Bloomberg Intelligence Health Care Outlook

Bloomberg Intelligence: US Healthcare Outlook 2015

Jul 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Bloomberg IntelligenceHealth Care Outlook

Let’s examine some intriguing trends expected for 2015 in the

health care sector:

Managed Care

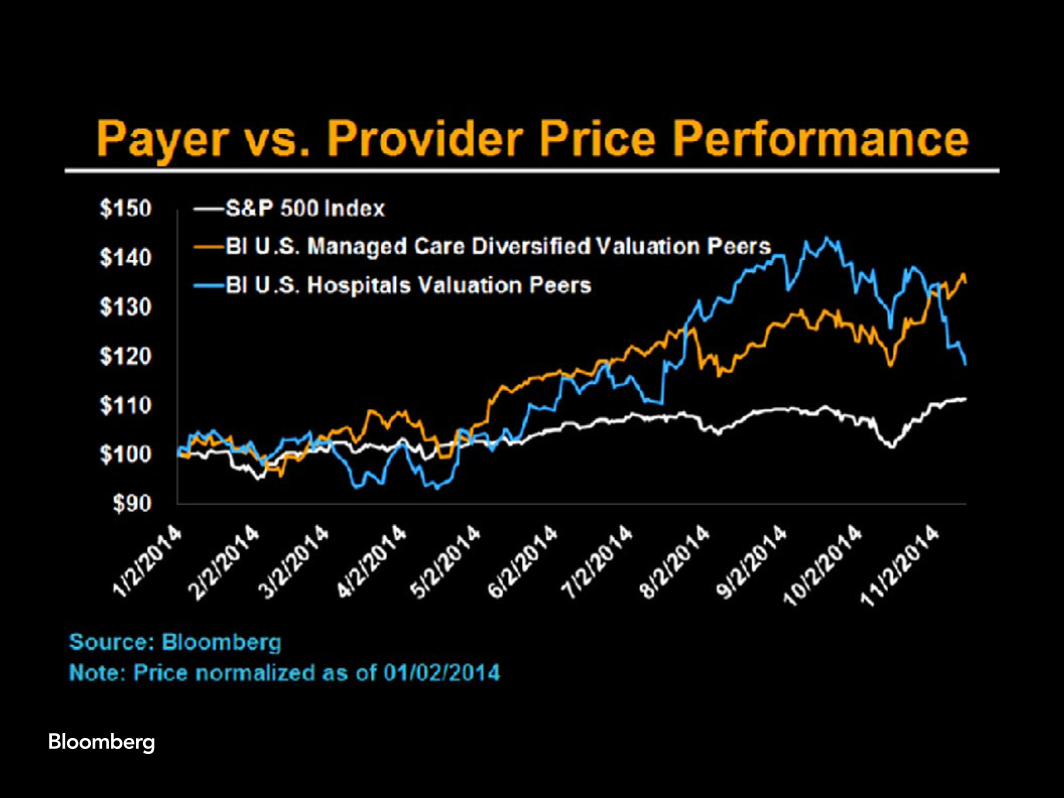

Payers Square Off With Providers as Obamacare Enters Second Year

A simultaneous rally for managed-care payers and providers is uncommon; the launch of the Affordable Care Act, which may provide health insurance to 26 million Americans, provided a boost to both. As the benefit of the new law unfolds, investors may need to assess which one – payer or provider – will obtain more favorable contract pricing.

Managed-care payers (up 35%) and hospitals (up 18%) have outperformed the S&P 500 Index (up 11%) in 2014 through Nov. 14.

Rising Specialty Drug Costs a Concern for Managed Care in 2015

Managed-care medical loss ratios may worsen in 2015 as premium growth wanes and costs rise for specialty drugs, which could increase 18% in 2015. Payers may have difficulty justifying double-digit premium increases given that medical cost growth has hovered near 6% for the past three years.

The shift to outpatient hospitals visits, as opposed to higher-cost inpatient admissions, may ease managed-care expenses in 2015 while cutting hospital revenue.

