1. Balance of payments Balance of payments (BoP) accounts are an accounting record of all monetary transactions betweena country and the rest of the world. These transactions include payments for the coun-try's exports and imports of goods, services, financial capital, and financial transfers. The BOP ac-counts summarise international transactions for a specific period, usually a year, and are prepared ina single currency, typically the domestic currency for the country concerned. Sources of funds for anation, such as exports or the receipts of loans and investments, are recorded as positive or surplusitems. Uses of funds, such as for imports or to invest in foreign countries, are recorded as negativeor deficit items.When all components of the BOP accounts are included they must sum to zero with no overall sur- plus or deficit. For example, if a country is importing more than it exports, its trade balance will bein deficit, but the shortfall will have to be counterbalanced in other ways –

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1. Balance of paymentsBalance of payments (BoP) accounts are an accounting record of all monetary transactions betweena country and the rest of the world. These transactions include payments for the coun-try's exports and imports of goods, services, financial capital, and financial transfers. The BOP ac-counts summarise international transactions for a specific period, usually a year, and are prepared ina single currency, typically the domestic currency for the country concerned. Sources of funds for anation, such as exports or the receipts of loans and investments, are recorded as positive or surplusitems. Uses of funds, such as for imports or to invest in foreign countries, are recorded as negativeor deficit items.When all components of the BOP accounts are included they must sum to zero with no overall sur- plus or deficit. For example, if a country is importing more than it exports, its trade balance will bein deficit, but the shortfall will have to be counterbalanced in other ways – such as by funds earnedfrom its foreign investments, bay running down central bank reserves or by receiving loans fromother countries.While the overall BOP accounts will always balance when all types of payments are included, im- balances are possible on individual elements of the BOP, such as the current account, the capitalaccount excluding the central bank's reserve account, or the sum of the two. Imbalances in the lattersum can result in surplus countries accumulating wealth, while deficit nations become

increasinglyindebted. The term "balance of payments" often refers to this sum: a country's balance of paymentsis said to be in surplus (equivalently, the balance of payments is positive) by a specific amount ifsources of funds (such as export goods sold and bonds sold) exceed uses of funds (such as payingfor imported goods and paying for foreign bonds purchased) by that amount. There is said to be a balance of payments deficit (the balance of payments is said to be negative) if the former are lessthan the latter.

Under a fixed exchange rate system, the central bank accommodates those flows by buying up anynet inflow of funds into the country or by providing foreign currency funds to the foreign exchangemarket to match any international outflow of funds, thus preventing the funds flows from affectingthe exchange rate between the country's currency and other currencies. Then the net change peryear in the central bank's foreign exchange reserves is sometimes called the balance of paymentssurplus or deficit. Alternatives to a fixed exchange rate system include a managed float where somechanges of exchange rates are allowed, or at the other extreme a purely floating exchange rate (alsoknown as a purely flexible exchange rate). With a pure float the central bank does not intervene atall to protect or devalue its currency, allowing the rate to be set by the market, and the central bank's foreign exchange reserves do not change.Historically there have been different approaches to the question of how or even whether to elimi-nate current account or trade imbalances. With record trade imbalances held up as one of the con-tributing factors to the financial crisis of 2007 –

2010, plans to address global imbalances have beenhigh on the agenda of policy makers since 2009.

CONCEPTUAL FRAMEWORK AND LITERATURE REVIEWntroductionThe purpose of this chapter is three-fold: firstly, to spell out the basic concepts pertaining to theBoP; secondly, to give a review of the evolution of the BoP adjustment theory to help in under-standing how the theory has evolved over time. Thirdly, to present the various approaches to theBoP adjustment. The chapter will end with a conclusion and an analytical framework showing sometheoretical linkages between domestic credit and the BoP. In the next section, a review of some basic BoP concepts is presented. The evolution of the BoP adjustment theory is discussed in section2.3, while in section 2.4, the three approaches to the BoP imbalances are presented. An overview ofsome previous studies on the MABP will also be done in this section. The chapter will end with asummary of the theoretical framework and an analytical framework.2.1 Some definitionsThis section highlights the BoP concepts that will be frequently used in the study. To begin with,the BoP is defined as a summary statement in which, all the transactions of residents of a nationwith the rest of the world are recorded during a particular period of time, usually a calendar or fiscalyear. An international transaction refers to the exchange of a good, service, or an asset (for which payment is usually required) between the residents of one nation and the rest of the world. The main purpose of the BoP is to inform the government of the country's international position and to help itin its formulation of monetary, fiscal, and trade policies. The BoP information is also useful to banks, firms and individuals directly or indirectly involved in international trade and finance. TheBoP comprises of two main sub-accounts;. (i) the current account, which deals with trade in goods and services, andtransfers,. (ii) the capital account, which records transactions in assets and liabilities.The sum of the balances on the two accounts, after allowing for errors and omissions, is equal to theoverall balance.Current AccountThe current account of the BoP records all international flows of goods and services, as well astransfer payments. This account comprises of both visible and invisible items. The visible flowsconstitute trade in goods, whereas, invisible flows include services such as insurance, transporta-tion, banking, tourism and many others. Invisible trade also includes payments for overseas embas-sies and military bases, interest, profit and dividends from overseas investments. The difference be-tween visible exports and imports is known as the trade balance or visible balance, while the differ-ence between invisible exports and imports is called the invisible balance. In most developing coun-tries, the trade balance is the most important. Thus, the sum of the trade balance, balance on invisi- ble items and transfer payments gives the current account balance. In practice, it is usually commonto consider one account of the BoP as an indicator of the performance of the country's BoP. Moststudies have traditionally focused on the current account or trade balance as an indicator in this re-spect. Notably, the trade balance is by far the largest component of Uganda's current account. Infact, fluctuations in the trade account are the primary cause of the movements on the current ac-count. A deficit on the current account of a nation means that more goods and services have beenimported into the nation than have been

