1 B.Com. (Hons.) Second Semester Examination (Year 2016) Business Maths Subject Code: BCOM-201 Paper Code: TMT-21 Time : 10 Minutes M.Marks : 10 Section A [k.M v (Objective Type Questions) ¼oLrqfu"B Á’u½ Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking the correct answer. lHkh iz’u vfuok;Z gSaA izR;sd iz’u gs rq 1 vad fu/kkZfjr gSA lgh mÙkj gs rq fn;s x;s ckDl esa () fpUg dk iz;ksx djsa A Q. No. 1. Choose the correct answer- lgh mÙkj pqfu,& 1. Which ratio is greater so? dkSu lk vuqikr cM+k gS& a) 3 : 5 b) 2 : 3 c) 3 : 4 d) 4 : 5 2. Value of X in 3 : 6 : : X : 18 is: 3 % 6 % % X % 18 esa X dk eku gS& a) 8 b) 9 c) 6 d) 4 3. 50 Paise is percentage of Rs. 25: 50 iS ls] 25 :Ik;s dk izfr'kr gS& a) 2% b) 2% c) .02% d) 5% 4. To earn Rs. 125 commission @ 6.25% amount of sales will be: 6-25% dh nj ls 125 :Ik;s deh'ku izkIr djus ds fy;s foØ; dh jkf'k gksxh& a) Rs. 2,000 b) Rs. 20,000 2]000 :- 20]000 :- c) Rs. 4,000 d) Rs. 40,000 4]000 :- 40]000 :- 5. Trade discount given on _________. O;kikfjd cV~ Vk ---------------------------- ij fn;k tkrk gSA a) List Price b) Selling Price lwph ewY; foØ; ewY; c) Cost Price d) Net Selling Price ykxr ewY; 'kq) foØ; ewY; Invigilator’s Signature Roll No. Enrollment No.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

B.Com. (Hons.) Second Semester Examination (Year 2016)

Business Maths Subject Code: BCOM-201

Paper Code: TMT-21 Time : 10 Minutes

M.Marks : 10

Section A

[k.M v

(Objective Type Questions)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking

the correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk iz;ksx djsaA

Q. No. 1. Choose the correct answer-

lgh mÙkj pqfu,&

1. Which ratio is greater so?

dkSu lk vuqikr cM+k gS&

a) 3 : 5 b) 2 : 3

c) 3 : 4 d) 4 : 5

2. Value of X in 3 : 6 : : X : 18 is:

3 % 6 % % X % 18 esa X dk eku gS&

a) 8 b) 9

c) 6 d) 4

3. 50 Paise is percentage of Rs. 25:

50 iSls] 25 :Ik;s dk izfr'kr gS&

a) 2% b) 2%

c) .02% d) 5%

4. To earn Rs. 125 commission @ 6.25% amount of sales will be:

6-25% dh nj ls 125 :Ik;s deh'ku izkIr djus ds fy;s foØ; dh jkf'k gksxh&

a) Rs. 2,000 b) Rs. 20,000

2]000 :- 20]000 :-

c) Rs. 4,000 d) Rs. 40,000

4]000 :- 40]000 :-

5. Trade discount given on _________.

O;kikfjd cV~Vk ---------------------------- ij fn;k tkrk gSA

a) List Price b) Selling Price

lwph ewY; foØ; ewY;

c) Cost Price d) Net Selling Price

ykxr ewY; 'kq) foØ; ewY;

Invigilator’s Signature

Roll No.

Enrollment No.

2

6. The sum of two numbers is 7 and their product is 12, the larger number is:

nks la[;kvksa dk ;ksx 7 gS rFkk xq.kuQy 12 gSA cM+h la[;k gS&

a) 7 b) 6

c) 5 d) 4

7. Value of If A = [1,2,3] B = [4,5,6] A+B is:

;fn A = [1,2,3] B = [4,5,6] gks rks A+B dk eku gS& a) [5,7,9] b) [3,3,3]

c) [5,7,8] d) [6,7,9]

8. Invoice includes:

chtd esa mYys[k fd;k tkrk gS&

a) Quantity of goods b) Value of goods

eky dh ek=k eky dk ewY;

c) Trade discount d) All of these

O;kikfjd cV~Vk mijksä lHkh

9. ________invoice prepared before purchase of goods:

eky Ø; djus ds iwoZ ---------------------- chtd cuk;k tkrk gS&

a) Ordinary invoice b) Proforma invoice

lk/kkj.k chtd lwpukFkZ chtd

c) Franco invoice d) All of these

loZO;; eqä chtd mijksä lHkh

10. The value of [𝑥 𝑦5 9

]=[3 12 3

] x,y, is) :

;fn [𝑥 𝑦5 9

]=[3 12 3

] gks rks x,y dk eku gS&

a) 3, 1 b) 1, 3

c) 5, 9 d) 2, 3

---------------------------

3

B.Com. (Hons.) Second Semester Examination (Year 2016)

Business Maths Subject Code: BCOM-201

Paper Code: TMT-21 Time : 2 Hrs.50 Mts.

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kqmÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q.No. 2. Two figures are in the ratio of 5 : 6. If 5 is added to both the figures, the new ratio

will be 6: 7. Find the figures.

nks jkf'k;k¡ 5 % 6 ds vuqikr esa gSaA ;fn bu jkf'k;ksa esa 5 tksM+ nsa] rks u;k vuqikr 6 % 7

gks tkrk gSA nksuksa jkf'k;k¡ Kkr dhft,A

OR

If 6 labourers make 18 kilometers road in a certain time, how many kilometers road

will be made by 15 labourers in the same time?

;fn 6 etnwj fdlh le; esa 18 fdyksehVj lM+d cukrs gSa rks 15 etnwj mruss gh le;

esa fdrus fdyksehVj lM+d cuk;saxsA

Q.No. 3. Twice of the total of two numbers are 80 and their difference is 8. Find the numbers.

nks la[;kvksa ds ;ksx dk nqxuk 80 gS rFkk varj 8 gSA la[;k;sa Kkr djksA

OR

Show items includes in an Invoice.

chtd esa 'kkfey gksus okyh ensa crkb,A

Q.No. 4. Describe the properties of multiplication of matrices.

nks vkO;wg ds xq.kuQy dh fo'ks"krk,¡ le>kb,A

OR

If A + C = B, Find the value of C, where:

;fn A + C = B gks] rks C dk eku Kkr dhft,] tcfd%&

A= [2 4 −104 0 12

] B = [18 8 1416 4 −2

]

Q.No. 5. What is meant by mantissa in logarithm?

y?kqxq.kd esa viw.kkZa'k (Mantissa) ls D;k vk'k; gS\

OR

Find the differential coefficient of y=5x3.

y=5x3 dk vodyu xq.kkad Kkr dhft,A

Q.No. 6. If the interest on Rs. 1,200 for 3 years is less than the interest on Rs. 1,500 for the

same period by Rs. 60, find the rate of interest.

;fn 3 o"kZ esa 1]200 :Ik;s dk C;kt mrus gh le; esa 1]500 :i;s ds C;kt ls 60 :Ik;s

de gks rks C;kt dh nj Kkr djksA

OR

Roll No.

4

A fruit vendor brought 3 dozens oranges for Rs. 50 and sold at 2 dozens for Rs. 60.

Find his gain percent.

