFDbbROI

uSGbSbLFDbbROI

uSGbSbSFDbbROI

uSGbSbLFDbbROA

uSGbSbSFDbbROA

uSGbSbTFDbbROA

uSGbSbLFDbbROE

uSGbSbSFDbbROE

uSGbSbTFDbbROE

FMF

FLF

FLF

FLF

FLF

FLF

FLF

FLF

FLF

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

−

−

−

−

−

−

−

−

−

3210

3210

3210

3210

3210

3210

3210

3210

3210

)9

)8

)7

)6

)5

)4

)3

)2

)1

Manufacturing Industry (IF(1)) – Medium

Firms (SF-M)

Service Industry (IF(0)) – Medium Firms

(SF-M)

uSGbSbLFDbbROI

uSGbSbSFDbbROI

uSGbSbTFDbbROI

uSGbSbLFDbbROA

uSGbSbSFDbbROA

uSGbSbTFDbbROA

uSGbSbLFDbbROE

uSGbSbSFDbbROE

uSGbSbTFDbbROE

FMF

FMF

FMF

FMF

FMF

FMF

FMF

FMF

FMF

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

−

−

−

−

−

−

−

−

−

3210

3210

3210

3210

3210

3210

3210

3210

3210

)9

)8

)7

)6

)5

)4

)3

)2

)1

uSGbSbLFDbbROI

uSGbSbSFDbbROI

uSGbSbTFDbbROI

uSGbSbLFDbbROA

uSGbSbSFDbbROA

uSGbSbTFDbbROA

uSGbSbLFDbbROE

uSGbSbSFDbbROE

uSGbSbTFDbbROE

FMF

FMF

FMF

FMF

FMF

FMF

FMF

FMF

FMF

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

−

−

−

−

−

−

−

−

−

3210

3210

3210

3210

3210

3210

3210

3210

3210

)9

)8

)7

)6

)5

)4

)3

)2

)1

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

9

Manufacturing Industry (IF(1)) – Small Firms

(SF-S)

Service Industry (IF(0)) – Small Firms (SF-S)

uSGbSbLFDbbROI

uSGbSbSFDbbROI

uSGbSbTFDbbROI

uSGbSbLFDbbROA

uSGbSbSFDbbROA

uSGbSbTFDbbROA

uSGbSbLFDbbROE

uSGbSbSFDbbROE

uSGbSbTFDbbROE

FSF

FSF

FSF

FSF

FSF

FSF

FSF

FSF

FSF

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

−

−

−

−

−

−

−

−

−

3210

3210

3210

3210

3210

3210

3210

3210

3210

)9

)8

)7

)6

)5

)4

)3

)2

)1

uSGbSbLFDbbROI

uSGbSbSFDbbROI

uSGbSbTFDbbROI

uSGbSbLFDbbROA

uSGbSbSFDbbROA

uSGbSbTFDbbROA

uSGbSbLFDbbROE

uSGbSbSFDbbROE

uSGbSbTFDbbROE

FSF

FSF

FSF

FSF

FSF

FSF

FSF

FSF

FSF

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

+⋅+⋅+⋅+=

−

−

−

−

−

−

−

−

−

3210

3210

3210

3210

3210

3210

3210

3210

3210

)9

)8

)7

)6

)5

)4

)3

)2

)1

4. EMPIRICAL RESULTS

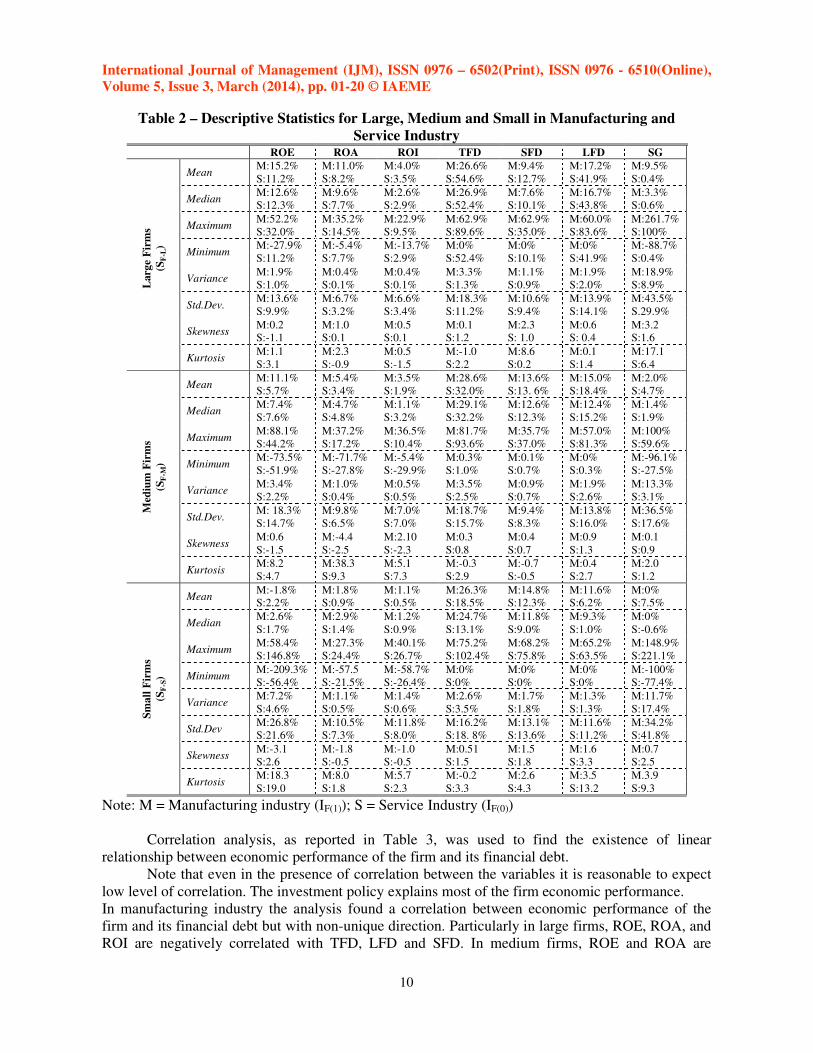

4.1. Descriptive statistics

Descriptive statistics for the large, medium and small firms in manufacturing and service

industry were reported in Tables 2.

On average both in manufacturing and service industry, the large firms have the best

economic performance followed by medium firms and small firms. In manufacturing industry on

average: i) ROE is 15% for large firms, 11% for medium firms and -2% for small firms; ii) ROA is

11% for large firms, 5% for medium firms and 2% for small firms; iii) ROI is 4% for large firms, 3%

for medium firms and 1% for small firms. In service industry on average: i) ROE is 11% for large

firms, 6% for medium firms and 2% for small firms; ii) ROA is 8% for large firms, 3% for medium

firms and 1% for small firms; iii) ROI is 3% for large firms, 2% for medium firms and 0.5% for

small firms.

In manufacturing industry on average the medium firms are the most indebted, where the

TFD is approximately 29% (of which 14% is SFD and the 15% is LFD) followed by large firms with

approximately 27% (of which 17% is LFD and 9% is SFD) and small firms with approximately 26%

(of which 15% is SFD and 11% is LFD). On average large firms have the highest level of LFD,

medium firms have the highest level of TFD, and small firms have the highest level of SFD. With

reference to the mix between long-term and short-term financial debt, while the large and medium

firms prefer long-term debt to short-term debt, the small firms prefer short-term debt to long-term

debt.