sold abroad, while a surplus on the same account meansmore goods and services have been exported than imported.A current account deficit is also defined as the difference between national savings and investments.Therefore, a deficit can emerge from either a fall in savings or an increase in investments. In thisregard, the sustainability of a given current account deficit will be affected by its source. For exam- ple, a deficit that is accompanied by high investment rates is considered to be less problematiccompared to one associated with a fall in savings (Blejer, 1999:24). This is because high invest-ments lead to increased productivity and growth in export earnings that will be available to financethe external debts. However, high investment rates could widen the cunent account deficit in theshort-term through increased demand for imported inputs, but if the investments turn out to be prof-itable, no major problems will be created in the long- run. A related issue is the relationship be-tween the rate of economic growth and the current account balance. Large current account deficitsmay be more sustainable if economic growth is high. High GDP growth tends to lead to higher in-vestments and increased net capital inflows as expected profitability increases.Capital AccountThe capital account records purchases and sales of assets, such as stocks, bonds, and land, otherthan the official reserve assets. A capital account can also be divided into two separate parts: (1) thetransactions of the private sector and (2) official reserves transactions, which correspond to the cen-tral banks activities. The capital account measures the change in the net stock of all non reserve fi-nancial assets. Financial reserves are excluded because they do not reflect changes in the marketforces, but rather changes in government policy (Salvatore, 1998:406). The outflows of money fromone country to buy stocks and shares abroad and inflows of resources into the country as foreigners buy factories and shares is recorded as net investment. Therefore, the sum of all items from net in-vestment and other net transactions infinancial assets represents the net inflows on the capital account. If a country runs a deficit in itscurrent account, or spends more abroad than it receives from sales to the rest of the world, the defi-cit needs to be financed by selling assets or foreign borrowing. The sale of assets or borrowing im- plies that the country is running a surplus on the capital account. Thus, a Current account is of ne-cessity financed by capital inflows, such that; current account deficit plus the net capital inflowsequals zero. A current account deficit can also be financed by running down the official internation-al reserves of the concerned country. However, this alternative has limitations since countries areobliged to hold a certain level of reserves with the Fund. Therefore, in the long run, governmentscould address BoP imbalances by reducing import demand or expansion of exports.Generally, persistent BoP deficits are not desirable and are an indication of macroeconomic prob-lems in the concerned economy. For example, a deficit indicates that a country's import bill and itslong-term commitments to the rest of the world (private or public or both) have exceeded its capaci-ty of meeting those obligations through foreign exchange earnings from the national exports andother inflows. Such a situation puts the country into a fundamental disequilibrium, which necessi-tates seeking for foreign borrowing (Hallwood and MacDonald, 1994:20). However, inflows of for-eign loans constitute a claim on the country's foreign reserves and if the deficit persists, all thecountry's foreign reserves may be depleted, which could lead to loss of confidence, as the country isdeclared unable to repay its foreign debts. Therefore, the BoP imbalances need to be corrected inorder to restore equilibrium in the external sector and to achieve internal macroeconomic stability.

2.2 The Balance of Payments Adjustment Theory This section is concerned with the evolution ofthe BoP adjustment theory. It is useful to examinehow this theory has evolved over time to broaden our understanding of the various adjustment poli-cies. The BoP adjustment theory has undergone extensive revision over the years. In the early peri-ods of the development path of international economics, very little attention was paid to the prob-lem of external disequilibria. Indeed, Dell and Lawrence (1980) observe that the whole range of policies that are now summed up under the heading of "adjustment process" is fairly new.Under the gold standard, it was generally believed that the trade and payments balances of countrieswould tend to move towards equilibrium automatically without the guidance any person or institu-tion (Dell and Lawrence, 1980:93). This view originated from the specie-flow analysis associatedwith the work of Hume in 17522. It was believed that there was a direct link between money sup- ply, price level and external balance. A country with a BoP deficit would lose its gold reserves, re-sulting into a fall in the monetary base and money supply. Consequently, the fall in money supplywould bring about a fall in the domestic price relative to the foreign price. The change in the rela-tive price would restrain domestic demand for imports and stimulate foreign demand for that coun-try's exports, and consequently lead to an Improvement of its BoP. However, the system did not prevent large instabilities in the prices of exports and imports and the attendant haphazard shifts inthe distribution of income among countries because it was based on unverified assumptions. Forexample, in the real world there exists trade restrictions imposed by tarifTs and other trade controls.Such weaknesses made Hume's mechanism less applicable to the BoP adjustment problem.After World War I, when the problems of resource allocation occupied the centre of the stage of theeconomic debate, Bickerdike (1920) initiated the concept of external adjustment by the ElasticityApproach. His concept was developed further in order to analyse the effects of a devaluation on thetrade balance of a devaluing country by Alexander (1952, 1959) and later became synthesised withthe Absorption Approach. The elasticity approach largely focuses on the price elasticities of de-mand and supplyof imports and exports and the Marshall-Lerner condition . It assumes a system of fixed exchangerates where a devaluation or revaluation may be used to rectify the BoP disequilibrium. However,under the Floating exchange rate regime, equilibrium is expected to be restored automatically with-out government intervention.The elasticity approach was also widely criticised, mainly for its restrictive assumptions such as the partial equilibrium analysis of the labour market and wage determination (Alexander, 1952:264).The approach proved extremely unsatisfactory in the post-war situation of general inflationary pres-sure and motivated the introduction of the income-absorption approach. This approach was largelydeveloped on the basis of research in the IMF under the guidance of Bernstein (Rhomberg and HeI-er (ed.), 1977:2-5). This approach underscores the relationship between the level of national incomeand the external sector disequilibrium, and views the balance on the current account as the differ-ence between national income and national

expenditure (absorption). However, the absorption ap- proach was also criticised for considering only the current account balance, and for ignoring the ef-fects of the changes in the exchange rates and prices. In the 1950s, attempts were made to integratethe income-absorption approach with the elasticity approach as well as toremedy the inadequacies of the elasticity approach, particularly, its partial equilibrium nature (see,inter alia, Harberger, 1950, Laursen and Matzler, 1950, Alexander, 1952, Johnson, 1956).After a period of domination by the Keynesians and the intense debates on the insufficiency of ag-gregate demand, unemployment and macroeconomic stabilisation during the post-war era, concern began to be shifted to inflation. The controversy between the Keynesians and Monetarists stronglyinfluenced the evolution of macroeconomic theory. In the 1950s, members of the University of Chi-cago led by Professor Milton Friedman spearheaded a renewal of academic interest in monetary problems, which became widely known as the "Chicago school of thought" and later became ac-cepted as "Monetarism"(Choonaratana, 1989:28). In the process, the Keynesian analytical toolswere supplemented, and in some instances replaced by the instruments of monetary an,!-lysis. Con-sequently, Polak, of the IMF laid some fundamental concepts in 1957 for the approach, which waslater called the Monetary Approach. This approach is given its most articulate exposition in a col-lection of papers edited by Frenkel and Johnson (1976). Although, there is still controversy aboutthe role of monetarism in solving problems of inflation and unemployment, the monetary approachis considered very important in the analysis of the BoP problem. Its strength lies precisely where theother approaches falter and it is relatively easy to apply. A detailed discussion of this approach is presented in section 2.5 of this chapter. The Balance of Payments Adjustment Policies