,d Qy foØsrk us dqN larjs 50 :- esa rhu ntZu dh nj ls [kjhns vkSj 60 :- esa nks

ntZu dh nj ls cspsA ykHk dk izfr'kr Kkr dhft,A

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Q.No. 7. The Manager of a mining company is paid a fixed monthly salary and commission

at a fixed rate per ton of output. If the manager received altogether Rs. 33,250 and

Rs. 32,000 on two consecutive years against the output of 43.7 ton and 41.2 ton

respectively. Find the rate of commission and the monthly salary paid to him.

fdlh [kku daiuh ds izca/kd dks ,d fuf'pr ekfld osru vkSj mRiknu ij izfr Vu ,d

fuf'pr nj ls osru fn;k tkrk gSA ;fn izca/kd yxkrkj nks o"kksZa ds 43-7 Vu rFkk 41-2

Vu ds mRiknu ij Øe'k% 33]250 :- vkSj 32]000 :- izkIr djrk gS] rks mls fn;s tkus

okys orZu dh nj rFkk ekfld osru crkb,A

OR

Mohan secured 30% marks in an examination and failed by 20 marks. Sohan

secured 40% marks and got 40 marks more than the minimum passing marks.

Determine the maximum marks and the minimum marks necessary to pass.

,d ijh{kk esa eksgu us dqy vadksa ds 30 vad izkIr fd, vkSj 20 vadksa ls vuqÙkh.kZ jgk]

tcfd lksgu us dqy vadksa rFkk U;wure mÙkh.kkZadksa dh x.kuk dhft,A

Q.No. 8. On 7th September 2011 Jonson & Sons of London Shipped 10 Boxes as

"D" marked by 'Princes' ship to the order of Deven Bose of Kolkata. Each box

containing 500 meter of silk @ 5 pound per meter. The charges in connection with

the shipment are:

Packing 10 pound per box, carriage to port 3 pound per box, bill of landing 1 pound

per box. Each box measures 90 cms. ×100 cms. × 120 cms. and freight to be

charged @ 20 pound per ton of 1.08 cubic meters and 10% primage. Insurance is

to be effected on 30,000 pound @ 1%. Commission is 5%. Prepare a local invoice

in foreign currency.

7 flrEcj 2011 dks tkulu ,.M lUl yanu us fizUlsl uked tgkt ls dksydkrk ds

Jh nsosu cksl ds vkns'kkuqlkj 10 isfV;k¡ "D" fpUgkfdar djds HksthA izR;sd isVh esa 500

ehVj flYd nj 5 ikSaM izfr ehVj ds fglkc ls iSd fd;s x;s FksA

bl ij fuEu O;; gq,&

iSfdax 10 ikSaM izfr isVh] okgu O;; cUnjxkg rd 3 ikSaM izfr isVh] tgkt ij yknus ds

O;; 1 ikSaM izfr isVh] tgkth HkkM+k 20 ikSaM izfr Vu ¼1-08 ?ku ehVj½ ij yxkuk gS] 10%

vfrfjä HkkM+k yxkuk gSA izR;sd isVh dk eki 90 ls-eh- × 100 ls-eh- × 120 ls-eh- gSA

chek O;; 30000 ikSaM ij 1 izfr'kr rFkk deh'ku 5%A mi;qZä lwpuk ds vk/kkj ij

fons'kh eqnzk esa LFkkuh; chtd cukb,A

OR

5

Rajesh say to Deepak, my present age is 5 times of your age of that time, when I

was as old as you are now. The sum of their ages is 48 years. Find their present

ages.

jkts'k nhid ls dgrk gSa] ^esjh vk;q ml le; dh rqEgkjh vk;q dh ikap xquh gS ftl

le; eSa mruk cM+k Fkk ftrus rqe vkt gksA* mudh orZeku vk;q dk ;ksx 48 o"kZ gSA

mudh orZeku vk;q crkvksA

Q.No. 9. A manufacturer sells three articles in the markets of Indore and Bhopal as shown

below. Find the total revenue from each city using matrix algebra:-

,d fuekZrk rhu izdkj dh oLrq,¡ bankSj vkSj Hkksiky ds cktkjksa esa fuEukuqlkj csprk gSA

izR;sd 'kgj ls mldh dqy izkIr vk; vkO;wg chtxf.kr dk iz;ksx djrs gq, crkb,A

City ¼'kgj½ Articles ¼oLrq,¡½

A B C

Indore 10,000 25,000 30,000

Bhopal 9,000 15,000 20,000

Sale price per unit Rs. 3 Rs. 4 Rs. 2

OR

If A= [ 3 1−1 2

] , then show A2−5A + 7I = 0.

;fn A= [ 3 1−1 2

] gS] rks n'kkZb, fd A2−5A + 7I = 0 gksxkA

Q.No. 10. Differentiate y = 1

(𝑥−𝑎)(𝑥−𝑏)(𝑥−𝑐)

y = 1

(𝑥−𝑎)(𝑥−𝑏)(𝑥−𝑐) dks vodfyr dhft,A

OR

{(60.45)3(3.48)2

√2696} ÷

2

.006

Q.No. 11. A scooter is sold for Rs. 6,500 at profit if it is sold for Rs. 5,900 there would be a

loss equal to three times of the profit earned. Find the cost of the scooter.

,d LdwVj dks ykHk ij 6]500 :- esa cspk tkrk gS] ;fn mls 5]900 :- esa cspk x;k] rks

ykHk dh 3 xquk gkfu gksrhA LdwVj dh ykxr crkb,A

OR

A sum of money was borrowed and paid back in two annual installments of Rs. 654

and Rs. 660 respectively. If the rate of compound interest was 10% per annum. Find

the sum borrowed.

dqN jde m/kkj yh xbZ vkSj Øe'k% 654 :Ik;s vkSj 660 :Ik;s dh nks okf"kZd fdLrksa esa

Hkqxrku dh xbZA pØo`f) C;kt 10% okf"kZd nj ls yxk;kA crkb, fdruh jde m/kkj

yh xbZ Fkh\

----------------------

6

B.Com. (Hons.) Second Semester Examination (Year 2016)

Business Organization & Communication Subject Code: BCOM -202

Paper Code: TMT-22 Time : 10 Minutes

M.Marks : 10

Section A

[k.M v

(Objective Type Questions)

(oLrqfu"B Á’u)

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking

the correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk iz;ksx djsaA

Q. No. 1. Choose the correct answer-

lgh mÙkj pqfu,&

3. Object of business is-

O;olk; dk mís'; gS&

a) Creation of utility

mi;ksfxrk dk l`tu

b) Profit earning

ykHk dekuk

c) Social responsibility

lkekftd mÙkjnkf;Ro

d) Profit with social responsibility

lkekftd mÙkjnkf;Ro ds lkFk ykHk dekuk

4. Which two are base of a business?

O;olk; ds nks vk/kkj dkSu ls gS\

a) Industry & commerce b) Industry & trade

m|ksx o okf.kT; m|ksx vkSj O;kikj

c) Industry & business d) Commerce & business

m|ksx vkSj O;olk; okf.kT; ,oa O;olk;

3. Ethics are important for -

lnkpkj O;ogkj egRoiw.kZ gS&

a) Top Management

'kh"kZ izcU/ku ds fy;s

b) Middle level Management

e/;&Lrjh; izcU/ku gsrq

c) Non Managerial employees

xSj izcU/kdh; deZpkjh gsrq

d) All of these

mijksä lHkh

4. Expenditure on social responsibility is -

lkekftd mÙkjnkf;Ro ds fy;s [kpZ&

Invigilator’s Signature

Roll No.

