DRAFT RED HERRING PROSPECTUS April 17, 2017 Please read Section 32 of the Companies Act, 2013 This Draft Red Herring Prospectus will be updated upon filing of the Red Herring Prospectus with the RoC 100% Book Built Issue CAPACIT'E INFRAPROJECTS LIMITED Our Company was originally incorporated as a private limited company at Mumbai under the name of “ Capacit'e Infraprojects Private Limited” under the Companies Act, 1956 and received a certificate of incorporation dated August 9, 2012, issued by the Registrar of Companies, Maharashtra at Mumbai. Subsequently, upon conversion from a private limited company to a public limited company, the name of our Company was changed to “Capacit'e Infraprojects Limited” and it received a fresh certificate of incorporation dated March 21, 2014 from the Registrar of Companies, Maharashtra at Mumbai. Registered and Corporate Office: 605-607, Shrikant Chambers, Phase-I, 6th Floor, Adjacent to R. K. Studios, Sion-Trombay Road, Mumbai 400 071, Maharashtra, India Telephone: +91 (22) 7173 3717; Facsimile: +91 (22) 7173 3733 For details regarding changes to the name of our Company and address of the registered office of our Company, please see “ History and Certain Corporate Matters” on page 150 of this Draft Red Herring Prospectus. Contact Person: Ms. Sai Kedar Katkar, Company Secretary and Compliance Officer Email: [email protected]; Website: www.capacite.in Corporate Identity Number: U45400MH2012PLC234318 PROMOTERS OF OUR COMPANY: MR. ROHIT R. KATYAL, MR. RAHUL R. KATYAL AND MR. SUBIR MALHOTRA INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE ` 10 EACH (“EQUITY SHARES”) OF CAPACIT'E INFRAPROJECTS LIMITED (“COMPANY” OR “ISSUER”) FOR CASH AT A PRICE OF ` [●] PER EQUITY SHARE INCLUDING A SHARE PREMIUM OF ` [●] PER EQUITY SHARE, AGGREGATING UP TO ` 4,000 MILLION, (THE “ISSUE”). THE ISSUE SHALL CONSTITUTE UP TO [●]% OF THE POST-ISSUE PAID-UP EQUITY SHARE CAPITAL OF OUR COMPANY. THE FACE VALUE OF THE EQUITY SHARES IS ` 10 EACH. THE ISSUE PRICE IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES. THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS (“BRLMs”), AND WILL BE ADVERTISED IN [●] EDITIONS OF [●], [●] EDITIONS OF [●] AND [●] EDITIONS OF [●] (WHICH ARE WIDELY CIRCULATED ENGLISH, HINDI AND MARATHI NEWSPAPERS, RESPECTIVELY, MARATHI BEING THE REGIONAL LANGUAGE OF MAHARASHTRA, WHERE OUR REGISTERED OFFICE IS LOCATED), AT LEAST FIVE WORKING DAYS PRIOR TO THE ISSUE OPENING DATE IN ACCORDANCE WITH THE SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE OF CAPITAL AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2009, AS AMENDED ( “ICDR REGULATIONS”) AND SUCH ADVERTISEMENT SHALL BE MADE AVAILABLE TO BSE LIMITED (“BSE”) AND NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”) FOR THE PURPOSE OF UPLOADING ON THEIR RESPECTIVE WEBSITES. In case of a revision in the Price Band, the Issue Period will be extended by at least three additional Working Days after revision of the Price Band, subject to the Issue Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Issue Period, if applicable, will be widely disseminated by notification to BSE and NSE, by issuing a press release and also by indicating the changes on the websites of the BRLMs and at the terminals of the Syndicate Members. In terms of Rule 19(2)(b) of the Securities Contracts Regulations Rules, 1957, as amended, read with Regulation 41 of the ICDR Regulations, the Issue is being made through the Book Building Process, in reliance on Regulation 26(1) of the ICDR Regulations, wherein not more than 50% of the Issue shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIB Portion”). Provided that our Company in consultation with the BRLMs, may allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis (“Anchor Investor Portion”). One-third of the Anchor Investor Portion shall be reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Issue shall be available for allocation on a proportionate basis to Non-Institutional Investors and not less than 35% of the Issue shall be available for allocation to Retail Individual Investors, in accordance with the ICDR Regulations, subject to valid Bids being received at or above the Issue Price. All Bidders, other than Anchor Investors, are required to mandatorily utilise the Application Supported by Blocked Amount (“ASBA”) process providing details of their respective bank accounts which will be blocked by the Self Certified Syndicate Banks (“SCSBs”), to participate in the Issue. Anchor Investors are not permitted to participate in the Issue through the ASBA process. For details, please see “Issue Procedure” on page 367 of this Draft Red Herring Prospectus. RISKS IN RELATION TO FIRST ISSUE This being the first public issue of Equity Shares of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ` 10 each. The Floor Price is [●] times the face value of the Equity Shares and the Cap Price is [●] times the face value of the Equity Shares. The Issue Price is [●] times the face value of the Equity Shares. The Issue Price (as has been determined by our Company in consultation with the BRLMs, and justified as stated in the section “Basis for Issue Price” on page 99 of this Draft Red Herring Prospectus) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding active and / or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing. GENERAL RISKS Investment in equity and equity-related securities involve a degree of risk and Bidders should not invest any funds in the Issue unless they can afford to take the risk of losing their investment. Bidders are advised to read the Risk Factors carefully before taking an investment decision in the Issue. For taking an investment decision, Bidders must rely on their own examination of our Company and the Issue, including the risks involved. The Equity Shares offered in the Issue have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of this Draft Red Herring Prospectus. Specific attention of the Bidders is invited to the section “Risk Factors” on page 17 of this Draft Red Herring Prospectus. COMPANY’S ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Issue, which is material in the context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions, misleading in any material respect. LISTING The Equity Shares, when offered through the Red Herring Prospectus, are proposed to be listed on BSE and NSE. Our Company has received “in-principle” approvals from BSE and NSE for listing of the Equity Shares pursuant to their letters dated [●] and [●], respectively. For the purposes of the Issue, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered to t he RoC for registration in accordance with the Companies Act, 2013. For details of the material contracts and documents that will be available for inspection from the date of the Red Herring Prospectus up to the Issue Closing Date, please see “Material Contracts and Documents for Inspection” on page 450 of this Draft Red Herring Prospectus. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE Axis Capital Limited 1 st Floor, Axis House C-2, Wadia International Centre, P.B. Marg Worli Mumbai 400 025 Maharashtra, India Telephone: + 91 (22) 4325 2183 Facsimile : +91 (22) 4325 3000 Email: [email protected] Investor grievance email: [email protected] Website: www.axiscapital.co.in Contact Person: Mr. Lohit Sharma SEBI registration number: INM000012029 IIFL Holdings Limited 10 th Floor, IIFL Centre Kamala City, Senapati Bapat Marg Lower Parel (West) Mumbai 400 013 Maharashtra, India Telephone: +91 (22) 4646 4600 Facsimile: +91 (22) 2493 1073 E-mail: [email protected] Investor Grievance email: [email protected] Website: www.iiflcap.com Contact Person: Mr. Sachin Kapoor/ Mr. Ankur Agarwal SEBI Registration Number: INM000010940 Vivro Financial Services Private Limited 607/608, 6th Floor, Marathon Icon Veer Santaji Lane, Off Ganpatrao Kadam Marg Opp. Peninsula Corporate Park Lower Parel, Mumbai 400 013 Maharashtra, India Telephone: +91 (22) 6666 8040/42 Facsimile: +91 (22) 6666 8047 Email: [email protected] Investor grievance email: [email protected] Website: www.vivro.net Contact Person: Mr. Harish Patel/ Mr. Yogesh Malpani SEBI Registration Number: INM000010122 Karvy Computershare Private Limited Karvy Selenium Tower B Plot 31-32, Gachibowli Financial District, Nanakramguda Hyderabad 500 032 Telangana, India Telephone: +91 (40) 6716 2222 Facsimile: +91 (40) 2343 1551 Email: [email protected] Investor Grievance e-mail: [email protected] Website: https://karisma.karvy.com/ Contact Person: Mr. M. Murali Krishna SEBI Registration No. INR000000221 ISSUE PROGRAMME * FOR ALL BIDDERS ISSUE OPENS ON: [●] ISSUE CLOSES ON (FOR QIBs) ** [●] ISSUE CLOSES ON (FOR NON-INSTITUTIONAL AND RETAIL INVESTORS) [●] *Our Company, in consultation with the BRLMs, may consider participation by Anchor Investors in accordance with the ICDR Regulations. The Anchor Investor Bidding Date shall be one Working Day prior to the Issue Opening Date i.e. [●]. ** Our Company, in consultation with the BRLMs, may decide to close the Issue Period for QIBs one Working Day prior to the Issue Closing Date i.e. [●] in accordance with the ICDR Regulations.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DRAFT RED HERRING PROSPECTUS

April 17, 2017

Please read Section 32 of the Companies Act, 2013

This Draft Red Herring Prospectus will be updated upon filing of the Red Herring Prospectus with the RoC

100% Book Built Issue

CAPACIT'E INFRAPROJECTS LIMITED

Our Company was originally incorporated as a private limited company at Mumbai under the name of “Capacit'e Infraprojects Private Limited” under the Companies Act, 1956 and received

a certificate of incorporation dated August 9, 2012, issued by the Registrar of Companies, Maharashtra at Mumbai. Subsequently, upon conversion from a private limited company to a public

limited company, the name of our Company was changed to “Capacit'e Infraprojects Limited” and it received a fresh certificate of incorporation dated March 21, 2014 from the Registrar of

Companies, Maharashtra at Mumbai.

Registered and Corporate Office: 605-607, Shrikant Chambers, Phase-I, 6th Floor, Adjacent to R. K. Studios, Sion-Trombay Road, Mumbai 400 071, Maharashtra, India

Telephone: +91 (22) 7173 3717; Facsimile: +91 (22) 7173 3733

For details regarding changes to the name of our Company and address of the registered office of our Company, please see “History and Certain Corporate Matters” on page 150 of this Draft

Red Herring Prospectus.

Contact Person: Ms. Sai Kedar Katkar, Company Secretary and Compliance Officer

Email: [email protected]; Website: www.capacite.in

Corporate Identity Number: U45400MH2012PLC234318

PROMOTERS OF OUR COMPANY: MR. ROHIT R. KATYAL, MR. RAHUL R. KATYAL AND MR. SUBIR MALHOTRA

INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE ` 10 EACH (“EQUITY SHARES”) OF CAPACIT'E INFRAPROJECTS LIMITED (“COMPANY” OR “ISSUER”) FOR

CASH AT A PRICE OF ` [●] PER EQUITY SHARE INCLUDING A SHARE PREMIUM OF ` [●] PER EQUITY SHARE, AGGREGATING UP TO ` 4,000 MILLION, (THE “ISSUE”). THE ISSUE SHALL

CONSTITUTE UP TO [●]% OF THE POST-ISSUE PAID-UP EQUITY SHARE CAPITAL OF OUR COMPANY.

THE FACE VALUE OF THE EQUITY SHARES IS ` 10 EACH. THE ISSUE PRICE IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES. THE PRICE BAND AND THE MINIMUM BID LOT

WILL BE DECIDED BY OUR COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS (“BRLMs”), AND WILL BE ADVERTISED IN [●] EDITIONS OF [●], [●] EDITIONS

OF [●] AND [●] EDITIONS OF [●] (WHICH ARE WIDELY CIRCULATED ENGLISH, HINDI AND MARATHI NEWSPAPERS, RESPECTIVELY, MARATHI BEING THE REGIONAL LANGUAGE OF

MAHARASHTRA, WHERE OUR REGISTERED OFFICE IS LOCATED), AT LEAST FIVE WORKING DAYS PRIOR TO THE ISSUE OPENING DATE IN ACCORDANCE WITH THE SECURITIES

AND EXCHANGE BOARD OF INDIA (ISSUE OF CAPITAL AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2009, AS AMENDED ( “ICDR REGULATIONS”) AND SUCH ADVERTISEMENT

SHALL BE MADE AVAILABLE TO BSE LIMITED (“BSE”) AND NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”) FOR THE PURPOSE OF UPLOADING ON THEIR RESPECTIVE

WEBSITES.

In case of a revision in the Price Band, the Issue Period will be extended by at least three additional Working Days after revision of the Price Band, subject to the Issue Period not exceeding 10 Working Days. Any revision in

the Price Band and the revised Issue Period, if applicable, will be widely disseminated by notification to BSE and NSE, by issuing a press release and also by indicating the changes on the websites of the BRLMs and at the

terminals of the Syndicate Members.