The BoP deficit can be adjusted in a number of ways. One method could be restriction imports byimposing tariffs on them. However, tariffs and other trade barriers cannot be used freely to adjustthe trade balance partly because international organisations such as the IMF, WTO and agreementslike the GATT do not support the use of such measures. Tariffs are becoming less important todayas the world moves to freer trade between nations. In the literature, there are three conventional ap- proaches to the BoP problem. The first two of these approaches are essentially Keynesian, one isthe "Elasticity Approach" or "Devaluation", it IS also referred to as Expenditure Switching". Thesecond approach is the "Income-Absorption Approach" or "Expenditure Cutting". The third ap- proach is the "Monetary Approach". All these approaches are discussed in the next part of thischapter.The Elasticity ApproachThe elasticity approach basically emerged as a short-run oriented tool of analysis to the BoP prob-lem during the inter-war period and still survives in one form or another to the present day. It con-siders how the responsiveness of imports and exports to changes in the exchange rate determinesthe extent to which devaluation can improve the current account balance from the short to long-run.The approach derives its name from the fact that the improvement in a nation's trade balance largelydepends on the price elasticity of demand for its imports and exports. It assumes a fixed exchangerate system where devaluation is expected to lower the price of a

country's exports abroad and raisethe price of imports in the domestic market resulting into a shift to home produced goods. This shiftis called expenditure switching. As already noted, for this approach to be successful, the Marshall-Lerner condition must be satisfied. However, if the change in the relative price of exports and im- ports leads to very minimal expenditure switching, for example in situations where there are nodomestic substitutes for imported goods as the case is in most LDCs, devaluation may worsen thedeficit. Under the floating exchange rate regime however, BoP equilibrium is attained without in-tervention in the exchange rate movements.The elasticity approach, therefore, considers the responsiveness of imports and exports to changesin the national currency. For example, if the import demand is highly elastic, a devaluation or de- preciation of a country's currency is expected to cause a substantial decline in imports. However, inreality, devaluation may take time to work since exports have inelastic supply, especially in theLDCs due to the nature of exports from these countries and external factors such as unfavourableterms of trade. Indeed, one might expect very little to happen to the volume of exports and importsdemanded initially as consumers take time to shift from consumption of imported to domestically produced goods. Moreover, there is limited scope for switching from imports to domestic substi-tutes in most in LDCs. Foreign consumers may also take time to adjust from domestic goods to for-eign exports. If this is the case, the BoP may actually worsen soon after devaluation, before improv-ing at a later stage. Therefore, the elasticity approach poses two problems for economic analysis;the conditions required to switch expenditure in the desired direction, and the source of the addi-tional output required to meet the increased demand for import substitutes. However, a rise in the prices of import substitutes and exports will induce domestic producers to shift production fromnon-tradable to tradable, and a shift in the labour market as well.With the passage of time, the quantity of exports rises and the quantity of imports falls, so that theinitial deterioration in a country's trade balance begins to reverse.

“Economists have called this tendency of a country's trade balance to first deteriorate before im- proving as a result of a devaluation of a country's currency, the J-curve effect" (Salvatore,1998:521). The explanation is that when a country's trade balance is plotted on the vertical axis, theresponse of the trade balance to a devaluation looks like letter J. This is demonstrated in Figure 2.1 below:The diagram above demonstrates that from the origin and a given trade balance, a devaluation of thedomestic currency will first result in a deterioration of the trade balance before an improvement isattained. Hence, even if the Marshall-Lerner condition is met, the current account may worsen inthe short-run before improving in the longer term, as noted in the outgoing discussion. However, itshould be noted that the J-curve effect is (an often, but not always) observed phenomenon.The Absorption ApproachThis approach is based on the Keynesian school of thinking and holds the view that the BoP islinked to changes in real domestic income (Choonaratana, 1989:29). Johnson also explains the es-sence of this approach as "a relation between the aggregate receipts and expenditures of the

econo-my, rather than as a relation between the country's credits and debits on international ac-count"(Johnson, 1976:47). Its formal development is credited to Alexander (1952) who named itAbsorption Approach, though many others contributed . He began with the identity that productionor income (Y) is equal to consumption (C) plus domestic investment (I) plus the trade balance (X-M), all in real in terms as an extension of the Keynesian Income/Output model.That is;Y = C + I + (X-M) (2.1)But then letting A equal domestic absorption, (C+I) and B equal the trade balance, (X- M) in equa-tion (2.1) yields;Y = A + B, (2.2)By subtracting A from both sides of (2.2), we get;Y-A=B (2.3)That is, domestic production/income minus absorption equals the trade balance. The formulationalso suggests that policies for correcting a trade imbalance can be broadly classified into two cate-gories; those aimed at increasing production (output- increasing), and those which aim at reducingexpenditure/absorption (expenditure- reducing). However, if a nation is at full employment, produc-ion or real income (Y) cannot rise and devaluation can only be effective if domestic absorption (A)falls, either automatically or as a result of contractionary fiscal and monetary policies (Salvatore,1998:559). In other words, a current account deficit is reduced through the implementation of poli-cies that reduce aggregate demand. However, LDCs normally have unemployed resources availa- ble, the additional output required to meet the increased demand could be provided by the re-absorption of these resources into employment. Under such circumstances, expenditure switchingcould increase employment and income. ]n this regard, the elasticity and absorption approaches areimportant and can be considered simultaneously.A devaluation of the exchange rate can affect the foreign balance (B), in two ways. Firstly; it canlead to a change in income (Y), which in turn induces a change in absorption (A). To this end, achange in the foreign balance will be composed of changes in both income and absorption. Second-ly, a devaluation may change absorption for any given level of real income. Thus, while the elastici-ty approach stresses the demand side and implicitly assumes that the economy adjusts to satisfy theadditional demand for exports and imports substitutes, the absorption approach stresses the supplyside and implicitly assumes adequate demand for the country's exports and import substitutes. The Monetary Approach to the Balance of Payments (MABP)

Development of the Monetary ApproachThe MABP has "a long, solid, and academically overwhelmingly reputable history" (Frenkel andJohnson (1976:29). It is one of the approaches that were developed in the 1950s and the early 1970swith a view of understanding the sequences of economic events that lead countries into BoP prob-lems and the policy measures that could prevent or correct such distortions. These changes reflectedthe dissatisfaction with the macroeconomic management, which was still dominated by the Keynes-ian thinking and its explanation of the economic problems. Many advocates of the MABP associateits roots to David Hume (1752), see Frenkel and Johnson, 1976:147-148. However, its modern formis linked to economists from the Research Department of the IMF, University of Chicago, and theLondon School of Economics. The list includes Mundell, Johnson, Polak, Frenkel, Mussa, andDornbusch among others. Some of the key factors that contributed to renewed interest in the area ofBoP adjustments were the policy challenges that were encountered by policy makers. Rhombergand Heller, (1977:6) note that the initial impetus towards research in this area came from the IMFstaff's work on problems of LDCs,