Enrollment No.

7

a) Investment b) Wastage

fofu;kstu gS viO;; gS

c) Unnecessary d) Non economic

vuko';d gS vukfFkZd gS

5. If service is the main motto, then institution is called –

lsokrRo ftldk ewy mís'; gks og laLFkk dgykrh gS&

a) Public Enterprise b) Co-operative organization

lkoZtfud miØe lgdkjh laxBu

c) Pvt. Enterprise d) Partnership firm

fuft miØe lk>snkjh laxBu

6. For which institution, Registration is not necessary?

fdl laLFkk dk iath;u vko';d ugha gS\

a) Company

ize.My

b) Co-operative society

lgdkjh lfefr

c) Partnership Camp

lk>snkjh dSEi

d) Joint Hindu Family Business

la;qä fgUnq ifjokj O;olk;

7. Which one is incorrect in case of Public company?

,d lkoZtfud dEiuh dh n'kk esa fuEufyf[kr esa ls dkSu lk lgh ugha gS\

a) Artificial person

d`f=e O;fä

b) Perpetual existence

'kk'or vfLrRo

c) Non transferability of share

va'kksa dh vgLrkrj.kh;rk

d) Separate statutory existence

izFkd oS|kfud vfLrRo

8. In case 56% share are with Govt., then company is named as –

;fn 56 izfr'kr va'k ljdkj ds ikl gks rks ,slh dEiuh dks dgrs gS&

a) Foreign Company b) Govt. Company

fons'kh dEiuh ljdkjh dEiuh

c) Public Company d) Public Enterprise

lkoZtfud dEiuh yksd fuxe

9. A company is said to be registered when –

,d dEiuh iathdr̀ ekuh tkrh gS tc&

a) Necessary documents are submitted with registrar

iath;d ds ikl vko';d izys[k tek dj fn;s tk;sa

b) After receiving certificate of incorporation

lekesyu izek.k i= izkIr gks tkus ij

8

c) When business is actually started

tc O;olk; okLro esa izkjEHk dj fn;k gks

d) None of these

mijksä esa ls dksbZ ugha

10. When did Industrial Financial Corporation established?

Hkkjrh; vkS|ksfxd foÙk fuxe dh LFkkiuk dc gqbZ\ a) 1948 b) 1956

lu~ 1948 lu~ 1956

c) 1964 d) 1947

lu~ 1964 lu~ 1947

------------------------------------

9

B.Com. (Hons.) Second Semester Examination (Year 2016)

Macro Economics Subject Code: BCOM-204

Paper Code: TMT-23 Time : 10 Minutes

M.Marks : 10

Section A

[k.M v

(Objective Type Questions)

(oLrqfu"B Á’u)

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking

the correct answer.

lHkh iz’u vfuok;Z gSaA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk iz;ksx djsaA

Q. No. 1. Choose the correct answer-

lgh mÙkj pqfu,&

5. Macro Economics is related to -

lef"V vFkZ'kkL= dk laca/k gS&

b) Level of production of goods and services

oLrqvksa ,oa lsokvksa ds mRiknu Lrj ls

b) General price level

lkekU; dher Lrj

c) Increase in income

vk; o`f) ls

d) All of these

mijksä lHkh

2. Macro Economics may be defined as the branch of -

lef"V vFkZ'kkL= dks bldh 'kk[kk ds :Ik esa Hkh ifjHkkf"kr fd;k tkrk gS&

a) Economic Development b) Economic Behaviour

vkfFkZd fodkl vkfFkZd O;ogkj

c) Economic analysis d) Economic equation

vkfFkZd fo'ys"k.k vkfFkZd lehdj.k

3. Which of the following is the main feature of Macro Economics?

fuEufyf[kr esa ls dkSu lh lef"V vFkZ'kkL= dh eq[; fo'ks"krk gS\

a) Study of individual b) Study of aggregates

O;fä dk v/;;u lewgksa dk v/;;u ¼lewgksa½

c) Partial equilibrium d) None of these

vkfFkZd larqyu mijksä esa ls dksbZ ugha

4. Micro Economics & Macro Economics are –

O;f"V vFkZ'kkL= ,oa lef"V vFkZ'kkL= gSa&

a) Independent of each other b) Competitive to each other

,d&nwljs ls Lora= ,d&nwljs ds izfrLi/khZ

c) Interdependent d) None of these

Invigilator’s Signature

Roll No.

Enrollment No.

10

ijLij fuHkZj mijksä esa ls dksbZ ugha

5. The item which is not included in National Income is –

tks en jk"Vªh; vk; esa lfEefyr ugha gksrh] og gS

a) Undistributed profit

vforfjr ykHk

b) Corporation tax

fuxe dj

c) Income from sale of old goods

iqjkuh oLrqvksa ds foØ; ls izkIr vk;

d) Rent and interest

yxku ,oa C;kt

6. Old age pension will not be included in National Income because it is -

o`)koLFkk ias'ku jk"Vªh; vk; esa lfEefyr ugha gksxh D;ksafd ;g gS&

a) Unproductive function b) Intermediary service

vuqRiknd fØ;k e/;orhZ lsok

c) Transfer payment d) Has no value

gLrkarj.k Hkqxrku bldk dksbZ ewY; ugha

7. Total monetary value of goods and services produced in a year is called –

,d o"kZ esa mRikfnr oLrqvksa vkSj lsokvksa ds dqy ekSfnzd ewY; dks dgrs gS&

a) Gross Domestic Product b) Net Domestic Product

ldy ?kjsyw mRikn 'kq) ?kjsyw mRikn

c) National Income d) Personal Income

jk"Vªh; vk; oS;fäd vk;

8. National Income is also known as –

jk"Vªh; vk; dks bl uke ls Hkh tkuk tkrk gS&

a) Net Product b) National Dividend

'kq) mRikn jk"Vªh; ykHkka'k

c) Gross Product d) Net National Product

ldy mRikn 'kq) jk"Vªh; mRikn

9. Wages paid only in money is called -

dsoy eqnzk esa nh tkus okyh etnwjh dks dgk tkrk gS&

a) Total wages b) Real wages

dqy etnwjh vly etnwjh

c) Money wages d) None of these

ekSfnzd etnwjh mijksä esa ls dksbZ ugha

10. The profounder of Wages Fund Theory is -

etnwjh dks"k fl)kar ds izfriknd gS& b) Adam Smith b) Keynes

,Me fLeFk dhUl

c) Pigou d) J.S. Mill

ihxw ts-,l- fey

------------------------------------

11

B.Com. (Hons.) Second Semester Examination (Year 2016)

Macro Economics Subject Code: BCOM-204

Paper Code: TMT-23 Time : 2 Hrs.50 Mts.

