Draft, October 21, 2003 Basle II Capital Requirements and Developing Countries: A Political Economy Perspective By Stijn Claessens Professor of International Finance Policy Geoffrey R. D. Underhill Professor of International Governance University of Amsterdam and Xiaoke Zhang Lecturer University of Nottingham Abstract The 1990s financial crises have triggered changes to the international financial system, the so-called international financial architecture. While much affected, developing countries have had very little influence on the changes, which the formulation of the new Basle capital accord (Basle II, B-II) illustrates. We show that B-II has largely been formulated to advance the interests of powerful market players, at the expense of those of developing economies. For these countries, B-II can raise the costs of and reduce the access to external financing. Importantly, B-II can exacerbate fluctuations in the availability of external financing, an unfortunate outcome, given that developing countries already suffer from volatile capital flows. For presentation at the workshop on Quantifying the Impact of Rich Countries’ Policies on Poor Countries, October 23-24, 2003, organized by the Center for Global Development and the Global Development Network. We would like Erik Feijen for excellent research assistance. 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Draft, October 21, 2003

Basle II Capital Requirements and Developing Countries:

A Political Economy Perspective

By

Stijn Claessens Professor of International Finance Policy

Geoffrey R. D. Underhill Professor of International Governance

University of Amsterdam and Xiaoke Zhang

Lecturer University of Nottingham

Abstract The 1990s financial crises have triggered changes to the international financial system, the so-called international financial architecture. While much affected, developing countries have had very little influence on the changes, which the formulation of the new Basle capital accord (Basle II, B-II) illustrates. We show that B-II has largely been formulated to advance the interests of powerful market players, at the expense of those of developing economies. For these countries, B-II can raise the costs of and reduce the access to external financing. Importantly, B-II can exacerbate fluctuations in the availability of external financing, an unfortunate outcome, given that developing countries already suffer from volatile capital flows. For presentation at the workshop on Quantifying the Impact of Rich Countries’ Policies on Poor Countries, October 23-24, 2003, organized by the Center for Global Development and the Global Development Network. We would like Erik Feijen for excellent research assistance.

1

1. Introduction

The financial crises of the 1990s have led to a debate on the reform of the international

financial system, the so-called international financial architecture debate. In response to

the crises, international financial institutions, such as the Basle Committee, the OECD,

the Financial Stability Forum (FSF), the IMF and World Bank, have promulgated and

established several sets of international standards to regulate market behavior. These new

standards are being held up as models for developing and other countries to follow and

are being assessed through various mechanisms (Financial Sector Assessment Program

(FSAP), Report on Standards and Codes (ROSC), etc.). There is also a debate

concerning standards of corporate governance in emerging market economies, though

this has yielded less in terms of concrete results.1

Developing countries are likely to be affected most by these standards, in part as they

are institutionally further from the “norms” being promulgated and as the leverage that

international institutions and (major) developed countries have over them is larger than in

case of more developed countries.

At the same time, developing countries have had very little influence on the

formulation of these standards, potentially undermining their legitimacy and

effectiveness. While the formation of the G-20 and the Financial Stability Forum might

have rendered the international decision-making process more inclusive, the membership

and structural hierarchy of these forums have left no doubt that the global financial

system will continue to be run by the leading industrial nations. The G-20 and the FSF

still exclude the majority of developing countries. Even the emerging markets that are 1 See George Vojta and Marc Uzan, “The Private Sector, International Standards, and the Architecture of Global Finance,” in Geoffrey R.D. Underhill and Xiaoke Zhang (eds.), International Financial Governance under Stress (Cambridge: Cambridge University Press, 2003), pp 283-301.

2

included realize that they have different interests from and lack collective bargaining

power vis-à-vis the dominant members.

A core set of new international standards is the proposed new Basle capital accord

(Basle II), which is in its final stages of negotiation. This has been shown to have

significant implications for the costs of capital for developing countries and could reduce

their access to external financing. As with the other standards, Basle II has been

developed largely to the exclusion of developing countries’ input. This paper, using Basle

II as an illustration of the skewed process of the international financial architecture

reform, seeks to achieve two different yet interrelated analytical objectives.

In the first place, this paper aims to examine the process through which the new Basle

capital accord has been formulated and to explain how and why the accord has become

standardized. The core argument to be developed is that Basle II capital requirements are

formulated in relatively exclusionary and closed policy communities consisting of

regulators and private agencies from the leading industrial nations. In these networks,

private market interests find respondents in finance ministers and central bankers and

have thus been able to influence the global agenda for policy changes. The rules and

standards to be sanctified by Basle II thus tend to advance the interests of powerful

market players at the expense of those of developing and emerging market economies.

Furthermore, the paper attempts to examine the impact of the Basle II capital

requirements on the long-term development prospects of developing countries and to

suggest some methods by which the impact can be quantified. A central hypothetical

proposition developed here is that the implementation of the new capital requirements

embodied in Basle II is most likely to exacerbate fluctuations in the costs and availability

3

of external financing for many developing countries. This would be a very unfortunate

outcome within the context of the potential contribution of the new international financial

architecture in general and of the new Basle capital accord in particular, given that they

have been designed to serve the most vulnerable members of the international

community.

The analysis of the Basel accord is relevant in its own right, but only one of the many

elements under discussion in the new international financial architecture. Many of these

elements need to be considered jointly. For example, one of the reasons why the Basel

outcome does not favor terms for (sovereign) lending to developing countries is the lack

of an international bankruptcy system. Yet, progress on such a system has been stymied

by, among others, the unwillingness of creditor countries to consider changes. As such,

our analysis is more important as an example of what the process of the reform of the

international financial architecture has delivered so far and what it can be expected to

deliver in the future for developing countries. The political economy analysis suggests

that developing countries have had little stake in the negotiations. To assure more

sustainable changes to the system, reform of the governance of the international financial

system itself is needed.

2. The new international financial architecture, a short overview

During the 1980s, Mexico made dramatic and unilateral alterations to its approach to

the economic development process. The strategy shifted from one based on state

intervention, capital controls, and trade protection/import substitution to one dominated

by economic openness, fiscal discipline, and a greater degree of market-led adjustment,

4

in line with what came to be called, in an article by John Williamson, the ‘Washington

Consensus’.2 In a number of respects, Mexico and other countries went further than what

Williamson specified as ‘consensus’ to embrace more radical aspects of the ‘neo-liberal’

platform of rapid opening of the capital account, rapid financial system liberalization,

far-reaching privatization, and a reduction of welfare provision,3 and often pegged

exchange rates as well.

The approach was seen in historical terms as a corrective to earlier approaches to

development involving state intervention and protection based on ‘infant industry’

arguments and problems associated with declining terms of trade for natural resources

exporters.4 The sovereign debt crisis and extreme inflation of the 1970s had spelled the

end this sort of development policy rationale. The extraordinary growth of private capital

markets from the 1980s onwards demonstrated the need to think not only about official

sector transfers in development policy, but also the need to create conditions conducive to

private sector investment. Private investors prefer developed countries to the developing

world at least partially because developing countries constituted greater investment risks,

even though they should also promise greater returns if growth were to take off as in the

case of the Asian tigers. If developing countries could reduce the risks posed by

inflation, exchange rate volatility, indebtedness, reduce the arbitrariness of what were

perceived to be politically driven state intervention strategies, and reduce structural

2 See John Williamson, "What Washington Means by Policy Reform", in J. Williamson, ed., Latin American Adjustment: How Much Has Happened? (Washington: Institute for International Economics, 1990). Williamson claimed, in a cautious assessment, that there was consensus around was a series of market-oriented reforms in development policy for Latin American countries, and which pointedly did not include capital account liberalisation. 3 As Williamson himself points out, the term also came to represent a more radical ‘neo-liberal’ ideology of minimalist state involvement, greatly reduced welfare provision, monetarism, and radical privatisation (“Did the Washington Consensus Fail?” Speech to Centre for Strategic and International Studies, 6 November 2002, http://www.iie.com/publications/papers/williamson1102.htm). 4 Ideas associate with Raul Prebisch and the UN Economic Commission on Latin America in the 1950s.

