www.moodys.com Banking Moody’s Global Credit Analysis Table of Contents: Summary Rating Rationale 1 Key Issues 2 Analysis of Rating Considerations 3 Discussion of Qualitative Rating Drivers 3 Franchise Value 3 Market Share and Sustainability 4 Geographic Diversification 4 Risk Positioning 5 Regulatory Environment 7 Operating Environment 7 Discussion of Quantitative Rating Drivers 7 Profitability 7 Liquidity 8 Capital Adequacy 8 Efficiency 8 Asset Quality 9 Discussion of Support Considerations 9 Company Annual Statistics 11 Moody’s Related Research 19 Analyst Contacts: New York 1.212.553.1653 0 Jeanne M. Del Casino VP - Senior Credit Officer M. Celina Vansetti Senior Vice President Felipe M. Carvallo Analyst Mexico City 52.55.1253.5700 15 David Olivares Villagomez Vice President - Senior Analyst September 2008 Banco del Estado de Chile Santiago, Chile Summary Rating Rationale Moody’s assigns a bank financial strength rating (BFSR) of C+ to Banco del Estado de Chile (BancoEstado), with a stable outlook, one of the highest BFSRs assigned to Latin American issuers. BancoEstado reported $27.4 billion in assets (Chilean Pesos CHP 13.765 billion), $16.7 billion in deposits, and $1.2 billion in equity as of June 30, 2008. The bank earned $106.8 million for the full year 2007 and $65.4 million for the first six months of 2008. BancoEstado is Chile’s third largest bank and is wholly-owned by the Republic. The bank performs significant economic and social roles as a full service commercial bank. Its primary mission is to promote home ownership and finance and to promote national savings by providing banking services to low- and middle- income individuals, and to other underserved segments of the population. The bank is also an active lender to large corporations and a leading provider of international trade finance. BancoEstado has the most geographically dispersed branch network in Chile and the most ATMs enhanced through its alliances with local retailers D&S and La Polar. Management is further diversifying the bank’s business mix through payment services, consumer, small business, and microfinance lending, as well as through bancassurance with its partner MetLife of the US. BancoEstado’s BFSR reflects its extensive and unique franchise within Chile as the only public sector bank, its solid profitability and asset quality, and its relatively low risk balance sheet. The bank’s profit ratios are lower than those of its large, privately-owned peers, reflecting a more liquid and less risky balance sheet, which results in lower interest margins and pre-tax profitability. Government ownership lends itself to a certain amount of public scrutiny that may slow the bank’s ability to keep costs low; however BancoEstado has been quite successful in managing its expense growth in recent years. This Credit Analysis provides an in-depth discussion of credit rating(s) for Banco del Estado de Chile and should be read in conjunction with Moody’s most recent Credit Opinion and rating information available on Moody's website. Click here to link.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.moodys.com

Banking Moody’s Global

Credit Analysis

Table of Contents: Summary Rating Rationale 1

Key Issues 2 Analysis of Rating Considerations 3

Discussion of Qualitative Rating Drivers 3 Franchise Value 3

Market Share and Sustainability 4 Geographic Diversification 4

Risk Positioning 5 Regulatory Environment 7 Operating Environment 7 Discussion of Quantitative Rating Drivers 7

Profitability 7 Liquidity 8 Capital Adequacy 8 Efficiency 8 Asset Quality 9

Discussion of Support Considerations 9 Company Annual Statistics 11 Moody’s Related Research 19

Analyst Contacts:

New York 1.212.553.1653

0 Jeanne M. Del Casino VP - Senior Credit Officer M. Celina Vansetti Senior Vice President Felipe M. Carvallo Analyst

Mexico City 52.55.1253.5700

15 David Olivares Villagomez Vice President - Senior Analyst

September 2008

Banco del Estado de Chile Santiago, Chile

Summary Rating Rationale

Moody’s assigns a bank financial strength rating (BFSR) of C+ to Banco del Estado de Chile (BancoEstado), with a stable outlook, one of the highest BFSRs assigned to Latin American issuers. BancoEstado reported $27.4 billion in assets (Chilean Pesos CHP 13.765 billion), $16.7 billion in deposits, and $1.2 billion in equity as of June 30, 2008. The bank earned $106.8 million for the full year 2007 and $65.4 million for the first six months of 2008.

BancoEstado is Chile’s third largest bank and is wholly-owned by the Republic. The bank performs significant economic and social roles as a full service commercial bank. Its primary mission is to promote home ownership and finance and to promote national savings by providing banking services to low- and middle-income individuals, and to other underserved segments of the population.

The bank is also an active lender to large corporations and a leading provider of international trade finance. BancoEstado has the most geographically dispersed branch network in Chile and the most ATMs enhanced through its alliances with local retailers D&S and La Polar. Management is further diversifying the bank’s business mix through payment services, consumer, small business, and microfinance lending, as well as through bancassurance with its partner MetLife of the US.

BancoEstado’s BFSR reflects its extensive and unique franchise within Chile as the only public sector bank, its solid profitability and asset quality, and its relatively low risk balance sheet. The bank’s profit ratios are lower than those of its large, privately-owned peers, reflecting a more liquid and less risky balance sheet, which results in lower interest margins and pre-tax profitability. Government ownership lends itself to a certain amount of public scrutiny that may slow the bank’s ability to keep costs low; however BancoEstado has been quite successful in managing its expense growth in recent years.

This Credit Analysis provides an in-depth discussion of credit rating(s) for Banco del Estado de Chile and should be read in conjunction with Moody’s most recent Credit Opinion and rating information available on Moody's website. Click here to link.

2 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

High loan growth and corporate borrower concentrations are important risks we see for BancoEstado and the Chilean banks in general. While BancoEstado’s exposures tend to be to top-quality borrowers or projects, they are still large relative to the bank’s profitability and capitalization. Banks also face stiff and increasing competition in all customer segments within Chile’s relatively mature market where margins are already relatively tight relative to other Latin American markets. Nevertheless, BancoEstado’s implicit government guarantee and funding and market share advantages provide it with a significant competitive edge and allow the bank to benefit from flights to quality.

BancoEstado’s Aa1 long term local currency deposit rating incorporates its C+ BFSR, which translates to a baseline credit assessment of A2 and which is lifted four notches based on our assumption of full systemic support in the event of high stress. This assumption is based on BancoEstado’s 100% government ownership and policy mandate, as well as its important deposit franchise, the third largest in Chile. Therefore any significant change in BancoEstado’s ownership would entail a credit event that could lead to a change in the local currency deposit rating.