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kqmÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q. No. 2. Write the main features of Macro Economics.

lef"V vFkZ'kkL= dh izeq[k fo'ks"krk, fyf[k;sA

OR

How do you distinguish between Micro and Macro Economics?

vki O;f"V ,oa lef"V vFkZ'kkL= esa varj fdl izdkj djsxsa\

Q.No.3. Write a short note on Gross National Products.

ldy jk"Vªh; mRikn ij laf{kIr fVIi.kh fyf[k,A

OR

Criticisms of Marshall’s view on National Income.

jk"Vªh; vk; ij ek'kZy ds n`f"Vdks.k dh vkykspuk;sa le>kb,A

Q. No.4. Differentiate between Gross Interest and Net Interest.

ldy C;kt ,oa 'kq) C;kt esa varj crkb,A

OR

Discuss Say’s law of market.

^^ls dk cktkj fu;e** crkb,A

Q. No.5. Define Money.

eqnzk dks ifjHkkf"kr dhft;sA

OR

Discuss Cambridge equation.

dsfEczt lehdj.k dh O;k[;k dhft,A

Q. No. 6. Mention the primary functions of Commercial Banks.

O;kikfjd cSadksa ds izkFkfed dk;Z crkb,A

OR

What do you mean by Open Market Operations?

[kqys cktkj dh fØ;kvksa ls vki D;k le>rs gSa\

Roll No.

12

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

Q. No. 7. Explain the concept and importance of Macro Economics.

lef"V vFkZ'kkL= dh vo/kkj.kk ,oa egRo dks le>kb,A

OR

What is Macro Economics? What are its various types? Explain its limitations.

lef"V vFkZ'kkL= D;k gS\ blds fdrus izdkj gksrs gSa\ bldh lhekvksa dks le>kb,A

Q. No.8. Explain critically the different concepts of national income.

jk"Vªh; vk; dh fofHkUu /kkj.kkvksa dh vkykspukRed O;k[;k dhft,A

OR

How national income is calculated? What are the difficulties in the measurement

of national income?

jk"Vªh; vk; dks dSls ekik tkrk gS\ blds ekiu esa dkSu lh dfBukb;k¡ vkrh gS\

Q. No. 9. Critically examine the Liquidity Preference Theory of interest.

C;kt ds rjyrk ilanxh fl)kar dh vkykspukRed O;k[;k dhft,A

OR

Explain the modern theory of wages with suitable examples.

mi;qä mnkgj.kksa lfgr etnwjh ds vk/kqfud fl)kar dks le>kb,A

Q.No.10. “The quantity theory of money is correct in principles but defective in practice”.

Examine.

^^eqnzk dk ifjek.k fl)kar Bhd gS] fdUrq O;ogkj esa nks"kiw.kZ gSA** O;k[;k dhft,A

OR

Discuss the factors which influence the supply of money.

eqnzk dh iwfrZ dks izHkkfor djus okys rRoksa dh O;k[;k dhft,A

Q, No.11. Discuss the causes of inflation. How can it be controlled?

eqnzk&LQhfr ds dkj.kksa dks crkb,A bls dSls fu;af=r fd;k tk ldrk gS\

OR

Discuss the role of Central Bank in developing economy.

fodkl'khy vFkZO;oLFkk esa dsUnzh; cSad dh Hkwfedk dk o.kZu dhft,A

-----------------------------

13

B.Com. (Hons.) Second Semester Examination (Year 2016)

Advanced Financial Accounting Subject Code: BCOMH-208

Paper Code: TMT-24 Time : 10 Minutes

M.Marks : 10

Section A

[k.M v (Objective Type Questions)

¼oLrqfu"B Á’u½

Attempt all questions. Each question carries 1 mark. Use the symbol () in the box for marking

the correct answer.

lHkh iz’u vfuok;Z gSA izR;sd iz’u gsrq 1 vad fu/kkZfjr gSA lgh mÙkj gsrq fn;s x;s ckDl esa () fpUg dk iz;ksx djsaA

Q. No. 1. Choose the correct answer-

lgh mÙkj pqfu,&

1. Favourable balance of cash book means-

jksdM+ cgha ds vuqdwy 'ks"k dk vk'k; gksrk gS&

a) Debit balance in the cash book

jksdM+ cgha dk MsfcV 'ks"k

b) Credit balance in the cash book

jksdM+ cgha dk ØsfMV 'ks"k

c) Debit balance in pass book

iklcqd dk MsfoV 'ks"k

d) Unfavourable balance in cash book

jksdM+ cgha esa izfrdwy 'ks"k

2. A Bank reconciliation statement is-

cSad lek/kku fooj.k gksrk gS&

a) A part of cash book

jksdM+ iqLrd dk Hkkx

b) A part of pass book

ikl cqd dk Hkkx

c) A part of current A/c

pkyw [kkrs dk Hkkx

d) A statement prepared by customer

xzkgd ds _.k [kkrs dk Hkkx

3. Interest is calculated on-

C;kt dh x.kuk dh tkrh gS&

a) Market price of securities b) Purchase price of securities

izfrHkwfr;ksa ds cktkj ewY; ij izfrHkwfr;ksa ds Ø; ewY; ij

c) Book value of securities d) Face value of securities

izfrHkwfr;ksa ds iqLrd ewY; ij izfrHkwfr;ksa ds vafdr ewwY; ij

Roll No.

Enrollment No.

Invigilator’s Signature

14

15

4. Meaning of cum-interest price of investment is-

fofu;ksx dk C;kt&lfgr ewY; ls vk'k; gS&

a) Market price + Interest b) Market price - Interest

Ckktkj ewY;$C;kt cktkj ewY;&C;kt

c) Market price d) None of these

cktkj ewY; mijksDr esa ls dksbZ ugha

5. The estimate of assets and liabilities for the year ended is called-

o"kZ ds var esa laifÙk;ksa rFkk nkf;Ro ds vkadyu dks dgrs gSa&

a) Balance sheet b) Statement of Affairs

fpV~Bk fLFkfr fooj.k

c) Statement of capital d) Trial Balance

iwath dk fooj.k ryiV

6. The closing balance of trade debtors is calculated-

O;kikfjd nsunkjksa ds vafre 'ks"k dh x.kuk dh tkrh gS&

a) From total debtors Alc b) From balance sheet

dqy nsunkj [kkrs ls fpV~Bs ls

c) From cash book d) None of these

jksdM+ iqLrd ls mijksDr esa ls dksbZ ugha

7. Single entry system can be adopted by-

,dkaxh izfof"V iz.kkyh viukbZ tk ldrh gS&

a) Small firms b) Joint stock companies

NksVh QeksZa }kjk la;qDr Lda/k izeaMy }kjk

c) Co-operative societies d) None of these

lgdkjh lfefr;k¡ }kjk mijksDr esa ls dksbZ ugha

8. Opening capital is ascertained by preparing-

izkjafHkd iwath Kkr dh tkrh gS&

a) Cash A/c b) Opening statement of affairs

jksdM+ [kkrk cukdj izkjafHkd fLFkfr fooj.k cukdj

c) Total creditors Alc d) None of these

dqy ysunkj [kkrk cukdj mijksDr esa ls dksbZ ugha

9. In case of Hire purchase system, assets account is debited with-

fdjk;k Ø; i)fr dh n'kk esa laifÙk [kkrk MsfcV fd;k tkrk gS&

a) Cash price b) Hire purchase price

jksdM+ ewY; ls fdjk;k Ø; ewY; ls

c) Cost price d) None of these

ykxr ewY; ls mijksä esasa ls dksbZ ugha

10. On seizure of the goods by the Hire vendor, the balance in the asset account is

transferred to-

fdjk;k foØsrk }kjk eky tCr fd;s tkus ij] laifÙk [kkrs dk 'ks"k gLrkarfjr fd;k tkrk

gS&

a) Profit & Loss A/c b) Hire vendor's A/c

ykHk&gkfu [kkrs esa fdjk;k foØsrk ds [kkrs esa

c) Good repossessed A/c d) Hire sales A/c

eky okilh [kkrs esa fdjk;k foØ; [kkrs esa

---------------------------

16

B.Com. (Hons.) Second Semester Examination (Year 2016) Advanced Financial Accounting

Subject Code: BCOMH-208

Paper Code: TMT-24 Time : 2 Hrs. 50 Mts.

