VIVEK SINGH VIVEK SINGH B.COM (H) B.COM (H) ROLL – 263 ROLL – 263 SEMESTER - VI SEMESTER - VI RESEARCH GUIDE-PROF.S.SAHA RESEARCH GUIDE-PROF.S.SAHA ACCOUNTING & FINANCE ACCOUNTING & FINANCE DEPARTMENT OF COMMERCE DEPARTMENT OF COMMERCE ST.XAVIERS COLLEGE, KOLKATA. ST.XAVIERS COLLEGE, KOLKATA. 2006 - 2009 2006 - 2009 Page 1 of 37

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 1/37

VIVEK SINGHVIVEK SINGH

B.COM (H)B.COM (H)

ROLL – 263ROLL – 263

SEMESTER - VISEMESTER - VI

RESEARCH GUIDE-PROF.S.SAHARESEARCH GUIDE-PROF.S.SAHA

ACCOUNTING & FINANCEACCOUNTING & FINANCE

DEPARTMENT OF COMMERCEDEPARTMENT OF COMMERCE

ST.XAVIERS COLLEGE, KOLKATA.ST.XAVIERS COLLEGE, KOLKATA.

2006 - 20092006 - 2009

Page 1 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 2/37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 3/37

The research presented here describes the study of Credit Rating of a firm by

Credit Rating Information Services of India Ltd. (CRISIL). Credit rating of a firm

is a very important issue in the field of finance. The use of credit ratings

originated in the U.S. during the 19th-century but they are now spreading

around the globe. This paper also examines how the financial risk of a

company affect credit ratings and to what extent credit ratings directly affect

the capital structure decisions of a firm.

This research will provide the fundamental understanding of the credit risk

analysis process and various aspects of financial statement analysis to help in

managing better credit-related issues.

This study is not meant to take decisions for the prospective investors and to

make subsequent investments. The research is only a study and not the

guidelines to make necessary investments.

TABLE OF CONTENTS

CHAPTER I.............................................................................................6

1. INTRODUCTION OF THE STUDY....................................................................6

1.1 BRIEF IDEA OF THE STUDY............................................................................................61.2 RESEARCH PROBLEMS..................................................................................................7

1.3 LITERATURE REVIEW....................................................................................................8

1.4 OBJECTIVE OF THE STUDY............................................................................................8

1.5 METHODOLOGY............................................................................................................8

SCHEME OF WORK .............................................................................................................9

1.8 LIMITATIONS OF THE STUDY.........................................................................................9

CHAPTER II............................................................................................9

Page 3 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 4/37

2. THEORETICAL ASPECTS OF THE STUDY.......................................................10

2.1. Evolution of Credit Ratings........................................................................................10

2.2. Meaning of Credit Ratings.........................................................................................11

2.3. Credit Information.....................................................................................................12

Information commonly used to assess the

creditworthiness of a firm includes the following:..................................122.4. Five C’s of Credit.......................................................................................................13

2.6 Overview of CRISIL.....................................................................................................17

2.6.1 CRISIL Ratings .....................................................................................................18

2.6.3 CRISIL Approach...................................................................................................19

2.6.4 CRISIL Rating Process..............................................................................................20

2.6.5.1 Interpretation & Evaluation............................................................................22

2.6.6 CRISIL Rating Scale..............................................................................................22

2.6.7 Long Term Rating Scale.......................................................................................23

2.6.7.1 Investment Grade Ratings.............................................................................23

2.6.7.2 Speculative Grade Ratings.............................................................................23

2.6.8. Short Term Rating Scale......................................................................................24

2.6.10 Time Frame for Credit Rating.............................................................................25

2.6.11 Recommendations to the Investors....................................................................26

2.7 Capital Structure and its Sources...............................................................................26

.........................................................................................................................................26

2.8 Financial Leverage......................................................................................................27

CHAPTER III..........................................................................................28

3. COLLECTION OF DATA & DATA PRESENTATION............................................28

3.1 Primary Data..............................................................................................................28

3.2 Secondary Data..........................................................................................................28

3.3 Data Presentation: Tabulation....................................................................................29

ANNEXURE 1.................................................................................................................293.4 Data Analysis & Interpretation....................................................................................31

3.4.1 Effect of Financial Leverage on Credit Rating ......................................................31

CHAPTER VI..........................................................................................33

4. DATA ANALYSIS.........................................................................................33

4.1 By Using Statistical Tools............................................................................................33

4.2 By using computer assistance....................................................................................33

CHAPTER V...........................................................................................34

5. Summary .................................................................................................34

5.1 Findings .....................................................................................................................34

5.2 Final Conclusion..........................................................................................................35

5.3 Areas of Further Research..........................................................................................35

REFERENCE & BIBLIOGRAPHY.........................................................................36

Figure 1...............................................................................................29

Figure 2...............................................................................................30

Figure 3...............................................................................................30

Page 4 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 5/37

CHART 1..............................................................................................31

List of Abbreviations

1. SEBI – Securities & Exchange Board of India

2. CRISIL- Credit Rating Information Services of India Ltd.

3. ICRA - Investment Information and Credit Rating Agency of India Limited

4. CARE: - Credit analysis and Research Limited

5. ICSI - Institute of Companies Secretary of India.

6. CR- Credit Ratings

7. FL – Financial Leverage.

8. APP – Approximated figure.

9. F.Y – Financial Year

10.PBIT- Profit Before Interest & Text

11.PBT – Profit Before Tax

12.Contd - continued

Page 5 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 6/37

CHAPTER I

1. INTRODUCTION OF THE STUDY1. INTRODUCTION OF THE STUDY

1.1 BRIEF IDEA OF THE STUDY1.1 BRIEF IDEA OF THE STUDY

Credit Ratings are a symbolic indication of the current

opinion regarding the relative capability of a corporate entity to service its

debt obligations in time with reference to the instrument being rated. Credit

ratings are judgments about firms financial and business prospects. Credit

rating is defined ‘as a process by which a statistical service prepares various

ratings identified by symbols which are indicators of the investment quality of

the credit rated’. The credit may be a debt instrument or equity. In case of

debt, ratings are given while in the case of shares grading is done.

It is an independent assessment of the creditworthinessof a bond (note or any security of any indebtness) by a credit rating agency. It

measures the probability of the timely repayment of principal and interest of a

bond. Generally, a higher credit rating would lead to a more favorable effect

on the marketability of a bond. The credit rating symbols (long term) are

Page 6 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 7/37

generally assigned with “triple A” as the highest and “triple B” as the lowest

in investment grade. Anything below “triple B” is commonly known as a ‘junk

bond’.

With the help of credit ratings, the lenders can evaluate the potential risk

posed by lending money to companies and to mitigate losses due to bad debt.