Differently in service industry on average the large firms are the most indebted, where the

TFD is approximately 55% (of which 42% is LFD and the 13% is SFD) followed by medium firms

with approximately 32% (of which 18% is LFD and 14% is SFD) and small firms with

approximately 18% (of which 12% is SFD and 6% is LFD). On average large firms have the highest

level of TFD and LFD, medium firms have the highest level of SFD. With reference to the mix

between long-term and short-term financial debt, while the large and medium firms prefer long-term

debt to short-term debt, the small firms prefer short-term debt to long-term debt.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

10

Table 2 – Descriptive Statistics for Large, Medium and Small in Manufacturing and

Service Industry

ROE ROA ROI TFD SFD LFD SG L

arg

e F

irm

s

(SF

-L)

Mean M:15.2% M:11.0% M:4.0% M:26.6% M:9.4% M:17.2% M:9.5%

S:11.2% S:8.2% S:3.5% S:54.6% S:12.7% S:41.9% S:0.4%

Median M:12.6% M:9.6% M:2.6% M:26.9% M:7.6% M:16.7% M:3.3%

S:12.3% S:7.7% S:2.9% S:52.4% S:10.1% S:43.8% S:0.6%

Maximum M:52.2% M:35.2% M:22.9% M:62.9% M:62.9% M:60.0% M:261.7%

S:32.0% S:14.5% S:9.5% S:89.6% S:35.0% S:83.6% S:100%

Minimum M:-27.9% M:-5.4% M:-13.7% M:0% M:0% M:0% M:-88.7%

S:11.2% S:7.7% S:2.9% S:52.4% S:10.1% S:41.9% S:0.4%

Variance M:1.9% M:0.4% M:0.4% M:3.3% M:1.1% M:1.9% M:18.9%

S:1.0% S:0.1% S:0.1% S:1.3% S:0.9% S:2.0% S:8.9%

Std.Dev. M:13.6% M:6.7% M:6.6% M:18.3% M:10.6% M:13.9% M:43.5%

S:9.9% S:3.2% S:3.4% S:11.2% S:9.4% S:14.1% S.29.9%

Skewness M:0.2 M:1.0 M:0.5 M:0.1 M:2.3 M:0.6 M:3.2

S:-1.1 S:0.1 S:0.1 S:1.2 S: 1.0 S: 0.4 S:1.6

Kurtosis M:1.1 M:2.3 M:0.5 M:-1.0 M:8.6 M:0.1 M:17.1

S:3.1 S:-0.9 S:-1.5 S:2.2 S:0.2 S:1.4 S:6.4

Med

ium

Fir

ms

(SF

-M)

Mean M:11.1% M:5.4% M:3.5% M:28.6% M:13.6% M:15.0% M:2.0%

S:5.7% S:3.4% S:1.9% S:32.0% S:13. 6% S:18.4% S:4.7%

Median M:7.4% M:4.7% M:1.1% M:29.1% M:12.6% M:12.4% M:1.4%

S:7.6% S:4.8% S:3.2% S:32.2% S:12.3% S:15.2% S:1.9%

Maximum M:88.1% M:37.2% M:36.5% M:81.7% M:35.7% M:57.0% M:100%

S:44.2% S:17.2% S:10.4% S:93.6% S:37.0% S:81.3% S:59.6%

Minimum M:-73.5% M:-71.7% M:-5.4% M:0.3% M:0.1% M:0% M:-96.1%

S:-51.9% S:-27.8% S:-29.9% S:1.0% S:0.7% S:0.3% S:-27.5%

Variance M:3.4% M:1.0% M:0.5% M:3.5% M:0.9% M:1.9% M:13.3%

S:2.2% S:0.4% S:0.5% S:2.5% S:0.7% S:2.6% S:3.1%

Std.Dev. M: 18.3% M:9.8% M:7.0% M:18.7% M:9.4% M:13.8% M:36.5%

S:14.7% S:6.5% S:7.0% S:15.7% S:8.3% S:16.0% S:17.6%

Skewness M:0.6 M:-4.4 M:2.10 M:0.3 M:0.4 M:0.9 M:0.1

S:-1.5 S:-2.5 S:-2.3 S:0.8 S:0.7 S:1.3 S:0.9

Kurtosis M:8.2 M:38.3 M:5.1 M:-0.3 M:-0.7 M:0.4 M:2.0

S:4.7 S:9.3 S:7.3 S:2.9 S:-0.5 S:2.7 S:1.2

Sm

all

Fir

ms

(SF

-S)

Mean M:-1.8% M:1.8% M:1.1% M:26.3% M:14.8% M:11.6% M:0%

S:2.2% S:0.9% S:0.5% S:18.5% S:12.3% S:6.2% S:7.5%

Median M:2.6% M:2.9% M:1.2% M:24.7% M:11.8% M:9.3% M:0%

S:1.7% S:1.4% S:0.9% S:13.1% S:9.0% S:1.0% S:-0.6%

Maximum M:58.4% M:27.3% M:40.1% M:75.2% M:68.2% M:65.2% M:148.9%

S:146.8% S:24.4% S:26.7% S:102.4% S:75.8% S:63.5% S:221.1%

Minimum M:-209.3% M:-57.5 M:-58.7% M:0% M:0% M:0% M:-100%

S:-56.4% S:-21.5% S:-26.4% S:0% S:0% S:0% S:-77.4%

Variance M:7.2% M:1.1% M:1.4% M:2.6% M:1.7% M:1.3% M:11.7%

S:4.6% S:0.5% S:0.6% S:3.5% S:1.8% S:1.3% S:17.4%

Std.Dev M:26.8% M:10.5% M:11.8% M:16.2% M:13.1% M:11.6% M:34.2%

S:21.6% S:7.3% S:8.0% S:18. 8% S:13.6% S:11.2% S:41.8%

Skewness M:-3.1 M:-1.8 M:-1.0 M:0.51 M:1.5 M:1.6 M:0.7

S:2.6 S:-0.5 S:-0.5 S:1.5 S:1.8 S:3.3 S:2.5

Kurtosis M:18.3 M:8.0 M:5.7 M:-0.2 M:2.6 M:3.5 M.3.9

S:19.0 S:1.8 S:2.3 S:3.3 S:4.3 S:13.2 S:9.3

Note: M = Manufacturing industry (IF(1)); S = Service Industry (IF(0))