In terms of Rule 19(2)(b) of the Securities Contracts Regulations Rules, 1957, as amended, read with Regulation 41 of the ICDR Regulations, the Issue is being made through the Book Building Process, in reliance on

Regulation 26(1) of the ICDR Regulations, wherein not more than 50% of the Issue shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIB Portion”). Provided that our Company in

consultation with the BRLMs, may allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis (“Anchor Investor Portion”). One-third of the Anchor Investor Portion shall be reserved for domestic

Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for

allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocat ion on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual

Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Issue shall be available for allocation on a proportionate basis to Non-Institutional Investors and not less than 35% of

the Issue shall be available for allocation to Retail Individual Investors, in accordance with the ICDR Regulations, subject to valid Bids being received at or above the Issue Price. All Bidders, other than Anchor Investors, are

required to mandatorily utilise the Application Supported by Blocked Amount (“ASBA”) process providing details of their respective bank accounts which will be blocked by the Self Certified Syndicate Banks (“SCSBs”),

to participate in the Issue. Anchor Investors are not permitted to participate in the Issue through the ASBA process. For details, please see “Issue Procedure” on page 367 of this Draft Red Herring Prospectus.

RISKS IN RELATION TO FIRST ISSUE

This being the first public issue of Equity Shares of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ` 10 each. The Floor Price is [●] times the

face value of the Equity Shares and the Cap Price is [●] times the face value of the Equity Shares. The Issue Price is [●] times the face value of the Equity Shares. The Issue Price (as has been determined by our Company in

consultation with the BRLMs, and justified as stated in the section “Basis for Issue Price” on page 99 of this Draft Red Herring Prospectus) should not be taken to be indicative of the market price of the Equity Shares after

the Equity Shares are listed. No assurance can be given regarding active and / or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS

Investment in equity and equity-related securities involve a degree of risk and Bidders should not invest any funds in the Issue unless they can afford to take the risk of losing their investment. Bidders are advised to read the

Risk Factors carefully before taking an investment decision in the Issue. For taking an investment decision, Bidders must rely on their own examination of our Company and the Issue, including the risks involved. The

Equity Shares offered in the Issue have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of this Draft Red Herring Prospectus.

Specific attention of the Bidders is invited to the section “Risk Factors” on page 17 of this Draft Red Herring Prospectus.

COMPANY’S ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Issue, which is material in the

context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed

herein are honestly held and that there are no other facts, the omission of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions,

misleading in any material respect.

LISTING

The Equity Shares, when offered through the Red Herring Prospectus, are proposed to be listed on BSE and NSE. Our Company has received “in-principle” approvals from BSE and NSE for listing of the Equity Shares

pursuant to their letters dated [●] and [●], respectively. For the purposes of the Issue, the Designated Stock Exchange shall be [●]. A copy of the Red Herring Prospectus and the Prospectus shall be delivered to the RoC for

registration in accordance with the Companies Act, 2013. For details of the material contracts and documents that will be available for inspection from the date of the Red Herring Prospectus up to the Issue Closing Date,

please see “Material Contracts and Documents for Inspection” on page 450 of this Draft Red Herring Prospectus.

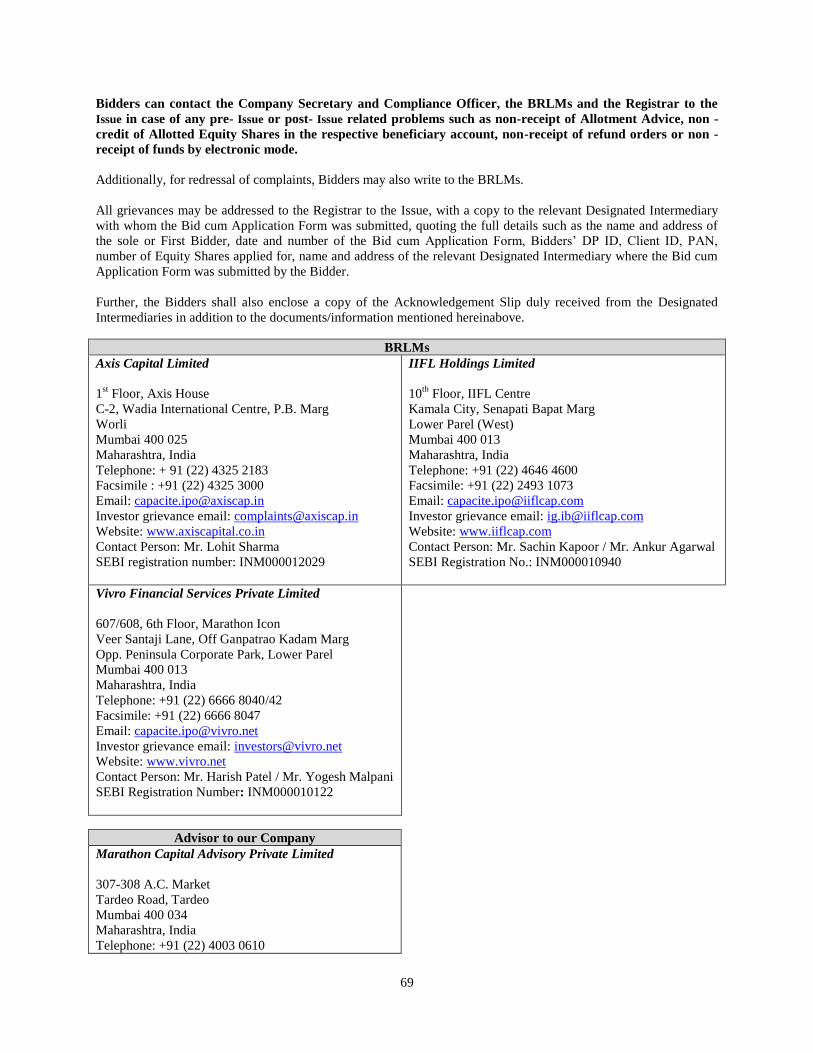

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

Axis Capital Limited

1st Floor, Axis House

C-2, Wadia International Centre, P.B. Marg

Worli

Mumbai 400 025

Maharashtra, India

Telephone: + 91 (22) 4325 2183

Facsimile : +91 (22) 4325 3000

Email: [email protected]

Investor grievance email:

Website: www.axiscapital.co.in

Contact Person: Mr. Lohit Sharma

SEBI registration number: INM000012029

IIFL Holdings Limited

10th Floor, IIFL Centre

Kamala City, Senapati Bapat Marg

Lower Parel (West)

Mumbai 400 013

Maharashtra, India

Telephone: +91 (22) 4646 4600

Facsimile: +91 (22) 2493 1073

E-mail: [email protected]

Investor Grievance email: [email protected]

Website: www.iiflcap.com

Contact Person: Mr. Sachin Kapoor/ Mr. Ankur

Agarwal

SEBI Registration Number: INM000010940

Vivro Financial Services Private Limited

607/608, 6th Floor, Marathon Icon

Veer Santaji Lane, Off Ganpatrao Kadam Marg

Opp. Peninsula Corporate Park

Lower Parel, Mumbai 400 013

Maharashtra, India

Telephone: +91 (22) 6666 8040/42

Facsimile: +91 (22) 6666 8047

Email: [email protected]

Investor grievance email: [email protected]

Website: www.vivro.net

Contact Person: Mr. Harish Patel/ Mr. Yogesh

Malpani

SEBI Registration Number: INM000010122

Karvy Computershare Private Limited

Karvy Selenium Tower B

Plot 31-32, Gachibowli

Financial District, Nanakramguda

Hyderabad 500 032

Telangana, India

Telephone: +91 (40) 6716 2222

Facsimile: +91 (40) 2343 1551

Email: [email protected]

Investor Grievance e-mail: [email protected]

Website: https://karisma.karvy.com/

Contact Person: Mr. M. Murali Krishna

SEBI Registration No. INR000000221

ISSUE PROGRAMME*

FOR ALL BIDDERS ISSUE OPENS ON: [●]

ISSUE CLOSES ON (FOR QIBs) ** [●]

ISSUE CLOSES ON (FOR NON-INSTITUTIONAL AND RETAIL

INVESTORS)

[●]

*Our Company, in consultation with the BRLMs, may consider participation by Anchor Investors in accordance with the ICDR Regulations. The Anchor Investor Bidding Date shall be one Working Day prior to the Issue

Opening Date i.e. [●].

** Our Company, in consultation with the BRLMs, may decide to close the Issue Period for QIBs one Working Day prior to the Issue Closing Date i.e. [●] in accordance with the ICDR Regulations.

TABLE OF CONTENTS

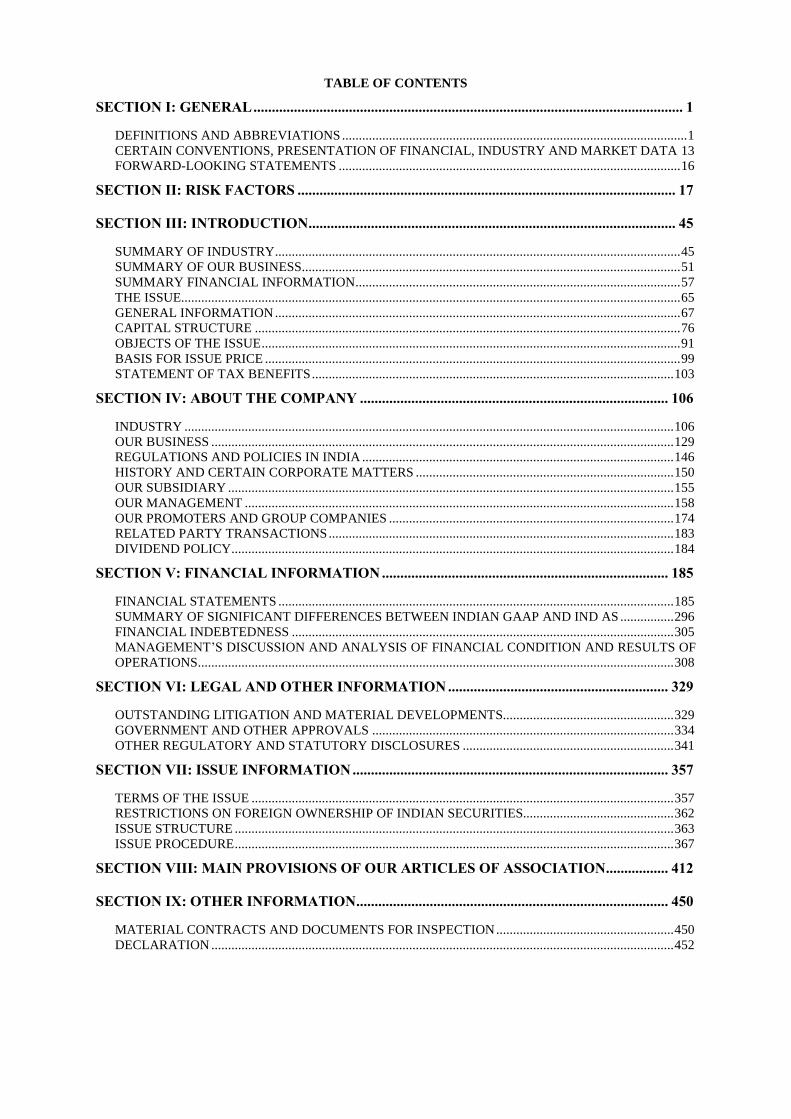

SECTION I: GENERAL ..................................................................................................................... 1

DEFINITIONS AND ABBREVIATIONS ....................................................................................................... 1 CERTAIN CONVENTIONS, PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA 13 FORWARD-LOOKING STATEMENTS ...................................................................................................... 16

SECTION II: RISK FACTORS ....................................................................................................... 17

SECTION III: INTRODUCTION .................................................................................................... 45

SUMMARY OF INDUSTRY ......................................................................................................................... 45 SUMMARY OF OUR BUSINESS................................................................................................................. 51 SUMMARY FINANCIAL INFORMATION ................................................................................................. 57 THE ISSUE..................................................................................................................................................... 65 GENERAL INFORMATION ......................................................................................................................... 67 CAPITAL STRUCTURE ............................................................................................................................... 76 OBJECTS OF THE ISSUE ............................................................................................................................. 91 BASIS FOR ISSUE PRICE ............................................................................................................................ 99 STATEMENT OF TAX BENEFITS ............................................................................................................ 103