The bank’s A2 long term foreign currency deposit rating is constrained by the A2 country ceiling for foreign currency deposits and is therefore sensitive to upward or downward movement in the foreign currency country ceiling.

Upward pressure on the C+ BFSR could come about if BancoEstado's core profitability improves significantly and the bank maintains strong asset quality and liquidity. Reduced borrower concentrations would also be an important ratings driver. Downward pressure on the BFSR could result from a marked decline in financial fundamentals or franchise value.

Key Issues

Unique public sector role: lower profit ratios for structural reasons

BancoEstado falls short of its large peers in terms of overall profitability, partly because of its social mission. The bank has a relatively liquid balance sheet mandated by its owner as well as higher operating leverage resulting from its "bancarización" mandate to penetrate underserved customer segments. Estado’s profit ratios are therefore not entirely comparable to those of the private sector banks that are more profit-oriented and devote a higher proportion of their balance sheets to riskier loan assets.

Slower economic growth, high inflation and interest rates could still dampen profits

Chile’s economy slowed during 2008 to 4.3% year over year in the second quarter of 2008 versus the 6.2 % reported in the prior year period. This was partly as a result of energy supply shortages during the first part of the year. Growth this year has still been fueled by strong domestic demand and gross capital formation, which is expected to result in a stronger showing by year end of between 4.5% and 5%. The economy is expected to weaken again in 2009 however as a function of the global slowdown and financial market pressures.

For the moment BancoEstado’s credit business and earnings show a continued strong growth trend, though higher inflation and volatile interest and exchange rate conditions have contributed to a slowing of that growth. With local interest rates rising sharply during the year by about 200 basis points, from 6.25% to 8.25% (monetary policy rate as of September 4, 2008), further increases are expected by year end.

While short term funding costs have risen, however, the resulting impact on bank net interest margins has so far been counterbalanced by the rise in inflation, which serves to buoy spreads on UF-denominated1 (inflation-indexed) assets. So far, local liquidity remains ample despite turmoil in the global financial markets. However, we remain cautious as to the potential effects of prolonged volatility in the international markets.

1 UF = Unidad de Fomento, Chile's inflation-linked currency unit.

3 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Credit costs continue to rise, though still manageable

As of June 30, 2008, BancoEstado’s credit costs absorbed a stable 33% of pre-provision profit, in line with the system average, reflecting the bank’s conservative credit policies and strong profit performance. While the level of credit costs is still low relative to BancoEstado’s record high of 53% in 2000, we consider it material, and one to watch.

The bank has limited its losses so far; however, increasing provisions and write-offs point to consumer asset quality deterioration. We expect the slower economy and higher inflation and interest rate environment to continue to take its toll on borrower quality in the near term.

High borrower concentrations

BancoEstado presents high single borrower concentrations relative to both earnings and capital as do all the large Chilean banks. In Moody’s view, high borrower concentrations increase a bank’s exposure to rapid asset quality deterioration and hence increase the risks to earnings.

BancoEstado’s twenty largest group exposures tend to be with top quality borrowers and projects in the financial services and corporate sectors; however, they remain large particularly relative to earnings.

Analysis of Rating Considerations

Discussion of Qualitative Rating Drivers

Franchise Value

Major retail bank with broad and diverse client base

BancoEstado’s franchise value reflects its importance as the third largest bank in Chile, its diversified earnings stream and extensive operating footprint across Chile. The bank serves a broad range of clients consisting of low- to middle-income individuals and companies that contribute to a fairly stable earnings stream.

Beginning in the 1990s, BancoEstado transformed its historically bureaucratic culture into a more nimble and commercially-oriented one, and has reduced to a minimum its dependence upon public sector balance and inflation-related revenues. The bank continues to explore opportunities to diversify its core lending and deposit business through organic growth and strategic alliances.

BancoEstado should continue to enhance its franchise value by leveraging its existing market shares in several business lines, its alliances with non-banks, and its public policy raison d'être. For example, BancoEstado has significantly expanded its distribution of insurance products through its alliance with MetLife, becoming the number 2 bank in Chile in providing insurance services to bank customers. Its ATM network has been enhanced through membership in the Redbanc automated teller network and through alliances with D&S and La Polar.

BancoEstado is also in a position to cross-sell multiple products to its massive client base given the still robust economic scenario in Chile and to improve its competitive position through advances in technology and service quality. The bank’s commitment to technology is already evident in a steady improvement in operating returns and efficiency ratios and an exemplary alignment with private sector performance metrics in general.

In Chile, BancoEstado operates 313 branches and 30 special access points (Puntos de Atención de Cercanía, PAC). The bank has a total of 1,133 ATMs, complemented by another 4,128 private ATMs (Redbanc), 1,088 sources for balances and deposit boxes, 300 CajaVecinas, and 25 branches of its ServiEstado subsidiary. Internet Banking represents over 2 million on-line transactions. Since 2005, the New York branch offers trade finance, working capital loans, and cash management services to Chilean corporations.

4 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Market Share and Sustainability

Leading market shares in Chile

BancoEstado is the market leader in savings deposits and residential mortgages for low and middle income individuals and also lends to large and medium sized corporations. Mortgages to low income customers are made at arms length pricing by BancoEstado, while subsidies may be provided by the government, with the bank acting only as administrator for such programs. The bank is also one of the largest providers of administrative and cash management services to government-owned and private enterprises, including payroll services. BancoEstado has one of the largest treasury operations in the country as a primary dealer in government securities and also serves as an important source of liquidity to the Chilean financial system.

BancoEstado’s position among the top five banks in Chile as of June 30, 2008 is provided below. BancoEstado ranks number 3 in all categories, except for net income where it ranks fourth, reflecting its higher proportion of low margin securities and mortgages, higher expense base, and higher than average tax rate.

The bank’s loan (14%) and deposit (16.2%) market shares have gradually expanded in recent years as has its share of the system’s net income (7%). Estado remains the leader in savings accounts with 87% of total accounts and in mortgages with 25% of the total market, though Santander is a very close second. Banco de Chile follows with 14.4% of total mortgages, Bci with 10%, and BBVA with 8%.

