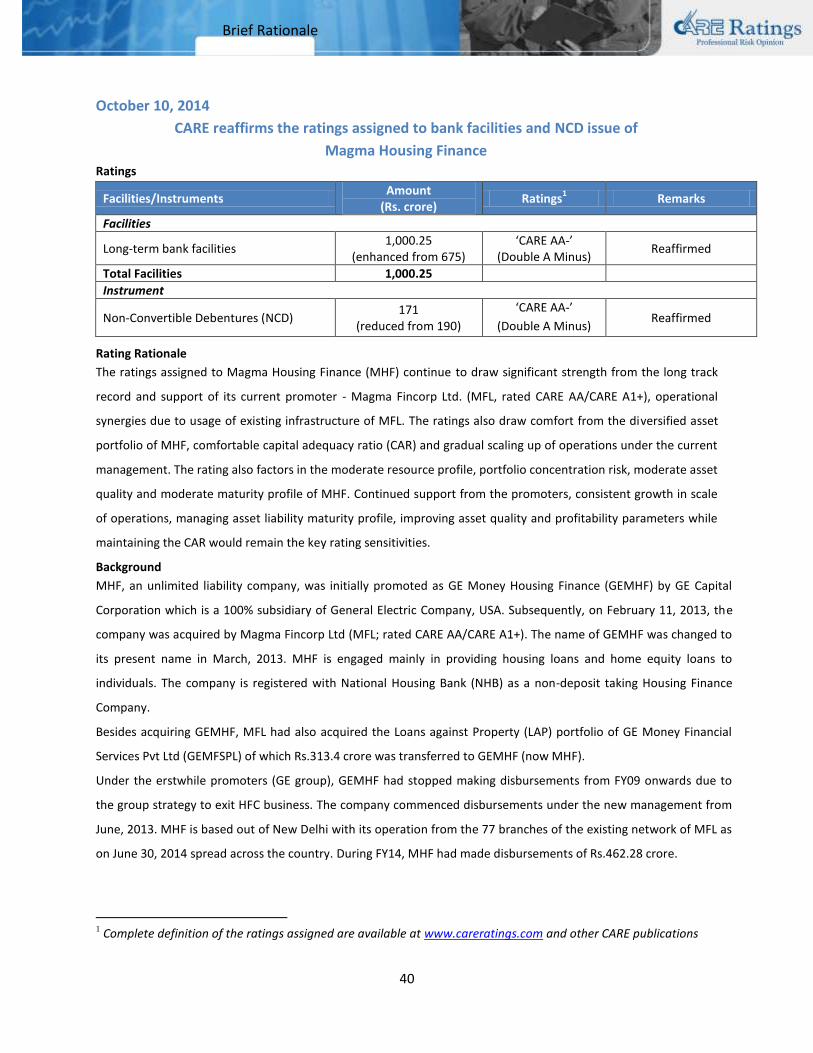

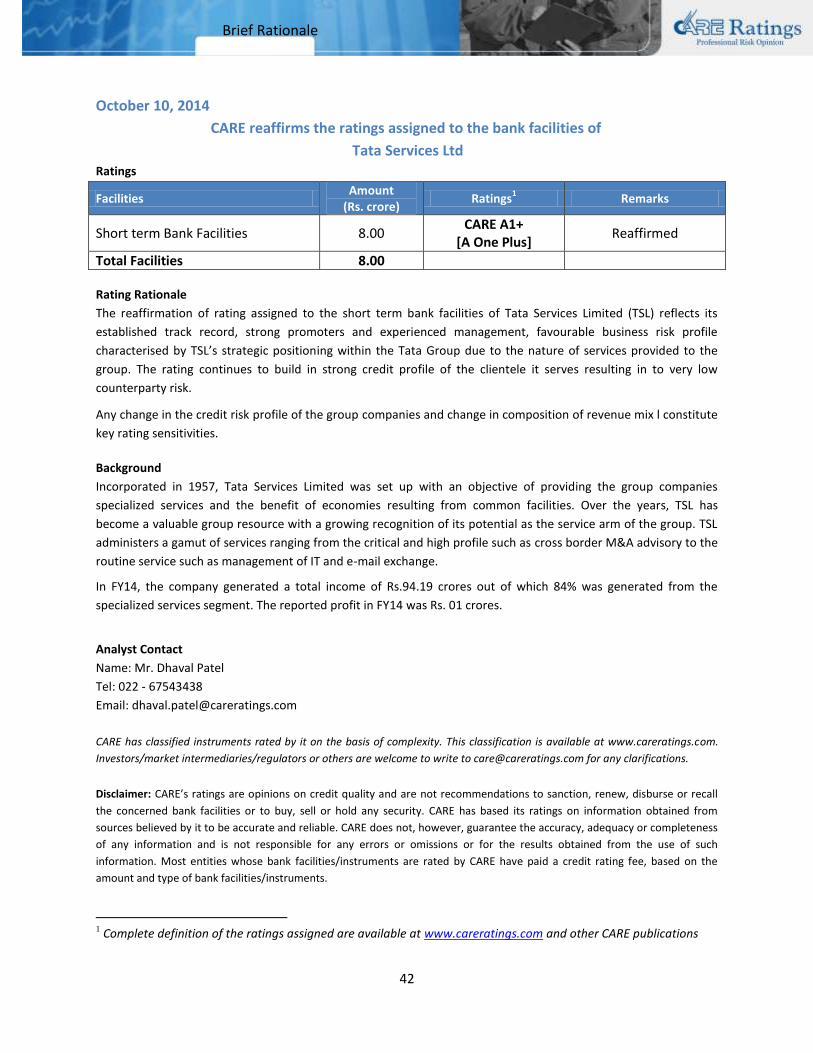

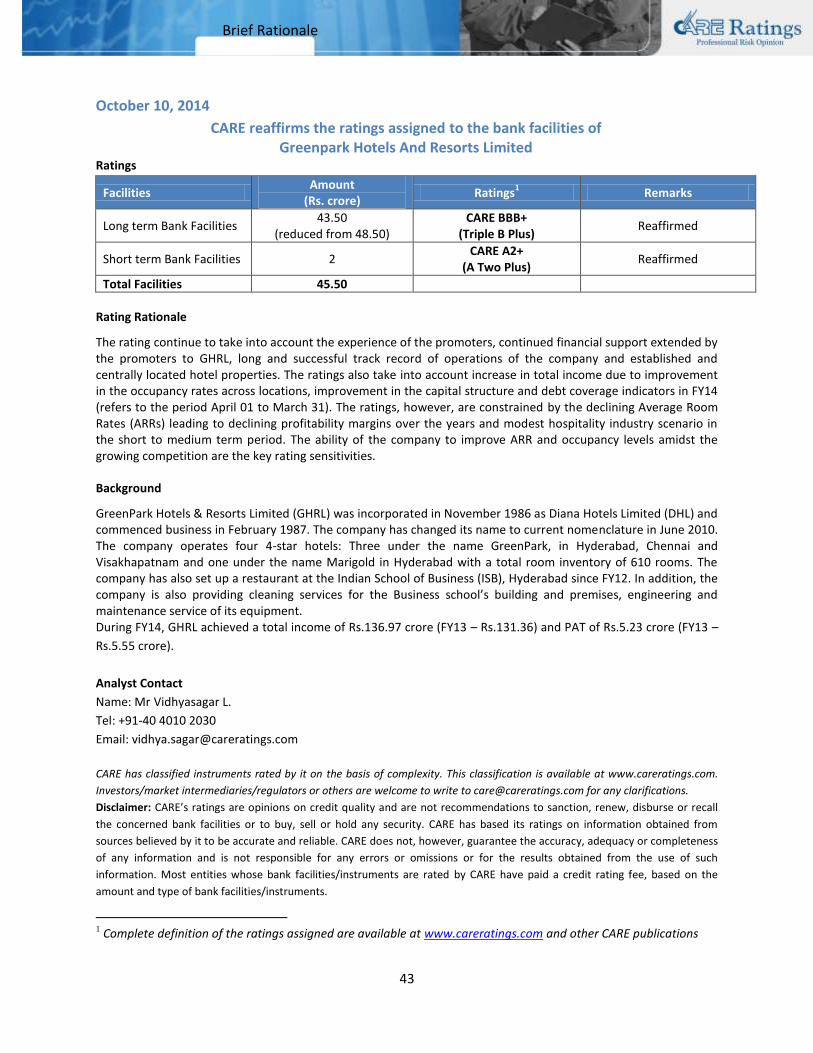

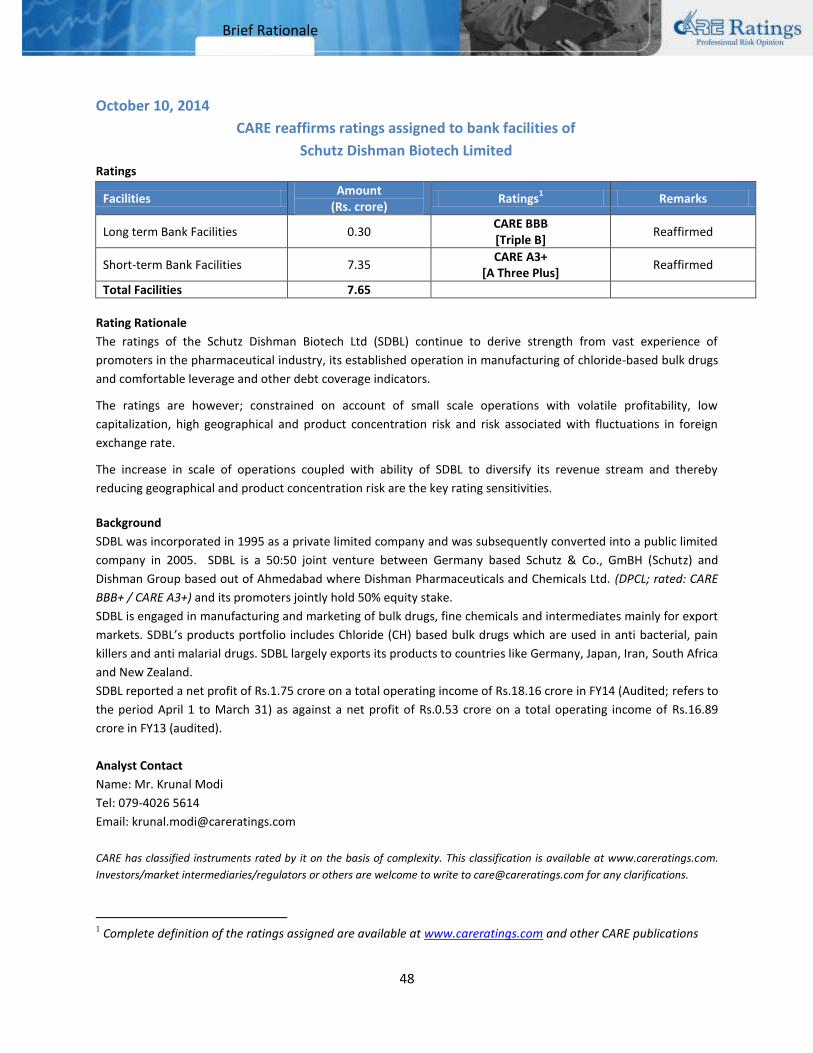

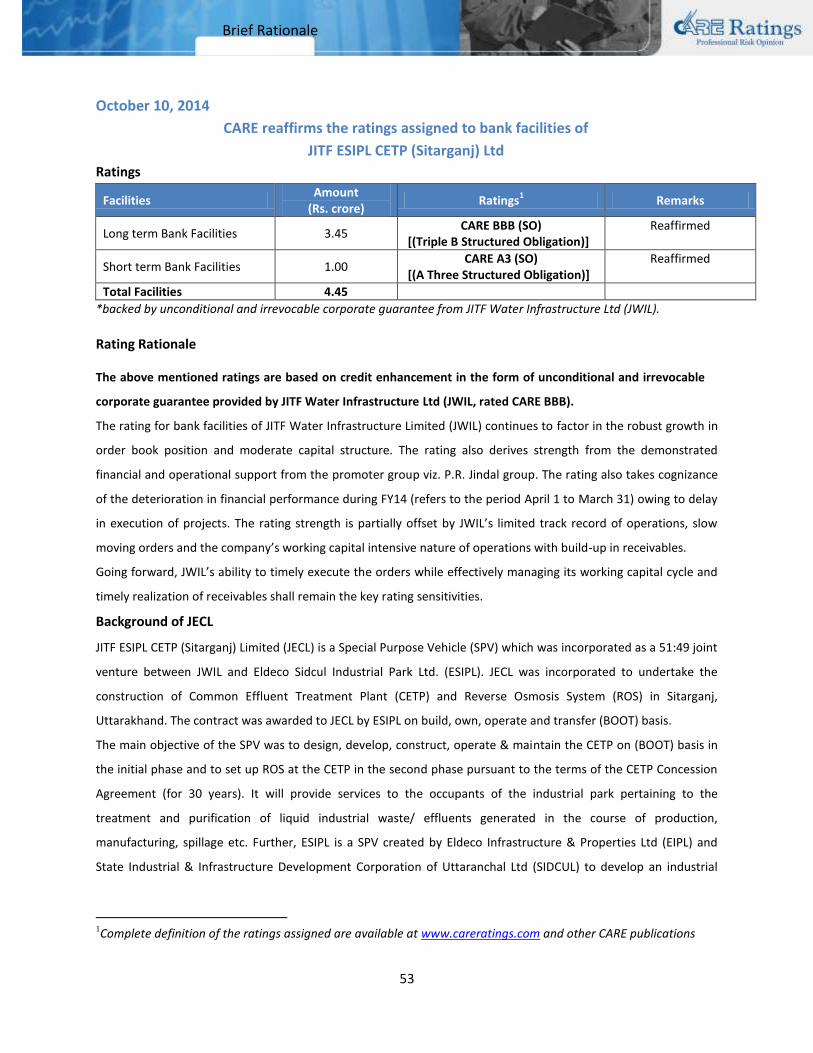

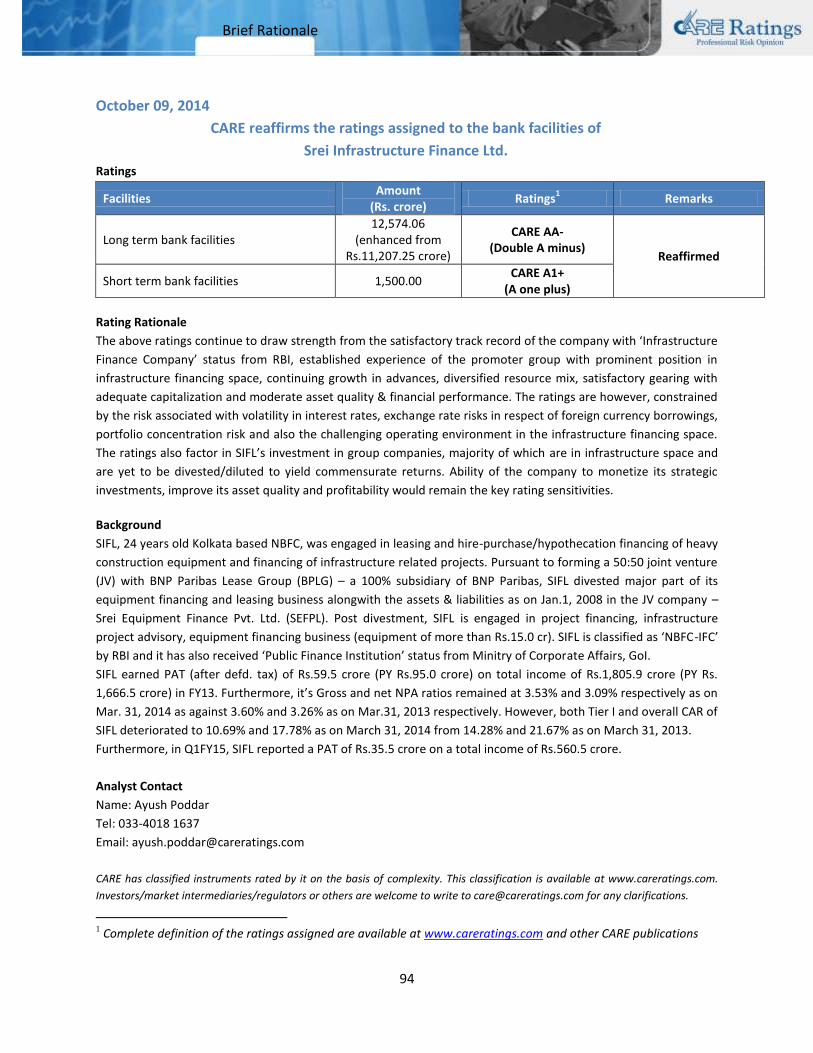

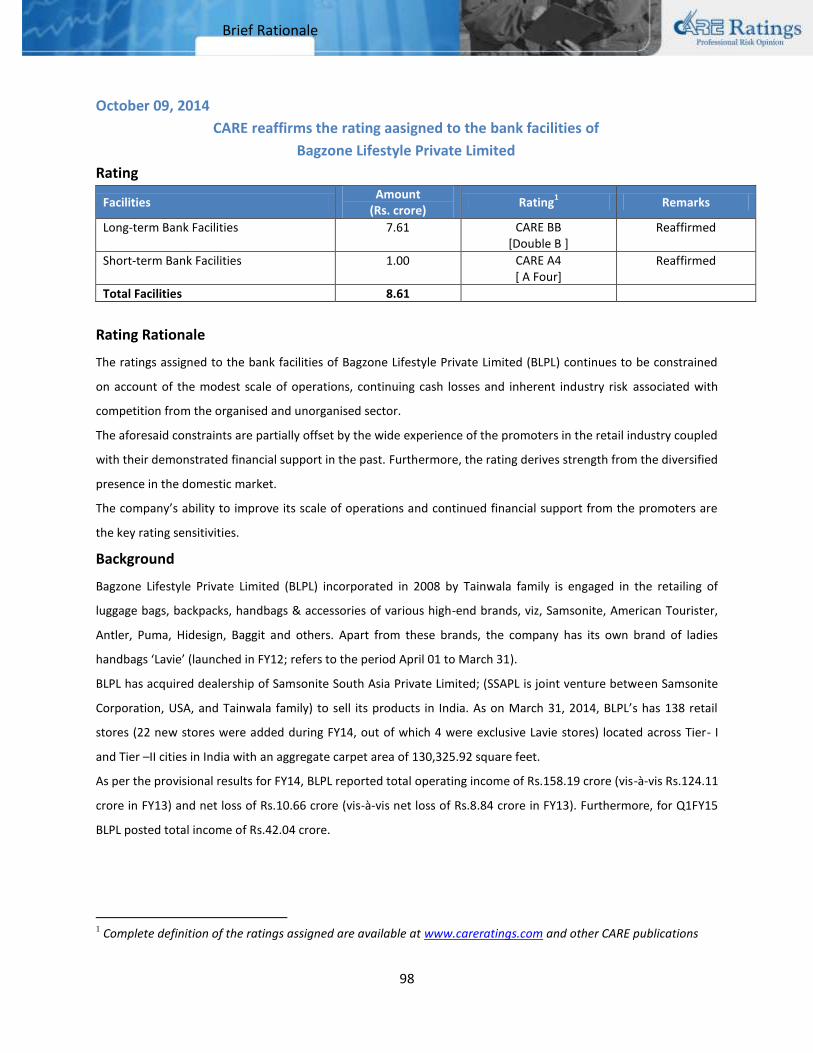

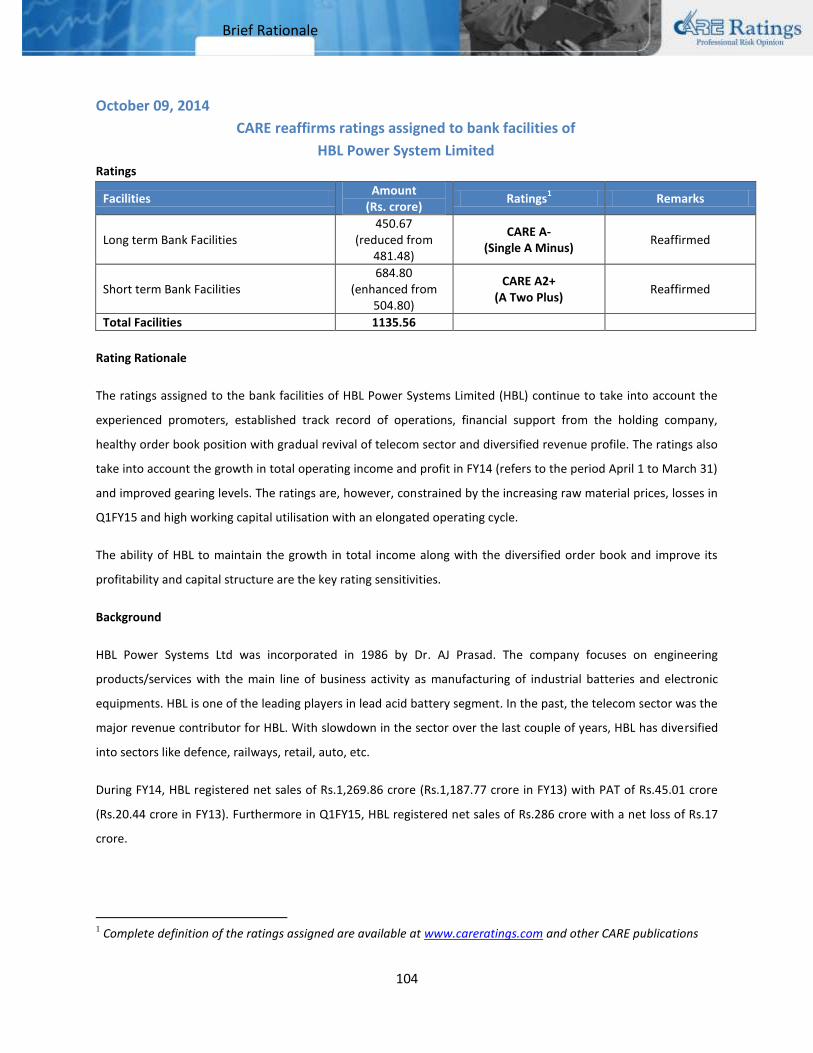

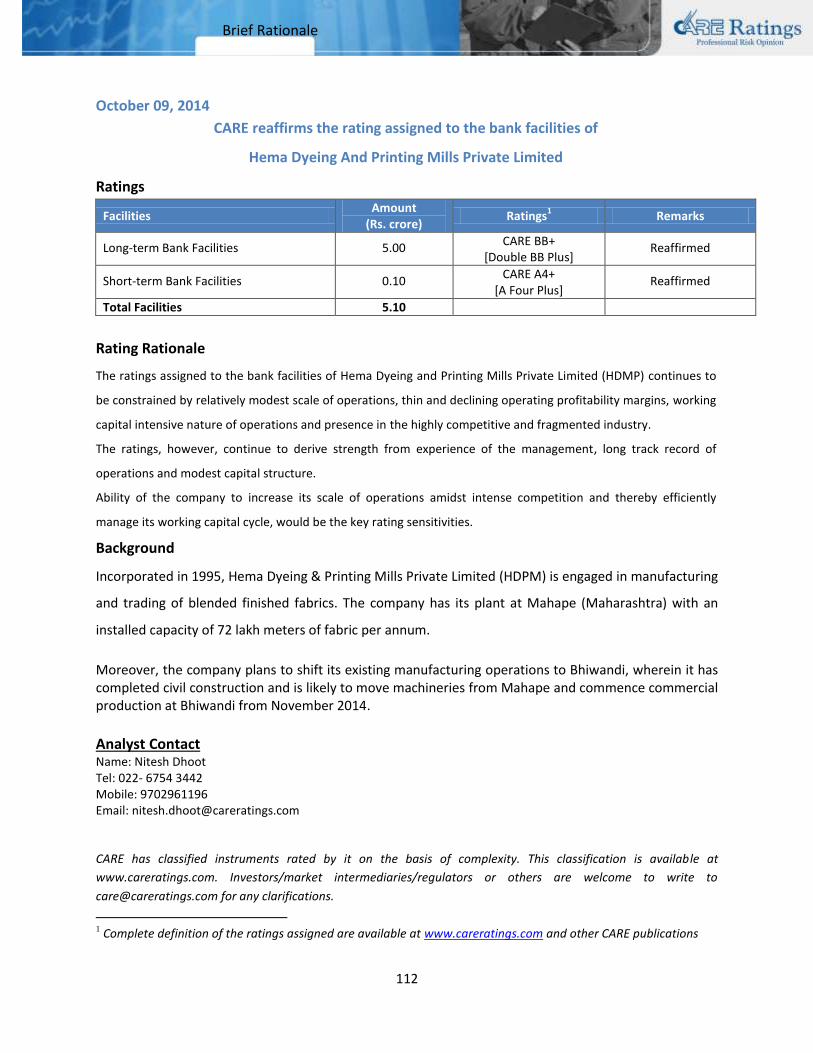

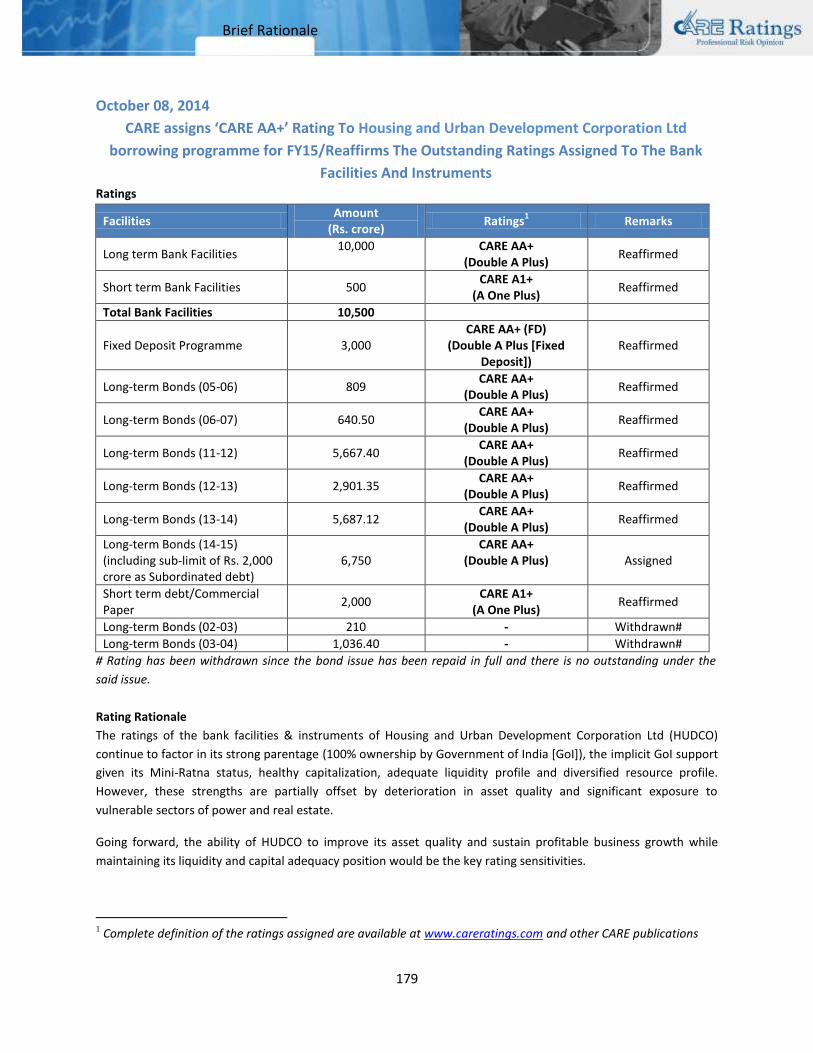

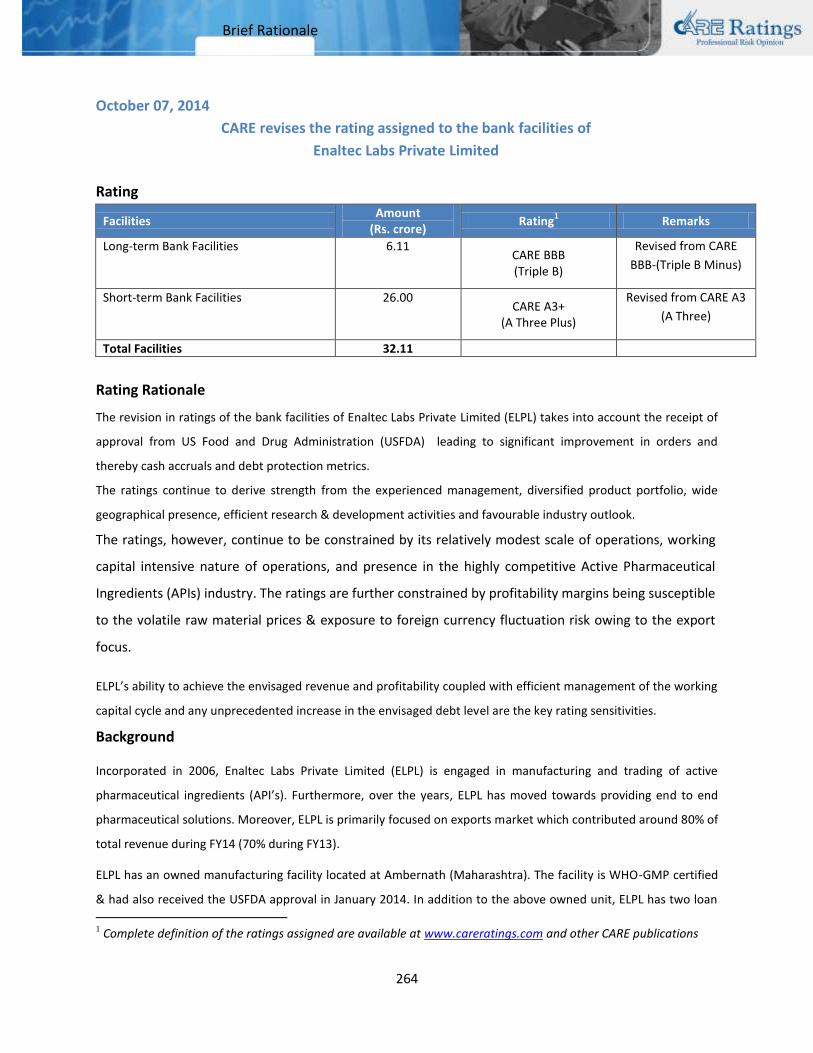

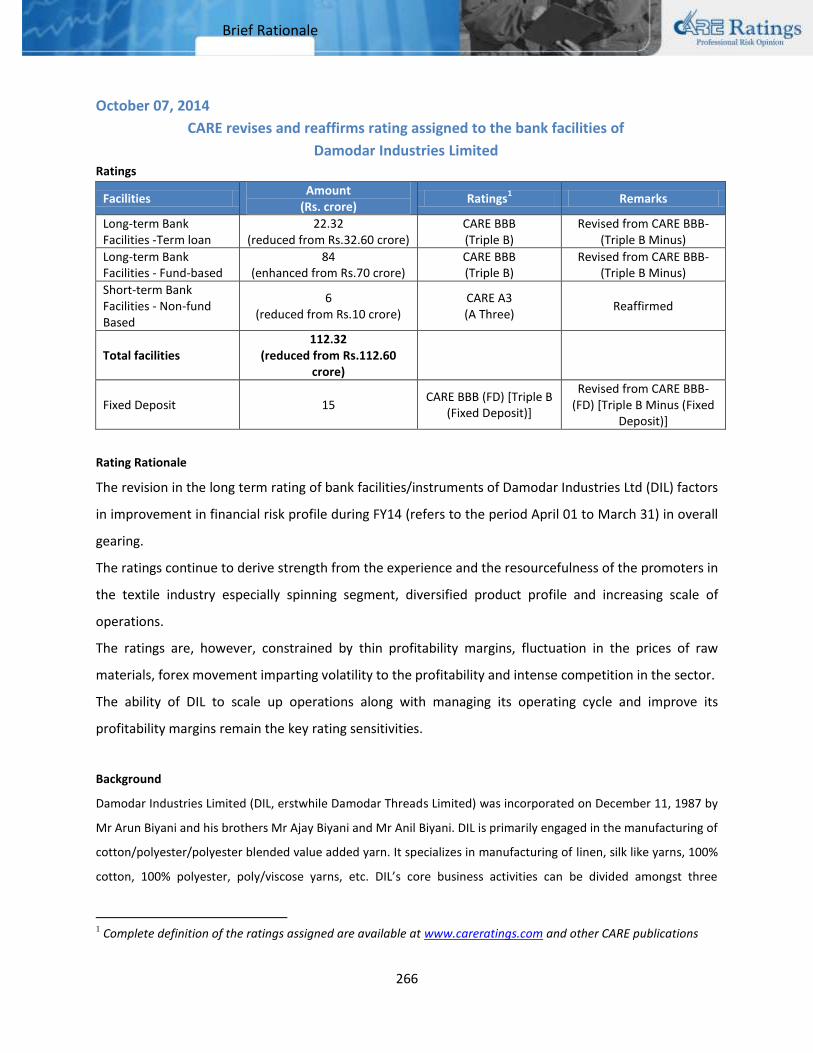

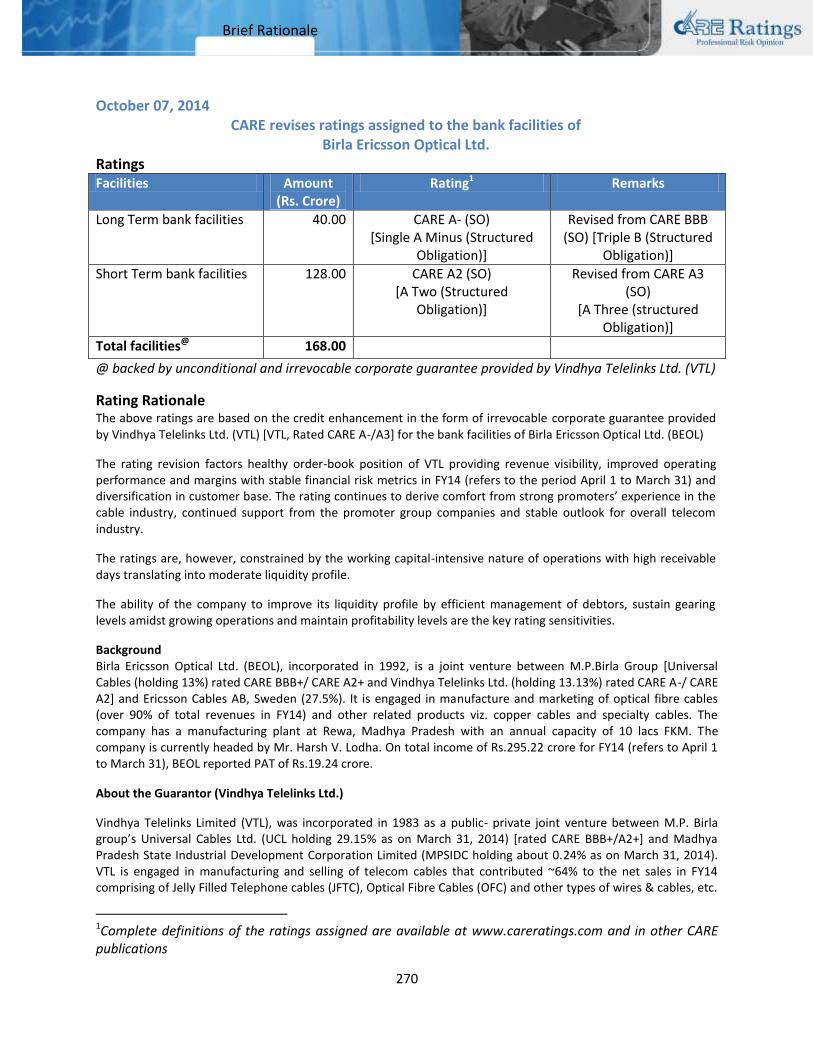

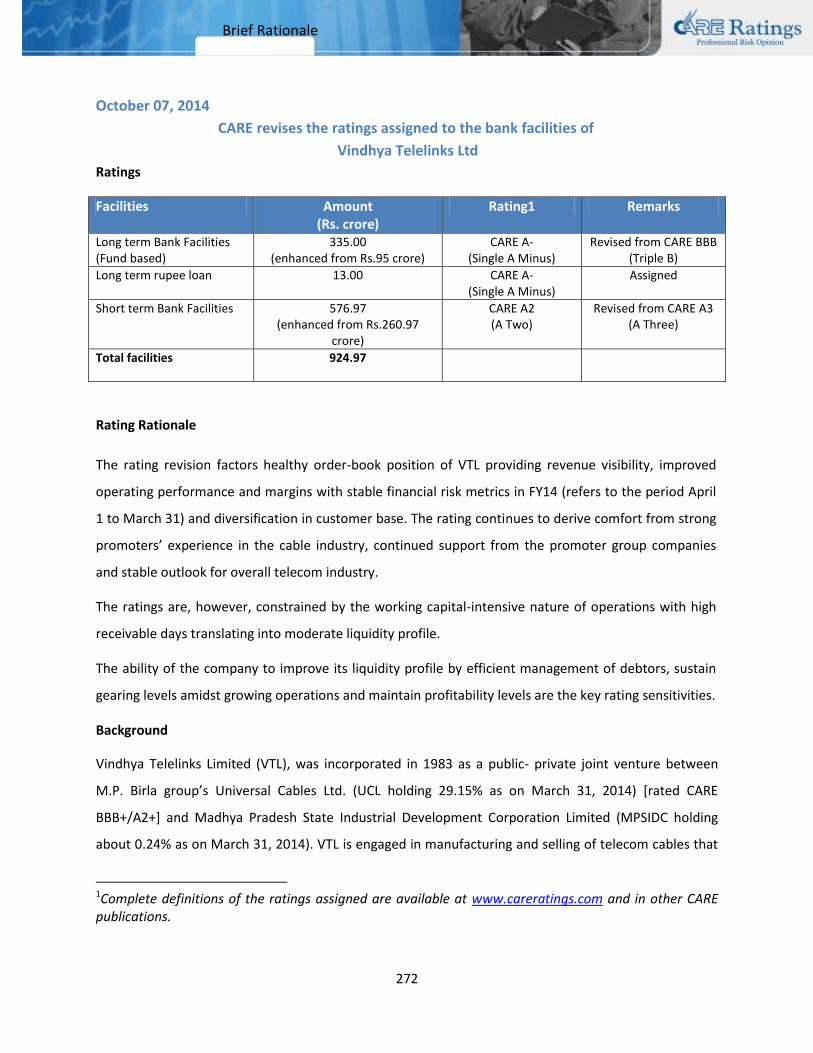

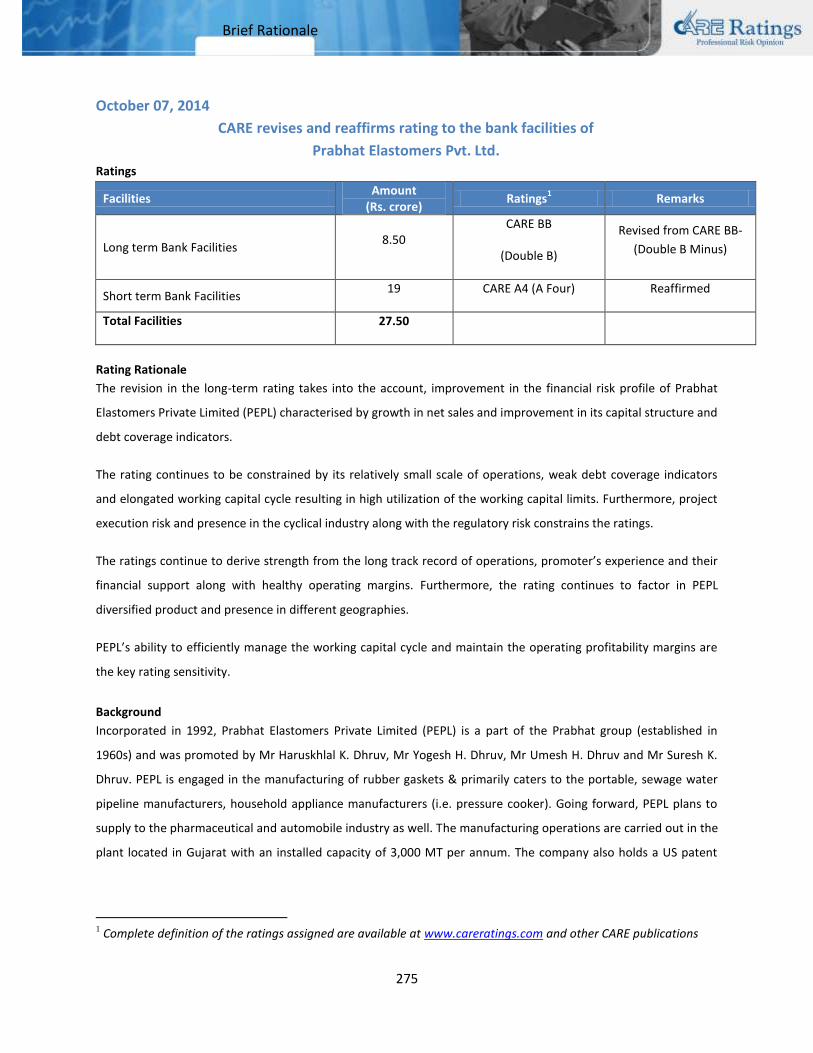

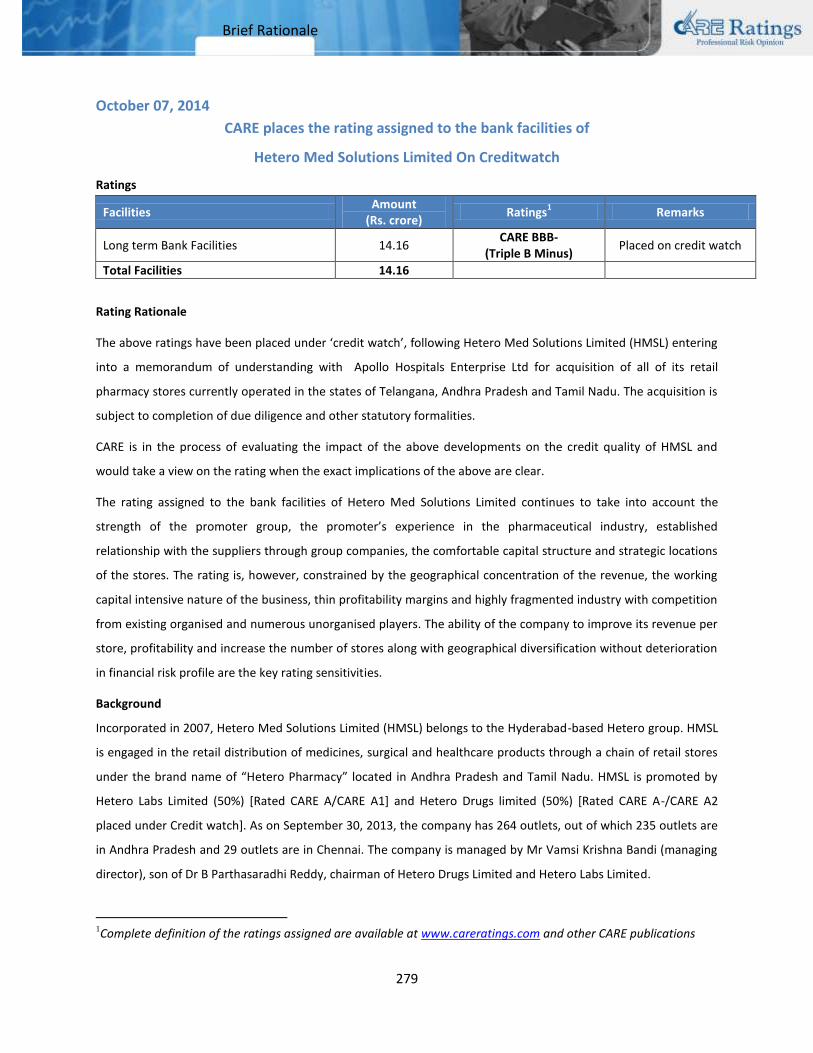

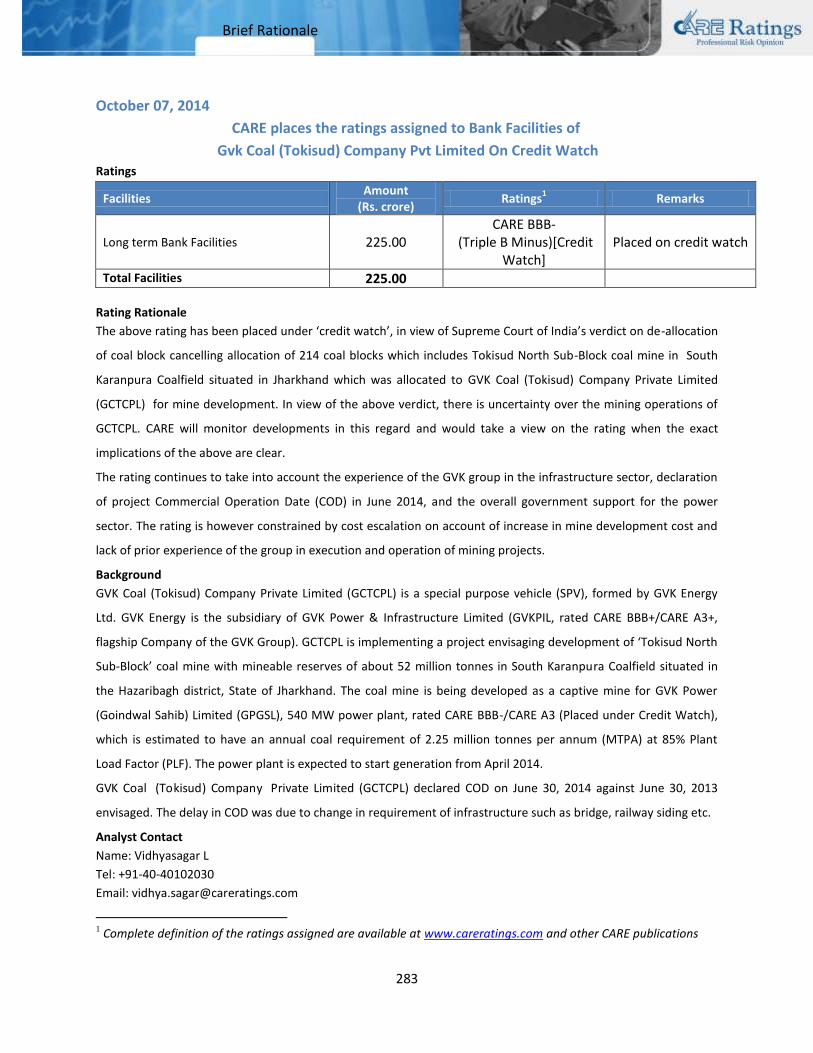

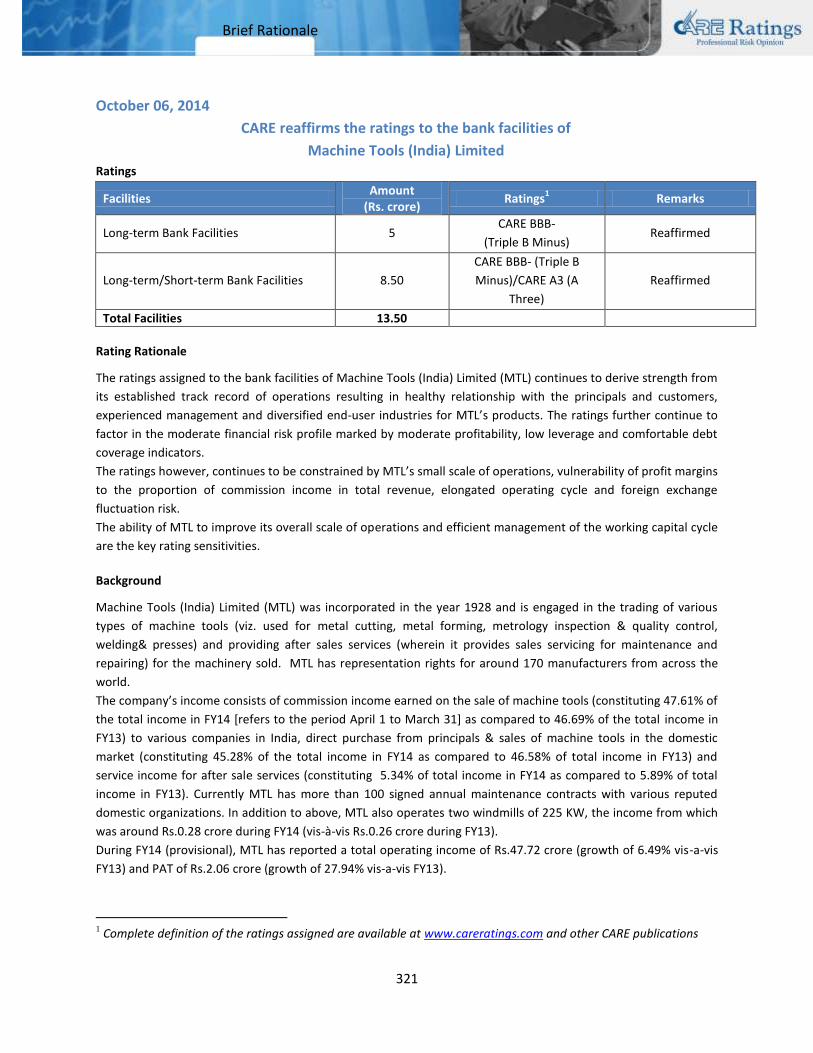

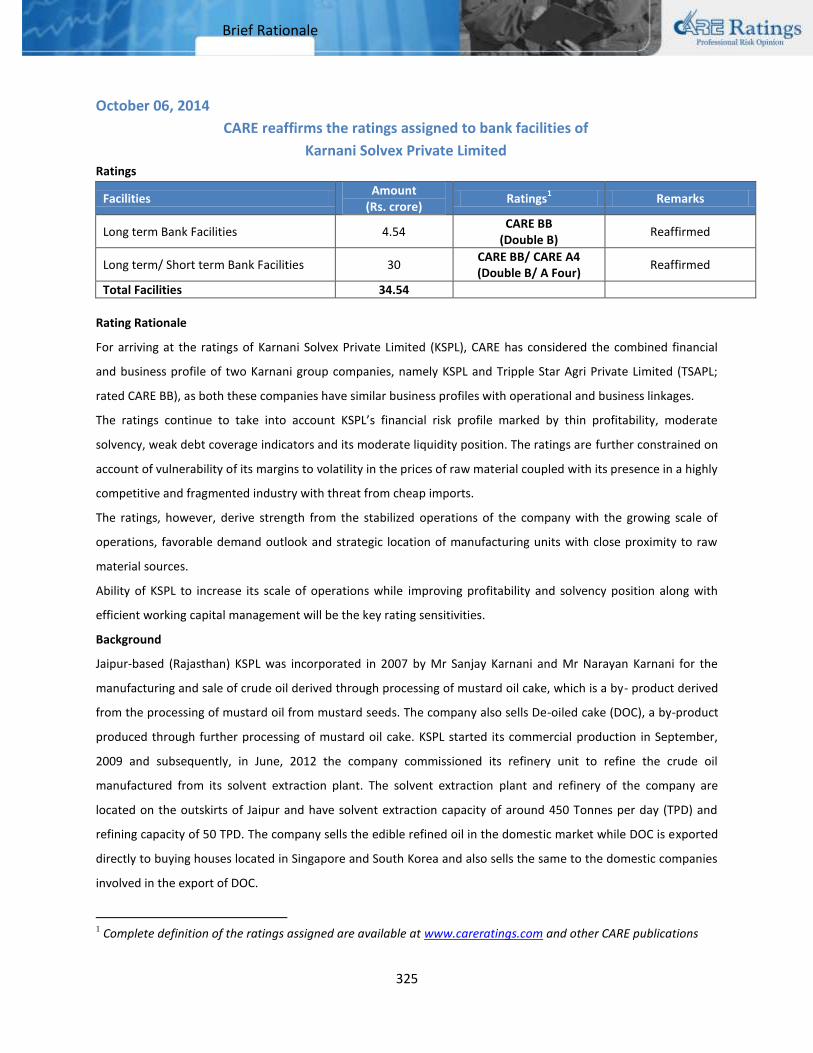

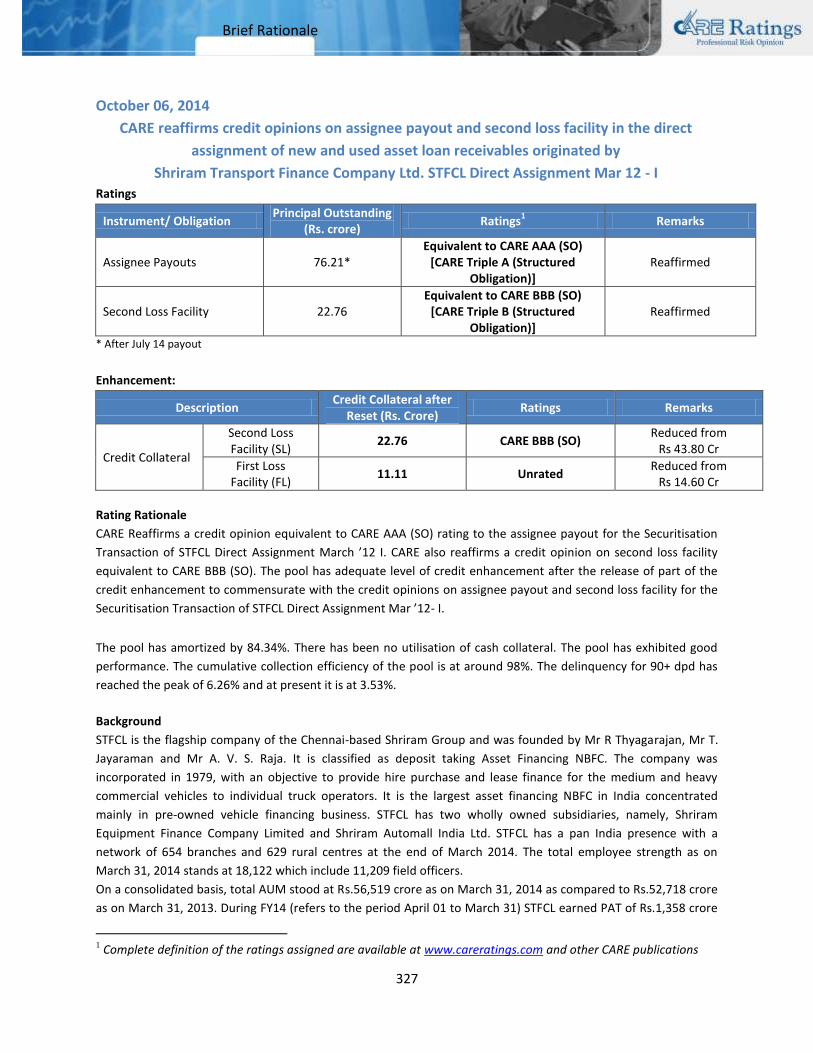

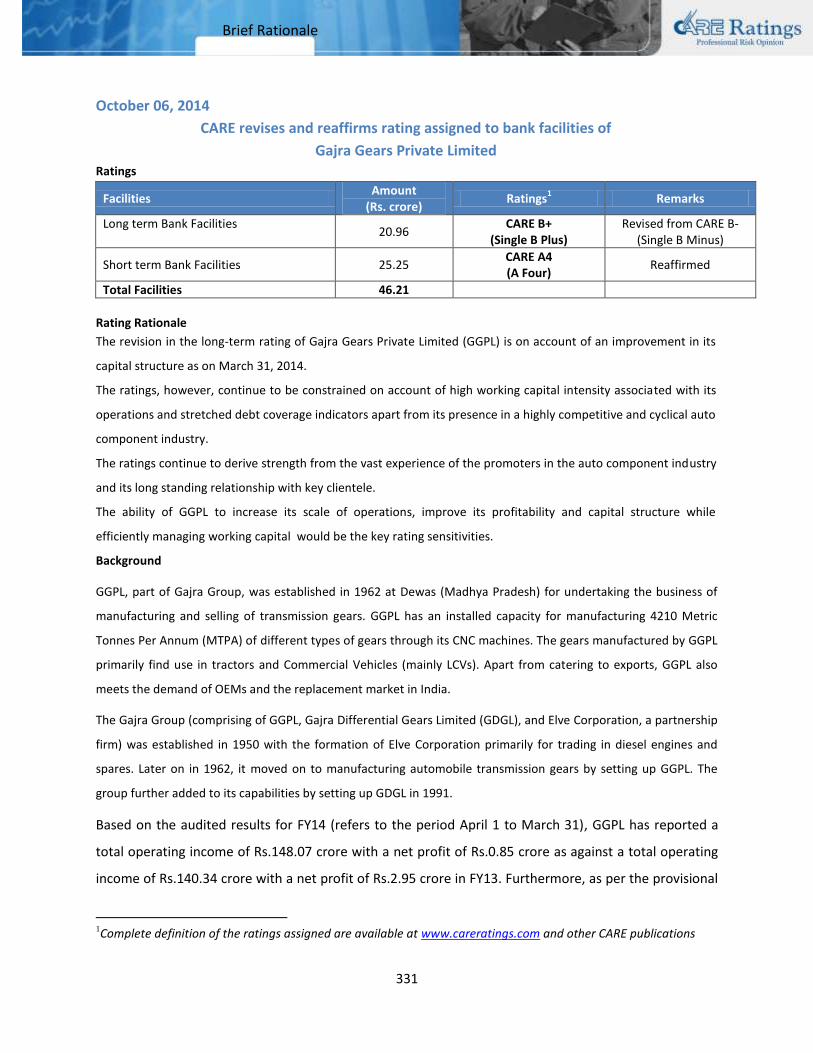

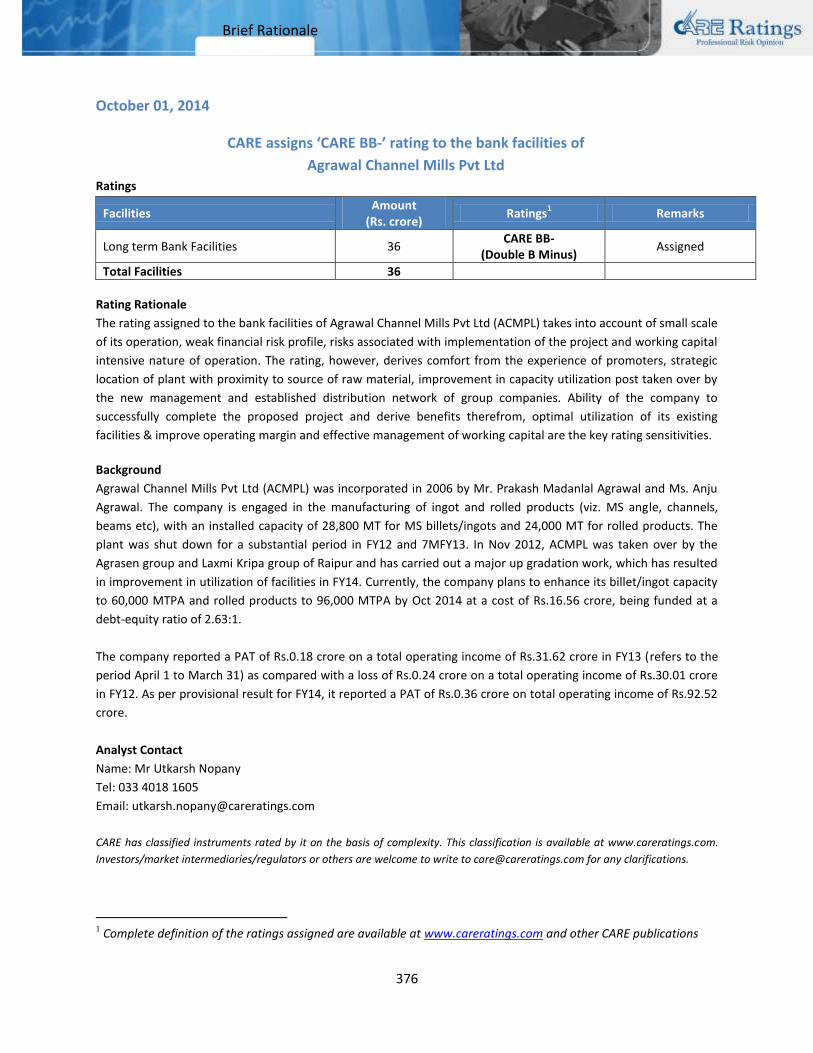

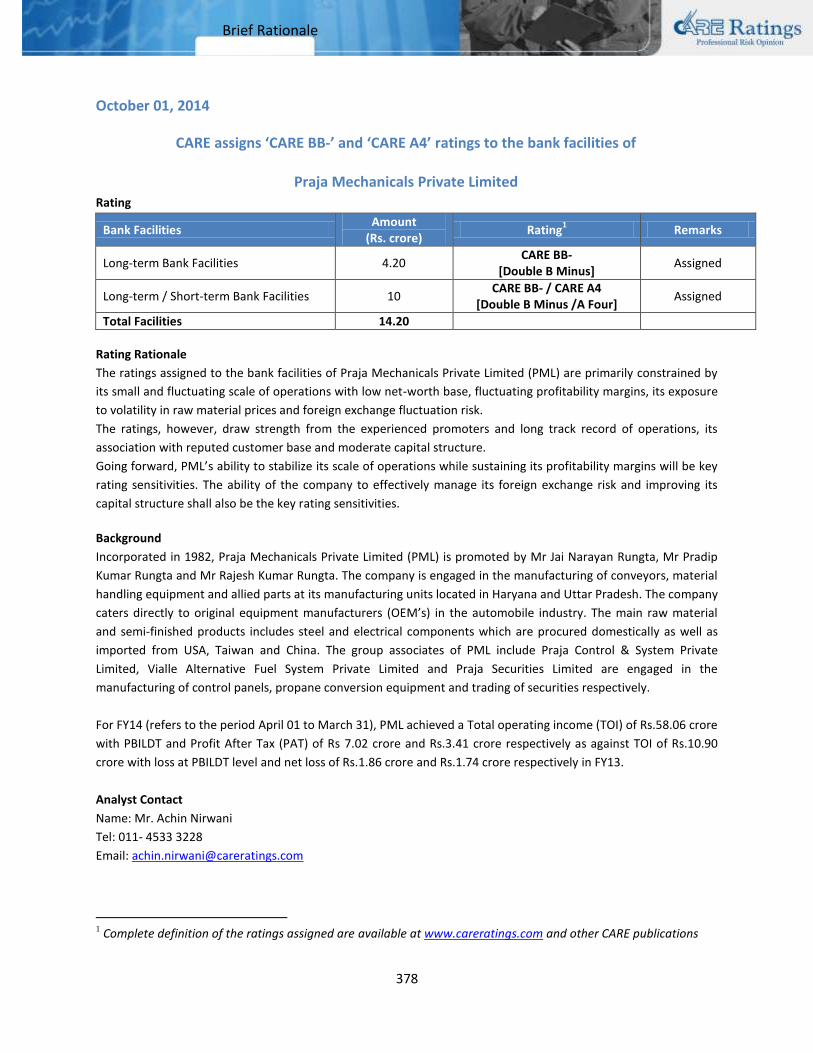

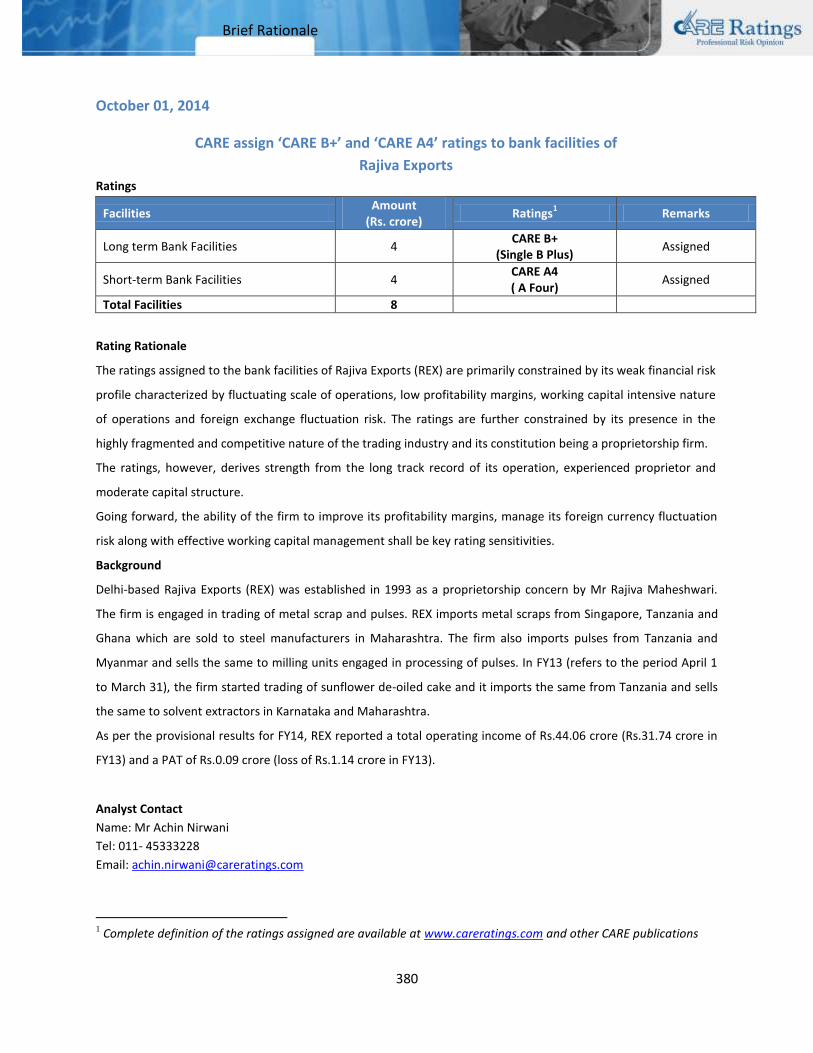

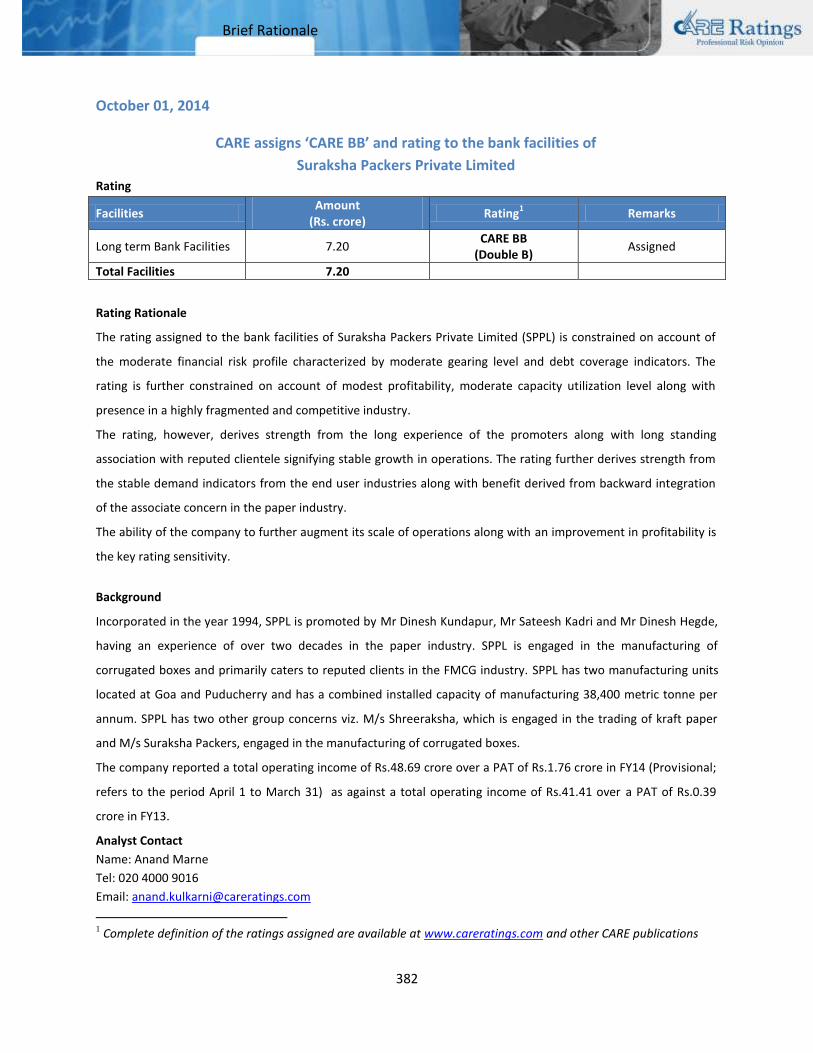

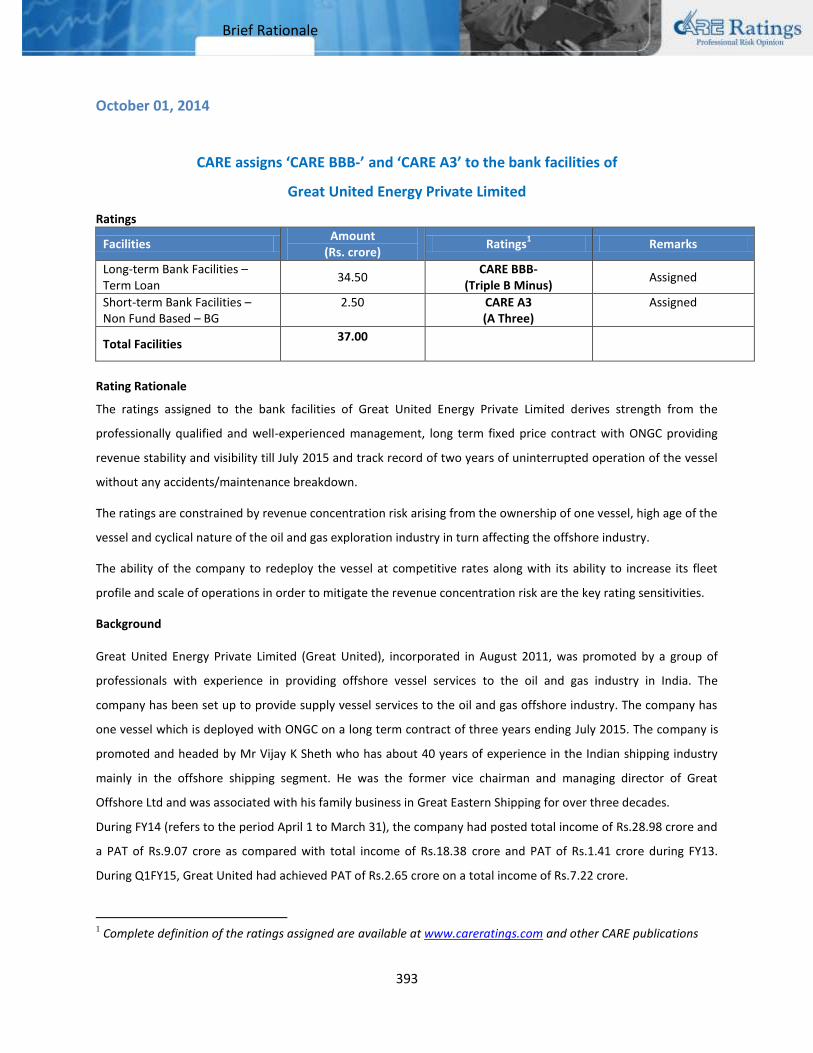

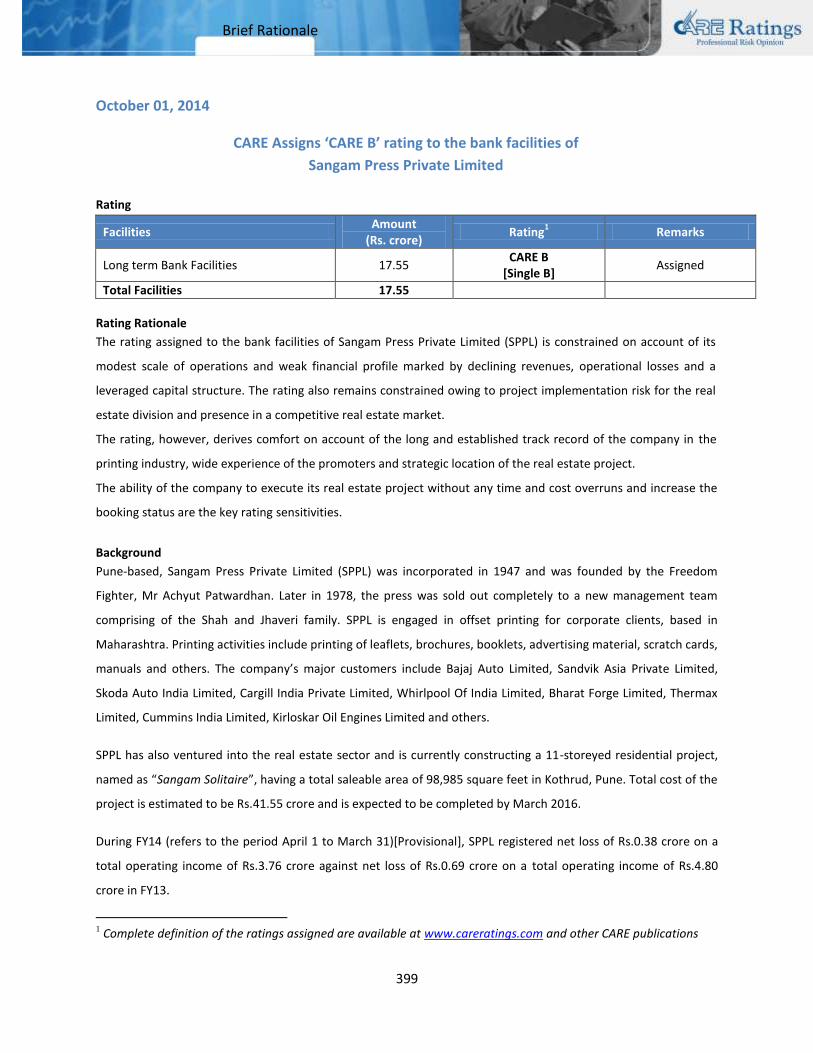

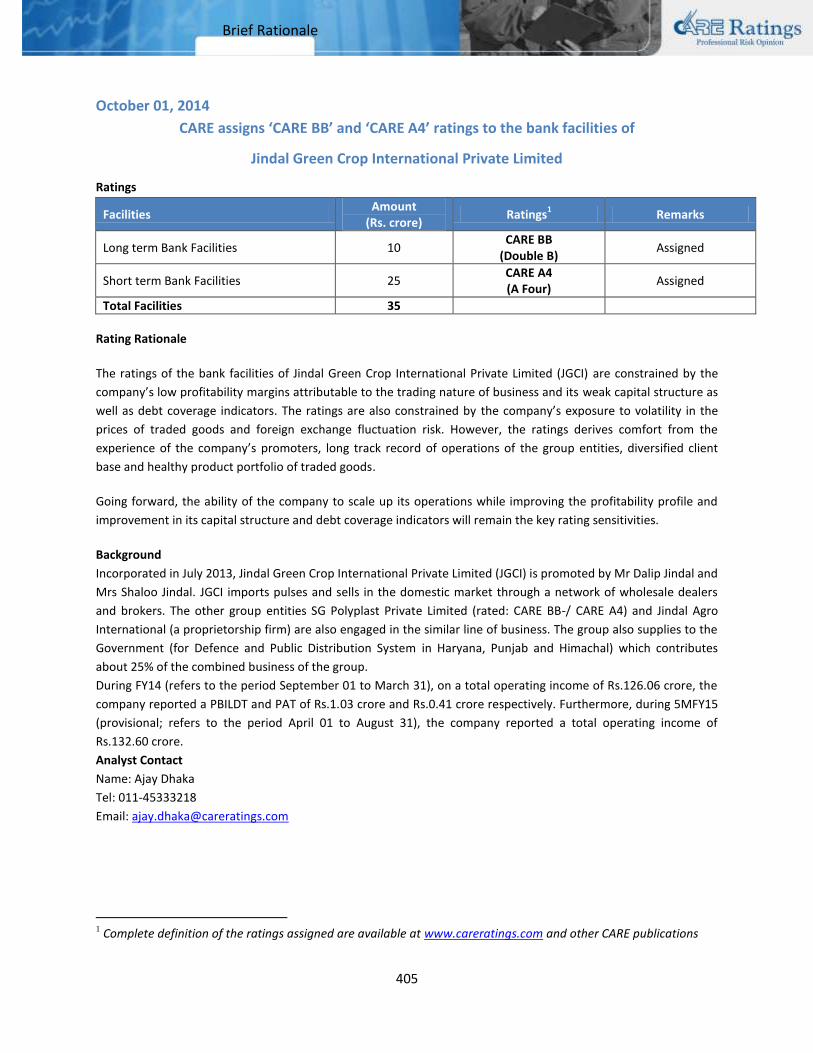

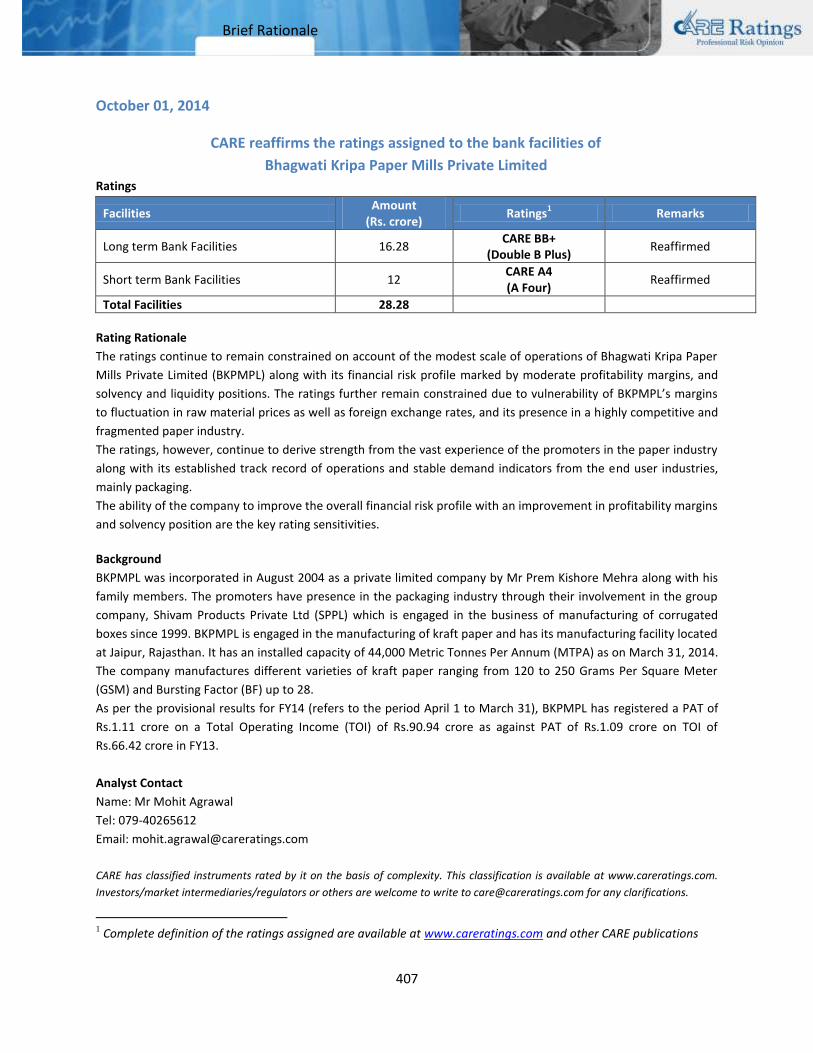

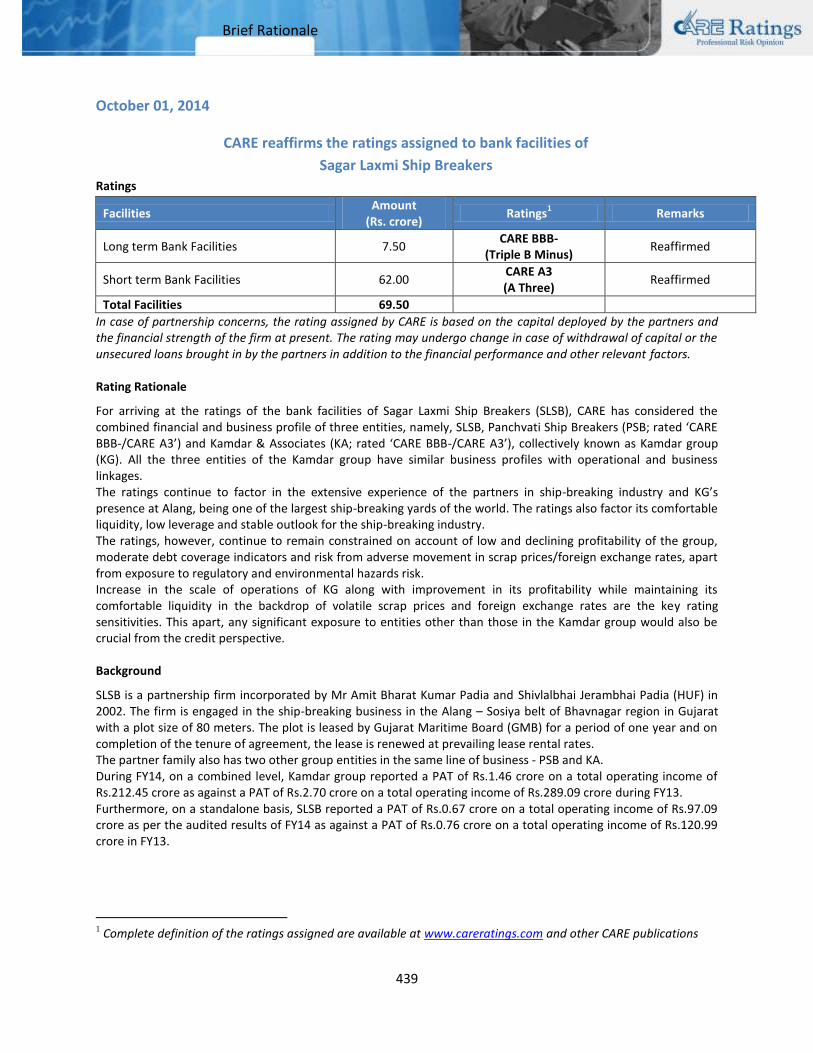

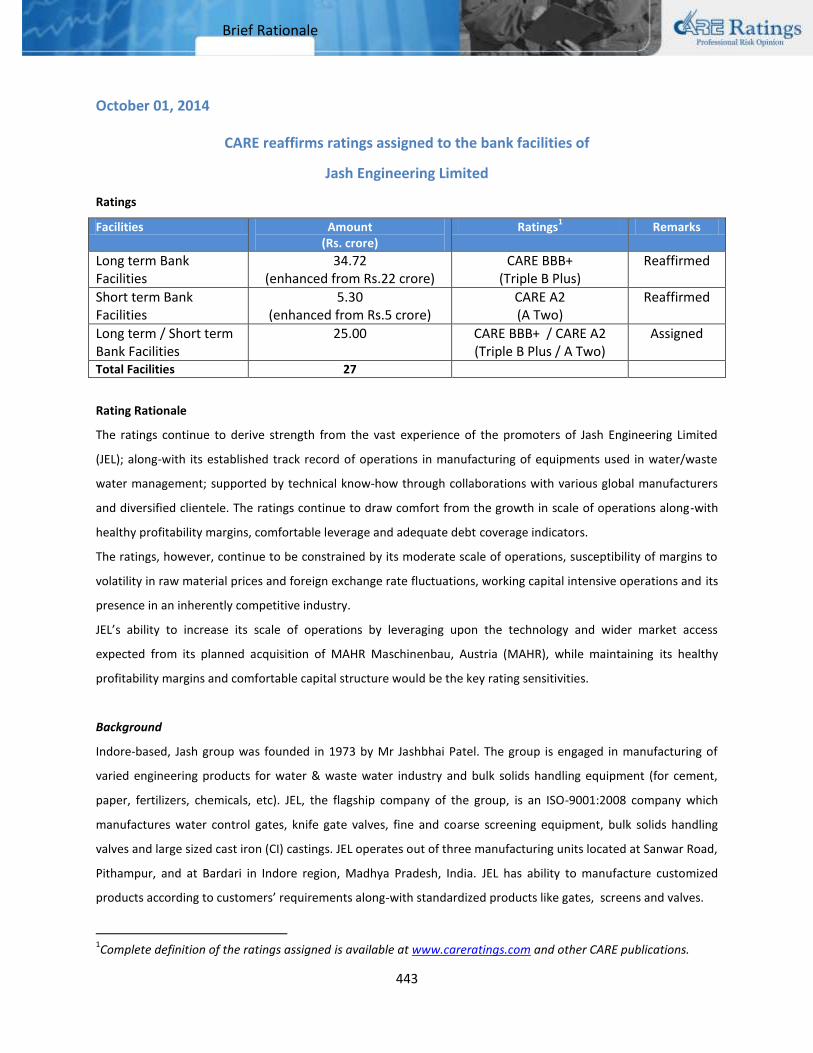

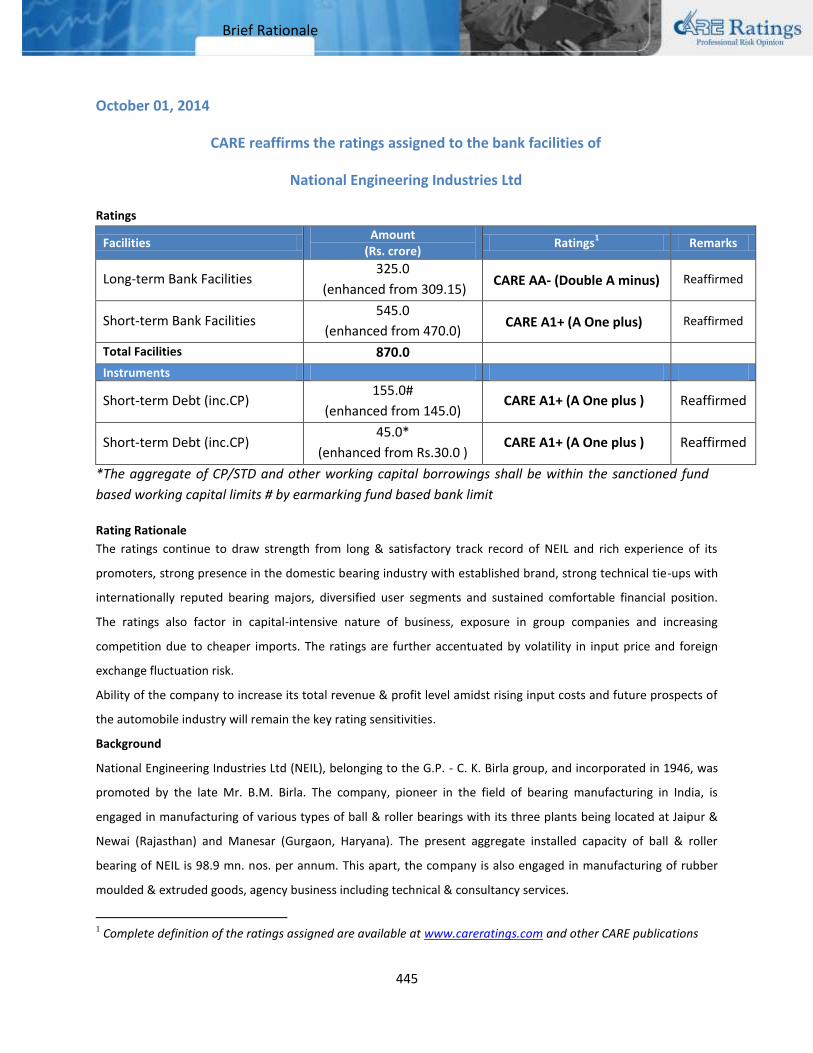

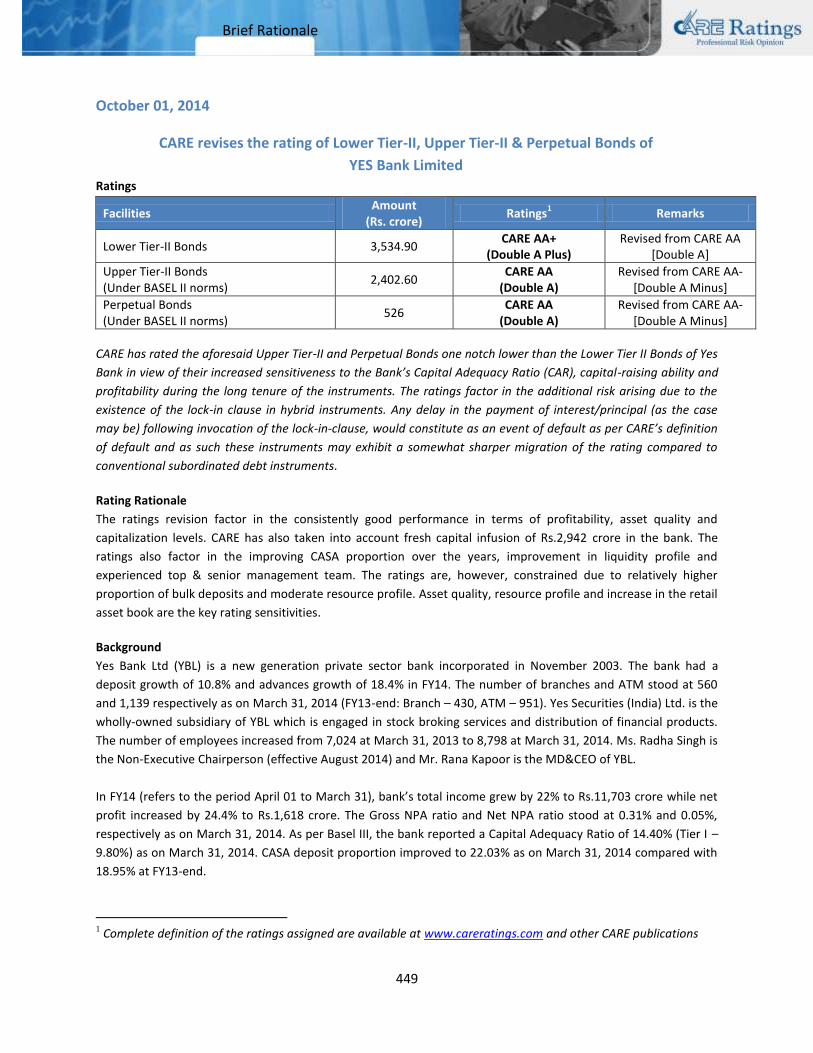

1 Credit Analysis & Research Limited Brief Rationale October 13, 2014 CARE ASSIGNS ‘CARE BB-’ RATING TO THE BANK FACILITIES OF ESSEM 18 CONSTRUCTIONS Rating Facilities Amount (Rs. crore) Rating 1 Remarks Long term Bank Facilities 7.99 CARE BB- (Double B Minus) Assigned Total Facilities 7.99 The rating assigned by CARE is based on capital deployed by the partners and the financial strength of the firm at present. The ratings may undergo a change in case of withdrawal of capital or the unsecured loans brought in by the partners in addition to the financial performance and other relevant factors. Rating Rationale The rating assigned to the bank facilities of Essem 18 Constructions (E18C) is constrained by its relatively small scale of operations, execution risks for the residential project under implementation with significant promoters contribution yet to be infused, marketing risks associated given the increasing competition within the real estate industry, geographical concentration risk with current projects being located at Bangalore region and its constitution as a partnership firm. The rating, however, derives strength from the experienced promoters in the real estate industry, successful execution of its initial project, comfortable capital structure and advantageous location of the project with moderate order booking status. The ability of the firm to execute project within envisaged cost and the ability to sell the flats in a highly competitive scenario at the envisaged prices in a timely manner are the key rating sensitivities. Background Essem 18 Construction (E18C) was setup in 2009 as a partnership firm by Mr. S M Venkatesh (Managing Partner) and Mrs. S Vimala (Partner). The firm is engaged in construction and sale of residential apartments. Till August 2014, the firm has completed one residential project aggregating saleable area of 68,942 sq. ft. E18C has two on-going projects with a total saleable area of 3.32 lakh sq ft. E18C adopts the Joint Development Agreement route of land development, keeping the investment in land at low levels. Under the JDA, the land owner is compensated through sharing of built-up area. 1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 Credit Analysis & Research Limited

Brief Rationale

October 13, 2014