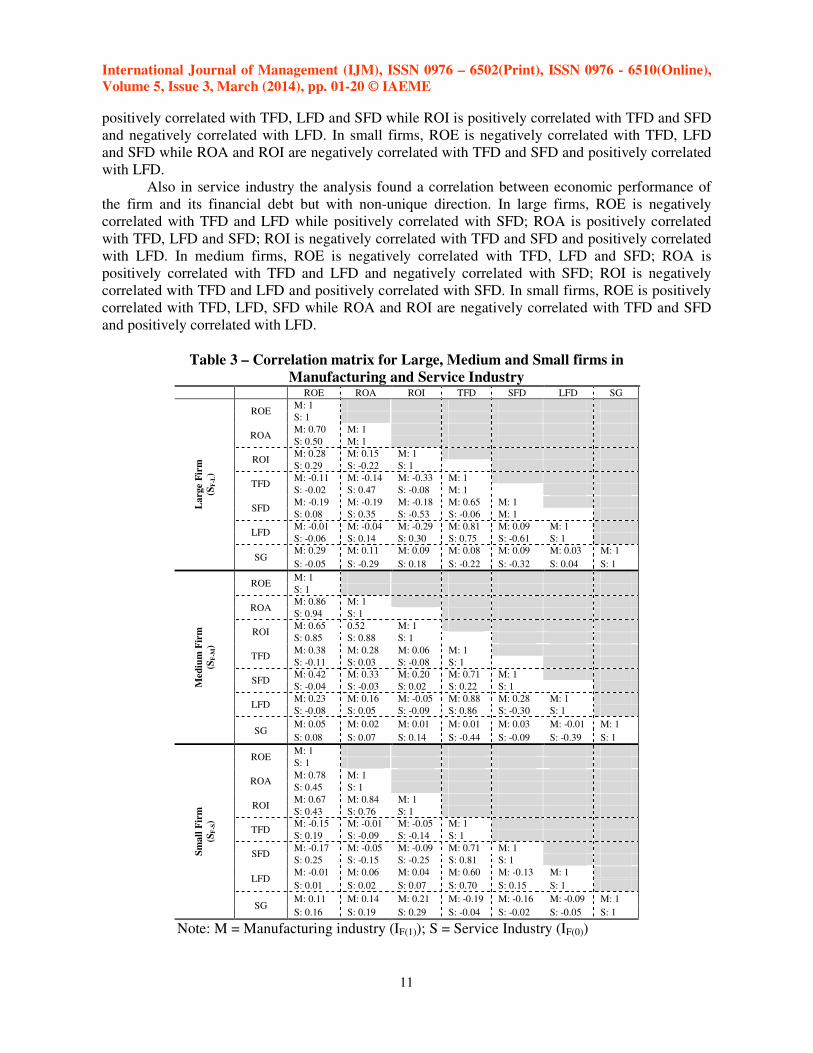

Correlation analysis, as reported in Table 3, was used to find the existence of linear

relationship between economic performance of the firm and its financial debt.

Note that even in the presence of correlation between the variables it is reasonable to expect

low level of correlation. The investment policy explains most of the firm economic performance.

In manufacturing industry the analysis found a correlation between economic performance of the

firm and its financial debt but with non-unique direction. Particularly in large firms, ROE, ROA, and

ROI are negatively correlated with TFD, LFD and SFD. In medium firms, ROE and ROA are

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

11

positively correlated with TFD, LFD and SFD while ROI is positively correlated with TFD and SFD

and negatively correlated with LFD. In small firms, ROE is negatively correlated with TFD, LFD

and SFD while ROA and ROI are negatively correlated with TFD and SFD and positively correlated

with LFD.

Also in service industry the analysis found a correlation between economic performance of

the firm and its financial debt but with non-unique direction. In large firms, ROE is negatively

correlated with TFD and LFD while positively correlated with SFD; ROA is positively correlated

with TFD, LFD and SFD; ROI is negatively correlated with TFD and SFD and positively correlated

with LFD. In medium firms, ROE is negatively correlated with TFD, LFD and SFD; ROA is

positively correlated with TFD and LFD and negatively correlated with SFD; ROI is negatively

correlated with TFD and LFD and positively correlated with SFD. In small firms, ROE is positively

correlated with TFD, LFD, SFD while ROA and ROI are negatively correlated with TFD and SFD

and positively correlated with LFD.

Table 3 – Correlation matrix for Large, Medium and Small firms in

Manufacturing and Service Industry

ROE ROA ROI TFD SFD LFD SG

Larg

e F

irm

(SF

-L)

ROE M: 1

S: 1

ROA M: 0.70 M: 1

S: 0.50 M: 1

ROI M: 0.28 M: 0.15 M: 1

S: 0.29 S: -0.22 S: 1

TFD M: -0.11 M: -0.14 M: -0.33 M: 1

S: -0.02 S: 0.47 S: -0.08 M: 1

SFD M: -0.19 M: -0.19 M: -0.18 M: 0.65 M: 1

S: 0.08 S: 0.35 S: -0.53 S: -0.06 M: 1

LFD M: -0.01 M: -0.04 M: -0.29 M: 0.81 M: 0.09 M: 1

S: -0.06 S: 0.14 S: 0.30 S: 0.75 S: -0.61 S: 1

SG M: 0.29 M: 0.11 M: 0.09 M: 0.08 M: 0.09 M: 0.03 M: 1

S: -0.05 S: -0.29 S: 0.18 S: -0.22 S: -0.32 S: 0.04 S: 1

Med

ium

Fir

m

(SF

-M)

ROE M: 1

S: 1

ROA M: 0.86 M: 1

S: 0.94 S: 1

ROI M: 0.65 0.52 M: 1

S: 0.85 S: 0.88 S: 1

TFD M: 0.38 M: 0.28 M: 0.06 M: 1

S: -0.11 S: 0.03 S: -0.08 S: 1

SFD M: 0.42 M: 0.33 M: 0.20 M: 0.71 M: 1

S: -0.04 S: -0.03 S: 0.02 S: 0.22 S: 1

LFD M: 0.23 M: 0.16 M: -0.05 M: 0.88 M: 0.28 M: 1

S: -0.08 S: 0.05 S: -0.09 S: 0.86 S: -0.30 S: 1

SG M: 0.05 M: 0.02 M: 0.01 M: 0.01 M: 0.03 M: -0.01 M: 1

S: 0.08 S: 0.07 S: 0.14 S: -0.44 S: -0.09 S: -0.39 S: 1

Sm

all

Fir

m

(SF

-S)

ROE M: 1

S: 1

ROA M: 0.78 M: 1

S: 0.45 S: 1

ROI M: 0.67 M: 0.84 M: 1

S: 0.43 S: 0.76 S: 1

TFD M: -0.15 M: -0.01 M: -0.05 M: 1

S: 0.19 S: -0.09 S: -0.14 S: 1

SFD M: -0.17 M: -0.05 M: -0.09 M: 0.71 M: 1

S: 0.25 S: -0.15 S: -0.25 S: 0.81 S: 1

LFD M: -0.01 M: 0.06 M: 0.04 M: 0.60 M: -0.13 M: 1

S: 0.01 S: 0.02 S: 0.07 S: 0.70 S: 0.15 S: 1

SG M: 0.11 M: 0.14 M: 0.21 M: -0.19 M: -0.16 M: -0.09 M: 1

S: 0.16 S: 0.19 S: 0.29 S: -0.04 S: -0.02 S: -0.05 S: 1

Note: M = Manufacturing industry (IF(1)); S = Service Industry (IF(0))

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

12

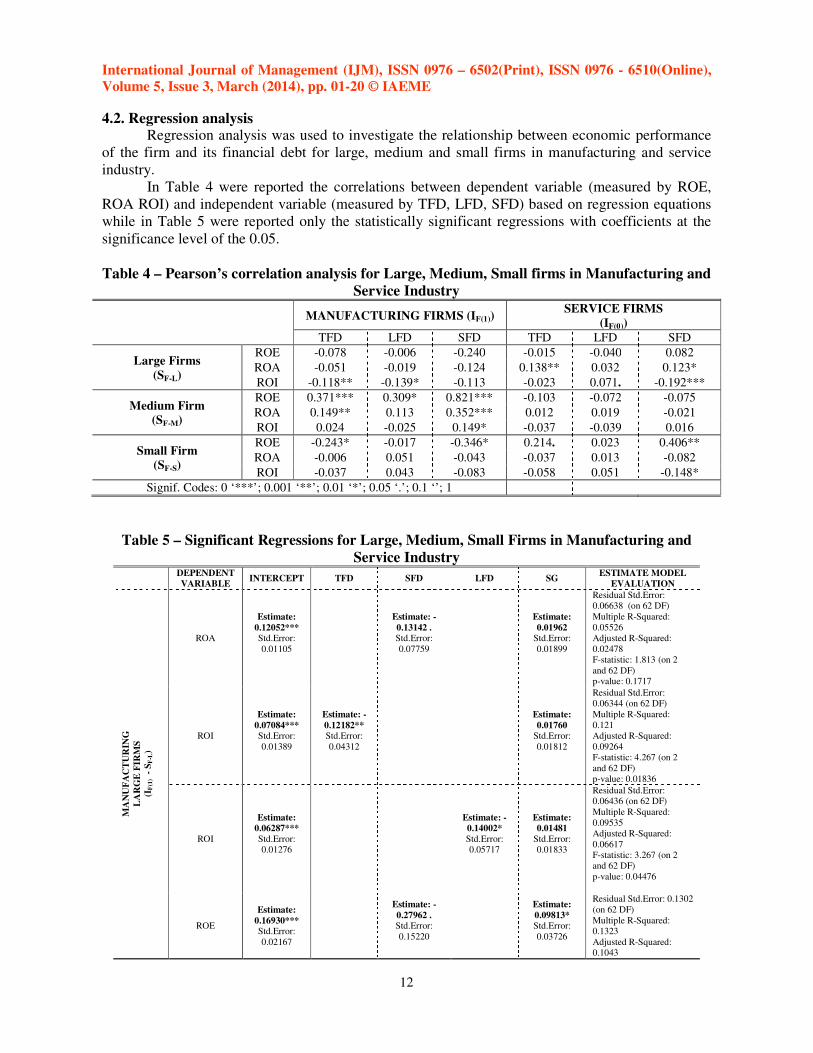

4.2. Regression analysis Regression analysis was used to investigate the relationship between economic performance

of the firm and its financial debt for large, medium and small firms in manufacturing and service

industry.

