BERGRIVIER MUNICIPALITY BERGRIVIER MUNISIPALITEIT FINAL BUDGET | FINALE BEGROTING 2017/2018 | 2018/2019 | 2019/2020 A prosperous community where all want to live, work, learn and play in a dignified manner

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BERGRIVIER MUNICIPALITY

BERGRIVIER MUNISIPALITEIT

FINAL BUDGET | FINALE BEGROTING

2017/2018 | 2018/2019 | 2019/2020

A prosperous community where all want to live, work, learn and play in a dignified manner

Table of Contents

PART 1 – ANNUAL BUDGET 1.1 MAYOR’S REPORT P.1

1.2 COUNCIL RESOLUTIONS P.2

1.3 EXECUTIVE SUMMARY P.5

1.4 OPERATING REVENUE FRAMEWORK P.6

1.5 OPERATING EXPENDITURE FRAMEWORK P.11

1.6 CAPITAL EXPENDITURE P.13

1.7 ANNUAL BUDGET TABLES P.14

PART 2 – SUPPORTING DOCUMENTATION

2.1 OVERVIEW OF ANNUAL BUDGET PROCESS P.24

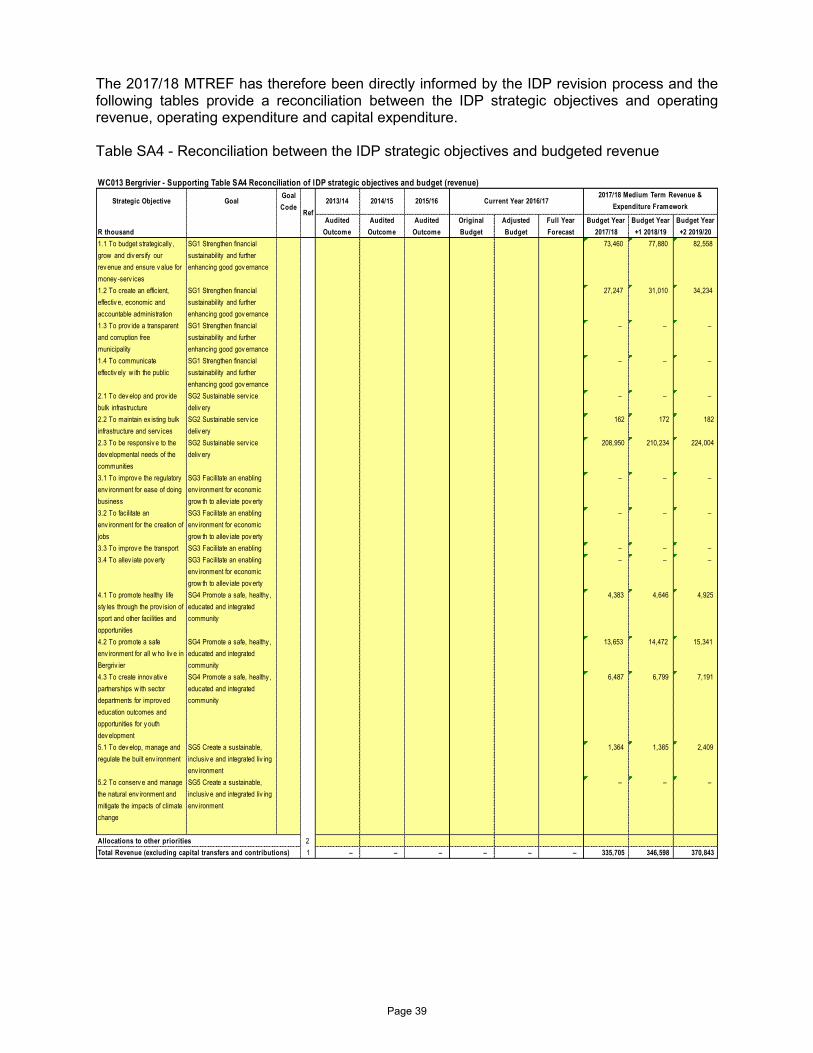

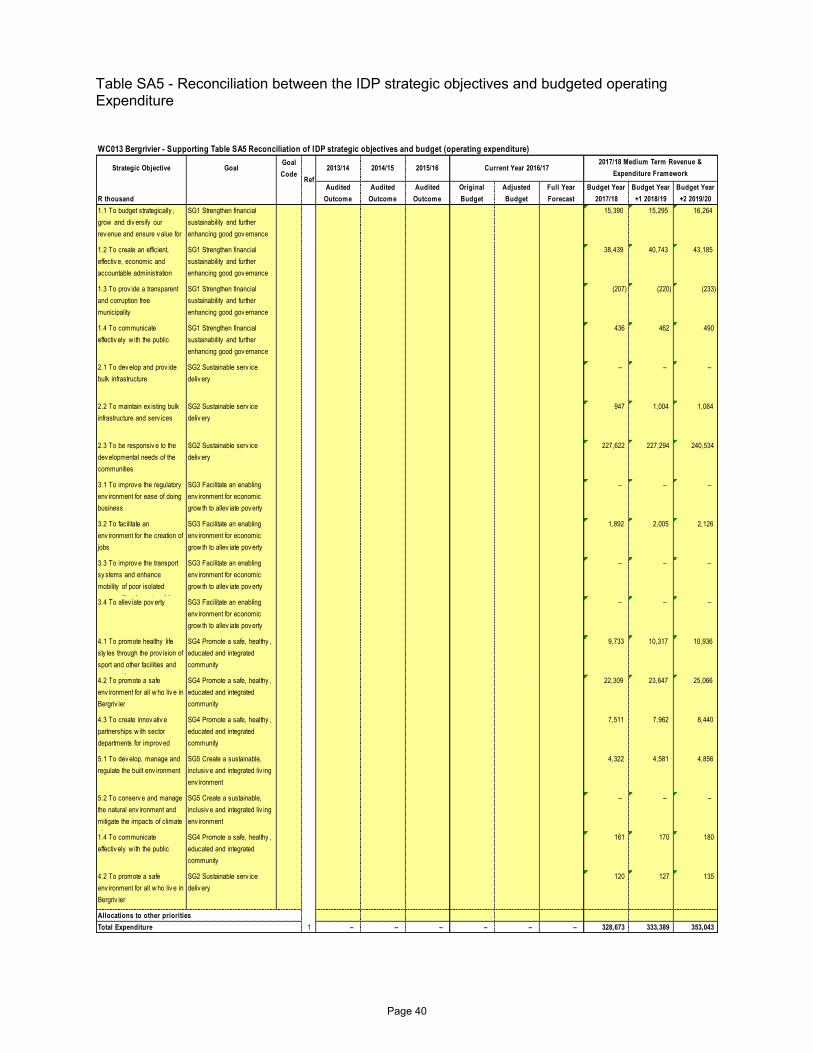

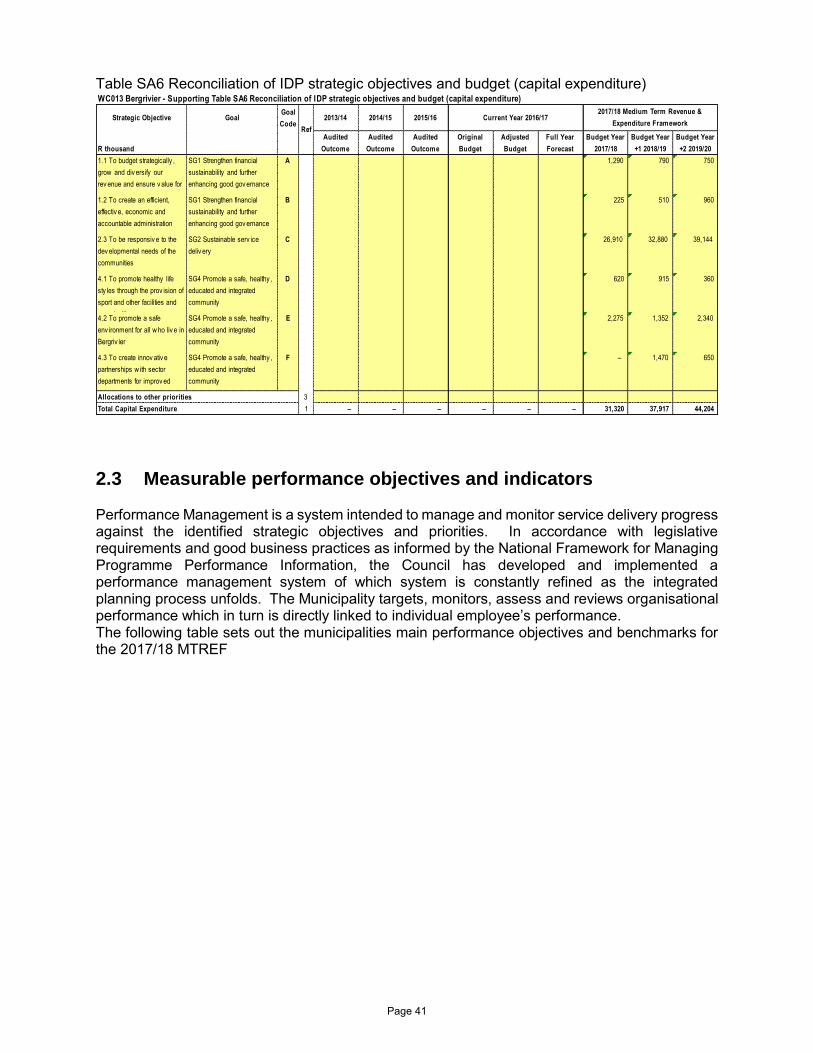

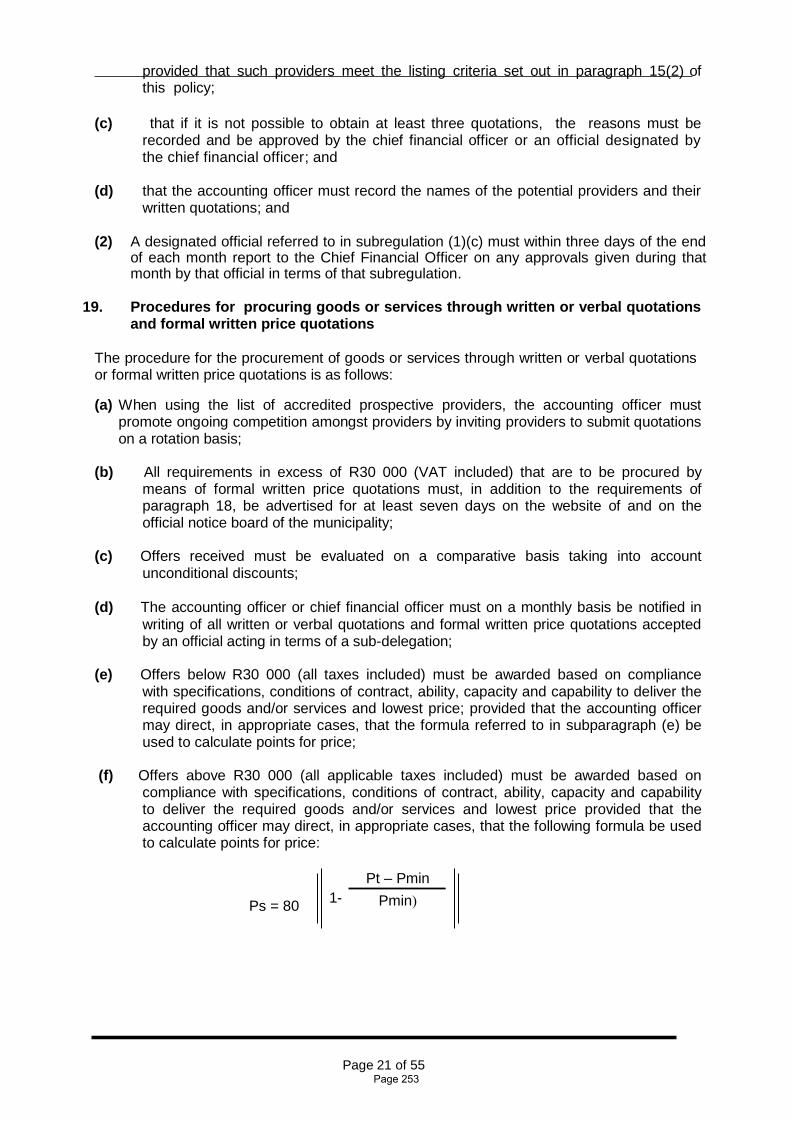

2.2 OVERVIEW OF ALIGNMENT OF ANNUAL BUDGET WITH IDP P.37

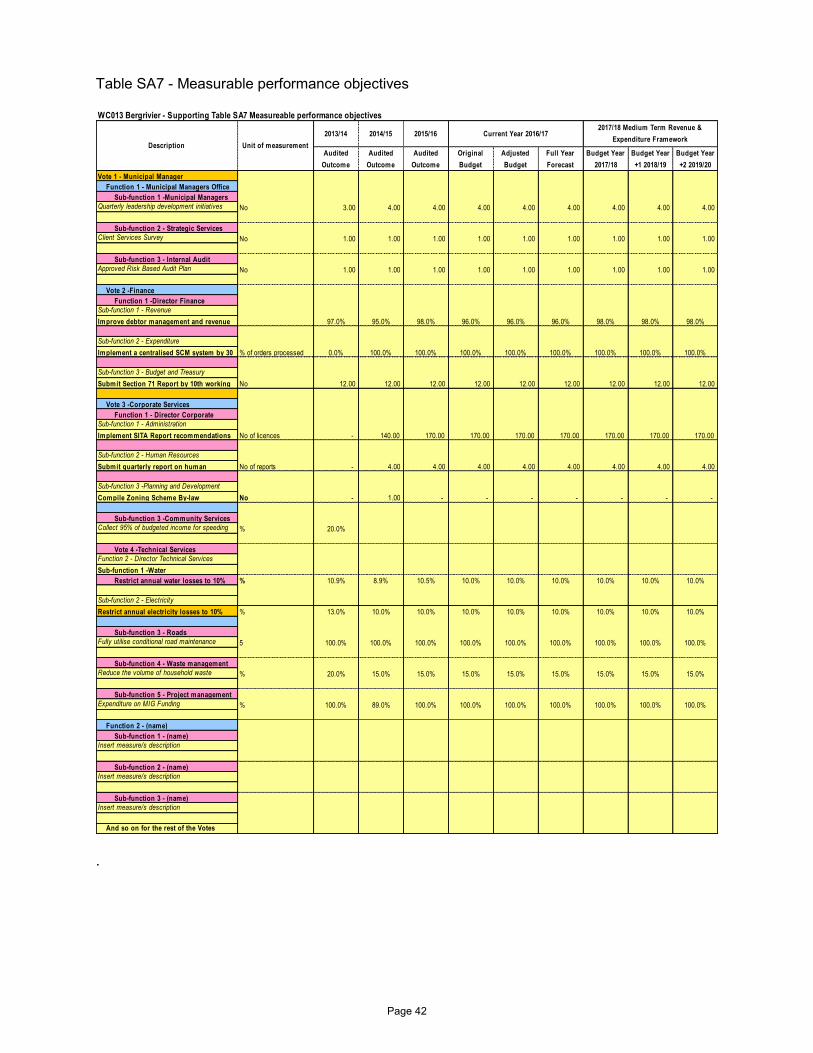

2.3 MEASURABLE PERFORMANCE OBJECTIVES AND INDICATORS P.41

2.4 OVERVIEW OF BUDGET RELATED-POLICIES P.44

2.5 OVERVIEW OF BUDGET ASSUMPTIONS P.46

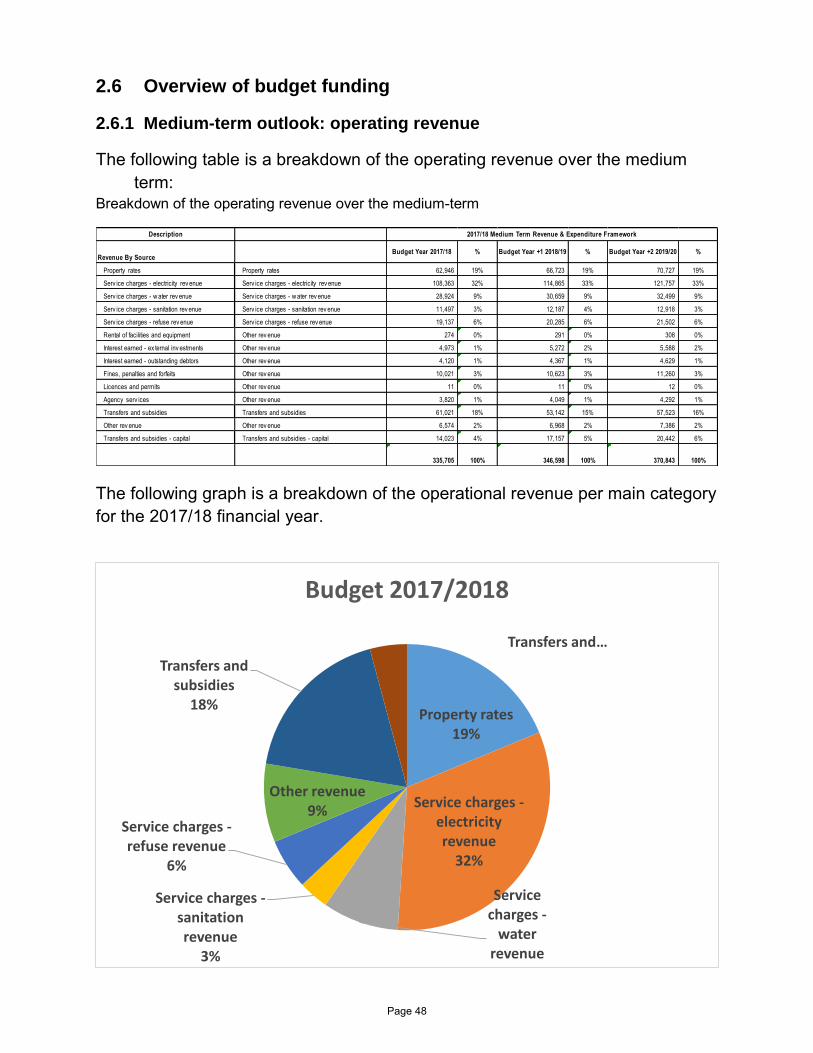

2.6 OVERVIEW OF BUDGET FUNDING P.48

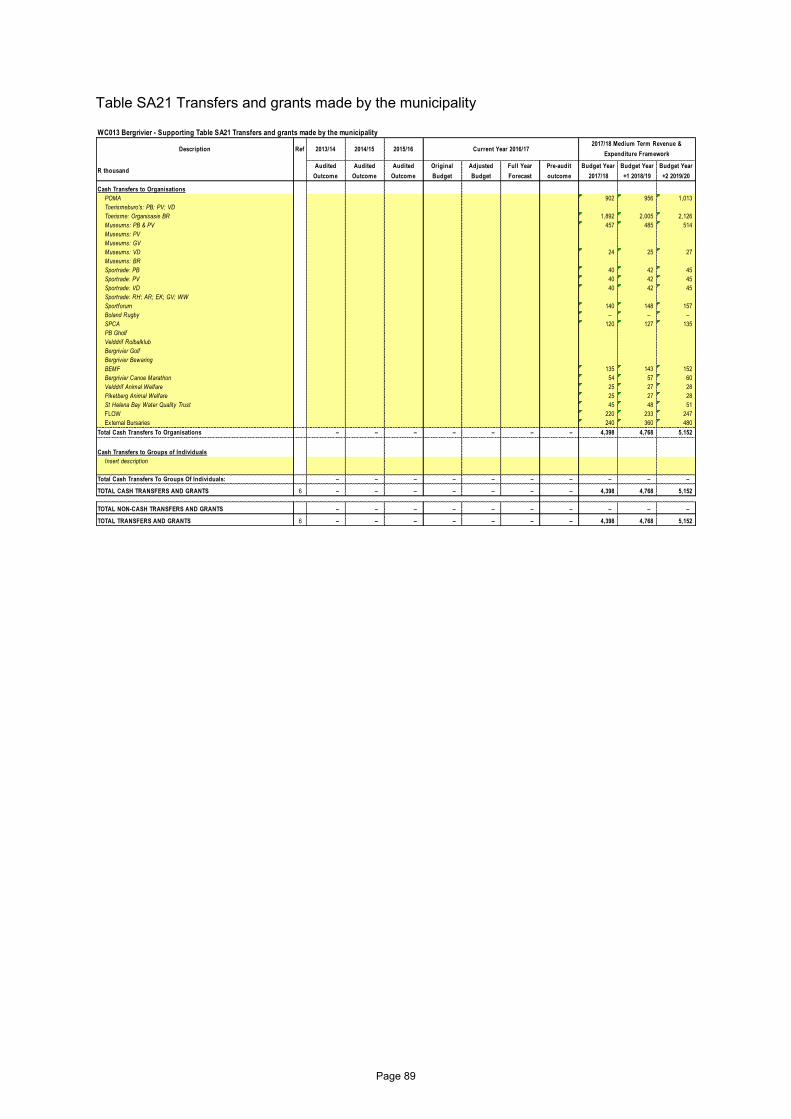

2.7 EXPENDITURE ON GRANTS AND RECONCILIATIONS OF UNSPENT FUNDS P.54

2.8 COUNCILLOR AND EMPLOYEE BENEFITS P.57

2.9 MONTHLY TARGETS FOR REVENUE, EXPENDITURE AND CASH FLOW P.60

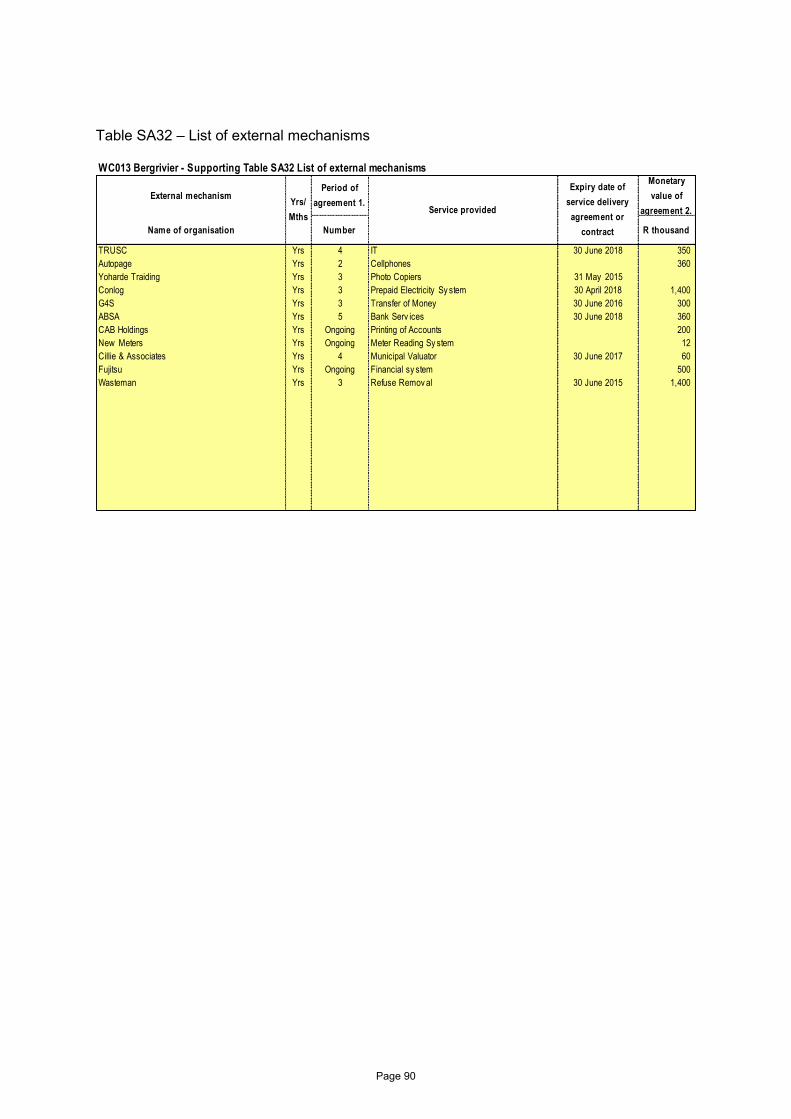

2.10 CONTRACTS HAVING FUTURE BUDGETARY IMPLICATIONS P.66

2.11 CAPITAL EXPENDITURE DETAILS P.67

2.12 LEGISLATION COMPLIANCE STATUS P.76

2.13 OTHER SUPPORTING DOCUMENTS P.78

2.14 MUNICIPAL MANAGER’S QUALITY CERTIFICATE P.92

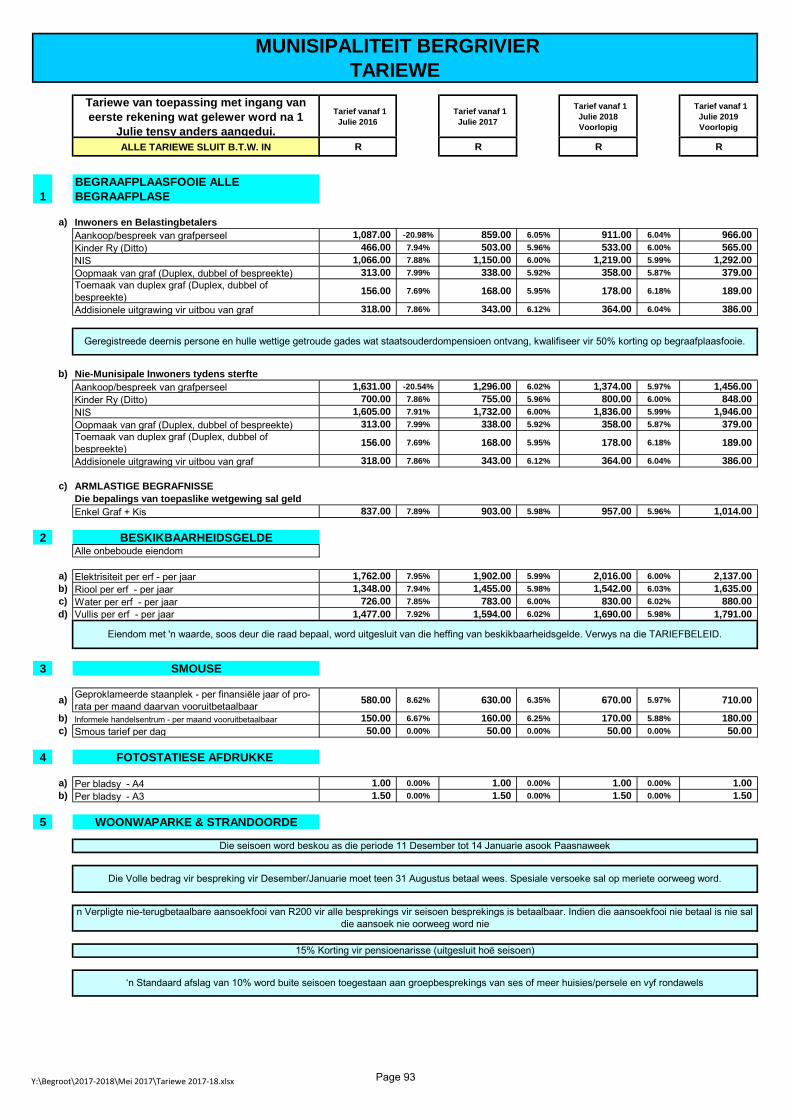

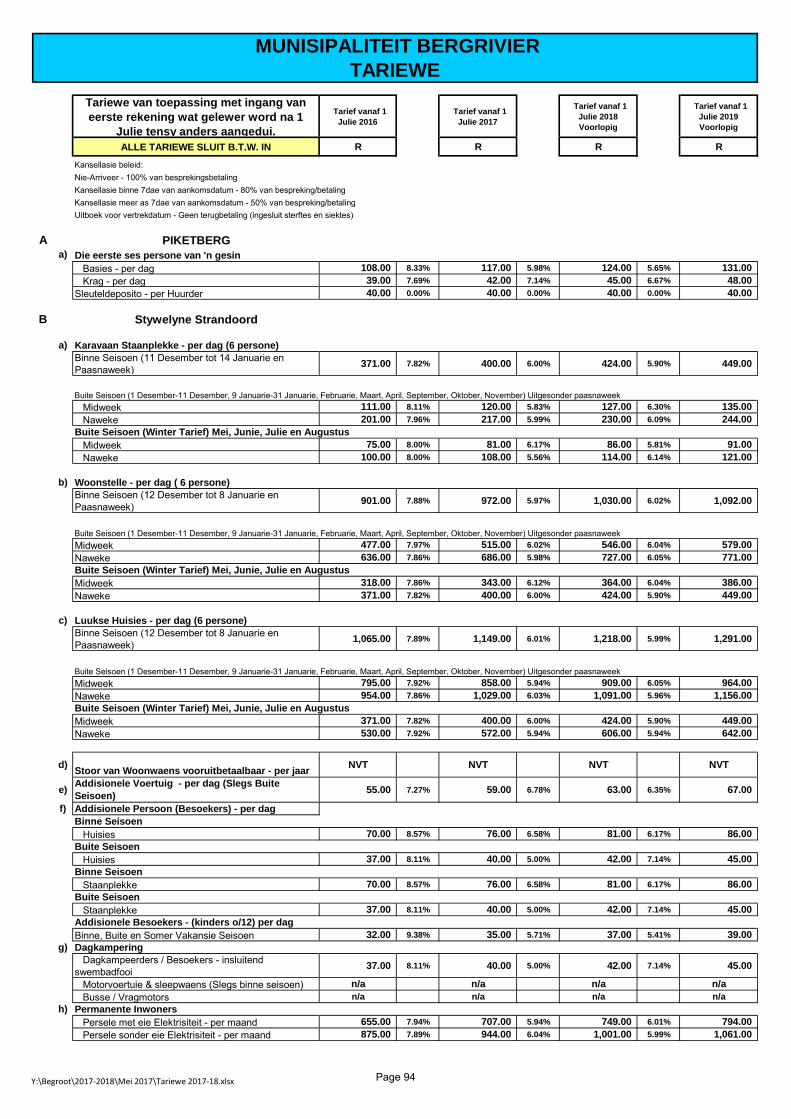

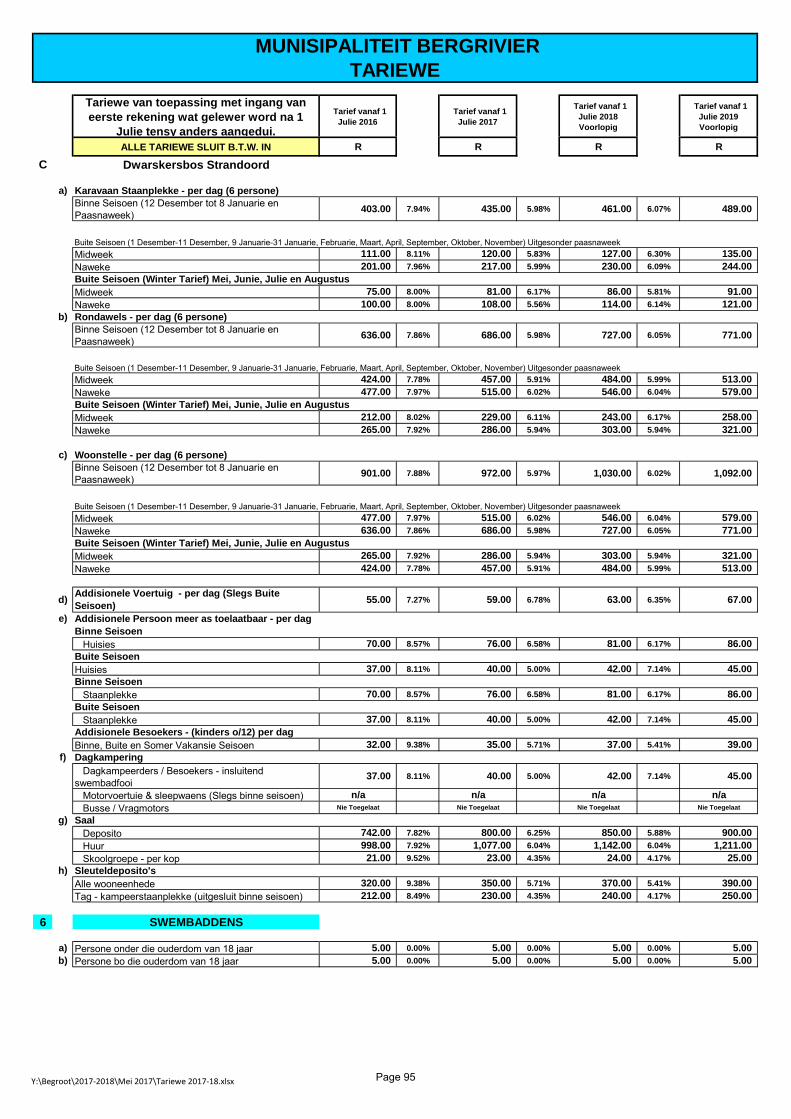

PART 3 – TARIFFS / TARIEWE P.93

PART 4 - POLICIES / BELEIDE

4.1 BATEBESTUURSBELEID P.103

4.2 KONTANTBESTUUR EN BELEGGINSBELEID P.130

4.3 KREDIETBEHEER EN SKULDINVORDERINGSBELEID P.150

4.4 PROPERTY RATES POLICY P.176

4.5 TARIEFBELEID P.211

4.6 VIREMENT POLICY P.222

4.7 PROPERTY RATES BY-LAW P.230

4.8 VOORSIENINGSKANAAL BESTUURSBELEID P.233

4.9 BORROWING POLICY P.291

4.10 FUNDING, RESERVES AND LONG TERM FINANCIAL PLANNING POLICY P.304

4.11 BUDGET IMPLEMENTATION AND MONITORING POLICY P.331

Part 1 – Annual Budget

1.1 Mayor’s Report

It is my privilege to table this budget and other related documents for 2017/2018 and the two outer years as prescribed in terms of section 16 of the Municipal Finance Management Act.