CARE ASSIGNS ‘CARE BB-’ RATING TO THE BANK FACILITIES OF

ESSEM 18 CONSTRUCTIONS

Rating

Facilities Amount

(Rs. crore)

Rating1 Remarks

Long term Bank Facilities 7.99 CARE BB-

(Double B Minus)

Assigned

Total Facilities 7.99

The rating assigned by CARE is based on capital deployed by the partners and the financial strength of the firm

at present. The ratings may undergo a change in case of withdrawal of capital or the unsecured loans brought

in by the partners in addition to the financial performance and other relevant factors.

Rating Rationale

The rating assigned to the bank facilities of Essem 18 Constructions (E18C) is constrained by its relatively small

scale of operations, execution risks for the residential project under implementation with significant

promoters contribution yet to be infused, marketing risks associated given the increasing competition within

the real estate industry, geographical concentration risk with current projects being located at Bangalore

region and its constitution as a partnership firm.

The rating, however, derives strength from the experienced promoters in the real estate industry, successful

execution of its initial project, comfortable capital structure and advantageous location of the project with

moderate order booking status.

The ability of the firm to execute project within envisaged cost and the ability to sell the flats in a highly

competitive scenario at the envisaged prices in a timely manner are the key rating sensitivities.

Background

Essem 18 Construction (E18C) was setup in 2009 as a partnership firm by Mr. S M Venkatesh (Managing

Partner) and Mrs. S Vimala (Partner). The firm is engaged in construction and sale of residential apartments.

Till August 2014, the firm has completed one residential project aggregating saleable area of 68,942 sq. ft.

E18C has two on-going projects with a total saleable area of 3.32 lakh sq ft. E18C adopts the Joint

Development Agreement route of land development, keeping the investment in land at low levels. Under the

JDA, the land owner is compensated through sharing of built-up area.

1Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications.

2

Brief Rationale

Analyst Contact

Name: Rajani Tenali

Tel: 040 40102030/40102031

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at

www.careratings.com. Investors/market intermediaries/regulators or others are welcome to write to

[email protected] for any clarifications.

Disclaimer

CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information

obtained from sources believed by it to be accurate and reliable. CARE does not, however, guarantee the

accuracy, adequacy or completeness of any information and is not responsible for any errors or omissions or for

the results obtained from the use of such information. Most entities whose bank facilities/instruments are rated

by CARE have paid a credit rating fee, based on the amount and type of bank facilities/instruments.

In case of partnership/proprietary concerns, the rating assigned by CARE is based on the capital deployed by the

partners/proprietor and the financial strength of the firm at present. The rating may undergo change in case of

withdrawal of capital or the unsecured loans brought in by the partners/proprietor in addition to the financial

performance and other relevant factors.

3

Brief Rationale

October 13, 2014

CARE ASSIGNS RATINGS AND REAFFIRMS SHORT TERM RATINGS TO BANK FACILITIES OF

MAGNUM ESTATES LIMITED Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 13.20 CARE BBB-

(Triple B Minus) Assigned

Short term Bank Facilities 13.85 CARE A3 (A Three)

Reaffirmed

Total Facilities 27.05