Market Share of Top 5 Chilean Banks As of June 30, 2008

Total Deposits Total Gross Loans

Banco Santander 20.8% Banco Santander 20.6%

Banco de Chile 18.5% Banco de Chile 19.3%

Banco del Estado de Chile 16.2% Banco del Estado de Chile 13.9%

Banco de Crédito e Inversiones (Bci) 12.9% Banco de Crédito e Inversiones 13.2%

BBVA 7.3% BBVA 7.6%

Total Net Income Total Equity

Banco Santander-Chile 32.2% Banco Santander-Chile 20.3%

Banco de Chile 25.2% Banco de Chile 17.7%

Banco del Estado de Chile 7.0% Banco de Crédito e Inversiones 10.4%

Banco de Crédito e Inversiones 14.7% Banco del Estado de Chile 9.3%

BBVA 4.3% BBVA 5.7%

Source: Moody's, SBIF

Geographic Diversification

Despite national coverage, primarily Chilean focus limits earnings diversification

BancoEstado is limited in its geographic diversification relative to global peers because of its largely Chilean operations. Moody’s assesses geographic diversification based on the Gross Domestic Product (GDP) of a bank’s operating footprint. Chile’s nominal GDP of US$163.9 billion for 2007 and population of some 15 million are relatively small, even when compared to other large Latin American countries such as Brazil and Mexico, and so the score for all Chilean banks is below average.

5 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Earnings Stability

Retail focus and core funding contribute to relatively stable earnings profile

Moody’s believes retail banks have more predictable earnings to the extent that their consumer lending, deposit, and transaction-based revenues comprise the lion’s share. This is an invaluable asset to banks in times of stress. Given BancoEstado’s strong retail deposit base, granular lending base, and a relatively low proportion of corporate and trading-related revenues, the stability of its earnings profile is above average.

BancoEstado derives more than half of its interest income and commissions from the consumer segment (55%), followed by the financial services and corporate segment (including small and medium-sized companies) (30%) and institutional customers (14%). About 80% of BancoEstado’s interest revenues originate from traditional lending and deposit products and 15% from securities.

Risk Positioning

Policies and practices commensurate with risk profile and business mix

BancoEstado’s risk positioning score is hurt by its high single corporate borrower concentrations, endemic to the large Chilean banks, and its single shareholder ownership by the Republic of Chile. However, its overall credit, market, and liquidity risk management structure, practices, and financial reporting transparency support a stable risk profile.

Corporate Governance

Government ownership equated to a closely held firm under one shareholder

BancoEstado’s corporate governance structure is comparable to the standards of private sector institutions. Nevertheless, Moody’s equates BancoEstado’s government ownership to a closely held firm dominated by one shareholder or family that could exercise undue influence on the bank’s operations. That said BancoEstado is not permitted to lend to public sector entities and hence is more insulated than the typical public sector bank from politically-based lending pressure. In addition, though a government-owned bank, BancoEstado meets Moody’s test for an independent board of at least 25% of its members.

BancoEstado’s senior management is conservative and professional, drawn from the private sector. Management has been effective in modernizing the bank and in transforming its traditionally bureaucratic culture into a market-oriented and competitive institution.

Controls & Risk Management

High and improving standards and procedures

Management sets high standards for the bank's risk management and controls, supported by a well established management structure and a deep bench of experienced credit and market professionals.

As an important depositary for public sector liquidity and public savings, the bank maintains a relatively conservative investment and credit portfolio. The bank's trading activities are devoted mainly to managing its government securities portfolio and to dealing in foreign exchange forwards on behalf of clients.

Financial Reporting Transparency

Timely and complete financial statements

BancoEstado’s financial reporting transparency is above average as is the case for most of the Chilean banks. The bank publishes complete financial statements on a monthly basis and has employed International Financial Reporting Standards (IFRS) since January 2008 in accordance with the regulations of the Superintendency of Banks and Financial Institutions (SBIF).

6 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

The bank’s published financial statements provide comprehensive information about profitability, asset quality, and capital. They are however limited with respect to individual business line performance, market risk exposures, and VaR stress testing information, as well as details on the largest credits.

Credit Risk Concentration

High concentrations particularly as a percent of earnings

BancoEstado presents high borrower risk concentrations that are not uncommon to major lenders in Chile partly because of their size, large lending books, and the limited depth of domestic loan sales and securitization markets. The top twenty group exposures, including loans and net derivatives, are compared against both pre-provision pre-tax profitability and tier one capital.

While BancoEstado scores very low for borrower concentrations, the bank's twenty largest exposures are with top quality and highly rated borrowers in the financial services sector, and include solidly performing large corporate or project-related exposures. During the last four years BancoEstado has expanded its consumer lending activities, which should lead to greater diversification and granularity of the loan portfolio.

At the same time the bank reports relatively low industry concentrations, reflecting a diversified loan portfolio consisting of financial services, construction, manufacturing, commercial, and energy companies in Chile. High corporate sector concentrations are discouraged by the banking regulators.

BancoEstado’s exposure to residential mortgages is however by far the most highly concentrated in Chile at almost 42% of total loans versus 23% for the total system. Delinquency levels on mortgages in Chile have historically been contained and as of the date of this writing remain low at 1% for the system and about 2% for BancoEstado. While household indebtedness in Chile has increased in recent years, it also remains low relative to global averages.

Liquidity Management

Ample liquidity supported by stable core deposit base and high proportion of liquid assets

BancoEstado’s strong liquidity position within the Chilean financial system derives from the combination of an extensive and granular deposit base, its large holdings of liquid assets and low dependence on market funding.

The bank’s large securities portfolio comprises about 22% of total assets versus the system average of 11.5%. Core deposits represent a relatively high 75% of total loans vis-à-vis the system and large peer average of 55% and 51% of total liabilities. Its large demand and savings account base makes it less dependent upon local institutional money (i.e., the AFPs or pension funds) for funding. Market funds relate to 49% of total liabilities, mostly in the form of institutional deposits (16%), notes payable (i.e., letras hipotecarias – 18%), bank borrowings and repurchase agreements (9%), and bonds (3%).

Estado is among the largest providers of institutional liquidity in the Chilean banking system. The bank has been called upon to provide liquidity and/or administrative back-up to other banks in the system in case of need, such as during the CORFO-Inverlink affair of 2003.

Market Risk Appetite

Large liquid holdings are proactively managed

BancoEstado’s market risk appetite is about average, reflecting its traditional deposit-taking and lending profile. Market-related income contributes little to the bank’s bottom line and has historically been uneven, earning between 3% and 17% of gross intermediation revenues over the past few years.

7 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

BancoEstado’s relatively large securities portfolio, 90% of which is categorized as available for sale, exposes the bank to interest rate risk. The bank employs asset/liability management tools, including Value at Risk models, in order to minimize the potential losses related to interest rate risk. The bank takes measured positions in proprietary trading. Foreign exchange risk is limited to customer-based activities (= fee business) and to a lesser extent, its investment portfolio.