Since, credit rating acts to extend loans from financial institutions, companies

will strive to maintain and improve their ratings. Credit rating agencies play a

key role in financial markets by helping to reduce the informative asymmetry

between lenders, on one side, and borrowers on the other side, about the

creditworthiness of a firm.

Rating is usually assigned to a specific instrument rather than the

company as a whole. In the Indian context, the rating is done at the instance

of the issuer, which pays rating fees for this service. If it is unsatisfied with the

rating assigned to its proposed instrument, it is at liberty not to disclose the

rating given to it.

1.2 RESEARCH PROBLEMS1.2 RESEARCH PROBLEMS

To present the whole Overview of the Project in a summarized form is quite a

difficult task, but in spite of it, sincere efforts has been put to present the

whole thing in a brief manner.

The debt instrument companies often do not provide the ratings of their

creditworthiness obtained from the agencies in the websites. So there arrived

a difficulty in analyzing and critically examine the worthiness of the

companies to that extent.

Page 7 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 8/37

The study more or less comes under the securities market line incorporated

with securities laws and compliances issued under the SEBI guidelines. So the

workings required expert knowledge in the field of regulatory framework

concerning Capital Market of India.

Thus due to small time frame the detailed knowledge to that effect was quite

impossible. Again there were lack of sufficient articles and journals regarding

the research.

Despite all the problems it was tried to overcome the same as maximum as it

was possible.

1.3 LITERATURE REVIEW1.3 LITERATURE REVIEW

The study presented here is brought up with the help of some well known

literatures. Some of them were India credit rating is raised by S&P, By Justin

Huggler, The State of Credit Rating in India; Ragunathan V Varma & Jayant R.

S&P downgrades Tata Motors’ credit rating By Joe Leahy in Mumbai.

1.4 OBJECTIVE OF THE STUDY1.4 OBJECTIVE OF THE STUDY

The objective of this research is to provide the understanding of how credit

rating helps the INVESTORS in making the risk and return analysis and

thereby helping the company to grow and maintain its success. The study also

aims to represent the overall effect of financial leverage of a company on its

credit ratings in the market.

1.51.5 METHODOLOGYMETHODOLOGY

The study is accompanied with simple data gathered from various books. The

data are very relevant to the study which are lucidly explained with the help

of some tables and chart. Since the time frame was small and due to lack of

resources available the primary data could not be collected. The study is

Page 8 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 9/37

solely based on secondary data like internet, books, journals, magazines and

various articles. In addition to this, quantitative research is used to analyze

the data.

SCHEME OF WORK SCHEME OF WORK

The work is divided into 5 chapters.

1.8 LIMITATIONS OF THE STUDY1.8 LIMITATIONS OF THE STUDY

The procedures and knowledge on credit ratings was limited only to one

rating agency, CRISIL. The rating processes, criteria and functioning of other

rating agencies like ICRA, CARE and Fitch Ratings India Private Limited were

not considered.

The research is limited to the secondary data only. Primary data could not be

incorporated due to time constraint. Lastly, credit ratings are on the verge of

rapid growth worldwide. The rating agencies are looking for fresh ways to

drive growth, such as introducing ratings for hospitals, educational

institutions, builders, state governments and even film projects. So theseaspects could not be taken into consideration due to the time limitation and

word limitation. Again further research on other case studies could not be

carried out due to the time factor.

CHAPTER IICHAPTER II

Page 9 of 37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 10/37

2. THEORETICAL ASPECTS OF THE STUDY2. THEORETICAL ASPECTS OF THE STUDY

2.1. Evolution of Credit Ratings

The concept of Credit Rating originated in the United States. The

first Credit Ratings were published by John Moody during 1909 in his analysis

or rail road investments. This evolved into the rating company, Moody’s

Investors Services Inc, a division of Dun and Bradstreet Inc.

Moody was followed by Poor’s publishing Company in 1916 and the

Standard Statistics Company in 1922, which merged, into Poor to become the

largest bond rating concern, Standard and Poor’s corporation, a subsidiary of

Mc Graw Hill, Inc. The third is Fitch publishing company of New York, which

was established in 1924. The fourth agency is Duff & Phelps of Chicago, which

was recognized by Securities and Exchange Commission in 1982. It acquired

Crisanti and Maffei Inc. of New York in 1991. These four security rating

agencies are the only ones with Securities and Exchange Commission

recognition as national bond rating agencies. There are other services that

rate securities especially stock, like Value Line Investment Survey.

The recognition of rating agency by Securities and Exchange

Commission in U.S.A does not constitute approval. Actually, such recognition

is not necessary to enter the security rating business. SEC uses the ratings of

recognized agencies for evaluation of bong assets of brokers and dealers

registered with it.

In India there are 4 credit rating agencies. First, Credit Rating Information

Services of India Limited (CRISIL) set up by ICICI AND UTI in 1988. Secondly

Investment Information and Credit Rating Agency of India limited (ICRA) set

up by IFCI in 1991. Thirdly, Credit Analysis and Research Limited (CARE)

Page 10 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 11/37

promoted by IDBI in 1993 in association with financial institutions. Fourthly,

Duff and Phelps Credit Rating India Private Limited (DCR India) for rating non-

banking financial companies for fixed deposits.

2.2. Meaning of Credit Ratings

"Credit rating agency" is a commercial concern engaged in the

business of credit rating of any debt obligation or of any project or program

requiring finance, whether in the form of debt or otherwise, and includes

credit rating of any financial obligation, instrument or security, which has the

purpose of providing a potential investor or any other person any information

pertaining to the relative safety to timely payment of interest or principal.1

Credit ratings are judgments about firms financial and business

prospects. Credit rating is defined ‘…as a process by which a statistical

service prepares various ratings identified by symbols which are indicators of

the investment quality of the credit rated’. The credit may be a debt

instrument or equity. In case of debt, ratings are given while in the case of

shares grading is done.

It is an independent assessment of the creditworthiness of a bond

(note or any security of any indebtness) by a credit rating agency. It measures

the probability of the timely repayment of principal and interest of a bond.

Generally, a higher credit rating would lead to a more favorable effect on the

marketability of a bond. The credit rating symbols (long term) are generally

assigned with “triple A” as the highest and “triple B” as the lowest in

investment grade. Anything below “triple B” is commonly known as a ‘junk

bond’.

CR is the process of assigning standard scores which summarize the

probability of the issuer being able to meet its repayment obligations for a

particular debt instrument in a timely manner. Credit rating is integral to debt

1 Ministryoffinance,GOI

Page 11 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 12/37

markets as it helps market participants to arrive at quick estimates and

opinions about various instruments. In this manner it facilitates trading in debt

and money market instruments especially in instruments other than

Government of India Securities. Credit rating is not a recommendation to buy,

hold or sell.