Rating Rationale

The aforesaid rating draws strength from the experience of promoters, long standing relationship with

clients, established procurement network and proximity to raw material sources, and satisfactory capital

structure with moderate profitability margin. The rating is, however, constrained by highly fragmented

industry with low entry barriers, intense competition in the export market, dependence on government

support in the form of export incentives, seasonal nature of the industry, geographical & client

concentration risk, foreign exchange fluctuation risk and inherent risk associated with sea food industry.

Ability to increase scale of operations & maintaining the capital structure and continuous government

support to the sector are the key rating sensitivities.

Background

Magnum Estates Limited (MEL) was incorporated by Mr. Ramesh Mahapatra in the year 1993; however,

the company commenced operations from the calendar year 1995. MEL is involved in the aquaculture

business, i.e. culturing of black tiger prawns and sea food exports. The company also has its own pre-

processing plant, including an ice-making plant at Naupalgadi, Balasore. It has an arrangement with its

other group entity engaged in the similar line of business, Magnum Sea Foods Limited for processing of

its products.

In FY14, the company’s total operating income was Rs. 101.47 crore with a PBILDT of Rs. 3.80 crore and

a PAT of Rs. 1.93 crore.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

4

Brief Rationale

Analyst Contact

Name: Mr. Vineet Chamaria

Tel: 033-40181600/1609

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

5

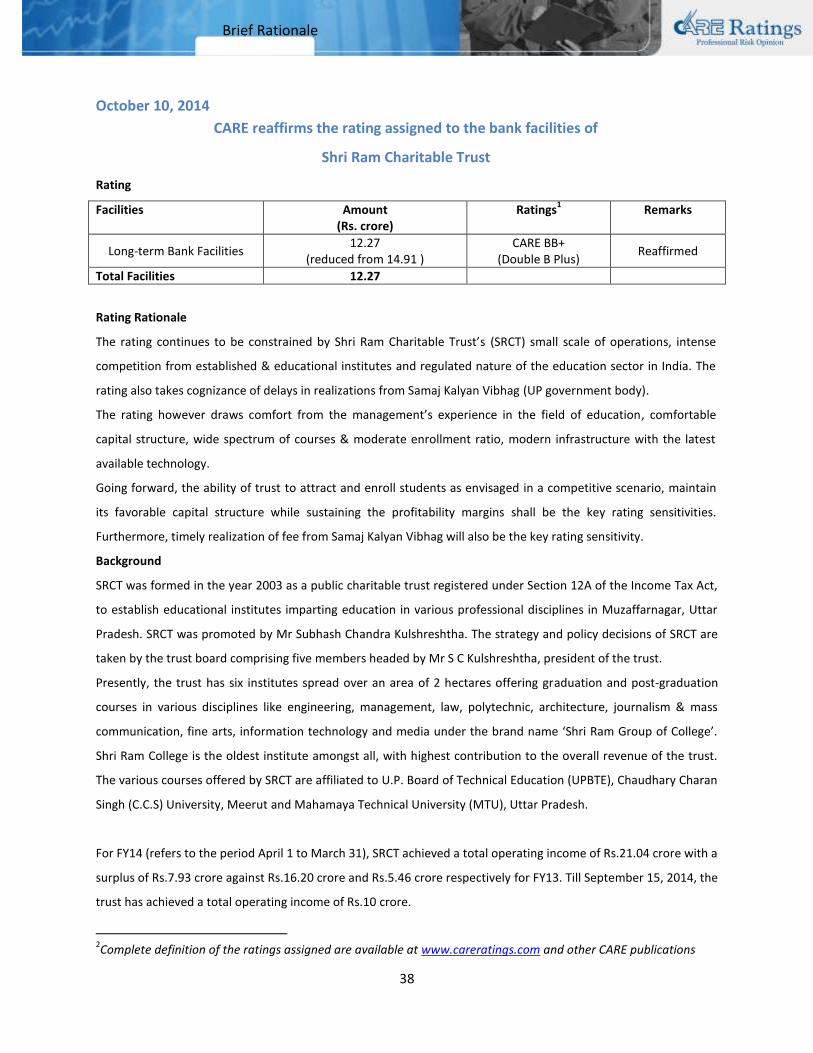

Brief Rationale

October 10, 2014

CARE assigns CARE BBB (SO)/CARE A3 (SO) to the bank facilities of Agroh Rewa Ring Road Private Limited

Ratings

Facilities Amount

(Rs. crore) Rating1

Remarks

Long Term Bank Facilities 55.00 CARE BBB (SO)

[Triple B (structured obligation)] Assigned

Long Term/Short Term Bank Facilities

3.33 CARE BBB (SO)/CARE A3 (SO)

[Triple B (structured obligation)]/ [A Three (structured obligation)]

Assigned

Short Term Bank Facilities 0.90 CARE A3 (SO)

[A Three (structured obligation)] Assigned

Total Facilities @ 59.23

@Backed by unconditional and irrevocable corporate guarantee of Agroh Infrastructure Developers Private Limited (AIDPL) Rating Rationale

The ratings assigned to the bank facilities of Agroh Rewa Ring Road Private Limited (ARRRPL) are based on the credit enhancement in the form of an unconditional and irrevocable corporate guarantee extended by Agroh Infrastructure Developers Private Limited (AIDPL; rated ‘CARE BBB/CARE A3’).

The ratings assigned to the bank facilities of AIDPL continue to take into account its established track record of healthy toll collection from its sole build, operate and transfer (BOT)-based road project, good revenue visibility in the medium term, experienced promoters and moderate debt protection indicators.

Further, ratings also take into account AIDPL’s demonstrated execution capabilities marked by completion of two BOT projects in special purpose vehicles (SPVs) ahead of its schedule which has also resulted in growth in scale of operations during FY14 (refers to the period April 1 to March 31).

The ratings, however, are constrained by AIDPL’s increasing exposure to BOT-based road projects elevated by ‘with recourse’ nature of debt of its SPVs, along with delay in liquidation of the advances/investment extended to various companies and underperformance of its two SPVs. The ratings continue to be constrained by its geographically concentrated operations and challenging business environment faced by the construction industry.