which at the time lacked the detailed national accounts data re-quired to analyse the BoP problem using the absorption and elasticity approaches. However, sincemonetary and payments statistics were available in most countries, there was a need to develop aframework that could utilise this database. In addition, there was a need to develop a quantitativeframework that would be manageable during staff missions during the period before wide access tocomputers. Therefore, the monetary approach was particularly considered appropriate in this re-spect.The Theoretical Framework of the Monetary ApproachThe task of this section is to examine the theoretical framework of the MABP. It attempts to explorethe theoretical propositions and assumptions on which the approach is based. The modern theoreti-cal foundation of the monetary approach is traced back to the work of Mundell (1968, 1971) at theUniversity of Chicago, Johnson, and other economists who have been working along similar lines.The MABP views the BoP as an essentially monetary phenomenon (Frenkel and Johnson, 1976:21)."Payments adjustment is viewed in terms of monetary adjustment instead of relative price and in-come changes", (Buzakuk, 1988:52). In other words, the MABP stresses the importance of mone-tary variables in explaining the changes in the BoP. The term "balance of payments" as a starting point is implicitly defined by MABP theorists as a set of items that are "below the line" in the over-all balance of payments. These items in principle constitute the "money account". Essentially, theMABP is a supply and demand analysis of the money market in an open economy (Taylor,1990:32). Thus, any excess demand or supply of money is exactly reflected in the movements inBoP. Accordingly, surpluses in the trade account and the capital account respectively reflect excessflows of goods and securities, while a surplus in the money account represents an excess domesticflow of demand for money. Consequently, when analysing the rate of increase or decrease in acountry's foreign reserves, the MABP focuses on the determinants of the excess domestic t10w de-mand or supply of money, where supply is believed to bc composed of international reserves anddomestic credit. Taylor (1990) observes that a BoP surplus emerges, if the domestic component ofthe monetary base is not adjusted in a situation where the demand for money exceeds its actualstock. In this case, money will be sucked into through the external account as individuals attempt toincrease their money balances.In the simplest empirical formulation of the MABP, most expositions assume a small open econo-my, in which a stable demand for money balances is determined by the price level, real income, andinterest rate, while the supply of money equals the money multiplier times high powered money(reserves plus domestic credit). In short,

Money demand, Md = L(p, y, r)Money supply, Ms = meR + D)so that in equilibrium, (Md = Ms); L(p, y, r)meR + D)Where, p - price level, y - real income, r - interest rate, m - multiplier, R - reserves and D - domesticcredit, (see Taylor, 1990:33). This formulation is based on the flow equilibrium condition for themoney market (Johnson, 1972). The basic message of the MABP as Taylor observed is that, thedomestic credit level should be high enough to satisfy the demand for the domestic money stock, toavoid payments disequilibria. Similarly, the MABP considers a deficit in the BoP as a consequenceof an excess in the domestic money stock over what is required in the economy. A variation in thesupply of money relative to its demand is associated with payments problems. Therefore, in theevent of a monetary disturbance, the MABP states that the international reserves component willcarry the burden of equating the demand for and supply of money. However, it should be noted thatauthorities can influence the domestic composition of the money stock, particularly under the fixedexchange rate regime. Under the flexible exchange rate system, attention is shifted from the BoP(which is always zero), to changes in the exchange

rate, which moves up and down toabsorb the consequences of policy and other changes, which would afTect the BoP under a fixedexchange rate system (Mussa, 1976:189). On the other hand, under a managed float system as in thecase of Uganda, monetary authorities can intervene in the foreign exchange market to moderate themovements in the exchange rate. Thus, under a managed float, the adjustment in official reserves isusually proportional to the degree of intervention in the foreign exchange market to influence thelevel and movement of exchange rate not, the BoP deficit.The Adjustment MechanismIn an open economy, the BoP plays an important role in determining changes in the stock of domes-tic money and it is viewed as part of the adjustment mechanism that works to restore equilibrium inthe money market (Buzakuk, 1988:57). According to the MABP, the adjustment works in such away that when an economy is initially in equilibrium, and runs a current account deficit, it wouldmean that the country has excess demand for goods and serVIces or national investment exceedsnational savings. Normally, external resources or increased domestic savings can finance this gap.On the other hand, a deficit in the capital account is an indication' of an excess demand in the coun-try's bond markets, which could be satisfied by importing more securities into the country than whatis being sold to the outside world. While according to Walras' law , if country runs a deficit on theoverall balance, it musthave an excess supply in the money market. The MABP views the BoP disequilibrim as a mecha-nism by which an excess supply of (demand for) money is removed from the domestic market. Forinstance, increases in the level of domestic credit result into growth in the money supply and distortthe monetary equilibrium. In order to restore equilibrium in the money market, the public needs todispose of the excess quantity of money over time by buying foreign goods. The direct effect ofsuch an action is a BoP deficit and running down the country's foreign reserves. The loss of reservesreduces the quantity of money and eliminates the excess supply over time. Therefore, when an ex-ogenous shock occurs, particularly under a fixed exchange rate regime, the adjustment process be-gins and keeps working until the excess supply of (demand for) money disappears and equilibriumis restored. At that point, the flow demand for goods and bonds match their flow supplies and theeconomy achieves equilibrium and payments balance (Buzakuk, 1988:59). Therefore, the monetaryauthorities need to monitor domestic credit creation to prevent a surge in money supply in the econ-omy.It should however be noted that the nature of adjustment greatly depends on the type of exchangerate regime in a particular country. In a fixed exchange rate system, adjustment is through changesin the BoP, whereas in a flexible exchange rate system, equilibrium in the money market is restoredthrough movements in the exchange rate. In the case of a managed t10at, the authorities usually in-tervene in the market using official reserves and the change in reserves is proportional to the degree of intervention in the foreign exchange market. Further expositions can be found in the work edited by Frenkel and Johnson, 1976, and Mundell, 1968.

The Structural Approach to the Balance of PaymentsOriginThis approach to the Balance of Payments arose from a consideration of developing countries, buthas also been applied to developed countries.