SECTION IV: ABOUT THE COMPANY .................................................................................... 106

INDUSTRY .................................................................................................................................................. 106 OUR BUSINESS .......................................................................................................................................... 129 REGULATIONS AND POLICIES IN INDIA ............................................................................................. 146 HISTORY AND CERTAIN CORPORATE MATTERS ............................................................................. 150 OUR SUBSIDIARY ..................................................................................................................................... 155 OUR MANAGEMENT ................................................................................................................................ 158 OUR PROMOTERS AND GROUP COMPANIES ..................................................................................... 174 RELATED PARTY TRANSACTIONS ....................................................................................................... 183 DIVIDEND POLICY.................................................................................................................................... 184

SECTION V: FINANCIAL INFORMATION .............................................................................. 185

FINANCIAL STATEMENTS ...................................................................................................................... 185 SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND IND AS ................ 296 FINANCIAL INDEBTEDNESS .................................................................................................................. 305 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.............................................................................................................................................. 308

SECTION VI: LEGAL AND OTHER INFORMATION ............................................................ 329

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS................................................... 329 GOVERNMENT AND OTHER APPROVALS .......................................................................................... 334 OTHER REGULATORY AND STATUTORY DISCLOSURES ............................................................... 341

SECTION VII: ISSUE INFORMATION ...................................................................................... 357

TERMS OF THE ISSUE .............................................................................................................................. 357 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES............................................. 362 ISSUE STRUCTURE ................................................................................................................................... 363 ISSUE PROCEDURE ................................................................................................................................... 367

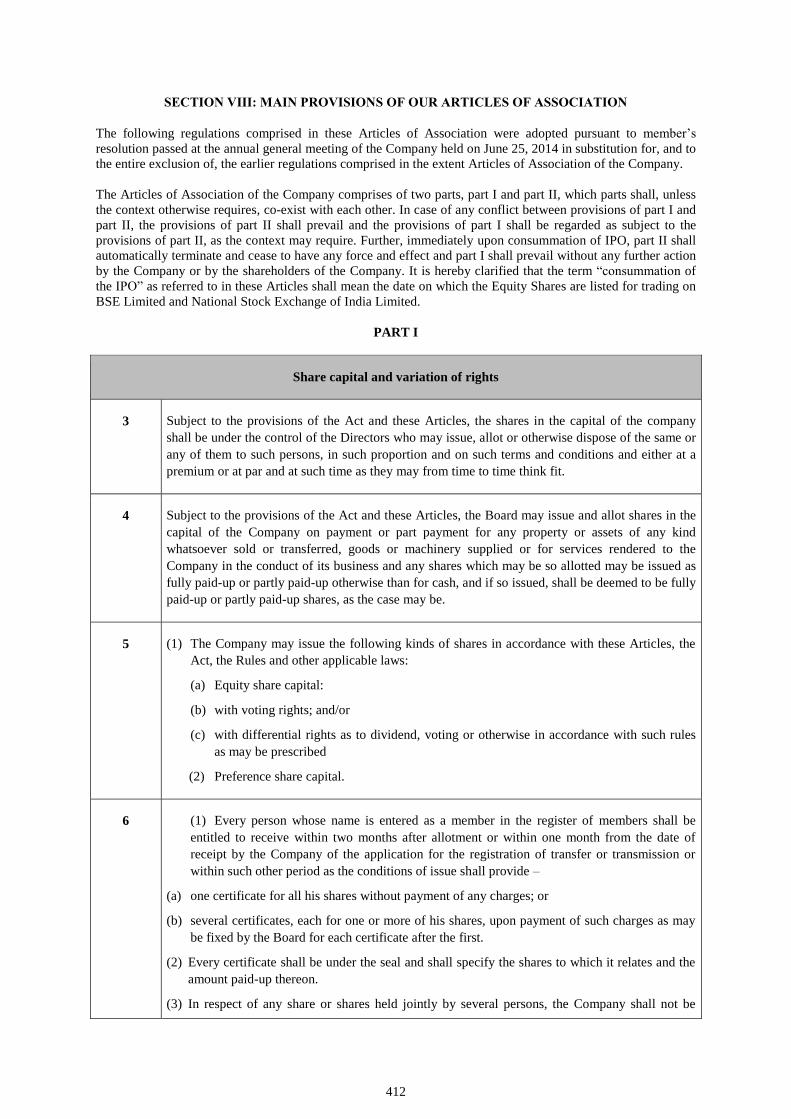

SECTION VIII: MAIN PROVISIONS OF OUR ARTICLES OF ASSOCIATION ................. 412

SECTION IX: OTHER INFORMATION ..................................................................................... 450

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ..................................................... 450 DECLARATION .......................................................................................................................................... 452

1

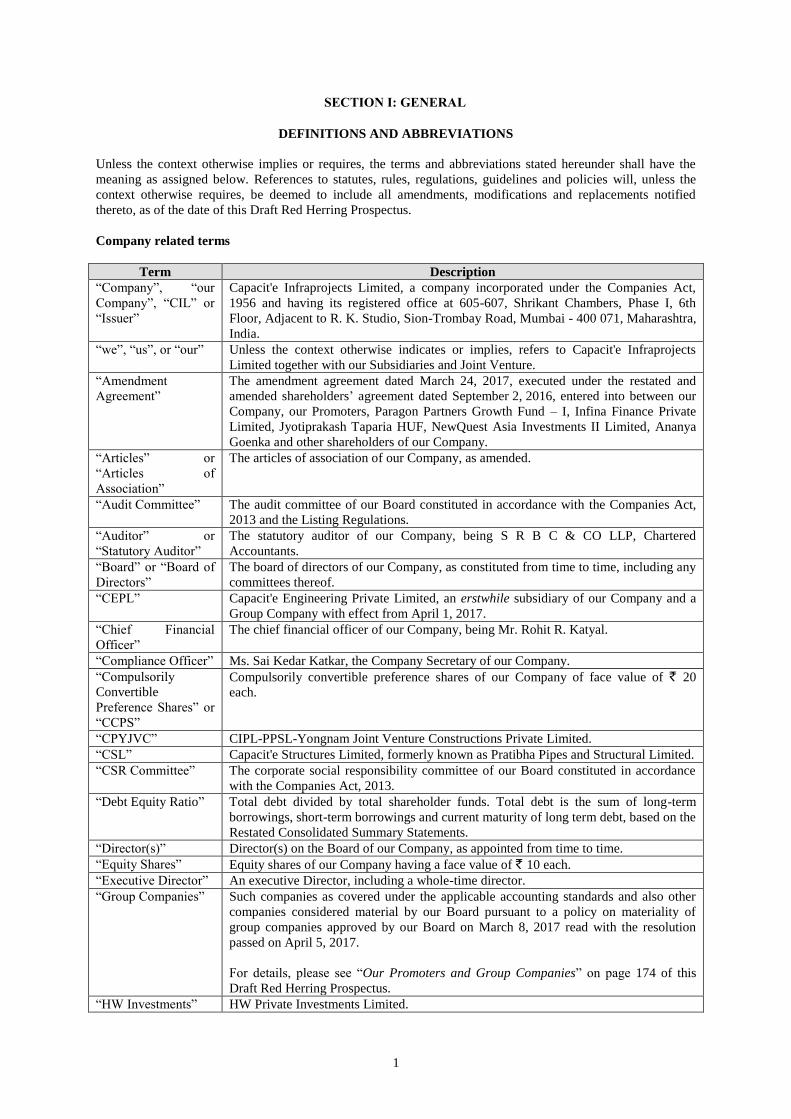

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

Unless the context otherwise implies or requires, the terms and abbreviations stated hereunder shall have the

meaning as assigned below. References to statutes, rules, regulations, guidelines and policies will, unless the

context otherwise requires, be deemed to include all amendments, modifications and replacements notified

thereto, as of the date of this Draft Red Herring Prospectus.

Company related terms

Term Description

“Company”, “our

Company”, “CIL” or

“Issuer”

Capacit'e Infraprojects Limited, a company incorporated under the Companies Act,

1956 and having its registered office at 605-607, Shrikant Chambers, Phase I, 6th

Floor, Adjacent to R. K. Studio, Sion-Trombay Road, Mumbai - 400 071, Maharashtra,

India.

“we”, “us”, or “our” Unless the context otherwise indicates or implies, refers to Capacit'e Infraprojects

Limited together with our Subsidiaries and Joint Venture.

“Amendment

Agreement”

The amendment agreement dated March 24, 2017, executed under the restated and

amended shareholders’ agreement dated September 2, 2016, entered into between our

Company, our Promoters, Paragon Partners Growth Fund – I, Infina Finance Private

Limited, Jyotiprakash Taparia HUF, NewQuest Asia Investments II Limited, Ananya

Goenka and other shareholders of our Company.

“Articles” or

“Articles of

Association”

The articles of association of our Company, as amended.

“Audit Committee” The audit committee of our Board constituted in accordance with the Companies Act,

2013 and the Listing Regulations.

“Auditor” or

“Statutory Auditor”

The statutory auditor of our Company, being S R B C & CO LLP, Chartered

Accountants.

“Board” or “Board of

Directors”

The board of directors of our Company, as constituted from time to time, including any

committees thereof.

“CEPL” Capacit'e Engineering Private Limited, an erstwhile subsidiary of our Company and a

Group Company with effect from April 1, 2017.

“Chief Financial

Officer”

The chief financial officer of our Company, being Mr. Rohit R. Katyal.

“Compliance Officer” Ms. Sai Kedar Katkar, the Company Secretary of our Company.

“Compulsorily

Convertible

Preference Shares” or

“CCPS”

Compulsorily convertible preference shares of our Company of face value of ` 20

each.

“CPYJVC” CIPL-PPSL-Yongnam Joint Venture Constructions Private Limited.

“CSL” Capacit'e Structures Limited, formerly known as Pratibha Pipes and Structural Limited.

“CSR Committee” The corporate social responsibility committee of our Board constituted in accordance

with the Companies Act, 2013.

“Debt Equity Ratio” Total debt divided by total shareholder funds. Total debt is the sum of long-term

borrowings, short-term borrowings and current maturity of long term debt, based on the

Restated Consolidated Summary Statements.

“Director(s)” Director(s) on the Board of our Company, as appointed from time to time.

“Equity Shares” Equity shares of our Company having a face value of ` 10 each.

“Executive Director” An executive Director, including a whole-time director.

“Group Companies” Such companies as covered under the applicable accounting standards and also other

companies considered material by our Board pursuant to a policy on materiality of

group companies approved by our Board on March 8, 2017 read with the resolution

passed on April 5, 2017.

For details, please see “Our Promoters and Group Companies” on page 174 of this

Draft Red Herring Prospectus.

“HW Investments” HW Private Investments Limited.

2

Term Description

“Independent

Director”

A non-executive, independent Director as per the Companies Act, 2013 and the Listing

Regulations.

“Infina” Infina Finance Private Limited.

“IPO Committee” The committee of our Board constituted pursuant to a Board resolution dated March 8,

2017.

“JM Financial” JM Financial Products Limited.

“JT HUF” Jyotiprakash Taparia HUF.

“Joint Venture” PPSL-Capacit'e JV.

“KMP” or “Key

Management

Personnel”

Key management personnel of our Company in terms of the ICDR Regulations and as

disclosed in “Our Management” on page 158 of this Draft Red Herring Prospectus.

“Memorandum” or

“Memorandum of

Association”

The memorandum of association of our Company, as amended.

“Nomination and

Remuneration

Committee”

The nomination and remuneration committee of our Board constituted in accordance

with the Companies Act, 2013 and the Listing Regulations.

“NewQuest” NewQuest Asia Investments II Limited.

“Non-Executive

Director”

A Director not being an Executive Director or an Independent Director.

“Paragon” Paragon Partners Growth Fund – I.

“Promoter Group” Such persons and entities which constitute the promoter group of our Company

pursuant to Regulation 2 (1)(zb) of the ICDR Regulations.

“Promoters” The promoters of our Company, namely, Mr. Rohit R. Katyal, Mr. Rahul R. Katyal and

Mr. Subir Malhotra. For details, please see “Our Promoters and Group Companies” on

page 174 of this Draft Red Herring Prospectus.

“Registered and

Corporate Office”

The registered and corporate office of our Company situated at 605-607, Shrikant

Chambers, Phase I, 6th Floor, Adjacent to R.K. Studio, Sion-Trombay Road, Mumbai -

400 071, Maharashtra, India.

“Registrar of

Companies” or

“RoC”

Registrar of Companies, Maharashtra located at Mumbai.

“Restated

Consolidated

Summary

Statements”

The consolidated financial information of our Company, its Subsidiaries and Joint

Venture as at and for the nine months period ended December 31, 2016 and as of and

for the financial years ended March 31, 2016, 2015 and 2014 and as at and for the

period August 9, 2012 to March 31, 2013, and the related notes, schedules and

annexures thereto included in this Draft Red Herring Prospectus, which have been

prepared in accordance with the requirements of the Companies Act, 2013 and Indian

GAAP and restated in accordance with the ICDR Regulations.