Completion of the ongoing BOT projects within the envisaged time and cost parameters, performance of the entities whose debt has been guaranteed by AIDPL and the extent of exposure to BOT-based road projects impacting the credit profile of the company are the key rating sensitivities. Liquidation of loans/advances to various companies and monetization of investments in immovable property in a time bound manner would also be key rating monitorable.

Background

ARRRPL is a joint venture (JV) between AIDPL (60% stake) and Bhaiya Lal Shukla Infrastructure Private Ltd (40% stake). ARRRPL has entered into a 15 year concession agreement with Madhya Pradesh Road Development Corporation Ltd [MPRDC; an undertaking of Government of Madhya Pradesh (GoMP)] for the design-build-finance-operate and transfer (DBFOT) of 8.93 km road project in Madhya Pradesh (MP) on toll plus annuity basis.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

6

Brief Rationale

The project road under consideration aims at construction and development of Rewa Ring Road by four laning of Rathera junction at km 229/10 on national highway – 7 (NH-7) in Rewa town and ends at km 6/2 at Shilpra village on state highway - 9 (SH-9).

The concession agreement includes construction period of two years from appointed date. The total cost of the project is Rs.77.05 crore being funded through debt of Rs.55 crore and promoter contribution of Rs.22.05 crore. Out of total engineering, procurement and construction (EPC) cost of Rs.68.79 crore, ARRRPL has completed the EPC work of Rs.36.76 crore up to- July 31, 2014.

About the Guarantor

Agroh Infrastructure Developers Private Limited

AIDPL was originally incorporated as a SPV promoted by Singhal family of Indore and entered into a Concession Agreement with MPRDC in November 2001 for the strengthening, widening and rehabilitation of Ujjain-Agar-Jhalawad (UAJ) road project (SH-27) on BOT basis. The project is debt free and has a track record of generating healthy cash accrual and is scheduled to be handed over in April 2017. With award of new BOT projects, AIDPL has started executing EPC work for its own BOT based road projects from FY12.

Apart from one operational BOT project (UAJ) structured in its standalone balance sheet, AIDPL has currently seven BOT-based road projects (five in joint venture SPVs and two in wholly owned SPV) in its portfolio, of which two are operational; two are partly operational while the rest three are at various stages of execution.

During FY14, AIDPL reported a total operating income of Rs.269.61 crore (FY13: Rs.131.55 crore) with profit after tax (PAT) of Rs.38.10 crore (FY13: Rs.27.29 crore).

For a detailed rationale of AIDPL, please refer to www.careratings.com

Analyst Contact

Name: Maulesh Desai

Tel: 079-40265605

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

7

Brief Rationale

October 10, 2014

CARE assigns ‘CARE AA-(SO)’ rating to bank facility of

Skyscape Developers Private Limited Rating

Facilities Amount

(Rs. crore) Rating

1 Remarks

Long-Term Bank Facility ^ 300 CARE AA- (SO)

[Double A Minus (Structured Obligation)] Assigned

^ backed by an unconditional and irrevocable continuing corporate guarantee from Shapoorji Pallonji & Co. Pvt. Ltd

(SPCPL) for maintenance of debt service reserve for an amount equal to the succeeding 90 (ninety) days of interest

payment and an amount equal to the principal payment due in succeeding 30 (thirty) days throughout the tenure of

the facility

Rating Rationale

The rating assigned to the long term bank facilities of Skyscape Developers Pvt. Ltd. (SDPL) principally derives