Principal Elements1. Distrust in the operation of markets. Balance of payments imbalances often arise from structuralimbalances within the economy which arise because growth and development involve continu-ous processes of structural change.These may lead to:(a) different regions growing at different speeds e.g. in the UK, the Southeast growing faster thanthe Northeast. High income in the Southeast leads to increased demand for imports, which cannot be produced in the Northeast. The lack of mobility of labour ensures that the imbalance remains.(b) different sectors growing at different speeds, causing supply bottlenecks e.g. in developingeconomies, urban sectors may grow rapidly, but agricultural sectors may be unable to adjust rapid-ly, leading to the increased import of food.(c) changing patterns of demand. Countries may be unable to shift resources away from productsthat are no longer competitive internationally into new products for which prospects appear bright-er. That is, imbalance is caused by the structural characteristics of goods on the supply side of themarket. Adjustment through changing prices (including through exchange rate variations) may beslow and ineffective in eliminating the disequilibrium. Thus, both traditional Keynesian and mone-tarist policies will be ineffective in overcoming balance of payments problems.2. Stress is placed, therefore, on the characteristics of imports and exports. Particular problems willarise where:(a) a country's exports are income-inelastic: as world income rises, the demand for exports does notkeep pace (old heavy industries: shipbuilding etc);(b) its imports are income-elastic: growth leads directly to balance of payments deficits (essentialraw materials, foreign-produced consumer goods, energy sources).3. It follows that the country's goods are non-competitive on non-price grounds. The elasticities andother approaches are generally concerned with price-competitiveness. Here, rather, the stress is onquality, delivery dates, after-sales service etc. Depreciation of the exchange rate, thus improving price-competitiveness, will only be of temporary assistance. The long-run decline continues becauseof non-price competitiveness. This is often due to inadequate investment and/or inadequate trainingof the work-force.These problems are often circular. For example, a structural problem arises leading to a balance of payments deficit. Traditional expenditure-switching or expenditure-reducing policies are followed.In the first case, depreciation leads to domestic inflation, which rapidly erodes any improvement in price competitiveness. In the second case, expenditure reduction may be achieved:(a) through increases in interest rate, but these lead to lower investment and industry becomes lesscompetitive on non-price grounds; or(b) through lower government expenditure or higher tax rates but lower government expendituremay lead to a deteriorating infrastructure again reducing non-price competitiveness. However re-duced income is achieved, it will be associated with higher unemployment and this may lead to lackof confidence in the economy and again to lower investment. Consider, alternatively, a developingcountry case:Worsening agricultural terms of trade leads to a balance of payments deficit, which in turn leads toa shortage of foreign exchange. This means the lack of ability to buy imported capital equipmentnecessary to diversify into other industries or to increase the productivity of already existing indus-tries.All this means that growth may induce balance of payments problems and that such problems mayact as a

constraint on further growth. Within developed countries, Balance of Payment constrainedgrowth may lead to deindustrialization and the shrinking of the country

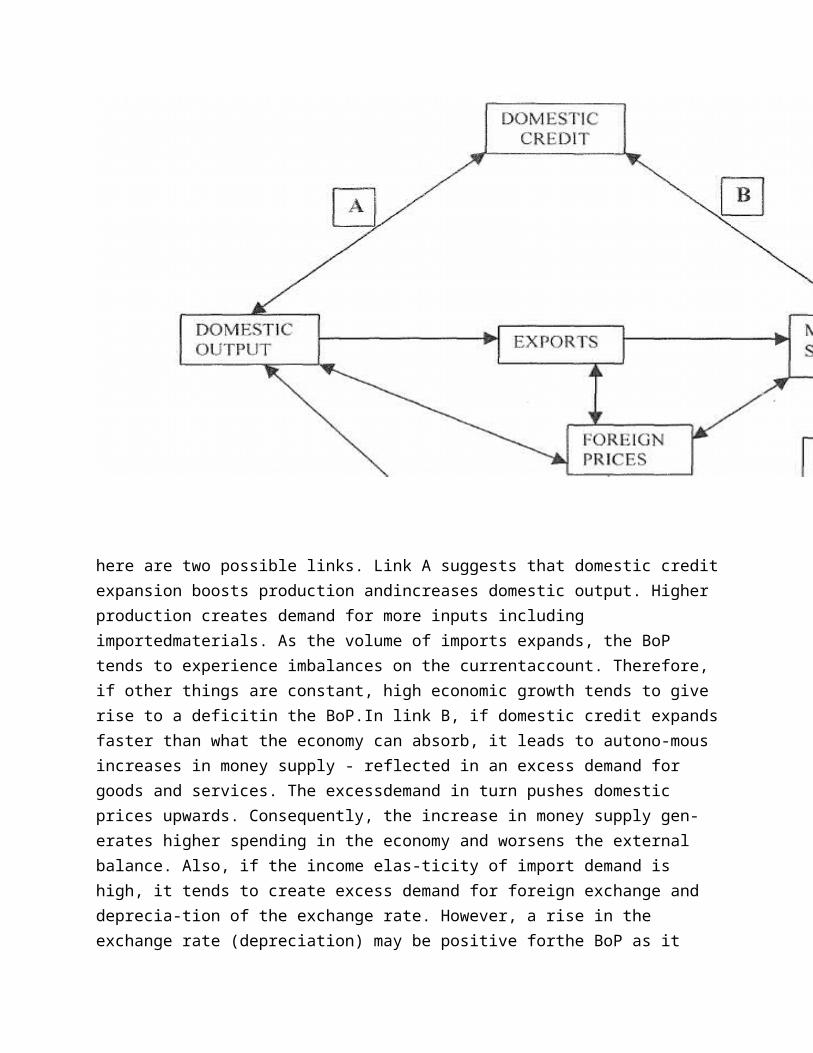

’s manufacturing base.The Structural Approach and Economic PolicyThe situation requires:(a) government intervention: government investment in order to improve non-price competitivenessand to foster a switch from exports with low income-elasticities to industries with high income-elasticities;(b) selected import controls to protect industries while they improve non-price competitiveness;(c) possibly exchange controls to help ration scarce foreign exchange.Criticisms of the approach include:(a) it adopts too pessimistic a view of the ability of a developing country to switch resources to theexport sector in line with changes in comparative advantage;(b) it underestimates the extent to which resources can be transferred through the price mechanism;c) assumptions about the possibilities of substitution between domestic and foreign inputs may betoo rigid.The Analytical Framework showing some of the possible linkages between domesticcredit and the BoP:

here are two possible links. Link A suggests that domestic credit expansion boosts production andincreases domestic output. Higher production creates demand for more inputs including importedmaterials. As the volume of imports expands, the BoP tends to experience imbalances

on the currentaccount. Therefore, if other things are constant, high economic growth tends to give rise to a deficitin the BoP.In link B, if domestic credit expands faster than what the economy can absorb, it leads to autono-mous increases in money supply - reflected in an excess demand for goods and services. The excessdemand in turn pushes domestic prices upwards. Consequently, the increase in money supply gen-erates higher spending in the economy and worsens the external balance. Also, if the income elas-ticity of import demand is high, it tends to create excess demand for foreign exchange and deprecia-tion of the exchange rate. However, a rise in the exchange rate (depreciation) may be positive forthe BoP as it improves the competitiveness of the country's exports. The opposite is true for an ap- preciation.In summary, growth in domestic output is expected to lead to a deterioration of the BoP (mainly thetrade balance), since it increases demand for goods and services, particularly imports. Also, exces-sive credit expansion leads to payments imbalances as the residents dispose of the extra money byspending it on goods and services. On the other hand, as the economy grows, the demand for moneyincreases, arid if there is no autonomous increase in money supply, a BoP surplus will be observedas the additional money is fed into the economy.