M.Marks : 60

Section B

[k.M c (Short Answer Type Questions)

(y?kq mÙkjh; iz’u)

Attempt all questions. Each question carries 4 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 4 vad fu/kkZfjr gSA

Q.No. 2 Discuss the importance of Bank Reconciliation Statement.

cSad lek/kku fooj.k ds egRo dh foospuk djsaA

OR

What are the types of securities?

izfrHkwfr;k¡ fdrus izdkj dh gksrh gS\

Q. No. 3 Explain the defects of the single entry system of book-keeping.

iqLrdikyu dh ,dkaxh izfof"V iz.kkyh ds nks"kksa dh O;k[;k dhft,A

OR

How does a trader ascertain the profit under single entry system?

,dkaxh izfof"V iz.kkyh ds varxZr ,d O;kikjh ykHk dh x.kuk fdl izdkj djrk gS\

Q. No. 4 Differentiate between hire purchase sale and credit sale.

fdjk;k [kjhn fcØh rFkk m/kkj fcØh esa varj dhft,A

OR

What is Interest Suspense Account?

“C;kt mpar [kkrk D;k gS\

Q. No. 5 Siddh ship commenced its voyage from Chennai to London and back to Chennai

on 1st June 2014. Ship was loaded on freight rate of 1,000 tons @ Rs. 50 per ton from

Chennai to London and 2,000 tons @ Rs. 40 per ton from London to Chennai.

i) Expenses on port amounted to for outward voyage Rs. 40,000 and for return

journey Rs. 28,000.

ii) During sailing period on fuel oil charges amounted to Rs. 25,000 and salary

Rs. 27,000.

iii) Insurance premium Rs. 5,000.

iv) Commission to agent Rs. 2,000.

v) Ship reached Chennai on 30th Sep. 2014. Prepare Voyage A/c.

fl) ty;ku us psUubZ ls yanu vkSj okilh dh viuh leqnzh ;k=k 1 twu 2014 dks iw.kZ

dhA ty;ku dk fdjk;k HkkM+k nj psUubZ ls yanu 1]000 Vu] :- 50 izfrVu dh nj ls rFkk

yanu ls psUubZ 2]000 Vu 40 :- izfrVu yxk;k x;kA

i) iksVZ ij ckgjh leqnzh O;; :- 40]000 rFkk okilh ;k=k ds :- 28]000 yxk, x,A

ii) ;k=k ds nkSjku bZa/ku] rsy ds 25]000 :- rFkk osru ds :- 27]000 [kpZ gq,A

iii) chek izhfe;e :- 5]000

iv) deh'ku ,tsaV dk :- 2]000

Roll No.

17

v) ty;ku 30 flrEcj 2014 dks psUubZ igq¡pkA leqnzh ;k=k [kkrk cukb,A

OR

Jain & Co. sent goods costing Rs. 20,000 to Sarkar & co. on consignment A/c and

incurred Rs. 1,800 on freight and insurance. Sales commission @ 5% and del-

credere commission @ 11

4% is payable. Consignee sold goods to the extent of Rs.

32,000 and expenses were Rs. 2,400. The unsold stock was worth Rs. 600 in the

hands of consignee. Open necessary accounts is the books of consignor.

tSu ,aM daiuh us ljdkj ,aM daiuh dks izs"k.k ij 20]000 :- dk eky Hkstk rFkk bl ij

1]800 :- fdjk;k ,oa chek ds fy, O;; fd;sA fcØh deh'ku 5% vkSj vfrfjDr deh'ku

11

4% gSA isz"kh us vf/kdre eky 32]000 :- dk cspk rFkk 2]400 :- fcØh O;; gq,A izs"kh

ds ikl vafre jgfr;k 600 :- ykxr ewY; dk FkkA izs"kd dh iqLrdksa esa vko';d ys[ks

dhft,A

Q. No. 6 Prepare Receipt and Payments A/c of the library for the year 2014. The following

informations are in the accounts of Library-cash balance (1.1.2014) Rs. 4,000,

Entry fees received in 2014 Rs 600, Subscription received for 2014 Rs. 1,000, for

2013 (during 2014) Rs. 200, Rent paid during 2014 Rs. 150, Book purchased Rs.

1,100, Newspapers purchased Rs. 500, Salaries Rs. 500 paid.

2014 o"kZ ds fy, ,d iqLrdky; dk izkfIr vkSj Hkqxrku [kkrk cukosaA iqLrdky; ds

ys[kksa esa fuEu fyf[kr lwpuk,¡ gS& udn 'ks"k ¼1-1-2014½ :- 4]000] 2014 esa izos'k 'kqYd

ik;k :- 600] 2014 ds fy, pank ik;k :- 1]000] 2013 ds fy, ¼2014 esa½ :- 200]

2014 ds nkSjku fdjk;k fn;k :- 150] fdrkcsa [kjhnh :- 1]100] lekpkj i= [kjhnas :-

500] osru :- 500 fn;kA

OR

Prepare Receipts and Payment Account of Abhilash club, Indore for the year ended

on 31st December 2014-

Cash balance-1st January 2014 Rs. 4,390, Subscriptions received-last year's Rs.

600, Current year's Rs. 33,000, Next year's Rs 4,000, Donation received Rs. 8,000, Entry

fees Rs. 4,300, Rent received Rs. 5,250, Electric charges Rs. 3,440, Wages Rs. 500,

Interest received Rs 2,950, Insurance premium Rs. 310, Printing and stationery Rs.

350, Sundry expenses Rs. 900, Salary Rs. 16,000, Honorarium to secretary Rs. 7,500,

Rent of club building Rs. 1,750 is accrued, outstanding expenses of printing and

stationery Rs. 150.