In Table 4 were reported the correlations between dependent variable (measured by ROE,

ROA ROI) and independent variable (measured by TFD, LFD, SFD) based on regression equations

while in Table 5 were reported only the statistically significant regressions with coefficients at the

significance level of the 0.05.

Table 4 – Pearson’s correlation analysis for Large, Medium, Small firms in Manufacturing and

Service Industry

MANUFACTURING FIRMS (IF(1))

SERVICE FIRMS

(IF(0))

TFD LFD SFD TFD LFD SFD

Large Firms

(SF-L)

ROE -0.078 -0.006 -0.240 -0.015 -0.040 0.082

ROA -0.051 -0.019 -0.124 0.138** 0.032 0.123*

ROI -0.118** -0.139* -0.113 -0.023 0.071. -0.192***

Medium Firm

(SF-M)

ROE 0.371*** 0.309* 0.821*** -0.103 -0.072 -0.075

ROA 0.149** 0.113 0.352*** 0.012 0.019 -0.021

ROI 0.024 -0.025 0.149* -0.037 -0.039 0.016

Small Firm

(SF-S)

ROE -0.243* -0.017 -0.346* 0.214. 0.023 0.406**

ROA -0.006 0.051 -0.043 -0.037 0.013 -0.082

ROI -0.037 0.043 -0.083 -0.058 0.051 -0.148*

Signif. Codes: 0 ‘***’; 0.001 ‘**’; 0.01 ‘*’; 0.05 ‘.’; 0.1 ‘’; 1

Table 5 – Significant Regressions for Large, Medium, Small Firms in Manufacturing and

Service Industry

DEPENDENT

VARIABLE INTERCEPT TFD SFD LFD SG

ESTIMATE MODEL

EVALUATION

MA

NU

FA

CT

UR

ING

LA

RG

E F

IRM

S

(IF

(1) -

SF

-L)

ROA

Estimate:

0.12052*** Std.Error:

0.01105

Estimate: -

0.13142 . Std.Error:

0.07759

Estimate:

0.01962 Std.Error:

0.01899

Residual Std.Error: 0.06638 (on 62 DF)

Multiple R-Squared:

0.05526 Adjusted R-Squared:

0.02478 F-statistic: 1.813 (on 2

and 62 DF) p-value: 0.1717

ROI

Estimate:

0.07084*** Std.Error:

0.01389

Estimate: -

0.12182** Std.Error:

0.04312

Estimate:

0.01760 Std.Error:

0.01812

Residual Std.Error: 0.06344 (on 62 DF)

Multiple R-Squared:

0.121 Adjusted R-Squared:

0.09264 F-statistic: 4.267 (on 2

and 62 DF) p-value: 0.01836

ROI

Estimate:

0.06287***

Std.Error: 0.01276

Estimate: -

0.14002*

Std.Error: 0.05717

Estimate:

0.01481

Std.Error: 0.01833

Residual Std.Error: 0.06436 (on 62 DF)

Multiple R-Squared:

0.09535 Adjusted R-Squared:

0.06617 F-statistic: 3.267 (on 2 and 62 DF)

p-value: 0.04476

ROE

Estimate:

0.16930*** Std.Error:

0.02167

Estimate: -

0.27962 . Std.Error:

0.15220

Estimate:

0.09813* Std.Error:

0.03726

Residual Std.Error: 0.1302

(on 62 DF)

Multiple R-Squared: 0.1323

Adjusted R-Squared: 0.1043

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

13

F-statistic: 4.725 (on 2 and 62 DF)

p-value: 0.01231

MA

NU

FA

CT

UR

ING

ME

DIU

M F

IRM

S

(IF

(1) -

SF

-L)

ROA

Estimate:

0.011529

Std.Error: 0.017493

Estimate:

0.148820**

Std.Error:

0.051258

Estimate:

0.006501

Std.Error:

0.026349

Residual Std.Error: 0.09599 (on 97 DF)

Multiple R-Squared: 0.08056

Adjusted R-Squared:

0.06161 F-statistic: 4.25 (on 2 and

97 DF) p-value: 0.01701

ROA

Estimate:

0.006092

Std.Error: 0.016651

Estimate:

0.351860***

Std.Error:

0.100787

Estimate:

0.004300

Std.Error:

0.025903

Residual Std.Error:

0.09432 (on 97 DF) Multiple R-Squared:

0.1122

Adjusted R-Squared:

0.09391 F-statistic: 6.13 (on 2 and

97 DF) p-value: 0.003112

ROI

Estimate:

0.015047

Std.Error: 0.012347

Estimate:

0.149222*

Std.Error: 0.074736

Estimate:

0.001494

Std.Error: 0.019207

Residual Std.Error:

0.06994 (on 97 DF) Multiple R-Squared:

0.03966

Adjusted R-Squared: 0.01985

F-statistic: 2.003 (on 2

and 97 DF) p-value: 0.1405

ROE

Estimate:

0.004613

Std.Error: 0.031365

Estimate:

0.371238***

Std.Error: 0.091904

Estimate:

0.025902

Std.Error: 0.047244

Residual Std.Error: 0.1721

(on 97 DF) Multiple R-Squared:

0.1465

Adjusted R-Squared: 0.1289

F-statistic: 8.323 (on 2

and 97 DF) p-value: 0.0004615

ROE

Estimate: -

0.0008932

Std.Error: 0.0298299

Estimate:

0.8185188***

Std.Error: 0.1805609

Estimate:

0.0208600

Std.Error: 0.0464045

Residual Std.Error: 0.169

(on 97 DF) Multiple R-Squared:

0.1772

Adjusted R-Squared: 0.1602

F-statistic: 10.45 (on 2

and 97 DF) p-value: 7.793e-0.5

ROE

Estimate:

0.06422* Std.Error:

0.02669

Estimate:

0.30957* Std.Error:

0.13119

Estimate:

0.02856

Std.Error: 0.04966

Residual Std.Error: 0.1809

(on 97 DF) Multiple R-Squared:

0.057026

Adjusted R-Squared: 0.03758

F-statistic: 2.933 (on 2

and 97 DF) p-value: 0.05799

MA

NU

FA

CT

UR

ING

SM

AL

L F

IRM

S

(IF

(1) -

SF

-L)

ROE

Estimate:

0.03873

Std.Error:

0.03497

Estimate: -

0.21428 .