5

rigidities impairing the adjustment process, then capital would be more likely to flow

towards emerging market countries. This would require a major adaptation of the legal,

institutional, and substantive policy framework within developing countries. Market-led

development would also lead to smoother adjustment processes, avoiding the pitfalls of

debt-financed state-led strategies.

By 1994 Mexico, along with Argentina and others who imperfectly embodied the

consensus, was regarded as a star pupil and had just entered the North American Free

Trade Agreement with Canada and the US and was on its way to admission to the OECD.

In late 1994 the world of the Washington Consensus was baffled as Mexico plunged into

a combination of exchange rate crisis and financial crisis that led to a controversial record

IMF loan package assembled under US leadership.5 At the Halifax G7 summit of June

1995 and subsequently at Lyons and Denver (1996-7), the summit placed considerable

emphasis on a re-examination of global financial and monetary governance.6 Although

the ‘Peso Crisis’ of 1994-5 threatened other emerging market economies with contagion,

and not only those in Latin America, it passed with little changed at the international

level despite a range of more and usually less radical proposals for change coming from

academics and official sources, and complacency reasserted itself.7 Proposals aimed at

improving supervision at the international level, improving the transparency of financial

markets, sensible macroeconomic policies and exchange rate regimes, better monitoring

5 It was of course always an option for more radical neo-liberals to claim that the real problem was that Mexico did not go far enough, and thus that the ‘consensus’ was in itself insufficiently radical. 6 See the Halifax Summit document on reform of financial governance at http://www.g7.utoronto.ca/summit/1995halifax/financial/index.html; re Lyons summit at http://www.g7.utoronto.ca/summit/1996lyon/finance.html; the final report of the G7 finance ministers concerning financial architecture was presented at the Denver summit of 1997 – see http://www.g7.utoronto.ca/summit/1997denver/finanrpt.htm. 7 Among the more radical proposals was that of an international bankruptcy court to facilitate sovereign debt workouts under more predictable conditions, and an international banking standard (see Morris Goldstein, The Case for an International Banking Standard, Institute for International Finance, 1997)

6

of macroeconomic performance by the IMF, and the like. A consensus had formed that

radical change was not necessary and that an incremental reform process would suffice.

The outbreak of the Asian crisis of 1997/98 once again caught officials and the

private sector by surprise. The Asian tigers, again star (if often misunderstood) pupils of

international development policy, were suddenly in the grip of financial and monetary

crises which appeared inexplicable. Explanations such as exchange rate rigidities, a lack

of transparency on macroeconomic policy, and poor financial supervision were of course

found ex post facto, among them the sin of ‘crony capitalism’ and a failure to develop

transparent market-based relationships in the corporate world. Though the shock of the

Asian crisis was quickly followed by troubles in Russia, Argentina, Turkey, and Brazil,

and indeed the LTCM incident nearly brought financial contagion and collapse to Wall

Street itself, the reform debate remained limited in scope and the process incremental in

nature. It is noteworthy that the one more radical proposal to originate from the official

sector, the Sovereign Debt Workout Mechanism (SDRM) proposed by Ann Krueger of

the IMF and which contained elements of a global bankruptcy procedure,8 was defeated

by a combination of developing and developed member states alike at the IMF meetings

of March 2003.

The goals of the financial architecture reform process were straightforward and in

keeping with the market-based approach to development signaled by the Washington

Consensus. Policies of economic openness, macroeconomic stability (including fiscal

discipline), and sound supervision and regulation were the aim, and these were to

8 Anne Krueger, A New Approach to Sovereign Debt Restructuring (Washington, DC: International Monetary Fund, 2002).

7

facilitate international financial stability and efficient allocation of global capital, spilling

into domestic financial sector stability and development.

In the 1980s and 1990s, many countries in and out of Latin America implemented

reform policies along the lines of the ‘Washington Consensus’ described by Williamson,

often going beyond it. The collapse of the Soviet Bloc and the emergence of ‘transition

economies’ contributed to the sense of a triumph of market-based approaches to

economic development. Some countries indeed pursued quite radical experiments.

When financial crises began regularly to punctuate this reform process, it was often

revealed that insufficient attention had been paid to the legal, institutional, and regulatory

aspects of reform. The debate on financial architecture focused on these questions at

both the international and national levels. There was no essential re-examination of the

market approach itself,9 but a serious reckoning with the way in which it had been

implemented in various settings, and how reform interacted with monetary and exchange

rate policies as well. An examination of the relevant G7 documents will serve as

guidance to the agenda; the Birmingham summit (1998) provides perhaps the clearest

statement of what it termed an “emerging consensus.”

The Birmingham document,10 developed at the height of the Asian Crisis, began with

‘transparency’: the provision of “accurate and timely” macroeconomic and financial

supervisory data, including the reserve positions of central banks and levels of national

public and private indebtedness. The IMF was charged with developing codes of

9 Although arguably the most successful examples of economic development, Japan and east/SE Asia, had based their strategies on state-led investment strategies, import substitution combined with trade protection (progressing in time to export promotion), financial repression, and strict local content rules relating to foreign direct investment. Such strategies were not insensitive to market forces and the need for competitiveness, they were anything but market-led. 10 See the report at http://www.g8.utoronto.ca/summit/1998B-Irmingham/g7heads.htm.

8

Special Data Dissemination Standards (SSDS) to which countries would adhere, and the

BIS would accelerate the publication of data on central bank reserve positions.

Policymaking should also be more open in government and at IFI’s, with a view to

enhancing the confidence of investors and rendering the investment climate predictable

and therefore easier to price on markets. Secondly, national economies needed better

preparation for international capital flows: weak financial systems needed to be reformed

through orderly capital account liberalization processes (sound macroeconomic,

regulatory and supervisory policies first, then capital account opening); foreign firms in

the financial sector should have full access to the markets of developing economies in

order to transfer skills and expertise. Thirdly, national financial systems needed

strengthening in relation to corporate governance practices and norms (something to

which a number of developed countries might have, in retrospect, paid more attention).

This could be achieved through the development and benchmarking of supervisory

practice and standards (Basle ‘Core Principles’), along with a system of multilateral

surveillance of supervisory practice. Fourthly, the private sector must take greater

responsibility for its lending decisions and the risks that they inherently involve. Implicit

or explicit government or IFI guarantees of ‘bailout’ in crisis must end as this leads to

moral hazard. The private sector must bear its share of the burdens in debt workouts,

continuing lending in times of crisis, so that public resources were not unduly

underpinning private gain. National policies should clarify bankruptcy procedures at the

national level, enhancing understanding of risks and the consequences of mistakes.

Fifthly, with the IMF as the specified lead institution, greater co-operation among IFIs

and a better relationship between multilateral and bilateral aspects of stabilization efforts

9

must be developed. Finally, global forums for a better dialogue between emerging

market and developed creditor countries should be developed; one should see the

establishment of the Financial Stability Forum/Institute (FSF/I) in Basle (1999) and the

G10-G20 consultation process as the principal results of this aspect of the reforms. 11

The reform measures largely assume that the causes of crises lay with the emerging

market economies themselves and their weak institutions and practices. In this sense,

global financial architecture was to be strengthened rather les that the individual

emerging markets economies within it. These proposals were thus not really proposals

for systemic architectural reform as such, except to the extent that they established the

FSF/I to enhance supervisory practice, and designated the IMF as the lead institution of

‘architecture’ such as it was. There was certainly no fundamental review, as there had

been at Bretton Woods, of the balance of international versus national policy obligations

in the face of market and other international systemic pressures in global monetary and

financial relations. Discretionary policymaking of developing countries was in essence to

be continuously constrained through enhanced monitoring and transparency/new

standards in order to ensure that the investment climate conformed to the expectations

and preferences of investors. Considerable empirical evidence was ignored that most

successful developing countries, including the development processes of European

countries, occurred under conditions of some financial repression, and not full openness

and market orientation.