31 fnlEcj 2014 dks lekIr gq, o"kZ ds fy, vfHkyk"k Dyc] bankSj dk izkfIr ,oa Hkqxrku

[kkrk cuk, udn 'ks"k& 1 tuojh 2014 :- 4]390] pank ik;k fiNys o"kZ dk :- 600] orZeku

o"kZ dk 33]000 :-] vkxkeh o"kZ dk 4]000 :-] nku ik;k :- 8]000] izos'k 'kqYd 4]300 :-] fdjk;k

ik;k :- 5]250] fo|qr izHkkj :- 3]440] etnwjh :- 500] C;kt ik;k :- 2]900] chek

izC;kft :- 310] NikbZ vkSj ys[ku lkexzh :- 350] fofo/k O;; :- 900] osru :- 16]000]

lfpo dks ekuns; :- 7]500] Dyc ds Hkou dk fdjk;k :- 1]750] mikftZr gks pqdk gSA

NikbZ vkSj ys[ku lekxzh ds vnÙk O;; :- 150 gSaA

Section C

[k.M l (Long Answer Type Questions)

(nh?kZ mÙkjh; iz’u)

Attempt all questions. Each question carries 8 marks.

lHkh iz’uksa ds mÙkj nsaA lHkh iz’uksa ds fy;s 8 vad fu/kkZfjr gSA

18

Q. No. 7 On December 31, 2014, the cash book of Jain Bros. showed an overdraft of Rs.

6,920, from the following particulars prepare a Bank Reconciliation Statement and

ascertain the balance as per Pass Book-

i) Debited by bank for Rs. 200 on account of interest on overdraft and Rs. 50

on account of bank charges.

ii) Cheques drawn but not encashed before December 31, 2014 for Rs. 4,000.

iii) The bank has collected interest and has credited Rs. 600, in pass book.

iv) A bill receivable for Rs. 700 previously discounted with the bank had been

dishonoured and debited in the pass book.

v) Cheques paid into bank but not collected and credited before December 31,

2014 amounted Rs. 6,000.

31 fnlEcj 2014 dks tSu cznlZ dh jksdM+ cgh 6]920 :- dk vf/kfod"kZ n'kkZ jgh FkhA

fuEu fooj.k dh lgk;rk ls cSad lek/kku fooj.k cukb, rFkk ikl cqd ds 'ks"k dh x.kuk

dhft,&

i) cSad }kjk :- 200] vf/kfod"kZ ij C;kt o :- 50 cSad 'kqYd ds uke fd;s x;sA

ii) :- 4]000 ds fuxZfer psd tks 31 fnlEcj 2014 ls iwoZ Hkqxrku ds fy, izLrqr

ugha gq,A

iii) cSad us :- 600 dk C;kt ,df=r dj iklcqd esa tek fd;k gSA

iv) ,d fofue; foi= tks fd :- 700 dk Fkk] igys cSad ls cV~Vk djok;k x;k Fkk]

vuknfjr gksus ds dkj.k uke i{k esa izfo"V fd;k x;kA

v) :- 6]000 ds psd tks cSad esa tek djk;s x;s] 31 fnlEcj 2014 ls igys laxzghr

ugha gq,A

OR

On 1st February, 2,000 Sudha purchased 200, 6% Housing Board debentures of Rs.

100 each @ Rs. 105 cum-interest. Interest is payable on 31st March and 30th September

each year. On 31st December, 2,000, these debenture were quoted in the market @

Rs. 95 each. These debentures are held as current assets brokerage is paid @ 1/10%.

Pass necessary Journal Entries in the books of Sudha for the year 2,000. Books are closed

on 31st December each year. Ignore income tax.

1 Qjojh 2]000 dks lq/kk us 100 :- okys gkmflax cksMZ ds 200] 6% _.ki= 105 :]

C;kt lfgr dh nj ls Ø; fd;sA C;kt izfro"kZ 11 ekpZ vkSj 30 flrEcj dks ns; gSA 31

fnlEcj 2]000 dks ;g _.ki= cktkj esa 95 :- izfr _.ki= dh nj ij mn~/ks̀r ¼quote½

fd;k tkrk gSA bu _.ki=ksa dks pkyw laifÙk dh Hkkafr j[kk tkrk gSA nykyh 1@10

izfr'kr dh nj ij pqdk;h tkrh gSA o"kZ 2]000 ds fy, lq/kk dh iqLrdksa esa tuZy dh

vko';d izfof"V;k¡ dhft,A iqLrdsa 31 fnlEcj dks can dh tkrh gS

Q. No. 8 Mr. Shailesh keeps his books on incomplete records. Following informations is

given below-

1 April 2013

Rs.

31 March

2014

Rs.

Cash in hand 1,000 1,500

Cash at bank 15,000 10,000

Stock 1,00,000 95,000

19

Debtors 42,500 70,000

Business premises 75,000 1,35,000

Furniture 9,000 7,500

Creditors 66,000 87,000

Bills payable 44,000 58,000

During the year he withdrew Rs. 45,000 and introduced Rs. 25,000 as further capital

in the business. Compute the Profit or Loss of the business.

Jh 'kSys"k tks viuh iqLrdksa dks ,dy izfof"V iz.kkyh ds vuqlkj j[krk gSA fuEu lwpuk,¡

nh xbZ gS&

1 vizSy 2013

:-

31 ekpZ 2014

:-

gkFk esa jksdM+ 1]000 1]500

cSad esa jksdM+ 15]000 10]000

LVkWd 1]00]000 95]000

nsunkj 42]500 70]000

O;kikfjd ifjlj 75]000 1]35]000

QuhZpj 9]000 7]500

ysunkj 66]000 87]000

ns; foi= 44]000 58]000

mlus o"kZ ds nkSjku 45]000 :- fudkys vkSj O;kikj esa 25]000 :-] vfrfjDr iwath yxkbZ

O;kikj dk ykHk ;k gkfu fudkysaA

OR

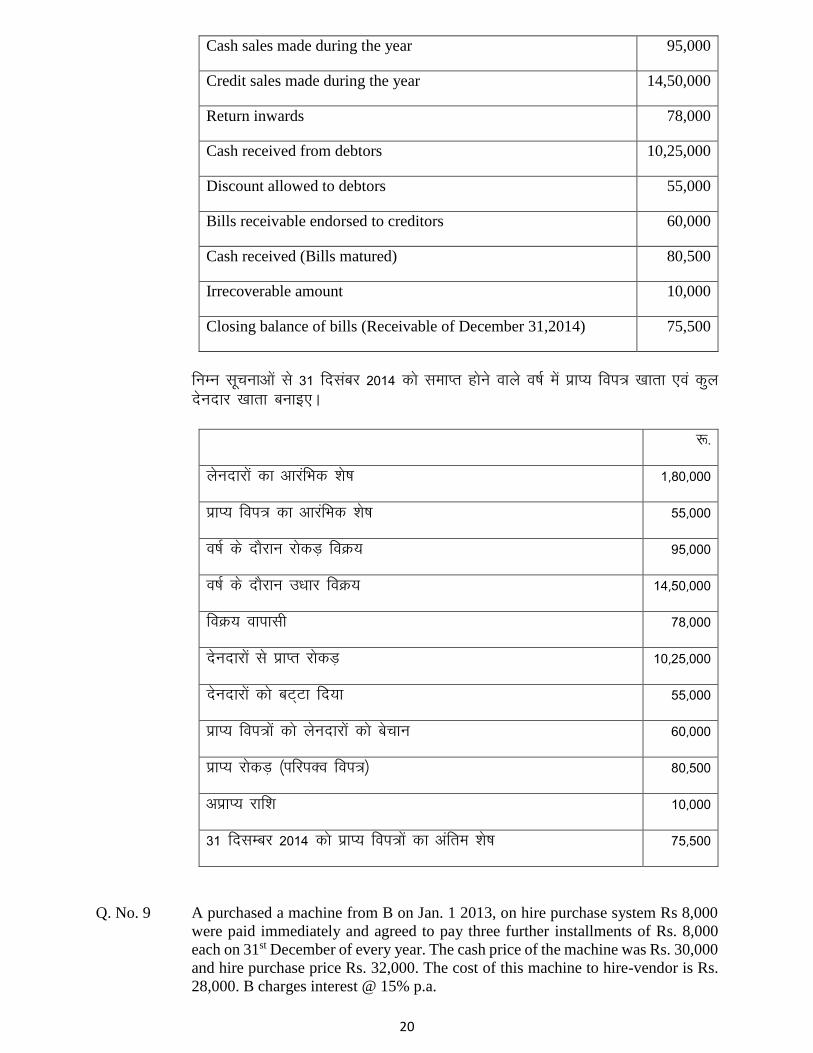

From the following information prepare the Bills Receivable Account and Total

Debtors Account for the year ended December 31, 2014.