“Restated Financial

Information”

Restated Consolidated Summary Statements and Restated Standalone Summary

Statements collectively.

“Restated Standalone

Summary

Statements”

The standalone financial information of our Company as at and for the nine months

period ended December 31, 2016 and as of and for the financial years ended March 31,

2016, 2015, 2014 and as at and for the period August 9, 2012 to March 31, 2013, and

the related notes, schedules and annexures thereto included in this Draft Red Herring

Prospectus, which have been prepared in accordance with the requirements of the

Companies Act, 2013 and Indian GAAP, and restated in accordance with the ICDR

Regulations.

“Series A CCPSs” 1,007,366 CCPSs with a coupon of 0.0001% issued at an issue price of ` 625.39 per

CCPS pursuant to a subscription agreement and a shareholders’ agreement both dated

August 6, 2015 respectively.

“Series A CCPS

Holder”

Paragon.

“Series B CCPSs” 649,322 CCPSs with a coupon of 0.0001% issued at an issue price of ` 924.04 per

CCPS pursuant to a subscription agreement and the restated and amended

shareholders’ agreements both dated September 2, 2016, which were subsequently

amended by way of addendum agreements dated September 2, 2016 and October 14,

2016, respectively.

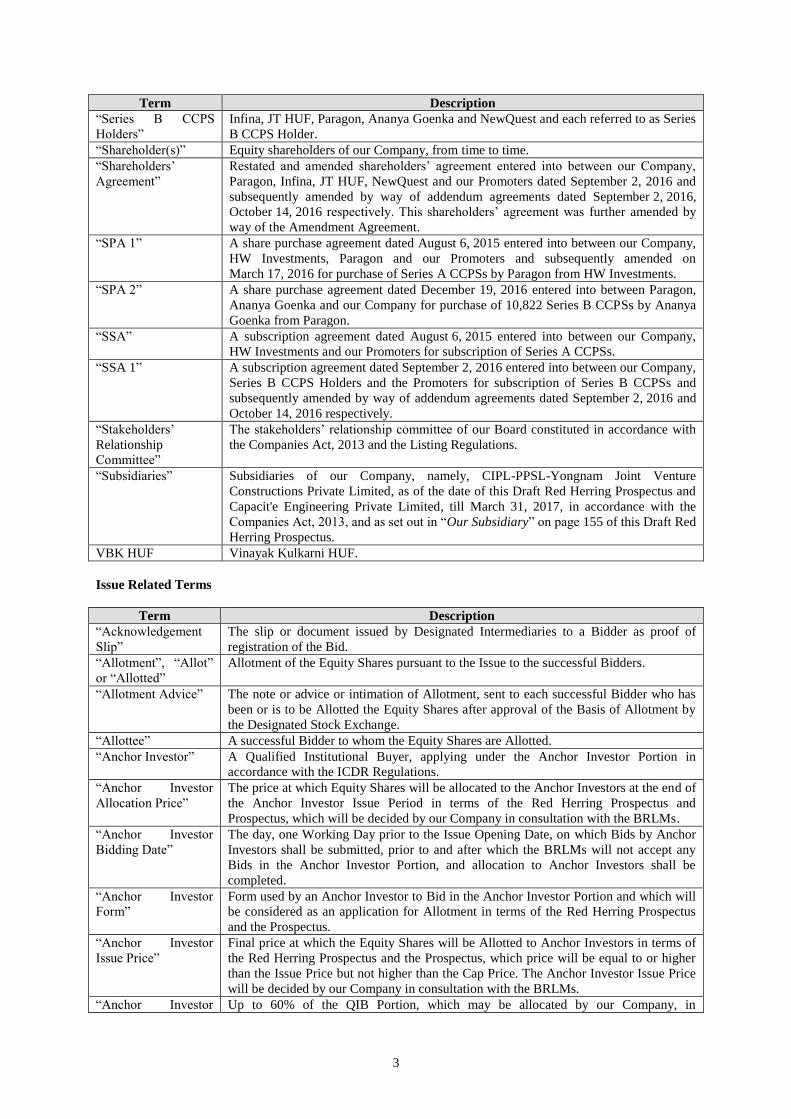

3

Term Description

“Series B CCPS

Holders”

Infina, JT HUF, Paragon, Ananya Goenka and NewQuest and each referred to as Series

B CCPS Holder.

“Shareholder(s)” Equity shareholders of our Company, from time to time.

“Shareholders’

Agreement”

Restated and amended shareholders’ agreement entered into between our Company,

Paragon, Infina, JT HUF, NewQuest and our Promoters dated September 2, 2016 and

subsequently amended by way of addendum agreements dated September 2, 2016,

October 14, 2016 respectively. This shareholders’ agreement was further amended by

way of the Amendment Agreement.

“SPA 1” A share purchase agreement dated August 6, 2015 entered into between our Company,

HW Investments, Paragon and our Promoters and subsequently amended on

March 17, 2016 for purchase of Series A CCPSs by Paragon from HW Investments.

“SPA 2” A share purchase agreement dated December 19, 2016 entered into between Paragon,

Ananya Goenka and our Company for purchase of 10,822 Series B CCPSs by Ananya

Goenka from Paragon.

“SSA” A subscription agreement dated August 6, 2015 entered into between our Company,

HW Investments and our Promoters for subscription of Series A CCPSs.

“SSA 1” A subscription agreement dated September 2, 2016 entered into between our Company,

Series B CCPS Holders and the Promoters for subscription of Series B CCPSs and

subsequently amended by way of addendum agreements dated September 2, 2016 and

October 14, 2016 respectively.

“Stakeholders’

Relationship

Committee”

The stakeholders’ relationship committee of our Board constituted in accordance with

the Companies Act, 2013 and the Listing Regulations.

“Subsidiaries” Subsidiaries of our Company, namely, CIPL-PPSL-Yongnam Joint Venture

Constructions Private Limited, as of the date of this Draft Red Herring Prospectus and

Capacit'e Engineering Private Limited, till March 31, 2017, in accordance with the

Companies Act, 2013, and as set out in “Our Subsidiary” on page 155 of this Draft Red

Herring Prospectus.

VBK HUF Vinayak Kulkarni HUF.

Issue Related Terms

Term Description

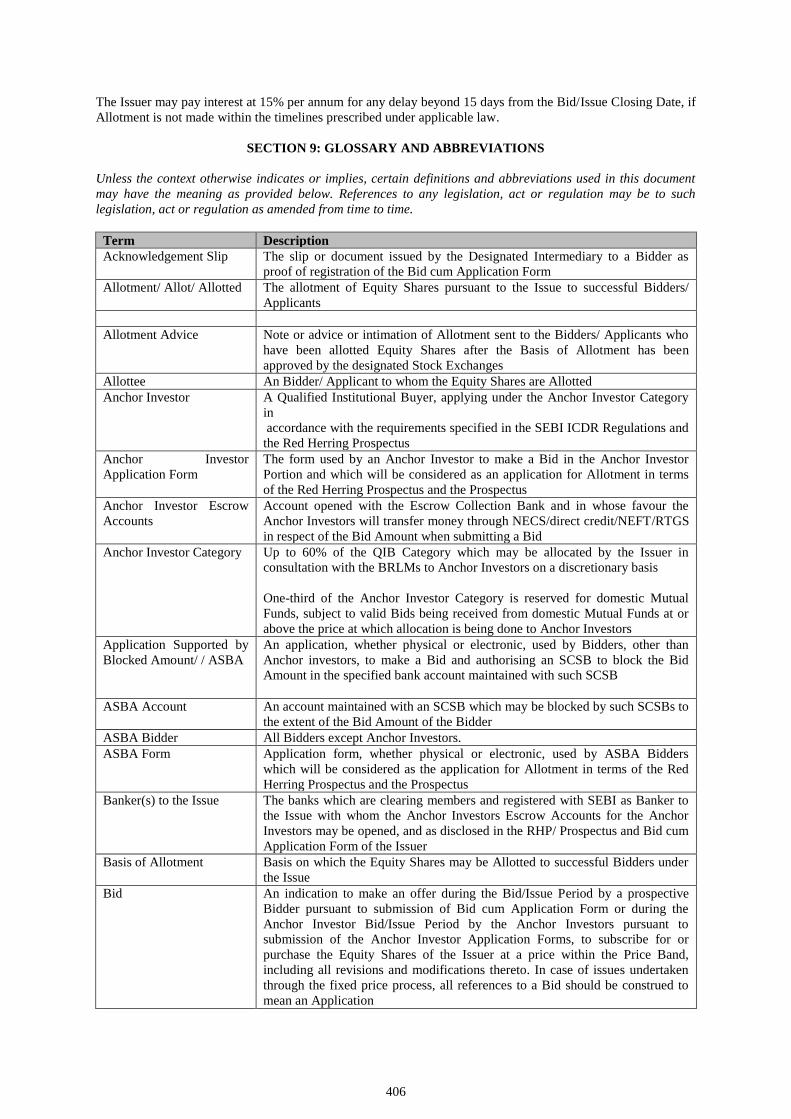

“Acknowledgement

Slip”

The slip or document issued by Designated Intermediaries to a Bidder as proof of

registration of the Bid.

“Allotment”, “Allot”

or “Allotted”

Allotment of the Equity Shares pursuant to the Issue to the successful Bidders.

“Allotment Advice” The note or advice or intimation of Allotment, sent to each successful Bidder who has

been or is to be Allotted the Equity Shares after approval of the Basis of Allotment by

the Designated Stock Exchange.

“Allottee” A successful Bidder to whom the Equity Shares are Allotted.

“Anchor Investor” A Qualified Institutional Buyer, applying under the Anchor Investor Portion in

accordance with the ICDR Regulations.

“Anchor Investor

Allocation Price”

The price at which Equity Shares will be allocated to the Anchor Investors at the end of

the Anchor Investor Issue Period in terms of the Red Herring Prospectus and

Prospectus, which will be decided by our Company in consultation with the BRLMs.

“Anchor Investor

Bidding Date”

The day, one Working Day prior to the Issue Opening Date, on which Bids by Anchor

Investors shall be submitted, prior to and after which the BRLMs will not accept any

Bids in the Anchor Investor Portion, and allocation to Anchor Investors shall be

completed.

“Anchor Investor

Form”

Form used by an Anchor Investor to Bid in the Anchor Investor Portion and which will

be considered as an application for Allotment in terms of the Red Herring Prospectus

and the Prospectus.

“Anchor Investor

Issue Price”

Final price at which the Equity Shares will be Allotted to Anchor Investors in terms of

the Red Herring Prospectus and the Prospectus, which price will be equal to or higher

than the Issue Price but not higher than the Cap Price. The Anchor Investor Issue Price

will be decided by our Company in consultation with the BRLMs.

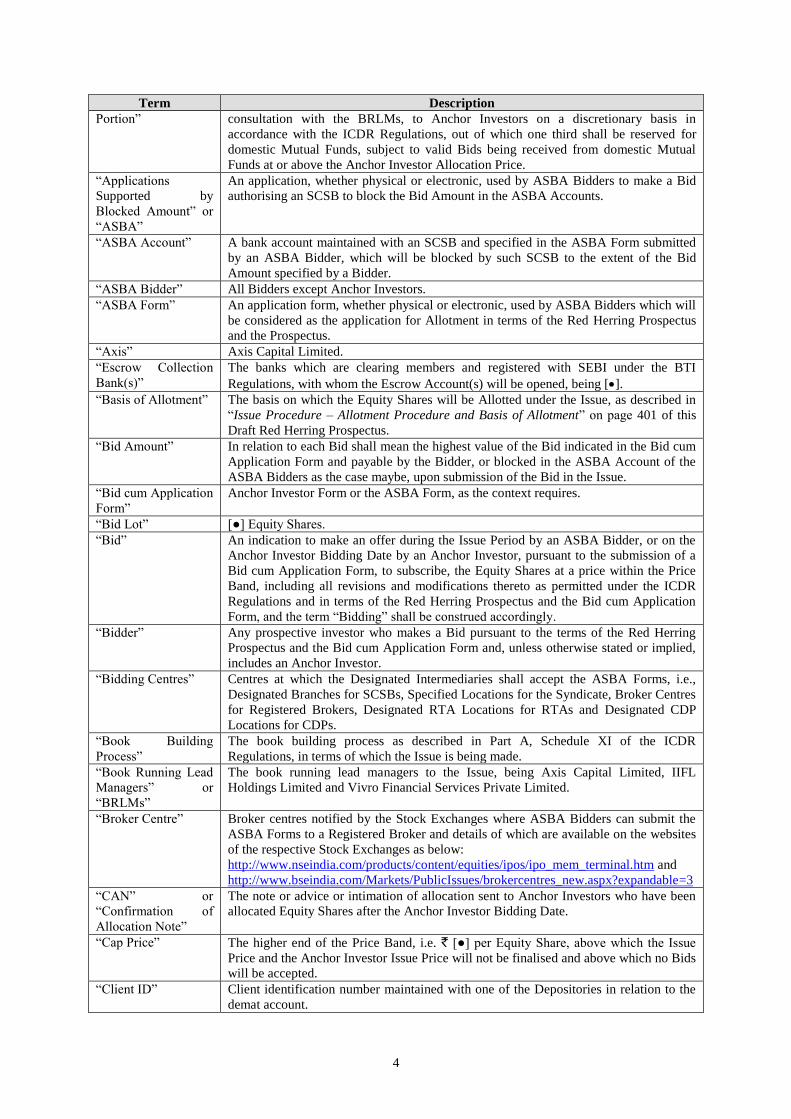

“Anchor Investor Up to 60% of the QIB Portion, which may be allocated by our Company, in

4

Term Description

Portion” consultation with the BRLMs, to Anchor Investors on a discretionary basis in

accordance with the ICDR Regulations, out of which one third shall be reserved for

domestic Mutual Funds, subject to valid Bids being received from domestic Mutual

Funds at or above the Anchor Investor Allocation Price.