Rating is usually assigned to a specific instrument rather

than the company as a whole. In the Indian context, the rating is done at the

instance of the issuer, which pays rating fees for this service. If it is

unsatisfied with the rating assigned to its proposed instrument, it is at liberty

not to disclose the rating given to it. There are 4 rating agencies in India.

These are as follows:

CR is a dynamic concept and all the rating companies are

constantly reviewing the companies rated by them with a view to changing

(either upgrading or downgrading) the rating. They also have a system

whereby they keep ratings for particular companies on "rating watch" in case

of major events, which may lead to change in rating in the near future.

Ratings are made public through periodic newsletters issued by rating

companies, which also elucidate briefly the rationale for particular ratings. In

addition, they issue press releases to all major newspapers and wire servicesabout rating events on a regular basis.

2.3. Credit Information

Information commonly used to assess the

creditworthiness of a firm includes the following:

Credit Reports: Many organizations sell information on the credit

strength of business firms. The best-known and largest firm of this type is

Dun & Bradstreet, which provides subscribers with a credit-reference book

and credit reports on individual firms.

Page 12 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 13/37

Financial Statements: Financial statements contain a wealth of

information. A searching analysis of the firm’s financial statements can

provide useful insights into the creditworthiness of the firm.

The firm’s payment history: The most obvious way to obtain an

estimate of a firm’s probability on nonpayment is whether it has paid

previous bills or not. A study of the promptness of past payments is very

useful.

Bank References: The bankers of the firm may be another source of

information. To ensure a higher degree of candour, the firm’s banker may

be approached indirectly through the bank granting credit. 2

2.4. Five C’s of Credit

A credit rating assesses the creditworthiness of a firm in terms of the “five C’s

of credit”.

Character: It refers to the firm’s willingness to honour its obligations. The

credit manager should judge whether the firm will make honest efforts to

honour its credit obligation.

Condition: It refers to the prevailing economic and other conditions which

may affect the firm’s ability to pay. Adverse economic conditions can affect

the ability or willingness of the firm to pay.

Capacity: It refers to the firm’s ablity to meet credit obligations. The

ability to pay can be judged by assessing the firm’s capital and assets

which it may offer as security. Capacity is evaluated by the financial

position of the firm.

Capital: It is the financial reserves of the firm. If the firm has problems in

meeting credit obligations from operating cash flow, the focus shifts to its

capital.

2 Corporatefinance,WesterfieldRoss&Jaffe

Page 13 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 14/37

Collateral: It refers to the security offered by the firm in the form of

pledged assets.3

2.5 Utility of Ratings

2.5.1 INVESTORS PROTECTION

The main purpose of credit rating is to communicate to the investors the

relative ranking of the default loss probability for a given fixed incomeinvestment, in comparison with other related instruments.4 Investors have

always received credit ratings with enthusiasm. But issuers do not share the

enthusiasm since they have to share their securities at higher yields if their

issue gets inferior rating.

Credit rating gives an investor a simple and easy indicator to

the credit quality of the debt instrument, the risks and likely returns, thus

providing a yardstick against which the risk inherent in an instrument can be

measured. An investor uses the rating to assess the risk level and compares

the offered rate of return, which is expected rate of return (for the given level

of risk) to optimize his risk return trade- off. Ratings also provide a

comparative framework, which allows the investor to compare investment

opportunities.

The advantages of credit rating data for investors are obvious:

Savings in research costs.

Ratings represent the informed opinion of a neutral third party.

Certainty about the financial strength of the issuer.

Identification of the risk involved in the debt instrument.

3 FinancialManagement,Pandey.I.M financialManagement,ChandraPrasanna4 securitieslaws&compliances,ICSI

Page 14 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 15/37

Guidance in making an investment decision by being presented with a

wide variety of safe choices.

Constant monitoring and surveillance by the agency on the debt

instrument leading to effective risk management strategies.5

Spending too much on credit risk research

diminishes the return on investment. In addition, unlike underwriters and

main banks, credit rating agencies are valued for their neutral viewpoint and

expertise in credit risk analysis. For these reasons, investors rely heavily on

credit rating data.

Credit rating also benefits the issuer. If a public offer is contemplated, the

financial manager must bear in mind the rating while determining the

appropriate leverage. Additional debt may lower the rating from an

investment to a speculative grade category, thus rendering the security

ineligible for investment by many institutional investors. It may well be that

the advantages of debt outweigh the disadvantages of the lower credit rating.

Junk bonds, for instance, are a high risk and a high yield (16 to

25% in USA) instruments. Investment may be limited in such instrument to

what an investor can afford to lose.

Ratings will also affect the pricing of the issue. Actually pricingshould reflect the rating. The marketability of a relatively unknown issuer who

is competent is enhanced and the role of name recognition in an investment

decision is minimized.

In actual practice ratings are reflected in prices. There is no

difference between the interest rates that are paid on the fixed deposits of

two companies even if they are rated differently. Same is true of long dated

debentures. But in commercial paper market where banks are major players’

differentials in ratings are reflected in pricing. A reliance CP would be cheaper

than of a company, which is not rated well.

5 Legalpundits.com

Page 15 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 16/37

Ratings are used by brokers for opinions and as a service for

their customers. Insurance companies and mutual funds use them in the

purchase of securities even though their own staff prepares investment

analysis. Portfolio managers also use them in security management. Banks

depend on them for their investment in commercial paper. Individual

investors depend on them for their decisions to place fixed deposits. Ratings

are bound to assume greater importance with the institutionalization of

investors in the form of unit trusts, mutual funds, pension and provident

funds. The debt has shown considerable buoyancy in 1996 not only at the

wholesale level (institutional investors) but also at retail level in view of poor

offerings of equity in the primary market. This has come about largely on

account of the availability of ratings on debt instruments, which boosted

investor confidence.

2.5.2 SEBI Regulations for Credit Rating Agencies

SEBI issued regulations for credit rating agencies in 1999. These

regulations are called as Securities and Exchange board of India. (CreditRating Agencies) Regulations, 1999.

Only commercial banks, public financial institutions, foreign banks

operating in India, foreign credit rating agencies, and companies with a

minimum net worth of Rs 100 crore as per its audited annual accounts for the

previous five years are eligible to promote rating agencies in India.

Rating agencies are required to have a minimum net worth of Rs 5

crore.

Rating agencies cannot assess financial instruments of their promoters

who have 10 % stake in them.

Page 16 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 17/37

Rating agencies cannot rate a security issued by an entity, which is (a) a

borrower of its promoter. (b) a subsidiary of its promoter. (c) An associate of

its promoter, if (i) there is common chairman, directors between credit rating

agency and these entities (ii) there are common employees (iii) there are

common chairman, directors, and employees on the rating committee.

Rating agencies cannot rate a security issued by its associated or

subsidiary, if the credit rating agency or its rating committee has a chairman,

director or employee, who is also a chairman, director or employee of any

such entity.