As a result of the intensive planning process undertaken through the IDP, the budget presented today is in line with the needs of the communities we serve. The operating revenue budget (excluding capital transfers and contributions) amounts to R321.682 million. The bulk of the income is derived from Assessment Rates and User Charges for Services.

The capital budget amounts to just more than R31.320 million. Expenditure out of own funds are R11.217 million. New loan funding of R6.080 million will be taken up in the financial year. In addition to this, external grants of R 14.023 million are included in this budget.

The following adjustments to the employee related costs were made: The general salary increase of 7.40% must be implemented.

Notch increases are limited to 2% where applicable.

Given the global economic realities the council’s tariff increases were limit to approximately 7.90% except for electricity where the increase will be 1.88% on condition that NERSA approves the tariffs.

Management within local government has a significant role to play in strengthening the link between the citizen and government’s overall priorities and spending plans. The goal should be to enhance service delivery aimed at improving the quality of life for all people within the Bergrivier Municipality. Budgeting is primarily about the choices that the municipality has to make between competing priorities and fiscal realities. The challenge is to do more with the available resources. We need to remain focused on the effective delivery of the core municipal services through the application of efficient and effective service delivery mechanisms.

The application of sound financial management principles in the compilation of the municipality’s financial plan is essential and critical to ensure that Bergrivier Municipality remains financially viable and that sustainable municipal services are provided economically and equitably to all communities.

Our responsibility as a sphere of government is to ensure that the quality of life of all that live and work in Bergrivier Municipality is improved. We will continue to engage in both progressive and meaningful discussions with our communities to shape a clear path from which governance, and development, will draw guidance and direction. The Council will continue to pursue and encourage community participation programmes to ensure our plans are in line with community needs.

In conclusion, I would like to thank the Municipal Manager, the Chief Financial Officer and the personnel in the Budget Office, Directors and other personnel who were involved in compiling this IDP and budget. The effort and hard work that have already gone into this have not gone unnoticed and Council would like to express their appreciation to all involved.

Page 1

1.2 Council Resolution (Recommended) 1) The Council of Bergrivier Municipality, acting in terms of section 24 of the Municipal Finance

Management Act, (Act 56 of 2003) approves and adopts: a) The annual budget of the municipality for the financial year 2017/18 and the multi-year

and single-year capital appropriations as set out in the following tables: i) Budgeted Financial Performance (revenue and expenditure by standard

classification) – Table A2; ii) Budgeted Financial Performance (revenue and expenditure by municipal vote) –

Table A3; iii) Budgeted Financial Performance (revenue by source and expenditure by type) –

Table A4; and iv) Multi-year and single-year capital appropriations by municipal vote and standard

classification and associated funding by source – Table A5. b) The financial position, cash flow budget, cash-backed reserve/accumulated surplus, asset

management and basic service delivery targets are approved as set out in the following tables: i) Budgeted Financial Position – Table A6; ii) Budgeted Cash Flows – Table A7; iii) Cash backed reserves and accumulated surplus reconciliation – Table A8; iv) Asset management – Table A9; and v) Basic service delivery measurement – Table A10.

2) The Council of Bergrivier Municipality, acting in terms of section 75A of the Local Government:

Municipal Systems Act (Act 32 of 2000) approves and adopts with effect from 1 July 2017: a) the tariffs for property rates, b) the tariffs for electricity, c) the tariffs for the supply of water d) the tariffs for sanitation services e) the tariffs for solid waste services

3) The Council of Bergrivier Municipality, acting in terms of 75A of the Local Government: Municipal Systems Act (Act 32 of 2000) approves and adopts with effect from 1 July 2017 the tariffs for other services as contained in the tariff list included in the budget document.

4) To give proper effect to the municipality’s annual budget, the Council of Bergrivier Municipality approves: a) That cash backing is implemented through the utilisation of a portion of the revenue

generated from property rates to ensure that all capital reserves and provisions, unspent long-term loans and unspent conditional grants are cash backed as required in terms of section 8 of the Municipal Budget and Reporting Regulations.

b) That the municipality be permitted to enter into long-term loans for the funding of the capital programmes in respect of the 2017/18 financial year limited to an amount of R6.080 million in terms of Section 46 of the Municipal Finance Management Act.

c) That the Municipal Manager be authorised to sign all necessary agreements and documents to give effect to the above lending programme.

Page 2

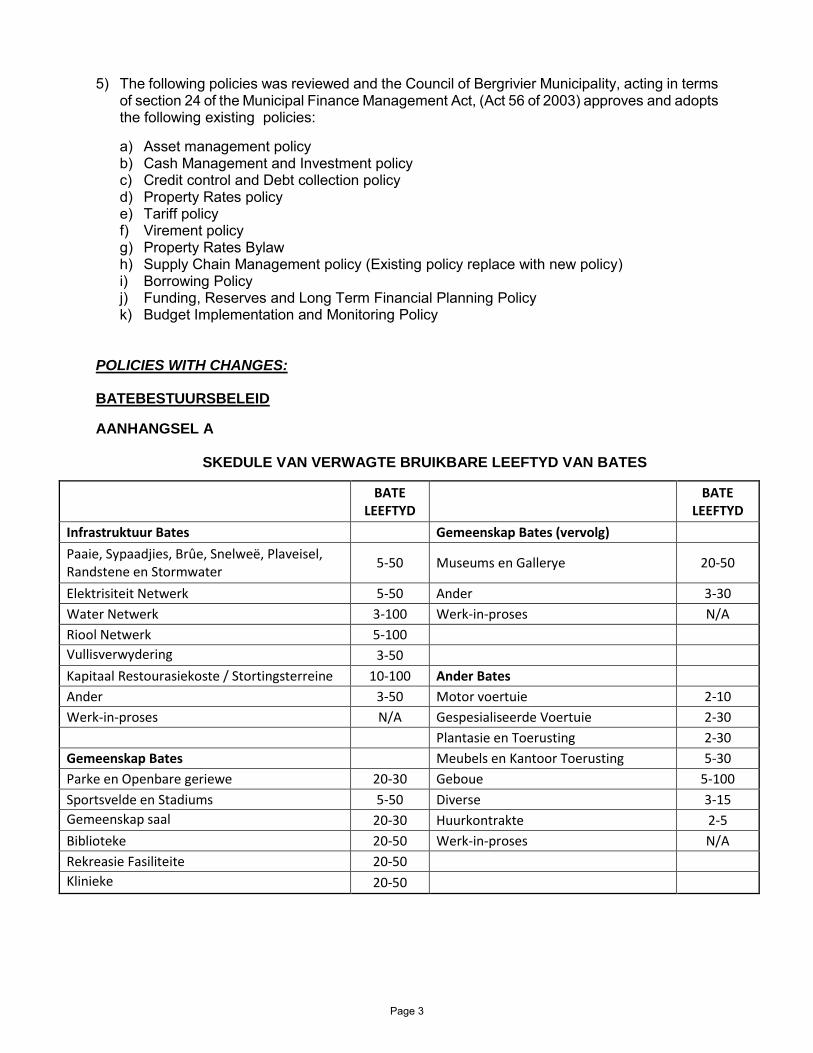

5) The following policies was reviewed and the Council of Bergrivier Municipality, acting in terms of section 24 of the Municipal Finance Management Act, (Act 56 of 2003) approves and adopts the following existing policies:

a) Asset management policy b) Cash Management and Investment policy c) Credit control and Debt collection policy d) Property Rates policy e) Tariff policy f) Virement policy g) Property Rates Bylaw h) Supply Chain Management policy (Existing policy replace with new policy) i) Borrowing Policy j) Funding, Reserves and Long Term Financial Planning Policy k) Budget Implementation and Monitoring Policy

POLICIES WITH CHANGES:

BATEBESTUURSBELEID

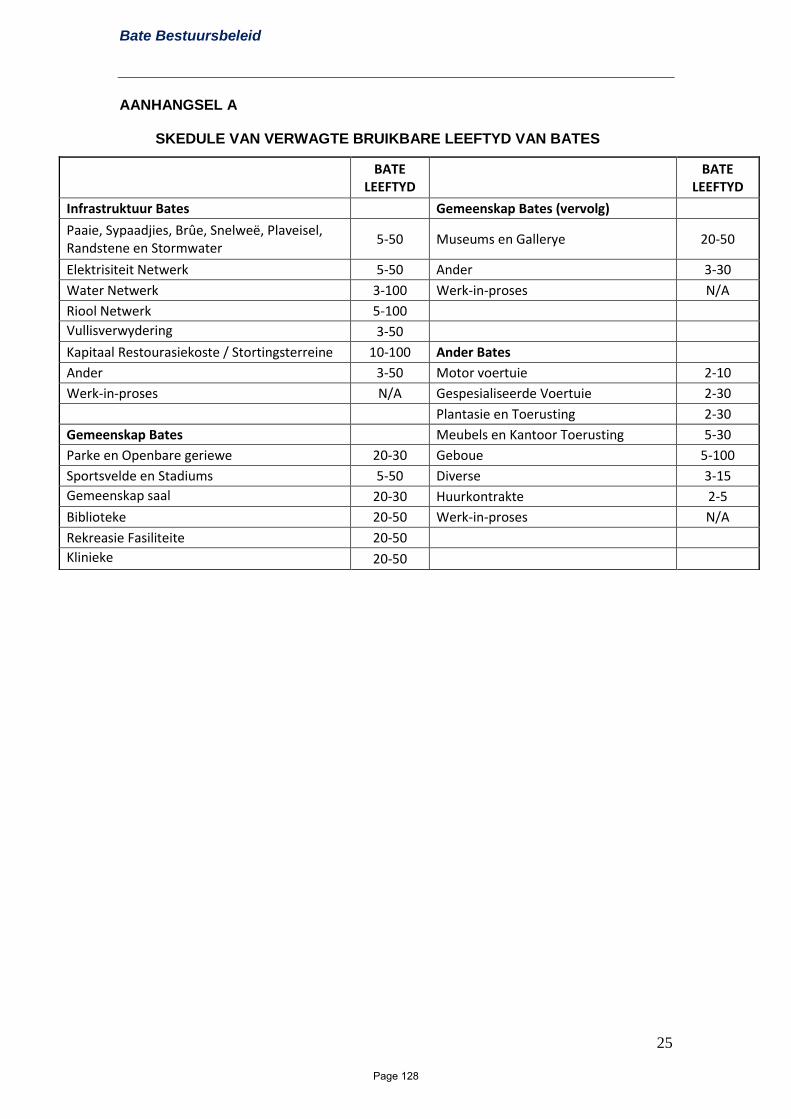

AANHANGSEL A

SKEDULE VAN VERWAGTE BRUIKBARE LEEFTYD VAN BATES

BATE

LEEFTYD

BATE LEEFTYD

Infrastruktuur Bates Gemeenskap Bates (vervolg)

Paaie, Sypaadjies, Brûe, Snelweë, Plaveisel, Randstene en Stormwater

5-50 Museums en Gallerye 20-50

Elektrisiteit Netwerk 5-50 Ander 3-30

Water Netwerk 3-100 Werk-in-proses N/A

Riool Netwerk 5-100

Vullisverwydering 3-50

Kapitaal Restourasiekoste / Stortingsterreine 10-100 Ander Bates

Ander 3-50 Motor voertuie 2-10

Werk-in-proses N/A Gespesialiseerde Voertuie 2-30

Plantasie en Toerusting 2-30

Gemeenskap Bates Meubels en Kantoor Toerusting 5-30

Parke en Openbare geriewe 20-30 Geboue 5-100

Sportsvelde en Stadiums 5-50 Diverse 3-15

Gemeenskap saal 20-30 Huurkontrakte 2-5

Biblioteke 20-50 Werk-in-proses N/A

Rekreasie Fasiliteite 20-50

Klinieke 20-50

Page 3

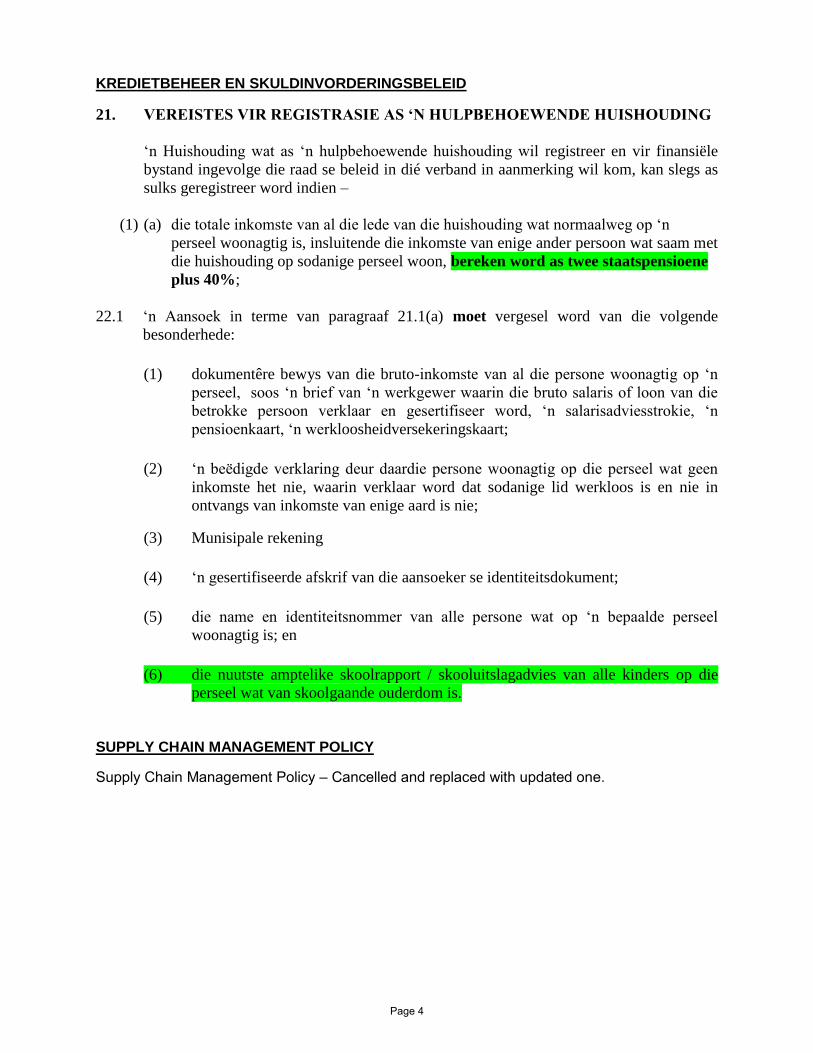

KREDIETBEHEER EN SKULDINVORDERINGSBELEID

21. VEREISTES VIR REGISTRASIE AS ‘N HULPBEHOEWENDE HUISHOUDING

‘n Huishouding wat as ‘n hulpbehoewende huishouding wil registreer en vir finansiële

bystand ingevolge die raad se beleid in dié verband in aanmerking wil kom, kan slegs as

sulks geregistreer word indien –

(1) (a) die totale inkomste van al die lede van die huishouding wat normaalweg op ‘n

perseel woonagtig is, insluitende die inkomste van enige ander persoon wat saam met

die huishouding op sodanige perseel woon, bereken word as twee staatspensioene

plus 40%;

22.1 ‘n Aansoek in terme van paragraaf 21.1(a) moet vergesel word van die volgende

besonderhede:

(1) dokumentêre bewys van die bruto-inkomste van al die persone woonagtig op ‘n

perseel, soos ‘n brief van ‘n werkgewer waarin die bruto salaris of loon van die

betrokke persoon verklaar en gesertifiseer word, ‘n salarisadviesstrokie, ‘n

pensioenkaart, ‘n werkloosheidversekeringskaart;

(2) ‘n beëdigde verklaring deur daardie persone woonagtig op die perseel wat geen

inkomste het nie, waarin verklaar word dat sodanige lid werkloos is en nie in

ontvangs van inkomste van enige aard is nie;

(3) Munisipale rekening

(4) ‘n gesertifiseerde afskrif van die aansoeker se identiteitsdokument;

(5) die name en identiteitsnommer van alle persone wat op ‘n bepaalde perseel

woonagtig is; en

(6) die nuutste amptelike skoolrapport / skooluitslagadvies van alle kinders op die

perseel wat van skoolgaande ouderdom is.

SUPPLY CHAIN MANAGEMENT POLICY

Supply Chain Management Policy – Cancelled and replaced with updated one.

Page 4

1.3 Executive Summary

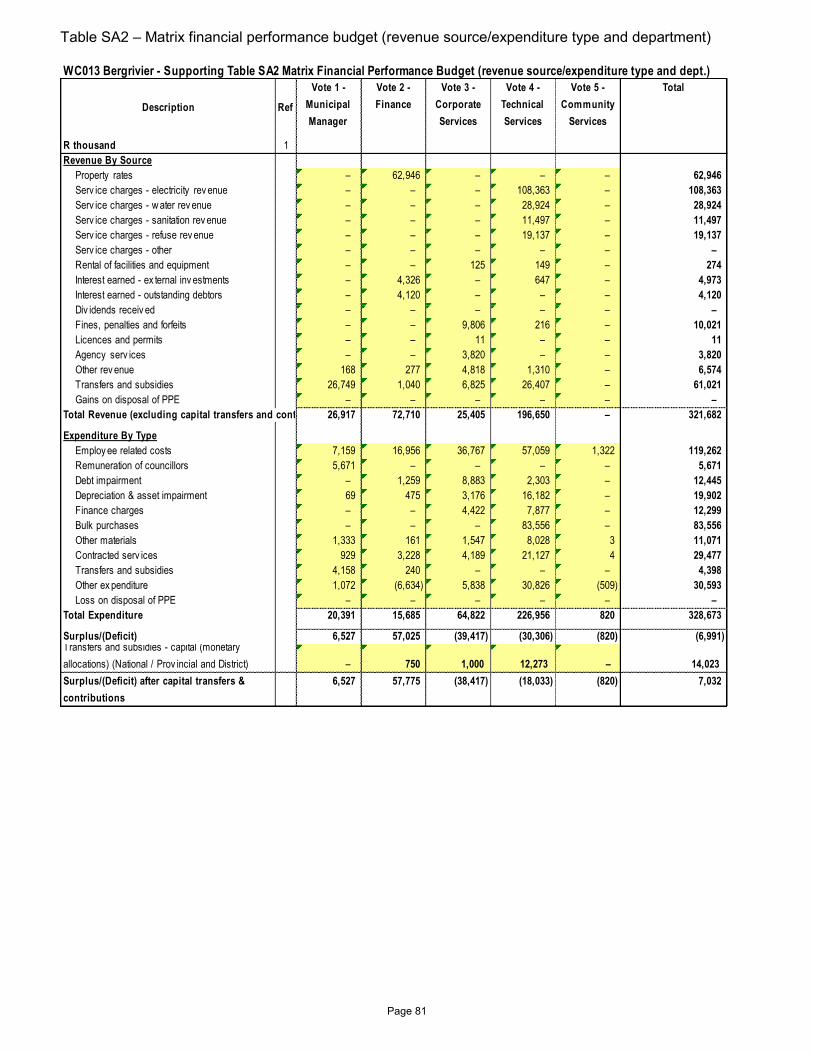

The application of sound financial management principles for the compilation of the Municipality’s financial plan is essential and critical to ensure that the Municipality remains financially viable and that municipal services are provided sustainably, economically and equitably to all communities. The Municipality’s business and service delivery priorities were reviewed as part of this year’s planning and budget process. Where appropriate, funds were transferred from low- to high-priority programmes so as to maintain sound financial stewardship. A critical review was also undertaken of expenditures on noncore and ‘nice to have’ items. The Municipality has embarked on implementing a range of revenue collection strategies to optimize the collection of debt owed by consumers. Furthermore, the Municipality has undertaken various customer care initiatives to ensure the municipality truly involves all citizens in the process of ensuring a people lead government. National Treasury’s MFMA Circular No. 85 and 86 was used to guide the compilation of the 2017/18 MTREF. The main challenges experienced during the compilation of the 2017/18 MTREF can be summarised as follows:

• The ongoing difficulties in the national and local economy; • Aging water, roads and electricity infrastructure; • The need to reprioritise projects and expenditure within the existing resource envelope

given the cash flow realities and declining cash position of the municipality; • The increased cost of bulk water and electricity (due to tariff increases from West Coast

District Municipality and Eskom), which is placing upward pressure on service tariffs to residents. Continuous high tariff increases are not sustainable - as there will be point where services will no-longer be affordable;

• Salary increases for municipal staff that continue to exceed consumer inflation, as well as the need to fill critical vacancies;

• Availability of affordable borrowing for the funding of capital projects. The following budget principles and guidelines directly informed the compilation of the 2017/18 MTREF: • The 2016/17 Adjustments Budget priorities and targets, as well as the base line allocations

contained in that Adjustments Budget were adopted as the upper limits for the new baselines for the 2017/18 annual budget;

• Intermediate service level standards were used to inform the measurable objectives, targets and backlog eradication goals;

• Tariff and property rate increases should be affordable and should generally not exceed inflation as measured by the CPI, except where there are price increases in the inputs of services that are beyond the control of the municipality, for instance the cost of bulk water and electricity. In addition, tariffs need to remain or move towards being cost reflective, and should take into account the need to address infrastructure backlogs;

• There will be no budget allocated to national and provincial funded projects unless the necessary grants to the municipality are reflected in the national and provincial budget and have been gazetted as required by the annual Division of Revenue Act;

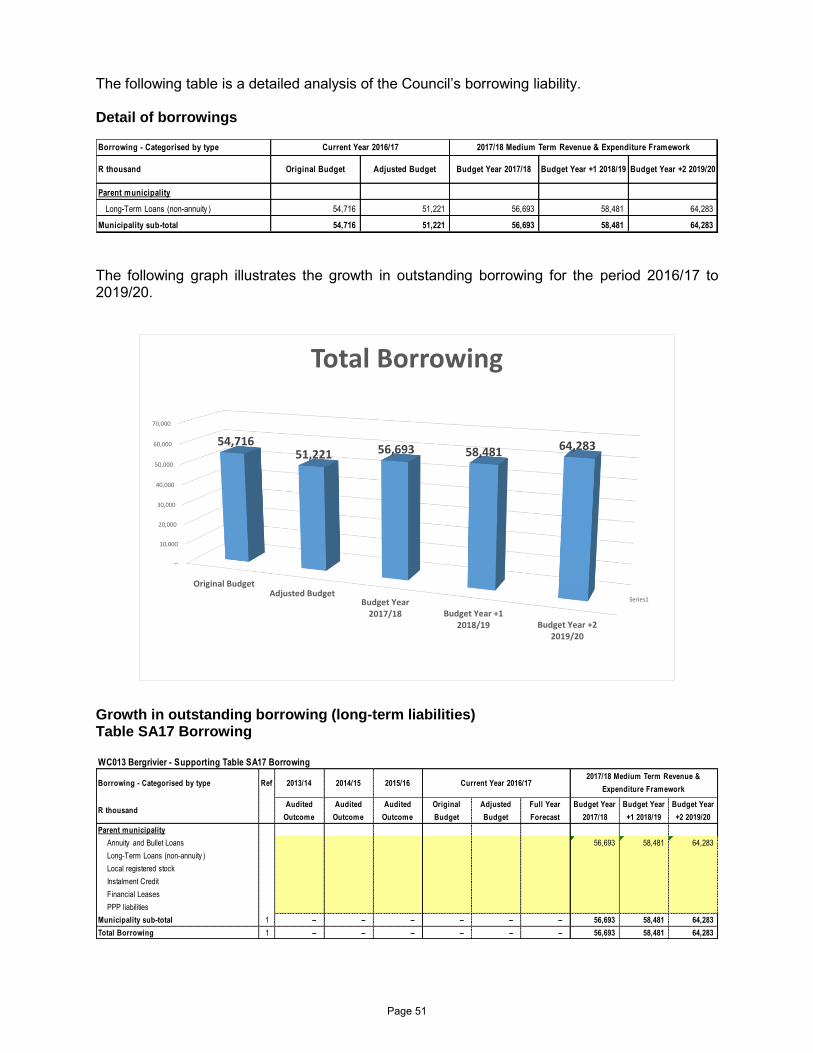

The following table is a consolidated overview of the proposed 2017/18 Medium-term Revenue and Expenditure Framework:

Page 5

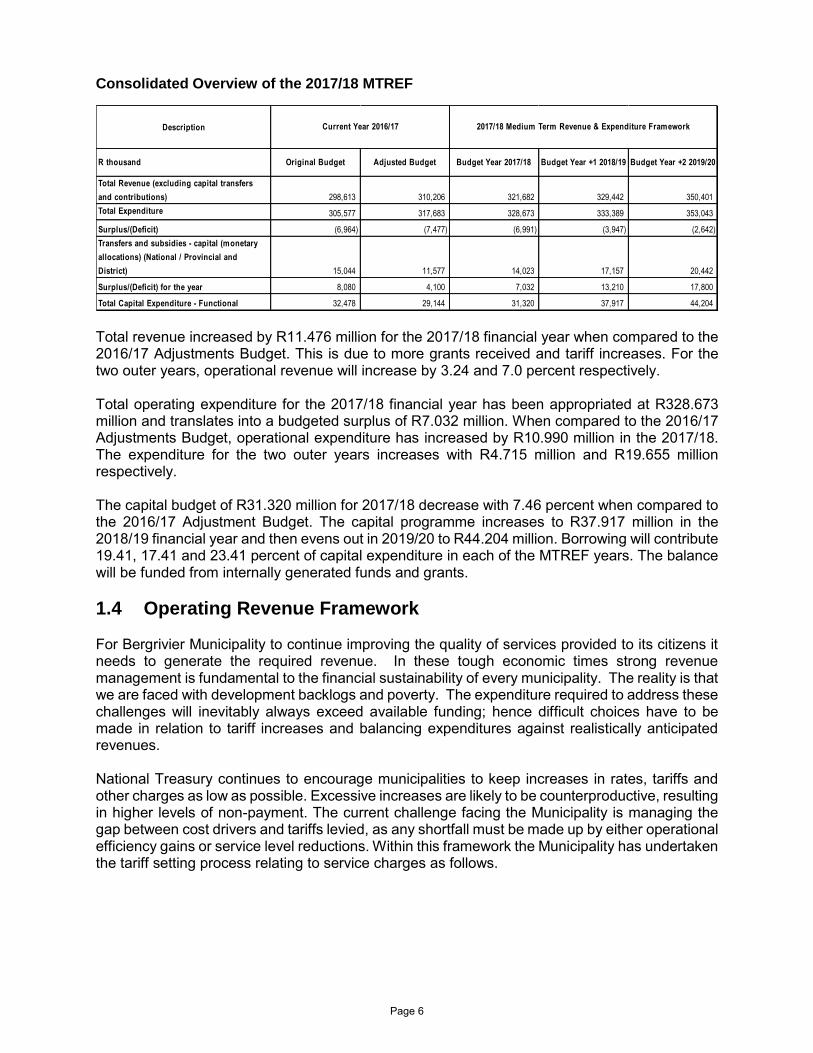

Consolidated Overview of the 2017/18 MTREF

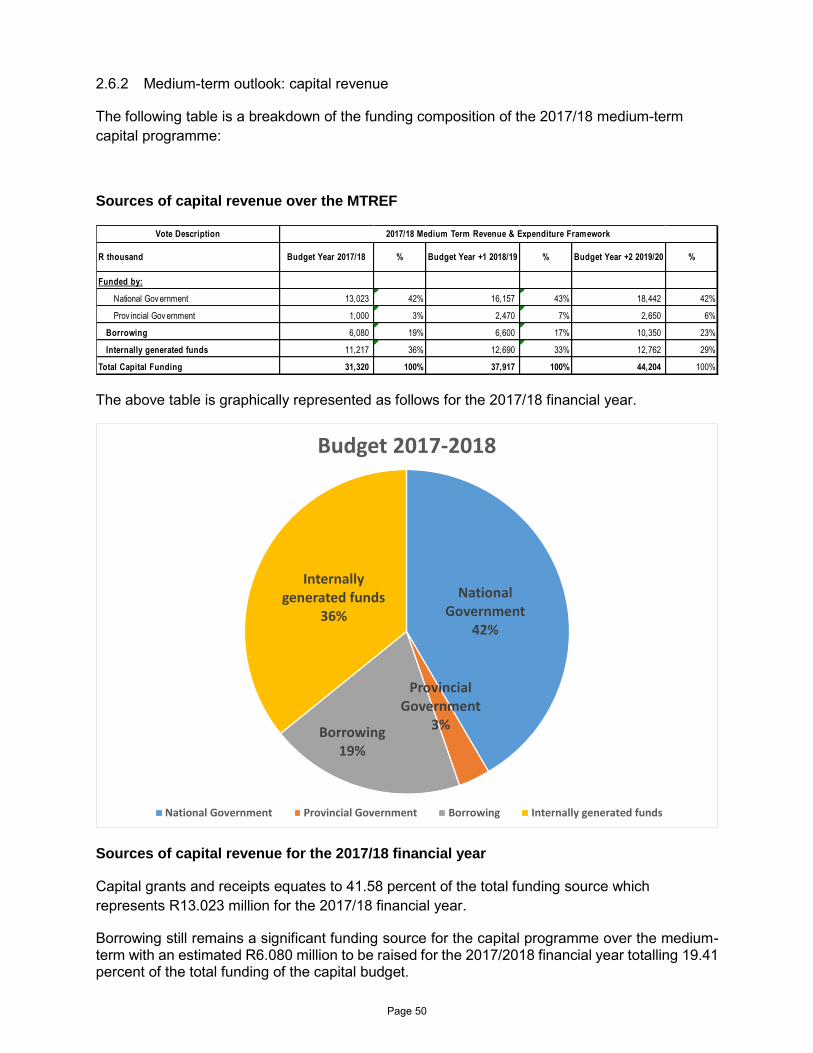

Total revenue increased by R11.476 million for the 2017/18 financial year when compared to the 2016/17 Adjustments Budget. This is due to more grants received and tariff increases. For the two outer years, operational revenue will increase by 3.24 and 7.0 percent respectively. Total operating expenditure for the 2017/18 financial year has been appropriated at R328.673 million and translates into a budgeted surplus of R7.032 million. When compared to the 2016/17 Adjustments Budget, operational expenditure has increased by R10.990 million in the 2017/18. The expenditure for the two outer years increases with R4.715 million and R19.655 million respectively. The capital budget of R31.320 million for 2017/18 decrease with 7.46 percent when compared to the 2016/17 Adjustment Budget. The capital programme increases to R37.917 million in the 2018/19 financial year and then evens out in 2019/20 to R44.204 million. Borrowing will contribute 19.41, 17.41 and 23.41 percent of capital expenditure in each of the MTREF years. The balance will be funded from internally generated funds and grants.