“Applications

Supported by

Blocked Amount” or

“ASBA”

An application, whether physical or electronic, used by ASBA Bidders to make a Bid

authorising an SCSB to block the Bid Amount in the ASBA Accounts.

“ASBA Account” A bank account maintained with an SCSB and specified in the ASBA Form submitted

by an ASBA Bidder, which will be blocked by such SCSB to the extent of the Bid

Amount specified by a Bidder.

“ASBA Bidder” All Bidders except Anchor Investors.

“ASBA Form” An application form, whether physical or electronic, used by ASBA Bidders which will

be considered as the application for Allotment in terms of the Red Herring Prospectus

and the Prospectus.

“Axis” Axis Capital Limited.

“Escrow Collection

Bank(s)”

The banks which are clearing members and registered with SEBI under the BTI

Regulations, with whom the Escrow Account(s) will be opened, being [].

“Basis of Allotment” The basis on which the Equity Shares will be Allotted under the Issue, as described in

“Issue Procedure – Allotment Procedure and Basis of Allotment” on page 401 of this

Draft Red Herring Prospectus.

“Bid Amount” In relation to each Bid shall mean the highest value of the Bid indicated in the Bid cum

Application Form and payable by the Bidder, or blocked in the ASBA Account of the

ASBA Bidders as the case maybe, upon submission of the Bid in the Issue.

“Bid cum Application

Form”

Anchor Investor Form or the ASBA Form, as the context requires.

“Bid Lot” [●] Equity Shares.

“Bid” An indication to make an offer during the Issue Period by an ASBA Bidder, or on the

Anchor Investor Bidding Date by an Anchor Investor, pursuant to the submission of a

Bid cum Application Form, to subscribe, the Equity Shares at a price within the Price

Band, including all revisions and modifications thereto as permitted under the ICDR

Regulations and in terms of the Red Herring Prospectus and the Bid cum Application

Form, and the term “Bidding” shall be construed accordingly.

“Bidder” Any prospective investor who makes a Bid pursuant to the terms of the Red Herring

Prospectus and the Bid cum Application Form and, unless otherwise stated or implied,

includes an Anchor Investor.

“Bidding Centres” Centres at which the Designated Intermediaries shall accept the ASBA Forms, i.e.,

Designated Branches for SCSBs, Specified Locations for the Syndicate, Broker Centres

for Registered Brokers, Designated RTA Locations for RTAs and Designated CDP

Locations for CDPs.

“Book Building

Process”

The book building process as described in Part A, Schedule XI of the ICDR

Regulations, in terms of which the Issue is being made.

“Book Running Lead

Managers” or

“BRLMs”

The book running lead managers to the Issue, being Axis Capital Limited, IIFL

Holdings Limited and Vivro Financial Services Private Limited.

“Broker Centre” Broker centres notified by the Stock Exchanges where ASBA Bidders can submit the

ASBA Forms to a Registered Broker and details of which are available on the websites

of the respective Stock Exchanges as below:

http://www.nseindia.com/products/content/equities/ipos/ipo_mem_terminal.htm and

http://www.bseindia.com/Markets/PublicIssues/brokercentres_new.aspx?expandable=3

“CAN” or

“Confirmation of

Allocation Note”

The note or advice or intimation of allocation sent to Anchor Investors who have been

allocated Equity Shares after the Anchor Investor Bidding Date.

“Cap Price” The higher end of the Price Band, i.e. ` [●] per Equity Share, above which the Issue

Price and the Anchor Investor Issue Price will not be finalised and above which no Bids

will be accepted.

“Client ID” Client identification number maintained with one of the Depositories in relation to the

demat account.

5

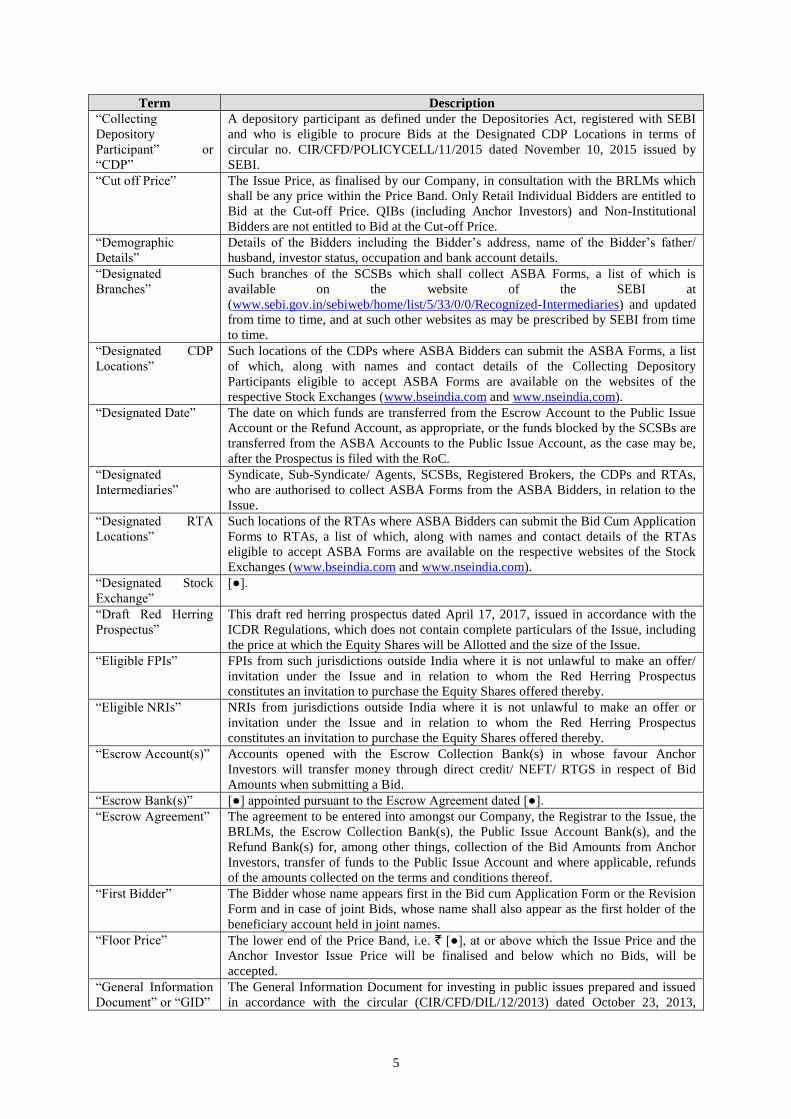

Term Description

“Collecting

Depository

Participant” or

“CDP”

A depository participant as defined under the Depositories Act, registered with SEBI

and who is eligible to procure Bids at the Designated CDP Locations in terms of

circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by

SEBI.

“Cut off Price” The Issue Price, as finalised by our Company, in consultation with the BRLMs which

shall be any price within the Price Band. Only Retail Individual Bidders are entitled to

Bid at the Cut-off Price. QIBs (including Anchor Investors) and Non-Institutional

Bidders are not entitled to Bid at the Cut-off Price.

“Demographic

Details”

Details of the Bidders including the Bidder’s address, name of the Bidder’s father/

husband, investor status, occupation and bank account details.

“Designated

Branches”

Such branches of the SCSBs which shall collect ASBA Forms, a list of which is

available on the website of the SEBI at

(www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognized-Intermediaries) and updated

from time to time, and at such other websites as may be prescribed by SEBI from time

to time.

“Designated CDP

Locations”

Such locations of the CDPs where ASBA Bidders can submit the ASBA Forms, a list

of which, along with names and contact details of the Collecting Depository

Participants eligible to accept ASBA Forms are available on the websites of the

respective Stock Exchanges (www.bseindia.com and www.nseindia.com).

“Designated Date” The date on which funds are transferred from the Escrow Account to the Public Issue

Account or the Refund Account, as appropriate, or the funds blocked by the SCSBs are

transferred from the ASBA Accounts to the Public Issue Account, as the case may be,

after the Prospectus is filed with the RoC.

“Designated

Intermediaries”

Syndicate, Sub-Syndicate/ Agents, SCSBs, Registered Brokers, the CDPs and RTAs,

who are authorised to collect ASBA Forms from the ASBA Bidders, in relation to the

Issue.

“Designated RTA

Locations”

Such locations of the RTAs where ASBA Bidders can submit the Bid Cum Application

Forms to RTAs, a list of which, along with names and contact details of the RTAs

eligible to accept ASBA Forms are available on the respective websites of the Stock

Exchanges (www.bseindia.com and www.nseindia.com).

“Designated Stock

Exchange”

[●].

“Draft Red Herring

Prospectus”

This draft red herring prospectus dated April 17, 2017, issued in accordance with the

ICDR Regulations, which does not contain complete particulars of the Issue, including

the price at which the Equity Shares will be Allotted and the size of the Issue.

“Eligible FPIs” FPIs from such jurisdictions outside India where it is not unlawful to make an offer/

invitation under the Issue and in relation to whom the Red Herring Prospectus

constitutes an invitation to purchase the Equity Shares offered thereby.

“Eligible NRIs” NRIs from jurisdictions outside India where it is not unlawful to make an offer or

invitation under the Issue and in relation to whom the Red Herring Prospectus

constitutes an invitation to purchase the Equity Shares offered thereby.

“Escrow Account(s)” Accounts opened with the Escrow Collection Bank(s) in whose favour Anchor

Investors will transfer money through direct credit/ NEFT/ RTGS in respect of Bid

Amounts when submitting a Bid.

“Escrow Bank(s)” [●] appointed pursuant to the Escrow Agreement dated [●].

“Escrow Agreement” The agreement to be entered into amongst our Company, the Registrar to the Issue, the

BRLMs, the Escrow Collection Bank(s), the Public Issue Account Bank(s), and the

Refund Bank(s) for, among other things, collection of the Bid Amounts from Anchor

Investors, transfer of funds to the Public Issue Account and where applicable, refunds

of the amounts collected on the terms and conditions thereof.

“First Bidder” The Bidder whose name appears first in the Bid cum Application Form or the Revision

Form and in case of joint Bids, whose name shall also appear as the first holder of the

beneficiary account held in joint names.

“Floor Price” The lower end of the Price Band, i.e. ` [●], at or above which the Issue Price and the

Anchor Investor Issue Price will be finalised and below which no Bids, will be

accepted.

“General Information

Document” or “GID”

The General Information Document for investing in public issues prepared and issued

in accordance with the circular (CIR/CFD/DIL/12/2013) dated October 23, 2013,

6

Term Description

notified by SEBI, suitably modified and included in “Issue Procedure” on page 367 of

this Draft Red Herring Prospectus.

“IIFL” IIFL Holdings Limited.

“Issue” Initial public offering of [●] Equity Shares for cash at a price of ₹ [●] per Equity Share

(including a share premium of ₹ [●] per Equity Share) aggregating up to ₹ 4,000

million.

“Issue Agreement” The agreement dated April 17, 2017 amongst our Company and the BRLMs, pursuant

to the ICDR Regulations, based on which certain arrangements are agreed to in relation

to the Issue.

“Issue Closing Date” Except in relation to Bids received from the Anchor Investors, [●], the date after which

the Designated Intermediaries will not accept any Bids, which shall also be notified in

[●] editions of [●], [●] editions of [●] and [●] editions of [●] (which are widely

circulated English, Hindi and Marathi newspapers, respectively, Marathi being the

regional language of Maharashtra, where our Registered Office is located).