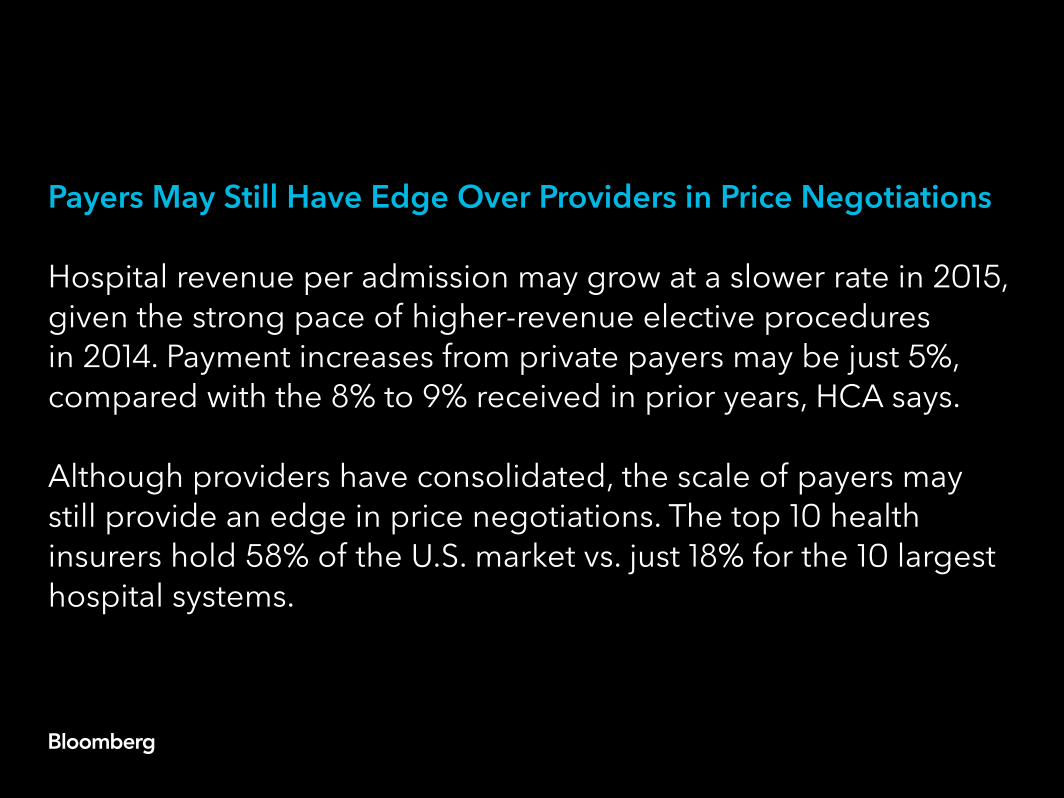

Payers May Still Have Edge Over Providers in Price Negotiations

Hospital revenue per admission may grow at a slower rate in 2015, given the strong pace of higher-revenue elective procedures in 2014. Payment increases from private payers may be just 5%, compared with the 8% to 9% received in prior years, HCA says.

Although providers have consolidated, the scale of payers may still provide an edge in price negotiations. The top 10 health insurers hold 58% of the U.S. market vs. just 18% for the 10 largest hospital systems.