Regulatory Environment

Moody’s assessment of Chile’s regulatory environment considers its proven institutional framework, the independence of its regulatory body, and its 20-year history of setting and enforcing prudential standards. The assessment also incorporates the supervisors’ effective enforcement of asset quality measurement and loan loss provisioning rules, capital and liquidity regulations, and restrictions regarding related-party transactions. We also consider the Chilean regulators’ track record of preventive and corrective measures and their increasing commitment to transparency assisted by an increasingly user-friendly website.

The Chilean regulators continued in 2007 and 2008 to bolster bank regulatory and accounting standards through the adoption of IFRS, the latter which became effective in January 2008, as well as improving risk management regulations and guidance on market and operational risk. The system’s transition toward Basel II dovetails with improvements in regulation and supervision that have been implemented during the last two decades.

Operating Environment

Chilean banks operate within a relatively stable environment with a well established and effective institutional framework. Our BFSR scorecard assesses a country’s operating environment based on three factors: economic stability, the level of integrity and corruption prevalent in the country, and its legal system.

Chile’s economic stability is evaluated based on the standard deviation of Chile's GDP growth rates during the last twenty years compared to that of other countries in the world. Chile’s economic stability scores low relative to that of developed countries because of its uneven growth trend and the slightly negative GDP growth experienced during 1999. This measure should therefore improve over time.

The level of integrity and corruption is measured using the World Bank index, which ranks 212 countries worldwide based on six different parameters including voice and accountability, political stability and absence of violence, government effectiveness, regulatory quality, rule of law, and control of corruption. In this regard, Chile compares very favorably with both local and global peers.

The predictability and fairness of the Chilean legal system also compares very favorably to other countries and is evaluated based on our chosen proxy of the typical time (i.e., one to two years) it takes to foreclose on a residential mortgage.

Discussion of Quantitative Rating Drivers

Profitability

Is profit expansion sustainable for second half of 2008 and 2009?

Banco Estado’s 2007 earnings rose 5.8% in peso terms to US $106.8 million, primarily reflecting higher trading and mark-to-market gains and affiliate income as net interest income rose a slight 1.8%. The adjusted net interest margin (including hedges) declined 3% from 3.33%, due mainly to higher funding rates that largely offset the benefits of growth in commercial and mortgage loan volumes. Provisions have also taken a larger bite out of earnings throughout the year (39% up from 30% in 2006). Net income from fees and commissions were also weaker by 4.7%.

BancoEstado continued to control operating costs, which grew a modest 4%, despite strong business growth. Pre-provision profit to average risk-weighted assets improved slightly to 3% from 2.8%, boosted by increased

8 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

income from subsidiaries and affiliates, and non-operating income. Return on average assets and equity remained relatively stable at 0.46% and 9.7%, respectively, reflecting higher provisions and monetary correction.

First half 2008 results continued the positive trend with an improved net interest margin that benefits from rising inflation and a stronger pre-provision profit to average risk-weighted assets ratio. Rising funding and provisioning costs were therefore offset by higher income on inflation-indexed assets, a general widening of spreads, and good cost control.

It remains to be seen whether and to what extent current volatile conditions in the global markets coupled with the high inflation and interest rate scenario in Chile will affect the country and the bank’s performance in the coming quarters.

While BancoEstado's risk-weighted recurring earnings power falls short when compared to that of its large private sector peers, its earnings power is comparable to the global peer average. Pre-provision profit to risk-weighted assets has averaged 2.9% for the last three years versus 3.6% for its private sector peer group.

BancoEstado's operating expense base relative to earnings reflects in part the bank's mission to increase banking penetration throughout Chile as well as continuous technology upgrades of its branch and ATM network and other points of sale. BancoEstado's higher cost structure and tax rate (56.5%) claim more of the bottom line than do those of the other banks, however, net income has grown healthily in recent years.

BancoEstado has been generating higher net interest income and fees aided by new business alliances and products (e.g., insurance, factoring, ATMs, and electronic banking). Nevertheless, the bank’s fee generation capacity and pricing policy remains limited because of its mandate to offer financial services to underbanked segments throughout Chile. Fee coverage of operating expenses – at an improved 33% for the first six months of 2008 - remained below the system average of 38%.

Liquidity

Conservative balance sheet liquidity

BancoEstado’s liquidity is well above average as a result of the bank's low dependence on market funds, high proportion of readily marketable liquid assets, and good asset quality. Expensive market funds represent a small percentage of the bank’s funding. BancoEstado also maintains relatively low loan leverage with a 60% loan to asset ratio as compared with the system average of 68% and large peer average of 72%. Cash and highly liquid, marketable government securities represent about 32% of total assets as compared with 22% for the system.

Capital Adequacy

Solid tier one capital supports risk profile

BancoEstado's capitalization ratios are good compared to global peers. The bank’s tier one capital ratio of 7.1% as of June 30, 2008 well exceeds the Chilean regulator’s minimum regulatory standards. Though this ratio is below the system’s 9.2% and its rated peers’ 8.6%, we consider it adequate in the context of BancoEstado’s implicit government support, asset mix, and level of risk undertaken by the bank.

Efficiency

Low efficiency relative to private sector rivals due to social mission and extensive network

BancoEstado's efficiency ratio compares very well to the global average, but less well to local peers such as Banco Santander Chile and Banco de Chile that have a track record of globally competitive efficiency ratios. Given its developmental role, management expects the bank’s efficiency ratio to remain above the system average (it is presently 7 percentage points higher).

BancoEstado has nevertheless gradually improved its operating efficiency, reaching a ratio of 56.9% as of June 2008 from 60.85% in June of 2007 supported by both higher operating revenues and contained expense

9 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

growth. Increasing economies of scale will depend on the continued streamlining and automation of the bank's operations given the breadth of its network and social mission.

BancoEstado has undertaken important investments in technology and innovative products. The bank’s low-cost Caja Vecina in which small shops provide everyday banking services, ServiEstado, and ATM network have helped improve the bank’s automated transaction ratio.

Asset Quality

Problem loans remain manageable, but are on the rise

BancoEstado presents a well diversified asset mix, consisting primarily of loans (60.6% of the balance sheet) and A1-rated Chilean government securities and Central Bank paper (21.7%). The corporate loan portfolio contributes 48% of total loans relating mainly to high quality national and international corporations. Lending to individuals comprises 52%, with over 80% representing residential mortgage loans.