Our Company in consultation with the BRLMs, may consider closing the Issue Period

for QIBs one Working Day prior to the Issue Closing Date in accordance with the

ICDR Regulations.

“Issue Opening Date” Except in relation to Bids received from the Anchor Investors, [●], the date on which

the Designated Intermediaries shall start accepting Bids for the Issue, which shall also

be notified in [●] editions of [●], [●] editions of [●] and [●] editions of [●] (which are

widely circulated English, Hindi and Marathi newspapers, respectively, Marathi being

the regional language of Maharashtra, where our Registered Office is located).

“Issue Period” Except in relation to Bids received from the Anchor Investors, the period from and

including the Issue Opening Date to and including the Issue Closing Date during which

ASBA Bidders can submit their Bids, including any revisions thereto. The Issue Period

will comprise of Working Days only.

“Issue Price” The final price at which the Equity Shares will be Allotted to successful Bidders other

than Anchor Investors in terms of the Red Herring Prospectus. The Issue Price will be

decided by our Company in consultation with the BRLMs, in accordance with the Book

Building Process on the Pricing Date.

“Issue Proceeds” The proceeds of the Issue that is available to our Company

“Mutual Fund

Portion”

5% of the QIB Portion (other than Anchor Investor Portion) available for allocation to

Mutual Funds only, on a proportionate basis, subject to valid Bids being received at or

above the Issue Price.

“Net Proceeds” Issue Proceeds less the Issue-related expenses. For further details about use of the Net

Proceeds and the Issue expenses, see “Objects of the Issue” on page 91 of this Draft

Red Herring Prospectus.

“Non-Institutional

Investors”

All Bidders, including Category III FPIs, that are not QIBs or Retail Individual

Investors who have Bid for Equity Shares for an amount of more than ` 200,000 (but

not including NRIs other than Eligible NRIs).

“Non-Institutional

Portion”

The portion of the Issue being not less than 15% of the Issue available for allocation to

Non-Institutional Investors on a proportionate basis, subject to valid Bids being

received at or above the Issue Price.

“Price Band” Any price between and including the Floor Price and the Cap Price and includes

revisions thereof.

The Price Band and the minimum Bid Lot for the Issue will be decided by our

Company in consultation with the BRLMs and will be advertised in [●] editions of [●],

[●] editions of [●] and [●] editions of [●] (which are widely circulated English, Hindi

and Marathi newspapers, respectively, Marathi being the regional language of

Maharashtra, where our Registered Office is located), at least five Working Days prior

to the Issue Opening Date.

“Pricing Date” The date on which our Company in consultation with the BRLMs, will finalise the

Issue Price.

“Prospectus” The prospectus to be filed with the RoC in accordance with the Companies Act, 2013

and the ICDR Regulations containing, inter-alia, the Issue Price that is determined at

7

Term Description

the end of the Book Building Process, the size of the Issue and certain other

information, including any addenda or corrigenda thereto.

“Public Issue

Account Bank(s)”

The banks which are clearing members and registered with SEBI under the BTI

Regulations, with whom the Public Issue Account(s) will be opened, being [●].

“Public Issue

Account(s)”

An account opened in accordance with the provisions of the Companies Act, 2013, with

the Public Issue Account Bank(s) to receive money from the Escrow Accounts and

from the ASBA Accounts on the Designated Date.

“QIB Portion” The portion of the Issue (including the Anchor Investor Portion) being not more than

50% of the Issue which shall be allocated to QIBs, including the Anchor Investors

(which allocation shall be on a discretionary basis, as determined by our Company in

consultation with the BRLMs) subject to valid Bids being received at or above the Issue

Price.

“Qualified

Institutional Buyers”

or “QIBs”

A qualified institutional buyer, as defined under Regulation 2(1)(zd) of the ICDR

Regulations.

“Red Herring

Prospectus”

The red herring prospectus that will be issued in accordance with the Companies Act,

2013, and the ICDR Regulations, which will not have complete particulars of the price

at which the Equity Shares will be offered and the size of the Issue, including any

addenda or corrigenda thereto.

“Refund Account(s)” The account opened with the Refund Bank(s), from which refunds to unsuccessful

Anchor Investors, if any, of the whole or part of the Bid Amount shall be made.

“Refund Bank(s)” The banks which are clearing members and registered with SEBI under the BTI

Regulations with whom the Refund Account(s) will be opened and in this case being

[●].

“Registered Broker” Stock brokers registered with the stock exchanges having nationwide terminals other

than the Syndicate, and eligible to procure Bids from ASBA Bidders in terms of the

circular No. CIR/CFD/14/2012 dated October 4, 2012 issued by SEBI.

“Registrar and Share

Transfer Agents” or

“RTAs”

Registrar and share transfer agents registered with SEBI and eligible to procure Bids

from ASBA Bidders at the Designated RTA Locations in terms of circular no.

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI.

“Registrar” or

“Registrar to the

Issue”

Karvy Computershare Private Limited.

“Resident Indian” A person resident in India, as defined under FEMA.

“Retail Individual

Investors”/ “RII(s)”

Individual Bidders (including HUFs applying through their karta and Eligible NRIs)

who have not submitted a Bid for Equity Shares for a Bid Amount of more than `

200,000 in any of the Bidding options in the Issue.

“Retail Portion” The portion of the Issue being not less than 35% of the Issue available for allocation to

Retail Individual Investor(s) in accordance with the ICDR Regulations, subject to valid

Bids being received at or above the Issue Price.

“Revision Form” The form used by the Bidders to modify the quantity of Equity Shares or the Bid

Amount in their Bid cum Application Forms or any prior Revision Form(s), as

applicable. QIBs and Non-Institutional Investors are not allowed to withdraw or lower

their Bids (in terms of quantity of Equity Shares or the Bid Amount) at any stage. RIIs

can revise their Bids during the Issue Period and withdraw their Bids until Issue

Closing Date.

“Self Certified

Syndicate Bank(s)”

or “SCSB(s)”

Banks which are registered with SEBI under the BTI Regulations, which offer the

facility of ASBA, a list of which is available on the website of the SEBI at

(www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries) and updated

from time to time and at such other websites as may be prescribed by SEBI from time

to time.

“Specified Cities” or

“Specified

Locations”

Bidding centres where the Syndicate shall accept ASBA Forms from ASBA Bidders, a

list of which is available on the website of the SEBI

(http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries) and

updated from time to time and at such other websites as may be prescribed by SEBI

from time to time.

“Stock Exchange(s)” BSE and NSE.

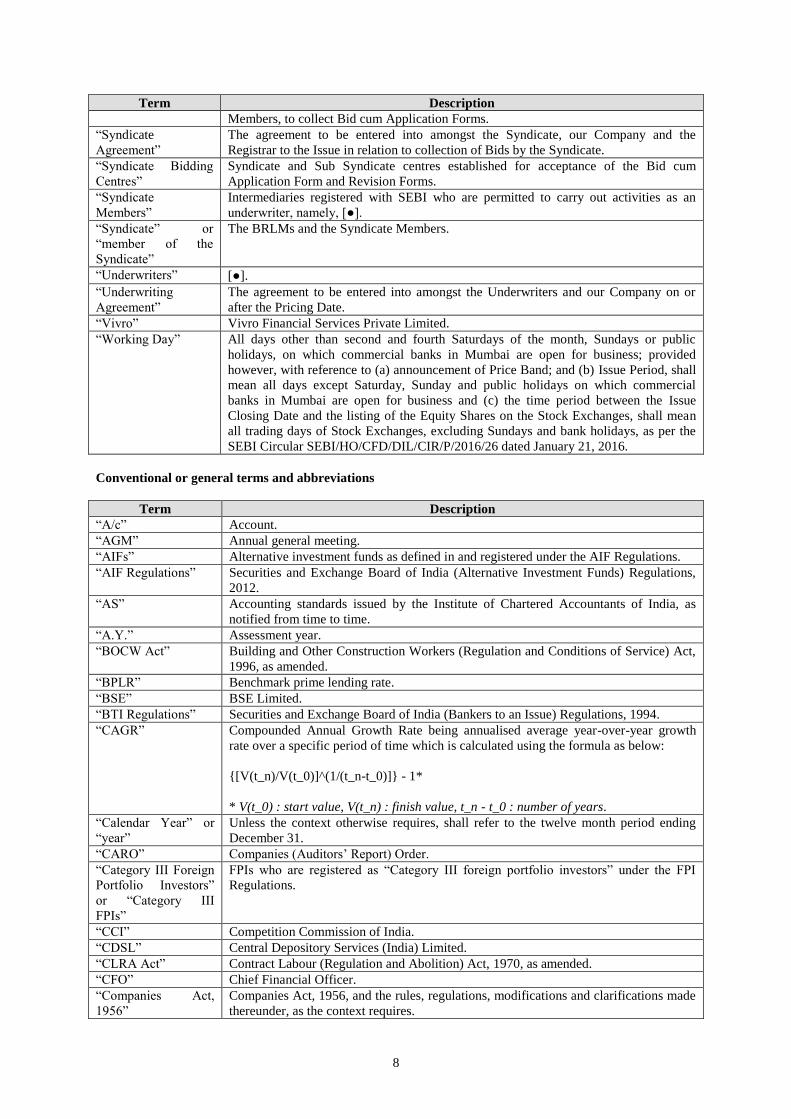

“Sub Syndicate” The sub-syndicate members, if any, appointed by the BRLMs and the Syndicate

8

Term Description

Members, to collect Bid cum Application Forms.

“Syndicate

Agreement”

The agreement to be entered into amongst the Syndicate, our Company and the

Registrar to the Issue in relation to collection of Bids by the Syndicate.

“Syndicate Bidding

Centres”

Syndicate and Sub Syndicate centres established for acceptance of the Bid cum

Application Form and Revision Forms.

“Syndicate

Members”

Intermediaries registered with SEBI who are permitted to carry out activities as an

underwriter, namely, [●].

“Syndicate” or

“member of the

Syndicate”

The BRLMs and the Syndicate Members.

“Underwriters” [●].

“Underwriting

Agreement”

The agreement to be entered into amongst the Underwriters and our Company on or

after the Pricing Date.

“Vivro” Vivro Financial Services Private Limited.

“Working Day” All days other than second and fourth Saturdays of the month, Sundays or public

holidays, on which commercial banks in Mumbai are open for business; provided

however, with reference to (a) announcement of Price Band; and (b) Issue Period, shall

mean all days except Saturday, Sunday and public holidays on which commercial

banks in Mumbai are open for business and (c) the time period between the Issue

Closing Date and the listing of the Equity Shares on the Stock Exchanges, shall mean

all trading days of Stock Exchanges, excluding Sundays and bank holidays, as per the

SEBI Circular SEBI/HO/CFD/DIL/CIR/P/2016/26 dated January 21, 2016.

Conventional or general terms and abbreviations

Term Description

“A/c” Account.

“AGM” Annual general meeting.

“AIFs” Alternative investment funds as defined in and registered under the AIF Regulations.

“AIF Regulations” Securities and Exchange Board of India (Alternative Investment Funds) Regulations,

2012.

“AS” Accounting standards issued by the Institute of Chartered Accountants of India, as

notified from time to time.

“A.Y.” Assessment year.

“BOCW Act” Building and Other Construction Workers (Regulation and Conditions of Service) Act,

1996, as amended.

“BPLR” Benchmark prime lending rate.

“BSE” BSE Limited.

“BTI Regulations” Securities and Exchange Board of India (Bankers to an Issue) Regulations, 1994.

“CAGR” Compounded Annual Growth Rate being annualised average year-over-year growth

rate over a specific period of time which is calculated using the formula as below:

{[V(t_n)/V(t_0)]^(1/(t_n-t_0)]} - 1*

* V(t_0) : start value, V(t_n) : finish value, t_n - t_0 : number of years.

“Calendar Year” or

“year”

Unless the context otherwise requires, shall refer to the twelve month period ending

December 31.

“CARO” Companies (Auditors’ Report) Order.

“Category III Foreign

Portfolio Investors”

or “Category III

FPIs”

FPIs who are registered as “Category III foreign portfolio investors” under the FPI

Regulations.

“CCI” Competition Commission of India.

“CDSL” Central Depository Services (India) Limited.

“CLRA Act” Contract Labour (Regulation and Abolition) Act, 1970, as amended.

“CFO” Chief Financial Officer.

“Companies Act,

1956”

Companies Act, 1956, and the rules, regulations, modifications and clarifications made

thereunder, as the context requires.

9

Term Description

“Companies Act,

2013”

Companies Act, 2013 and the rules, regulations, modifications and clarifications

thereunder, to the extent notified.