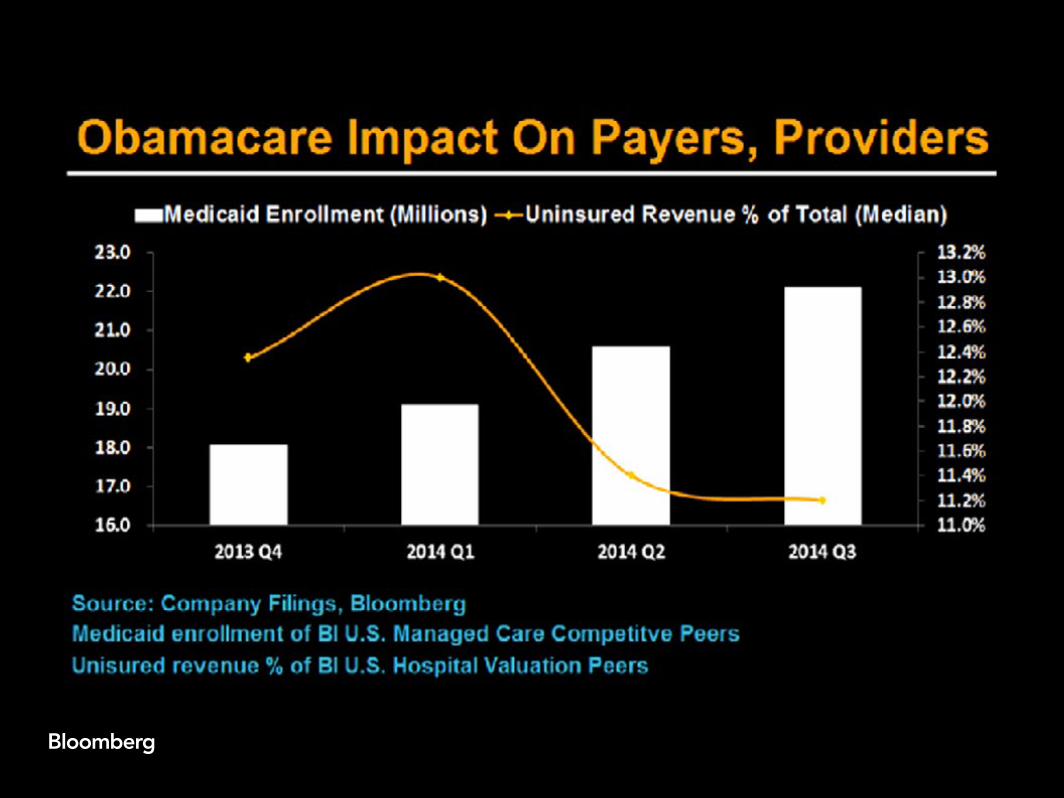

Obamacare Could Add Enrollment, Cut Uncompensated Care in 2015

The Affordable Care Act may boost managed-care enrollment and reduce hospital uncompensated care in 2015. Medicaid expansion in Pennsylvania, along with a push for expansion in Tennessee, may lower bad debt at Community Health and LifePoint.

The second year of the public health-care exchanges may add 7 million members, who could be healthier and require lower costs. Payer margins may be pressured by competitive pricing and reduced risk payments.

Medical Devices

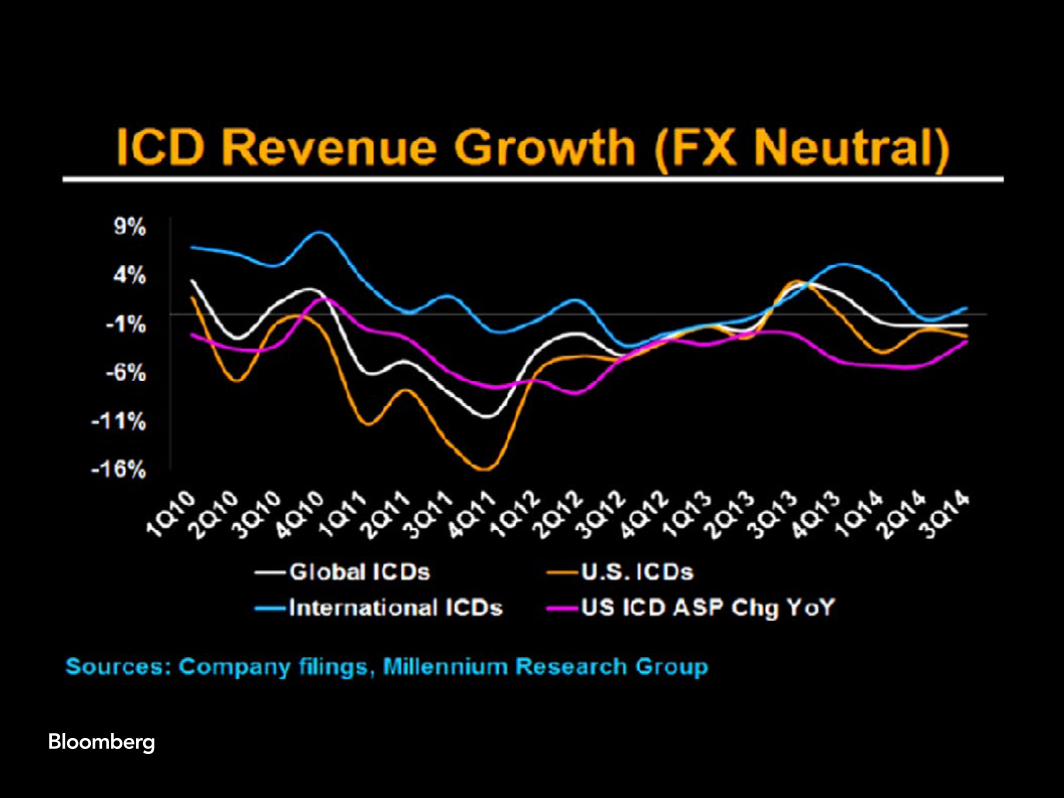

Defibrillator Sales May Continue to Decline for Medtronic, Peers

Implantable cardioverter defibrillators may continue to decline in 2015 as falling prices offset rising procedures, pressuring device makers such as Medtronic, St. Jude Medical and Boston Scientific.