1.4 Operating Revenue Framework For Bergrivier Municipality to continue improving the quality of services provided to its citizens it needs to generate the required revenue. In these tough economic times strong revenue management is fundamental to the financial sustainability of every municipality. The reality is that we are faced with development backlogs and poverty. The expenditure required to address these challenges will inevitably always exceed available funding; hence difficult choices have to be made in relation to tariff increases and balancing expenditures against realistically anticipated revenues. National Treasury continues to encourage municipalities to keep increases in rates, tariffs and other charges as low as possible. Excessive increases are likely to be counterproductive, resulting in higher levels of non-payment. The current challenge facing the Municipality is managing the gap between cost drivers and tariffs levied, as any shortfall must be made up by either operational efficiency gains or service level reductions. Within this framework the Municipality has undertaken the tariff setting process relating to service charges as follows.

Description

R thousand Original Budget Adjusted Budget Budget Year 2017/18 Budget Year +1 2018/19 Budget Year +2 2019/20

Total Revenue (excluding capital transfers

and contributions) 298,613 310,206 321,682 329,442 350,401

Total Expenditure 305,577 317,683 328,673 333,389 353,043

Surplus/(Deficit) (6,964) (7,477) (6,991) (3,947) (2,642)

Transfers and subsidies - capital (monetary

allocations) (National / Provincial and

District) 15,044 11,577 14,023 17,157 20,442

Surplus/(Deficit) for the year 8,080 4,100 7,032 13,210 17,800

Total Capital Expenditure - Functional 32,478 29,144 31,320 37,917 44,204

Current Year 2016/17 2017/18 Medium Term Revenue & Expenditure Framework

Page 6

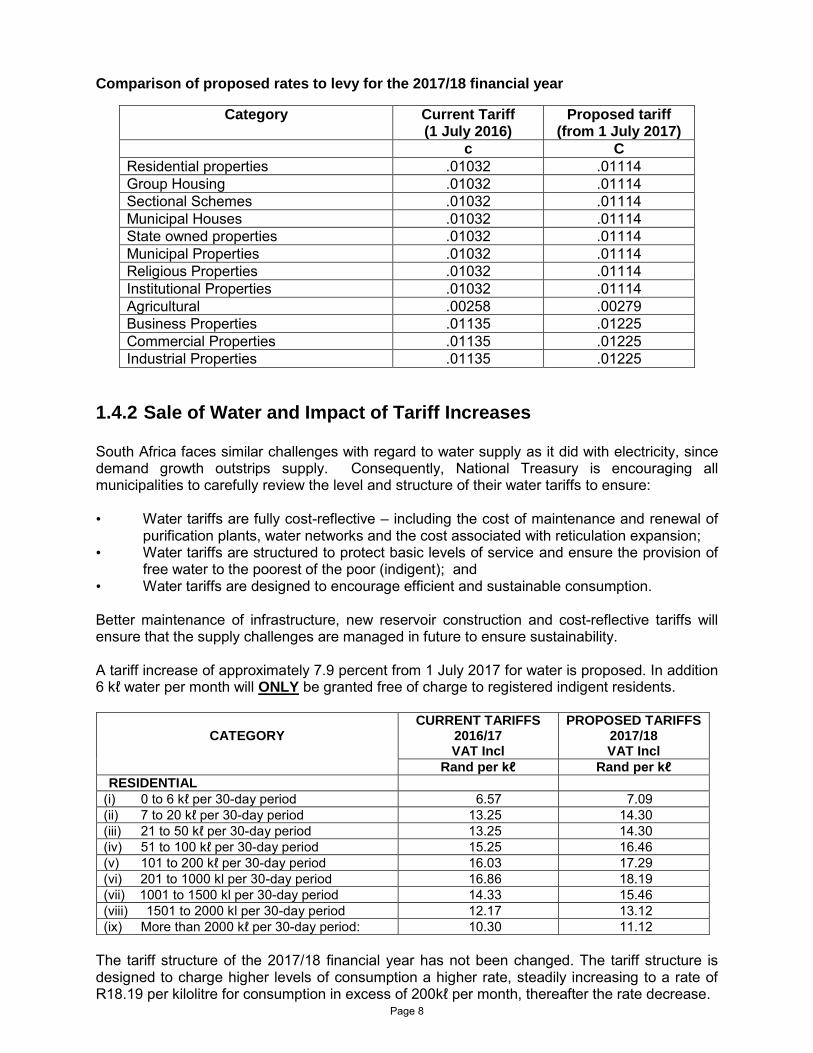

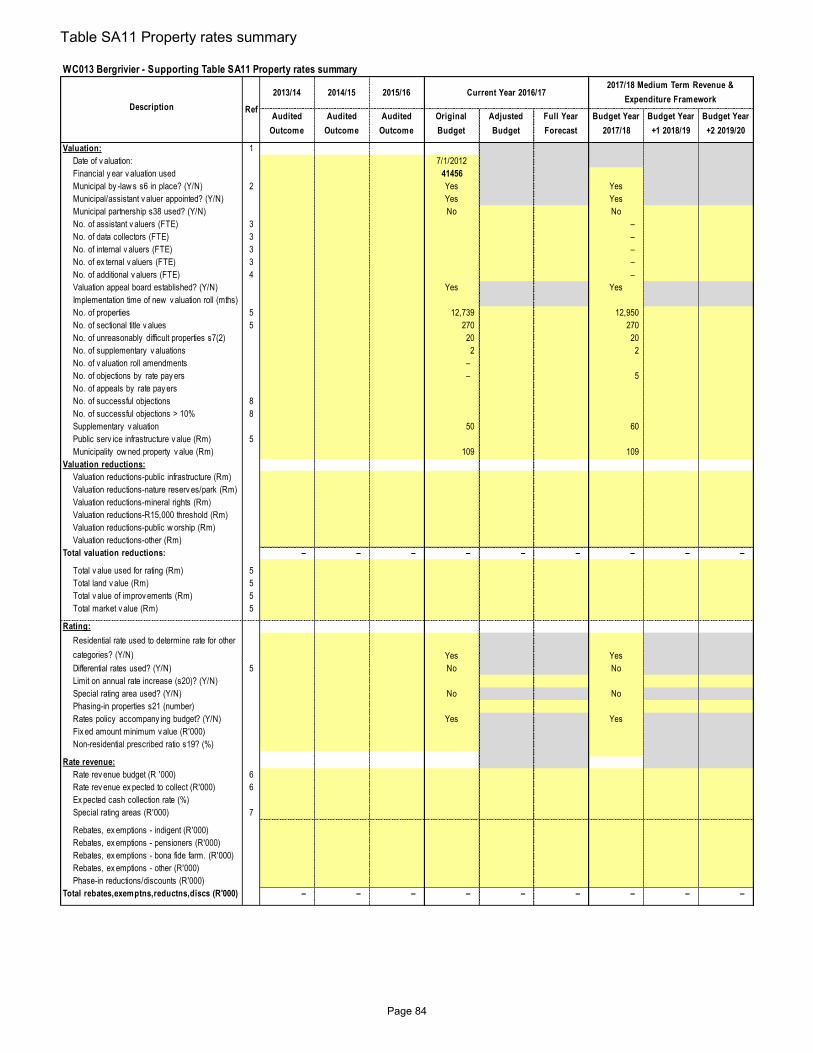

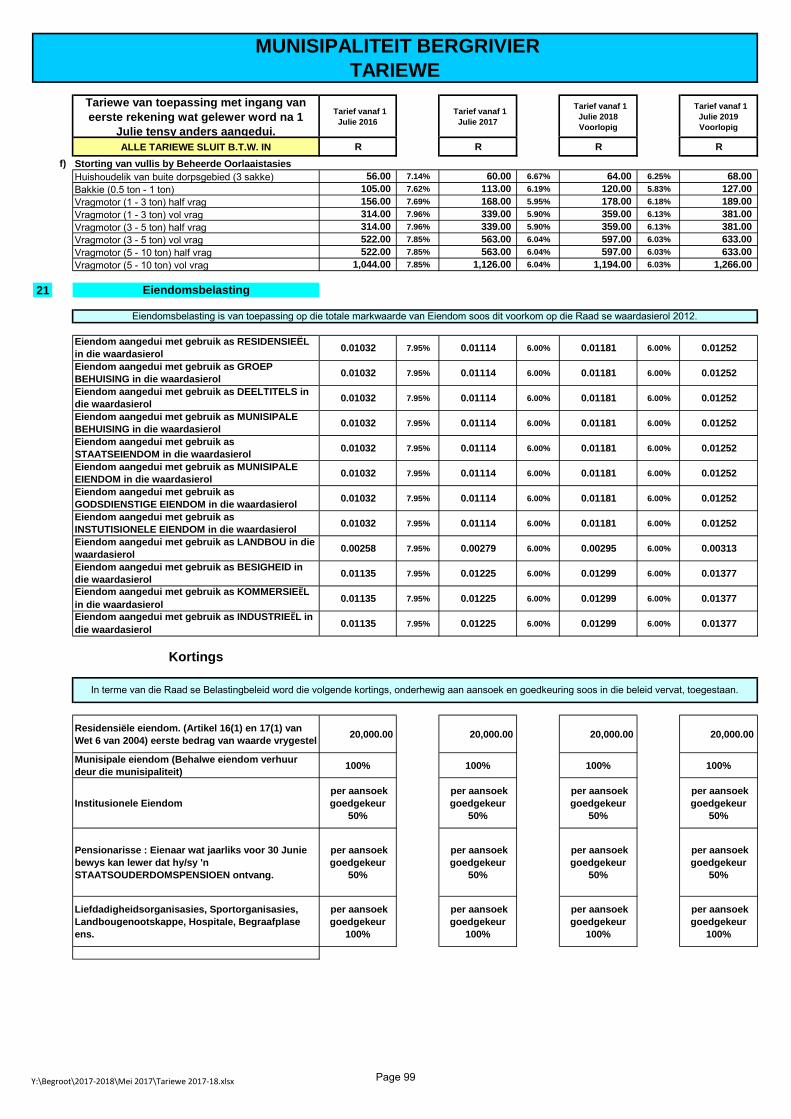

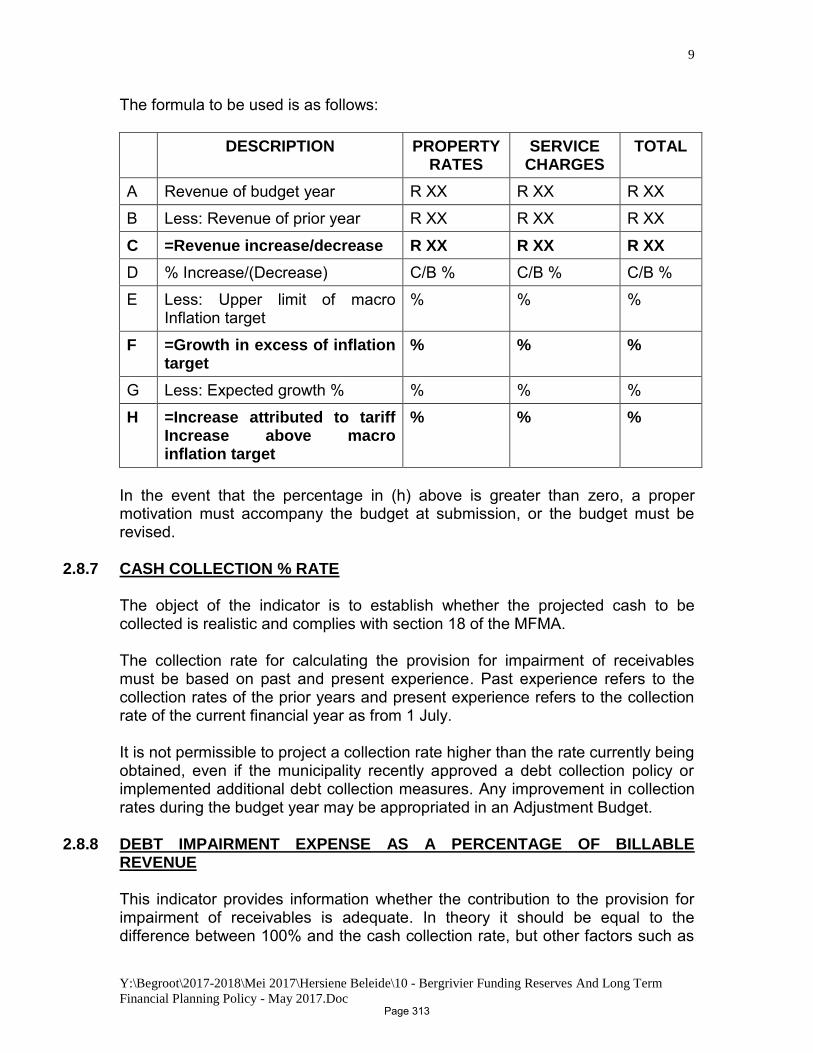

1.4.1 Property Rates Property rates cover the cost of the provision of general services. Determining the effective property rate tariff is therefore an integral part of the municipality’s budgeting process. National Treasury’s MFMA Circular No. 51 deals, inter alia with the implementation of the Municipal Property Rates Act, with the regulations issued by the Department of Co-operative Governance. These regulations came into effect on 1 July 2009 and prescribe the rate ratio for the non-residential categories, public service infrastructure and agricultural properties relative to residential properties to be a minimum of 0,25:1. The implementation of these regulations was done in the previous budget process and the Property Rates Policy of the Municipality has been amended accordingly. The following stipulations in the Property Rates Policy are highlighted: • The first R15 000 of the market value of a property used for residential purposes is

excluded from the rate-able value (Section 17(h) of the MPRA). In addition to this rebate, a further R5 000 reduction on the market value of a property will be granted in terms of the Municipality’s own Property Rates Policy;

• For pensioners, physically and mentally disabled persons, a maximum rebate of 50 percent will be granted to owners of rate-able property. In this regard the following stipulations are relevant:

- The rate-able property concerned must be occupied only by the applicant and his/her spouse, if any, and by dependants without income;

- The applicant must submit proof of his/her age and identity and, in the case of a physically or mentally handicapped person, proof of certification by a Medical Officer of Health, also proof of the annual income from a social pension;

- The applicant’s account must be paid in full, or if not, an arrangement to pay the debt should be in place; and

- The property must be categorized as residential. • The Municipality may award a 100 percent grant-in-aid on the assessment rates of rate-

able properties of certain classes such as registered welfare organizations, institutions or organizations performing charitable work, sports grounds used for purposes of amateur sport. The owner of such a property must apply to the Chief Financial Officer in the prescribed format for such a grant.

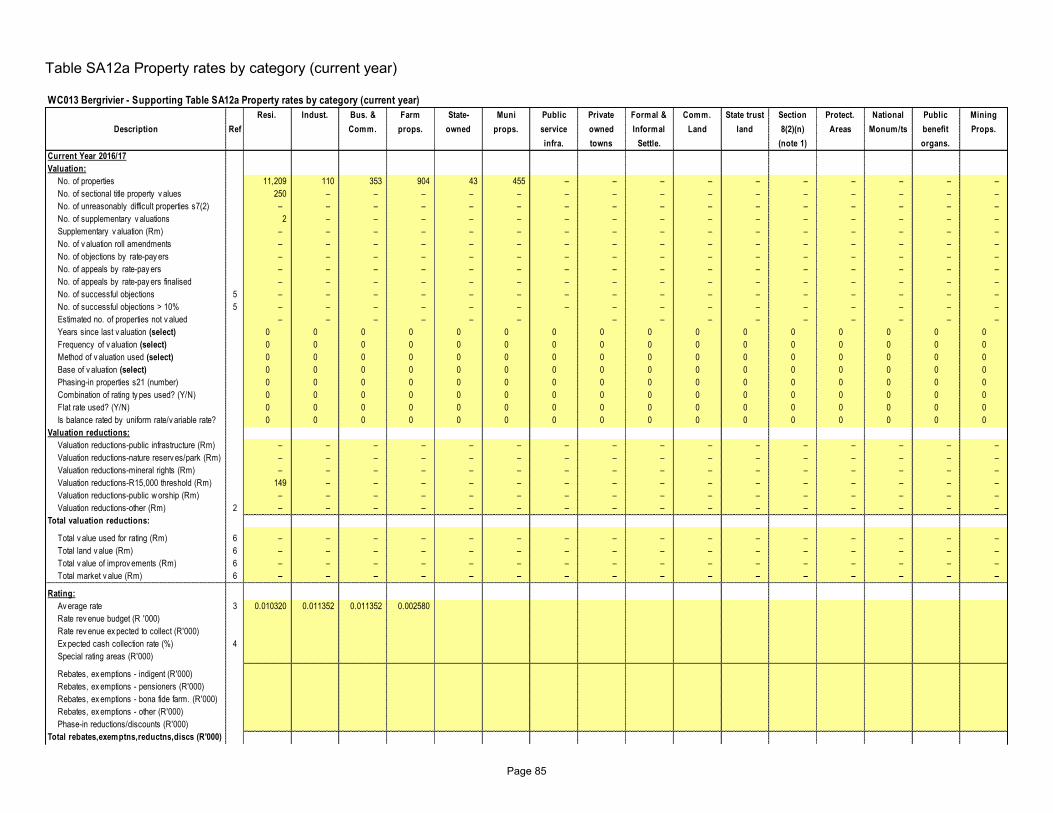

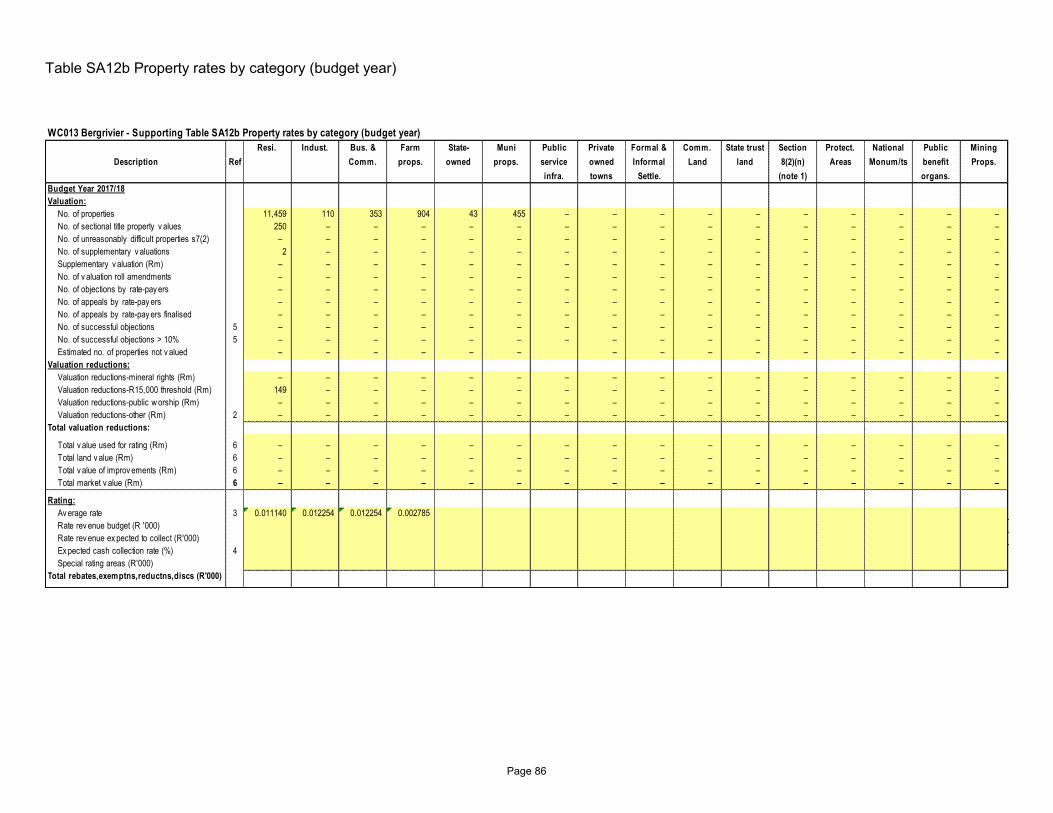

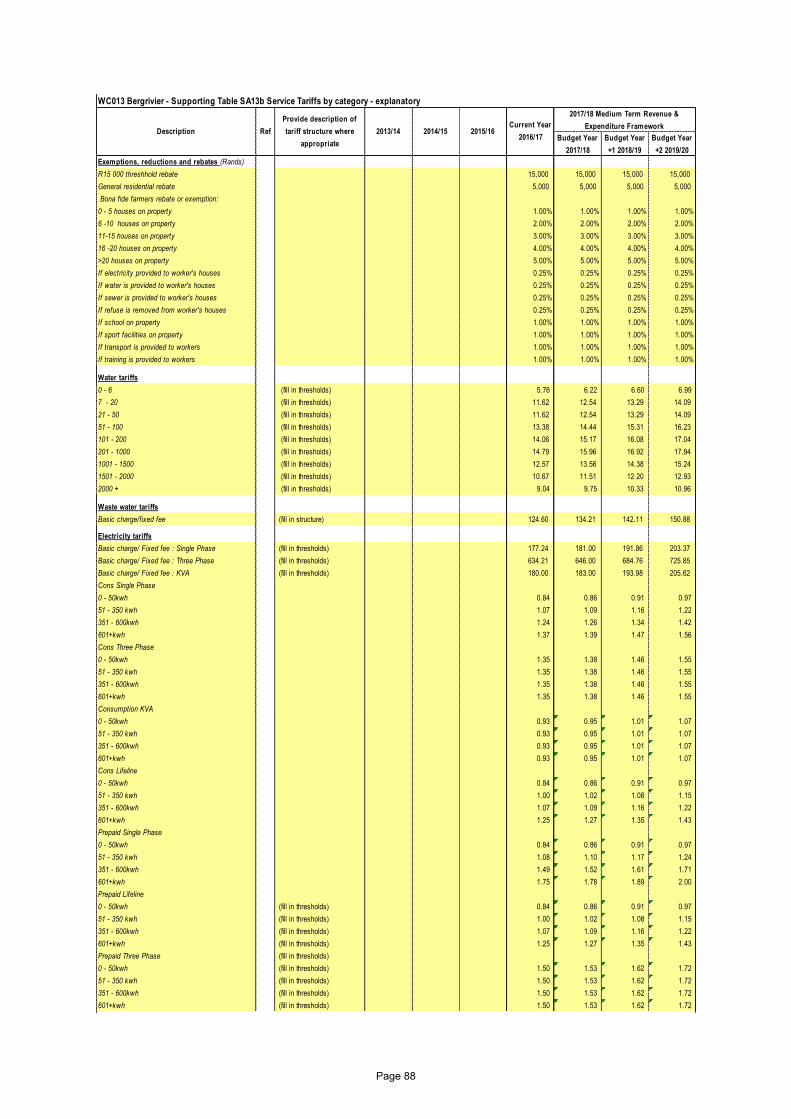

The categories of rate-able properties for purposes of levying rates and the proposed rates for the 2017/18 financial year based on approximately 7.9 percent increase from 1 July 2017 is contained below:

Page 7

Comparison of proposed rates to levy for the 2017/18 financial year

Category Current Tariff (1 July 2016)

Proposed tariff (from 1 July 2017)

c C

Residential properties .01032 .01114

Group Housing .01032 .01114

Sectional Schemes .01032 .01114

Municipal Houses .01032 .01114

State owned properties .01032 .01114

Municipal Properties .01032 .01114

Religious Properties .01032 .01114

Institutional Properties .01032 .01114

Agricultural .00258 .00279

Business Properties .01135 .01225

Commercial Properties .01135 .01225

Industrial Properties .01135 .01225

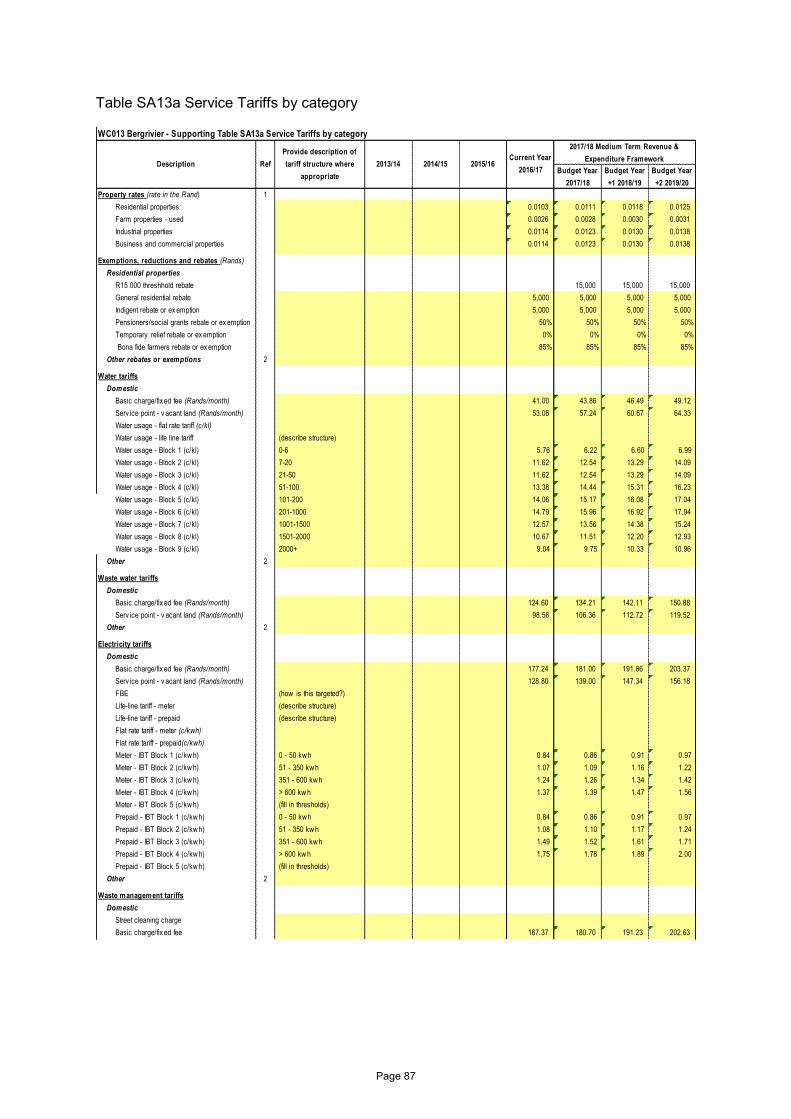

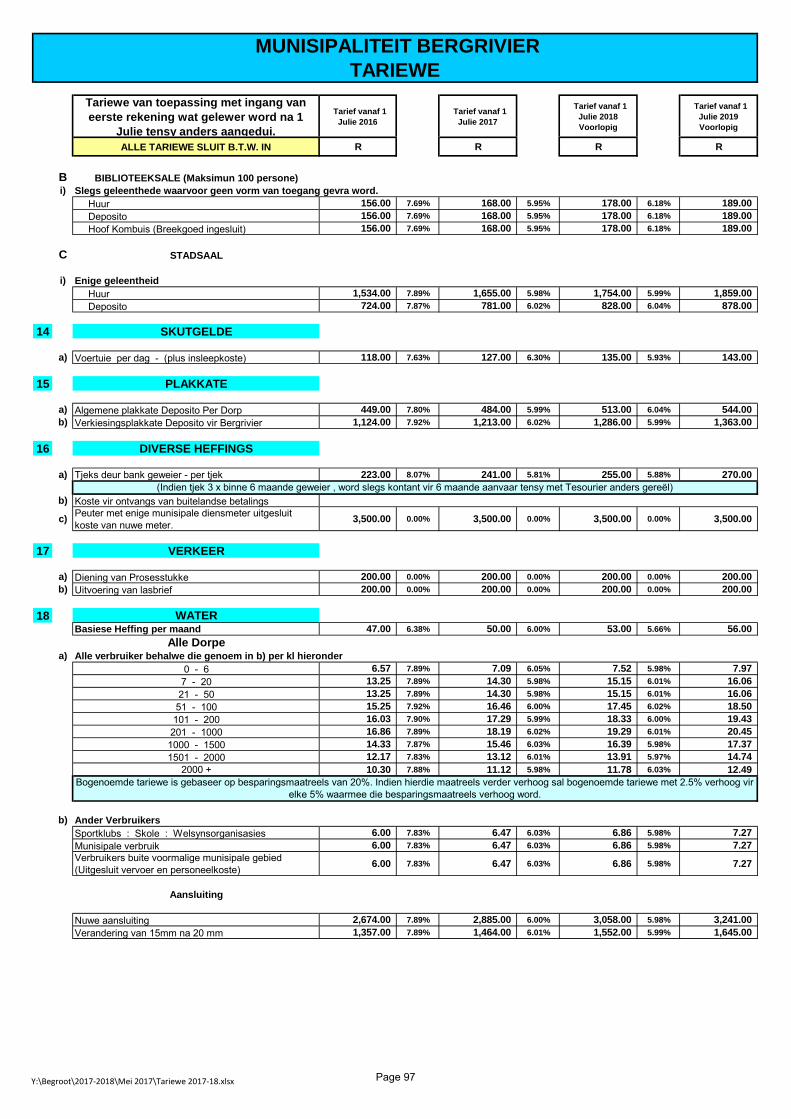

1.4.2 Sale of Water and Impact of Tariff Increases South Africa faces similar challenges with regard to water supply as it did with electricity, since demand growth outstrips supply. Consequently, National Treasury is encouraging all municipalities to carefully review the level and structure of their water tariffs to ensure: • Water tariffs are fully cost-reflective – including the cost of maintenance and renewal of

purification plants, water networks and the cost associated with reticulation expansion; • Water tariffs are structured to protect basic levels of service and ensure the provision of

free water to the poorest of the poor (indigent); and • Water tariffs are designed to encourage efficient and sustainable consumption. Better maintenance of infrastructure, new reservoir construction and cost-reflective tariffs will ensure that the supply challenges are managed in future to ensure sustainability. A tariff increase of approximately 7.9 percent from 1 July 2017 for water is proposed. In addition 6 kℓ water per month will ONLY be granted free of charge to registered indigent residents.

CATEGORY CURRENT TARIFFS

2016/17 VAT Incl

PROPOSED TARIFFS 2017/18 VAT Incl

Rand per kℓ Rand per kℓ

RESIDENTIAL

(i) 0 to 6 kℓ per 30-day period 6.57 7.09

(ii) 7 to 20 kℓ per 30-day period 13.25 14.30

(iii) 21 to 50 kℓ per 30-day period 13.25 14.30

(iv) 51 to 100 kℓ per 30-day period 15.25 16.46

(v) 101 to 200 kℓ per 30-day period 16.03 17.29

(vi) 201 to 1000 kl per 30-day period 16.86 18.19

(vii) 1001 to 1500 kl per 30-day period 14.33 15.46

(viii) 1501 to 2000 kl per 30-day period 12.17 13.12

(ix) More than 2000 kℓ per 30-day period: 10.30 11.12

The tariff structure of the 2017/18 financial year has not been changed. The tariff structure is designed to charge higher levels of consumption a higher rate, steadily increasing to a rate of R18.19 per kilolitre for consumption in excess of 200kℓ per month, thereafter the rate decrease.