It is also worth drawing attention to the way in which the debate about reform was

carried out: who were the key players, who controlled the agenda, and who responded to

11 For a broader account of standards and what was developed from the B-Birmingham principles, see the Financial Stability Forum web site “Compendium of Standards/12 Key Standards for Sound Financial Systems.” http://www.fsforum.org/compendium/key_standards_for_sound_financial_system.html.

10

and shaped proposals over time? Given that the emerging market economies were

identified as the primary obstacles to a smoothly operating global financial system, and

given the considerable diversity of financial systems and legal/policy making institutions

in the developing world, one might expect some considerable attention to the ‘one-size-

fits-all’ problem and therefore considerable consultation between those proposing the

reforms and those who must accept and implement them. Although there are those who

argue optimistically that emerging market participation in global financial governance

has significantly increased,12 the case, it may be argued, is a weak one. The G7 and G10

governments are in a commanding position relative to the IMF, the G7 process, the

design and establishment of the FSF/I, and other relevant institutions such as the OECD

or the Basle Committee on Banking Supervision or the broader ‘Basle Process’ based at

the BIS. With the exception of the IMF and the OECD, there is no emerging market

membership of any of these bodies,13 and in the IMF a considerable number of the

executive directors representing transition or developing countries are in fact from

developed countries (e.g., Belgium, The Netherlands, Spain, Italy, Canada, Iceland and

Australia together represent some 71 countries, or 64 in addition to themselves14). The

G7 finance ministers have developed the agenda and led the debate themselves. The

institutions which are central to implementation and further decision-making on the

process (the IMF, World Bank, the FSF/I, the Basle Committee, OECD) are again

dominated by G7/G10 membership, and these institutions were developed by them for

12 See Randall Germain, “Global Financial Governance and the Problem of Inclusion,” Global Governance, vol. 7 (2001), pp 411-26. 13 The establishment of the G20 group of emerging market economies as a consultative body to the G10/G7 process, including deliberations in the broader ‘Basle Process’, constitutes progress but not membership of key bodies. Hong Kong and Singapore are in fact members of the FSF/I, but they hardly qualify as developing countries under current circumstances, and they represent a tiny population. 14 See IMF web site, http://www.imf.org/external/np/sec/memdir/eds.htm.

11

the governance of monetary and financial relationships in the developed world. G7/G10

central banks and treasury ministries have close and long-standing relationships to their

respective private financial sectors and are responsive to their preferences.15 It is far

more likely that developed country private sector preferences were central to the

proposals than the preferences of either developing country states or the corresponding

financial institutions thereof. We now turn to an analysis of the Basle Committee on

Banking Supervision as an example of a crucial policy-making community shaped by the

integration of private sector financial institutions into the official decision-making

institutions of developed country economies.

3. Basel II specifically

The motivations for the new Accord (B-II), arise from a number of technical

weaknesses in Basel I (B-I), changes in financial services industries globally, changes in

the forms of financial services provision, and the corresponding emergence of new, and

changes in the pattern of old, risks. The main weakness of B-I was its limited number of

credit risk classifications and the rather crude or distorted way in which some types of

loans were weighted for capital adequacy purposes. One obvious distortion was the zero

weight given to loans to OECD government, irrespective of the riskiness of the country.

This led countries like Korea and Mexico to be treated for capital adequacy requirements

the same as developed countries. Also, little attention was given to the correlations

15 For a comparative analysis of state-financial sector relations under conditions of global integration in developing countries, see William D. Coleman, Financial Services, Globalization, and Domestic Policy Change, (Basingstoke: Macmillan 1996); and for an analysis of finance-government relationships relative to the negotiation of the EU single financial market, see J. Story and I. Walter, Political Economy of European Financial Integration (Manchester: Manchester University Press, 1998); for a classic characterization of state-financial sector relations in the UK, see Michael Moran, The Politics of Banking, 2nd edition, (London: Macmillan 1986).

12

among the various risks, which ignored the potential gains from diversification. More

generally, the risks assigned to bank loans did not attempt to distinguish between the real

default risks of different sorts of clients: there is a considerable difference between loans

to major, stable and recognized companies versus risky ventures with new technologies

or the uncertainty of speculative minerals exploration.16 Finally, the earlier accord had

not properly accounted for operational risk in loan and securities market portfolios of

banks.

These weaknesses led to the current round of negotiations on a new accord. Given

the many changes in the financial services industries and the growing difficulties

experienced by supervisors in keeping up with the complexity and changing nature of

risk in contemporary financial markets, the starting point was to emphasize the role of

market discipline in risk management. This led to the so-called three pillars consisting of

1. minimum capital requirements; 2. supervisory review of capital adequacy; and 3.

public disclosure.17 Under the three pillar system supervisors, bank risk managers, and

market forces combine in the supervisory process, meaning that bank supervisors will no

longer be exclusively responsible for the supervisory process and specifying levels of

capital adequacy.

Pillar one maintains the basic provisions of B-I but institutes important changes in the

way aspects of credit risk are to be calculated and expanding the range of risks to include

operational risks. Three different options are available to banks under the proposals. The

standardized approach for less sophisticated institutions is based on B-I but enhances risk

16 See A New Capital Adequacy Framework, (Basle: Bank for International Settlements, 1999), pp. 8-9, at http://www.bis.org/publ/bcbs50.pdf. 17 See Basel Committee, Overview of the New Basle Capital Accord, consultative document, (Basle: Bank for International Settlements, April 2003).

13

sensitivity by differentiating among exposure to different sorts of bank clients. It

includes differential ‘risk weightings’ for sovereign and corporate exposures, to be

calculated according to external credit assessments such as the OECD or commercial

ratings agencies (Standards and Poor, Moody’s etc). Option two is a simplified or

‘foundation’ version of the ‘Internal Ratings Based’ (IRB) approach for risk

management, making limited use of internal Value at Risk (VaR) models. And option

three is an ‘advanced’ IRB approach meant for the largest and most sophisticated

financial institutions. In the foundation version, only the probability of default is

calculated by the bank, and all other capital ratios specified by the supervisor. In the

advanced version, all aspects of credit risk are estimated by the bank itself, i.e., it is a

complete ‘self-supervision’ approach, except that the bank has to qualify and the models

it uses have to be approved by the supervisor. Collateral and loan guarantees are to be

taken into account as well. Pillar two is about compliance, and consists of an ongoing

review by the supervisor of the options under pillar one as they pertain to particular

financial institutions. Supervisors must initially approve and regularly assess (stress

testing) the internal application of VaR models in the risk management process. Pillar

three consists of ‘Market Discipline’ as a compliment to the first two pillars. Crucial to

discipline is public disclosure of bank risk profiles and capitalization. This approach is

based on claims by the industry itself18 that market discipline is the best guarantor of

sound risk management, and that supervisory oversight is essentially redundant in a

soundly functioning system of market disciplines. There is also a potential clash with

18 And therefore surely suspect as deriving from narrow self-interest, given the costs associated with supervisory capital. Recent corporate scandals must also surely cast doubt on public disclosure as an essential ingredient of the pillar.

14

national laws concerning the confidentiality of information developed in the supervisory

process.

The initial paper announcing B-II was published in 1999, and is now in its third

version.19 Officially, the proposal is still under review, to be finalized by end of 2003

with implementation by 2006, perhaps postponed to 2007. The long process of

developing the proposals reveals disagreements among four sets of actors: a).

disagreement among Basle Committee members themselves; b). disagreement between

Basle Committee members and other official interlocutors in for example developing

countries; c). disagreements between private sector consultation partners (principally the

Institute for International Finance or IIF), and Basle Committee members; d).

commentary from expert and academic circles. Disagreements among Basle committee

members principally concerns whether the proposal should apply to all banks in a country

or only to ‘internationally active’ banks, and concerning the extent to which it is

mandatory. In part this disagreement reflects political economy factors among major

developed countries, notably Germany and the US. Developing country criticism has

focused on problems of implementation for the less sophisticated financial institutions in

emerging market economies. These are almost by definition corralled into the

‘foundation’ approach of pillar one, which is by definition more costly and will therefore

affect the competitive playing field. Private sector criticisms have focused on the

complexity and stringency of the agreement, and on the extent of corporate disclosure

required.