A penalty of suspension of the certificate of registration or a penalty of

cancellation of registration may be imposed on the rating agency if it fails to

comply with the condition or contravenes any of the provisions of the Act.6

2.6 Overview of CRISIL

7

CRISIL is India's leading Ratings, Research, Risk and Policy Advisory

Company. At the core of CRISIL are its unimpeachable credibility and

unmatched analytical rigor. CRISIL offers domestic and international

customers a unique combination of local insights and global perspectives,

delivering independent information, opinions and solutions that help them

make better-informed business decisions and improve the efficiency of markets and market participants and help shape infrastructure policy and

projects.

6www. Sebi.gov.in

7 www.crisilonline.com/images Page 17 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 18/37

CRISIL's majority shareholder is Standard & Poor's, the world's foremost

provider of independent credit ratings, indices, risk evaluation, investment

research and data. CRISIL's association with Standard & Poor's, a division of

The McGraw-Hill Companies, dates back to 1996 when both companies

started working together on rating methodologies and joint projects.8

2.6.1 CRISIL Ratings

A CRISIL rating is CRISIL's opinion on the relative degree of risk associated

with timely payment of interest and repayment of principal on a specifiedbank facility. CRISIL assigns rating on the long-term and short-term rating

scales. Ratings can be used by banks to determine risk weights for their loan

exposures, in keeping with the Reserve Bank of India's (RBI's) April 2007

Guidelines for Implementation of the New Capital Adequacy Framework. The

new framework mandates that the amount of capital provided by a bank

against any loan and facility will be based on the credit rating assigned to the

loan issue by an external rating agency. This means that a loan and a facility

with a higher credit will attract a lower risk weight than one with a lower

credit rating. 9

2.6.2. Benefits of CRISIL Ratings

For Bank: The new guidelines from RBI create an incentive for banks to

use ratings, by giving significant relief in the capital that banks must hold

against their corporate loan exposures. The highest relief of 80 per cent is

available for 'AAA' and 'P1+' rated exposures, but there is substantial

8 www.crisil.com/about-crisil.htmlwww.iloveindia.com/finance/encyclopedia/crisil.html

9 crisilrating,journal Page 18 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 19/37

relief for exposures that are rated below the highest category as well. For

instance, both 'A' category-rated long-term loans and 'P2' category-rated

short-term facilities provide 50 per cent relief. Ratings will also be a key

input for appropriate pricing of credit risk by banks.

For Borrowers: A CRISIL’s rating will help borrowers obtain more precise

risk-based pricing on bank loans. Borrowers may also benefit when the

capital savings that the banks enjoy are reflected in loan pricing. In the

long run, as many lower rated borrowers obtain ratings, and the market

understands the risk associated with such lower ratings, access to

markets for lower rated corporate is likely to improve significantly.

For the Debt Market: Ratings will help develop a secondary market for

loans, and will provide a uniform scale for analyzing credit risk of bank

loans. 10

2.6.3 CRISIL Approach

CRISIL’s framework for assessing credit quality covers the four broad areas of

business risk, financial risk, management risk and project risk.

o Business risk analysis covers the business fundamentals of the rated

company, the characteristics of the industry in which it operates, its

competitive market position in the industry and operational efficiencies.

o Financial risk analysis includes an assessment of the company’s past

financial performance, its future performance and its financial flexibility

with particular emphasis on its balance sheet.

10 http://www.crisil.com/credit-ratings-risk-assessment/bank-loan-ratings.jsp

Page 19 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 20/37

o An evaluation of the company’s management, its philosophies, strategies

and risk appetite is undertaken in assessing management risk.

o If the company is implementing any large project, the risks associated

with the project’s implementation, its funding and marketing risks are also

evaluated. 11

2.6.4 CRISIL Rating Process

CRISIL employs a multi-layered decision making process in assigning a rating.

It has structured its rating processes as well as its rating committee to ensure

that all assigned ratings are based on the highest standards of independence

and analytical rigor. CRISIL strongly believes that the interest of investors is

best served if open dialogue is maintained with the issuer. Engaging the

issuer in a direct dialogue not only enables it to incorporate non-public

information in a rating report, but also makes it forward looking.

CRISIL's analysis on each credit is carried out by a team of at least two

analysts who interact with the company’s management. The analysis is based

on information obtained from the issuer, and on an understanding of thebusiness environment in which the issuer operates and it is carried out within

the framework of clearly spelt-out rating criteria. The analysis is then

presented to a rating committee comprising members who have the

professional competence to meaningfully assess the credit, and have no

interest in the entity being rated. The rating committee determines the rating

to be assigned. 12

11 Journal, ‘Ratings Methodology for Manufacturing Firms ’12 book, Corporate Finance by Vishwanath S.R. and the site, http://www.crisil.com/credit-