comfort from the credit enhancement in the form of an unconditional and irrevocable revolving commitment from

SPCPL (rated CARE AA+) for maintenance of debt service reserve for an amount equal to the succeeding 90 (ninety)

days of interest payment and an amount equal to the principal payment due in succeeding 30 (thirty) days

throughout the tenure of the facility.

The rating is, however, tempered by inactive stage of project development, vacancy despite completion of one of

the towers since the past four years and cyclical nature of the real estate industry.

The rating remains sensitive primarily to any variation in credit rating of the guarantor i e SPCPL.

Rating Rationale of SPCPL

The rating of SPCPL principally derives strength from resourcefulness of the Shapoorji Pallonji group (SP group) and

its substantive financial strength mainly on account of being the largest private shareholder in Tata Sons Ltd (TSL,

holding company of the Tata group) with 18.37% stake. Additionally, strong financial flexibility of SPCPL with

considerably high level of unlocked value of its investments in diverse fields & land parcels further enhance credit

profile of the company.

The rating is also supported by the company’s proven track record in the construction, infrastructure & real estate

space, its well-diversified order book, healthy revenue visibility over the medium term and adequate liquidity.

The rating is, however, constrained by subdued profitability in its core business segment, weakening standalone

financial profile with leveraged capital structure, rise in the collection period and increasing financial support

extended to the group companies.

Ability of SPCPL to improve its operational profitability, manage working capital efficiently and unlock the optimum

value from its various assets continues to be the key rating sensitivities.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

8

Brief Rationale

Background

SDPL, incorporated in 2006, is a wholly owned subsidiary of Sprite Developers Mauritius Ltd. SDPL is carrying out a

development of three IT towers admeasuring 10.20 lacs square feet (lsf) under the name ‘SP Infocity’ along with 1

tower for service apartment and 1 tower for commercial and recreational activities in Manesar, Gurgaon. SPCL was

allotted an open plot admeasuring 9.44 acres by Haryana State Industrial & Infrastructure Development

Corporation LTD (HSIIDC) in 2006 to carry out the development. SDPL has entered in brand usage agreement with

SPCPL and the latter has been appointed as contractor and project management consultant.

About the DSRA Guarantor-SPCPL

SPCPL, the flagship company of the SP group, is one of the leading construction companies of India. SPCPL is

equally held by Mr Shapoor P Mistry and Mr Cyrus P Mistry through the group’s investment companies.

During its more than 148 years of operations, SP group has built diverse civil and engineering structures like

factories, nuclear waste handling establishments, stadiums and auditoriums, airports, hospitals, hotels, housing

complexes, water treatment plants, roads and power plants around the world.

Analyst Contact

Name: Ms. Rajashree Murkute

Tel: 022-6144 3505

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments. In case of partnership/proprietary concerns, the rating assigned by CARE is based on the capital deployed by the

partners/proprietor and the financial strength of the firm at present. The rating may undergo change in case of withdrawal of

capital or the unsecured loans brought in by the partners/proprietor in addition to the financial performance and other relevant

factors.