19 See note 15 re the 1999 document; the second version was The New Basel Capital Accord, consultative document (Basle: Bank for International Settlements, January 2001) at http://www.bis.org/publ/bcbsca03.pdf; and the third version same title, April 2003, at http://www.bis.org/bcbs/cp3full.pdf.

15

Other criticisms may be classified in four categories, three of which are on the overall

approach and one on the specific risks measures being suggested.20

• Arguably, B-II misses the key issue: the importance of systemic risks and

systemic monitoring. Under B-II, supervisors will only designate prudential

standards for ‘systematically’ significant financial institutions operating

internationally. Other banks do not require special treatment in the form of

regulation and supervision and rather, as any non-financial firm, could be

overseen by their shareholders, creditors and other stakeholders. By requiring all

types of banks to adopt B-II, potentially additional and unnecessary costs would

be imposed on the banking system and borrowers. Furthermore, if B-II were

more generally applicable, supervisors might spread themselves too thinly and

thereby not reduce the systemic risks they are set out to manage in the first place.

• B-II relies extensively on market signals, in the form of both asset prices as well

as ratings. The new approach essentially assumes that aggregation of good

practice in individual ‘systemically important’ institutions leads to stability at the

systemic level. However, if a wide range of banks responds to similar perceived

risks in the market, their aggregate behaviour may lead to problems at the

systemic level. In particular, procyclicality is inherent in approaches based on

market prices, such as VaRs and to some extent also rating agencies (although the

latter claim to rate borrowers across business cycles on relative, not absolute

terms). B-II may thus be enhancing the procyclicality already inherent in

financial markets and bank lending. Procyclicality is further aggravated by

encouraging many banks to use the same tools: downturns and upturns are thus

potentially reinforced as banks may en masse downgrade or upgrade clients.

Given these what ought to be obvious difficulties inherent in the approach, it is

perhaps less than coincidental that B-II will cost the major financial institutions to

which it applies rather less in terms of supervisory capital.

20See, for example, Persaud, The Political Economy of Basle II, Inaugural Lecture As Mercer Chair in Commerce at Gresham College.

16

• The hallmark of B-I was its simplicity, even when flawed in some respects. That

of B-II maybe its complexity and stress on sophisticated use of market data. This

is creating unnecessary costs for (small) banks, favors large banks and erects

barriers to entry and competition (especially for financial institutions in emerging

markets). As mentioned above, the advanced approach of pillar is likely to result

in considerable savings in terms of supervisory capital, directly affecting the

transaction costs and thus the competitiveness of institutions. B-II also relies too

much on hard information and too little on ‘soft’ or local information. It is thus

biased against lending to SMEs, which is often more based on relationships. Its

stress on models and rules can furthermore generate a false sense of security and

possibly facilitates regulatory capture of supervisors as they supervisors ‘hide’

behind technical complexity.

• The differential risks weightings of B-II compared to B-I would lead to a

significant increase in capital requirements for loans to lower rated borrowers,

thereby increasing costs and reducing quantity of lending.21 These lower rated

borrowers of course tend to be those who need capital most, or may be those in

the most innovative sectors of the economy. For example, by some calculations

B-II proposals would require spreads for B-minus rated borrowers to rise by 1000

basis points or more (see further below). Furthermore, B-II may place insufficient

emphasis on the risk reduction effects of (international) diversification.

Many of these criticisms apply especially to the lending to firms and sovereigns in

developing countries. Borrowers in these countries are typically lower rated, there is

more limited data on which to base judgments concerning their credit risks, and they

already suffer from procyclical lending patterns. The shift in risk weights is particularly 21 The general agreement has been that B-II cannot lead to an increase in overall capital adequacy requirements compared to B-I; higher requirements for lower rated firms thus will be compensated by reduced requirements for lower rated firms.

17

significant for those developing countries, which are also OECD-members (Hungary,

Mexico, Korea), where under B-I lending is subject to a zero weight. Furthermore,

lending to clients in developing countries may provide risk diversification benefits, which

are not sufficiently recognized in B-II. As a consequence, developing countries could see

the cost of capital increase and lending volumes reduced, with a reinforcement of

procyclicality. We analyze these effects in more the next section, but first discuss the

specific political economy factors underlying the development of B-II.

4. The political economy of Basel II

The Basle Committee on Banking Supervision (initially ‘Basle Committee on

Banking Regulations and Supervisory Practices’) was founded in 1974. The Committee

was an initiative of the G10 central bank governors, who were spurred into action

following the twin collapse of the Franklin National Bank and the Bankhaus Herstatt in

eurocurrency trading, both of which nearly toppled the global financial system at the

time.22 The Committee thus reports to the G10 central bank governors, and membership

(currently in fact 13 countries23) consists of one representative of each national central

bank, and if this is not the banking supervisor, then in addition a representative of the

national supervisory agency (this does not add an extra ‘vote’ and the committee does not

vote anyway, operating on a consensus basis). The initial policy question under

consideration was one of supervisory responsibility for internationally active banking

institutions: who precisely was responsible for supervising bank branches and

22 For more on the history of the Basle Committee, see Duncan Wood, The Basle Committee and the Governance of the Global Financial System (Aldershot: Ashgate Publishing, forthcoming 2004). 23 Belgium, Canada, France, Germany, Italy, Japan, Luxemburg, Netherlands, Spain, Sweden, Switzerland, the UK, and the US.

18

subsidiaries across borders – home or host country? The result was the Basle Concordat

of 1975, which has since undergone numerous refinements and amendments.24

The committee quickly gained a reputation for ‘Olympian’ detachment as a guardian

of the public, essentially state, interest.25 The Committee operated under conditions of

strict secrecy and relative insulation from public and private institutions of government

and market. The institutional culture of its earlier years contributed to this impression:

global financial integration was in its early stages, and the strong ‘public domain’ of the

Bretton Woods post-war era underpinned the Committee’s role and decision-making

processes. The negotiation process leading to Basle I in 1988 was the crowning

achievement, and occurred with little formal consultation with ‘outside’ interests.

There is no doubt that up until the negotiation of the Market Risk Accord of 1996 (in

fact an amendment to the 1988 B-I agreement26), the Committee did operate in a

considerably more detached manner than is the case today. However, Olympian

detachment and insulation from the traditional politics of government lobbies covered up

a more prosaic reality. Financial policy-making has historically taken place in relatively

closed and exclusionary policy communities with central banks and autonomous

regulatory agencies at the core of the system. These policy communities have often been

characterized by ‘business corporatism’ and the delegation of public authority to private

agencies via self-regulation,27 which continues to be a primary instrument in the

regulatory process. This close relationship between regulatory/supervisory agencies and 24 See analysis in Geoffrey R.D. Underhill, “Private Markets and Public Responsibility in a Global System,” in Underhill (ed.), The New World Order in International Finance (Basingstoke: Macmillan, 1997), pp. 23-8. 25 See the state-centric account of Basle by Ethan B. Kapstein, Governing the Global Economy: International Finance and the State (Harvard University Press, 1994). 26 See Basle Committee, Amendment to the Capital Accord to Incorporate Market Risks (Basle: Bank for International Settlements, January 1996). 27 See Coleman, Moran, cited above.