Loan growth of 23.3% was slightly higher for BancoEstado than the Chilean system’s 21.7% for the twelve months ended June 2008 and higher than the year earlier’s 14.3%, reflecting strong expansion of both the commercial and consumer loan portfolios. We expect slower loan growth in the latter part of 2008 and into 2009 because of higher interest rates and delinquencies.

Asset quality deteriorated during 2007 as non-performing loans (NPLs), mainly to consumers, rose a sharp 78.6% on a nominal basis to reach 1.2% of gross loans, a 50 basis point increase from the record lows of a year earlier. As of June 30, 2008, the NPL ratio rose a further 7 basis points, but a 14 basis point increase when adjusted for loan growth. Reserve coverage declined due mainly to write-offs but still covered 135% of problem loans, down from 171% as of year end 2007, and below the three-year average of 220%. Problem loans also represented a high of 14.5% of reserves plus shareholders’ equity, up from the prior three year average of 9.6%.

This trend is in line with rising non-performers within the Chilean system, whose loan portfolio has been growing in the double digits for the past five years with a special emphasis on consumer credit. Nevertheless, BancoEstado's rate of increase continued to surpass that of the system this year. Though non-performing loans are still at a manageable level, they are the highest the bank has reported since 2003 and its ratio is the highest among the four largest banks in Chile.

In our last report we had anticipated asset quality deterioration as a result of loan seasoning and double digit loan growth.. This has come to fruition, and therefore we remain cautious as to the pace of deterioration. We expect NPL ratios to continue to rise in the coming quarters, particularly in light of slower loan growth.

Discussion of Support Considerations

Full systemic support incorporated in deposit ratings

Moody's assigns a global local currency deposit rating of Aa1 for BancoEstado, incorporating the bank's baseline credit assessment of A2 that is directly mapped from the C+ BFSR. The deposit rating is then lifted to Aa1, reflecting full systemic support because of the bank’s 100% government ownership, policy mandate, and the importance of its retail deposit franchise in the Chilean financial system.

Moody's assesses Chile as a high support country because of the Chilean authorities' high level of interest and willingness to support the stability of the financial system. The support probability is measured against Chile's Aaa local currency country ceiling for deposits. This ceiling represents the risk that an important bank would be allowed to default upon local currency deposits either due to a lack of local currency resources or the imposition of a domestic deposit freeze.

10 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Exhibit A: Mapping the BFSR to the Baseline Credit Assessment (BCA)

The discussions of qualitative and quantitative rating drivers presented in this report forms the analytical basis for assigning a Bank Financial Strength Rating (BSFR) of “C+” to Banco del Estado de Chile.

BFSRs are Moody’s opinions on the intrinsic safety and soundness of a bank enterprise and, in effect, address the susceptibility of a particular institution to financial distress.

The BFSR array of ratings is not on Moody’s traditional rating scale (Aaa, Aa, etc.). There is a useful method, however, for translating BFSRs to Moody’s traditional scale – the baseline credit assessment. In effect, the baseline credit assessment measures a bank’s stand-alone default risk assuming there is no systemic or other external support.

Banco del Estado de Chile’s “C+” BFSR maps to a baseline credit assessment of A2, yet, considering external support factors, its deposit ratings are Aa1.

BFSR/Baseline Risk Assessment Mapping for Banco del Estado de Chile

BFSR Baseline Credit Assessment (BCA)

A Aaa

A- Aa1

B+ Aa2

B Aa3

B- A1

C+ A2

C A3

C- Baa1

C- Baa2

D+ Baa3

D+ Ba1

D Ba2

D- Ba3

E+ B1

E+ B2

E+ B3

E Caa1

E Caa2

E Caa3

11 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Company Annual Statistics

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 BALANCE SHEET (US$ Million)