Page 8

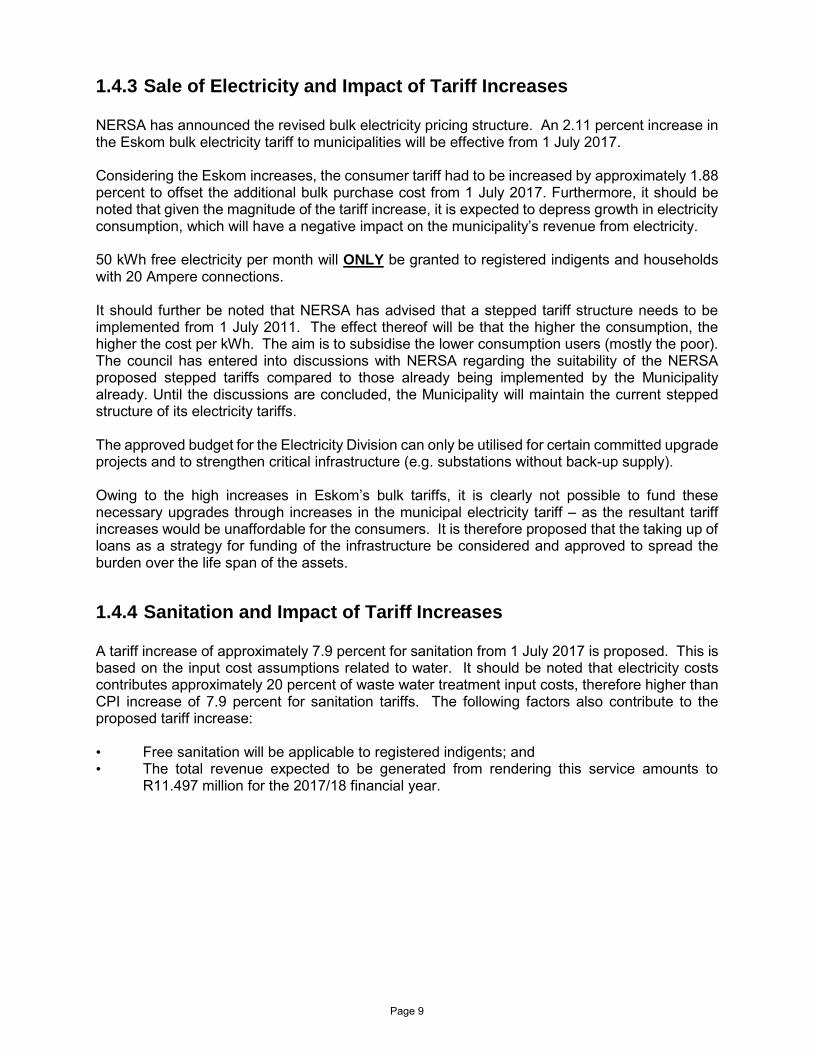

1.4.3 Sale of Electricity and Impact of Tariff Increases NERSA has announced the revised bulk electricity pricing structure. An 2.11 percent increase in the Eskom bulk electricity tariff to municipalities will be effective from 1 July 2017. Considering the Eskom increases, the consumer tariff had to be increased by approximately 1.88 percent to offset the additional bulk purchase cost from 1 July 2017. Furthermore, it should be noted that given the magnitude of the tariff increase, it is expected to depress growth in electricity consumption, which will have a negative impact on the municipality’s revenue from electricity. 50 kWh free electricity per month will ONLY be granted to registered indigents and households with 20 Ampere connections. It should further be noted that NERSA has advised that a stepped tariff structure needs to be implemented from 1 July 2011. The effect thereof will be that the higher the consumption, the higher the cost per kWh. The aim is to subsidise the lower consumption users (mostly the poor). The council has entered into discussions with NERSA regarding the suitability of the NERSA proposed stepped tariffs compared to those already being implemented by the Municipality already. Until the discussions are concluded, the Municipality will maintain the current stepped structure of its electricity tariffs. The approved budget for the Electricity Division can only be utilised for certain committed upgrade projects and to strengthen critical infrastructure (e.g. substations without back-up supply). Owing to the high increases in Eskom’s bulk tariffs, it is clearly not possible to fund these necessary upgrades through increases in the municipal electricity tariff – as the resultant tariff increases would be unaffordable for the consumers. It is therefore proposed that the taking up of loans as a strategy for funding of the infrastructure be considered and approved to spread the burden over the life span of the assets.

1.4.4 Sanitation and Impact of Tariff Increases A tariff increase of approximately 7.9 percent for sanitation from 1 July 2017 is proposed. This is based on the input cost assumptions related to water. It should be noted that electricity costs contributes approximately 20 percent of waste water treatment input costs, therefore higher than CPI increase of 7.9 percent for sanitation tariffs. The following factors also contribute to the proposed tariff increase: • Free sanitation will be applicable to registered indigents; and • The total revenue expected to be generated from rendering this service amounts to

R11.497 million for the 2017/18 financial year.

Page 9

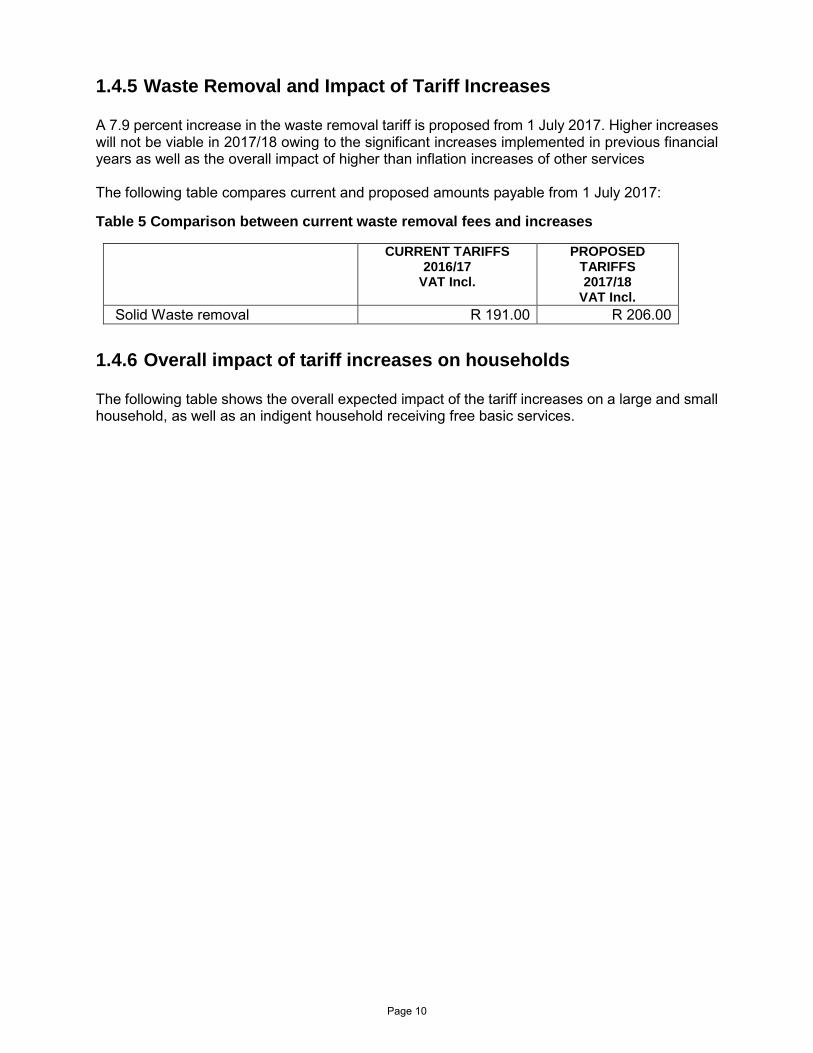

1.4.5 Waste Removal and Impact of Tariff Increases A 7.9 percent increase in the waste removal tariff is proposed from 1 July 2017. Higher increases will not be viable in 2017/18 owing to the significant increases implemented in previous financial years as well as the overall impact of higher than inflation increases of other services The following table compares current and proposed amounts payable from 1 July 2017:

Table 5 Comparison between current waste removal fees and increases

CURRENT TARIFFS 2016/17

VAT Incl.

PROPOSED TARIFFS 2017/18

VAT Incl.

Solid Waste removal R 191.00 R 206.00

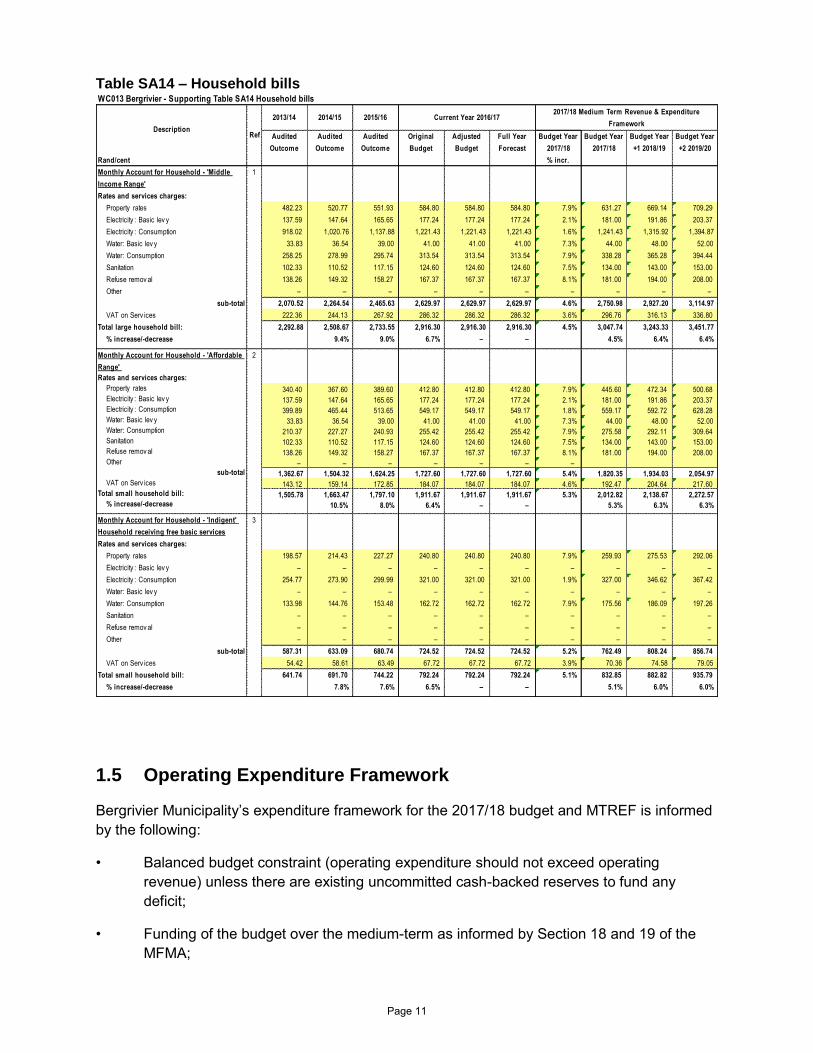

1.4.6 Overall impact of tariff increases on households

The following table shows the overall expected impact of the tariff increases on a large and small household, as well as an indigent household receiving free basic services.

Page 10

Table SA14 – Household bills

2

1.5 Operating Expenditure Framework

Bergrivier Municipality’s expenditure framework for the 2017/18 budget and MTREF is informed

by the following:

• Balanced budget constraint (operating expenditure should not exceed operating

revenue) unless there are existing uncommitted cash-backed reserves to fund any

deficit;

• Funding of the budget over the medium-term as informed by Section 18 and 19 of the

MFMA;

WC013 Bergrivier - Supporting Table SA14 Household bills

2013/14 2014/15 2015/162017/18 Medium Term Revenue & Expenditure

Framework

Audited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Budget Year

2017/18

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Rand/cent % incr.

Monthly Account for Household - 'Middle

Income Range'

1

Rates and services charges:

Property rates 482.23 520.77 551.93 584.80 584.80 584.80 7.9% 631.27 669.14 709.29

Electricity : Basic lev y 137.59 147.64 165.65 177.24 177.24 177.24 2.1% 181.00 191.86 203.37

Electricity : Consumption 918.02 1,020.76 1,137.88 1,221.43 1,221.43 1,221.43 1.6% 1,241.43 1,315.92 1,394.87

Water: Basic lev y 33.83 36.54 39.00 41.00 41.00 41.00 7.3% 44.00 48.00 52.00

Water: Consumption 258.25 278.99 295.74 313.54 313.54 313.54 7.9% 338.28 365.28 394.44

Sanitation 102.33 110.52 117.15 124.60 124.60 124.60 7.5% 134.00 143.00 153.00

Refuse remov al 138.26 149.32 158.27 167.37 167.37 167.37 8.1% 181.00 194.00 208.00

Other – – – – – – – – – –

sub-total 2,070.52 2,264.54 2,465.63 2,629.97 2,629.97 2,629.97 4.6% 2,750.98 2,927.20 3,114.97

VAT on Serv ices 222.36 244.13 267.92 286.32 286.32 286.32 3.6% 296.76 316.13 336.80

Total large household bill: 2,292.88 2,508.67 2,733.55 2,916.30 2,916.30 2,916.30 4.5% 3,047.74 3,243.33 3,451.77

% increase/-decrease 9.4% 9.0% 6.7% – – 4.5% 6.4% 6.4%

Monthly Account for Household - 'Affordable

Range'

2

Rates and services charges:

Property rates 340.40 367.60 389.60 412.80 412.80 412.80 7.9% 445.60 472.34 500.68

Electricity : Basic lev y 137.59 147.64 165.65 177.24 177.24 177.24 2.1% 181.00 191.86 203.37

Electricity : Consumption 399.89 465.44 513.65 549.17 549.17 549.17 1.8% 559.17 592.72 628.28

Water: Basic lev y 33.83 36.54 39.00 41.00 41.00 41.00 7.3% 44.00 48.00 52.00

Water: Consumption 210.37 227.27 240.93 255.42 255.42 255.42 7.9% 275.58 292.11 309.64

Sanitation 102.33 110.52 117.15 124.60 124.60 124.60 7.5% 134.00 143.00 153.00

Refuse remov al 138.26 149.32 158.27 167.37 167.37 167.37 8.1% 181.00 194.00 208.00

Other – – – – – – –

sub-total 1,362.67 1,504.32 1,624.25 1,727.60 1,727.60 1,727.60 5.4% 1,820.35 1,934.03 2,054.97

VAT on Serv ices 143.12 159.14 172.85 184.07 184.07 184.07 4.6% 192.47 204.64 217.60

Total small household bill: 1,505.78 1,663.47 1,797.10 1,911.67 1,911.67 1,911.67 5.3% 2,012.82 2,138.67 2,272.57

% increase/-decrease 10.5% 8.0% 6.4% – – 5.3% 6.3% 6.3%

-0.23 -0.21 -1.00 - Monthly Account for Household - 'Indigent'

Household receiving free basic services

3

Rates and services charges:

Property rates 198.57 214.43 227.27 240.80 240.80 240.80 7.9% 259.93 275.53 292.06

Electricity : Basic lev y – – – – – – – – – –

Electricity : Consumption 254.77 273.90 299.99 321.00 321.00 321.00 1.9% 327.00 346.62 367.42

Water: Basic lev y – – – – – – – – – –

Water: Consumption 133.98 144.76 153.48 162.72 162.72 162.72 7.9% 175.56 186.09 197.26

Sanitation – – – – – – – – – –

Refuse remov al – – – – – – – – – –

Other – – – – – – – – – –

sub-total 587.31 633.09 680.74 724.52 724.52 724.52 5.2% 762.49 808.24 856.74

VAT on Serv ices 54.42 58.61 63.49 67.72 67.72 67.72 3.9% 70.36 74.58 79.05

Total small household bill: 641.74 691.70 744.22 792.24 792.24 792.24 5.1% 832.85 882.82 935.79

% increase/-decrease 7.8% 7.6% 6.5% – – 5.1% 6.0% 6.0%

Ref

Current Year 2016/17

Description

Page 11

• The capital programme is aligned to the asset renewal strategy and backlog eradication

plan;

• Operational gains and efficiencies will be directed to funding the capital budget and other

core services; and

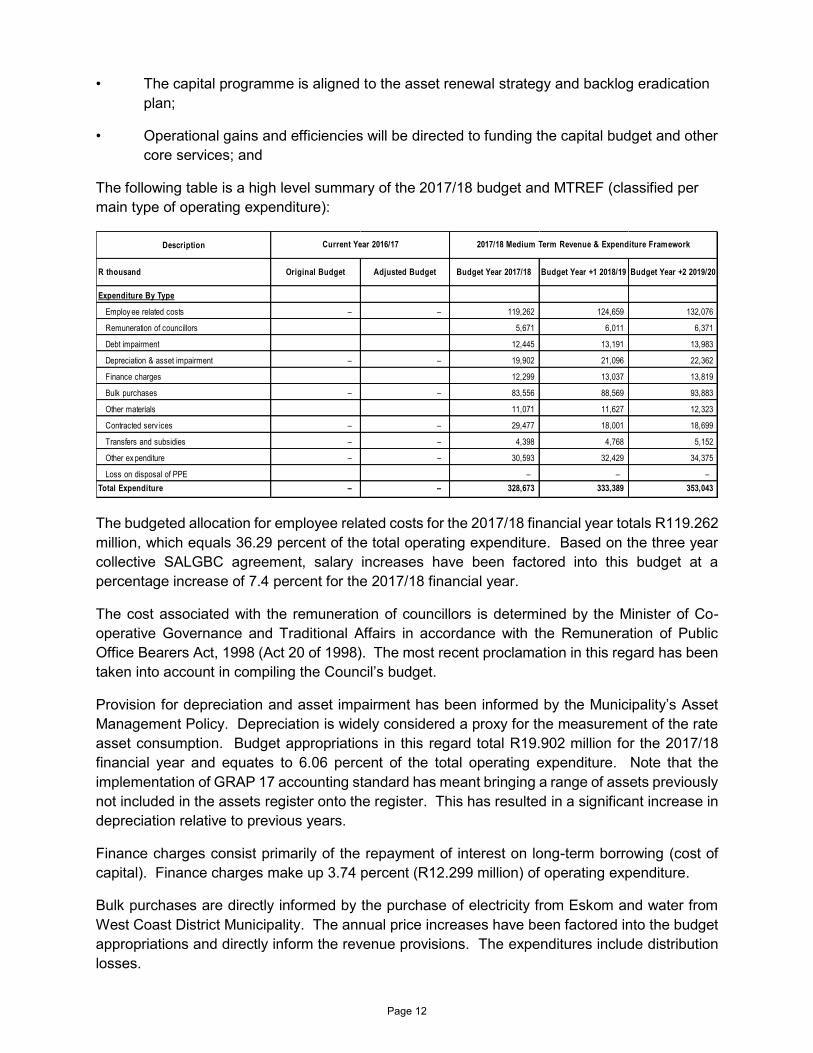

The following table is a high level summary of the 2017/18 budget and MTREF (classified per

main type of operating expenditure):

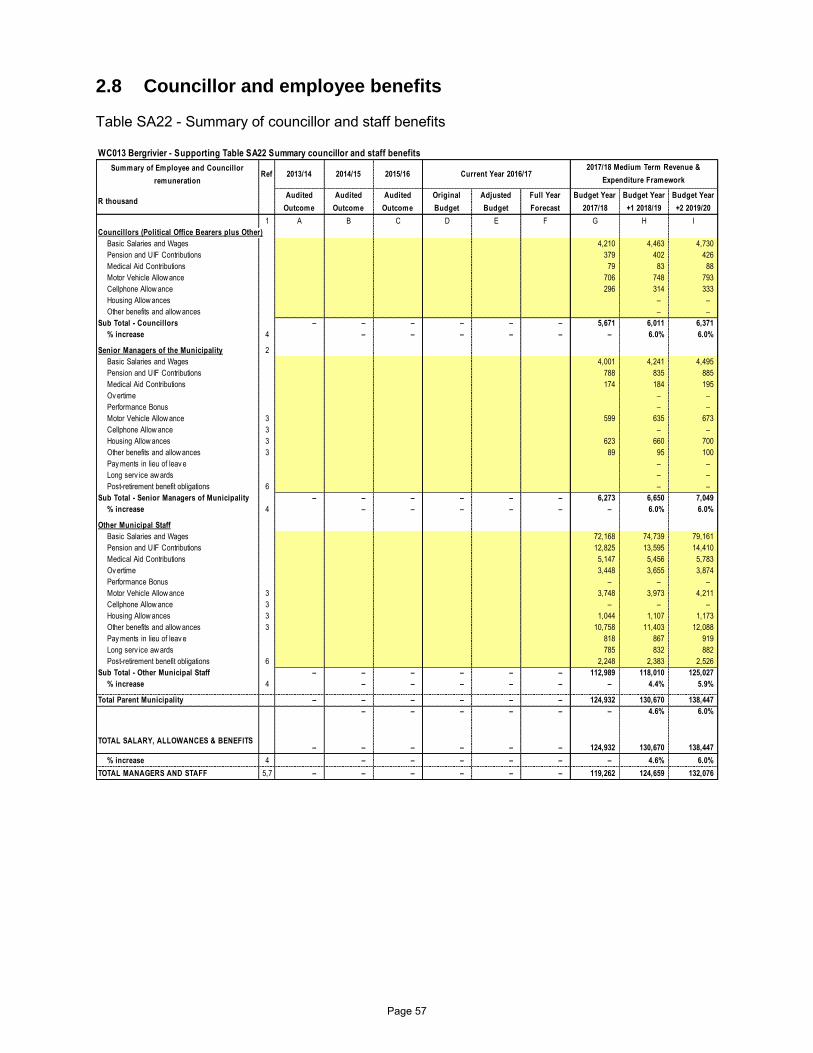

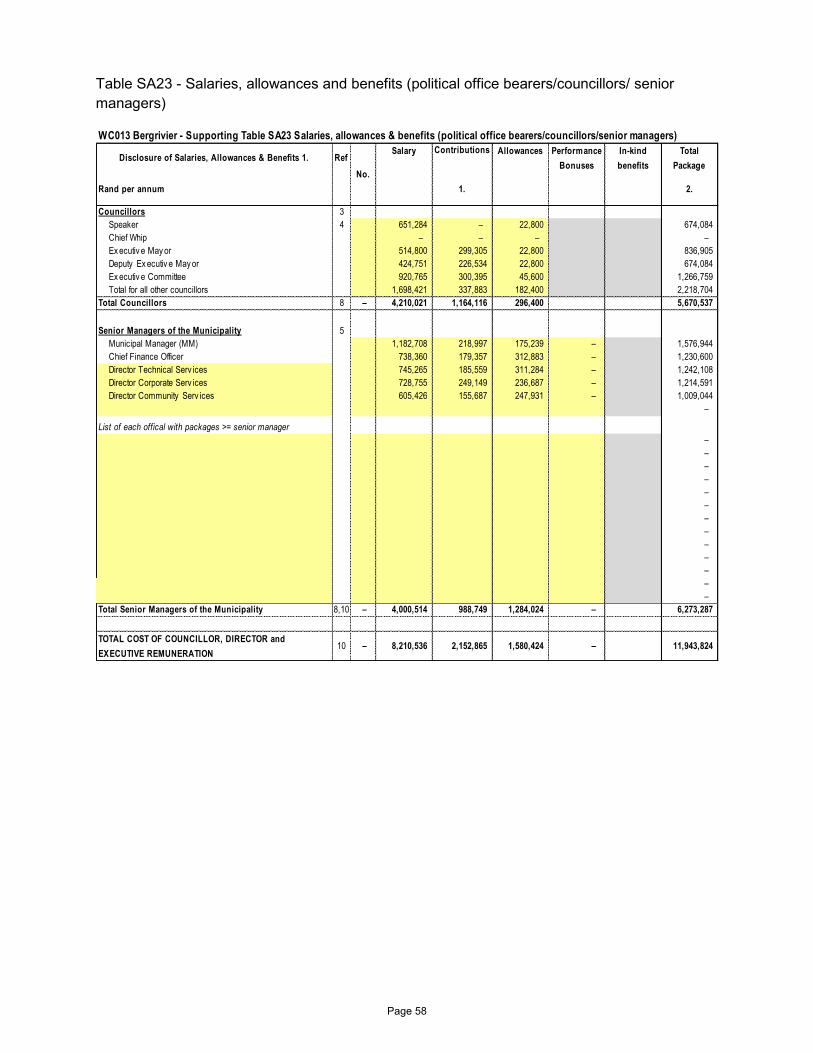

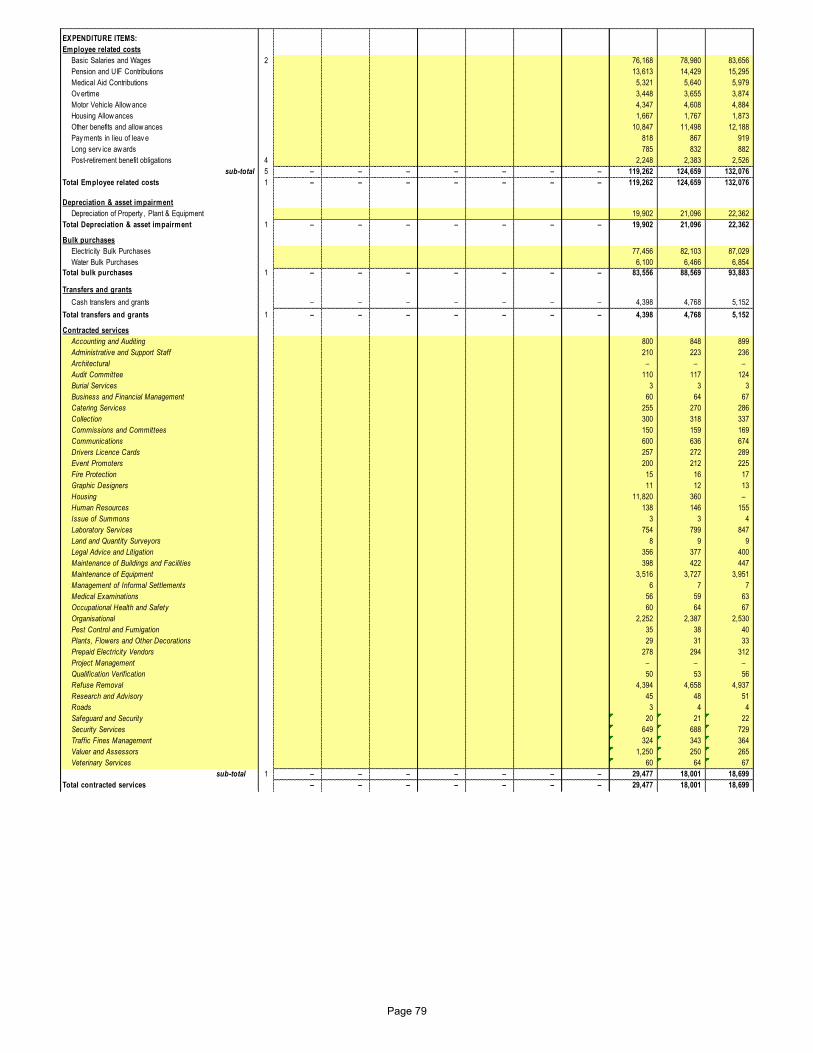

The budgeted allocation for employee related costs for the 2017/18 financial year totals R119.262

million, which equals 36.29 percent of the total operating expenditure. Based on the three year

collective SALGBC agreement, salary increases have been factored into this budget at a

percentage increase of 7.4 percent for the 2017/18 financial year.

The cost associated with the remuneration of councillors is determined by the Minister of Co-

operative Governance and Traditional Affairs in accordance with the Remuneration of Public

Office Bearers Act, 1998 (Act 20 of 1998). The most recent proclamation in this regard has been

taken into account in compiling the Council’s budget.

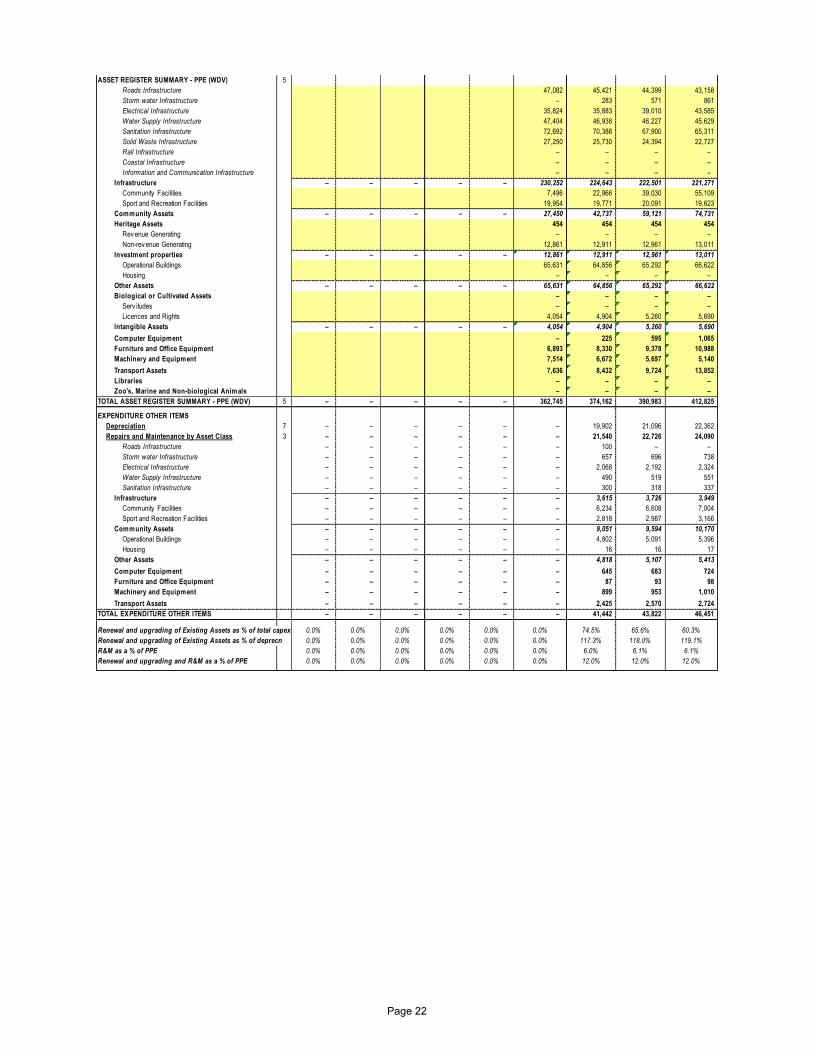

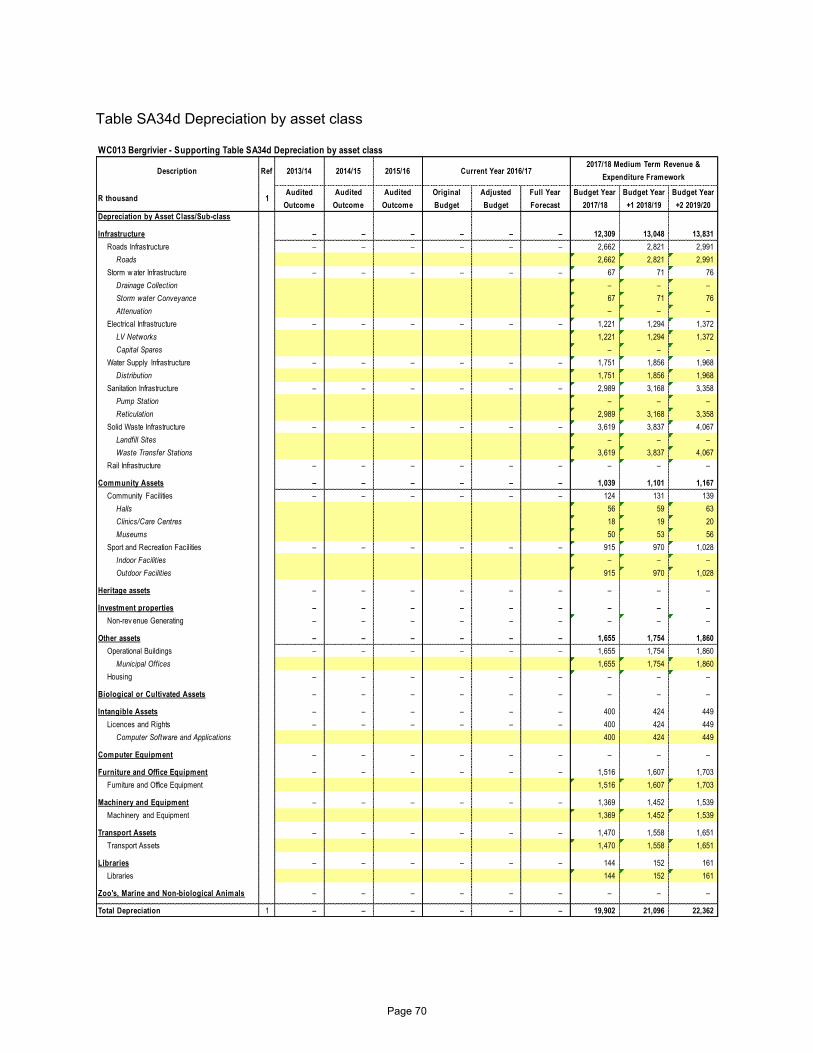

Provision for depreciation and asset impairment has been informed by the Municipality’s Asset

Management Policy. Depreciation is widely considered a proxy for the measurement of the rate

asset consumption. Budget appropriations in this regard total R19.902 million for the 2017/18

financial year and equates to 6.06 percent of the total operating expenditure. Note that the

implementation of GRAP 17 accounting standard has meant bringing a range of assets previously

not included in the assets register onto the register. This has resulted in a significant increase in

depreciation relative to previous years.