19

their correspondents in the financial services industry is in fact enhanced by the

‘Olympian’ distance of central banks and other autonomous agencies with regulatory and

supervisory responsibilities from the rough and tumble of traditional policy-making in

democratic governments, as in the case of trade negotiations. Thus the politics of

financial governance the national and the transnational level is far removed from

traditional, democratically accountable policy-making, and takes place in relatively

closed communion between financial sector private interests and autonomous public

authorities who share skills and knowledge which enhance their power and effectiveness

in controlling the policy agenda and outcome.28 This is the case even in developing

countries with strong traditions of financial repression and state control of the credit

allocation process.29

The Basle Committee therefore might well deliberate in Olympian detachment, but

national central banks and financial supervisors never did. Supervision and regulation

was developed in close co-operation with a small community of private interests which

shared more with central banks and supervisors than with the other sectors of the

economy and the rest of society (central banks are, after all, banks, and many in Europe

were only nationalized some 60-70 years ago). The process of transnational financial

integration led to a need to renegotiate supervisory and regulatory bargains reached at the

national level in the post-depression/Bretton Woods era. Basle I was the first attempt to

achieve this in relation to capital adequacy, and the outcome of the agreement

redistributed the pattern of competitive advantages and disadvantages across national

28 These points are developed and supported empirically in Underhill, “Private Markets,” op. cit. 17-49; and Underhill, “Keeping Governments out of Politics: Transnational Securities Markets, Regulatory Co-operation, and Political Legitimacy,” Review of International Studies, vol. 21/3, July 1995, pp. 251-78. 29 See Xiaoke Zhang, The Changing Politics of Finance in Korea and Thailand: from deregulation to debacle (London: Routledge, 2003), pp 38-41.

20

sectors: some national banking sectors had to raise substantial amounts of new capital

following the conclusion of the accord, affecting transaction costs. Coupled with

criticisms voiced about B-I (see above), calls emerged for the Committee to consider

more closely the impact of its decisions on the sector. The result was the emergence of a

consultation process with the Institute for International Finance (IIF)30 based in

Washington, and this consultation process developed with Committee’s 1993 proposals

to amend B-I to include securities markets risks as applied to Banks.31

This at first informal and so far unprecedented consultation process began when the

IIF issued a paper sharply criticizing the 1993 Committee paper: the proposals “fail[ed]

to create sufficient regulatory incentives for banks to operate more sophisticated risk

measurement systems than those necessary to meet the regulatory minimum”,32 meaning

VaR models. A well-circulated and authoritative paper by Dimson and Marsh of the

London Business School, claiming to demonstrate that VaR models were more effective

than the Committee’s proposed approach, added to the pressure.33 The result was a new

consultative document from the Committee embracing the approach advocated by the

IIF.34 The pressure had worked, but the Committee’s new and soon to become formal

interlocutor was hardly representative of the range of interested parties which would be

affected by the new amended accord or its successor, B-II. There were no emerging 30 The IIF was originally formed as a consultative group of major US and European banks during the debt crisis of the 1980s, and became a more broadly based organisation representing some 350 member banks worldwide. See website for membership, http://www.iif.com/about/member_list.quagga. 31See Basle Committee, The Supervisory Treatment of Market Risks, consultative paper, (Basle: Bank for International Settlements, April 1993). 32Institute for International Finance, Report of the Working Group on Capital Adequacy (Washington: IIF, 1993), cited in Financial Regulation Report, December 1993, p. 3. 33 Elroy Dimson and Paul Marsh, The Debate on International Capital Requirements: Evidence on Equity Position Risk for UK Securities Firms, (London: City Research Project, London Business School, February 1994). 34 Basle Committee, Proposal to Issue a Supplement to the Basle Capital Accord to Cover Market Risks (April 1995), and — , An Internal Model-Based Approach to Market Risk Capital Requirements (April 1995).

21

market representations and the process did not extend beyond the traditionally close

relationship between banks and supervisors/regulators. At the transnational level, one

may argue, the emerging policy community was even further removed from traditional

lines of democratic accountability in the policy process.

Following the successful consultation process, the industry’s preferences as

articulated by the IIF were translated into Committee policy. The IIF-Basle Committee

relationship became regular practice as the Committee began to consider B-II in the face

of ongoing criticisms of B-I treatment of credit risk, which remained so far unchanged.

In fact, the private sector was playing an even stronger agenda-setting role than in the

past. The review of B-I began with a study group of the Group of thirty, a private think-

tank like body of members drawn from the public/official and private institutions in the

financial sector alike, many of whom had held prestigious appointments in both. The

group formed a study group and issued a report on systemic risk in the changing global

financial system in 1997.35 As Paul Volcker, chairman of the G30 stated in the

‘Foreword’ to the report,

The report concludes that an ambitious effort to produce an international framework to serve as a guide to the management, reporting and supervision of major financial institutions and markets is justified and even imperative, beginning with the global commercial and investment banks. A collaborative effort between financial institutions and their supervisors would be most likely to be effective and broadly acceptable over a wide range of institutions and countries.36

The report observed that management controls should play a central role in the

supervision of financial systems, and that ‘core’ financial institutions should take the

35 Group of Thirty, Global Institutions, National Supervision, and Systemic Risk, (Washington, DC: Group of Thirty/Study Group Report, 1997). The report includes the names of study group participants (pp. ix-x), and members of the G30 itself (pp. 47-8). 36 Ibid., p. ii.

22

initiative to develop a new system along with ‘international groupings of supervisors’.

The conclusions of the report imply that,

supervisors will be readier to rely on the institutions that they supervise, and that the institutions themselves will accept the responsibility to improve the structure of, and the discipline imposed by, their internal control functions.37

Here lie the origins of the market-based supervisory approach contained in the three

pillars of B-II. In 1998 the IIF issued its own report specifically urging the Basle

Committee to update B-I on the basis of banks’ market-based internal control

mechanisms.38 Although the Basle Committee invited consultations on its (now three)

sets of proposals for B-II, the IIF remains the principal interlocutor, and comments come

overwhelmingly from financial institutions, to a lesser extent official agencies, and a few

academics.39

Basle does appear to be opening up. The web site displays the comments of various

interested parties, and who made them. There is, according to Germain, the beginning of

a broader consultation process involving the G20 and banking supervisors in emerging

market countries.40 Yet this is only a beginning and the historically close and isolated

policy community will take time to change. It may be argued that the structural power of

private financial institutions and the knowledge and assumptions about the market shared

by public and private agencies alike constitute the strongest element of the consensus that

little needs to change in global financial architecture.

37 Ibid., p. 12. 38 Institute for International Finance, Recommendations for Revising the Regulatory Capital Rules for Credit Risk, Report of the Working Group on Capital Adequacy (Washington, DC: IIF, March 1998). 39 See Committee web site section on comments on proposals at http://www.bis.org/bcbs/cacomments.htm (comments on second proposal) and http://www.bis.org/bcbs/cp3comments.htm (comments on third consultative document); it is clear that few groups outside financial industry have responded. 40 See Germain, “Global Financial Governance,” op. cit.

23

The minimal claim which this section needs to support anyway is that it is far more

likely the Basel Committee and its member institutions will take into the account the

articulated preferences of private sector interlocutors in developed countries than the

interests of developing country supervisors and their corresponding financial sectors.41

The long-institutionalized relationship between regulators and the regulated in financial

supervision, which approximates conditions of capture, is now developing at the

transnational level. Basle makes decisions which affect global financial governance

without passing the floor of anyone’s legislature and reporting only to a central bankers’

caucus, the Basle Committee increasingly thinks like its private sector and increasingly

acts like it too. Policy outcomes derive directly from the positions of the private sector as

financial globalization renders the supervisory process increasingly difficult and beyond

the reach of national supervisors.