9

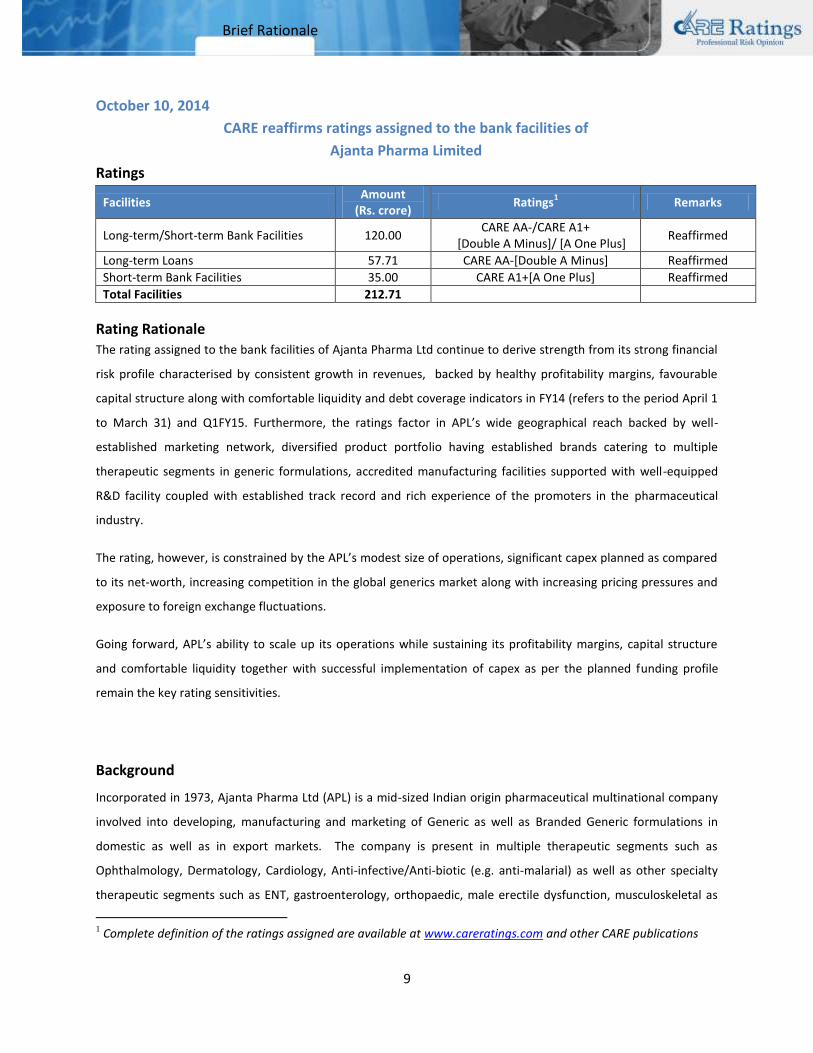

Brief Rationale

October 10, 2014

CARE reaffirms ratings assigned to the bank facilities of

Ajanta Pharma Limited

Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long-term/Short-term Bank Facilities 120.00 CARE AA-/CARE A1+

[Double A Minus]/ [A One Plus] Reaffirmed

Long-term Loans 57.71 CARE AA-[Double A Minus] Reaffirmed

Short-term Bank Facilities 35.00 CARE A1+[A One Plus] Reaffirmed

Total Facilities 212.71

Rating Rationale The rating assigned to the bank facilities of Ajanta Pharma Ltd continue to derive strength from its strong financial

risk profile characterised by consistent growth in revenues, backed by healthy profitability margins, favourable

capital structure along with comfortable liquidity and debt coverage indicators in FY14 (refers to the period April 1

to March 31) and Q1FY15. Furthermore, the ratings factor in APL’s wide geographical reach backed by well-

established marketing network, diversified product portfolio having established brands catering to multiple

therapeutic segments in generic formulations, accredited manufacturing facilities supported with well-equipped

R&D facility coupled with established track record and rich experience of the promoters in the pharmaceutical

industry.

The rating, however, is constrained by the APL’s modest size of operations, significant capex planned as compared

to its net-worth, increasing competition in the global generics market along with increasing pricing pressures and

exposure to foreign exchange fluctuations.

Going forward, APL’s ability to scale up its operations while sustaining its profitability margins, capital structure

and comfortable liquidity together with successful implementation of capex as per the planned funding profile

remain the key rating sensitivities.

Background

Incorporated in 1973, Ajanta Pharma Ltd (APL) is a mid-sized Indian origin pharmaceutical multinational company

involved into developing, manufacturing and marketing of Generic as well as Branded Generic formulations in

domestic as well as in export markets. The company is present in multiple therapeutic segments such as

Ophthalmology, Dermatology, Cardiology, Anti-infective/Anti-biotic (e.g. anti-malarial) as well as other specialty

therapeutic segments such as ENT, gastroenterology, orthopaedic, male erectile dysfunction, musculoskeletal as

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

10

Brief Rationale

well as OTC segments. The manufacturing operations spans around five (four in Maharashtra (India) - managed by

APL and one in Mauritius-managed by its wholly owned subsidiary APML) manufacturing plants and a state-of-the-

art R&D centre under the name of “Advent” at Mumbai. During FY14, the company derived around 64% of its

overall revenues from export markets i.e. primarily from emerging markets such as Africa, Asia (excluding India)

etc. and remaining comes from domestic market.

As per FY14, APL posted a PAT of Rs.220.86 crore (FY13 – Rs 101.12 crore) on a total income of Rs.1,126.09 crore

(FY13 – Rs.846.08 crore). Furthermore, during Q1FY15 (un-audited), the company posted PAT of Rs.58.72 crore

(Q1FY14 – Rs 32.54 crore) on a total income of Rs.287.60 crore (Q1FY14 – Rs.220.99 crore).

Analyst Contact Name: Mr. Ravi.kumar Dasari

Tel: 022-67543421

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

11

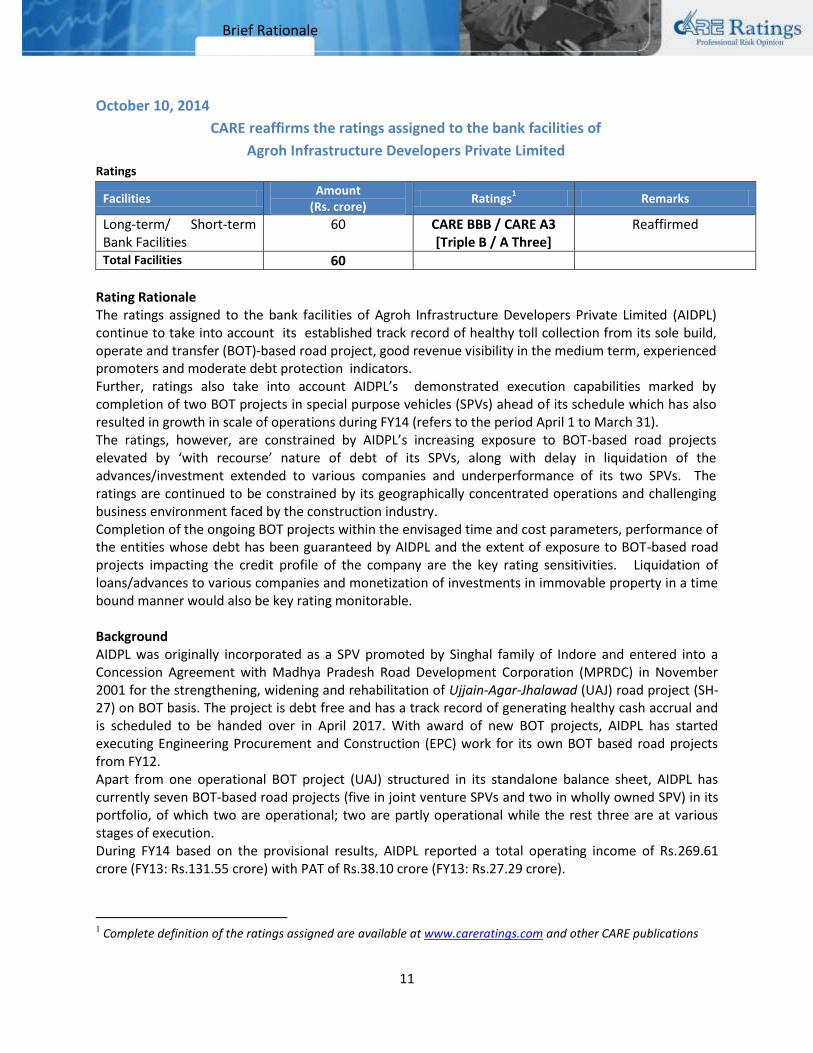

Brief Rationale

October 10, 2014

CARE reaffirms the ratings assigned to the bank facilities of

Agroh Infrastructure Developers Private Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long-term/ Short-term Bank Facilities

60 CARE BBB / CARE A3 [Triple B / A Three]

Reaffirmed

Total Facilities 60

Rating Rationale The ratings assigned to the bank facilities of Agroh Infrastructure Developers Private Limited (AIDPL) continue to take into account its established track record of healthy toll collection from its sole build, operate and transfer (BOT)-based road project, good revenue visibility in the medium term, experienced promoters and moderate debt protection indicators. Further, ratings also take into account AIDPL’s demonstrated execution capabilities marked by completion of two BOT projects in special purpose vehicles (SPVs) ahead of its schedule which has also resulted in growth in scale of operations during FY14 (refers to the period April 1 to March 31). The ratings, however, are constrained by AIDPL’s increasing exposure to BOT-based road projects elevated by ‘with recourse’ nature of debt of its SPVs, along with delay in liquidation of the advances/investment extended to various companies and underperformance of its two SPVs. The ratings are continued to be constrained by its geographically concentrated operations and challenging business environment faced by the construction industry. Completion of the ongoing BOT projects within the envisaged time and cost parameters, performance of the entities whose debt has been guaranteed by AIDPL and the extent of exposure to BOT-based road projects impacting the credit profile of the company are the key rating sensitivities. Liquidation of loans/advances to various companies and monetization of investments in immovable property in a time bound manner would also be key rating monitorable. Background AIDPL was originally incorporated as a SPV promoted by Singhal family of Indore and entered into a Concession Agreement with Madhya Pradesh Road Development Corporation (MPRDC) in November 2001 for the strengthening, widening and rehabilitation of Ujjain-Agar-Jhalawad (UAJ) road project (SH-27) on BOT basis. The project is debt free and has a track record of generating healthy cash accrual and is scheduled to be handed over in April 2017. With award of new BOT projects, AIDPL has started executing Engineering Procurement and Construction (EPC) work for its own BOT based road projects from FY12. Apart from one operational BOT project (UAJ) structured in its standalone balance sheet, AIDPL has currently seven BOT-based road projects (five in joint venture SPVs and two in wholly owned SPV) in its portfolio, of which two are operational; two are partly operational while the rest three are at various stages of execution. During FY14 based on the provisional results, AIDPL reported a total operating income of Rs.269.61 crore (FY13: Rs.131.55 crore) with PAT of Rs.38.10 crore (FY13: Rs.27.29 crore).

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

12

Brief Rationale

Analyst Contact

Name: Maulesh Desai

Tel # 079-40265605

Mobile # +91 9925139180

Email:[email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the amount and type of bank facilities/instruments. In case of partnership/proprietary concerns, the rating assigned by CARE is based on the capital deployed by the partners/proprietor and the financial strength of the firm at present. The rating may undergo change in case of withdrawal of capital or the unsecured loans brought in by the partners/proprietor in addition to the financial performance and other relevant factors.

13

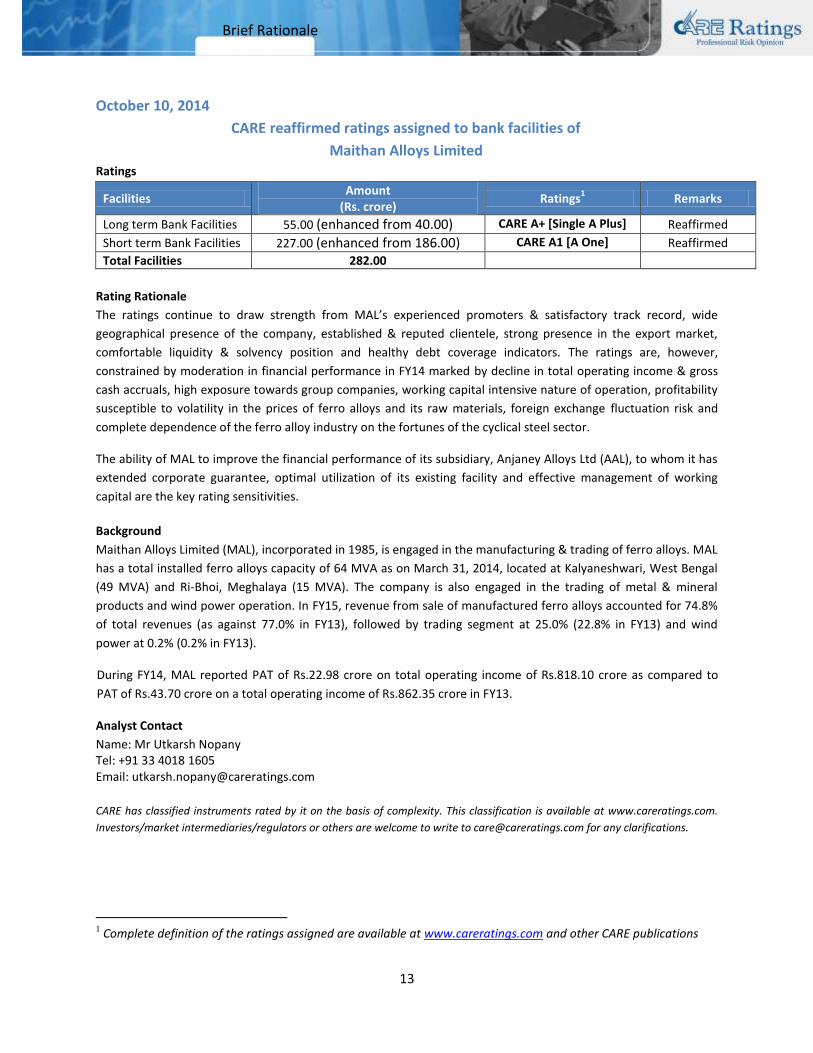

Brief Rationale

October 10, 2014

CARE reaffirmed ratings assigned to bank facilities of

Maithan Alloys Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 55.00 (enhanced from 40.00) CARE A+ [Single A Plus] Reaffirmed

Short term Bank Facilities 227.00 (enhanced from 186.00) CARE A1 [A One] Reaffirmed

Total Facilities 282.00

Rating Rationale

The ratings continue to draw strength from MAL’s experienced promoters & satisfactory track record, wide

geographical presence of the company, established & reputed clientele, strong presence in the export market,

comfortable liquidity & solvency position and healthy debt coverage indicators. The ratings are, however,

constrained by moderation in financial performance in FY14 marked by decline in total operating income & gross

cash accruals, high exposure towards group companies, working capital intensive nature of operation, profitability

susceptible to volatility in the prices of ferro alloys and its raw materials, foreign exchange fluctuation risk and

complete dependence of the ferro alloy industry on the fortunes of the cyclical steel sector.

The ability of MAL to improve the financial performance of its subsidiary, Anjaney Alloys Ltd (AAL), to whom it has

extended corporate guarantee, optimal utilization of its existing facility and effective management of working

capital are the key rating sensitivities.

Background

Maithan Alloys Limited (MAL), incorporated in 1985, is engaged in the manufacturing & trading of ferro alloys. MAL

has a total installed ferro alloys capacity of 64 MVA as on March 31, 2014, located at Kalyaneshwari, West Bengal

(49 MVA) and Ri-Bhoi, Meghalaya (15 MVA). The company is also engaged in the trading of metal & mineral

products and wind power operation. In FY15, revenue from sale of manufactured ferro alloys accounted for 74.8%

of total revenues (as against 77.0% in FY13), followed by trading segment at 25.0% (22.8% in FY13) and wind

power at 0.2% (0.2% in FY13).

During FY14, MAL reported PAT of Rs.22.98 crore on total operating income of Rs.818.10 crore as compared to

PAT of Rs.43.70 crore on a total operating income of Rs.862.35 crore in FY13.

Analyst Contact

Name: Mr Utkarsh Nopany Tel: +91 33 4018 1605 Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

14

Brief Rationale

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

15

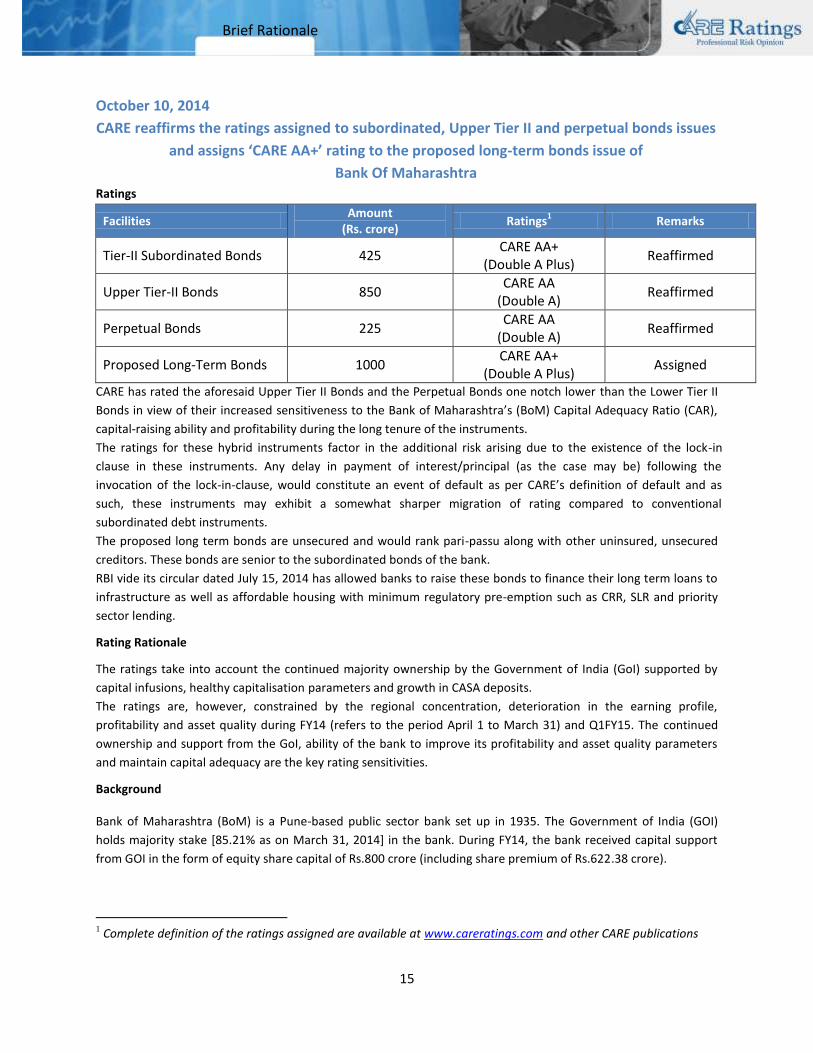

Brief Rationale

October 10, 2014

CARE reaffirms the ratings assigned to subordinated, Upper Tier II and perpetual bonds issues

and assigns ‘CARE AA+’ rating to the proposed long-term bonds issue of

Bank Of Maharashtra Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Tier-II Subordinated Bonds 425 CARE AA+

(Double A Plus) Reaffirmed

Upper Tier-II Bonds 850 CARE AA

(Double A) Reaffirmed

Perpetual Bonds 225 CARE AA

(Double A) Reaffirmed

Proposed Long-Term Bonds 1000 CARE AA+

(Double A Plus) Assigned

CARE has rated the aforesaid Upper Tier II Bonds and the Perpetual Bonds one notch lower than the Lower Tier II

Bonds in view of their increased sensitiveness to the Bank of Maharashtra’s (BoM) Capital Adequacy Ratio (CAR),

capital-raising ability and profitability during the long tenure of the instruments.

The ratings for these hybrid instruments factor in the additional risk arising due to the existence of the lock-in

clause in these instruments. Any delay in payment of interest/principal (as the case may be) following the

invocation of the lock-in-clause, would constitute an event of default as per CARE’s definition of default and as

such, these instruments may exhibit a somewhat sharper migration of rating compared to conventional

subordinated debt instruments.

The proposed long term bonds are unsecured and would rank pari-passu along with other uninsured, unsecured

creditors. These bonds are senior to the subordinated bonds of the bank.

RBI vide its circular dated July 15, 2014 has allowed banks to raise these bonds to finance their long term loans to

infrastructure as well as affordable housing with minimum regulatory pre-emption such as CRR, SLR and priority

sector lending.

Rating Rationale

The ratings take into account the continued majority ownership by the Government of India (GoI) supported by

capital infusions, healthy capitalisation parameters and growth in CASA deposits.

The ratings are, however, constrained by the regional concentration, deterioration in the earning profile,

profitability and asset quality during FY14 (refers to the period April 1 to March 31) and Q1FY15. The continued

ownership and support from the GoI, ability of the bank to improve its profitability and asset quality parameters

and maintain capital adequacy are the key rating sensitivities.

Background

Bank of Maharashtra (BoM) is a Pune-based public sector bank set up in 1935. The Government of India (GOI)

holds majority stake [85.21% as on March 31, 2014] in the bank. During FY14, the bank received capital support

from GOI in the form of equity share capital of Rs.800 crore (including share premium of Rs.622.38 crore).

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

16

Brief Rationale

The bank had a network of 1,890 branches and 1,827 ATMs as on March 31, 2014 with nearly 62% of the branches

in the state of Maharashtra. About 58% of the branches are in rural and semi-urban areas. All the branches of the

bank are Core Banking Solution (CBS) enabled.

During FY14, the bank’s deposits and advances grew by 23.81% and 17.82%, respectively. The total income for

FY14 grew 22.09% to Rs.12,851 crore The Net Interest Income (NII) grew by y-o-y 11.60% in FY14. During the year,

the CASA remained at healthy level at 35.89% of the total deposits. The gross NPA ratio and net NPA ratio stood at

3.18% and 2.03%. BoM reported a Capital Adequacy Ratio (as per Basel III) of 10.79% (Tier I – 7.44%) as on March

31, 2014.

In Q1FY15 (refers to the period April 1 to June 30), the bank reported a PAT of Rs.117.82 crore on a total income of

Rs.3286.12 crore. The asset quality has deteriorated moderately compared with March 2014 with gross NPA at

4.23% and net NPA at 2.94%. The Total Capital Adequacy Ratio remained at 10.75% and Tier-I CAR at 7.42% as on

June 30, 2014. CASA deteriorated to 34.01% as on June 30, 2014.