Finance charges consist primarily of the repayment of interest on long-term borrowing (cost of

capital). Finance charges make up 3.74 percent (R12.299 million) of operating expenditure.

Bulk purchases are directly informed by the purchase of electricity from Eskom and water from

West Coast District Municipality. The annual price increases have been factored into the budget

appropriations and directly inform the revenue provisions. The expenditures include distribution

losses.

Description

R thousand Original Budget Adjusted Budget Budget Year 2017/18 Budget Year +1 2018/19 Budget Year +2 2019/20

Expenditure By Type

Employ ee related costs – – 119,262 124,659 132,076

Remuneration of councillors 5,671 6,011 6,371

Debt impairment 12,445 13,191 13,983

Depreciation & asset impairment – – 19,902 21,096 22,362

Finance charges 12,299 13,037 13,819

Bulk purchases – – 83,556 88,569 93,883

Other materials 11,071 11,627 12,323

Contracted serv ices – – 29,477 18,001 18,699

Transfers and subsidies – – 4,398 4,768 5,152

Other ex penditure – – 30,593 32,429 34,375

Loss on disposal of PPE – – –

Total Expenditure – – 328,673 333,389 353,043

Current Year 2016/17 2017/18 Medium Term Revenue & Expenditure Framework

Page 12

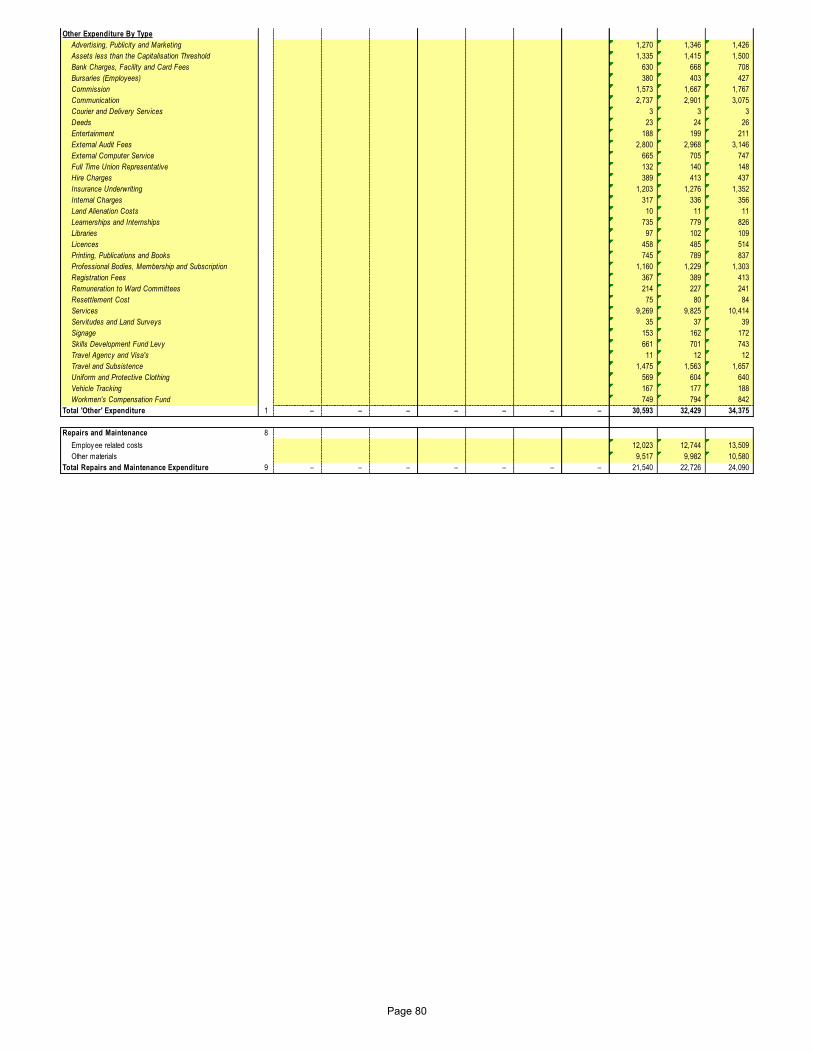

Other expenditure comprises of various line items relating to the daily operations of the

municipality. This group of expenditure has also been identified as an area in which cost

savings and efficiencies can be achieved. Further details relating to contracted services can be

seen in Table SA1.

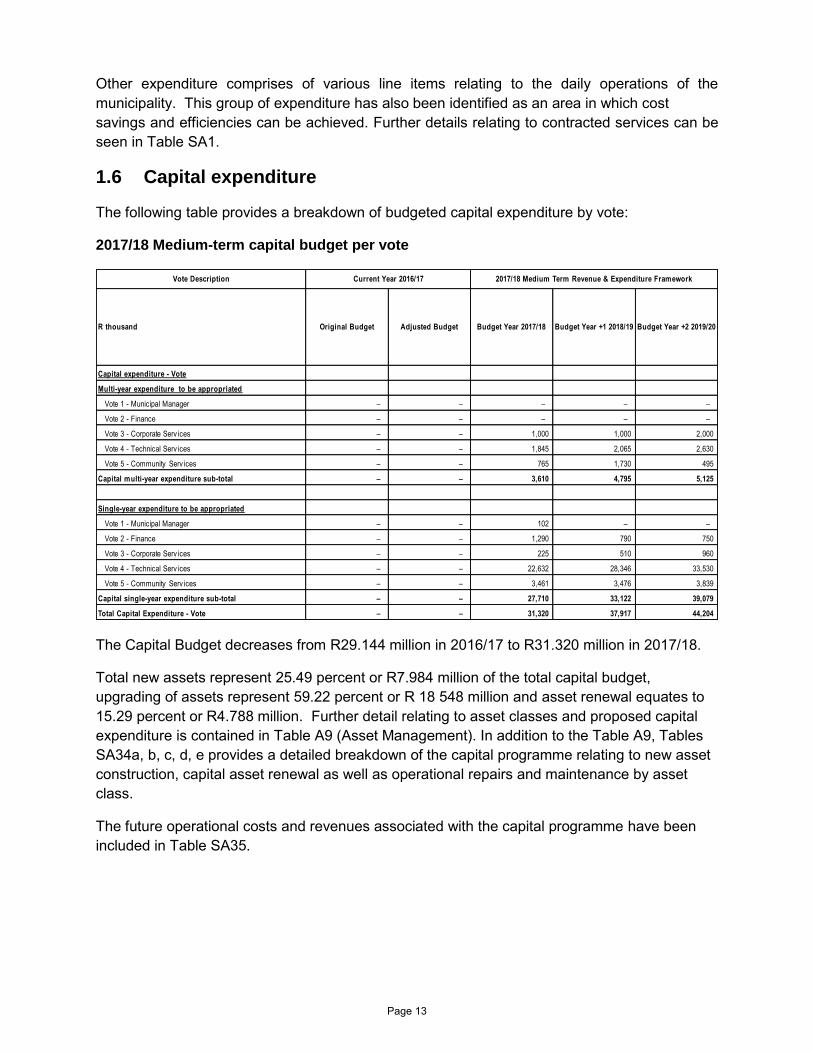

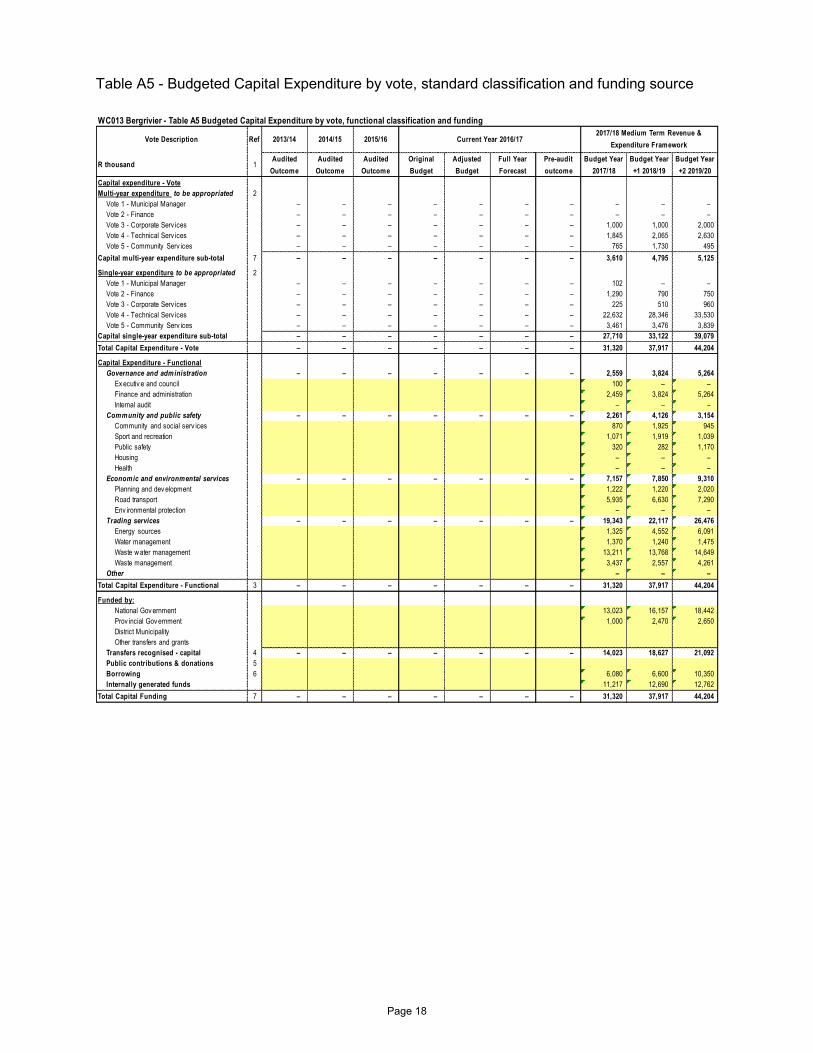

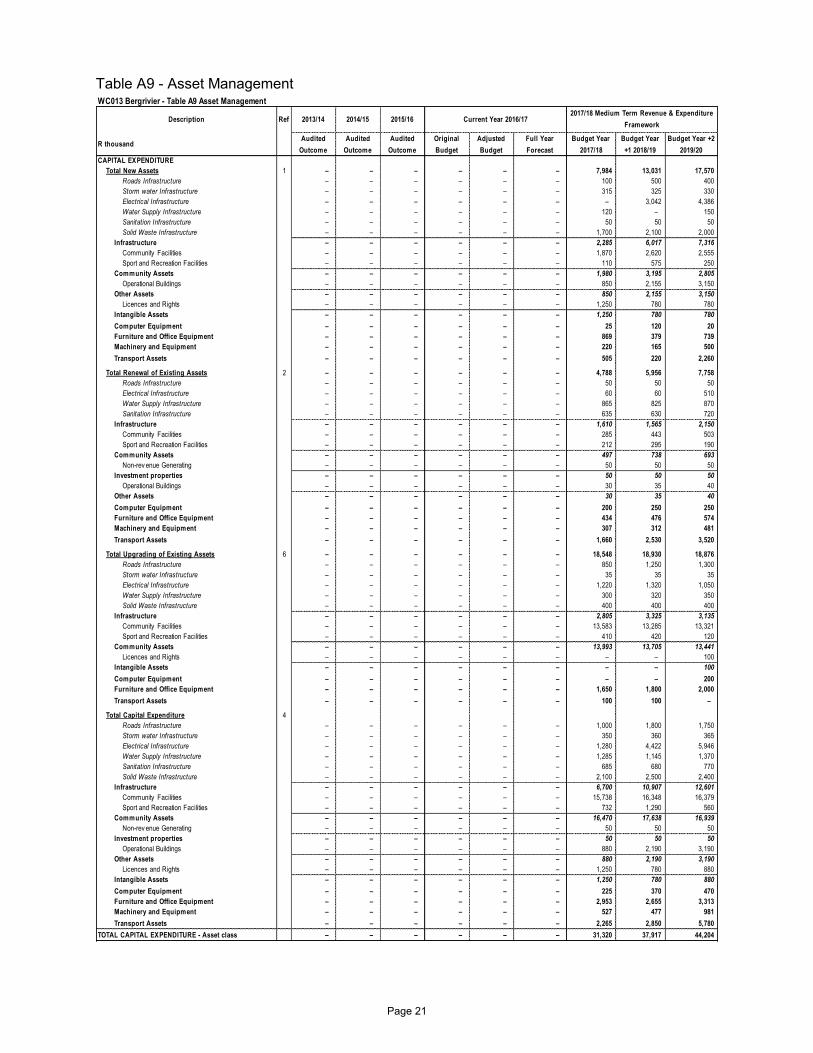

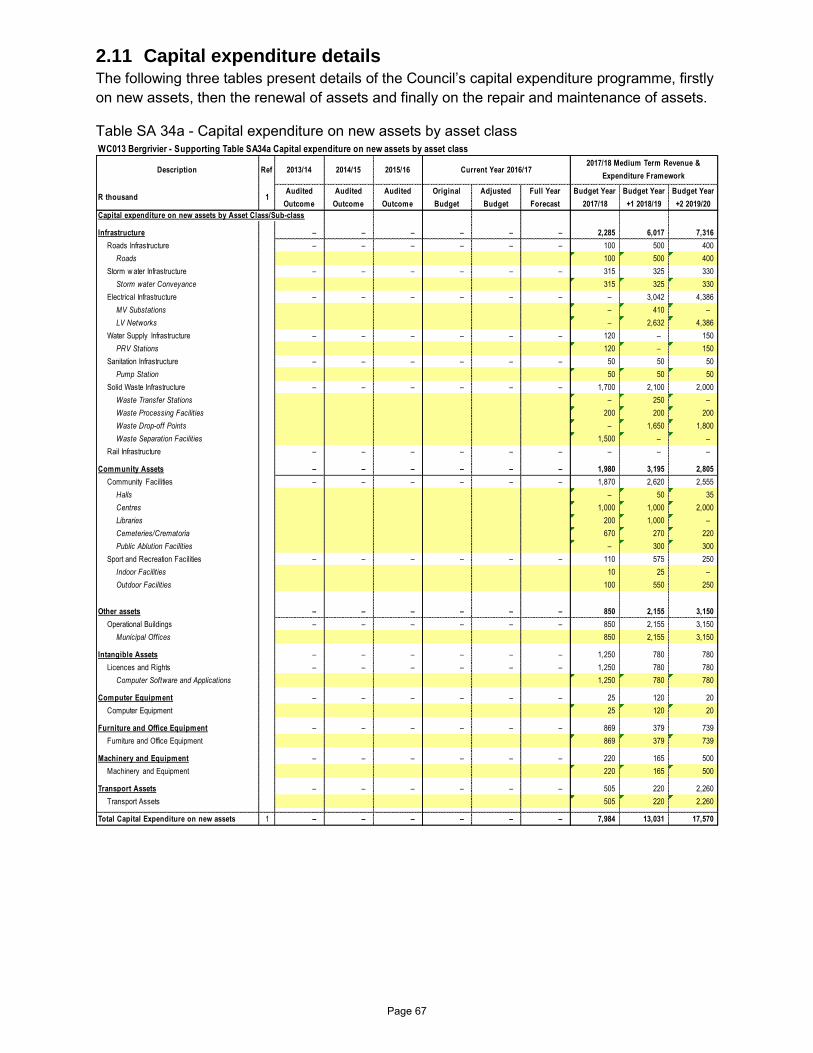

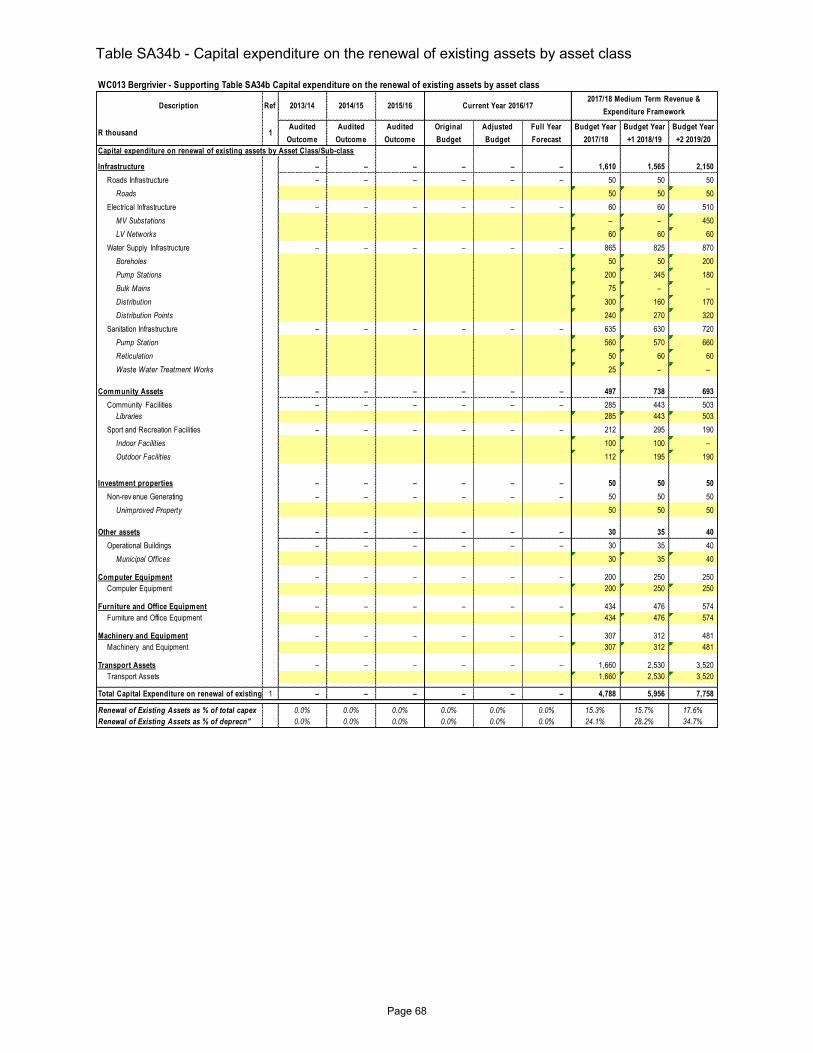

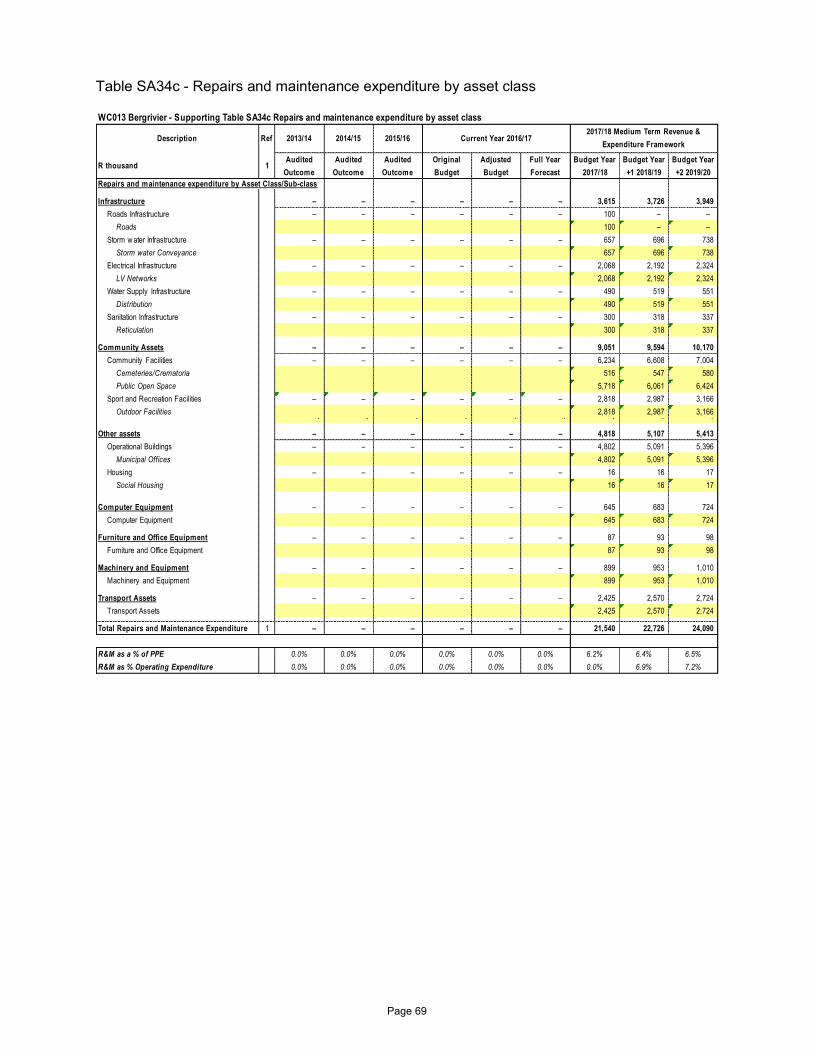

1.6 Capital expenditure

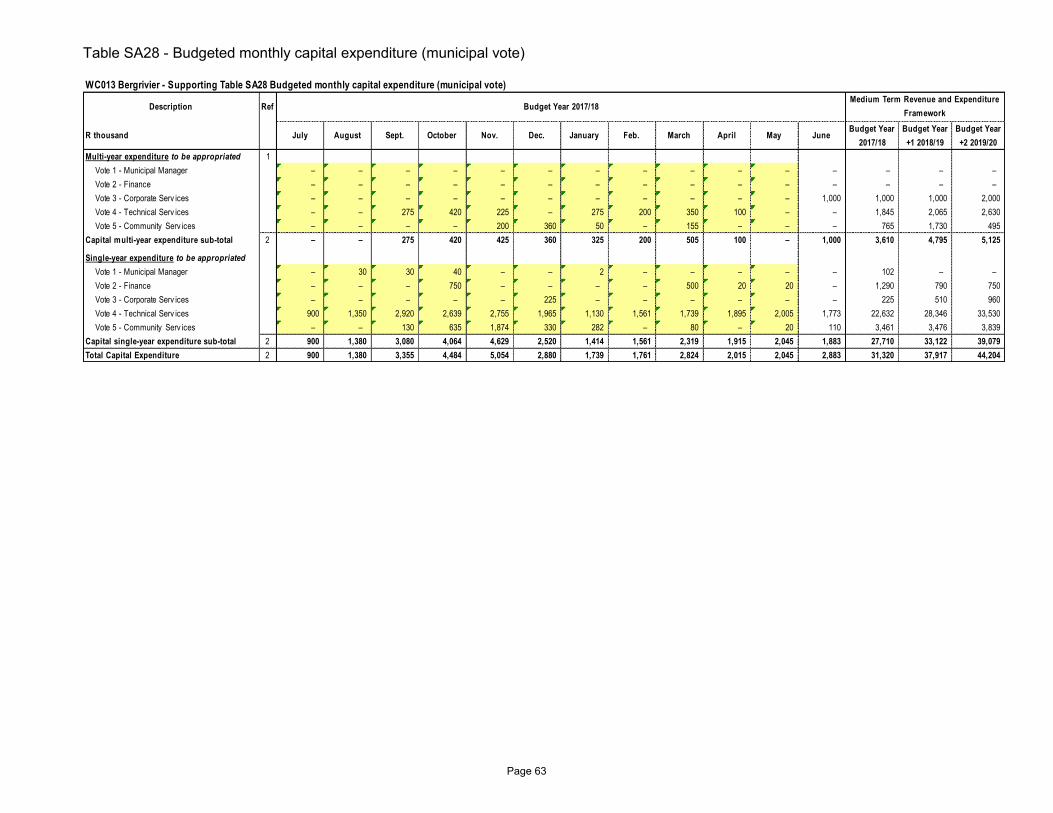

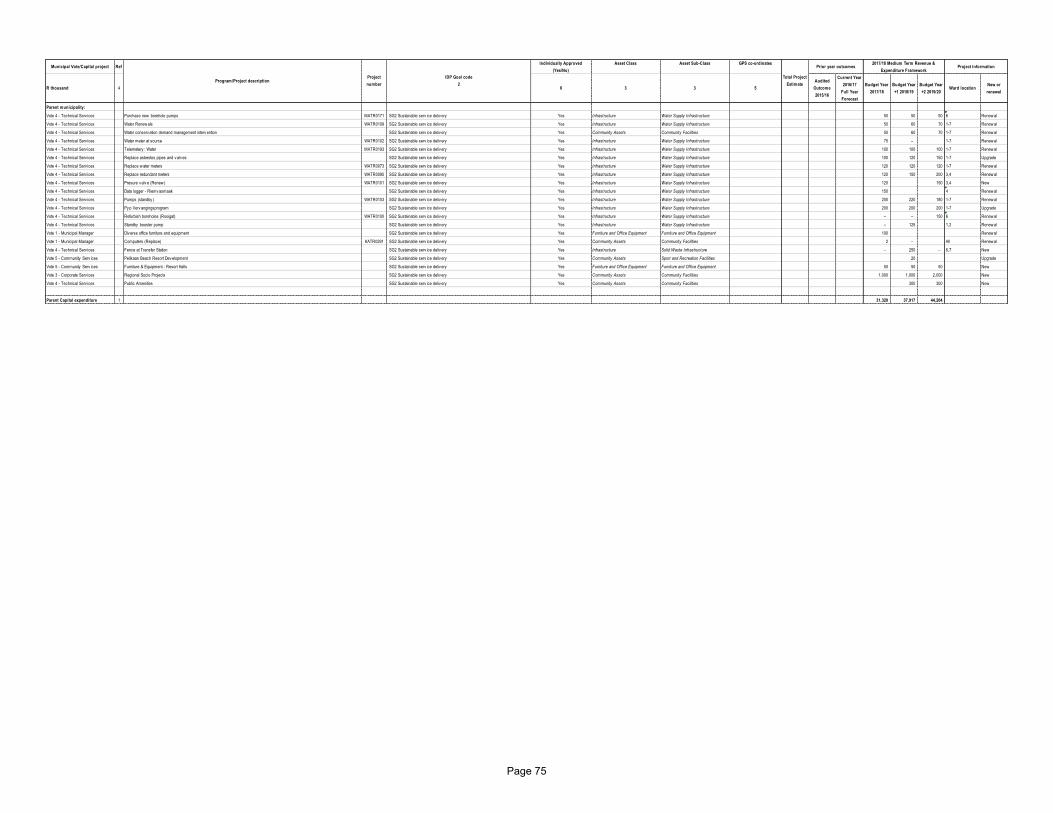

The following table provides a breakdown of budgeted capital expenditure by vote:

2017/18 Medium-term capital budget per vote

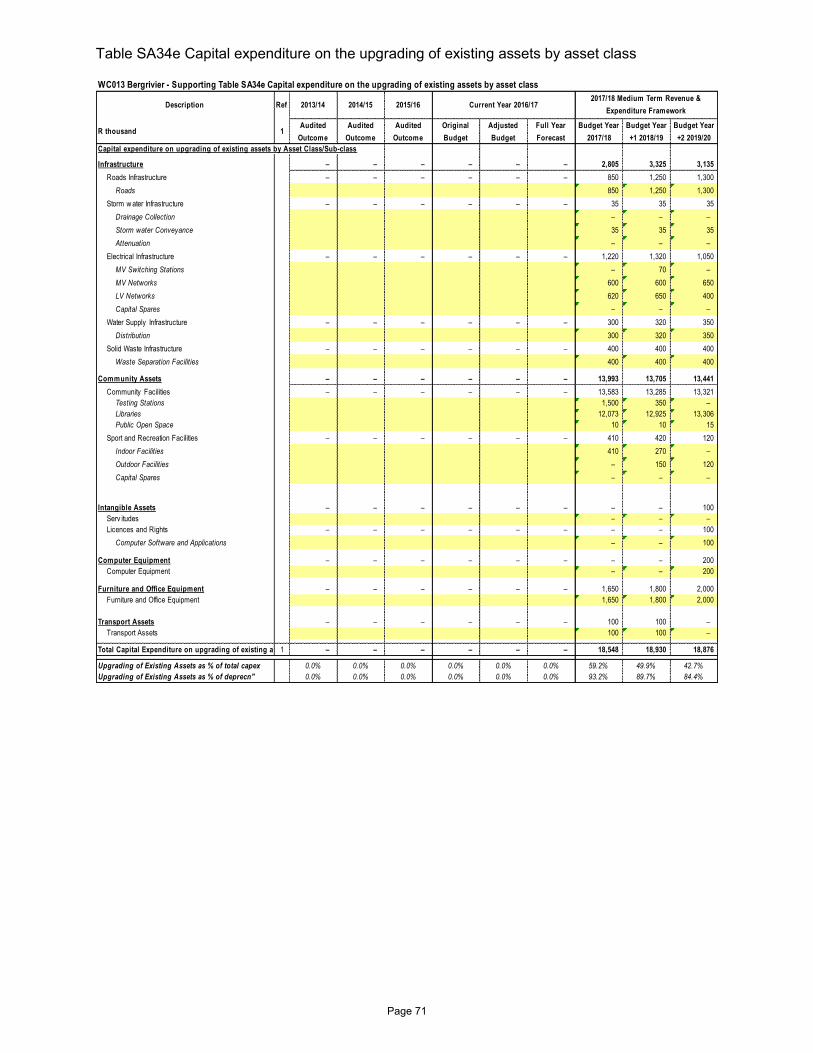

The Capital Budget decreases from R29.144 million in 2016/17 to R31.320 million in 2017/18.

Total new assets represent 25.49 percent or R7.984 million of the total capital budget,

upgrading of assets represent 59.22 percent or R 18 548 million and asset renewal equates to

15.29 percent or R4.788 million. Further detail relating to asset classes and proposed capital

expenditure is contained in Table A9 (Asset Management). In addition to the Table A9, Tables

SA34a, b, c, d, e provides a detailed breakdown of the capital programme relating to new asset

construction, capital asset renewal as well as operational repairs and maintenance by asset

class.

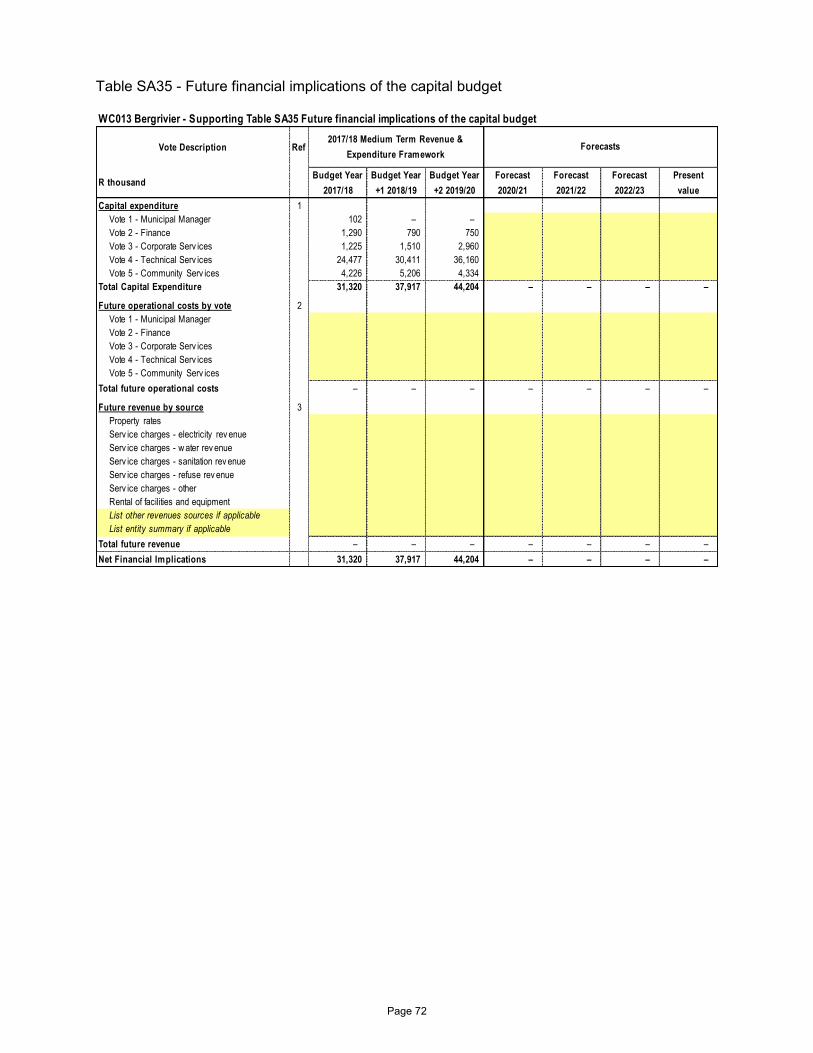

The future operational costs and revenues associated with the capital programme have been

included in Table SA35.