Rs.

Opening balance of debtors 1,80,000

Opening balance of bills receivable 55,000

20

Cash sales made during the year 95,000

Credit sales made during the year 14,50,000

Return inwards 78,000

Cash received from debtors 10,25,000

Discount allowed to debtors 55,000

Bills receivable endorsed to creditors 60,000

Cash received (Bills matured) 80,500

Irrecoverable amount 10,000

Closing balance of bills (Receivable of December 31,2014) 75,500

fuEu lwpukvksa ls 31 fnlacj 2014 dks lekIr gksus okys o"kZ esa izkI; foi= [kkrk ,oa dqy

nsunkj [kkrk cukb,A

:-

ysunkjksa dk vkjafHkd 'ks"k 1]80]000

izkI; foi= dk vkjafHkd 'ks"k 55]000

o"kZ ds nkSjku jksdM+ foØ; 95]000

o"kZ ds nkSjku m/kkj foØ; 14]50]000

foØ; okiklh 78]000

nsunkjksa ls izkIr jksdM+ 10]25]000

nsunkjksa dks cV~Vk fn;k 55]000

izkI; foi=ksa dks ysunkjksa dks cspku 60]000

izkI; jksdM+ ¼ifjiDo foi=½ 80]500

vizkI; jkf'k 10]000

31 fnlEcj 2014 dks izkI; foi=ksa dk vafre 'ks"k 75]500

Q. No. 9 A purchased a machine from B on Jan. 1 2013, on hire purchase system Rs 8,000

were paid immediately and agreed to pay three further installments of Rs. 8,000

each on 31st December of every year. The cash price of the machine was Rs. 30,000

and hire purchase price Rs. 32,000. The cost of this machine to hire-vendor is Rs.

28,000. B charges interest @ 15% p.a.

21

Hire-vendor B agreed to make ordinary repairs in the machine free of cost

for a period of three years from the date of sale and for this purpose 1/2 of the profit

on sale may be taken to cover this service. Assuming that cost of repairs amended

to Rs. 200 in the first year Rs. 300 in the 2nd year and Rs. 400 in the 3rd year, prepare

A's account, maintenance suspense account and hire-sale account in the books of

B. B closes his books every year on 31st December.

A us 1 tuojh 2013 dks B ls ,d e'khu fdjk;k Ø; i)fr ij Ø; dhA 8]000 :-

mlh le; udn fn,A :- 8]000 dh rhu fdLrsa nsus ds fy, lger gks x;k tks izR;sd

o"kZ 31 fnlEcj dks ns; gksrh gSA e'khu dk udn ewY; 30]000 :- gSA fdjk;k Ø; ewY;

:- 32]000 gSA bl e'khu dk fdjk;k foØsrk dks ykxr 28]000 :- gSA B 5% izfro"kZ

dh nj ls C;kt ysrk gSA

fdjk;k foØsrk B us foØ; dh frfFk ls rhu o"kZ rd e'khu dh lkekU; ejEer

fu% 'kqYd djus dh lgefr nh vkSj bl lsok ds fy, fcØh ij ykHk dk 1@2 Hkkx iz;ksx

fd;k tk ldrk gSA ;g ekurs gq, fd izFke o"kZ esa ejEer dk O;; 200 :-] f}rh; o"kZ

esa 300 :- vkSj r`rh; o"kZ esa :- 400 gqvk] B dh iqLrdksa esa A dk [kkrk] esaVsusal lLisal

[kkrk vkSj fdjk;k fcØh [kkrk cukb,A B vius [kkrs izR;sd o"kZ 31 fnlEcj dks can

djrk gSA

OR

Transport Co. Ltd. purchased Truck from Paras motors Ltd. on installment system.

The cash price of the Truck was Rs. 3,20,000 which was payable as under: Rs. 1,00,000

on the date of purchase i.e. 1st January 2011, Rs. 80,000 on 31st Dec. 2011, Rs. 80,000

on 31st December, 2012 Rs. 82,478 on 31st December, 2013. Paras Motors Ltd.

charged interest at the rate of 5% per annum on the unpaid amount. The purchasing

co. decided to write off depreciation at 20% of the Cash Price each year. Prepare

necessary accounts in the books of Transport Co. Ltd. for three years.

ikjl eksVlZ fyfeVsM ls fdLr i)fr ij VªkaliksVZ daiuh fyfeVsM us ,d Vªd [kjhnkA

Vªd dk jksdM+ ewY; 3]20]000 :- Fkk tks fd bl izdkj pqdk;k x;k&

:- 1]00]000 Ø; dh frfFk dks vFkkZr~ 1 tuojh 2011 dks :- 80]000] 31 fnlEcj 2011

dks] :- 80]000 31 fnlEcj 2012 dks] :- 82]478] 31 fnlEcj 2013 dksA ikjl eksVlZ

fyfeVsM 5% okf"kZd nj ls vo'ks"k jkf'k ij C;kt yxkrk gSA Øsrk daiuh us 20% ykxr

ewY; ij izfro"kZ gzkl vifyf[kr djuk r; fd;kA VªkaliksVZ daiuh fyfeVsM dh iqLrdksa

esa vko';d [kkrs rhu o"kZ ds fy, rS;kj dhft,A

Q. No. 10 Preet ship commenced a voyage from Kolkata to Mumbai on 1st Nov 2014. The

ship was insured. Its premium for this voyage was Rs 10,000. This voyage was

completed on 31st Dec. 2014. Following particulars about this voyage are available.

Post charges Rs. 3,000

Wages & Salaries Rs. 24,000

Banker Rs. 20,000

Stores Rs. 18,000

Sundry expenses Rs. 10,000

Depreciation annual Rs. 30,000

Passage money received Rs. 15,000

22

Manager's commission is 5% on such net profit which is arrived after charging such

commission. Store on hand Rs. 5,000.

Address commission 4% on all freights, Outward freight Rs. 1,00,000, Inward

freight Rs. 1,50,000, Primage on 10%. Prepare Voyage Account.

izhr ty;ku us 1 uoEcj 2014 dks leqnzh ;k=k dksydÙkk ls eqacbZ izkjaHk dhA ty;ku

chfer FkkA leqnzh ;k=k ds fy, bldk izhfe;e 10]000 :- FkkA ;g leqnzh ;k=k 31

fnlEcj 2014 dks iw.kZ gqbZA bl leqnzh ;k=k ds laca/k esa fuEu fooj.k miyC/k gS&

:-

Mkd O;; 3]000

etnwjh rFkk osru 24]000

cadj 20]000

LVkslZ 18]000

fofo/k O;; 10]000

okf"kZd gzkl 30]000

iSlst /ku izkIr 15]000

deh'ku dkVus ds ckn vk;s 'kq) ykHk ij eSustj dk deh'ku 5%A gkFk esa LVkslZ :-

5]000 ,Mªsl deh'ku 4% ¼lHkh HkkM+ksa ij½ ckg~; HkkM+k :- 1]00]000] vkarfjd HkkM+k :-

1]50]000] izkbesst 10%] leqnzh ;k=k [kkrk cukb,A

OR

Ajanta electronics, Mumbai consigned 10 Deluxe Portable Television sets to Ashok

Traders, Ujjain at the rate of Rs. 8,000 each, the invoice price of which is 25% more

than that. Consigner incurred Rs 860 for packing and Rs. 640 for railway freight.