3 3.1 STRUCTURE OF BALANCE OF PAYMENTSThe Balance of Payment (BOP) of a country is a systematic account of all economic transactions between a country and the rest of the world, undertaken during a specific period of time. BOP is thedifference between all receipts from foreign countries and all payments to foreign countries. If thereceipts exceed payments, then a country is said to have favourable BOP, and vice versa.According to Charles Kindle Berger "The BOP of a country is a sy

DIAGRAM stematic recording of all economic transactions between residents of that country and the rest ofthe world during a given period of time".The Balance of payments record is maintained in a stand-ard double - entry book - keeping method. International transactions enter into record as credit ordebit. The payments received from foreign countries enter as credit and payments made to othercountries as debit. The following table shows the elements of BOP.BALANCE OF PAYMENTS ACCOUNT1. Trade Balance :-Trade balance is the difference between export and import of goods, usually referred as visi- ble or tangible items. If the exports are more than imports, there will be trade surplus and if importsare more than exports, there will be trade deficit. Developing countries have most of the time suf-fered a deficit in their balance of payments. The trade balance forms a part of current account. In2008-09, trade deficit of India was 118.6 US $ billion.2.

Current Account Balance :-It is the difference between the receipts and payments on account of current account whichincludes trade balance. The current account includes export of services, interest, profits, dividendsand unilateral receipts from abroad and the import of services, profits, interest, dividends and uni-lateral payments abroad. There can be either surplus or deficit in current account. When debits aremore than credits or when payments are more than receipts deficit takes place. Current account sur- plus will take place when credits are more and debits are less.Current account balance is very significant. It shows a country's earning and payments inforeign exchange. A surplus balance strengthens the country's international financial position. Itcould be used for development of the country. A deficit is a problem for any country but it creates aserious situation for developing countries. In 2009-10 India’s current account deficit was 38.4 US $ billion.3. Capital Account Balance :-It is the difference between receipts and payments on account of capital account. The trans-actions under this title involves inflows and outflows relating to investments, short term borrowing-sI lending, and medium term to long term borrowings / lending. There can be surplus or deficit incapital account. When credits are more than debits surplus will take place and when debits are morethan credits deficit will take place. In 2009-10. India’s capital account surplus was 51.8 US $ bil-lion.4. Errors and Omissions :-The double entry book - keeping principle states that for every credit, there is a correspond-ing debit and therefore, there should be a balance in BOP as well. In reality BOP may not balance,due to errors and omissions. Errors may be due to statistical discrepancies (differences) and omis-sions may be due to certain transactions may not get recorded. For Eg., remittance by an Indianworking abroad to India may not get recorded etc. If the current and capital account shows a surplusof 20,000 $, then the BOP should show an increase of 20,000 $. But, if the statement shows an in-crease of 22,000 $, then there is an error or omission of 2,000 $ on credit side.5. Foreign Exchange Reserves :-The balance of foreign exchange reserve is the combined effect of current and capital ac-count balances. The reserves will increase when:-a)

The surplus capital account is much more than the deficit in current account. b) The surplus in current account is much more than deficit in capital account.c) Both the current account and capital account shows a surplus.In 2009-10 India’s foreign exchange reserves increased by 13.4 US $ billion..2 EQUILIBRIUM AND DISEQUILIBRIUM IN BOP Balance of payments is the difference between the receipts from and payments to foreigners by residents of a country. In accounting sense balance of payments, must always balance. Debitsmust be equal to credits. So, there will be equilibrium in balance of payments.Symbolically, B = R - PWhere : - B = Balance of PaymentsR = Receipts from ForeignersP = Payments made to ForeignersWhen B = Zero, there is said to be equilibrium in balance of payments.When B is positive there is favourable balance of payments; When &. B is negative there isunfavourable or adverse balance of payments.' When there is a surplus or a deficit in balance of payments there is said : to be disequilibrium in balance of payments. Thus disequilibrium refers toimbalance in balance of payments.Meaning of Disequilibrium in Balance of PaymentThough the credit and debit are written balanced in the balance of payment account, it may not re-main balanced always. Very often, debit exceeds credit or the credit exceeds debit causing an im- balance in the balance of payment account. Such an imbalance is called the disequilibrium. Disequi-librium may take place either in the form of deficit or in the form of surplus.Disequilibrium of Deficit arises when our receipts from the foreigners fall below our payment toforeigners. It arises when the effective demand for foreign exchange of the country exceeds its sup- ply at a given rate of exchange. This is called an 'unfavourable balance'.Disequilibrium of Surplus

arises when the receipts of the country exceed its payments. Such a situa-tion arises when the effective demand for foreign exchange is less than its supply. Such a surplusdisequilibrium is termed as 'favourable balance’.3.3 TYPES OF DISEQUILIBRIUM IN BOPThe following are the main types of disequilibrium in the balance of payments:-1. Structural Diseguilibrium :-Structural disequilibrium is caused by structural changes in the economy affecting demandand supply relations in commodity and factor markets. Some of the structural disequilibrium are asfollows :-a. A shift in demand due to changes in tastes, fashions, income etc. woulddecrease or increase the demand for imported goods thereby causing adisequilibrium in BOP. b. If foreign demand for a country's products declines due to new and cheaper substitutesabroad, then the country's exports will decline causing a deficit.c. Changes in the rate of international capital movements may also cause structuraldisequilibrium.d. If supply is affected due to crop failure, shortage of raw-materials, strikes, political instabil-ity etc., then there would be deficit in BOP.e. A war or natural calamities also result in structural changes which may affect not only goods but also factors of production causing disequilibrium in BOP.f. Institutional changes that take place within and outside the country may result in BOPdisequilibrium. For Eg. if a trading block imposes additional import duties on products imported inmember countries of the block, then the exports of exporting country would be restricted or re-duced. This may worsen the BOP position of exporting country. 2. Cyclical Disequilibrium :-Economic activities are subject to business cycles, which normally have four phases Boomor Prosperity, Recession, Depression and Recovery. During boom period, imports may

increaseconsiderably due to increase in demand for imported goods. During recession and depression, im- ports may be reduced due to fall in demand on account of reduced income. During recession exportsmay increase due to fall in prices. During boom period, a country may face deficit in BOP on ac-count of increased imports.Cyclical disequilibrium in BOP may occur becausea. Trade cycles follow different paths and patterns in different countries. b. Income elasticities of demand for imports in different countries are not identical.c. Price elasticities of demand for imports differ in different countries.3. Short - Run Disequilibrium :-This disequilibrium occurs for a short period of one or two years. Such BOP disequilibriumis temporary in nature. Short - run disequilibrium arises due to unexpected contingencies like failureof rains or favourable monsoons, strikes, industrial peace or unrest etc. Imports may increase ex- ports or exports may increase imports in a year due to these reasons and causes a temporary disequi-librium exists.International borrowing or lending for a short - period would cause short - run disequilibri-um in balance of payments of a country. Short term disequilibrium can be corrected through short -term borrowings. If short - run disequilibrium occurs repeatedly it may pave way for long - run dis-equilibrium. 4. Long - Run I Secular Disequilibrium :-Long run or fundamental disequilibrium refers to a persistent deficit or a surplus in the bal-ance of payments of a country. It is also known as secular disequilibrium. The causes of long - termdisequilibrium area. Continuous increase in demand for imports due to increasing population. b.