Vote Description

R thousand Original Budget Adjusted Budget Budget Year 2017/18 Budget Year +1 2018/19 Budget Year +2 2019/20

Capital expenditure - Vote

Multi-year expenditure to be appropriated

Vote 1 - Municipal Manager – – – – –

Vote 2 - Finance – – – – –

Vote 3 - Corporate Serv ices – – 1,000 1,000 2,000

Vote 4 - Technical Serv ices – – 1,845 2,065 2,630

Vote 5 - Community Serv ices – – 765 1,730 495

Capital multi-year expenditure sub-total – – 3,610 4,795 5,125

Single-year expenditure to be appropriated

Vote 1 - Municipal Manager – – 102 – –

Vote 2 - Finance – – 1,290 790 750

Vote 3 - Corporate Serv ices – – 225 510 960

Vote 4 - Technical Serv ices – – 22,632 28,346 33,530

Vote 5 - Community Serv ices – – 3,461 3,476 3,839

Capital single-year expenditure sub-total – – 27,710 33,122 39,079

Total Capital Expenditure - Vote – – 31,320 37,917 44,204

Current Year 2016/17 2017/18 Medium Term Revenue & Expenditure Framework

Page 13

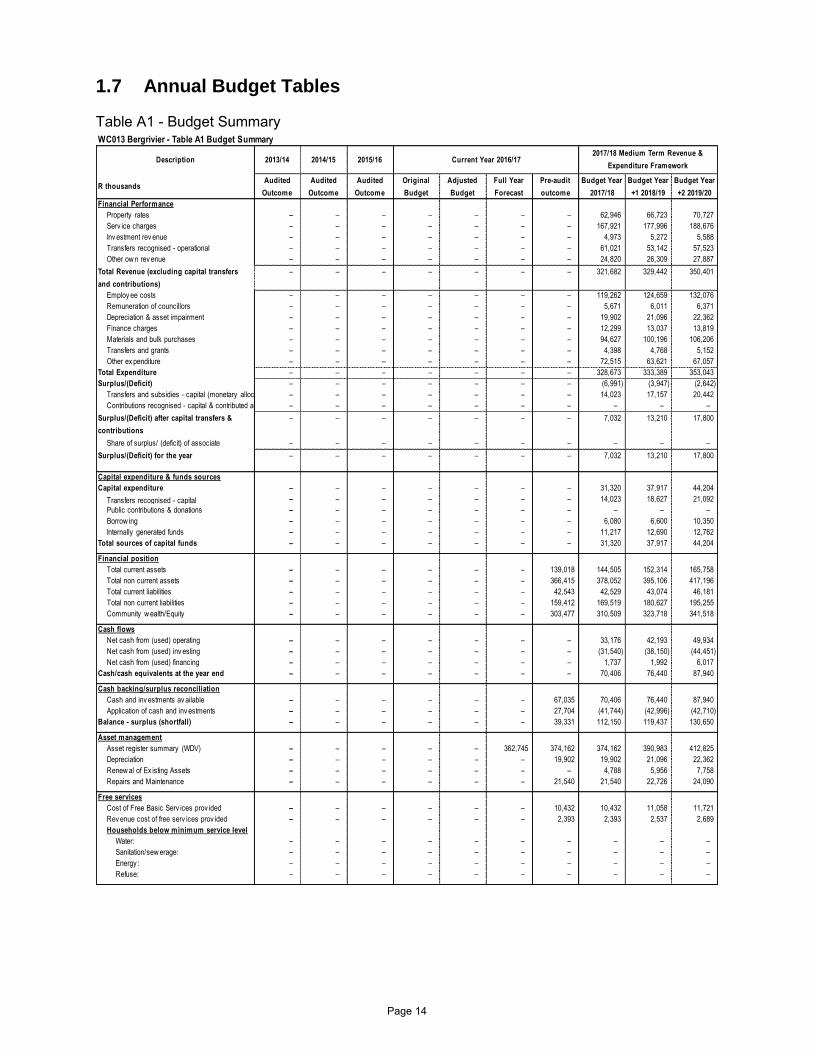

1.7 Annual Budget Tables

Table A1 - Budget Summary

Description 2013/14 2014/15 2015/16

R thousandsAudited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Pre-audit

outcome

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Financial Performance

Property rates – – – – – – – 62,946 66,723 70,727

Serv ice charges – – – – – – – 167,921 177,996 188,676

Inv estment rev enue – – – – – – – 4,973 5,272 5,588

Transfers recognised - operational – – – – – – – 61,021 53,142 57,523

Other ow n rev enue – – – – – – – 24,820 26,309 27,887

Total Revenue (excluding capital transfers

and contributions)

– – – – – – – 321,682 329,442 350,401

Employ ee costs – – – – – – – 119,262 124,659 132,076

Remuneration of councillors – – – – – – – 5,671 6,011 6,371

Depreciation & asset impairment – – – – – – – 19,902 21,096 22,362

Finance charges – – – – – – – 12,299 13,037 13,819

Materials and bulk purchases – – – – – – – 94,627 100,196 106,206

Transfers and grants – – – – – – – 4,398 4,768 5,152

Other ex penditure – – – – – – – 72,515 63,621 67,057

Total Expenditure – – – – – – – 328,673 333,389 353,043

Surplus/(Deficit) – – – – – – – (6,991) (3,947) (2,642)

Transfers and subsidies - capital (monetary allocations) (National / Prov incial and District)– – – – – – – 14,023 17,157 20,442

Contributions recognised - capital & contributed assets – – – – – – – – – –

Surplus/(Deficit) after capital transfers &

contributions

– – – – – – – 7,032 13,210 17,800

Share of surplus/ (deficit) of associate – – – – – – – – – –

Surplus/(Deficit) for the year – – – – – – – 7,032 13,210 17,800

Capital expenditure & funds sources

Capital expenditure – – – – – – – 31,320 37,917 44,204

Transfers recognised - capital – – – – – – – 14,023 18,627 21,092

Public contributions & donations – – – – – – – – – –

Borrow ing – – – – – – – 6,080 6,600 10,350

Internally generated funds – – – – – – – 11,217 12,690 12,762

Total sources of capital funds – – – – – – – 31,320 37,917 44,204

Financial position

Total current assets – – – – – – 139,018 144,505 152,314 165,758

Total non current assets – – – – – – 366,415 378,052 395,106 417,196

Total current liabilities – – – – – – 42,543 42,529 43,074 46,181

Total non current liabilities – – – – – – 159,412 169,519 180,627 195,255

Community w ealth/Equity – – – – – – 303,477 310,509 323,718 341,518

Cash flows

Net cash from (used) operating – – – – – – – 33,176 42,193 49,934

Net cash from (used) inv esting – – – – – – – (31,540) (38,150) (44,451)

Net cash from (used) financing – – – – – – – 1,737 1,992 6,017

Cash/cash equivalents at the year end – – – – – – – 70,406 76,440 87,940

Cash backing/surplus reconciliation

Cash and inv estments av ailable – – – – – – 67,035 70,406 76,440 87,940

Application of cash and inv estments – – – – – – 27,704 (41,744) (42,996) (42,710)

Balance - surplus (shortfall) – – – – – – 39,331 112,150 119,437 130,650

Asset management

Asset register summary (WDV) – – – – – 362,745 374,162 374,162 390,983 412,825

Depreciation – – – – – – 19,902 19,902 21,096 22,362

Renew al of Ex isting Assets – – – – – – – 4,788 5,956 7,758

Repairs and Maintenance – – – – – – 21,540 21,540 22,726 24,090

Free services

Cost of Free Basic Serv ices prov ided – – – – – – 10,432 10,432 11,058 11,721

Rev enue cost of free serv ices prov ided – – – – – – 2,393 2,393 2,537 2,689

Households below minimum service level

Water: – – – – – – – – – –

Sanitation/sew erage: – – – – – – – – – –

Energy : – – – – – – – – – –

Refuse: – – – – – – – – – –

2017/18 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2016/17

WC013 Bergrivier - Table A1 Budget Summary

Page 14

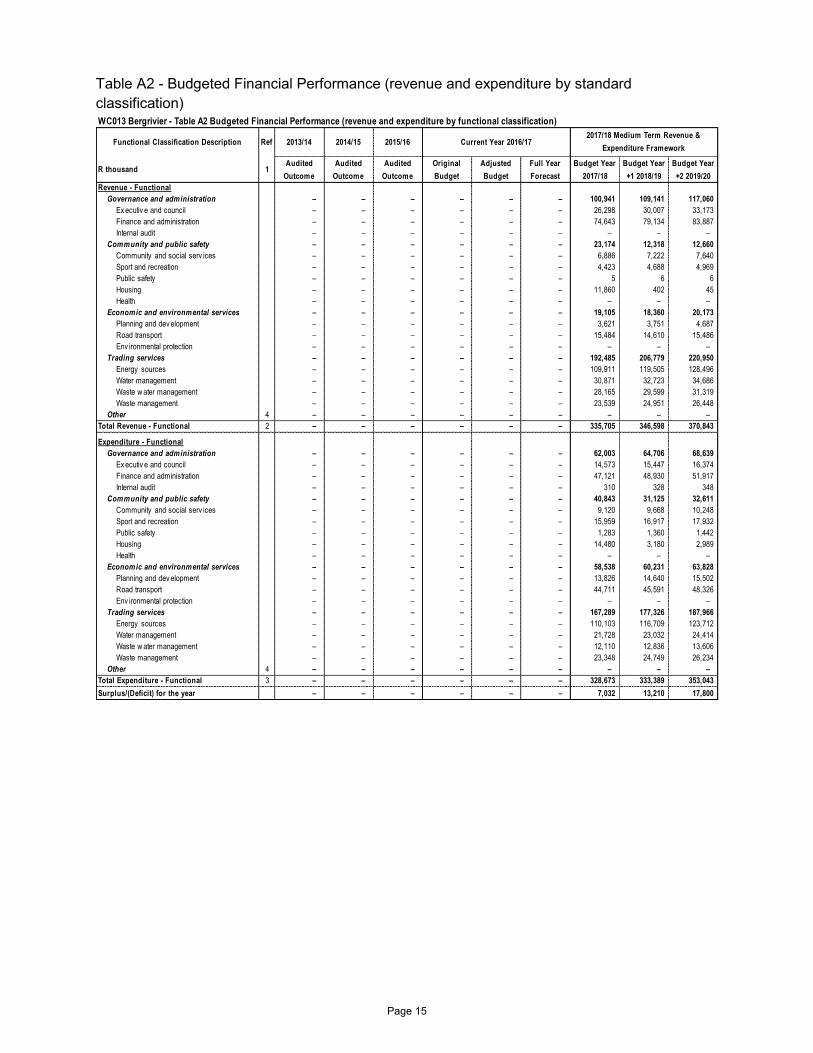

Table A2 - Budgeted Financial Performance (revenue and expenditure by standard

classification)

WC013 Bergrivier - Table A2 Budgeted Financial Performance (revenue and expenditure by functional classification)

Functional Classification Description Ref 2013/14 2014/15 2015/16

R thousand 1Audited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Revenue - Functional

Governance and administration – – – – – – 100,941 109,141 117,060

Ex ecutiv e and council – – – – – – 26,298 30,007 33,173

Finance and administration – – – – – – 74,643 79,134 83,887

Internal audit – – – – – – – – –

Community and public safety – – – – – – 23,174 12,318 12,660

Community and social serv ices – – – – – – 6,886 7,222 7,640

Sport and recreation – – – – – – 4,423 4,688 4,969

Public safety – – – – – – 5 6 6

Housing – – – – – – 11,860 402 45

Health – – – – – – – – –

Economic and environmental services – – – – – – 19,105 18,360 20,173

Planning and dev elopment – – – – – – 3,621 3,751 4,687

Road transport – – – – – – 15,484 14,610 15,486

Env ironmental protection – – – – – – – – –

Trading services – – – – – – 192,485 206,779 220,950

Energy sources – – – – – – 109,911 119,505 128,496

Water management – – – – – – 30,871 32,723 34,686

Waste w ater management – – – – – – 28,165 29,599 31,319

Waste management – – – – – – 23,539 24,951 26,448

Other 4 – – – – – – – – –

Total Revenue - Functional 2 – – – – – – 335,705 346,598 370,843

Expenditure - Functional

Governance and administration – – – – – – 62,003 64,706 68,639

Ex ecutiv e and council – – – – – – 14,573 15,447 16,374

Finance and administration – – – – – – 47,121 48,930 51,917

Internal audit – – – – – – 310 328 348

Community and public safety – – – – – – 40,843 31,125 32,611

Community and social serv ices – – – – – – 9,120 9,668 10,248

Sport and recreation – – – – – – 15,959 16,917 17,932

Public safety – – – – – – 1,283 1,360 1,442

Housing – – – – – – 14,480 3,180 2,989

Health – – – – – – – – –

Economic and environmental services – – – – – – 58,538 60,231 63,828

Planning and dev elopment – – – – – – 13,826 14,640 15,502

Road transport – – – – – – 44,711 45,591 48,326

Env ironmental protection – – – – – – – – –

Trading services – – – – – – 167,289 177,326 187,966

Energy sources – – – – – – 110,103 116,709 123,712

Water management – – – – – – 21,728 23,032 24,414

Waste w ater management – – – – – – 12,110 12,836 13,606

Waste management – – – – – – 23,348 24,749 26,234

Other 4 – – – – – – – – –

Total Expenditure - Functional 3 – – – – – – 328,673 333,389 353,043

Surplus/(Deficit) for the year – – – – – – 7,032 13,210 17,800

Current Year 2016/172017/18 Medium Term Revenue &

Expenditure Framework

Page 15

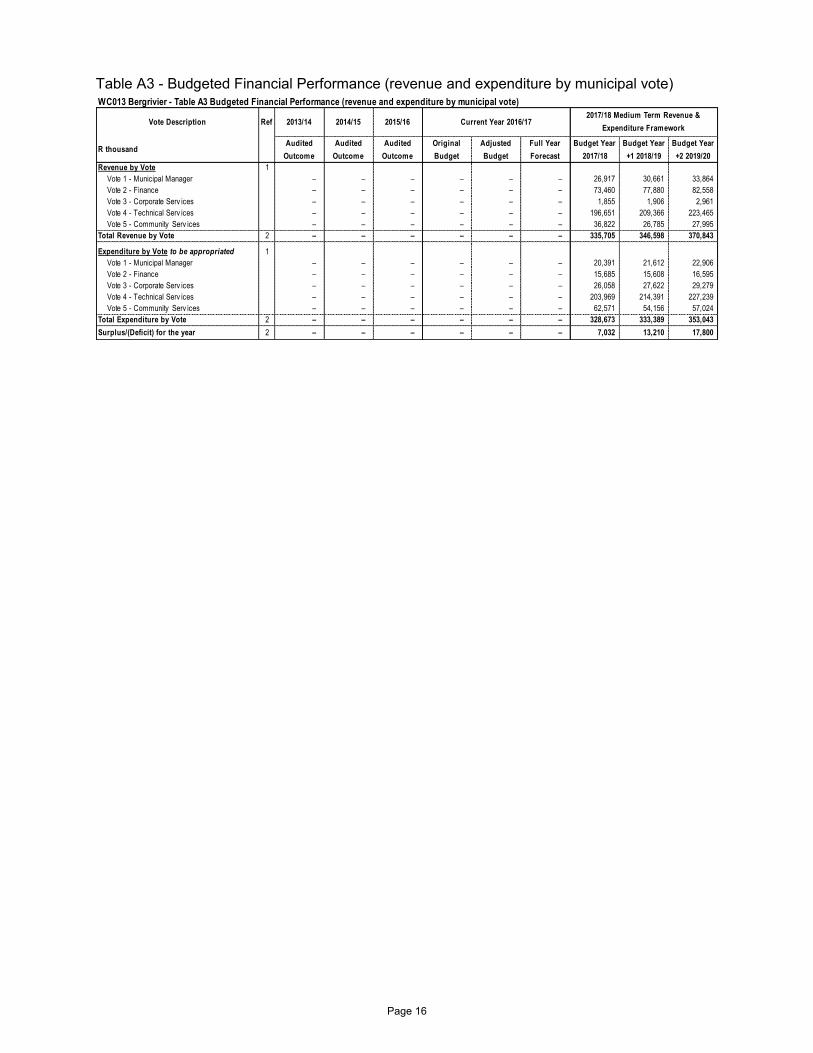

Table A3 - Budgeted Financial Performance (revenue and expenditure by municipal vote)

WC013 Bergrivier - Table A3 Budgeted Financial Performance (revenue and expenditure by municipal vote)

Vote Description Ref 2013/14 2014/15 2015/16

R thousandAudited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Revenue by Vote 1

Vote 1 - Municipal Manager – – – – – – 26,917 30,661 33,864

Vote 2 - Finance – – – – – – 73,460 77,880 82,558

Vote 3 - Corporate Serv ices – – – – – – 1,855 1,906 2,961

Vote 4 - Technical Serv ices – – – – – – 196,651 209,366 223,465

Vote 5 - Community Serv ices – – – – – – 36,822 26,785 27,995

Total Revenue by Vote 2 – – – – – – 335,705 346,598 370,843

Expenditure by Vote to be appropriated 1

Vote 1 - Municipal Manager – – – – – – 20,391 21,612 22,906

Vote 2 - Finance – – – – – – 15,685 15,608 16,595

Vote 3 - Corporate Serv ices – – – – – – 26,058 27,622 29,279

Vote 4 - Technical Serv ices – – – – – – 203,969 214,391 227,239

Vote 5 - Community Serv ices – – – – – – 62,571 54,156 57,024

Total Expenditure by Vote 2 – – – – – – 328,673 333,389 353,043

Surplus/(Deficit) for the year 2 – – – – – – 7,032 13,210 17,800

Current Year 2016/172017/18 Medium Term Revenue &

Expenditure Framework

Page 16

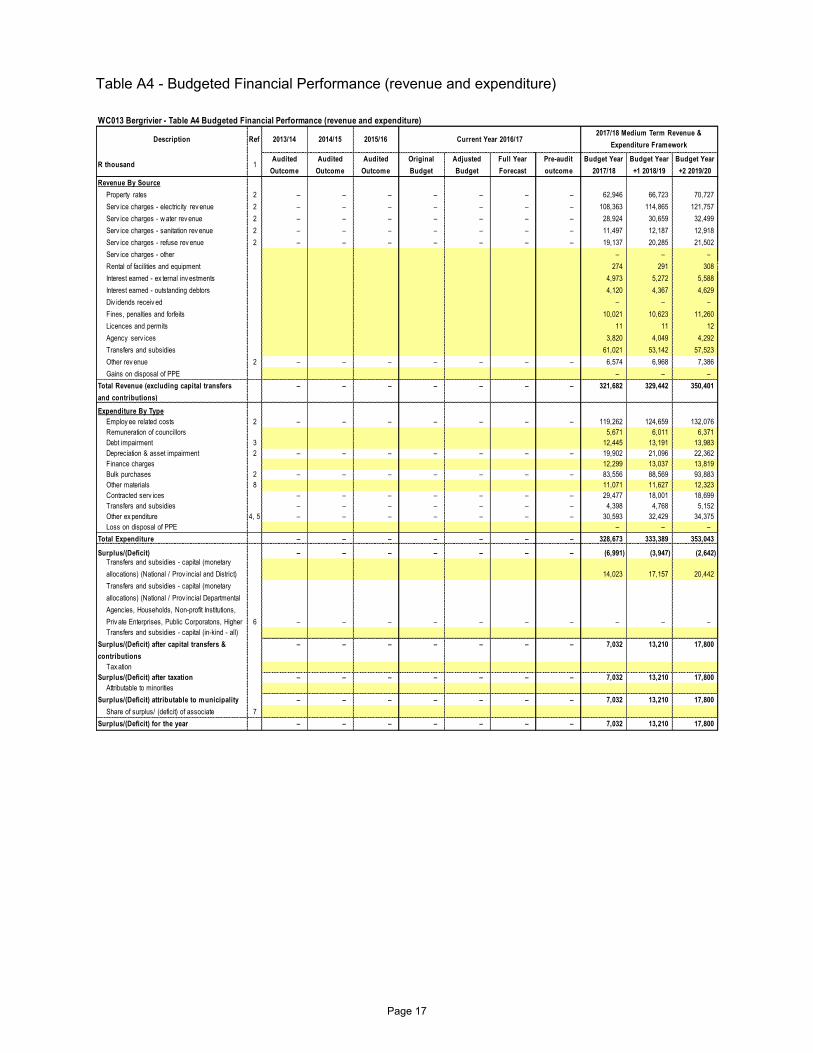

Table A4 - Budgeted Financial Performance (revenue and expenditure)

WC013 Bergrivier - Table A4 Budgeted Financial Performance (revenue and expenditure)

Description Ref 2013/14 2014/15 2015/16

R thousand 1Audited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Pre-audit

outcome

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Revenue By Source

Property rates 2 – – – – – – – 62,946 66,723 70,727

Serv ice charges - electricity rev enue 2 – – – – – – – 108,363 114,865 121,757

Serv ice charges - w ater rev enue 2 – – – – – – – 28,924 30,659 32,499

Serv ice charges - sanitation rev enue 2 – – – – – – – 11,497 12,187 12,918

Serv ice charges - refuse rev enue 2 – – – – – – – 19,137 20,285 21,502

Serv ice charges - other – – –

Rental of facilities and equipment 274 291 308

Interest earned - ex ternal inv estments 4,973 5,272 5,588

Interest earned - outstanding debtors 4,120 4,367 4,629

Div idends receiv ed – – –

Fines, penalties and forfeits 10,021 10,623 11,260

Licences and permits 11 11 12

Agency serv ices 3,820 4,049 4,292

Transfers and subsidies 61,021 53,142 57,523

Other rev enue 2 – – – – – – – 6,574 6,968 7,386

Gains on disposal of PPE – – –

Total Revenue (excluding capital transfers

and contributions)

– – – – – – – 321,682 329,442 350,401

Expenditure By Type

Employ ee related costs 2 – – – – – – – 119,262 124,659 132,076

Remuneration of councillors 5,671 6,011 6,371

Debt impairment 3 12,445 13,191 13,983

Depreciation & asset impairment 2 – – – – – – – 19,902 21,096 22,362

Finance charges 12,299 13,037 13,819

Bulk purchases 2 – – – – – – – 83,556 88,569 93,883

Other materials 8 11,071 11,627 12,323

Contracted serv ices – – – – – – – 29,477 18,001 18,699

Transfers and subsidies – – – – – – – 4,398 4,768 5,152

Other ex penditure 4, 5 – – – – – – – 30,593 32,429 34,375

Loss on disposal of PPE – – –

Total Expenditure – – – – – – – 328,673 333,389 353,043

Surplus/(Deficit) – – – – – – – (6,991) (3,947) (2,642)

Transfers and subsidies - capital (monetary

allocations) (National / Prov incial and District) 14,023 17,157 20,442

Transfers and subsidies - capital (monetary

allocations) (National / Prov incial Departmental

Agencies, Households, Non-profit Institutions,

Priv ate Enterprises, Public Corporatons, Higher 6 – – – – – – – – – –

Transfers and subsidies - capital (in-kind - all)

Surplus/(Deficit) after capital transfers &

contributions

– – – – – – – 7,032 13,210 17,800

Tax ation

Surplus/(Deficit) after taxation – – – – – – – 7,032 13,210 17,800

Attributable to minorities

Surplus/(Deficit) attributable to municipality – – – – – – – 7,032 13,210 17,800

Share of surplus/ (deficit) of associate 7

Surplus/(Deficit) for the year – – – – – – – 7,032 13,210 17,800

2017/18 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2016/17

Page 17

Table A5 - Budgeted Capital Expenditure by vote, standard classification and funding source

WC013 Bergrivier - Table A5 Budgeted Capital Expenditure by vote, functional classification and funding

Vote Description Ref 2013/14 2014/15 2015/16

R thousand 1Audited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Pre-audit

outcome

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Capital expenditure - Vote

Multi-year expenditure to be appropriated 2

Vote 1 - Municipal Manager – – – – – – – – – –

Vote 2 - Finance – – – – – – – – – –

Vote 3 - Corporate Serv ices – – – – – – – 1,000 1,000 2,000

Vote 4 - Technical Serv ices – – – – – – – 1,845 2,065 2,630

Vote 5 - Community Serv ices – – – – – – – 765 1,730 495

Capital multi-year expenditure sub-total 7 – – – – – – – 3,610 4,795 5,125

Single-year expenditure to be appropriated 2

Vote 1 - Municipal Manager – – – – – – – 102 – –

Vote 2 - Finance – – – – – – – 1,290 790 750

Vote 3 - Corporate Serv ices – – – – – – – 225 510 960

Vote 4 - Technical Serv ices – – – – – – – 22,632 28,346 33,530

Vote 5 - Community Serv ices – – – – – – – 3,461 3,476 3,839

Capital single-year expenditure sub-total – – – – – – – 27,710 33,122 39,079

Total Capital Expenditure - Vote – – – – – – – 31,320 37,917 44,204

Capital Expenditure - Functional

Governance and administration – – – – – – – 2,559 3,824 5,264

Ex ecutiv e and council 100 – –

Finance and administration 2,459 3,824 5,264

Internal audit – – –

Community and public safety – – – – – – – 2,261 4,126 3,154

Community and social serv ices 870 1,925 945

Sport and recreation 1,071 1,919 1,039

Public safety 320 282 1,170

Housing – – –

Health – – –

Economic and environmental services – – – – – – – 7,157 7,850 9,310

Planning and dev elopment 1,222 1,220 2,020

Road transport 5,935 6,630 7,290

Env ironmental protection – – –

Trading services – – – – – – – 19,343 22,117 26,476

Energy sources 1,325 4,552 6,091

Water management 1,370 1,240 1,475

Waste w ater management 13,211 13,768 14,649

Waste management 3,437 2,557 4,261

Other – – –

Total Capital Expenditure - Functional 3 – – – – – – – 31,320 37,917 44,204

Funded by:

National Gov ernment 13,023 16,157 18,442

Prov incial Gov ernment 1,000 2,470 2,650

District Municipality

Other transfers and grants

Transfers recognised - capital 4 – – – – – – – 14,023 18,627 21,092

Public contributions & donations 5

Borrowing 6 6,080 6,600 10,350

Internally generated funds 11,217 12,690 12,762

Total Capital Funding 7 – – – – – – – 31,320 37,917 44,204

2017/18 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2016/17

Page 18

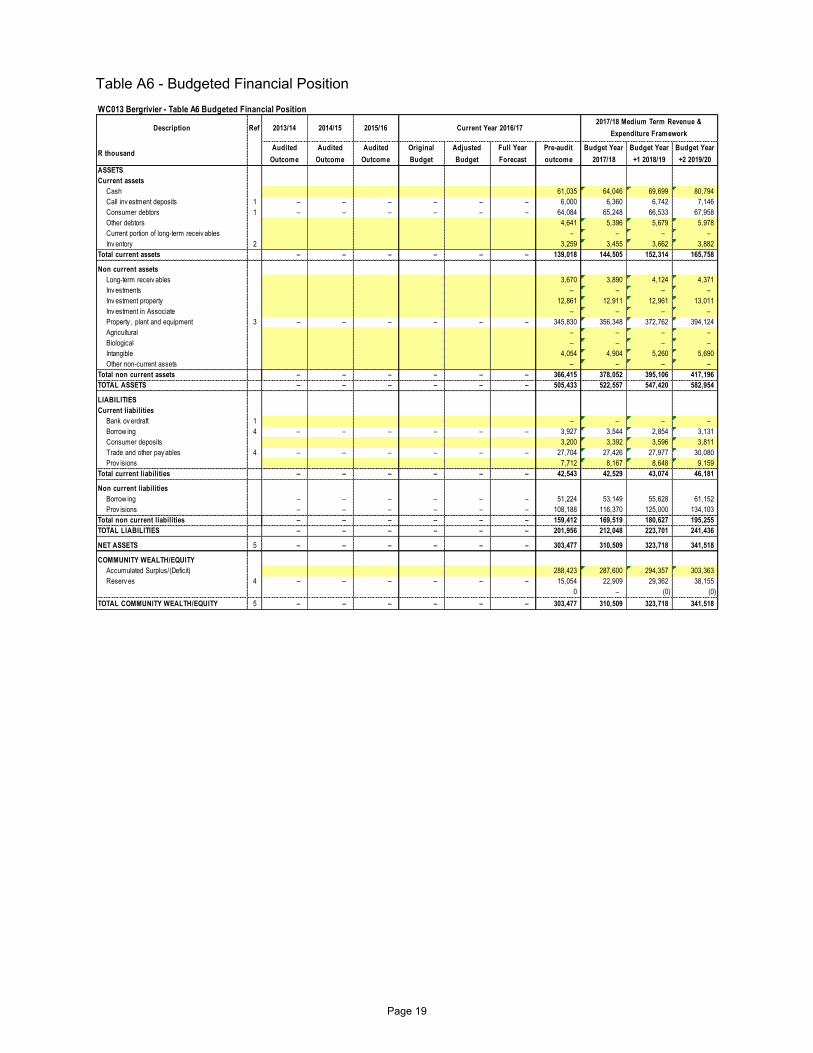

Table A6 - Budgeted Financial Position

WC013 Bergrivier - Table A6 Budgeted Financial Position

Description Ref 2013/14 2014/15 2015/16

R thousandAudited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Pre-audit

outcome

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

ASSETS

Current assets

Cash 61,035 64,046 69,699 80,794

Call inv estment deposits 1 – – – – – – 6,000 6,360 6,742 7,146

Consumer debtors 1 – – – – – – 64,084 65,248 66,533 67,958

Other debtors 4,641 5,396 5,679 5,978

Current portion of long-term receiv ables – – – –

Inv entory 2 3,259 3,455 3,662 3,882

Total current assets – – – – – – 139,018 144,505 152,314 165,758

Non current assets

Long-term receiv ables 3,670 3,890 4,124 4,371

Inv estments – – – –

Inv estment property 12,861 12,911 12,961 13,011

Inv estment in Associate – – – –

Property , plant and equipment 3 – – – – – – 345,830 356,348 372,762 394,124

Agricultural – – – –

Biological – – – –

Intangible 4,054 4,904 5,260 5,690

Other non-current assets – – – –

Total non current assets – – – – – – 366,415 378,052 395,106 417,196

TOTAL ASSETS – – – – – – 505,433 522,557 547,420 582,954

LIABILITIES

Current liabilities

Bank ov erdraft 1 – – – –

Borrow ing 4 – – – – – – 3,927 3,544 2,854 3,131

Consumer deposits 3,200 3,392 3,596 3,811

Trade and other pay ables 4 – – – – – – 27,704 27,426 27,977 30,080

Prov isions 7,712 8,167 8,648 9,159

Total current liabilities – – – – – – 42,543 42,529 43,074 46,181

Non current liabilities

Borrow ing – – – – – – 51,224 53,149 55,628 61,152

Prov isions – – – – – – 108,188 116,370 125,000 134,103

Total non current liabilities – – – – – – 159,412 169,519 180,627 195,255

TOTAL LIABILITIES – – – – – – 201,956 212,048 223,701 241,436

NET ASSETS 5 – – – – – – 303,477 310,509 323,718 341,518

COMMUNITY WEALTH/EQUITY

Accumulated Surplus/(Deficit) 288,423 287,600 294,357 303,363

Reserv es 4 – – – – – – 15,054 22,909 29,362 38,155

0 – (0) (0)