Std.Error:

0.11369

Estimate:

0.06965 Std.Error:

0.05399

Residual Std.Error: 0.2663 (on 213 DF)

Multiple R-Squared:

0.02919 Adjusted R-Squared:

0.02008

F-statistic: 3.202 (on 2 and 213 DF)

p-value: 0.04263

ROE

Estimate:

0.02902

Std.Error:

0.02746

Estimate: -

0.31606*

Std.Error:

0.14009

Estimate:

0.06952 Std.Error:

0.05350

Residual Std.Error: 0.2654 (on 213 DF)

Multiple R-Squared:

0.03604 Adjusted R-Squared:

0.02699

F-statistic: 3.981 (on 2 and 213 DF)

p-value: 0.02006

SE

RV

I

CE

LA

RG ROA

Estimate:

0.01357 Std.Error:

Estimate:

0.12485* Std.Error:

Estimate: -

0.02238 Std.Error:

Residual Std.Error:

0.02972 (on 32 DF) Multiple R-Squared:

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

14

0.02562 0.04594 0.01724

0.2579

Adjusted R-Squared: 0.2115 F-statistic: 5.56 (on 2 and

32 DF)

p-value: 0.008461

ROI

Estimate:

0.058905***

Std.Error: 0.008812

Estimate: -

0.190478**

Std.Error: 0.056868

Estimate:

0.001585

Std.Error: 0.017947

Residual Std.Error: 0.03

(on 32 DF)

Multiple R-Squared: 0.2848

Adjusted R-Squared: 0.2401 F-statistic: 6.371 (on 2

and 32 DF)

p-value: 0.004689

ROI

Estimate:

0.00558

Std.Error: 0.017562

Estimate:

0.069704 .

Std.Error: 0.039698

Estimate:

0.019470

Std.Error: 0.018876

Residual Std.Error: 0.0333

(on 32 DF)

Multiple R-Squared: 0.1189

Adjusted R-Squared: 0.06384 F-statistic: 2.159 (on 2

and 32 DF)

p-value: 0.1319

SE

RV

ICE

SM

AL

L F

IRM

S

(IF

(1) -

SF

-L)

ROI

Estimate:

0.01829 . Std.Error:

0.01004

Estimate: -

0.14556**

Std.Error: 0.05428

Estimate:

0.05505**

Std.Error: 0.01758

Residual Std.Error:

0.07522 (on 102 DF) Multiple R-Squared:

0.1446

Adjusted R-Squared: 0.1278 F-statistic: 8.622 (on 2

and 102 DF) p-value: 0.0003472

ROE

Estimate: -

0.02492 Std.Error:

0.02931

Estimate:

0.22147*

Std.Error: 0.10999

Estimate:

0.08594 .

Std.Error: 0.04950

Residual Std.Error: 0.2116 (on 102DF)

Multiple R-Squared:

0.06268

Adjusted R-Squared: 0.0443 F-statistic: 3.411 (on 2

and 102 DF) p-value: 0.03683

ROE

Estimate: -

0.03436 Std.Error:

0.02780

Estimate:

0.40952** Std.Error:

0.15036

Estimate:

0.08424 . Std.Error:

0.04871

Residual Std.Error: 0.2083 (on 102 DF)

Multiple R-Squared:

0.0915 Adjusted R-Squared:

0.07368 F-statistic: 5.136 (on 2

and 102 DF) p-value: 0.007493

Signif. Codes: 0 ‘***’; 0.001 ‘**’; 0.01 ‘*’; 0.05 ‘.’; 0.1‘’; 1

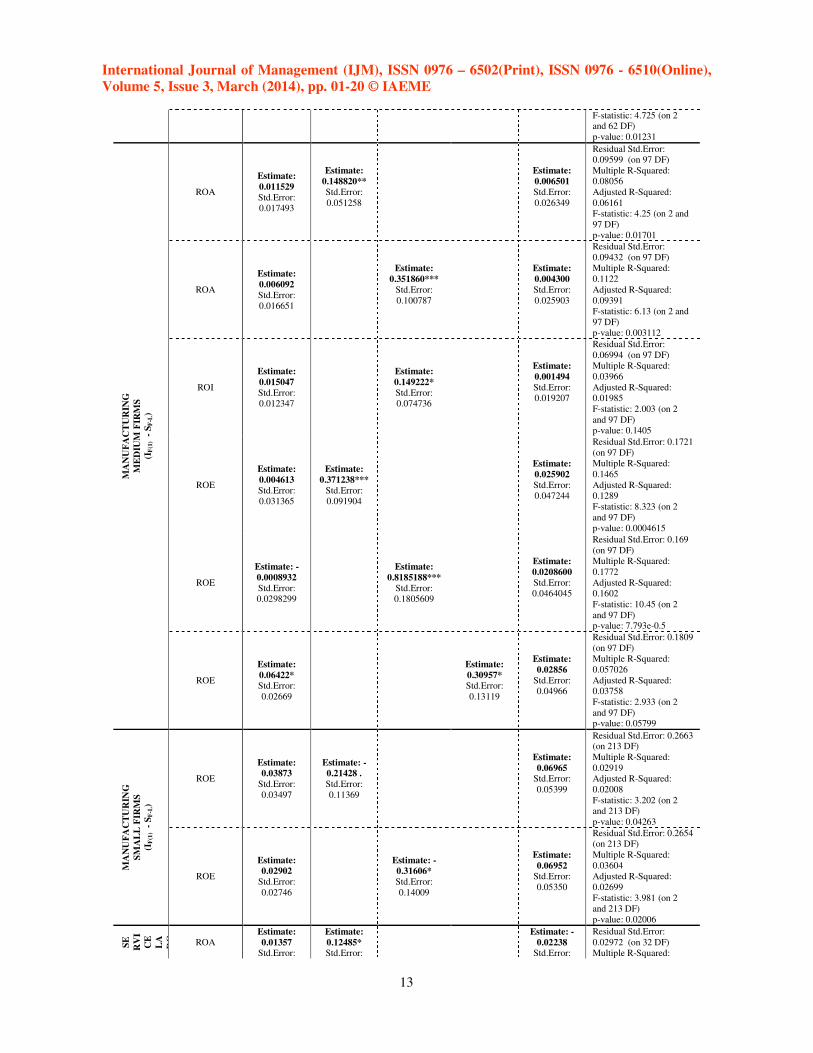

In manufacturing industry the relationship between economic performance of the firm and its

financial debt are more evident than in service industry.

In manufacturing industry, the analysis found discordant results. While negative relationship

between firm economic performance and financial debt in the large and small firms was found, in

medium firms a positive relationship between them was found. Particularly in large manufacturing

firms were found negative relationships between ROE, ROA and SFD and between ROI and TFD,

LFD. Therefore the increase of financial debt has negative effect on firm performance. While the

increase of TFD and LFD has a negative effect on ROI with its decrease, the increase of SFD has a

negative effect on ROE and ROA with their decrease. Between ROE, ROA and TFD, LFD and

between ROI and SFD were not found statistically significant relationships. In medium

manufacturing firms were found positive relationships between ROE and TFD, LFD, SFD, between

ROI and SFD and between ROA and TFD, SFD. Therefore the increase of TFD has a positive effect

on ROE and ROA with their increase, the increase of LFD has a positive effect on ROE with its

increase and the increase of SFD has a positive effect on ROE, ROA and ROI with their increase.