ICD revenue has fallen 1% on average since 2012, excluding currency exchange, while prices have fallen about 4% in the U.S., according to Millennium Research Group. While revenue could improve with new device launches, hospitals continue to push for lower prices.

U.S Orthopedic Growth May Continue to Rise, Aid Zimmer, Stryker

U.S. orthopedic implant growth may continue to rise in 2015, boosting revenue per adjusted admission for hospitals, though falling prices may hurt revenue growth for device makers such as Stryker and Zimmer.

Rising employment and expanding manufacturing have helped many regain insurance coverage in the U.S., though demand is becoming more seasonal toward 4Q due to health plan designs. An aging population may also boost growth.

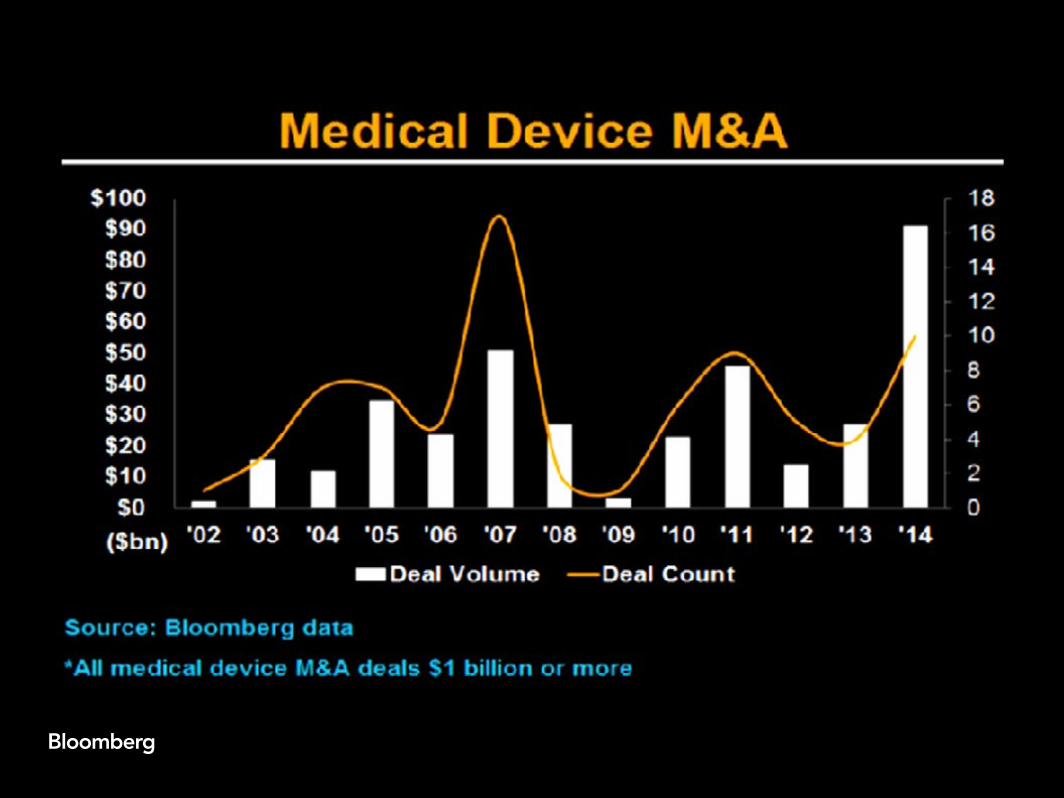

Medical-Device M&A at 10-Year High May Offer Spoils to Onlookers

Large medical-device manufacturers that have engaged in blockbuster deals such as Medtronic and Zimmer may lose market share in 2015 as they focus on integrating large businesses and sales representatives leave for competitors.

Medical device M&A volume is at a 10-year high with more than $90 billion announced in 2014, led by Medtronic’s $46 billion purchase of Covidien. Some of the deals may help companies in the long term as companies seek a stronger pipeline of products.

Edwards, Medtronic Heart Valves May Propel Sales Growth in 2015

Heart valve revenue growth may rise in 2015 for device makers if Edwards Lifesciences or Medtronic get new, smaller transcatheter heart valves approved in the U.S. that may treat more patients.

U.S. transcatheter heart valve sales have grown about 75% in 2014 due to a broader range of sizes available, increasing the treatable patient population. Boston Scientific and St. Jude are evaluating their transcatheter valves in U.S. clinical studies.

Bloomberg Intelligence offers valuable industry and company data, interactive charting and written analysis with government and credit insights from a team of independent experts, giving trading and investment professionals deep insight into where crucial industries stand today and where they may be heading next.

Related Documents