ratings-risk-assessment/rating-process.htm

Page 20 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 21/37

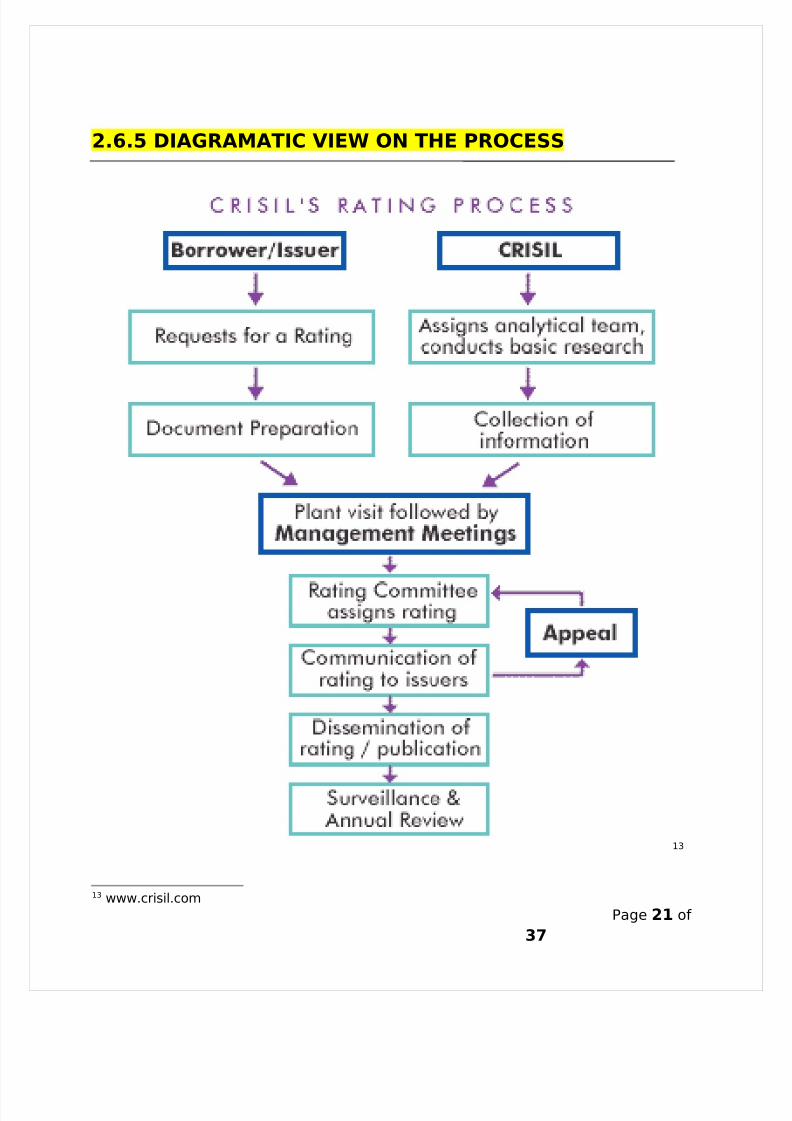

2.6.5 DIAGRAMATIC VIEW ON THE PROCESS

13

13 www.crisil.com

Page 21 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 22/37

2.6.5.1 Interpretation & Evaluation

Specific process safeguards that ensure independence from organizational

bias include:

∗ Multi-member rating teams

∗ Multi-tier rating process

∗ All rating decisions taken by a rating committee comprising

experienced, competent and reputed professionals

∗ Organization-wide internal transparency, with each stage of the rating

process for all ratings, including the final rating committee's discussions

- being open to all analytical staff in CRISIL's rating division

∗ Rating methodologies and criteria that are clearly spelt out and

published, and are consistently applied.

After the rating has been assigned, CRISIL continues to monitor the

performance of the issuer, and the economic environment in which the issuer

operates. This surveillance ensures that the analysts are aware of current

developments, so that they can review sensitive areas and learn about

changes in an issuer's plans. All ratings are under continuous surveillance.

Moreover, CRISIL has a policy of conducting detailed management meetings

with each issuer at least once a year. These meetings essentially focus on

developments over the period since the last meeting, and the outlook for the

coming year.

2.6.6 CRISIL Rating Scale

Page 22 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 23/37

CRISIL ratings are assigned on a scale that is analogous to CRISIL's rating

scale for long-term and short-term debt ratings. The scale ranges from 'AAA'

to 'D' for a long-term rating (with maturity over 365 days), and from 'P1+' to

'P5' for a short-term rating (maturity of up to 365 days).14

2 .6.7 Long Term Rating Scale

2.6.7.1 Investment Grade Ratings

•

AAA (Triple A) - Highest Safety: Instruments rated ‘AAA’ are judged tooffer the highest degree of safety with regard to timely payment of

financial obligations.

• AA (Double A) - High Safety: Instruments rated 'AA' are judged to offer

a high degree of safety with regard to timely payment of financial

obligations. They differ only marginally in safety from `AAA' issues.

• A - Adequate Safety: Instruments rated 'A' are judged to offer an

adequate degree of safety with regard to timely payment of financial

obligations.

• BBB (Triple B) - Moderate Safety: Instruments rated 'BBB' are judged

to offer a moderate safety with regard to timely payment of financial

obligations.

2.6.7.2 Speculative Grade Ratings

14 monthly journal on credit quality – Rating Scan

Page 23 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 24/37

• BB (Double B) - Inadequate Safety: Instruments rated 'BB' are judged

to carry inadequate safety with regard to timely payment of financial

obligations. They are less likely to default in the immediate future than

other speculative grade instruments.

• B - High Risk: Instruments rated 'B' are judged to have greater likelihood

of default; while currently financial obligations are met, adverse business

or economic conditions would lead to lack of ability or willingness to pay

interest or principal.

• C - Substantial Risk: Instruments rated 'C' are judged to have factors

present that make them vulnerable to default; timely payment of financial

obligations is possible only if favorable circumstances continue.

• D - Default: Instruments rated 'D' are expected to default on scheduled

payment dates. Such instruments are extremely speculative and returns

from these may be realized only on reorganization or liquidation.

CRISIL may apply '+' (plus) or '-' (minus) signs for ratings from 'AA' to 'C' toreflect comparative standing within the category.

2.6.8. Short Term Rating Scale

∗ P1: This rating indicates that the degree of safety regarding timely

payment on the instrument is very strong.

∗ P2: This rating indicates that the degree of safety regarding timely

payment on the instrument is strong. However, the relative degree of

safety is lower than that for instruments rated 'P-1'.

Page 24 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 25/37

∗ P3: This rating indicates that the degree of safety regarding timely

payment on the instrument is adequate.

∗ P4: This rating indicates that the degree of safety regarding timely

payment on the instrument is minimal and it is likely to be adversely

affected by short-term adversity or less favourable conditions.

∗ P5: This rating indicates that the instrument is expected to be in default

on maturity or is in default.

CRISIL may apply "+" (plus) sign for ratings from 'P-1' to 'P-3' to reflect a

comparatively higher standing within the category.

2.6.9 Confidentiality of Credit Rating Exercise

CRISIL keeps information obtained for the rating exercise confidential, by

enforcing appropriate process safeguards. For instance, all CRISIL employees

are required to sign a confidentiality agreement. CRISIL does not disclose

confidential information that it has obtained for the purpose of credit rating to

anyone (other than to market regulators or law enforcement authorities). 15

2.6.10 Time Frame for Credit Rating

CRISIL deputes a two-member team to carry out the assignment and the team

after having gone through the information submitted by the company, visits

their office for meetings in connection with the credit assessment. The

meetings take around 1 to 2 days with the involvement of functional,

divisional and business heads. On completion of management meetings, the

team prepares analytical note on the company that is discussed at the Rating

15 http://www.crisil.com/credit-ratings-risk-assessment/rating-process-confidentiality.htm

Page 25 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 26/37

Committee Meeting, and the committee assigns the final rating. Starting from

meetings, CRISIL assign a rating in a period of around 2 weeks. 16

2.6.11 Recommendations to the Investors.

By and large, the rating is a very good estimate of the actual creditworthiness

of the company; however, it is not able to predict extreme situations such as

the ones described above, which are unlikely to have been predicted by most

investors in any case. Investors should realize that a credit rating is not

sacrosanct and that one has to do one’s own due diligence and investigation

before investing in any instrument. They should use the rating as a reference

and a base point for their own effort.

One good way of doing this is examining the behavior of

the stock price in case the stock is listed. As a collective, the market is far

smarter at predicting problems than any credit rating agency. Witness the

sharp erosion in stock prices of companies much before their credit ratings

were downgraded. Witness also the fact that foreign currency bonds from

Indian issuer’s trade at yields lower than countries which have been rated

higher by rating agencies.