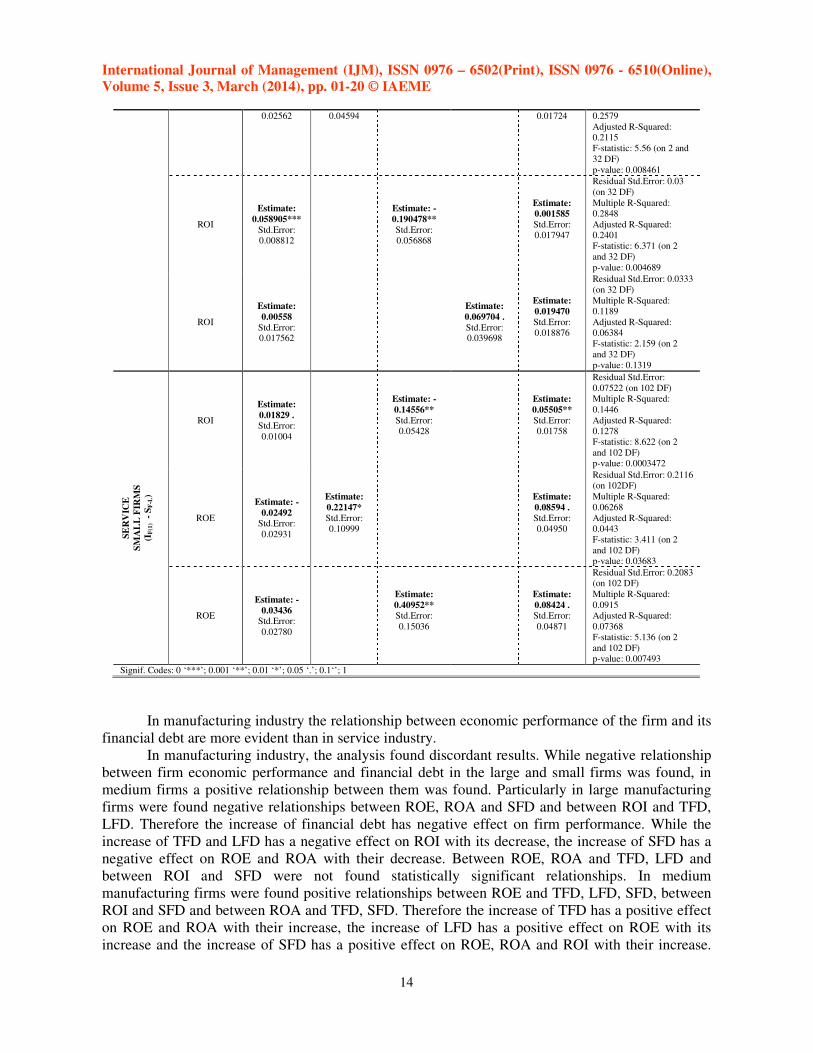

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

15

Between ROI and TFD, LFD and between ROA and LFD were not found statistically significant

relationships. Finally in small manufacturing firms were found negative relationships between ROE

and TFD, SFD. Thus the increase of TFD and SFD has a negative effect on ROE with its decrease.

Between ROA, ROI and TFD, LFD, SFD and between ROE and LFD were not found statistically

significant relationships.

Also in service industry the analysis found discordant results. In large service firms were

found positive relationships between ROA and TFD and between ROI and LFD while a negative

relationship was found between ROI and SFD. Therefore the increase of TFD and LFD has a

positive effect on ROA and ROI respectively with their increase while the increase of SFD has a

negative effects on ROI with its decrease. Between ROE and TFD, LFD, SFD, between ROA and

LFD, SFD, and between ROI and TFD, SFD, were not found statistically significant relationships. In

small service firms were found positive relationships between ROE and TFD, SFD while a negative

relationship was found between ROI and SFD. Therefore the increase of TFD and SFD has positive

effect on ROE while the increase in SFD has negative effect on ROI. Between ROE and LFD,

between ROA and TFD, LFD, SFD, and between ROI and TFD, LFD, were not found statistically

significant relationships. For all medium service firms were not found a statistically significant

relationship between dependent and independent variables.

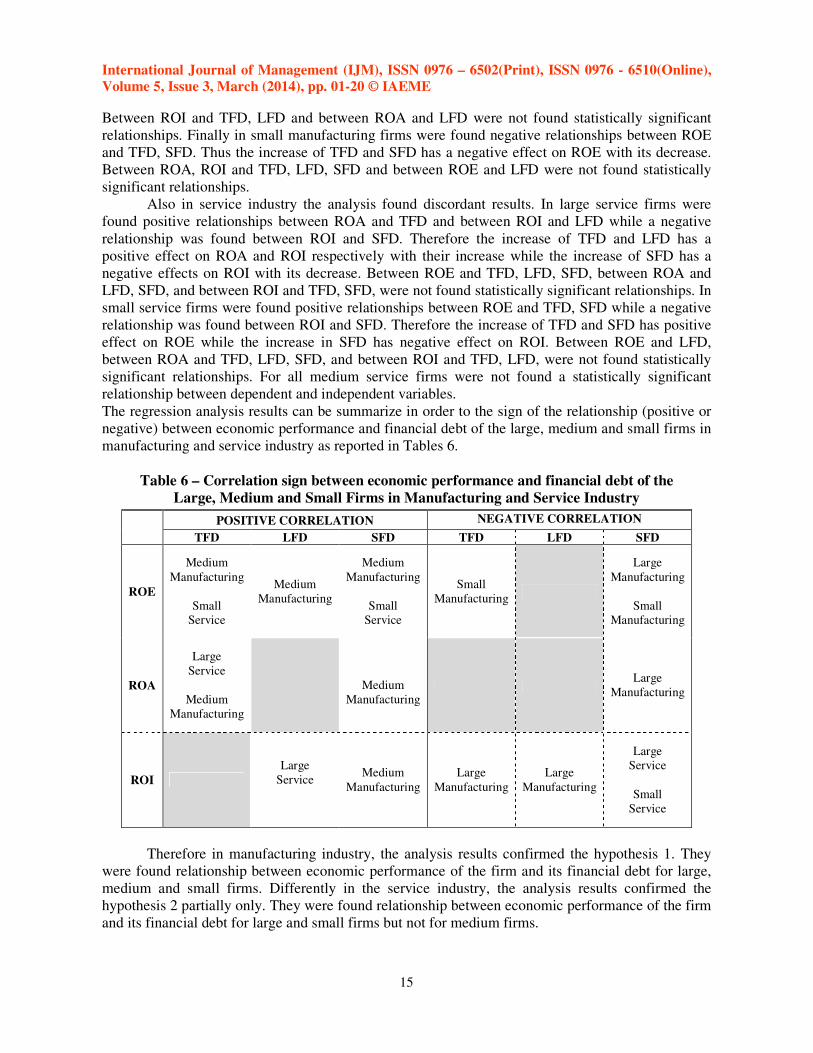

The regression analysis results can be summarize in order to the sign of the relationship (positive or

negative) between economic performance and financial debt of the large, medium and small firms in

manufacturing and service industry as reported in Tables 6.

Table 6 – Correlation sign between economic performance and financial debt of the

Large, Medium and Small Firms in Manufacturing and Service Industry

POSITIVE CORRELATION NEGATIVE CORRELATION

TFD LFD SFD TFD LFD SFD

ROE

Medium

Manufacturing

Small

Service

Medium

Manufacturing

Medium

Manufacturing

Small

Service

Small

Manufacturing

Large

Manufacturing

Small

Manufacturing

ROA

Large

Service

Medium

Manufacturing

Medium

Manufacturing

Large

Manufacturing

ROI

Large

Service

Medium

Manufacturing

Large

Manufacturing

Large

Manufacturing

Large

Service

Small

Service

Therefore in manufacturing industry, the analysis results confirmed the hypothesis 1. They

were found relationship between economic performance of the firm and its financial debt for large,

medium and small firms. Differently in the service industry, the analysis results confirmed the

hypothesis 2 partially only. They were found relationship between economic performance of the firm

and its financial debt for large and small firms but not for medium firms.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

16

5. CONCLUSIONS

This paper is a moderate attempt to understand the relationship between capital structure and

economic performance of the Italian large, medium and small firms in manufacturing and service

industry listed in Italian Stock Exchange.