Analyst Contact

Name: Leena Marne

Tel: 020-40009019

Mobile: 7738003771

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

17

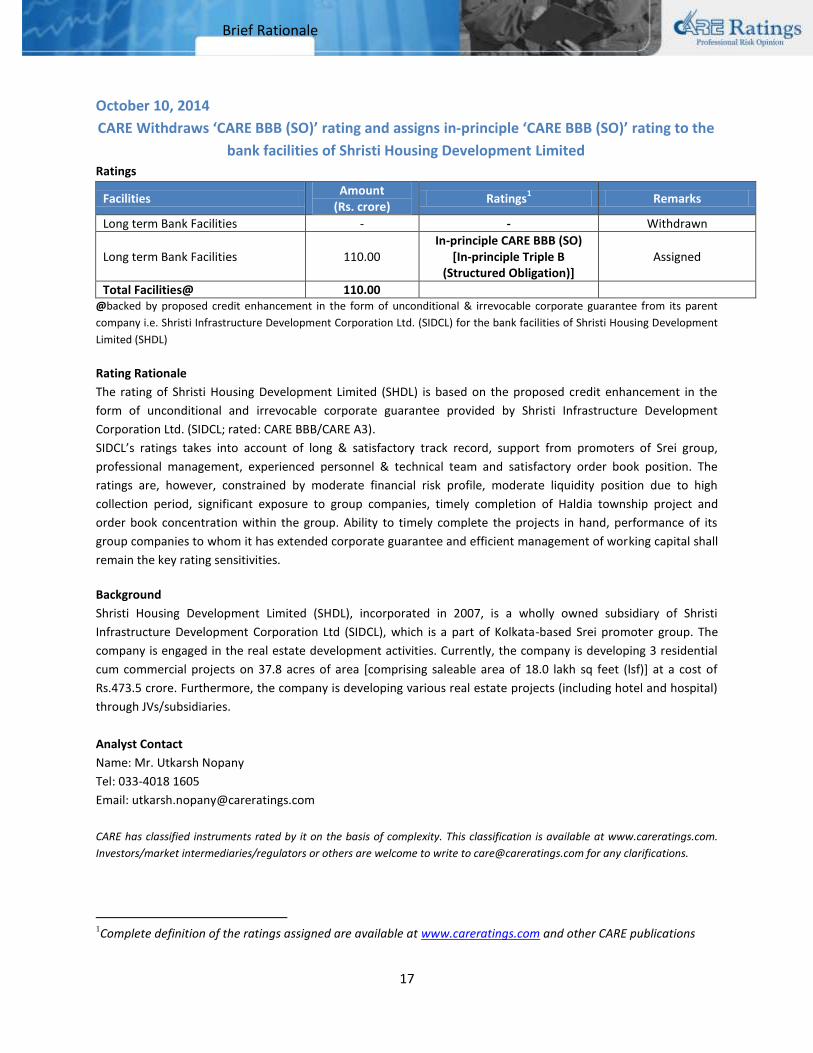

Brief Rationale

October 10, 2014

CARE Withdraws ‘CARE BBB (SO)’ rating and assigns in-principle ‘CARE BBB (SO)’ rating to the

bank facilities of Shristi Housing Development Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities - - Withdrawn

Long term Bank Facilities 110.00 In-principle CARE BBB (SO)

[In-principle Triple B (Structured Obligation)]

Assigned

Total Facilities@ 110.00 @backed by proposed credit enhancement in the form of unconditional & irrevocable corporate guarantee from its parent

company i.e. Shristi Infrastructure Development Corporation Ltd. (SIDCL) for the bank facilities of Shristi Housing Development

Limited (SHDL)

Rating Rationale

The rating of Shristi Housing Development Limited (SHDL) is based on the proposed credit enhancement in the

form of unconditional and irrevocable corporate guarantee provided by Shristi Infrastructure Development

Corporation Ltd. (SIDCL; rated: CARE BBB/CARE A3).

SIDCL’s ratings takes into account of long & satisfactory track record, support from promoters of Srei group,

professional management, experienced personnel & technical team and satisfactory order book position. The

ratings are, however, constrained by moderate financial risk profile, moderate liquidity position due to high

collection period, significant exposure to group companies, timely completion of Haldia township project and

order book concentration within the group. Ability to timely complete the projects in hand, performance of its

group companies to whom it has extended corporate guarantee and efficient management of working capital shall

remain the key rating sensitivities.

Background

Shristi Housing Development Limited (SHDL), incorporated in 2007, is a wholly owned subsidiary of Shristi

Infrastructure Development Corporation Ltd (SIDCL), which is a part of Kolkata-based Srei promoter group. The

company is engaged in the real estate development activities. Currently, the company is developing 3 residential

cum commercial projects on 37.8 acres of area [comprising saleable area of 18.0 lakh sq feet (lsf)] at a cost of

Rs.473.5 crore. Furthermore, the company is developing various real estate projects (including hotel and hospital)

through JVs/subsidiaries.

Analyst Contact

Name: Mr. Utkarsh Nopany

Tel: 033-4018 1605

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

1Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

18

Brief Rationale

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

19

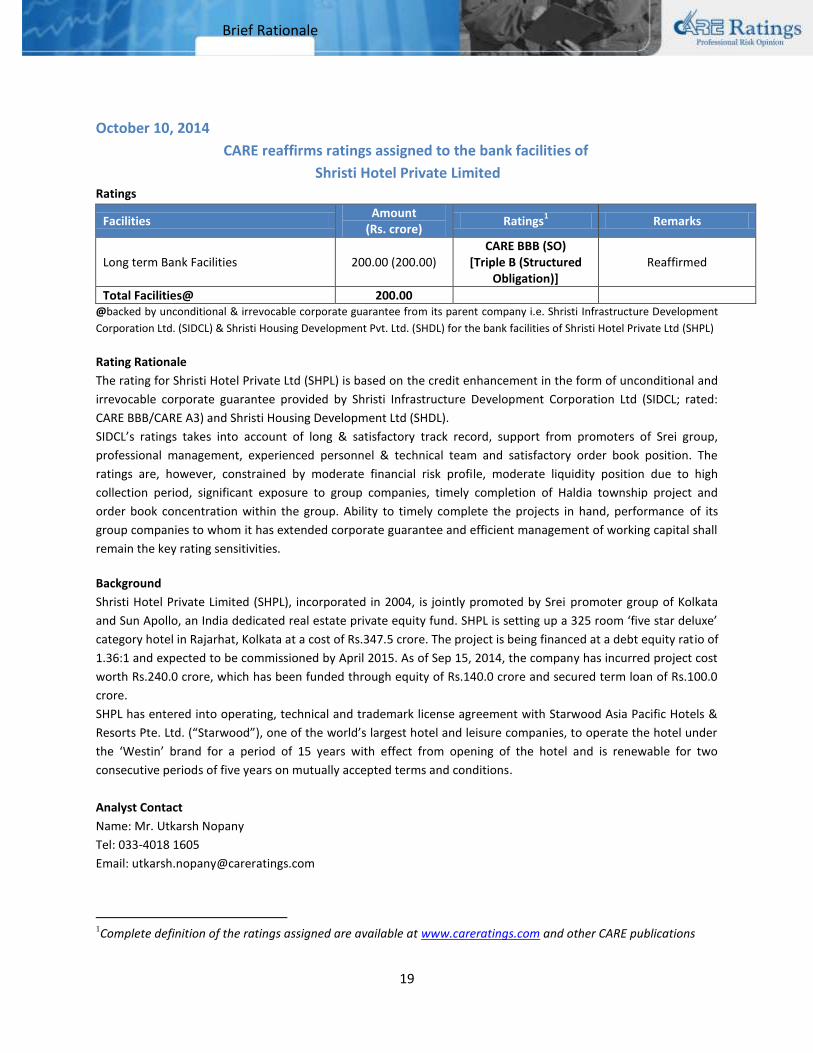

Brief Rationale

October 10, 2014

CARE reaffirms ratings assigned to the bank facilities of

Shristi Hotel Private Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 200.00 (200.00) CARE BBB (SO)

[Triple B (Structured Obligation)]

Reaffirmed

Total Facilities@ 200.00 @backed by unconditional & irrevocable corporate guarantee from its parent company i.e. Shristi Infrastructure Development

Corporation Ltd. (SIDCL) & Shristi Housing Development Pvt. Ltd. (SHDL) for the bank facilities of Shristi Hotel Private Ltd (SHPL)

Rating Rationale

The rating for Shristi Hotel Private Ltd (SHPL) is based on the credit enhancement in the form of unconditional and

irrevocable corporate guarantee provided by Shristi Infrastructure Development Corporation Ltd (SIDCL; rated:

CARE BBB/CARE A3) and Shristi Housing Development Ltd (SHDL).

SIDCL’s ratings takes into account of long & satisfactory track record, support from promoters of Srei group,

professional management, experienced personnel & technical team and satisfactory order book position. The

ratings are, however, constrained by moderate financial risk profile, moderate liquidity position due to high

collection period, significant exposure to group companies, timely completion of Haldia township project and

order book concentration within the group. Ability to timely complete the projects in hand, performance of its

group companies to whom it has extended corporate guarantee and efficient management of working capital shall

remain the key rating sensitivities.

Background

Shristi Hotel Private Limited (SHPL), incorporated in 2004, is jointly promoted by Srei promoter group of Kolkata

and Sun Apollo, an India dedicated real estate private equity fund. SHPL is setting up a 325 room ‘five star deluxe’

category hotel in Rajarhat, Kolkata at a cost of Rs.347.5 crore. The project is being financed at a debt equity ratio of

1.36:1 and expected to be commissioned by April 2015. As of Sep 15, 2014, the company has incurred project cost

worth Rs.240.0 crore, which has been funded through equity of Rs.140.0 crore and secured term loan of Rs.100.0

crore.

SHPL has entered into operating, technical and trademark license agreement with Starwood Asia Pacific Hotels &

Resorts Pte. Ltd. (“Starwood”), one of the world’s largest hotel and leisure companies, to operate the hotel under

the ‘Westin’ brand for a period of 15 years with effect from opening of the hotel and is renewable for two

consecutive periods of five years on mutually accepted terms and conditions.

Analyst Contact

Name: Mr. Utkarsh Nopany

Tel: 033-4018 1605

Email: [email protected]

1Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

20

Brief Rationale

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

21

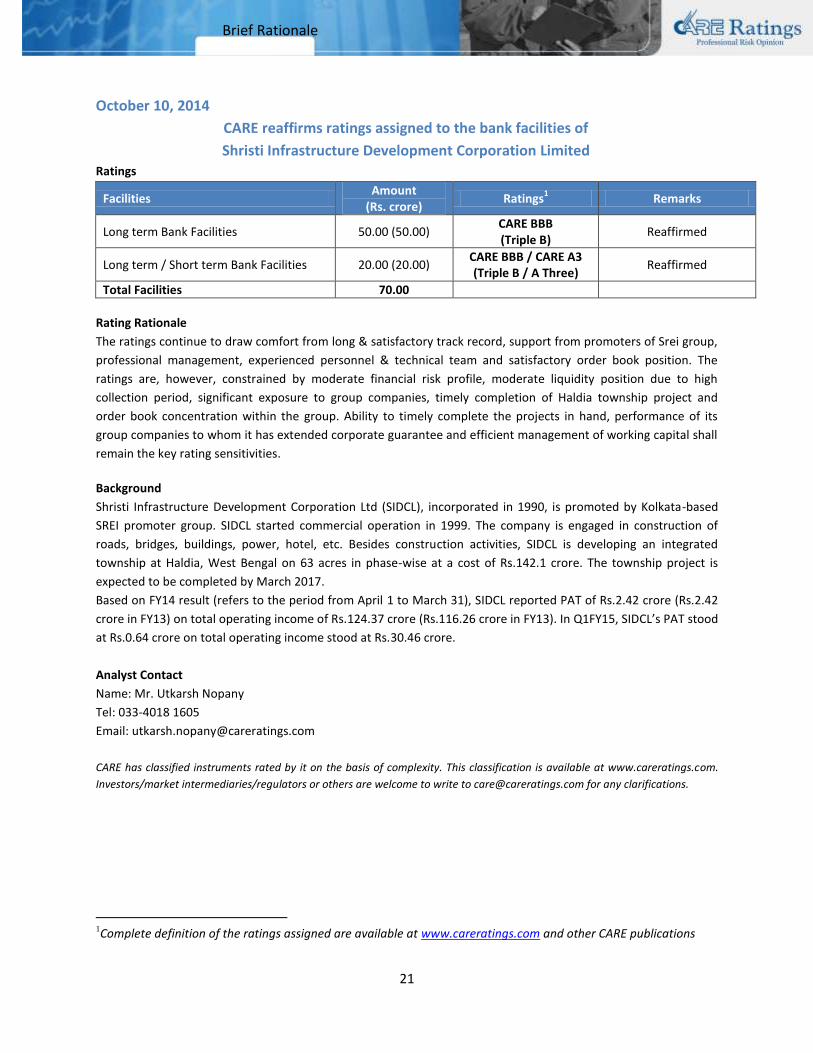

Brief Rationale

October 10, 2014

CARE reaffirms ratings assigned to the bank facilities of

Shristi Infrastructure Development Corporation Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 50.00 (50.00) CARE BBB (Triple B)

Reaffirmed

Long term / Short term Bank Facilities 20.00 (20.00) CARE BBB / CARE A3 (Triple B / A Three)

Reaffirmed

Total Facilities 70.00

Rating Rationale

The ratings continue to draw comfort from long & satisfactory track record, support from promoters of Srei group,

professional management, experienced personnel & technical team and satisfactory order book position. The

ratings are, however, constrained by moderate financial risk profile, moderate liquidity position due to high

collection period, significant exposure to group companies, timely completion of Haldia township project and

order book concentration within the group. Ability to timely complete the projects in hand, performance of its

group companies to whom it has extended corporate guarantee and efficient management of working capital shall

remain the key rating sensitivities.

Background

Shristi Infrastructure Development Corporation Ltd (SIDCL), incorporated in 1990, is promoted by Kolkata-based

SREI promoter group. SIDCL started commercial operation in 1999. The company is engaged in construction of

roads, bridges, buildings, power, hotel, etc. Besides construction activities, SIDCL is developing an integrated

township at Haldia, West Bengal on 63 acres in phase-wise at a cost of Rs.142.1 crore. The township project is

expected to be completed by March 2017.

Based on FY14 result (refers to the period from April 1 to March 31), SIDCL reported PAT of Rs.2.42 crore (Rs.2.42

crore in FY13) on total operating income of Rs.124.37 crore (Rs.116.26 crore in FY13). In Q1FY15, SIDCL’s PAT stood

at Rs.0.64 crore on total operating income stood at Rs.30.46 crore.

Analyst Contact

Name: Mr. Utkarsh Nopany

Tel: 033-4018 1605

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

1Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

22

Brief Rationale

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

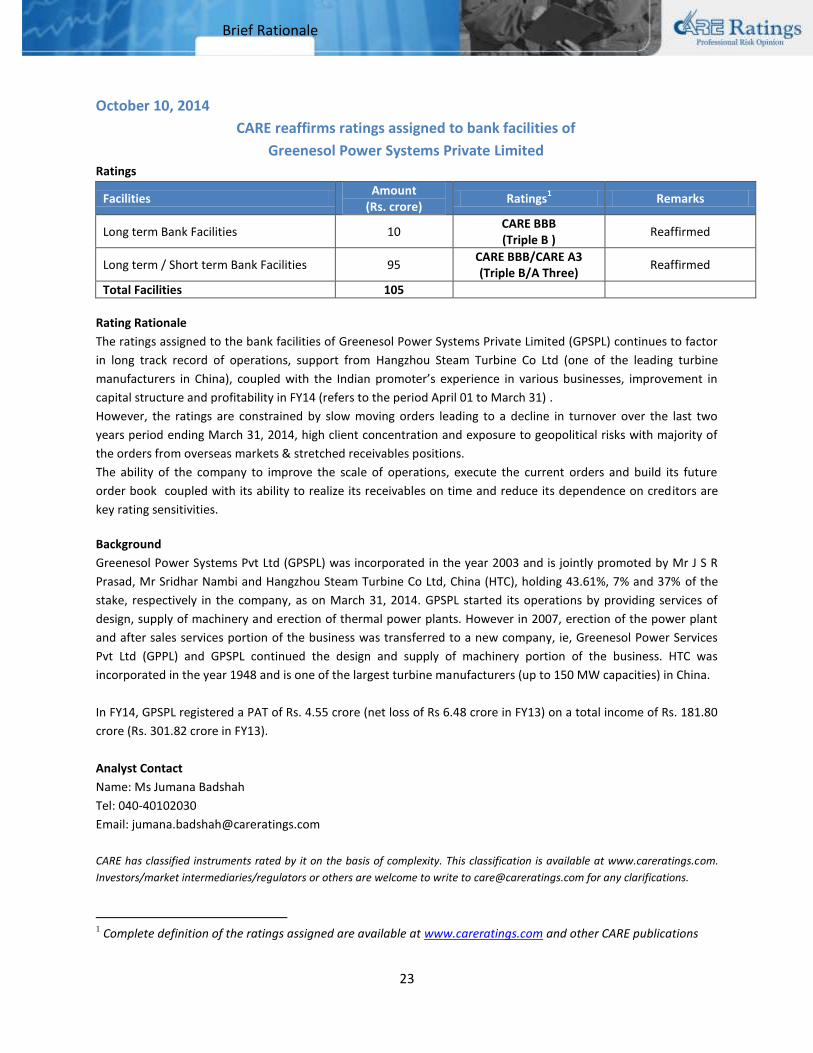

23

Brief Rationale

October 10, 2014

CARE reaffirms ratings assigned to bank facilities of

Greenesol Power Systems Private Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 10 CARE BBB (Triple B )

Reaffirmed

Long term / Short term Bank Facilities 95 CARE BBB/CARE A3 (Triple B/A Three)

Reaffirmed

Total Facilities 105

Rating Rationale

The ratings assigned to the bank facilities of Greenesol Power Systems Private Limited (GPSPL) continues to factor

in long track record of operations, support from Hangzhou Steam Turbine Co Ltd (one of the leading turbine

manufacturers in China), coupled with the Indian promoter’s experience in various businesses, improvement in

capital structure and profitability in FY14 (refers to the period April 01 to March 31) .

However, the ratings are constrained by slow moving orders leading to a decline in turnover over the last two

years period ending March 31, 2014, high client concentration and exposure to geopolitical risks with majority of

the orders from overseas markets & stretched receivables positions.

The ability of the company to improve the scale of operations, execute the current orders and build its future

order book coupled with its ability to realize its receivables on time and reduce its dependence on creditors are

key rating sensitivities.

Background

Greenesol Power Systems Pvt Ltd (GPSPL) was incorporated in the year 2003 and is jointly promoted by Mr J S R

Prasad, Mr Sridhar Nambi and Hangzhou Steam Turbine Co Ltd, China (HTC), holding 43.61%, 7% and 37% of the

stake, respectively in the company, as on March 31, 2014. GPSPL started its operations by providing services of

design, supply of machinery and erection of thermal power plants. However in 2007, erection of the power plant

and after sales services portion of the business was transferred to a new company, ie, Greenesol Power Services

Pvt Ltd (GPPL) and GPSPL continued the design and supply of machinery portion of the business. HTC was

incorporated in the year 1948 and is one of the largest turbine manufacturers (up to 150 MW capacities) in China.

In FY14, GPSPL registered a PAT of Rs. 4.55 crore (net loss of Rs 6.48 crore in FY13) on a total income of Rs. 181.80

crore (Rs. 301.82 crore in FY13).

Analyst Contact

Name: Ms Jumana Badshah

Tel: 040-40102030

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

24

Brief Rationale

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

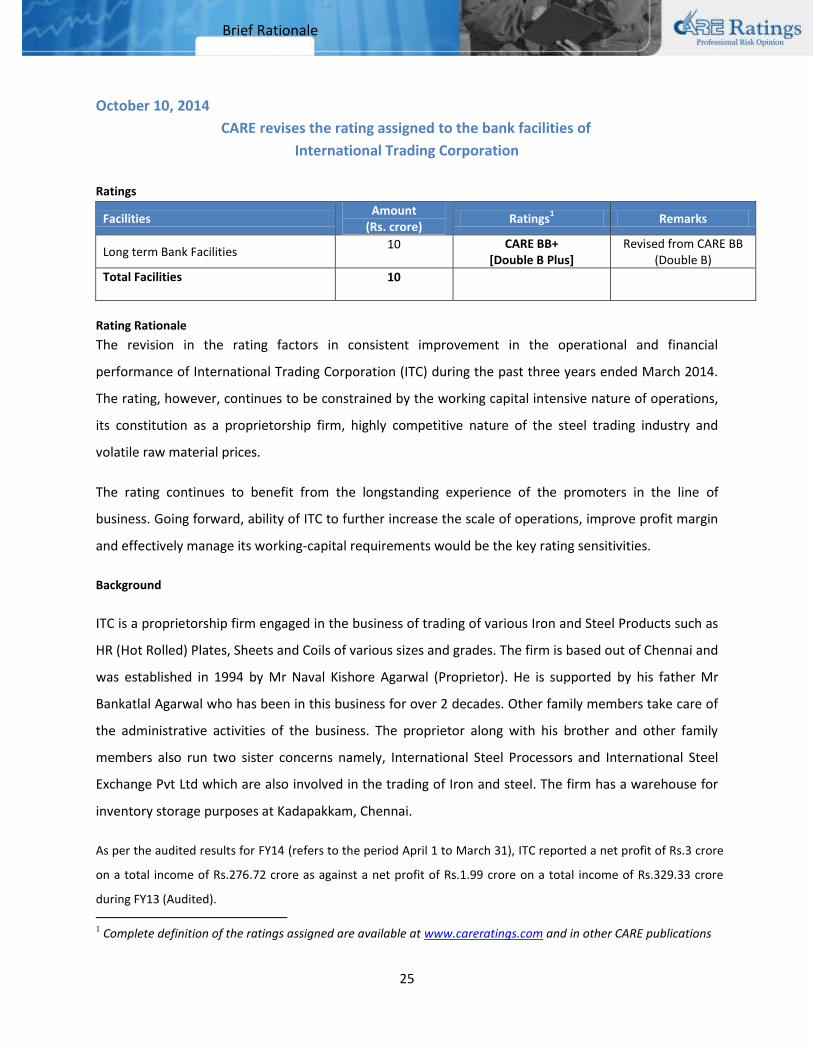

25

Brief Rationale

October 10, 2014

CARE revises the rating assigned to the bank facilities of

International Trading Corporation

Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 10 CARE BB+

[Double B Plus] Revised from CARE BB

(Double B)

Total Facilities 10

Rating Rationale

The revision in the rating factors in consistent improvement in the operational and financial

performance of International Trading Corporation (ITC) during the past three years ended March 2014.