2.7 Capital Structure and its SourcesCapital structure means the type, composition and proportion of securities to

be issued that make up the total capital of the firm. The two principal sources

of finance for a business firm are equity and debt. For example, a firm that

sells $20 billion in equity and $80 billion in debt is said to be 20% equity

financed and 80% debt financed. Credit ratings are a material consideration

for managers in making capital structure decisions due to discrete costs

(benefits) associated with different ratings levels.

16 sources of the Company, CRISIL

Page 26 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 27/37

2.8 Financial Leverage

CRISIL’s framework for assessing credit quality covers various analysis like

business risk analysis, financial risk analysis and project risk analysis.

However, financial risk analysis is considered the most important for credit

rating, as it provides insight into how a risky a company is. It is an assessment

of the company’s past financial performance and its financial flexibility with

particular emphasis on its balance sheet.

The financial risk of a company can be measured by calculating its financial

leverage. A company more heavily financed by debt poses greater risk.

The financial leverage helps in determining the level of fixed financial charge

or in other words the extent of debt financing. As the debt financing is

relatively a cheaper source of finance, the financial leverage may suggest for

more and more use of debt financing, but with every increase in debt

financing, the financial risk, the risk of bankruptcy also increases. More over

the risk perception in the eyes of the equity shareholders also tends to

increase.

Analysis of financial leverage is the most important tool in the hands of a

finance manager who is engaged in framing the capital structure of the firm.

Any firm can easily adopt an all equity capital structure and thus can avoid

the financial risk. With financial leverage, the advantage arises from the

possibility that funds borrowed at a fixed interest rate can be used for

investment opportunities earning a rate of return higher than the interest

paid. The opposite effect will apply if the company fails to earn higher returns.

Page 27 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 28/37

CHAPTER IIICHAPTER III

3. COLLECTION OF DATA & DATA PRESENTATION3. COLLECTION OF DATA & DATA PRESENTATION

3.1 Primary Data3.1 Primary Data

There is no use primary data’s in the form of interviews, surveys,

questionnaires, etc.

3.2 Secondary Data3.2 Secondary Data

The secondary data has been collected majorly through various books on

financial management books and websites. Some of the magazines & journals

Page 28 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 29/37

were also brought into use .However there were very few journals & articles

available on the study. Necessary steps were taken to incorporate the right

data in a summarized form.

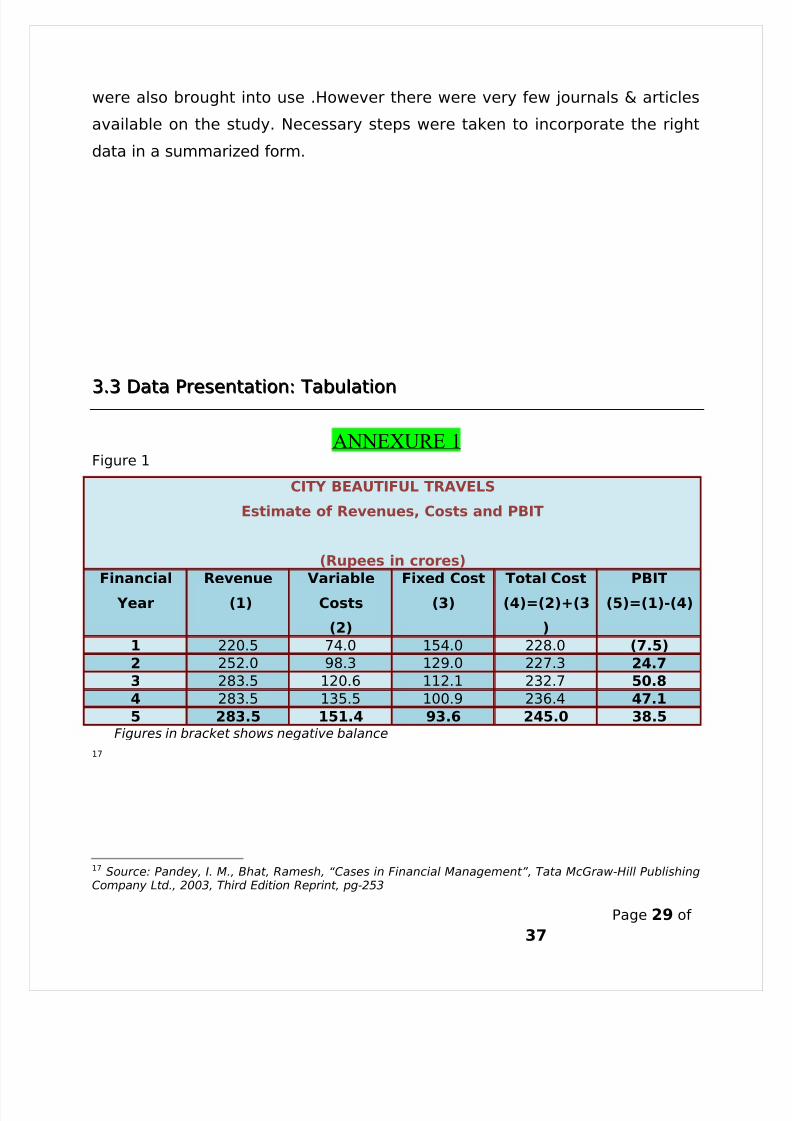

33.3 Data Presentation: Tabulation.3 Data Presentation: Tabulation

ANNEXURE 1Figure 1

CITY BEAUTIFUL TRAVELS

Estimate of Revenues, Costs and PBIT

(Rupees in crores)

Financial

Year

Revenue

(1)

Variable

Costs

(2)

Fixed Cost

(3)

Total Cost

(4)=(2)+(3

)

PBIT

(5)=(1)-(4)

1 220.5 74.0 154.0 228.0 (7.5)

2 252.0 98.3 129.0 227.3 24.7

3 283.5 120.6 112.1 232.7 50.8

4 283.5 135.5 100.9 236.4 47.1

5 283.5 151.4 93.6 245.0 38.5 Figures in bracket shows negative balance

17

17 Source: Pandey, I. M., Bhat, Ramesh, “Cases in Financial Management”, Tata McGraw-Hill PublishingCompany Ltd., 2003, Third Edition Reprint, pg-253