TOTAL COMMUNITY WEALTH/EQUITY 5 – – – – – – 303,477 310,509 323,718 341,518

2017/18 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2016/17

Page 19

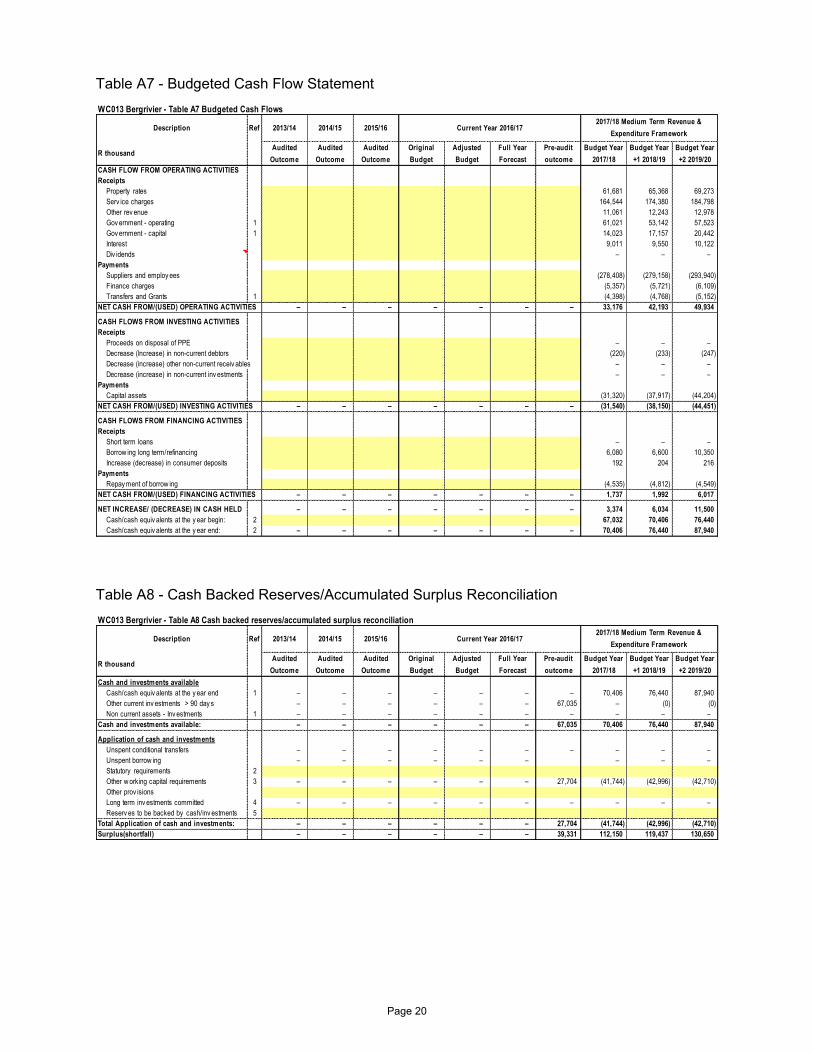

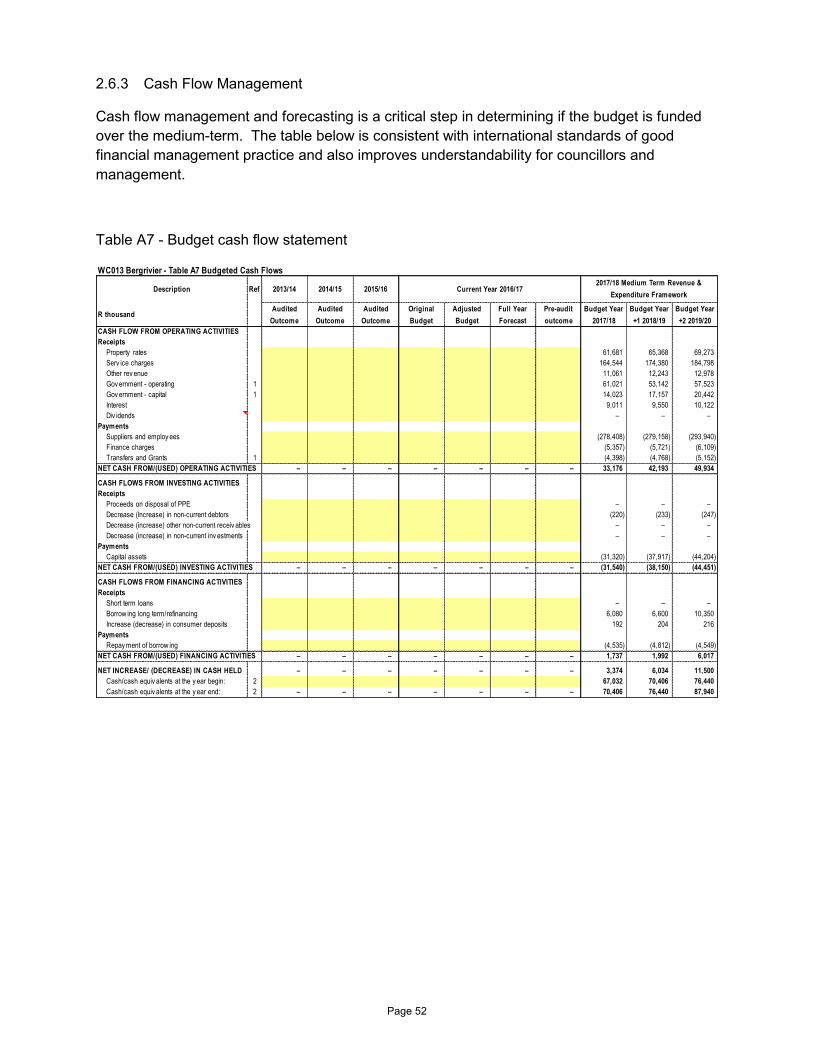

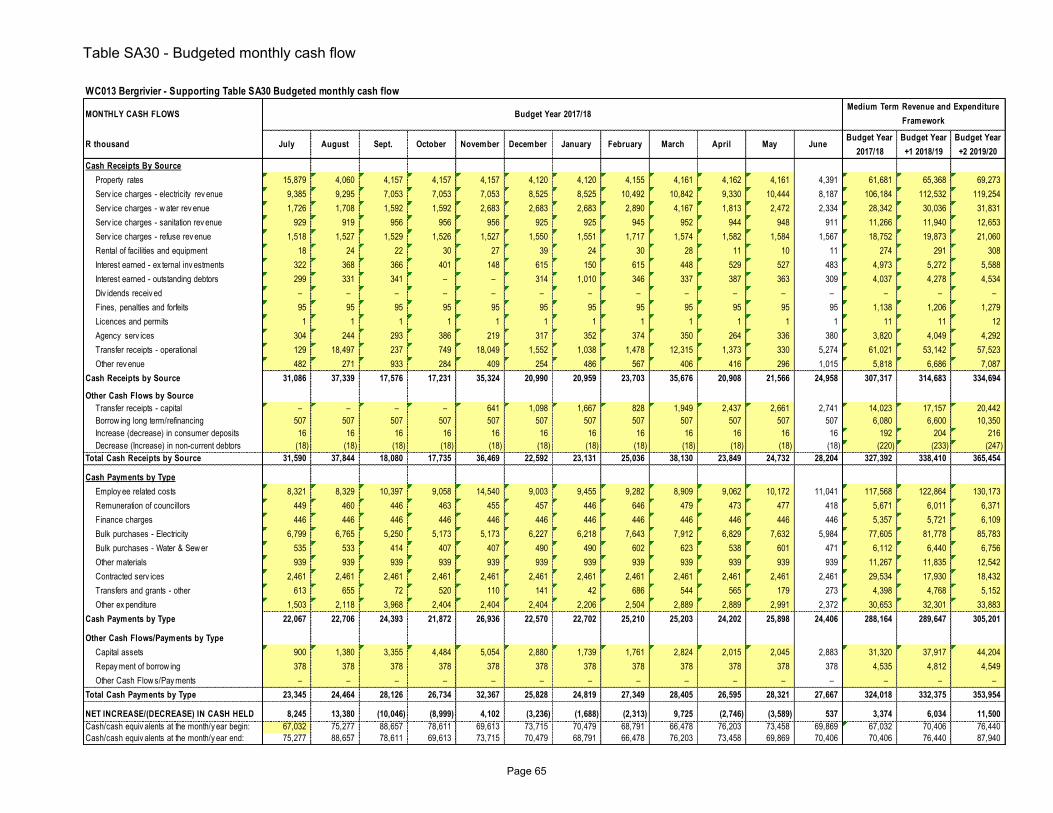

Table A7 - Budgeted Cash Flow Statement

Table A8 - Cash Backed Reserves/Accumulated Surplus Reconciliation

WC013 Bergrivier - Table A7 Budgeted Cash Flows

Description Ref 2013/14 2014/15 2015/16

R thousandAudited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Pre-audit

outcome

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

CASH FLOW FROM OPERATING ACTIVITIES

Receipts

Property rates 61,681 65,368 69,273

Serv ice charges 164,544 174,380 184,798

Other rev enue 11,061 12,243 12,978

Gov ernment - operating 1 61,021 53,142 57,523

Gov ernment - capital 1 14,023 17,157 20,442

Interest 9,011 9,550 10,122

Div idends – – –

Payments

Suppliers and employ ees (278,408) (279,158) (293,940)

Finance charges (5,357) (5,721) (6,109)

Transfers and Grants 1 (4,398) (4,768) (5,152)

NET CASH FROM/(USED) OPERATING ACTIVITIES – – – – – – – 33,176 42,193 49,934

CASH FLOWS FROM INVESTING ACTIVITIES

Receipts

Proceeds on disposal of PPE – – –

Decrease (Increase) in non-current debtors (220) (233) (247)

Decrease (increase) other non-current receiv ables – – –

Decrease (increase) in non-current inv estments – – –

Payments

Capital assets (31,320) (37,917) (44,204)

NET CASH FROM/(USED) INVESTING ACTIVITIES – – – – – – – (31,540) (38,150) (44,451)

CASH FLOWS FROM FINANCING ACTIVITIES

Receipts

Short term loans – – –

Borrow ing long term/refinancing 6,080 6,600 10,350

Increase (decrease) in consumer deposits 192 204 216

Payments

Repay ment of borrow ing (4,535) (4,812) (4,549)

NET CASH FROM/(USED) FINANCING ACTIVITIES – – – – – – – 1,737 1,992 6,017

NET INCREASE/ (DECREASE) IN CASH HELD – – – – – – – 3,374 6,034 11,500

Cash/cash equiv alents at the y ear begin: 2 67,032 70,406 76,440

Cash/cash equiv alents at the y ear end: 2 – – – – – – – 70,406 76,440 87,940

2017/18 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2016/17

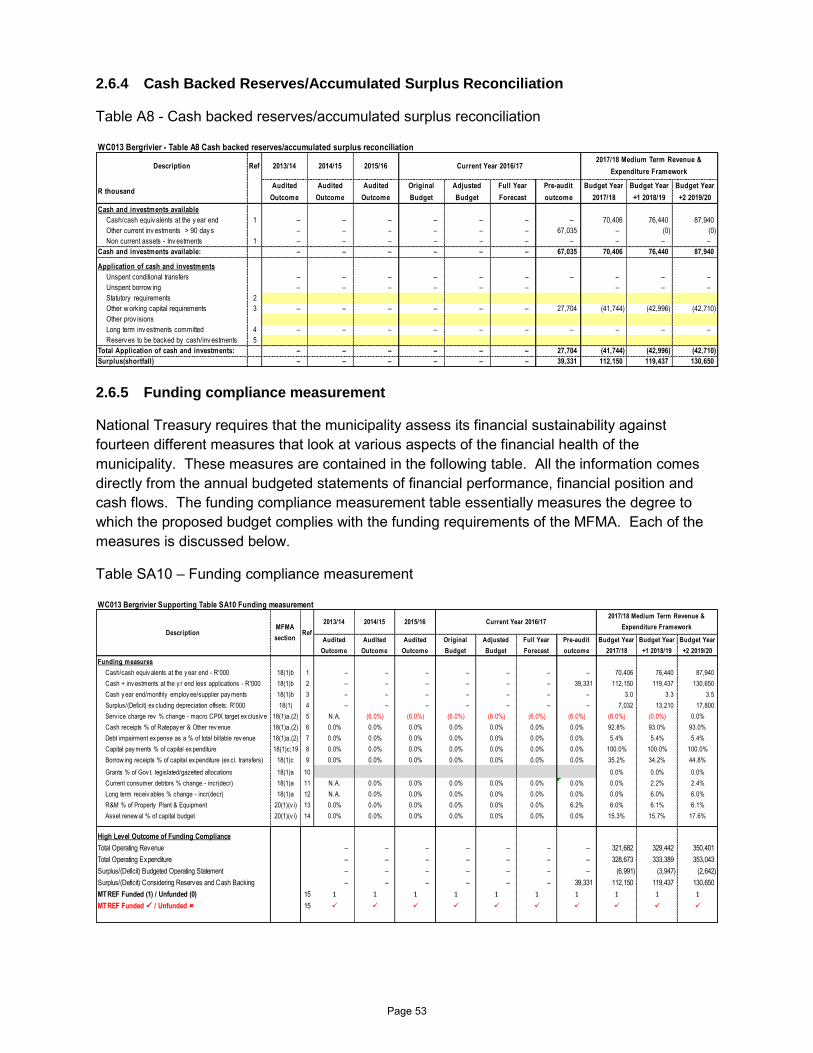

WC013 Bergrivier - Table A8 Cash backed reserves/accumulated surplus reconciliation

Description Ref 2013/14 2014/15 2015/16

R thousandAudited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Pre-audit

outcome

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Cash and investments available

Cash/cash equiv alents at the y ear end 1 – – – – – – – 70,406 76,440 87,940

Other current inv estments > 90 day s – – – – – – 67,035 – (0) (0)

Non current assets - Inv estments 1 – – – – – – – – – –

Cash and investments available: – – – – – – 67,035 70,406 76,440 87,940

Application of cash and investments

Unspent conditional transfers – – – – – – – – – –

Unspent borrow ing – – – – – – – – –

Statutory requirements 2

Other w orking capital requirements 3 – – – – – – 27,704 (41,744) (42,996) (42,710)

Other prov isions

Long term inv estments committed 4 – – – – – – – – – –

Reserv es to be backed by cash/inv estments 5

Total Application of cash and investments: – – – – – – 27,704 (41,744) (42,996) (42,710)

Surplus(shortfall) – – – – – – 39,331 112,150 119,437 130,650

2017/18 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2016/17

Page 20

Table A9 - Asset Management

WC013 Bergrivier - Table A9 Asset Management

Description Ref 2013/14 2014/15 2015/16

R thousandAudited

Outcome

Audited

Outcome

Audited

Outcome

Original

Budget

Adjusted

Budget

Full Year

Forecast

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year +2

2019/20

CAPITAL EXPENDITURE

Total New Assets 1 – – – – – – 7,984 13,031 17,570

Roads Infrastructure – – – – – – 100 500 400

Storm water Infrastructure – – – – – – 315 325 330

Electrical Infrastructure – – – – – – – 3,042 4,386

Water Supply Infrastructure – – – – – – 120 – 150

Sanitation Infrastructure – – – – – – 50 50 50

Solid Waste Infrastructure – – – – – – 1,700 2,100 2,000

Infrastructure – – – – – – 2,285 6,017 7,316

Community Facilities – – – – – – 1,870 2,620 2,555

Sport and Recreation Facilities – – – – – – 110 575 250

Community Assets – – – – – – 1,980 3,195 2,805

Operational Buildings – – – – – – 850 2,155 3,150

Other Assets – – – – – – 850 2,155 3,150

Licences and Rights – – – – – – 1,250 780 780

Intangible Assets – – – – – – 1,250 780 780

Computer Equipment – – – – – – 25 120 20

Furniture and Office Equipment – – – – – – 869 379 739

Machinery and Equipment – – – – – – 220 165 500

Transport Assets – – – – – – 505 220 2,260

Total Renewal of Existing Assets 2 – – – – – – 4,788 5,956 7,758

Roads Infrastructure – – – – – – 50 50 50

Electrical Infrastructure – – – – – – 60 60 510

Water Supply Infrastructure – – – – – – 865 825 870

Sanitation Infrastructure – – – – – – 635 630 720

Infrastructure – – – – – – 1,610 1,565 2,150

Community Facilities – – – – – – 285 443 503

Sport and Recreation Facilities – – – – – – 212 295 190

Community Assets – – – – – – 497 738 693

Non-rev enue Generating – – – – – – 50 50 50

Investment properties – – – – – – 50 50 50

Operational Buildings – – – – – – 30 35 40

Other Assets – – – – – – 30 35 40

Computer Equipment – – – – – – 200 250 250

Furniture and Office Equipment – – – – – – 434 476 574

Machinery and Equipment – – – – – – 307 312 481

Transport Assets – – – – – – 1,660 2,530 3,520

Total Upgrading of Existing Assets 6 – – – – – – 18,548 18,930 18,876

Roads Infrastructure – – – – – – 850 1,250 1,300

Storm water Infrastructure – – – – – – 35 35 35

Electrical Infrastructure – – – – – – 1,220 1,320 1,050

Water Supply Infrastructure – – – – – – 300 320 350

Solid Waste Infrastructure – – – – – – 400 400 400

Infrastructure – – – – – – 2,805 3,325 3,135

Community Facilities – – – – – – 13,583 13,285 13,321

Sport and Recreation Facilities – – – – – – 410 420 120

Community Assets – – – – – – 13,993 13,705 13,441

Licences and Rights – – – – – – – – 100

Intangible Assets – – – – – – – – 100

Computer Equipment – – – – – – – – 200

Furniture and Office Equipment – – – – – – 1,650 1,800 2,000

Transport Assets – – – – – – 100 100 –

Total Capital Expenditure 4

Roads Infrastructure – – – – – – 1,000 1,800 1,750

Storm water Infrastructure – – – – – – 350 360 365

Electrical Infrastructure – – – – – – 1,280 4,422 5,946

Water Supply Infrastructure – – – – – – 1,285 1,145 1,370

Sanitation Infrastructure – – – – – – 685 680 770

Solid Waste Infrastructure – – – – – – 2,100 2,500 2,400

Infrastructure – – – – – – 6,700 10,907 12,601

Community Facilities – – – – – – 15,738 16,348 16,379

Sport and Recreation Facilities – – – – – – 732 1,290 560

Community Assets – – – – – – 16,470 17,638 16,939

Non-rev enue Generating – – – – – – 50 50 50

Investment properties – – – – – – 50 50 50

Operational Buildings – – – – – – 880 2,190 3,190

Other Assets – – – – – – 880 2,190 3,190

Licences and Rights – – – – – – 1,250 780 880

Intangible Assets – – – – – – 1,250 780 880

Computer Equipment – – – – – – 225 370 470

Furniture and Office Equipment – – – – – – 2,953 2,655 3,313

Machinery and Equipment – – – – – – 527 477 981

Transport Assets – – – – – – 2,265 2,850 5,780

TOTAL CAPITAL EXPENDITURE - Asset class – – – – – – 31,320 37,917 44,204

Current Year 2016/172017/18 Medium Term Revenue & Expenditure

Framework

Page 21

ASSET REGISTER SUMMARY - PPE (WDV) 5

Roads Infrastructure 47,082 45,421 44,399 43,158

Storm water Infrastructure – 283 571 861

Electrical Infrastructure 35,824 35,883 39,010 43,585

Water Supply Infrastructure 47,404 46,938 46,227 45,629

Sanitation Infrastructure 72,692 70,388 67,900 65,311

Solid Waste Infrastructure 27,250 25,730 24,394 22,727

Rail Infrastructure – – – –

Coastal Infrastructure – – – –

Information and Communication Infrastructure – – – –

Infrastructure – – – – – 230,252 224,643 222,501 221,271

Community Facilities 7,496 22,966 39,030 55,109

Sport and Recreation Facilities 19,954 19,771 20,091 19,623

Community Assets – – – – – 27,450 42,737 59,121 74,731

Heritage Assets 454 454 454 454

Rev enue Generating – – – –

Non-rev enue Generating 12,861 12,911 12,961 13,011

Investment properties – – – – – 12,861 12,911 12,961 13,011

Operational Buildings 65,631 64,856 65,292 66,622

Housing – – – –

Other Assets – – – – – 65,631 64,856 65,292 66,622

Biological or Cultivated Assets – – – –

Serv itudes – – – –

Licences and Rights 4,054 4,904 5,260 5,690

Intangible Assets – – – – – 4,054 4,904 5,260 5,690

Computer Equipment – 225 595 1,065

Furniture and Office Equipment 6,893 8,330 9,378 10,988

Machinery and Equipment 7,514 6,672 5,697 5,140

Transport Assets 7,636 8,432 9,724 13,852

Libraries – – – –

Zoo's, Marine and Non-biological Animals – – – –

TOTAL ASSET REGISTER SUMMARY - PPE (WDV) 5 – – – – – 362,745 374,162 390,983 412,825

EXPENDITURE OTHER ITEMS

Depreciation 7 – – – – – – 19,902 21,096 22,362

Repairs and Maintenance by Asset Class 3 – – – – – – 21,540 22,726 24,090

Roads Infrastructure – – – – – – 100 – –

Storm water Infrastructure – – – – – – 657 696 738

Electrical Infrastructure – – – – – – 2,068 2,192 2,324

Water Supply Infrastructure – – – – – – 490 519 551

Sanitation Infrastructure – – – – – – 300 318 337

Infrastructure – – – – – – 3,615 3,726 3,949

Community Facilities – – – – – – 6,234 6,608 7,004

Sport and Recreation Facilities – – – – – – 2,818 2,987 3,166

Community Assets – – – – – – 9,051 9,594 10,170

Operational Buildings – – – – – – 4,802 5,091 5,396

Housing – – – – – – 16 16 17

Other Assets – – – – – – 4,818 5,107 5,413

Computer Equipment – – – – – – 645 683 724

Furniture and Office Equipment – – – – – – 87 93 98

Machinery and Equipment – – – – – – 899 953 1,010

Transport Assets – – – – – – 2,425 2,570 2,724

TOTAL EXPENDITURE OTHER ITEMS – – – – – – 41,442 43,822 46,451

Renewal and upgrading of Existing Assets as % of total capex 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 74.5% 65.6% 60.3%

Renewal and upgrading of Existing Assets as % of deprecn 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 117.3% 118.0% 119.1%

R&M as a % of PPE 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 6.0% 6.1% 6.1%

Renewal and upgrading and R&M as a % of PPE 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 12.0% 12.0% 12.0%

Page 22

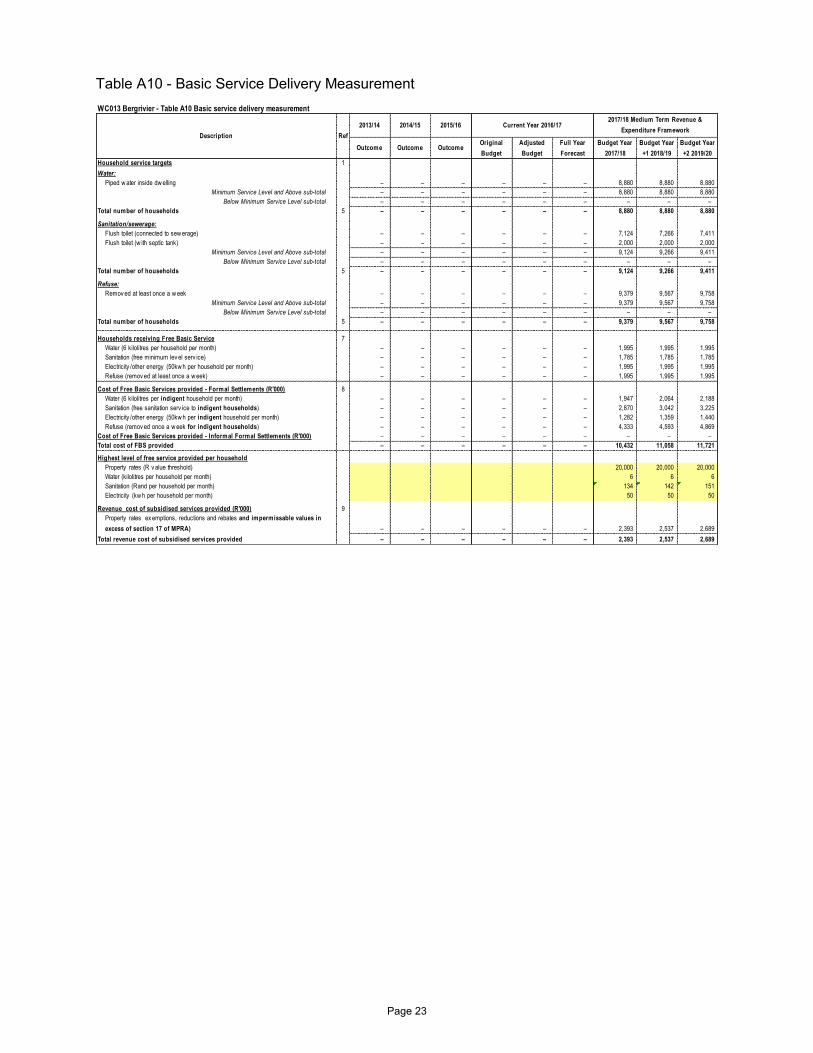

Table A10 - Basic Service Delivery Measurement

3

WC013 Bergrivier - Table A10 Basic service delivery measurement

2013/14 2014/15 2015/16

Outcome Outcome OutcomeOriginal

Budget

Adjusted

Budget

Full Year

Forecast

Budget Year

2017/18

Budget Year

+1 2018/19

Budget Year

+2 2019/20

Household service targets 1

Water:

Piped w ater inside dw elling – – – – – – 8,880 8,880 8,880

Minimum Service Level and Above sub-total – – – – – – 8,880 8,880 8,880

Below Minimum Service Level sub-total – – – – – – – – –

Total number of households 5 – – – – – – 8,880 8,880 8,880

Sanitation/sewerage:

Flush toilet (connected to sew erage) – – – – – – 7,124 7,266 7,411

Flush toilet (w ith septic tank) – – – – – – 2,000 2,000 2,000

Minimum Service Level and Above sub-total – – – – – – 9,124 9,266 9,411

Below Minimum Service Level sub-total – – – – – – – – –

Total number of households 5 – – – – – – 9,124 9,266 9,411

Refuse:

Remov ed at least once a w eek – – – – – – 9,379 9,567 9,758

Minimum Service Level and Above sub-total – – – – – – 9,379 9,567 9,758

Below Minimum Service Level sub-total – – – – – – – – –

Total number of households 5 – – – – – – 9,379 9,567 9,758

Households receiving Free Basic Service 7

Water (6 kilolitres per household per month) – – – – – – 1,995 1,995 1,995

Sanitation (free minimum lev el serv ice) – – – – – – 1,785 1,785 1,785

Electricity /other energy (50kw h per household per month) – – – – – – 1,995 1,995 1,995

Refuse (remov ed at least once a w eek) – – – – – – 1,995 1,995 1,995

Cost of Free Basic Services provided - Formal Settlements (R'000) 8

Water (6 kilolitres per indigent household per month) – – – – – – 1,947 2,064 2,188

Sanitation (free sanitation serv ice to indigent households) – – – – – – 2,870 3,042 3,225

Electricity /other energy (50kw h per indigent household per month) – – – – – – 1,282 1,359 1,440

Refuse (remov ed once a w eek for indigent households) – – – – – – 4,333 4,593 4,869

Cost of Free Basic Services provided - Informal Formal Settlements (R'000) – – – – – – – – –

Total cost of FBS provided – – – – – – 10,432 11,058 11,721

Highest level of free service provided per household

Property rates (R v alue threshold) 20,000 20,000 20,000

Water (kilolitres per household per month) 6 6 6

Sanitation (Rand per household per month) 134 142 151

Electricity (kw h per household per month) 50 50 50

Revenue cost of subsidised services provided (R'000) 9

Property rates ex emptions, reductions and rebates and impermissable values in

excess of section 17 of MPRA) – – – – – – 2,393 2,537 2,689

Total revenue cost of subsidised services provided – – – – – – 2,393 2,537 2,689

Current Year 2016/172017/18 Medium Term Revenue &

Expenditure FrameworkDescription Ref

Page 23

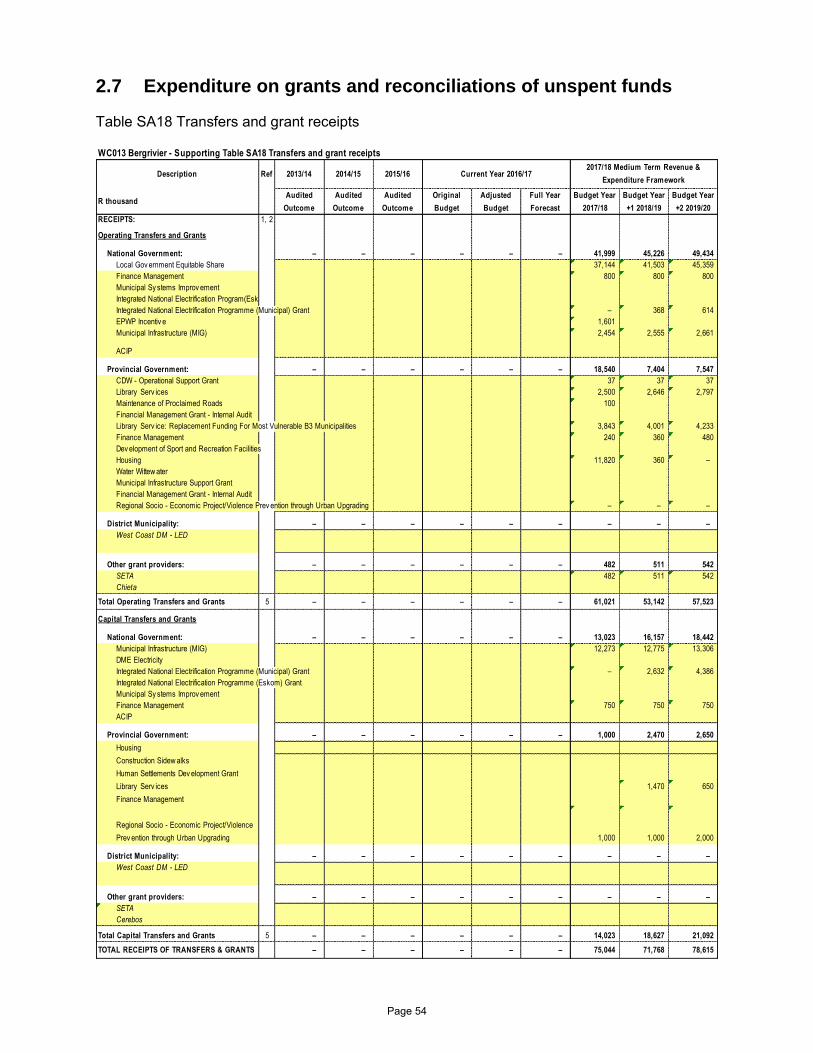

4 Part 2 – Supporting Documentation

2.1 Overview of the annual budget process Section 53 of the MFMA requires the Mayor of the municipality to provide general political guidance in the budget process and the setting of priorities that must guide the preparation of the budget. In addition Chapter 2 of the Municipal Budget and Reporting Regulations states that the Mayor of the municipality must establish a Budget Steering Committee to provide technical assistance to the Mayor in discharging the responsibilities set out in section 53 of the Act. The Budget Steering Committee consists of the Municipal Manager and senior officials of the municipality meeting under the chairpersonship of the Deputy Mayor. The primary aims of the Budget Steering Committee are to ensure:

that the process followed to compile the budget complies with legislation and good budget practices;

that there is proper alignment between the policy and service delivery priorities set out in the Councils IDP and the budget, taking into account the need to protect the financial sustainability of municipality;

that the municipality’s revenue and tariff setting strategies ensure that the cash resources needed to deliver services are available; and

that the various spending priorities of the different municipal departments are properly evaluated and prioritised in the allocation of resources.