“Companies Act” Companies Act, 1956 to the extent not repealed, and/ or the Companies Act, 2013.

“Competition Act” Competition Act, 2002.

“CRISIL” CRISIL Research, a division of CRISIL Limited.

“CSR” Corporate social responsibility.

“Depositories Act” Depositories Act, 1996.

“Depository” or

“Depositories”

NSDL and CDSL.

“DIN” Director Identification Number.

“DP” or “Depository

Participant”

A depository participant as defined under the Depositories Act.

“DP ID” Depository Participant’s Identification Number.

“EBITDA” Earnings before interest, tax, depreciation and amortisation. For further details please

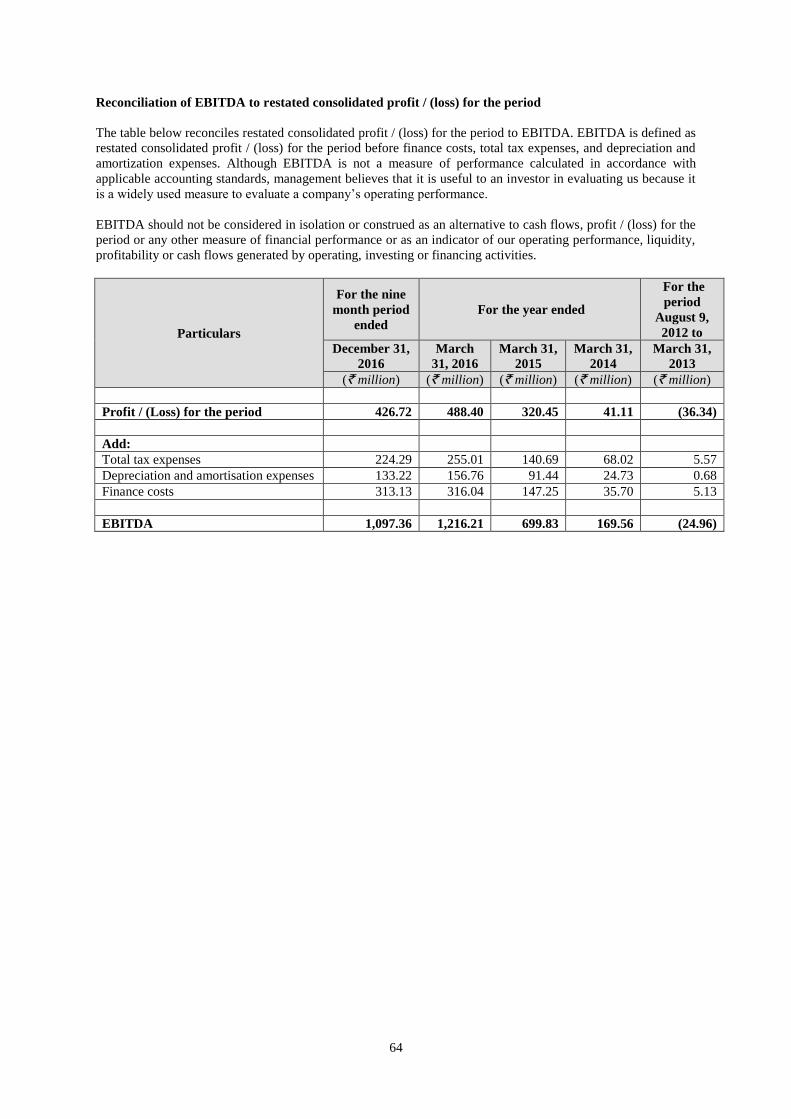

see “Summary Financial Information - Reconciliation of EBITDA to restated

consolidated profit / (loss) for the period” on page 64 of this Draft Red Herring

Prospectus.

“EGM” Extraordinary general meeting.

“EPS” Earnings per share (as calculated in accordance with AS-20).

“ERP” Enterprise Resource Planning.

“FDI” Foreign direct investment.

“FEMA” Foreign Exchange Management Act, 1999, including the rules and regulations

thereunder.

“FEMA Regulations” Foreign Exchange Management (Transfer or Issue of Security by a Person Resident

Outside India) Regulations, 2000.

“Financial Year”,

“Fiscal”, “FY” or

“F.Y.”

Period of twelve months ending on March 31 of that particular year, unless stated

otherwise, except for the period ended March 31, 2013 (being from August 9, 2012 to

March 31, 2013)

“FII(s)” Foreign Institutional Investor, as defined under the erstwhile Securities and Exchange

Board of India (Foreign Institutional Investors) Regulations, 1995.

“FII Regulations” Erstwhile Securities and Exchange Board of India (Foreign Institutional Investors)

Regulations, 1995.

“FPI(s)” Foreign Portfolio Investor, as defined under the FPI Regulations, including FIIs and

qualified foreign investors, which are deemed to be foreign portfolio investors.

“FPI Regulations” Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations,

2014.

“Finance Act” Finance Act, 1994.

“FIPB” Foreign Investment Promotion Board.

“FVCI” Foreign venture capital investors, as defined and registered with SEBI under the FVCI

Regulations.

“FVCI Regulations” Securities and Exchange Board of India (Foreign Venture Capital Investor)

Regulations, 2000.

“GDP” Gross domestic product.

“GIR Number” General index registration number.

“GoI” Government of India.

“GST” Goods and services tax.

“HUF” Hindu undivided family.

“ICAI” The Institute of Chartered Accountants of India.

“ICDS” Income Computation and Disclosure Standards.

“IFRS” International Financial Reporting Standards.

“Ind AS” Indian Accounting Standards.

“I.T. Act” The Income Tax Act, 1961.

“IT” Information technology.

“ICDR Regulations” Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009.

“Indian GAAP” Accounting principles generally accepted in India.

“Insider Trading Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations,

10

Term Description

Regulations” 2015.

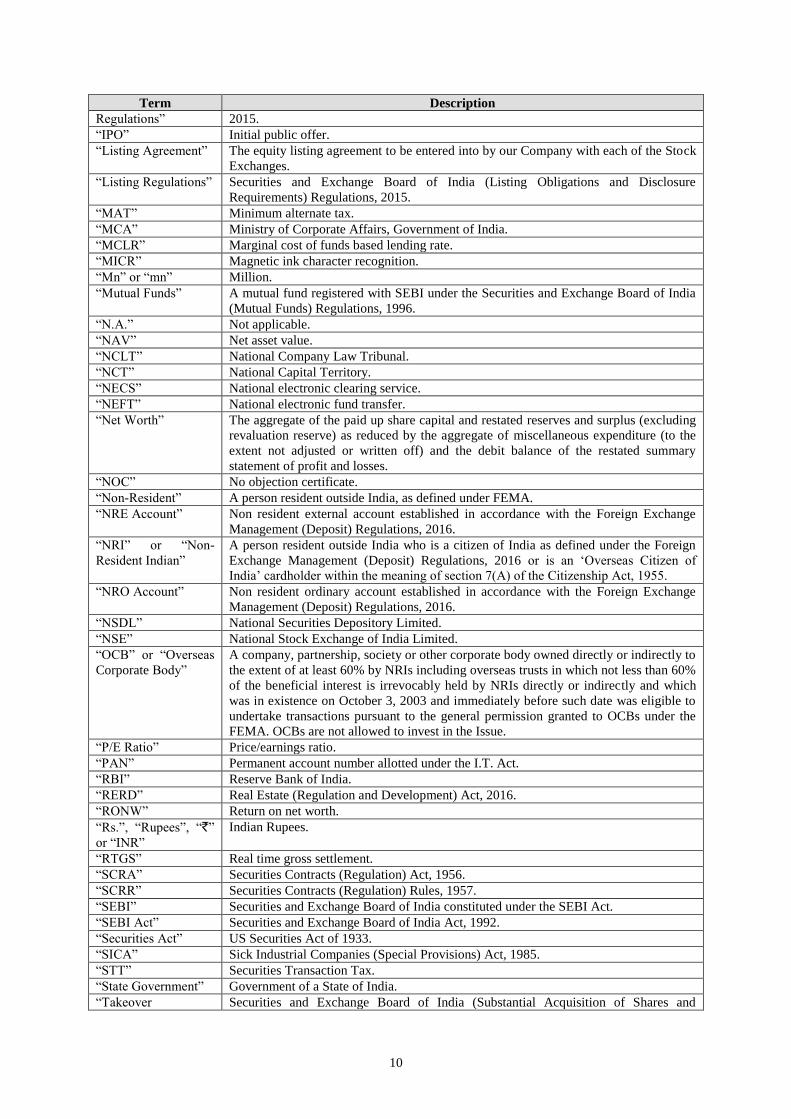

“IPO” Initial public offer.

“Listing Agreement” The equity listing agreement to be entered into by our Company with each of the Stock

Exchanges.

“Listing Regulations” Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015.

“MAT” Minimum alternate tax.

“MCA” Ministry of Corporate Affairs, Government of India.

“MCLR” Marginal cost of funds based lending rate.

“MICR” Magnetic ink character recognition.

“Mn” or “mn” Million.

“Mutual Funds” A mutual fund registered with SEBI under the Securities and Exchange Board of India

(Mutual Funds) Regulations, 1996.

“N.A.” Not applicable.

“NAV” Net asset value.

“NCLT” National Company Law Tribunal.

“NCT” National Capital Territory.

“NECS” National electronic clearing service.

“NEFT” National electronic fund transfer.

“Net Worth” The aggregate of the paid up share capital and restated reserves and surplus (excluding

revaluation reserve) as reduced by the aggregate of miscellaneous expenditure (to the

extent not adjusted or written off) and the debit balance of the restated summary

statement of profit and losses.

“NOC” No objection certificate.

“Non-Resident” A person resident outside India, as defined under FEMA.

“NRE Account” Non resident external account established in accordance with the Foreign Exchange

Management (Deposit) Regulations, 2016.

“NRI” or “Non-

Resident Indian”

A person resident outside India who is a citizen of India as defined under the Foreign

Exchange Management (Deposit) Regulations, 2016 or is an ‘Overseas Citizen of

India’ cardholder within the meaning of section 7(A) of the Citizenship Act, 1955.

“NRO Account” Non resident ordinary account established in accordance with the Foreign Exchange

Management (Deposit) Regulations, 2016.

“NSDL” National Securities Depository Limited.

“NSE” National Stock Exchange of India Limited.

“OCB” or “Overseas

Corporate Body”

A company, partnership, society or other corporate body owned directly or indirectly to

the extent of at least 60% by NRIs including overseas trusts in which not less than 60%

of the beneficial interest is irrevocably held by NRIs directly or indirectly and which

was in existence on October 3, 2003 and immediately before such date was eligible to

undertake transactions pursuant to the general permission granted to OCBs under the

FEMA. OCBs are not allowed to invest in the Issue.

“P/E Ratio” Price/earnings ratio.

“PAN” Permanent account number allotted under the I.T. Act.

“RBI” Reserve Bank of India.

“RERD” Real Estate (Regulation and Development) Act, 2016.

“RONW” Return on net worth.

“Rs.”, “Rupees”, “`”

or “INR”

Indian Rupees.

“RTGS” Real time gross settlement.

“SCRA” Securities Contracts (Regulation) Act, 1956.

“SCRR” Securities Contracts (Regulation) Rules, 1957.

“SEBI” Securities and Exchange Board of India constituted under the SEBI Act.

“SEBI Act” Securities and Exchange Board of India Act, 1992.

“Securities Act” US Securities Act of 1933.

“SICA” Sick Industrial Companies (Special Provisions) Act, 1985.

“STT” Securities Transaction Tax.

“State Government” Government of a State of India.

“Takeover Securities and Exchange Board of India (Substantial Acquisition of Shares and

11

Term Description

Regulations” Takeovers) Regulations, 2011, as amended.

“U.S.A” The United States of America.

“VAT” Value added tax.

“VCFs” Venture capital funds as defined in, and registered with SEBI under, the VCF

Regulations.

“VCF Regulations” The erstwhile Securities and Exchange Board of India (Venture Capital Fund)

Regulations, 1996.