Page 29 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 30/37

Figure 2

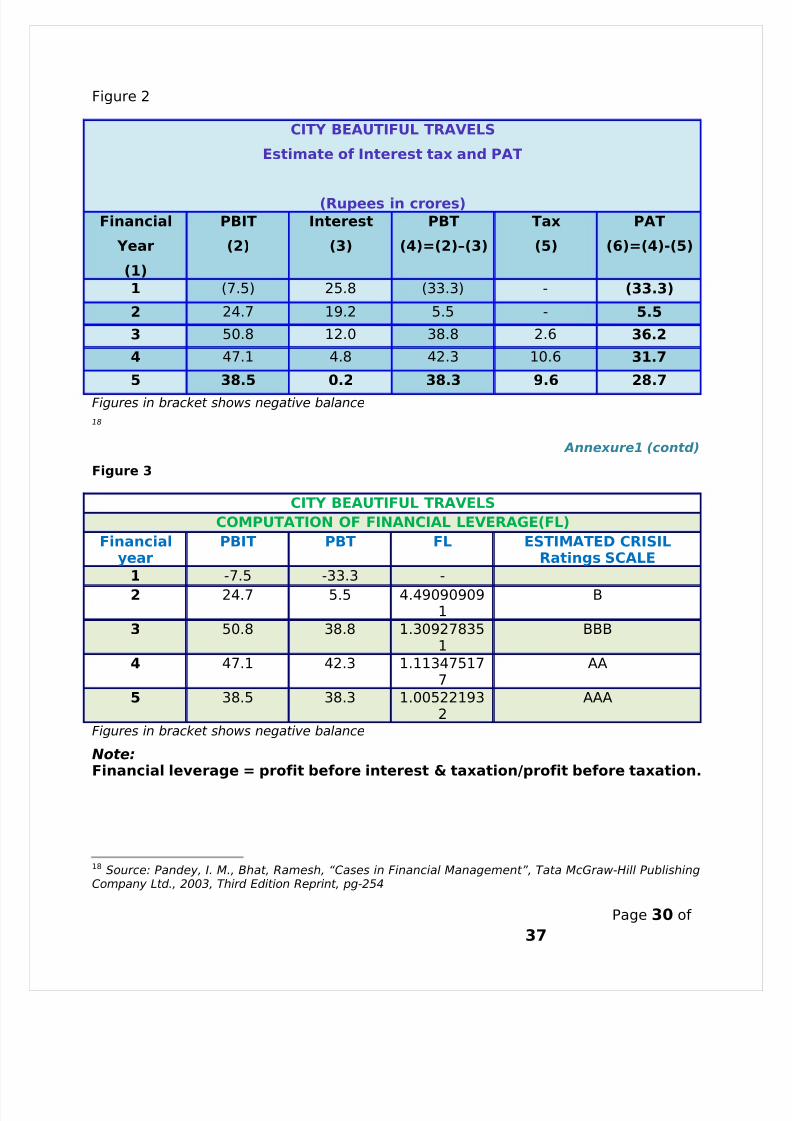

CITY BEAUTIFUL TRAVELS

Estimate of Interest tax and PAT

(Rupees in crores)

Financial

Year

(1)

PBIT

(2)

Interest

(3)

PBT

(4)=(2)–(3)

Tax

(5)

PAT

(6)=(4)-(5)

1 (7.5) 25.8 (33.3) - (33.3)

2 24.7 19.2 5.5 - 5.5

3 50.8 12.0 38.8 2.6 36.2

4 47.1 4.8 42.3 10.6 31.7

5 38.5 0.2 38.3 9.6 28.7

Figures in bracket shows negative balance

18

Annexure1 (contd)

Figure 3

CITY BEAUTIFUL TRAVELS

COMPUTATION OF FINANCIAL LEVERAGE(FL)

Financialyear

PBIT PBT FL ESTIMATED CRISILRatings SCALE

1 -7.5 -33.3 -

2 24.7 5.5 4.490909091

B

3 50.8 38.8 1.309278351

BBB

4 47.1 42.3 1.113475177

AA

5 38.5 38.3 1.005221932

AAA

Figures in bracket shows negative balance

Note:Financial leverage = profit before interest & taxation/profit before taxation.

18 Source: Pandey, I. M., Bhat, Ramesh, “Cases in Financial Management”, Tata McGraw-Hill PublishingCompany Ltd., 2003, Third Edition Reprint, pg-254

Page 30 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 31/37

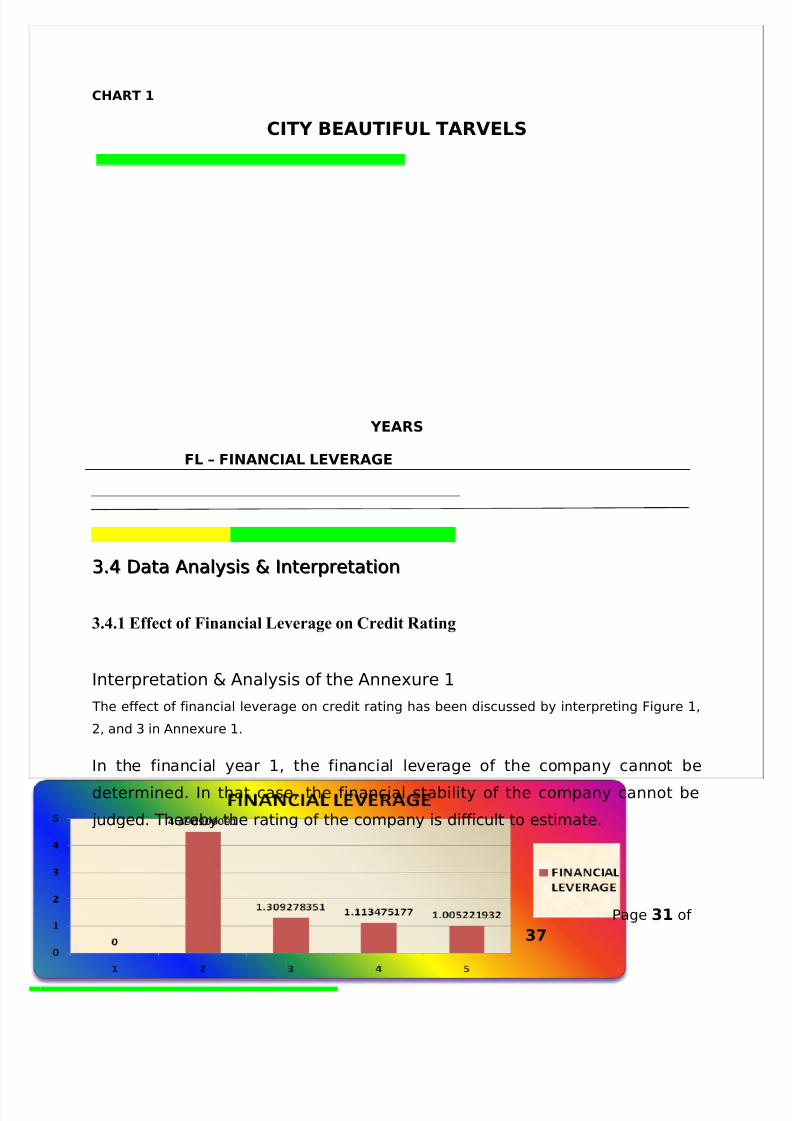

CHART 1

CITY BEAUTIFUL TARVELS

YEARS

FL – FINANCIAL LEVERAGE

33.4 Data Analysis & Interpretation.4 Data Analysis & Interpretation

3.4.1 Effect of Financial Leverage on Credit Rating

Interpretation & Analysis of the Annexure 1

The effect of financial leverage on credit rating has been discussed by interpreting Figure 1,

2, and 3 in Annexure 1.