5. The impact of Basel II on developing countries.

If one may conclude from the analysis so far that B-II has largely been negotiated

with the interests of developed country financial systems and institutions in mind, it

remains for us to determine if the new accord might in fact have an adverse impact on the

interests of developing country economies and financial systems. Financial flows to

developing countries are particularly closely associated with the development prospects

of these economies, and any negative effect of B-II on already low capital flows to the

41 This claim is well supported in Geoffrey R.D. Underhill, “The Public Good versus Private Interests in the Global Monetary and Financial System,” International and Comparative Corporate Law Journal, vol. 2/3, 2000, pp 335-359; — , “States, Markets, and Governance for Emerging Market Economies: private interests, the public good, and the legitimacy of the development process,” International Affairs, vol. 79/4, July 2003, esp. pp. 771-774.

24

broad range of emerging markets is not to be welcomed. As noted, B-II may affect

capital flows to developing countries in two ways: through the cost of bank lending,

affecting in turn the sustainable supply of external financing; and through the

procyclicality of lending. Both must however be evaluated relative to the B-I regime, to

the extent the current regime is already binding on banks, or relative to what would have

constituted a first-best solution. We do not analyze the impact of B-II on developing

countries’ financial systems; there are many arguments to be made, however, that such

standards are not only well suited and may done more harm than good to developing

countries.42

Cost of external financing. Several papers have highlighted the increased costs of

external financing for many developing countries as a result of the new Basel accord.43

Some of these estimates are country specific, some for all developing countries, but we

can use nevertheless use them to demonstrate the potential impact of B-II on the cost of

capital. A recent, publicly accessible analysis is Weder and Wedow (2002). They show

that by simply applying B-II versus B-I using publicly available ratings from rating

agencies (on the basis of the proposal as of November 2001), spreads charged by banks

could change between a). –40 basis points for A-rated borrowers and 2000 basis points

for CCC-rated borrowers under the IRB approach and b). between –40 basis points for A-

rated borrowers and 350 basis points for CCC-rated borrowers under the standard

42 Standards applying at the country level raises issues of who sets the standards, whether standards are realistic, who enforces the standards, how to square the standards with countries’ sovereignty, and how to apply penalties for any non-compliance. See further Stijn Claessens, The International Financial Architecture: What is News(s)?, Inaugural Lecture, University of Amsterdam, October 24, 2002. 43 Stephany Griffith-Jones, Miguel Segoviano, and Stephen Spratt, Basel II and Developing Countries: Diversification and Portfolio Effects, mimeo, Institute of Development Studies, University of Sussex, Financial Markets Group, The Londosn School of Economics, December 2002; Helmut Reisen Will Basel II Contribute to Convergence in International Capital Flows?, OECD Development Centre, Paris, 2001; Weder and Wedow, Will Basel II Affect International Capital Flows to Emerging Markets?, OECD Development Centre Technical Paper 199, October 2002.

25

approach. These effects are significant. Countries rated less than BB- by S&P could see

their cost of capital go up under the IRB-approach, which as of 2001, were 10 out of 26

rated developing countries. But, for the standardized approach only borrowers rated

worse than B- would see their spreads increase, which, as of 2001, were only 3 out of 26

rated developing countries. Some, but not the majority of rated developing countries

would thus see an increase in spreads on the basis of a mechanical application of B-II.

The B-II accord allows sophisticated banks not only to use external ratings, but also

internal ratings. There can be a difference between external and internal ratings, which

might alter this conclusion if internal ratings provide a higher share of lower rated

borrowers. We have access to internal ratings of a large Dutch bank, which is

internationally very active and has actually a longer record than the rating agencies in

rating countries and also covers more countries. This bank thus covers many countries

which have not had (or sought) access to international bond markets and which have

consequently not (yet) been rated by S&P. Since these countries are typically the less

creditworthy countries, this bank’s internal ratings are on average lower than the S&P

ratings. This already suggests that the overall impact of B-II on developing countries can

be more adverse than previously noted using external ratings.44

We first map the ratings from the bank with those of S&P and Moody’s (Table 1).

We also provide in the Table the default probabilities as calculated by S&P and Moody’s

for equivalently rated corporate sector borrowers, so as to calculate needed capital

adequacy requirements and resulting spreads.

44 See further Claessens and Embrechts, Basel II, Sovereign Ratings and Transfer Risk External versus Internal Ratings, CEPR Working Paper, 2002 for a description of the data.

26

Table 1: Risk Mapping between internal and external ratings and default probabilities of S&P and Moody’s

S&P ratings Internal rating Default Moody's Default prob. S&P AAA 18 0 0 AA+ 17 0 0

AA 16 0 0 AA- 15 0,06 0,03 A+ 14 0 0,02 A 13 0 0,05 A- 12 0 0,05

BBB+ 11 0,07 0,12 BBB 10 0,06 0,22 BBB- 9 0,39 0,35 BB+ 8 0,64 0,44 BB 7 0,54 0,94 BB- 6 2,47 1,33 B+ 5 3,48 2,91 B 4 6,23 8,38 B- 3 11,88 10,32

CCC+ 2 18,85 21,32 CCC 2 18,85 21,32 CCC- 2 18,85 21,32 CC 2 18,85 21,32

Selective Default 1 18,85 21,32

Note: The risk mapping assumptions are based on Table 3 from Claessens and Embrechts (2002). The default probabilities are taken from Weder and Wedow (2002), Tabel II.2, with the modification that the C-category and SD are separately classified, altgoug they have the same default probability.

We next recalculate the results for the changes in spreads using these internal

ratings for the various credit classes instead of the usual external ratings. Table 2a and 2b

provide the results for Moody’s and S&P respectively. Our results show similar effects

ax for the external ratings, as the cost of bank financing could rise under B-II by up to

1700 to 1900 basis points compared to B-I. The better-rated countries, however, could

see their costs decline by up to some 150 to 180 basis points.45

45 There is again the assumption that the capital adequacy requirements are binding and that the required rates of return are determined in line with the observed spreads for each borrower.

27

Table 2a: Adjustments in spreads for equivalent rates of return under B-I and B-II Using S&P default probabilities

Internal rating

Assumed spread

Default S&P

BRW S&P

S&P cap. req./100$

S&P risk adj. Return (%)

S&P spread change (b.p.)

18 0 0,00 0,00 0,00NA 0,0017 0 0,00 0,00 0,00NA 0,0016 0 0,00 0,00 0,00NA 0,0015 0 0,03 15,72 1,26 0,00 0,0014 0,5 0,02 13,87 1,11 45,07 -43,0713 0,5 0,05 19,17 1,53 32,60 -40,4112 0,5 0,05 19,17 1,53 32,60 -40,4111 1 0,12 28,82 2,31 43,37 -71,1810 1 0,22 39,19 3,14 31,90 -60,81

9 1 0,35 49,62 3,97 25,19 -50,388 4 0,44 55,62 4,45 89,90 -177,547 4 0,94 79,34 6,35 63,02 -82,656 4 1,33 92,04 7,36 54,32 -31,845 7 2,91 126,89 10,15 68,96 188,234 7 8,38 215,47 17,24 40,61 808,263 7 10,32 242,79 19,42 36,04 999,512 7 21,32 362,43 28,99 24,14 1837,032 7 21,32 362,43 28,99 24,14 1837,032 7 21,32 362,43 28,99 24,14 1837,032 7 21,32 362,43 28,99 24,14 1837,031 7 21,32 362,43 28,99 24,14 1837,03

28

Table 2b: Adjustments in spreads for equivalent rates of return under B-I and B-II Using Moody’s default probabilities

Internal rating

Assumed spread

Default Moody's

BRW-Moody's

Moody cap. req./100$

Moody's risk adj. Return (%)

Moody's spreadchange (b.p.)

Notes: The table provides the decrease/increase in spreads such the rates of return under B-II is the same as under B-I. Note that the only differences between the two Tables a and b is that we report estimates based on S&P default probabilities (2001) or Moody default probabilities from 2000. The mapping of internal risk ratings to Moody’s and S&P ratings can be found in Table 1. Appendix 1 provides the calculations. BRW=benchmark risk weight.