Constant price changes - mostly inflation which affects exports on continuous basis.c. Decline in demand for exports due to technological improvements in importing countries, and assuch the importing countries depend less on imports.The long run disequilibrium can be corrected by making constant efforts to increase ex- ports and to reduce imports.5. Monetary DiseguilibriumMonetary disequilibrium takes place on account of inflation or deflation. Due to inflation, prices of products in domestic market rises, which makes exports expensive. Such a situation mayaffect BOP equilibrium. Inflation also results in increase in money income with people, which inturn may increase demand for imported goods. As a result imports may turn BOP position in dise-quilibrium. 6. Exchange Rate Fluctuations :-A high degree of fluctuation in exchange rate may affect the BOP position. For Eg. if Indi-an Rupee gets appreciated against dollar, then Indian exporters will receive lower amounts of for-eign exchange, whereas, there will be more outflow of foreign exchange on account of higher im- ports. Such a situation will adversely affect BOP position. But, if domestic currency depreciatesagainst foreign currency, then the BOP position may have positive impact.44.1 CAUSES OF DISEQUILIBRIUM IN B O PAny disequilibrium in the balance of payment is the result of imbalance between receipts and pay-ments for imports and exports. Normally, the term disequilibrium is interpreted from a negative an-gle and therefore, it implies deficit in BOP.The disequilibrium in BOP is caused due to various factors. Some of them areI. Import - Related CausesThe rise in imports has been the most important factor responsible for large BOP deficits.The causes of rapid expansion of imports are :-1. Population GrowthPopulation Growth may increase the demand for imported goods such as food items andnon food items, to meet their growing needs. Thus, increase in imports may lead to BOP disequilib-rium.2. Development ProgrammeIncrease in development programmes by developing countries may require import of capi-tal goods, raw materials and technology. As development is a continuous process, imports of theseitems continue for a long time landing the developing countries in BOP deficit.3.

Imports Of Essential ItemsCountries which do not have enough supply of essential items like Crude oil or Capitalequipments are required to import them. Again due to natural calamities government may resort toheavy imports, which adversely affect the BOP position.4. Reduction Of Import DutiesWhen import duties are reduced, imports becomes cheaper as such imports increases. Thisincreases the deficit in BOP position.5. InflationInflation in domestic markets may increase the demand for imported goods, provided theimported goods are available at lower prices than in domestic markets.6. Demonstration EffectAn increase in income coupled with awareness of higher living standard of foreigners, in-duce people at home to imitate the foreigners. Thus, when people become victims of demonstrationeffect, their propensity to import increases.II. Export Related Causes :- Even though export earnings have increased but they have not been sufficient enough tomeet the rising imports. Exports may reduce without a corresponding decline in imports. Followingare the causes for decrease in exports1. Increase In Population :- Goods which were earlier exported may be consumed by rising population. This reducesthe export earnings of the country leading to BOP disequilibrium.2. Inflation :- When there is inflation in domestic market, prices of export goods increases. This reducesthe demand of export goods which in turn results in trade deficit.3. Appreciation Of Currency

:-Appreciation of domestic currency against foreign currencies results in lower foreign ex-change to exporters. This demotivates the exporters. 4. Discovery Of Substitutes :- With technological development new substitutes have come up. Like plastic for rubber, syn-thetic fibre for cotton etc. This may reduce the demand for raw material requirement. 5. Technological Development :-Technological Development in importing countries may reduce their imports. This can be possible when they start manufacturing goods which they were exporting earlier. This will have anadverse effect on exporting countries.6. Protectionist Trade Policy :- Protectionist trade policy of importing country would encourage domestic producers by giv-ing them incentives, whereas, the imports would be discouraged by imposing high duties. This willaffect exports. III. Other Causes :-1. Flight of Capital Due to speculative reasons, countries may lose foreign exchange or gold stocks. Investorsmay also withdraw their investments, which in turn puts pressure on foreign exchange reserves. 2. Globalisation Globalisation and the rules of WTO have brought a liberal and open environment in globaltrade. It has positive as well as negative effects on imports, exports and investments. Poor countriesare unable to cope up with this new environment. Ultimately they become loser and their BOP isadversely affected.3. Cyclical Transmission International trade is also affected by Business cycles. Recession or depression in one ormore developed countries may affect the rest of the world. The negative effects of trade cycle

(lowincome, low demand, etc.) are transmitted from one country to another. For eg. The current finan-cial crisis in U.S.A. is affecting the rest of the world. 4. Structural Adjustments Many countries in recent years are undergoing structural changes. Their economies are be-ing liberalised. As a result, investment, income and other variables are changing resulting in chang-es in exports and imports. 5. Political factorsThe existence of political instability may result in disrupting the productive apparatus of thecountry causing a decline in exports and increase in imports. Likewise, payment of war expensesmay also serious affect disequilibrium in the country’s BOP. Thus political factors may also pro-duce serious disequilibrium in the country’s BOPs.3.2 Methods of correcting disequilibrium in the balance of paymentsThere are several methods to correct balance of payment disequilibrium. The methods depend onthe nature and causes of disequilibrium.The methods can be classified into two groups: viz. monetary and non monetary methodsMonetary methodsMonetary methods of correction affect the balance payments by changing the value or flow of cur-rencies; both domestic and foreign. Indirectly, it affects the volume and value of exports and im- ports. With flexible exchange rate it is possible to affect the value and volume of exports and im- ports.Following are the various monetary methods of BOP correction:1. DevaluationDevaluation refers to deliberate try made by using monetary authorities to bring down the worth ofhome foreign money towards foreign exchange. while depreciation is a spontaneous fall due to in-teractions of market forces, devaluation is professional act enforced with the aid of the financial au-thority. in most cases the international monetary fund advocates the coverage of devaluation as acorrective measure of disequilibrium for the countries going through adversarial steadiness of fee position. When India’s balance of fee worsened in 1991, IMF steered devaluation. for that reason,the worth of Indian forex has been reduced with the aid of 18 to twenty% relating to quite a lot ofcurrencies. The 1991 devaluation introduced the specified impact. The very next yr the import de-clined whereas exports picked up.