The rating, however, continues to be constrained by the working capital intensive nature of operations,

its constitution as a proprietorship firm, highly competitive nature of the steel trading industry and

volatile raw material prices.

The rating continues to benefit from the longstanding experience of the promoters in the line of

business. Going forward, ability of ITC to further increase the scale of operations, improve profit margin

and effectively manage its working-capital requirements would be the key rating sensitivities.

Background

ITC is a proprietorship firm engaged in the business of trading of various Iron and Steel Products such as

HR (Hot Rolled) Plates, Sheets and Coils of various sizes and grades. The firm is based out of Chennai and

was established in 1994 by Mr Naval Kishore Agarwal (Proprietor). He is supported by his father Mr

Bankatlal Agarwal who has been in this business for over 2 decades. Other family members take care of

the administrative activities of the business. The proprietor along with his brother and other family

members also run two sister concerns namely, International Steel Processors and International Steel

Exchange Pvt Ltd which are also involved in the trading of Iron and steel. The firm has a warehouse for

inventory storage purposes at Kadapakkam, Chennai.

As per the audited results for FY14 (refers to the period April 1 to March 31), ITC reported a net profit of Rs.3 crore

on a total income of Rs.276.72 crore as against a net profit of Rs.1.99 crore on a total income of Rs.329.33 crore

during FY13 (Audited).

1 Complete definition of the ratings assigned are available at www.careratings.com and in other CARE publications

26

Brief Rationale

Analyst Contact

Name: Harihara Subramanian C

Tel: 044-28490876

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

In case of partnership/proprietary concerns, the rating assigned by CARE is based on the capital deployed by the

partners/proprietor and the financial strength of the firm at present. The rating may undergo change in case of withdrawal of

capital or the unsecured loans brought in by the partners/proprietor in addition to the financial performance and other relevant

factors.

27

Brief Rationale

October 10, 2014

CARE revises ratings assigned to bank facilities of

ACE Tyres Limited Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long term Bank Facilities 41.92

(reduced from 46) CARE A-

(Single A Minus) Revised from CARE BBB

[Triple B]

Short term Bank Facilities 6.63 CARE A2 (A Two)

Revised from CARE A3 [A Three]

Total Facilities 48.55

Rating Rationale

The revision in the ratings assigned to the bank facilities of Ace Tyres Limited (ATL) reflects its improved financial

and operational performance during FY14 (refers to the period April 01 to March 31), and successful completion of

major expansion plan which increased installed capacity leading to higher volumes in FY14. The company was also

able to get higher conversion rates from its clients in FY14.

The ratings continue to derive strength from experienced promoters and long track record of the group in the tyre

industry, long-term off-take agreement with its major client and established relationship with major tyre

manufacturers. The ratings are however constrained by relatively small scale of operations due to low value added

job work and high client concentration risk.

The ability of the company to pass on increase in the costs, ensure increased off-take from the existing clients,

acquire new clients to reduce concentration risk, and further rationalize its debt thereby improving its capital

structure would be the key rating sensitivities.

Background

ATL incorporated in August, 2001 belongs to Hyderabad-based Exel Group. The group is into manufacturing of

automotive tubes, tyres, flaps & bladder, since inception in 1987. ATL is primarily engaged in manufacturing of

automotive tyres (two wheelers, three wheelers) on job work basis. ATL has two manufacturing plants on the

outskirts of Hyderabad. The company commenced operations initially by manufacturing only two and three

wheeler tyres on conversion basis for CEAT Ltd (rated CARE A/CARE A1). ATL completed a major expansion which

increased the manufacturing capacity from 24,000 MT/year in FY12 to 48,000 MT/year in FY14.

Analyst Contact

Name: Ms Jumana Badshah

Tel: 040-40102030

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

28

Brief Rationale

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

29

Brief Rationale

October 10, 2014

CARE revises the ratings assigned to bank facilities of

AHW Steels Ltd Ratings

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long-term Bank Facilities 75 ‘CARE BBB-’ (Triple B Minus) Revised from CARE BB+

(Double B Plus)

Short-term Bank Facilities 5 ‘CARE A3’ (A Three) Revised from CARE A4+

(A Four Plus )

Long-term Bank Facilities - - Withdrawn

Total Facilities 80

Rating Rationale

The revision in the ratings of AHW Steels Ltd. (AHW) takes into account the consistent increase in scale of

operation over the last three fiscals with relatively stable profit margins and comfortable capital structure. The

ratings continue to draw strength from the experience of the promoters, long track record of operation and

established network of suppliers and customers. The ratings are, however, constrained by the company’s thin

profitability margins as well as exposure of the company’s profitability to volatility in the prices of traded products,

high working capital intensity of the operations and intense competition. Improving profitability margins,

maintaining capital structure and effective management of working capital would remain the key rating

sensitivities.

Background

AHW was promoted in 1941 by the Beriwal family and was engaged in manufacturing of tor steel. The Bagaria

family of Kolkata took over the company in 1982 and since then AHW is a part of the Bagaria group, which has

interests in tea plantations, steel, power and real estate sectors. AHW, the steel company of the group, began

rolling mill operation in 1985 and has a capacity of 48,000 tpa (tonne per annum) for rolled products. However, the

rolling mill has been mostly non-operational since January 2012 due to unviable operation on account of high raw

material cost and almost the entire operating income in FY14 is derived from trading in wire rods, TMT bars &

other steel products.

The company currently has two wind turbine generators, with a total power generation capacity of 2.5 megawatts,

in Maharashtra.

In FY14 AHW achieved PAT of Rs.2.19 crore on net sales of Rs.580.24 crore. The company achieved net sales of

Rs.141 crore in Q1FY15.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

30

Brief Rationale

Analyst Contact

Name: Mamta Muklania Tel: 033-4018 1600 Mobile: 98304 07120 Email: [email protected] CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

31

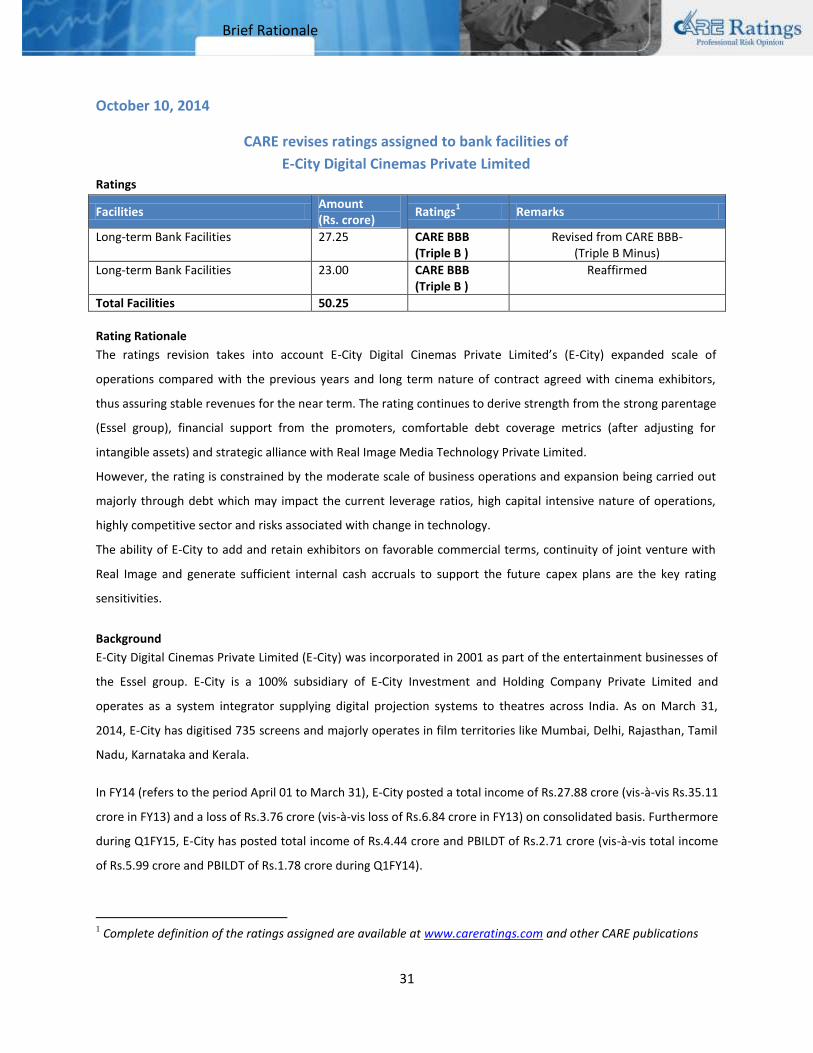

Brief Rationale

October 10, 2014

CARE revises ratings assigned to bank facilities of

E-City Digital Cinemas Private Limited Ratings

Facilities Amount (Rs. crore)

Ratings1 Remarks

Long-term Bank Facilities 27.25 CARE BBB (Triple B )

Revised from CARE BBB- (Triple B Minus)

Long-term Bank Facilities 23.00 CARE BBB (Triple B )

Reaffirmed

Total Facilities 50.25

Rating Rationale

The ratings revision takes into account E-City Digital Cinemas Private Limited’s (E-City) expanded scale of

operations compared with the previous years and long term nature of contract agreed with cinema exhibitors,

thus assuring stable revenues for the near term. The rating continues to derive strength from the strong parentage

(Essel group), financial support from the promoters, comfortable debt coverage metrics (after adjusting for

intangible assets) and strategic alliance with Real Image Media Technology Private Limited.

However, the rating is constrained by the moderate scale of business operations and expansion being carried out

majorly through debt which may impact the current leverage ratios, high capital intensive nature of operations,

highly competitive sector and risks associated with change in technology.

The ability of E-City to add and retain exhibitors on favorable commercial terms, continuity of joint venture with

Real Image and generate sufficient internal cash accruals to support the future capex plans are the key rating

sensitivities.

Background

E-City Digital Cinemas Private Limited (E-City) was incorporated in 2001 as part of the entertainment businesses of

the Essel group. E-City is a 100% subsidiary of E-City Investment and Holding Company Private Limited and

operates as a system integrator supplying digital projection systems to theatres across India. As on March 31,

2014, E-City has digitised 735 screens and majorly operates in film territories like Mumbai, Delhi, Rajasthan, Tamil

Nadu, Karnataka and Kerala.

In FY14 (refers to the period April 01 to March 31), E-City posted a total income of Rs.27.88 crore (vis-à-vis Rs.35.11

crore in FY13) and a loss of Rs.3.76 crore (vis-à-vis loss of Rs.6.84 crore in FY13) on consolidated basis. Furthermore

during Q1FY15, E-City has posted total income of Rs.4.44 crore and PBILDT of Rs.2.71 crore (vis-à-vis total income

of Rs.5.99 crore and PBILDT of Rs.1.78 crore during Q1FY14).

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

32

Brief Rationale

Analyst Contact Name: Ms. Savita Iyer Tel # 022 6754 3406 Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

33

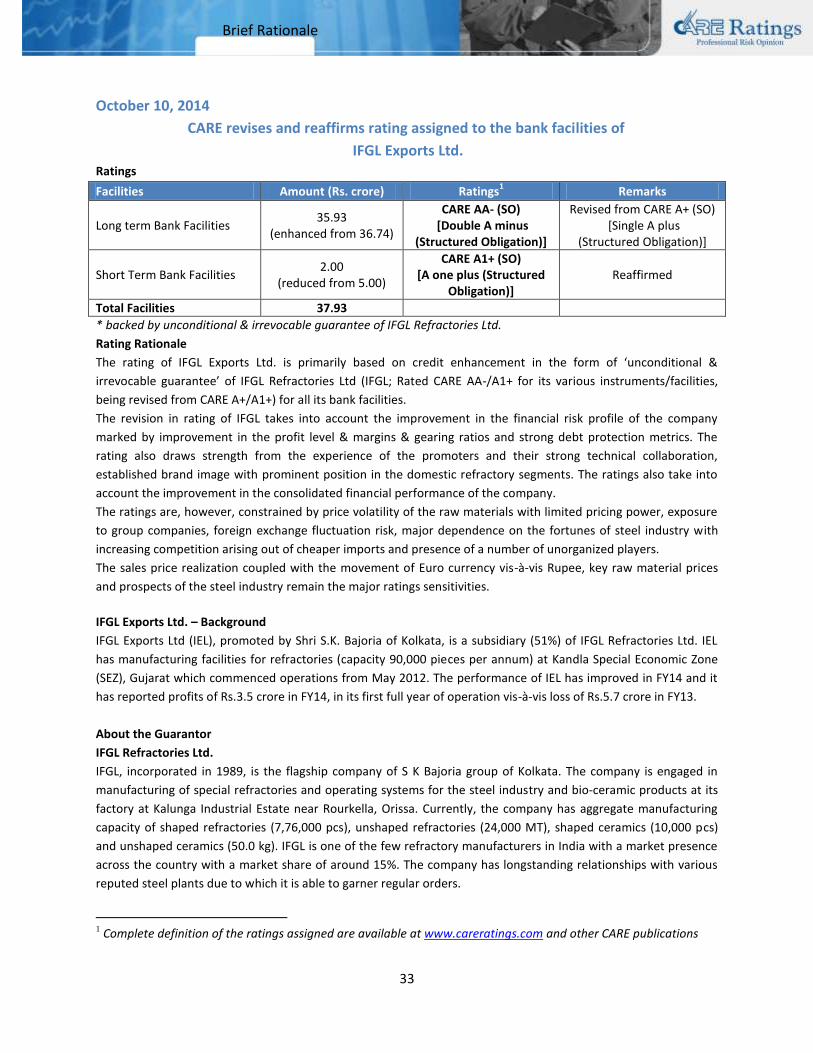

Brief Rationale

October 10, 2014

CARE revises and reaffirms rating assigned to the bank facilities of

IFGL Exports Ltd. Ratings

Facilities Amount (Rs. crore) Ratings1 Remarks

Long term Bank Facilities 35.93

(enhanced from 36.74)

CARE AA- (SO) [Double A minus

(Structured Obligation)]

Revised from CARE A+ (SO) [Single A plus

(Structured Obligation)]

Short Term Bank Facilities 2.00

(reduced from 5.00)

CARE A1+ (SO) [A one plus (Structured

Obligation)] Reaffirmed

Total Facilities 37.93

* backed by unconditional & irrevocable guarantee of IFGL Refractories Ltd.

Rating Rationale

The rating of IFGL Exports Ltd. is primarily based on credit enhancement in the form of ‘unconditional &

irrevocable guarantee’ of IFGL Refractories Ltd (IFGL; Rated CARE AA-/A1+ for its various instruments/facilities,

being revised from CARE A+/A1+) for all its bank facilities.

The revision in rating of IFGL takes into account the improvement in the financial risk profile of the company

marked by improvement in the profit level & margins & gearing ratios and strong debt protection metrics. The

rating also draws strength from the experience of the promoters and their strong technical collaboration,

established brand image with prominent position in the domestic refractory segments. The ratings also take into

account the improvement in the consolidated financial performance of the company.

The ratings are, however, constrained by price volatility of the raw materials with limited pricing power, exposure

to group companies, foreign exchange fluctuation risk, major dependence on the fortunes of steel industry with

increasing competition arising out of cheaper imports and presence of a number of unorganized players.

The sales price realization coupled with the movement of Euro currency vis-à-vis Rupee, key raw material prices

and prospects of the steel industry remain the major ratings sensitivities.

IFGL Exports Ltd. – Background

IFGL Exports Ltd (IEL), promoted by Shri S.K. Bajoria of Kolkata, is a subsidiary (51%) of IFGL Refractories Ltd. IEL

has manufacturing facilities for refractories (capacity 90,000 pieces per annum) at Kandla Special Economic Zone

(SEZ), Gujarat which commenced operations from May 2012. The performance of IEL has improved in FY14 and it

has reported profits of Rs.3.5 crore in FY14, in its first full year of operation vis-à-vis loss of Rs.5.7 crore in FY13.

About the Guarantor

IFGL Refractories Ltd.

IFGL, incorporated in 1989, is the flagship company of S K Bajoria group of Kolkata. The company is engaged in

manufacturing of special refractories and operating systems for the steel industry and bio-ceramic products at its

factory at Kalunga Industrial Estate near Rourkella, Orissa. Currently, the company has aggregate manufacturing

capacity of shaped refractories (7,76,000 pcs), unshaped refractories (24,000 MT), shaped ceramics (10,000 pcs)

and unshaped ceramics (50.0 kg). IFGL is one of the few refractory manufacturers in India with a market presence

across the country with a market share of around 15%. The company has longstanding relationships with various

reputed steel plants due to which it is able to garner regular orders.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

34

Brief Rationale

IFGL earned PBILDT of Rs.45.0 crore and PAT (after defd. tax provision) of Rs.24.3 crore on Total Operating Income

of Rs.327.4 crore in FY14.

Analyst Contact

Name: Vineet Chamaria

Tel: 033-40181609

Mobile: +91 9051730850

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

In case of partnership/proprietary concerns, the rating assigned by CARE is based on the capital deployed by the

partners/proprietor and the financial strength of the firm at present. The rating may undergo change in case of withdrawal of

capital or the unsecured loans brought in by the partners/proprietor in addition to the financial performance and other relevant

factors.

35

Brief Rationale

October 10, 2014

CARE revises the ratings assigned to the bank facilities of Cl Gupta Exports Ltd

Rating

Facilities Amount

(Rs. crore) Ratings

1 Remarks

Long-term Bank Facilities 34.47

(14.42) CARE BBB (Triple B)

Revised from CARE BBB- (Triple B Minus)

Short-term Bank Facilities

70.25 (55.67)

CARE A3 (A Three) Reaffirmed

Total Facilities 104.72

Rating Rationale

The revision in the ratings of bank facilities of CL Gupta Exports Ltd (CLGEL) takes into account the improvement in

the company’s financial risk profile and profitability driven by its increasing scale of operations and backward

integration initiatives undertaken by it. The ratings continue to draw support from CLGEL’s experienced promoters

and its position as one of the leading exporters of the decorative and utility-based handicraft items with a

diversified product profile. The ratings also take into consideration the company’s long-standing association with

reputed international clientele and the government support to the handicraft industry.

However, the ratings are constrained by the working-capital intensive nature of the company’s operations,

susceptibility of the company’s operating margins to the fluctuation in raw material prices and foreign exchange

rates.

Going forward, the company’s ability to profitably scale up its operations while effectively managing its working

capital requirements and maintain a moderate capital structure shall remain the key rating sensitivities.

Background

CL Gupta Exports Ltd (CLGEL) was incorporated in March 2004. However, the commercial operation of the

company’s manufacturing unit commenced from April 2005. The company is primarily involved in the

manufacturing & export of handicraft/decorative items made of glass, wood and metals such as aluminum, brass,

steel and iron. Its manufacturing unit is situated in Moradabad (UP) having integrated facilities for processing

metal, glass and wood with in-house facilities for casting, pressing, spinning, welding, polishing and plating. Major

export destinations for CLGEL are the USA, European Union, China, Malaysia etc.

During FY14 (refers to the period April 1 to March 31), on a total operating income of Rs.225.33 crore, the

company reported a PBILDT and PAT of Rs.25.31 crore and Rs.8.26 crore, respectively. Furthermore, during

Q1FY15 (provisional) (refers to the period April 1 to June 30), the company has reported a PBILDT of Rs.6.69 crore

on a total operating income of Rs.53 crore.

1 Complete definition of the ratings assigned are available at www.careratings.com and other CARE publications

36

Brief Rationale

Analyst Contact

Name: Ajay Dhaka

Tel: 011-45333218

Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at www.careratings.com.

Investors/market intermediaries/regulators or others are welcome to write to [email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such

information. Most entities whose bank facilities/instruments are rated by CARE have paid a credit rating fee, based on the

amount and type of bank facilities/instruments.

In case of partnership/proprietary concerns, the rating assigned by CARE is based on the capital deployed by the

partners/proprietor and the financial strength of the firm at present. The rating may undergo change in case of withdrawal of

capital or the unsecured loans brought in by the partners/proprietor in addition to the financial performance and other relevant

factors.

37

Brief Rationale

October 10, 2014

CARE suspends the rating assigned to the bank facilities of

Unix Connections Private Limited

CARE has suspended, with immediate effect, the ratings assigned to the long- term bank facilities of Unix

Connections Private Limited. The ratings have been suspended as the company has not furnished the information

required by CARE for monitoring of the rating.

Analyst Contact

Name: Nitesh Dhoot

Tel: 022- 6754 3442 Email: [email protected]

CARE has classified instruments rated by it on the basis of complexity. This classification is available at

www.careratings.com. Investors/market intermediaries/regulators or others are welcome to write to

[email protected] for any clarifications.

Disclaimer: CARE’s ratings are opinions on credit quality and are not recommendations to sanction, renew, disburse or recall

the concerned bank facilities or to buy, sell or hold any security. CARE has based its ratings on information obtained from

sources believed by it to be accurate and reliable. CARE does not, however, guarantee the accuracy, adequacy or completeness

of any information and is not responsible for any errors or omissions or for the results obtained from the use of such