18 0 0,00 0,00 0,00NA 0,0017 0 0,00 0,00 0,00NA 0,0016 0 0,00 0,00 0,00NA 0,0015 0 0,06 20,75 1,66 0,00 0,0014 0,5 0,00 0,00 0,00NA -50,0013 0,5 0,00 0,00 0,00NA -50,0012 0,5 0,00 0,00 0,00NA -50,0011 1 0,07 22,24 1,78 56,20 -77,7610 1 0,06 20,75 1,66 60,25 -79,259 1 0,39 52,39 4,19 23,86 -47,618 4 0,64 66,61 5,33 75,06 -133,567 4 0,54 61,44 4,92 81,37 -154,226 4 2,47 118,50 9,48 42,19 74,005 7 3,48 137,14 10,97 63,80 259,974 7 6,23 182,67 14,61 47,90 578,723 7 11,88 263,18 21,05 33,25 1142,272 7 18,85 339,80 27,18 25,75 1678,572 7 18,85 339,80 27,18 25,75 1678,572 7 18,85 339,80 27,18 25,75 1678,572 7 18,85 339,80 27,18 25,75 1678,571 7 18,85 339,80 27,18 25,75 1678,57

According to this calculation, and only considering those 40 countries for which we

have both external and internal ratings, the number of countries that would see their cost

of external financing increase is actually less than half on the basis of the internal ratings

as of end 2000 (Figure 1). The impact of Basel II can be therefore interpreted as generally

positive, as most middle-income countries have a rating higher than a scale of 6. If the

ratings were used as of early 1990s, then there would be more countries with a rise in

costs than countries with a drop. Essentially, the number of countries in lower rating

29

classes diminishes over time (Figure 2). The internal ratings may have improved over

time as the fundamentals of the countries improved or as the bank has learned more of the

countries or is able to better manage risks over time. Regardless, there remain a number

of countries for which B-II has adverse impacts on cost of external financing; since these

countries already have difficulty obtaining financing, they are further negatively affected

by the new accord.

Figure 1

Number of countries which have a positive, neutral, or negative spread change due to Basel II according to Internal ratings in Oct-90, Oct-96, and Apr-01 (total in sample=40)

0

5

10

15

20

25

30

35

positive spread change neutral spread change negative spread change

Oct-90Oct-96Apr-01

30

Figure 2

Number of countries in each internal rating class in Oct-90, Oct-96, and Apr-01 (sample=40 countries)

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Number of countries

Oct-90Oct-96Apr-01

The average impact of Basel II, based on these results, seems to be modest. Using the

internal ratings, however, the average increase still tends to be higher than for the

external ratings, since the bank also rates more countries, including lower creditworthy

countries. Figure 3 shows the average required spread increase for the complete sample

of developing countries for which we have either the internal or the external ratings.46

Under both ratings, the spread change is positive, and actually increasing, over the last

years. This confirms that under Basel II to keep the risk-adjusted returns the same as

under Basel I, spreads have to increase. For the internal ratings, the level of required

spread is larger for all periods as the bank rates more less creditworthy countries. The

earlier results that were based only on the externally rated borrowers did thus

46 Note that internal ratings includes almost all countries; only around 1997 does S&P has as much countries as the internal ratings cover. Since in the beginning of the period, S&P rated only the best, capital requirements based on external ratings are lower on average, so the graph before 1997 is biased.

31

underestimate the effects of the cost of capital as only the more creditworthy borrowers

are rated by S&P and Moody’s.

Figure 3

Average spread change in basis points under Basel II to produce risk adjusted return under Basel I

based on S&P and Internal ratings

-200

-100

0

100

200

300

400

500

600

700

okt-90

feb-91

jun-91

okt-91

feb-92

jun-92

okt-92

feb-93

jun-93

okt-93

feb-94

jun-94

okt-94

feb-95

jun-95

okt-95

feb-96

jun-96

okt-96

feb-97

jun-97

okt-97

feb-98

jun-98

okt-98

feb-99

jun-99

okt-99

feb-00

jun-00

okt-00

feb-01

avg. int . spread djII I i lAvg. spread adj. S&P

Nevertheless, as several papers have pointed out, there are some flaws in this form of

analysis and a number of factors might actually mitigate the impact of B-II. These

corrections include the fact that the simple analysis presumes that banks want to keep the

risk-adjusted rates of return the same under B-I compared to B-II. The ex-ante required

rates of return implied by the capital adequacy weights under B-I are quite high, however.

For low rated borrowers, for example, the capital adequacy requirements combined with

the default probabilities of the corresponding rated class of corporations imply required a

three-fold increase in spreads (for B-rated assets). These very high required spreads for

lower rated borrowers are the result of applying the same ex-ante required rates for each

credit class under B-II as under B-I. Using a more realistic assumption that banks use a

fixed hurdle rate across all asset classes (of, say, 18 percent as suggested by Powell,

32

2001)47 would lower the increases in required spreads to between 100 and 200 basis

points for lower rated borrowers. Of course, this hurdle rate is ad-hoc and potentially

inconsistent with the principles of the risk-based approach, which requires different rates

as adjustments are made for risks, but it still shows some of the flaws.

Another mitigating factor is that developing countries receive funds from sources

other than banks, such as capital markets and non-bank financial institutions that are not

subject to capital adequacy requirements. This would reduce the impact of B-II; of

course, the access to capital markets and other financing may be more limited for

precisely these same lower rated countries, thus negating this effect. Also, banks subject

to the standard approach face lower capital requirements that those using the IRB

approach when lending to lower rated borrowers (specifically in the range below BB+).

Some clientele relationships may arise where banks using the IRB-approach choose the

safer borrowers and the banks using the standardized approach the riskier borrowers.48

This competition and clientele effects can mitigate some of the impact, although it cannot

be assumed that there are perfect substitutes available. There can, for example, be value

for borrowers from bank lending (from IRB-banks) which is not obtainable elsewhere.

For example, banks may better be able to assess, monitor and manage risk, and for those

reasons may be able to provide financing to countries relatively more cheaply. Without

these gains, the presence of perfect substitutes would raise the general question whether

mandatory capital adequacy requirements would ever be relevant as there always would

be some perfect substitute somewhere available.

47 Andrew Powell, A Capital Accord for Emerging Economies. Documento de Trabajo, No. 08/2001, Universidad Torcuato Di Tella, September. 48 While this may mitigate the effects on developing countries, it would go against the objectives of the new Basel accord in the first place as it introduces another distortion and may lead to risk-taking by those banks least qualified to assess risks.

33

The most important adjustment to the simple calculations is that banks may not be

constrained by the (new) capital adequacy requirements as they may already be adjusting

their economic capital in line with the risk associated with particular countries. Of

course, this argument can make B-II in a general sense irrelevant: if banks are already

doing what economic capital models require, there would not be any impact of capital

adequacy regulations properly based on such economic models. This goes against the

general trust of having an accord in the first place, so it is reasonable to assume there is

some binding effects of the accord. Consequently, there will have to be some effect on

spreads. Weder and Wedow (2002) investigate this issue as well by studying the

relationships between actual loan volumes to emerging markets and the capital charges as

would be required under B-II using the IRB. They find that the capital flows from BIS

reporting banks to 25 emerging markets over the period 1993-2001 are already affected

by the simulated B-II capital adequacy requirements, consistent with the interpretation

that banks have already largely adjusted their claims using a model anticipating the new

capital adequacy requirements. They do find that German banks may have been

constrained, but not the other countries.