Assets

Cash and Cash Equivalents 2,510 1,541 1,748 1,478 853

Short-Term Interbank Investments 365 - - - -

Investments in Securities 6,078 6,722 5,254 6,519 4,526

Held-to-Maturity 555 - - - -

Trading 59 - - - -

Available-for-Sale 5,464 - - - -

Liquid Assets 8,953 8,263 7,002 7,997 5,379

Loans, Leases, Disc. Notes 16,986 15,769 12,483 11,276 8,800

Short-Term Loans - 2,335 2,228 1,866 1,611

Interbank Loans - - 31 191 185

Commercial Loans - 1,558 1,563 1,191 1,024

Consumer Loans - 164 133 119 99

Trade Finance - 439 421 343 299

Other Loans - 174 80 22 3

Long-Term Loans - 9,322 6,417 5,350 3,643

Interbank Loans - - - - 0

Commercial Loans 6,775 4,297 3,119 2,922 2,181

Consumer Loans 1,817 1,609 1,264 1,109 857

Trade Finance 839 93 122 154 147

Leasing & Discounts 461 419 261 243 138

Mortgage Loans 7,095 2,904 1,650 922 320

Restructured Loans - 7 10 15 18

Bills of Exchange Repass - 3,915 3,728 3,964 3,454

Net Contingent Assets - - - - 0

Non Performing Loans 215 189 99 81 74

Less: Loan Loss Reserves 291 324 219 191 160

Total Net Loans 16,696 15,444 12,264 11,085 8,641

Net Adjust & Control Acct. - - - 0 -

Total Risk Assets 23,140 22,166 17,518 17,604 13,166

Repurchase Agreements 424 54 99 221 242

Other Investments - 70 46 26 53

Investments in Subs. & Affiliates 8 71 51 47 36

Net Futures Operations 966 30 27 80 141

Other Assets 972 663 433 517 427

Fixed Assets (Net) - 282 234 221 188

Less Other Provisions - 0 0 0 8

Total Assets 28,019 24,878 20,156 20,194 15,099

12 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 Liabilities

Short Term Deposits - 12,267 10,228 11,265 7,786

Demand Deposits 4,719 5,474 3,995 3,219 2,792

Savings Deposits 3,877 - - - -

Time Deposits 8,506 6,746 6,189 8,024 4,982

Other Time Deposits 15 47 44 22 12

Interbank & Other Long Term Deposits - 3,271 2,282 1,316 829

Total Deposits 17,116 15,538 12,510 12,582 8,616

Short-Term Due to Banks 1,417 72 740 350 843

Domestic (ST) - 38 430 334 778

Foreign (ST) - 35 309 17 65

Notes Payable - 4,168 3,894 4,069 3,400

Repurchase Agreements 1,058 1,327 680 966 545

Long-Term Due to Banks - 420 200 257 245

Domestic (LT) - - - 9 17

Foreign (LT) - 420 200 248 229

Total Borrowed Funds 2,474 5,987 5,515 5,642 5,033

Bonds & Debentures 5,183 1,020 305 146 142

Net Contingent Liabilities - 3 3 0 -

Net Futures Operations 702 - - - -

Subordinated Bonds 739 682 510 359 192

Other Liabilities 609 470 359 596 341

Net Adjust & Control Acct. - 0 0 - 33

Total Liabilities 26,824 23,701 19,203 19,325 14,357

Paid in Capital 8 8 8 8 7

Capital & Legal Reserves 1,156 15 12 12 10

Other Reserves - 1,070 842 797 643

Equity Adjustment Account (27) (22) (3) (25) 2

Net Income 58 106 94 77 80

Total Shareholders' Equity 1,195 1,176 953 868 742

Total Liabilities and Shareholders’ Equity 28,019 24,878 20,156 20,194 15,099

Off-Balance Sheet Amounts: - - - - -

Futures Operations - 373 122 9,608 8,732

Contingents - 674 667 368 269

Adjust & Control Acct. - 1,337 452 963 1,196

13 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 Income Statement (US$ Million) - - - - -

Interest Income 1,168 2,014 1,306 1,205 767

Loan Income - 1,653 1,021 937 659

Interest on Securities - 273 233 - -

Other Interest Income - 87 52 269 108

Interest Expense 738 1,396 738 743 431

Savings and Time Deposits - 808 368 315 140

Repurchase Agreements - 64 51 44 19

Notes Payable - 496 296 366 264

Due to Banks, Domestic - 5 4 6 3

Due to Banks, Foreign - 6 13 5 4

Other Interest Expense - 17 6 7 2

Net Interest Income 430 617 568 462 336

Non Interest Income 39 123 56 59 88

Trading & Marked-to-Market (Loss) 16 124 48 25 40

Forex Operations (Loss) (134) (1) 6 24 40

Other Operations (Loss) 157 (0) 3 11 8

Gross Revenue from Intermed. 468 740 624 521 424

Net Commission and Fee Income 110 154 151 141 117

Gross Operating Revenue 579 894 775 663 541

Operating Expenses 329 515 464 402 349

Personnel Expense 214 319 300 261 224

General and Admin. Expenses 115 196 163 141 125

Net Operating Income 250 379 311 260 192

Net Income from Loan Sales/Securitizations 2 9 11 - -

Non Operating Income - 23 12 9 41

Non Operating Expense - 12 45 32 43

Net Income from Subsid. and Affiliates 1 23 18 17 18

Pre Provision Profit 252 422 307 254 207

Net Provisions 82 165 92 55 50

Voluntary Provisions - - - - -

Recoveries - - - - -

Monetary Correction (25) (48) (11) (19) (10)

Net Income Before Tax 145 209 204 180 147

Income Tax 80 103 110 103 66

Net Income 65 106 94 77 80

Ratios

Asset Quality (%)

NPL / Gross Loans & Leases 1.27 1.20 0.79 0.72 0.84

NPLs / Prev. Yr. Gross Loans 1.56 1.52 0.88 0.92 1.01

Reserve Coverage / NPL 134.99 171.33 221.19 234.81 216.63

14 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

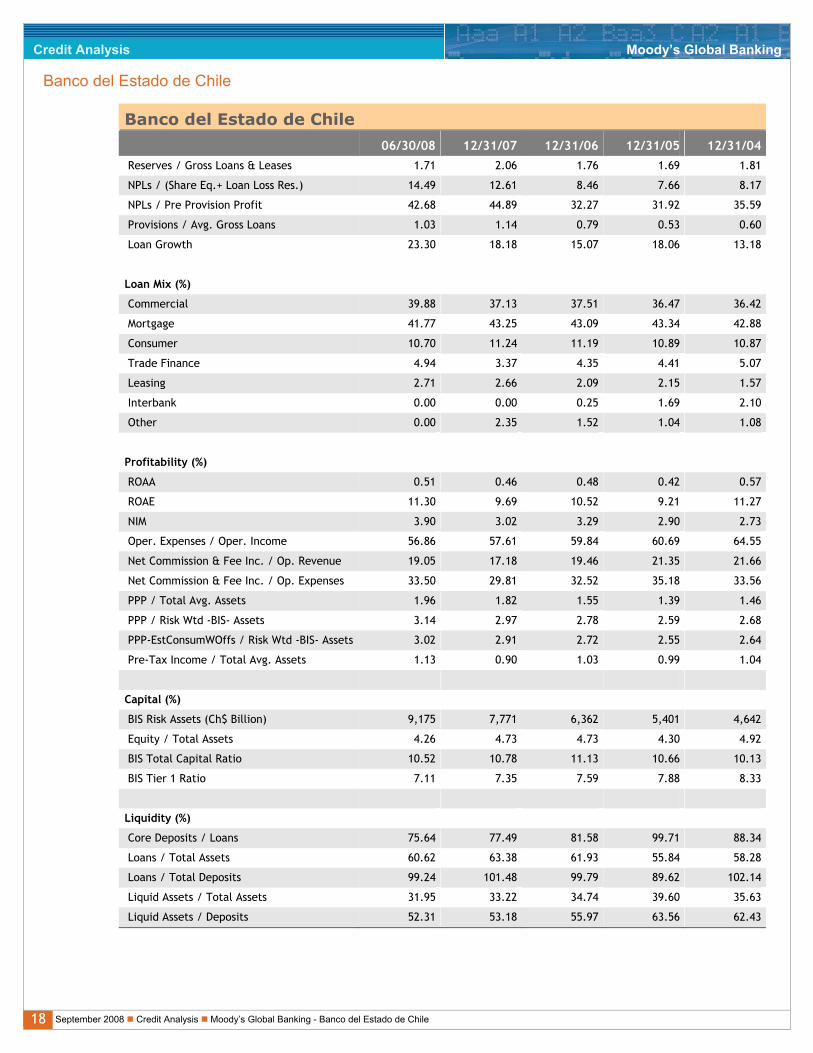

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 Reserves / Gross Loans & Leases 1.71 2.06 1.76 1.69 1.81