In the financial year 1, the financial leverage of the company cannot be

determined. In that case, the financial stability of the company cannot be

judged. Thereby the rating of the company is difficult to estimate.

Page 31 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 32/37

However in the year 2, the company has managed to derive revenues out of

operational sales. The financial leverage of the company is 4.5

(approximated) which is very high compared to other years. Thus the

company is not expecting a high rating in the year 2 because the financial risk

is high.

However, the financial leverage is expected to decrease to 1.31(app) in the

financial year 3, because, the company has projected that their net revenue

from the sales would rise from 252.0 crores to 283.5 crores in the financial

year 4. This will lead to an increase of Rs 26.2 crores in EBIT. Apart from this,

the interest payable is also expected to fall from 19.2 crores to 12 crores.

Thus the risk of the defaults will decrease and hence the company has

projected that their ratings would be upgraded in the F.Y 3.

The company’s financial leverage is projected to decrease to 1.11 in the F.Y 4.

The EBIT in the same year is expected to decrease from 50.8 crores to 47.1

crores but along with it the fixed charge i.e., the interest burden has slipped

from 12.0 crores to 4.8 crores registering decrease in the fixed charges to the

extent of 60 percent. On the other hand due to this effect the PBT has risen to

the extent of 42.3 percent. The combined effect has lowered down the

financial leverage of the 1.3 to 1.1. This is why; it has been projected by thecompany that they will be able to obtain a higher rating in F.Y 4 in comparison

to F.Y 3.

Furthermore, in the F.Y 5, the company is expecting that their financial

leverage will fall from 1.1 in F.Y 4 to 1.00 (app) F.Y 5. This is because the EBIT

& PBT has both declined to the extent of 18.1 percent (app) & 9.5 percent

(app) respectively. The company still manages to meet the current year’s

financial charge of 0.2 crores. It also indicates that the company is currently

having no or very minimal capital from debt financing. This will help the

company to further upgrade their ratings in F.Y 5.

Therefore, it is evident from table 1 that the company has tried to minimize

the capital raised from debt – financing to increase the creditability in the

Page 32 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 33/37

market. The significant fall in the financial leverage would enhance the

creditworthiness of the company. This will help them to take more loans from

the bank at a cheaper rate of interest and the goodwill of the company will

also improve. As the F.Y has progressed Chart 1 has recorded a significant

downfall in the financial leverage of the company. This has helped the

company to enhance its ratings in the market.

Again it should be noted that the ratings proposed above to the City Beautiful

Travels in all the financial years is based on the assumption that no other

factors are present.

But in reality CRISIL considers many factors while calculating the ratings to a

particular concern.

The calculations for financial leverage have been done in fig 3 in Annexure 1.

CHAPTER VICHAPTER VI

4. DATA ANALYSIS4. DATA ANALYSIS

44.1 By Using Statistical Tools.1 By Using Statistical Tools

There were no uses of any statistical tool analysis.

44.2 By using computer assistance.2 By using computer assistance

The computation of the financial leverage of the company on the basis of

different data available has been done through Microsoft Excel. No other

computer assistance is used to determine and analyze the values.

Page 33 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 34/37

CHAPTER VCHAPTER V

5. Summary5. Summary

5.1 Findings5.1 Findings

Capital structure decisions are affected by the potential for both an upgrade

as well as a downgrade in credit ratings. The rating of a company is inversely

related to its financial leverage. The firms, if their ratings are expected to

upgrade, can increase its debt capital by extending loans from banks and

other financial institutions. However, if the ratings are expected to

downgrade, then the debt capital of the firm will be reduced. Therefore it can

be said that credit ratings directly affect the equity and debt financing

decisions of a firm. Hence, credit ratings are a material consideration for

managers in making capital structure decisions.

Page 34 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 35/37

5.2 Final Conclusion5.2 Final Conclusion

Ratings are opinions on credit worthiness based on objective and subjective

analysis. Rating agencies play an important role in the world markets; they

can best serve markets when they operate independently, adopt and enforce

internal guidelines to avoid conflicts of interest and protect confidential

information received from issuers. Credit rating agencies cannot afford to

commit too many mistakes as it the investors who pays the price for their

mistakes. Credit rating agencies should be made accountable for any faulty

rating by panelizing them or even de-recognizing them, if needed. Since

lending money has become more global and diverse, it is difficult for the

lenders to determine which companies have a minimum risk of default and

assure themselves of the continuous soundness of borrowers after a loan has

been extended. The financial intermediaries such as banks turn to credit

rating agencies to provide necessary information on borrower’s

creditworthiness. Credit rating appraises the default risk which is a

combination of business risk and financial risk.

These agencies help lenders decide how risky it is to lend money to a certain

company. In sum, credit ratings can help lenders pierce the fog of asymmetric

information that surrounds lending relationships. Equivalently, credit ratings

can help borrowers emerge from that same fog.

5.35.3 Areas of Further ResearchAreas of Further Research

A CR agency takes into account various factors while grading a particularcompany. The major ones are cash flow adequacy, operating efficiency,

accounting quality, long term earning powers, management evaluation,

industry interface and risk and of course financial leverage. However in the

paper, the research is carried only on the financial leverage factor. So there is

Page 35 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 36/37

a scope of further research on the other factors affecting the creditworthiness

of the company.

REFERENCE & BIBLIOGRAPHY

careratings.com

www.crisil.com

sebi.gov.in

WWW.Defaultrisk.com

www.Moneycontro.com

www.Dailytimes.com

Hindustantimes.com- corporate news

press trust of india articles

India credit rating is raised by S&P,By Justin Huggler

The State of Credit Rating in Indi, Ragunathan V Varma Jayant R

S&P downgrades Tata Motors’ credit rating By Joe Leahy in Mumbai

Published: March 25 2009

I.M. PANDEY 9TH EDITION.

Pandey, I. M., Bhat, Ramesh, “Cases in Financial Management”, Tata

McGraw-Hill Publishing Company Ltd., 2003, Third Edition Reprint, pg-254

., Bhat, Ramesh, “Cases in Financial Management”, Tata McGraw-Hill

Publishing Company Ltd., 2003, Third Edition Reprint, pg-254

Page 36 of

37

8/3/2019 My Complete Project B.com HONS

http://slidepdf.com/reader/full/my-complete-project-bcom-hons 37/37

Related Documents