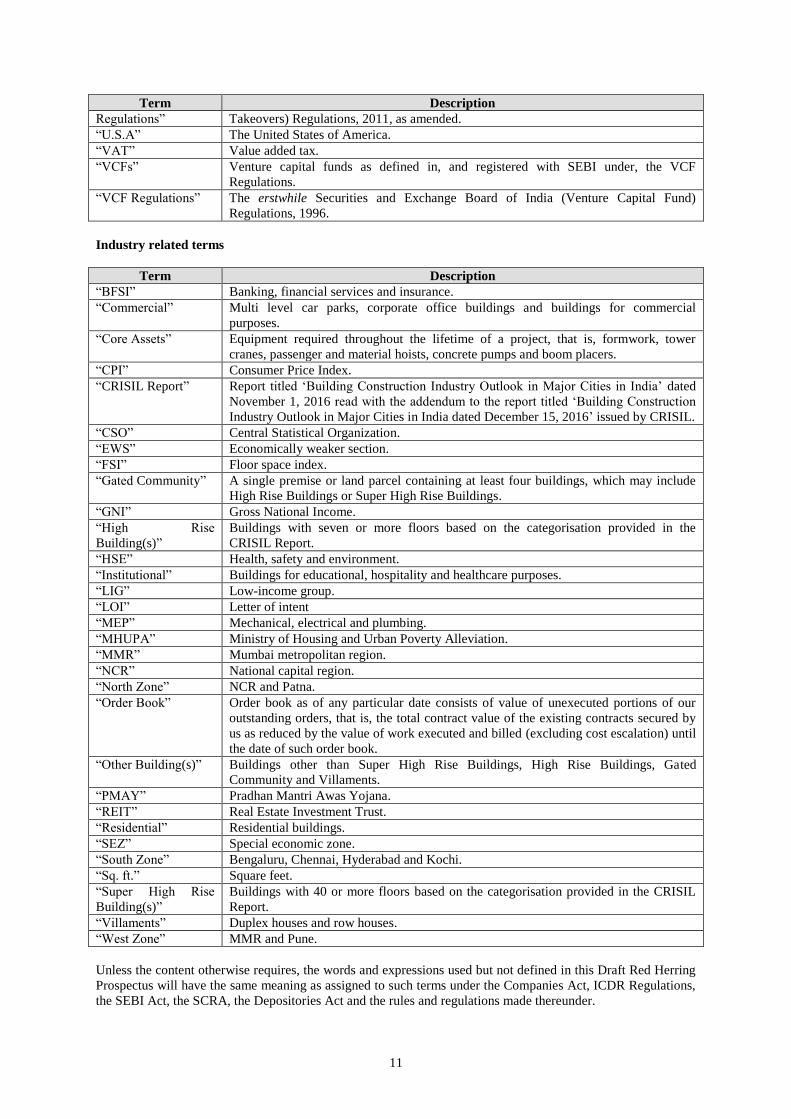

Industry related terms

Term Description

“BFSI” Banking, financial services and insurance.

“Commercial” Multi level car parks, corporate office buildings and buildings for commercial

purposes.

“Core Assets” Equipment required throughout the lifetime of a project, that is, formwork, tower

cranes, passenger and material hoists, concrete pumps and boom placers.

“CPI” Consumer Price Index.

“CRISIL Report” Report titled ‘Building Construction Industry Outlook in Major Cities in India’ dated

November 1, 2016 read with the addendum to the report titled ‘Building Construction

Industry Outlook in Major Cities in India dated December 15, 2016’ issued by CRISIL.

“CSO” Central Statistical Organization.

“EWS” Economically weaker section.

“FSI” Floor space index.

“Gated Community” A single premise or land parcel containing at least four buildings, which may include

High Rise Buildings or Super High Rise Buildings.

“GNI” Gross National Income.

“High Rise

Building(s)”

Buildings with seven or more floors based on the categorisation provided in the

CRISIL Report.

“HSE” Health, safety and environment.

“Institutional” Buildings for educational, hospitality and healthcare purposes.

“LIG” Low-income group.

“LOI” Letter of intent

“MEP” Mechanical, electrical and plumbing.

“MHUPA” Ministry of Housing and Urban Poverty Alleviation.

“MMR” Mumbai metropolitan region.

“NCR” National capital region.

“North Zone” NCR and Patna.

“Order Book” Order book as of any particular date consists of value of unexecuted portions of our

outstanding orders, that is, the total contract value of the existing contracts secured by

us as reduced by the value of work executed and billed (excluding cost escalation) until

the date of such order book.

“Other Building(s)” Buildings other than Super High Rise Buildings, High Rise Buildings, Gated

Community and Villaments.

“PMAY” Pradhan Mantri Awas Yojana.

“REIT” Real Estate Investment Trust.

“Residential” Residential buildings.

“SEZ” Special economic zone.

“South Zone” Bengaluru, Chennai, Hyderabad and Kochi.

“Sq. ft.” Square feet.

“Super High Rise

Building(s)”

Buildings with 40 or more floors based on the categorisation provided in the CRISIL

Report.

“Villaments” Duplex houses and row houses.

“West Zone” MMR and Pune.

Unless the content otherwise requires, the words and expressions used but not defined in this Draft Red Herring

Prospectus will have the same meaning as assigned to such terms under the Companies Act, ICDR Regulations,

the SEBI Act, the SCRA, the Depositories Act and the rules and regulations made thereunder.

12

Notwithstanding the foregoing, terms specifically defined in this Draft Red Herring Prospectus, including

“Statement of Tax Benefits” and “Financial Statements” on pages 103 and 185 of this Draft Red Herring

Prospectus, respectively, shall have the meanings given to such terms in the sections.

13

CERTAIN CONVENTIONS, PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

All references to “India” contained in this Draft Red Herring Prospectus are to the Republic of India.

Unless stated otherwise, all references to page numbers in this Draft Red Herring Prospectus are to the page

numbers of this Draft Red Herring Prospectus.

Financial Data

Unless the context requires otherwise, the financial data in this Draft Red Herring Prospectus is derived from

our Restated Financial Information. Our Restated Financial Information has been prepared in accordance with

the Companies Act, 2013 and Indian GAAP and restated in accordance with the ICDR Regulations. The audited

standalone and consolidated financial statements of our Company as of and for the nine month period ended

December 31, 2016 and for the financial years ended March 31, 2016, 2015, 2014 and 2013 (as of and for the

period August 9, 2012 to March 31, 2013), respectively, have been approved by our Board and adopted by our

Shareholders.

Our Company’s Financial Year commences on April 1 and ends on March 31 of the following year accordingly,

all references to a particular financial year, except for the period ended March 31, 2013 (being from the date of

incorporation of our Company i.e. from August 9, 2012 to March 31, 2013) unless stated otherwise, are to the

12 month period ended on March 31 of that year. Unless the context otherwise requires, all references to a year

in this Draft Red Herring Prospectus are to a calendar year and references to a Fiscal Year are to March 31 of

that calendar year.

Certain figures contained in this Draft Red Herring Prospectus, including financial information, have been

subject to rounding adjustments. All decimals have been rounded off to two decimal places. In certain instances,

(i) the sum or percentage change of such numbers may not conform exactly to the total figure given; and (ii) the

sum of the numbers in a column or row in certain tables may not conform exactly to the total figure given for

that column or row.

There are significant differences between Indian GAAP and accounting principles and auditing standards with

which prospective investors may be familiar in other countries, including IFRS and U.S. GAAP. We have not

attempted to explain those differences or quantify their impact on the financial data included herein, and we

urge you to consult your own advisors regarding such differences and their impact on our financial data.

Accordingly, the degree to which the Restated Financial Information included in this Draft Red Herring

Prospectus will provide meaningful information is entirely dependent on the reader’s level of familiarity with

Indian accounting practices. Any reliance by persons not familiar with Indian accounting practices on the

financial disclosures presented in this Draft Red Herring Prospectus should accordingly be limited. Our

Company does not provide a reconciliation of its financial statements to IFRS or U.S. GAAP financial

statements.

Further, with effect from April 1, 2017, we will be required to prepare our financial statements in accordance

with Ind AS. Given that Ind AS is different in many respects from Indian GAAP under which our financial

statements are currently prepared, our financial statements for the period commencing from April 1, 2017 may

not be comparable to our historical financial statements including the financial statements included in this Draft

Red Herring Prospectus. For details in connection with risks involving differences between Indian GAAP and

other accounting principles and accounting standards and risks in relation to Ind AS, please see “Risk Factors –

Risk factor 54 - Companies in India (based on notified thresholds), including our Company, will be required to

prepare financial statements under Ind-AS (which is India's convergence to IFRS). The transition to Ind-AS in

India is very recent and there is no clarity on the impact of such transition on our Company. All income tax

assessments in India will also be required to follow the Income Computation Disclosure Standards” on page 38

of this Draft Red Herring Prospectus. For further details, please see “Summary of significant differences between

Indian GAAP and Ind AS” on page 296 of this Draft Red Herring Prospectus.

Any percentage amounts, as set forth in “Risk Factors”, “Our Business” and “Management’s Discussion and

Analysis of Financial Condition and Results of Operations” on pages 17, 129 and 308 of this Draft Red Herring

Prospectus, respectively, and elsewhere in this Draft Red Herring Prospectus, unless otherwise stated or context

requires otherwise, have been calculated on the basis of our Restated Financial Information.

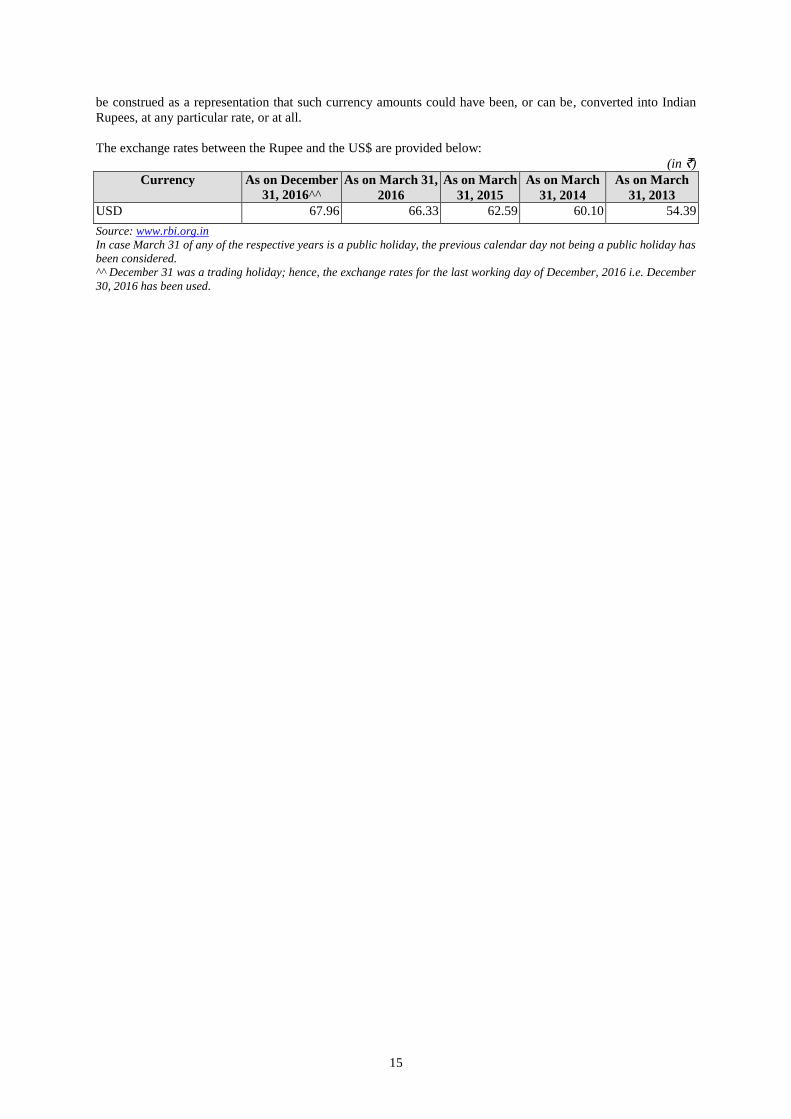

Currency and units of presentation

14

All references to “Rupees” or “Rs.” or “`” or “INR” are to Indian Rupees, the official currency of the Republic

of India.

Except where specified in this Draft Red Herring Prospectus, our Company has presented the numerical

information in “million” and “billion” units. The words “lakh” or “lac” mean “100,000”, and the word “million”

means “10 lakh”, and the word “crore” means “10 million” or “100 lakh” and the word “billion” means “1,000

million” or “100 crore”.

Industry and Market Data

Unless stated otherwise, industry data used throughout this Draft Red Herring Prospectus has been obtained or

derived from publicly available information as well as industry publications and sources.

Industry publications generally state that the information contained in those publications has been obtained from

sources believed to be reliable but that their accuracy and completeness are not guaranteed and their reliability

cannot be assured. Although we believe that the industry data used in this Draft Red Herring Prospectus is

reliable, it has not been independently verified by our Company, the BRLMs or any of their affiliates or

advisors. The data used in these sources may have been reclassified by us for the purposes of presentation. Data

from these sources may also not be comparable.

Information has been included in this Draft Red Herring Prospectus from the report titled “Building