NPLs / (Share Eq.+ Loan Loss Res.) 14.49 12.61 8.46 7.66 8.17

NPLs / Pre Provision Profit 42.68 44.89 32.27 31.92 35.59

Provisions / Avg. Gross Loans 1.00 1.17 0.78 0.55 0.62

Loan Growth 23.25 26.32 10.71 28.13 20.68

Loan Mix (%)

Commercial 39.88 37.13 37.51 36.47 36.42

Mortgage 41.77 43.25 43.09 43.34 42.88

Consumer 10.70 11.24 11.19 10.89 10.87

Trade Finance 4.94 3.37 4.35 4.41 5.07

Leasing 2.71 2.66 2.09 2.15 1.57

Interbank 0.00 0.00 0.25 1.69 2.10

Other 0.00 2.35 1.52 1.04 1.08

Profitability (%)

ROAA 0.49 0.47 0.47 0.44 0.58

ROAE 10.99 9.99 10.33 9.57 11.61

NIM 3.79 3.11 3.23 3.00 2.81

Oper. Expenses / Oper. Income 56.86 57.61 59.84 60.69 64.55

Net Commission & Fee Inc. / Op. Revenue 19.05 17.18 19.46 21.35 21.66

Net Commission & Fee Inc. / Op. Expenses 33.50 29.81 32.52 35.18 33.56

PPP / Total Avg. Assets 1.91 1.87 1.52 1.44 1.51

PPP / Risk Wtd -BIS- Assets 3.06 3.06 2.73 2.69 2.76

PPP-EstConsumWOffs / Risk Wtd -BIS- Assets 2.93 3.01 2.67 2.66 2.73

Pre-Tax Income / Total Avg. Assets 1.10 0.93 1.01 1.02 1.07

Capital (%)

BIS Risk Assets (US$ Million) 17,412 15,606 11,953 10,548 8,353

Equity / Total Assets 4.26 4.73 4.73 4.30 4.92

BIS Total Capital Ratio 10.52 10.78 11.13 10.66 10.13

BIS Tier 1 Ratio 7.11 7.35 7.59 7.88 8.33

Liquidity (%)

Core Deposits / Loans 75.64 77.49 81.58 99.71 88.34

Loans / Total Assets 60.62 63.38 61.93 55.84 58.28

Loans / Total Deposits 99.24 101.48 99.79 89.62 102.14

Liquid Assets / Total Assets 31.95 33.22 34.74 39.60 35.63

Liquid Assets / Deposits 52.31 53.18 55.97 63.56 62.43

15 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 BALANCE SHEET (Ch$ Billion)

Assets

Cash and Cash Equivalents 1,322 768 930 757 474

Short-Term Interbank Investments 193 - - - -

Investments in Securities 3,203 3,347 2,797 3,338 2,515

Held-to-Maturity 292

Trading 31

Available-for-Sale 2,879

Liquid Assets 4,718 4,115 3,727 4,095 2,989

Loans, Leases, Disc. Notes 8,951 7,852 6,644 5,774 4,891

Short-Term Loans - 1,163 1,186 955 895

Interbank Loans - - 17 98 103

Commercial Loans - 776 832 610 569

Consumer Loans - 82 71 61 55

Trade Finance - 218 224 176 166

Other Loans - 87 43 11 2

Long-Term Loans - 4,642 3,415 2,739 2,025

Interbank Loans - - - - 0

Commercial Loans 3,570 2,140 1,660 1,496 1,212

Consumer Loans 957 801 673 568 477

Trade Finance 442 46 65 79 82

Leasing & Discounts 243 209 139 124 77

Mortgage Loans 3,739 1,446 878 472 178

Restructured Loans - 4 5 8 10

Bills of Exchange Repass - 1,950 1,984 2,030 1,919

Net Contingent Assets - - - - 0

Non Performing Loans 113 94 53 42 41

Less: Loan Loss Reserves 153 161 117 98 89

Total Net Loans 8,798 7,690 6,527 5,676 4,802

Net Adjust & Control Acct. - - - 0 -

Total Risk Assets 12,193 11,038 9,324 9,014 7,317

Repurchase Agreements 224 27 53 113 135

Other Investments - 35 24 13 30

Investments in Subs. & Affiliates 4 35 27 24 20

Net Futures Operations 509 15 14 41 78

Other Assets 512 330 231 265 237

Fixed Assets (Net) - 140 124 113 105

Less Other Provisions - 0 0 0 5

Total Assets 14,765 12,388 10,728 10,340 8,391

16 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 Liabilities

Short Term Deposits 6,108 5,444 5,768 4,327

Demand Deposits 2,487 2,726 2,126 1,648 1,552

Savings Deposits 2,043

Time Deposits 4,482 3,359 3,294 4,108 2,769

Other Time Deposits 8 24 23 12 7

Interbank & Other Long Term Deposits - 1,629 1,215 674 461

Total Deposits 9,019 7,737 6,658 6,442 4,788

Short-Term Due to Banks 746 36 394 179 468

Domestic (ST) - 19 229 171 432

Foreign (ST) - 17 165 8 36

Notes Payable - 2,075 2,073 2,083 1,890

Repurchase Agreements 557 661 362 495 303

Long-Term Due to Banks - 209 107 132 136

Domestic (LT) - - - 5 9

Foreign (LT) - 209 107 127 127

Total Borrowed Funds 1,304 2,981 2,935 2,889 2,797

Bonds & Debentures 2,731 508 162 75 79

Net Contingent Liabilities - 2 2 0 -

Net Futures Operations 370 - - - -

Subordinated Bonds 389 340 272 184 107

Other Liabilities 321 234 191 305 189

Net Adjust & Control Acct. - 0 0 - 18

Total Liabilities 14,135 11,802 10,221 9,896 7,979

Paid in Capital 4 4 4 4 4

Capital & Legal Reserves 609 7 6 6 6

Other Reserves - 533 448 408 357

Equity Adjustment Account (14) (11) (2) (13) 1

Net Income 31 53 50 39 45

Total Shareholders' Equity 630 586 507 445 412

Total Liabilities and Shareholders’ Equity 14,765 12,388 10,728 10,340 8,391

Off-Balance Sheet Amounts:

Futures Operations 186 65 4,920 4,853

Contingents 336 355 188 150

Adjust & Control Acct. 666 241 493 664

17 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 Income Statement (Ch$ Billion)