One T.V. set was lost in transit. The agent Ashok Traders, Ujjain paid Rs. 245 for

cartage, Rs. 335 for godown rent and 1% brokerage. Agent sold 8 T.V. sets at the

rate of Rs. 11,000 each. Ashok Traders are entitled to 7.5% commission on the

invoice price and 20% on additional price realised. Agent remitted the remaining

amount deducting their expenses and commission. Consignors received Rs. 8,000

from railway as compensation for the lost goods. Prepare the following accounts in

the books of consignors-

i) Consignment A/c

ii) Ashok Trader's A/c

iii) Abnormal Loss A/c

(Show the calculations)

vtark bysDVªksfuDl eqacbZ esa 10 MhyDl iksVsZcy Vsyhfotu v'kksd VªsMlZ mTtSu dks 8]000

:- izfr Vh- oh- lsV dh nj ls isz"kd ij Hksts] ftudk chtd ewY; 25% vf/kd FkkA isz"kd

us 860 :- iSfdax vkSj 640 :- jsy HkkM+s rFkk chek ds O;; fd,A ,d Vh- oh- lsV jkLrs

esa [kks x;kA ,tsaV v'kksd VsªMlZ mTtSu us 245 :- xkM+h HkkM+k] 335 :- xksnke fdjk;k

vkSj 1% nykyh ds fn,A ,st.V us 8 Vh- oh- lsV 11]000 :- izfr lsV dh nj ls cspsA

v'kksd VsªMlZ dks 7-5% deh'ku chtd ewY; ij vkSj 20% deh'ku chtd ewY; ls vf/kd

jde ij feysxkA ,tsaV us deh'ku ,oa vius O;; dkVrs gq, 'ks"k jkf'k foØ; fooj.k ds

23

lkFk Hkst nhA izs"kd dks eky jkLrs esa [kks tkus ds 8]000 :- jsYos }kjk {kfriwfrZ ds izkIr

gq,A izs"kd dh iqLrdksa esa fuEu [kkrs cukb,A

i) izs"kd [kkrk

ii) ,tsaV v'kksd VªsMlZ dk [kkrk

iii) vlkekU; gkfu [kkrk

¼x.kuk,¡ Hkh n'kkZb,½

Q. No. 11 Prepare Income and Expenditure Account and Balance Sheet for a club for the year

ended 31-12-2014 on the basis of following informations:

Receipts and Payments Account

(For the year ended 31-12-2014)

Receipts Rs. Payments Rs.

To Opening Balance 10,000 By Rent 17,800

To Subscription By Printing 6,000

2013 1000 By Fuel 2,500

2014 31000 By Machinery 2,000

2015 1500 33,500 By Electricity 1,200

By closing Balance 14,000

43,500 43,500

Additional informations-

i) The value of machinery as at 31-12-2013 is Rs. 15,000 and depreciation rate

is 20% p.a.

ii) Outstanding amount of rent for the year 2014 is Rs. 2,000.

iii) Subscription in arrears for 2014 is Rs. 1,500.

fuEufyf[kr lwpukvksa ds vk/kkj ij 31&12&2014 dks lekIr gq, o"kZ ds fy, ,d Dyc

dk vk;&O;; [kkrk vkSj rqyu i= cukosa%

izkfIr vkSj Hkqxrku [kkrk

¼31&12&2014 dks lekIr gksus okys o"kZ ds fy,½

izkfIr;k¡ jkf'k tek jkf'k

izkjafHkd 'ks"k 10]000 fdjk;k 17]800

pank NikbZ 6]000

2013 1]000 bZa/ku 2]500

2014 31]000 e'khujh 2]000

2015 1]500 33]500 fo|qr 1]200

24

vafre 'ks"k 14]000

43]500 43]500

vfrfjDr lwpuk,¡&

i) 31&12&2013 dks e'khujh dk ewY; 15]000 :- gS vkSj gzkl dh nj 20% okf"kZd

gSA

ii) fdjk;k dh vnÙk jkf'k 2014 ds fy, 2]000 :- gSA

iii) 2014 ds fy, cdk;k pank 1]500 :- gSA

OR

The following is the Receipts and Payments Account of Siddhpreet club, Jabalpur

for the year ended 31st December 2014.

Receipts Amount Payments Amount

To Bal. b/d 1,500 By Rent 26,000

To Entrance Fees 2,750 By Stationery 15,340

To Subscription 2013 1,000 By Wages 26,650

2014 84,500 By Billiard Table 19,500

2015 1,500 By Repairs 4,030

To Locker's Rent 2,500 By Misc. Exp. 7,500

To special subscription for

government's part

17,250

By Bal. C/d 11,980

1,11,000 1,11,000

The following adjustments are to be made-

a) Locker's rent includes Rs. 300 for 2013 and Rs. 550 is still owing for year

2014.

b) Subscription unpaid for 2014 Rs. 2,400 and Rs. 260 for stationery were

outstanding.

c) Entrance fees is to be capitalized.

d) The club's other assets on 1 January 2014 were Rs. 39,000

From the above informations, prepare an Income and Expenditure Account for the

year ending 31st December 2014 and a Balance Sheet as on that date.

31 fnlEcj 2014 dks lekIr gq, o"kZ dk fl)izhr Dyc tcyiqj dk fuEu fyf[kr izkfIr

vkSj Hkqxrku [kkrk gS&

izkfIr;k¡ jkf'k Hkqxrku jkf'k

izkjafHkd 'ks"k 1]500 fdjk;k 26]000

izos'k 'kqYd 2]750 LVs'kujh 15]340

25

pank 2013 1]000 etnwjh 26]650

2014 84]500 fcfy;MZ Vsfcy 19]500

2015 1]500 ejEer 4]030

ykWdj pank 2]500 fofo/k O;; 7]500

jkT;iky dh ikVhZ ds fy,

fo'ks"k pank

17]250

vafre 'ks"k 11]980

1]11]000 1]11]000

fuEufyf[kr lek;kstu djus gSa&

v½ ykWdj fdjk;k esa 2013 dk 300 :- 'kkfey gS vkSj 2014 dk 550 :- vHkh Hkh

ckdh gSA

c½ 2014 dk 2]400 :- pank ckdh gS vkSj LVs'kujh dk :- 260 vnÙk gSA

l½ izos'k 'kqYd dks iwathd̀r djuk gSA

n½ 1 tuojh 2014 dks 39]000 :- dh Dyc dh vU; laifÙk;k¡ FkhA

mi;qZDr lwpukvksa ds vk/kkj ij 31 fnlEcj 2014 dks lekIr gksus okys o"kZ dks vk;&O;;

[kkrk cukb, vkSj mDr frfFk dk vkfFkZd fpV~Bk cukb,A

-----------------------------

Related Documents