2.1.1 Budget Process Overview In terms of section 21 of the MFMA the Mayor is required to table in Council ten months before the start of the new financial year (i.e. in August 2016) a time schedule that sets out the process to revise the IDP and prepare the budget. The Mayor tabled in Council the required the IDP and budget time schedule on 23 August 2016.

Page 24

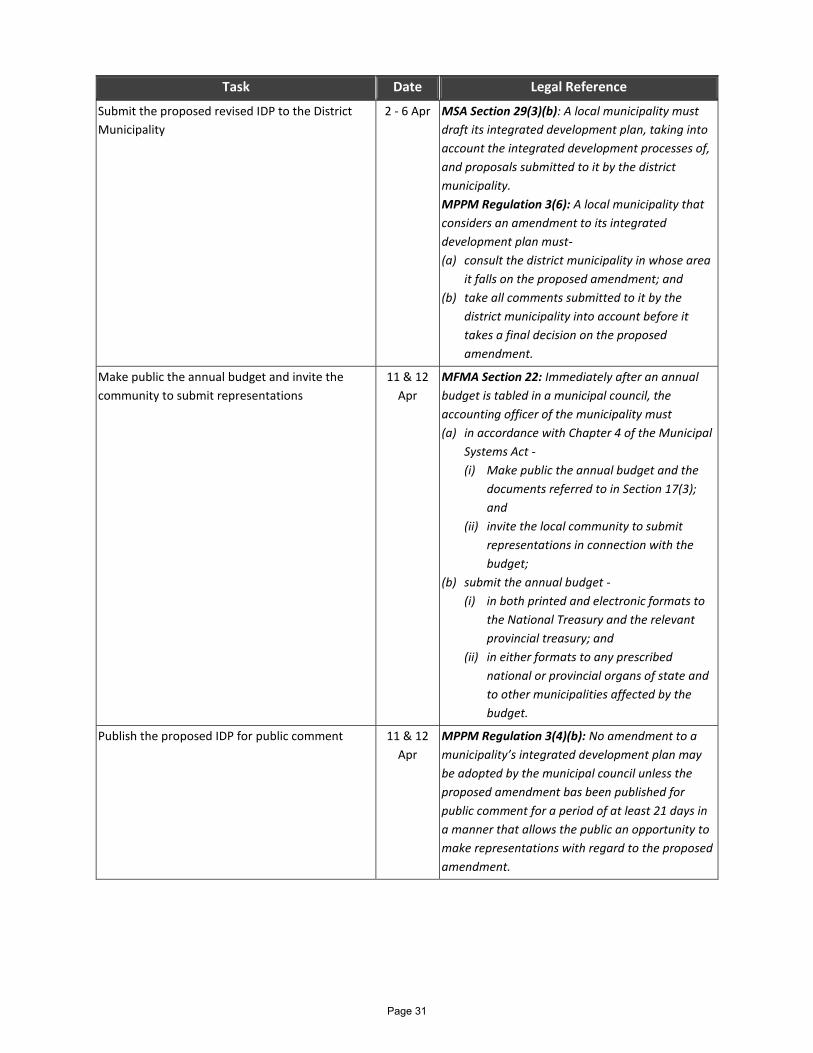

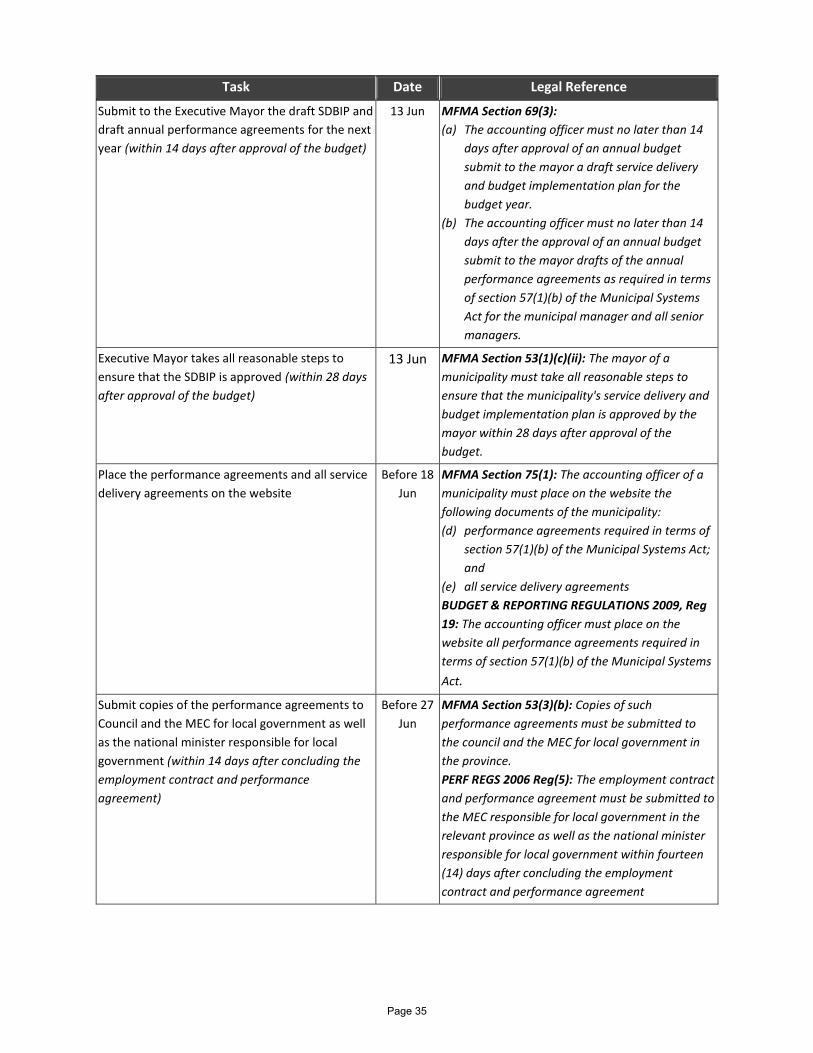

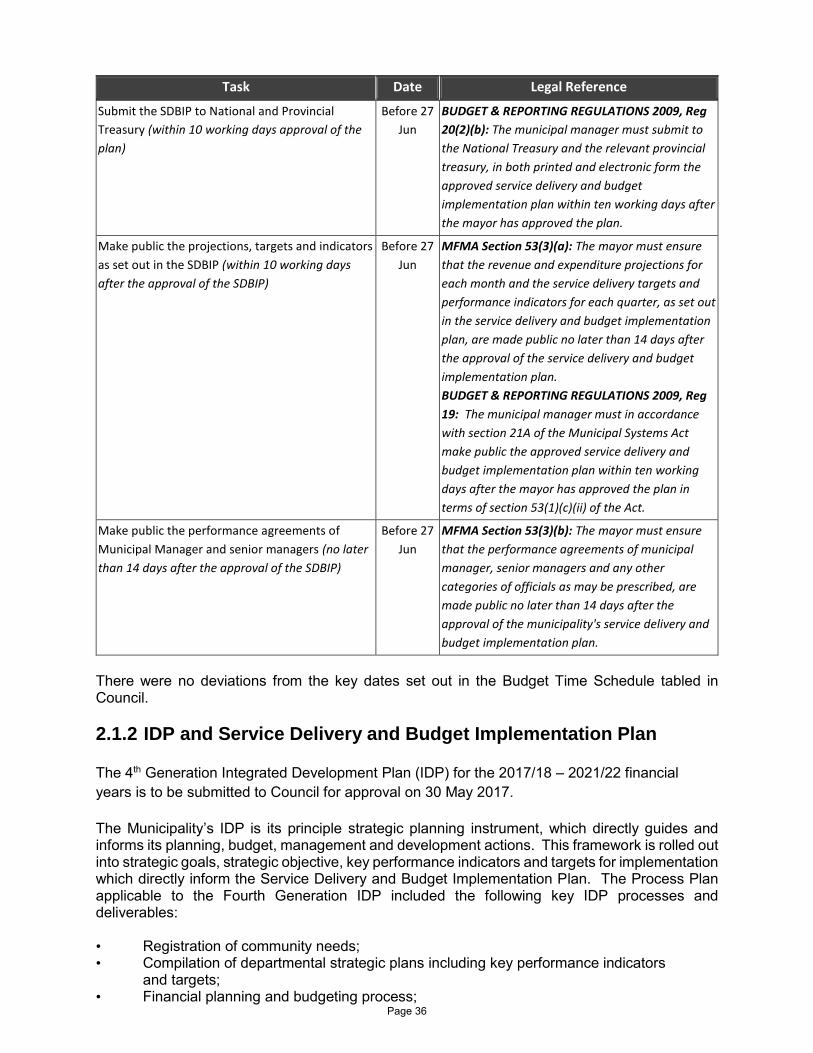

SCHEDULE OF KEY DEADLINES SUMMARY

SUMMARY OF KEY ACTIVITIES OF THE TIME SCHEDULE OF KEY DEADLINES (PROCESS PLAN) FOR THE 2017/18 BUDGET AND IDP REVIEW

Task Date Legal Reference

Jul - August 2016

Women’s Day 9 Aug

Table in Council the IDP Process Plan (Happens

once every 5 years. The time schedule in terms of

Section 21(1)(b) of the Municipal Finance

Management Act (MFMA) is replaced annually).

18 Jul MSA Section 28:

(1) Each municipal council, within a prescribed

period after the start of its elected term, must

adopt a process set out in writing to guide the

planning, drafting, adoption and review of its

integrated development plan.

(2) The municipality must through appropriate

mechanisms, processes and procedures

established in terms of Chapter 4, consult the

local community before adopting the process.

(3) A municipality must give notice to the local

community of particulars of the process it

intends to follow.

August 2016 Planning

September 2016 Public Participation (Inputs)

October 2016 Management Planning

November 2016 Mayoral Committee / Council Planning

December 2016- March

2017

Budget Process / IDP Development

Draft IDP Review and Budget Approvals

April 2017 Public participation (Report back)

May 2017 Final approval Of IDP Review and Budget

June 2017 Performance System Development (SDBIP)

Page 25

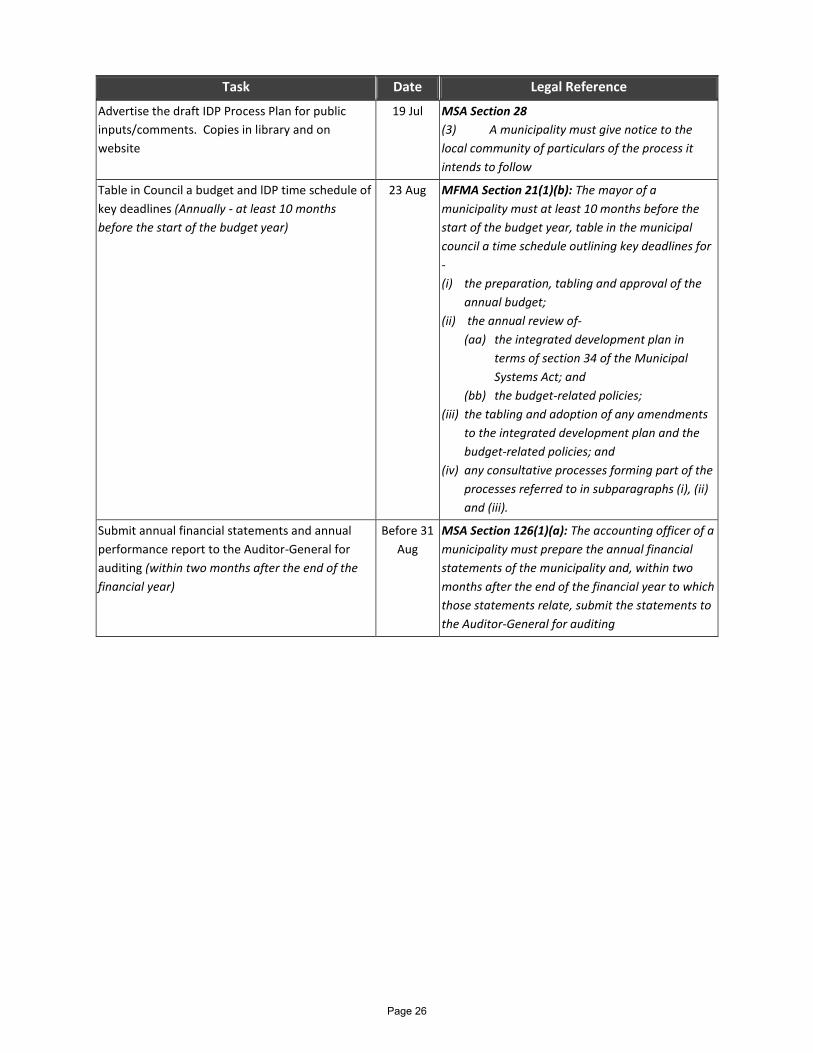

Task Date Legal Reference

Advertise the draft IDP Process Plan for public

inputs/comments. Copies in library and on

website

19 Jul MSA Section 28

(3) A municipality must give notice to the

local community of particulars of the process it

intends to follow

Table in Council a budget and lDP time schedule of

key deadlines (Annually - at least 10 months

before the start of the budget year)

23 Aug MFMA Section 21(1)(b): The mayor of a

municipality must at least 10 months before the

start of the budget year, table in the municipal

council a time schedule outlining key deadlines for

-

(i) the preparation, tabling and approval of the

annual budget;

(ii) the annual review of-

(aa) the integrated development plan in

terms of section 34 of the Municipal

Systems Act; and

(bb) the budget-related policies;

(iii) the tabling and adoption of any amendments

to the integrated development plan and the

budget-related policies; and

(iv) any consultative processes forming part of the

processes referred to in subparagraphs (i), (ii)

and (iii).

Submit annual financial statements and annual

performance report to the Auditor-General for

auditing (within two months after the end of the

financial year)

Before 31

Aug

MSA Section 126(1)(a): The accounting officer of a

municipality must prepare the annual financial

statements of the municipality and, within two

months after the end of the financial year to which

those statements relate, submit the statements to

the Auditor-General for auditing

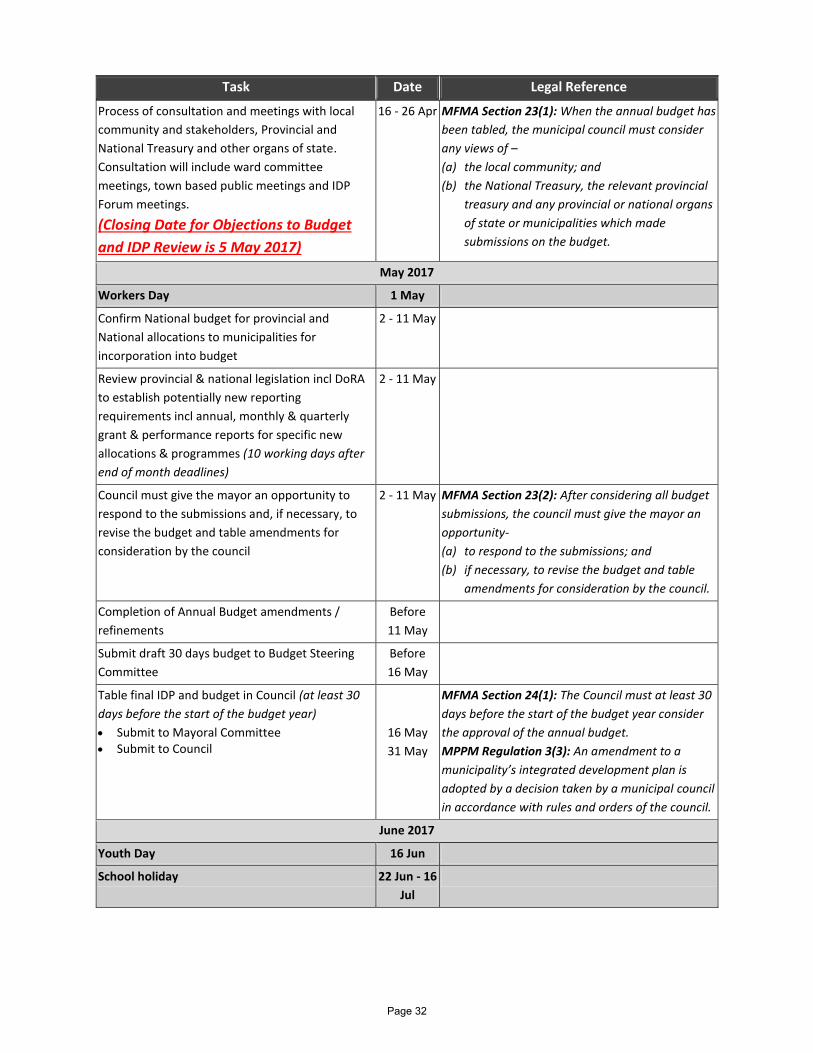

Page 26

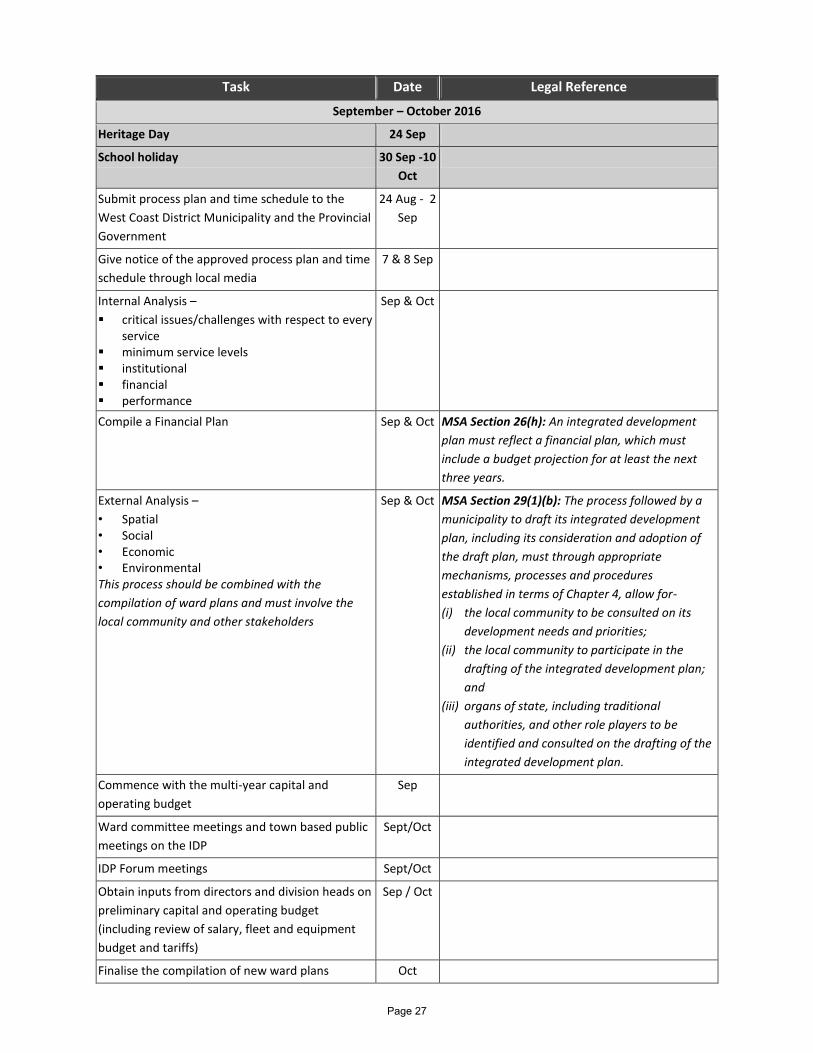

Task Date Legal Reference

September – October 2016

Heritage Day 24 Sep

School holiday 30 Sep -10

Oct

Submit process plan and time schedule to the

West Coast District Municipality and the Provincial

Government

24 Aug - 2

Sep

Give notice of the approved process plan and time

schedule through local media

7 & 8 Sep

Internal Analysis –

critical issues/challenges with respect to every service

minimum service levels institutional financial performance

Sep & Oct

Compile a Financial Plan Sep & Oct MSA Section 26(h): An integrated development

plan must reflect a financial plan, which must

include a budget projection for at least the next

three years.

External Analysis –

• Spatial • Social • Economic • Environmental This process should be combined with the

compilation of ward plans and must involve the

local community and other stakeholders

Sep & Oct MSA Section 29(1)(b): The process followed by a

municipality to draft its integrated development

plan, including its consideration and adoption of

the draft plan, must through appropriate

mechanisms, processes and procedures

established in terms of Chapter 4, allow for-

(i) the local community to be consulted on its

development needs and priorities;

(ii) the local community to participate in the

drafting of the integrated development plan;

and

(iii) organs of state, including traditional

authorities, and other role players to be

identified and consulted on the drafting of the

integrated development plan.

Commence with the multi-year capital and

operating budget

Sep

Ward committee meetings and town based public

meetings on the IDP

Sept/Oct

IDP Forum meetings Sept/Oct

Obtain inputs from directors and division heads on

preliminary capital and operating budget

(including review of salary, fleet and equipment

budget and tariffs)

Sep / Oct

Finalise the compilation of new ward plans Oct

Page 27

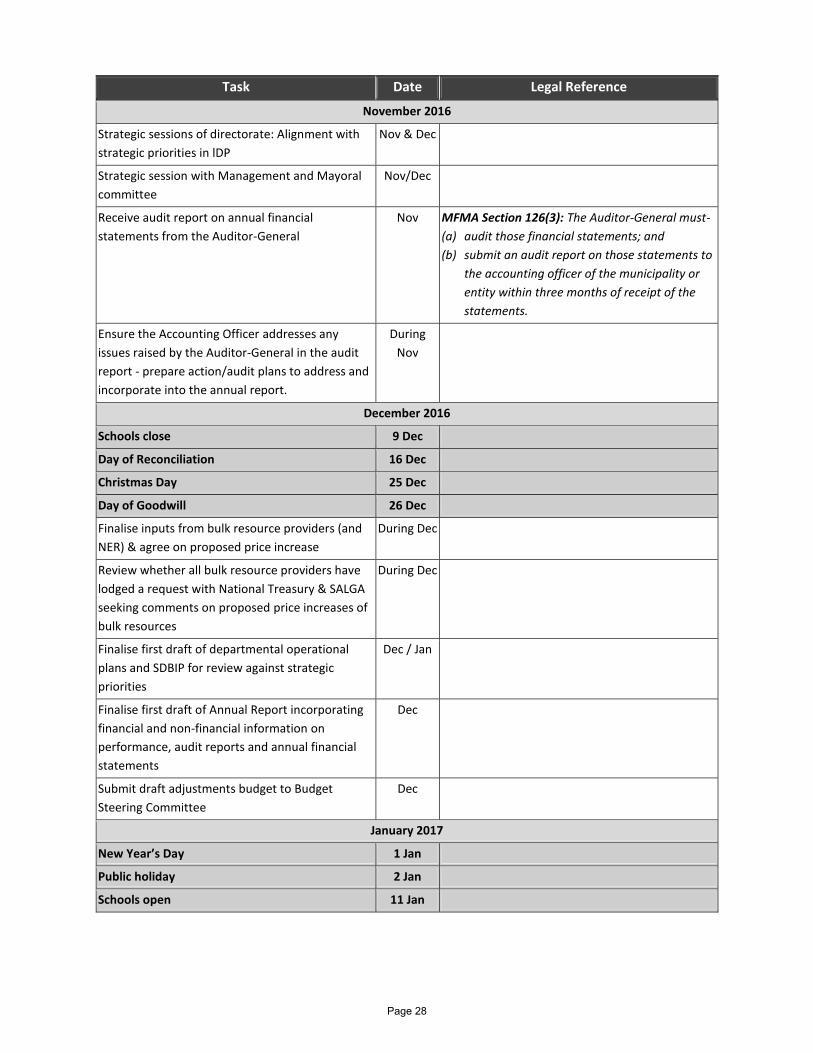

Task Date Legal Reference

November 2016

Strategic sessions of directorate: Alignment with

strategic priorities in lDP

Nov & Dec

Strategic session with Management and Mayoral

committee

Nov/Dec

Receive audit report on annual financial

statements from the Auditor-General

Nov MFMA Section 126(3): The Auditor-General must-

(a) audit those financial statements; and

(b) submit an audit report on those statements to

the accounting officer of the municipality or

entity within three months of receipt of the

statements.

Ensure the Accounting Officer addresses any

issues raised by the Auditor-General in the audit

report - prepare action/audit plans to address and

incorporate into the annual report.

During

Nov

December 2016

Schools close 9 Dec

Day of Reconciliation 16 Dec

Christmas Day 25 Dec

Day of Goodwill 26 Dec

Finalise inputs from bulk resource providers (and

NER) & agree on proposed price increase

During Dec

Review whether all bulk resource providers have

lodged a request with National Treasury & SALGA

seeking comments on proposed price increases of

bulk resources

During Dec

Finalise first draft of departmental operational

plans and SDBIP for review against strategic

priorities

Dec / Jan

Finalise first draft of Annual Report incorporating

financial and non-financial information on

performance, audit reports and annual financial

statements

Dec

Submit draft adjustments budget to Budget

Steering Committee

Dec

January 2017

New Year’s Day 1 Jan

Public holiday 2 Jan

Schools open 11 Jan

Page 28

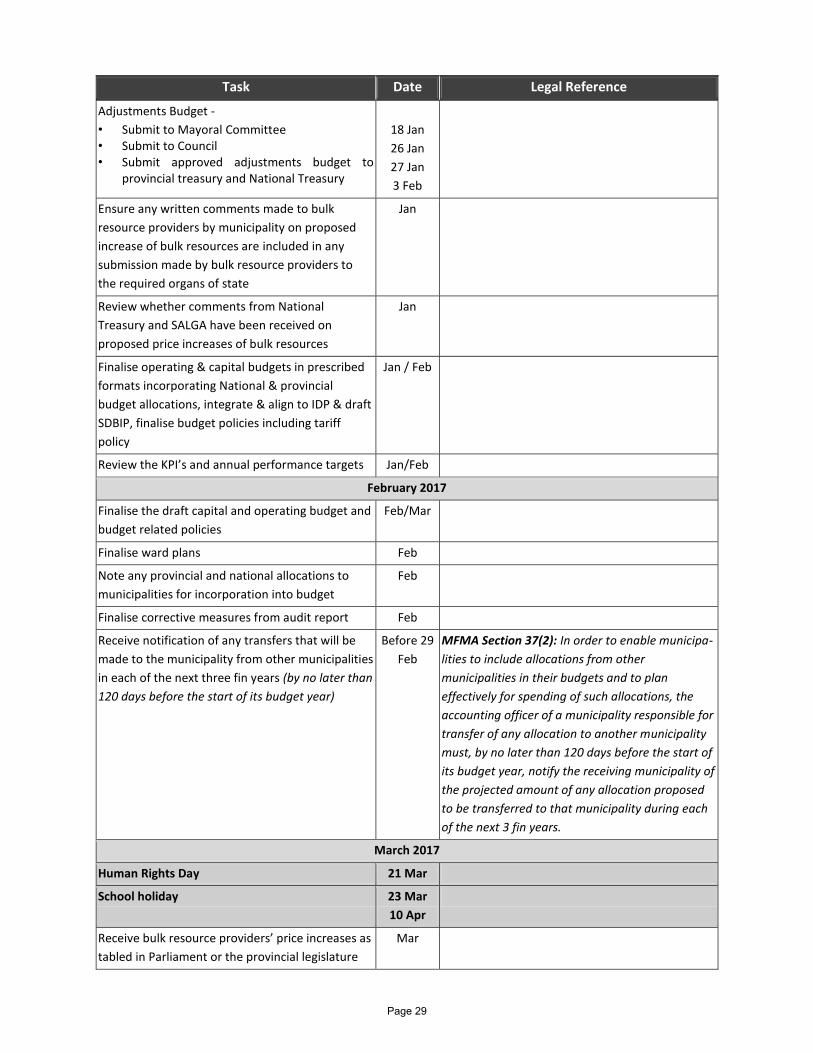

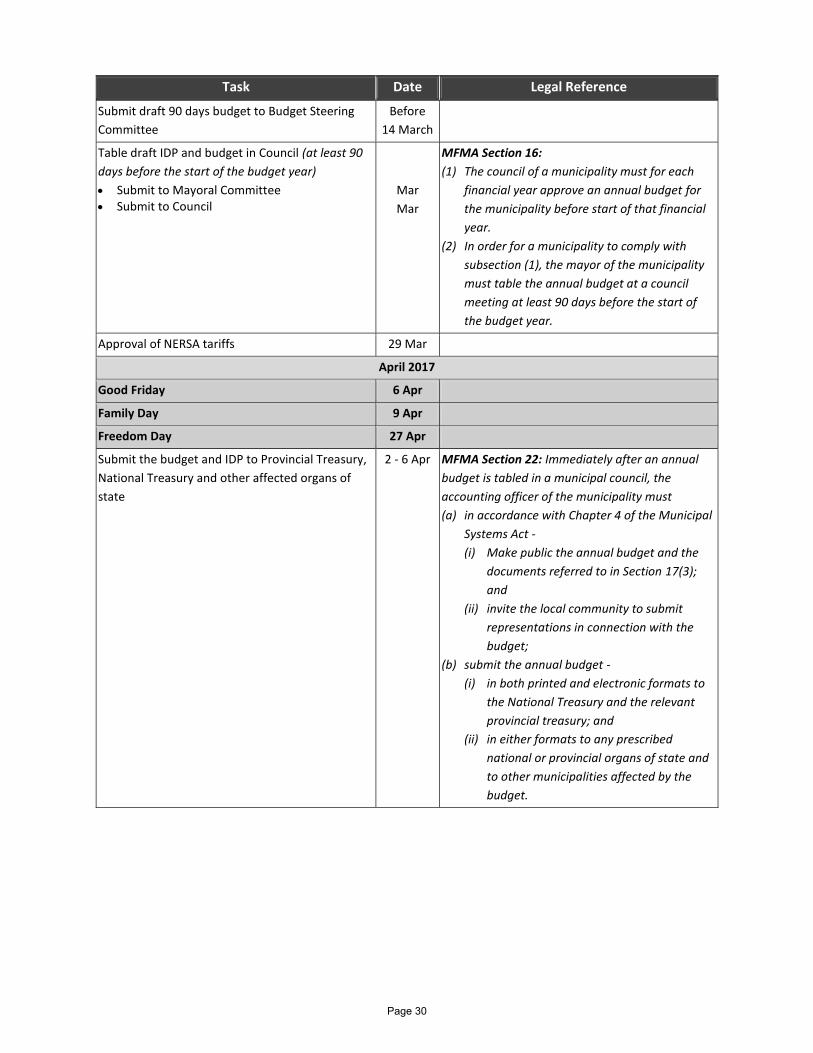

Task Date Legal Reference

Adjustments Budget -

• Submit to Mayoral Committee • Submit to Council • Submit approved adjustments budget to

provincial treasury and National Treasury

18 Jan

26 Jan

27 Jan

3 Feb

Ensure any written comments made to bulk

resource providers by municipality on proposed

increase of bulk resources are included in any

submission made by bulk resource providers to

the required organs of state

Jan

Review whether comments from National

Treasury and SALGA have been received on

proposed price increases of bulk resources

Jan

Finalise operating & capital budgets in prescribed

formats incorporating National & provincial

budget allocations, integrate & align to IDP & draft

SDBIP, finalise budget policies including tariff

policy

Jan / Feb

Review the KPI’s and annual performance targets Jan/Feb

February 2017

Finalise the draft capital and operating budget and

budget related policies

Feb/Mar

Finalise ward plans Feb

Note any provincial and national allocations to

municipalities for incorporation into budget

Feb

Finalise corrective measures from audit report Feb

Receive notification of any transfers that will be

made to the municipality from other municipalities

in each of the next three fin years (by no later than

120 days before the start of its budget year)

Before 29

Feb

MFMA Section 37(2): In order to enable municipa-

lities to include allocations from other