Interest Income 616 1,003 695 617 426

Loan Income - 823 544 480 366

Interest on Securities - 136 124

Other Interest Income - 44 28 138 60

Interest Expense 389 695 393 381 240

Savings and Time Deposits - 402 196 161 78

Repurchase Agreements - 32 27 22 11

Notes Payable - 247 158 187 146

Due to Banks, Domestic - 2 2 3 2

Due to Banks, Foreign - 3 7 3 2

Other Interest Expense - 9 3 4 1

Net Interest Income 226 307 302 237 187

Non Interest Income 20 61 30 30 49

Trading & Marked-to-Market (Loss) 8 62 26 13 22

Forex Operations (Loss) (70) (1) 3 12 22

Other Operations (Loss) 83 (0) 1 5 5

Gross Revenue from Intermed. 247 369 332 267 236

Net Commission and Fee Income 58 76 80 72 65

Gross Operating Revenue 305 445 412 339 301

Operating Expenses 173 256 247 206 194

Personnel Expense 113 159 160 134 125

General and Admin. Expenses 61 98 87 72 69

Net Operating Income 132 189 166 133 107

Net Income from Loan Sales/Securitizations 1 4 6

Non Operating Income - 11 6 4 23

Non Operating Expense - 6 24 16 24

Net Income from Subsid. and Affiliates 0 12 10 9 10

Pre Provision Profit 133 210 164 130 115

Net Provisions 43 82 49 28 28

Voluntary Provisions - - - - -

Recoveries - - - - -

Monetary Correction (13) (24) (6) (10) (6)

Net Income Before Tax 77 104 108 92 81

Income Tax 42 51 58 53 37

Net Income 34 53 50 39 45

Ratios

Asset Quality (%)

NPL / Gross Loans & Leases 1.27 1.20 0.79 0.72 0.84

NPLs / Prev. Yr. Gross Loans 1.56 1.42 0.91 0.85 0.95

Reserve Coverage / NPL 134.99 171.33 221.19 234.81 216.63

18 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Banco del Estado de Chile

06/30/08 12/31/07 12/31/06 12/31/05 12/31/04 Reserves / Gross Loans & Leases 1.71 2.06 1.76 1.69 1.81

NPLs / (Share Eq.+ Loan Loss Res.) 14.49 12.61 8.46 7.66 8.17

NPLs / Pre Provision Profit 42.68 44.89 32.27 31.92 35.59

Provisions / Avg. Gross Loans 1.03 1.14 0.79 0.53 0.60

Loan Growth 23.30 18.18 15.07 18.06 13.18

Loan Mix (%)

Commercial 39.88 37.13 37.51 36.47 36.42

Mortgage 41.77 43.25 43.09 43.34 42.88

Consumer 10.70 11.24 11.19 10.89 10.87

Trade Finance 4.94 3.37 4.35 4.41 5.07

Leasing 2.71 2.66 2.09 2.15 1.57

Interbank 0.00 0.00 0.25 1.69 2.10

Other 0.00 2.35 1.52 1.04 1.08

Profitability (%)

ROAA 0.51 0.46 0.48 0.42 0.57

ROAE 11.30 9.69 10.52 9.21 11.27

NIM 3.90 3.02 3.29 2.90 2.73

Oper. Expenses / Oper. Income 56.86 57.61 59.84 60.69 64.55

Net Commission & Fee Inc. / Op. Revenue 19.05 17.18 19.46 21.35 21.66

Net Commission & Fee Inc. / Op. Expenses 33.50 29.81 32.52 35.18 33.56

PPP / Total Avg. Assets 1.96 1.82 1.55 1.39 1.46

PPP / Risk Wtd -BIS- Assets 3.14 2.97 2.78 2.59 2.68

PPP-EstConsumWOffs / Risk Wtd -BIS- Assets 3.02 2.91 2.72 2.55 2.64

Pre-Tax Income / Total Avg. Assets 1.13 0.90 1.03 0.99 1.04

Capital (%)

BIS Risk Assets (Ch$ Billion) 9,175 7,771 6,362 5,401 4,642

Equity / Total Assets 4.26 4.73 4.73 4.30 4.92

BIS Total Capital Ratio 10.52 10.78 11.13 10.66 10.13

BIS Tier 1 Ratio 7.11 7.35 7.59 7.88 8.33

Liquidity (%)

Core Deposits / Loans 75.64 77.49 81.58 99.71 88.34

Loans / Total Assets 60.62 63.38 61.93 55.84 58.28

Loans / Total Deposits 99.24 101.48 99.79 89.62 102.14

Liquid Assets / Total Assets 31.95 33.22 34.74 39.60 35.63

Liquid Assets / Deposits 52.31 53.18 55.97 63.56 62.43

19 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

Moody’s Related Research

Credit Opinion: Banco del Estado de Chile, September 2008

Company Profile: Banco del Estado de Chile, September 2007 (104709)

Banking System Outlook: Chile, July 2007 (103948)

Andean Banks, February 2008 (107477)

Banking Statistical Supplement: Chile, April 2008 (108667)

Country Statistics: Chile, May 2008

Special Comment: Moody’s Outlook for Latin American Banks, October 2007 (105399)

Bank Ratings and Government Bond Ratings, August 2007 (103903)

Moody’s First Annual Survey of Latin American Banks’ Single Client Exposures, May 2007 (103239)

Rating Methodologies: Guidelines for Rating Bank Junior Securities, April 2007 (102726)

Incorporation of Joint-Default Analysis into Moody’s Bank Ratings: A Refined Methodology, March 2007 (102639)

Bank Financial Strength Ratings: Global Methodology, February 2007 (102151)

Piercing the Country Ceiling: An Update, January 2005 (91215)

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of this report and that more recent reports may be available. All research may not be available to all clients.

20 September 2008 Credit Analysis Moody’s Global Banking - Banco del Estado de Chile

Credit Analysis Moody’s Global Banking

Banco del Estado de Chile

© Copyright 2008, Moody’s Investors Service, Inc. and/or its licensors and affiliates (together, “MOODY’S”). All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, such information is provided “as is” without warranty of any kind and MOODY’S, in particular, makes no representation or warranty, express or implied, as to the accuracy, timeliness, completeness, merchantability or fitness for any particular purpose of any such information. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The credit ratings and financial reporting analysis observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding or selling. MOODY’S hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MOODY’S have, prior to assignment of any rating, agreed to pay to MOODY’S for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,400,000. Moody’s Corporation (MCO) and its wholly-owned credit rating agency subsidiary, Moody’s Investors Service (MIS), also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually on Moody’s website at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Report number: 111584

Author Analyst Production Associate Jeanne M. Del Casino

Felipe Carvallo M. Shubhra Bhatnagar

Related Documents