The basic hypothesis is that the financial debt affects (negatively or positively) the economic

performance of the large, medium and small firms in manufacturing and service industry. The

analysis found a significant relationship between economic performance of the firm and its financial

debt but with discordant results. Also the relationship is more relevant in manufacturing industry

than in service industry.

The results of the analysis can be summarize as following:

1. The economic performances of the firms, on average, are higher in manufacturing industry than

in service industry. On average, both in manufacturing and service industry, the large firm have

the best economic performance followed by medium firm and small firm.

2. In manufacturing industry financial debt is lower than service industry for large and medium

firms. It is relevant to note that Italian firms usually tend to use commercial debt (trade payables)

as a substitute of financial debts. Looking at financial debt duration, both in the manufacturing

and service industry, large and medium firms prefers long-term debt to short-term debt while

small firms prefer short-term debt to long-term debt. It is mainly due to the possibility for the

large and medium firms obtain debt at better condition than small firms.

3. For the large firms the analysis found discordant results between manufacturing and service

industry.

In large manufacturing firms, compared to positive economic performances (on average ROE is

15%, ROA is 11% and ROI is 4%), TFD is 27% (of which LFD is 17% and SFD is 9%). For

these firms, the analysis found a negative correlation between ROI and TFD, LFD, and between

ROA, ROE and SFD.

In large service firms, compared to positive economic performances lower than large

manufacturing firms (on average ROE is 11%, ROA is 8% and ROI is 3%), TFD is higher than

large manufacturing firms (on average 55% of which the LFD is 42% and SFD is 13%). For

these firms, the analysis found a positive correlation between ROA and TFD and between ROI

and LFD and negative correlation between ROI and SFD.

4. Also for the medium firms the analysis found discordant results between manufacturing and

service industry.

In medium manufacturing firms, compared to positive economic performances (on average ROE

is 11%, ROA is 5% and ROI is 3%), TFD is 29% (of which LFD is 15% and SFD is 14%). For

these firms, the analysis found a positive correlation between ROE and TFD, LFD, SFD, between

ROA and TFD, SFD, and between ROI and SFD.

In medium service firms, compared to positive economic performances lower than medium

manufacturing firms (on average ROE is 6%, ROA is 3% and ROI is 2%), TFD is higher than

medium manufacturing firms (on average 32% of which the LFD is 18% and SFD is 14%). For

these firms, the analysis did not found a correlation between ROE, ROA, ROI and TFD, LFD,

SFD.

5. For the small firms the analysis found a concordant results in manufacturing and service industry.

In small manufacturing firms, compared to negative ROE (-2%) and positive ROA (2%) and ROI

(1%), TFD is 26% (of which SFD is 15% and LFD is 12%). For these firms, the analysis found a

negative correlation between ROE and TFD, SFD.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

17

In small service firms, compared to positive economic performances (on average ROE is 2%,

ROA is 1% and ROI is 0.5%), TFD is lower than small manufacturing firms (on average 18% of

which the SFD is 12% and LFD is 6%). For these firms, the analysis found a negative correlation

between ROI and SFD and positive correlation between ROE and TFD, SFD.

Therefore in manufacturing industry, the analysis results confirmed the hypothesis 1 while in

service industry the hypothesis 2 was confirmed only partially.

REFERENCES

1. Abor J., 2005. The effect of capital structure on profitability: empirical analysis of listed firms

in Ghana. Journal of Risk Finance, 6(5), pp. 438-445.

2. Amihud Y., Lev B., 1981. Risk reduction as a managerial motive for conglomerate mergers.

Bell Journal of Economics, 12(2), pp. 605-6017.

3. Balakrishnan S., Fox I., 1993. Asset specificity, firm heterogeneity and capital structure.

Strategic Management Journal, 14 (1), pp.3-16.

4. Barclay M.J., Smith C.W., 1995. The maturity structure of Corporate Debt. Journal of

Finance, 50, pp.609-632.

5. Barton S.L., Gordon P.J., 1987. Corporate strategy: useful perspective for the study of capital

structure?. Academy of Management Review, 12, pp.67-75.

6. Barton S.L., Gordon P.J., 1988. Corporate strategy and capital structure. Strategic

Management Journal, 9(6), pp.623-632.

7. Bergh D.D., 1995. Size and relatedness of units sold. Strategic Management Journal, 16(3),

pp. 221-240.

8. Bethel J.E., Liebeskind J., 1993. The effects of ownership structure on corporate restructuring.

Strategic Management Journal (summer special issue), 14, pp. 15-31.

9. Bettis R., 1983. Modern Financial Theory, Corporate Strategy and Public Policy: Three

Conundrums. Academy of Management Review, 8, 3, pp. 406-415.

10. Bistrova J., Lace N., Peleckiene V., 2011. The Influence of Capital Structure on Baltic

Corporate Performance. Journal of Business Economics and Management, 12(4), pp. 655-669.

11. Booth L., Aivazian V., Demirguc-Kunt, Maksimovic V., 2001. Capital structure in developing

countries. Journal of Finance, 55(1), pp.87-130.

12. Bradley M., Jarrel G.A, Han Kim E., 1984. On the existence of an optimal capital structure:

Theory and evidence. Journal of Finance, 39, pp. 857-880.

13. Brennan M., Kraus A., 1987. Efficient financing under asymmetric information. Journal of

Finance, 42, pp. 1225-1243.

14. Chittenden F., Hall G., Hutchinson P., 1996. Small firm growth, access to capital markets and

financial structure: review of issue and an empirical investigation. Small Business Economics,

8 (1), pp. 59-67.

15. Constantinides G.M., Grundy B.D., 1989. Optimal investment with stock repurchase and

financing as signals. The review of Financial Studies, 2, pp. 445-466.

16. Diamond D.W., 1989. Reputation acquisition in debt markets. Journal of Political Economy,

97, pp. 828-862.

17. Esperanca J.P., Ana P.M.G., Mohamed A.G., 2003. Corporate debt policy of small firms: An

empirical (re)examination. Journal of Small Business and Enterprise Development, 10(1), pp.

62-80.

18. Fama E.F., French K.R., 1998. Taxes, financing decisions, and firm value. Journal of Finance,

vol.53, pp.819-843.

19. Fama E.F., French K.R., 2002. Testing trade-off and pecking order predictions about

dividends and debt. Review of Financial Studies, 15, pp.1-33.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

18

20. Friend I., Lang H.P., 1988. An empirical test of the impact of managerial self-interest on

corporate capital structure. Journal of Finance, 43, pp. 271-281.

21. Friend I., Hasbrouck J., 1988. Determinants of capital structure. Research in Finance, 7(1),

pp. 1-19.

22. Gill A., Biger N., Mathur N., 2011. The Effect of Capital Structure on Profitability: Evidence

from the United States. International Journal of Management, 28(4), pp.3-15.

23. Gi Shian Su, Hong Tam Vo, 2010. The Relationship between Corporate Strategy, Capital

Structure and Firm Performance: An empirical Study of the Listed Companies in Vietnam.

International Research Journal of Finance and Economics, 50, pp. 62-71.

24. Gleason K.C., Mathur L.K., Mathur I., 2000. The Interrelationship between Culture, Capital

Structure and Performance: Evidence from European Retailers. Journal of Business Research,

50(2), pp. 185-191.

25. Gupta P., Srivastava A., Sharma D., 2011. Capital Structure and Economic performance:

Evidence from India, Third Annual American Business Research Conference, Adelphi

University, Long Island, New York on 6-7 June 2011.

26. Harris M., Raviv A., 1990. Capital structure and the information role of debt. Journal of

Finance, 45, pp. 321-349;

27. Harris M., Raviv A., 1991. The theory of Capital Structure. The Journal of Finance, 1, pp.

297-355.

28. Heinkel R., 1982. A theory of capital structure relevance under imperfect information. Journal

of Finance, 37, pp. 1141-1150.