Nevertheless, there might still adjustment necessary for some countries if the new

accord is not well calibrated; the simulation above suggest that some lower rated

countries may see their costs increase. Furthermore, internal ratings may differ from

external ratings, important as B-II allows greater use of internal ratings. Analysis by

Claessens and Embrechts (2002) suggests that the differences between the two types of

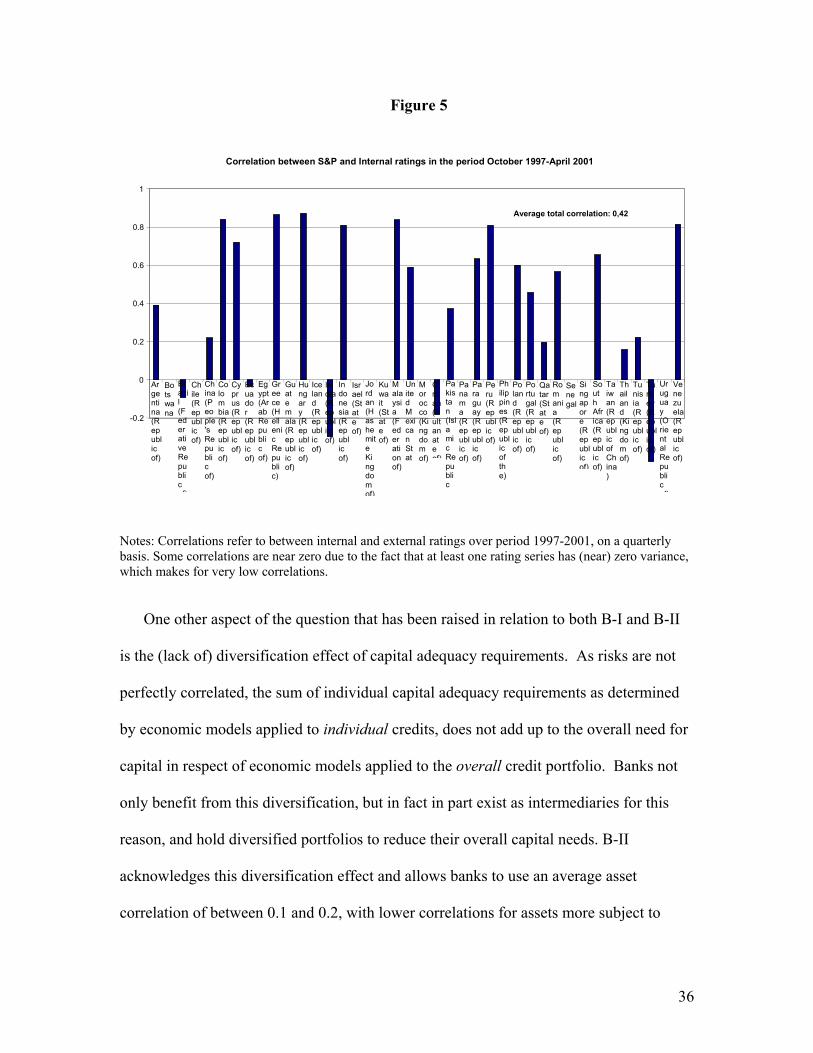

ratings are generally small (Figure 4). Still, on a country-by-country basis, the ratings are

not perfectly correlated over time (Figure 5). The average correlation for a sample of 40

34

developing countries over the 1997-2001 period between the two ratings is only 0.42.49

There has also been evidence reported that external ratings are slower to adjust to large

events, such as the East Asian countries’ financial crisis, than internal ratings are.

Figure 4

April 2001

0

2

4

6

8

10

12

14

16

18

20

0 2 4 6 8 10 12 14 16 18

Internal Rating

Exte

rnal

Rat

ing

Moody's S&P Linear (Moody's) Linear (S&P)

Note: internal and external ratings compared as of April 2001, using the conversion scale of Table 1.

35

49 The sample is small and short as few countries were rated in the early 1990s.

Figure 5

Correlation between S&P and Internal ratings in the period October 1997-April 2001

-0.2

0

0.2

0.4

0.6

0.8

1

Argentina (Republic of)

Botswana

Brazil (Federative Republic of)

Chile (Republic of)

China (People's Republic of)

Colombia(Republic of)

Cyprus (Republic of)

Ecuador (Republic of)

Egypt (Arab Republic of)

Greece (Hellenic Republic)

Guatemala(Republic of)

Hungary (Republic of)

Iceland (Republic of)

India (Republic of)

Indonesia (Republic of)

Israel(State of)

Jordan (Hashemite Kingdom of)

Kuwait (State of)

Malaysia (Federation of)

United Mexican States

Morocco (Kingdom of)

Oman (Sultanate of)

Pakistan (Islamic Republic

f)

Panama (Republic of)

Paraguay (Republic of)

Peru (Republic of)

Philippines (Republic of the)

Poland (Republic of)

Portugal (Republic of)

Qatar (State of)

Romania (Republic of)

Senegal

Singapore (Republic of)

South Africa (Republic of)

Taiwan (Republic of China)

Thailand (Kingdom of)

Tunisia (Republic of)

Turkey (Republic of)

Uruguay (Oriental Republic of)

Venezuela (Republic of)

Average total correlation: 0,42

Notes: Correlations refer to between internal and external ratings over period 1997-2001, on a quarterly basis. Some correlations are near zero due to the fact that at least one rating series has (near) zero variance, which makes for very low correlations.

One other aspect of the question that has been raised in relation to both B-I and B-II

is the (lack of) diversification effect of capital adequacy requirements. As risks are not

perfectly correlated, the sum of individual capital adequacy requirements as determined

by economic models applied to individual credits, does not add up to the overall need for

capital in respect of economic models applied to the overall credit portfolio. Banks not

only benefit from this diversification, but in fact in part exist as intermediaries for this

reason, and hold diversified portfolios to reduce their overall capital needs. B-II

acknowledges this diversification effect and allows banks to use an average asset

correlation of between 0.1 and 0.2, with lower correlations for assets more subject to

36

probable default (an increase in the asset default risk is argued to indicate a more

idiosyncratic nature of the asset, thus justifying a lower correlation). Still, as argued by

Griffith Jones et al. (2001), developing countries as a group exhibit a lower correlation

with developed countries than the correlations between most assets within countries or

from different developed countries. The potential diversification benefits from lending to

developing countries are therefore argued to be large, justifying lower capital adequacy

requirements. Griffith Jones et al. (2001) show that the chance of unexpectedly large

losses on a portfolio evenly distributed across developed and developing countries is

some 25 percent lower than that of a portfolio only distributed among developed

countries. Consequently, the capital adequacy charges should be set lower for a well-

balanced portfolio that includes developing countries.

This argument, however, also is only relevant if the capital adequacy requirements are

binding and not if banks already can, and do, allocate capital according to economic

criteria without regard to formal capital constraints. Furthermore, there is presumably

also a supply of assets within developed countries which also have low correlations with

other assets and that could also provide the diversification benefits sought.50 The issue of

low(-er) correlation for some specific assets also raises the question whether adjustments

should be allowed within the approach for specific assets or whether a generic approach

should be maintained.

In short, this section has demonstrated that on balance, the cost argument is not the

most important to the new accord from the point of view of most developing countries.

While there can be some impact for some borrowers, and especially for those with

50 A complete test would then also require comparing the div benefits from investing in emerging markets with those available from investing in all type of assets; this is done in the so called spanning literature.

37

limited access to market-based external financing, it need not be large on average for

developing countries as a group. At the same time, the analysis has shown that there is

little in the new accord that specifically addresses concerns of developing countries or

anything that could be attributed to developing countries’ specific inputs.

Volatility. Basel II may also have a potential adverse effect through the possible

increase in volatility of access of borrowers to bank financing and increased volatility.

As noted, there is an element of procyclicality in the new accord as it encourages greater

use of models that rely more on market data, including asset prices, which are procyclical

to begin with. Furthermore, requiring the same type of model to be used by many banks

will induce more commonality among banks, thus increasing the risks of financial

contagion as banks react simultaneously to the same or similar signals. These tendencies

may be aggravated as the accord encourages greater use of external and internal ratings.

Both types of ratings are arguably volatile and probably procyclical (see Lowe, 2002).51

Since developing country assets are arguably already subject to more volatility and

procyclicality than other asset classes are, the introduction of B-II might be particularly

harmful for emerging markets.

This issue may be analyzed by comparing the volatility of developing country ratings