When devaluation is effected, the worth of house forex goes down in opposition to foreign curren-cy, let us believe the trade fee continues to be $1 = Rs. 10 before devaluation. let us suppose, deval-uation takes situation which reduces the worth of residence currency and now the exchange priceturns into $1 = Rs. 20. After this sort of exchange our items turns into cheap in overseas market. itis because, after devaluation, dollar is exchanged for extra Indian currencies which push up the de-mand for exports. at the same time, imports grow to be dearer as Indians need to pay more curren-cies to obtain one buck. hence demand for imports is lowered.Typically devaluation is resorted to where there’s severe adverse steadiness of cost drawback. Boundaries of Devaluation :- 1. Devaluation is successful simplest when different us of a does now not retaliate the identical. Ifeach the countries go for the same, the impact is nil. 2. Devaluation is successful most effective when the demand for exports and imports is elastic. Incase it is inelastic, it is going to flip the placement worse. 3. Devaluation, although helps correcting disequilibrium, is thought to be to be a weak point forthe usa. 4. Devaluation may bring inflation within the following prerequisites :- 1. Devaluation brings the imports down, When imports are diminished, the home supply ofsuch items need to be elevated to the identical extent. If no longer, shortage of such goodsunleash inflationary developments. 2. A rising usa like India is capital thirsty. due to non availability of capital items in India,we have no option but to proceed imports at greater prices. this will force the industriesdepending upon capital goods to push up their costs. 3. When demand for our export rises, increasingly goods produced in a country would go forexports and thus developing scarcity of such items at the home stage. This ends up in ris-ing prices and inflation. 4.

Devaluation is probably not effective if the deficit arises due to cyclical or structuralchanges. 2. Pegging Operations• Pegging down the value of currency is done by the Government. The Central bank de- pending on the need may artificially, increase or decrease the value of currency, tempo-rarily.Pegging operations can be done any number of times. Since it is done by the Government,it may be beneficial. It is reversible; it offers the Government the flexibility to manage thevalue of the currency for its advantage.DeflationDeflation method falling costs. Deflation has been used as a measure to correct deficit disequilibri-um. a country faces deficit when its imports exceeds exports.Deflation is introduced via financial measures like financial institution price coverage, open marketoperations, etc or through fiscal measures like larger taxation, reduction in public expenditure, andso forth. Deflation would make our objects more cost effective in international market resulting aupward thrust in our exports. on the similar time the calls for for imports fall due to greater taxationand reduced earnings. this is able to constructed a favourable environment within the steadiness offee position. then again Deflation can be a success when the exchange charge remains fixed.Exchange Controls1. Deliberate management of exchange markets, value, and volumes of currencies form the ex-change controls. There are several methods of exchange controls which can affect thevalue and flows of currencies for improving the BOP position.2. Exchange controls include methods like, pegging operations, multiple exchange rates, mutualclearing agreements etc.3. It can be seen that, monetary methods of correcting BOP disequilibrium aim at solving the crisison capital account and directly managing flow of foreign exchange. Indirectly, the valuef currency can bring equilibrium on current account as well by changing volume of ex- ports and imports.Non-financial Measures for Correcting the BoPA deficit united states of america along with financial measures may undertake the following non-monetary measures too so as to both prohibit imports or promote exports.1. TariffsTariffs are obligations (taxes) imposed on imports. When tariffs are imposed, the prices of importswould raise to the extent of tariff. The elevated prices will reduced the demand for imported goodsand at the same time result in domestic producers to provide more of import substitutes. Non-veryimportant imports will also be significantly lowered by using imposing an extraordinarily excessivefee of tariff.Drawbacks of Tariffs

:- 1. Tariffs deliver equilibrium through reducing the volume of exchange. 2. Tariffs impede the expansion of world exchange and prosperity. 3. Tariffs don’t need to essentially cut back imports. hence the effects of tariff on the steadiness ofcost position are uncertain. 4. Tariffs are trying to find to establish equilibrium without disposing of the foundation causes ofdisequilibrium. 5. a new or the next tariff may worsen the disequilibrium within the stability of payments of a rus-tic already having a surplus.. Tariffs to be successful require an efficient & sincere administration which sadly is tough tohave in most of the international locations. Corruption among the many administrative group ofworkers will render tariffs ineffective. 2. QuotasUnderneath the quota machine, the federal government may fix and permit the utmost amount or price of a commodity to be imported all over a given length. with the aid of limiting imports duringthe quota machine, the deficit is diminished and the stability of payments place is greater.Sorts of Quotas :- 1. the tariff or custom quota, 2. the unilateral quota, 3. the bilateral quota, 4.

the mixing quota, and 5. import licensing. Deserves of Quotas :- 1. Quotas are more effective than tariffs as they’re certain. 2. they’re simple to enforce. 3. they are simpler even when demand is inelastic, as no imports are that you can imagine abovethe quotas. 4. more versatile than tariffs as they’re topic to administrative resolution. Tariffs on the other handare topic to legislative sanction. Demerits of Quotas :-1. they aren’t lengthy-run answer as they don’t tackle the real cause for disequilibrium.2. below the WTO quotas are discouraged.3. Implements of quotas is open invitation to corruption.3. Export promoting

The federal government can undertake export advertising measures to proper disequilibrium in thestability of payments. This includes substitutes, tax concessions to exporters, advertising facilities,credit score and incentives to exporters, and so forth. The federal government might also assist toadvertise export through exhibition, change festivals; conducting advertising research & throughoffering the required administrative and diplomatic assist to faucet the possible markets.4. Import SubstitutionA rustic may motel to import substitution to scale back the quantity of imports and make it self-reliant. Fiscal and financial measures could also be adopted to inspire industries producing importsubstitutes. Industries which produce import substitutes require special consideration in the type ofquite a lot of concessions, which include tax concession, technical assistance, subsidies, providingscarce inputs, etc. Non-monetary strategies are simpler than financial methods and are generallyacceptable in correcting an antagonistic steadiness of payments.Drawbacks of Import Substitution :-1. Such industries could lose the spirit of competitiveness.2. home industries playing more than a few incentives will increase vested pursuits and ask for such con-cessions all the time.3. Deliberate merchandising of import replace industries go against the theory of comparative benefit.

ConclusionIn short, correction of disequilibrium calls for a judicious mix of the following methods:. a) Monetary and fiscal changes affecting income and price in the country;. b) Exchange rate adjustment, i.e., depreciation or appreciation of the home currency;. c) Trade restrictions, i.e., tariffs, quotas, etc.;. d) Capital Movements, i.e., borrowing or lending abroad.No reliance can be placed on any single tool. There is room for more than one approach and formore than one device. But the application of the tool depends on the nature of disequilibrium. Thereare four types of disequilibrium, two in income (cyclical and secular) and two in prices or structural(at the goods and factor level). It is more appropriate that the cyclical and secular disequilibria betackled by monetary and fiscal measures. In structural disequilibria, exchange rate adjustment playsa greater role. Generally, trade restrictions should be avoided. Capital movements by time in short-run disturbances and are needed to offset deep-seated forces in secular disequilibrium.The main methods of desirable adjustments are, therefore, a monetary and fiscal policy which di-rectly affects income, and exchange depreciation which affects prices in the first instance. It canalso have income effect through price effects. Monetary and fiscal policies affect relative prices al-so.Bibliography

1) www.rbi.org.in2) en.wikipedia.org/wiki/Balance_of_payments3) http://kalyan-city.blogspot.com4) www.economicshelp.org5) www.preservearticles.com

Related Documents