29. Heinkel R., Zechner J., 1990. The role of debt and preferred stock as a solution to adverse

investment incentives. Journal of Financial and Quantitative Analysis, 25, pp. 1-24.

30. Hitt M.A., Hoskisson R.E., Harrison J.S., 1991. Strategic competitiveness in the 1990s:

Challenges and opportunities for U.S. executives. Academy of Management Executive, 5 (2),

pp.7-22.

31. Hoskisson R.E., Johnson J.R.A., Moesel D.D., 1994. Corporate divestiture intensity in

restructuring firms: effects of governance, strategy and performance. Academy of Management

Journal, 37(5), pp. 1207-1238.

32. Huang G., Song F.M., 2006. The Determinants of Capital Structure: Evidence from China.

China Economic Review, 17(1), pp. 14-36.

33. Jensen M.C., 1986. Agency cost of free cash flow, corporate finance and takeovers. American

Economic Review, 76, pp.323-329.

34. Jensen M.C. and Meckling W., 1976. Theory of the firm: Managerial behaviour, agency costs,

and ownership structure. Journal of Financial Economics, 3, pp.305-360.

35. Johnson S.A., 1997. An empirical analysis of the determinants of corporate debt ownership

structure. Journal of Financial and Quantitative Analysis, 32, pp. 47-69.

36. Jordan J., Lowe J., Taylor P., 1998. Strategy and financial policy in UK small firms. Journal

of Business Finance and Accounting, 25(1), pp. 1-27.

37. Kale J.R., Thomas H.N., Ramirez G.G., 1991. The effect of business risk on corporate capital

structure: Theory and evidence. Journal of Finance, 46, pp. 1693-1715.

38. Kester W.C., Luehrman T.A., 1992. The myth of Japan’s low-cost capital. Harvard Business

Review, 70(3), pp.130-138.

39. Kim W.S., Sorensen E.H., 1986. Evidence on the impact of the agency costs of debt on

corporate debt policy. Journal of Financial and Quantitative Analysis, 21, pp. 131.143.

40. Kim C., Mauer D.C., Sherman A.E., 1998. The determinants of corporate liquidity: Theory

and evidence. Journal of Financial and Quantitative Analysis, 33, pp. 335-359.

41. Kochhar R., 1996. Explaining firm capital structure: The role of agency theory vs. transaction

cost economics. Strategic Management Journal, 17(9), pp.713-728.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

19

42. Kochhar R., Hitt M.A., 1998. Linking corporate strategy to capital structure: Diversification

strategy, type and source of financing. Strategic Management Journal, 19(6), pp.601-610.

43. Kraus A., Litzenberger R.H., 1973. A State-Preference Model of Optimal Financial Leverage.

Journal of Finance, pp. 911-922.

44. Lane P.J., Cannella Jr.A.A., Lubatkin M.H., 1998. Agency problems as antecedents to

unrelated mergers and diversification: Amihud and lev reconsidered. Strategic Management

Journal, 19(6), pp. 555-578.

45. Leland H., Pyle D., 1977. Information asymmetrics, financial structure, and financial

intermediation. Journal of Finance, 32, pp. 371-388.

46. MacKie-Mason J.K., 1990. Do taxes effect corporate financing decisions?, Journal of

Finance, 45, pp. 1471-1493.

47. Majumdar S.K., Sen K., 2010. Debt in the Indian Corporate Sector: Its effect on firm strategy

and performance. Decision, 37(3), pp. 30-47.

48. Mesquita J.M.C., Lara J.E., 2003. Capital structure and profitability: the Brazilian case.

Academy of Business and Administration Sciences Conference, Vancouver, July 11-13.

49. Michaelas N., Chittenden F., Poutziouris P., 1999. Financial policy and capital structure

choice in IK SMEs: Empirical evidence from company panel data. Small Business Economics,

12, pp. 113-130.

50. Modigliani F., Miller M., 1958. The Cost of Capital, Corporation Finance and the Theory of

Finance, American Economic Review, 48, pp.261-297.

51. Modigliani F., Miller M., 1963. Corporate income taxes and the cost of capital: A correction.

American Economic Review, 53, pp.433-443.

52. Miller M., 1977. Debt and taxes. Journal of Finance, 32, pp. 261-276.

53. Muzir E., 2011. Triangle Relationship among Firm Size, Capital Structure Choice and

Economic performance. Some Evidence form Turkey. Journal of Management Research,

11(2), pp.87-98.

54. Myers S.C., 1977. Determinants of corporate borrowing. Journal of Financial Economics,

5(5), pp. 147-175.

55. Myers S.C., 1984. The capital structure puzzle. Journal of Finance, 39, pp. 575-592.

56. Myers S.C., 2001. Capital structure. Journal of Economic Perspectives, 15(2), pp. 81-102.

57. Myers S.C., Majluf N.S., 1984. Corporate financing and investment decision when firms have

information that investors do not have. Journal of Financial Economics, 13, pp.187-221.

58. Narayanan M.P., 1988. Debt versus equity under asymmetric information. Journal of

Financial and Quantitative Analysis, 23, pp. 39-51.

59. Nimalathasan B., Valeriu B., 2010. Capital structure and Its Impact on Profitability: A Study

of Listed Manufactoring Companies in Sri Lanka. The Young Economists Journal, 1(15), pp.

7-16.

60. Noe T., 1988. Capital structure and signalling game equilibria. Review of Financial Studies, 1,

pp. 331-356.

61. Noe T., Rebello M.J., 1996. Asymmetric information, managerial opportunism, financing, and

payout policies. Journal of Finance, 51(2), pp. 637-660.

62. Norvaisiene R., 2012. The Impact of Capital Structure on the Performance Efficiency of Baltic

Listed Companies, Inzinerine Ekonomika-Engineering Economics, 23 (5), pp. 505-516.

63. Ozkan A., 2002. The determinants of corporate debt maturity: Evidence from UK firms.

Applied Financial Economics, 12, pp. 19-24.

64. Poitevin M., 1989. Financial signalling and the “deep-pocket” argument. Rand Journal of

Economics, 20, pp. 26-40.

65. Rajan R.G., Zingales L., 1995. What do we know about capital structure: some evidence from

international data. Journal of Finance, 50, pp.1421-1460.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 3, March (2014), pp. 01-20 © IAEME

20

66. Roden D.M., Lewellen W.G., 1995. Corporate capital structure decisions: Evidence from

leveraged buyouts. Financial Management, 24, pp. 76-87.

67. Ross S., 1977. The determination of financial structure: The incentive signalling approach.

Bell Journal of Economics, 8, pp.23-40.

68. San O.T., Heng T.B., 2011. Capital Structure and Corporate Performance of Malaysian

Construction Sector. International Journal of Humanities and Social Science, 1(2), 28-36.

69. Salehi M., Manesh N.B., 2012. A Study of the Roels of Firm and Country on Specific

Determinates in Capital Structure: Iranian Evidence. International Management Review, 8 (2),

pp. 51-62.

70. Shleifer A., Vishny R.W., 1997. A survey of corporate governance. Journal of Finance, 52(2),

pp. 737-783.

71. Short H., 1994. Ownership, control, financial structure and the performance of firms. Journal

of Economic Surveys, 8(3), pp. 203-249.

72. Simerly R.L., Mingfang Li, 2000. Environmental dynamism, capital structure and

performance: a theoretical integration and an empirical test. Strategic management Journal,

21, pp. 31-49.

73. Stohs M.H., Mauer D.C., 1996. The determinants of corporate debt maturity structure. Journal

of Business, 69, pp.279-312.

74. Stulz R., 1990. Managerial discretion and optimal financing policies. Journal of Financial

Economics, 26, pp. 3-27.